Embed Size (px)

Citation preview

Real EstateReal Estate Principles and Practices Principles and Practices

Chapter 16Chapter 16

Investment and Tax Aspects Investment and Tax Aspects of Ownershipof Ownership

© 2014 OnCourse Learning

© 2014 OnCourse Learning

Key TermsKey Terms

Adjusted basis

Basis

Cash flow

Corporations

Depreciation

Gain

General partnership

Installment sale

Joint venture

Leverage

Limited partnership

Negative cash flow

Partnership

Passive income

Prospectus

Real Estate Investment Trust (REIT)

S Corporation

© 2014 OnCourse Learning

Key TermsKey Terms

Salvage value

Securities and Exchange Commission (SEC)

Straight-line depreciation

Syndication

Tax-free exchange

Tax shelter

Useful life

© 2014 OnCourse Learning

OverviewOverview

Investing in a residenceAdvantages of homeownership as an investment

Investing in income-producing real estateBenefits to the real estate investor

© 2014 OnCourse Learning

Homeownership as an Homeownership as an InvestmentInvestment

Itemized deductions on taxes, mortgage interest for 1st and 2nd homes

2nd home: annual occupancy for at least 14 days or 10% of useful rental period

Equity loans

Tax Reform Act of 1986

© 2014 OnCourse Learning

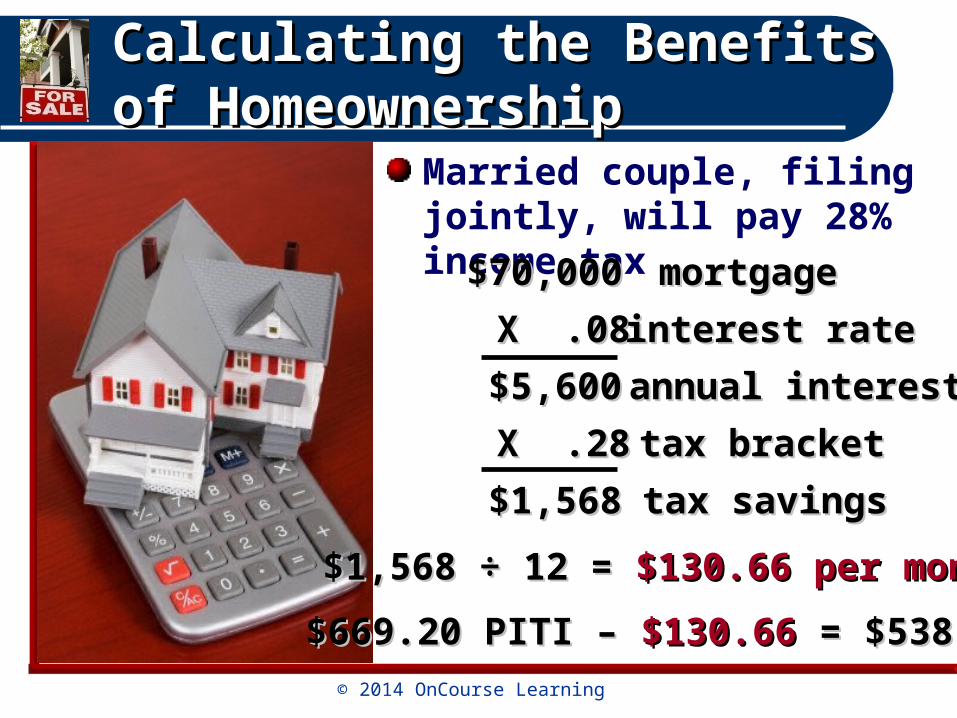

Calculating the Benefits of Calculating the Benefits of HomeownershipHomeownership

Married couple, filing jointly, will pay 28% income tax

$70,000$70,000 mortgagemortgage

X .08X .08 interest rateinterest rate

$5,600$5,600 annual interestannual interest

X .28X .28

tax savingstax savings

tax brackettax bracket

$1,568$1,568

$1,568 ÷ 12 = $1,568 ÷ 12 = $130.66 per month$130.66 per month

$669.20 PITI – $669.20 PITI – $130.66$130.66 = $538.54 = $538.54

© 2014 OnCourse Learning

Calculating the Benefits of Calculating the Benefits of HomeownershipHomeownership

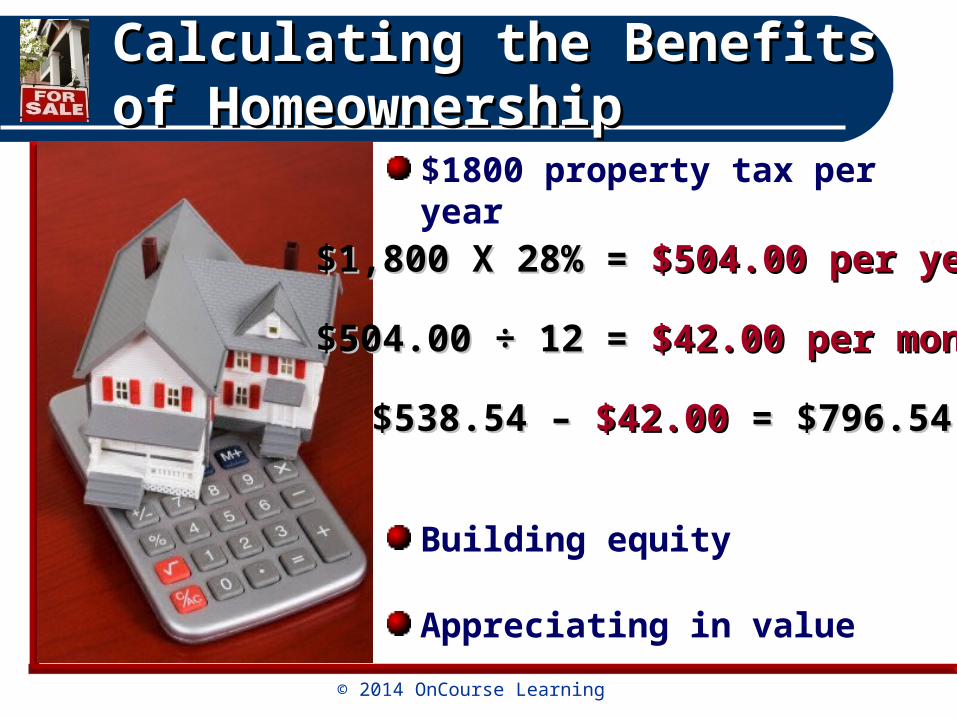

$1800 property tax per year

Building equity

Appreciating in value

$1,800 X 28% = $1,800 X 28% = $504.00 per year$504.00 per year

$538.54 – $538.54 – $42.00 $42.00 = $796.54= $796.54

$504.00 ÷ 12 = $504.00 ÷ 12 = $42.00 per month$42.00 per month

© 2014 OnCourse Learning

Appreciation and Appreciation and HomeownershipHomeownership

Rising construction and land cost

Supply of funds and market conditions

Demand for housing

Needs of each generation

© 2014 OnCourse Learning

Depreciation of a ResidenceDepreciation of a Residence

Depreciation not allowed for a residence

Exception: portion allowed for in home office

© 2014 OnCourse Learning

How Tax Provisions Affect How Tax Provisions Affect Sale of Principal ResidenceSale of Principal Residence

Excluded amount

$500,000 married filing jointly

$250,000 single return

May be claimed every 2 years

Death of spouse results in 2 year limit to maintain the $500,000 exclusion

© 2014 OnCourse Learning

How Tax Provisions Affect How Tax Provisions Affect Sale of Principal ResidenceSale of Principal Residence

Eligibility requirements:

1. Ownership: . Ownership: minimum 2 of the last 5 years

2. Use: Use: principal residence for at least 2 of the last 5 years

3. Waiting period: Waiting period: exclusion may not have been used for any sale during the past 2 years

© 2014 OnCourse Learning

How Tax Provisions Affect How Tax Provisions Affect Sale of Principal ResidenceSale of Principal Residence

Loss on sale is not deductible

Gain which exceeds the excluded amount is taxed as a capital gain

Rate of tax: 20% (10% for taxpayers in 15% bracket)

1. Assets sold after 7/28/87: 18 month holding period

2. Deprecation recapture: 25% rate

3. Maximum rate after 12/31/2000:18%

© 2014 OnCourse Learning

How Tax Provisions Affect How Tax Provisions Affect Sale of Principal ResidenceSale of Principal Residence

BasisBasis is adjusted:adjusted:Cost of new residence minus gaingain on old residence

$65,000$65,000 1990 Purchase price1990 Purchase price

1992 added family room1992 added family room8,5008,500

$73,500$73,500 Adjusted basisAdjusted basis

88,00088,000 2008 sale price2008 sale price

6,3306,330 Less selling expensesLess selling expenses

$81,670$81,670

© 2014 OnCourse Learning

How Tax Provisions Affect How Tax Provisions Affect Sale of Principal ResidenceSale of Principal Residence

BasisBasis is adjusted:adjusted:Cost of new residence minus gaingain on old residence

73,50073,500 Less adjusted basisLess adjusted basis

Gains from saleGains from sale8,1708,170

$95,000$95,000 New purchase priceNew purchase price

8,1708,170 Less gain from saleLess gain from sale

Adjusted basisAdjusted basis$86,830$86,830

$81,670$81,670

© 2014 OnCourse Learning

How Tax Provisions Affect How Tax Provisions Affect Sale of Principal ResidenceSale of Principal Residence

Calculate the purchase price

Rollover (IRS Form 2119: Sale of Your Home”)

Capital improvements are deductible

Costs of sale are deductible

Not tax deductable

Determining the Basis for Measuring Gain Determining the Basis for Measuring Gain

Selling at a LossSelling at a Loss

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

Reasons for investing in real estateAppreciation

Cash flow

Equity buildup

Tax shelter

Primary purpose: Generate income

Long term capital growth without risk

Purchasing Real Estate vs. Fixed Income InvestmentPurchasing Real Estate vs. Fixed Income Investment

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

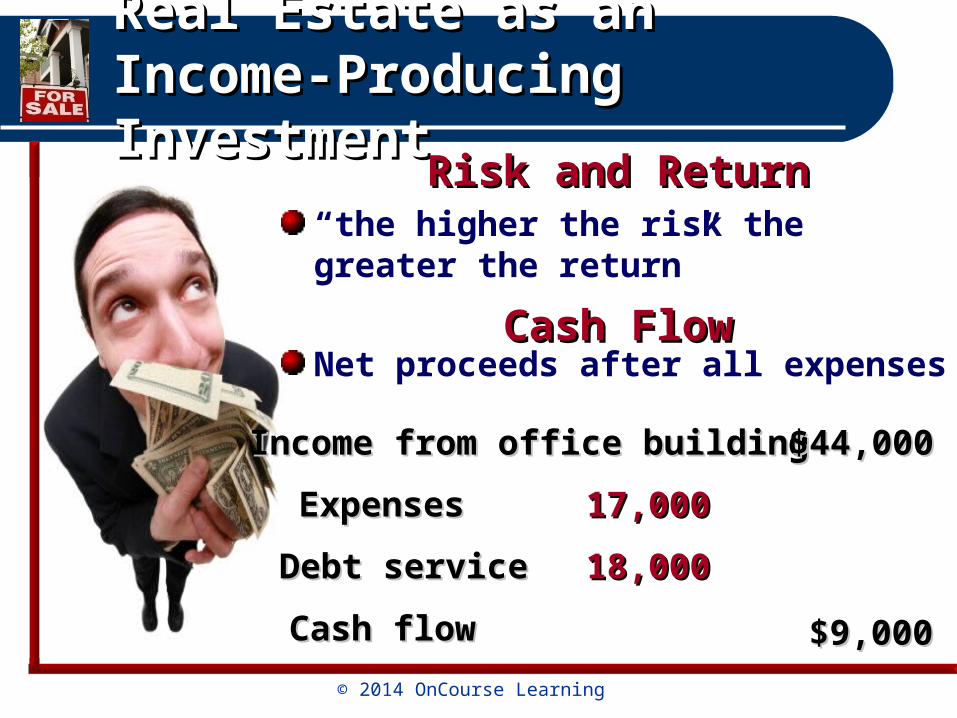

“the higher the risk the greater the return”

Net proceeds after all expenses

Risk and ReturnRisk and Return

Cash FlowCash Flow

Income from office buildingIncome from office building $44,000$44,000

ExpensesExpenses 17,00017,000

Debt serviceDebt service 18,00018,000

Cash flowCash flow $9,000$9,000

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

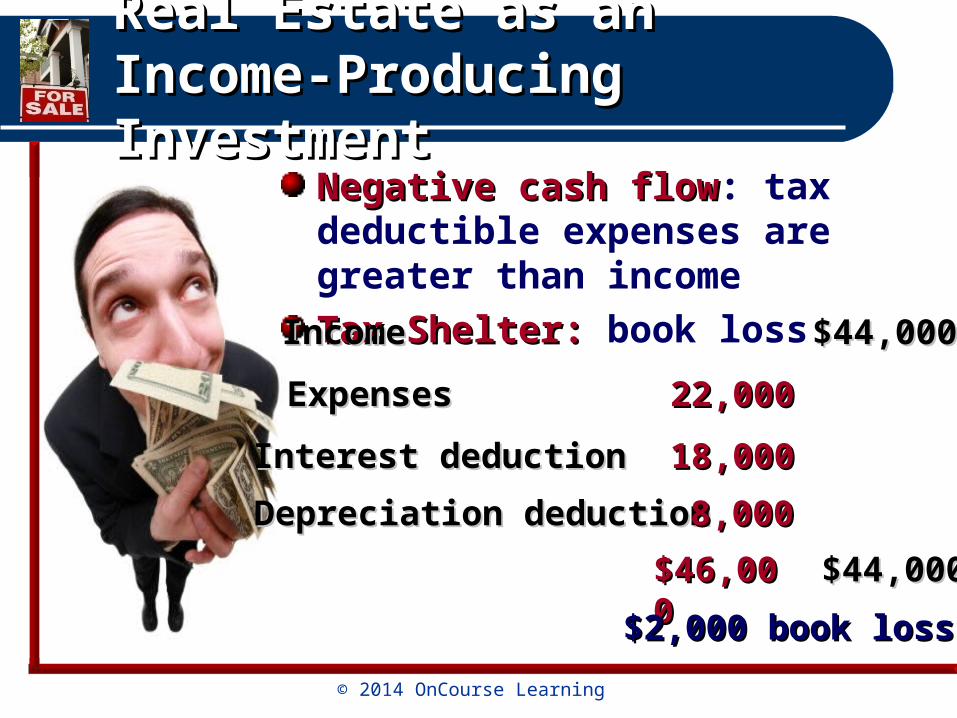

Negative cash flowNegative cash flow: tax deductible expenses are greater than income

Tax Shelter: Tax Shelter: book lossIncome Income $44,000$44,000

ExpensesExpenses 22,00022,000

Interest deductionInterest deduction 18,00018,000

Depreciation deductionDepreciation deduction

$44,000$44,000

8,0008,000

$46,000$46,000

$2,000 book loss$2,000 book loss

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

Passive income: Passive income: not containing the taxpayers’ active involvement

3 Classifications of income

Active incomeActive income

Portfolio incomePortfolio income

Passive activity incomePassive activity income

Losses up to $25,000 may be used to offset salaries and active business income

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

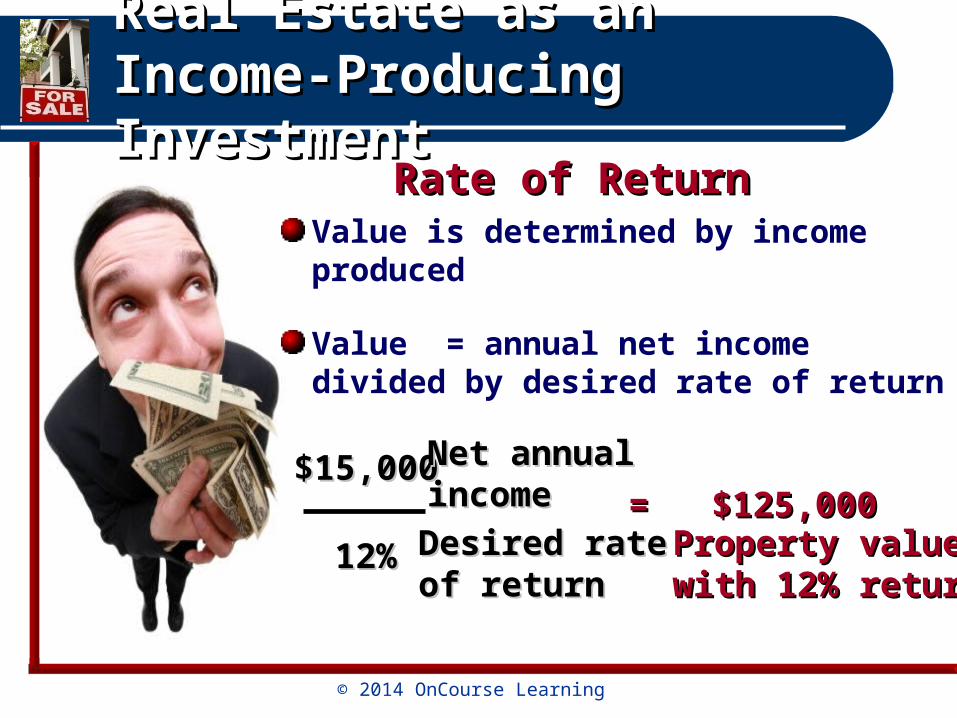

Value is determined by income produced

Value = annual net income divided by desired rate of return

Rate of ReturnRate of Return

$15,000$15,000 Net annual Net annual incomeincome

12%12% Desired rate Desired rate of returnof return

= $125,000= $125,000Property value Property value with 12% returnwith 12% return

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

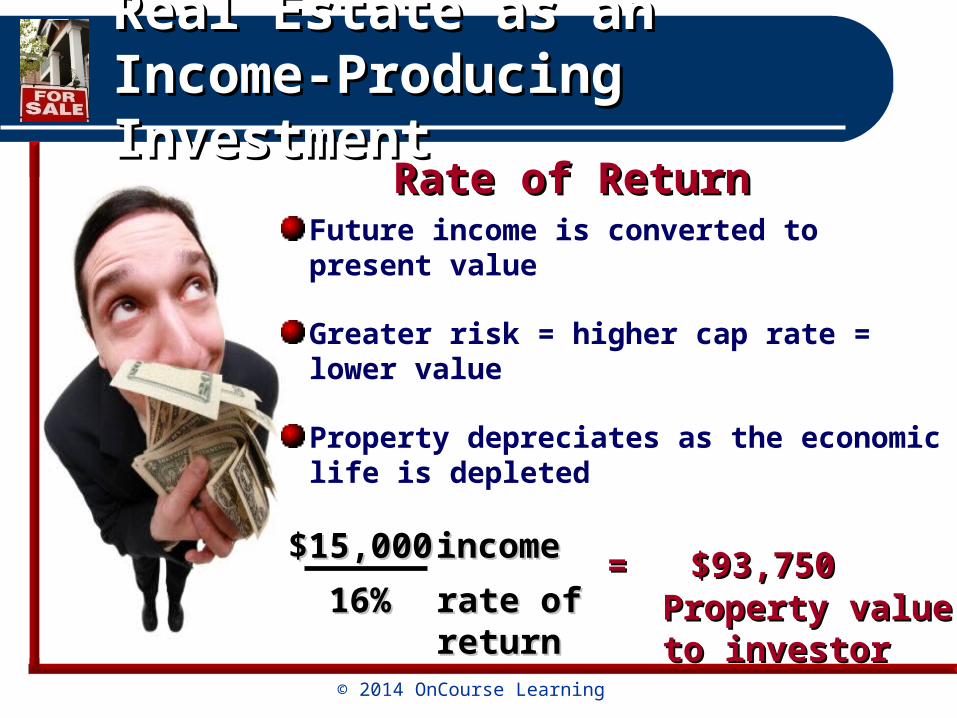

Future income is converted to present value

Greater risk = higher cap rate = lower value

Property depreciates as the economic life is depleted

Rate of ReturnRate of Return

$15,000$15,000 incomeincome

16%16% rate of returnrate of return= $93,750= $93,750

Property value Property value to investorto investor

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

Accounting concept for tax purposes

Estimates future decreases in value

Useful life: Useful life: economic life

Salvage value: Salvage value: value after useful life

DepreciationDepreciation

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

1981 – Tax Recover Act: “recovering the cost”

TRA 86: straight line depreciation straight line depreciation over 27 ½ years

Properties deprecate in equal installments over a predetermined period of time

Land does not depreciate

DepreciationDepreciation

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

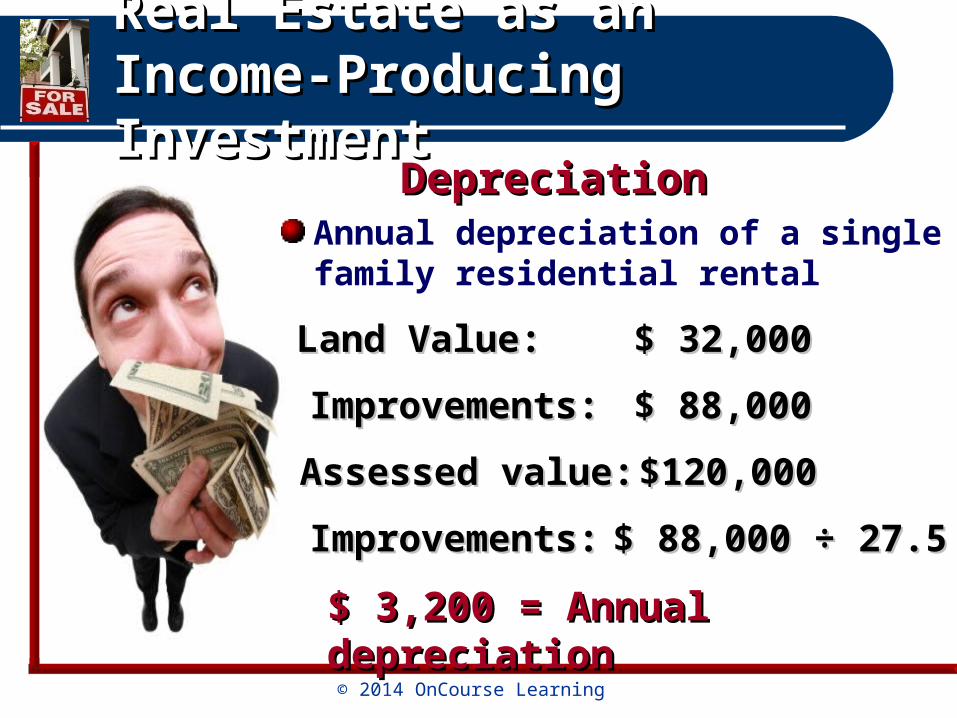

Annual depreciation of a single family residential rental

DepreciationDepreciation

Land Value: Land Value: $ 32,000$ 32,000

Improvements:Improvements: $ 88,000$ 88,000

Assessed value:Assessed value: $120,000$120,000

Improvements:Improvements: $ 88,000 ÷ 27.5$ 88,000 ÷ 27.5

$ 3,200 = Annual depreciation$ 3,200 = Annual depreciation

© 2014 OnCourse Learning

Real Estate as an Income-Real Estate as an Income-Producing InvestmentProducing Investment

2. Investment financed:

$125,000 investment$125,000 investment

$93,750 mortgage = $31,250 equity $93,750 mortgage = $31,250 equity invested invested

subtract one year’s interest at 10% from subtract one year’s interest at 10% from $15,000 income:$15,000 income:

$15,000 - $9,375 = $5,625 net income$15,000 - $9,375 = $5,625 net income

$5,625 ÷ 31,250 = 18% annual return$5,625 ÷ 31,250 = 18% annual return

LeverageLeverage

© 2014 OnCourse Learning

Investment OpportunitiesInvestment Opportunities

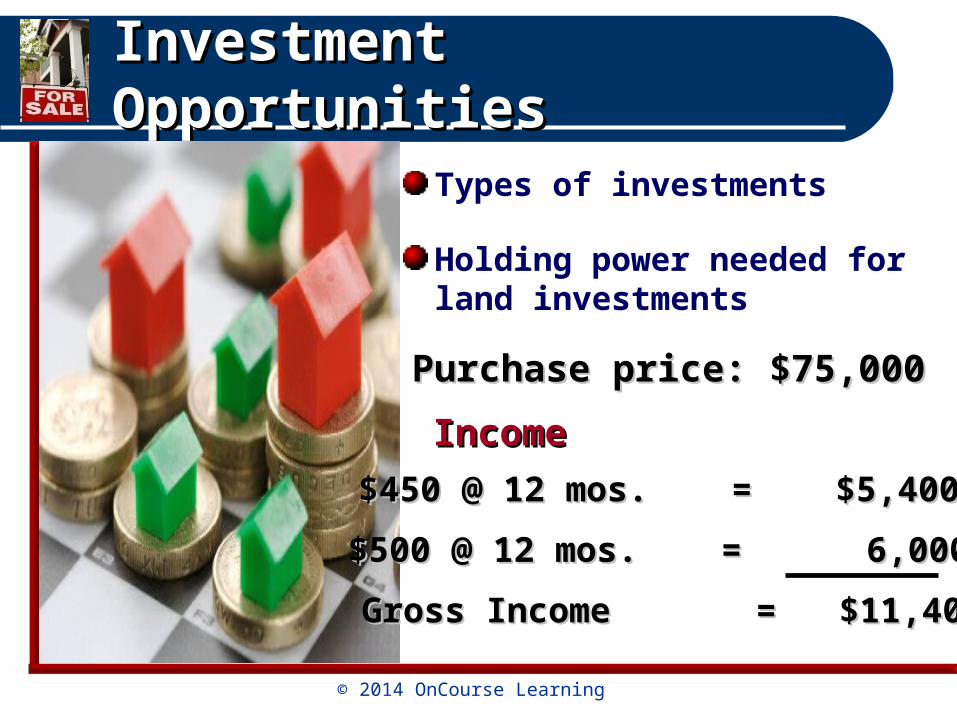

Types of investments

Holding power needed for land investments

IncomeIncome

Purchase price: $75,000Purchase price: $75,000

$450 @ 12 mos. = $5,400.00$450 @ 12 mos. = $5,400.00

$500 @ 12 mos. = 6,000.00$500 @ 12 mos. = 6,000.00

Gross Income = $11,400.00Gross Income = $11,400.00

© 2014 OnCourse Learning

Investment OpportunitiesInvestment Opportunities

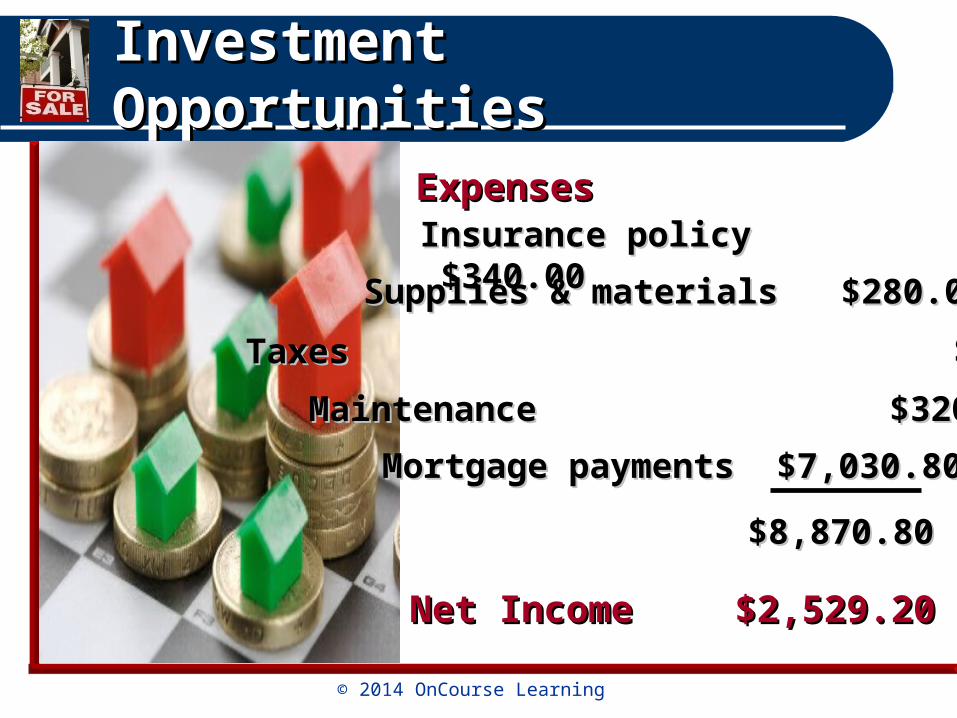

ExpensesExpensesInsurance policy $340.00Insurance policy $340.00

Supplies & materials $280.00Supplies & materials $280.00

TaxesTaxes $ $900.00900.00

Maintenance $320.00Maintenance $320.00

Mortgage payments $7,030.80Mortgage payments $7,030.80

Net IncomeNet Income

$8,870.80$8,870.80

$2,529.20$2,529.20

© 2014 OnCourse Learning

Investment OpportunitiesInvestment Opportunities

The Investment Scenario

Rehabilitation Tax Credit

Refinancing vs. Selling

Tax-Deferred Exchanges

Installment Sales

© 2014 OnCourse Learning

Group Business VentureGroup Business Venture

General partnership

Limited partnership

Corporation

S Corporation

Syndication

REITs

© 2014 OnCourse Learning

Real Estate Offerings as Real Estate Offerings as SecuritiesSecurities

Real estate purchased for investment is considered a security

Securities Act of 1933 – 4 elements of an “investment contract”

1. Investment of money

2. Common enterprise

3. Undertaken for prospect of a profit

4. Profit derived from management efforts of others

© 2014 OnCourse Learning

Real Estate Offerings as Real Estate Offerings as SecuritiesSecurities

Purpose of Securities Act: full and fair disclosure

Prospectus: Prospectus: disclosure of basic information of the enterprise

Exception for interstateinterstate

Blue sky laws: Blue sky laws: securities license required