Embed Size (px)

Citation preview

Real Estate Summary

Edition 4, 2018

Caution mounts despite real estate's firm underlying fundamentals.

We look closely at the industrial boom.

04 Global overview

16 European summary

10 APAC summary

22 US summary

UBS Asset Management

Content

04 Global overview

10 APAC summary

Our research team

Adeline Chan Amy Holmes Brice Hoffer Christopher DeBerry Fergus Hicks Gunnar Herm Joshua Rome Kurt Edwards Melanie Brown

16 European summary

Nicola Franceschini Paul M. Guest Samantha Hartwell Sean Rymell Shaowei Toh Tiffany Gherlone William Hughes Zachary Gauge

22 US summary

Global overview

Real estate capitalization rates and yields are leveling off and rents are growing in most markets. There are multiple risks, including the steady escalation of the US-China trade war. We expect advanced economies to slow in 2019 but still remain in growth mode. New government policies increase the risk of error as central banks withdraw stimulus.

Real Estate Summary Edition 4, 2018

Page 6 of 28

Macroeconomic overview At the start of 2018 we were broadly optimistic about the outlook, but still aware of the current risks. As we enter the

closing months of the year some of those risks have

materialized while new ones have emerged. Notably we have seen another pull-back in equity markets, with the S&P 500

suffering a 10%+ correction from its September peak to late

November. This is the same scale of drop that occurred in February and reflects nervousness on the part of investors. A

stock market re-pricing from elevated levels is healthy if it

stops excessive valuations, but more worrying if it becomes

larger with the potential to spill over to the broader economy.

At the current juncture we can cite a number of other risks as being present. Donald Trump's trade war with China has

escalated steadily and tariffs have been ratcheted up on both

sides; there is nervousness over emerging markets and crises in several; while a populist government in Italy is sparring with

the EU over its budget proposals. Inflation is also a risk given

tight labor markets in many countries and firming wage growth, now above 3% in the US for the first time since

2009. On the positive side, and showing that the Trump

administration can do deals if the terms are right, a successor to the North American Free Trade Agreement (NAFTA) has

been agreed. This would be subject to ratification, in the form

of the United States-Mexico-Canada Agreement (USMCA).

Despite these risks economies have held up reasonably well,

but did slow in 3Q. The US has been strongest, benefitting from a fiscal boost this year, with growth slowing to 3.5%

annualized in 3Q from 4.2% in 2Q. The Eurozone has been

weaker, registering 0.2% quarter on quarter (QoQ) growth in 3Q, the slowest in five years and down from 0.4% QoQ in 2Q.

It's worth noting that the initial estimate for 2Q Eurozone

growth was revised higher, which may yet happen to the 3Q figure. However, survey data has also weakened, implying the

slowdown is real rather than imagined. In China growth

slowed to 6.5% year over year (YoY) in 3Q, in line with the government's target for the year and expectations of slower

growth in the years ahead.

World trade growth has slowed slightly but not fallen

precipitously. It has received support from some exporters

expediting sales prior to tariffs coming into force. The

escalation of the trade war between the US and China poses a

significant risk. To date the US is imposing additional tariffs on

washing machines, solar panels, steel, aluminum and USD 250 billion of its annual USD 506 billion of imports from China (see

Figure 1). China is imposing tariffs on USD 110 billion of its

annual USD130 billion of imports from the US. President Trump has warned that the 10% tariff announced in

September on USD 200 billion of Chinese imports will rise to

25% in January if no agreement is reached, and threatened tariffs on another USD 267 billion of goods.

With China nearly out of runway in terms of additional goods

to tariff, it would need to look to other options for retaliation,

such as withholding supplies of essential rare earth materials on which it has a monopoly, or curbing the number of

Chinese tourists and students heading to the US. The IMF has

estimated that an escalation of the conflict which saw tariffs extended to cover all US-Chinese trade, all US car imports with

retaliation by trade partners, along with confidence and

market effects, could knock nearly 1% off US Gross Domestic Product (GDP) in 2019, around 1.6% off Chinese GDP and

0.8% off world GDP. However, some commentators suggest a

much larger impact on global GDP of perhaps 2-3%.

Figure 1: US-Chinese mutual goods tariffs (annual, USD

billions)

Sources: UBS Asset Management, Real Estate & Private Markets (REPM), November 2018

Against this backdrop the job of central bankers has arguably

become harder. So far the Fed has tried to discourage the notion of a "Powell put" and is expected to press ahead with

a rate increase in December given the strong economy.

However, a further knock to equity markets or the unfolding of another risk could see the Fed mimic its actions under Alan

Greenspan of easing policy in times of crisis, and hold back on

a December rise. Meanwhile, the European Central Bank (ECB) has tentatively announced that it will finish its asset purchases

at the end of the year, while the Bank of Japan continues with

asset purchases and rates at zero.

Moving into 2019 we expect growth to slow in the advanced

economies. The fiscal boost the US received in 2018 will fade while the Eurozone, already slowing, will face capacity

constraints in some countries due to low unemployment rates.

In general economic expansions do not die of old age, but longer expansions can encourage risk taking. Moreover, as we

exit an unprecedented period of new and unconventional

monetary policies there is scope for error by central banks. Even with supportive government policies, navigating these

waters successfully will prove tricky. Unhelpful government

policies could make the challenge harder still.

0

100

200

300

400

500

600

Tariffs 2017 totalimports

Tariffs 2017 totalimports

Applied July/August Applied September Threatened

US

China

Real Estate Summary Edition 4, 2018

Page 7 of 28

Capital markets Real estate investment activity has been healthy in 2018 as investors look to further build their real estate allocations. At

the global level investment volumes for income producing

assets were up 2.6% in the first nine months of the year compared to 2017 (in dollar terms). However, activity remains

below the peak levels reached in 2015, partly due to a

mismatch between buyer and seller price expectations in some markets, and partly due to a lack of available product. Indeed,

to counter this investors are increasingly turning to forward

funding and building to core as a means of deploying capital.

Figure 2: Global investment volumes (12 month, USD

billions)

Sources: RCA; UBS Asset Management, Real Estate & Private Markets (REPM), October 2018

Underlying activity in the office sector has been pretty stable, while retail and industrial have mirrored one another.

Industrial volumes showed strong growth in 2017, while from

the second half of 2015 retail volumes trended downwards. More recent data show a tentative recovery in retail volumes,

while industrial volumes have levelled off. Indeed, on a trailing

12 month basis global industrial investment volumes have

reached near parity with retail, having been nearly 40% below

them as recently as mid-2017 (see Figure 2).

Of the markets reporting performance on a higher frequency

basis, figures relating to 2018 so far have been positive. For

example, National Council of Real Estate Investment Fiduciaries (NCREIF) reported direct, all property, unleveraged

returns in the US of 7.1% for the year to 3Q, while MSCI-IPD

reported UK All Property returns of 8.2% over the same period. Meanwhile in the Netherlands, for which the latest

MSCI-IPD data available relates to 2Q, annual returns were a

punchy 14.9%. We think returns will slow in most markets moving into 2019 as capital growth fades.

Strategy viewpoint For the past couple of years we have been upbeat on the industrial sector and it has consistently topped our table of

performance expectations in most countries. This expectation

has been broadly met as the well-reported expansion in e-commerce has seen supply chains re-purposed and demand

for logistics facilities surge, pushing rents higher. If anything

our expectations proved too cautious and performance has been even higher than we were expecting.

For example industrial property recorded returns 20% in the

UK in 2017, 13% in the US and 12% in the Eurozone.

Moreover, even now we are expecting all these markets to

deliver double-digit returns in 2018. Over the next couple of years we expect industrial to continue outperforming, before

converging with the other sectors in 2021. In particular, we

think there is room for catch-up in some continental European markets where on-line sales are less developed than in the UK

and US, and Australia where Amazon arrived in 2017.

However, strong outperformance of any asset class can be a

worry and lead to fears of a correction. For example, the

industrial equivalent yield in the UK in 3Q 2017 was 5.9%, the highest of the three main commercial sectors. By 3Q 2018,

however, it had fallen to 5.3% and become the lowest

yielding sector, not previously seen in data going back to 1980. For the time being we expect the outperformance of

industrial to continue as strong demand drives rental growth.

Moreover, rents are coming off low levels and are a relatively low share of logistics companies' costs, whereas tight labor

markets mean staff availability and labor costs are becoming

more of an issue for them.

We would certainly be wary of transaction prices which are a

long way ahead of valuations. In particular, in a period of strong demand purchasers must do thorough due diligence on

assets they are considering purchasing and ensure they do not

factor in excessive rental growth expectations. We have previously discussed in this publication some of the things

which could derail the industrial story. They include any

disruption to the online distribution model, be that changing consumer preferences, or regulatory intervention on the basis

of environmental protection, traffic congestion or protecting

traditional retailers. Indeed, we have already seen some moves

in this area, including online retailers in the US being forced to

collect sales tax and granting business rates relief to small

retailers in the UK. Calls for such moves to level the playing field look set to only get louder.

0

100

200

300

400

500

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Office Retail Industrial

Real Estate Summary Edition 4, 2018

Page 8 of 28

Any hit to global trade volumes also presents a threat. Conceptually though, we think some types of industrial property are more at risk from a trade war than others. By definition, we think any reduction in trade volumes would likely have a disproportionate impact on real estate around key international transport modes such as ports and airports. With fewer goods flowing through these facilities demand for industrial space around them would likely weaken.

However, logistics facilities used to distribute goods to final consumers, particularly for online sales, look less exposed. Hence last mile, urban logistics facilities used by parcel companies and those used by retailers to fulfil online orders would seem more resilient. A caveat would be if the trade war triggered a broader downturn in the economy which impacted consumer spending. Under this scenario logistics focused on fulfilling consumer demand would likely suffer too.

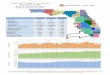

Real estate investment performance outlook 2017 performance and outlook are measured against the sector's long-term average performance, with a margin of 100bps around the average described as "on trend" or "stable".

Asia Pacific

Office Retail Industrial Multifamily

Australia

Japan

Europe

France

Germany

Switzerland

UK

North America

Canada

United States

Icon color: 2017 performance Icon style: Outlook (2018-2020)

Above trend

Positive

On trend

Stable

Below trend

Negative

Source: UBS Asset Management, Real Estate & Private Markets (REPM), November 2018

Real Estate Summary Edition 1, 2018

APAC summary

Real Estate Summary Edition 4, 2018

Economic sentiment is likely to trend lower amidst uncertainty over trade tensions. Commercial property leasing demand is mixed but generally robust. Capital markets are buoyant although activity is centered on a few key cities. The industrial sector still sees value in general but the immediate winners and losers are unclear.

Real Estate Summary Edition 4, 2018

Page 12 of 28

APAC summary Demand and supply Trade seems to have gone from hero to zero these days, not due to its diminished importance to GDP growth, but because

the factor which has provided the uplift for much of APAC's economic recovery over late 2017 and early 2018 threatens to

become the very element which may hasten the growth

slowdown in the coming quarters. This is especially so given the recent escalation in the US-China trade conflict.

At a glance, it is not immediately clear what the eventual effect of the trade measures will be. Trade linkages are vast

and complex, and direct exposure to trade can only tell part of

the story. Take Singapore for example – export of goods to China and the US make up a combined ~17% of GDP, which

is dwarfed by Hong Kong's export exposure to both countries,

making it appear like Singapore would be relatively more insulated from the trade tariffs than Hong Kong (Figure 3). But

the final impact of trade is obscured by other factors such as

indirect trade linkages, the composition of exports and the diversity of the economy; given that Association of Southeast

Asian Nations (ASEAN) economies, which are among

Singapore's largest export partners, are also expected to take

a hit from the tariffs. Singapore would thus experience the

impact of the US-China tariffs via other channels as well. Thus,

it may serve us better to gauge the effect of the trade tariffs using the more general indicator of trade openness instead.

The countries more likely to be affected by an overall waning

of trade momentum in the near term are probably small and highly open economies, namely Singapore and Hong Kong

(Figure 4). In the longer term, each country has built up its

respective competitive advantage which is unlikely to be substituted and replaced so easily.

The common refrain across APAC economies in 3Q 2018 is that growth is slowing – China and Singapore both saw GDP

growth moderate while early indicators are signaling that the

same can be expected for Hong Kong and Australia.

The traditional sectors that used to fuel China's rapid rise have

slid in 3Q – industrial production growth cooled, credit growth slipped, and fixed asset investment (FAI) growth rate fell to

5.3% YoY for 8M 2018, a record low. Services sector growth

was the bright spot, outpacing GDP (6.5% YoY as at 3Q 2018) with a ~8% YoY expansion.

Australia's economy is holding up well as the country logs its 107th straight quarter of growth in 2Q 2018. Growth drivers

have broadened out from exports in 1Q to household

consumption and government expenditure in 2Q. Nevertheless, there are several factors that would keep us

from getting carried away on Australia's outlook, such as

potential negative wealth effect from falling home prices, lack of wage growth from the continued slack in the labor market,

and the fact that over a third of Australia's merchandise

exports go to China.

Hong Kong has seen its economy supported by consumer

spending in 1H 2018 but that looks to be less of a certainty

given that both home prices and the stock market have started to turn south. Singapore's economy has largely been

lifted by the external and manufacturing sectors but the latest

3Q 2018 GDP growth figures have slipped as it approaches late-stage expansion.

In Japan, GDP rebounded to an expansion of 0.7% QoQ in 2Q 2018 from a contraction of 0.2% in 2Q 2018. Business

investment and private consumption were the main

contributors to growth. Household spending is expected to pick up in the coming quarters given the tight labor market

and a possible frontloading of spending from the planned

consumption tax hike in 2019. Nevertheless, a trade slowdown remains a risk given its impact on sentiment.

Figure 3: Export of goods to US and China (% of GDP, 2017)

Figure 4: Export of goods and services (% of GDP, 2017)

Source: IMF, October 2018

Industrial

The sector most likely to bear the immediate brunt of a trade slowdown is ostensibly the logistics space. Hong Kong in

particular, being an open economy where almost all of its

exports are re-exports from China, is the prime candidate to take the strongest hit. Recent rental performance betrays any

sign of trepidation.

0

30

60

90

120

Hong Kong Singapore Australia Japan

China US

0

50

100

150

200

250

Singapore Hong Kong China Australia Japan

Real Estate Summary Edition 4, 2018

Page 13 of 28

According to CBRE data, overall warehouse rents rose 1.5%

QoQ, the strongest quarterly increase since 4Q 2014. This

comes amid a drop in warehouse vacancy rate to 2.9%, the lowest since 4Q 2015. Leasing activity was robust, although

this was partly due to frontloaded trading activity. The

buoyancy of demand for warehouse space may eventually soften when the impact of the tariffs trickle through, but

Hong Kong's industrial and logistics space will still be buffered

by demand from other high value-added occupiers as well as limited space availability.

Tier 1 cities in China are similarly facing tight supply, particularly in the high quality logistics space – vacancy rates in

cities like Beijing, Suzhou and Wuxi are below 1%, and new

supply in 3Q 2018 was readily absorbed with the net take-up in Tier 1 cities rising to a record high of 0.7 million sqm.

Notwithstanding a trade slowdown, the Chinese domestic

market is already sizable and a shortage of quality logistics space in Tier 1 cities will likely keep the rental outlook positive.

The rest of the APAC markets are similarly seeing strong performance in the industrial sector. Major infrastructure

projects are supporting the construction sector and

corresponding demand for industrial space. Melbourne, Australia is an outperformer with a 6% YoY increase in rents

in 3Q 2018. Rental growth in Sydney is more muted at 1.9%

YoY but demand is still strong, with vacancy across the major submarkets already at cyclical lows. Tokyo's logistics market is

facing a wave of major new supply but demand is similarly

robust. For example, 1Q 2019 is expected to see the highest

ever quarterly new supply, but some properties are already

reported to be fully let. The rise in vacancy rate from

upcoming supply is thus expected to be limited, although there is still a sharp distinction between the inland and the Bay

area, the latter of which has a tighter vacancy rate.

In Singapore, business park rents appear to be approaching

late-cycle expansion with growth starting to slow.

Nevertheless, the broader industrial market is expected to bottom in the near term given the tapering off of pipeline

supply. Retail

The performance of the retail market in APAC in 3Q 2018 was

largely shaped by two broad forces – growing inbound tourists and disruption due to e-commerce.

The markets which have been benefitting from inbound tourists are Hong Kong, Singapore and Tokyo. Tourism-

oriented retailers such as personal care companies, cosmetic

brands and watch and jewelry shops have been driving leasing activity in Hong Kong's high street. In Singapore, demand was

boosted by new entrants, while landlords have also been fine-

tuning their store offerings by bringing in more activity-based retailers like gyms, arcades and cooking studios.

Tokyo's prime retail market has also been a beneficiary of the rise in visitor arrivals, although that dipped in September in

part due to a recent spate of natural disasters. Leasing

demand was still healthy in 3Q 2018, led by luxury brands and

F&B operators. The outlook is positive in the near term given

the expected front-loading of consumer spending ahead of

the planned consumption tax hike.

Australia, on the other hand, has still been dealing with the

effects of the online disruption. Despite the rise in household consumption, major retailers such as David Jones are still

consolidating stores and regional centers are bearing the

brunt of the structural challenges posed by e-commerce. Prime Central Business District (CBD) retail, however, still

benefits from locational advantages and is still seeing rental

growth.

The Tier 1 cities of Beijing and Shanghai saw average ground

floor shopping center rents rise 0.9% and 0.2% QoQ respectively in 3Q 2018. The retail market is still driven by the

structural growth of the middle class and rising income levels.

Some new projects had pre-commitment rates of over 90% and it is reported that several others have secured full

occupancy ahead of completion. While the long-term

prospects for retail in China's Tier 1 cities remain positive, the near-term outlook will be impacted by substantial pipeline

supply.

Office

Strong demand and a lack of supply continued to drive

positive rental performance for most APAC markets in 3Q 2018 (Figure 5). Aside from the Tier 1 cities in China, vacancy

rates in most cities in APAC continued to tighten.

Figure 5: APAC CBD office vacancy rates (%of existing stock)

Source: CBRE, 3Q 2018

Nowhere is this more evident than in Tokyo, where the Grade

A vacancy rate fell below 1% for the first time since 2007.

Strong corporate profitability and a tight labor market are driving companies to increase their footprint. New builds in

2Q were almost fully let, and upcoming completions in 2019

are almost fully let. This resulted in a 2.2% YoY rise in rents in 3Q 2018, accelerating from the 1.2% increase in 2Q 2018.

Prime rents in Sydney grew by an enviable 6.8% YoY in 3Q 2018 as stock withdrawals continue in an already tight office

market (Figure 6).

0

10

20

30

40

Tokyo

Sin

gapore

Seoul

Ho

ng K

ong

Syd

ney

Melb

ourn

eBrisb

an

ePert

h

Guangzh

ou

Beiji

ng

Shenzh

en

Nanjin

gN

ingb

oShanghai

Dalia

nH

angzh

ou

Ch

engdu

Qin

gdao

Shenya

ng

Ch

ongqin

gW

uhan

Tia

njin

2Q18 3Q18

Real Estate Summary Edition 4, 2018

Page 14 of 28

Prime rents in close rival Melbourne also rose by a similarly

robust 6.8%, driven by strong economic performance and

white collar employment. Demand is expected to remain strong but substantial pipeline supply is expected to result in

rental growth slowing over the next 12 months.

Hong Kong's prime submarket is similarly tight, with rents in

central rising to a historical peak in 3Q 2018. There are,

however, signs that the market euphoria should start to cool soon. Leasing momentum slowed and the rental growth in

central has moderated from 3.1% QoQ in 2Q 2018 to 2.0%

in 3Q 2018. In general, leasing demand in Tier 1 cities in China seem to have been weighed down by concerns over the

US-China trade conflict as well as the regulatory clampdown

in the peer-to-peer lending sector. Average asking rents in Beijing was flat on a YoY basis while rents fell 1.2% YoY in

Shanghai. Singapore's office market was the outperformer in

3Q 2018, with a 15.6% YoY increase in CBD prime office rents, partly due to a low base effect. Demand was broad-

based and with pipeline supply tightening, further rental

growth is expected in the near-term.

Figure 6: APAC CBD prime office rent growth (% p.a.)

Source: CBRE, 3Q 2018

Capital markets Investment interest in APAC commercial property lost some

momentum in 3Q 2018 relative to 2Q 2018 but nevertheless

remains robust (Figure 7). Data from Real Capital Analytics

(RCA) shows that the rolling 12-month transaction volume in commercial property (excluding sales of development sites) in

APAC in 3Q 2018 was worth USD 165 billion, slightly lower

than the USD 176 billion recorded in 2Q 2018 but 3% higher than the total value for 2017. Transaction volumes received a

whopping 57% YoY boost from Hong Kong in 9M 2018,

followed by a 23% growth in transaction volumes in South Korea. Australia, Singapore and Japan also saw low single

digit contractions (1.3%, 3.2% and 4.4% YoY respectively),

with China being the only market with a more severe 15.9% YoY contraction, reflecting dampened sentiment due to the

government's deleveraging efforts.

Despite the dip in transaction volume, China still holds the

biggest share of investments in 3Q 2018 with 20% of total

transaction volumes in APAC, down from 25% a year ago. While the bulk of investment interest has centered on Tier 1

cities, capital has increasingly found its way into Tier 2 cities,

which likely reflects a search for yield and value.

Hong Kong, in the meantime, has been the most visible

recipient of abundant capital spilling over from the Mainland as it sees its share of total APAC investment volumes rise from

about 12% in 3Q 2017 to about 17% in 3Q 2018,

representing an almost doubling of the absolute value of transactions. Office properties traded hands most often, and

in a reflection of how the stratospheric rise in capital values

has forced investors to purchase smaller and smaller parcels of space, all but one of the office transactions in 3Q 2018 were

of strata floors and units, according to RCA data. The sole en

bloc transaction in 3Q 2018 was for Lever Tech Centre for USD 159 million (USD 1,390 psf), but the biggest office deal

worth goes to the sale of the 58th and half of the 21st floor of

The Center at USD 229m (USD 6,202 psf), which only made headlines about a year ago for being the largest single office

building transaction in history. Just a year on, the building is

already being sliced and diced up for sale and at values that are almost 50% higher than its original sale price of USD

4,198 psf. This is emblematic of the trend that has been going

on in Hong Kong for years – huge amounts of capital looking for assets, driving capital values to ever higher values and Cap

Rate to ever lower levels.

Total value of deals in Japan has largely held steady from a

year ago, and transaction activity remained anchored by J-

REITs in the office sector. Australia has experienced a rise in transaction volumes in 9M 2018 with investors drawn to its

relatively higher yields while owners are increasingly open to

taking profit on their holdings.

While strong investor interest has presided over a multi-year

Cap Rate compression in APAC, we think the yield compression story is starting to lose momentum. Most

markets are already experiencing a squeeze in the yield

spreads, and investors would be well-advised not to underwrite significant capital growth in their investments.

Figure 7: Commercial real estate transaction volumes (USD billion)

Source: RCA, 3Q 2018

(15)

(10)

(5)

0

5

10

15

20

Pert

h

Brisb

ane

Melb

ourn

e

Syd

ney

Chon

gqin

g

Shenzh

en

Wu

han

Shang

hai

Tia

njin

Beiji

ng

Nanjin

g

Shenya

ng

Hangzh

ou

Guang

zhou

Cheng

du

Hong

Kong

Tokyo

Seoul

Sin

gap

ore

3Q18 3Q17

0

20

40

60

80

100

120

140

160

180

'13 '14 '15 '16 '17 '18

Individual Portfolio Entity

Real Estate Summary Edition 4, 2018

Page 15 of 28

Viewpoint Trade wars – you can't win, Darth

In several meetings with investors and associates over the past

months, we have often been asked to 'pick sides' and predict whether China or the US will emerge triumphant in this

protracted trade scuffle. There has to be a loser, no? Adam

Smith, in his book "The Wealth of Nations" puts forth trade (mercantilism) as a zero-sum game, which obviously is no

longer valid in our increasingly interlinked global production

networks. It is also not true that the side that exports more

(i.e. China) stands to lose more relative to the net importing

party (i.e. US), given the globalized nature of intermediate

inputs in manufacturing. Many of the imports from China, on which the US is slapping tariffs are vital inputs in the

production chains of companies producing in the US itself.

Suffice to say, it is near impossible to pick a winner (or loser) from the ongoing trade fracas. When the dust settles, if it

does, both the US and China will feel the pain inflicted

mutually. At the same time, some real estate markets will benefit more, albeit serendipitously, while many others will

become collateral damage.

While many market watchers have commented on the arsenal

of tools that China has at its disposal, it will not come away

unscathed. Our ground checks have surfaced anecdotal feedback that some manufacturers in China are starting to

feel the stress on their profit margins, as major US customers

start to pass through part of the tariffs to these exporters. In response, the Chinese government has relaxed its financing

guidelines and directed more funding towards the small and

mid-sized firms in China in a bid to tide these manufacturers over this rough period. The State Council has also recently

announced tax cuts that will provide more than USD 6bn of

tax relief in 2018 alone. In early October, China further slashed the reserve requirements on banks to inject an

estimated USD 100 billion into the economy. For sure, these

are just the tip of the iceberg in terms of the supportive measures China can engage in.

What is worrying is that this trade issue may distract China from its ongoing deleveraging efforts, as it takes two steps

back and potentially starts to ease up on its monetary policy.

There are many 'what-ifs' here. Any excessive credit that is not directed at productive sectors may end up spurring greater

indebtedness and sow the seeds of financial woes in the

future. If this does get out of hand, we can expect domestic investments into commercial real estate to further increase,

pushing up already frothy capital values. In the residential

sector, inventory destocking is still underway, especially in the lower tier cities, and if Beijing allows residential construction

and investment to grow, the current destocking efforts will be

partly derailed after years of strong progress. Furthermore, if China embarks on the devaluation of the currency to offset

the tariffs, it will risk capital flight and imply a willingness to

retreat from financial liberalization goals. So even if China wins the trade war, it still loses.

From a regional perspective, the trade tensions have spillover

effects on regional commercial real estate markets that extend

beyond China. Generally there are two main channels of transmission; one, through a slowdown in economic growth

and business sentiments, and two, via the re-routing of real

estate locations in the supply chain. It is also likely that weakened business confidence, if persistent, will have a

significant impact on growth, and consequently the demand

for commercial real estate such as industrial space.

More than half of China’s exports to the US are produced at

facilities owned by foreign companies. Tariffs directed at China exports in reality affects many American and European

companies that have production facilities in China. For a while

now, many manufacturers, foreign or domestic, have already started to diversify their production bases, partly as a result of

rising labor costs in China. The beneficiaries of the re-direction

of manufacturing locations have been the likes of emerging Southeast Asian countries such as Vietnam, Indonesia and

Malaysia. While the trade issue has increased the urgency for

manufacturers to explore alternative options, it would be naïve for anyone to believe there will be a mass exodus of

manufacturing from China to Southeast Asia overnight.

Companies cannot immediately respond to tariffs by hastily moving their operations out of China, and there is significant

capital expenditure yet to be amortized. Our view is that

emerging Asia continues to be a hotspot for industrial property, but there is no reason why the trade skirmish has

accelerated or enhanced the investment appeal of these

emerging markets. There are huge risks associated with

investing in an emerging economy, and much of the

institutional logistics stock is not available for sale or

investment yet. Manufacturers who do enter the likes of Indonesia or Vietnam often struggle with identifying industrial

facilities of good specifications if they do not have local

partners. On the other hand, there is also market mention of Japanese and Korean manufacturers shifting production in

China back home. Again, this will likely not happen on a

massive scale, and we should not expect industrial property prices in Japan or Korea to surge in the near term.

In the mid to long term, the regionalization of APAC through greater multilateral cooperation and trade linkages, such as

the ASEAN bloc or the Regional Comprehensive Economic

Partnership, is likely to offer fortification against trade and economic shocks. Can these regional partnerships shield Asia

from the stray bullets of the trade war? No. Should it even be

desirable for Asia to move towards insularity? Again, the answer is a resounding no. What a solid trade and economic

bloc can do for Asia, is to create an enlarged hinterland of

demand and supply for goods and services, and that is likely to be positive for commercial real estate prospects.

In conclusion, this is going to be a long game. The fundamental growth drivers are intact but there will be losers

and some fringe winners. To that end, we do not believe

opportunistic investing in industrial real estate will bring about attractive risk adjusted returns.

16

European summary

17

Take-up and rents continue to rise despite softening fundamentals, while the development pipeline remains muted in most locations. Investment volumes continued to fall in 3Q as caution persists. Yields remain stable in almost all locations.

Real Estate Summary Edition 4, 2018

Page 18 of 28

European summary Demand The 'Euroboom' expected at the start of 2018 appears to have lost more momentum in the third quarter as soft economic

fundamentals and political uncertainty appear to be weighing on demand (see Figure 8). GDP growth in 3Q was highly

disappointing at just 0.2%, its lowest level in five years. While

part of this can be explained by transitory factors, sentiment has declined over the year hinting we may not see a stellar

rebound in 4Q. Manufacturing appears to have also had a

slow start in 4Q with PMIs sinking below 50, indicating contraction. As a result, European equity markets have

tumbled in line with a global sell-off in recent months; the

Stoxx Europe 600 is currently trading at around 7% below its level at the start of the year.

A large factor is the political situation in Italy, where the populist government is at loggerheads with the European

Commission over its high spending budget, despite already

high levels of government debt. As a result, the spread on Italian bond yields over German bunds has reached record

highs. Economic activity has also reduced in the third quarter,

as the situation shows no sign of resolving itself soon.

It is perhaps unfair to single out Italy, as other countries have

not had a great quarter either. Germany saw almost flat GDP growth, although part of this can be explained by disruptions

to the auto industry as well as problems with shipping on the

Rhine. On a brighter note, Spain continues to expand at a healthy pace and France has performed reasonably well too,

benefitting from growth in both consumption and fixed

investment.

In spite of softening economic indicators, office take-up

remains strong and 3Q18 saw a rise of 2.1% YoY as rolling annual volumes continued to trend upwards. Take up in UK

regional cities has been stronger than in London with Glasgow

and Liverpool both seeing strong leasing compared with the previous year. London has actually been fairly resilient with

most of the new supply in the pipeline pre-leasing at a decent

rate. Take-up in the City actually increased by 14%, although a growing share of the market is accounted for by serviced

office providers such as WeWork. Since much of the take-up is

also relocations of tenants already in situ, there are also concerns about older more secondary stock which will likely

be released in the near future. Elsewhere, Munich (+32%) and

Frankfurt (+19%) had a strong 3Q, while Paris (+13%) and Lyon (+22%) also saw high levels of tenant demand as the

economy continues to improve. Utrecht in the Netherlands has

become popular with occupiers as availability in Amsterdam continued to decline; leasing here grew by 167% when

compared with the same point in the previous year (on a four

quarter cumulative basis). Porto also had a stellar four quarters up to 3Q, with volumes rising by 347%.

There were not too many poor performers this quarter;

Aberdeen saw take-up fall by 3% most likely due to concerns

about its ongoing reliance on the oil market. The West End of London also saw take-up decline by 21%, however this has

more to do with low levels of supply than demand. We are

hearing anecdotally that occupiers will still pay top rents for modern offices as and when they become available.

Pan-European rental growth remains strong with prime rents increasing by 3.2% when compared with the same period last

year. Utrecht and Porto both saw stellar growth following

surging levels of take-up with rents rising by 21% and 18% respectively. Stockholm saw yet another good quarter with

rents rising by 17%; the Swedish capital has been a

consistently strong performer of late, with rents seeing double digit growth for the past 13 quarters. Also showing

persistently strong performance was Berlin, with rents

growing by a further 12%. There were relatively few cities seeing prime rental decline: the City of London has seen rents

decline fractionally, with values falling by 2% despite high

levels of leasing activity, while rents in Vienna also fell by 2%.

Figure 8: Aggregate European office take-up volumes

(000s sqm, select key centers)

Source: JLL, 3Q18

The retail sector has had a rough year, especially in the UK where values have finally started to fall. There have been

numerous administrations and company voluntary

arrangements (CVA), while a private equity-owned shopping

center in Maidenhead entered into administration. The picture

in Europe is somewhat less severe, due at least in part to

lower levels of online shopping. JLL estimate the current share of online sales in Europe will reach 11.9% in 2022, compared

with 22% in the UK. Nonetheless, prime remains more

resilient than average with pan-European rents growing by 1.3% YoY. We are hearing anecdotally that tenants have

become much more aggressive when negotiating rental levels

which is limiting further income growth for landlords. Nonetheless, Italian cities performed well with Rome (+16%),

Milan (+14%) and Verona (+14%) all seeing strong levels of

growth. At the other end of the spectrum, rents are now falling in several locations including Hamburg (-2%), Antwerp

(-6%) and Brussels (-7.5%).

0

3000

6000

9000

12000

15000

18000

0

1'000

2'000

3'000

4'000

5'000

1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q

14 15 16 17 18

Take-up Rolling annual

Real Estate Summary Edition 4, 2018

Page 19 of 28

Figure 9: Consumer confidence - outlook next 12 months

(Balance - SA)

Sources: Datastream; DG ECFIN, August 2018

As is now very well known, logistics is very much the 'in'

sector having become mainstream thanks to the growth of

online shopping. Demand from operators such as Amazon remain very strong, as they compete with retailers and

traditional manufacturers for space (see Figure 9). This

ensured rents continued to tick-up in 3Q; on a pan-European basis with prime rents growing by 1.6% YoY.

There is, however a big discrepancy between urban rents and warehouses in out of town locations. Larger format sheds

tend to see lower rental growth due to the predominance of

design and build in this market and cheaper land value. In cities, however there are many other uses jostling for space

which makes logistics schemes hard to zone due to the

relatively low capital values and high land usage. For this reason, industrial supply in key cities remains

incredibly scarce and rental growth on existing sites has been

double-digit the past few years. Rents in Berlin grew by 8% to 3Q18, while the Schiphol area in Amsterdam saw values jump

by 15%. In the UK the story has very much been about

London and the South East, however the regions are likely to catch up. In 3Q rents in the South East still grew by 5.4%,

however the highest growth was in the South West of the

country at 11.6%. By way of caveat, values here are almost half the levels currently on offer in London and the South East.

Supply Supply continues to be very restricted as most European cities

are seeing relatively low levels of development (see Figure 10). Speculative space under construction as a proportion of total

stock remains under 5% in most European cities. The

standout exception is Warsaw, where there is currently 11.5% of additional speculative stock under development, although

this has moderated from 15% during the previous quarter.

The City of London continues to see high levels of development although speculative volumes have been pared

back to just 5.6% of total stock. La Defense in Paris now

actually has more speculative space underway at 6%. The 'big 7' German cities by contrast (Frankfurt, Munich, Berlin,

Hamburg, Dusseldorf, Stuttgart, Cologne) all have less than

2% of speculative space under construction.

Unsurprisingly office vacancy continues to trend down, falling

from 7.3% in 2Q to 7.1% in 3Q. As ever, there are significant

regional differences. Berlin and Munich remain the German cities with lowest availability with respective vacancy rates of

just 2.5% and 3.1%, though Frankfurt (8.3%) and Dusseldorf

(7.6%) are somewhat higher. London remains low despite high levels of development and wavering demand, with the

City at just 5.5% and the West End at 3.7%. However, as

alluded to above, this is due to effective pre-leasing on the new schemes and we could see the release of more

secondhand space going forward. Paris has seen its vacancy

fall over the past couple of years from above 7% in 2015 to just 5.1% in 3Q 2018. The only recorded areas with vacancy

above 10% in this quarter were Rome and the Schiphol area

of Amsterdam.

Retail continues to be blighted by the issues discussed above

and has subsequently seen very low levels of development in all segments. It is likely that there is now too much retail space

in Europe, although the situation is not nearly as bad as in the

US. The UK has the highest per capita supply and as such is facing the greatest challenges. Secondary shopping centers

are particularly vulnerable, although retail warehouses are

showing some distress following recent administrations. Going forward, the question will not be so much where to build

retail space, but which locations to convert to other uses.

There is a lack of supply data available for logistics, however in

most areas monitored by CBRE there has been a decline in

availability particularly for prime stock. It is increasingly

challenging to secure zoning for use by logistics development

as facilities are unpopular with residents and local authorities.

The former are generally hostile to increased Heavy Goods Vehicle (HGV) traffic while the latter gets much lower tax

revenue compared with other uses. For this reason, industrial

land is particularly constrained in urban areas, which has fueled strong rental growth for existing sites. In more remote

locations, development is easier but this tends to command

lower capital values. For these reasons, there is a lack of speculative development across Europe and occupiers are

increasingly turning to pre-lease deals with landlords to meet

their specifications.

Figure 10: Prime rent index (3Q08 = 100)

Source: CBRE, 3Q18

(30)

(20)

(10)

0

10

Oct-11 Oct-12 Oct-13 Oct-14 Oct-15 Oct-16 Oct-17 Oct-18

Europe UK

80

90

100

110

120

130

140

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

3Q

16

1Q

17

3Q

17

1Q

18

3Q

18

Retail Industrial Office

Real Estate Summary Edition 4, 2018

Page 20 of 28

Capital markets Capital markets continued to slow in the third quarter with volumes down around -30% when compared with the same

period the previous year. While the third quarter is often a

quieter one, it cannot be denied this represents a notable lull in market activity. It is hard to pin down what has spooked

investors; there does not appear to be a huge fall in sentiment

and pricing has remained solid. One explanation is general concerns about geopolitical issues, such as the Italian budget

and Brexit. Additionally the prospect of a trade war will be a

worry for what is ultimately an exporting continent (see viewpoint). However, it could just be a brief pause as the

early indications are that 4Q has got off to a dynamic start.

The slowdown was reflected across all sources of capital,

although the biggest fall was among buyers from China (-

54%) and Hong Kong (-61%). Other Asian investors appear to have picked up the slack to some extent and it is likely it will

be a record year for South Korean investment into Europe

with around EUR 7 billion either completed or under contract. Overall, US investors remain strong net sellers and 2018 has

not been able to maintain the momentum of the previous

years in terms of foreign capital shoring up the market. Interestingly, there has been an increase in European money

coming into the UK indicating continental investors may not

be as concerned about Brexit as initially thought.

The fall in volumes seemed to weigh heavily on the office and

retail sectors, though even logistics fell slightly when compared with the previous year. The most resilient sectors

were accommodation services, as investors look to add

diversification through assets less exposed to the business cycle. Apartments only saw a slight decline YoY, while senior

housing and care homes actually saw volumes increase

fractionally.

Activity varied significantly by country as Germany, Sweden

and Spain all saw more money spent than in the previous

quarter, while the French market slowed by around -60% following a year of strong spending. Italy continues to be

plagued by political uncertainty and saw its slowest three

months since the Euro crisis in 2012.

In line with the general market, there have been few cities

where volumes have increased. Lisbon is an exception, where nearly EUR 2 billion of assets were traded in 2018 as

international investors look to take advantage of Portugal's

slightly delayed recovery. Frankfurt also saw volumes jump as several of the large towers traded, possibly related to

anticipated benefits from Brexit. London remains in demand

with volumes only declining fractionally, despite the number of deals coming off significantly. This reflects ongoing demand

for prime assets even as the UK prepares to withdraw from

the EU. At the other end of the spectrum volumes into regional centers were not as buoyant with Manchester and

Birmingham both seeing a fall in transactions, while Berlin saw

volumes decline by a third possibly reflecting the very stretched yields now on offer there.

As alluded to above, pricing remains strong; pan-European yields declined by a further 3 bps to reach 3.8%. Most of this

compression came from the industrial sector which came

down by a further 15 bps, while office yields and retail remained largely flat. Office yields were flat in most locations,

although increased investment in Portuguese real estate saw

the relatively high-yielding Porto compress by 50 bps,

although Lisbon surprisingly remained flat. Multiple logistics

centers across Europe continued to see compression of around

30-50 bps. Selective well-performing retail assets continued to compress, although spreads between prime and secondary

assets remain at elevated levels.

Figure 11: EU-15 Yield Index Figure 12: European Investment volumes (EUR billion)

Sources: CBRE; RCA, 3Q18

3.00

4.00

5.00

6.00

7.00

8.00

3Q

12

3Q

13

3Q

14

3Q

15

3Q

16

3Q

17

3Q

18

Retail Yield Industrial Yield Office Yield

0

50

100

150

200

250

300

350

0

20

40

60

80

100

120

3Q

07

3Q

08

3Q

09

3Q

10

3Q

11

3Q

12

3Q

13

3Q

14

3Q

15

3Q

16

3Q

17

3Q

18

Quarterly Rolling annual

Real Estate Summary Edition 4, 2018

Page 21 of 28

Overall, it is likely most investors are adopting a wait and see

approach. Rising bond yields will be on their minds as the

Federal Reserve and Bank of England (BoE) continue to tighten and the ECB prepares to phase out its quantitative easing

program. This led to October being one of the worst months

for equities since the financial crisis as rising bond yields led to a global sell-off. Real estate is similarly vulnerable to a higher

interest rate environment, and while there is as yet no

discernible upward pressure on yields investors will likely be feeling more apprehensive about the current levels of pricing

in the European market. A slight mitigation of this is that the

ECB (and to a lesser extent the BOE) are well behind the Federal Reserve in terms of monetary tightening. Also, factors

such as rental growth (real or anticipated) are driving property

returns and occupier markets are reasonably strong at present.

Nonetheless, considering prime office yields are now below

3% in some major cities, it would not take much of a shift to see some impact.

Viewpoint Trade Wars: the view from Europe

As detailed above (see Figure 1), 2018 has been the year

Donald Trump's rhetoric about tariffs has been ramped up and begun to impact supply chains. The acrimony between

the two countries is about more than tariffs; the resentment

has to do with alleged intellectual property theft, forced technology transfers and a good old fashioned rivalry between

the current world hegemon and the rising one. This topic is

too lengthy to discuss here, but escalating tensions will have some immediate consequences for real estate.

Europe, as an exporting continent, is likely to suffer from any impediments to free trade. UK car manufacturer Jaguar Land

Rover's recent production freeze was touted as a response to

Brexit, but in reality the cause was a fall in sales to China. Meanwhile, the disappointing outturn in Germany's GDP data

is heavily linked to a soft demand for its exports in China with

many producers complaining of weaker Chinese sales. It could be argued these issues relate more to an inevitable slowdown

in breakneck economic growth in China; however the trade

war will most definitely exacerbate this decline.

The capital account is also likely to take a hit. Chinese and

Hong Kong investors have been strong net buyers of European real estate, having invested over EUR 21.5 billion in

2017 alone. Chinese capital has shored up the London office

market since the EU referendum, accounting for a large share of some of the trophy office purchases and keeping volumes

at elevated levels. As detailed above (see Figure 12), 3Q has

seen a -54% decline in capital coming from China and a -61% decline in capital coming from Hong Kong, indicating

this important source of capital may be starting to dry up.

Again, in the instance of escalating tensions over trade, it is likely Chinese companies will be more nervous about foreign

assets or the Chinese government may look to restrict

outward investment.

The asset class likely to be most affected by this is logistics.

Domestic demand (especially e-commerce) has become a big

driver, however this still only accounts for a negligible share of warehousing overall (see Figure 13). To this end, occupier

demand will still be driven by external trade factors, especially

in Germany where car manufacturers account for a large share of the market. This raises several red flags for landlords

who have export-oriented tenants, as those covenants could

well be weakened by a protracted trade war.

This could also pose issues for industrial real estate from a

portfolio allocation perspective. Traditionally, the higher income return in logistics was compensation for the fact that

rental growth tended to be moderate and has consistently

underperformed inflation. As shown by the charts in the previous section, yields for logistics are at record lows. And

while rental growth has been higher than its historical average

it is not expected to surge significantly over the next five years. Should there also be a weaker demand environment, this

could put further downward pressure on rents.

Strategy

Notwithstanding the above, we are not recommending a sell-

off just yet. While a trade war is bad for everyone in the long term, Europe could perversely benefit from tariffs imposed on

US companies. This is already apparent in Asia where

Vietnamese companies are filling gaps left in the market by their Chinese counterparts. Real estate investors should simply

be more mindful of the risks surrounding manufacturing

tenants and assessing how reliant an asset's location is on a particular industry. Careful underwriting is more important

than ever (considering the already stretched valuations in the

logistics sector) as a dip in demand for exports may just be the straw that breaks the industrial camel's back.

Figure 13: Share of industrial floorspace by occupier

type (%)

Source: Prologis, 2017

0 5 10 15

Home Goods

Packaging/Plastics

Construction

Healthcare/Pharma

Transport/Freight

Industry/Machinery

Diversified Retailer

Apparel

Food & Beverage

Auto & Parts

Consumer Products

Electronics/Appliances

Real Estate Summary Edition 4, 2018

US summary

Major US property sectors are more than two years into a period of income-driven returns with one exception. The industrial sector claimed the highest returns of the major US property sectors in 2018 with more than half of the return coming from capital appreciation. With capital market pressures building, it is likely that returns will settle down somewhat in 2019. Demand is still strong, reflecting positive economic and labor market conditions and should continue to drive income growth in excess of inflation.

Real Estate Summary Edition 4, 2018

Page 24 of 28

US Summary Real estate fundamentals Overall, US commercial real estate performance remains true to our expectation for steady, income-driven returns. The

industrial sector is the only sector experiencing meaningful

Cap Rate compression, leading to outsized appreciation, (see Figure 14). Office and multifamily appreciation is in-line with

inflationary levels, which results in a total return reflective of a

long-term expectation. Retail depreciated recently, meaning that retail return is positive but below its income return. The

mall segment, which comprises approximately half of the

value of the retail component of the NCREIF Property Index, is responsible for most of the weakness.

Pressure is building in the capital markets as interest rates are increasing, pushing up the cost of debt and pushing down the

spread available on real estate investments. Commercial real

estate can and has operated in a reduced spread environment, as long as income and economic growth remain supportive of

strong cash flows. Real estate performance responds to the

fundamentals and expectations for fundamental growth.

Currently, income growth is strong, and we expect positive conditions in the economy and labor markets to continue to

support fundamentals.

As the Fed raises short-term rates, the market is putting

upward pressure on long-term rates, leading to a flatter yield

curve. Even after seven years of a flattening yield curve in the 1990s and three years of a flat yield curve in the mid-2000s,

US real estate generated positive quarterly total returns until

the recession of 2008, as real estate investors continued to benefit from income-driven performance

US equity market volatility increased in late 2018, including

periods of correction. There is no immediate implication for

the private US real estate sector from the public market

volatility, however, as investors we should be mindful of changes in the investment environment.

When looking at real estate revenue in relation to occupancy and rents, occupancy rates are high relative to the past 10

years. With the exception of the industrial sector, occupancy

faces a small degree of downward pressure with supply growth matching or exceeding demand. As there is little room

to increase occupancy, rent growth (see Figure 15), is the

driving force behind income gains. Economic conditions create some optimism that growth will continue to reflect positive

momentum for the US.

Figure 14: US real estate returns across property types - Rolling four-quarter total return (%)

Source: NCREIF Property Index, September 2018

Figure 15: Property sector rent growth - Year-over-year change (%)

Sources: Axiometrics; CBRE-Econometric Advisors, September 2018

-30

-20

-10

0

10

20

30

4Q08 2Q09 4Q09 2Q10 4Q10 2Q11 4Q11 2Q12 4Q12 2Q13 4Q13 2Q14 4Q14 2Q15 4Q15 2Q16 4Q16 2Q17 4Q17 3Q18

Apartments Industrial Office Retail

0

1

2

3

4

5

6

7

3Q14 3Q15 3Q16 3Q17 3Q18

Apartment Industrial Office Retail

Real Estate Summary Edition 4, 2018

Page 25 of 28

Apartments

Apartment vacancy rates have trended lower over the past

three quarters, even as new construction reached a peak point. At 4.2%, vacancy remains below the 20-year average

of 5.4%. Rent growth is above inflation at 4.3% in the year

ended September 2018 per Axiometrics.

US homeownership was fairly flat near 64.4% during the first

three-quarters of 2018, representing an anticipated pause in a two-year trend of increasing homeownership. Strength in the

labor market and steady household formation help offset a

renewed consumer preference for homeownership, leading to sustained demand for institutional multifamily rentals.

Industrial

Growth in net rents is strong but decelerating as supply

increases. Rents grew by 5.4% in the year ended September

2018 compared to 7.5% growth in the year ended September 2017.

Industrial availability was 7.1% in 3Q18, down a total of 30 bps from year-end 2017, as low as it has been since 1Q01.

We anticipate 2018 will be another good year for US

industrial. As we progress into 2019, the sector will have to contend with higher construction levels, (see Figure 16), which

could bring strong rent growth figures down toward

inflationary levels.

Office

Three quarters into 2018, deliveries of new office buildings

remain elevated, especially in technology related sectors and secondary markets. At 1.9%, office rent growth

underperformed inflation during the year ended September

2018 with downtown rents growing at half the pace of suburban office's 3.1% rent growth.

Average office vacancy decreased 10 bps over the year ended September 2018. The gap between downtown office vacancy

at 10.5% and suburban vacancy at 14.1% remains wide.

Downtown locations are likely sacrificing some rent growth to keep space occupied.

Retail

Consumer spending is up due to increased disposable income

and low unemployment, which should support retail sales in

2018. Sales in brick and mortar stores increased by 4.9% during the year ended August 2018.

The mall/lifestyle and power center segments are facing higher availability of 5.8% and 6.8%, respectively. Rent growth is

volatile as landlords compete for tenants. Stability in high-

quality properties is likely offset by deterioration in others. At 9.1%, availability in Neighborhood, Community and Strip

(NCS) retail is down 40 bps since the end of 2017. Rent

growth was just above inflation at 2.8% in the year ending September 2018.

Figure 16: Supply trends - Year-over-year completion rate (%)

Sources: Axiometrics; CBRE-Econometric Advisors, September 2018. Supply is shown as a completion rate (i.e. completions as a percent of existing inventory). Shaded area indicates forecast data.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Apartment

17 18 19 17-yr avg

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Industrial

17 18 19 20-yr avg

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Office

17 18 19 20-yr avg

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Retail

17 18 19 20-yr avg

Real Estate Summary Edition 4, 2018

Page 26 of 28

Capital markets US commercial real estate is now nearly three years into a period of sustainable, income-driven returns. Historically, the

income return component generated 70% to 90% of

property-level total return in the US. Unlevered property returns have been between 1.5% and 2.0% per quarter since

mid-2016. 3Q18 saw the NCREIF Property Index rise by 1.7%,

(see Figure 17), with more than 60% of that return coming from income.

US transaction markets remain liquid in aggregate with the

absolute volume of sales at USD 473 billion for the year ended

September 2018, (see Figure 18). After slowing a bit in 2016 and 2017, sales volume showed signs of leveling off during

the first three-quarters of 2018 with total volume up by USD

18 billion compared to the first three-quarters of 2017. Broad trends remain similar to 2017 with sales of retail and office

properties decreasing over the year and sales of apartments,

industrial and hotels increasing.

Figure 17: US property returns (%) Figure 18: US transactions - Transaction volume (USD

billions)

Source: NCREIF Property Index, September 2018 Source: Real Capital Analytics, September 2018

One reason transaction volume is lower for retail and office is that lenders have a higher debt appetite for industrial and

apartment assets. Real estate debt capital is low cost and

generally available but not free-flowing, a situation that arose prior to the last downturn. Increasing interest rates compress

spreads available to lenders in a competitive marketplace. The

spread between property yields and the cost of debt further compressed in early 2018. On the whole, US debt markets can

be described as operational, but not excessive, which

encourages development but not an abundance of supply.

Long-term interest rates remain low relative to US history even

as those rates moved higher in 2018. The 10-year US Treasury

rate was 2.4% at the end of 2017 but rose 50 bps over the

first two months of 2018. As of early November 2018, the 10-

year US Treasury remains above 3.0%.

With little movement in Cap Rates, the upward move in

Treasury rates condensed spreads available in US real estate (see Figure 19). Recent spreads offered by real estate

investments are below long-term expectations, representing a

change from the wide spreads that drew capital so quickly in the wake of the last recession. This in turn relieved one of the

pressures that had been pushing Cap Rates lower.

While the real estate spread is well-above historic lows, it is already low enough to be putting upward pressure on Cap

Rates, even though Cap Rates appear to be holding flat near

historic lows. There is no noticeable distress in the market that might put stronger upward pressure on Cap Rates. Income is

growing, while potential sellers can afford to be patient. Debt

is available, and capital expenditures are increasing.

Figure 19: Commercial real estate spread (basis points)

Sources: NCREIF Fund Index, Open-end Diversified Core Equity; Moody's Analytics, September 2018.

0.0

1.0

2.0

3.0

4.0

5.0

1Q11 2Q12 3Q13 4Q14 1Q16 2Q17 3Q18

Income return Appreciation return

0

100

200

300

400

500

2012 2013 2014 2015 2016 2017 2018YTD

Apartment Industrial Office Retail Hotel

0

100

200

300

400

500

1Q97 1Q00 1Q03 1Q06 1Q09 1Q12 1Q15 3Q18

Spread (cap rate minus 10-year Treasury rate)

20-year average spread

Real Estate Summary Edition 4, 2018

Page 27 of 28

A growing economy and tight labor market should continue

to generate the demand for real estate, further supporting

income growth. Realized and expected growth in real estate income has directly offset the upward pressure on real estate

Cap Rates from the tight spread. Current economic expansion

is considered to be self-sustaining at or above the long-term average, with US GDP increasing by 3.5% during 3Q18 (see

Figure 20).

Figure 20: US real GDP growth - Real GDP growth (%)

Source: Moody's Analytics, September 2018

In September 2018, the unemployment rate was 3.7%,

continuing downward movement. A tight labor market

generally makes it tougher to fill open positions and has put slow, upward pressure on wage inflation. Job growth has

been bumpy but strong (see Figure 21). Over the past year,

average monthly job gains exceeded 200,000 per month.

The tight labor market is one reason wage growth is expected

to continue to accelerate in the US. Higher wages and consumer spending should reinforce expectations for more

inflation. Over the year ended September 2018, consumer

price inflation was 2.3% in the US. A strong labor market implies that consumers should continue to spend on retail

purchases and afford increases in rental rates.

Figure 21: US job growth and unemployment rate (%)

Change in employment (thousands of jobs)

Source: Moody's Analytics, 2 November 2018

The labor market is strong enough, and inflation is just high

enough to justify expectations for continuing the Fed's

monetary tightening through the balance of the year. In September 2018, the Fed increased the target range for the

short-term Federal Funds Rate (2% to 2.25%). Another 25

bps increase in the short-term rate is expected in December 2018 and is already priced into the market.

Even as capital markets face some pressure on spreads and the cost of debt, fundamental strength in the US economy,

labor market and confidence measures support relatively good

occupancy rates and continued rent growth in the real estate sector.

Strategy viewpoint US properties are appreciating at about the pace of inflation.

Appreciation now relates back to the positive rent growth

generated by properties, as opposed to the outsized influence of capital flows the US experienced in 2014 and 2015.

Beginning in early 2016, US real estate entered a widely-

anticipated period of income-driven performance.

Looking more closely at the drivers of income, rent growth is

the true powerhouse behind the gains. A continued positive outlook for economic growth reinforces our view that

property-level income growth should outpace inflation even as

the pace of growth moderated in recent years. Income-generated performance is consistent with a long-term

expectation for private commercial real estate.

As anticipated, interest rates rose in 2018 condensing the

spread available on real estate. Cap Rates are not currently

increasing in most property sectors; however, we expect a small upward movement over the coming year.

Capital investment into stabilized assets is increasing, an expected outcome in a long expansion. Debt and equity

capital is seeking growth strategies, and existing assets are

under some pressure to compete with new construction.

Investors should pay careful attention to the risk-return

expectations for incremental capital. A low return environment with excess capital competing for a small number

of value-add deals can quickly become hostile.

We expect markets to continue on a stabilized path, which

will likely result in a continued convergence of expected

performance and, relative to past years, limit the investment opportunities that seem obvious. In light of this, diversification

will grow in importance.

-4

-2

0

2

4

6

3Q09 1Q11 3Q12 1Q14 3Q15 1Q17 3Q18

Quarterly annualized Annual growth

4.0

5.0

6.0

7.0

8.0

0

100

200

300

400

May-14 Mar-15 Jan-16 Nov-16 Sep-17 Oct-18

Job growth (L) Unemployment rate (R)

Page 28 of 28

For more information please contact UBS Asset Management

Real Estate & Private Markets (REPM)

Research & Strategy

Paul Guest

+44-20-7901 5302 [email protected]

Follow us on LinkedIn

www.ubs.com/repm-research

This publication is not to be construed as a solicitation of an offer to buy or sell any securities or other financial instruments relating to UBS AG or its affiliates in Switzerland, the United States or any other jurisdiction. UBS specifically prohibits the redistribution or reproduction of this material in whole or in part without the prior written permission of UBS and UBS accepts no liability whatsoever for the actions of third parties in this respect. The information and opinions contained in this document have been compiled or arrived at based upon information obtained from sources believed to be reliable and in good faith but no responsibility is accepted for any errors or omissions. All such information and opinions are subject to change without notice. Please note that past performance is not a guide to the future. With investment in real estate/infrastructure/private equity (via direct investment, closed- or open-end funds) the underlying assets are illiquid, and valuation is a matter of judgment by a valuer. The value of investments and the income from them may go down as well as up and investors may not get back the original amount invested. Any market or investment views expressed are not intended to be investment research. The document has not been prepared in line with the requirements of any jurisdiction designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The information contained in this document does not constitute a distribution, nor should it be considered a recommendation to purchase or sell any particular security or fund. A number of the comments in this document are considered forward-looking statements. Actual future results, however, may vary materially. The opinions expressed are a reflection of UBS Asset Management’s best judgment at the time this document is compiled and any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise is disclaimed. Furthermore, these views are not intended to predict or guarantee the future performance of any individual security, asset class, markets generally, nor are they intended to predict the future performance of any UBS Asset Management account, portfolio or fund. Source for all data / charts, if not stated otherwise: UBS Asset Management, Real Estate & Private Markets. The views expressed are as of November 2018 and are a general guide to the views of UBS Asset Management, Real Estate & Private Markets. All information as at November 2018 unless stated otherwise. Published November 2018. Approved for global use. © UBS 2018 The key symbol and UBS are among the registered and unregistered trademarks of UBS. Other marks may be trademarks of their respective owners. All rights reserved.