Embed Size (px)

Citation preview

rmNc, iuriReport No. 560a-MAI 3-Excutive Directo

r ermanent OfficeCp

Recent Economic DeveloD fe Copy

and Prospertc of M&AbAXAiLAIMA I -.9 r~ % L--F -. I I U 11-4114V v I

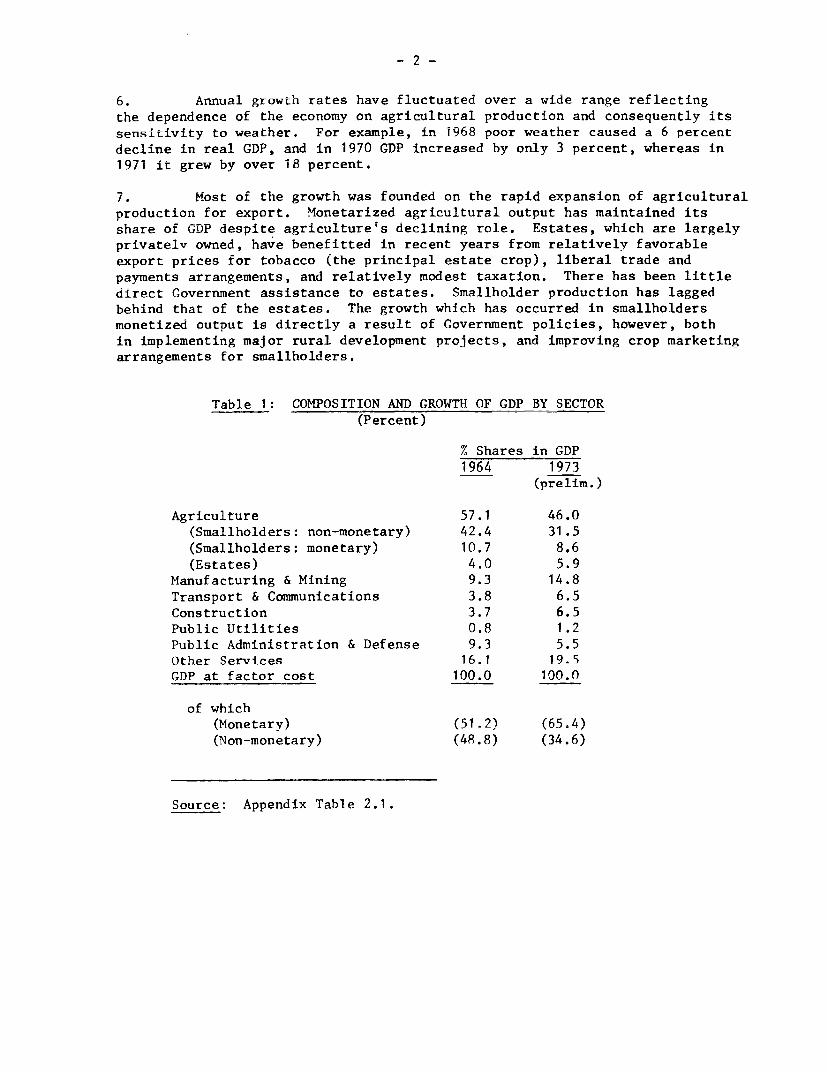

January 14, 1975

itU4111y rurogdrams DepaLtmnLuLt 11

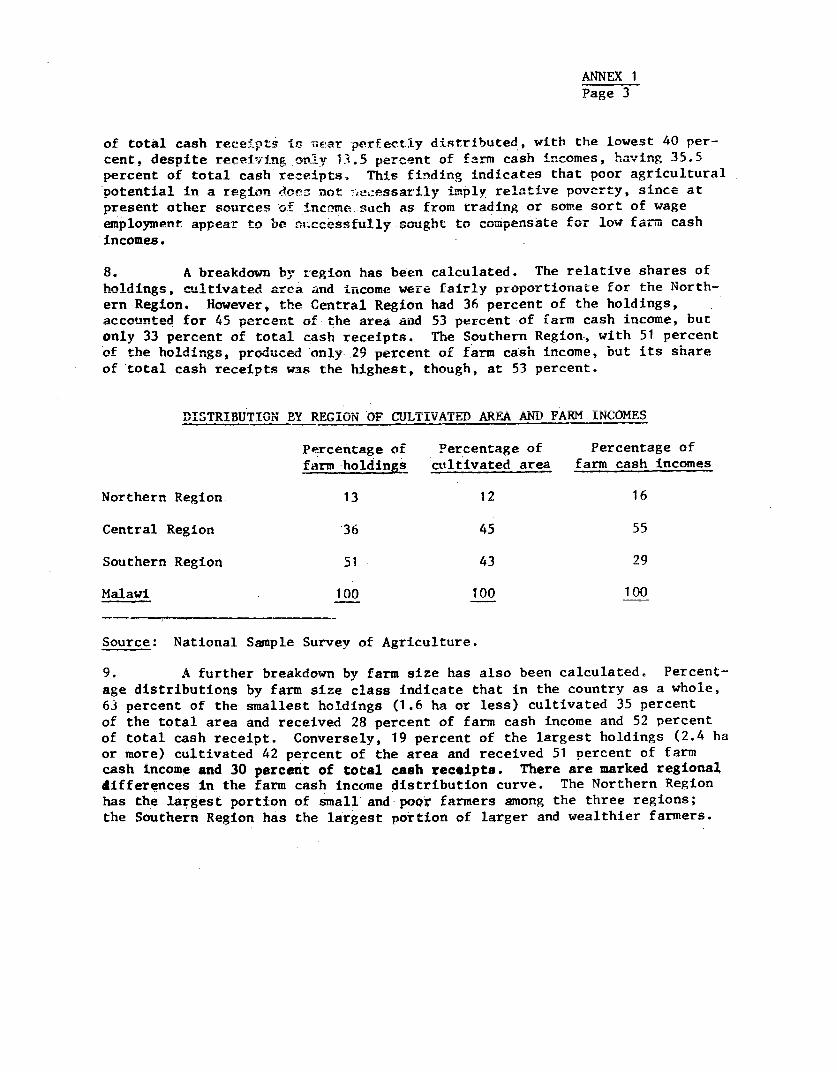

Eastern Africa Region

Not for Public Use

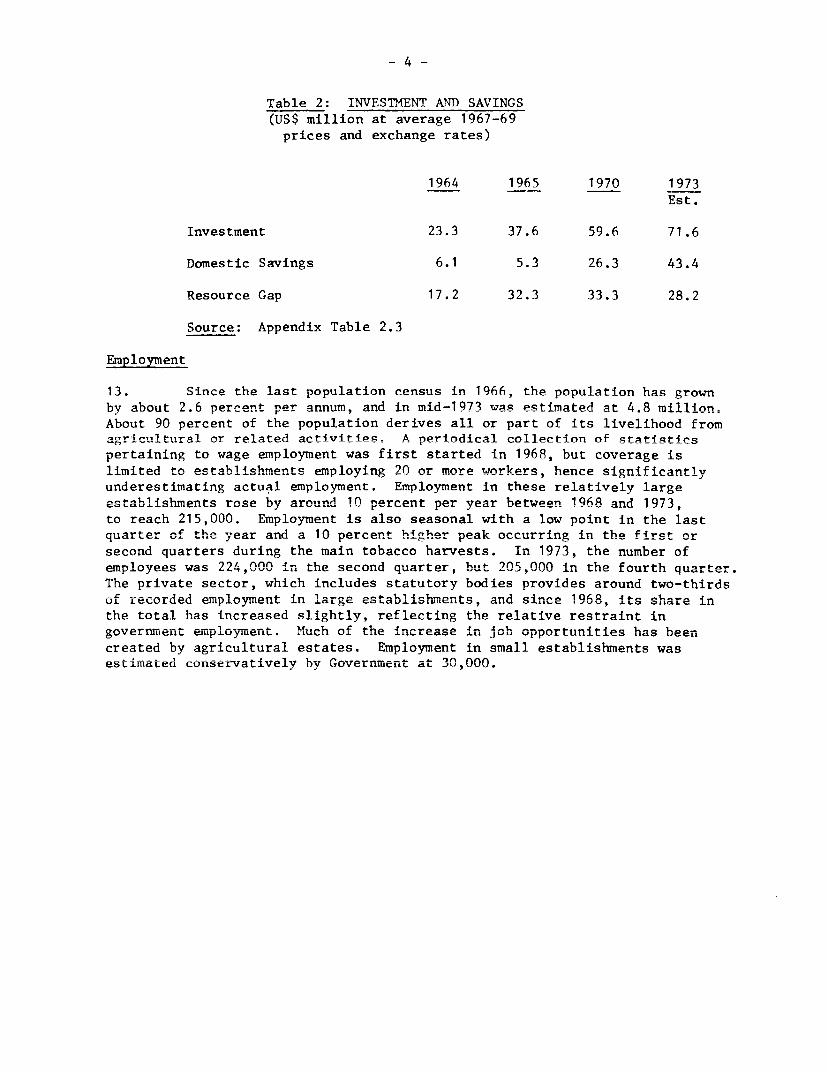

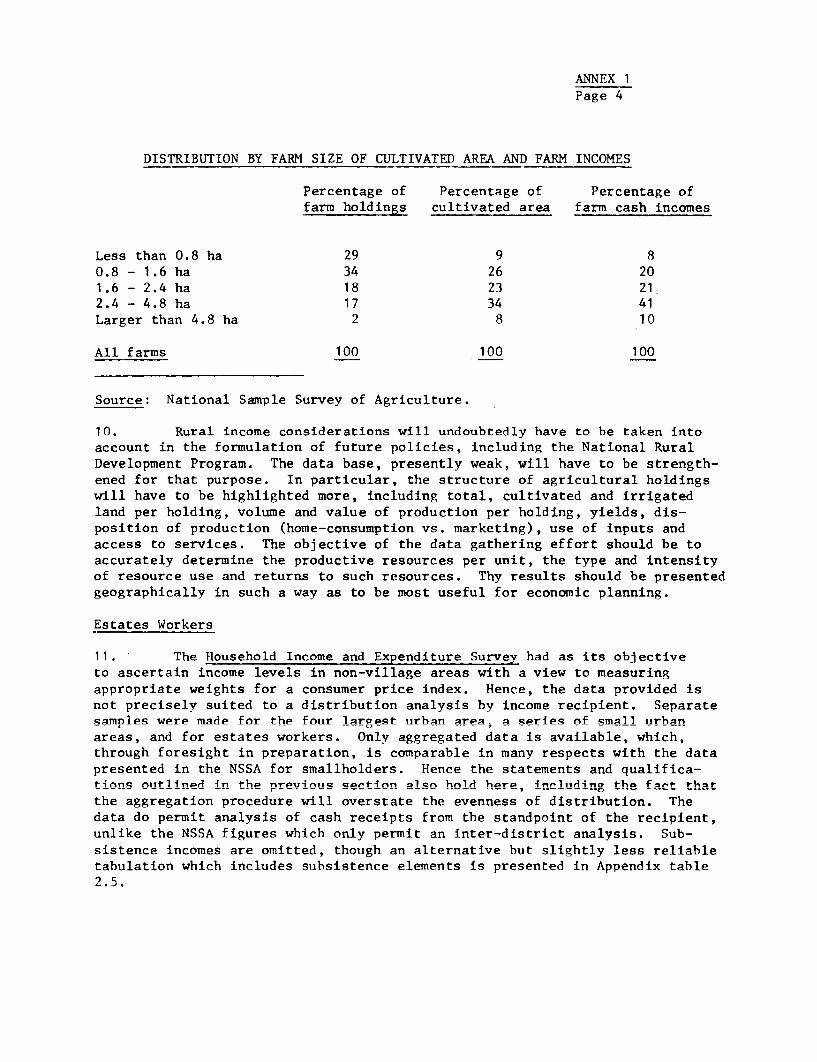

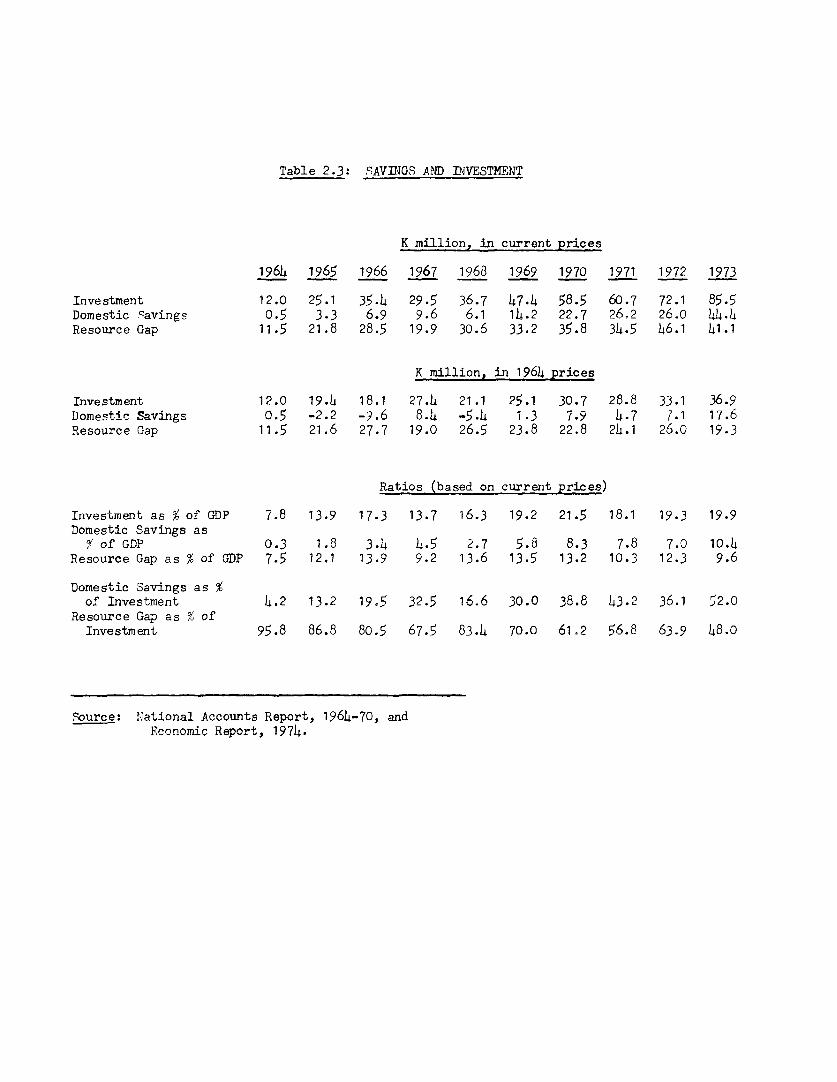

Document of the International Bank for Reconstruction and Developmentinternational Development Association

_ _11 ___

This report was prepared for official use only by the Bank Group. It may notbe published, quoted or cited without Bank Group authorization. The Bank Group doesnot accept responsibility for the accuracy or completeness of the report.

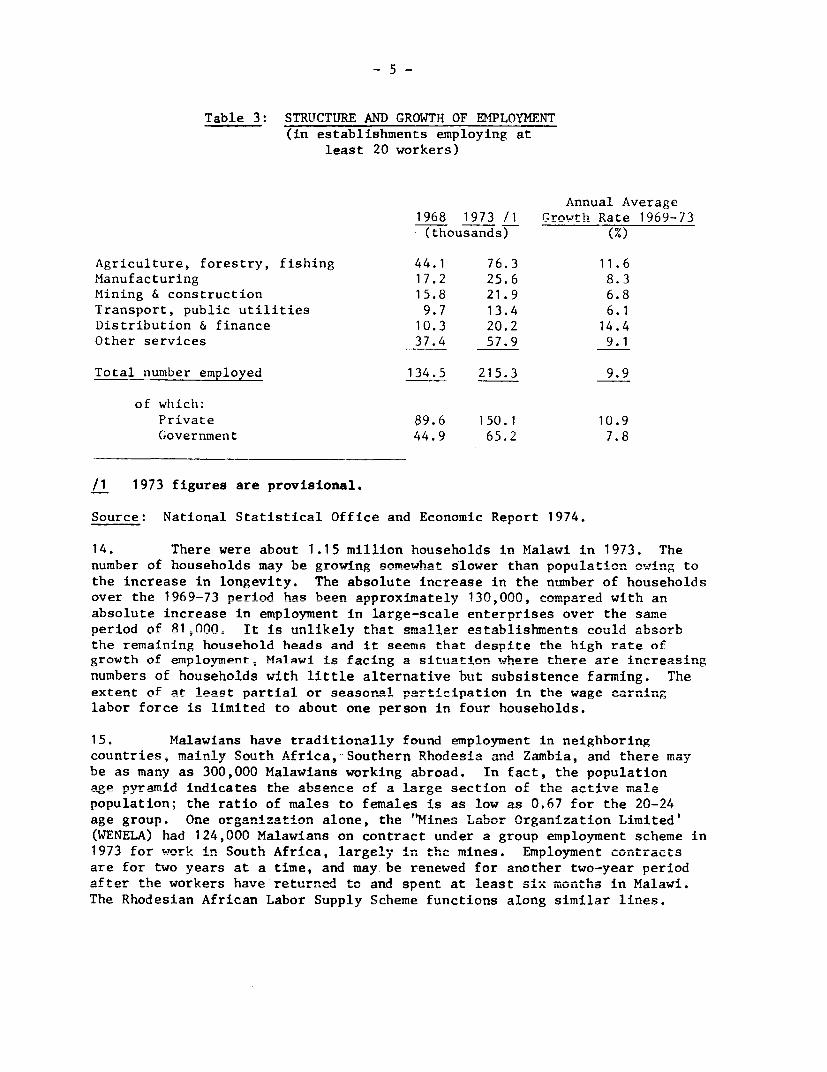

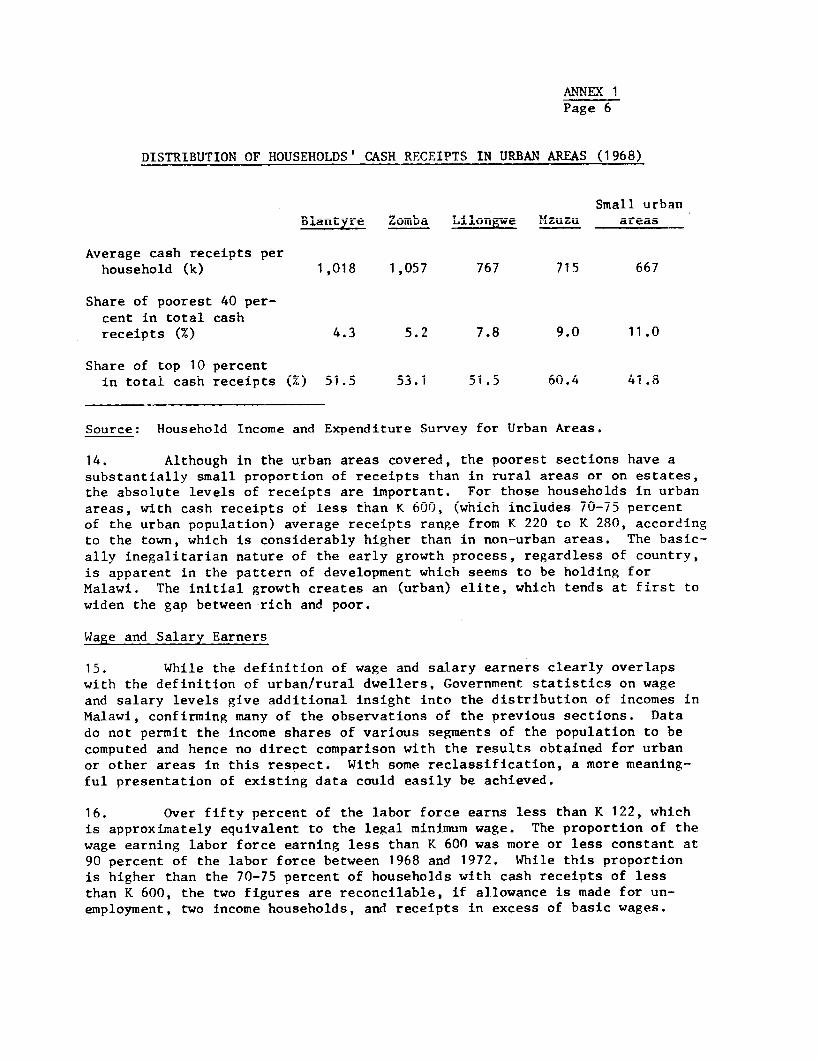

Pub

lic D

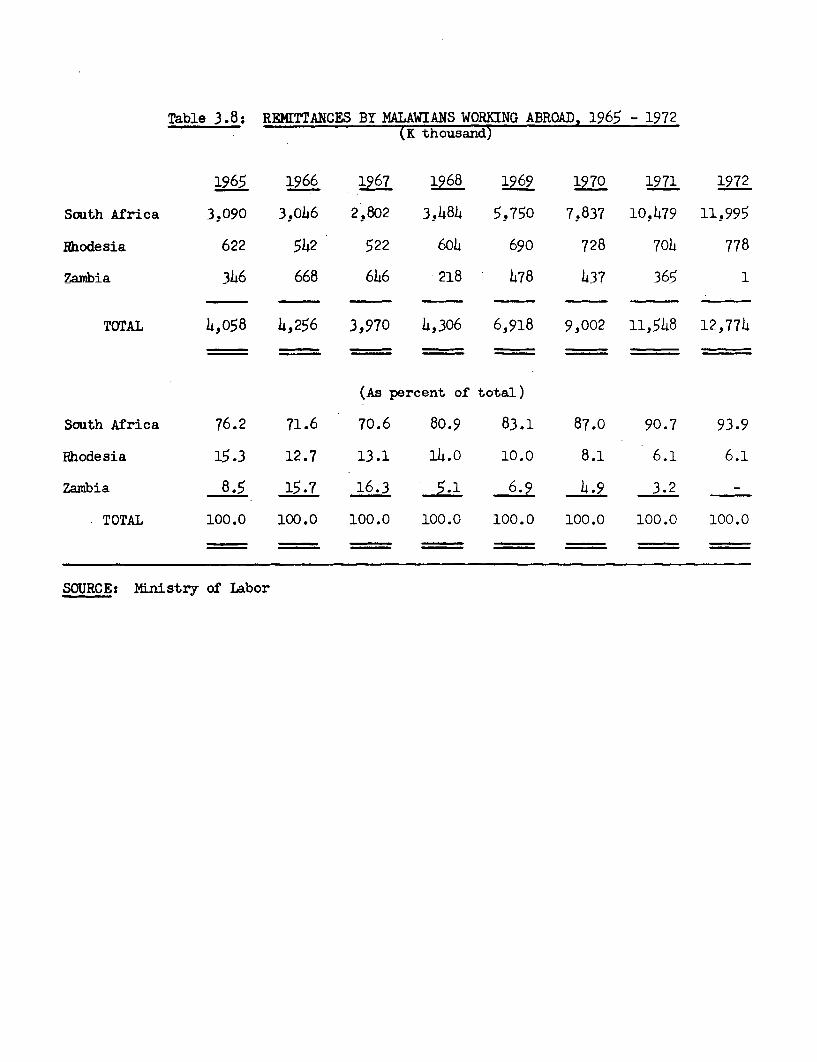

iscl

osur

e A

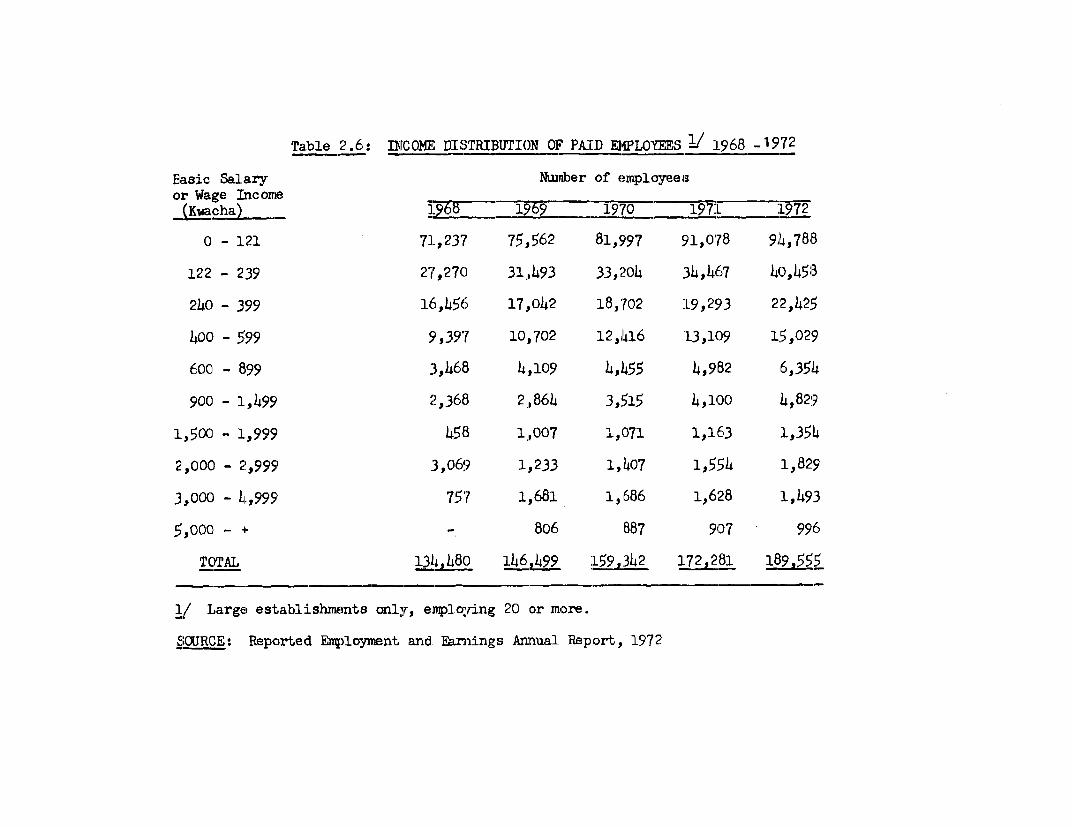

utho

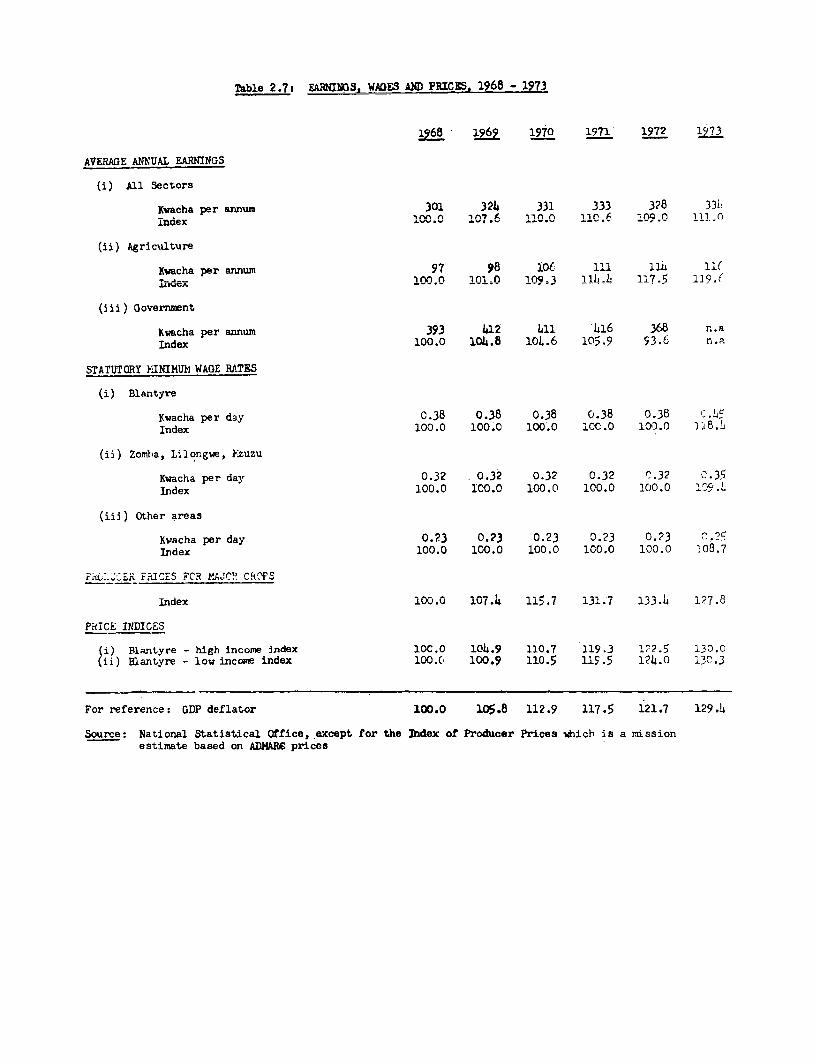

rized

Pub

lic D

iscl

osur

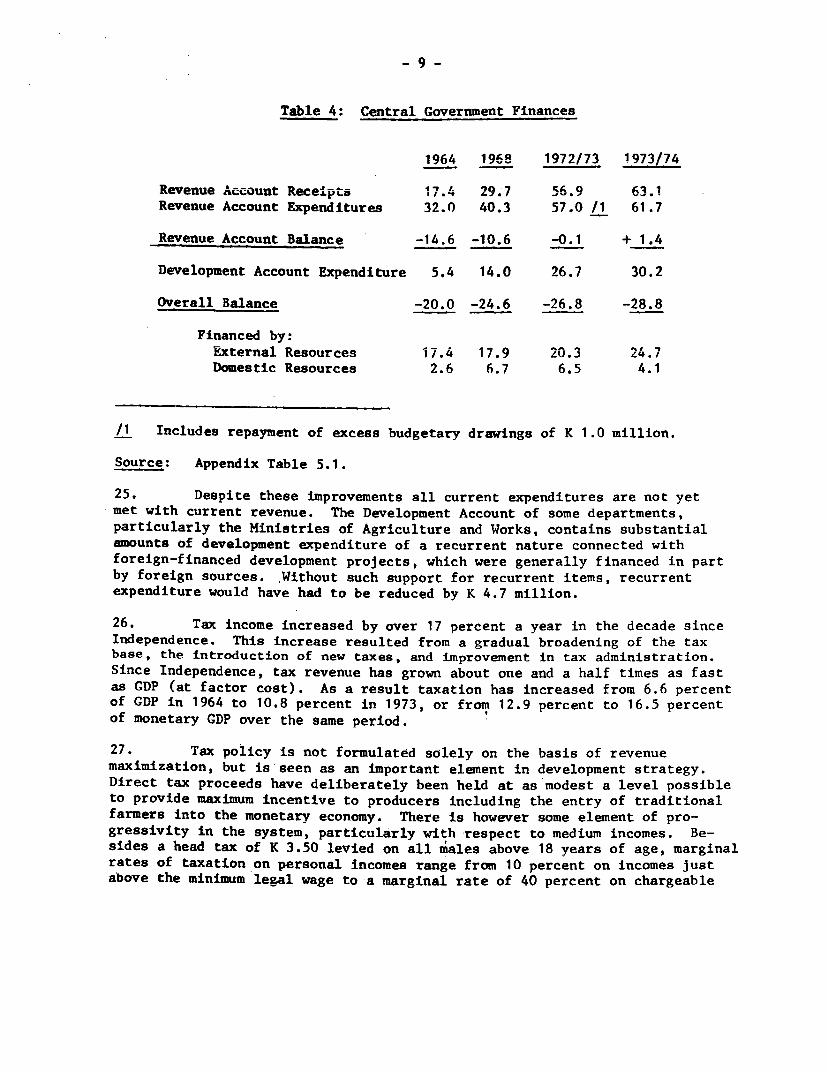

e A

utho

rized

Pub

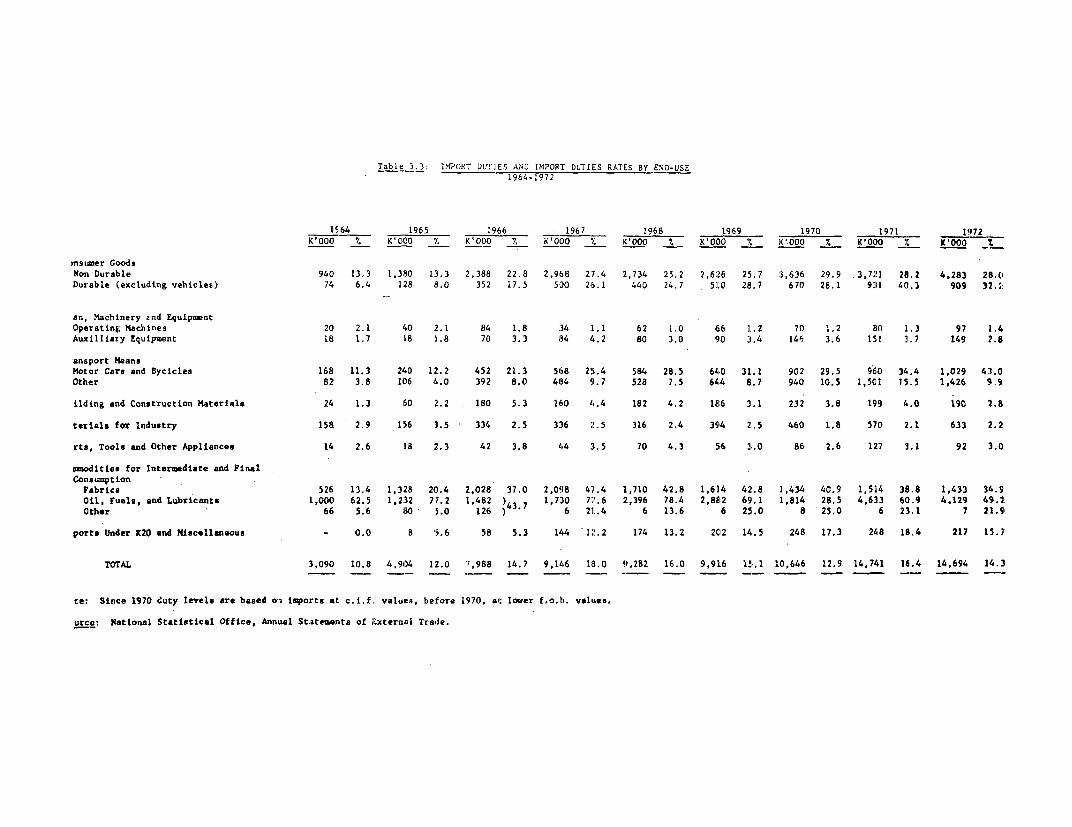

lic D

iscl

osur

e A

utho

rized

Pub

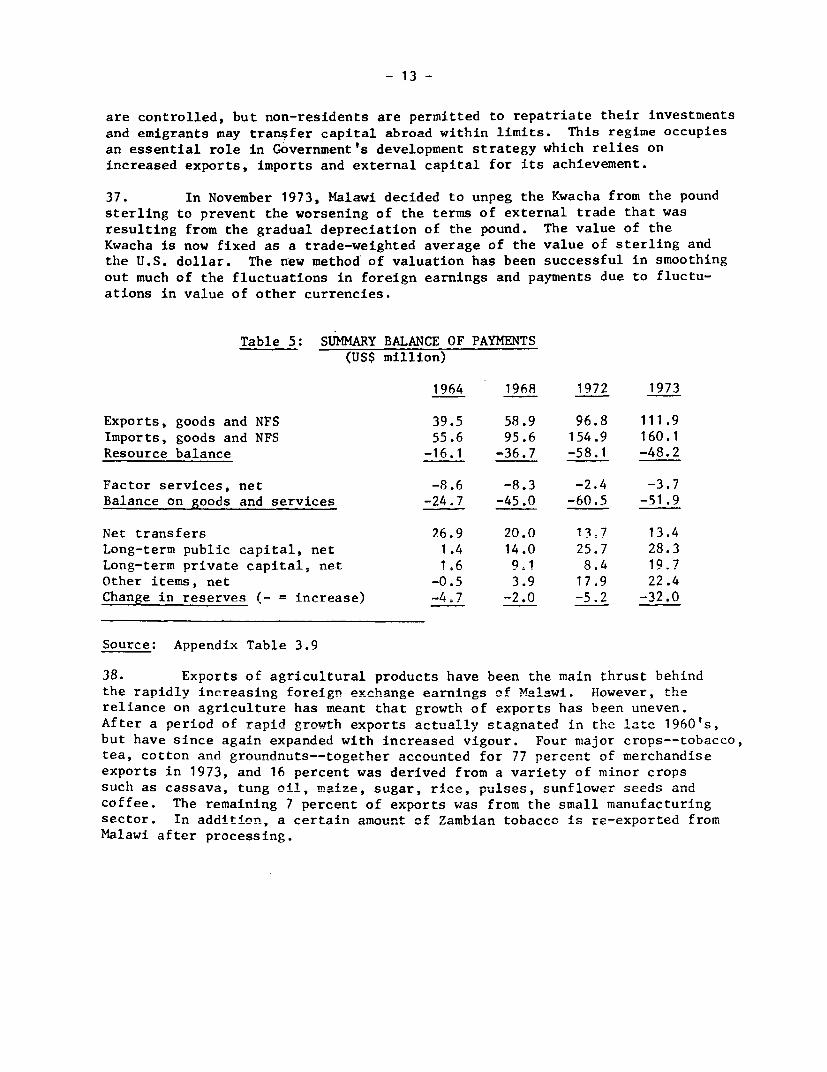

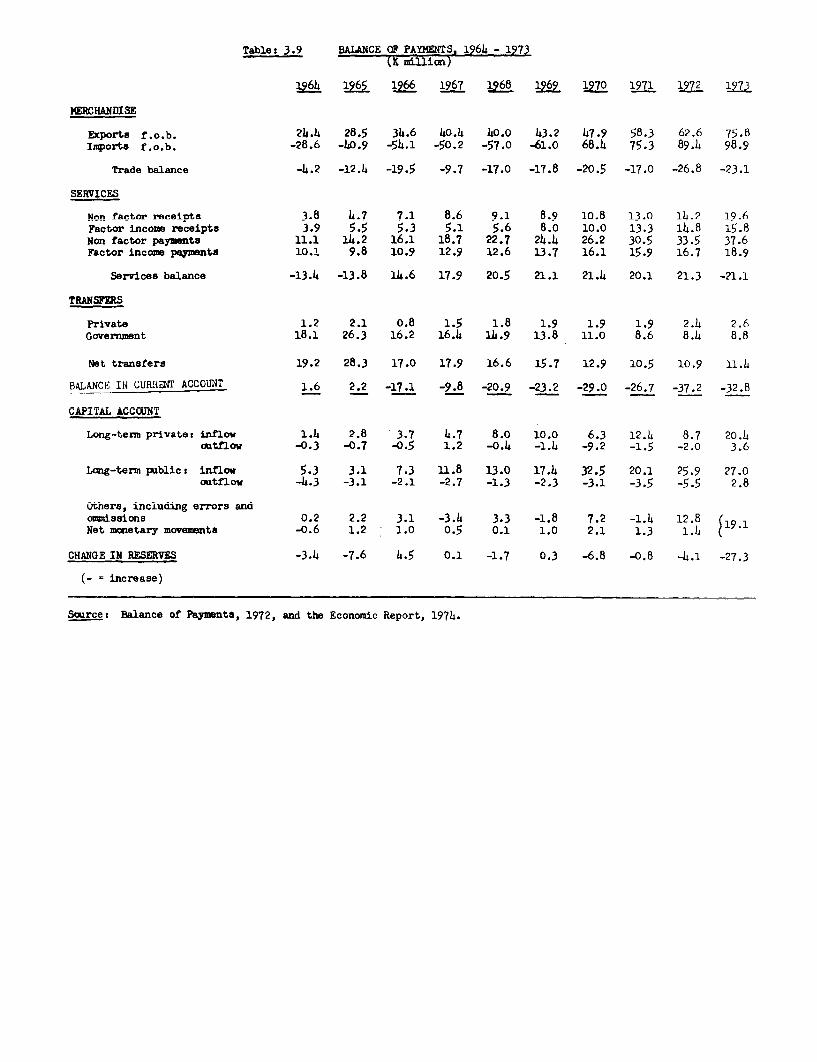

lic D

iscl

osur

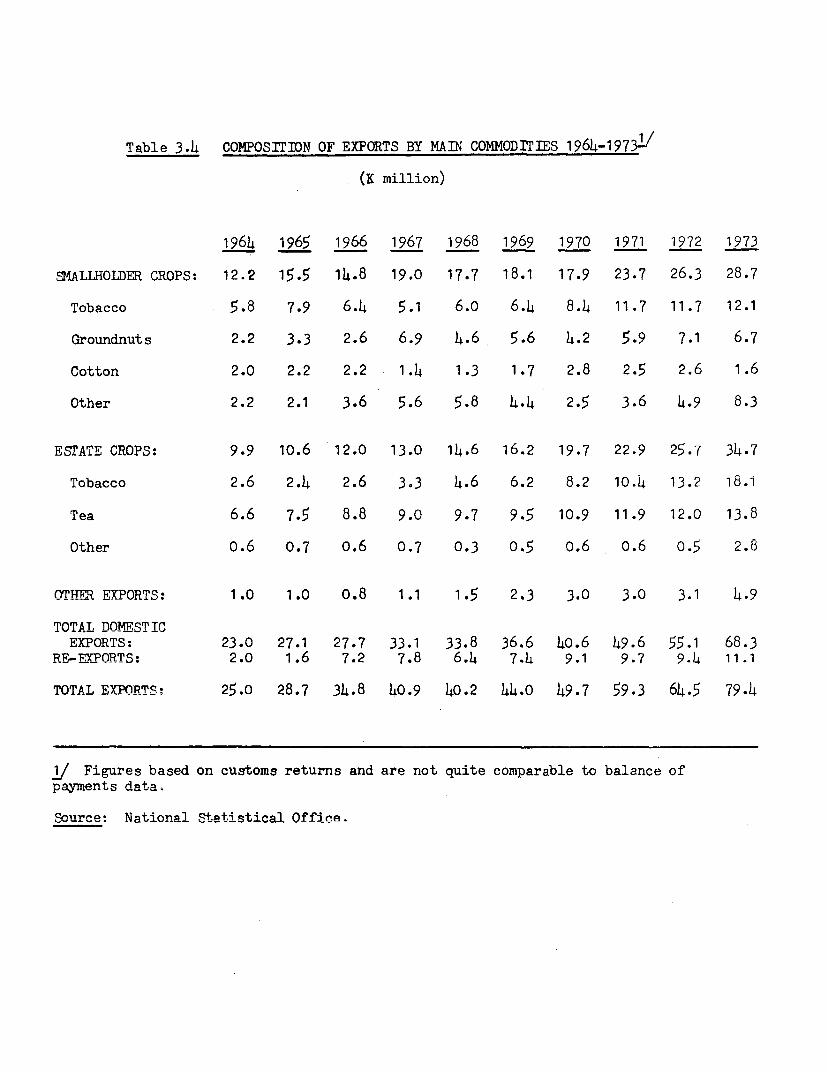

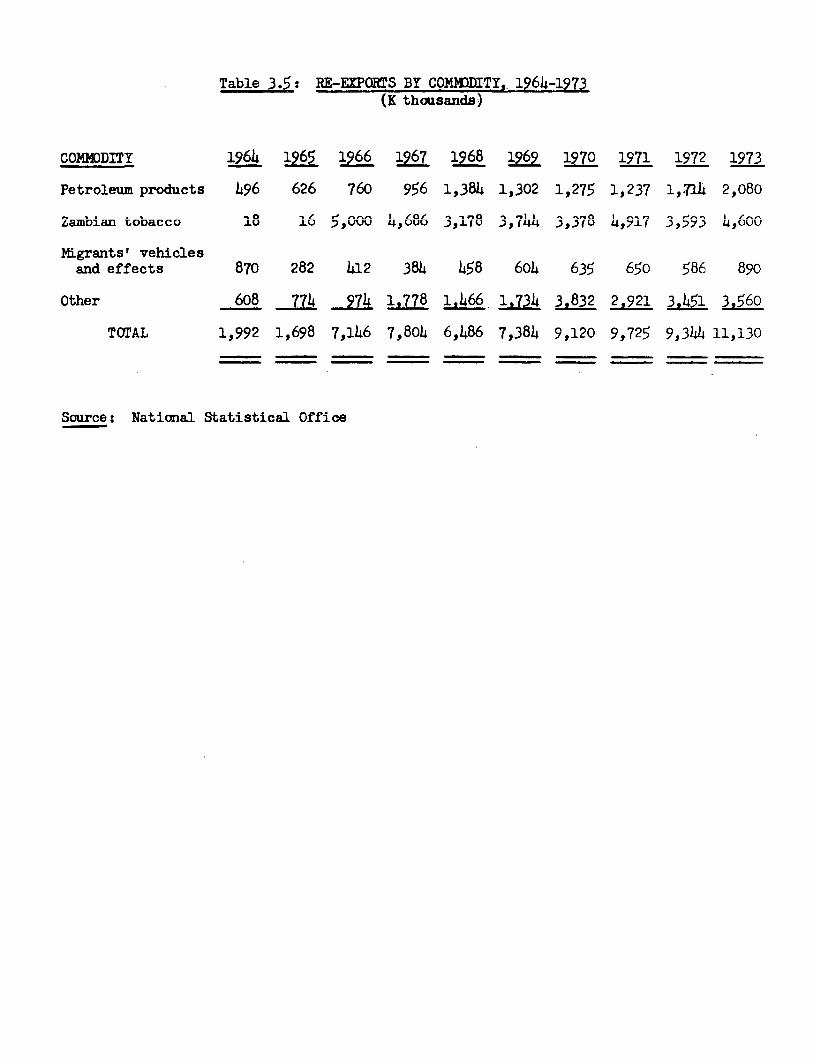

e A

utho

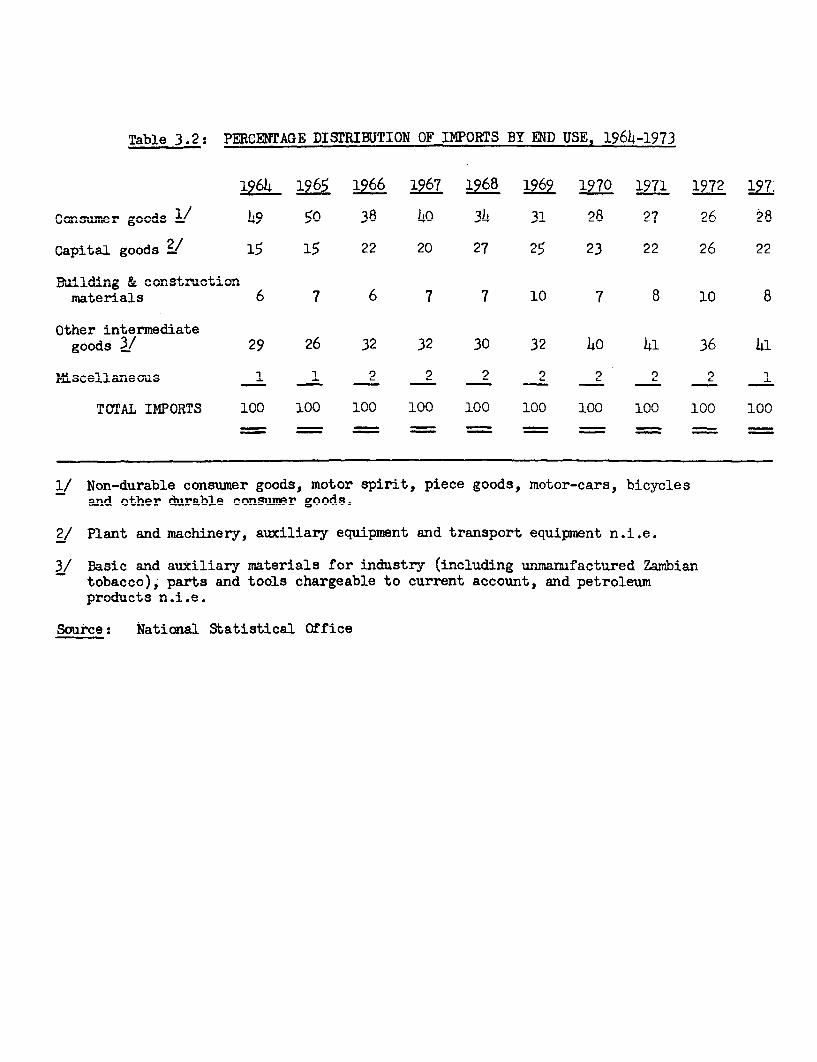

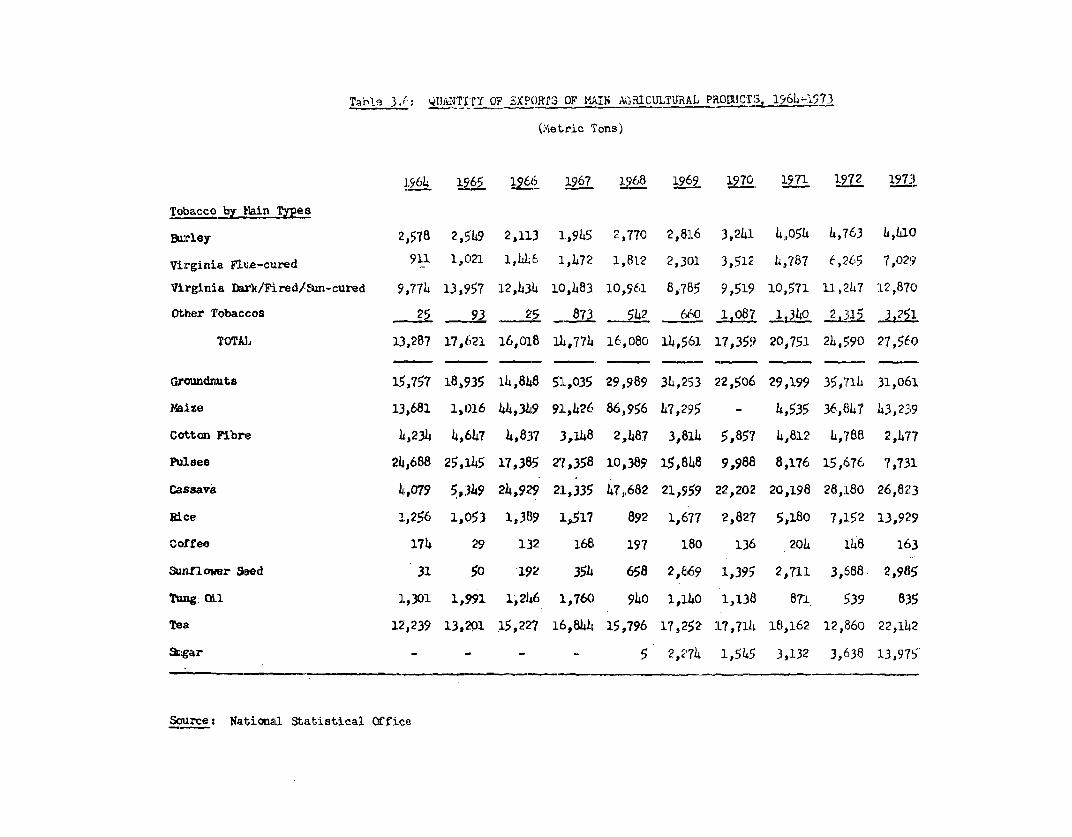

rized

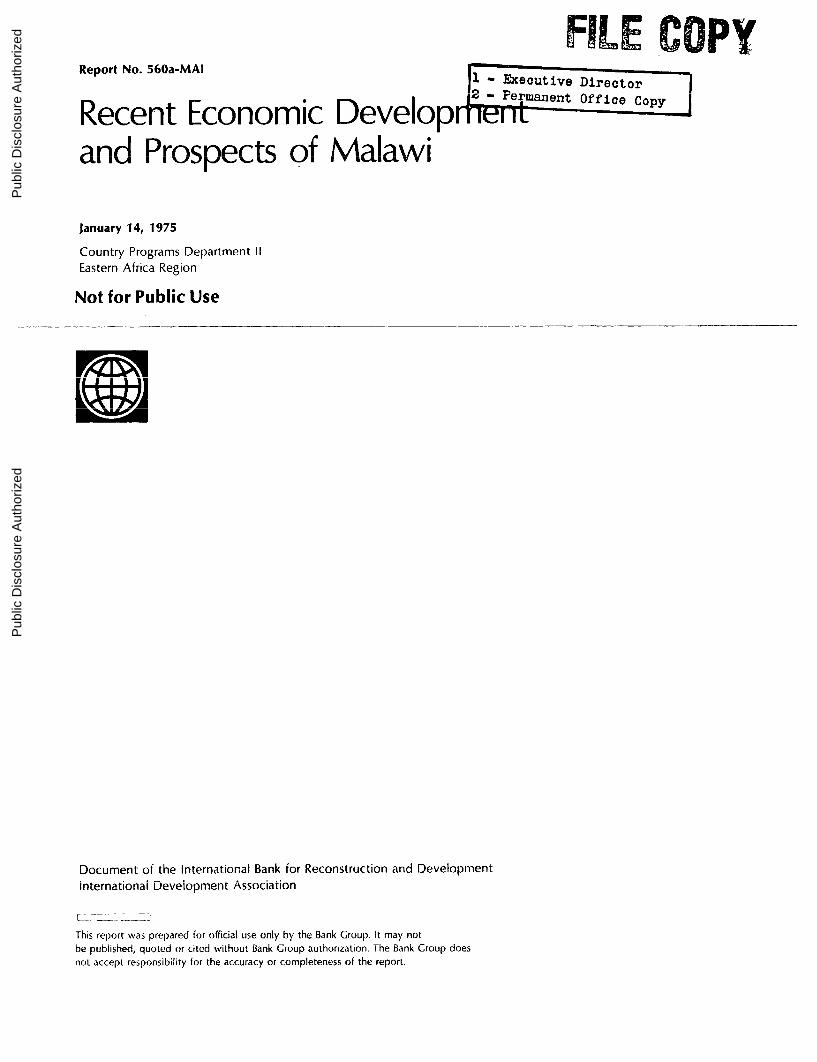

CURRENCY UNIT

The Malavi Kwacha (K)

K3CGAN(YE RATE

The Malawi Kwacha was pegged to thp npond. sterling intil Novem.ber 1973. Sincethen, it has been calculated on a daily basis according to a weighted averageof the TUS '$ and the pundn- For the prn-ose of this rep-ort,- tihe foel ova-I

exchange rates have been used

1964-66 1967 1968-70 1971 1972 1973 1974

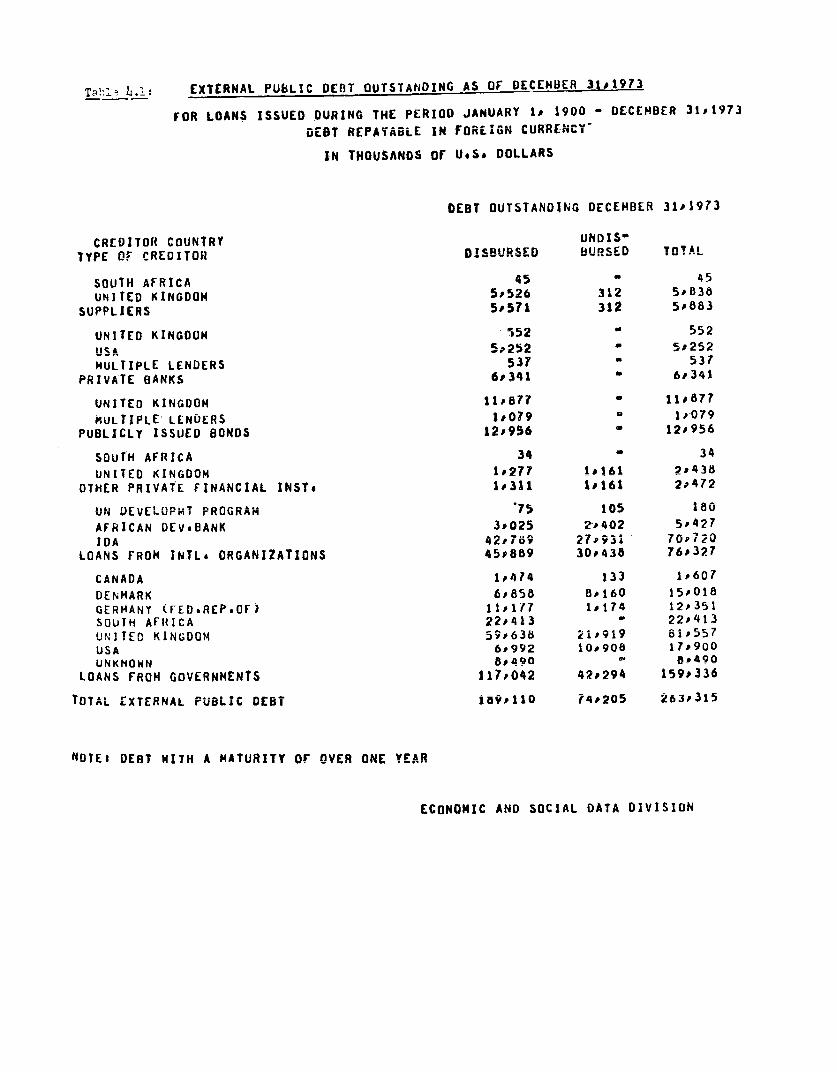

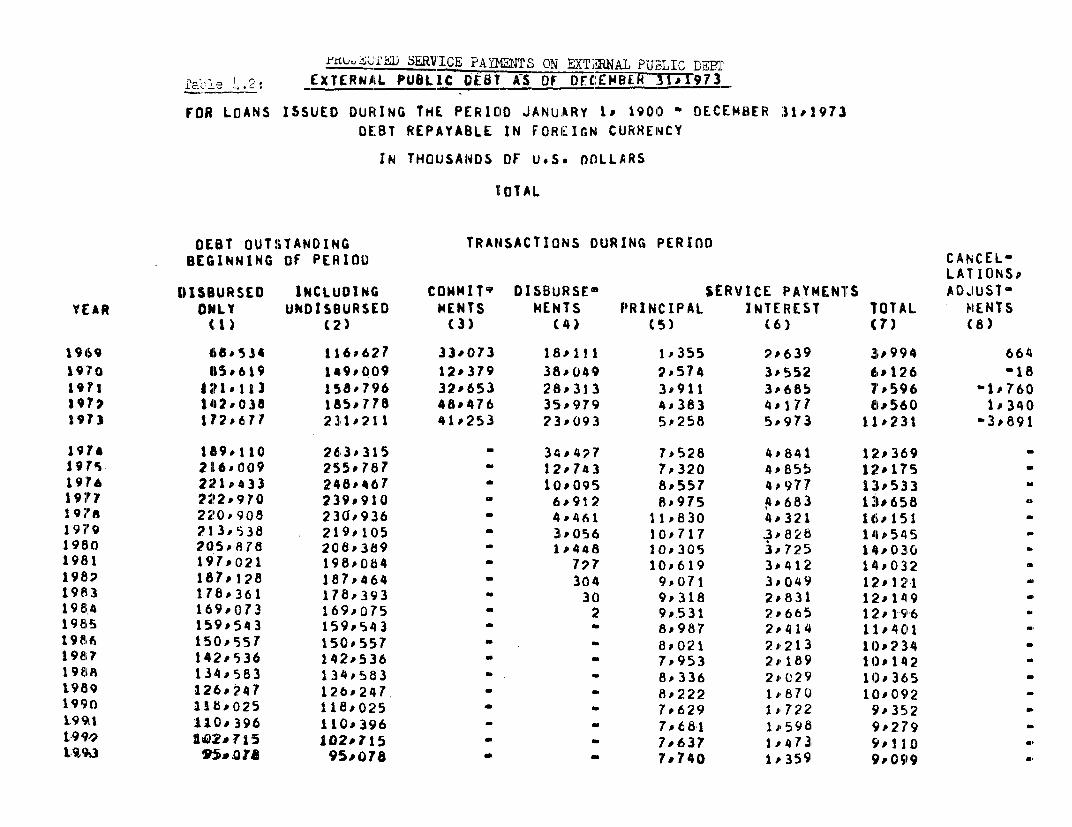

K1.00=US $ 1.40o 1.383 1.200 1.216 1.260 1.173 1.200US 1 .00=K 0.7?1 0.723 o.833 0.822 0.794 o.853 0o833

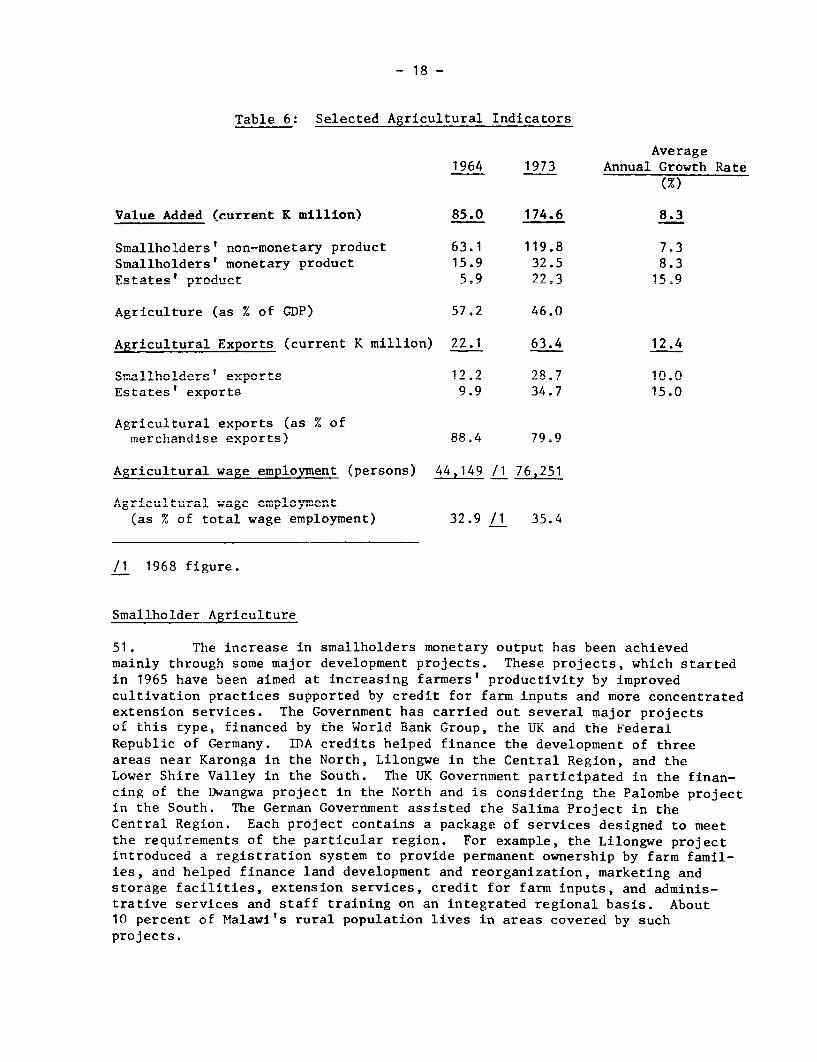

FISCAL YEARS

January 1, December 31 until end 1968Januarv 1. 1969 March 31. 1970 (15 months)April 1 - March 31, since 1970

WE;T.TlTS ANTl MEASTTRES

Al thouih M>l.ri is offini nl lv ronvert.ina from the nRritiih Tminn?r_al

system of measurement to the-metric system, practically no metric unitsare as yet in commnn usage. Many nrnits in this report have had to beconverted.

1 kilometer = 0.62 mile1 square kil. = 0.3861 square m,ile

1 hectare = 2.47 acres1 r+tr c +on = 1.10 long ton

0.984 long ton

TABLE OF CONTENTS

Page No.

COUNTRY DATA

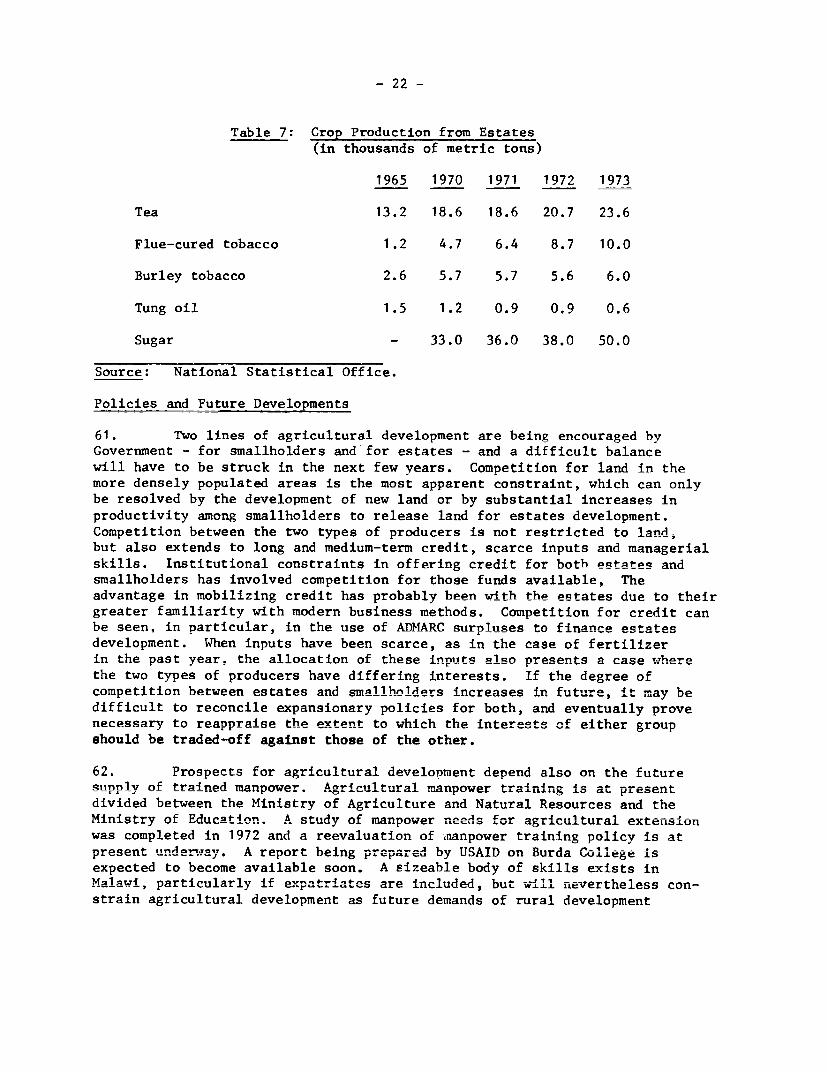

SUMMAR-Y AND CONCLUSIONS .......... ........ . i L iii

I. * INTRODUCTION .................................. .

II. RECENT ECONOMIC DEVELOPMENTS ........... ..........

A. The Growth of the Economy ...... * ........ 1

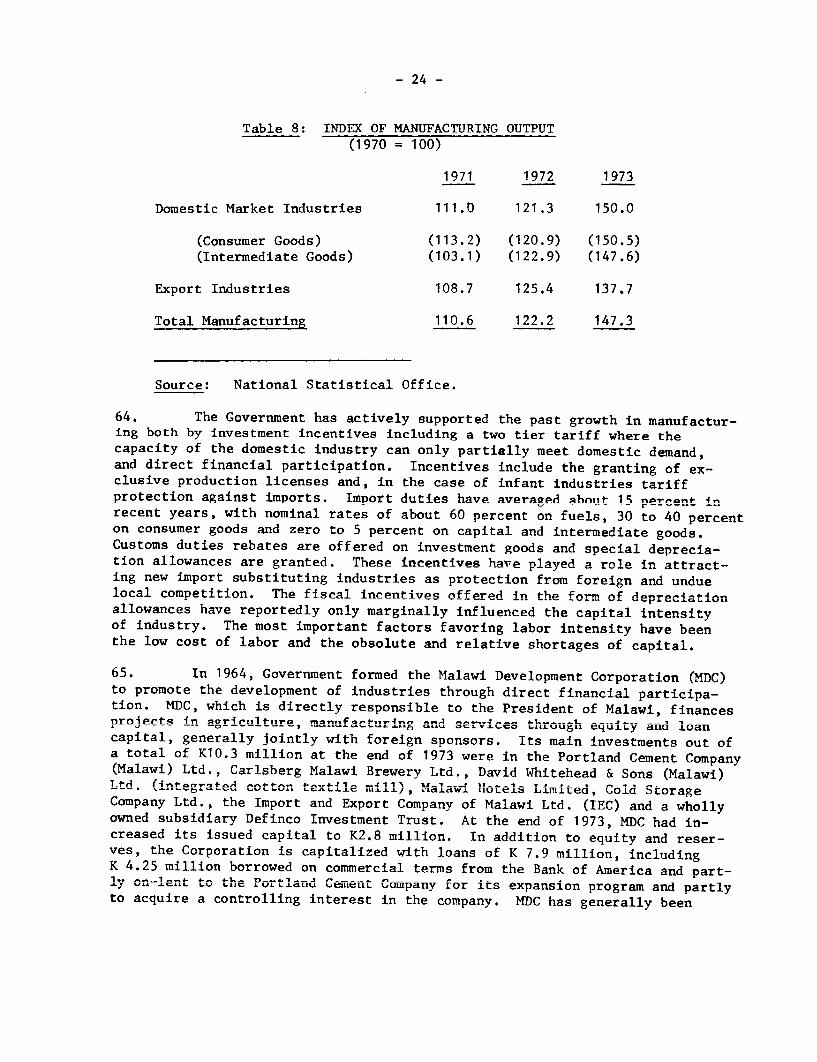

Output ...... ,.. ........

Savings and Investment ................ 3

Employment .. . . .......... 4

B. Income Distribution ........ 6

C. Public Finance . ............... 8

D. External Financing . ......... * ..........*.*.*...*.*. *, 12

III. MAJOR SECTORS ... 16

A. Agriculture ................ 16

Smallholder Agriculture .... ............ 18

Estates Agriculture .................. 21

Policies and Future Developments .22

B. Industry ............. , , 23

C. Education and Training .... ** ............... 27

D. Transport ........................ . 30

IV. POLICY ISSUES AND PROSPECTS .34

ANNEX 1 - Income Distribution

STATISTICAL ANNEX

MAP

This report is based on the findings of a mission that visited Malawi in

April/May 1974. The mission was composed of Roger Kev (mission chief),

Gottfried Ablasser (agricultural economist) and Andrew Hilton (economist).

LIST OF TEXT TABLES

1. Composition and Growth of GDP by Sector

2. Investment and Savings

3. Structure and Growth of Employment

4. Central Government Finances

5. Summary Balance of Payments

6. Selected Agricultural Indicators

7. Crop Production from Estates

8. Indes of Manufacturing Output

9. Projected Production of Major Crops

10. Projections of GDP by Sector

11. Projected Savings and Investment

12. Projected Real Resource Gap and Financial Gap

13. Projected Balance of Payments

14. External Public Debt and Debt Service

Page I of 3 paegs

ODMnRY DATA - KALAWI

AMLA PCUI.ATION NSITY!IR 1,8km 2e Tr.7__liic (eid-197 2)

102 Psr ka2of arable land

SOCIAL NDIATOfiS

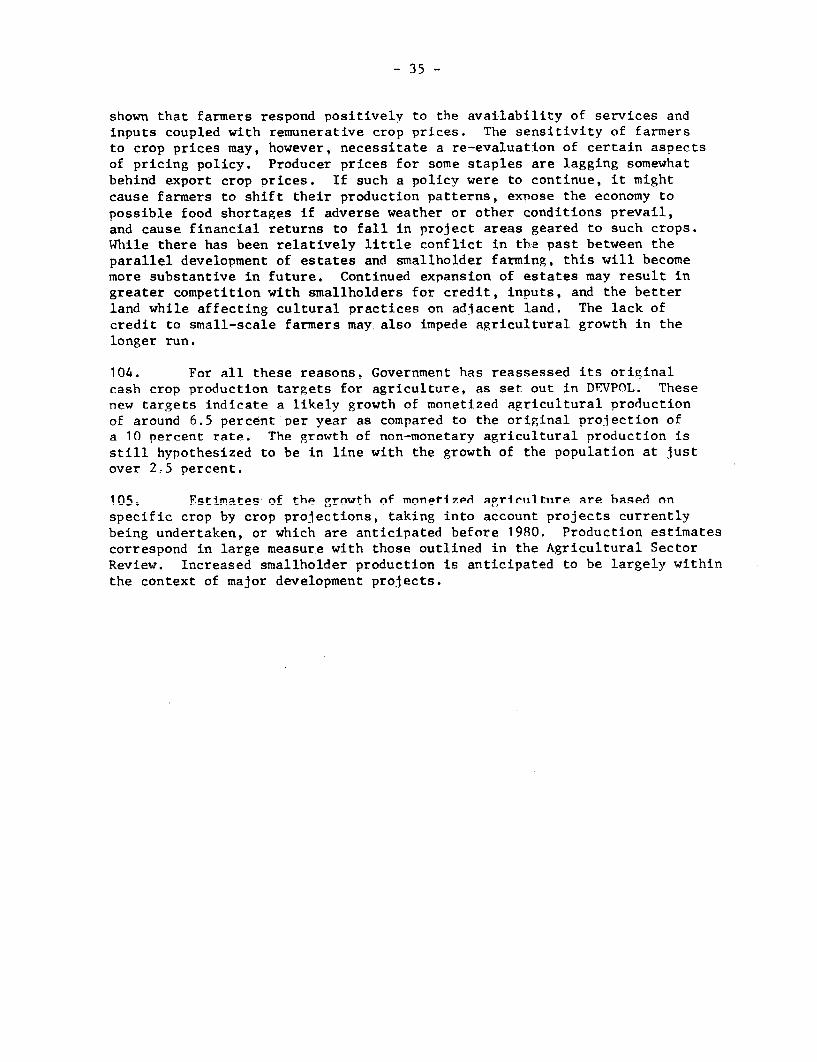

Reoferenoe CountriesNKIAVI ~ Somali Tansania Ys...

MNF ZRE OAflT U (,%TIAS BASIS) 1 .. i /a BOL /a 120 3,670 A

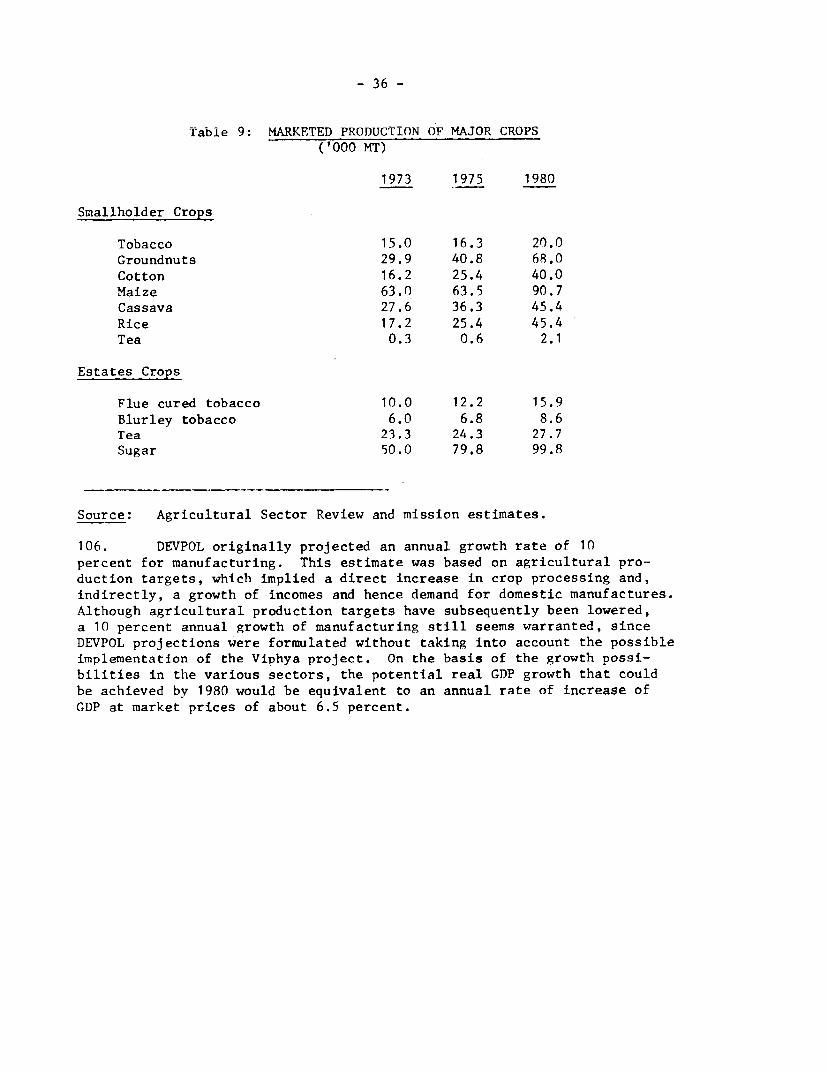

DUMORAPMCM MM- rate (per tousand) .. 54 Lb [.7 47 /9 14~.4

Crude teath rate (per w.ocusansd) . 22 22 / .

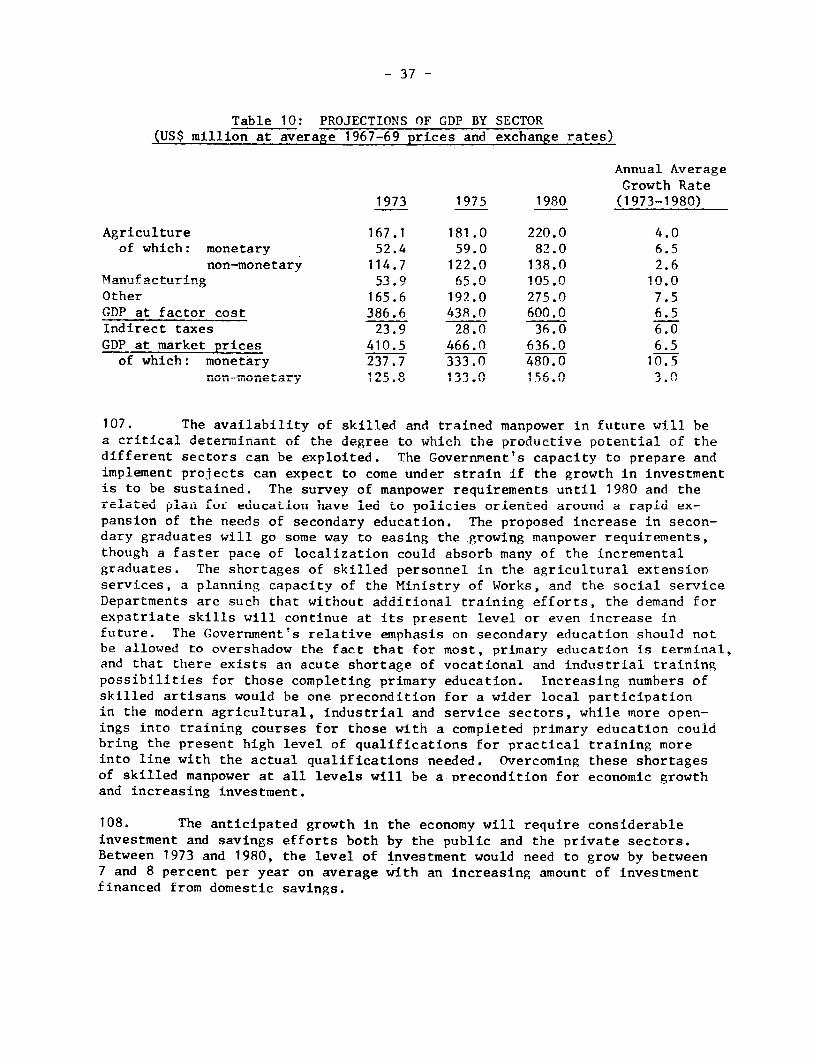

rnfant mertaility raet (Per thousand lise births) I8.8 Ld 16m65i 1,38 39 11. 3 73

Gpo., Me ductiw. rate j2 3.2 3.2 3.0 3.2 1.2Population growth rate tj2.2 2.6 2.4A 3.0 0 7PPpulation growth rate - urban 7Lf 7 5 .. ~6.2~Age structure (persan t)

0-in L.SA 8./ 146 C 23.715-66 5o7 527 52 5 4 65 ced over S7I 4. 234 .9

Dersendocy ratio 1.0 X 0.9 ~Ti 0.9A~ 0.9 Tc.m 0.8

Urban PoPulation as psroent of total .. 6 ~.6/bco 80 Family planning: NM of acoeptor cumulativs (thou..) ..

No. of uoors (1 of married wmen) ..

ToMMbor form. (thouaaods) .. 2,300 If 1,002 La 5,750 /c.h 2,100 loPercetage employed in agriculture .8 808/ch 1Percentage umemployed 8. if 20 88. 3c l

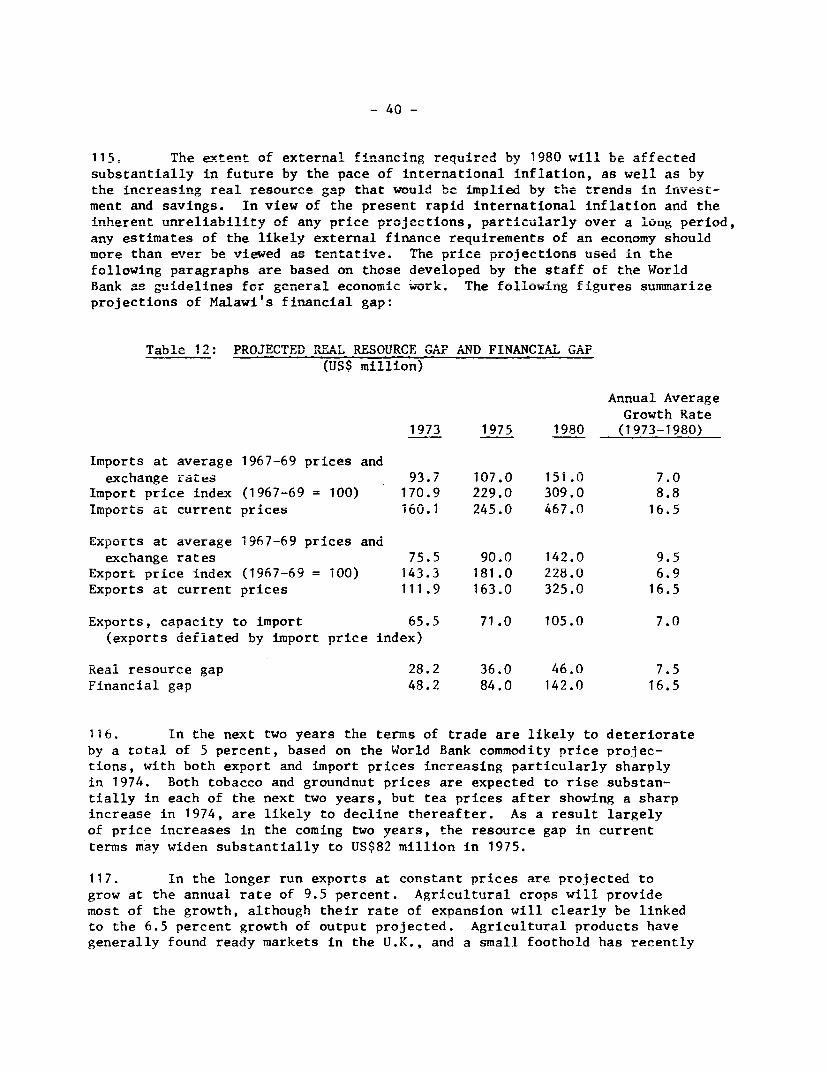

I DISTRIBUTIONPeroent Of naionlh6J income reoeived by hbltest 5% .. 27 ~.X,_ a . 34. 22 9.!Pearoeart of national moons received by highest 20% 44i./ai . 60 / 18 5Peroent of nainlinocome reneived by lowest 20% 4.1 . LPercent of national income received by lowest 40% .. 21Jsa IC1. Ic 1. /.o

MISMtI?0 0F LARD OiNCmHIA owned by top 1(5 of aes...

o-med bY aaelleat 10% of cvaers ..

N M P ca 35,000 A 75,250 21,180 fl,570 /h 690Population Per borning person . 16.090 a 3 .220 /u 1,890 Th 210population per hoepital bed 94.0 v 68.0 570 - 702 7h 100 /W

Per capita calorie supply as % of(requiramonta 78 98 72 Li 69 119Per capita Protein ouPPIY, total (puce per day) L6 9 /x 63 57 y 1.3 89

Of Which,eaniua and pulse 6 7 36Death rats 1-4. yeers /76T 9. 27 .. 23 0.62

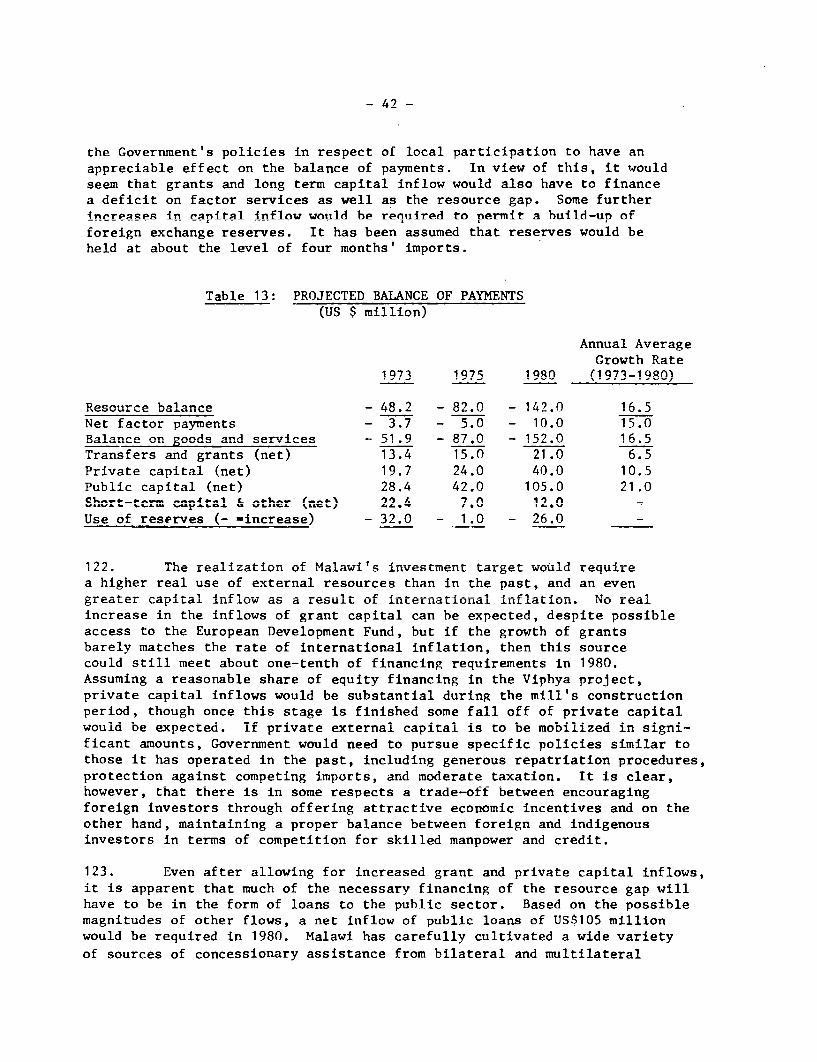

Aijia 8 prmay chool enrafleent ratio 39 37 10 37/ 98Adjusfted co iayschool enrollmeont ratio 1 3 4. 3/9 87Tears Of a8ooling provided, firsft and cecond level IL. 11. 11-18 13 13Vocational enroll1Ment AS % of sac, school enrollment 21. 3 2 baa 3 /q 32Adult literacy rate % 5ZZ. 7ob.ac ..- 99 lao

Ave-rage Mc. of persons per rcosa (urbans) .. 1.9 Ic . 0.9 /0dpercent of occupied units without piped water .. 78/9. 4E 3aAccess to electricity (as % Of total PuPulation) .. 16 /c. 97 /adPercet of tura1 population conncted to elcrct . 0.0 _

1 Lciv ra per 1000 population 9 /e 20 18 15 /94f 325Passenger cars per 1020 population .2 /at 2 3 /9fj 219 /afElectric power consuaption (kvho p.c.) 10 ar 32 7 29 lb 2,981newsprict censumptim p.c. kg per year -0.03 /ad 0.01. 0.6 Z& 0.1 30.3

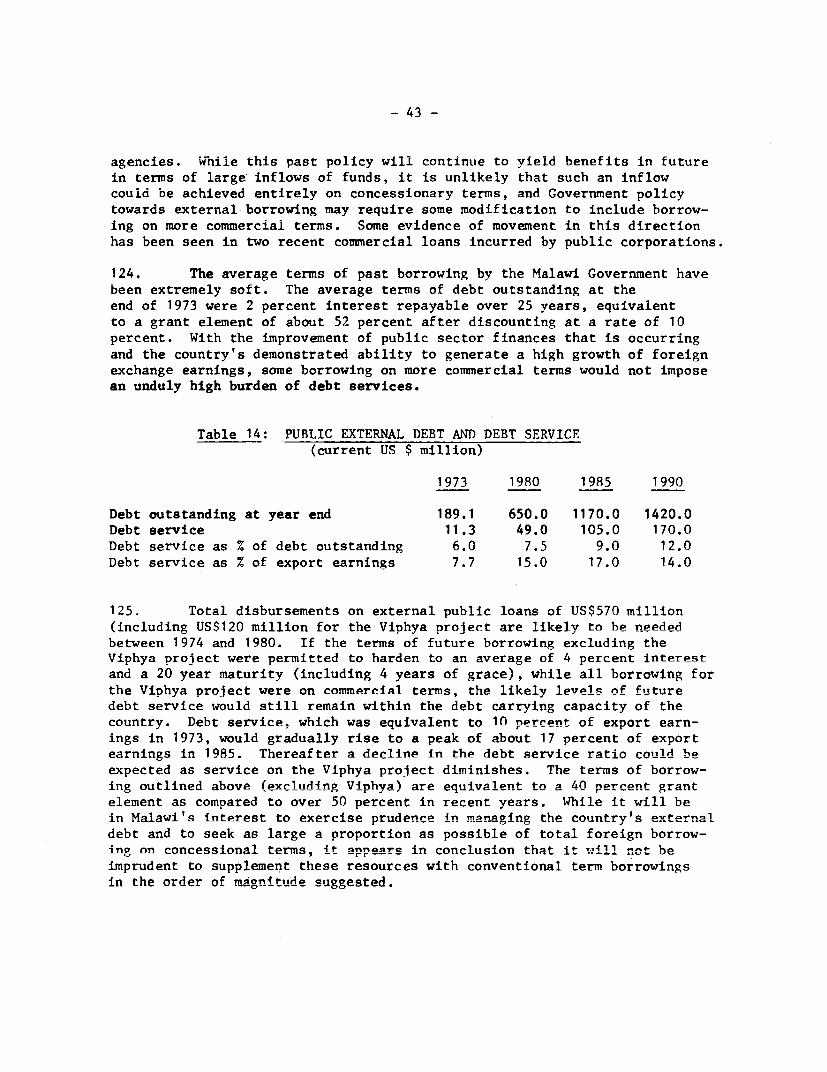

Motess Figures refer either to the latest periods or to acocousit of enviromsental temperature, body veigbt., andthe latest years. latest periods refer in principle to dIistribution by age man sex of national populations.the years 1956-60 or 1966-70; the latest years in pmi- /6 Prtein stiowdards (requir.ementso fur all countriesas tbciple to 1960 and 1970. lished by USDA Economic Research Sermite provide for~ a mininmuA9 The Per Capita DsNP esatimte ias at market prices for allowance of 60 grams of total protein per day, and 20 gras of

ea'c other thani 1960, calculated by the same coniversion anial- and pulse protein, of which 10 pens should he animatechnique as the 1972 World lank Atlas. pr"t.ain. Th-aseat.andazds &~are msht!mrta hoeo

L2 Averags number of daughters per women of reproductive grass of total protein and 23 grans of ani-al protein as an,age, average for the world, proposed by TAO in the Third World FoodF Ppulation growth rates a"e for ths decades ending in , Survey. __1960 end 197. IL, Sono tdes.., haveo *aggeaed th,tad t.rtso cideRafitic of undsr 15 ansd 65 end over age brackets to apes 1 through 4. ma be .sed as a first approxiatino index ofthose in labor fomes bracket of ages 15 throwu)h 68.. malnutrition.~,PAO reference atarndarda represent p1sysiologhcal re. /8 Percetage enrolled of cor~respoding p-opulation of sched1 agequiremects for norwel activIty and health, taking asdfra o ec o" ty

/a 1,,; 1 19711 /c 19671 Ld l?531 4e 1?60-72; If 7cirtrate; /p All township. snd tmc,planning areas an- all district centersa; & Tanganyika; aL 15 gazetted townships, 1957-67; Lj Agglomerationsof 20D or more inhabitants; /9 1962, UK estimate for African population; a9 1966; /m Ratio of population under15 and 65 and over. are berckats ino those in lq-&8 age bracket; LA Ratio of population under 15 and 65 and overto, total labor force; La. 16 gesetted townsships; 1971 La1968; LL Urban only;Economically active population; L 1962; Lt Includes midwives; /' 1963; /w 1969; ~A 1961-63;196L-66; Exicluding Faeroe Isands and Greenland; /an Ehcludes private cocastional schools; /ab 15 years andover;i~ Defir tin,,,. 16!,,.,., A 96Sni. L±e T,,,.i,I.e. 5,,tharsn R-hnd.,lA o-nd ZAmbl-4, Iaf Ter-_Li,,l..w,hOperated by police or other governmm.t security orgcisations; /9aA 1961; Lh Coverage of data inc...plsts;

alHouseholds.

*Deasark has been aslacted as an objective ccuntry, becauss it is an example of a emall, denssely populated, but highly developedcountry. Nalawi has sought incieasing assistance fras Densmark in recent years.

HIS Janu-ary 10, 1975

Page 2 of 3 pages

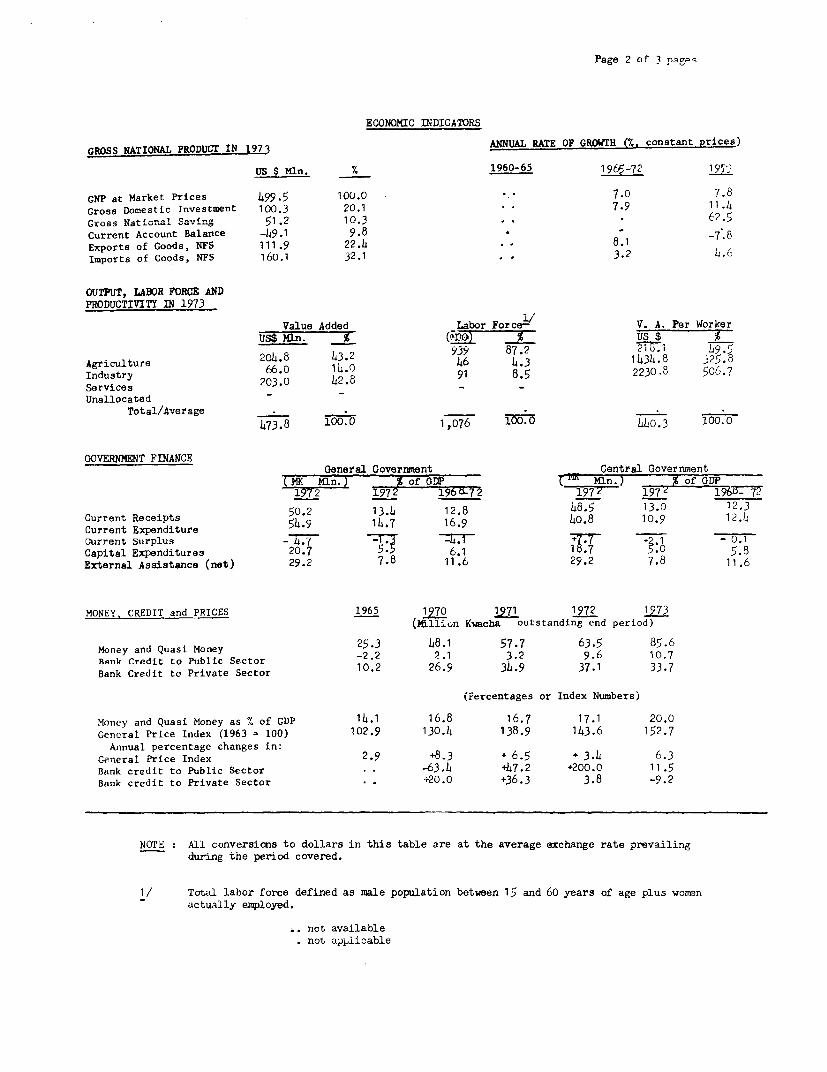

ECONOMIC INDICATORS

GROSS NATIONAL PRODUCT IN 1973 ANNUAL RATE OF GROWrH (Z. constant prices)

US $ Mn. % 1960-65 1965-72 19'

cNP at Market Prices 499.5 10o.o .7 7.0 7.8Gross Domestic Investment 100.3 20.1 . . 7.9 11.4Gross Natior.al Sa"Fing 5:1 .2 10.3 62 =5Current Account Balance -49.1 9.8 .7.8Exports of Goods, NPS 111.9 22.4 8.1 -7 Imports of Goods, NFS 160.1 32.1 , 3.2 .C)

OUTPUT, LABOR FORCE ANDPRODUCTIVITY IN 1973

Value Added Labor Force- V. A. Per WorkerAdde Laor Frce ______I_____US$ Kin. X . usa $__

2014.8 143.2 939 87.2 el19.Agriculture 204.o 143.0 46 .4.3 1 434.8 32 .

aricute 2 o 91 8.5 2230.8 506.7Iedustry 203.0 142.8

UnallocatedTotal/Average

473.8 l 00.0 1,076 I0Th 440.3 100.0

GOVERNM4T FINANCEGeneral Government Central Government

(K Mln, 4 of GDP Min.) Of GDP197 2 197 2 19 6 7_ 2 ~ 197 Z 7 _

Current Receipts 50.2 13.4 12.8 40.5 13.0 12.3Current Expenditure 514.9 114.7 16.9 14o.8 10.9124

Current Surplus -4.7 +4 1 - 0.1Capital Expenditures 20.7 5 6.1 10.7 5.0 5.8Ercternal Assistance (net) 29.2 7.8 11.6 29.2 7.8 11.6

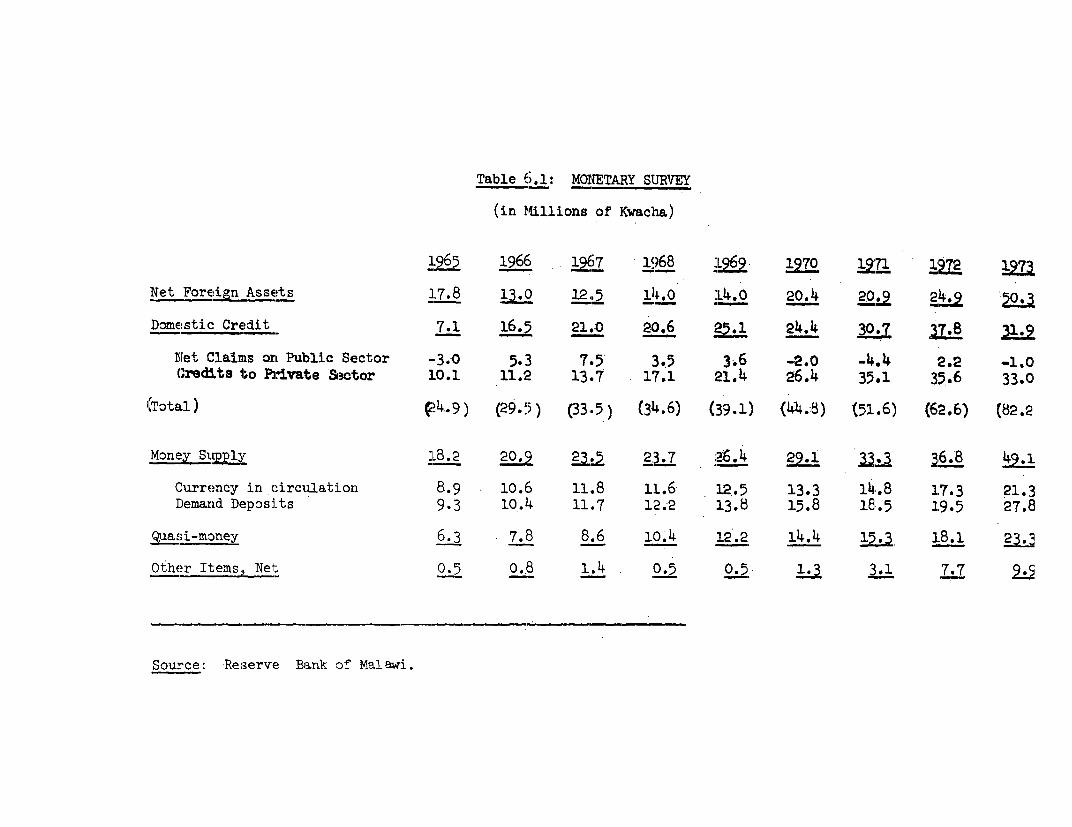

MONEY, CREDIT and PRICES 1965 1970 1971 1972 1973(.fllion Kiacha outstanding end period)

Money and Quasi Money 25.3 48.1 57.7 63.5 85.6Bank Credit to Public Sector -2.2 2.1 3.2 9.6 10.7Bank Credit to Private Sector 10.2 26.9 34.9 37.1 33.7

(Percentages or Index Numbers)

Money and Quasi Money as % of GDP 14.1 16.8 16.7 17.1 20.0Gencral Price Index (1963 = 100) 102.9 130.14 138.9 143.6 152.7

Annual percentage changes in:General Price Index 29.3 l6.5 4.3-4 6.3Bank credit to Public Sector -. -63.4 +47.2 +200.0 11.5Bank credit to Private Sector . ;20.0 +36.3 3.8 -9.2

NOTE : All conversions to dollars in this table are at the average exchange rate prevailingduring the period covered.

1/ Total labor force defined as male population between 15 and 60 years of age plus womenactually emrployed.

.. not availablenot apilicable

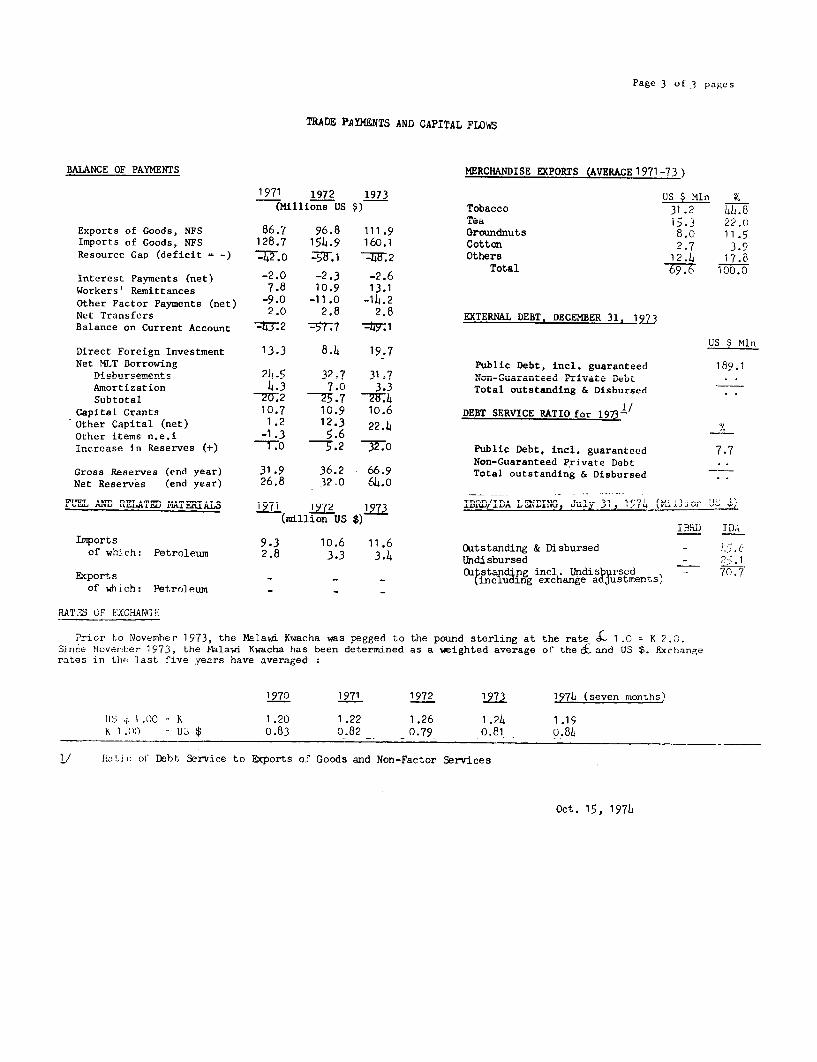

Page 3 of 3 pages

TRADE PAYMEIJTq ANJT OADTIAT Fw'n

BALANCE OF PAYMENTS MERCHANDISE EXPORTS (AVERAGE 1971-73)

1971 1972 1973 US $Mln V.(Millions US $) Tobacco 31.2 44.8

Tea 15.3 22.0Exports of Goods, NFS 86.7 96.8 111.9 Groamdnuts 8.0 11.5Imports of Goods, NFS 128.7 154.9 160.1 Cotton 2.7 3.9Resource Gap (deficit = -) -42.o -T.1 --4.2 Others 12.4 17.8

Interest Payments (net) -2.0 -2.3 -2.6 Total 7 100.0Workers' Remittances 7.8 10.9 13.1Other Factor Payments (net) -9.0 -11.0 -14.2Net Transfers 2.0 2.8 i .8 EXTERNAL UEBT, DECE ER 31, 1973Balance on Current Account tjy.2 -5r7 -4y.

US S MlnDirect Foreign Investment 13.3 8.4 19.7Net MLT Borrowing Public Debt, incl. guaranteed 189.1

Disbursements 2h4 32.7 31=7 Non-Guaranteed rivate DebtAmortization 4.3 7.0 3.3 Total outstanding & DisbursedSubtotal 27T2 2 -5.7 -ZF4 I/

Capital Grants 10.7 10.9 10.6 DEBT SERVICE RATIO for 1973-'Other Capital (net) 1 .2 12.3 22.4 %Other items n.e.i -1.3 5.6Increase in Reserves (+) 1.0 5.2 32.0 Public Debt, incl. guaranteed 7.7

Non-Guaranteed Private DebtGross -Reserves (end year), 31.9 36.2 66.9 Total outstandin'g& DisbuseNet Reserves (end year) 26.8 32.0 64.o Dursed

F' 4-.A1 Ahm R IA TSALAP~ 19(1 197-2 1973 IBRD/IDA LDING, Jul ,1, 1,71 ( U-,,(million US $)IBU IDA

Imports 9.3 10.6 11.6 Outstanding & Disbursed-of which: Petroleum 2.8 3.3 3.14 Undisbursed -

Ecports - - - Cat.standing incl. U.disbursed - 70.7of which : Petrnum - - (including exchange adjustments)

RATZS OF EXCHANGE

Prior to November 1973, the Malawi Kwacha was pegged to the pound sterling at the rate £ 1.0 = K 2.C.aiuce November 1973, the Malawi Kwacha has been determined as a weighted average of' the &and US $. Exchangerates in th* last five years have averaged

i970 1971 1972 1973 1974 (seven months)

US I .00 K 1.20 1.22 1.26 1.24 1 .19h 1.()0 -- US $ 0.83 0.82 0.79 0.81 o.80

Lj/ Hta-ic oi Debt Service to Exports o.- Goods and Non-Factor Services

Oct. 15, 1974

SUritiA±Y AN)D CONCLUSIONS

i. When Malawi attained political independence in 1964, it was thepoorest of the three territories of the former Central African Federation.Unlike Zambia and Southern Rhodesia it did not possess any substantialmineral resources. Infrastructure had been neglected and the country didnot have enough revenues to support even a rudimentary type of adminis-tration. Its prospects for economic development were generally regardedas bleak. With an average annual GNP per capita of just under US$105Malawi is still one of the poorest countries in the world. Its recordof economic development since independence has, however, been impressive.This has been largely due to a dynamic, but prrudent management of theeconomy in which both the public and the private sectors have played animportant part.

ii. Agriculture dominates the economy, directly contributing over45 percent of GDP and about 90 percent of merchandise exports. It alsoprovides a livelihood to 90 percent of the population. In 1973, small-holders' production accounted for 87 percent of agricultural output and59 percent of monetary agricultural output. Estates agriculture is stronglyexport-oriented and its production of tobacco, tea and some sugar contri-butes over half to agricultural exports.

iii. Over the 1965-73 period real GDP grew by an average of 8 percentannually to reach about US$500 million in 1973. The rapid increase in agri-cultural production, particularly from the estates, has stimulated directlythe growth of crop processing and related service activities, and indirectlythe demand for domestically produced manufactures. The dependence on agri-culture has meant somewhat uneven growth. For example, GDP fell by 6 per-cent in 1968 but increased by 18 percent in 1971.

iv. In addition to rapid economic growth, government policies aimedat preventing maldistribution between urban and rural incomes. In thisrespect, the Government has successfully made use of price and wagepolicies. Since 1968, real incomes of wage earners in urban areas havebeen eroded by price increases while crop prices paid to farmers have keptabreast of consumer nrices- Most farners are involved in some cash produc-tion and the attractiveness of the urban cash earning sector is limited.However, the Government's nolicv of encouragling relatively large enterprlsein agriculture, manufacturing, and commerce has caused a substantial concen-tration in the ton income levels in recent years, with a correspondingreduction of the share of wages in value added. In addition, the importantrole played in these ventures by foreign capital and managementI has led torelatively high outflows of profits and incomes.

v. At the time of independence, Malawi's domestic consumptionabsorbed nearly all of its product. With a combination of the rapidgrowth in GDP and a high propensity to save, gross domestic savings in-creased from less than 3 percent of GDP in 1964 to over 10 percent in 1973.

- ii -

Over the same period, investment also rose from 11 percent to 17 percentof GDP. Although in current terms the resource gap has widened, in real

terms it has remained approximately constant since 1965 with most of the

real increase in investment financed by domestic resources.

vi. In 1964, the MAlawi Government inherited a verv difficult finan-

cial position. A narrow tax base and low rates of taxation left the admin-istration with insufficient rpvpnuP to sunnort itself without Britishbudgetary aid, which was at the time equivalent to 45 percent of currentexpend4ture. A -radual broadenina of the tax base, the introduction of

new taxes and improvements in tax administration, combined with a remark-able restraint in current expenditures havep inrp made for a substantial

improvement in government finances. As a result Government has been ableto dispense ent'irel with external budgetary support sinre 1972/73.

vii, With th4 e imrovement in tila government turront htifdgt there

has been a rapid build-up of investment expenditure. In the last fiveyears, three=quarters of this investment has been directly nor indirectlv

for productive projects in agriculture, transportation and other infra-structure with only a relatively small share of investment going intosocial services. The year-to-year composition of public investment hasbeenr heavily influenced by a small number of large projects.; in nartirular

the Nacala rail link, some roads, a few large agricultural projects and

Lhe new capital at Llong e-.

Viii. Timports and exports have both averaged 15 percent annual growthin current prices since 1964 though as the terms of trade deteriorated,the volume of exports in fact gew faster than that of imports. The

resource gap amounted to US $48 million in 1973, equivalent to 30 percentof ir,ports of goodds anA se-vices. Government policies towairAs trade and

UL L L. -. L - -IJL L'.------ -----

payments have been liberal and apart from permitting the rapid growth ofexternal trade, have enabled Malawi to mobilize substantial amounts offoreign capital. Private inflows have financed many commercial, agricul-

tural and ind-ustrial ventures. overnmLent has allso succeeded in rais4ng

and diversifying external official aid to finance its investment program.

ix. Since 1971, three-year "rolling" development plans have been

lormulated withiin the LrarLie-wor'k ofL the Stater,ent of Development Polidies,

1971-80 (DEVPOL). Government's main socio-economic objectives have been:

(a) to raise tne iiving standards adiiU productivity of sriL,adLLlhoLdUers throughl

integrated rural development schemes; (b) to achieve an average annual

growth of GDP or 8 percent, partly through increased smallhloluer output,

but also through parallel development of estates agriculture and industry;

(c) to promote a balanced regional development with due emphasis on the

North and Central Regions; and (d) to develop local initiatives with a

gradual increase of local participation in the management and ownership

of productive enterprises.

x. The achievement of DEVPOL's objectives will continue to depend

in large measure on developments in agriculture. Both small farmers and

larger estates have seized the opportunities to increase output in recent

years ard the emergence of a class of estate farmers combined with theGovernment's continuing emphasis on rural development is likely to resultin a sustained growth of production, p.articularly of export crops. While

there has been relatively little conflict in the past between the simul-taneous expansion of output of estates and smallholders, this may in futureresult in some competition between the two groups for the better land,

credtuL , inputs ad n,t.anagement skills.

xi. Th e availaubl Jy of. si.L.Ledu andU trained m-anpoer will also be a

critical determinant of future growth. Government policy is directed

towards increasing the output of secondary education so as to permit a

greater degree of localization than in the past. To sustain public invest-

ment would require a strengthening of various Dranches of Governmentr through

greater reliance on Malawi nationals, especially in the agricultural exten-sion services, the planning capacity of the Ministry of Works andU the socialservice departments. The growth of the private sector will also increasethe demand for certain vocational and industrial skills, thus necessitatinga greater degree of localization. In the short run, however, the desire to

pursue a policy of localization may be difficult to reconcile with-I the ixtie=

diate need for expatriate skills to maintain the impetus of economic growth.

xii. The growth of the economy will necessitate the increased mobil-

ization of both domestic savings and external finance. The level of savings

will depend to a large extent on the continuation of the Government's lib-

eral encouragement of investment in agriculture and industry. The openingof economic opportunities to a wide cross section of the population that

is implied in the government's rural development projects should ultimately

create a wider savings base than at present.

xiii. Expected increases in foreign private investment will only meeta part of the future capital requirements. As no real increase in grant

aid can be expected, higher inflows of loan capital will be necessary,

possibly on terms harder than have been obtained up to now. While thecareful cultivation of concessionary aid sources in recent years should

enable Mlalawi to receive substantial amounts of concessionary assistance,

some borrowing on harder terms may be justified, most notably to financethe Viphya pulpmill. External borrowing should not, however, harden

beyond an average of 40 percent grant element compared with 50 percentin the past if Malawi's debt service is to be kept within reasonable limits

in the 1980's.

I. INTRODUCTION

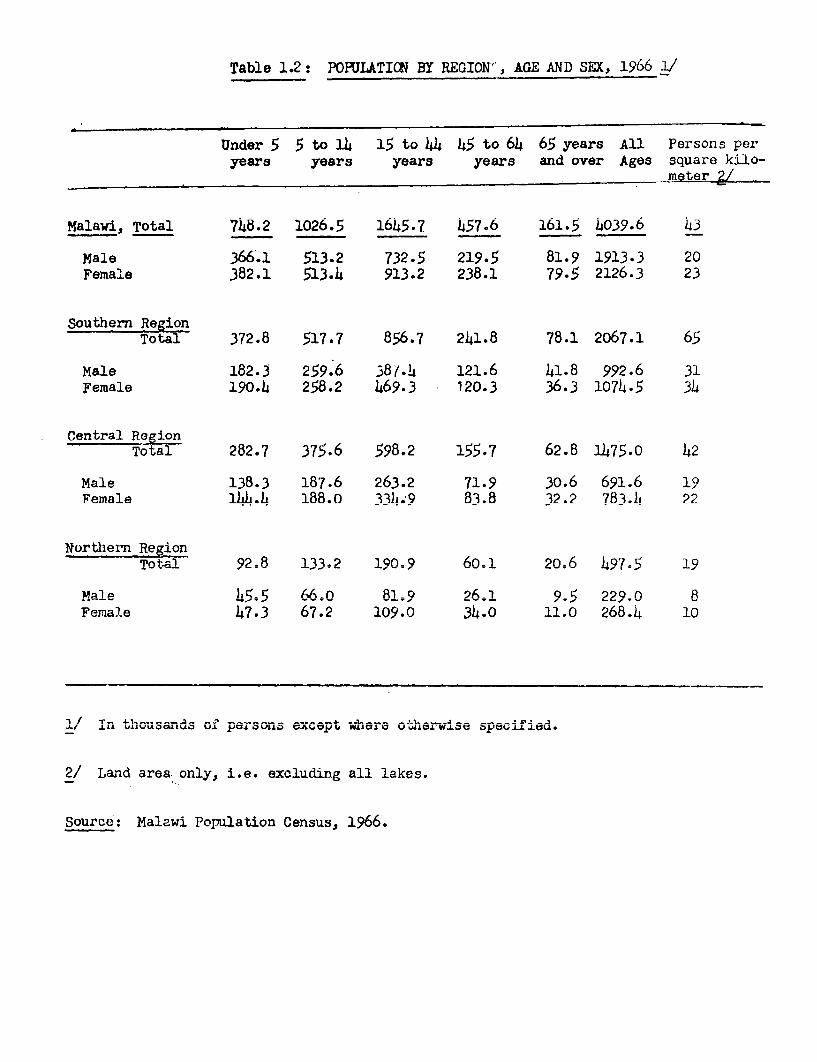

1. Mtalawi is a land-locked country in south eastern Africa on thewestern shore of Lake Malawi. Its central part consists largely of plateausof about 1,500 meters in height; the north is mountainous with altitudesup to aDout 2,500 meters while the Shire Valley in the extreme south is alow-lying flat of about 500 meters above sea level. With a land area ofabout 94,000 sq. 'km. and a population of about 4.8 million, Malawi is oneof the most densely populated countries in Africa.

2. Most of the people live in the southern and central regions whichare the most fertile parts of the country. In 1966, the population densityin the south was 65 persons per sq. km, in the center 42 persons per sq. km, andin the north 19 persons per sq. km. The uneven distribution of the populationpartly reflects differences in land fertility, but is also the result ofinternal migration which made for an early start in economic development inthe south.

3. Malawi has few mineral resources, and agriculture, for which it iswell suited, is the basis of the economy. Agriculture contributes over 45percent of GDP and about 90 percent of the population depend on it. Influencedby weather agricultural production fluctuates considerably from year to year.Estate agriculture contributed half of merchandise exports in 1973 butsmallholder production accounted nonetheless for 87 percent of total agri-cultural output.

4. Malawi became an independent country in 1964 after the break-up ofthe Federation of Rhodesia and Nyasaland. The ruling Mlalawi Congress Partywhich is the sole political party, has been in power since and its machineryreaches down to the village level. Decision making is centralized andPresident Kamuzu Banda, who has been in office since 1964, exercises a strongpersonal influence on the life of the country. In 1970, the party's annualconvention elected Dr. Banda, Life President of the Republic.

II. RECENT ECONOMIC DEVELOPMENTS

A. The Growth of the Economy

Output

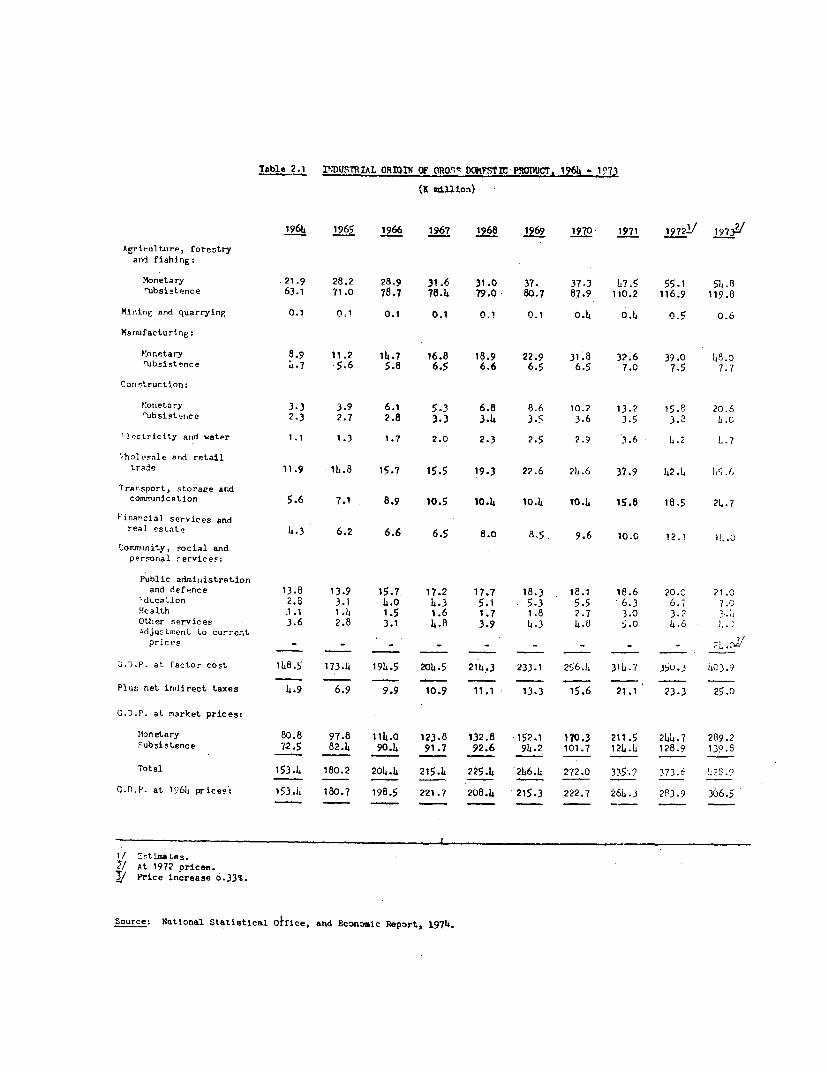

5. Over the period 1965-1973 Malawi's gross domestic product at 1964constant prices grew by an average of 8 percent per year to reach 'K 429 mrillionin 1973. Per capita income grew at an average rate of 5.5 percent sinceindependence, and was equivalent to about US$105 in 1973. Tne growth ratesachieved compare favorably with those of other African countries at a similarstage of development and also with the country's own targets. The target GDPgrowth rate set for 1971-1980 in the Statement of Development Policies,-(DEVPOL) was 7.8 percent per year.

-2-

6. rAnnual growth rates have fluctuated over a wide range reflectingthe dependence of the economy on agricultural production and consequently itssensitivity to weather. For example, in 1968 poor weather caused a 6 percentdecline in real GDP, and in 1970 GDP increased by only 3 percent, whereas in1971 it grew by over 18 percent.

7. Most of the growth was founded on the rapid expansion of agriculturalproduction for export. Monetarized agricultural output has maintained itsshare of GDP despite agriculture's declining role. Estates, which are largelyprivatelv owned, have benefitted in recent years from relatively favorableexport prices for tobacco (the principal estate crop), liberal trade andpayments arrangements, and relatively modest taxation. There has been littledirect Government assistance to estates. Smallholder production has laggedbehind that of the estates. The growth which has occurred in smallholdersmonetized output is directly a result of Government policies, however, bothin implementing major rural development projects, and improving crop marketingarrangements for smallholders.

Table 1: COMPOSITION AND GROWTH OF GDP BY SECTOR(Percent)

% Shares in GDP1964 1973

(prelim.)

Agriculture 57.1 46.0(Smallholders: non-monetary) 42.4 31.5(Smallholders: monetary) 10.7 8.6(Estates) 4.0 5.9

Manufacturing & Mining 9.3 14.8Transport & Communications 3.8 6.5Construction 3.7 6.5Public Utilities 0.8 1.2Public Administration & Defense 9.3 5.5Other Services 16.1 19.5GDP at factor cost 100.0 100.0

of which(Monetary) (51.2) (6564)(Non-monetary) (48.8) (34.6)

Source: Appendix Table 2.1.

-3-

8. Much of the stimulus behind the rapidly increasing output in themanufacturing and some service sectors has come from agriculture. Theincreased output of export crops has necessitated a comparable increase inprimary processing. distributive and re-mmprrinl aetivities; while the cashincomes generated by the export of agricultural products have generated awider demand for consumer goods, many of whirh are mantifarrtirPd Ine'allv

9. The growth nroaes has been further stimulnted hu the high invest-ment program, which has promoted a rapid expansion of construction and bywage remittanrpS frnm Malawiann orkers abroad, which have served to generategreater consumer demand. The overall share of the services sector has remainedstable- during the period, despite the growth of transport and co^m^ercralactivities, reflecting restraint in expenditures on public administrationanrd dPfp,nQw tjhnan ^ 1n4-A - 4._4 rTnD __ .1A14A-A from 9 3 o A R Aprc

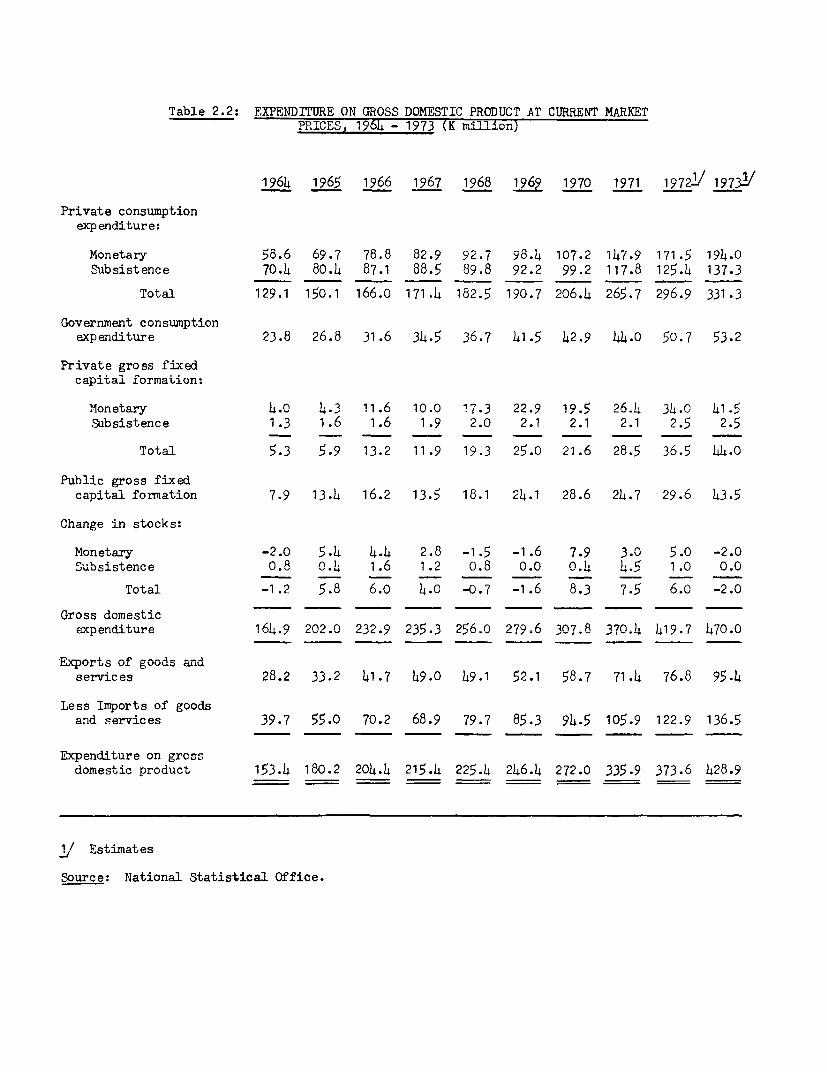

Savins and Invest..ent

10. At1 the uiM=. of Independence 'Mlcaawi's dom,estic consum,ption abusorbednearly all of its product. For many years the Government incurred a deficiton its recurrent bDUdg6-et wh-iCIhI wa-S finnery-rts--deay U~LLvs .LcuuLCLz UuuiCL llul W":i nanced Dy Dr.LL.l5l L)UUgtL.ULY bUpPULL.

With a combination of rapid growth in GDP and a high marginal propensity tosave, gross domestic savings if increased from iess tnan 3 percent of GDP in1964 to 10.6 percent in 1973. National savings increased more slowly asthe fiscal posit'ion improved and U.K. budgetary support was gradually eliminated.

11. Gross domestic investment rose at an average annuai rate of 25percent; as a percentage of GDP it increased from 11.3 percent in 1964 to17.4 percent in 1973. The share of the public sector in gross fixed capitalformation averaged a little over 50 percent during this period. A breakdownOL capital formation by sector is not available, but there has clearly been ahigh concentration in transport and agriculture. The fast liquidating natureof many private investments has kept the incremental capital/value added ratioaround 2.0, despite the concentration of public investment in infrastructureprojects with less immediate impact on output. Towards the end of the period,the incremental capital/value added ratio may have been around 1.9 comparedwith 2.1 at the beginning as several of these infrastructure schemes reachedmaturity and began to realize economic benefits.

12. Since 1964 the rate of growth of investment in current prices hasexceeded that of savings, with the result that Malawi's resource gap haswidened considerably. As most investment goods were imported the rise inimport prices in recent years has considerably eroded the purchasing powerof external finance, and in fact the resource gap in real terms has been moreor less constant at US$30 million since 1965. Domestic savings, which finan-ced only 26 percent of investment in 1964, financed 61 percent in 1973.

1/ Averagie 1967-6Q pvri4acs nA-ehange rates are widely used in this reportas a basis for constant price data expressed in US dollars.

- 4 -

Table 2: INVESTMENT AND SAVINGS(US$ million at average 1967-69prices and exchange rates)

1964 1965 1970 1973Est.

Investment 23.3 37.6 59.6 71.6

Domestic Savings 6.1 5.3 26.3 43.4

Resource Gap 17.2 32.3 33.3 28.2

Source: Appendix Table 2.3

Employment

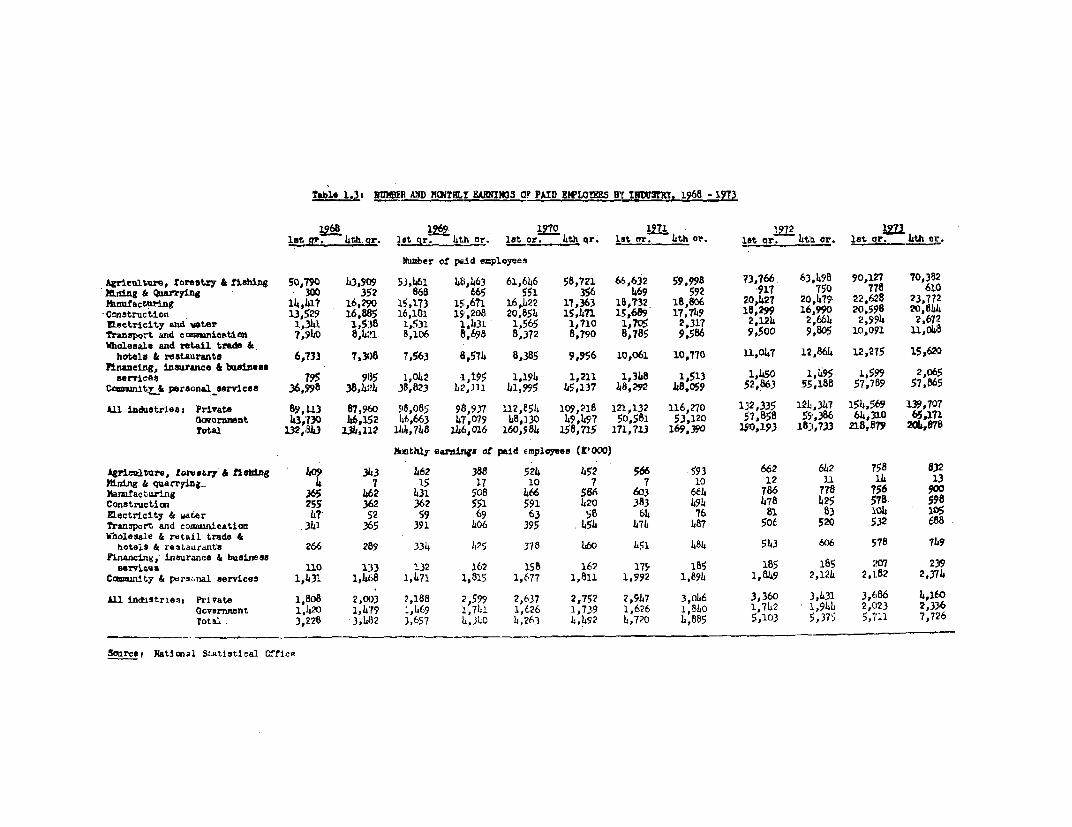

13. Since the last population census in 1966, the population has grown

by about 2.6 percent per annum, and in mid-1971 was Pstimated at 4.8 million.About 90 percent of the population derives all or part of its livelihood fromagricultur--1 on-r related activities. A periodical collection of statistirspertaining to wage employment was first started in 1968, but coverage is

limited to establishments employIng 90 nr more workers, hence significantiyunderestimating actual employment. Employment in these relatively largeestablishments rose by around 10 nercent per year between 1968 and 1973,

to reach 215,000. Employment is also seasonal with a low point in the last

quarter of the year arnd a 10 percent higher peak occurring in the first or

second quarters during the main tobacco harvests. In 1973, the number of

er,ip'loyees was 224,000 in the second qua-ter, but 205,000 in the fourth quarter.

The private sector, which includes statutory bodies provides around two-thirds

oL recorded em,plo-yment in Large establish...ents, anA since 1968, its slhare ir.

the total has increased slightly, reflecting the relative restraint ingoverrirtent eipLoyLuent. Much ofi the increase in Job opportunities has b.een

created by agricultural estates. Employment in small establishments was

estimated conservatively by Government at 30,000.

- 5 -

Table 3: STRUCTURE AND GROWTH OF DEPLOYMENT(in establishments employing at

least 20 workers)

Annual Average1968 1973 /1 Grnowth Rate 1969-73(thousands) (%)

Agriculture, forestry, fishing 44.1 76.3 11.6Manufacturing 17.2 25.6 8.3Mining & construction 15.8 21.9 6.8Transport, public utilities 9.7 13.4 6.1Distribution & finance 10.3 20.2 14.4Other services 37.4 57.9 9.1

Total number employed 134.5 215.3 9.9

of whicih:Private 89.6 150.1 10.9Government 44.9 65.2 7.8

/1 1973 figures are provisional.

Source: National Statistical Office and Economic Report 1974.

14. There were about 1.15 million households in Malawi in 1973. Thenumber of households may be growing somewhat slower than population owing tothe increase in longevity. The absolute increase in the number of householdsover the 1969-73 neriod has been approximately 130,000, compared with anabsolute increase in employment in large-scale enterprises over the sameoeriod of 81O00W It is unlikely that smaller establishm,ents could absorbthe remaining household heads and it seems that despite the high rate ofgrowth of emplovment; Malawi is farcnv a situation where there are increasin-numbers of households with little alternative but subsistence farming. Theextent of at leant nartial or seasonal partici-ation in the wage earninglabor force is limited to about one person in four households.

15. Malawians have traditionally found employment in neighboringcountries, mainly South Africa, -Southern Rhodesia and Zambia, and there maybe as many as 300,000 Malawians working abroad. In fact, the populationagei nvra-…id indicates the absence of a large sectior. of the active mzlepopulation; the ratio of males to females is as low as 0.67 for the 20-24age group. One organzation alone, the "Mines Lsbor Organ.ization `LL4r.LiLe

(WENELA) had 124,000 Malawians on contract under a group employment scheme in1973 for work in South Africa, largely in the mines. EUmployment contractsare for two years at a time, and may be renewed for another two-year periodafter the workers have returned to and spent at least six months in MalawiThe Rhodesian African Labor Supply Scheme functions along similar lines.

- 6 -

16. Historically, an outlet for excess labor supply has been supplied bythese opportunities for employment abroad, which have been expanding rapidlyfor several years. More recent-y, the Government's focus on rural developmentschemes to improve the conditions of life in rural areas has probably alsobeen responsible for removing some of the potential pressure for employment.Thus, despite the apparent increase in the number of households whose mainalternative i4s subsistence farming, there h,as 'Deen l"ittle evider.ce of excesslabor supply. Rural-urban migration has been kept under control, and thegr^wth rate of the population of Blantyre h.as in fact lbeen estiLmated' at only6.5 percent per annum. Both these figures are relatively low compared withother African countries at a similar level of development. 'Urban unemploy-ment has also not been a major problem - the Blantyre Sample Census found only3.1 percent of the labor for.e 4n Blantyre une.IIployeU.

17. As long as employment poss 't.lLes remain available abroad, it isunlikely that Malawi will suffer from widespread unemployment. EmploymentopportunLtites '£n Joutl Ai'rca are Likely to continue to be available, probablyin increasing numbers, though there are indications of rising difficulties forforeign workers in Zambia and less favorable employment conditions in SouthernRhodesia. The stabilization (or even reduction) of the number of Malawiansemployed abroad would transfer rm-uch greater pressure onto the domestic labormarket, and would underscore the need to promote attractive self-employmentopportun'ties in the smalilholder farming sector and other smallscaleactivities.

B. Income Distribution

18. Government policy towards the distribution of incomes has beenformulated within the longer term aims or DEvvOL, and is linked both toregional objectives and wage and price policies. The rationale underlyinggovernment policy is the following. Minimum wage rates have been appliedin Malawi since the early 1960's and have reportedly been adjusted only inresponse to changes in productivity. This policy was aimed at (a) avoidingany widening of income disparities between urban and rural workers, (b) pre-venting wage cost increases in the agricultural output of estates fromjeopardizing the competitiveness of Malawi's exports, and (c) broadening themarket for local industry to bring about a demand-induced expansion ofdomestic production. Specific measures to encourage industrialization werealso taken and have resulted in the creation of a small urban class.

19. Since 1968 real incomes of wage employees have been eroded by priceincreases. The GDP deflator rose by about 30 percent in the 1969-1973 period,while average earnings of all wage workers increased by only 11 percent. InBlantyre the low income price index went up by 30 percent while the minimumwage index rose by 18 percent. In other urban areas prices probably increasedmore slowly, but minimum wages rose by only 9 percent.

20. At the same time prices paid to farmers for their crops have keptabreast of consumer price increases. The mission estimates 1/ that 1973 farm

1/ Based on an index of crop prices weighing each crop by its share in totalADMARC purchases from 1968 to 1973.

-7-

prices were about 28 percent above their 1968 levels Even assuming noincrease in productivity, earnings would therefore have stayed more or lessconstant i: term-s. of their purchasing power. Ir fact evidencefrom rural development project areas in particular, suggests that productivitybs rise,.. It even seems that farmers 1have even fared better than wage workers

in agricultural estates where average earnings increased by about 20 percentin ~ the 0I-7 perio.oUU

The 'LLLUtc rpt'es bLetween urba. a.L-d rural areas has thus -ro-

bably been reduced since 1968. Even in 1968 it was not extreme. Annual cashrece'Lpts per rural househoold averaged 'U 40 in 1 7 WhiLL Le thle minru, wage ir

urban areas other than Blantyre was equivalent to about K 90. The current gap,as perceived by a typical farmer with little education or em-uployable skills,between his earning capacity in farming and in the likely urban employmentalternatives is probably not great, particularly when the higher cost of urbanliving is taken into account.

22. The success of Government policy in minimizing the gap between urbanand rural incomes has held the pace of urbanization to a low level and hascontributed to low levels of urban unemployment. As a result, excesses ofpoverty are conspicuously absent in Malawi, while urban development has so farnot involved the extremes found in many large cities of the world. In economicterms this aspect of Government policy also appears to have justified itself bywidening the market for domestic manufactures and reducing the demand forimports. The success of import substituting industry in Malawi is due in nosmall part to the wideness of the markets for its products, and it is likelythat a greater concentration of incomes or wider urban-rural income disparitieswould have led to levels and types of demand that could only be met throughthe import market.

23. However, the Government's policy of encouraging large manufacturesand agricultural estates has been accompanied by relatively high financialreturns to those with the ability and willingness to develop new productiveenterprises. This has made for a substantial concentration of incomes intorelatively few hands over recent years. Thus, while there is a close balancebetween the incomes of the vast majority of the population, there has also beena tendency for a small number to increase their overall share in incomes. Onthe basis of various data relative to 1969, the mission estimated that thepoorest 40 percent of the population probably received about 25 percent of in-comes, and the next 40 percent of the population about 30 percent of incomes.On the other hand the top 5 percent may have had as much as 30 percent of in-comes. That there has been a trend towards greater concentration is shown bythe fact that the share of wages and salaries in value added 1/ in bothagricultural estates and industry has declined since 1968, indicating a highershare for profits, dividends, depreciation and direct taxes. This concentration,which on the surface suggests a growing income disparity has to be seen in the

1/ Va'Lue aaded here excludes interest, corresponding to net output as definedin Government publications.

- 8 -

context of Malawi's growth objectives and the purpose served by a high andgrowing level of profits. The structure of company tax heavily favors the re-investment of profits over their distribution. No tax is levied on the former.i h- as been a malJor an essential actor iLn ensurLng thLa prof"Lts are used

not for conspicuous consumption by a small elite but for financing the contin-uing growth of innvestment. If a concept of disposable personal incomeincluding only the distributed part of profits were used for in-comue comapaeuisons, the intra-personal distribution of income would be lessskewed than is otherwise suggested. The concentration of ownership of assetsimpliedain the longer run'cycurrent trends is considered by government as aprice to be paid for the development of the private sector economy.

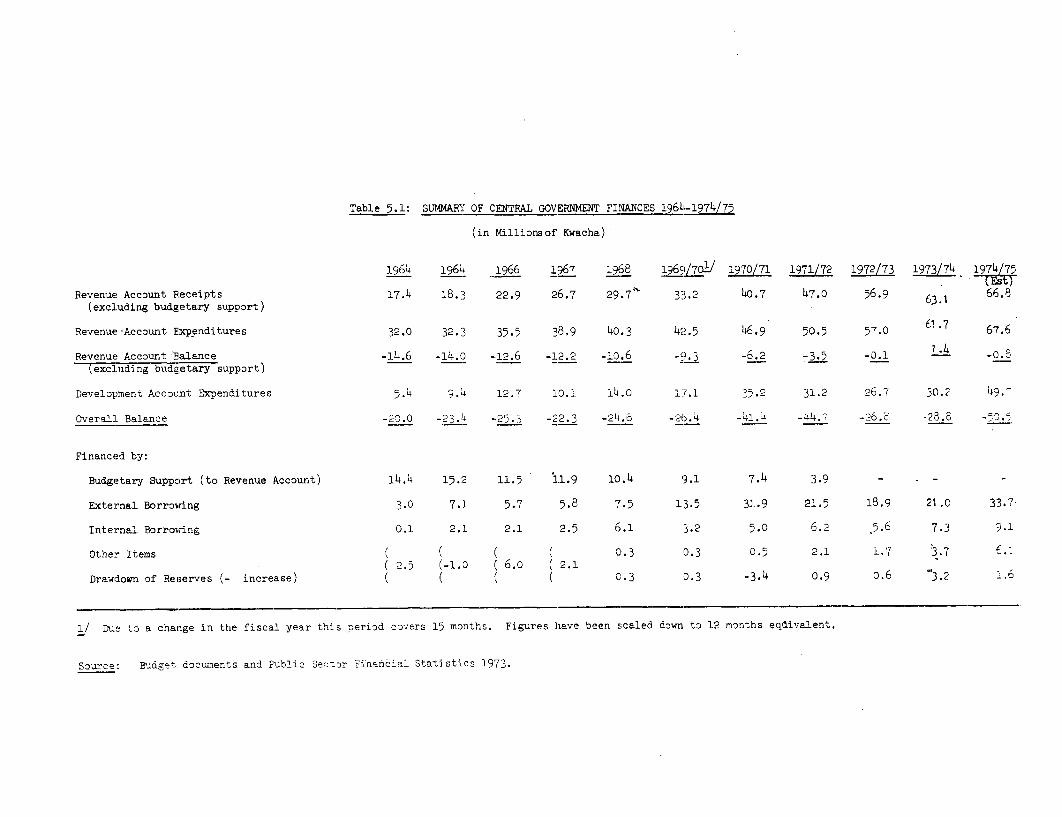

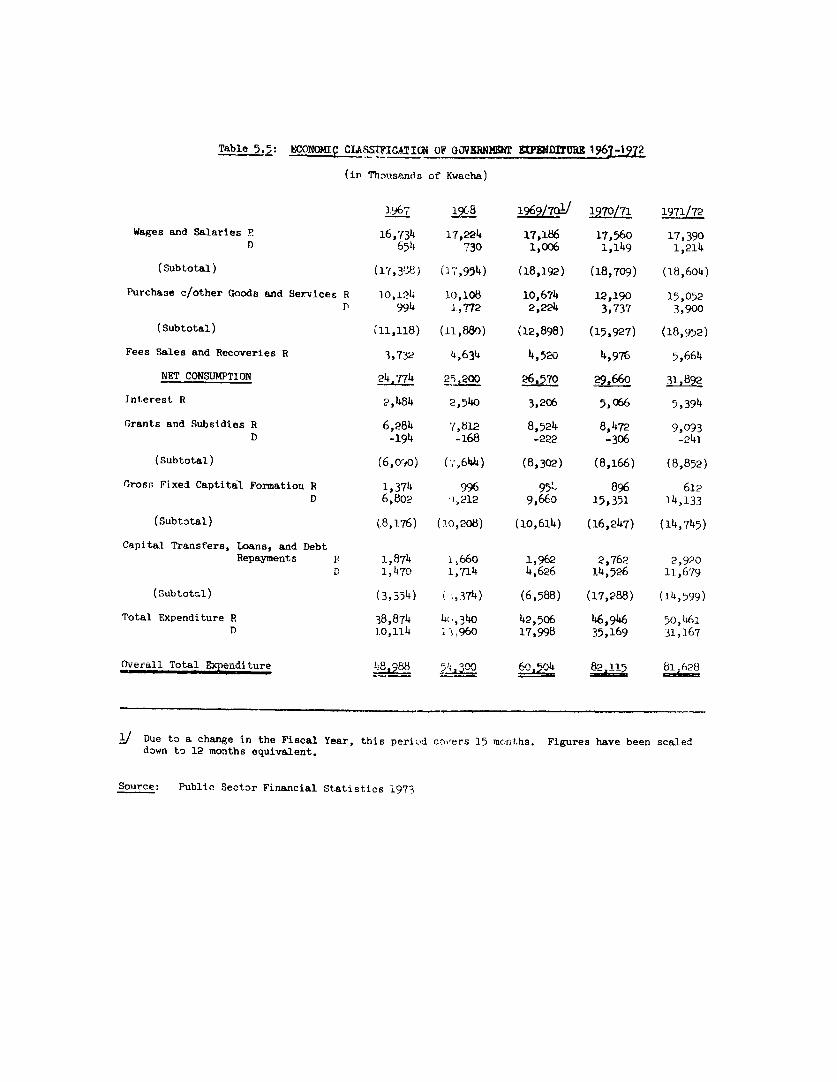

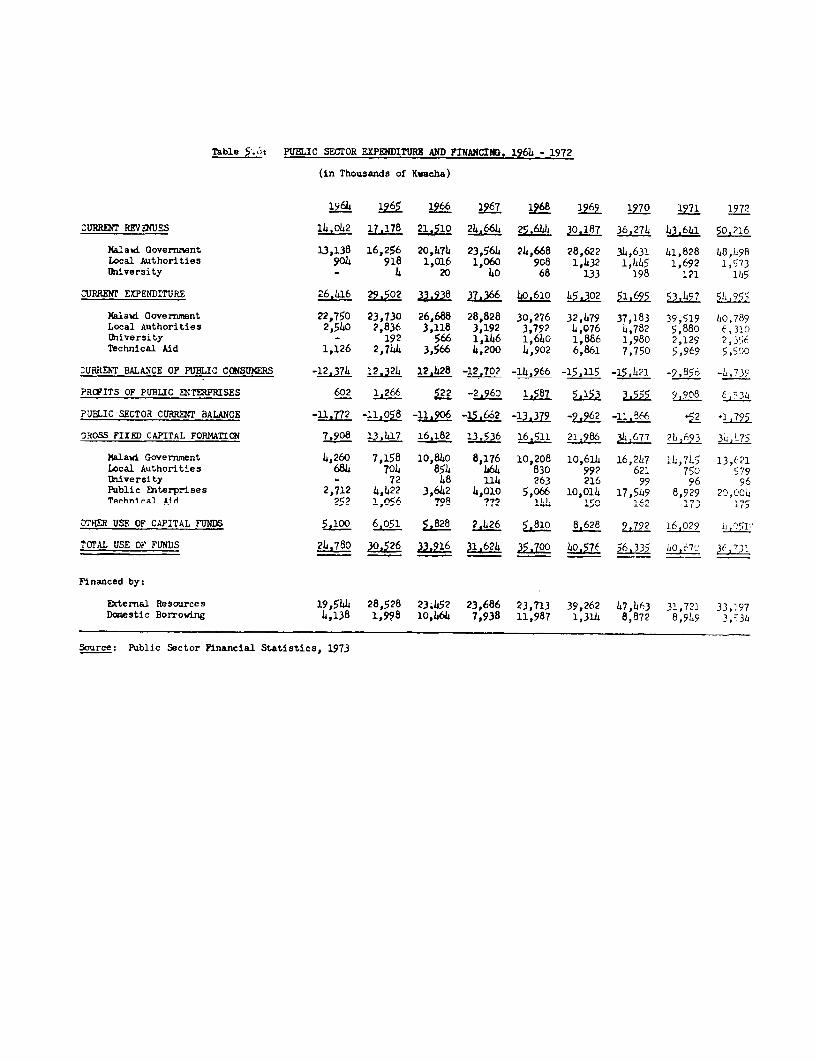

C. Public Finance 1/

24. At Independence, the Malawi Government inherited a very difficultfinancial position from the former Central African Federation Government. Anarrow tax base and a low level of taxation enabled only just over half ofthe expenditures on Revenue Account 2/ to be financed from local resources,the balance being met by the United Kingdom mainly in the form of grants. Im-provements in government finance have been achieved by restraining expendi-tures on Revenue Account to a modest rate of growth (averaging 8 percent peryear since independence), while revenues increased at a much more rapid rateof 15 percent per year. In 1972/73, this account was balanced without externalsupport for the first time.

1/ The public sector includes, in addition to Central Government, localauthorities and 13 state-owned corporations. Local authorities receivemost of their funds from Central Government, either as personal taxescollected on their behalf or outright grants. Public corporationsgenerally operate on a commercial basis, with access to commercial andgovernment sources to meet capital finance requirements.

2/ Government maintains two budgetary accounts -- a Revenue Account whichis credited with tax and other receipts, and which finances mainly re-current expenditure, and a Development Account into which foreign loansare paid, and which finances mainly capital expenditures. The fiscalyear was January-December until the end of 1969, an exceptional 15 monthsfrom January 1969 to March 1970, and April-March since then.

Table 4: Central Government Finances

1964i- 1968 1972/73 1973/74

Reve-Uue Accout Recceipts I.4 7 5,6.9 63.1Revenue Account Expenditures 32.0 40.3 57.0 /1 61.7

Revenue Account Balance -14.6 -10.6 -0.1 + 1.4

Development Account Expenditure 5.4 14.0 26.7 30.2

Overall Balance -20.0 -24.6 -26.8 -28.8

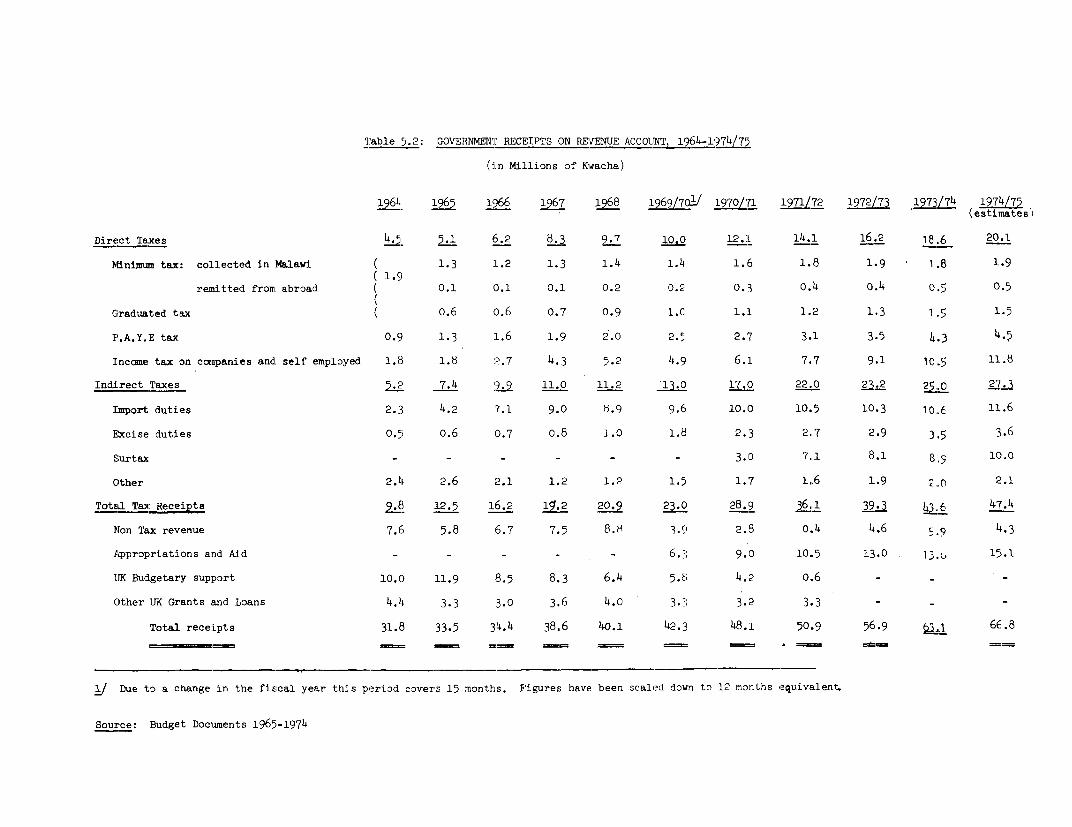

Financed by:External Resources 17.4 17.9 20.3 24.7Domestic Resources 2.6 6.7 6.5 4.1

/1 Includes repayment of excess budgetary drawings of K 1.0 million.

Source: Appendix Table 5.1.

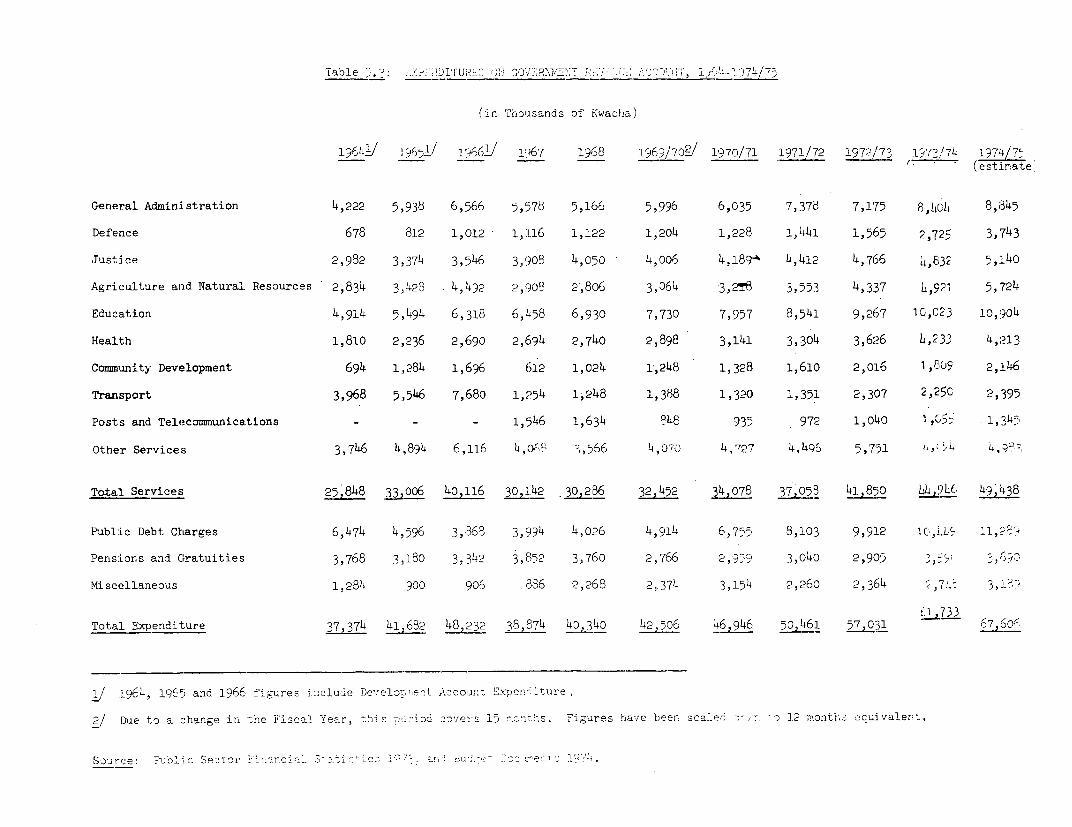

25. Despite these improvements all current expenditures are not yetmet with current revenue. The Development Account of some departments,particularly the Ministries of Agriculture and Works, contains substantialamounts of development expenditure of a recurrent nature connected withforeign-financed development projects, which were generally financed in partby foreign sources. .Without such support for recurrent items, recurrentexpenditure would have had to be reduced by K 4.7 million.

26. Tax income increased by over 17 percent a year in the decade sinceIndependence. This increase resulted from a gradual broadening of the taxbase, the introduction of new taxes, and improvement in tax administration.Since Independence, tax revenue has grown about one and a half times as fastas GDP (at factor cost). As a result taxation has increased from 6.6 percentof GDP in 1964 to 10.8 percent in 1973, or from 12.9 percent to 16.5 percentof monetary GDP over the same period.

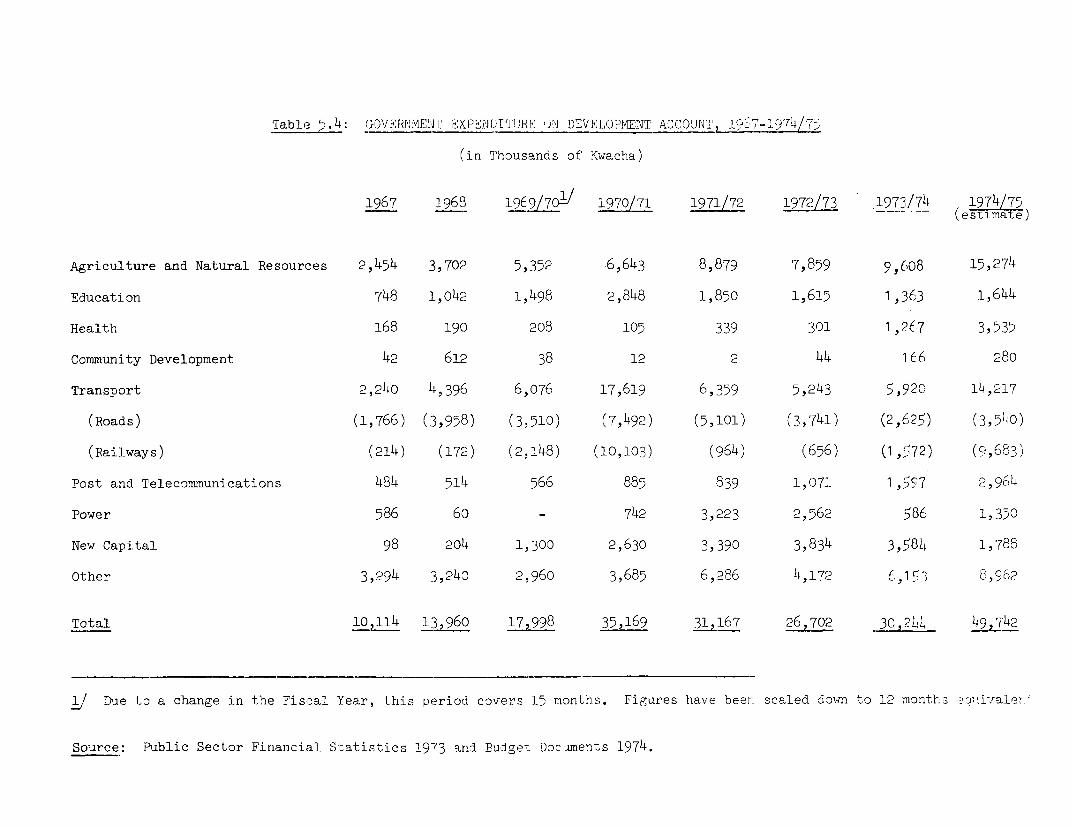

27. Tax policy is not formulated solely on the basis of revenuemaximization, but is seen as an important element in development strategy.Direct tax proceeds have deliberately been held at as modest a level possibleto provide maximum incentive to producers including the entry of traditionalfarmers into the monetary economy. There is however some element of pro-gressivity in the system, particularly with respect to medium incomes. Be-sides a head tax of K 3.50 levied on all miales above 18 years of age, marginalrates of taxation on personal incomes range from 10 percent on incomes justabove the minimum legal wage to a marginal rate of 40 percent on chargeable

- Lu -

incomes above K 11.000. Company taxation has also been devised to attractprivate foreign investment. Company income is taxed at 40 percent, with a5 percent surcharge for companies not registered in Malawi. This surchargeis, however, not paid where companies can demonstrate that the inrcome wouldnot be liable for tax in the country of origin, thus avoiding excessiveremittance abroad because of differential tax liability. Wnile 40 percent isnot particularly low, there are special deductions which can be claimed byfarmers and industrialists including generous capital allowances. in 1973/74,company tax was expected to yield K 10.1 million and personal taxes K 7.8million out of a total tax revenue of K 43.5 million. Direct taxation hastended to grow somethat slower than other taxes.

28. Instead of direct taxes, a more indirect system has been preferred,with relatively greater emphasis on consumption. Domestic consumer goods aretaxed in part by excise taxes, and in part by surtax, introduced in 1970/71and which now provides over one-fifth of tax revenues. This tax is a goodexample of Malawi's policy to extend indirect taxation. Essentially a salestax levied at the wholesale level on domestic and imported goods, surtax isbasically progressive because food is excluded, and because it is levied onthe value of products after excise or import duties. As excise tax is leviedonly on a limited number of luxury items and import taxes are higher onluxuries, this increases the degree of luxury taxation. At the same time,investment is encouraged because capital goods are excluded. These featuresare combined with the advanitages of simplicity, ease of administration, widecoverage and 1/ minimal collection costs. Imported goods are taxed at ratesup to 60 percent and averaging 15 percent. The tariff structure is thus usedto protect domestic industry in certain cases, as well as to raise revenue.

29. Fccurrent expenditures for social services, particularly education,increased rapidly after Independence, as a response to the need to improveon the low education levels then prevailing- The share of qorial serviresin the Revenue Account budget rose from 18 to 26 percent from 1964 to 1968,where it has stabilized in recent years. The share of agriculture fluictutatedbetween 6 percent and 8 percent, from 1964 to 1974 while the share of infra-strucrture, such as transnort, posts and commimnrntions, and public works

declined from 21 percent to 13 percent. Administration and security expend-itures rose in the first years of Independence but have since had a combinedshare of 25 percent. At Independence, one-fifth of expenditure on RevenueAccount expenditure was claimed by public debt service, with the proportionfalling to around 10 percent in the late 1960s, reflecting an increase in,grant aid to Malawi. IJith increased borrowing i-,n ------ yer,i priuaLY cars, in jCIL L±AU1ar,

for the Nacala railway link, public debt service has risen again, and nowaccounts for 16 percent of the expenditure.

I I U~L L L .. WS, .. . L~£ L L IL~ IL~U£ iI~LL a eit/ Fruit machines which are an insignificant share ofL imports are taxes

at 100 percent. Protection of industry has generally been modest, withrates pragmatiLca L'Ly determLined wIlere a possible monopoly Eituation mightexist. Industries are ultimately expected to become competitive andprotectilon may be withdrawn. AIn two tj'er system o tarifr protection isoperated to minimize abuse of protection.

30.~I-n 191710, thle Gver,-ment introluced three-year ceilings on recurrentexpenditures of individual Ministries as a new method of budgetary controladu plann'1rLg. Ii. le present ceilings, which are net oUL LincoUme f r Om1 d epartr,IentL

services, have been successfully applied and allow annual increases of 10prcent1L £or Ltne Ministries OI worKs and Agriculture, oI 7.5 percent for cneMinistries of Education and Health, of 5 percent for the university and of4 percent for most other Ministries and departments. Tne system of three-year ceilings is linked to the three-vear rolling budget system that hasbeen adopted for development expenditures. Tne first year of the three-yearprogram contains firm figures and proposals while the figures for the secondand third years are indications of further investment contemplated by theGovernment. The approach is innovative, and combines an approach to planningwith flexibility that has proved successful so far in implementing theobjectives of the 10-year Statement of Development Policies.

31. Concurrently with the improvements in the recurrent budget, thegovernment outlays on Development Account rose from K 5.4 million in 1964to over K 34 million in 1973/74. The share of economic infrastructure,mainly transportation and agriculture, increased from 67 percent in 1964-68to 74 percent in 1969-73, while the share of social infrastructure, mainlyeducation and health, was reduced from 23 to 8 percent. The change in thecomposition of the development budget during 1969-73 was heavily influencedby a small number of large projects, particularly the Nacala railway link,some roads, a few large agricultural projects, and the first phase of thenew capital city at Lilongwe. The lack of basic transport infrastructurewith which the Government was faced at Independence justified a relativelylarge weight for this sector in development expenditures, both in the con-struction of an internal highway network from north to south, and in providingalternative links to the sea.

32. In the absence of budgetary savings until 1973, most of the develop-ment outlay since 1964 was financed by external assistance, which averagedK 22 million annually for the last five years. Throughout the period, theUnited Kingdom remained the single main source of foreign aid, although ofdiminishing importance. Aid from the U.K. -to Malawi has gradually changedfrom grants to soft loans, and from contributions to the recurrent budgetto only aid to the development budget. In this process, total disbursementsfrom the U.K. decreased from K 17 million (70 percent grants) in 1964 to K 9million (95 percent grant) in 1973/74. While the U.K. reduced its aid,Malawi was able gradually to mobilize finance from other foreign sources,both bilateral (mainly South Africa, Germany, Canada, Denmark and U.S.A.)and multilateral (mainly World Bank Group), so that sources other than theU.K. now provide about 70 percent of Malawi's external capital assistance.To date, direct government borrowing has only been on the most concessionaryterms.

33. Domestic borrowing remains relatively small. It is tailored to theneed to provide a local contribution to externally financed nroiec-t and tofinance projects which generally do not attract external finance. During thepast five years; domestic borrowing averaged K 5.3 millinn per year. The main

- 12 -

instrument for Government's domestic borrowing are securities with maturitiesranging between two and twenty years (locally rpeiqtprpd stork)- The ReserveBank issues these securities and holds any unsubscribed balances. The bankingsyst- hka hbn, hold4in about 20-25 npre-ont of tha ln.ocl raeictaerA ctntL-

during recent years. Outside the banking system, the most important subscribersare local financlal4 f institutions such as the Post Office Savings Bank, insurance

companies, and a building society.

34. The financial position of the public sector in toto has been ratherstronger than that of Government alone. Careful financial management ofpublic enterprises has succeeded in making the majority profitable. Minor-leic its A are generally incurred by the Smi..lholder TeSa Authty, Uth Capital

City Development Corporation and Malawi Broadcasting Corporation (which israte ^ v4 _. ..k14 A.4AE 2 A,^ k.. MA1 .. 4 Railways.

operated *Ln any Lcas as a L V UJ pLsV yisX iay X s W4 O -

On the other hand, the Agricultural Development and Marketing Corporation(A h- ADC)% has - nrt larg surpluses in r1 - t - years, a g K 6¶1-WJLJ-LLUXt,J iiat ~ r,=LICL a LMU .a OUtIt ~ l L C%_LC1 y a M,aVZL.2r,.LL1, I U .U

million, which have outweighed by far not only the small losses of certainpublic corporatiLons, but aLso the surpluses oL otLers. tOveraLL pUUliL cUL

porations probably generated combined surpluses of around K 7 million beforetax Ln eachl ofl thle 'Last LlV years, which have graduualy become 'arger thlanthe deficits of Government. 1971 was the first year in which real publicsavings were achieved. In 1972, pub.l savings we I .0 equiv-

alent to 4 percent of domestic savings, and while no definite figures are yetavailable, greater savings may have been realized in 1973.

D. External Financing

35. Over the period 1965-1973, Malawi's exports and imports in currentprices (including non-factor services) have both risen at just under 15percent annually. The resource gap has risen from US$16.1 million in 1964to USS48.2 million in 1973, averaging slightly less than 35 percent of totalimports throughout the period. Tnere have been increasing wage remittancesbv Malawians working abroad, which reached about US$15 million in 1973. Thuscatching up with the amount of investment incomes paid abroad in recentyears. Net transfers have declined substantially, owing to the phasing outof British budgetary aid. The reduction of budgetary aid has been accompaniedby increased capital inflows to both public and private sectors. Foreignexchange reserves were gradually built up and, as of the end of 1973,stood at $67 million, equivalent to 6 months' imports.

36. Government policy towards trade and payments has been liberal. In1973 exports plus imports were equivalent to 54 percent of GDP in value. Asa general rule, imports originatinig in the sterling area are free of license,while those originating in GATT countries outside the sterling area are underopen general license. The only restrictions on payments and transfers forcurrent transactions are those applied to foreign exchange allocations fortravel and a few other invisibles. There are no restrictions on the transferabroad of dividends and profits of non-resident controlled companies providedthat no recourse is made to local borrowing. Outward transfers of capital

- 13 -

are controlled, but non-residents are permitted to repatriate their investmentsand emigrants may transfer capital abroad within limits. This regime occupiesan essential role in Government's development strategy which relies onincreased exports, imports and external capital for its achievement.

37. In November 1973, Malawi decided to unpeg the Kwacha from the poundsterling to prevent the worsening of the terms of external trade that wasresulting from the gradual depreciation of the pound. The value of theKwacha is now fixed as a trade-weighted average of the value of sterling andthe U.S. dollar. The new method of valuation has been successful in smoothingout much of the fluctuations in foreign earnings and payments due to fluctu-ations in value of other currencies.

Table 5: SUMMARY BALANCE OF PAYMENTS(US$ million)

1964 1968 1972 1973

Exports, goods and NFS 39.5 58.9 96.8 111.9Imports, goods and NFS 55.6 95.6 154.9 160.1Resource balance -16.1 -36.7 -58.1 -48.2

Factor services, net -8.6 -8.3 -2.4 -3.7Balance on goods and services -24.7 -45.0 -60.5 -51.9

Net transfers 26.9 20.0 13.7 13.4Long-term public capital, net 1.4 14.0 25.7 28.3Long-term private caDital. net 1.6 9.1 8.4 19.7Other items, net -0.5 3.9 17.9 22.4ChanRe in reserves (- = increase) -4.7 -2.0 -5.2 -32.0

Source: Appendix Table 3.9

38. Exports of agricultural products have been the main thrust behindthe rapidly increasing foreign exchange earnings of Malawi. However, thereliance on agriculture has meant that growth of exports has been uneven.After a period of ranid grnwth exports actually stagnated in the late 1960's,but have since again expanded with increased vigour. Four major crops--tobacco,tea, cotton and groundnuts--together accounted for 77 percent of merchandiseexports in 1973, and 16 percent was derived from a variety of minor cropssuch as cassava. tunp oil, maize, sugar, rice, pulses, sunflower seeds andcoffee. The remaining 7 percent of exports was from the small manufacturingsector. In addition, a certain amount of ZaM.bian tobacco is re-exported fromMalawi after processing.

- 14 -

39. In 1973, exports of agricultural crops produced by agriculturalestates exceeded 50 percent of total merchandise exports for the first time,prompted by the expansion of areas under cultivation by estates in recentyears, combined with favorable Government policies and higher internationalprices in 1973. Most of the increase in exports from estates has beenachieved through volume increases or by systematic movement into higherquality grades of tea and tobacco. Export of smallholder crops has grownless rapidly than estates crops; the volume of exports of some crops suchas vroundnuts; cotton and pulses has stagnated or declined over the lastfive years, while the volume of exports of other crops such as tobacco andrice has increased. Export prices of smallholders crops have, however, risenfaster than those of estate crops on averages.

40. The volume of exports in 1973 rose by 4.6 percent, while exportprices rose by 9Q8 nprr-nt- Tobacco and tea exnorts hoth rose substantia11yby volume, by 12 and 15 percent respectively, although these figures concealniquaity c-hanogs Th. volium in^rpaspe weprp stim,latnpid in the rca of the

former by an 8 percent price rise and in the case of the latter by favorablegrowing conditions. On the other hand the vuim of many other crops fell,including groundnuts, cassava, maize and cotton. In the case of all theseproducts the decline in volume was cushioned by in-ea-e in pri-c Su- and

rice have both been introduced into Malawi's exports in recent years, and in1973 both attained record volumes and prices. For the f4rst t4me the two

crops were able to make a significant contribution to export earnings of 4percent each.

. 1 L M 4o A4ec!.. f.hJ 4. 0 , e L e . i. Aer h nd se importJ - ,4- A 1 / j .7 _ S I ICLIzOL .F# _ssu11 L, V 1s IIX|L<LV/Iv* sXWL

since 1964, showed important structural changes. The share of consumer goodshlas decreased -Prom. 49 percent of m,erchandise 4n !964 to 28O ppercent in 1973.IL0 ci.L ca c £ LJL t2 p ic i L_ J UI_ A L.iLuuOc . ,U-t Li. £.)V ~ L LI I 1 J -

This reflects the substitution by the production of a number of local indus-tries oL gooUs previAous'ly imLILportedU. Mlost o'L thle new consumer goodus i'UnLustrLes

are based on imported raw materials. Important exceptions are cotton process-ing and the umanuf'acture of textiles, sugar and somue beverages, in wnicn tne

nature or volume of local raw materials endows Malawi with a comparative ad-vantage. imports of industrial raw materiais have grown more rapidly thanother imports, their share increasing from 29 to 40 percent in the 1965-1973period. Tne import of intermediate goods, particularly cement and buildingmaterials has grown rapidly to meet the needs imposed by increasing investment.Fuel and petroleum products accounted for about M percent of merchandise im-ports in 1973, and were some 30 percent greater in value than two yearspreviousiv. Recent oil price increases have not yet affected Malawi substan-tially, but total payments for fuel and petroleum products can be expected todouble from 1973 to 1974.

42. in 1973 the volume of imports declined by 9 percent, which afterallowing for a 12 percent increase in prices, implied an overall growth ofimport values of 3 percent. The decline in volume was due to reduced importsof capital goods and an exceptional decline in building and constructionmaterials imports. The volume of construction work undertaken by the Ministryof Works fell as several major works were completed, and private building

- 15 -

aciv4it- in Blantyre annd T gwe anlsoe fell of-f slightl Simultaneously;

the domestic production of building and construction materials increased byalmost 25 percent and competed effectively with imported produicts- There was

a reduction in the volume of imports of transport equipment for Malawi Railways,andI -in additon 1972 volume figur- w-r- raise hby the 4 mnnfrt nf n RAr 1-il&u X UA.L 1 -1 I -s s - | vv - ---- -j -.. , E-^ -- &^~

jet for Air Malawi. The overall decline in volume of imports does not suggestany~~1__ logtr, as n th-e level ofg AemandI in Malawi. In fact imports of

aiy IQ 1 JLr,-LCLtL ii .LL L -LIA .L V u - I L .. . .. o

consumer goods and most intermediate goods, apart from those related to con-struction, rose in volume in 1973. Th.e overall balance on non factor servicesremains negative due to the high incidence of freight and insurance charges on

Ma.law.' s ow,. trad'e.

*4. ractor service receipts lave grow.. Ja_ Ls Ltan pay si.

Independence, and the deficit on factor services was reduced to US$3.7 mil-

lion by 1973 compared to a deficit of US$8.6 M.Lillion in 1964. The number ofMalawians abroad working under the various mines labor recruitment schemeshas increased and at the same time wage rates paid have rLsen also. Assuch schemes provide for compulsory savings to be remitted to the workers'home country, there has been a rapid build-up of wage remittances, whichreached USS15 million in 1973 three times their level at Independence.Simultaneously, the growing use of technical assistance necessitated bythe development program and the increased number of expatriates in managerialpositions in the private sector has raised remittances abroad of earningsand profits. In total profits, interest and dividends reached US$15 millionin 1973, while earnings remittances were US$4 million.

44. Net transfers declined by just over 40 percent since Independenceto USS12.8 million in 1973, mainly as a result of the phasing out of Britishbudgetary aid. On the other hand, public long-term capital inflows havegrown, as British Development loans were increased, and as other assistancewas obtained from multilateral and bilateral sources. Inflows of publiccapital reached a peak in 1970 when the financing requirements for theNacala rail link were highest, but have generally shown an upward trendreaching US$28.4 million in 1973. Until 1972, most loans were made directlyto Government, with relatively little borrowing by public corporations.In 1972, significant borrowing was made for the first time by public enter-prises which to date have drawn on some commercial loans as well as theexisting channels of external public assistance that are being used by Govern-ment. The Government's policy has been to diversify and extend the sourcesof external aid as much as possible, and has been successful in this regard.

Whereas at Independence 90 percent of aid (grants and loans) originatedin the United Kingdom, aid donors now include West Germany, Canada, UnitedStates, Denmark, South Africa, African Development Bank, UNDP, and the WorldBank Group. Additional sources are still being sought, and are expected to

include the European-Development Fund, once negotiations have been completedfor associate membership in the European Economic Community.

- 16 -

45. Encouraged by the libera1 nrocedures on foreign exchange transac-tions and profit and capital repatriation and by other domestic policiesfavorabe1 to the onperatlons of private enter-rise, there has been a growth"in the amount of private capital inflows. Whereas they were minimal duringthe mid 1960s, these inflows amounted to US$,19.7 ,million in 19'73, Just over40 percent of total long-term capital inflow. The conditions accorded toprivate capital, particular!y re-ardin- taxat4on, are liberal. Clearlycaution would be essential in making any adjustments, given the role thatMalawi wishes private capital (external and internal) to pl-ay in the develop=-ment process.

46. Net foreign exchange reserves have risen every year since 1969.A particularly large rise was achieved in 1973, when reserves doubUed toUS$65 million or 6 months' imports. In a period of international inflationand co-m.odity price adjustments , iLt may ue desirable to old o1 lig amounts ofreserves and in this respect the windfall gains of 1973 may serve a usefulpurpose in th.. e years to come.

47. The external public debt of Malawi hdas increased as U.K. grantshave been replaced by loans and as other committed loans were disbursed.At the end of 1973, public sector externally held debt amounted to US$189.1million. The terms of overall assistance have hardened gradually as grantswere withdrawn, tLough a determi-uination to use whatever concessionary fundsmight be available has meant a gradual softening of the terms of new commit-ments. The average termLs of Government debt at the end of 1973 were equiva-lent to 2 percent interest and an average maturity of 25 years, though thetLerm,s of other public debt were raised by a loan of US$5 million incurredduring 1973 on commercial terms. Debt service on public debt in 1973 wasUS$11 million or about 10 percent of export earnings (including non-factorservices). This ratio remains well within the country's debt carryingcapacity.

III. MAJOR SECTORS

A. Agriculture

48. Agriculture is the mainstay of Malawi's economy, currently accountingfor almost half of GDP and providing the main occupation for most of the ruralpopulation, as well as over one-third of modern wage employment. Agriculturalcommodities account for most of the country's foreign exchange earnings andprovide raw materials for domestic industry. About 5.3 million hectares(about half of the total land area) are arable, of which 1.7 million arepresently utilized, three-quarters for maize production. Although there isunused arable land, much of this is classified as marginal, and the unevenpopulation density has in fact meant land has been relatively scarce in someareas. Despite reasonably good soils, the mountainous nature of the countryprecludes mono-cropping without special conservation measures in all butthe most favorable areas.

- 17 -

49. Prompted by a belief that further increases in acreage would leadto erosion, loss of fertility and the possibility of an ultimate shortage ofland, particularly in the Southern Region, the Government adopted as the mainobjective of agricultural policy rises in the productivity of smallholdersto realize an exportable surplus of various crops such as groundnuts, rice,cotton, tobacco and cassava and maintain self-sufficiency in food staples. 1/Secondly, to increase production of exportable crops still further, Governmentprovided a liberal institutional framework to encourage the development ofagricultural estates. Given Malawi's lack of mineral or manufactured goodsfor export, the role of these estates in the development process has beencrucial. They have concentrated on export crops and thus provided a rapidlygrowing source of foreign exchange, and in 1973 this accounted for half ofexports. At the same time, the expansion of estates has proved an effectivemeans of supplementing cash incomes in rural areas. Government's policy hasbeen to avoid direct intervention in estates development, preferring to limititself to defining the framework within which estates can operate.

50. The basic food crop is maize; other food crops are pulses, ground-nuts, cassava, rice; sugar and wheat. The princinal expnort crons are tobacco,tea, groundnuts, and cotton, with some export of foodcrop surpluses, notablynulses; cassava, rice and, more recently, maize. In 1973, 69 percent ofagricultural production was for subsistence. Estate production accounts forthree fifths of marketeAd out-ut. It mainly consists of tea, certain varietiesof tobacco, tung oil and some sugar.

/ n Uetailed review of' smallholder agricuLture is available in thae IBRDreport entitled-Agricultural Sector Review, Malawi, No. 235a datedDecember 28, 1973.

- 18 -

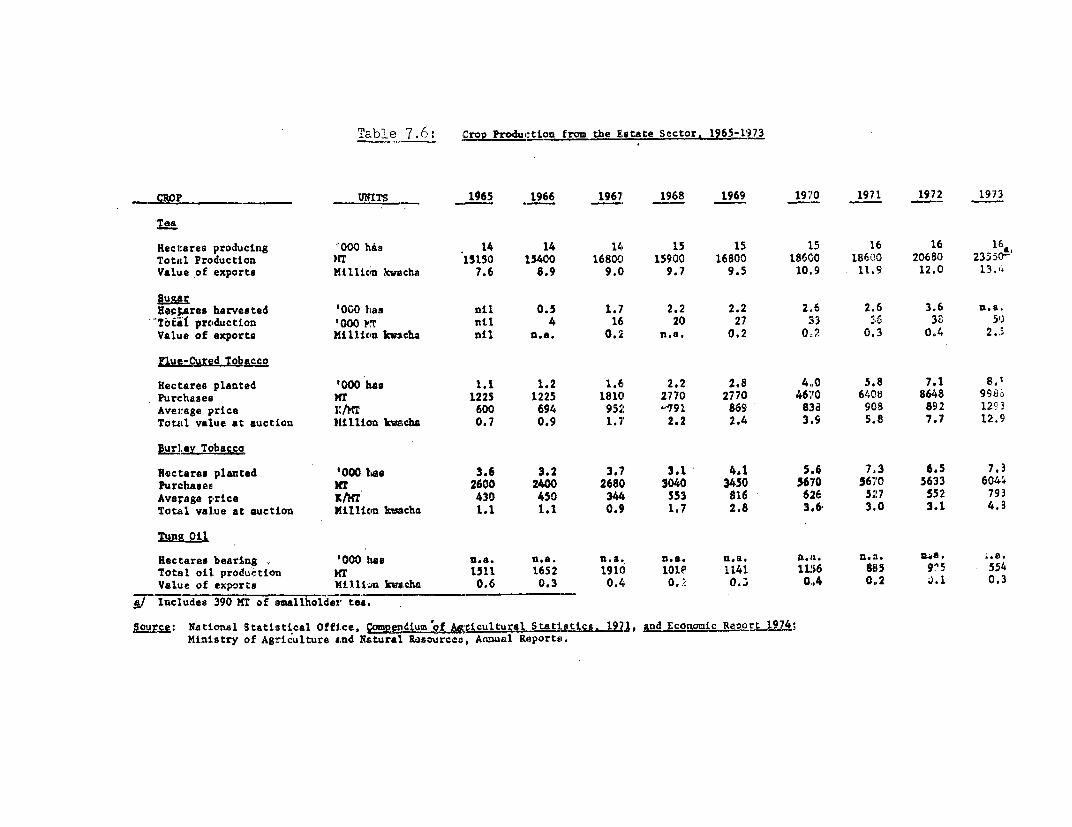

Table 6: Selected Agricultural Indicators

Average1964 1973 Annual Growth Rate

M%)

Value Added (current K million) 85.0 174.6 8.3

Smallhnldepr! non-monetarv Droduct 63.1 119.8 7.3Smallholders' monetary product 15.9 32.5 8.3Estates' product 5.9 22-3 15.9

Agriculture (as L nf GnP' '7-2 46.0

Agricultural Exports (current V million) 22.1 63.4 12.4

Sm1llholders't expts 12 89R7 lA nEstates' exports 9.9 34.7 15.0

Agricultural exports (as % ofmerchandise exports) 88.4 79.9

Agricultural wage em.ploym-entflLAgr4CU.L ural wage emlymn

(as % of total wage employment) 32.9 /1 35.4

/I 1968 figure.

Smallholder Agriculture

51. The increase in smallholders monetary output has been achievedmainly through some major development projects. These projects, which startedin 1965 have been aimed at increasing farmers' productivity by improvedcultivation practices supported by credit for farm inputs and more concentratedextension services. The Government has carried out several major projectsof this type, financed by the World Bank Group, the UK and the FederalRepublic of Germany. IDA credits helped finance the development of threeareas near Karonga in the North, Lilongwe in the Central Region, and theLower Shire Valley in the South. The UK Government participated in the finan-cing of the Dwangwa project in the North and is considering the Palombe projectin the South. The German Government assisted the Salima Project in theCentral Region. Each project contains a package of services designed to meetthe requirements of the particular region. For example, the Lilongwe projectintroduced a registration system to provide permanent ownership by farm famil-ies, and helped finance land development and reorganization, marketing andstorage facilities, extension services, credit for farm inputs, and adminis-trative services and staff training on an integrated regional basis. About10 percent of Malawi's rural population lives in areas covered by suchprojects.

- 19 -

52. Little is known about the efficiency of investment in extensionschemes. A World Bank survey on the performance of the Lilongweproject could only conr1lude in qualita-tivP terms that the nroiect has had apositive effect on cultural practices, and has been successful in encourag-ing the use of fertilizers, credit and other innruts Howevevr; owine to the

wide variety of services provided, the cost of these projects per family isrelatively high ranging from K 450 to K 1000 per fnmily. The need to reacha wider proportion of the population at a lower unit cost is apparent, anda proposed National Rural Development Program. (NRDP) to achieve this ob4ec-tive is presently being considered by Government.

53. The basic concept underlying such a program should be to maximizethe returns on existing resources anL inves-LtmUents --A increasing the latteronly after marginal returns begin to decrease. This approach would be incontrast with the past approatch ofL Goverrau,ent whLi 'chL L-a" injected sizableinfrastructure improvements at the outset of the development sequence. ForeAdmple, a sh-ift in approach muight lead to thle udrelopm.ent of project areaaround existing roads, research stations or market centers, enabling maximumbenefLit to bve made o01 tlehLr presence f0or certa'Ln serCLvices, providing other

services as necessary to enable potential benefits to be realized. The lower-ing of unit costs that this wou;li entail would enable wider proportions of thepopulation to be reached. One of Government's proposals is to integrate therural development effort horizontally by defining development foci, andorganizing activities around these. Administrative and institutional in-frastructure might be used to cover a continuously expanding geographicalarea, and hence technical experience and innovations specifically suited toa given planning area could gradually be transferred outwards until muchwider geographic coverage was achieved. Existing major development projectscould serve as some of the development foci, enabling use to be made ofstaff already trained for these projects.

54. In addition to the major rural development project, there arevarious settlement schemes aimed at increasing in an orderly fashion theacreage cultivated, especially in the less densely populated areas. Some ofthese schemes are linked to the major development projects, while others func-tion independently. Government's objective was originally to settle about1,000 families annually, though only half these numbers were actually settied,and unit costs have tended to be high, averaging over K 500 per dryland farmer.Implementation difficulties adversely affected settlement results. Participantswere drawn from Malawi Young Pioneers (one-third) and local inhabitants (two-thirds). A number of Young Pioneers, sometimes as much as 50 percent of theoriginal settlers left the scheme after a relatively short time, and in somecases local participants were not available in sufficient numbers to occupyall available plots. An initial step should be to proceed to a more compre-hensive evaluation of the problems of existing settlement schemes. In caseswhere present settlement schemes are under-utilized, their insertion into aNational Rural Development Program could be beneficial.

- 20 -

55. O..e c-lusion of the Bank repnort (on. cit. page 28) was that

smallholder credit needs were not adequately met. Many smallholders pre-viously served during the project imnl1epntatinn found themselves without

access to credit once the development phase was completed. In view of the

high cost of providing credit to this sector, Government has some reservations

about continuing to provide credit with the present structure of charges, and

is cos'L.er'.rg continuing creAit on a- experitental basis with higher charges,

56. UovernLmenLt agricultural price polic-y has generall favored export

crops in line with production objectives. Prices paid to smallholders are

controlled uy Governr,.ent , wit the aim, inter alia, of selding smailholders

from fluctuations in prices. The Agricultural Marketing and Development

Corporation (AUrARC) an-ouices its pr-ices far enough in advance to be useful

to farmers in their planting decisions, and are generally held constant

throughout a cropping season. A"DARC prices are guaranteed minima, and are

not binding on sales to local private traders though export crops have to

pass through ADHARC. Helped by risirlg export prices, AD.MARC has been verysuccessful in avoiding downward price movements which, it is believed, would

have a strong disincentive effective. In general, however, prices have been

well below export parities, enabling substantial surpluses to be accumulated

by ADMARC. Higher farm prices were offered irn 1974, with increases ranging

generally from 20 percent to 40 percent for groundnuts, cotton, pulses, sun-

flower seed, sesame, castor seed and wneat. There was also a r'ise of 40 per-

cent in the farm price of maize. Smallholder tobacco prices remained unchanged,

but a second payment will be made at the end or thre season depending on

realized prices.

57. While raising prices of export crops is clearly consistent with

Government's desire to raise exports, increasing foodcrop prices may also be

necessary to achieve the goal of self-sufficiency in food staples. Keeping

producer prices of these to previous levels dampens increases in consumer

food prices, and thus plays a part in Government's wage-price policy. However,

changes in relative prices between export and food crops could alter produc-

tion patterns significantly, assuming that producers respond to price incen-tives. This could compromise the country's basic food supply, particularlyfor urban consumers, by reducing the incentive to concentrate on increased

production of foodcrops. Moreover, relatively lower prices for foodcropscould affect financial returns in some rural development projects where maize

and paddy constitute major components. Continuing attention should be givento these aspects and foodcrops prices revised if evidence appears that the

possibilities outlined above are actually occurring.

58. The nutritional diet is generally satisfactory. But recent study

by a Freedom From Hunger Campaign nutrition team indicated that in certain

areas nutritional problems exist, owing to general food shortage. Among the

suggestions (which Government supports) were that the Ministry of Agriculture

be made responsible for a food and nutrition program within the presentextension services effort, future projects containing a nutrition component.

Staffing and funding difficulties are at present slowing progress in this

respect. A nutrition unit is also being established in the Ministry of Health.

- 21 -

Estates Agriculture

J. Es'ltatLes agriculture ir. Malawi'u dates bUackll to th'e colonr.ial -periodL-U

prior to 1964, when freehold or leasehold titles to land were given mainlyto expatrjLate fLaruers uy the coloni'.1 administration. Ln ger.eral, freeholdtitles were given to tea growers and leasehold titles to other producers.Most estates established prior Lo independence remain in producLion. Some74 still exist, with an average size of 200 ha. Shortly after Independence,Government adopted a policy of maintaining Lhe estates as productive concernsand later on amplified this policy to one of gradual expansion. Only Malawinationals are granted new leases. Resourceful individuals, including (poli-tical personalities) civil servants are encouraged to establish new estateswith initial assistance in land selection from the Ministry of Agriculture.Such new estates are exclusively on a leasehold basis and produce mainlytobacco. Only Malawi nationals are granted new leases. Although Governmentencourages estates, it provides little active support to operators, preferringto concentrate on smallholders. Management, input supply, marketing and, withthe exception of INDEBANK, financing are left entirely to the private sector.Estates are taxed, like corporations, at the rate ot 4u percent of unretainedprofits.