Embed Size (px)

Citation preview

OVERVIEW

Sublease Space Spills Back Over 9.0 Million SF The Houston office sector is off to a slow start in 2018 as the market continues to find its footing following the energy downturn and recent construction cycle. Direct vacancy and availability rates both saw increases over the quarter. Vacancy rate increases were due to a combination of downsizing tenants, subleases expiring and tenants vacating direct space for sublease alternatives. Availability was pushed upwards by new sublease offerings on the market. After dropping to 8.7 million SF, sublease space spilled back over 9.0 million SF in the first quarter as Technip put up 375,000 SF (Energy Corridor) and Hess Energy added 123,000 SF (CBD) as the year ended. Additional energy related sublease offerings are anticipated to come online as the year progresses.

The first quarter saw several large renewals, led by Apache's extension of 524,000 SF in Post Oak Central, further postponing any potential for their long-discussed build-to-suit project. Also of note, Williams renewed for 353,944 SF in Williams Tower (Galleria/Uptown). Market fundamentals are likely to soften further through the first half of the year as additional fallout continues to avail itself. However, an uptick in the second half of the year is anticipated as sustained oil prices begin to translate into job growth. Furthermore, the long-term outlook on Houston remains bright, underscored by the heightened level of investor activity in the market.

HOUSTON OFFICE MARKETFIRST QUARTER 2018

REAL ESTATE OUTLOOK

Office Market Off to a Slow Start in 2018Direct Vacancy and Sublease Supply Rise

NET ABSORPTION AND VACANCY RATE TRENDS HOUSTON METRO AREA

CONTIGUOUS BLOCKS OF AVAILABLE SPACE HOUSTON METRO

SOURCE CoStar, Transwestern *Through Q1 2018

SOURCE CoStar, Transwestern *At Q1 2018

Note: Delivery of preleased space counts as positive net absorption

Notable Q1 LeasesTENANT SF LEASE TYPE BUILDING SUBMARKET

Apache Corporation 524,342 Lease Extension 1990 & 2000 Post Oak Blvd Galleria/Uptown

Williams 353,944 Renewal Williams Tower Galleria/Uptown

Dashiell Corporation 79,308 Renewal/Expansion 12301 Kurland Dr Gulf Freeway/Pasadena

Hunting Energy Services 62,137 Renewal 16825 Northchase Dr Greenspoint/N Belt West

PFS Group 54,891 Renewal 2600 N Loop Fwy W North Loop West

NextEra Energy 50,283 Renewal 601 Travis CBD

-4000-3000-2000-1000

010002000300040005000600070008000

Net Absorption

18*17161514131211100908075%

10%

15%

20%

25%Total AvailabilityDirect Vacancy

In Th

ousa

nds

0

50

100

150

200Class A SubletClass A Direct

200,000 SF100,000 SF50,000 SF25,000 SF

Class B SubletClass B Direct

NET ABSORPTION

Absorption Stays in the RedThe office market continues to experience fallout from the energy downturn with negative absorption of 946,738 SF for all classes of space over the first quarter. Class A absorption was negative 343,853 SF and Class B space recorded negative 549,406 SF. There were several large move outs that occurred during the first quarter that drove negative absorption. United Airlines vacated 200,000 SF (1801 Smith, CBD) followed by NRG at 145,000 SF (1000 Main, CBD), Baker Hughes at 128,000 SF (America Tower, Midtown) and Cameron at 128,000 SF (Westway One, West Belt). The first half of 2018 is likely to experience additional negative absorption as 1.0 million SF of sublease space is set to expire over the balance of 2018. It is anticipated that absorption will start to see a rebound in the second half of the year as higher energy trading prices begin to result in office using job growth.

DIRECT VACANCY & TOTAL AVAIL ABILIT Y

Hess and Technip Push Availability UpwardsThe overall office availability rate (all space marketed as available for lease, both direct and sublet) increased 0.5% over the quarter, closing Q1 at 23.2%. After seeing a decrease in sublease space towards the end of the year, sublease space jumped back over 9.0 million SF at the close of the first quarter. This was driven by Technip listing 375,000 SF of space on the sublease market in Energy Tower II (Katy Freeway West, Class A) and Hess putting an additional 123,000 SF online in 1501 McKinney (CBD, Class A). Class A availability was 25.1%, up from 24.1% at the close of 2017 and Class B total availability was 21.7%, unchanged quarter-over-quarter.

Overall direct vacancy saw a 0.5% increase over the quarter ending at 15.9%. Class A direct vacancy closed the quarter at 15.8%, up 0.5% over the quarter. Class B direct vacancy increased by 0.6% over the same period, ending the first quarter at 16.9%. With 1.0 million SF of sublease space set to expire by the end of 2018, direct vacancy will continue to increase over the course of the year.

RENTAL R ATES

Rents Increase Over Q1Overall asking rates for the Houston metro area increased slightly over the quarter to $30.99 PSF full service as compared to $30.66 PSF full service at the end of 2017. Rental rates for both classes of space saw an increase in the first quarter. Class A rental rates increased 1.1% to $36.26 PSF full service and Class B rates increased 0.3% to $21.81 PSF full service. Despite the recent increases in rental rates, the market remains in the tenants favor as generous concession packages continue to be offered. The submarkets with the highest full service asking rents are the Central Business District (Class A - $44.64 PSF), Katy Fwy East (Class A, $40.77 PSF), and Greenway Plaza (Class A - $39.60 PSF). The most value friendly Class A submarkets include Northwest Far ($19.58 PSF), Southwest/Hillcroft ($19.89 PSF) and Southwest/Beltway 8 ($21.10 PSF).

Office Under ConstructionHouston Metro | Q1 2018

SUBMARKET NUMBER OF BLDGS SF % PRE-

LEASED

CBD 1 778,344 32%

Woodlands 3 704,800 97%

Total 4 1,483,144 63%

AVERAGE OFFICE RENTS HOUSTON METRO AREA

SOURCE CoStar, Transwestern *Through Q1 2018 Note: All classes of office space

Total Available SpaceHouston Metro | Q1 2018

SUBMARKETSUBLEASE SPACE (SF)

% OF SUPPLY

% OF TOTAL AVAILABLE

CBD 2,186,786 5.0% 18.0%Katy Fwy/Energy Corridor 2,584,916 7.1% 27.7%

Westchase 1,353,204 7.7% 26.4%

West Loop 885,406 2.6% 12.2%

N Houston District 687,027 6.8% 11.4%

All of Houston 9,059,105 3.8% 16.1%

$15

$20

$25

$30

$35

$40Class BClass AOverall

18*1716151413121110090807

2 REAL ESTATE OUTLOOK HOUSTON METRO Q1 2018

HOUSTON METRO MARKETFIRST QUARTER 2018

SUPPLY AND DEVELOPMENT

Build-to-Suit Projects Driving ActivityConstruction activity continues to dwindle in the Houston market following the close of the recent development cycle. High availability and increasing vacancy have developers hesitant to build without a significant prelease commitment. At the close of the first quarter, the construction pipeline totaled 1.5 M SF as 63% preleased. Currently, there are four developments under construction which include Capitol Tower (CBD, 778,000 SF - 32% leased to Bank of America and Quantum Energy), CityPlace 2 (The Woodlands, 326,000 SF - 100% Leased to ABS) and HP's Build-to-Suit Campus (The Woodlands, two-189,000 SF buildings).

Three deliveries occurred in the first quarter, the most notable of these was the Kirby Collection, a 246,989 SF mixed-use property in Greenway Plaza delivered at 44% preleased. Tillman Fertitta’s, The Post Oak a 104,579 SF mixed-use property in Galleria/Uptown delivered at 68% preleased. Also of note, Grandway West IV a 72,045 SF building in Katy Far West delivered at 93% preleased. Despite the vast amount of space on the market, potential exists for an additional 3-4 buildings to break ground over the year as tenants remain enamored with new construction given the efficiencies, amenities and ability to impact employee retention.

INVESTMENT MARKET

Investors Keep Eyes on Houston Sales were robust for the quarter totaling $715.7 million, driven largely by the closing of several notable portfolio sales. Brookhollow Central (3-building campus totaling 797,971 SF) was purchased by Hertz Investment Group for approximately $70.5 million. Other notable transactions include, Loop Central's acquisition by Griffin Partners (3-building portfolio totaling 575,000 SF, undisclosed price) and The Offices at Pin Oak Park's acquisition by Norvin Healthcare Properties (5-building portfolio totaling 504,721 SF, $110.0 million). These figures represent assets for which pricing information could be obtained.

COMPARATIVE OFFICE INVESTMENT SALES VOLUME SELECT METRO AREAS

SOURCE Real Capital Analytics, Transwestern ,*Through Q1 2018

AVERAGE OFFICE SALE PRICE HOUSTON METRO AREA

SOURCE Real Capital Analytics, Transwestern,*Through Q1 2018

Notable Q1 TransactionsBUILDING SUBMARKET SF SALE PRICE SELLER BUYER

Brookhollow Central(3-bldg Campus) North Loop West 797,971 $70,500,000 Parmenter Realty Partners Hertz Investment Group

Loop Central(3-bldg Campus) Bellaire 575,000 N/A TIER REIT Griffin Partners

The Offices at Pin Oak Park (5-bldg Campus) Bellaire 504,721 $110,000,000 Griffin Partners Norvin Healthcare Properties

One Northwest Centre Northwest Far 151,835 N/A Boxer Property ManhattanLife

SOURCE Real Capital Analytics, Costar, Transwestern

Sales

Volu

me i

n Billi

ons

$0

$1

$2

$3

$4

$5

$6

$7

$8HoustonDenverDallasAtlanta

18*1716151413121110090807

$0

$50

$100

$150

$200

$250 Average Sale Price Per SF

18*1716151413121110090807

REAL ESTATE OUTLOOK HOUSTON METRO Q1 2018 3

Investors are maintaining a watchful eye on the Houston office market as the long-term outlook of the city is highly desirable. Of particular interest are well located urban infill properties that can be renovated to compete alongside new construction. While distressed assets are always of interest to investors, this ownership cycle has been well capitalized and able to weather the downturn. However, as sublease space converts to direct space pushing vacancy ever higher, fatigue could begin setting in.

OUTLOOK

Despite Speed Bumps, Future Still BrightThe Houston office market has had its fair share of turbulence over the past few years as it begins to recover from the impacts of a hurricane and the downturn of the energy market. The Houston economy has seen diversification outside of the energy sector resulting job growth, but it hasn't translated to office using employment. However, with energy prices sustaining in the low-mid $60s and the professional and business services sector picking up steam (9,700 jobs created in the first two months of 2018), the office sector could begin to experience a slow and measured recovery starting in the second half of 2018 and on into 2019.

While office market fundamentals may weaken in the short term with over 1.0 million SF of sublease space set to expire, the long term outlook for the Houston market remains strong. This prognosis is underscored by the heightened investment activity in the market with major transactions such as Houston Center, Brookhollow Central and Greenway Plaza changing hands. Look for job growth to become more robust throughout the year with office using employment trending upwards in the second half. As it stands several employers are already in expansion mode such as Amazon, SABIC, Zenith Energy and KPMG. Look for this list to increase as more companies right their books on the backs of $60 oil.

Multi-tenant market vs Transwestern comprehensive market coverage

MULTI-TENANT ENTIRE MARKET

Inventory 198.6 MSF 241.0 MSF

Total Availability 22.0% 23.2%

Q1 2018 Net Absorption (813,083) SF (946,738) SF

WHY OUR METHODOLOGY IS THE BEST INDICATOR OF CURRENT MARKET CONDITIONSWe include owner occupied and single-tenant buildings in our inventory, vacancy and absorption statistics to capture more market activity than many of our competitors. This allows us to better correlate changes in the market with changes in employment. As single-tenant space does compete with multi-tenant space, we believe it is critical to understand all components of the market. The inclusion of single-tenant and owner-occupied space tends to yield lower vacancy rates and higher absorption totals than some of our competitors’ results, but our coverage of the market is more comprehensive.

OFFICE ABSORPTION AND EMPLOYMENT HOUSTON METRO AREA

SOURCE Bureau of Labor Statistics, Transwestern *12-month job growth through Feb 2018, net absorption YTD through Q1 2018

-4000

-2700

-1400

-100

1200

2500

3800

5100

6400

7700

9000Net Absorption (Thousands of SF)

18*1716151413121110090807-80

-60

-40

-20

0

20

40

60

80

100

120Payroll Job Growth (in Thousands)

4 REAL ESTATE OUTLOOK HOUSTON METRO Q1 2018

HOUSTON METRO MARKETFIRST QUARTER 2018

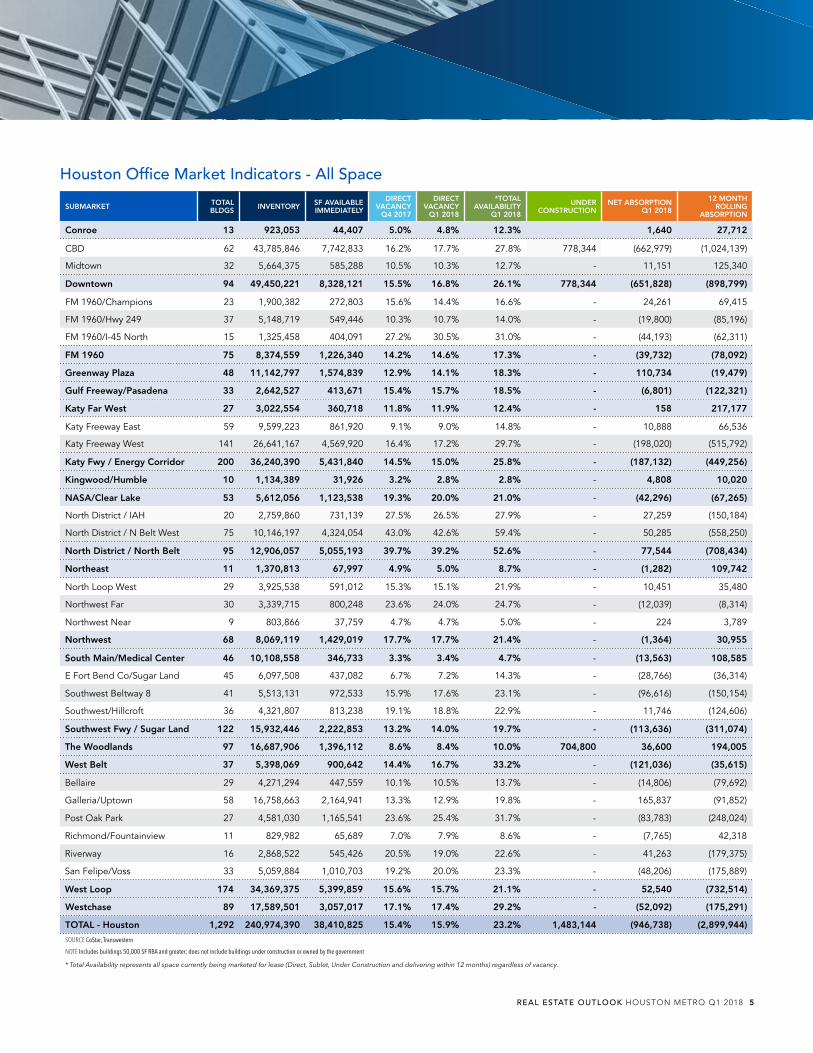

Houston Office Market Indicators - All Space

SUBMARKET TOTAL BLDGS INVENTORY SF AVAILABLE

IMMEDIATELY

DIRECT VACANCY

Q4 2017

DIRECT VACANCY

Q1 2018

*TOTAL AVAILABILITY

Q1 2018

UNDER CONSTRUCTION

NET ABSORPTION Q1 2018

12 MONTH ROLLING

ABSORPTION

Conroe 13 923,053 44,407 5.0% 4.8% 12.3% 1,640 27,712

CBD 62 43,785,846 7,742,833 16.2% 17.7% 27.8% 778,344 (662,979) (1,024,139)

Midtown 32 5,664,375 585,288 10.5% 10.3% 12.7% - 11,151 125,340

Downtown 94 49,450,221 8,328,121 15.5% 16.8% 26.1% 778,344 (651,828) (898,799)

FM 1960/Champions 23 1,900,382 272,803 15.6% 14.4% 16.6% - 24,261 69,415

FM 1960/Hwy 249 37 5,148,719 549,446 10.3% 10.7% 14.0% - (19,800) (85,196)

FM 1960/I-45 North 15 1,325,458 404,091 27.2% 30.5% 31.0% - (44,193) (62,311)

FM 1960 75 8,374,559 1,226,340 14.2% 14.6% 17.3% - (39,732) (78,092)

Greenway Plaza 48 11,142,797 1,574,839 12.9% 14.1% 18.3% - 110,734 (19,479)

Gulf Freeway/Pasadena 33 2,642,527 413,671 15.4% 15.7% 18.5% - (6,801) (122,321)

Katy Far West 27 3,022,554 360,718 11.8% 11.9% 12.4% - 158 217,177

Katy Freeway East 59 9,599,223 861,920 9.1% 9.0% 14.8% - 10,888 66,536

Katy Freeway West 141 26,641,167 4,569,920 16.4% 17.2% 29.7% - (198,020) (515,792)

Katy Fwy / Energy Corridor 200 36,240,390 5,431,840 14.5% 15.0% 25.8% - (187,132) (449,256)

Kingwood/Humble 10 1,134,389 31,926 3.2% 2.8% 2.8% - 4,808 10,020

NASA/Clear Lake 53 5,612,056 1,123,538 19.3% 20.0% 21.0% - (42,296) (67,265)

North District / IAH 20 2,759,860 731,139 27.5% 26.5% 27.9% - 27,259 (150,184)

North District / N Belt West 75 10,146,197 4,324,054 43.0% 42.6% 59.4% - 50,285 (558,250)

North District / North Belt 95 12,906,057 5,055,193 39.7% 39.2% 52.6% - 77,544 (708,434)

Northeast 11 1,370,813 67,997 4.9% 5.0% 8.7% - (1,282) 109,742

North Loop West 29 3,925,538 591,012 15.3% 15.1% 21.9% - 10,451 35,480

Northwest Far 30 3,339,715 800,248 23.6% 24.0% 24.7% - (12,039) (8,314)

Northwest Near 9 803,866 37,759 4.7% 4.7% 5.0% - 224 3,789

Northwest 68 8,069,119 1,429,019 17.7% 17.7% 21.4% - (1,364) 30,955

South Main/Medical Center 46 10,108,558 346,733 3.3% 3.4% 4.7% - (13,563) 108,585

E Fort Bend Co/Sugar Land 45 6,097,508 437,082 6.7% 7.2% 14.3% - (28,766) (36,314)

Southwest Beltway 8 41 5,513,131 972,533 15.9% 17.6% 23.1% - (96,616) (150,154)

Southwest/Hillcroft 36 4,321,807 813,238 19.1% 18.8% 22.9% - 11,746 (124,606)

Southwest Fwy / Sugar Land 122 15,932,446 2,222,853 13.2% 14.0% 19.7% - (113,636) (311,074)

The Woodlands 97 16,687,906 1,396,112 8.6% 8.4% 10.0% 704,800 36,600 194,005

West Belt 37 5,398,069 900,642 14.4% 16.7% 33.2% - (121,036) (35,615)

Bellaire 29 4,271,294 447,559 10.1% 10.5% 13.7% - (14,806) (79,692)

Galleria/Uptown 58 16,758,663 2,164,941 13.3% 12.9% 19.8% - 165,837 (91,852)

Post Oak Park 27 4,581,030 1,165,541 23.6% 25.4% 31.7% - (83,783) (248,024)

Richmond/Fountainview 11 829,982 65,689 7.0% 7.9% 8.6% - (7,765) 42,318

Riverway 16 2,868,522 545,426 20.5% 19.0% 22.6% - 41,263 (179,375)

San Felipe/Voss 33 5,059,884 1,010,703 19.2% 20.0% 23.3% - (48,206) (175,889)

West Loop 174 34,369,375 5,399,859 15.6% 15.7% 21.1% - 52,540 (732,514)

Westchase 89 17,589,501 3,057,017 17.1% 17.4% 29.2% - (52,092) (175,291)

TOTAL - Houston 1,292 240,974,390 38,410,825 15.4% 15.9% 23.2% 1,483,144 (946,738) (2,899,944)

SOURCE CoStar, Transwestern

NOTE Includes buildings 50,000 SF RBA and greater; does not include buildings under construction or owned by the government

* Total Availability represents all space currently being marketed for lease (Direct, Sublet, Under Construction and delivering within 12 months) regardless of vacancy.

REAL ESTATE OUTLOOK HOUSTON METRO Q1 2018 5

Houston Office Market Indicators - Class A

SUBMARKET TOTAL BLDGS INVENTORY SF AVAILABLE

IMMEDIATELY

DIRECT VACANCY

Q4 2017

DIRECT VACANCY

Q1 2018

*TOTAL AVAILABILITY

Q1 2018

UNDER CONSTRUCTION

NET ABSORPTION

Q1 2018

12 MONTH ROLLING

ABSORPTION

Conroe 2 128,832 13,011 10.1% 10.1% 10.1% - (3,763)

CBD 37 34,126,465 4,870,808 12.9% 14.3% 26.0% 778,344 (462,086) (874,937)

Midtown 8 2,486,094 359,141 15.0% 14.4% 17.3% - 14,978 24,902

Downtown 45 36,612,559 5,229,949 13.1% 14.3% 25.4% 778,344 (447,108) (850,035)

FM 1960/Champions 1 150,000 0 0.0% 0.0% 0.0% - - -

FM 1960/Hwy 249 17 3,729,412 346,914 8.8% 9.3% 10.3% - (19,017) (39,900)

FM 1960/I-45 North 2 206,705 46,138 26.4% 22.3% 22.3% - 8,374 (17,013)

FM 1960 20 4,086,117 393,052 9.4% 9.6% 10.5% - (10,643) (56,913)

Greenway Plaza 20 7,417,120 1,111,539 14.0% 15.0% 20.6% - 179,850 74,568

Gulf Freeway/Pasadena - - - - - - - - -

Katy Far West 15 1,628,104 360,096 21.7% 22.1% 23.0% - (1,443) 198,543

Katy Freeway East 24 5,767,926 625,765 11.5% 10.8% 17.4% - 34,066 21,677

Katy Freeway West 72 18,759,363 2,839,092 15.1% 15.1% 30.7% - (2,530) (359,626)

Katy Fwy / Energy Corridor 96 24,527,289 3,464,857 14.3% 14.1% 27.6% - 31,536 (337,949)

Kingwood/Humble 2 144,312 7,466 6.5% 5.2% 5.2% - 1,927 1,927

NASA/Clear Lake 15 2,028,136 179,727 6.1% 8.9% 9.7% - (56,592) (65,227)

North District / IAH 8 1,213,677 526,203 46.2% 43.4% 44.9% - 34,026 (137,988)

North District / N Belt West 17 4,336,484 2,311,861 53.2% 53.3% 76.3% - (5,031) (317,723)

North District / North Belt 25 5,550,161 2,838,064 51.7% 51.1% 69.5% - 28,995 (455,711)

Northeast 3 640,700 21,702 2.6% 3.4% 3.4% - (4,945) (21,702)

North Loop West 6 1,240,544 264,587 22.7% 21.3% 41.1% - 17,379 75,193

Northwest Far 4 797,237 330,922 41.0% 41.5% 44.4% - (4,089) (2,487)

Northwest Near - - - - - - - - -

Northwest 10 2,037,781 595,509 29.9% 29.2% 42.4% - 13,290 72,706

South Main/Medical Center 15 4,558,989 196,931 4.4% 4.3% 6.5% - (2,094) 85,665

E Fort Bend Co/Sugar Land 20 3,773,331 281,820 7.0% 7.5% 15.0% - (19,465) (75,859)

Southwest Beltway 8 3 566,699 104,545 18.5% 18.4% 18.5% - 274 (55,590)

Southwest/Hillcroft 6 1,487,219 361,417 24.7% 24.3% 36.3% - 5,746 (110,376)

Southwest Fwy / Sugar Land 29 5,827,249 747,782 12.6% 12.8% 20.8% - (13,445) (241,825)

The Woodlands 45 11,977,463 983,510 8.7% 8.2% 9.6% 704,800 58,142 182,210

West Belt 23 4,095,444 712,795 14.4% 17.4% 35.1% - (123,652) (36,625)

Bellaire 8 1,476,268 182,708 11.7% 12.4% 18.9% - (10,437) (17,124)

Galleria/Uptown 35 13,416,434 1,833,145 14.0% 13.7% 21.0% - 144,760 (116,984)

Post Oak Park 9 2,617,868 866,867 31.0% 33.1% 40.2% - (54,339) (109,199)

Richmond/Fountainview - - - - - - - - -

Riverway 5 1,885,813 377,365 22.4% 20.0% 24.3% - 45,006 (175,876)

San Felipe/Voss 3 1,720,793 466,363 26.1% 27.1% 27.9% - (27,859) (101,205)

West Loop 60 21,117,176 3,726,448 17.7% 17.6% 24.1% - 97,131 (520,388)

Westchase 33 9,961,734 1,878,210 17.9% 18.9% 32.1% - (94,802) (242,659)

TOTAL - Houston 458 142,339,166 22,460,648 15.3% 15.8% 25.1% 1,483,144 (343,853) (2,217,178)

SOURCE CoStar, Transwestern

Includes buildings 50,000 SF RBA and greater; does not include buildings under construction or owned by the government.

* Total Availability represents all space currently being marketed for lease (Direct, Sublet, Under Construction and delivering within 12 months) regardless of vacancy.

6 REAL ESTATE OUTLOOK HOUSTON METRO Q1 2018

HOUSTON METRO MARKETFIRST QUARTER 2018

SOURCE CoStar, Transwestern

NOTE Includes buildings 50,000 SF RBA and greater; does not include buildings under construction or owned by the government

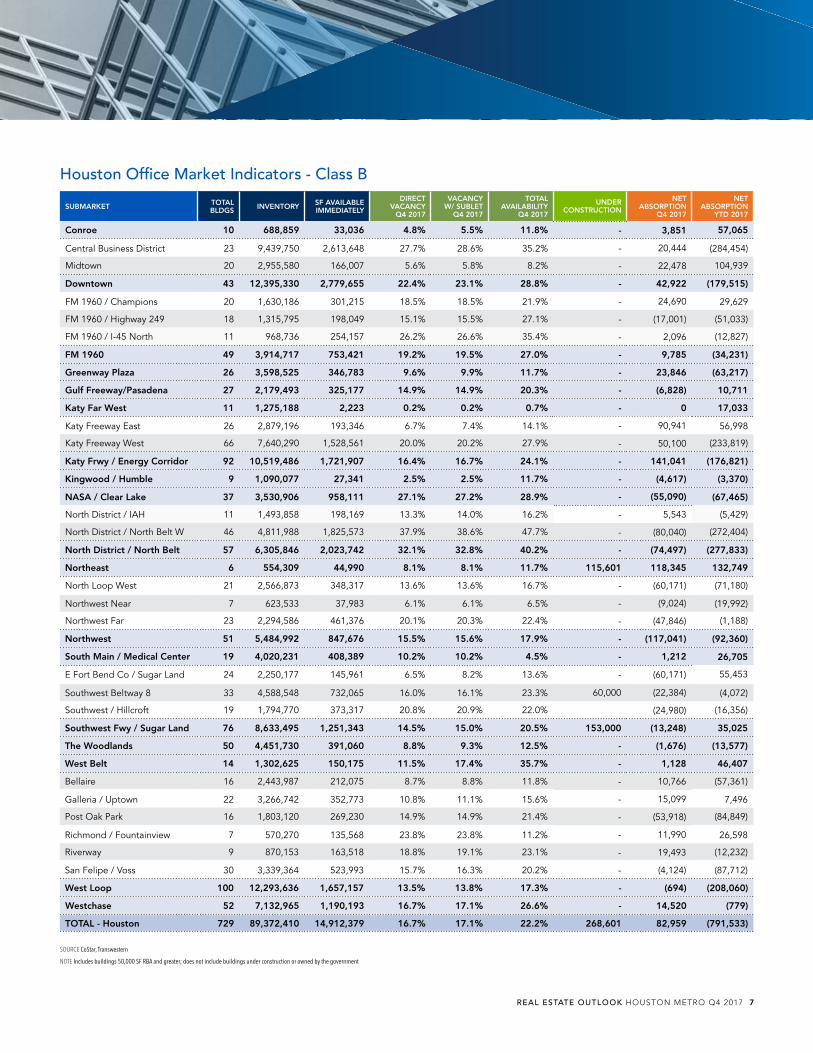

Houston Office Market Indicators - Class B

SUBMARKET TOTAL BLDGS INVENTORY SF AVAILABLE

IMMEDIATELY

DIRECT VACANCY

Q4 2017

DIRECT VACANCY

Q1 2018

*TOTAL AVAILABILITY

Q1 2018

UNDER CONSTRUCTION

NET ABSORPTION

Q1 2018

12 MONTH ROLLING

ABSORPTION

Conroe 10 691,631 31,396 4.8% 4.5% 14.5% - 1,640 31,475

CBD 23 9,439,327 2,848,868 28.1% 30.2% 34.9% - (200,893) (140,691)

Midtown 20 2,955,580 171,730 5.6% 5.8% 7.9% - (5,723) 98,542

Downtown 43 12,394,907 3,020,598 22.7% 24.4% 28.5% - (206,616) (42,149)

FM 1960/Champions 20 1,630,186 261,022 17.6% 16.0% 18.6% - 26,102 74,856

FM 1960/Hwy 249 18 1,315,795 194,108 15.1% 14.8% 24.4% - 3,941 (49,924)

FM 1960/I-45 North 11 968,736 309,159 26.2% 31.9% 32.7% - (55,002) (50,569)

FM 1960 49 3,914,717 764,289 18.9% 19.5% 24.0% - (24,959) (25,637)

Greenway Plaza 26 3,585,380 414,933 9.6% 11.6% 12.9% - (68,150) (96,368)

Gulf Freeway/Pasadena 27 2,179,493 326,023 14.9% 15.0% 18.4% - (846) (123,694)

Katy Far West 11 1,275,188 622 0.2% 0.0% 0.0% - 1,601 18,634

Katy Freeway East 26 2,879,196 214,088 6.7% 7.4% 13.6% - (20,742) 44,940

Katy Freeway West 66 7,640,290 1,689,943 20.0% 22.1% 27.4% - (161,382) (122,058)

Katy Fwy / Energy Corridor 92 10,519,486 1,904,031 16.4% 18.1% 23.6% - (182,124) (77,118)

Kingwood/Humble 8 990,077 24,460 2.8% 2.5% 2.5% - 2,881 8,093

NASA/Clear Lake 37 3,530,902 943,811 27.1% 26.7% 27.8% - 14,296 (2,038)

North District / IAH 11 1,493,858 204,936 13.3% 13.7% 15.0% - (6,767) (12,196)

North District / N Belt West 46 4,792,893 1,777,572 37.9% 37.1% 51.6% - 48,001 (231,104)

North District / North Belt 57 6,286,751 1,982,508 32.1% 31.5% 42.9% - 41,234 (243,300)

Northeast 6 554,309 41,327 8.1% 7.5% 11.1% - 3,663 136,412

North Loop West 21 2,566,873 323,912 12.3% 12.6% 13.5% - (9,363) (52,640)

Northwest Far 23 2,295,051 469,326 20.1% 20.4% 20.6% - (7,950) (5,827)

Northwest Near 7 623,533 37,759 6.1% 6.1% 6.4% - 224 (16,107)

Northwest 51 5,485,457 830,997 14.8% 15.1% 15.7% - (17,089) (74,574)

South Main/Medical Center 19 4,020,231 111,644 2.6% 2.8% 3.6% - (8,861) 7,279

E Fort Bend Co/Sugar Land 24 2,250,177 155,262 6.5% 6.9% 13.7% - (9,301) 39,545

Southwest Beltway 8 33 4,588,548 829,896 16.0% 18.1% 24.6% - (97,831) (73,374)

Southwest/Hillcroft 19 1,794,770 346,554 20.8% 19.3% 18.5% - 26,763 18,436

Southwest Fwy / Sugar Land 76 8,633,495 1,331,712 14.5% 15.4% 20.5% - (80,369) (15,393)

The Woodlands 50 4,429,758 412,602 8.8% 9.3% 11.9% - (21,542) 11,795

West Belt 14 1,302,625 187,847 14.6% 14.4% 27.2% - 2,616 1,010

Bellaire 17 2,411,520 231,774 9.5% 9.6% 11.4% - (2,799) (68,757)

Galleria/Uptown 22 3,266,437 331,796 10.8% 10.2% 15.2% - 21,077 25,132

Post Oak Park 16 1,803,120 298,674 14.9% 16.6% 22.1% - (29,444) (138,825)

Richmond/Fountainview 7 570,270 61,715 9.3% 10.8% 11.8% - (8,647) 20,316

Riverway 9 870,153 168,061 18.8% 19.3% 22.0% - (4,543) (7,711)

San Felipe/Voss 30 3,339,091 544,340 15.7% 16.3% 21.0% - (20,347) (74,684)

West Loop 101 12,260,591 1,636,360 13.0% 13.3% 17.4% - (44,703) (244,529)

Westchase 52 7,133,914 1,152,271 16.7% 16.2% 26.6% - 37,922 68,342

TOTAL - Houston 729 89,188,912 15,117,431 16.3% 16.9% 21.7% - (549,406) (661,760)

* Total Availability represents all space currently being marketed for lease (Direct, Sublet, Under Construction and delivering within 12 months) regardless of vacancy.

REAL ESTATE OUTLOOK HOUSTON METRO Q1 2018 7

Copyright © 2018 Transwestern. All rights reserved. No part of this work may be reproduced or distributed to third parties without written permission of the copyright owner. The information contained in this report was gathered by Transwestern from various primary and secondary sources believed to be reliable. Transwestern, however, makes no representation concerning the accuracy or completeness of such information and expressly disclaims any responsibility for any inaccuracy contained herein.

METHODOLOGY

The information in this report is the result of a compilation of information on office, industrial, retail, multifamily and healthcare properties

located in the Houston metropolitan area. This report includes single-tenant, multi-tenant and owner-user properties and excludes properties

owned and occupied by a government agency.

CONTACT

Stuart ShowersDirector of [email protected]

Rachel HornbeakResearch [email protected]

Jennifer Woodruff Research [email protected]

SUBMARKET Q1 2017 CLASS B

% CHANGE Y-O-Y

CLASS B

Q4 2017 CLASS B

% CHANGE OVER

QUARTER CLASS B

Q1 2018 CLASS B

Q1 2017 CLASS A

% CHANGE Y-O-Y

CLASS A

Q4 2017 CLASS A

% CHANGE OVER

QUARTER CLASS A

Q1 2018 CLASS A

Conroe $24.33 -9.1% $21.92 0.9% $22.11 $31.05 0.1% $31.09 0.0% $31.09

CBD $30.53 -3.4% $30.25 -2.5% $29.50 $44.20 1.0% $44.72 -0.2% $44.64

Midtown $33.25 -3.9% $32.26 -0.9% $31.95 $34.79 -0.1% $34.49 0.8% $34.76

Downtown $30.97 -3.8% $30.46 -2.2% $29.80 $43.32 1.7% $43.90 0.4% $44.07

FM 1960/Champions $13.77 8.4% $14.95 -0.2% $14.92 - - - - -

FM 1960/Hwy 249 $20.24 -2.8% $19.74 -0.3% $19.68 $27.98 0.0% $27.77 0.7% $27.98

FM 1960/I-45 North $18.02 2.3% $18.36 0.4% $18.43 $23.69 5.2% $25.00 0.0% $25.00

FM 1960 $17.12 3.5% $17.66 0.3% $17.71 $27.34 0.9% $27.33 1.0% $27.59

Greenway Plaza $26.05 2.3% $26.76 -0.4% $26.65 $37.78 4.9% $37.42 5.8% $39.60

Gulf Freeway/Pasadena $21.91 3.4% $21.89 3.5% $22.66 - - - - -

Katy Far West - - - - - $29.27 -1.5% $28.82 0.0% $28.83

Katy Freeway East $27.32 -3.8% $26.26 0.1% $26.29 $41.01 -0.6% $41.42 -1.6% $40.77

Katy Freeway West $23.79 -4.7% $23.11 -1.8% $22.69 $38.01 -3.9% $36.68 -0.3% $36.56

Katy Fwy / Energy Corridor $24.28 -5.1% $23.44 -1.7% $23.04 $38.45 -3.0% $37.51 -0.5% $37.33

Kingwood/Humble $23.41 2.5% $23.25 3.2% $23.99 $31.94 -0.4% $31.82 0.0% $31.82

NASA/Clear Lake $17.86 4.4% $18.41 1.2% $18.64 $24.43 0.0% $24.49 -0.2% $24.44

North District / IAH $16.59 -10.5% $15.51 -4.3% $14.84 $21.34 5.5% $22.51 0.3% $22.58

North District / N Belt West $17.42 -9.7% $15.54 1.3% $15.74 $26.43 -7.2% $24.72 -0.3% $24.65

North District / North Belt $17.34 -9.8% $15.53 0.7% $15.64 $25.36 -4.4% $24.33 -0.2% $24.29

Northeast $22.71 0.0% $22.71 0.0% $22.71 - - - - -

North Loop West $23.16 -3.7% $21.94 1.6% $22.29 $26.48 0.2% $26.56 -0.1% $26.54

Northwest Far $15.90 -3.0% $15.19 1.6% $15.43 $18.89 3.5% $19.54 0.2% $19.58

Northwest Near $18.13 9.0% $19.72 0.2% $19.76 - - - - -

Northwest $18.81 -2.4% $17.98 2.1% $18.36 $22.84 3.2% $23.83 -1.0% $23.59

South Main/Medical Center $23.06 7.2% $23.50 5.2% $24.71 $34.28 -0.9% $33.59 1.1% $33.97

E Fort Bend Co/Sugar Land $22.37 8.6% $23.41 3.8% $24.30 $31.81 0.8% $31.88 0.6% $32.08

Southwest Beltway 8 $18.33 0.6% $18.54 -0.5% $18.44 $21.14 -0.2% $20.93 0.8% $21.10

Southwest/Hillcroft $17.66 -6.4% $16.72 -1.1% $16.54 $19.57 1.6% $19.73 0.8% $19.89

Southwest Fwy / Sugar Land $18.82 -0.6% $18.60 0.6% $18.70 $23.90 1.5% $24.01 1.0% $24.25

The Woodlands $25.55 1.6% $25.90 0.2% $25.96 $35.23 0.2% $35.27 0.1% $35.31

West Belt $21.62 13.7% $24.58 0.0% $24.57 $32.29 3.0% $33.38 -0.2% $33.29

Bellaire $23.41 2.9% $24.12 -0.1% $24.10 $27.61 1.6% $27.81 0.9% $28.04

Galleria/Uptown $28.81 0.0% $28.66 0.5% $28.82 $39.33 -0.4% $39.59 -1.0% $39.19

Post Oak Park $27.37 -9.3% $24.99 -0.7% $24.82 $40.11 -9.8% $36.64 -0.3% $36.52

Richmond/Fountainview $19.25 0.3% $19.51 -1.1% $19.30 - - - - -

Riverway $26.42 -3.0% $25.65 -0.1% $25.63 $33.10 0.4% $33.13 0.3% $33.25

San Felipe/Voss $24.96 4.2% $25.79 0.9% $26.02 $36.38 -0.7% $35.82 0.8% $36.11

West Loop $25.84 -0.1% $25.77 0.2% $25.82 $37.80 -1.8% $37.35 -0.6% $37.12

Westchase $18.45 9.6% $19.85 1.9% $20.23 $37.29 -3.2% $36.12 0.0% $36.12

TOTAL - Houston $22.03 -1.0% $21.74 0.3% $21.81 $36.05 0.6% $35.85 1.1% $36.26

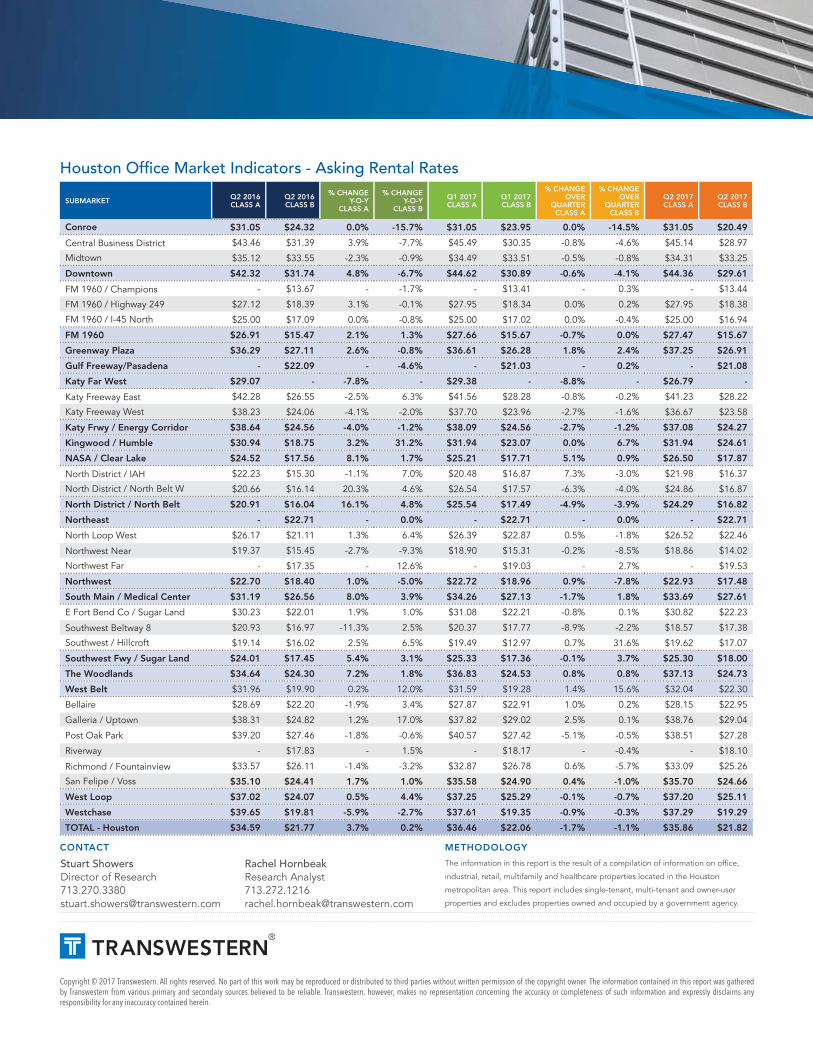

Houston Office Market Indicators - Asking Rental Rates

OVERVIEW

Availability Continues to Decline as Co-Working Rises The Houston office market ended 2017 on a strong note, as total availability declined for the second straight quarter, the investment market remained hot, and WTI crude prices settled above $60 per barrel. Despite absorption remaining negative for the fourth quarter, citywide availability declined by 0.5%, ending the year at 22.8%. This change was largely attributable to the reduction in sublease supply (-900k square feet) as tenants Motiva (Saudi Aramco), Stewart Title, Empyrean Benefits Solutions, and several others opted for sublease alternatives. At the end of the year, sublease space totaled 8.9 M SF with 1.3 M SF set to expire over the next 12 months. Late year activity also saw the rise of co-working space throughout the market. Several providers such as WeWork, Spaces, The Cannon and The Work Lodge announced or opened locations, pushing co-working space totals past 500k SF with both urban and suburban alternatives. The quick expansion of co-working space has both providers and landlords taking notice. In December, Brookfield Properties and Onex made an indicative proposal on IGW, the holding company of Regus and Spaces, as Brookfield Asset Management looks to gain a foothold in the co-working market. Additionally, Servcorp, announced that they will pivot into a co-working strategy in order to capitalize on the trend.

NET ABSORPTION

Quarterly Absorption Flat After Down YearCumulative annual absorption totals of negative 3.9 million square feet highlight the delayed impacts of the energy downturn. However, the

HOUSTON OFFICE MARKETYEAR-END 2017

REAL ESTATE OUTLOOK

Office Market Signals RecoveryThe Rise of Co-Working in Houston

NET ABSORPTION AND VACANCY RATE TRENDS HOUSTON METRO AREA

CONTIGUOUS BLOCKS OF AVAILABLE SPACE HOUSTON METRO

SOURCE CoStar, Transwestern *Through Q4 2017

SOURCE CoStar, Transwestern *Through Q4 2017

Note: Delivery of preleased space counts as positive net absorption

Notable Q4 LeasesTENANT SF LEASE TYPE BUILDING SUBMARKET

Motiva (Saudi Aramco) 173,000 Sublease Two Allen Center CBD

Stewart Title 156,151 Sublease 1360 Post Oak Galleria/Uptown

Empyrean Benefits* 106,904 Sublease 3010 Briarpark Dr Westchase

Talos Energy 98,000 Relocation/Expansion Three Allen Center CBD

TransCanada 82,916 Expansion Bank of America Center CBD

-4000-3000-2000-1000

010002000300040005000600070008000

Net Absorption

171615141312111009080706 5%

10%

15%

20%

25%Total AvailabilityDirect Vacancy

0

50

100

150

200Class A SubletClass A Direct

200,000 SF100,000 SF50,000 SF25,000 SF

Class B SubletClass B Direct

* Empyrean leveraged sublease alternative with minimal remaining term to execute direct deal.

fourth quarter saw negative absorption of only 51,628 SF. This represents a marked improved over the recent quarter totals of -2.1M SF (1Q 2017), -1.1 M SF (2Q 2017), and -0.6 M SF (3Q 2017). Class A absorption for the fourth quarter totaled -86,067 SF, bringing the 2017 annual absorption for the property class to -3.1 M SF. Class B absorption for the fourth quarter was positive 82,959 SF with Class B annual absorption totaling negative 791,000 SF.

DIRECT VACANCY & TOTAL AVAIL ABILIT Y

Total Availability Declines, Vacancy IncreasesThe overall office availability rate (all space marketed as available for lease, both direct and sublet) decreased 0.5% over the quarter, ending the year at 22.8%. The fourth quarter saw several tenants (Stewart Title, Empyrean Benefits Solutions and Saudi Aramco) opt to leverage sublease alternatives. In total, sublease supply decreased by 894,000 SF over the quarter. Class A availability finished the year at 24.0%, down by 0.4% over the quarter. Class B availability decreased by 0.7% over the period, ending the year at 22.2%.

While decreases in sublease space triggered declines in availability, vacancy continued to rise over the quarter. Overall direct vacancy ended 2017 at 15.5%, increasing by 1.7% year-over-year. Class A direct vacancy ended the year at 15.2%, up 2.1% annually and 0.1% over the quarter. Class B direct vacancy increased by 1.1% year-over-year, ending 2017 at 16.7%. With 1.3 million SF of sublease space set to expire over the next 12 months, direct vacancy is anticipated to continue increasing through the first half of 2018. This is especially pronounced in the North Houston District where 868,845 SF is set to expire by end of year 2018.

RENTAL R ATES

Asking Rates Level OffOverall asking rates for the Houston metro area decreased marginally over the quarter, finishing 2017 at $30.59 PSF full service. Class A rates declined by 1.9% over the year, closing at $35.83 PSF full service, while Class B asking rates declined by 4.0%, ending at $21.78 PSF full service. Though there are signs of improvement, the market remains firmly in the tenants favor with credit grade tenants able to attain generous concession packages. The submarkets with the highest gross asking rents are the Central Business District (Class A - $45.17 PSF), the Katy Fwy East (Class A, $42.41 PSF), and Galleria/Uptown (Class A - $39.26 PSF).

SUPPLY AND DEVELOPMENT

Construction Pipeline After the delivery of 33.0M SF over the past seven years, construction activity has slowed greatly. Considering the number of large blocks and total space available for lease, developers are wary of additional speculative construction. Still, as tenants strive to retain talent and attain efficiency both in their space footprint as well as their operating expenses, the potential for additional construction tethered to a lead tenant or build-to-suit remains in play. At year end, the Houston area

Office Under ConstructionHouston Metro | Q4 2017

SUBMARKET NUMBER OF BLDGS SF % PRE-

LEASED

CBD 1 778,344 32%

Woodlands 3 704,800 97%

South 2 300,000 7%

West Loop 1 104,579 70%

Kingwood 1 100,000 0%

FM 1960 1 73,000 100%

Katy 1 72,045 51%

Total 7 2,032,768 67%

AVERAGE OFFICE RENTS HOUSTON METRO AREA

SOURCE CoStar, Transwestern *Through Q4 2017 Note: All classes of office space

Total Available SpaceHouston Metro | Q4 2017

SUBMARKETSUBLEASE SPACE (SF)

% OF SUPPLY

% TOTAL AVAILABLE

CBD 2,067,450 4.7% 18.4%

Katy Fwy West 1,924,169 7.2% 26.3%

Westchase 1,445,315 8.2% 28.0%

West Loop 932,700 2.7% 12.8%

N Houston District 905,617 7.0% 14.2%

All of Houston 8,935,719 3.7% 16.2%

$15

$20

$25

$30

$35

$40Class BClass AOverall

171615141312111009080706

2 REAL ESTATE OUTLOOK HOUSTON METRO Q4 2017

HOUSTON METRO MARKETYEAR-END 2017

construction pipeline totaled 2.1 M SF with 33.0% available for lease. Houston's largest office developments currently under construction are Capitol Tower (CBD, 778,000 SF - 27% leased to Bank of America), CityPlace 2 (The Woodlands, 326,000 SF - 100% Leased to ABS) and HP's Build-to-Suit Campus (The Woodlands, two-189,000 SF buildings). Notable fourth quarter deliveries include The Kirby Collection, a mixed-use project with a significant office component (Greenway Plaza, 188,547 SF, 21% leased) and Members Choice Credit Union (Katy Fwy West, 86,265 SF, 62% leased).

INVESTMENT MARKET

Investments Rebound Sharply Over 2017 Houston investment activity rebounded sharply in 2017, as annual sales totaled $3.8 billion, marking the highest total since registering $4.6 billion in 2013. Regardless of elevated vacancy figures, the strength in the underlying fundamentals of the market have investors buying into Houston's future. Of particular interest to investors are well located urban infill properties with upside available through renovation and lobby/service activation. Notable properties that traded over the course of 2017 include Greenway Plaza (4.9 M SF, $210 PSF), Houston Center (4.2 M SF, $218 PSF) and Greenspoint Place (2.0 M SF, undisclosed).

Sales for the quarter totaled $1.3 billion, bolstered by the closing of Houston Center, as Brookfield Properties officially acquired the 4.2 M SF Class A property portfolio for $875 million. The fourth quarter saw another iconic property trade hands, as M-M Properties and Baupost Group were reported as having acquired Marathon Oil Tower, a 41-story 1.2 M SF Class A office building for $175.0 M from CBRE Global Investors. These figures represent assets for which pricing information could be obtained.

COMPARATIVE OFFICE INVESTMENT SALES VOLUME SELECT METRO AREAS

SOURCE Real Capital Analytics, Transwestern ,*Through Q4 2017

AVERAGE OFFICE SALE PRICE HOUSTON METRO AREA

SOURCE Real Capital Analytics, Transwestern,*Through Q4 2017

Notable Q4 TransactionsBUILDING SUBMARKET SF SALE PRICE SELLER BUYER

Marathon Oil Tower Galleria/Uptown 1,197,300 $175.0 million CBRE Global Investors M-M Properties/Baupost Group

Westchase Park Plaza Westchase 232,108 $24.0 million Parmenter Realty Partners Hertz Group

Nitya Tower (FKA Norfolk Tower) Greenway Plaza 207,562 Undisclosed TA Realty Nitya

5757 Woodway San Felipe/Voss 162,888 Undisclosed Fuller Realty Braun Enterprises/ Harbert Mgmt

SOURCE Real Capital Analytics, HFF, Transwestern

Sales

Volu

me i

n Billi

ons

$0

$1

$2

$3

$4

$5

$6

$7

$8HoustonDenverDallasAtlanta

17*1615141312111009080706

$0

$50

$100

$150

$200

$250 Average Sale Price Per SF

171615141312111009080706

REAL ESTATE OUTLOOK HOUSTON METRO Q4 2017 3

OUTLOOK

A Return To Normal or More of the Same in 2018?After suffering through the worst of the effects of the energy downturn, the Houston office market appears poised to begin a tangible recovery in 2018 as WTI prices have settled over $60 per barrel, more favorable corporate tax rates are set to kick in and a strong national economy has consumer confidence near 20-yr highs. Diversification in industries such as healthcare, petrochemical, distribution and retail/hospitality have helped offset many of the jobs lost through the energy downturn; however, there is little doubt that the market needs a return to form for energy or the emergence to help alleviate the vacant and available supply. As such, the late year surge in crude prices is especially notable. Still, job growth in the sector will require prices to maintain in the $60's for the balance of 2018.

Considering current market conditions, overall market activity is projected to remain light over the first half of 2018 with the second quarter seeing direct vacancy crest. Tangible improvement should begin in the second half of 2018, as job growth stimulates absorption. All core metrics are forecast to improve, with availability and vacancy deceasing, while absorption returns to positive absorption. Additionally, the quick rise of co-working should continue to benefit landlords (in the short-run) as their demand for space increases co-working market totals significantly and helps to reduce direct available supply. With all signs pointing up, the only headwinds remaining for the Houston office market center around the energy sector and the highly unpredictable nature of crude prices.

Multi-tenant market vs Transwestern comprehensive market coverage

MULTI-TENANT ENTIRE MARKET

Inventory 200.4 MSF 241.8 MSF

Overall Vacancy 20.7% 17.0%

2017 Net Absorption (2,035,970) SF (3,990,948) SF

WHY OUR METHODOLOGY IS THE BEST INDICATOR OF CURRENT MARKET CONDITIONSWe include owner occupied and single-tenant buildings in our inventory, vacancy and absorption statistics to capture more market activity than many of our competitors. This allows us to better correlate changes in the market with changes in employment. As single-tenant space does compete with multi-tenant space, we believe it is critical to understand all components of the market. The inclusion of single-tenant and owner-occupied space tends to yield lower vacancy rates and higher absorption totals than some of our competitors’ results, but our coverage of the market is more comprehensive.

OFFICE ABSORPTION AND EMPLOYMENT HOUSTON METRO AREA

SOURCE Bureau of Labor Statistics, Transwestern *12-month job growth through Nov 2017, net absorption YTD through Q4 2017

-4000

-2700

-1400

-100

1200

2500

3800

5100

6400

7700

9000Net Absorption (Thousands of SF)

171615141312111009080706-80

-60

-40

-20

0

20

40

60

80

100

120Payroll Job Growth (in Thousands)

4 REAL ESTATE OUTLOOK HOUSTON METRO Q4 2017

HOUSTON METRO MARKETYEAR-END 2017

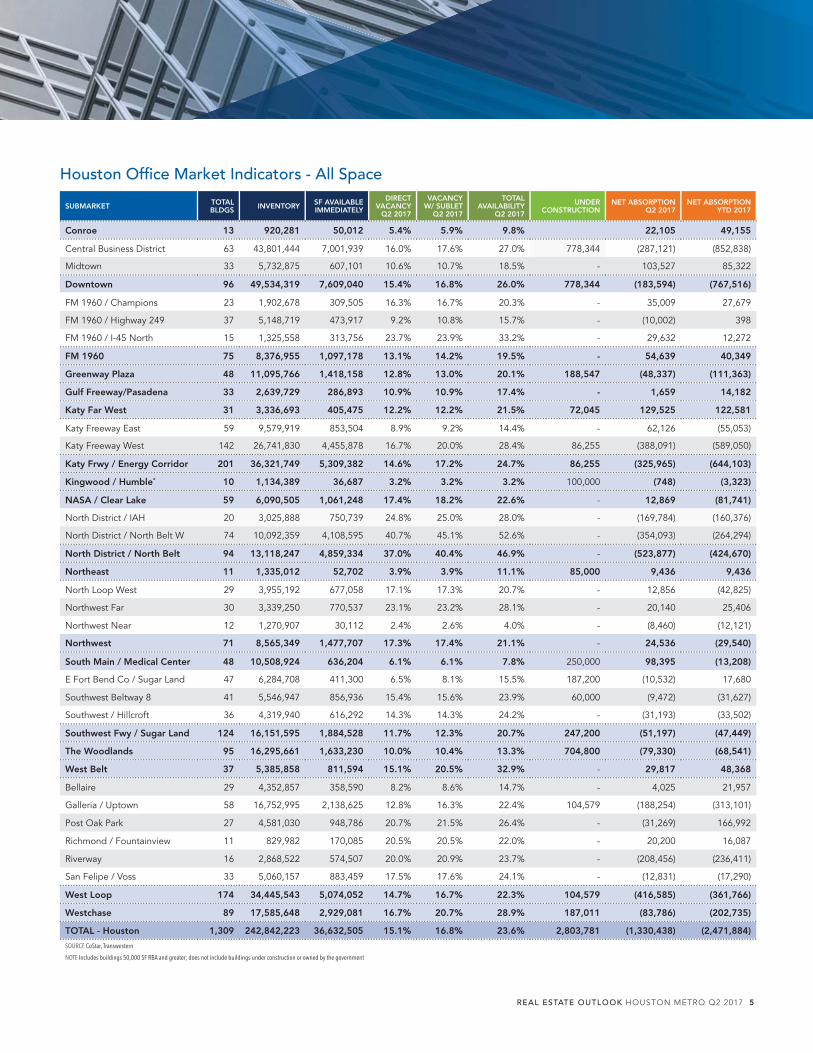

Houston Office Market Indicators - All Space

SUBMARKET TOTAL BLDGS INVENTORY SF AVAILABLE

IMMEDIATELY

DIRECT VACANCY

Q4 2017

VACANCY W/ SUBLET

Q4 2017

TOTAL AVAILABILITY

Q4 2017

UNDER CONSTRUCTION

NET ABSORPTION Q4 2017

NET ABSORPTION YTD 2017

Conroe 13 920,281 46,047 5.0% 5.5% 10.9% 3,851 53,302

Central Business District 62 43,786,269 7,045,527 16.1% 18.2% 25.6% 778,344 (32,095) (1,497,427)

Midtown 32 5,664,375 596,439 10.5% 11.0% 15.2% - 43,141 95,984

Downtown 94 49,450,644 7,641,966 15.5% 17.3% 24.5% 778,344 11,046 (1,401,443)

FM 1960 / Champions 23 1,900,382 311,155 16.4% 16.4% 19.3% - 24,690 26,029

FM 1960 / Highway 249 37 5,148,719 506,126 9.8% 10.1% 14.8% - (22,272) (31,811)

FM 1960 / I-45 North 15 1,325,458 359,898 27.2% 27.4% 33.8% - 2,096 (33,870)

FM 1960 75 8,374,559 1,177,179 14.1% 14.3% 18.8% - 4,514 (39,652)

Greenway Plaza 48 11,095,766 1,435,116 12.9% 13.4% 19.2% 188,547 (21,878) (132,883)

Gulf Freeway/Pasadena 33 2,642,527 406,870 15.4% 15.4% 19.8% - 2,337 18,561

Katy Far West 27 3,022,554 355,537 11.8% 12.2% 16.3% 72,045 72,527 210,342

Katy Freeway East 59 9,593,191 835,819 8.7% 9.5% 15.1% - 108,144 (28,725)

Katy Freeway West 141 26,653,982 4,371,900 16.4% 18.9% 27.5% 86,255 68,590 (506,214)

Katy Frwy / Energy Corridor 200 36,247,173 5,207,719 14.4% 16.4% 24.2% 86,255 176,734 (534,939)

Kingwood / Humble* 11 1,234,389 36,734 3.0% 3.0% 11.1% - (6,544) (3,370)

NASA / Clear Lake 53 5,612,060 1,081,246 19.3% 19.6% 22.4% - (75,664) (105,105)

North District / IAH 20 2,759,860 758,398 27.5% 27.9% 29.7% - 8,687 (168,035)

North District / North Belt W 75 10,164,618 4,374,339 43.0% 45.8% 54.5% - (191,752) (539,042)

North District / North Belt 95 12,924,478 5,132,737 39.7% 41.9% 49.2% - (183,065) (707,077)

Northeast 11 1,370,813 66,715 4.9% 4.9% 8.7% 115,601 134,053 111,024

North Loop West 29 3,925,538 635,231 16.2% 16.2% 25.6% - 8,644 (30,745)

Northwest Near 10 1,041,250 37,983 3.6% 3.6% 3.9% - (9,024) (19,992)

Northwest Far 30 3,339,250 788,209 23.6% 23.9% 26.2% - (48,433) 7,734

Northwest 69 8,306,038 1,461,423 17.6% 17.7% 23.1% - (48,813) (43,003)

South Main / Medical Center 47 10,360,561 643,463 6.2% 6.3% 5.4% - (26,907) (20,467)

E Fort Bend Co / Sugar Land 45 6,097,508 408,316 6.7% 7.9% 11.9% 187,200 49,518 20,664

Southwest Beltway 8 41 5,513,131 875,917 15.9% 16.0% 22.0% 60,000 (61,484) (75,884)

Southwest / Hillcroft 36 4,321,807 781,234 18.1% 18.4% 21.8% - (97,368) (135,444)

Southwest Fwy / Sugar Land 122 15,932,446 2,065,467 13.0% 13.5% 18.1% 247,200 (109,334) (190,664)

The Woodlands 96 16,520,878 1,518,816 9.2% 9.6% 11.3% 515,800 90,461 45,806

West Belt 37 5,398,069 739,318 13.7% 19.5% 32.5% - 55,489 130,767

Bellaire 28 4,298,130 415,853 9.7% 10.0% 14.2% - 13,353 (40,033)

Galleria / Uptown 58 16,760,379 2,226,099 13.3% 15.9% 20.0% 104,579 (32,718) (474,135)

Post Oak Park 27 4,581,030 1,081,758 23.6% 26.0% 31.3% - (55,975) (345,980)

Richmond / Fountainview 11 829,982 140,424 16.9% 16.9% 9.2% - 16,778 45,748

Riverway 16 2,868,522 586,689 20.5% 21.4% 23.6% - 8,196 (248,593)

San Felipe / Voss 33 5,060,157 904,582 17.9% 18.3% 23.1% - 12,586 (79,132)

West Loop 173 34,398,200 5,355,405 15.6% 17.3% 21.3% 104,579 (37,780) (1,142,125)

Westchase 89 17,588,552 3,004,925 17.1% 20.4% 29.3% 187,011 (92,655) (240,022)

TOTAL - Houston 1,293 241,399,988 37,376,683 15.5% 17.0% 22.8% 2,295,382 (51,628) (3,990,948)

SOURCE CoStar, Transwestern

NOTE Includes buildings 50,000 SF RBA and greater; does not include buildings under construction or owned by the government

-

REAL ESTATE OUTLOOK HOUSTON METRO Q4 2017 5

Houston Office Market Indicators - Class A

SUBMARKET TOTAL BLDGS INVENTORY SF AVAILABLE

IMMEDIATELY

DIRECT VACANCY

Q4 2017

VACANCY W/ SUBLET

Q4 2017

TOTAL AVAILABILITY

Q4 2017

UNDER CONSTRUCTION

NET ABSORPTION

Q4 2017

NET ABSORPTION

YTD 2017

Conroe 2 128,832 13,011 10.1% 10.1% 14.3% - (3,763)

Central Business District 37 34,126,465 4,408,722 12.9% 15.3% 23.1% 778,344 (52,539) (1,204,462)

Midtown 8 2,486,094 374,119 15.0% 15.9% 22.7% - 20,663 (2,642)

Downtown 45 36,612,559 4,782,841 13.1% 15.4% 23.1% 778,344 (31,876) (1,207,104)

FM 1960 / Champions 1 150,000 0 0.0% 0.0% 0.0% -

FM 1960 / Highway 249 17 3,729,412 304,377 8.2% 8.3% 10.5% - (8,063) 4,642

FM 1960 / I-45 North 2 206,705 54,512 26.4% 26.4% 26.4% - (25,387)

FM 1960 20 4,086,117 358,889 8.8% 8.9% 10.9% - (8,063) (20,745)

Greenway Plaza 20 7,356,944 1,040,932 14.1% 14.7% 22.6% 188,547 (49,011) (71,427)

Gulf Freeway/Pasadena -

Katy Far West 15 1,628,104 353,314 21.7% 22.6% 29.7% 72,045 72,527 193,309

Katy Freeway East 24 5,761,894 622,842 10.8% 11.8% 17.7% - 34,175 (93,761)

Katy Freeway West 72 18,772,178 2,836,562 15.1% 18.5% 27.5% 86,255 18,490 (272,395)

Katy Frwy / Energy Corridor 96 24,534,072 3,459,404 14.1% 16.9% 25.2% 86,255 52,665 (366,156)

Kingwood / Humble 2 144,312 9,393 6.5% 6.5% 6.5% - (1,927)

NASA / Clear Lake 15 2,028,136 123,135 6.1% 6.9% 11.4% - (20,574) (37,640)

North District / IAH 8 1,213,677 560,229 46.2% 46.2% 47.7% - 3,144 (162,606)

North District / North Belt W 17 4,334,810 2,306,830 53.2% 58.8% 68.9% - (93,801) (241,865)

North District / North Belt 25 5,548,487 2,867,059 51.7% 56.0% 64.2% - (90,657) (404,471)

Northeast 3 640,700 16,757 2.6% 2.6% 2.6% - 15,708 (16,757)

North Loop West 6 1,240,544 281,966 22.7% 22.7% 45.1% - 73,260 44,624

Northwest Near 1 237,384 0 0.0% 0.0% 0.0% - 0

Northwest Far 4 797,237 326,833 41.0% 41.5% 45.2% - (587) 8,922

Northwest 11 2,275,165 608,799 26.8% 26.9% 40.4% - 72,673 53,546

South Main / Medical Center 16 4,810,992 199,524 4.1% 4.3% 7.0% - (19,979) (35,724)

E Fort Bend Co / Sugar Land 20 3,773,331 262,355 7.0% 7.9% 11.1% 94,200 15,402 (34,789)

Southwest Beltway 8 3 566,699 104,819 18.5% 18.5% 18.5% - (21,864) (56,219)

Southwest / Hillcroft 6 1,487,219 323,413 21.7% 22.5% 29.0% - (59,216) (94,964)

Southwest Fwy / Sugar Land 29 5,827,249 690,587 11.9% 12.6% 16.4% 94,200 (65,678) (185,972)

The Woodlands 44 11,788,463 1,127,756 9.6% 10.0% 11.2% 704,800 92,137 59,383

West Belt 23 4,095,444 589,143 14.4% 20.2% 31.5% - 54,361 84,360

Bellaire 8 1,470,637 172,271 11.7% 12.4% 19.8% - (4,637) 13,214

Galleria / Uptown 35 13,417,845 1,873,326 14.0% 17.1% 21.2% 104,579 (47,817) (481,631)

Post Oak Park 9 2,617,868 812,528 31.0% 35.2% 40.1% - (2,057) (261,131)

Richmond / Fountainview -

Riverway 5 1,885,813 422,371 22.4% 23.8% 25.3% - (13,397) (246,622)

San Felipe / Voss 3 1,720,793 380,589 22.1% 22.1% 28.6% - 16,710 8,580

West Loop 60 21,112,956 3,661,085 17.3% 20.0% 24.4% 104,579 (51,198) (967,590)

Westchase 33 9,961,734 1,783,408 17.9% 23.5% 32.4% 187,011 (107,175) (225,435)

TOTAL - Houston 459 142,580,266 21,685,037 15.2% 17.5% 24.0% 2,026,781 (86,067) (3,152,186)

SOURCE CoStar, Transwestern

NOTE Includes buildings 50,000 SF RBA and greater; does not include buildings under construction or owned by the government

6 REAL ESTATE OUTLOOK HOUSTON METRO Q4 2017

HOUSTON METRO MARKETYEAR-END 2017

SOURCE CoStar, Transwestern

NOTE Includes buildings 50,000 SF RBA and greater; does not include buildings under construction or owned by the government

Houston Office Market Indicators - Class B

SUBMARKET TOTAL BLDGS INVENTORY SF AVAILABLE

IMMEDIATELY

DIRECT VACANCY

Q4 2017

VACANCY W/ SUBLET

Q4 2017

TOTAL AVAILABILITY

Q4 2017

UNDER CONSTRUCTION

NET ABSORPTION

Q4 2017

NET ABSORPTION

YTD 2017

Conroe 10 688,859 33,036 4.8% 5.5% 11.8% - 3,851 57,065

Central Business District 23 9,439,750 2,613,648 27.7% 28.6% 35.2% - 20,444 (284,454)

Midtown 20 2,955,580 166,007 5.6% 5.8% 8.2% - 22,478 104,939

Downtown 43 12,395,330 2,779,655 22.4% 23.1% 28.8% - 42,922 (179,515)

FM 1960 / Champions 20 1,630,186 301,215 18.5% 18.5% 21.9% - 24,690 29,629

FM 1960 / Highway 249 18 1,315,795 198,049 15.1% 15.5% 27.1% - (17,001) (51,033)

FM 1960 / I-45 North 11 968,736 254,157 26.2% 26.6% 35.4% - 2,096 (12,827)

FM 1960 49 3,914,717 753,421 19.2% 19.5% 27.0% - 9,785 (34,231)

Greenway Plaza 26 3,598,525 346,783 9.6% 9.9% 11.7% - 23,846 (63,217)

Gulf Freeway/Pasadena 27 2,179,493 325,177 14.9% 14.9% 20.3% - (6,828) 10,711

Katy Far West 11 1,275,188 2,223 0.2% 0.2% 0.7% - 0 17,033

Katy Freeway East 26 2,879,196 193,346 6.7% 7.4% 14.1% - 90,941 56,998

Katy Freeway West 66 7,640,290 1,528,561 20.0% 20.2% 27.9% - 50,100 (233,819)

Katy Frwy / Energy Corridor 92 10,519,486 1,721,907 16.4% 16.7% 24.1% - 141,041 (176,821)

Kingwood / Humble 9 1,090,077 27,341 2.5% 2.5% 11.7% - (4,617) (3,370)

NASA / Clear Lake 37 3,530,906 958,111 27.1% 27.2% 28.9% - (55,090) (67,465)

North District / IAH 11 1,493,858 198,169 13.3% 14.0% 16.2% - 5,543 (5,429)

North District / North Belt W 46 4,811,988 1,825,573 37.9% 38.6% 47.7% - (80,040) (272,404)

North District / North Belt 57 6,305,846 2,023,742 32.1% 32.8% 40.2% - (74,497) (277,833)

Northeast 6 554,309 44,990 8.1% 8.1% 11.7% 115,601 118,345 132,749

North Loop West 21 2,566,873 348,317 13.6% 13.6% 16.7% - (60,171) (71,180)

Northwest Near 7 623,533 37,983 6.1% 6.1% 6.5% - (9,024) (19,992)

Northwest Far 23 2,294,586 461,376 20.1% 20.3% 22.4% - (47,846) (1,188)

Northwest 51 5,484,992 847,676 15.5% 15.6% 17.9% - (117,041) (92,360)

South Main / Medical Center 19 4,020,231 408,389 10.2% 10.2% 4.5% - 1,212 26,705

E Fort Bend Co / Sugar Land 24 2,250,177 145,961 6.5% 8.2% 13.6% - (60,171) 55,453

Southwest Beltway 8 33 4,588,548 732,065 16.0% 16.1% 23.3% 60,000 (22,384) (4,072)

Southwest / Hillcroft 19 1,794,770 373,317 20.8% 20.9% 22.0% (24,980) (16,356)

Southwest Fwy / Sugar Land 76 8,633,495 1,251,343 14.5% 15.0% 20.5% 153,000 (13,248) 35,025

The Woodlands 50 4,451,730 391,060 8.8% 9.3% 12.5% - (1,676) (13,577)

West Belt 14 1,302,625 150,175 11.5% 17.4% 35.7% - 1,128 46,407

Bellaire 16 2,443,987 212,075 8.7% 8.8% 11.8% - 10,766 (57,361)

Galleria / Uptown 22 3,266,742 352,773 10.8% 11.1% 15.6% - 15,099 7,496

Post Oak Park 16 1,803,120 269,230 14.9% 14.9% 21.4% - (53,918) (84,849)

Richmond / Fountainview 7 570,270 135,568 23.8% 23.8% 11.2% - 11,990 26,598

Riverway 9 870,153 163,518 18.8% 19.1% 23.1% - 19,493 (12,232)

San Felipe / Voss 30 3,339,364 523,993 15.7% 16.3% 20.2% - (4,124) (87,712)

West Loop 100 12,293,636 1,657,157 13.5% 13.8% 17.3% - (694) (208,060)

Westchase 52 7,132,965 1,190,193 16.7% 17.1% 26.6% - 14,520 (779)

TOTAL - Houston 729 89,372,410 14,912,379 16.7% 17.1% 22.2% 268,601 82,959 (791,533)

REAL ESTATE OUTLOOK HOUSTON METRO Q4 2017 7

Copyright © 2017 Transwestern. All rights reserved. No part of this work may be reproduced or distributed to third parties without written permission of the copyright owner. The information contained in this report was gathered by Transwestern from various primary and secondary sources believed to be reliable. Transwestern, however, makes no representation concerning the accuracy or completeness of such information and expressly disclaims any responsibility for any inaccuracy contained herein.

METHODOLOGY

The information in this report is the result of a compilation of information on office, industrial, retail, multifamily and healthcare properties

located in the Houston metropolitan area. This report includes single-tenant, multi-tenant and owner-user properties and excludes properties

owned and occupied by a government agency.

CONTACT

Stuart ShowersDirector of [email protected]

Rachel HornbeakResearch [email protected]

Jennifer Woodruff Research [email protected]

SUBMARKET Q4 2016 CLASS A

Q4 2016 CLASS B

% CHANGEY-O-Y

CLASS A

% CHANGEY-O-Y

CLASS B

Q3 2017 CLASS A

Q3 2017 CLASS B

% CHANGE OVER

QUARTER CLASS A

% CHANGE OVER

QUARTER CLASS B

Q4 2017 CLASS A

Q4 2017 CLASS B

Conroe $31.05 $23.53 0.1% -6.8% $31.05 $22.92 0.1% -4.4% $31.09 $21.92

Central Business District $45.00 $31.10 0.4% -3.3% $45.16 $29.58 0.0% 1.7% $45.17 $30.08

Midtown $34.31 $33.44 0.4% -1.9% $34.49 $33.65 -0.1% -2.5% $34.44 $32.81

Downtown $44.27 $31.58 0.2% -3.6% $44.29 $30.18 0.1% 0.8% $44.35 $30.43

FM 1960 / Champions - $13.77 - 4.8% - $14.04 - 2.8% - $14.43

FM 1960 / Highway 249 $27.84 $21.74 -0.2% -11.9% $27.94 $19.48 -0.6% -1.7% $27.78 $19.15

FM 1960 / I-45 North $23.69 $17.33 5.5% 5.9% $25.00 $18.07 0.0% 1.6% $25.00 $18.36

FM 1960 $27.09 $17.39 1.0% -1.0% $27.44 $17.01 -0.3% 1.3% $27.35 $17.22

Greenway Plaza $37.89 $26.22 -1.9% 3.3% $38.12 $26.92 -2.4% 0.6% $37.19 $27.08

Gulf Freeway/Pasadena - $21.50 - 1.8% - $21.82 - 0.3% - $21.89

Katy Far West - - - - $28.73 - 0.3% - $28.82 -

Katy Freeway East $41.92 $27.20 1.2% -2.2% $42.80 $28.10 -0.9% -5.3% $42.41 $26.61

Katy Freeway West $39.24 $23.22 -6.5% -0.5% $36.72 $23.25 -0.1% -0.7% $36.68 $23.10

Katy Frwy / Energy Corridor $39.49 $23.85 -4.7% -1.6% $37.83 $23.93 -0.5% -1.9% $37.64 $23.46

Kingwood / Humble $31.73 $20.61 0.3% 12.8% $31.94 $20.36 -0.4% 14.2% $31.82 $23.25

NASA / Clear Lake $24.80 $19.58 -1.2% -6.3% $24.50 $18.24 0.0% 0.6% $24.49 $18.36

North District / IAH $22.28 $16.57 3.8% -6.4% $23.09 $15.27 0.2% 1.5% $23.13 $15.51

North District / North Belt W $25.22 $16.81 -1.5% -1.5% $25.37 $16.41 -2.1% 0.9% $24.85 $16.55

North District / North Belt $24.67 $16.79 -0.6% -2.0% $24.93 $16.29 -1.6% 0.9% $24.53 $16.45

Northeast - $22.71 - 0.0% - $22.71 - 0.0% - $22.71

North Loop West $26.17 $22.77 1.5% -3.6% $26.84 $21.84 -1.1% 0.4% $26.56 $21.94

Northwest Near $19.26 $15.69 1.5% -3.1% $19.48 $15.25 0.3% -0.4% $19.54 $15.19

Northwest Far - $18.38 - 7.3% - $19.71 - 0.1% - $19.72

Northwest $22.83 $18.71 4.4% -3.9% $23.34 $17.83 2.1% 0.8% $23.83 $17.98

South Main / Medical Center $32.34 $26.99 3.9% -12.9% $34.27 $27.87 -2.0% -15.7% $33.59 $23.50

E Fort Bend Co / Sugar Land $30.70 $22.73 2.3% 3.0% $31.52 $22.40 -0.4% 4.5% $31.41 $23.41

Southwest Beltway 8 $23.83 $15.92 -12.2% 16.5% $21.15 $18.92 -1.0% -2.0% $20.93 $18.54

Southwest / Hillcroft $19.50 - 1.3% - $19.58 $17.26 0.9% -3.1% $19.76 $16.72

Southwest Fwy / Sugar Land $27.30 $20.73 -11.7% -10.3% $24.07 $19.02 0.1% -2.2% $24.10 $18.60

The Woodlands $36.55 $23.65 -10.8% 9.5% $32.33 $25.18 0.9% 2.9% $32.62 $25.90

West Belt $27.12 $16.64 19.5% 47.7% $32.58 $21.86 -0.5% 12.4% $32.42 $24.58

Bellaire $27.68 $23.52 0.5% 2.5% $27.67 $23.56 0.5% 2.3% $27.81 $24.12

Galleria / Uptown $38.16 $29.16 2.9% -1.7% $39.14 $28.35 0.3% 1.1% $39.26 $28.66

Post Oak Park $39.70 $28.43 -7.3% -7.8% $38.75 $26.33 -5.0% -0.5% $36.79 $26.20

Richmond / Fountainview - $17.76 - 9.8% - $19.70 - -0.9% - $19.51

Riverway $34.74 $26.61 -4.6% -3.6% $33.10 $25.30 0.1% 1.3% $33.13 $25.65

San Felipe / Voss $35.90 $25.70 -0.2% 0.3% $36.50 $25.22 -1.8% 2.3% $35.82 $25.79

West Loop $37.13 $25.92 0.0% 0.3% $37.61 $25.56 -1.3% 1.7% $37.12 $26.00

Westchase $36.45 $20.01 -0.9% -0.7% $36.79 $19.26 -1.8% 3.2% $36.12 $19.87

TOTAL - Houston $36.66 $22.68 -1.9% -4.0% $36.30 $21.85 -1.0% -0.3% $35.94 $21.78

Houston Office Market Indicators - Asking Rental Rates

OVERVIEW

Harvey Delays Office Recovery Slightly While the office market has been under storm clouds for several quarters, the third quarter saw Hurricane Harvey eclipse the sun and pour over five feet of water on the Houston Metro area. Initial reports on the storm's capital impacts were significantly exaggerated as they were tethered to estimates based upon flood maps. However, a detailed review indicated that the storm damaged just under 70 office buildings with a net rentable area impact of 2.0 million square feet, or 0.8% of total supply, significantly less than initially anticipated. A lack of strong winds spared most office buildings from significant harm, leaving property damages mostly to parking garages, first and sub-floors as well as minor roof leaks. Of the properties damaged, over 75% were fully operational within two weeks of the event. The most tangible impact that Harvey had upon the Houston office market was essentially delaying the sectors recovery for an additional quarter.

NET ABSORPTION

2017 Year-to-Date Absorption Totals Negative 3.9M SFYear-to-date absorption totals of negative 3.9 million square feet continue to highlight the delayed impacts of the energy downturn as well as the trend of companies striving for efficiency and reducing their space footprint. Absorption for the quarter totaled negative 732,000 square feet and was equally distributed among classes. Class A properties totaled negative 360,000 square feet with the West Loop

HOUSTON OFFICE MARKETTHIRD QUARTER 2017

REAL ESTATE OUTLOOK

Hurricane Harvey Takes a Toll on HoustonSublease space decreases by 930K SF

NET ABSORPTION AND VACANCY RATE TRENDS HOUSTON METRO AREA

CONTIGUOUS BLOCKS OF AVAILABLE SPACE HOUSTON METRO

SOURCE CoStar, Transwestern *Through Q3 2017

SOURCE CoStar, Transwestern *Through Q3 2017

Note: Delivery of preleased space counts as positive net absorption

SF In

Thou

sand

s

Notable Q3 LeasesTENANT SF LEASE TYPE BUILDING SUBMARKET

NRG Energy 431,307 Sublease One Shell Plaza CBD

McDermott 186,000 Sublease Westway Plaza II West Belt

USCIS 100,020 Renewal Northpoint Plaza North District

EDF Trading 60,000 New Lease 601 Travis CBD

-4000-3000-2000-1000

010002000300040005000600070008000

Net Absorption

17*1615141312111009080706

Vacancy RateNet Absorption

0

50

100

150

200Class A SubletClass A Direct

200,000 SF100,000 SF50,000 SF25,000 SF

Class B SubletClass B Direct

and Central Business District primarily accounting for the negative absorption. Class B finished the third quarter with negative 398,000 square feet of absorption, due to space give backs in the Houston North District and the West Loop submarkets.

DIRECT VACANCY & TOTAL AVAIL ABILIT Y

Total Availability Declines While Vacancy RisesThe overall office availability rate (all space marketed as available for lease, both direct and sublet) decreased 0.3% over the quarter, ending at 23.3%. Class A properties drove the decrease, declining by 0.5% to finish the period at 24.4%. While Class B properties ticked up marginally, finishing at 23.0%.

Direct vacancy rose for the twelfth consecutive quarter, up 0.3% and closing at 15.4% overall. Class A properties saw vacancy increase by 0.2%, ending at 15.1%, while Class B properties were up 0.4% to 16.7%. Currently, over 1.5 million SF of sublease space is set to expire over the next 12 months, equating to roughly 20% of total sublease supply. This is especially pronounced in the North Houston District where 868,845 SF is set to expire by end of year 2018. As more sublease space expires city-wide, vacancy rates will continue to trend up.

RENTAL R ATES

Asking Rates Continue to AscendOverall asking rates for the Houston Metro area increased by 1.5% over the quarter and 2.0% over the year, finishing the period at $30.92 PSF full service. Despite the increase in asking rates, concessions remain elevated throughout the market with generous concession packages and tenant improvement allowances being offered in order to maintain the highest rent figures.

Class A rates closed the quarter up 0.6% (+$0.20), ending at $35.83 PSF full service, while Class B asking rates declined by 1.2%, ending at $21.97 PSF full service. The submarkets with the highest asking rents are the Katy Fwy East ($45.00 PSF), the Central Business District ($44.35 PSF) and Galleria/Uptown ($38.83 PSF).

SUPPLY AND DEVELOPMENT

Development Pipeline Remains in CheckHouston area construction activity has slowed greatly due to both the delivery of over 33.0M SF in the past seven years and the downturn in the energy sector. Given the ample amount of space currently on the market for lease, developers are wary of additional speculative construction. Still, as tenants strive to retain talent and attain efficiency both in their space footprint as well as their operating expenses, the potential for additional construction tethered to a lead tenant remains high. Specifically, in core office submarkets such as the CBD, the Woodlands and West Loop. At the close of the third quarter, the Houston construction pipeline totaled 2.3 million square feet and is currently 52.5% preleased.

Office Under ConstructionHouston Metro | Q3 2017

SUBMARKET NUMBER OF BLDGS SF % PRE-

LEASED

CBD 1 778,344 27.0%

Woodlands 2 515,800 100.0%E Fort Bend Co/Sugar Land 3 247,200 30.1%

Greenway Plaza 1 188,547 0.0%

Westchase 1 187,011 80.9%

Northeast 1 115,601 100.0%

West Loop 1 104,579 46.8%

Energy Corridor 1 86,255 61.5%

Katy 1 72,045 50.8%

Total 12 2,295,382 52.5%

AVERAGE OFFICE RENTS HOUSTON METRO AREA

SOURCE CoStar, Transwestern *Through Q3 2017 Note: All classes of office space

Total Available SpaceHouston Metro | Q3 2017

SUBMARKETSUBLEASE SPACE (SF)

% OF SUPPLY

SUBMARKET % TOTAL

AVAILABLE

Energy Corridor 2,386,277 6.6% 25.3%

CBD 2,178,987 5.0% 25.8%

Westchase 1,543,705 8.8% 29.0%

Galleria 842,634 5.0% 21.3%

North District 877,698 6.8% 48.8%

All of Houston 9,829,433 4.1% 23.3%

$15

$20

$25

$30

$35

$40Class BClass AOverall

17*1615141312111009080706

2 REAL ESTATE OUTLOOK HOUSTON METRO Q3 2017

HOUSTON METRO MARKETTHIRD QUARTER 2017

The largest projects currently under construction are Capitol Tower (CBD, 778,000 SF - 27% leased to Bank of America), CityPlace 3 (The Woodlands, 328,000 SF - 100% Leased to HP), CityPlace 2 (The Woodlands, 326,000 SF - 100% Leased to ABS) and The Kirby Collection, a mixed-use project with a significant office component (Greenway Plaza, 212,000 SF, 0% preleased).

INVESTMENT MARKET

Houston Investment Market is Red-HotHarvey had little impact on Houston's investment market as a flurry of activity took place throughout the quarter. The underlying fundamentals of the market are strong and stabilization in the energy sector should begin to avail itself over the next 9-12 months, keeping sentiment positive amongst the investor community. Sales for the quarter (including the under contract Houston Center), totaled $1.4 billion and were comprised of 15 transactions.

The most significant transaction of the third quarter was Brookfield Properties acquisition of Houston Center from JPMorgan Asset Management. The four building portfolio located in Houston's Central Business District totals over 4.0 million square feet and is under contract for approximately $875 million. Additionally, Bank of America corporation acquired Energy Center IV from Trammell Crow Company for $275 million or $461.00 PSF (6.0% cap rate). The 597,000 square foot Class A facility is located in the Katy Fwy West submarket and is under long-term lease to ConocoPhillips.

The market remains full of potential with a plethora of well located infill properties representing value add opportunities to investors. As such, investment activity should remain strong through the balance of 2017. These figures represent assets for which pricing information could be obtained.

COMPARATIVE OFFICE INVESTMENT SALES VOLUME SELECT METRO AREAS

SOURCE Real Capital Analytics, Transwestern ,*Through Q3 2017

AVERAGE OFFICE SALE PRICE HOUSTON METRO AREA

SOURCE Real Capital Analytics, Transwestern,*Through Q3 2017

Notable Q3 TransactionsBUILDING SUBMARKET SF SALE PRICE SELLER BUYER

Houston Center CBD 4,200,000 $875.0 million(under contract) JPMorgan Asset Management Brookfield Asset Management

Greenspoint Plaza North District 2,080,000 N/A Northwestern Mutual Lincoln Property Co & H.I.G. Realty Partners joint venture

Energy Center IV Katy Freeway West 597,000 $275.0 million Trammell Crow Company Bank of America Corporation

1700 W Loop S Galleria/Uptown 272,941 $52.0 million Bridge Investment Group Lingerfelt Commonwealth Partners

SOURCE Real Capital Analytics, HFF, Transwestern

Sales

Volu

me i

n Billi

ons

$0

$1

$2

$3

$4

$5

$6

$7

$8HoustonDenverDallasAtlanta

17*1615141312111009080706

$0

$50

$100

$150

$200

$250 Average Sale Price Per SF

17*1615141312111009080706

REAL ESTATE OUTLOOK HOUSTON METRO Q3 2017 3

OUTLOOK

Light at the End of the Tunnel?The Houston office market has been in limbo for several quarters as office using job growth has been all but non-existent following the energy sector downturn. Large swaths of expiring sublease space compete head-to-head with direct vacant blocks and recent activity has been a shuffling of tenants as opposed to expansionary. While diversification in industries such as healthcare, petrochemical, distribution and retail/hospitality have helped offset many of the jobs lost in the energy sector, there is little doubt that the market needs a return to form for crude prices or the emergence of an alternative industry to help alleviate the vacant and available supply. As such, eyes will continue to focus upon Houston's strategy to support Tech growth, North American crude inventories, OPEC’s willingness to maintain production cuts, and the resulting impacts to the spot price of WTI.

Overall market activity is projected to remain flat through the remainder of the year as leasing activity continues to fall below historical averages. Tenants with near term expirations are in a favorable market to extend early and lock in favorable terms. The energy sector will continue to see Mergers and acquisitions at a rapid pace leaving the potential for additional blocks of space to be brought on-line due to redundancies.

Multi-tenant market vs Transwestern comprehensive market coverage

MULTI-TENANT ENTIRE MARKET

Inventory 199.2 MSF 241.8 MSF

Overall Vacancy 21.0% 17.1%

Q3 Net Absorption (291,372) SF (3,993,708) SF

WHY OUR METHODOLOGY IS THE BEST INDICATOR OF CURRENT MARKET CONDITIONSWe include owner occupied and single-tenant buildings in our inventory, vacancy and absorption statistics to capture more market activity than many of our competitors. This allows us to better correlate changes in the market with changes in employment. As single-tenant space does compete with multi-tenant space, we believe it is critical to understand all components of the market. The inclusion of single-tenant and owner-occupied space tends to yield lower vacancy rates and higher absorption totals than some of our competitors’ results, but our coverage of the market is more comprehensive.

OFFICE ABSORPTION AND EMPLOYMENT HOUSTON METRO AREA

SOURCE Bureau of Labor Statistics, Transwestern *12-month job growth through May 2017, net absorption YTD through Q2 2017

-4000

-2700

-1400

-100

1200

2500

3800

5100

6400

7700

9000Net Absorption (Thousands of SF)

17*1615141312111009080706-80

-60

-40

-20

0

20

40

60

80

100

120Payroll Job Growth (in Thousands)

4 REAL ESTATE OUTLOOK HOUSTON METRO Q3 2017

HOUSTON METRO MARKETTHIRD QUARTER 2017

Houston Office Market Indicators - All Space

SUBMARKET TOTAL BLDGS INVENTORY SF AVAILABLE

IMMEDIATELY

DIRECT VACANCY

Q3 2017

VACANCY W/ SUBLET

Q3 2017

TOTAL AVAILABILITY

Q3 2017

UNDER CONSTRUCTION

NET ABSORPTION Q3 2017

NET ABSORPTION YTD 2017

Conroe 13 920,281 49,898 5.4% 5.9% 9.8% 116 49,451

Central Business District 62 43,693,078 7,023,493 16.1% 17.9% 25.8% 778,344 (62,154) (1,473,646)

Midtown 32 5,664,375 639,580 11.3% 11.8% 17.3% - (32,479) 52,843

Downtown 94 49,357,453 7,663,073 15.5% 17.2% 24.8% 778,344 (94,633) (1,420,803)

FM 1960 / Champions 23 1,900,382 335,845 17.7% 17.7% 21.5% - (26,340) 1,339

FM 1960 / Highway 249 37 5,148,719 483,854 9.4% 11.1% 15.9% - (9,937) (9,539)

FM 1960 / I-45 North 15 1,325,458 361,994 27.3% 27.8% 34.2% - (48,238) (35,966)

FM 1960 75 8,374,559 1,181,693 14.1% 15.2% 20.0% - (84,515) (44,166)

Greenway Plaza 48 11,095,766 1,413,238 12.7% 13.2% 19.4% 188,547 4,920 (111,005)

Gulf Freeway/Pasadena 33 2,642,527 294,851 11.2% 11.2% 17.4% - 2,042 16,224

Katy Far West 27 2,954,733 360,241 12.2% 12.7% 16.7% 72,045 15,234 137,815

Katy Freeway East 60 9,674,691 935,320 9.7% 10.1% 16.4% - (81,816) (136,869)

Katy Freeway West 141 26,654,315 4,484,804 16.8% 20.5% 28.5% 86,255 (95,822) (540,187)

Katy Frwy / Energy Corridor 201 36,329,006 5,420,124 14.9% 17.7% 25.3% 86,255 (177,638) (677,056)

Kingwood / Humble* 11 1,234,389 30,190 2.4% 2.4% 2.6% - 6,497 3,174

NASA / Clear Lake 53 5,613,374 1,006,896 17.9% 18.8% 22.6% - 25,788 (30,925)

North District / IAH 20 2,759,860 767,085 27.8% 28.0% 30.6% - (16,346) (176,722)

North District / North Belt W 75 10,184,568 4,290,148 42.1% 44.8% 53.7% - (155,687) (434,901)

North District / North Belt 95 12,944,428 5,057,233 39.1% 41.2% 48.8% - (172,033) (611,623)

Northeast 11 1,370,813 85,167 6.2% 6.2% 10.0% 115,601 (32,465) (23,029)

North Loop West 29 3,955,285 673,622 17.0% 17.1% 20.9% - 3,436 (39,389)

Northwest Far 30 3,339,250 739,776 22.2% 22.3% 27.9% - 30,761 56,167

Northwest Near 12 1,290,803 28,959 2.2% 2.5% 3.4% - 1,153 (10,968)

Northwest 71 8,585,338 1,442,357 16.8% 16.9% 21.0% - 35,350 5,810

South Main / Medical Center 47 10,338,924 616,556 6.0% 6.1% 7.9% - 19,648 6,440

E Fort Bend Co / Sugar Land 47 6,284,708 457,834 7.3% 8.9% 15.9% 187,200 (46,534) (28,854)

Southwest Beltway 8 41 5,546,947 814,433 14.7% 14.8% 22.9% 60,000 16,526 (14,400)

Southwest / Hillcroft 36 4,321,807 612,462 14.2% 14.9% 23.7% - 5,889 (29,672)

Southwest Fwy / Sugar Land 124 16,153,462 1,884,729 11.7% 12.5% 20.4% 247,200 (24,119) (72,926)

The Woodlands 96 16,485,335 1,609,344 9.8% 10.1% 12.4% 515,800 23,886 (44,655)

West Belt 37 5,387,946 784,684 14.6% 19.3% 36.7% - 26,910 75,278

Bellaire 28 4,302,857 433,933 10.1% 10.3% 14.9% - (75,343) (53,386)

Galleria / Uptown 58 16,833,939 2,266,941 13.5% 16.6% 21.3% 104,579 (128,316) (441,417)

Post Oak Park 27 4,581,030 1,025,783 22.4% 23.8% 28.5% - (76,997) (290,005)

Richmond / Fountainview 11 829,982 157,202 18.9% 18.9% 10.7% - 12,883 28,970

Riverway 16 2,868,522 594,885 20.7% 22.1% 24.4% - (20,378) (256,789)

San Felipe / Voss 33 5,060,157 917,168 18.1% 18.0% 24.5% - (74,428) (91,718)

West Loop 173 34,476,487 5,395,912 15.7% 17.5% 21.9% 104,579 (362,579) (1,104,345)

Westchase 89 17,585,648 2,873,713 16.3% 20.5% 29.0% 187,011 55,368 (147,367)

TOTAL - Houston 1,298 241,850,469 37,169,899 15.4% 17.1% 23.3% 2,295,382 (732,223) (3,993,708)

SOURCE CoStar, Transwestern

NOTE Includes buildings 50,000 SF RBA and greater; does not include buildings under construction or owned by the government

-

REAL ESTATE OUTLOOK HOUSTON METRO Q3 2017 5

Houston Office Market Indicators - Class A

SUBMARKET TOTAL BLDGS INVENTORY SF AVAILABLE

IMMEDIATELY

DIRECT VACANCY

Q3 2017

VACANCY W/ SUBLET

Q3 2017

TOTAL AVAILABILITY

Q3 2017

UNDER CONSTRUCTION

NET ABSORPTION

Q3 2017

NET ABSORPTION

YTD 2017

Conroe 2 128,832 13,011 10.1% 10.1% 14.3% - (3,763) (3,763)

Central Business District 37 34,033,274 4,366,244 12.8% 14.9% 23.3% 778,344 (99,593) (1,160,237)

Midtown 8 2,486,094 394,782 15.9% 16.8% 25.0% - (20,358) (23,305)

Downtown 45 36,519,368 4,761,026 13.0% 15.1% 23.4% 778,344 (119,951) (1,183,542)

FM 1960 / Champions 1 150,000 0.0% 0.0% 0.0% -

FM 1960 / Highway 249 17 3,729,412 296,314 7.9% 8.4% 10.5% - 19,013 12,705

FM 1960 / I-45 North 2 206,705 54,512 26.4% 26.4% 26.4% - (25,387)

FM 1960 20 4,086,117 350,826 8.6% 9.0% 10.9% - 19,013 (12,682)

Greenway Plaza 20 7,356,944 991,921 13.5% 13.9% 22.4% 188,547 25,460 (22,416)

Gulf Freeway/Pasadena 0 - - - - - - - -

Katy Far West 15 1,560,283 358,018 22.9% 23.8% 31.1% 72,045 15,234 120,782

Katy Freeway East 24 5,761,894 648,374 11.3% 11.6% 18.4% - (56,676) (127,936)

Katy Freeway West 72 18,772,511 2,846,601 15.2% 20.1% 28.1% 86,255 (10,403) (290,885)

Katy Frwy / Energy Corridor 96 24,534,405 3,494,975 14.2% 18.1% 25.8% 86,255 (67,079) (418,821)

Kingwood / Humble 2 144,312 7,466 5.2% 5.2% 6.5% - 1,927 1,927

NASA / Clear Lake 15 2,028,136 102,561 5.1% 7.3% 13.6% - 12,699 (17,066)

North District / IAH 8 1,213,677 563,373 46.4% 46.9% 48.6% - (12,657) (165,750)

North District / North Belt W 17 4,334,810 2,213,029 51.1% 56.7% 66.5% - 14,091 (148,064)

North District / North Belt 25 5,548,487 2,776,402 50.0% 54.5% 62.6% - 1,434 (313,814)

Northeast 3 640,700 32,465 5.1% 5.1% 5.1% - (32,465) (32,465)

North Loop West 6 1,240,544 355,226 28.6% 28.8% 30.2% - 10,736 (28,636)

Northwest Near 4 797,237 326,246 40.9% 41.4% 42.7% - (10,157) 9,509

Northwest Far 1 237,384 - 0.0% 0.0% 0.0% -

Northwest 11 2,275,165 681,472 30.0% 30.2% 31.4% - 579 (19,127)

South Main / Medical Center 16 4,810,992 179,545 3.7% 3.9% 6.3% - 18,818 (15,745)

E Fort Bend Co / Sugar Land 21 3,867,531 277,757 7.2% 9.4% 14.8% 94,200 (44,458) (50,191)

Southwest Beltway 8 3 566,699 82,955 14.6% 14.6% 16.3% - (34,000) (34,355)

Southwest / Hillcroft 6 1,487,219 225,793 15.2% 17.3% 35.2% - (1,392) 2,656

Southwest Fwy / Sugar Land 30 5,921,449 586,505 9.9% 11.9% 20.1% 94,200 (79,850) (81,890)

The Woodlands 44 11,752,920 1,219,960 10.4% 10.8% 12.3% 704,800 (15,665) (32,754)

West Belt 23 4,085,321 633,381 15.5% 19.9% 34.8% - 26,910 29,999

Bellaire 8 1,470,637 167,634 11.4% 11.9% 21.3% - (1,882) 17,851

Galleria / Uptown 35 13,491,405 1,899,069 14.1% 18.0% 22.8% 104,579 (106,168) (433,814)

Post Oak Park 9 2,617,868 810,471 31.0% 33.5% 37.9% - (37,037) (259,074)

Riverway 0 - - - - - - - -

Richmond / Fountainview 5 1,885,813 408,974 21.7% 23.6% 25.6% - (19,644) (233,225)

San Felipe / Voss 3 1,720,793 397,299 23.1% 22.2% 31.7% - (39,729) (8,130)

West Loop 60 21,186,516 3,683,447 17.4% 20.3% 25.5% 104,579 (204,460) (916,392)

Westchase 33 9,958,830 1,637,676 16.4% 23.4% 32.4% 187,011 40,941 (118,260)

TOTAL - Houston 460 142,538,777 21,510,657 15.1% 17.7% 24.5% 2,026,781 (360,218) (3,036,029)

SOURCE CoStar, Transwestern

NOTE Includes buildings 50,000 SF RBA and greater; does not include buildings under construction or owned by the government

6 REAL ESTATE OUTLOOK HOUSTON METRO Q3 2017

HOUSTON METRO MARKETTHIRD QUARTER 2017

SOURCE CoStar, Transwestern

NOTE Includes buildings 50,000 SF RBA and greater; does not include buildings under construction or owned by the government

Houston Office Market Indicators - Class B

SUBMARKET TOTAL BLDGS INVENTORY SF AVAILABLE

IMMEDIATELY

DIRECT VACANCY

Q3 2017

VACANCY W/ SUBLET

Q3 2017

TOTAL AVAILABILITY

Q3 2017

UNDER CONSTRUCTION

NET ABSORPTION

Q3 2017

NET ABSORPTION

YTD 2017

Conroe 10 688,859 36,887 5.4% 6.0% 10.4% - 3,879 53,214

Central Business District 23 9,439,750 2,634,092 27.9% 28.7% 35.1% - 37,439 (304,898)

Midtown 20 2,955,580 188,485 6.4% 6.5% 10.3% - (12,121) 82,461

Downtown 43 12,395,330 2,822,577 22.8% 23.4% 29.2% - 25,318 (222,437)

FM 1960 / Champions 20 1,630,186 325,905 20.0% 20.1% 24.4% - (16,400) 4,939

FM 1960 / Highway 249 18 1,315,795 181,048 13.8% 19.0% 31.3% - (29,458) (34,032)

FM 1960 / I-45 North 11 968,736 256,253 26.5% 27.1% 35.9% - (48,238) (14,923)

FM 1960 49 3,914,717 763,206 19.5% 21.4% 29.6% - (94,096) (44,016)