Embed Size (px)

Citation preview

FULL YEAR RESULTS 2014March 17, 2015

AGENDA

2

RECAP: STRATEGIC ANNOUNCEMENT JANUARY 2015

FULL YEAR 2014 ― FINANCIAL REVIEWTRADING UPDATE

STRATEGY FOCUSED ON GLOBAL AND GROWING TRAVEL SERVICES

NEW MID-TERM TARGETS 2017

ADDITIONAL INFORMATION

2

3

1

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

4

RECAP: STRATEGIC ANNOUNCEMENT JANUARY 2015

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 20154

FOCUS ON CORE DIVISIONS FOLLOWINGCOMPREHENSIVE STRATEGY REVIEW

PORTFOLIO CHANGE OVER TIME

► Focus on core business as a service provider tothe global travel industry and to governments

► Focus on growing three Divisions:

− Global Travel Distribution (previously FIT)− Global Travel Services (previously Group

Travel and DM Specialists)− VFS Global

► Intention to find new owners for all touroperating activities: Kuoni Switzerland, UK,Benelux, Hong Kong, India andScandinavia/Finland

OutboundEurope & Asia

Outbound Nordic

DM Specialists

Group Travel

FIT

VFS5 508

3 894

Turnover (CHF milion)

Of whichTourOperating

75% 39%

2009 2014

CoreDivisions

Exit ofTour

OperatingActivities

5

NEW STRUCTURE REFLECTS FOCUS ON THREEDIVISIONS WITH LEADING GLOBAL POSITIONS

OLD STRUCTURE NEW STRUCTURE

VFS

Glo

bal

Tour

Ope

rati

ngD

esti

nati

on &

Acc

omm

odat

ion

Man

agem

ent

Global TravelDistribution

(GTD)

► Leading and highly experienced B2B providerof accommodation and land components

Global TravelServices

(GTS)

► Long-standing and leading provider of grouptravel and destination management services

VFS Global ► Pioneer and global leader as visa serviceprovider

Outbound ► Exit of tour operating activities

Fully IndependentTraveller (FIT)

Group Travel

VFS Global

OutboundEurope/Asia

DestinationManagement

Specialists

OutboundNordic

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

56%36%

8%

VFS Global

GlobalTravelDistribution(GTD)

GlobalTravelServices(GTS)

Total: CHF 3 436 mFTEs: 8 081

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 20156

2 OUT OF 3 DIVISIONS POSTED POSITIVEORGANIC GROWTH, 43% APAC AS A SOURCE

► Three divisions concentrated on markets andservices with attractive long-term growthpotential and in which Kuoni has globally leadingpositions

► Unique set-up with strong focus on Asia willenable Kuoni to expand positions further byleveraging scale and exploring cross-sellingopportunities

► Launch of strategic initiatives to accelerategrowth and improve profitability across businesssegments

TURNOVER 2014(EXCLUDING OUTBOUND UNITS)

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 20157

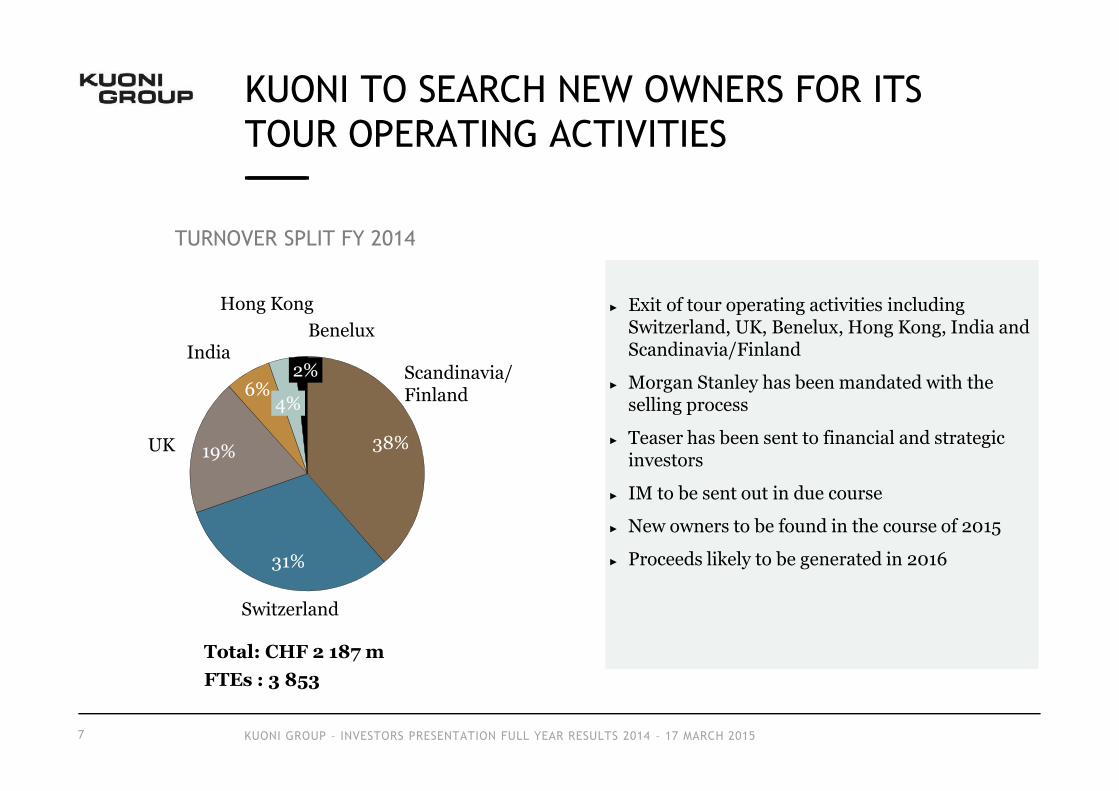

► Exit of tour operating activities includingSwitzerland, UK, Benelux, Hong Kong, India andScandinavia/Finland

► Morgan Stanley has been mandated with theselling process

► Teaser has been sent to financial and strategicinvestors

► IM to be sent out in due course

► New owners to be found in the course of 2015

► Proceeds likely to be generated in 2016

38%

31%

19%

6%4%

2%

Switzerland

UK

India

Hong KongBenelux

Scandinavia/Finland

TURNOVER SPLIT FY 2014

Total: CHF 2 187 mFTEs : 3 853

KUONI TO SEARCH NEW OWNERS FOR ITSTOUR OPERATING ACTIVITIES

FULL YEAR 2014 ‒ FINANCIAL REVIEW

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 20159

ORGANIC TURNOVER GROWTH OF 2.8%IN THE FUTURE CORE BUSINESS (FX IMPACT ‒1.7%)

TURNOVER

(CHF million) FY14 FY13 Δ %nominal

Δ %organic

Global Travel Distribution (previously FIT) 1 933 1 802 +7.3 +8.8

Global Travel Services 1 238 1 360 -9.0 -7.3

Group Travel Experts 873 943 -7.4 -6.5

Destination Management Specialists 365 417 -12.5 -8.9

VFS Global 271 244 +11.1 +13.9

Subtotal 3 436 3 406 +0.9 +2.8

Outbound Units 2 187 2 396 -8.7 -4.5

Outbound Nordic 844 982 -14.1 -9.0

Outbound Europe/Asia 1 343 1 414 -5.0 -1.4

Kuoni Group 5 508 5 669 -2.8 -0.1

Futu

re c

ore

busi

ness

TURNOVER BASED ON OLD STRUCTURE

(CHF million) FY14 FY13 Δ %nominal

Δ %organic

Group Travel 873 943 -7.4 -6.5

FIT (Fully Independent Traveller) 1 933 1 802 +7.3 +8.8

Outbound Nordic 844 982 -14.1 -9.0

Outbound Europe/Asia 1 343 1 414 -5.0 -1.4

Destination Management Specialists 365 417 -12.5 -8.9

VFS Global 271 244 +11.1 +13.8

Less turnover between segments -121 -133

Kuoni Group 5 508 5 669 -2.8 -0.1

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201510

ORGANIC TURNOVER GROWTH OF ‒0.1%IN A CHALLENGING ENVIRONMENT

PROFIT & LOSS

(CHF million) FY14 FY13adjusted*) Δ % FY13

As reported

Turnover 5 508 5 669 -2.8 5 669

GOP Margin 18.6% 19.5% 19.5%

EBITAEBITA-Margin

122.22.2

150.12.6

-18.6 191.43.4

EBITEBIT-Margin

85.71.6

112.92.0

-24.1 154.22.7

Net result 67.4 36.7 +83.7 69.2

Diluted earnings per registered share ADiluted earnings per registered share B

3.4417.20

3.5517.77

Free cash flow 33.2 124.6 -73.4 124.6

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201511

NET RESULT IN LINE WITH PREVIOUS YEAR

*) excluding the effect of Swiss pension plan changes and a curtailment of CHF 41.3m in total

GROUP TRAVEL: MAINTAINS STRONG MARKET POSITIONIN A CHALLENGING ENVIRONMENT

12

(CHF million)FY14 FY13 ∆% Organic turnover decline by 6.5%

Lower demand in the important Japanesemarket persists (35% of top line)

Weak economy and currency continues

Increase of consumer tax

Smaller group sizes

China (over 20% of top line) slow start into2014 due to changes of travel law, picking uptowards the end of the year

Higher volumes from Taiwan, South Korea,India and Hong Kong

# of room nights fell by 3.0% to 3.1 million

excl Swisspension

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

Turnover 873 943 ‒7.4

GOP 145.9 165.6 ‒11.9

EBITA 16.9 23.2 ‒27.2

FTE (end of period) 1 618 1 633

Turnover 1 933 1 802 +7.3

GOP 220.6 224.1 ‒1.6

EBITA 63.2 73.0 ‒13.4

FTE (end of period) 1 414 1 366

FIT: ORGANIC GROWTH OF 8.8% ‒WELL ABOVE 13M ROOM NIGHTS SOLD

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201513

(CHF million)FY14 FY13 ∆% Room nights up by 7.2% to 13.6 million

Growth in Asia ex Japan as a source of +13%achieved

Double digit growth rates for Asia as adestination

More competitive margins fuelled growthstrategy

Investment in improved booking systems andnew applications/features as well as higherstaffing costs resulting from growth strategy

excl Swisspension

OUTBOUND NORDIC: EXCESS FLIGHT CAPACITYLOWERED PRICES AND MARGINS

14

(CHF million)FY14 FY13 ∆% Organic turnover decline of 9.0%

Challenging market environment

Excess flight capacity

Reduced demand due to geopolitical eventsand exceptional summer weather

Measures initiated:

Renegotiated agreements with Novair crew

Streamlined product/destination portfolio

Reduction of headcount

New managing director

75% of turnover sold direct (vs 73% in 2013)

excl Swisspension

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

Turnover 844 982 ‒14.1

GOP 125.9 188.1 ‒33.1

EBITA ‒ 7.6 37.8 ‒120.1

FTE (end of period) 782 867

Turnover remaining 1 343 1 355 ‒0.9

Turnover sold/closed n/a 59 n/a

GOP 273.5 272.0 +0.6

EBITA remaining 20.5 8.6 +138.4

EBITA sold/closed n/a ‒3.0 n/a

FTE (end of period) 3 071 2 928

OUTBOUND EUROPE/ASIA: SUBSTANTIALIMPROVEMENT OF OPERATING EARNINGS

15

(CHF million) FY14 FY13 ∆% Positive development of the Swiss, Indian andHong Kong units

Switzerland improved profitability to a doubledigit EBITA

India improved considerably its operatingperformance (low single digit vs high singledigit loss in 2013)

Hong Kong recorded a 32% improvement in itsoperating performance

UK suffered from the travel warning to Kenyaand Thailand, but still achieved higher EBIT inabsolute terms and also margin wise

excl Swisspension

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

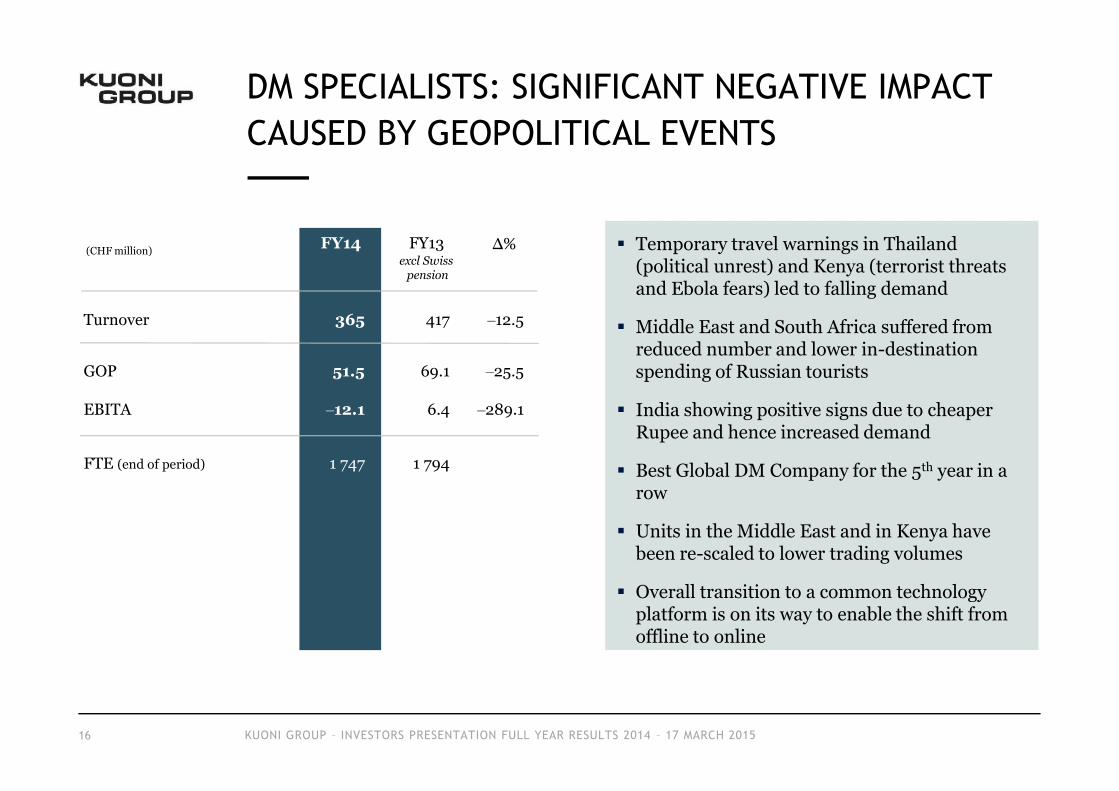

Turnover 365 417 ‒12.5

GOP 51.5 69.1 ‒25.5

EBITA ‒12.1 6.4 ‒289.1

FTE (end of period) 1 747 1 794

DM SPECIALISTS: SIGNIFICANT NEGATIVE IMPACTCAUSED BY GEOPOLITICAL EVENTS

16

(CHF million) FY14 FY13 ∆% Temporary travel warnings in Thailand(political unrest) and Kenya (terrorist threatsand Ebola fears) led to falling demand

Middle East and South Africa suffered fromreduced number and lower in-destinationspending of Russian tourists

India showing positive signs due to cheaperRupee and hence increased demand

Best Global DM Company for the 5th year in arow

Units in the Middle East and in Kenya havebeen re-scaled to lower trading volumes

Overall transition to a common technologyplatform is on its way to enable the shift fromoffline to online

excl Swisspension

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

Turnover 271 244 +11.1

GOP 207.7 178.3 +16.5

EBITA 52.5 40.2 +30.6- whereof JV ‒2.0 ‒2.7 +25.9

FTE (end of period) 3 209 2 752

VFS GLOBAL: ORGANIC GROWTH +13.9%

17

(CHF million)FY14 FY13 ∆% 18.2m # of applications processed – just a slight

increase vs 2013

Substantial drop in # of visas from Russia

Withdrawal from unprofitable contracts

Two new global contracts won in 2014 (Norwayand Slovenia)

Non-religious applications for the SaudiGovernment are being processed

850k # of applications in 54 centres in 26countries

First Front Office Services (FOS) went live in2014

In-country public citizen services

Launched in Asia, Africa and Europe

excl Swisspension

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

EBIT BRIDGE ‒ DECREASE DRIVEN MAINLY BYMARGIN DEVELOPMENT

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201518

41.3

18.9

53.2 41.8

EBIT 2014REPORTED

543EBIT 2013ADJUSTED

21

3.1

EBIT 2013REPORTED

16.7

1: Impact of exit of European tour operator activities in 20132: One-time positive effect from pension fund plan change and curtailment in Switzerland3: Impact of turnover development on EBIT4: Impact of gross profit margin development5: Impact of decrease in operating costs, including one-time positive effect from the sale of Geroldstrasse (CHF 10.1 million)

(CHF million)

10.1

154.2

85.7

116.0

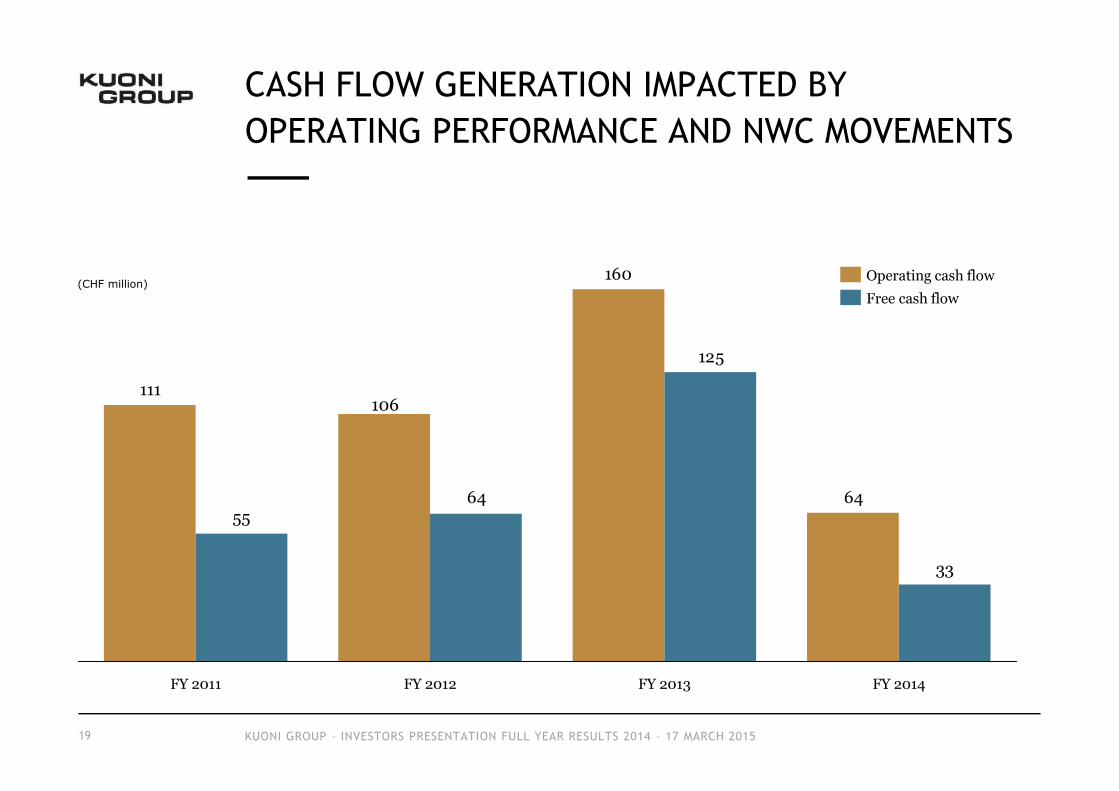

CASH FLOW GENERATION IMPACTED BYOPERATING PERFORMANCE AND NWC MOVEMENTS

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201519

(CHF million)

64

160

111

33

125

6455

FY 2012FY 2011 FY 2013 FY 2014

Operating cash flowFree cash flow

106

HEALTHY AND STABLE EQUITY RATIOAND SOUND BALANCE SHEET STRUCTURE

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201520

(CHF million)

738 699 779 779

1'748 1'703 1'614 1'640

32.2

32.6

29.129.7

0

500

1'000

1'500

2'000

2'500

024

681012

14161820

22242628

303234

31 Dec 2014

2’419

31 Dec 2013

2’393

31 Dec 2012

2’402

31 Dec 2011

2’486

EquityLiabilityEquity ratio

in %

LIQUIDITY AND DEBT POSITIONAS PER 31.12.2014

21

200

51

-274

99

350

Net debt positionAdvance paymentsby customers

-373

Net Liquid FundsOther debtBond nominalLiquid funds

(CHF million)

vs. 31.12.2013CHF 141m

vs. 31.12.2013CHF -241m

SENIOR CREDIT FACILITY USED AT 31.12.2014 CHF 15M

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

FX VOLATILITY COULD HAVE A SIGNIFICANTTRANSLATION IMPACT ON 2015

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201522

TURNOVER CURRENCY MIX FOR TRANSLATION FOR THE NEW CORE AS OF 2015

Due to the currency mix of the subsidiaries’ operating activities, it is expected that the SNB’sdecision to remove the CHF peg will have considerable, negative impact on the Swiss francs-denominated consolidated income statement.

52%

18%

8%

8%

3%4%

4%

3%

EURUSD

Other

AEDINR

AUD

GBPCHF

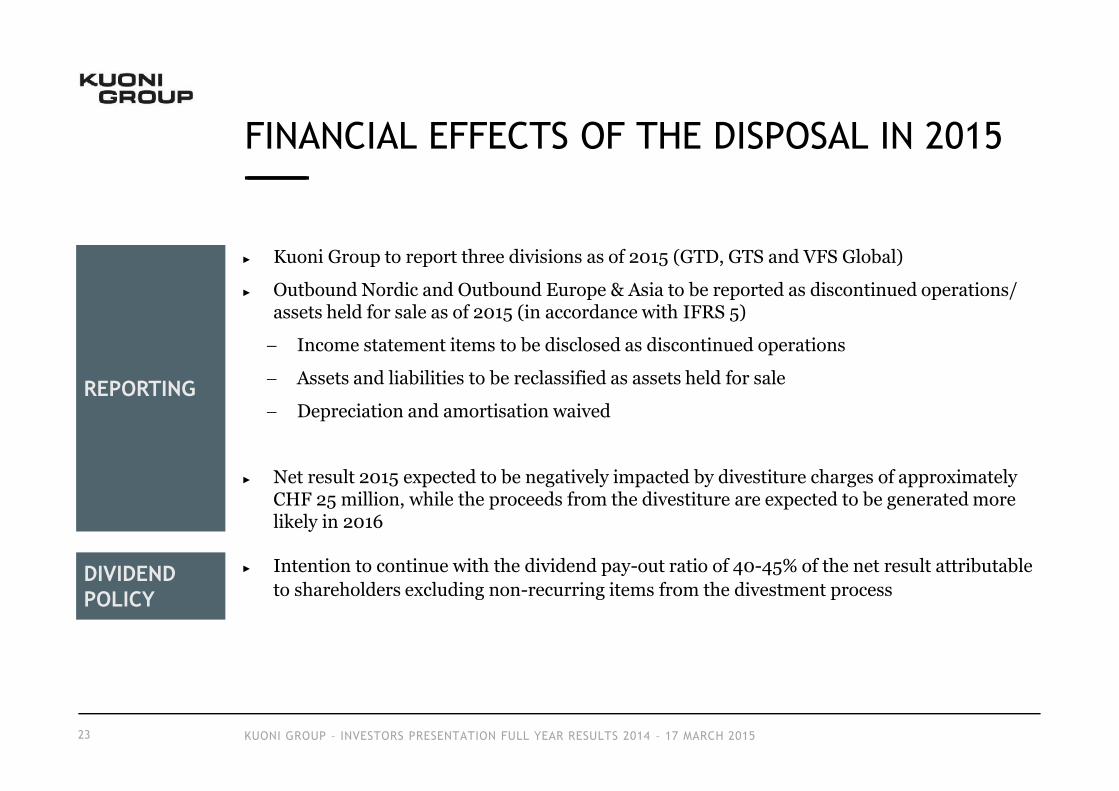

FINANCIAL EFFECTS OF THE DISPOSAL IN 2015

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201523

► Intention to continue with the dividend pay-out ratio of 40-45% of the net result attributableto shareholders excluding non-recurring items from the divestment process

► Kuoni Group to report three divisions as of 2015 (GTD, GTS and VFS Global)

► Outbound Nordic and Outbound Europe & Asia to be reported as discontinued operations/assets held for sale as of 2015 (in accordance with IFRS 5)

Income statement items to be disclosed as discontinued operations

Assets and liabilities to be reclassified as assets held for sale

Depreciation and amortisation waived

► Net result 2015 expected to be negatively impacted by divestiture charges of approximatelyCHF 25 million, while the proceeds from the divestiture are expected to be generated morelikely in 2016

REPORTING

DIVIDENDPOLICY

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201524

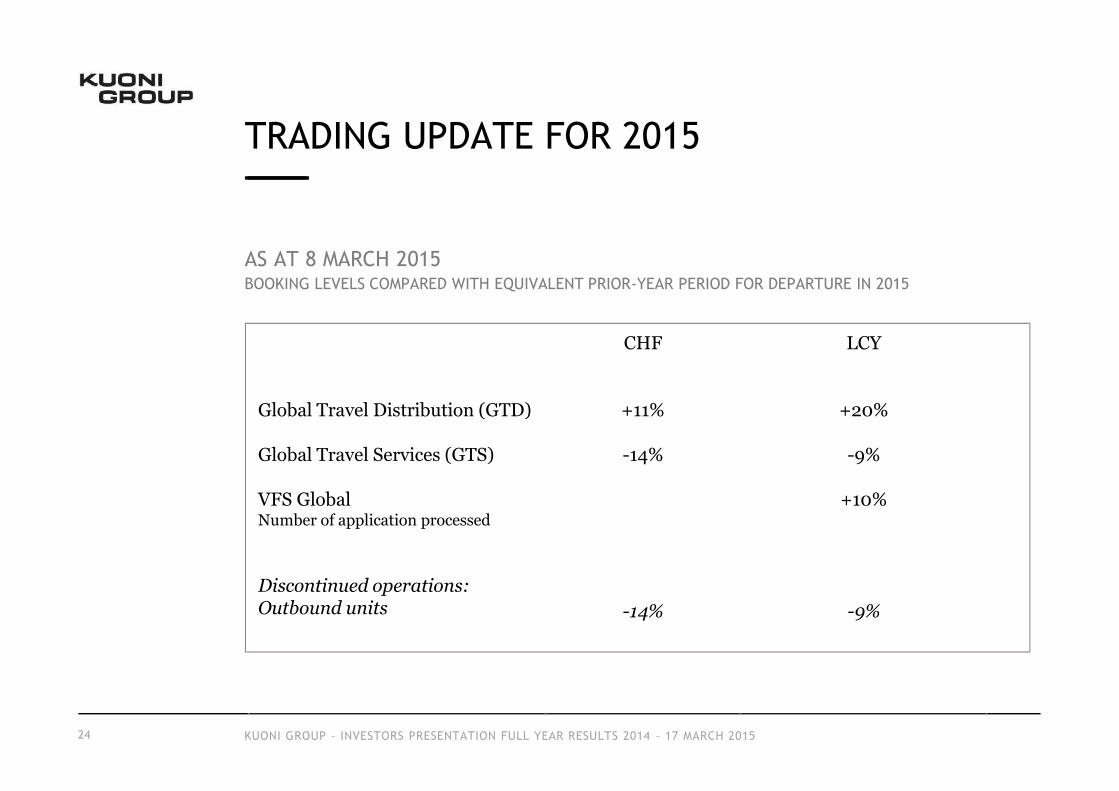

TRADING UPDATE FOR 2015

Global Travel Distribution (GTD)

Global Travel Services (GTS)

VFS GlobalNumber of application processed

Discontinued operations:Outbound units

CHF

+11%

-14%

-14%

LCY

+20%

-9%

+10%

-9%

AS AT 8 MARCH 2015BOOKING LEVELS COMPARED WITH EQUIVALENT PRIOR-YEAR PERIOD FOR DEPARTURE IN 2015

STRATEGY FOCUSED ON GLOBAL AND GROWINGTRAVEL SERVICESNEW MID-TERM TARGETS 2017

THREE STRATEGIC INITIATIVES TO ACCELERATEGROWTH AND IMPROVE PROFITABILITY

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201526

EXPANDING FOOTPRINT INASIA, MIDDLE EAST AND

AFRICA

► Invest additional resources inAsia, the Middle East andAfrica by leveraging existingfootprint and expandingcapabilities across allsegments

FURTHERDIGITALISATION

► Enhance customer serviceand increase efficiency byimplementing new state-of-the-art technology platforms

► Develop new service offeringfor digital travellers

EXPANDSERVICE OFFERING

► Build on existing customerbase and global footprint

► Provide existing services to awider range of customersegments by realisingcross-selling potential

► Introduce new products andservices

27

EXPAND FOOTPRINT AND OFFERING, FURTHERDIGITALISATION WILL LEAD TO MORE GROWTH

Global Travel Distribution(GTD)

► Expand service and product offering to cater specific needs of Asian,Middle Eastern and African source markets

► Deploy innovative customer facing systems and implemente-commerce platform

► Enhance mobile features of existing applications► Increase number of beach destinations and third party products► Exploit new sales opportunities by introducing mobile travel assistant

VFS Global► Digital visa processing for interaction with governments► Expand into services adjacent to visa processing and new disciplines

such as front office services

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

Global Travel Services(GTS)

► Rollout new proprietary reservation systems► Increase sales activities with key accounts for smaller groups► Group travel online sales► Grow share of DM Services for non-Europe customer segments

Fost

er c

ross

-sel

ling

oppo

rtun

itie

s su

ch a

s de

stin

atio

nse

rvic

es o

r vi

sa s

ervi

ces

acro

ss d

ivis

ions

off

ice

serv

ices

AS A CONSEQUENCE OF NEW STRATEGYNEW FINANCIAL TARGETS 2017

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201528

FORECASTING HAS BECOME MORE CHALLENGING ON ACCOUNT OF THEUNCERTAINTIES REGARDING THE LEVEL OF THE SWISS CURRENCY

3.53.0

3.4 -14%

2017 Target2014 FXadjusted

2014 asreported

70

56

2014 FXadjusted

2014 asreported

-21%

2017 target

8110

2.5% 5% p.a.

Turnover growth per annum1)

above the global travel marketEBIT margin Free Cash Flow margin

3%

1.9%

3%

► Capex expected in line withdepreciations

► Tax rate estimated at ~25%

► NWC changes and non-cashitems expected neutral

Turn

over

in C

HF

bln

EBIT

in C

HF

mill

ion

1) >5% turnover growth on CHF 3.0bn baseline in 2014. Aspiration is to grow significantly faster than the global travel markets, which accordingto UNWTO will expand by 3.8% p.a.

Assumption: Tour operating entities can be divested by 2016 as planned

3.6% EBITA margin

ADDITIONAL INFORMATION

DestinationManagement

WELL POSITIONED WITHIN THE COMPLEX TRAVELDISTRIBUTION ECO-SYSTEM AND CLEAR FOCUS ON B2B

30

TRAVEL ECO-SYSTEM Kuoni Group

Supplier.com

Large international OTAs

TravelRetail

Metasearch

Smaller/regional OTAs

Visa ProcessingServices

Hotels

Transfers

Tours

Flights

Highlyfragmented

2014: >1bninternationalarrivals

Switches/GDS

Consolidators/Brokers

Grouptravel

Tour Operators

Changingbehaviours

Countlessdesires

SUPPLIERS CUSTOMERS

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

GTD(FIT Wholesaler)

31 KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

► Leading and highly experienced B2B wholesalerand provider of accommodation and landcomponents to tour operators and offline andonline travel agencies globally

► 7% share in the intermediated accommodationmarket with 38’000 room nights sold online perday

► 48’000 hotels in the database (online bookable,real-time pricing)

► ~43% of turnover generated in fast-growingAsia/Pacific, the Middle East and Africa markets

► Top source markets: UK, Australia, Spain

► Top destinations: USA, Italy, France

► Launch of a prototype mobile application fortravel agents

CHF million

TURNOVER

1 7031 802

1 933

2012 2013 2014

BUSINESS OVERVIEW

GLOBAL TRAVEL DISTRIBUTION (GTD)

32 KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

964 943 873

400 417365

1 364 1 3601 238

2012 2013 2014

Group Travel Experts DM Specialists

CHF million

TURNOVER1)

► Long-standing and leading provider of grouptravel and destination management services totour operators and travel agencies globally

► Sources and coordinates destination servicesincluding accommodation, transportation, toursand activities, venues and event management(MICE)2)

► #1 player in the growing Asian group travelmarket with 80% of turnover generated fromAsia/Pacific source markets

− ~50 000 leisure tours per year

− ~3.1 million room nights booked

− 25 sales offices

► Among top 3 destination managementcompanies in respective destinations

GLOBAL TRAVEL SERVICES (GTS)

BUSINESS OVERVIEW

1) Aggregated without turnover elimination between segments; 2) MICE=Meetings, Incentives, Conferences & Events

33 KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

205

244271

2012 2013 2014

CHF million

TURNOVER

► Pioneer and world’s leading visa servicesprovider for governments and public institutions

− ~18 million applications processed in 2014

− ~ 6million biometric data sets recorded in2014

− ~50% global market share

− ~70% turnover generated from travellersfrom Asia/Pacific

− 1 486 application centres in 120 countries for45 governments

► Differentiated market position with leadingtechnologies, infrastructure and capabilities

► Long-term customer relationships and contracts

► Introduction of the first Front Office Services(in-country public citizen services)

BUSINESS OVERVIEW

VFS GLOBAL

Group Travel DM Specialists

NEW CORE BUSINESS GENERATES 43% IN ASIAAND HAS EUROPE AS A MAIN DESTINATION

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201534

GEOGRAPHICAL SPREAD OF TURNOVER 2014 IN THE FUTURE CORE BUSINESS (IN %)

Europe

37%

MEA

9%

APAC43%

Americas

11%

58%

MEA

Europe

10%

APAC 18%

Americas

14%

New Group

CHF 3’436m CHF 1’933m

15%

Europe

43%

13%

MEA

APAC 29%

Americas

19%

Europe

MEA

51%

APAC10%

20%

Americas

Americas

81%

7%

Europe

12%

APAC

3%

MEA

93%

APAC

1%

Americas

3%

Europe

CHF 873m

GTS

GTS

VFSGTD

Americas 15%

Europe

69%

MEA

6%APAC10%

MEA37%

APAC

46%

Americas

17%

CHF 271m

Europe

15%

MEA

15%

APAC 67%

Americas3%

Europe

56%

MEA

12%APAC

14%

Americas

18%

CHF 365m

By s

ourc

e M

arke

tBy

des

tina

tion

FINANCIALS ON THE BUSINESS TO BEDISPOSED OFF IN MORE DETAILS

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201535

07 9

1 38

37

41 0

67 9

844

59661 25

39

402

7 23

982

UKSwitzerlandNordic Sold/closedentities

HongkongIndiaBenelux

0.02.9

-2.0

0.7

9.01 2.2

-7 .6

-3 .0

2.2

-8.8

1 .6

8.08.3

37 .8

Sold/closedentities

HongkongIndiaBeneluxUKSwitzerlandNordic

01 2

25

8

7 8

1 50

1 26

81 022

8

7 4

1 57

1 88

SwitzerlandNordic Sold/closedentities

HongkongIndiaBeneluxUK

2014 = dark2013 = light

TURNOVER GOP

EBITA

(CHF million)

excl Swiss pension impact

36

KUONI GROUP ORGANISATIONAL STRUCTUREAS OF 14 JANUARY 2015

Member of Executive Board

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 2015

Peter Meier

Chief ExecutiveOfficer

Exit of Tour OperatingActivities

Ivan Walter

Global TravelDistribution

Rolf Schafroth

Global TravelServices

Zubin Karkaria

VFS Global

Rolf Schafroth

Outbound

Thomas Peyer

Finance1)Human Resources

IT

Strategy &Communication2)

1) Including Risk, Legal & Compliance; 2) Including Investor Relations

REPORTS ON BUSINESS PERFORMANCE ON THE FOLLOWING DATES:

Annual Results 2014 17 March

General Meeting of Shareholders 20 April in Zurich

Capital Markets Day 2015 11 June in London

Half-Year Results 2015 21 August

Q3/9months Results 2015 5 November

CONTACT DETAILS

Corporate Communications Phone: + 41 44 277 4363 [email protected] Relations Phone: + 41 44 277 4529 [email protected]

www.kuoni.com mailing list: www.kuoni.com/group-news

FINANCIAL CALENDAR 2015

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201537

DISCLAIMER

KUONI GROUP – INVESTORS PRESENTATION FULL YEAR RESULTS 2014 – 17 MARCH 201538

THIS COMMUNICATION CONTAINS STATEMENTS THAT CONSTITUTE “FORWARD-LOOKING STATEMENTS” INCLUDING, BUT NOT LIMITED TO,

THOSE USING THE WORDS “BELIEVES”, “ASSUMES”, “EXPECTS” OR FORMULATIONS OF A SIMILAR KIND. IN THIS COMMUNICATION, SUCH

FORWARD-LOOKING STATEMENTS INCLUDE, WITHOUT LIMITATION, STATEMENTS RELATING TO OUR FINANCIAL CONDITION, RESULTS OF

OPERATIONS AND BUSINESS AND CERTAIN OF OUR STRATEGIC PLANS AND OBJECTIVES. SUCH FORWARD-LOOKING STATEMENTS ARE MADE

ON THE BASIS OF ASSUMPTIONS AND EXPECTATIONS THAT WE BELIEVE TO BE REASONABLE AT THIS TIME, BUT MAY PROVE TO BE

ERRONEOUS. BECAUSE THESE FORWARD-LOOKING STATEMENTS ARE SUBJECT TO RISKS AND UNCERTAINTIES, ACTUAL FUTURE RESULTS,

THE FINANCIAL CONDITION, THE DEVELOPMENT OR PERFORMANCE OF KUONI TRAVEL HOLDING AND/OR ITS AFFILIATES (REFERRED TO AS

“KUONI”) MAY DIFFER MATERIALLY FROM THOSE EXPRESSED IN OR IMPLIED BY THE STATEMENTS. MANY OF THESE RISKS AND

UNCERTAINTIES RELATE TO FACTORS WHICH ARE BEYOND KUONI'S ABILITY TO CONTROL OR ESTIMATE PRECISELY, SUCH AS FUTURE

MARKET CONDITIONS, CURRENCY FLUCTUATIONS, THE BEHAVIOUR OF OTHER MARKET PARTICIPANTS, THE ACTIONS OF GOVERNMENTAL

REGULATORS AND OTHER RISK FACTORS DETAILED IN KUONI’S PAST AND FUTURE FILINGS AND REPORTS, INCLUDING PRESS RELEASES,

REPORTS AND OTHER INFORMATION POSTED ON KUONI’S WEBSITES OR IN OTHER FORM. READERS ARE CAUTIONED NOT TO PUT UNDUE

RELIANCE ON FORWARD-LOOKING STATEMENTS WHICH SPEAK ONLY OF THE DATE OF THIS COMMUNICATION. KUONI DISCLAIMS ANY

INTENTION OR OBLIGATION TO UPDATE AND REVISE ANY FORWARD-LOOKING STATEMENTS, WHETHER AS A RESULT OF NEW INFORMATION,

FUTURE EVENTS OR OTHERWISE. IT SHOULD BE NOTED THAT PAST PERFORMANCE IS NOT A GUIDE TO FUTURE PERFORMANCE. PLEASE ALSO

NOTE THAT INTERIM RESULTS ARE NOT NECESSARILY INDICATIVE OF THE FULL-YEAR RESULTS. MOREOVER, THE PRO FORMA INFORMATION

PROVIDED IN THIS PRESENTATION SERVES AS AN ILLUSTRATION AND CONTAINS SIMPLIFIED ASSUMPTIONS. ROUNDING EFFECTS MAY OCCUR.

THE REPRESENTATION OF THIS FINANCIAL INFORMATION IS BASED ON HYPOTHETICAL BUSINESS EVENTS AND FACTS AND DOES NOT REFLECT

KUONI'S ACTUAL ASSET, FINANCIAL AND INCOME SITUATION. THE ASSET, FINANCIAL AND INCOME SITUATION OF KUONI IN FUTURE

FINANCIAL STATEMENTS AND REPORTS MAY SUBSTANTIALLY DIFFER FROM THE INFORMATION PROVIDED HEREIN. THE REASON FOR THIS IS A

STRING OF FACTORS, SUCH AS, FOR EXAMPLE, BUSINESS DEVELOPMENTS, CHANGES IN THE MARKET, AND IN THE LEGAL, REGULATORY

AND/OR ECONOMIC FRAMEWORK, AS WELL AS AMENDED ACCOUNTING REGULATIONS. PERSONS REQUIRING ADVICE SHOULD CONSULT AN

INDEPENDENT ADVISER. THIS COMMUNICATION DOES NOT CONSTITUTE AN OFFER OR AN INVITATION FOR THE SALE OR PURCHASE OF

SECURITIES IN ANY JURISDICTION.

THANK YOU FOR YOUR ATTENTION

![6TSCH Webex 05/24/2013. Agenda BoF recap[5min] Webinar announcement[5min] Centralized routing requirements draft [10min + 5min Q&A] updated TSCH draft[5min]](https://img.pdfslide.us/doc/110x75/56649f275503460f94c3fa42/6tsch-webex-05242013-agenda-bof-recap5min-webinar-announcement5min-centralized.jpg)