Embed Size (px)

Citation preview

1

Recent Regulatory Efforts – What is the Nexus to Audit Quality?

Panelists: Denny Beresford, University of Georgia

Bill Platt, Deloitte LLP

Moderator: Cindy Fornelli, Center for Audit Quality

AAA Auditing Section Mid-Year MeetingJanuary 13, 2012

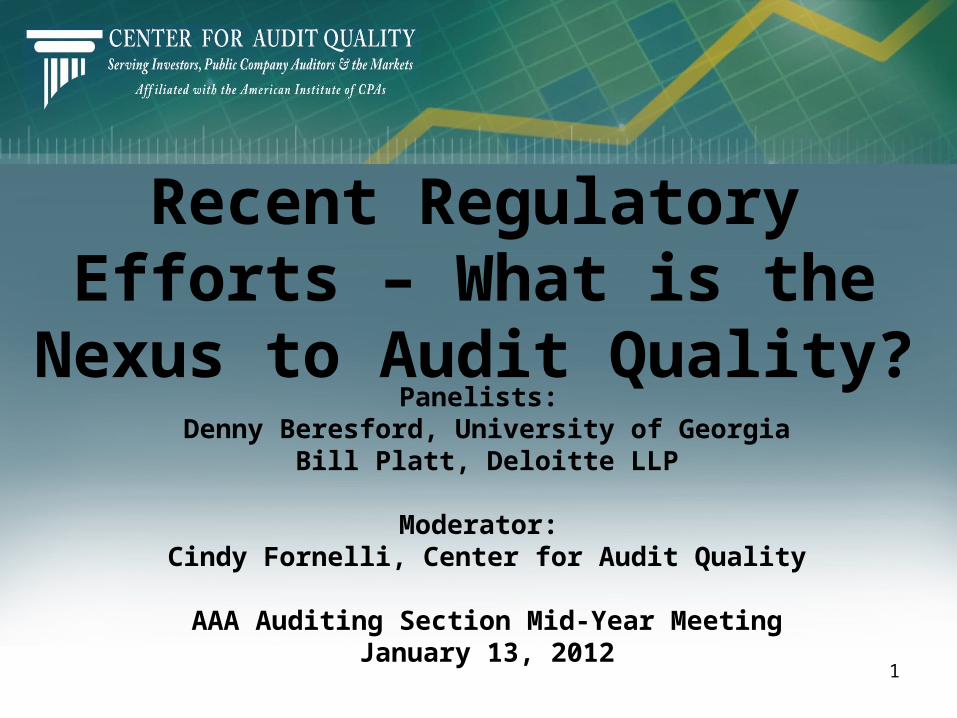

2

Auditor-Audit Committee Communications• PCAOB issued reproposed standard Dec. 20; comments due Feb. 29 • Seeks to enhance relevance and quality of communications

between auditor and AC• New requirement that auditor communicate to AC any significant

unusual transactions• Reproposal reflects PCAOB’s oversight of Broker-Dealers,

implementation of new risk assessment standards• Requirement in original proposal that auditors evaluate two-way

communications process deleted• Requirements concerning auditor communications regarding

management’s CAE streamlined

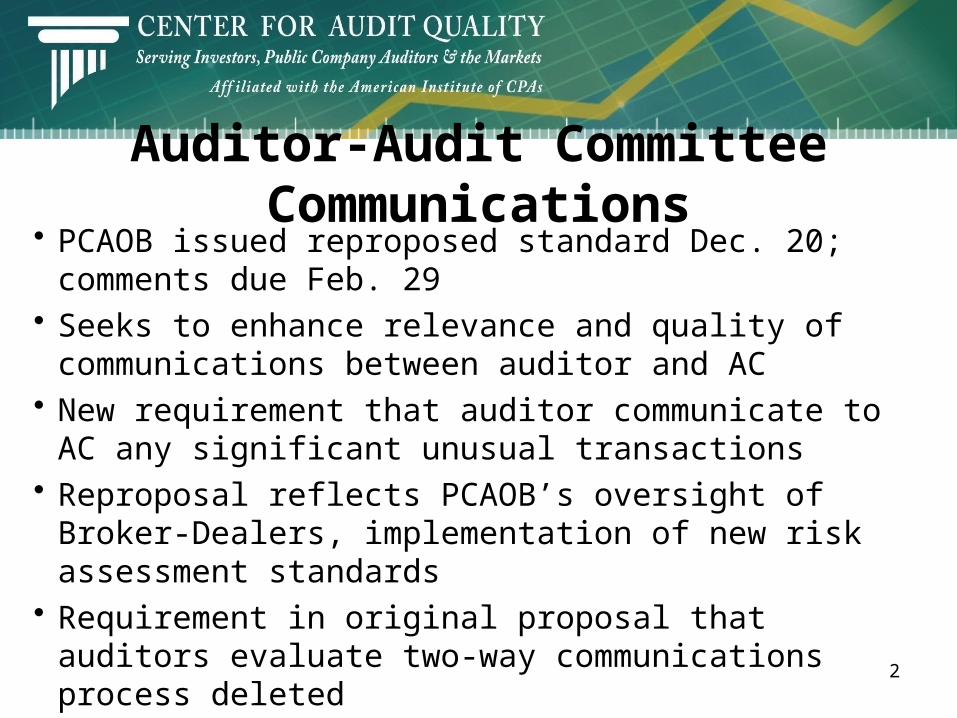

3

Mandatory Firm Rotation• All in process share common goal of increasing audit quality, of

which skepticism and objectivity are key components• Further, MFR would undermine the authority and responsibilities

of audit committee• No studies suggest a negative correlation between audit quality

and long-tenured engagements• Majority of comment letters received were critical of MFR as a

solution• CAQ, NACD and others are developing constructive ideas to

increase objectivity and skepticism• PCAOB Roundtables beginning in March

4

Auditor’s Reporting Model• PCAOB will issue proposed standard in Q2 2012• CAQ comment letter on concept release included

proposals for consideration:– Auditor association with Critical Accounting Estimates

disclosure in MD&A– Use of expanded emphasis paragraphs in the audit report– Addition of clarifying language to standard audit report

• One approach raised by the PCAOB – an Auditor’s Discussion & Analysis – is problematic

5

Implications for the Future?Other proposals – PCAOB Engagement Partner Identification proposal, European Commission legislation• If all that we’ve discussed today is enacted, what are the

implications for the profession? • What are the implications for the academic community?• What will the impact be on the pipeline?• Do new regulatory proposals present opportunities for

research?

6

Implications for the Future?

To view the video, please click the link below:

http://www.CAQforinvestors.org/

The System of Investor Protection

7

The System of Investor Protection

8

COMING SOON – Ledger & team in a new video!

9

www.TheCAQ.orgTwitter: @theCAQ