Embed Size (px)

Citation preview

1

Finance Professional Speaker Series

February 7, 2014

REAL ESTATE INVESTMENT BANKING

SECTOR: REAL ESTATE

Real Estate Capital Markets Overview

2

TABLE OF CONTENTS

SECTION 1 | Introduction

SECTION 2 | Overview and History of REIT Industry

SECTION 3 | REIT Capital Market Conditions

SECTION 4 | Overview of Preferred Stock and Offerings

SECTION 5 | Overview of Non-Traded REITs

SECTION 6 | Real Estate Illustrative Transactions

3

Introduction

SECTION 1

4

INTRODUCTION

Introduction

Go Gators!

Matt Stein – Sr. Associate; University of Florida BSBA – Finance ‘04

Lisa Ramey – Associate; University of Florida BSBA – Finance ‘07, MSF ’08

Orlando Gutierrez – Analyst; University of Florida BSBA – Finance ‘13

5

Overview and History of REIT Industry

SECTION 2

6

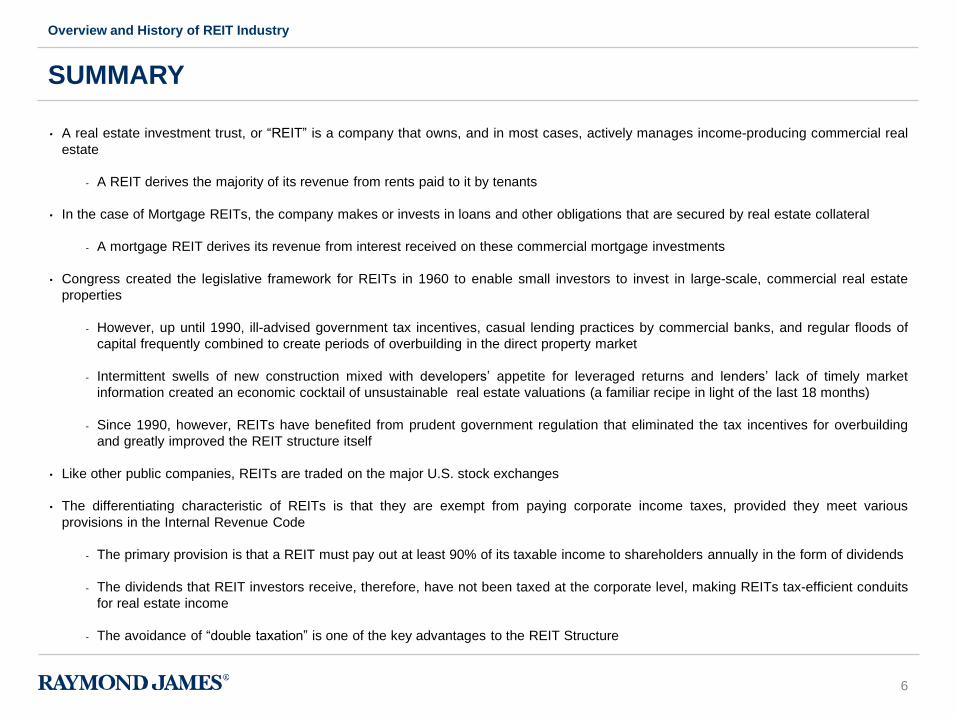

SUMMARY

Overview and History of REIT Industry

• A real estate investment trust, or “REIT” is a company that owns, and in most cases, actively manages income-producing commercial real

estate

- A REIT derives the majority of its revenue from rents paid to it by tenants

• In the case of Mortgage REITs, the company makes or invests in loans and other obligations that are secured by real estate collateral

- A mortgage REIT derives its revenue from interest received on these commercial mortgage investments

• Congress created the legislative framework for REITs in 1960 to enable small investors to invest in large-scale, commercial real estate

properties

- However, up until 1990, ill-advised government tax incentives, casual lending practices by commercial banks, and regular floods of

capital frequently combined to create periods of overbuilding in the direct property market

- Intermittent swells of new construction mixed with developers’ appetite for leveraged returns and lenders’ lack of timely market

information created an economic cocktail of unsustainable real estate valuations (a familiar recipe in light of the last 18 months)

- Since 1990, however, REITs have benefited from prudent government regulation that eliminated the tax incentives for overbuilding

and greatly improved the REIT structure itself

• Like other public companies, REITs are traded on the major U.S. stock exchanges

• The differentiating characteristic of REITs is that they are exempt from paying corporate income taxes, provided they meet various

provisions in the Internal Revenue Code

- The primary provision is that a REIT must pay out at least 90% of its taxable income to shareholders annually in the form of dividends

- The dividends that REIT investors receive, therefore, have not been taxed at the corporate level, making REITs tax-efficient conduits

for real estate income

- The avoidance of “double taxation” is one of the key advantages to the REIT Structure

7

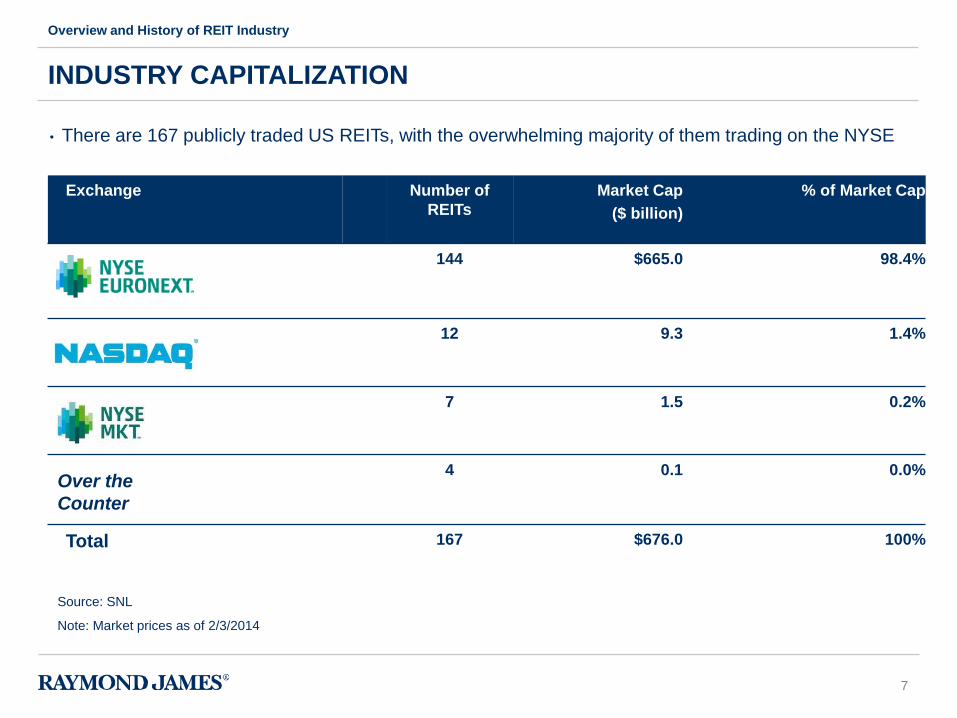

INDUSTRY CAPITALIZATION

Overview and History of REIT Industry

• There are 167 publicly traded US REITs, with the overwhelming majority of them trading on the NYSE

Exchange Number of

REITs

Market Cap

($ billion)

% of Market Cap

144 $665.0 98.4%

12 9.3 1.4%

7 1.5 0.2%

4 0.1 0.0%

Total 167 $676.0 100%

Over the

Counter

Source: SNL

Note: Market prices as of 2/3/2014

8

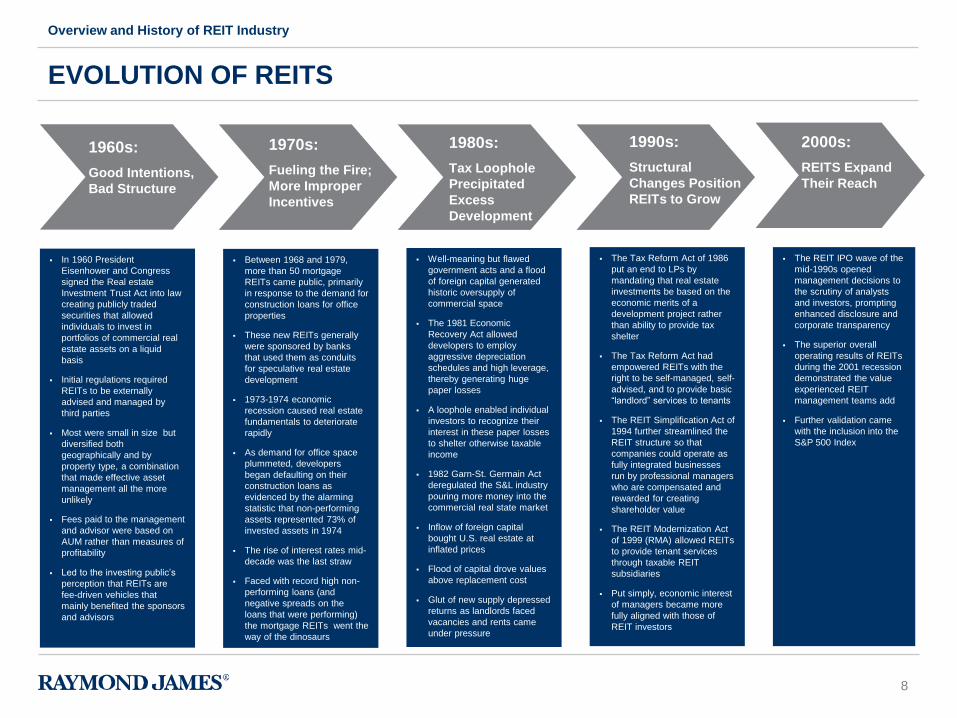

EVOLUTION OF REITS

Overview and History of REIT Industry

1960s:

Good Intentions,

Bad Structure

In 1960 President

Eisenhower and Congress

signed the Real estate

Investment Trust Act into law

creating publicly traded

securities that allowed

individuals to invest in

portfolios of commercial real

estate assets on a liquid

basis

Initial regulations required

REITs to be externally

advised and managed by

third parties

Most were small in size but

diversified both

geographically and by

property type, a combination

that made effective asset

management all the more

unlikely

Fees paid to the management

and advisor were based on

AUM rather than measures of

profitability

Led to the investing public’s

perception that REITs are

fee-driven vehicles that

mainly benefited the sponsors

and advisors

1970s:

Fueling the Fire;

More Improper

Incentives

Between 1968 and 1979,

more than 50 mortgage

REITs came public, primarily

in response to the demand for

construction loans for office

properties

These new REITs generally

were sponsored by banks

that used them as conduits

for speculative real estate

development

1973-1974 economic

recession caused real estate

fundamentals to deteriorate

rapidly

As demand for office space

plummeted, developers

began defaulting on their

construction loans as

evidenced by the alarming

statistic that non-performing

assets represented 73% of

invested assets in 1974

The rise of interest rates mid-

decade was the last straw

Faced with record high non-

performing loans (and

negative spreads on the

loans that were performing)

the mortgage REITs went the

way of the dinosaurs

1980s:

Tax Loophole

Precipitated

Excess

Development

Well-meaning but flawed

government acts and a flood

of foreign capital generated

historic oversupply of

commercial space

The 1981 Economic

Recovery Act allowed

developers to employ

aggressive depreciation

schedules and high leverage,

thereby generating huge

paper losses

A loophole enabled individual

investors to recognize their

interest in these paper losses

to shelter otherwise taxable

income

1982 Garn-St. Germain Act

deregulated the S&L industry

pouring more money into the

commercial real state market

Inflow of foreign capital

bought U.S. real estate at

inflated prices

Flood of capital drove values

above replacement cost

Glut of new supply depressed

returns as landlords faced

vacancies and rents came

under pressure

1990s:

Structural

Changes Position

REITs to Grow

The Tax Reform Act of 1986

put an end to LPs by

mandating that real estate

investments be based on the

economic merits of a

development project rather

than ability to provide tax

shelter

The Tax Reform Act had

empowered REITs with the

right to be self-managed, self-

advised, and to provide basic

“landlord” services to tenants

The REIT Simplification Act of

1994 further streamlined the

REIT structure so that

companies could operate as

fully integrated businesses

run by professional managers

who are compensated and

rewarded for creating

shareholder value

The REIT Modernization Act

of 1999 (RMA) allowed REITs

to provide tenant services

through taxable REIT

subsidiaries

Put simply, economic interest

of managers became more

fully aligned with those of

REIT investors

The REIT IPO wave of the

mid-1990s opened

management decisions to

the scrutiny of analysts

and investors, prompting

enhanced disclosure and

corporate transparency

The superior overall

operating results of REITs

during the 2001 recession

demonstrated the value

experienced REIT

management teams add

Further validation came

with the inclusion into the

S&P 500 Index

2000s:

REITS Expand

Their Reach

9

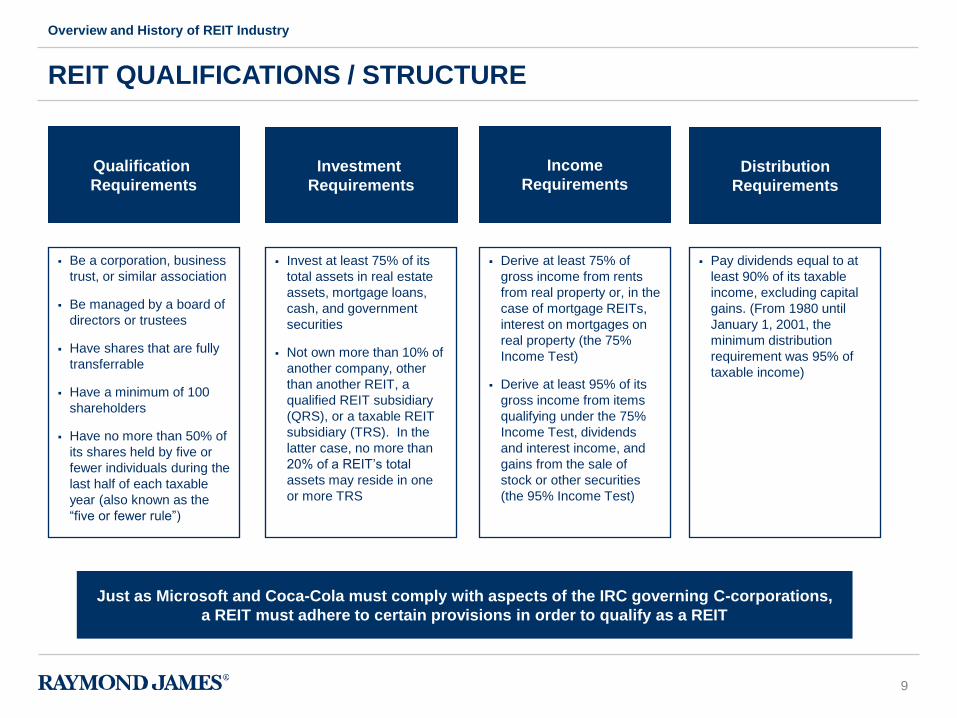

REIT QUALIFICATIONS / STRUCTURE

Overview and History of REIT Industry

Qualification

Requirements

Investment

Requirements

Income

Requirements Distribution

Requirements

Be a corporation, business

trust, or similar association

Be managed by a board of

directors or trustees

Have shares that are fully

transferrable

Have a minimum of 100

shareholders

Have no more than 50% of

its shares held by five or

fewer individuals during the

last half of each taxable

year (also known as the

“five or fewer rule”)

Derive at least 75% of

gross income from rents

from real property or, in the

case of mortgage REITs,

interest on mortgages on

real property (the 75%

Income Test)

Derive at least 95% of its

gross income from items

qualifying under the 75%

Income Test, dividends

and interest income, and

gains from the sale of

stock or other securities

(the 95% Income Test)

Pay dividends equal to at

least 90% of its taxable

income, excluding capital

gains. (From 1980 until

January 1, 2001, the

minimum distribution

requirement was 95% of

taxable income)

Invest at least 75% of its

total assets in real estate

assets, mortgage loans,

cash, and government

securities

Not own more than 10% of

another company, other

than another REIT, a

qualified REIT subsidiary

(QRS), or a taxable REIT

subsidiary (TRS). In the

latter case, no more than

20% of a REIT’s total

assets may reside in one

or more TRS

Just as Microsoft and Coca-Cola must comply with aspects of the IRC governing C-corporations,

a REIT must adhere to certain provisions in order to qualify as a REIT

10

CATEGORIES OF REITS BY INVESTMENT APPROACH

Overview and History of REIT Industry

• Own real estate and derive the majority of their revenue from rents paid by tenants

• Particularly since the REIT Modernization Act of 1999, Equity REITs increasingly

operate as fully integrated real estate companies that also derive income from a

range of real estate-related business activities

• Largest category of REITs in the United States

• Lend money to real estate owners directly by issuing mortgages, or indirectly by

acquiring existing loans or mortgage-backed securities

• The principal and interest payments mortgage REITs receive from their

investments comprise the majority of their revenue

Equity

REITs

Mortgage

REITs

• Combine the investment strategies of both equity and mortgage REITs Hybrid

REITs

11

• REITs are classified by the type of properties they invest in

CATEGORIES OF REITS BY ASSET CLASS

Overview and History of REIT Industry

Office

Industrial

Retail / Malls Lodging / Resorts Residential/

Student Housing

Health Care Self-Storage Triple Net & Specialty

12

• REITs are classified by the type of properties they invest in

CATEGORIES OF REITS BY ASSET CLASS (CONT’D)

Overview and History of REIT Industry

Single Family Rental Timber Diversified

13

REIT Capital Market Conditions

SECTION 3

14

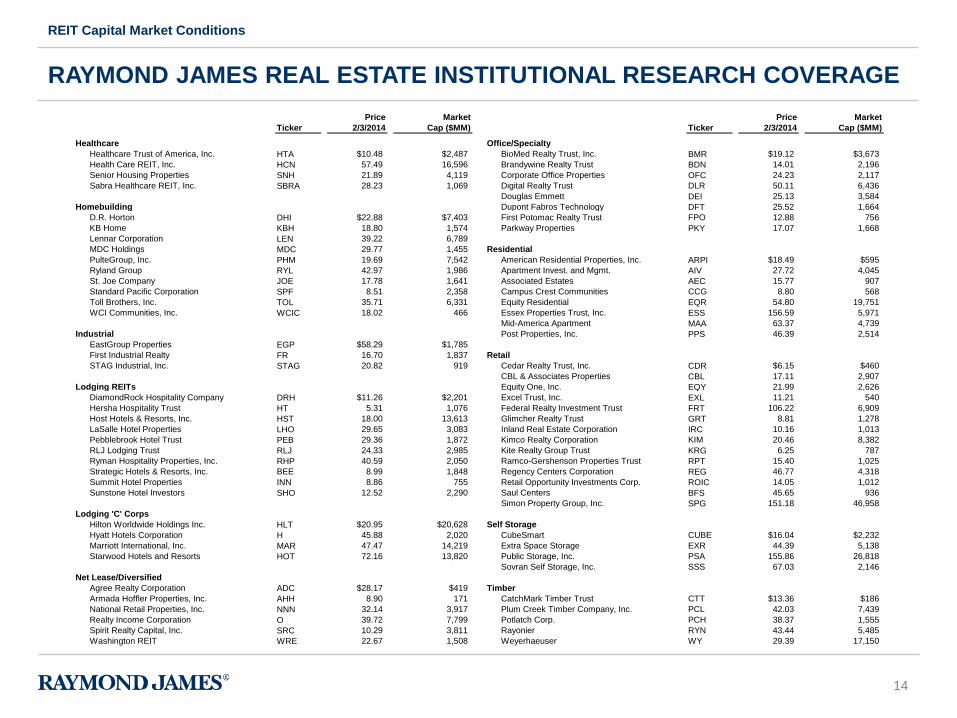

Price Market Price Market

Ticker 2/3/2014 Cap ($MM) Ticker 2/3/2014 Cap ($MM)

Healthcare Office/Specialty

Healthcare Trust of America, Inc. HTA $10.48 $2,487 BioMed Realty Trust, Inc. BMR $19.12 $3,673

Health Care REIT, Inc. HCN 57.49 16,596 Brandywine Realty Trust BDN 14.01 2,196

Senior Housing Properties SNH 21.89 4,119 Corporate Office Properties OFC 24.23 2,117

Sabra Healthcare REIT, Inc. SBRA 28.23 1,069 Digital Realty Trust DLR 50.11 6,436

Douglas Emmett DEI 25.13 3,584

Homebuilding Dupont Fabros Technology DFT 25.52 1,664

D.R. Horton DHI $22.88 $7,403 First Potomac Realty Trust FPO 12.88 756

KB Home KBH 18.80 1,574 Parkway Properties PKY 17.07 1,668

Lennar Corporation LEN 39.22 6,789

MDC Holdings MDC 29.77 1,455 Residential

PulteGroup, Inc. PHM 19.69 7,542 American Residential Properties, Inc. ARPI $18.49 $595

Ryland Group RYL 42.97 1,986 Apartment Invest. and Mgmt. AIV 27.72 4,045

St. Joe Company JOE 17.78 1,641 Associated Estates AEC 15.77 907

Standard Pacific Corporation SPF 8.51 2,358 Campus Crest Communities CCG 8.80 568

Toll Brothers, Inc. TOL 35.71 6,331 Equity Residential EQR 54.80 19,751

WCI Communities, Inc. WCIC 18.02 466 Essex Properties Trust, Inc. ESS 156.59 5,971

Mid-America Apartment MAA 63.37 4,739

Industrial Post Properties, Inc. PPS 46.39 2,514

EastGroup Properties EGP $58.29 $1,785

First Industrial Realty FR 16.70 1,837 Retail

STAG Industrial, Inc. STAG 20.82 919 Cedar Realty Trust, Inc. CDR $6.15 $460

CBL & Associates Properties CBL 17.11 2,907

Lodging REITs Equity One, Inc. EQY 21.99 2,626

DiamondRock Hospitality Company DRH $11.26 $2,201 Excel Trust, Inc. EXL 11.21 540

Hersha Hospitality Trust HT 5.31 1,076 Federal Realty Investment Trust FRT 106.22 6,909

Host Hotels & Resorts, Inc. HST 18.00 13,613 Glimcher Realty Trust GRT 8.81 1,278

LaSalle Hotel Properties LHO 29.65 3,083 Inland Real Estate Corporation IRC 10.16 1,013

Pebblebrook Hotel Trust PEB 29.36 1,872 Kimco Realty Corporation KIM 20.46 8,382

RLJ Lodging Trust RLJ 24.33 2,985 Kite Realty Group Trust KRG 6.25 787

Ryman Hospitality Properties, Inc. RHP 40.59 2,050 Ramco-Gershenson Properties Trust RPT 15.40 1,025

Strategic Hotels & Resorts, Inc. BEE 8.99 1,848 Regency Centers Corporation REG 46.77 4,318

Summit Hotel Properties INN 8.86 755 Retail Opportunity Investments Corp. ROIC 14.05 1,012

Sunstone Hotel Investors SHO 12.52 2,290 Saul Centers BFS 45.65 936

Simon Property Group, Inc. SPG 151.18 46,958

Lodging 'C' Corps

Hilton Worldwide Holdings Inc. HLT $20.95 $20,628 Self Storage

Hyatt Hotels Corporation H 45.88 2,020 CubeSmart CUBE $16.04 $2,232

Marriott International, Inc. MAR 47.47 14,219 Extra Space Storage EXR 44.39 5,138

Starwood Hotels and Resorts HOT 72.16 13,820 Public Storage, Inc. PSA 155.86 26,818

Sovran Self Storage, Inc. SSS 67.03 2,146

Net Lease/Diversified

Agree Realty Corporation ADC $28.17 $419 Timber

Armada Hoffler Properties, Inc. AHH 8.90 171 CatchMark Timber Trust CTT $13.36 $186

National Retail Properties, Inc. NNN 32.14 3,917 Plum Creek Timber Company, Inc. PCL 42.03 7,439

Realty Income Corporation O 39.72 7,799 Potlatch Corp. PCH 38.37 1,555

Spirit Realty Capital, Inc. SRC 10.29 3,811 Rayonier RYN 43.44 5,485

Washington REIT WRE 22.67 1,508 Weyerhaeuser WY 29.39 17,150

RAYMOND JAMES REAL ESTATE INSTITUTIONAL RESEARCH COVERAGE

REIT Capital Market Conditions

15

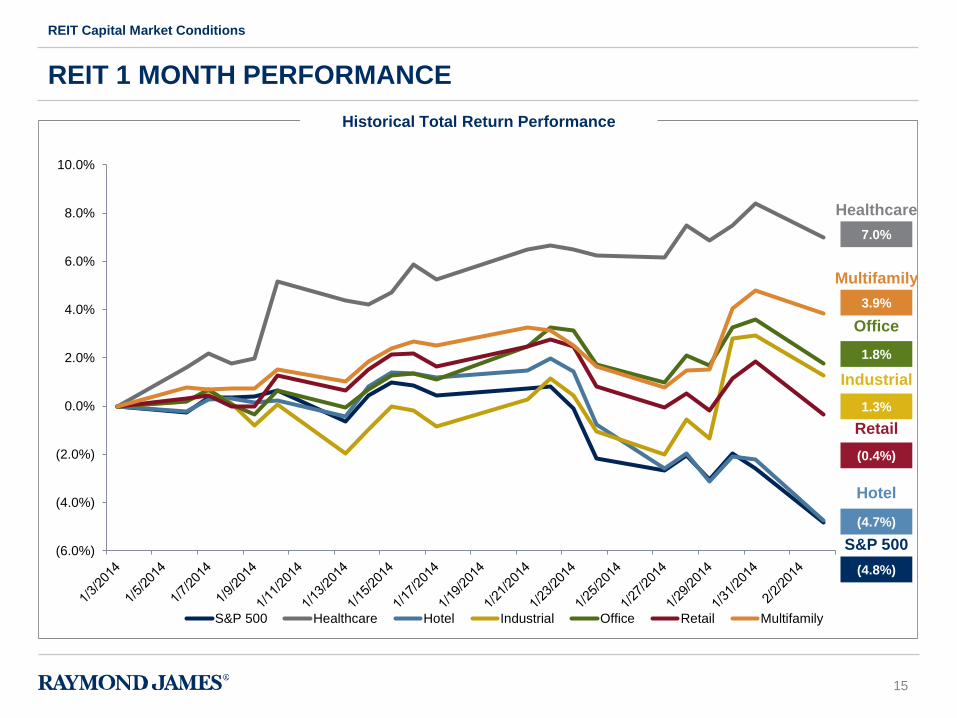

Office

(0.4%)

Retail

7.0%

Healthcare

REIT 1 MONTH PERFORMANCE

REIT Capital Market Conditions

(4.8%)

(4.7%)

Hotel

S&P 500

Historical Total Return Performance

(6.0%)

(4.0%)

(2.0%)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

S&P 500 Healthcare Hotel Industrial Office Retail Multifamily

1.3%

Industrial

1.8%

3.9%

Multifamily

16

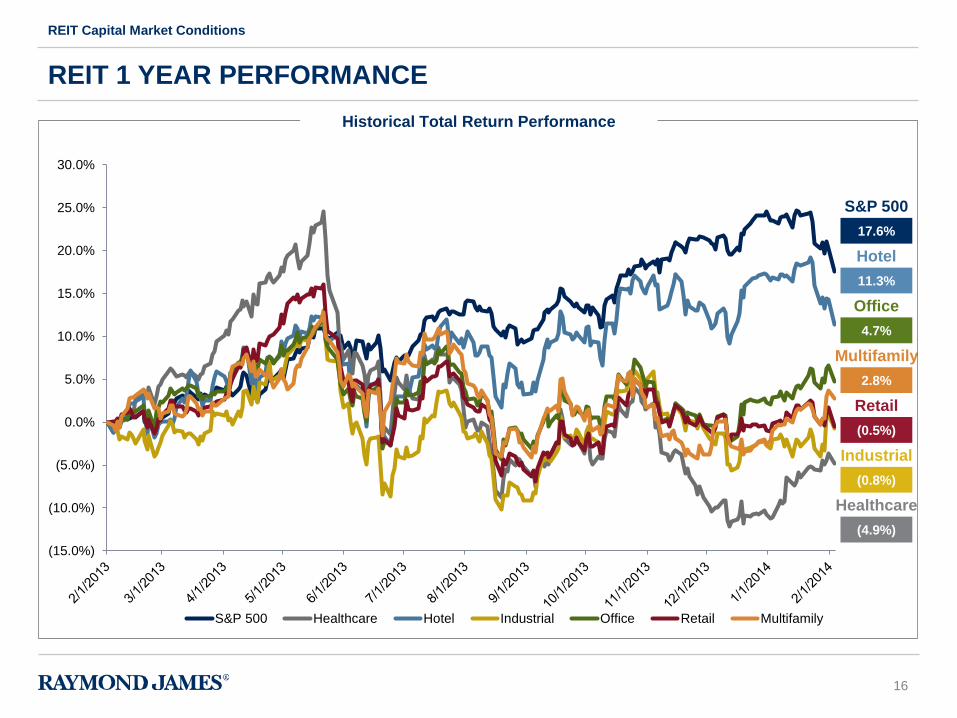

Multifamily

Office

(0.5%)

Retail

(4.9%)

Healthcare

REIT 1 YEAR PERFORMANCE

REIT Capital Market Conditions

17.6%

11.3%

Hotel

S&P 500

Historical Total Return Performance

(15.0%)

(10.0%)

(5.0%)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

S&P 500 Healthcare Hotel Industrial Office Retail Multifamily

(0.8%)

Industrial

4.7%

2.8%

17

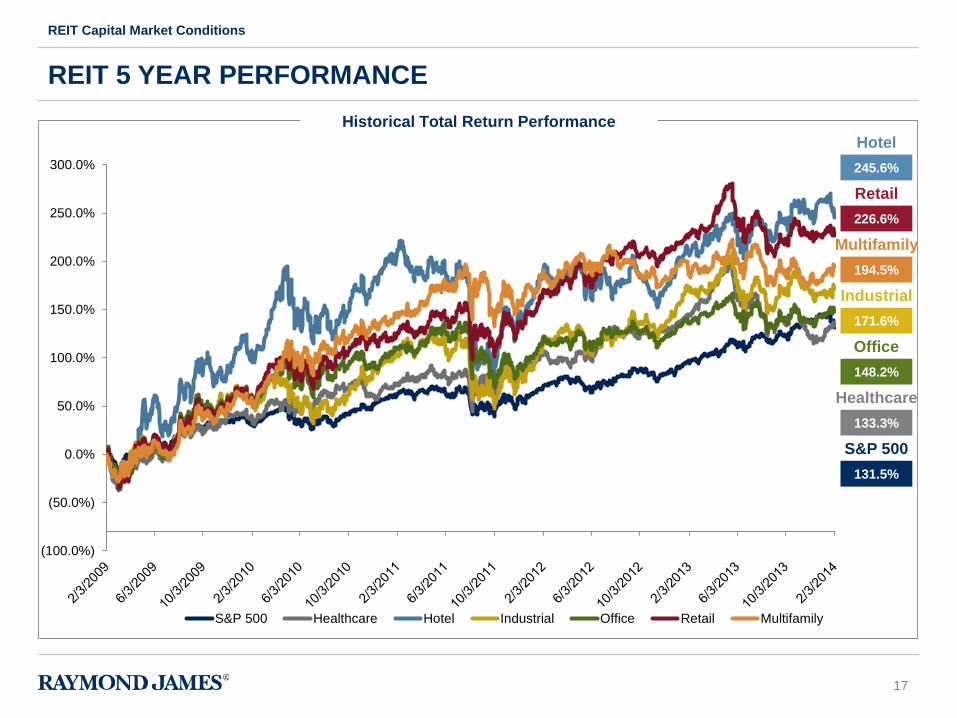

Office

226.6%

Retail

133.3%

Healthcare

REIT 5 YEAR PERFORMANCE

REIT Capital Market Conditions

131.5%

245.6%

Hotel

S&P 500

Historical Total Return Performance

(100.0%)

(50.0%)

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

S&P 500 Healthcare Hotel Industrial Office Retail Multifamily

171.6%

Industrial

148.2%

194.5%

Multifamily

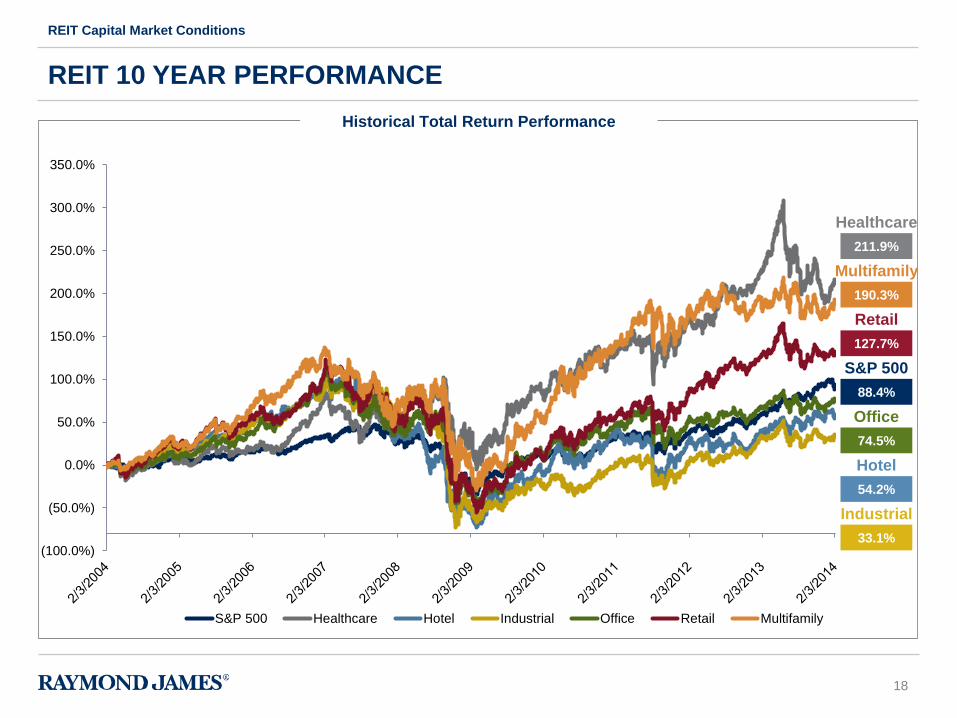

18

Office

127.7%

Retail

211.9%

Healthcare

REIT 10 YEAR PERFORMANCE

REIT Capital Market Conditions

88.4%

54.2%

Hotel

S&P 500

Historical Total Return Performance

(100.0%)

(50.0%)

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

350.0%

S&P 500 Healthcare Hotel Industrial Office Retail Multifamily

33.1%

Industrial

74.5%

190.3%

Multifamily

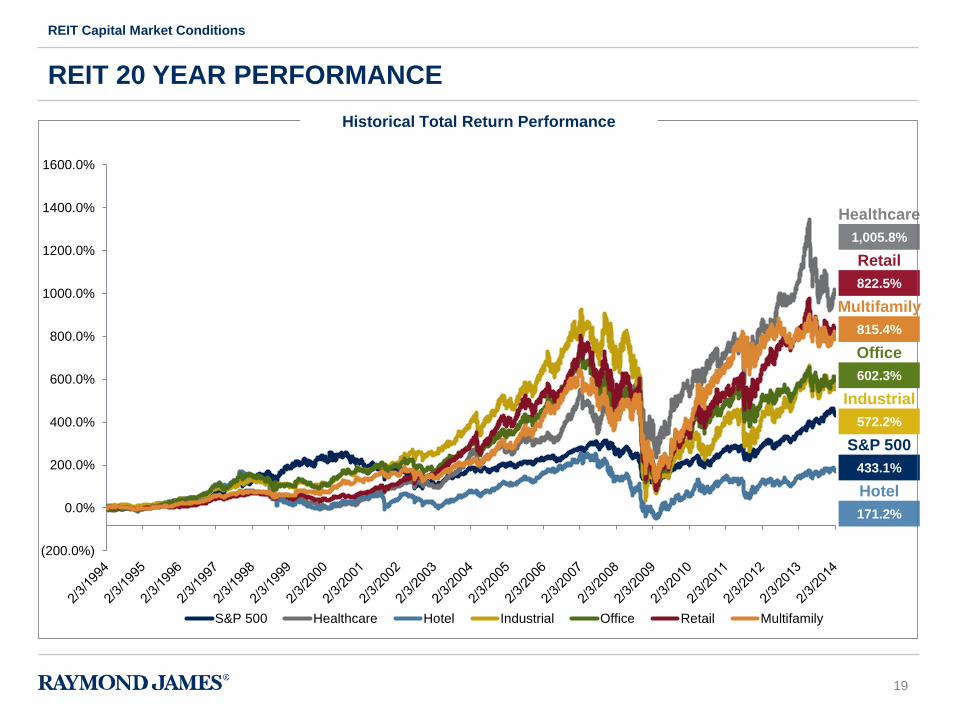

19

Office

822.5%

Retail

1,005.8%

Healthcare

REIT 20 YEAR PERFORMANCE

REIT Capital Market Conditions

433.1%

171.2%

Hotel

S&P 500

Historical Total Return Performance

(200.0%)

0.0%

200.0%

400.0%

600.0%

800.0%

1000.0%

1200.0%

1400.0%

1600.0%

S&P 500 Healthcare Hotel Industrial Office Retail Multifamily

572.2%

Industrial

602.3%

815.4%

Multifamily

20

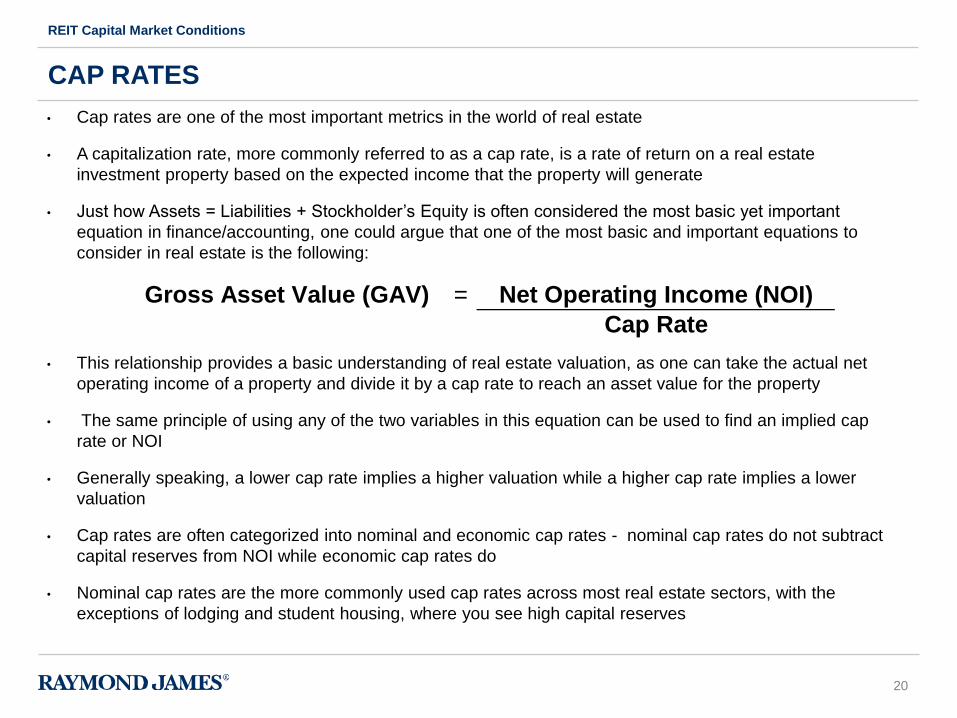

CAP RATES

REIT Capital Market Conditions

• Cap rates are one of the most important metrics in the world of real estate

• A capitalization rate, more commonly referred to as a cap rate, is a rate of return on a real estate

investment property based on the expected income that the property will generate

• Just how Assets = Liabilities + Stockholder’s Equity is often considered the most basic yet important

equation in finance/accounting, one could argue that one of the most basic and important equations to

consider in real estate is the following:

• This relationship provides a basic understanding of real estate valuation, as one can take the actual net

operating income of a property and divide it by a cap rate to reach an asset value for the property

• The same principle of using any of the two variables in this equation can be used to find an implied cap

rate or NOI

• Generally speaking, a lower cap rate implies a higher valuation while a higher cap rate implies a lower

valuation

• Cap rates are often categorized into nominal and economic cap rates - nominal cap rates do not subtract

capital reserves from NOI while economic cap rates do

• Nominal cap rates are the more commonly used cap rates across most real estate sectors, with the

exceptions of lodging and student housing, where you see high capital reserves

Gross Asset Value (GAV) = Net Operating Income (NOI)

Cap Rate

21

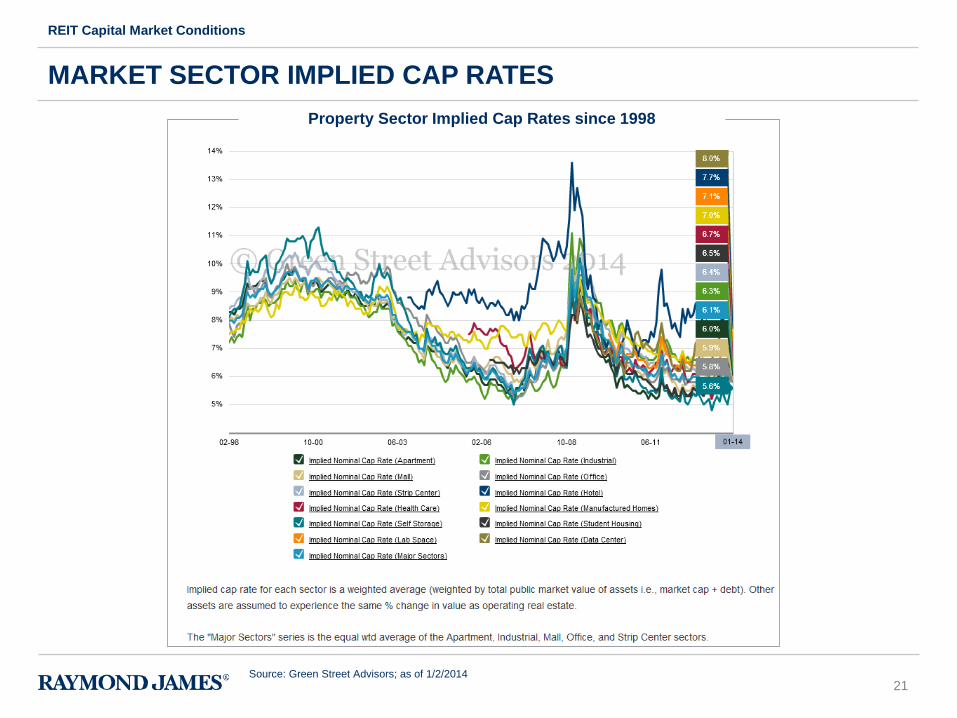

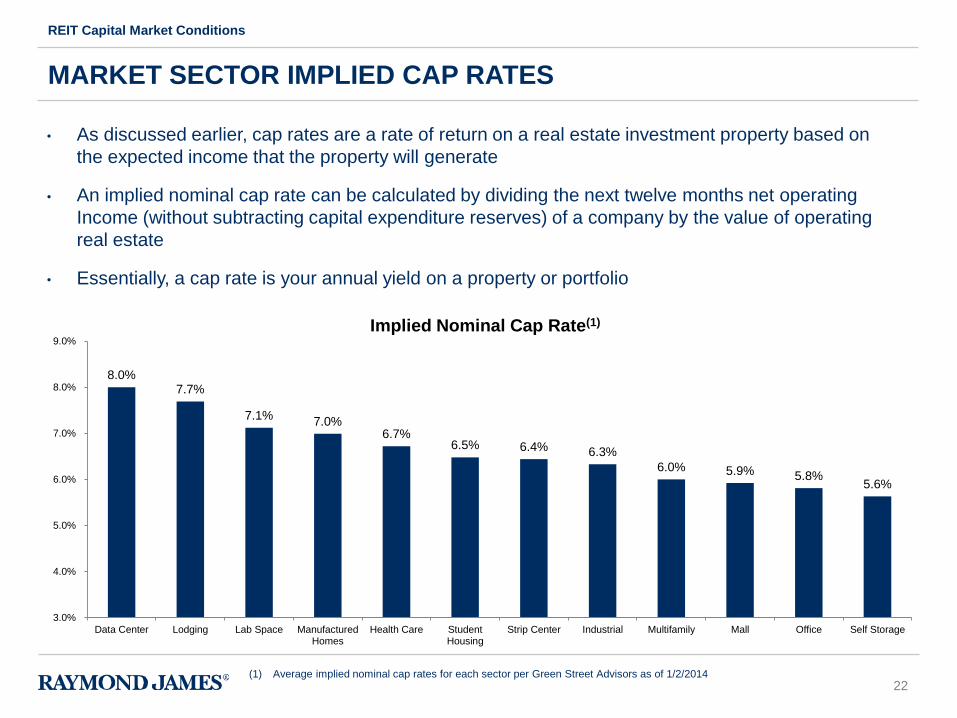

MARKET SECTOR IMPLIED CAP RATES

REIT Capital Market Conditions

Property Sector Implied Cap Rates since 1998

Source: Green Street Advisors; as of 1/2/2014

22

8.0% 7.7%

7.1% 7.0%

6.7% 6.5% 6.4% 6.3%

6.0% 5.9% 5.8% 5.6%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

Data Center Lodging Lab Space ManufacturedHomes

Health Care StudentHousing

Strip Center Industrial Multifamily Mall Office Self Storage

Implied Nominal Cap Rate(1)

MARKET SECTOR IMPLIED CAP RATES

REIT Capital Market Conditions

(1) Average implied nominal cap rates for each sector per Green Street Advisors as of 1/2/2014

• As discussed earlier, cap rates are a rate of return on a real estate investment property based on

the expected income that the property will generate

• An implied nominal cap rate can be calculated by dividing the next twelve months net operating

Income (without subtracting capital expenditure reserves) of a company by the value of operating

real estate

• Essentially, a cap rate is your annual yield on a property or portfolio

23

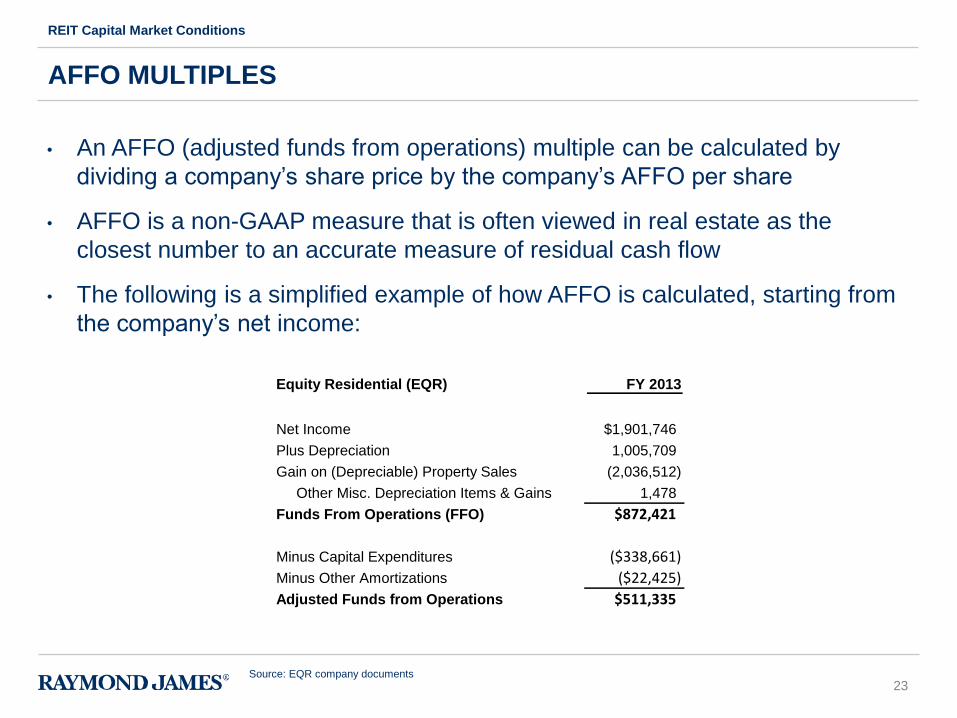

Equity Residential (EQR) FY 2013

Net Income $1,901,746

Plus Depreciation 1,005,709

Gain on (Depreciable) Property Sales (2,036,512)

Other Misc. Depreciation Items & Gains 1,478

Funds From Operations (FFO) $872,421

Minus Capital Expenditures ($338,661)

Minus Other Amortizations ($22,425)

Adjusted Funds from Operations $511,335

AFFO MULTIPLES

REIT Capital Market Conditions

• An AFFO (adjusted funds from operations) multiple can be calculated by

dividing a company’s share price by the company’s AFFO per share

• AFFO is a non-GAAP measure that is often viewed in real estate as the

closest number to an accurate measure of residual cash flow

• The following is a simplified example of how AFFO is calculated, starting from

the company’s net income:

Source: EQR company documents

24

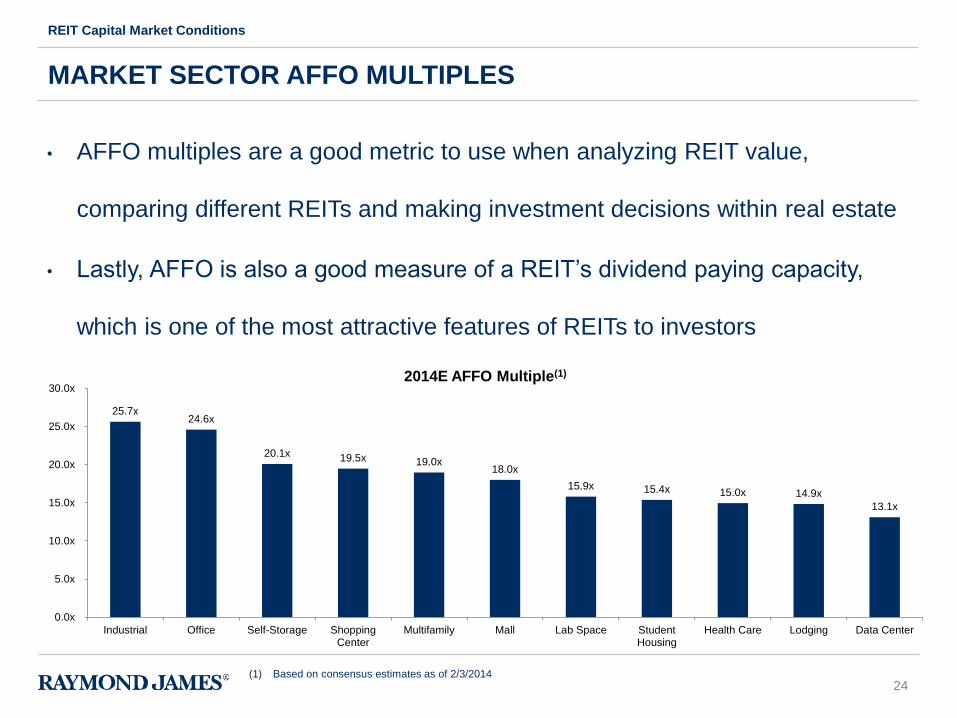

25.7x 24.6x

20.1x 19.5x 19.0x 18.0x

15.9x 15.4x 15.0x 14.9x

13.1x

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

Industrial Office Self-Storage ShoppingCenter

Multifamily Mall Lab Space StudentHousing

Health Care Lodging Data Center

2014E AFFO Multiple(1)

MARKET SECTOR AFFO MULTIPLES

REIT Capital Market Conditions

(1) Based on consensus estimates as of 2/3/2014

• AFFO multiples are a good metric to use when analyzing REIT value,

comparing different REITs and making investment decisions within real estate

• Lastly, AFFO is also a good measure of a REIT’s dividend paying capacity,

which is one of the most attractive features of REITs to investors

25

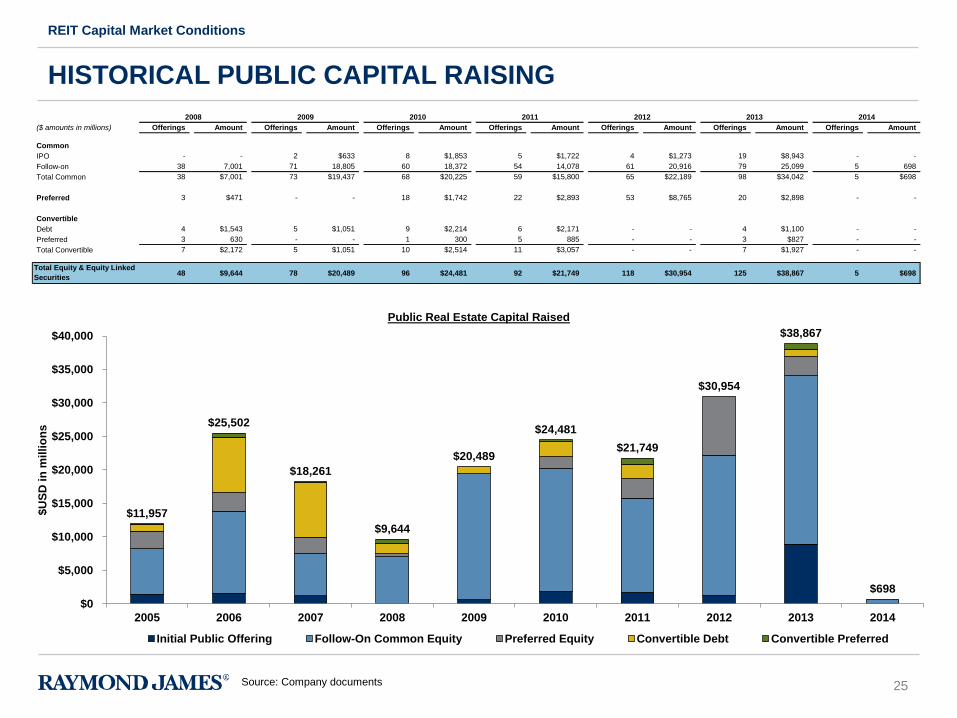

$11,957

$25,502

$18,261

$9,644

$20,489

$24,481

$21,749

$30,954

$38,867

$698

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$U

SD

in

mil

lio

ns

Public Real Estate Capital Raised

Initial Public Offering Follow-On Common Equity Preferred Equity Convertible Debt Convertible Preferred

HISTORICAL PUBLIC CAPITAL RAISING

REIT Capital Market Conditions

Source: Company documents

2008 2009 2010 2011

($ amounts in millions) Offerings Amount Offerings Amount Offerings Amount Offerings Amount Offerings Amount Offerings Amount Offerings Amount

Common

IPO - - 2 $633 8 $1,853 5 $1,722 4 $1,273 19 $8,943 - -

Follow-on 38 7,001 71 18,805 60 18,372 54 14,078 61 20,916 79 25,099 5 698

Total Common 38 $7,001 73 $19,437 68 $20,225 59 $15,800 65 $22,189 98 $34,042 5 $698

Preferred 3 $471 - - 18 $1,742 22 $2,893 53 $8,765 20 $2,898 - -

Convertible

Debt 4 $1,543 5 $1,051 9 $2,214 6 $2,171 - - 4 $1,100 - -

Preferred 3 630 - - 1 300 5 885 - - 3 $827 - -

Total Convertible 7 $2,172 5 $1,051 10 $2,514 11 $3,057 - - 7 $1,927 - -

Total Equity & Equity Linked

Securities48 $9,644 78 $20,489 96 $24,481 92 $21,749 118 $30,954 125 $38,867 5 $698

2012 2013 2014

26

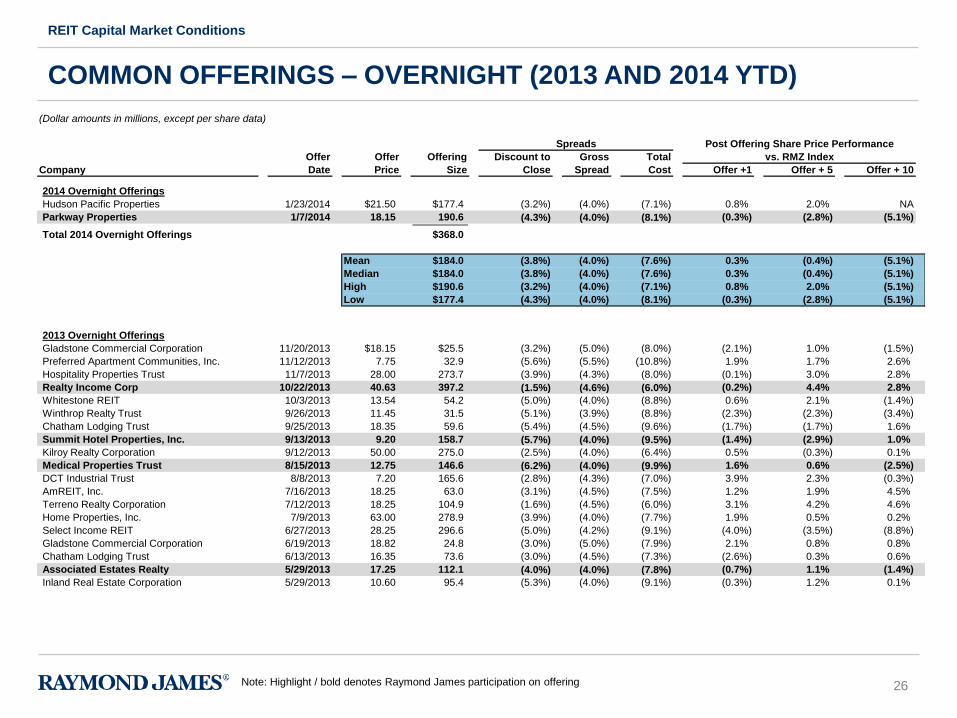

(Dollar amounts in millions, except per share data)

Spreads Post Offering Share Price Performance

Offer Offer Offering Discount to Gross Total vs. RMZ Index

Company Date Price Size Close Spread Cost Offer +1 Offer + 5 Offer + 10

2014 Overnight Offerings

Hudson Pacific Properties 1/23/2014 $21.50 $177.4 (3.2%) (4.0%) (7.1%) 0.8% 2.0% NA

Parkway Properties 1/7/2014 18.15 190.6 (4.3%) (4.0%) (8.1%) (0.3%) (2.8%) (5.1%)

Total 2014 Overnight Offerings $368.0

Mean $184.0 (3.8%) (4.0%) (7.6%) 0.3% (0.4%) (5.1%)

Median $184.0 (3.8%) (4.0%) (7.6%) 0.3% (0.4%) (5.1%)

High $190.6 (3.2%) (4.0%) (7.1%) 0.8% 2.0% (5.1%)

Low $177.4 (4.3%) (4.0%) (8.1%) (0.3%) (2.8%) (5.1%)

2013 Overnight Offerings

Gladstone Commercial Corporation 11/20/2013 $18.15 $25.5 (3.2%) (5.0%) (8.0%) (2.1%) 1.0% (1.5%)

Preferred Apartment Communities, Inc. 11/12/2013 7.75 32.9 (5.6%) (5.5%) (10.8%) 1.9% 1.7% 2.6%

Hospitality Properties Trust 11/7/2013 28.00 273.7 (3.9%) (4.3%) (8.0%) (0.1%) 3.0% 2.8%

Realty Income Corp 10/22/2013 40.63 397.2 (1.5%) (4.6%) (6.0%) (0.2%) 4.4% 2.8%

Whitestone REIT 10/3/2013 13.54 54.2 (5.0%) (4.0%) (8.8%) 0.6% 2.1% (1.4%)

Winthrop Realty Trust 9/26/2013 11.45 31.5 (5.1%) (3.9%) (8.8%) (2.3%) (2.3%) (3.4%)

Chatham Lodging Trust 9/25/2013 18.35 59.6 (5.4%) (4.5%) (9.6%) (1.7%) (1.7%) 1.6%

Summit Hotel Properties, Inc. 9/13/2013 9.20 158.7 (5.7%) (4.0%) (9.5%) (1.4%) (2.9%) 1.0%

Kilroy Realty Corporation 9/12/2013 50.00 275.0 (2.5%) (4.0%) (6.4%) 0.5% (0.3%) 0.1%

Medical Properties Trust 8/15/2013 12.75 146.6 (6.2%) (4.0%) (9.9%) 1.6% 0.6% (2.5%)

DCT Industrial Trust 8/8/2013 7.20 165.6 (2.8%) (4.3%) (7.0%) 3.9% 2.3% (0.3%)

AmREIT, Inc. 7/16/2013 18.25 63.0 (3.1%) (4.5%) (7.5%) 1.2% 1.9% 4.5%

Terreno Realty Corporation 7/12/2013 18.25 104.9 (1.6%) (4.5%) (6.0%) 3.1% 4.2% 4.6%

Home Properties, Inc. 7/9/2013 63.00 278.9 (3.9%) (4.0%) (7.7%) 1.9% 0.5% 0.2%

Select Income REIT 6/27/2013 28.25 296.6 (5.0%) (4.2%) (9.1%) (4.0%) (3.5%) (8.8%)

Gladstone Commercial Corporation 6/19/2013 18.82 24.8 (3.0%) (5.0%) (7.9%) 2.1% 0.8% 0.8%

Chatham Lodging Trust 6/13/2013 16.35 73.6 (3.0%) (4.5%) (7.3%) (2.6%) 0.3% 0.6%

Associated Estates Realty 5/29/2013 17.25 112.1 (4.0%) (4.0%) (7.8%) (0.7%) 1.1% (1.4%)

Inland Real Estate Corporation 5/29/2013 10.60 95.4 (5.3%) (4.0%) (9.1%) (0.3%) 1.2% 0.1%

COMMON OFFERINGS – OVERNIGHT (2013 AND 2014 YTD)

REIT Capital Market Conditions

Note: Highlight / bold denotes Raymond James participation on offering

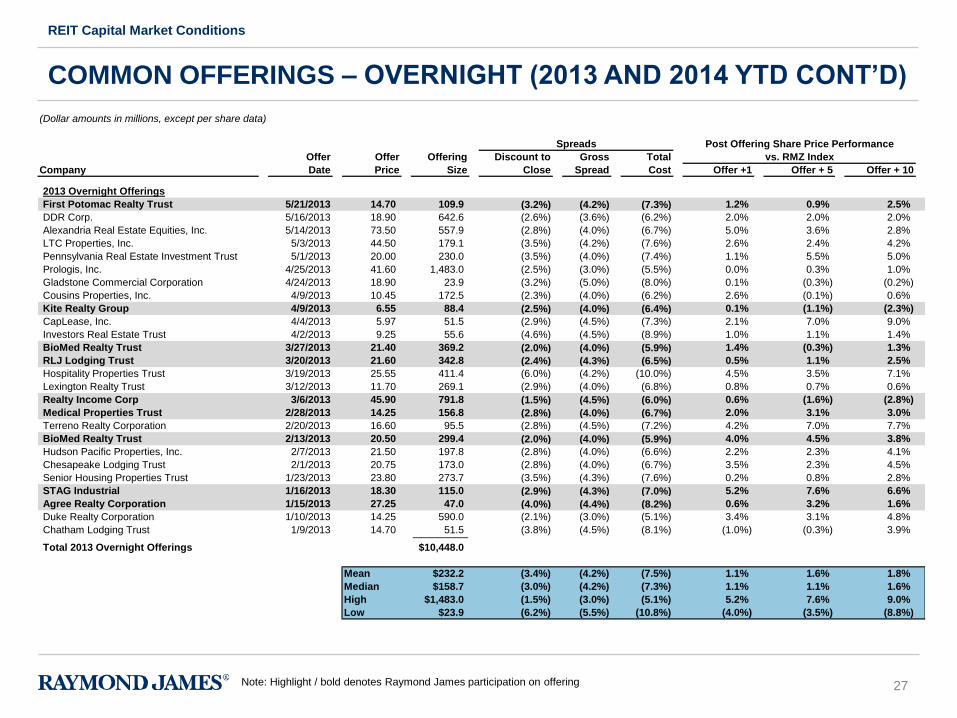

27

(Dollar amounts in millions, except per share data)

Spreads Post Offering Share Price Performance

Offer Offer Offering Discount to Gross Total vs. RMZ Index

Company Date Price Size Close Spread Cost Offer +1 Offer + 5 Offer + 10

2013 Overnight Offerings

First Potomac Realty Trust 5/21/2013 14.70 109.9 (3.2%) (4.2%) (7.3%) 1.2% 0.9% 2.5%

DDR Corp. 5/16/2013 18.90 642.6 (2.6%) (3.6%) (6.2%) 2.0% 2.0% 2.0%

Alexandria Real Estate Equities, Inc. 5/14/2013 73.50 557.9 (2.8%) (4.0%) (6.7%) 5.0% 3.6% 2.8%

LTC Properties, Inc. 5/3/2013 44.50 179.1 (3.5%) (4.2%) (7.6%) 2.6% 2.4% 4.2%

Pennsylvania Real Estate Investment Trust 5/1/2013 20.00 230.0 (3.5%) (4.0%) (7.4%) 1.1% 5.5% 5.0%

Prologis, Inc. 4/25/2013 41.60 1,483.0 (2.5%) (3.0%) (5.5%) 0.0% 0.3% 1.0%

Gladstone Commercial Corporation 4/24/2013 18.90 23.9 (3.2%) (5.0%) (8.0%) 0.1% (0.3%) (0.2%)

Cousins Properties, Inc. 4/9/2013 10.45 172.5 (2.3%) (4.0%) (6.2%) 2.6% (0.1%) 0.6%

Kite Realty Group 4/9/2013 6.55 88.4 (2.5%) (4.0%) (6.4%) 0.1% (1.1%) (2.3%)

CapLease, Inc. 4/4/2013 5.97 51.5 (2.9%) (4.5%) (7.3%) 2.1% 7.0% 9.0%

Investors Real Estate Trust 4/2/2013 9.25 55.6 (4.6%) (4.5%) (8.9%) 1.0% 1.1% 1.4%

BioMed Realty Trust 3/27/2013 21.40 369.2 (2.0%) (4.0%) (5.9%) 1.4% (0.3%) 1.3%

RLJ Lodging Trust 3/20/2013 21.60 342.8 (2.4%) (4.3%) (6.5%) 0.5% 1.1% 2.5%

Hospitality Properties Trust 3/19/2013 25.55 411.4 (6.0%) (4.2%) (10.0%) 4.5% 3.5% 7.1%

Lexington Realty Trust 3/12/2013 11.70 269.1 (2.9%) (4.0%) (6.8%) 0.8% 0.7% 0.6%

Realty Income Corp 3/6/2013 45.90 791.8 (1.5%) (4.5%) (6.0%) 0.6% (1.6%) (2.8%)

Medical Properties Trust 2/28/2013 14.25 156.8 (2.8%) (4.0%) (6.7%) 2.0% 3.1% 3.0%

Terreno Realty Corporation 2/20/2013 16.60 95.5 (2.8%) (4.5%) (7.2%) 4.2% 7.0% 7.7%

BioMed Realty Trust 2/13/2013 20.50 299.4 (2.0%) (4.0%) (5.9%) 4.0% 4.5% 3.8%

Hudson Pacific Properties, Inc. 2/7/2013 21.50 197.8 (2.8%) (4.0%) (6.6%) 2.2% 2.3% 4.1%

Chesapeake Lodging Trust 2/1/2013 20.75 173.0 (2.8%) (4.0%) (6.7%) 3.5% 2.3% 4.5%

Senior Housing Properties Trust 1/23/2013 23.80 273.7 (3.5%) (4.3%) (7.6%) 0.2% 0.8% 2.8%

STAG Industrial 1/16/2013 18.30 115.0 (2.9%) (4.3%) (7.0%) 5.2% 7.6% 6.6%

Agree Realty Corporation 1/15/2013 27.25 47.0 (4.0%) (4.4%) (8.2%) 0.6% 3.2% 1.6%

Duke Realty Corporation 1/10/2013 14.25 590.0 (2.1%) (3.0%) (5.1%) 3.4% 3.1% 4.8%

Chatham Lodging Trust 1/9/2013 14.70 51.5 (3.8%) (4.5%) (8.1%) (1.0%) (0.3%) 3.9%

Total 2013 Overnight Offerings $10,448.0

Mean $232.2 (3.4%) (4.2%) (7.5%) 1.1% 1.6% 1.8%

Median $158.7 (3.0%) (4.2%) (7.3%) 1.1% 1.1% 1.6%

High $1,483.0 (1.5%) (3.0%) (5.1%) 5.2% 7.6% 9.0%

Low $23.9 (6.2%) (5.5%) (10.8%) (4.0%) (3.5%) (8.8%)

COMMON OFFERINGS – OVERNIGHT (2013 AND 2014 YTD CONT’D)

REIT Capital Market Conditions

Note: Highlight / bold denotes Raymond James participation on offering

28

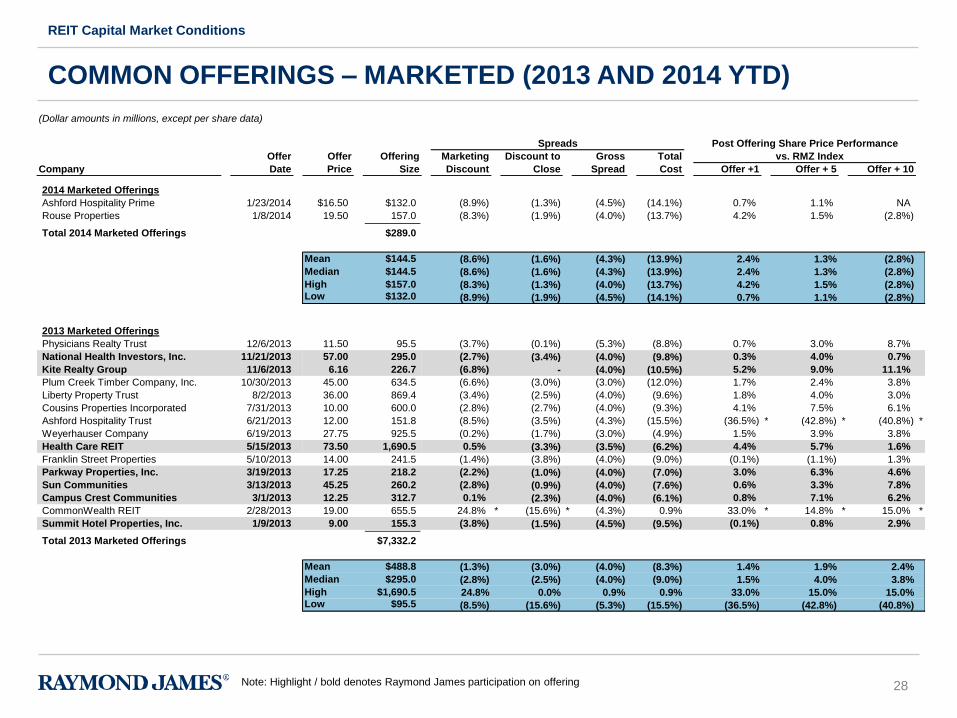

(Dollar amounts in millions, except per share data)

Spreads Post Offering Share Price Performance

Offer Offer Offering Marketing Discount to Gross Total vs. RMZ Index

Company Date Price Size Discount Close Spread Cost Offer +1 Offer + 5 Offer + 10

2014 Marketed Offerings

Ashford Hospitality Prime 1/23/2014 $16.50 $132.0 (8.9%) (1.3%) (4.5%) (14.1%) 0.7% 1.1% NA

Rouse Properties 1/8/2014 19.50 157.0 (8.3%) (1.9%) (4.0%) (13.7%) 4.2% 1.5% (2.8%)

Total 2014 Marketed Offerings $289.0

Mean $144.5 (8.6%) (1.6%) (4.3%) (13.9%) 2.4% 1.3% (2.8%)

Median $144.5 (8.6%) (1.6%) (4.3%) (13.9%) 2.4% 1.3% (2.8%)

High $157.0 (8.3%) (1.3%) (4.0%) (13.7%) 4.2% 1.5% (2.8%)Low $132.0 (8.9%) (1.9%) (4.5%) (14.1%) 0.7% 1.1% (2.8%)

2013 Marketed Offerings

Physicians Realty Trust 12/6/2013 11.50 95.5 (3.7%) (0.1%) (5.3%) (8.8%) 0.7% 3.0% 8.7%

National Health Investors, Inc. 11/21/2013 57.00 295.0 (2.7%) (3.4%) (4.0%) (9.8%) 0.3% 4.0% 0.7%

Kite Realty Group 11/6/2013 6.16 226.7 (6.8%) - (4.0%) (10.5%) 5.2% 9.0% 11.1%

Plum Creek Timber Company, Inc. 10/30/2013 45.00 634.5 (6.6%) (3.0%) (3.0%) (12.0%) 1.7% 2.4% 3.8%

Liberty Property Trust 8/2/2013 36.00 869.4 (3.4%) (2.5%) (4.0%) (9.6%) 1.8% 4.0% 3.0%

Cousins Properties Incorporated 7/31/2013 10.00 600.0 (2.8%) (2.7%) (4.0%) (9.3%) 4.1% 7.5% 6.1%

Ashford Hospitality Trust 6/21/2013 12.00 151.8 (8.5%) (3.5%) (4.3%) (15.5%) (36.5%) * (42.8%) * (40.8%) *

Weyerhauser Company 6/19/2013 27.75 925.5 (0.2%) (1.7%) (3.0%) (4.9%) 1.5% 3.9% 3.8%

Health Care REIT 5/15/2013 73.50 1,690.5 0.5% (3.3%) (3.5%) (6.2%) 4.4% 5.7% 1.6%

Franklin Street Properties 5/10/2013 14.00 241.5 (1.4%) (3.8%) (4.0%) (9.0%) (0.1%) (1.1%) 1.3%

Parkway Properties, Inc. 3/19/2013 17.25 218.2 (2.2%) (1.0%) (4.0%) (7.0%) 3.0% 6.3% 4.6%

Sun Communities 3/13/2013 45.25 260.2 (2.8%) (0.9%) (4.0%) (7.6%) 0.6% 3.3% 7.8%

Campus Crest Communities 3/1/2013 12.25 312.7 0.1% (2.3%) (4.0%) (6.1%) 0.8% 7.1% 6.2%

CommonWealth REIT 2/28/2013 19.00 655.5 24.8% * (15.6%) * (4.3%) 0.9% 33.0% * 14.8% * 15.0% *

Summit Hotel Properties, Inc. 1/9/2013 9.00 155.3 (3.8%) (1.5%) (4.5%) (9.5%) (0.1%) 0.8% 2.9%

Total 2013 Marketed Offerings $7,332.2

Mean $488.8 (1.3%) (3.0%) (4.0%) (8.3%) 1.4% 1.9% 2.4%

Median $295.0 (2.8%) (2.5%) (4.0%) (9.0%) 1.5% 4.0% 3.8%

High $1,690.5 24.8% 0.0% 0.9% 0.9% 33.0% 15.0% 15.0% Low $95.5 (8.5%) (15.6%) (5.3%) (15.5%) (36.5%) (42.8%) (40.8%)

COMMON OFFERINGS – MARKETED (2013 AND 2014 YTD)

REIT Capital Market Conditions

Note: Highlight / bold denotes Raymond James participation on offering

29

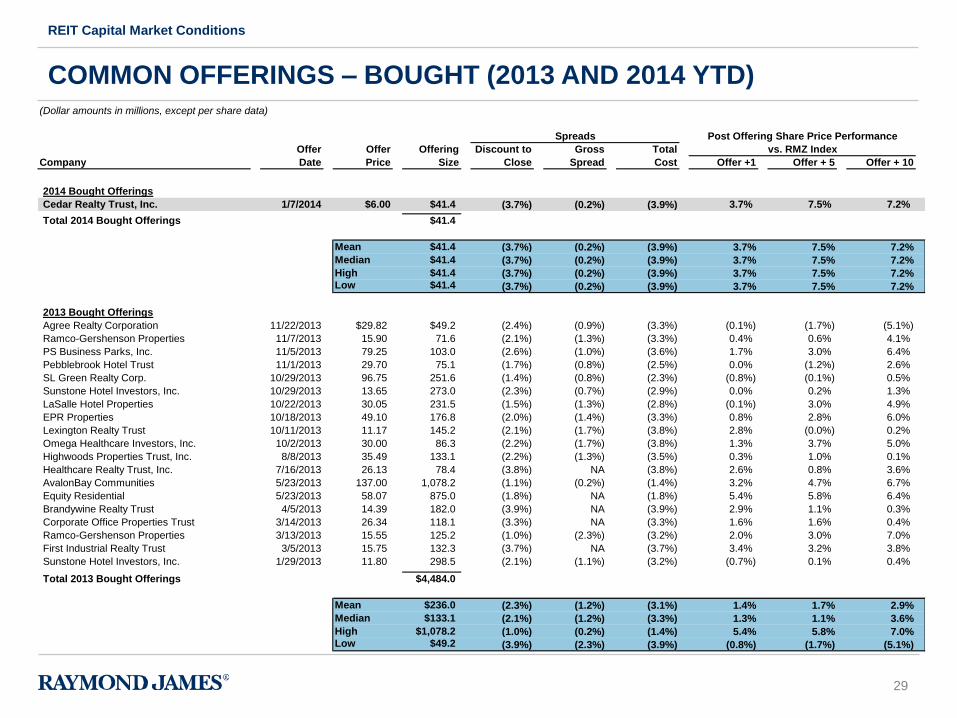

(Dollar amounts in millions, except per share data)

Spreads Post Offering Share Price Performance

Offer Offer Offering Discount to Gross Total vs. RMZ Index

Company Date Price Size Close Spread Cost Offer +1 Offer + 5 Offer + 10

2014 Bought Offerings

Cedar Realty Trust, Inc. 1/7/2014 $6.00 $41.4 (3.7%) (0.2%) (3.9%) 3.7% 7.5% 7.2%

Total 2014 Bought Offerings $41.4

Mean $41.4 (3.7%) (0.2%) (3.9%) 3.7% 7.5% 7.2%

Median $41.4 (3.7%) (0.2%) (3.9%) 3.7% 7.5% 7.2%

High $41.4 (3.7%) (0.2%) (3.9%) 3.7% 7.5% 7.2% Low $41.4 (3.7%) (0.2%) (3.9%) 3.7% 7.5% 7.2%

2013 Bought Offerings

Agree Realty Corporation 11/22/2013 $29.82 $49.2 (2.4%) (0.9%) (3.3%) (0.1%) (1.7%) (5.1%)

Ramco-Gershenson Properties 11/7/2013 15.90 71.6 (2.1%) (1.3%) (3.3%) 0.4% 0.6% 4.1%

PS Business Parks, Inc. 11/5/2013 79.25 103.0 (2.6%) (1.0%) (3.6%) 1.7% 3.0% 6.4%

Pebblebrook Hotel Trust 11/1/2013 29.70 75.1 (1.7%) (0.8%) (2.5%) 0.0% (1.2%) 2.6%

SL Green Realty Corp. 10/29/2013 96.75 251.6 (1.4%) (0.8%) (2.3%) (0.8%) (0.1%) 0.5%

Sunstone Hotel Investors, Inc. 10/29/2013 13.65 273.0 (2.3%) (0.7%) (2.9%) 0.0% 0.2% 1.3%

LaSalle Hotel Properties 10/22/2013 30.05 231.5 (1.5%) (1.3%) (2.8%) (0.1%) 3.0% 4.9%

EPR Properties 10/18/2013 49.10 176.8 (2.0%) (1.4%) (3.3%) 0.8% 2.8% 6.0%

Lexington Realty Trust 10/11/2013 11.17 145.2 (2.1%) (1.7%) (3.8%) 2.8% (0.0%) 0.2%

Omega Healthcare Investors, Inc. 10/2/2013 30.00 86.3 (2.2%) (1.7%) (3.8%) 1.3% 3.7% 5.0%

Highwoods Properties Trust, Inc. 8/8/2013 35.49 133.1 (2.2%) (1.3%) (3.5%) 0.3% 1.0% 0.1%

Healthcare Realty Trust, Inc. 7/16/2013 26.13 78.4 (3.8%) NA (3.8%) 2.6% 0.8% 3.6%

AvalonBay Communities 5/23/2013 137.00 1,078.2 (1.1%) (0.2%) (1.4%) 3.2% 4.7% 6.7%

Equity Residential 5/23/2013 58.07 875.0 (1.8%) NA (1.8%) 5.4% 5.8% 6.4%

Brandywine Realty Trust 4/5/2013 14.39 182.0 (3.9%) NA (3.9%) 2.9% 1.1% 0.3%

Corporate Office Properties Trust 3/14/2013 26.34 118.1 (3.3%) NA (3.3%) 1.6% 1.6% 0.4%

Ramco-Gershenson Properties 3/13/2013 15.55 125.2 (1.0%) (2.3%) (3.2%) 2.0% 3.0% 7.0%

First Industrial Realty Trust 3/5/2013 15.75 132.3 (3.7%) NA (3.7%) 3.4% 3.2% 3.8%

Sunstone Hotel Investors, Inc. 1/29/2013 11.80 298.5 (2.1%) (1.1%) (3.2%) (0.7%) 0.1% 0.4%

Total 2013 Bought Offerings $4,484.0

Mean $236.0 (2.3%) (1.2%) (3.1%) 1.4% 1.7% 2.9%

Median $133.1 (2.1%) (1.2%) (3.3%) 1.3% 1.1% 3.6%

High $1,078.2 (1.0%) (0.2%) (1.4%) 5.4% 5.8% 7.0% Low $49.2 (3.9%) (2.3%) (3.9%) (0.8%) (1.7%) (5.1%)

COMMON OFFERINGS – BOUGHT (2013 AND 2014 YTD)

REIT Capital Market Conditions

30

Overview of Preferred Stock and Offerings

SECTION 4

31

PREFERRED STOCK

Overview of Preferred Stock and Offerings

• Some of the features of preferred stock include:

- A class of ownership in a corporation that has a higher claim on the

assets and earnings than common stock

- Generally has a dividend that must be paid out before dividends to

common stockholders and typically accrues if the company doesn’t

pay it

- The value of preferred stock, similar to a bond, is sensitive to interest

rates

- While preferred stock has no maturity date, the shares may be called

by the issuer after a certain date

o The motivation for the redemption is generally the same as for

bonds; a company calls securities that pay higher rates than what

the market is currently offering

32

PREFERRED STOCK (CONT’D)

Overview of Preferred Stock and Offerings

• Preferred stock is attractive to investors because:

- Preferred shareholders have priority over common stockholders on

earnings and assets in the event of liquidation

- Preferred stock, similar to a bond, has a fixed periodic cash payment in

the form of a dividend (paid before common stockholders)

• Some of the negatives of preferred stock in comparison to common stock

are:

- Preferred shareholders often have no voting rights

- There is less potential for price appreciation

33

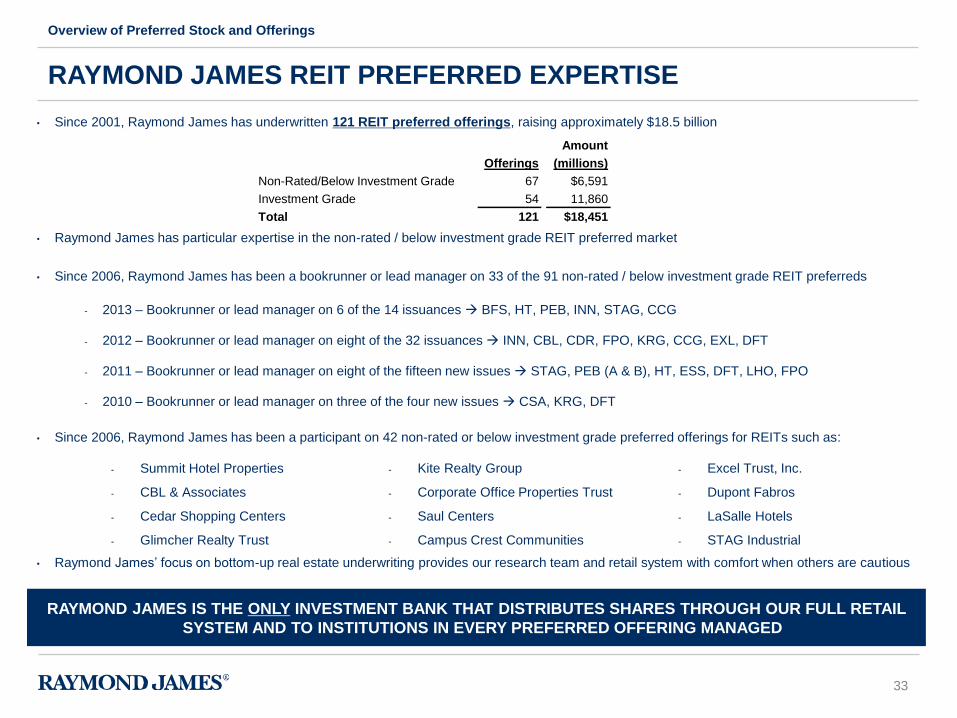

• Since 2001, Raymond James has underwritten 121 REIT preferred offerings, raising approximately $18.5 billion

• Raymond James has particular expertise in the non-rated / below investment grade REIT preferred market

• Since 2006, Raymond James has been a bookrunner or lead manager on 33 of the 91 non-rated / below investment grade REIT preferreds

- 2013 – Bookrunner or lead manager on 6 of the 14 issuances BFS, HT, PEB, INN, STAG, CCG

- 2012 – Bookrunner or lead manager on eight of the 32 issuances INN, CBL, CDR, FPO, KRG, CCG, EXL, DFT

- 2011 – Bookrunner or lead manager on eight of the fifteen new issues STAG, PEB (A & B), HT, ESS, DFT, LHO, FPO

- 2010 – Bookrunner or lead manager on three of the four new issues CSA, KRG, DFT

• Since 2006, Raymond James has been a participant on 42 non-rated or below investment grade preferred offerings for REITs such as:

• Raymond James’ focus on bottom-up real estate underwriting provides our research team and retail system with comfort when others are cautious

RAYMOND JAMES REIT PREFERRED EXPERTISE

Overview of Preferred Stock and Offerings

- Summit Hotel Properties

- CBL & Associates

- Cedar Shopping Centers

- Glimcher Realty Trust

- Kite Realty Group

- Corporate Office Properties Trust

- Saul Centers

- Campus Crest Communities

- Excel Trust, Inc.

- Dupont Fabros

- LaSalle Hotels

- STAG Industrial

RAYMOND JAMES IS THE ONLY INVESTMENT BANK THAT DISTRIBUTES SHARES THROUGH OUR FULL RETAIL

SYSTEM AND TO INSTITUTIONS IN EVERY PREFERRED OFFERING MANAGED

Amount

Offerings (millions)

Non-Rated/Below Investment Grade 67 $6,591

Investment Grade 54 11,860

Total 121 $18,451

34

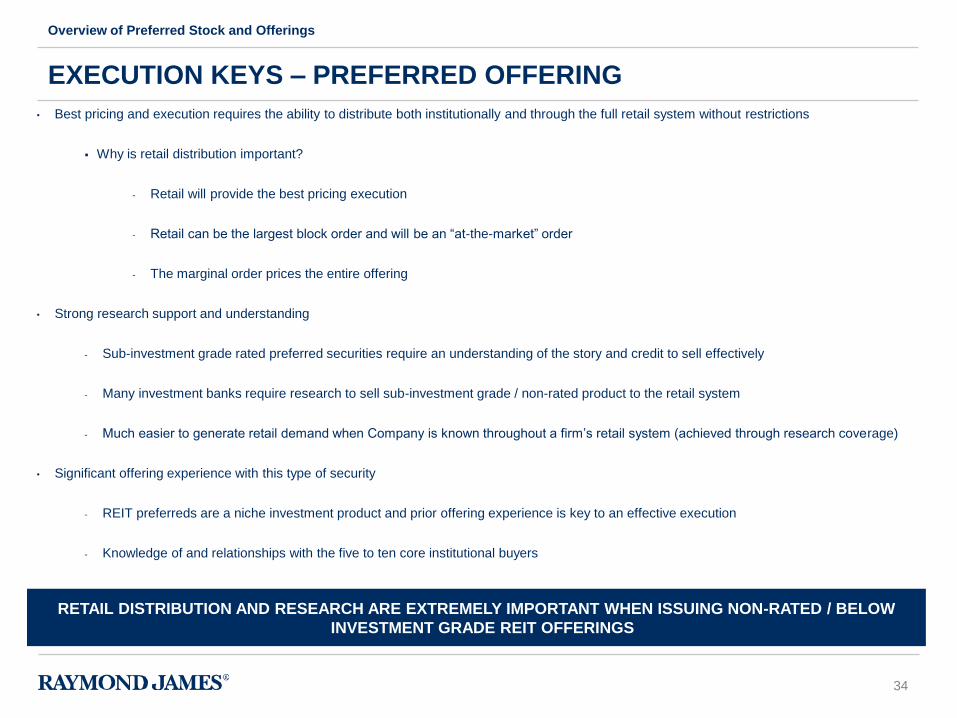

EXECUTION KEYS – PREFERRED OFFERING

Overview of Preferred Stock and Offerings

• Best pricing and execution requires the ability to distribute both institutionally and through the full retail system without restrictions

Why is retail distribution important?

- Retail will provide the best pricing execution

- Retail can be the largest block order and will be an “at-the-market” order

- The marginal order prices the entire offering

• Strong research support and understanding

- Sub-investment grade rated preferred securities require an understanding of the story and credit to sell effectively

- Many investment banks require research to sell sub-investment grade / non-rated product to the retail system

- Much easier to generate retail demand when Company is known throughout a firm’s retail system (achieved through research coverage)

• Significant offering experience with this type of security

- REIT preferreds are a niche investment product and prior offering experience is key to an effective execution

- Knowledge of and relationships with the five to ten core institutional buyers

RETAIL DISTRIBUTION AND RESEARCH ARE EXTREMELY IMPORTANT WHEN ISSUING NON-RATED / BELOW

INVESTMENT GRADE REIT OFFERINGS

35

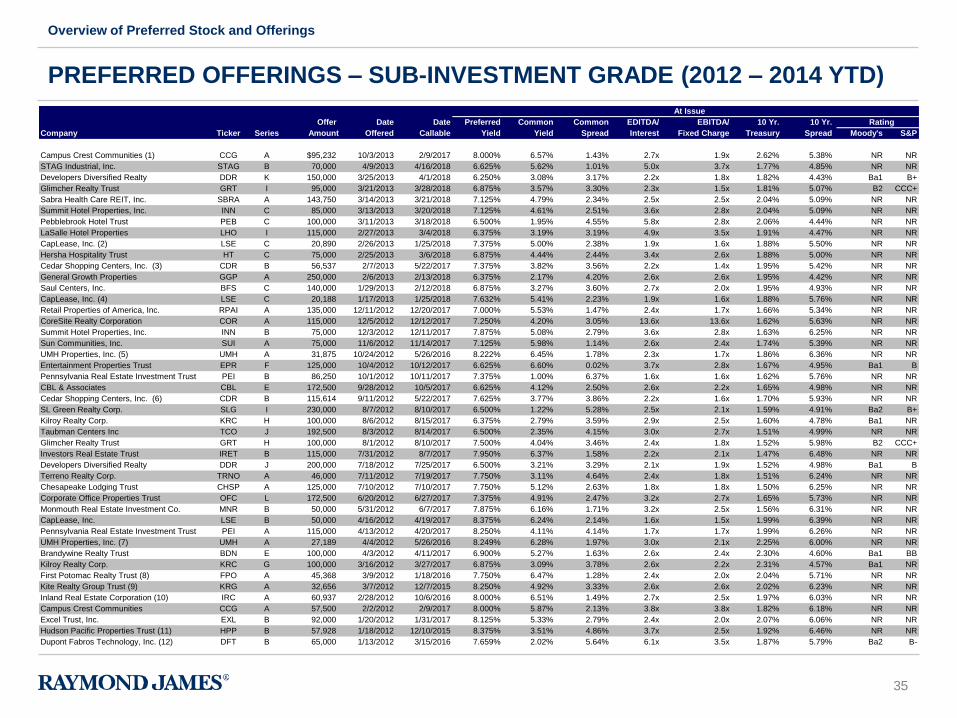

PREFERRED OFFERINGS – SUB-INVESTMENT GRADE (2012 – 2014 YTD)

Overview of Preferred Stock and Offerings

At Issue Current

Offer Date Date Preferred Common Common EDITDA/ EBITDA/ 10 Yr. 10 Yr. Rating

Company Ticker Series Amount Offered Callable Yield Yield Spread Interest Fixed Charge Treasury Spread Moody's S&P

Campus Crest Communities (1) CCG A $95,232 10/3/2013 2/9/2017 8.000% 6.57% 1.43% 2.7x 1.9x 2.62% 5.38% NR NR

STAG Industrial, Inc. STAG B 70,000 4/9/2013 4/16/2018 6.625% 5.62% 1.01% 5.0x 3.7x 1.77% 4.85% NR NR

Developers Diversified Realty DDR K 150,000 3/25/2013 4/1/2018 6.250% 3.08% 3.17% 2.2x 1.8x 1.82% 4.43% Ba1 B+

Glimcher Realty Trust GRT I 95,000 3/21/2013 3/28/2018 6.875% 3.57% 3.30% 2.3x 1.5x 1.81% 5.07% B2 CCC+

Sabra Health Care REIT, Inc. SBRA A 143,750 3/14/2013 3/21/2018 7.125% 4.79% 2.34% 2.5x 2.5x 2.04% 5.09% NR NR

Summit Hotel Properties, Inc. INN C 85,000 3/13/2013 3/20/2018 7.125% 4.61% 2.51% 3.6x 2.8x 2.04% 5.09% NR NR

Pebblebrook Hotel Trust PEB C 100,000 3/11/2013 3/18/2018 6.500% 1.95% 4.55% 5.8x 2.8x 2.06% 4.44% NR NR

LaSalle Hotel Properties LHO I 115,000 2/27/2013 3/4/2018 6.375% 3.19% 3.19% 4.9x 3.5x 1.91% 4.47% NR NR

CapLease, Inc. (2) LSE C 20,890 2/26/2013 1/25/2018 7.375% 5.00% 2.38% 1.9x 1.6x 1.88% 5.50% NR NR

Hersha Hospitality Trust HT C 75,000 2/25/2013 3/6/2018 6.875% 4.44% 2.44% 3.4x 2.6x 1.88% 5.00% NR NR

Cedar Shopping Centers, Inc. (3) CDR B 56,537 2/7/2013 5/22/2017 7.375% 3.82% 3.56% 2.2x 1.4x 1.95% 5.42% NR NR

General Growth Properties GGP A 250,000 2/6/2013 2/13/2018 6.375% 2.17% 4.20% 2.6x 2.6x 1.95% 4.42% NR NR

Saul Centers, Inc. BFS C 140,000 1/29/2013 2/12/2018 6.875% 3.27% 3.60% 2.7x 2.0x 1.95% 4.93% NR NR

CapLease, Inc. (4) LSE C 20,188 1/17/2013 1/25/2018 7.632% 5.41% 2.23% 1.9x 1.6x 1.88% 5.76% NR NR

Retail Properties of America, Inc. RPAI A 135,000 12/11/2012 12/20/2017 7.000% 5.53% 1.47% 2.4x 1.7x 1.66% 5.34% NR NR

CoreSite Realty Corporation COR A 115,000 12/5/2012 12/12/2017 7.250% 4.20% 3.05% 13.6x 13.6x 1.62% 5.63% NR NR

Summit Hotel Properties, Inc. INN B 75,000 12/3/2012 12/11/2017 7.875% 5.08% 2.79% 3.6x 2.8x 1.63% 6.25% NR NR

Sun Communities, Inc. SUI A 75,000 11/6/2012 11/14/2017 7.125% 5.98% 1.14% 2.6x 2.4x 1.74% 5.39% NR NR

UMH Properties, Inc. (5) UMH A 31,875 10/24/2012 5/26/2016 8.222% 6.45% 1.78% 2.3x 1.7x 1.86% 6.36% NR NR

Entertainment Properties Trust EPR F 125,000 10/4/2012 10/12/2017 6.625% 6.60% 0.02% 3.7x 2.8x 1.67% 4.95% Ba1 B

Pennsylvania Real Estate Investment Trust PEI B 86,250 10/1/2012 10/11/2017 7.375% 1.00% 6.37% 1.6x 1.6x 1.62% 5.76% NR NR

CBL & Associates CBL E 172,500 9/28/2012 10/5/2017 6.625% 4.12% 2.50% 2.6x 2.2x 1.65% 4.98% NR NR

Cedar Shopping Centers, Inc. (6) CDR B 115,614 9/11/2012 5/22/2017 7.625% 3.77% 3.86% 2.2x 1.6x 1.70% 5.93% NR NR

SL Green Realty Corp. SLG I 230,000 8/7/2012 8/10/2017 6.500% 1.22% 5.28% 2.5x 2.1x 1.59% 4.91% Ba2 B+

Kilroy Realty Corp. KRC H 100,000 8/6/2012 8/15/2017 6.375% 2.79% 3.59% 2.9x 2.5x 1.60% 4.78% Ba1 NR

Taubman Centers Inc TCO J 192,500 8/3/2012 8/14/2017 6.500% 2.35% 4.15% 3.0x 2.7x 1.51% 4.99% NR NR

Glimcher Realty Trust GRT H 100,000 8/1/2012 8/10/2017 7.500% 4.04% 3.46% 2.4x 1.8x 1.52% 5.98% B2 CCC+

Investors Real Estate Trust IRET B 115,000 7/31/2012 8/7/2017 7.950% 6.37% 1.58% 2.2x 2.1x 1.47% 6.48% NR NR

Developers Diversified Realty DDR J 200,000 7/18/2012 7/25/2017 6.500% 3.21% 3.29% 2.1x 1.9x 1.52% 4.98% Ba1 B

Terreno Realty Corp. TRNO A 46,000 7/11/2012 7/19/2017 7.750% 3.11% 4.64% 2.4x 1.8x 1.51% 6.24% NR NR

Chesapeake Lodging Trust CHSP A 125,000 7/10/2012 7/10/2017 7.750% 5.12% 2.63% 1.8x 1.8x 1.50% 6.25% NR NR

Corporate Office Properties Trust OFC L 172,500 6/20/2012 6/27/2017 7.375% 4.91% 2.47% 3.2x 2.7x 1.65% 5.73% NR NR

Monmouth Real Estate Investment Co. MNR B 50,000 5/31/2012 6/7/2017 7.875% 6.16% 1.71% 3.2x 2.5x 1.56% 6.31% NR NR

CapLease, Inc. LSE B 50,000 4/16/2012 4/19/2017 8.375% 6.24% 2.14% 1.6x 1.5x 1.99% 6.39% NR NR

Pennsylvania Real Estate Investment Trust PEI A 115,000 4/13/2012 4/20/2017 8.250% 4.11% 4.14% 1.7x 1.7x 1.99% 6.26% NR NR

UMH Properties, Inc. (7) UMH A 27,189 4/4/2012 5/26/2016 8.249% 6.28% 1.97% 3.0x 2.1x 2.25% 6.00% NR NR

Brandywine Realty Trust BDN E 100,000 4/3/2012 4/11/2017 6.900% 5.27% 1.63% 2.6x 2.4x 2.30% 4.60% Ba1 BB

Kilroy Realty Corp. KRC G 100,000 3/16/2012 3/27/2017 6.875% 3.09% 3.78% 2.6x 2.2x 2.31% 4.57% Ba1 NR

First Potomac Realty Trust (8) FPO A 45,368 3/9/2012 1/18/2016 7.750% 6.47% 1.28% 2.4x 2.0x 2.04% 5.71% NR NR

Kite Realty Group Trust (9) KRG A 32,656 3/7/2012 12/7/2015 8.250% 4.92% 3.33% 2.6x 2.6x 2.02% 6.23% NR NR

Inland Real Estate Corporation (10) IRC A 60,937 2/28/2012 10/6/2016 8.000% 6.51% 1.49% 2.7x 2.5x 1.97% 6.03% NR NR

Campus Crest Communities CCG A 57,500 2/2/2012 2/9/2017 8.000% 5.87% 2.13% 3.8x 3.8x 1.82% 6.18% NR NR

Excel Trust, Inc. EXL B 92,000 1/20/2012 1/31/2017 8.125% 5.33% 2.79% 2.4x 2.0x 2.07% 6.06% NR NR

Hudson Pacific Properties Trust (11) HPP B 57,928 1/18/2012 12/10/2015 8.375% 3.51% 4.86% 3.7x 2.5x 1.92% 6.46% NR NR

Dupont Fabros Technology, Inc. (12) DFT B 65,000 1/13/2012 3/15/2016 7.659% 2.02% 5.64% 6.1x 3.5x 1.87% 5.79% Ba2 B-

36

PREFERRED OFFERINGS – SUB-INVESTMENT GRADE (2012 – 2014 YTD)

Overview of Preferred Stock and Offerings

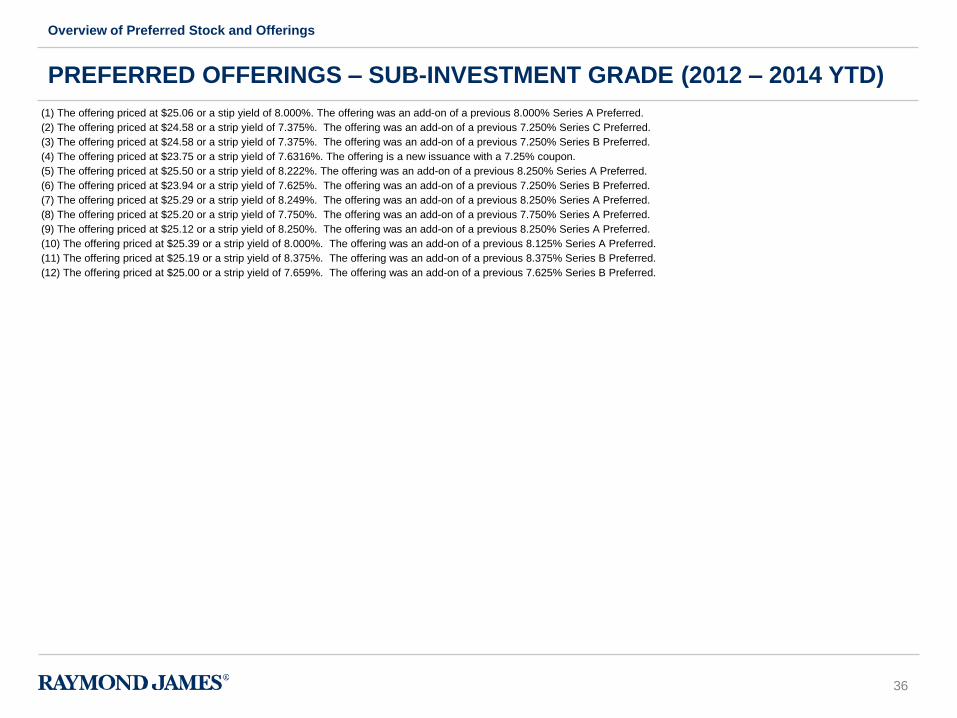

(1) The offering priced at $25.06 or a stip yield of 8.000%. The offering was an add-on of a previous 8.000% Series A Preferred.

(2) The offering priced at $24.58 or a strip yield of 7.375%. The offering was an add-on of a previous 7.250% Series C Preferred.

(3) The offering priced at $24.58 or a strip yield of 7.375%. The offering was an add-on of a previous 7.250% Series B Preferred.

(4) The offering priced at $23.75 or a strip yield of 7.6316%. The offering is a new issuance with a 7.25% coupon.

(5) The offering priced at $25.50 or a strip yield of 8.222%. The offering was an add-on of a previous 8.250% Series A Preferred.

(6) The offering priced at $23.94 or a strip yield of 7.625%. The offering was an add-on of a previous 7.250% Series B Preferred.

(7) The offering priced at $25.29 or a strip yield of 8.249%. The offering was an add-on of a previous 8.250% Series A Preferred.

(8) The offering priced at $25.20 or a strip yield of 7.750%. The offering was an add-on of a previous 7.750% Series A Preferred.

(9) The offering priced at $25.12 or a strip yield of 8.250%. The offering was an add-on of a previous 8.250% Series A Preferred.

(10) The offering priced at $25.39 or a strip yield of 8.000%. The offering was an add-on of a previous 8.125% Series A Preferred.

(11) The offering priced at $25.19 or a strip yield of 8.375%. The offering was an add-on of a previous 8.375% Series B Preferred.

(12) The offering priced at $25.00 or a strip yield of 7.659%. The offering was an add-on of a previous 7.625% Series B Preferred.

37

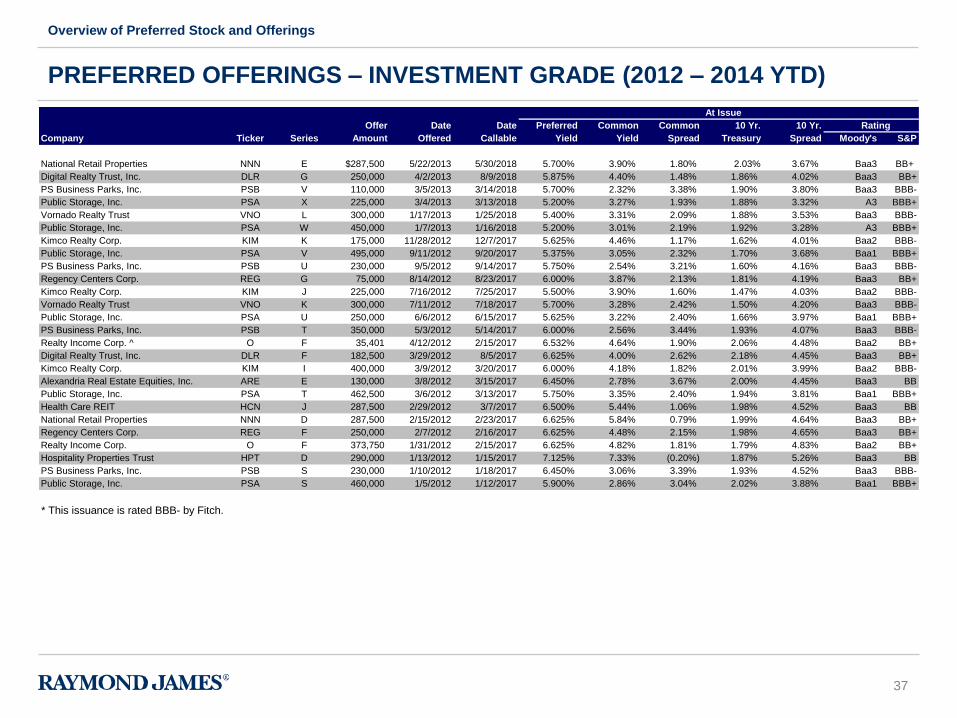

PREFERRED OFFERINGS – INVESTMENT GRADE (2012 – 2014 YTD)

Overview of Preferred Stock and Offerings

At Issue Current

Offer Date Date Preferred Common Common 10 Yr. 10 Yr. Rating

Company Ticker Series Amount Offered Callable Yield Yield Spread Treasury Spread Moody's S&P

National Retail Properties NNN E $287,500 5/22/2013 5/30/2018 5.700% 3.90% 1.80% 2.03% 3.67% Baa3 BB+

Digital Realty Trust, Inc. DLR G 250,000 4/2/2013 8/9/2018 5.875% 4.40% 1.48% 1.86% 4.02% Baa3 BB+

PS Business Parks, Inc. PSB V 110,000 3/5/2013 3/14/2018 5.700% 2.32% 3.38% 1.90% 3.80% Baa3 BBB-

Public Storage, Inc. PSA X 225,000 3/4/2013 3/13/2018 5.200% 3.27% 1.93% 1.88% 3.32% A3 BBB+

Vornado Realty Trust VNO L 300,000 1/17/2013 1/25/2018 5.400% 3.31% 2.09% 1.88% 3.53% Baa3 BBB-

Public Storage, Inc. PSA W 450,000 1/7/2013 1/16/2018 5.200% 3.01% 2.19% 1.92% 3.28% A3 BBB+

Kimco Realty Corp. KIM K 175,000 11/28/2012 12/7/2017 5.625% 4.46% 1.17% 1.62% 4.01% Baa2 BBB-

Public Storage, Inc. PSA V 495,000 9/11/2012 9/20/2017 5.375% 3.05% 2.32% 1.70% 3.68% Baa1 BBB+

PS Business Parks, Inc. PSB U 230,000 9/5/2012 9/14/2017 5.750% 2.54% 3.21% 1.60% 4.16% Baa3 BBB-

Regency Centers Corp. REG G 75,000 8/14/2012 8/23/2017 6.000% 3.87% 2.13% 1.81% 4.19% Baa3 BB+

Kimco Realty Corp. KIM J 225,000 7/16/2012 7/25/2017 5.500% 3.90% 1.60% 1.47% 4.03% Baa2 BBB-

Vornado Realty Trust VNO K 300,000 7/11/2012 7/18/2017 5.700% 3.28% 2.42% 1.50% 4.20% Baa3 BBB-

Public Storage, Inc. PSA U 250,000 6/6/2012 6/15/2017 5.625% 3.22% 2.40% 1.66% 3.97% Baa1 BBB+

PS Business Parks, Inc. PSB T 350,000 5/3/2012 5/14/2017 6.000% 2.56% 3.44% 1.93% 4.07% Baa3 BBB-

Realty Income Corp. ^ O F 35,401 4/12/2012 2/15/2017 6.532% 4.64% 1.90% 2.06% 4.48% Baa2 BB+

Digital Realty Trust, Inc. DLR F 182,500 3/29/2012 8/5/2017 6.625% 4.00% 2.62% 2.18% 4.45% Baa3 BB+

Kimco Realty Corp. KIM I 400,000 3/9/2012 3/20/2017 6.000% 4.18% 1.82% 2.01% 3.99% Baa2 BBB-

Alexandria Real Estate Equities, Inc. ARE E 130,000 3/8/2012 3/15/2017 6.450% 2.78% 3.67% 2.00% 4.45% Baa3 BB

Public Storage, Inc. PSA T 462,500 3/6/2012 3/13/2017 5.750% 3.35% 2.40% 1.94% 3.81% Baa1 BBB+

Health Care REIT HCN J 287,500 2/29/2012 3/7/2017 6.500% 5.44% 1.06% 1.98% 4.52% Baa3 BB

National Retail Properties NNN D 287,500 2/15/2012 2/23/2017 6.625% 5.84% 0.79% 1.99% 4.64% Baa3 BB+

Regency Centers Corp. REG F 250,000 2/7/2012 2/16/2017 6.625% 4.48% 2.15% 1.98% 4.65% Baa3 BB+

Realty Income Corp. O F 373,750 1/31/2012 2/15/2017 6.625% 4.82% 1.81% 1.79% 4.83% Baa2 BB+

Hospitality Properties Trust HPT D 290,000 1/13/2012 1/15/2017 7.125% 7.33% (0.20%) 1.87% 5.26% Baa3 BB

PS Business Parks, Inc. PSB S 230,000 1/10/2012 1/18/2017 6.450% 3.06% 3.39% 1.93% 4.52% Baa3 BBB-

Public Storage, Inc. PSA S 460,000 1/5/2012 1/12/2017 5.900% 2.86% 3.04% 2.02% 3.88% Baa1 BBB+

* This issuance is rated BBB- by Fitch.

38

Overview of Non-Traded REITs

SECTION 5

39

NON-TRADED REITS

Overview of Non-Traded REITs

• While the majority of REITs are publicly traded, there are REITs that are known as

non-traded (or non-listed) REITs

• Non-traded REITs are asset vehicles with no employees of their own, but rather they

are managed by an external advisor/sponsor

• There are currently 71 non-traded REITs in the US

• The external advisor may manage multiple non-traded REITs at the same time, in

exchange for a series of fees

• Because they are not publicly traded, non-traded REITs raise capital through one

time investors who have access to the investment through a broker, who receives a

commission for the sale of this illiquid investment

• Once the non-traded REIT has either reached the maximum of capital that it may

raise or has decided to no longer raise more capital, the non-traded REIT is “closed”

and no further investments are accepted

• Non-traded REITs end with a liquidity event – the most common liquidity events are

initial public offerings (IPOs) and direct acquisitions by other corporations or private

equity firms.

40

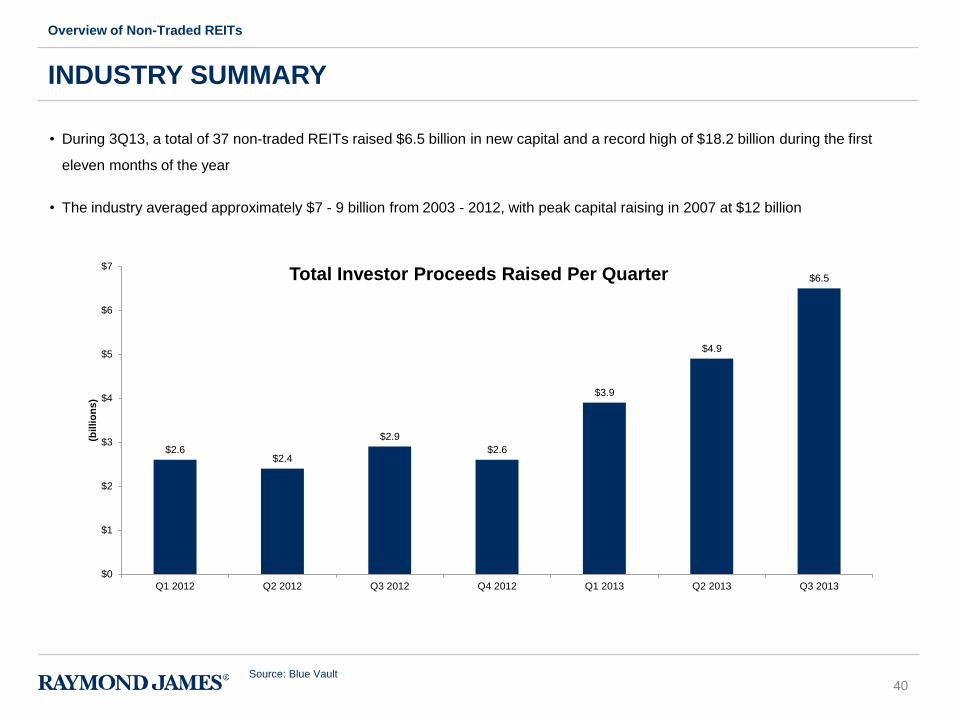

• During 3Q13, a total of 37 non-traded REITs raised $6.5 billion in new capital and a record high of $18.2 billion during the first

eleven months of the year

• The industry averaged approximately $7 - 9 billion from 2003 - 2012, with peak capital raising in 2007 at $12 billion

INDUSTRY SUMMARY

Overview of Non-Traded REITs

$2.6$2.4

$2.9

$2.6

$3.9

$4.9

$6.5

$0

$1

$2

$3

$4

$5

$6

$7

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013

(bil

lio

ns

)

Total Investor Proceeds Raised Per Quarter

Source: Blue Vault

41

Top-10 Sponsors:$63.6 Billion or

81%

Remaining 24 Sponsors:$15.2 Billion

or 19%

Top-10 Non-traded REIT Sponsor Market Share (as of 9/30/2013)

$1,777.7

$1,495.4 $1,477.8 $1,460.0

$1,247.0

$967.5$932.1

$865.3

$762.0

$511.6

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

Griffin-AmericanHealthcare REIT II

Cole CorporateIncome Trust

American RealtyCapital Trust IV

American RealtyCapital Trust V

American RealtyCapital Healthcare

Trust

Cole CreditProperties Trust

IV

Phillips Edison -ARC ShoppingCenter REIT

American RealtyCapital New YorkRecovery REIT

Industrial IncomeTrust

Hines GlobalREIT

(millio

ns)

Top-10 REITs Ranked by Investor Proceeds Raised(YTD as of 9/30/2013)

Closed Non-traded REITs: $58.2 Billion or 73.9%

Open Non-traded REITs: $20.6 Billion or 26.1%

Total Non-traded REIT Industry Assets: $78.8 Billion (as of 9/30/2013)

$5,289.8

$2,500.4

$1,951.1

$932.1$808.8

$518.4 $511.6 $443.3$338.4 $333.7

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

AR Capital Cole Real Estate Griffin Capital /Griffin-American

Phillips Edison Dividend Capital Northstar Hines W.P. Carey CNL Carter

(millio

ns)

Top-10 Sponsors Ranked by Investor Proceeds Raised(YTD as of 9/30/2013)

INDUSTRY SUMMARY

Overview of Non-Traded REITs

Source: Blue Vault

42

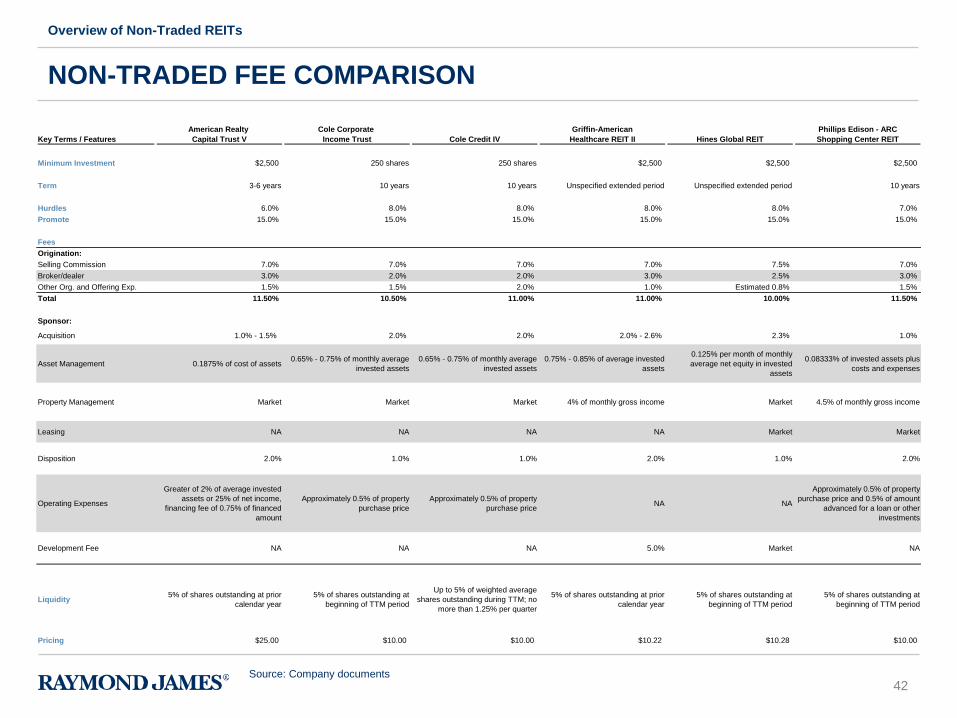

American Realty Cole Corporate Griffin-American Phillips Edison - ARC

Key Terms / Features Capital Trust V Income Trust Cole Credit IV Healthcare REIT II Hines Global REIT Shopping Center REIT

Minimum Investment $2,500 250 shares 250 shares $2,500 $2,500 $2,500

Term 3-6 years 10 years 10 years Unspecified extended period Unspecified extended period 10 years

Hurdles 6.0% 8.0% 8.0% 8.0% 8.0% 7.0%

Promote 15.0% 15.0% 15.0% 15.0% 15.0% 15.0%

Fees

Origination:

Selling Commission 7.0% 7.0% 7.0% 7.0% 7.5% 7.0%

Broker/dealer 3.0% 2.0% 2.0% 3.0% 2.5% 3.0%

Other Org. and Offering Exp. 1.5% 1.5% 2.0% 1.0% Estimated 0.8% 1.5%

Total 11.50% 10.50% 11.00% 11.00% 10.00% 11.50%

Sponsor:

Acquisition 1.0% - 1.5% 2.0% 2.0% 2.0% - 2.6% 2.3% 1.0%

Asset Management 0.1875% of cost of assets0.65% - 0.75% of monthly average

invested assets

0.65% - 0.75% of monthly average

invested assets

0.75% - 0.85% of average invested

assets

0.125% per month of monthly

average net equity in invested

assets

0.08333% of invested assets plus

costs and expenses

Property Management Market Market Market 4% of monthly gross income Market 4.5% of monthly gross income

Leasing NA NA NA NA Market Market

Disposition 2.0% 1.0% 1.0% 2.0% 1.0% 2.0%

Operating Expenses

Greater of 2% of average invested

assets or 25% of net income,

financing fee of 0.75% of financed

amount

Approximately 0.5% of property

purchase price

Approximately 0.5% of property

purchase priceNA NA

Approximately 0.5% of property

purchase price and 0.5% of amount

advanced for a loan or other

investments

Development Fee NA NA NA 5.0% Market NA

Liquidity5% of shares outstanding at prior

calendar year

5% of shares outstanding at

beginning of TTM period

Up to 5% of weighted average

shares outstanding during TTM; no

more than 1.25% per quarter

5% of shares outstanding at prior

calendar year

5% of shares outstanding at

beginning of TTM period

5% of shares outstanding at

beginning of TTM period

Pricing $25.00 $10.00 $10.00 $10.22 $10.28 $10.00

NON-TRADED FEE COMPARISON

Overview of Non-Traded REITs

Source: Company documents

43

Real Estate Illustrative Transactions

SECTION 6

44

ILLUSTRATIVE TRANSACTIONS

Real Estate Illustrative Transactions

• Raymond James has substantial experience in partnering with real estate companies to successfully grow their business

• Unequivocal success in advisory and capital raising roles in variety of strategies, products, and markets

• High level of repeat business from several clients over extended period of time is evidence of successful and valued partnership

• Transactions with the following companies showcase the client-centric business model and broad capabilities of the Raymond James Real

Estate Group

• LaSalle Hotel Properties

• Hersha Hospitality Trust

• American Homes 4 Rent

• Encore Enterprises Inc.

• Kaplan Development Group

• Woolbright Development

• BioMed Realty Trust

• Pebblebrook Hotel Trust

• Campus Crest Communities, Inc.

45

Transaction Size

Type Offer Date ($MM)

Preferred 2/27/2013 $110.0

Common 12/13/2012 218.0

Current At-the-Market 3/4/2011 250.0

Preferred 1/19/2011 68.8

Preferred 5/14/2010 36.2

At-the-Market 4/21/2010 150.0

Common 3/2/2010 113.8

Common 6/10/2009 147.5

Common 4/23/2009 124.9

Preferred 11/14/2006 100.0

Preferred 2/3/2006 87.5

Common 2/2/2006 142.9

Common 10/7/2005 75.5

Preferred 8/19/2005 79.3

Common 11/16/2004 57.2

Preferred 9/23/2003 27.5

Common 6/25/2003 33.1

Preferred 2/28/2002 99.8

Total 18 $1,921.9

CASE STUDY: LASALLE HOTEL PROPERTIES

Real Estate Illustrative Transactions

$1.9 BILLION RAISED TOGETHER SINCE 2002

RAYMOND JAMES HAS HELPED LASALLE GROW

TO A $4.1 BILLION REIT WITH 40 ASSETS IN 13

MARKETS

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

$1,400.0

$1,600.0

$1,800.0

$2,000.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Through 2003:

$160 million

Through 2009:

$997 million

Through 2005:

$394 million

Through 2004:

$240 million

Through 2006:

$725 million

Through 2011:

$1.6 billion

Since 2002: $1.9 billion

San Francisco Washington, DC

Newport

San Diego

Los Angeles

Santa Cruz

Seattle

Indianapolis

Chicago Philadelphia

New York City

Boston

Leesburg

Target Urban Market

Current Market

46

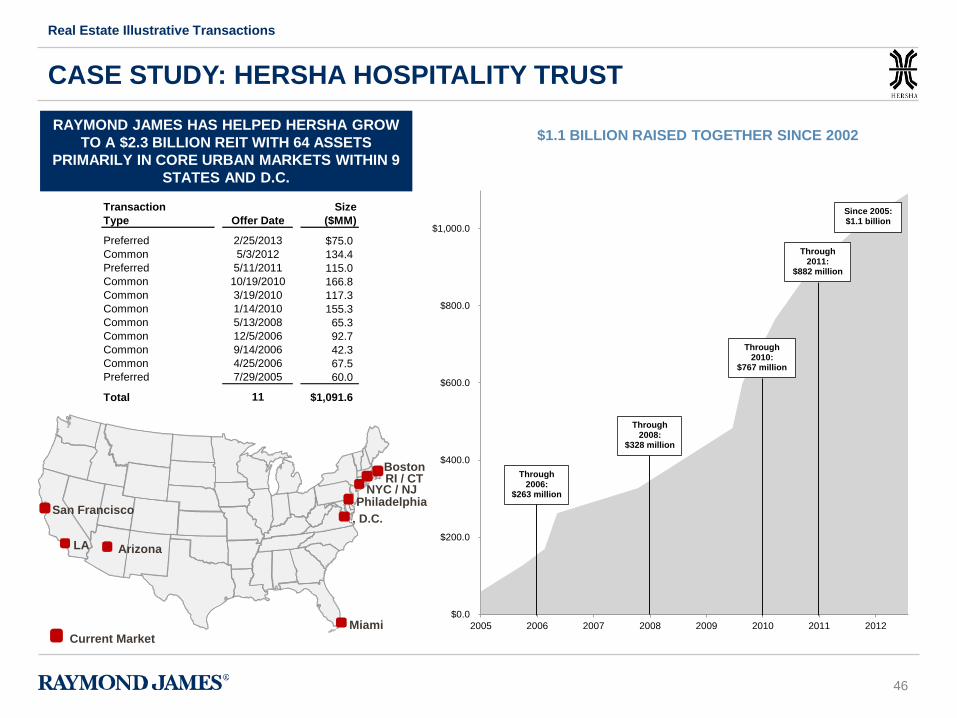

CASE STUDY: HERSHA HOSPITALITY TRUST

Real Estate Illustrative Transactions

$1.1 BILLION RAISED TOGETHER SINCE 2002

RAYMOND JAMES HAS HELPED HERSHA GROW

TO A $2.3 BILLION REIT WITH 64 ASSETS

PRIMARILY IN CORE URBAN MARKETS WITHIN 9

STATES AND D.C.

, D.C.

LA

Miami

Philadelphia NYC / NJ

Boston

San Francisco

Current Market

Arizona

RI / CT

Transaction Size

Type Offer Date ($MM)

Preferred 2/25/2013 $75.0

Common 5/3/2012 134.4

Preferred 5/11/2011 115.0

Common 10/19/2010 166.8

Common 3/19/2010 117.3

Common 1/14/2010 155.3

Common 5/13/2008 65.3

Common 12/5/2006 92.7

Common 9/14/2006 42.3

Common 4/25/2006 67.5

Preferred 7/29/2005 60.0

Total 11 $1,091.6

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

2005 2006 2007 2008 2009 2010 2011 2012

Through 2010:

$767 million

Through 2008:

$328 million

Through 2006:

$263 million

Through 2011:

$882 million

Since 2005: $1.1 billion

47

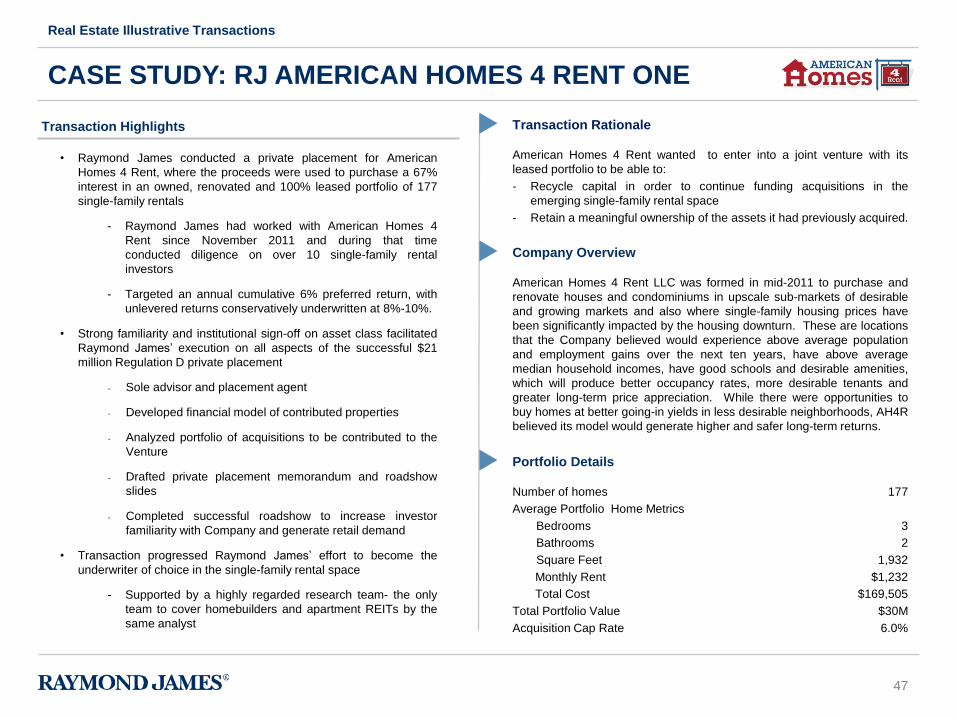

Transaction Highlights

• Raymond James conducted a private placement for American

Homes 4 Rent, where the proceeds were used to purchase a 67%

interest in an owned, renovated and 100% leased portfolio of 177

single-family rentals

- Raymond James had worked with American Homes 4

Rent since November 2011 and during that time

conducted diligence on over 10 single-family rental

investors

- Targeted an annual cumulative 6% preferred return, with

unlevered returns conservatively underwritten at 8%-10%.

• Strong familiarity and institutional sign-off on asset class facilitated

Raymond James’ execution on all aspects of the successful $21

million Regulation D private placement

- Sole advisor and placement agent

- Developed financial model of contributed properties

- Analyzed portfolio of acquisitions to be contributed to the

Venture

- Drafted private placement memorandum and roadshow

slides

- Completed successful roadshow to increase investor

familiarity with Company and generate retail demand

• Transaction progressed Raymond James’ effort to become the

underwriter of choice in the single-family rental space

- Supported by a highly regarded research team- the only

team to cover homebuilders and apartment REITs by the

same analyst

CASE STUDY: RJ AMERICAN HOMES 4 RENT ONE

Real Estate Illustrative Transactions

Company Overview

American Homes 4 Rent LLC was formed in mid-2011 to purchase and

renovate houses and condominiums in upscale sub-markets of desirable

and growing markets and also where single-family housing prices have

been significantly impacted by the housing downturn. These are locations

that the Company believed would experience above average population

and employment gains over the next ten years, have above average

median household incomes, have good schools and desirable amenities,

which will produce better occupancy rates, more desirable tenants and

greater long-term price appreciation. While there were opportunities to

buy homes at better going-in yields in less desirable neighborhoods, AH4R

believed its model would generate higher and safer long-term returns.

177

3

2

1,932

$1,232

$169,505

$30M

6.0%

Portfolio Details

Number of homes

Average Portfolio Home Metrics

Bedrooms

Bathrooms

Square Feet

Monthly Rent

Total Cost

Total Portfolio Value

Acquisition Cap Rate

Transaction Rationale

American Homes 4 Rent wanted to enter into a joint venture with its

leased portfolio to be able to:

- Recycle capital in order to continue funding acquisitions in the

emerging single-family rental space

- Retain a meaningful ownership of the assets it had previously acquired.

48

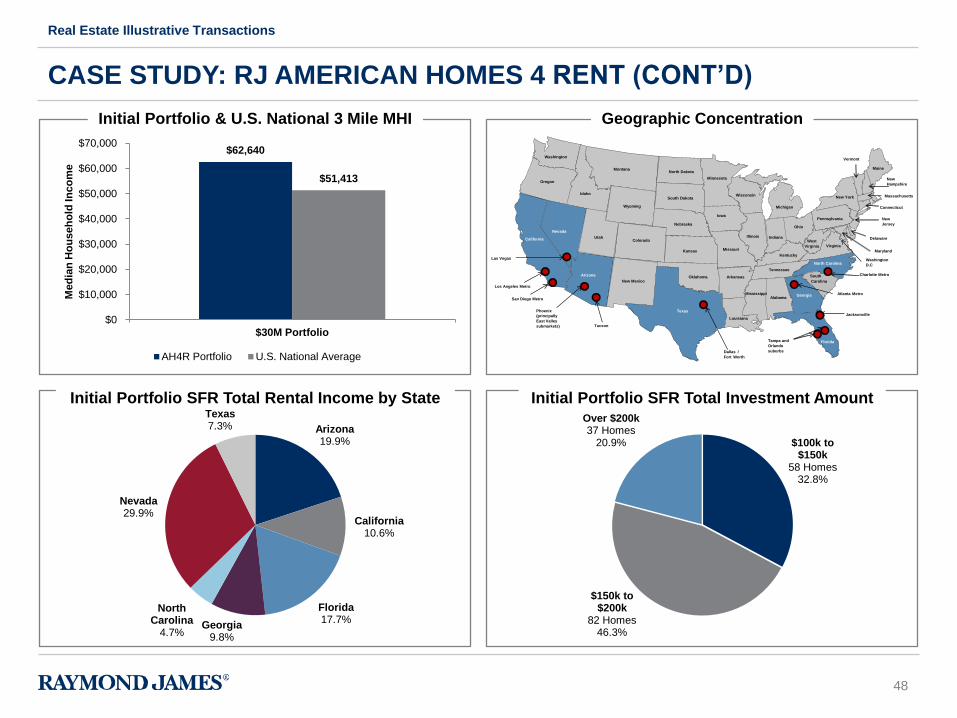

CASE STUDY: RJ AMERICAN HOMES 4 RENT (CONT’D)

Initial Portfolio & U.S. National 3 Mile MHI Geographic Concentration

Initial Portfolio SFR Total Rental Income by State Initial Portfolio SFR Total Investment Amount

Arizona 19.9%

California 10.6%

Florida 17.7%

Georgia 9.8%

North Carolina

4.7%

Nevada 29.9%

Texas 7.3%

$62,640

$51,413

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$30M Portfolio

Med

ian

Ho

us

eh

old

In

co

me

AH4R Portfolio U.S. National Average

$100k to $150k

58 Homes 32.8%

$150k to $200k

82 Homes 46.3%

Over $200k 37 Homes

20.9%

Real Estate Illustrative Transactions

Washington

Oregon

California

Idaho

Montana

Wyoming

Nevada

Arizona

Colorado

New Mexico

North Dakota

South Dakota

Nebraska

Kansas

Oklahoma

Texas

Minnesota

Iowa

Missouri

Louisiana

Wisconsin

Illinois

Michigan

Indiana

Kentucky

Tennessee

Alabama

Ohio

New York

Pennsylvania

Virginia

North Carolina

South

Carolina

Georgia

Maine

Arkansas

Utah

Los Angeles Metro

San Diego Metro

Phoenix

(principally

East Valley

submarkets) Tucson

Dallas /

Fort Worth

Tampa and

Orlando

suburbs

Jacksonville

Atlanta Metro

Charlotte Metro

Las Vegas

Vermont

New

Hampshire

Massachusetts

Connecticut

New

Jersey

Washington

D.C

Maryland

Delaware

Mississippi

West

Virginia

Florida

49

CASE STUDY: ENCORE ENTERPRISES INC.

Real Estate Illustrative Transactions

Transaction Rationale

• Company raised capital to leverage its management team and

operating infrastructure into larger asset base

• Aggressively grew asset base while secondary market assets

were out of favor

• Capitalized on secondary market compression and strong

operating performance to monetize large portfolio

• Use proceeds to provide dry powder for more attractive

investment environment, which has been effectively deployed

into multiple other profitable investments

Transaction Highlights

• Evaluated the Company and its growth capital alternatives,

including asset vs. entity and pari passu vs. senior equity capital

• Performed valuation analysis, developed budgets, financial

model and offering materials, and identified appropriate partners

based cultural fit

• Successfully executed highly structured $85 million entity

investment by respected investor, Rothschild Realty

• Encore used the capital to increase its room count from 1,880 to

3,371 in 18 months

• Evaluated asset and capital market conditions to determine if the

Company should monetize its holding in 2007

• Advised the Company on its $400 million portfolio sale in August

2007 to a Goldman Sachs sponsored fund

• Achieved aggressive pricing (14x pro forma year 1 EBITDA) and

closing despite market turmoil by establishing stalking horse bid

• Round trip transactions resulted in a $100 million+ profit to

Encore in approximately two years

• Raymond James continues to act as Encore’s advisor for its

hospitality, multifamily, retail and office vehicles

Company Overview

Encore Enterprises, Inc. (“Encore”) is a private real estate acquisition,

development and management company investing in branded limited

service hotels located in primary, secondary and tertiary markets

primarily focused in the Southeast. The Company’s strategy is to

capitalize on management’s sophisticated management information

systems and communications network to acquire and improve the

performance of underperforming, independently managed Marriott,

Hilton and InterContinental branded limited service hotels. Following the

transaction, the Company owned or had an ownership interest in and

managed 17 limited service hotels with 1,482 rooms.

Transaction Overview (Capital Raise)

Transaction size

Investment structure

Governance

Fees

Portfolio size

Locations

June 2005

$85 million

9.0% convertible debenture

Equal representation

Property management and acquisition

21 hotels (1,880 rooms)

Southeastern United States

Encore Hospitality and

Private Capital Raise – Entity Investment

50

CASE STUDY: KAPLAN DEVELOPMENT GROUP

Real Estate Illustrative Transactions

Transaction Highlights

• Provided extensive financial analysis on its portfolio of properties

and operating business and advised Kaplan Development on

available strategic alternatives

• Negotiated the buyout of Kaplan’s multiple partners at an

attractive valuation

• Ultimately structured a programmatic joint venture:

• generating liquidity for Kaplan’s principals to pull out of

the Company via the majority sale of 6 properties

• commitment of equity to fund growth

• high margin development and management fees

Transaction Rationale

• Provided liquidity for principals

• Capital to pursue growth strategy

• Like-minded equity partner

Transaction Background

Having previously worked with the head of Raymond James Real Estate

Investment Banking to take Kapson Senior Quarters public, a senior housing

company controlled by the principals of Kaplan, and to subsequently sell the

company to Lazard Freres for a significant profit, Kaplan approached Raymond

James to once again find a financial partner to help the Company grow.

Transaction Overview

Transaction size

Portfolio size

Locations

Initial Property Valuation

$350 million ($74.3 million of equity)

6 properties (560 Units)

New Jersey, Pennsylvania,

Delaware & Georgia

$78.5 million

joint-venture with

51

CASE STUDY: WOOLBRIGHT DEVELOPMENT

Real Estate Illustrative Transactions

Transaction Highlights

• Evaluated asset and capital market conditions to determine if the

Company should be a net investor or seller

• Evaluated monetization alternatives including raising a fund,

recapitalizing existing joint-ventures, going public via an IPO or

an outright sale

• Advised the Company on identifying a portfolio for sale based on

project status, homogeneity and joint-venture partner goals

• Executed parallel bulk and individual asset sales to maximize

value, ultimately resulting three separate transactions, including

with some public companies

• Achieved aggressive pricing (6.1% implied cap rate on pro forma

year 1 NOI, inclusive of master lease income)

• Opined as to transaction fairness to 5 institutional partners

Transaction Rationale

• Capitalize on current market conditions to monetize large portfolio,

benefitting limited partners and capturing large promotes

• Sell assets that had been substantially redeveloped or where full

value could be harvested

• Use proceeds to repay debt and provide dry powder for more

attractive investment environment

Company Overview

Woolbright Development Inc. is a private real estate company focused on value

add shopping center opportunities in the six major metros of Florida. The

Company has successfully partnered with sophisticated investors such as Heitman,

Principal, Black Rock, Morgan Stanley and Lone Star to acquire, redevelop,

develop and sell several billion dollars of assets over the past ten years.

Woolbright's success is driven by its focus on the key areas of research,

technology, acquisitions, leasing, and customer-focused property management.

The Company’s current portfolio includes more than 30 projects totaling nearly 5

million square feet of retail and mixed-use real estate.

portfolio sale to

Transaction Overview

Transaction size

Portfolio size

Locations

Implied cap rate

Price per square foot

Bidders

$425 million

10 centers (1.7 million sq. ft)

Miami, Palm Beach, Orlando, Tampa

6.1%

$250

35

52

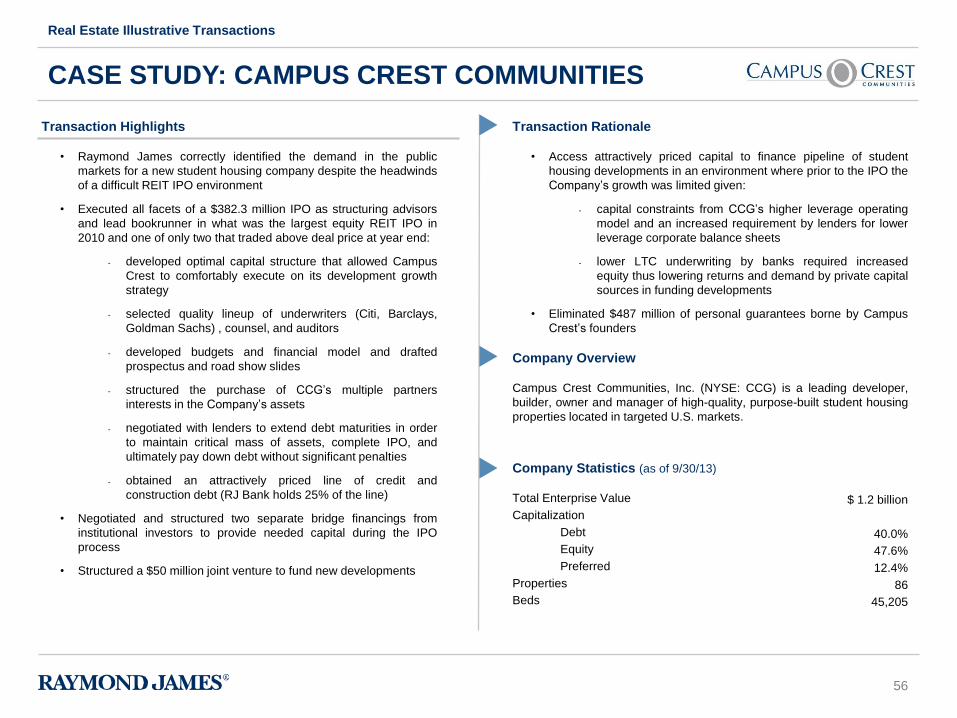

Transaction Highlights

• Evaluated strategic alternatives and developed strategic plan for 3

person Company with $120 million of assets

• Executed all aspects of the successful $465 million IPO as

structuring advisor and lead bookrunner 18 months later

- Refined marketing identity

- Selected board members and underwriters

- Developed budgets and financial model

- Analyzed acquisitions

- Negotiated line of credit

- Drafted prospectus and roadshow slides

• Partnered with Company on all major transactions, executed or not,

over the next nine years

- Raised $4.5 billion in capital in common stock, preferred

stock, joint-venture, convertible bonds and bond offerings

- Effectuated conservative KISS capital markets strategy

leading to strong performance through 2008-09 credit

crisis, culminating in investment grade bond rating in April

2010

- Evaluated several large acquisitions, successfully

acquiring and financing several and most importantly

passing on most

• Company has successfully grown into 175 person, 14.4 million

square foot, $6.2 billion public REIT with 100.6% cumulative total

return since its IPO

CASE STUDY: BIOMED REALTY TRUST

Real Estate Illustrative Transactions

Transaction Rationale

• BioMed accessed the public markets due to a financing arbitrage

that existed between the public and private markets

• 2004-06: The Company aggressively invested and match funded its

capital requirements to capitalize on this arbitrage

• 2007-09: Slowed its acquisition pace and re-equitized the company

via public and private JV capital in advance of credit crunch

• 2010-current: BioMed was awarded an investment grade rating and

accelerated investment armed with this new, lower cost of capital

Company Overview

BioMed Realty Trust is a $6.2 billion enterprise value REIT focused on

Providing Real Estate to the Life Science Industry®. The Company's

tenants primarily include biotechnology and pharmaceutical companies,

scientific research institutions, government agencies and other entities

involved in the life science industry. BioMed has interests in properties

comprising approximately 14.4 million rentable square feet located

predominantly in all major U.S. life science markets that have well-

established reputations as centers for scientific research.

$6.2 billion

40.6%

59.4%

0.0%

Baa3 / BBB-

173

14.4 million sq. ft.

Company Statistics (as of 9/30/2013)

Total Enterprise Value

Capitalization

Debt

Equity

Preferred

Credit Rating (Moody’s / S&P)

Buildings

Square Feet

53

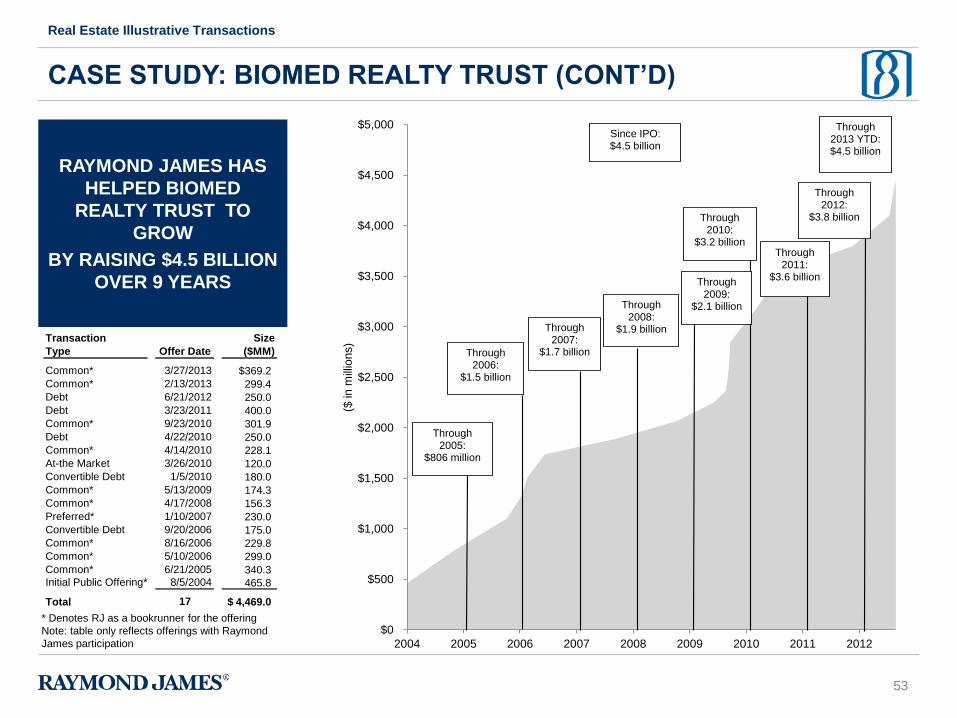

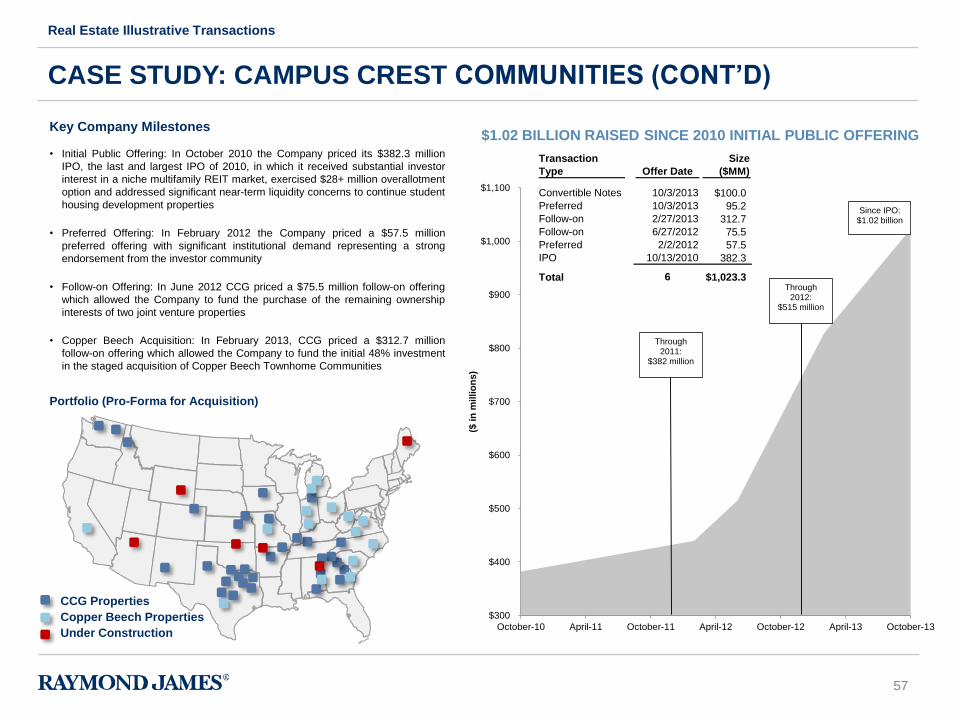

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

2004 2005 2006 2007 2008 2009 2010 2011 2012

($ in m

illio

ns)

Through 2005:

$806 million

Through 2006:

$1.5 billion

Through 2007:

$1.7 billion

Through 2008:

$1.9 billion

Since IPO:$4.5 billion

Through 2009:

$2.1 billion

Through 2010:

$3.2 billionThrough

2011: $3.6 billion

Through 2012:

$3.8 billion

Through 2013 YTD: $4.5 billion

Transaction Size

Type Offer Date ($MM)

Common* 3/27/2013 $369.2

Common* 2/13/2013 299.4

Debt 6/21/2012 250.0

Debt 3/23/2011 400.0

Common* 9/23/2010 301.9

Debt 4/22/2010 250.0

Common* 4/14/2010 228.1

At-the Market 3/26/2010 120.0

Convertible Debt 1/5/2010 180.0

Common* 5/13/2009 174.3

Common* 4/17/2008 156.3

Preferred* 1/10/2007 230.0

Convertible Debt 9/20/2006 175.0

Common* 8/16/2006 229.8

Common* 5/10/2006 299.0

Common* 6/21/2005 340.3Initial Public Offering* 8/5/2004 465.8

Total 17 4,469.0$

CASE STUDY: BIOMED REALTY TRUST (CONT’D)

Real Estate Illustrative Transactions

RAYMOND JAMES HAS

HELPED BIOMED

REALTY TRUST TO

GROW

BY RAISING $4.5 BILLION

OVER 9 YEARS

* Denotes RJ as a bookrunner for the offering

Note: table only reflects offerings with Raymond

James participation

54

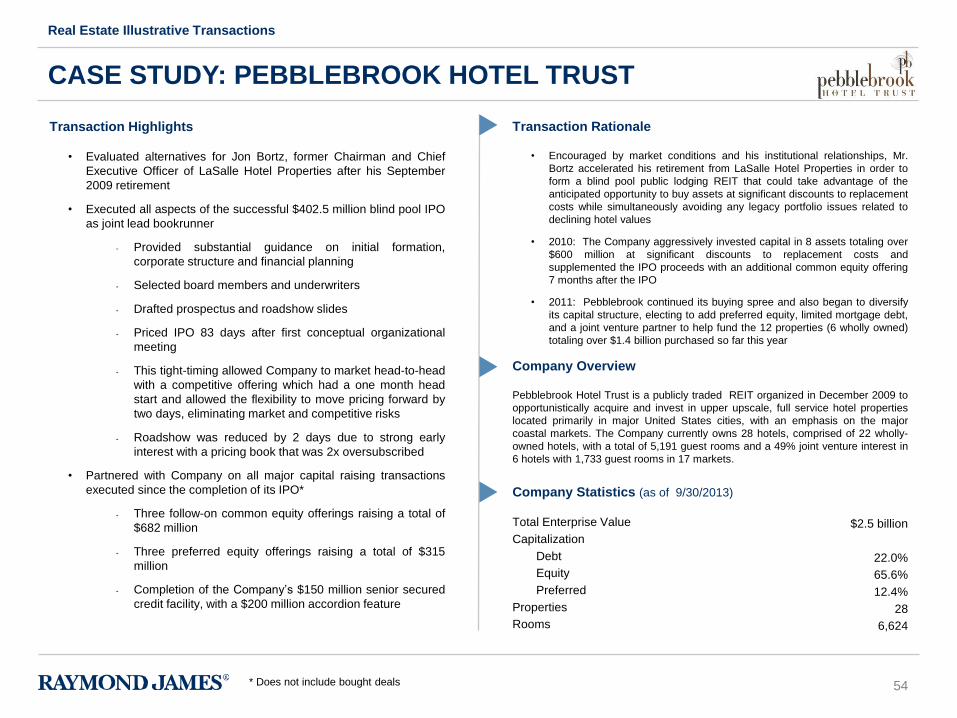

Transaction Highlights

• Evaluated alternatives for Jon Bortz, former Chairman and Chief

Executive Officer of LaSalle Hotel Properties after his September

2009 retirement

• Executed all aspects of the successful $402.5 million blind pool IPO

as joint lead bookrunner

- Provided substantial guidance on initial formation,

corporate structure and financial planning

- Selected board members and underwriters

- Drafted prospectus and roadshow slides

- Priced IPO 83 days after first conceptual organizational

meeting

- This tight-timing allowed Company to market head-to-head

with a competitive offering which had a one month head

start and allowed the flexibility to move pricing forward by

two days, eliminating market and competitive risks

- Roadshow was reduced by 2 days due to strong early

interest with a pricing book that was 2x oversubscribed

• Partnered with Company on all major capital raising transactions

executed since the completion of its IPO*

- Three follow-on common equity offerings raising a total of

$682 million

- Three preferred equity offerings raising a total of $315

million

- Completion of the Company’s $150 million senior secured

credit facility, with a $200 million accordion feature

CASE STUDY: PEBBLEBROOK HOTEL TRUST

Real Estate Illustrative Transactions

Transaction Rationale

• Encouraged by market conditions and his institutional relationships, Mr.

Bortz accelerated his retirement from LaSalle Hotel Properties in order to

form a blind pool public lodging REIT that could take advantage of the

anticipated opportunity to buy assets at significant discounts to replacement

costs while simultaneously avoiding any legacy portfolio issues related to

declining hotel values

• 2010: The Company aggressively invested capital in 8 assets totaling over

$600 million at significant discounts to replacement costs and

supplemented the IPO proceeds with an additional common equity offering

7 months after the IPO

• 2011: Pebblebrook continued its buying spree and also began to diversify

its capital structure, electing to add preferred equity, limited mortgage debt,

and a joint venture partner to help fund the 12 properties (6 wholly owned)

totaling over $1.4 billion purchased so far this year

Company Overview

Pebblebrook Hotel Trust is a publicly traded REIT organized in December 2009 to

opportunistically acquire and invest in upper upscale, full service hotel properties

located primarily in major United States cities, with an emphasis on the major

coastal markets. The Company currently owns 28 hotels, comprised of 22 wholly-

owned hotels, with a total of 5,191 guest rooms and a 49% joint venture interest in

6 hotels with 1,733 guest rooms in 17 markets.

$2.5 billion

22.0%

65.6%

12.4%

28

6,624

Company Statistics (as of 9/30/2013)

Total Enterprise Value

Capitalization

Debt

Equity

Preferred

Properties

Rooms

* Does not include bought deals

55

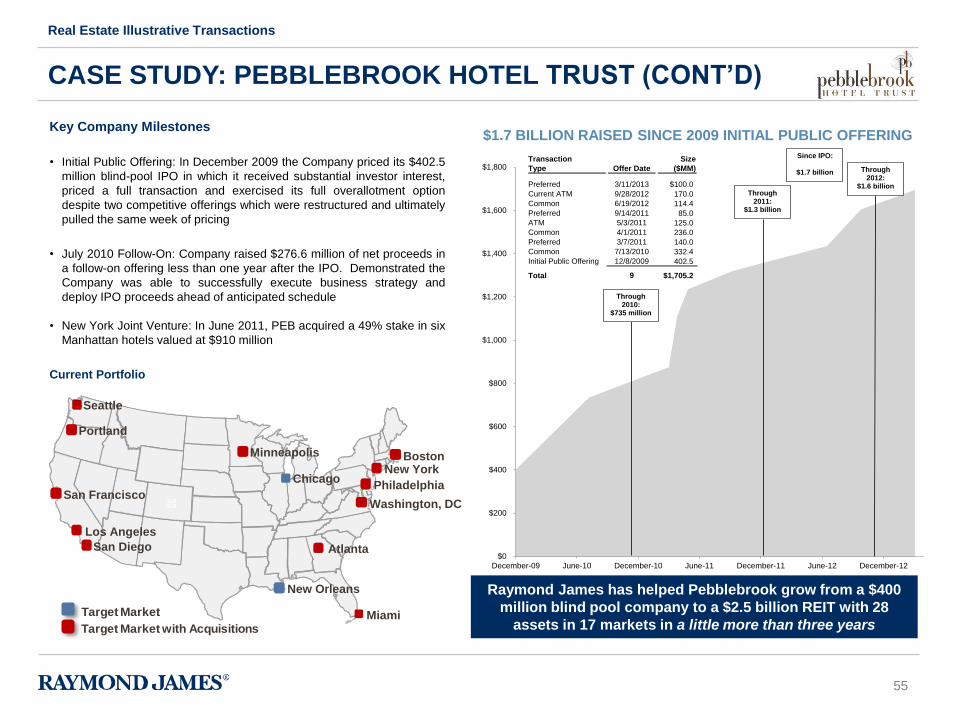

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

December-09 June-10 December-10 June-11 December-11 June-12 December-12

Through 2010:

$735 million

Through 2011:

$1.3 billion

Since IPO:

$1.7 billion Through 2012:

$1.6 billion

CASE STUDY: PEBBLEBROOK HOTEL TRUST (CONT’D)

Real Estate Illustrative Transactions