Embed Size (px)

DESCRIPTION

Su Han Chan, John Erickson and Ko Wangv The only book that provides a systematic and comprehensive look at the REITs industry.

Citation preview

1

Real Estate Investment Trusts Structure, Performance and Investment Opportunities

Su Han Chan, John Erickson and Ko Wang v The only book that provides a systematic and comprehensive look at the REITs industry.

here are currently around 200 publicly traded Real Estate Investment Trusts (REITs) operating in the United States and their equity values total about $160 billion. Originating just a little over a century ago, most analysts would agree that REITs have proven their eligibility as a good way for investors to diversify their portfolios.

They were, in fact, created to allow institutional and individual investors to invest in real estate via a corporate entity. While they trade like stocks, their market path most often tracks in a different direction - often outperforming the stock market in tough times and declining over the term of aggressive equity bull markets.

REAL ESTATE INVESTMENT TRUSTS: Structure, Performance and Investment Opportunities analyzes and synthesizes the existing scholarly research on REITs in a way that will enable managers to improve their investment decisions and the operating performance of their REITs portfolios. This book is designed to help investors evaluate REITs and identify those with the greatest investment potential. It also provides the investing public, real estate practitioners, regulators, and real estate and finance academics with up-to-date information on what modern scholarly research tells us about REITs. Also included is up-to-date original research on REITs based on the authors’ own database, which is the most extensive data base available on REITs that is free of survivorship bias. As well as offering a broad understanding of the evolution of this important industry, this book discusses the likely future prospects of this unique investment vehicle. This book is one of the newest additions to the Financial Management Association's (FMA) Survey and Synthesis Series. AVAILABLE OCTOBER 2002 copyright 2003; 352 pp., 6-1/8 x 9-1/4

0-19-515534-3 $45.00

The Authors Su Han Chan is a Professor of Finance at California State University-Fullerton and a Visiting Professor at the School of Business, University of Hong Kong. She has published in the leading finance and real estate journals on various topics including REITs and co-authored 19 teaching cases. She currently serves on the editorial board of the Financial Management Association’s Survey and Synthesis Series, the Journal of Real Estate Research and the International Real Estate Review. John Erickson is a Professor and the Chair of Finance at California State University-Fullerton. He has published articles on REITs in Real Estate Economics and the Journal of Real Estate Research. He has also published in the Journal of Finance and the Journal of Law and Economics. Ko Wang is a Professor of Real Estate and Finance at California State University-Fullerton and an Honorary Professor at the Chinese University of Hong Kong. He has published extensively in the leading real estate and finance journals on various topics including REITs, co-edited a monograph on real estate valuation theory, and co-authored 19 teaching cases. He is the editor of the Journal of Real Estate Research, the founding executive editor of International Real Estate Review, and an associate editor of seven other journals.

T

2

Advance Praise for Real Estate Investment Trusts: "REITs provide a convenient and liquid structure that allows investors to hold a diversified portfolio of commercial real estate. The use of this investment vehicle is likely to continue to grow, both in the U.S. and abroad. Authors Chan, Erickson, and Wang provide an excellent comprehensive analysis of the REIT market that is sure to be a valuable resource for stock market investors interested in diversification opportunities and real estate professionals interested in REITs as funding vehicles."

Sheridan Titman McAllister Centenial Chair in Financial Services Department of Finance University of Texas

"Most previous treatises on REITs suffer from their excessive focus on institutional and legal structure alone, devoid of the broader existence of REITs within the real estate and capital markets. Chan, Erickson, and Wang stands out in this regard. It is the first effort to integrate the latest academic insights from the economics and finance literature with the relevant applied issues faced by investment professionals to create a truly useful text -- an invaluable reference guide that will become the standard against which all subsequent efforts will be judged.”

Kerry D. Vandell Tiefenthaler Chair in Real Estate and Urban Land Economics Director, Center for Urban Land Economics Research University of Wisconsin-Madison

"Mssrs. Chan, Erickson, and Wang have created a first-class book about Real Estate Investment Trusts, with a timely and interesting integration of academic knowledge and the frontier of practitioner activities. The book is informative and analytic, yet, quite readable for the sophisticated lay-audience. The book provides an unusually balanced presentation among analytic-theoretic issues, pragmatic real estate activities, and public markets behavior. The book demonstrates a special sensitivity about how the United States' experience with real estate investment trusts may parallel and extend the inexorable trend towards the real estate securitization throughout the world."

Robert H. Edelstein Chairholder, Real Estate Development Professorship Co-chair, Fisher Center for Real Estate & Urban Economics Haas School of Business University of California at Berkeley

“Authors Chan, Erickson, and Wang have done a masterful job of explaining the world of REITs from the perspective of a very experienced financial analyst but in a fashion that less experienced reader can easily follow and understand. As finance investors have begun to recognize the enormous profit opportunities in inner cites and distressed communities, REIT is one vehicle that both community development professions and Wall Street analysts are examining to help bring private capital to distressed communities.”

Isaac Megbolugbe Vice President of Fannie Mae Foundation's Office of Research & Adjunct Professor of City and Regional Planning, University of Pennsylvania

“The REIT industry has changed dramatically over the last decade, and Real Estate Investment Trusts provides the most up-to-date view of industry available today. Understanding the complexities and nuances of modern REITs is very important to making good investment decisions, thus Real Estate Investment Trusts is a must for any investor interested in REITs. This book will also help investors understand a REIT analyst's thought process and better interpret their reports.”

Glenn R. Mueller Professor at Johns Hopkins University Real Estate Institute and Real Estate Investment Strategist on Legg Mason's REIT Research Team.

3

ORDERING INFORMATION Qty Title ISBN Price

___ REAL ESTATE INVESTMENT TRUSTS: Structure, Performance 0-19-515343 $45.00

and Investment Opportunities (Available OCTOBER 2002) Subtotal $ ________ CA, CT and NC Residents add appropriate sales tax $ ________ Shipping (Please add $5.00 for the first book plus $1.25 for each additional book) TOTAL $ ________ v Call (800) 451-7556 or fax this form to 1-919-677-1303 v Order online at www.oup-usa.org v Send completed form to: OXFORD UNIVERSITY PRESS, Attention: Order Department, 2001 Evans Road, Cary, NC 27513 q P.O. Number_____________________________________________ q Enclosed is a check or money order for $__________ q Please charge my credit card: ____VISA ____ MasterCard ____American Express Credit card no. ______________________________ Exp. date ________________________ Signature___________________________________ (Required on all credit card purchases) ________________________________

BILL TO: SHIP TO (IF DIFFERENT FROM BILL TO): Name ____________________________________ Name____________________________________

Address ___________________________________ Address __________________________________

City, State, Zip ____________________________ City, State, Zip ____________________________

Real Estate Trusts• Currently, the only book available to provide an up-to-date,

systematic and comprehensive look at the REIT industry• Shows how to invest in REITs• Helps identify those REITs with the greatest

investment potential• Includes authors’ exclusive database which

tracks REITs performance• Contains original research never before

published on REITs security offeringsand the role REITs play in countriesoutside the USA

• Looks at the future of REITs-likelytrends, changes and regulation

“ Chan, Ericksonand Wang provide anexcellent and com-prehensive analysisof the REITs market that issure to be a valuable resource for stockmarket investors interested in diversification opportunities andreal estate professionals interested in REITs as funding vehicles.”

$45.00 352pp.0-19-515534-3

To Order, call 1-800-451-7556 or visit www.oup-usa.orgFor more about this title and other Oxford Finance titles, visit www.oup-fma.org

Oxford Finance-What Today’s “Scholar-Professionals” Need To Know

O x f o r d U n i v e r s i t y Pre s s A n n o u n c e s

Real Estate Trusts

—SHERIDAN TITMAN, McAllister Centennial Chair inFinancial Services, Department of Finance, University ofTexas-Austin

Investment Investment

Chan, Erickson, and Wang

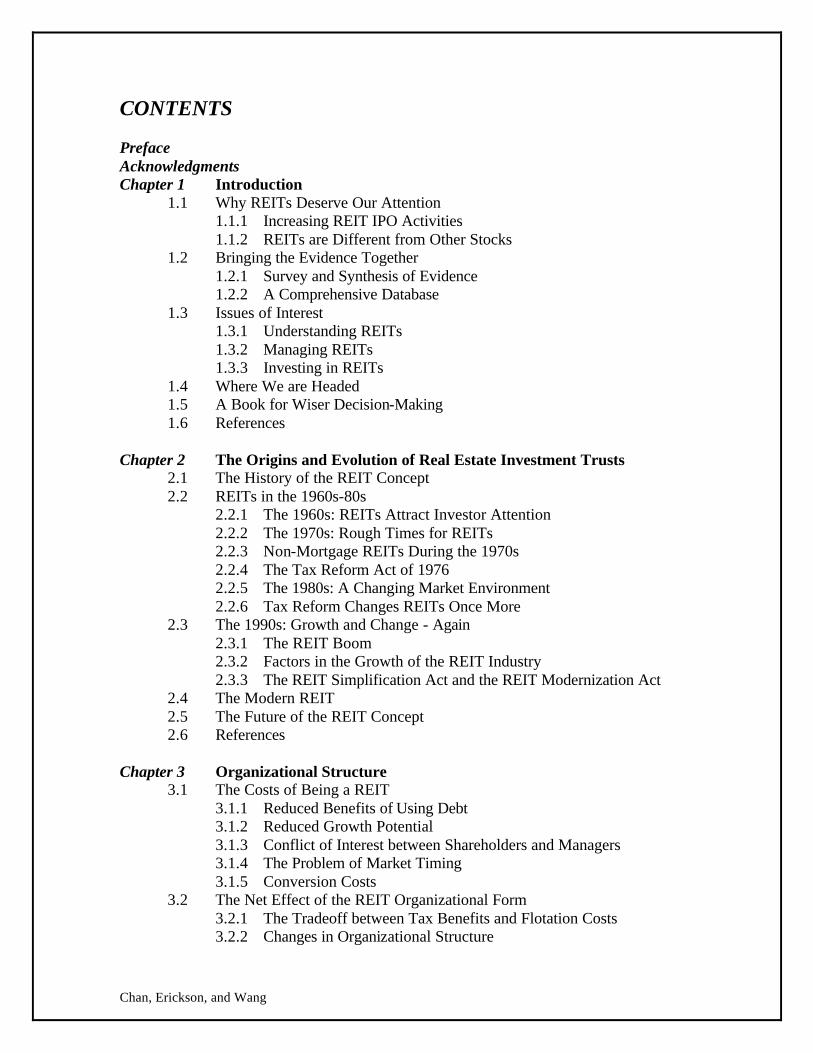

CONTENTS Preface Acknowledgments Chapter 1 Introduction

1.1 Why REITs Deserve Our Attention 1.1.1 Increasing REIT IPO Activities 1.1.2 REITs are Different from Other Stocks

1.2 Bringing the Evidence Together 1.2.1 Survey and Synthesis of Evidence 1.2.2 A Comprehensive Database

1.3 Issues of Interest 1.3.1 Understanding REITs 1.3.2 Managing REITs 1.3.3 Investing in REITs

1.4 Where We are Headed 1.5 A Book for Wiser Decision-Making 1.6 References

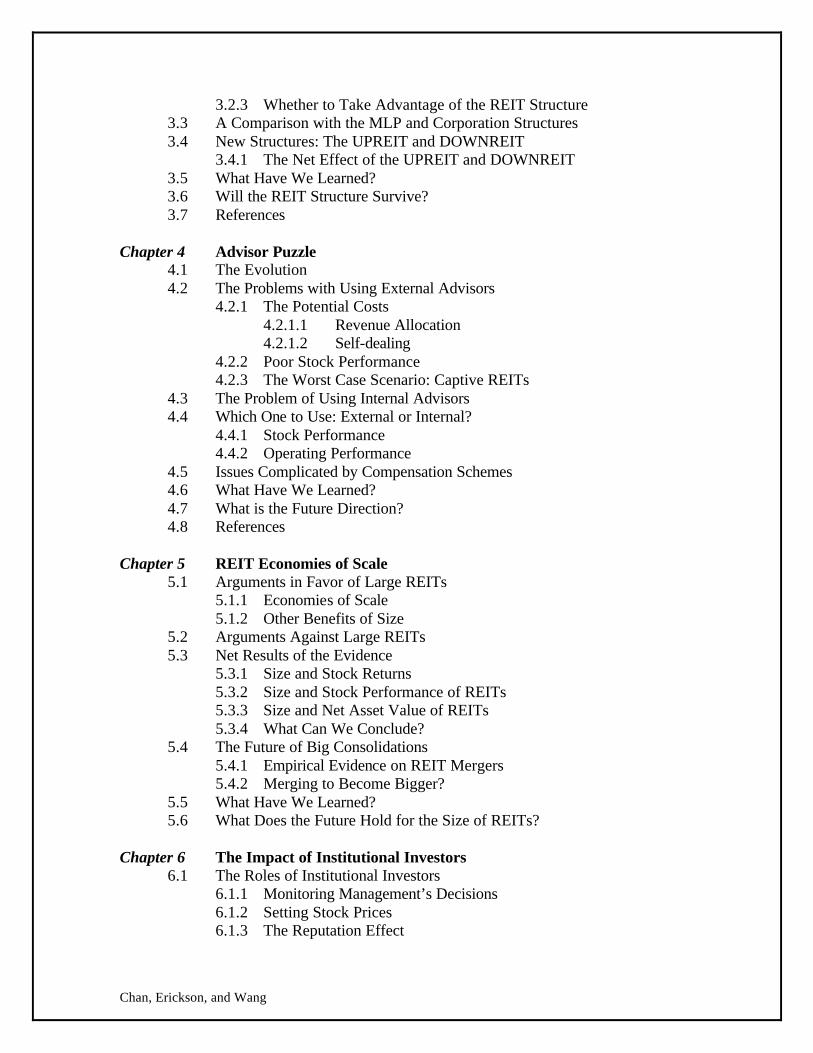

Chapter 2 The Origins and Evolution of Real Estate Investment Trusts

2.1 The History of the REIT Concept 2.2 REITs in the 1960s-80s

2.2.1 The 1960s: REITs Attract Investor Attention 2.2.2 The 1970s: Rough Times for REITs 2.2.3 Non-Mortgage REITs During the 1970s 2.2.4 The Tax Reform Act of 1976 2.2.5 The 1980s: A Changing Market Environment 2.2.6 Tax Reform Changes REITs Once More

2.3 The 1990s: Growth and Change - Again 2.3.1 The REIT Boom 2.3.2 Factors in the Growth of the REIT Industry 2.3.3 The REIT Simplification Act and the REIT Modernization Act

2.4 The Modern REIT 2.5 The Future of the REIT Concept 2.6 References

Chapter 3 Organizational Structure

3.1 The Costs of Being a REIT 3.1.1 Reduced Benefits of Using Debt 3.1.2 Reduced Growth Potential 3.1.3 Conflict of Interest between Shareholders and Managers 3.1.4 The Problem of Market Timing 3.1.5 Conversion Costs

3.2 The Net Effect of the REIT Organizational Form 3.2.1 The Tradeoff between Tax Benefits and Flotation Costs 3.2.2 Changes in Organizational Structure

Chan, Erickson, and Wang

3.2.3 Whether to Take Advantage of the REIT Structure 3.3 A Comparison with the MLP and Corporation Structures 3.4 New Structures: The UPREIT and DOWNREIT

3.4.1 The Net Effect of the UPREIT and DOWNREIT 3.5 What Have We Learned? 3.6 Will the REIT Structure Survive? 3.7 References

Chapter 4 Advisor Puzzle

4.1 The Evolution 4.2 The Problems with Using External Advisors

4.2.1 The Potential Costs 4.2.1.1 Revenue Allocation 4.2.1.2 Self-dealing

4.2.2 Poor Stock Performance 4.2.3 The Worst Case Scenario: Captive REITs

4.3 The Problem of Using Internal Advisors 4.4 Which One to Use: External or Internal?

4.4.1 Stock Performance 4.4.2 Operating Performance

4.5 Issues Complicated by Compensation Schemes 4.6 What Have We Learned? 4.7 What is the Future Direction? 4.8 References

Chapter 5 REIT Economies of Scale

5.1 Arguments in Favor of Large REITs 5.1.1 Economies of Scale 5.1.2 Other Benefits of Size

5.2 Arguments Against Large REITs 5.3 Net Results of the Evidence

5.3.1 Size and Stock Returns 5.3.2 Size and Stock Performance of REITs 5.3.3 Size and Net Asset Value of REITs 5.3.4 What Can We Conclude?

5.4 The Future of Big Consolidations 5.4.1 Empirical Evidence on REIT Mergers 5.4.2 Merging to Become Bigger?

5.5 What Have We Learned? 5.6 What Does the Future Hold for the Size of REITs?

Chapter 6 The Impact of Institutional Investors

6.1 The Roles of Institutional Investors 6.1.1 Monitoring Management’s Decisions 6.1.2 Setting Stock Prices 6.1.3 The Reputation Effect

Chan, Erickson, and Wang

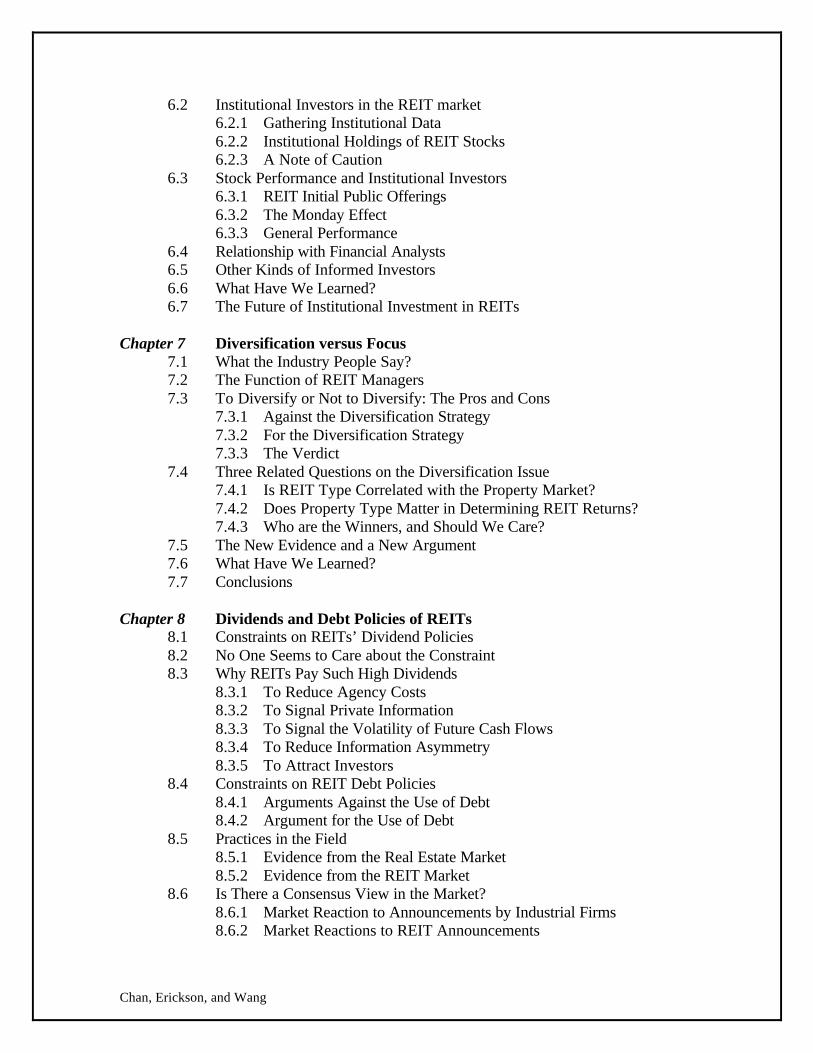

6.2 Institutional Investors in the REIT market 6.2.1 Gathering Institutional Data 6.2.2 Institutional Holdings of REIT Stocks 6.2.3 A Note of Caution

6.3 Stock Performance and Institutional Investors 6.3.1 REIT Initial Public Offerings 6.3.2 The Monday Effect 6.3.3 General Performance

6.4 Relationship with Financial Analysts 6.5 Other Kinds of Informed Investors 6.6 What Have We Learned? 6.7 The Future of Institutional Investment in REITs

Chapter 7 Diversification versus Focus

7.1 What the Industry People Say? 7.2 The Function of REIT Managers 7.3 To Diversify or Not to Diversify: The Pros and Cons

7.3.1 Against the Diversification Strategy 7.3.2 For the Diversification Strategy 7.3.3 The Verdict

7.4 Three Related Questions on the Diversification Issue 7.4.1 Is REIT Type Correlated with the Property Market? 7.4.2 Does Property Type Matter in Determining REIT Returns? 7.4.3 Who are the Winners, and Should We Care?

7.5 The New Evidence and a New Argument 7.6 What Have We Learned? 7.7 Conclusions

Chapter 8 Dividends and Debt Policies of REITs

8.1 Constraints on REITs’ Dividend Policies 8.2 No One Seems to Care about the Constraint 8.3 Why REITs Pay Such High Dividends

8.3.1 To Reduce Agency Costs 8.3.2 To Signal Private Information 8.3.3 To Signal the Volatility of Future Cash Flows 8.3.4 To Reduce Information Asymmetry 8.3.5 To Attract Investors

8.4 Constraints on REIT Debt Policies 8.4.1 Arguments Against the Use of Debt 8.4.2 Argument for the Use of Debt

8.5 Practices in the Field 8.5.1 Evidence from the Real Estate Market 8.5.2 Evidence from the REIT Market

8.6 Is There a Consensus View in the Market? 8.6.1 Market Reaction to Announcements by Industrial Firms 8.6.2 Market Reactions to REIT Announcements

Chan, Erickson, and Wang

8.7 What Have We Learned? 8.8 Conclusions

Chapter 9 REIT Security Offerings

9.1 What Is Unique About REIT IPOs? 9.1.1 Uncertainty About the Value of the Properties 9.1.2 The Buyers of REIT IPOs 9.1.3 The Fund-Like Organizational Structure

9.2 Empirical Evidence on REIT IPOs 9.2.1 Data Collection 9.2.2 IPO Activities 9.2.3 Pricing of REIT IPOs

9.3 Factors Determining the Initial-Day Return 9.3.1 Underwriter and Stock Listing 9.3.2 Institutional Investors 9.3.3 The Distribution Method 9.3.4 Valuation Uncertainty 9.3.5 Fund Duration

9.4 The Changing Nature of REITs: Pre- and Post-1990 9.4.1 Changes in Organizational Structure 9.4.2 Ownership of REIT Shares

9.5 The Lesson We Learned 9.6 Price Performance Following IPOs 9.7 Secondary Offerings of REIT Securities

9.7.1 Secondary-Offering Activities 9.7.2 Performance of REIT SEOs 9.7.3 Which Types of REITs Should Use SEOs?

9.8 Link between IPOs and SEOs 9.9 What Have We Learned? 9.10 Conclusions

Chapter 10 The Performance of REIT Stocks

10.1 REIT Stocks and Unsecuritized Real Estate 10.1.1 Common Factors 10.1.2 Unique Factors 10.1.3 Is There a General Consensus?

10.1.3.1 Evidence for Integration 10.1.3.2 Evidence for Partial or No Integration

10.1.4 Is There a Compromise? 10.2 The Risk and Return Characteristics of REITs

10.2.1 REIT Stocks versus the Stock Market 10.2.1.1 The General Trend of the Evidence 10.2.1.2 Performance by Subperiod 10.2.1.3 Overall REIT Performance

10.2.2 REITs and Asset Type 10.2.3 Market Factors Affecting REIT Stocks

Chan, Erickson, and Wang

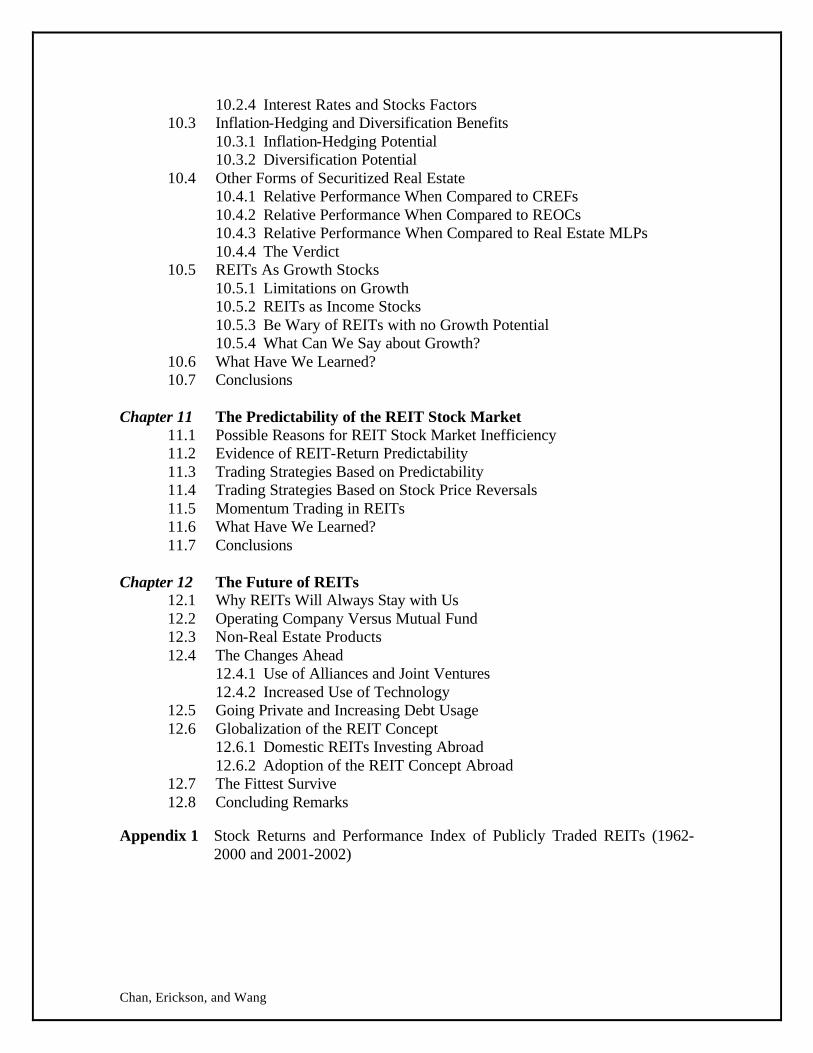

10.2.4 Interest Rates and Stocks Factors 10.3 Inflation-Hedging and Diversification Benefits

10.3.1 Inflation-Hedging Potential 10.3.2 Diversification Potential

10.4 Other Forms of Securitized Real Estate 10.4.1 Relative Performance When Compared to CREFs 10.4.2 Relative Performance When Compared to REOCs 10.4.3 Relative Performance When Compared to Real Estate MLPs 10.4.4 The Verdict

10.5 REITs As Growth Stocks 10.5.1 Limitations on Growth 10.5.2 REITs as Income Stocks 10.5.3 Be Wary of REITs with no Growth Potential 10.5.4 What Can We Say about Growth?

10.6 What Have We Learned? 10.7 Conclusions

Chapter 11 The Predictability of the REIT Stock Market

11.1 Possible Reasons for REIT Stock Market Inefficiency 11.2 Evidence of REIT-Return Predictability 11.3 Trading Strategies Based on Predictability 11.4 Trading Strategies Based on Stock Price Reversals 11.5 Momentum Trading in REITs 11.6 What Have We Learned? 11.7 Conclusions

Chapter 12 The Future of REITs

12.1 Why REITs Will Always Stay with Us 12.2 Operating Company Versus Mutual Fund 12.3 Non-Real Estate Products 12.4 The Changes Ahead

12.4.1 Use of Alliances and Joint Ventures 12.4.2 Increased Use of Technology

12.5 Going Private and Increasing Debt Usage 12.6 Globalization of the REIT Concept

12.6.1 Domestic REITs Investing Abroad 12.6.2 Adoption of the REIT Concept Abroad

12.7 The Fittest Survive 12.8 Concluding Remarks

Appendix 1 Stock Returns and Performance Index of Publicly Traded REITs (1962-

2000 and 2001-2002)