Embed Size (px)

Citation preview

US Securities and Exchange Commission Office of FOIA Services 100 F Street NE Mail Stop 2745 Washington DC 20549-5100

Dear FOIA Office

August 3 2018

RECEIVEgt AUG 63 2018

Under the Freedom of Information Act (FOIA) we are requesting a copy of the following

KRAFT HEINZ CO comment letters DOC DATE 112001 to 12312006 CIK NUM 0001637459

Process this request up to our education-use entitlements

Thank You

Dr Amy Hutton Boston College Carroll School of Management Chestnut Hill Massachusetts 02467

Office of FOIA Services

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

STATION PLACE 100 F STREET NE

WASHINGTON DC 20549-2465

Dr Amy P Hutton Boston College Carroll School o f Management Chestnut Hill MA 02467

August 14 2018

RE Freedom of I n f o rmation Act (FOIA) 5 U S C sect 552 Request No 18-02709-FOIA

Dear Dr Hutton

This letter is in response to your request dated and received in this o f fice on August 3 2018 f o r SEC comment letters to Kraft Heinz Co from January 1 2001 to December 31 2006

The search f or responsive records has resulted in the retrieval o f the enclosed l ett ers dated Apr i l 26 2002 January 17 2003 September 30 2004 December 1 200 4 January 19 2005 February 14 2005 January 26 2006 February 15 2006 May 30 2006 June 23 2006 June 30 2006 Ju l y 1 10 20 and 21 2006 and August 9 2006 that may be responsive to your request

I f you have any quest i ons p l ease contact me at jacksonwsec gov or (202) 551 - 8312 You may a l so contact me at foiapasec gov or (202) 551-7 900 You also have the right t o seek ass i stance f rom Jef fery Oval l as a FOIA Publ ic Li aison or contact the Of fice of Government I nformati on Services (OGIS) f or d i spute resolut ion servi ces OGI S can be reached at 1 - 877-68 4-6448 or Archives gov or via e - mai l at ogi snara gov

Si ncerely

tJ~rmicro__ Warren E Jackson FOIA Research Speci al i st

Enclosures

S-4

0000000000-03-016783-1002 Page 1 of 8

April 26 2002

via facsimile and US mail

Mr Leonard A Cullo JrPresident H J Heinz Finance CompanyTreasurer H J Heinz Company600 Grant Street Pittsburgh PA 15219

RE H J Heinz Finance CompanyForm S-4 filed March 27 2002File No 333-85064

H J Heinz CompanyForm 10-K for year ended May 2 2001 Filed July 27 2001File No 1-3385

Dear Mr Cullo

We have reviewed the above filings and have the following comments Where indicated we think you should revise your documents in response to these comments However if you disagree we will consider your explanation as to why our comment is inapplicable or a revision is unnecessary Please be as detailed as necessary in your explanation In some of our comments we may ask you to provide us with supplemental information so we may better understand your disclosure After reviewing this information we may or may not raise additional comments

Please understand that the purpose of our review process is to assist you in your compliance with the applicable disclosure requirements and to enhance the overall disclosure in your filing We look forward to working with you in these respects We welcome any questions you may have about our comments or on any other aspect of our review Feel free to call us at the telephone numbers listed at the end of this letter

Where comments on one filing impact disclosure in another filing please make corresponding changes to all affected sections and documents

General

1 The staff notes that you are registering the new notes in reliance on the staff`s position enunciated in Exxon Capital Holdings Corporation (available April 13 1989) Morgan Stanley amp Co Incorporated (available June 5 1991) regarding resales and Shearman amp Sterling (available July 2 1993) with respect to the participation of broker-dealers Accordingly with the next amendment please provide a supplemental letter to the staff stating that the issuer is registering the exchange offer in reliance on the staff`s position in such letters and including the statements and representations substantially in the form set forth in the Morgan Stanley and Shearman amp Sterling letters We may comment further upon reviewing your response

2 Prior to printing and any distribution of the preliminary prospectus please provide us with copies of all artwork and any graphics you wish to include in the prospectus Also provide accompanying captions if any We may have comments after reviewing the materials

3 Please update your disclosure in the amended registration statement so that it is current as of the latest practicable date Also supply information you now omit

4 We note that you intend to use two forms of prospectuses for the exchange offers that you will conduct simultaneously Ensure that you make corresponding changes to parallel provisions of both

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-03-016783-1002 Page 2 of 8

documents in response to the staff`s comments

5 Briefly mention the other simultaneous exchange offer on the cover page of each prospectus Add a cross reference to later in the document where you discuss the other offer in greater detail

6 Under the Exxon Capital line of letters the exchange offer may only remain in effect for a limited time Disclose the maximum period of time that the exchange offer will remain in effect from the date the registration statement is declared effective through the expiration date as extended

7 Quantify on the cover page the current amount of indebtedness prior in right of payment to the notes if any Also quantify as of the most recent practicable date the amount available for borrowing that would be prior in right of payment to the notes

Forward-Looking Statements - page 2

8 The safe harbor provided by the Private Securities Litigation Reform Act for forward-looking statements is not available to you as you are not a reporting company Refer to Section 27A(a)(1) of the Securities Act and Section 21E(a)(1) of the Exchange Act Accordingly delete all references to the Litigation Reform Act from your current prospectus and ensure that the disclosure at page 2 and elsewhere does not incorrectly suggest that the forward-looking statements are covered by the safe harbor or that the disclosure constitutes forward-looking statements within the meaning of the Federal securities laws This includes any disclosure you incorporate from other filings We note for example that the section from the Heinz Form 10-K that you cite includes these references

9 If you retain it move this section and the next two sections so that they appear in the text after the Risk Factors section Refer to Item 503(c) of Regulation S-K

Where You Can Find More Information page 3

10 Remove from this section and the next your references to the Commission`s regional offices Persons may inspect and copy reports at the Public Reference office located at Commission Headquarters in Washington DC but the reports are not available for these purposes at our regional offices

Summary page 5

11 Provide the telephone number of your principal executive offices See Item 3(a) of Form S-4

Risk Factors page 9

12 You do not precisely identify and discuss the risks in the second risk factor Please revise the caption and discussion accordingly Also ensure that all your captions precisely identify the particular risk and harm that could result

13 Rather than stating there can be no assurances please revise this risk factor and the fourth risk factor to state the risk plainly and directly

14 The last two sentences under We Depend Upon Our Subsidiaries mitigate the risk This information may appear later in the document but it should not appear in the Risk Factors discussion

15 The last risk factor does not state a risk of the exchange offer but instead discusses issues relating to the failure to exchange This information may appear later in the prospectus

No Cash Proceeds - page 11

16 Disclose how you used the funds originally obtained through both initial offerings of notes Refer to Instruction 4 to Item 504 of Regulation S-K for example

Ratio of Earnings to Fixed Charges page 11

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-03-016783-1002 Page 3 of 8

17 Please comply with Instructions 2(D) and 3 to Item 503(d) of Regulation S-K

Overview of Entity Structure - page 12

18 Ensure that you disclose here or later in the prospectus the applicable interest rate for all material outstanding debt obligations Also use cross-references rather than repeating disclosure word-for-word at page 18

Reorganization

19 Revise your disclosure here and elsewhere in your filing as appropriate to explain in reasonable detail the business purpose of the reorganization Also explain how the reorganization helped you to achieve the described business purpose

20 Revise your discussion of the ownership of Heinz LP here and elsewhere in your filing including your financial statements to explain the terms of the Class A and Class B interests Quantify the ownership interest represented by each class

Management`s Discussion and Analysis of Financial Condition and Results of Operations -- page 18

Liquidity and Financial Position

21 Your balance sheet as of January 30 2002 indicates that you have substantially more debt than has historically been associated with the US Group Revise your MDampA to include a discussion of this and to describe in reasonable detail the impact that increased debt levels will have on your financial position results of operations and liquidity in future periods

22 We note that reported balances of accounts receivable as of January 30 2002 and May 2 2001 are materially higher than amounts reported as of May 2 2001 and May 3 2000 respectively We also note that as of May 2 2001 the allowance for doubtful accounts is significantly lower both as an absolute amount and as a percentage of accounts receivable than as of May 3 2000 Revise your MDampA to include a reasonably detailed discussion of the causes of these trends Describe any implication that these may have on your financial position liquidity or results of operations in future periods

23 Clarify your reference to the decrease in cash used during the most recent 9-month period

24 We note your references to credit agreements and other indebtedness If you must maintain any financial ratios pursuant to your agreements or otherwise identify and quantify them in this section Also discuss any other material limitations on future capital expenditures or the incurrence of additional indebtedness

25 Expand the discussion of the changed credit ratings on Heinz`s debt to explain briefly the significance of these changes

Business page 36

26 You state that you have the most popular brand and that you are one of the most innovative companies In the MDampA section you refer to various products or divisions as being leaders Clarifyin context all references to leadership to explain what this signifies in each case For all assertions of this nature please provide us with independent supplemental support You may includeexcerpts from appropriate studies or other sources but you should clearly mark the documents to expedite the staff`s review

Consumer Marketing and Advertising - page 39

27 Ensure that your disclosure is fair and balanced For examplethe reference to 100 million viewers watching NFL football on television does not relate to the number of viewers who are watching games from Heinz Field Also explain in context your assertion regarding $44 million in advertising if you retain the claim

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-03-016783-1002 Page 4 of 8

Trademarks Patents and Licenses - page 41

28 Expand the disclosure to provide all the information Item 101(c)(1)(iv) of Regulation S-K requires

Related Party Transactions - page 43

29 The reference to apportionment on an arm`s length basis is not appropriate given the affiliation of the parties Instead disclosewhether each of the listed transactions are or will be on terms no less favorable to you than could be obtained from unaffiliated parties

Management - Directors and Executive Officers - page 44

30 Revise the biographical sketches to eliminate any potential gaps or ambiguities with regard to time in the five-year business descriptions For example it is unclear when in 1999 Ms Stein left Clorox whether Mr Winkleblack immediately joined Indigo Capital upon leaving C Dean Metropoulos in 1999 and whether he joined CDM immediately after leaving Six Flags in 1998

31 Revise the sketches to provide the principal business conducted by each of the Clorox Company Global Securitization Services LLC Indigo Capital C Dean Metropoulos and Six Flags Entertainment Corporation Refer to Item 401(e)(1) of Regulation S-K Description of the New Notes - page 49

32 Delete the second and third sentences of the introductory paragraph In the alternative revise to clarify that this section discusses all material terms rather than just certain incomplete provisions and explain the plural reference to documents in the third sentence

33 Rather than using embedded lists in this section use bullet points or a similar presentation Refer to Plain English Comes to the High Yield Market a Latham amp Watkins Standard Form Prepared in Consultation with the SEC August 1999

Events of Default - page 52

34 You do not describe in necessary detail all material events of default For example we refer you to items (v) and (vi) in the first paragraph List and describe in necessary detail all material events of default

The Exchange Offer - page 58

35 Revise the fifth paragraph including the second sentence to eliminate any suggestion that the staff views your exchange offer as like those that were the subject of other no-action letters You may instead use the language that appears at pages 60 and 68 - certain no-action letters issued to third parties -- in that regard

Procedures for Tendering - page 61

36 Holders need not represent that they understand any particular provisions requirements or consequences Revise the fourth bullet point at page 63 and any related materials accordingly

Taxation - page 66

37 You state that note holders should consult with their own tax advisors Because note holders may rely on the disclosure that appears in your registration statement including disclosure relating to tax consequences revise to eliminate this language You mayreplace the admonition with language to the effect that you recommend or encourage that consultation

Report of Independent Accountants

38 Ensure that the dates cited in the report are accurate It appears that May 3 2000 is the correct date for example

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

S-4

0000000000-03-016783-1002 Page 5 of 8

Part II

Item 21 Exhibits

Legality Opinion

39 Obtain an opinion that does not assume the due authorization execution and delivery of the Indenture or explain to us why you believe this is an acceptable assumption

40 Obtain an opinion that does not assume the New Notes will have been authorized or explain this assumption further

41 If counsel intends to render an opinion on the tax consequences that can be listed as Exhibit 81 the opinion must either constitute a short-form or long-form opinion Refer to Item 601(b)(8) of Regulation S-K The current reference in the fourth paragraph constitutes neither

42 Counsel`s opinion should include the file number for the registration statement

43 Obtain an opinion that is not rendered solely to you The opinion also may not suggest that investors cannot rely upon the opinion

44 If counsel limits its opinion to the state laws of a particular state the opinion should make clear why this limitation is appropriate

45 The opinion should clearly state that counsel consents to the use of its name in the registration statement

Item 22 Undertakings

46 Include the disclosure required by Item 22(c) of Form S-4

10-K for the fiscal year ended May 2 2001

Item 1 Business page 2

47 On page 4 we note that you are subject to inspections by various governmental agencies Please revise your disclosure to identify and if necessary briefly describe the applicable laws to which you are subject

Item 7 Management`s Discussion and Analysis of Financial Condition and Results of Operations page 9

48 Describe your material commitments for capital expenditures as of the end of the latest fiscal period Indicate the general purpose of such commitments and the anticipated source of funds needed to fulfill such commitments See Item 303(a)(2)(i) of Regulation S-K

ACCOUNTING COMMENTS

Heinz Finance Selected Historical Consolidated and Combined Financial Data page 14

49 The introduction to your presentation of selected financial data indicates that data for 1997 and 1998 has been prepared using the domestic segment information in the Heinz annual reports and removing those items that are not part of the US Group`s operations To helpus understand the basis for this presentation send us as supplemental information a description and quantification of the items removed from the domestic segment information to produce the reported amounts Also tell us whether or not the methodology employed produces a presentation that is comparable to amounts included in your filing for periods subsequent to 1998

Financial Statements

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-03-016783-1002 Page 6 of 8

Annual Financial Statements of US Group

Statement of Cash Flows page F-5

50 Supplementally provide an analysis of the items included in the line items Other net in the operating and investing section of your cash flow statements Explain your basis for presenting these items on a net basis

Note 1 Basis of Presentation page F-6

51 We note that prior to the reorganization entities and operations included in the US Group had operated as components of Heinz In view of this explain to us your basis for presenting historical financial statements of the US group on a stand-alone basis As part of your response tell us whether or not the financial statements of the US Group include all of the assets liabilities operations and costs that have historically been associated with the entities and operations presented Refer to SAB Topic 1-B1

Note 14 Segment Data page F-19

52 Refer to the segment information presented here and in Note 12 page F-32 and the segment information included in the quarterly reports on Form 10-Q filed by Heinz for the periods ended August 1 2001 and January 30 2002 Supplementally quantify and explain the reasons for the differences in amounts reported for Heinz North America US Pet Products and Seafood and US Frozen in the S-4 as compared to amounts reported by Heinz Based on our understanding of the businesses included in Heinz Finance we would expect a difference in the Heinz North America segment due to the exclusion of Heinz Canada from amounts reported by Heinz Finance However it isnot clear why amounts for other segments do not agree Please clarify this for us

Interim Financial Statements of H J Finance Company and Subsidiaries

Note 1 Basis of Presentation page F-26

53 Revise this section to include a note indicating if true that accounting policies of Heinz Finance are the same as those described for the US Group Explain any situations where this is not the case

54 We understand that your interest in H J Heinz Company LP (Heinz LP) consists of Class B limited partnership interests and that you do not own or otherwise control the general partner interest If our understanding is incorrect please advise Otherwise explain to us why you believe that reporting Heinz LP on a consolidated basis is appropriate Include reference to specific authoritative literature

55 We note your disclosure indicating that certain assets and liabilities that are included in the May 2 2001 carve-out balance sheet were not contributed to Heinz Finance Revise the disclosure to clarify the nature and amount of all items including inventory that were not transferred Separately given that certain assets and liabilities were not transferred supplementally explain to us why you believe your current presentation is appropriate

Note 6 Acquisitions page F-28

56 Revise your disclosure under this note to include the items required by SFAS 141 par 58

57 Your disclosure under this note indicates in part that pro forma results reflecting the acquisitions would not be materially different from the results reported However based on discussion in various parts of your MDampA it appears that the impact of acquisitions may have been material In this regard we note the discussion in MDampA page 23 of the impact of acquisitions on sales during the nine months ended January 30 2002 In view of this send us as supplemental information an analysis supporting your

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-03-016783-1002 Page 7 of 8

conclusion that pro forma amounts would not differ materially from reported amounts Address all of the measures identified in APB 16 par 96

58 Send us as supplemental information your analysis of the significance of the acquisitions completed by Heinz Finance during the nine months ended January 30 2002 Refer to Item 3-05(b)(2) of Regulation S-X

H J Heinz Company

Report on Form 10-Q for the Quarterly Period Ended January 30 2002

Financial Statements

Note 6 Acquisitions page 8

59 Revise your disclosure under this note to include the items required by SFAS 141 par 58

60 Your disclosure under this note indicates in part that pro forma results reflecting the acquisitions would not be materially different from the results reported However based on discussion in various parts of your MDampA it appears that the impact of acquisitions may have been material In this regard we note the discussion in MDampA page 16 of the impact of acquisitions on sales during the nine months ended January 30 2002 In view of this send us as supplemental information an analysis supporting your conclusion that pro forma amounts would not differ materially from reported amounts Address all of the measures identified in APB 16 par 96

General Information

As appropriate please amend your registration statement in response to these comments and comply with Rule 310 of Regulation regarding the marking of changed material You may also wish to provide us with marked copies of the amendment to expedite our review

Please furnish a cover letter with your amendment that keys your responses to our comments and provides any requested supplemental information Detailed cover letters greatly facilitate our review Include in your response letter page references to the amended registration statement indicating where you made changes in response to our comments Also please note the location of any material changes made for reasons other than responding to a specific comment Please understand that we may have additional comments after reviewing your amendment and responses to our comments

We direct your attention to Rules 460 and 461 regarding requesting acceleration of a registration statement Please allow adequate time after the filing of any amendment for further review before to submitting a request for acceleration Please provide this request at least two business days in advance of the requested effective date

Please direct questions regarding accounting issues and related disclosures to Brad Skinner at (202) 942-1922 or in his absence to Barry Stem Senior Assistant Chief Accountant at (202) 942-1919 Direct all other questions regarding disclosure issues to Carrie Cleaver at (202) 942-2972 or in her absence to Timothy Levenberg Special Counsel at (202) 942-1896

Sincerely

H Roger SchwallAssistant Director

cc H Roger SchwallBarry Stem

Timothy LevenbergBrad Skinner

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-03-016783-1002 Page 8 of 8

Carrie Cleaver HJ Heinz Finance CompanyApril 26 2002page 12

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON DC 20549-0405

DIVISION OF CORPORATION FINANCE

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

S-4

0000000000-03-016788-1002 Page 1 of 4

January 17 2003

via facsimile and US mail

Mr Leonard A Cullo JrPresident H J Heinz Finance CompanyTreasurer H J Heinz Company600 Grant Street Pittsburgh PA 15219

RE H J Heinz Finance CompanyForm S-4 as amended December 4 2002 File No 333-85064

H J Heinz CompanyForm 10-K for year ended May 2 2001 Filed July 27 2001File No 1-3385

Dear Mr Cullo

We have reviewed the above filings and have the following comments Where indicated we think you should revise your documents in response to these comments Where comments on one filing impact disclosure in another filing please make corresponding changes to all affected sections and documents

General

1 We note your response to the first comment from our letter dated April 26 2002 Please provide a supplemental letter from the company that includes the statements and representations prior comment 1 requested A letter from counsel is not sufficient

Forward-Looking Statements - page 77

2 We note your responses to prior comment 8 and 13 If you repeatthe staff`s comments in your letter of response please ensure that you repeat the comment precisely as rendered originally 3 Moreover please note that the safe harbor provided by the Private Securities Litigation Reform Act for forward-looking statements does not apply to statements made in connection with a tender offer Please make appropriate revisions as necessary to comply with our original comment Refer to Section 27A(b)(2)(C) of the Securities Act and Section 21E(b)(2)(c) of the Exchange Act

Summary - page 3

4 Please include updated information throughout the prospectus including in the new Recent Developments section

Risk Factors - page 8

5 To expedite our review we suggest that you prepare marked versions of documents that would be helpful You have not accurately and precisely marked the changes to pages 9 through 11 for example You likely would substantially reduce the necessary review time for future submissions by us providing documents that have been properly marked

MDampA - page 9

6 We note your disclosure in the MDampA section of your annual report (incorporated by reference into the MDampA section of your 10-K for 2002) regarding commitments However either specifically state whether or not you have material commitments for capital expenditures as of the end of the latest period or identify where you state this in your document If you do have such commitments please indicate the general purpose of such commitments and the anticipated source of funds needed to fulfill such commitments See Item 303(a)(2)(i) of Regulation S-K

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-03-016788-1002 Page 2 of 4

Incorporation of Certain Documents by Reference - page 10

7 Please refer to the text that appears in bold face type at the end of the second paragraph While it is appropriate to indicate by brackets or other means any information such as dates that is subject to change please ensure that the document you file with the Commission does not include text that could suggest to the reader it is a draft version

No Cash Proceeds - page 11

8 Please quantify the amount of commercial paper you retired with the proceeds and disclose the average interest rate

Management - Directors and Executive Officers - page 50

9 Revise Mr Winkleblack`s sketch to describe his business experience from the time he left Six Flags in April 1998 until the time he joined C Dean Metropoulos in August of that year Refer to prior comment 30

Legality Opinion

10 Please obtain an opinion on the guarantees We note that you have obtained an opinion on the notes In that regard the limitation to the state laws of New York and Delaware would appear to be insufficient as HJ Heinz Company is a Pennsylvania corporation

Financial Statements and Related Disclosure

General

11 Update the financial statements as required by Rule 3-12 of Regulation S-X

12 Provide a currently dated consent of the independent accountant with each amendment

13 Please call our accountants to discuss your responses to comments 51 57 58 and 60

Form 10-K Annual Report to Shareholders

Management`s Discussion and Analysis page 31

14 In future filings remove per share disclosure of the effect of special items on reported results from textual discussions of the charges and tabular presentations in each period presented See Question 15 of SAB Topic 5-P

Market Risk Factors page 43

15 In future filings summarize the market risk information from the preceding fiscal year to highlight changes in exposure See Item 305(a)(3) of Regulation S-K

16 Supplement the tabular presentation of debt obligations with a discussion of the terms underlying the floating rate debt in future filings Are the rates tied to LIBOR US Treasuries or another index

Note 4 - Restructuring Charges page 59

17 In future filings remove per share disclosure of charges stemming from the company`s Streamline and Operation Excel restructuring initiatives See Question 15 of SAB Topic 5-P

Note 12 - Financial Instruments page 70

18 In future filings revise disclosures to include the tabular presentation and other information specified by paragraph 10 of SFAS 107 and paragraph 532(a) and (b) of SFAS 133 Provide comparative

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-03-016788-1002 Page 3 of 4

information for all periods for which a balance sheet is presented

Form 10-Q for the quarter ended October 30 2002

Note 5 - Recently Adopted Accounting Standards page 8

19 Supplementally provide us with a more detailed description of the methodology used for your transitional goodwill impairment tests Include a summary schedule of your calculations

Management`s Discussion and Analysis page 15

20 Expand your discussion of the $778m transition impairment of goodwill to indicate what circumstances contributed to the deterioration of goodwill value in the European and Other Operating Entity reporting units Discuss whether these circumstances continue to exist indicating the possibility of additional impairment charges in the near term

Closing Comments

As appropriate please amend your registration statement in response to these comments and comply with Rule 310 of Regulation regarding the marking of changed material You may also wish to provide us with marked copies of the amendment to expedite our review

Please furnish a cover letter with your amendment that keys your responses to our comments and provides any requested supplemental information Detailed cover letters greatly facilitate our review Include in your response letter page references to the amended registration statement indicating where you made changes in response to our comments Also please note the location of any material changes made for reasons other than responding to a specific comment Please understand that we may have additional comments after reviewing your amendment and responses to our comments

We direct your attention to Rules 460 and 461 regarding requesting acceleration of a registration statement Please allow adequate time after the filing of any amendment for further review before to submitting a request for acceleration Please provide this request at least two business days in advance of the requested effective date

Please direct questions regarding accounting issues and related disclosures to Gabrielle Malits at (202) 942-2873 or in her absence to Kim Calder Assistant Chief Accountant at (202) 942-1879 Direct all other questions regarding disclosure issues to Carrie Cleaver at (202) 942-2972 or in her absence to Timothy Levenberg Special Counsel at (202) 942-1896

Sincerely

H Roger SchwallAssistant Director

cc H Roger SchwallKim Calder

Timothy LevenbergGabrielle Malits Carrie Cleaver

HJ Heinz Finance CompanyJanuary 17 2003page 5

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON DC 20549-0405

DIVISION OF CORPORATION FINANCE

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-03-016788-1002 Page 4 of 4

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-04-031471-1001 Page 1 of 4

September 30 2004

Mr Arthur B Winkleblack Executive Vice President and Chief Financial Officer H J Heinz Company600 Grant Street Pittsburgh Pennsylvania 15219

Re H J Heinz CompanyForm 10-K filed June 17 2004Form 10-Q filed August 24 2004File No 1-03385

Dear Mr Winkleblack

We have reviewed your filings referred to above and have the following comments If you disagree we will consider your explanation as to why our comment is inapplicable or a revision is unnecessary Please be as detailed as necessary in your explanation In some of our comments we may ask you to provide us with supplemental information so we may better understand your disclosure After reviewing this information we may or may not raise additional comments

We have limited our review to the areas per our comments below Please understand that the purpose of our review process is to assist you in your compliance with the applicable disclosure requirements and to enhance the overall disclosure in your filings We look forward to working with you in these respects We welcome any questions you may have about our comments or on any other aspect of our review Feel free to call us at the telephone numbers listed at the end of this letter

Form 10-K for the year ended April 28 2004

Cover Page

1 Revise your filing to state the aggregate market value of the voting and non-voting common equity held by non-affiliates as of the last business day of your most recently completed second fiscal quarter rather than as of May 28 2004 Refer to the instructions for Form 10-K

Management`s Discussion and Analysis page 11

2 Supplementally support your inclusion of the measures noted below

adjusted gross profit margin adjusted operating income operating free cash flow net debt

Note that if a measure is determined to be a non-GAAP measure we expect you to either amend your filings to remove the measure or expand your current disclosure to fully comply with the requirements of Regulation S-K Item 10(e) You may also wish to refer to our Frequently Asked Questions (FAQ) which may be found at httpwwwsecgovdivisionscorpfinfaqsnongaapfaqhtm

3 Please expand your disclosure to explain how you calculate your measure roic

4 Expand your disclosures to explain what Stock Keeping Units are which you mention on page 12

5 We note your disclosure on page 13 that Del Monte transaction costs and costs to reduce overhead of the remaining business totaled $1646 million pretax and that Of that amount $61 million was included in costs of products sold This information appears to conflict with your disclosure at the bottom of page 14 where you state that gross profit was also impacted by Del Monte transaction related costs costs to reduce overhead of the remaining businesses of $61 million and losses on the exit of non-strategic businesses of $473 million The page 14 disclosure implies that Del Monte costs

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-04-031471-1001 Page 2 of 4

recorded to costs of products sold were in addition to the $61 million costs for remaining businesses whereas the disclosure on page 13 implies that $61 million total was recorded in costs of products sold for Del Monte and the remaining businesses Revise to clarify

6 We note your disclosure of marketing support expenses on page 15 Explain to us why you do not believe it is necessary to disclose the portion of expense recorded as a reduction of revenue In yourresponse quantify that amount for all periods presented Explain tous the differences among marketing support expenses which you disclose to be $244 billion in fiscal 2004 marketing expenses displayed in your Key Performance Measures chart which reflects costs equal to 35 of sales or about $3029 million and advertising expenses disclosed in Note 19 to your Financial Statements which reflect $3604 million in fiscal 2004

Critical Accounting Policies page 24

7 We note that you identify certain areas of accounting that are the most significant policies used that rely upon management`s judgment to measure your financial position and results of operations Please revise your disclosure as follows

Expand your discussion by area of accounting to identify the assumptions made methods used to develop those assumptions and the extent to which management judgment is required to formulate conclusions

Identify the extent to and frequency in which the assumptions and conclusions made are subject to changes Also identify the reasons why the assumptions are subject to change and the extent to which management does or does not have the ability to influence those changes

Identify specific uncertainties associated with the methods assumptions or levels of judgment utilized in estimating the amounts reported in your financial statements (or in determining that no accounting was required) where resolution is reasonably likely to impair the indicative value of your reported financial information or materially impact future results

Explain how the specific accounting estimates made by management impact your liquidity capital resources and results of operations

Where practicable quantify the effects noted above to the extent that they are considered to be reasonably likely and material Please refer to Section V of the Commission Guidance Regarding Management`s Discussion and Analysis of Financial Condition and Results of Operations (Release Nos 33-8350 34-48960 and FR-72) for further guidance

Financial Statements and Supplementary Data page 29

Consolidated Statements of Income page 31

8 Please tell us why your fiscal 2004 sale of a bakery business in northern Europe as well as your fiscal 2003 divestitures primarily the UK frozen pizza business and a North American fish and frozen vegetable business were not accounted for as discontinued operations Please address the criteria of FAS 144 paragraphs 41- 44 in your response

9 We note that you recorded certain costs relating to the Del Monte transaction in continuing operations in fiscal 2003 as disclosed on pages 9 13 and 14 Please explain to us why these costs are not reflected in discontinued operations

10 Please address each of following regarding your accounting for the Zimbabwe operations

Explain to us in detail the information you considered in reaching your decision to deconsolidate your Zimbabwe operations

Tell us the specific accounting literature upon which you relied to determine that it was appropriate to deconsolidate the Zimbabwe

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-04-031471-1001 Page 3 of 4

operations

Explain why the factors that resulted in your conclusion to deconsolidate the Zimbabwe operations did not also result in an impairment of the assets located in that country

Explain how these operations are now being accounted for and how you evaluate your investment in these operations for impairment

Statement of Shareholders` Equity page 34

11 Explain to us the nature of items characterized as Other items net for each period reported

Statements of Cash Flows page 36

12 Explain to us the nature of items characterized as Other items net in operating investing and financing activities for each period reported

Note 1 - Significant Accounting Policies page 37

Principles of consolidation page 37

13 Expand your consolidation accounting policy to specifically state the criteria that you use to determine whether or not an ownership interest in an entity is consolidated We expect that you will specifically address both voting equity ownership and control in your revised accounting policy footnote

Revenue Recognition page 38

14 Expand your revenue recognition policy disclosures to clarify when revenue is recognized relative to the physical transfer of the goods

Note 5 - Special Items page 42

15 Amend your disclosures to present for each major type of cost associated with each exit activity the reconciliation of beginning and ending liability balances for each period and the other disclosure requirements specified in each subpart of FAS 146 paragraph 20 or for those activities initiated before your adoption of FAS 146 the disclosure requirements of EITF 94-03

Note 19 - Advertising Costs page 63

16 Expand your disclosures to clarify the amount of advertising costs recorded to expense versus costs recorded as a reduction to revenue

Closing Comments

Please respond to this comment within 10 business days or tell us when you will provide us with a response In your correspondence please provide any requested supplemental information Please file your correspondence on EDGAR Please understand that we may have additional comments after reviewing your response to our comment

If you have any questions regarding these comments you may contact Sandy Eisen at (202) 942-1805 or in her absence Jill Davis at (202) 942-1996 If you have any additional questions you may contact the undersigned at (202) 942-1870

Sincerely

H Roger SchwallAssistant Director

cc S Eisen J Davis

H J Heinz CompanySeptember 30 2004

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-04-031471-1001 Page 4 of 4

Page 1

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON DC 20549-0405

DIVISION OF CORPORATION FINANCE

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

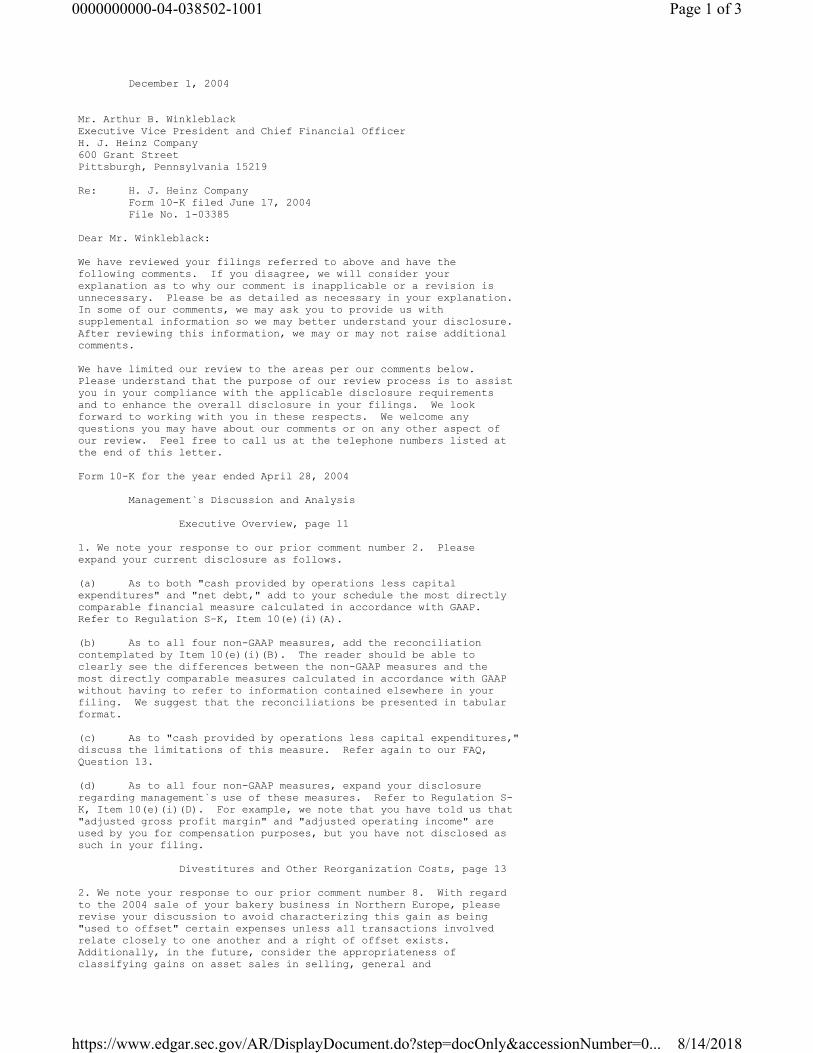

0000000000-04-038502-1001 Page 1 of 3

December 1 2004

Mr Arthur B Winkleblack Executive Vice President and Chief Financial Officer H J Heinz Company600 Grant Street Pittsburgh Pennsylvania 15219

Re H J Heinz CompanyForm 10-K filed June 17 2004File No 1-03385

Dear Mr Winkleblack

We have reviewed your filings referred to above and have the following comments If you disagree we will consider your explanation as to why our comment is inapplicable or a revision is unnecessary Please be as detailed as necessary in your explanation In some of our comments we may ask you to provide us with supplemental information so we may better understand your disclosure After reviewing this information we may or may not raise additional comments

We have limited our review to the areas per our comments below Please understand that the purpose of our review process is to assist you in your compliance with the applicable disclosure requirements and to enhance the overall disclosure in your filings We look forward to working with you in these respects We welcome any questions you may have about our comments or on any other aspect of our review Feel free to call us at the telephone numbers listed at the end of this letter

Form 10-K for the year ended April 28 2004

Management`s Discussion and Analysis

Executive Overview page 11

1 We note your response to our prior comment number 2 Please expand your current disclosure as follows

(a) As to both cash provided by operations less capital expenditures and net debt add to your schedule the most directly comparable financial measure calculated in accordance with GAAP Refer to Regulation S-K Item 10(e)(i)(A)

(b) As to all four non-GAAP measures add the reconciliation contemplated by Item 10(e)(i)(B) The reader should be able to clearly see the differences between the non-GAAP measures and the most directly comparable measures calculated in accordance with GAAP without having to refer to information contained elsewhere in your filing We suggest that the reconciliations be presented in tabular format

(c) As to cash provided by operations less capital expenditures discuss the limitations of this measure Refer again to our FAQ Question 13

(d) As to all four non-GAAP measures expand your disclosure regarding management`s use of these measures Refer to Regulation S- K Item 10(e)(i)(D) For example we note that you have told us that adjusted gross profit margin and adjusted operating income are used by you for compensation purposes but you have not disclosed as such in your filing

Divestitures and Other Reorganization Costs page 13

2 We note your response to our prior comment number 8 With regardto the 2004 sale of your bakery business in Northern Europe please revise your discussion to avoid characterizing this gain as being used to offset certain expenses unless all transactions involved relate closely to one another and a right of offset exists Additionally in the future consider the appropriateness of classifying gains on asset sales in selling general and

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-04-038502-1001 Page 2 of 3

administrative expense

Other

3 We note your response to our prior comment 6 With regard to your marketing support expenses please provide to us your draft disclosure in response to our prior comment 6 That is provide your draft discussion of the impact of fiscal 2004 and 2003 marketing support expense on revenues and selling general and administrative expenses that you intend to include in your Management`s Discussion and Analysis of your fiscal 2005 Form 10-K Note also that we would expect that such disclosure will be made on a quarterly basis

Financial Statements

Consolidated Statements of Income page 31

4 We note your response to our prior comment 10 concerning your operations in Zimbabwe (Olivine) With regard to the Olivine assets please provide to us your comprehensive assessment of impairment Be certain to include in your discussions the following issues

(a) An explanation of how you are able to assess that fair value exceeds your cost investment when you are unable to repatriate earnings outside of Zimbabwe In this regard explain in detail why you believe that any decline in your cost investment is temporary

(b) An explanation of how you are able to assess impairment when the currency exchange rate cannot be determined In this regard demonstrate how you are able to assess fair value based on cash flows in local currency relative to your USD $110 million investment balance

(c) A description of your assessment of the likelihood that the government may seize your share of the Olivine assets

(d) A full description of any agreements that you have entered into with the Zimbabwe government that may be relevant to these issues or other assurances that you have received with regard to the anticipated future of the Olivine assets and operations

Statements of Cash Flows page 36

5 We note your response to our prior comment number 12 With regardto your investing activities it is unclear whether the activities that you describe in your response as the change in our investments involved cash receipts or expenditures If non-cash changes were presented in this section we would expect this misclassification to be corrected on a retroactive basis in future filings

Note 1 - Significant Accounting Policies

Principles of Consolidation

6 We note your response to our prior comment numbers 10 and 13 Expand your footnotes to disclosure that the Zimbabwe subsidiary is accounted for using the cost method and why or tell us why you do not believe such disclosure is required

Closing Comments

Please respond to this comment within 10 business days or tell us when you will provide us with a response In your correspondence please provide any requested supplemental information Please file your correspondence on EDGAR Please understand that we may have additional comments after reviewing your response to our comment

If you have any questions regarding these comments you may contact Sandy Eisen at (202) 942-1805 or in her absence Jill Davis at (202) 942-1996 If you have any additional questions you may contact the undersigned at (202) 942-1870

Sincerely

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-04-038502-1001 Page 3 of 3

H Roger SchwallAssistant Director

cc S Eisen J Davis

H J Heinz CompanyDecember 1 2004Page 1

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON DC 20549-0405

DIVISION OF CORPORATION FINANCE

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-05-003973-1001 Page 1 of 2

January 19 2005

Mr Arthur B Winkleblack Executive Vice President and Chief Financial Officer H J Heinz Company600 Grant Street Pittsburgh Pennsylvania 15219

Re H J Heinz CompanyForm 10-K filed June 17 2004File No 1-03385

Dear Mr Winkleblack

We have reviewed your filings referred to above and have the following comments If you disagree we will consider your explanation as to why our comment is inapplicable or a revision is unnecessary Please be as detailed as necessary in your explanationIn some of our comments we may ask you to provide us with supplemental information so we may better understand your disclosure After reviewing this information we may or may not raise additional comments

We have limited our review to the areas per our comments below Please understand that the purpose of our review process is to assist you in your compliance with the applicable disclosure requirements and to enhance the overall disclosure in your filings We look forward to working with you in these respects We welcome any questions you may have about our comments or on any other aspect of our review Feel free to call us at the telephone numbers listed at the end of this letter

Form 10-K for the year ended April 28 2004

Management`s Discussion and Analysis

Executive Overview page 11

1 We have reviewed your response to prior comment number 1(c) and your proposed disclosure Please expand this disclosure to explainthat this measure does not provide insight in the entire scope of the historical cash inflows or outflows of your operations that are captured in the other cash flow measures reported in the statement of cash flows Expand your disclosure to also report the other cash flow measures to provide a more balanced presentation Refer to FRC 20203

Liquidity and Financial Position

2 We have reviewed your response to prior comment number 4 Please explain why you use an undiscounted cash flow calculation as the basis to determine the fair value of your cost method investment in Zimbabwe for your impairment test Refer to paragraph 6(a) of APBO NO 18 and paragraph 5 of SFAS 144

3 Additionally expand disclosures regarding your investment in the Olivine operations in Zimbabwe to include a discussion in this

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-05-003973-1001 Page 2 of 2

section concerning your inability to receive cash dividends

Closing Comments

Please respond to this comment within 10 business days or tell us when you will provide us with a response In your correspondenceplease provide any requested supplemental information Please file your correspondence on EDGAR Please understand that we may have additional comments after reviewing your response to our comment

If you have any questions regarding these comments you may contact Sandy Eisen at (202) 942-1805 or in her absence Jill Davis at (202) 942-1996 If you have any additional questions you may contact the undersigned at (202) 942-1870

Sincerely

H Roger SchwallAssistant Director

cc S Eisen J Davis

H J Heinz CompanyJanuary 26 2005Page 2

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON DC 20549-0405

DIVISION OF CORPORATION FINANCE

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-05-007339-1001 Page 1 of 1

February 14 2005

Mr Arthur B Winkleblack Executive Vice President and Chief Financial Officer H J Heinz Company600 Grant Street Pittsburgh Pennsylvania 15219

Re H J Heinz CompanyForm 10-K filed June 17 2004File No 1-03385

Dear Mr Winkleblack

We have completed our review of your Form 10-K and related filings and do not at this time have any further comments

Sincerely

H Roger SchwallAssistant Director

cc S Eisen J Davis

H J Heinz CompanyFebruary 14 2005Page 2

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON DC 20549-0405

DIVISION OF CORPORATION FINANCE

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-06-004520-1 Page 1 of 3

January 26 2006

Mr Arthur B Winkleblack Executive Vice President and Chief Financial Officer H J Heinz Company600 Grant Street Pittsburgh Pennsylvania 15219

Re H J Heinz CompanyForm 10-K for Fiscal Year Ended April 27 2005

Filed June 17 2005File No 1-03385

Dear Mr Winkleblack

We have reviewed your filing and have the following comments We have limited our review of your filing to those issues we have addressed in our comments Where indicated we think you should revise your document in response to these comments If youdisagreewe will consider your explanation as to why our comment is inapplicable or a revision is unnecessary Please be as detailed as necessary in your explanation In some of our comments we may ask you to provide us with information so we may better understand yourdisclosure After reviewing this information we may raise additional comments

Please understand that the purpose of our review process is to assist you in your compliance with the applicable disclosure requirements and to enhance the overall disclosure in your filing We look forward to working with you in these respects We welcome any questions you may have about our comments or any other aspect of our review Feel free to call us at the telephone numbers listed at the end of this letter

Form 10-K for the Fiscal Year Ended April 27 2005

Management`s Discussion and Analysis of Financial Condition and Results of Operations

Fiscal Years Ended April 27 2005 and April 28 2004 page 13

1 We note the decline in your effective tax rate for the three yearspresented and the impact of this trend on your income from continuingoperations and related earnings per share Describe if you reasonably expect this known trend to continue and if so how it will impact income from continuing operations and any known events that will cause a material change in this relationship as requiredby Regulation S-K Item 303(a)(3)(ii)

Liquidity and Financial Position page 19

2 You have discussed a $125 million tax pre-payment as a reason for

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-06-004520-1 Page 2 of 3

reduced cash flow from operations On page 49 in Note 6 of your financial statements you disclose that you incurred a $1249 million foreign liability that was settled in the third quarter of 2005 Tell us in greater detail the nature of the item and how it has impacted and will impact your financial statements Revise yourdiscussion and footnote as appropriate to consistently describe this item and its impact on your financial position and results of operations

Financial Statements and Supplementary Data

Consolidated Statements of Cash Flows page 38

3 We note your presentation of the effect of discontinued operations Statement of Financial Accounting Standards (SFAS) Number 95 requires all cash flows to be reported as either an operating investing or financing activity SFAS 95 does not supportaggregating operating investing and financing cash flows from discontinued operations into a single line item Revise your statements of cash flows accordingly

Note 7 - Debt page 49

4 We note your new $20 billion credit agreement which supports yourcommercial paper borrowings and remarketable securities File this agreement as an exhibit or incorporate such document by reference as required by Regulation S-K Item 601(a) and (b)(10)

Note 7 - Debt page 50

5 You have disclosed that SFAS No 150 applies to your mandatorilyredeemable preferred shares Revise your disclosure to provide all the disclosures required under SFAS No 150 paragraphs 26-28 or tell us why such disclosures are not required

Closing Comments

As appropriate please amend your filing and respond to these comments within 10 business days or tell us when you will provide us with a response You may wish to provide us with marked copies of the amendment to expedite our review Please furnish a cover letter with your amendment that keys your responses to our comments and provides any requested information Detailed cover letters greatlyfacilitate our review Please understand that we may have additional comments after reviewing your amendment and responses to our comments

We urge all persons who are responsible for the accuracy and adequacy of the disclosure in the filing to be certain that the filing includes all information required under the Securities Exchange Act of 1934 and that they have provided all information investors require for an informed investment decision Since the company and its management are in possession of all facts relating to a company`s disclosure they are responsible for the accuracy and adequacy of the disclosures they have made

In connection with responding to our comments please providein writing a statement from the company acknowledging that

the company is responsible for the adequacy and accuracy of the

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

0000000000-06-004520-1 Page 3 of 3

disclosure in the filing

staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing and

the company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States

In addition please be advised that the Division of Enforcement has access to all information you provide to the staff of the Division of Corporation Finance in our review of your filing or in response to our comments on your filing

You may contact Gary Newberry at (202) 551-3761 if you have questions regarding comments on the financial statements and related matters Please contact me at (202) 551- 3684 with any other questions

Sincerely

April SiffordBranch Chief

Mr Arthur B Winkleblack H J Heinz CompanyJanuary 26 2006page 1

UNITED STATES SECURITIES AND EXCHANGE COMMISSION 100 F Street NEWASHINGTON DC 20549-7010

DIVISION OF CORPORATION FINANCE MAIL STOP 7010

httpswwwedgarsecgovARDisplayDocumentdostep=docOnlyampaccessionNumber=0 8142018

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

100 F Street NE WASHINGTON DC 20549-7010

DIVISION OF CORPORATION FINANCE MAIL STOP 7010

February 15 2006

Mr Arthur B Winkleblack Executive Vice President and Chief Financial Officer H J Heinz Company 600 Grant Street Pittsburgh Pennsylvania 15219

Re H J Heinz Company Form 10-K for Fiscal Year Ended April 27 2005 Filed June 17 2005 File No 1-03385

Dear Mr Winkleblack

We have completed our review of your Form 10-K and related filings and do not at this time have any further comments

Sincerely

April Sifford Branch Chief

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON DC 20549-3628

DIVISION OF CORPORATION FINANCE

May 30 2006

Via US Mail

Mr Nelson Peltz Mr Peter May Mr Ed Garden Trian Fund Management LP 280 Park Avenue 41st Floor New York NY 10017

Re HJ Heinz Company Soliciting Materials pursuant to Rule 14a-12 filed by Trian Partners GP

LP et al Filed May 23 2006 File No 1-03385

Dear Messrs Peltz May and Garden

We have reviewed your filing and have the following comments Where indicated we think you should revise your document in response to these comments If you disagree we will consider your explanation as to why our comment is inapplicable or a revision is unnecessary Please be as detailed as necessary in your explanation In some of our comments we may ask you to provide us with supplemental information so we may better understand your disclosure After reviewing this information we may or may not raise additional comments

Please understand that the purpose of our review process is to assist you in your compliance with the applicable disclosure requirements and to enhance the overall disclosure in your filing We look forward to working with you in these respects We welcome any questions you may have about our comments or on any other aspect of our review Feel free to call us at the telephone numbers listed at the end of this letter

Rule 14a-12 Soliciting Materials

1 On a supplemental basis support the quantified statements you make relating to the Companyrsquos financial performance including the following

Table 1 - Relative Shareholder Returns as well as the percentage of shareholder returns for The Hershey Company PepsiCo Inc and Wm Wrigley Jr Company

HJ Heinz Company May 30 2006 Page 2

Table 2 - Change in Financial Performance Since 1998 and Net Capital Investment (1999-2006)

Table 4 ndash Trian Action Plan Potential Incremental Impact to EPS Table 5 ndash SGampA as a Percentage of Net Revenue Since Fiscal 2000 as well as the

percentage of gross margins at Wm Wrigley Jr Company Kellogg Company and General Mills Inc

Table 6 ndash Heinz Operating Efficiency Metrics Relative to Peers Reference to 13 and 14 of average spend on deals and allowances by Heinzrsquos

peers on page 6 Reference to 6 of spending on true advertising at ldquocomparable food companiesrdquo

on page 7 Table 8 ndash Recent Performance in the European Segment Table 9 ndash AsiaPacific and lsquoRest of World Segmentsrsquo (ldquoROWrdquo) vs Other

Operating Segments at Heinz Table 10 ndash Comparison of Acquisition Divestiture Activity Since 1998 Table 11 ndash Potential Financial Impact of the Trian Grouprsquos Action Plan Table 12 ndash Implied Value Target Following Implementation of the Trian Grouprsquos

Action Plan Table 13 ndash Potential Incremental Impact of Revitalized Marketing Campaign and Appendix B

Where the support for your calculations appears in other documents such as the companyrsquos Form 10-Qs or 10-Ks provide copies of the relevant portions of the documents so that we can assess the context of the information upon which you rely Again mark the supporting documents provided to identify the specific information relied upon such as financial statement line items and mathematical computations

2 Please characterize consistently each statement or assertion of opinion or belief as such and ensure that a reasonable basis for each opinion or belief exists Also refrain from making any insupportable statements Support for opinions or beliefs should be self-evident disclosed in the proxy statement or provided to the staff on a supplemental basis with a view towards disclosure by submitting a Schedule 14A that has been annotated with support for each of the assertions made We cite the following examples of statements or assertions in the proxy statement that must be supported on a supplemental basis and where not already categorized as such must be stated as your belief

ldquohellipTrianrsquos Pincipals have successfully helped management teams significantly reduce costs and increase value by bringing fresh perspectives and a more entrepreneurial approach to their businessesrdquo on page 5 and

ldquoToday Weight Watchers has a market capitalization of $42 billion an enterprise value of $49 billion and has grown EBITDA more than three-fold since the salerdquo on page 11

Where the bases are other documents such as prior proxy statements Forms 10-K and

HJ Heinz Company May 30 2006 Page 3

10-Q annual reports analystsrsquo reports and newspaper articles provide either complete copies of the documents or sufficient pages of information so that we can assess the context of the information upon which you rely Mark the supporting documents provided to identify the specific information relied upon such as quoted statements financial statement line items press releases and mathematical computations and identify the sources of all data utilized

As appropriate please amend your filing and respond to these comments within 10 business days or tell us when you will provide us with a response You may wish to provide us with marked copies of the amendment to expedite our review Please furnish a cover letter with your amendment that keys your responses to our comments and provides any requested supplemental information Detailed cover letters greatly facilitate our review Please understand that we may have additional comments after reviewing your amendment and responses to our comments

In connection with responding to our comments please provide in writing a statement acknowledging that

the filing person is responsible for the adequacy and accuracy of the disclosure in the filing

staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing and

the filing person may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States

In addition please be advised that the Division of Enforcement has access to all information you provide to the staff of the Division of Corporation Finance in our review of your filing or in response to our comments on your filing

We urge all persons who are responsible for the accuracy and adequacy of the disclosure in the filing reviewed by the staff to be certain that they have provided all information investors require for an informed decision Since the filing persons are in possession of all facts relating to a companyrsquos disclosure they are responsible for the accuracy and adequacy of the disclosures they have made

You may contact me at (202) 551-3264 with any questions You may also reach me via facsimile at (202) 772-9203

Sincerely

Mara L Ransom

HJ Heinz Company May 30 2006 Page 4

Special Counsel Office of Mergers and Acquisitions

cc Marc Weingarten Esq Schulte Roth amp Zabel LLP

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON DC 20549-3628

DIVISION OF CORPORATION FINANCE

June 23 2006

Via facsimile at (412) 456-6059 and US Mail

Edward J McMenamin Senior Vice President ndash Finance and Corporate Controller HJ Heinz Company 600 Grant Street Pittsburgh Pennsylvania 15219

Re HJ Heinz Company Schedule 14A Filed June 15 2006 File No 1-03385

Dear Mr McMenamin

We have reviewed your filing and have the following comments Where indicated we think you should revise your document in response to these comments If you disagree we will consider your explanation as to why our comment is inapplicable or a revision is unnecessary Please be as detailed as necessary in your explanation In some of our comments we may ask you to provide us with supplemental information so we may better understand your disclosure After reviewing this information we may or may not raise additional comments

Please understand that the purpose of our review process is to assist you in your compliance with the applicable disclosure requirements and to enhance the overall disclosure in your filing We look forward to working with you in these respects We welcome any questions you may have about our comments or on any other aspect of our review Feel free to call us at the telephone numbers listed at the end of this letter

Schedule 14A

1 We note that you filed your proxy statement under the EDGAR header tag of ldquoPRE 14Ardquo when in fact it would appear that it should have been filed under ldquoPREC14Ardquo Please keep this in mind for future reference

2 Please characterize consistently each statement or assertion of opinion or belief as such and ensure that a reasonable basis for each opinion or belief exists Also refrain from making any insupportable statements Support for opinions or beliefs should be self-evident disclosed in the proxy statement or provided to the staff on a supplemental basis with a view towards disclosure by submitting a Schedule 14A that has been annotated with support for each of the assertions made We cite the following examples of

HJ Heinz Company June 23 2006 Page 2

statements or assertions in the proxy statement that must be supported on a supplemental basis and where not already categorized as such must be stated as your belief

References to the ldquoself-interestedrdquo and ldquodivisiverdquo voices in your Letter to Shareholders

ldquohellipindependent stock analysts have characterized his plans as lsquooverly aggressiversquo and lsquonot achievablersquo and his corporate governance record is poorrdquo in your Letter to Shareholders

ldquo[Peltz] would cripple Heinz and his representatives would represent themselves not [shareholders]rdquo after the Notice of Annual Meeting of Shareholders and in the forepart of the proxy statement

The reference to ldquounrealisticrdquo in relation to the cuts suggested by Peltz to SGampA and other expenses and your indication that your ldquoSGampA is and has for a number of years been below the average for peer companies in the industryrdquo in the forepart of the proxy statement

Reference to ldquohidden agendardquo in the soliciting materials filed June 15 2006 Two of Peltzrsquos nominees ldquohave a public and well-documented record of

shareholder lawsuitsrdquo in the soliciting materials filed June 22 2006

Where the bases are other documents such as prior proxy statements Forms 10-K and 10-Q annual reports analystsrsquo reports and newspaper articles provide either complete copies of the documents or sufficient pages of information so that we can assess the context of the information upon which you rely Mark the supporting documents provided to identify the specific information relied upon such as quoted statements financial statement line items press releases and mathematical computations and identify the sources of all data utilized

Letter to Shareholders

3 You indicate that the Board is ldquocomprised of strong independent leadershelliprdquo Here and elsewhere in your proxy materials clarify what you mean by your reference to ldquoindependentrdquo Is this your definition or is this the definition as applied by the listing standards of the NYSE If this constitutes your definition briefly define it for readers

This yearrsquos vote at the Annual Meeting is extremely importanthellip

4 We note your indication that you received a notice of intent from Trian Partners on March 2 2006 Please tell us whether you have received timely notice of this or any other matter for consideration by shareholders under the companyrsquos governing instruments or the applicable state law We note your indication that you ldquocontinue to evaluate this notice under the Companyrsquos By-Law requirements for shareholders wishing to make nominations of directors at this yearrsquos Annual Meetingrdquo but it is not clear whether you are referring specifically to the notice provided by Trian or whether you are more generally evaluating this provision

HJ Heinz Company June 23 2006 Page 3

5 You indicate that the ldquoPeltzTrian plan lacks specificity lacks a time frame for implementation and associated restructuring costs ignores industry dynamics and inflationary headwinds is based on unsupported assumptions and does not offer new insightsrdquo As requested in the comment above please characterize this statement as your belief and provide support for each belief Consider whether it might be more helpful for readers for you to provide support for this statement in your soliciting materials

Peltz Nominees do not Satisfy Heinz Director Independence Standards

6 Please provide us with copies of the ISS reports regarding Triarc Companies Inc and you as well as the Corporate Library Report to which you make reference

Employment Contracts and Termination of Employment and Change-in-Control Agreements page 26

7 We note your indication towards the end of this discussion that the election of any PeltzTrian nominees would count toward a Change in Control Please revise to clarify that even if all of the PeltzTrian nominees were elected this would not trigger a Change in Control at this point

Rule 14a-12 Soliciting Materials dated June 15 and 22 2006

8 On a supplemental basis support the statements you make relating to the Companyrsquos Superior Value amp Growth Plan including your quantified statements as to 1) EPS Growth of 10 in FY07 2) Sales growth of 3-4 in FY07 3) and Operating income growth of more than 8 in FY07 Please also provide support for the statement you make as to TSR and your delivery of 189 since December 20 2002 Where the support for your calculations appears in other documents such as the companyrsquos Form 10-Qs or 10-Ks provide copies of the relevant portions of the documents so that we can assess the context of the information upon which you rely Again mark the supporting documents provided to identify the specific information relied upon such as financial statement line items and mathematical computations

Rule 14a-12 Soliciting Materials dated June 19 2006

9 You indicate that ldquohellippeople around the world have different value systems Particularly people yoursquore dealing with in a proxy contest And those value systems do not mirror the value systems that we hold near and dear in this companyrdquo Please provide sufficient factual foundation to support this statement Also in any future materials you must avoid statements that directly or indirectly impugn the character integrity or personal reputation or make charges of illegal or immoral conduct without factual foundation In this regard note that the factual foundation for such assertions must be reasonable Refer to Rule 14a-9

HJ Heinz Company June 23 2006 Page 4

As appropriate please amend your filing and respond to these comments within 10 business days or tell us when you will provide us with a response You may wish to provide us with marked copies of the amendment to expedite our review Please furnish a cover letter with your amendment that keys your responses to our comments and provides any requested supplemental information Detailed cover letters greatly facilitate our review Please understand that we may have additional comments after reviewing your amendment and responses to our comments

In connection with responding to our comments please provide in writing a statement acknowledging that

the filing person is responsible for the adequacy and accuracy of the disclosure in the filing

staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing and

the filing person may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States

In addition please be advised that the Division of Enforcement has access to all information you provide to the staff of the Division of Corporation Finance in our review of your filing or in response to our comments on your filing

We urge all persons who are responsible for the accuracy and adequacy of the disclosure in the filing reviewed by the staff to be certain that they have provided all information investors require for an informed decision Since the filing persons are in possession of all facts relating to a companyrsquos disclosure they are responsible for the accuracy and adequacy of the disclosures they have made

You may contact me at (202) 551-3264 with any questions You may also reach me via facsimile at (202) 772-9203

Sincerely

Mara L Ransom Special Counsel Office of Mergers and Acquisitions

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON DC 20549-3628

DIVISION OF CORPORATION FINANCE

June 30 2006

Via US Mail

Mr Nelson Peltz Mr Peter W May Mr Edward P Garden Trian Fund Management LP 280 Park Avenue 41st Floor New York NY 10017

Re HJ Heinz Company Schedule 14A filed by Trian Partners GP LP et al Filed June 22 2006 File No 1-03385

Dear Messrs Peltz May and Garden

We have reviewed your filing and have the following comments Where indicated we think you should revise your document in response to these comments If you disagree we will consider your explanation as to why our comment is inapplicable or a revision is unnecessary Please be as detailed as necessary in your explanation In some of our comments we may ask you to provide us with supplemental information so we may better understand your disclosure After reviewing this information we may or may not raise additional comments

Please understand that the purpose of our review process is to assist you in your compliance with the applicable disclosure requirements and to enhance the overall disclosure in your filing We look forward to working with you in these respects We welcome any questions you may have about our comments or on any other aspect of our review Feel free to call us at the telephone numbers listed at the end of this letter

Schedule 14A

Letter to Shareholders