Embed Size (px)

Citation preview

REAL ESTATE BENCHMARKING SURVEY

PRO

FESSIO

NA

LSTA

ND

AR

DS

EXECUTIVE SUMMARYPwC and ANREV are delighted to publish the results of our real estate fund managers’ benchmarking survey, which was designed to gather, analyse, and share information about key industry operational trends and metrics of real estate fund managers with significant operations in Asia Pacific. We gathered data covering industry practices relating to organisational information, governance, risk management, administration, valuation, technology and operations, regulatory information and reporting. This report represents the summary of the data and includes key takeaways, by section, to assist you with your review.

Given the data is collected from various fund managers with different business models and structures, the same operational arrangement does not apply to all the fund managers. Naturally the scale of investment mandates, the number, location and diversity of investments, reporting and governance needs of investors, together with the institutionalisation of the wider business, are factors which will impact the operational structures needing to be put in place. Thus, we have explored how the practices may vary depending on the geographical locations and the size of the managers.

PwC conducted this survey to explore trends that would help real estate fund executives and management teams benchmark their practices against their industry peers. We have extracted some key takeaways on the next page. We hope that you find our results and analysis helpful.

Headcount expected to increase up to 20% in the coming year, clearly indicating that industry players still retain a positive outlook for Asia-Pacific business in 2018 and beyond.

Market risk is seen as the top risk priority for all respondents. Other risks such as liquidity and regulatory risks come close, and are also high on the radar of managers.

Headcount Risk priorities

Accounting services are mostly outsourced whilst investor reporting and treasury functions are mainly performed in-house. Those who do not outsource indicate they have no plans to do so in the near term.

Administrators

100% of managers use external valuers at least annually. Most respondents use global valuation firms and over 60% of managers engage more than one valuer. Furthermore, most managers conduct quarterly valuations in efforts to provide regular reporting and more insightful investor reports.

Independentvaluation

The majority of our respondents are regulated. At least 38% of the managers have been reviewed by relevant regulatory bodies in last 12 months. Regulatory risk remains a key risk priority to the managers.

Regulation

The majority of respondents received investors’ queries relating to historical performance and future outlook; while half of them got queries about environmental information, indicating that ESG is a key focus to LPs.

Investor reporting

AustraliaAvg. AUM — US$ 13.28bn Avg. FTE – 136No. of respondents — 6

Europe and North Americas

Avg. AUM — US$ 3.03bnAvg. FTE – 62No. of respondents — 7

Hong Kong, China and Singapore

Avg. AUM — US$ 2.54bn Avg. FTE – 45No. of respondents — 7

0%

10%

20%

30%

40%

50%

HQ of respondents by geographical location

AustraliaAsiaEurope and

North Americas

RESPONDENTS’ PROFILE

Number of respondents: 20

Below shows the average AUM and average number of full time employees (FTEs) operating in the region, based on the location of respondents’ head quarters.

The overview of respondents’ profiles indicate there is a low correlation between assets under management (AUM) and headcount.

TAbLE OF CONTENTS

SECTIONS

1 ORgANISATIONAL INFORMATION 01

2 gOVERNANCE & RISk MANAgEMENT 07

3 ADMINISTRATION 13

4 VALUATION 17

5 TEChNOLOgY AND OPERATIONS 21

6 REgULATORY INFORMATION 24

7 REPORTINg 28

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

01

Section 1OrganiSatiOnal infOrmatiOn

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

02

FTE* number by role

by location of head office

key takeaways:

•Majorfocusremainswithinfrontoffice,i.e.assetmanagement,portfoliomanagementandacquisition.

•Brokendownbygeographicallocation,Europe,NorthAmericaheadquarteredmanagershaveagreater emphasis on front office, while Australian managers have a relatively bigger team in back/middle office and corporate/management functions comparing to their peers.

•Cross-checkingtodatainSection3,Australianmanagerstendtoperformmostoftheadministrationfunctionsin-house,explainingthehigherpercentageintheirmiddle/backofficeandcorporate/management functions.

4%3%

20% 20%

53%

ExecutiveCorporate/ManagementFront OfficeOthersBack/Middle Office

3%

16%

6%

14%

61%

Europe and North Americas

ExecutiveCorporate/ManagementFront OfficeOthersBack/Middle Office

7managers

7%

21%

5%

14%

53%

Asia

ExecutiveCorporate/ManagementFront OfficeOthersBack/Middle Office

8managers

4%

23%

0%

24%

49%

Australia

ExecutiveCorporate/ManagementFront OfficeOthersBack/Middle Office

5managers

* Full Time Employee

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

03

The median FTE number of our respondents is 60, we compared the split by functional area between the respondents with more or less FTEs than the median:

8%4%

61%

7%

20%

Under 60 FTEs

ExecutiveCorporate/ManagementBack/Middle OfficeFront OfficeOthers

9managers

Average AUM: USD 1.67 bnAverage FTE: 33

ExecutiveCorporate/ManagementBack/Middle OfficeFront OfficeOthers

3% 3%

51%

22%

21%

Over 60 FTEs

11managers

Average AUM: USD 9.4 bnAverage FTE: 114

key takeaways:

•Keyimpactoflargerheadcountseemstobetakingfrontofficestaffintoanewtierofmiddlemanagement.

•Back/middleofficepercentageisquiteconsistentforbothlargerandsmallermanagers.

•Absolutenumberofexecutivesaresimilarforbothlargerandsmallermanagers,thusthereisamuchlowerpercentageinproportionforthelargermanagers.

•Smallermanagersusuallyhavelesspeoplededicatedforcorporate/managementfunctions,i.e.themajorityofthemonlyhavededicatedheadcountforlegaland investor relations.

by size

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

04

staff composition for each functional area:

Fund Accounting/AdministrationCompliance, Internal Auditand RegulatoryTaxEnvironmental, Social and GovernanceValuationPerformance Measurement and Attribution

4% 5%

1%1%

11%

78%

Back/Middle office

Human ResourcesInvestor Services/RelationsInformation TechnologyCorporate Finance FunctionLegalSales and Marketing

17%

16%

17%

16%

18%16%

Corporate/Management

Asset ManagersPortfolio ManagersResearchAcquisitionInvestment Management

41%

25%

11%

19%

4%

Front office

key takeaways:

•Veryfewfundmanagershavededicatedpersonnelforvaluation.Internalvaluationsareusuallycarriedoutbyfrontofficestaff.

•Fundaccounting/administrationpercentageremainsveryhigh.ThisisconsistentwiththefindingsinSection3,wherethemajorityofadministrationworkisstillperformedin-house.

•Thepercentageofenvironmental,socialandgovernance(‘ESG’)andtaxaresimilar.However,mostmanagershadasinglededicatedheadcountfortaxwhilstEsG was much more polarised for Australian managers who had one or more dedicated personnel for EsG. This is consistent with our prior year’s Review ofInvestorReportingTrendsAsia-Pacific2016survey,whichfoundthatAustralianmanagersputmorefocusonESGimplementationandreportingduetoregulatory requirement and investors’ expectations.

•Researchpercentageappearsverylow.Similartovaluation,researchworkmaybecarriedoutbyinvestmentmanagementoracquisitionteams.

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

05

headcount information

other options of “increase by over 20%” and “decrease” both had nil responses.

No Change

Executives

Corporate / management

Back / middle office

Front office

Expected headcount movement within the next year:

Increase 0-20%

0 2 4 6 8 10 12 14 16 18

Employer drivenLosing staff to market

50%50%

Turnover is largely due to:key takeaways:

No fund managers expect a decrease in headcount and the majorityexpectanincreaseinheadcount in front office, showing that industry players still retain a positiveoutlookforAsia-Pacificbusiness in 2018.

key takeaways:

•Thereappearstobeastrongappetitefor hiring accounting staff – two thirds of respondents are actively hiring in this area.

• Itisrelativelychallengingtohiretherightvaluation specialist.

Compliance

Accounting

Risk Management

Valuation specialist

Information technology

How challenging is it for the respondent's organisation to find the rightresources in the following areas?

Very challenging Somewhat challenging Not challenging Not hiring

0 3 6 9 12 15 18

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

06

Consideration on fund domicile

Investor marketing

Cost of doing business

Regulatory

Costs Benefits

What are the key costs / benefits influencing the choice to use a fund “offshore” domicile compared to “onshore”, i.e. where the fund is subject to regulation?

0% 20% 40% 60% 80% 100%

BEPSAbility to market to investorsMIT (or similar non-Australian regimes)

21%

54%

25%

What would make you consider different domicile for a new product/re-domiciliation of current products?, or to use multi-jurisdiction structure?

key takeaways:

Clearly onshore funds are very much driven by the ability to market the product. The additional costs of an onshore product are unsurprisingly indicated as the key downside.

key takeaways:

Marketing again is shown as the clear priority forthoseconsideringre-domiciliation.

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

07

Section 2gOvernance & riSk management

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

08

Relative frequency of committee meetings

key takeaways:

•Unlikeothercommitteemeetingsconductedonafixedcycle,investmentcommitteeswillbecalledasand when investment opportunities arise.

•Seniormanagement/executivecommitteemeetingsareconductedmorefrequentlythanothers.

•Managersarealsofocusedonvaluationandcompliance/riskmanagement,thesemeetingsareusuallyconducted quarterly.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Investment committee

Shareholder/Investor committee

Compliance/Risk management committee

Senior management/Executive committee

Valuation committee

Audit committee

Corporate governance committee

Remuneration committee

Appointment committee

For the following committees in place, how frequently do they meet?

Monthly Quarterly Semi Annually Annually Ad-hoc No committee

55%

50%

75%

60%

35%25%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

09

board of Directors (boD) composition

key takeaways:

Higherinvestorandindependentdirectorparticipationontheboardsofcorefundswhichisunsurprisinggiventhatmorecorefundsbeingsubjecttoregulatoryrequirements.Anyopen-endedfund,whicharenormallyCoreproducts,wewouldexpecttohaveveryrobustgovernanceduetoinvestorstransactingatthe subscription/redemption NAVs. Core fund investors would seem to expect lower portfolio risk, coupled with a higher level of corporate governance and transparency.

All investorsLarger investors or rotation of investorsNo investorsMajority of executive directorsMinority of executive directors

11%

52%

5%

21%

11%

Core funds

All investorsLarger investors or rotation of investorsNo investorsMajority of executive directorsMinority of executive directors

25%

63%

6%

0%

6%

Non-core funds

YesNo

71%

29%

Independent directors on the core funds’ BoD

YesNo

55%

45%

Independent directors on the core funds’ BoD

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

10

Investment committee

Less than 30 minutesBetween 30 minutes and 1 hourBetween 1 hour and 2 hoursMore than 2 hours

17%

33%

50%

The length of time spent discussing each investment opportunity

Less than 2 weeksBetween 2 weeks and 1 monthBetween 1 month and 2 monthsMore than 2 months

25%

32%

32%

11%

For majority of cases, how much time passes after a positive decision is made on an investment to closing the investment?

By local committeeOne global committeeBoth, it depends on thenature of the deal(e.g. location, size, complexity)

Where is investment decision made?

33% 33%

33%

UnanimousSimple majoritySuper-majority

13%

47%

40%

How is investment decision made?

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

11

Risk management priorities

Top 5 risk priorities

1 Market

2 liquidity

3 Regulatory

4 operational

5 Tax

key takeaways:

•Marketriskisthetoppriorityforallregions.

•Theoverallriskprioritiesarequiteconsistentin all regions; overall top 5 remain the top 5 in both Asia and Europe/North America.

•Surprisingly,taxriskisnotviewedasanykind of priority in Australia. Ranked ninth compared to third in Europe and North America. A possible reason is that Australian managers mainly invest in Australia only, they are familiar with the local tax rules and exposures and therefore it is no longer a key risk.

Model risk

Cyber Security

Fraud

Regulatory

Operational

Credit / counterparty

Tax

Liquidity

Market

European and North American HQ managers' priority

Tax

Fraud

Model risk

Credit / counterparty

Cyber Security

Regulatory

Liquidity

Operational

Market

Australian HQ managers' priority

Model risk

Cyber Security

Fraud

Credit / counterparty

Tax

Operational

Liquidity

Regulatory

Market

Asian HQ managers' priority

0 3 6 9 12 15

0 3 6 9 12 15

0 5 10 15 20

18 21 24 27

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

12

Foreign currency and interest rate risks

key takeaways:

•93%oftherespondentshedgetheirinterestraterisk,comparedto84%hedgingforeigncurrencyrisk.

•Basedontheinterviewresultofourprioryears’ReviewofInvestorReportingTrendsAsia-Pacificsurvey,someparticipantscommentedthatthehedgingcostofcertain Asian currencies is very high. This is a possible reason for no foreign currency hedging being implemented.

International financial institutions

Local financial institutions

Boutique firms/specialists (eg. Chatham Financial)

No hedging is implemented

No risk exposure

What kind of organisations do you work with to hedge your foreign currency/interest rate exposure?

Interest rate risk Foreign currency risk

0% 10% 20% 30% 40% 50% 60%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

13

Section 3adminiStratiOn

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

14

Administration Scope of the primary administrator’s services

key takeaways:

•Thereappearstobenomarketleaderin either the fund or sPV administration business. The respondents are using 14 differentadministratorsforfundsand9administrators for sPV administration.

•24%oftherespondentsusemultipleadministrators. Managers may use different administrators for different funds and also may split administration between fund level and sPVs.

Other observations:

•Forthosewhocurrentlydonotoutsource,allhave indicated that there are no plans or they are unlikely to outsource in the coming year.

•Asfortranslationofinternal/externalreports,40% of participants used independent translationagencieswhilstothersreliedonin-house capabilities.

•Dependingonanyregulatoryrequirements,the depth of outsourcing needs, and geographic coverage needs, different administrators maybe more or less suitable for any particular scenario.

key takeaways:

Accounting-relatedwork(i.e.accounting,financialstatementspreparation,taxfilings)aremorelikelytobeoutsourced.In-housestafffocusmoreonanalyticalandgovernancerelatedworksuchasBoard/GPreporting, treasury and internal audit.

None usedOneTwoThreeFour or more

17%

59%

21%

21%

How many administrators does the fund manager presently use?

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Fund Accounting

SPV Accounting

Property Accounting

Fund Performance

Cash Management/Treasury

Bank Reconciliations (Cash, investments)

Tax Filing/Returns Preparation

Financial Statement Preparation/Consolidation

Management/GP Reporting

Assistance with Board Reporting

Internal audit

Fund/Property Accounting and administration

Full third party Partial third party In-house

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

15

Scope of the primary administrator’s services

key takeaways:

Themajorityofinvestorservicesfunctionsareperformedin-houseasfundmanagersprefertokeep interaction and relationships with investors at close quarters.

key takeaways:

VeryhighoutsourcingrateinFATCA/AIFMDtype of compliance work, which is unsurprising, due to the high complexity and changing requirements, naturally external supports are needed.

0% 20% 40% 60% 80% 100%

Subscriptions/Redemptions

Capital Calls/Distributions

Promote Waterfall/IRR calculation

Investor Reporting

Investor Risk Reporting

Assistance with Investor Reporting Guidelines(ANREV, ARES, specific reporting, etc)

Other Investor Services

Investor services

Full third party Partial third party In-house

U.S. SEC Form PF

AIFMD Depositary

AIFMD – AIF Reporting

FATCA and CRS reporting

AML/KYC

Local country specific periodic filings

Regulatory

Full third party Partial third party In-house

Manager’s regulatory reporting (i.e. the fundmanager’s corporate reporting obligations)

0% 20% 40% 60% 80% 100%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

16

Administrator service assessment and fees

50% 50%

Are key performance indicators (KPIs) usedto evaluate the administrator’s performance?

YesNo

11%

25%

3%

11%

11%7%

11%

If the answer to the above question is yes, indicate which KPIs are used:

Aged open itemsNumber of audit adjustmentsTimeliness of annual and interim financial reportsPrior period correctionsPercent of NAV produced on timeNumber of NAV errorsOthersN/A as answered no above

21%

5%6%

24%

6%

12%

How does the administrator currently price its services?

Fixed chargeBasis-point model using net assets/partners’ capitalBased on number of entitiesBased on number of transactions/investmentsBased on number of investorsOthersBasis-point model using committed capital

47%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

17

Section 4valuatiOn

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

18

Property valuation firms

key takeaways:

•Mostmanagersusemultiplevaluersvaryingbylocations/typeofproperties.Somemanagersengagedifferentvaluersbyrotation.

•Mostrespondentsusereputablevaluers.Thereisnoclearmarketleader.

Number of valuers used

13%

33%

41%12-34-5>6

13%89%

74%

63%

63%

63%

58%

32%

21%

CBRE

Savills

DTZ Cushman & Wakefield

Jones Lang Lasalle

Knight Frank

Colliers

Other (please specify)

Big 4 financial services firms

Valuers used

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

19

The frequency of third party appraisal

Other observation:

•82%ofrespondentsindicatedthatallinvestmentsaresubjecttoexternalvaluations.The remaining respondents may determine the use of external valuation by nature or size of investments.

key takeaways:

•100%ofassetsaresubjecttoexternalvaluation, of which 12% do not have fixed frequencies.

•Mostmanagersconductinternalvaluationsat least quarterly to meet investor reporting requirements, updates typically being distributed quarterly.

•Managersthatrequirequarterlyexternalvaluations usually pursue a core strategy.

47%

41%

12%

17%

66%

17%

External valuations Internal valuations

As needed Quarterly Annually

External and internal valuation frequency

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

20

Management override of external valuations

key takeaways:

•Themajorityofmanagersarenotpermittedtooverrideexternalvaluations.Evenforthosebeinggrantedtheauthoritytooverrideexternalvaluations,notsurprisinglytheyseldomadjustexternalvaluationasitmayattractalotofqueriesfrominvestorsandexternalauditors.

•FrompreviousPwCANREVsurveys,managersstatedthattheywouldonlyoverridevaluationswhichtheybelievedweretooaggressive,theywouldnotoverride external values to increase the market value.

56% 44%

Can management override external valuations if management disagrees?

YesNo

57% 43%

If yes, what would management use for financial reporting?

Internal valuation modelUse external valuation as base, but make specific amendments to model

33%

67%

If yes, how often does management make adjustments to external valuer’sfigures if they disagree?

SeldomNever

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

21

Section 5technOlOgy and OperatiOnS

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

22

Outsourced technology functions

•Othersincludeemailsecurityenhancement. •Othersincludeperformanceenhancement.

Data Management – externally managed data (Data Center/ Cloud)

Data Management – internally managed data

Disaster Recovery

IT/Cyber Security

Technical support

Risk Management

Other (please specify)

Which of the following functions are outsourced by the investment manager?

Full Partial Parallel In-house

0% 20% 40% 60% 80% 100%

16%

10%

16%

16%

23%

6%

If it is likely for the respondent's organisation to make technology investments in the next 12 months, what are the likely areas where spending goes to?

Enhancing big data capabilitiesRisk managementGeneral ledger/fund or SPV accountingPortfolio managementHuman resources systemOthersNot applicable

13%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

23

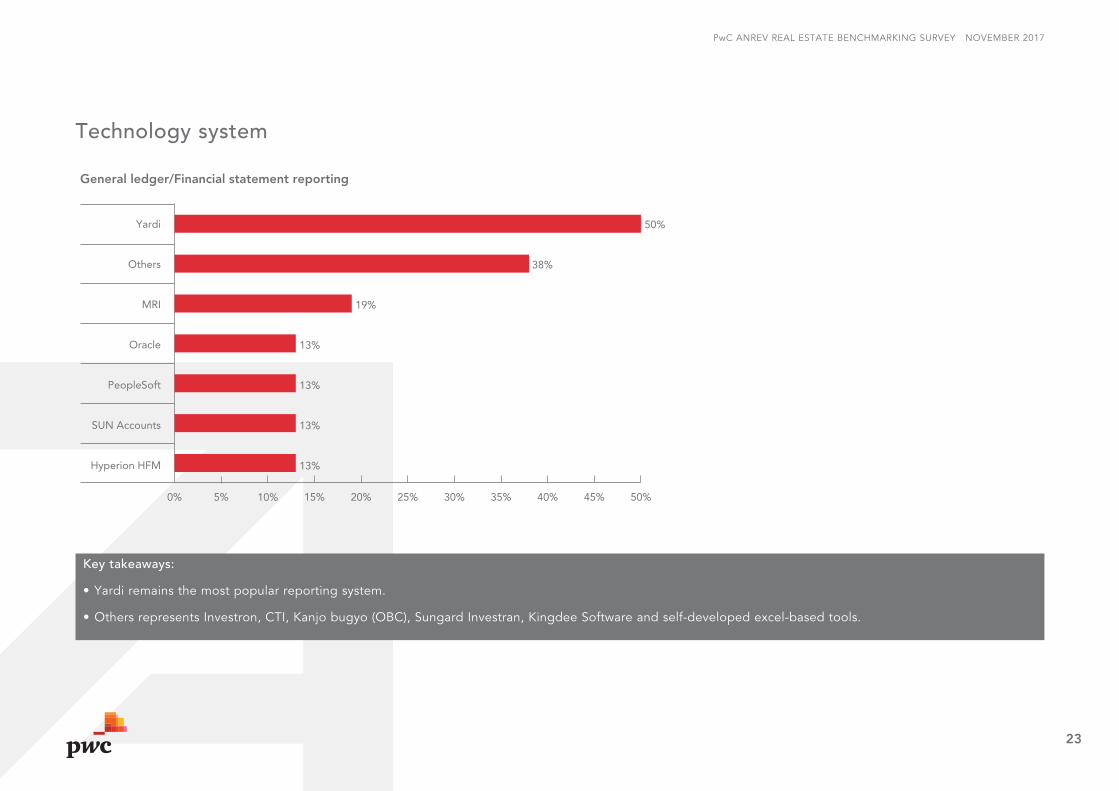

Technology system

key takeaways:

•Yardiremainsthemostpopularreportingsystem.

•OthersrepresentsInvestron,CTI,Kanjobugyo(OBC),SungardInvestran,KingdeeSoftwareandself-developedexcel-basedtools.

50%

38%

19%

13%

13%

13%

13%

Yardi

Others

MRI

Oracle

PeopleSoft

SUN Accounts

Hyperion HFM

General ledger/Financial statement reporting

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

24

Section 6regulatOry infOrmatiOn

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

25

Regulatory information

key takeaways:

•Majorityofthefundmanagersarenowregulated.Movetoonshorefundsor access to preferential tax treatment may drive regulation in addition to regulators expending their remit.

•Atleast38%oftherespondentshavebeenreviewedbyatleastoneregulatory body in last 12 months!

11%

61%28%

Regulatory supervision – fund manager

Regulated – Asian fund managerRegulated – non-Asian fund managersNot regulated

13%

25%

0%

0%

19%

43%

Within last 6 months

7-12 months ago

13-24 months ago

25-60 months ago

More than 60 months ago

Have not been reviewed

When was the last time the fund manager was reviewed by the relevant securities commission or other regulatory (non-tax) bodies?

0% 10% 20% 30% 40% 50%

37%

37%

16%

10%

Chief Financial Officer

Chief Compliance Officer

General Counsel

Others

Who is primarily responsible for overseeing the regulatory reporting process

0% 10% 20% 30% 40%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

26

Tax audit

key takeaways:

•Majorityofthemanagershavenotbeenauditedbyataxauthoritywithinthelast5years.

•ConsistentwithSection2riskpriorities,sincelessmanagerswerereviewedbytaxauthoritiesinlast2years,theyviewregulatoryriskasahigherpriorityovertax risk.

6%

94%

7%

93%

7-12 months ago

How recently has the fund manager been audited by a government/local or foreign tax authority?

Government/local jurisdiction audit

Foreign jurisdiction audit

N/A or not within 5 years

0%

20%

40%

60%

80%

100%

67%

22%17% 17%

11%

None Payroll Sales Tax CorporateTax

Transferpricing

What types of tax audits are currently in progress?

0%

20%

40%

60%

80%

100%

19%

81%

Has the fund manager engaged an outside firmto perform a mock tax (or other jurisdiction) audit?

YesNo

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

27

Regulatory risks

key takeaways:

•Thereisahighappreciationofmacroglobal risks, recognising the responsibility of marketing to global investors and the increasing regulations impacting business.

•HighleveloffocusonBEPSwouldsuggestmany organisations updating their tax planning which may have been designed in a “different age”.

0% 20% 40% 60% 80% 100%

47%

47%

40%

33%

27%

33%

20%

13%

33%

40%

20%

27%

40%

27%

27%

6%

7%

7%

6%

Anti-Money Laundering(“AML”)

Base erosion and profit shifting (“BEPS”)

Foreign Corrupt Practices Act(“FCPA”)

Foreign Account Tax Compliance Act(“FATCA“)

Common reporting standard(“CRS“)

How important are the below risks to your organisation?

Very important Important Somewhat important Not important

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

28

Section 7repOrting

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

29

Investor reporting

key takeaways:

•Historicperformanceandfutureoutlookrelated information remain the most interested areas of investors.

•Halfofthemanagersreceiverequestsinrelation to environmental information, which is consistent with our prior year’s Review of InvestorReportingTrendsAsia-Pacific2016survey results, which reported that many western investors pay close attention to EsG reporting. investor reporting usually lacks detailed EsG information, so investors request additional EsG information from managers.

25%

75%

For reporting and/or disclosures toLimited Partners, what is the level of information provided?

Specific LP level only informationFund level information

75%

69%

56%

50%

50%

50%

31%

31%

6%

Historic performance related

Future outlook

Use of reporting templates (ie. SDDS vs. bespoke templates)

Asset quality

Environmental

Compliance or fraud related

Regulatory

Internal control assessment of the fund manager

Others

For reporting and/or disclosures to Limited Partners, what type of additional reportingor further information do LPs typically request?

0% 20% 40% 60% 80% 100%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

30

Investor reporting

key takeaways:

•Theresultisconsistentwiththefrequencyofconductinginternalvaluations.

•FrompreviousPwCANREVsurveys,managersstatedthatifprincipallyUSinvestorstheymayfollowUSmarketpracticeratherthanINREVindustryguidelines.AsthestandardizationprojectwiththeUStradeassociationcompletes,weexpectcompliancewouldbemuchstronger.

5%

11%

16%

68%

Frequency of financial statement reporting releasedto investors

QuarterlySemi-annuallyAnnuallyMonthly

47%

29%

12%

ANREV / INREV

Guidelines per offering documents

If ANREV / INREV is applicable, dothe entities comply with SDDS?

In terms of investor reporting, what trade association guidelines do the entities comply with?

0% 10% 20% 30% 40% 50%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

31

Investor reporting

Other observation:

Core fund investors usually expect earlier reporting of preliminary NAV. Based on the interview result of our prior years’ Review of investor Reporting Trends Asia-Pacificsurvey,someparticipantscommentedthattheyneedtoreportpreliminaryNAVbeforetheyearenddate.

44%

28% 28%

0%

22%

28%

44%

6%

Less than2 weeks

Over 2 weeksto 1 month

Over 1 month3 months

More than 3 months

Average number of business daysto issue NAV? (Core fund)

Core fund − Preliminary NAV

Core fund − Final NAV

0%

10%

20%

30%

40%

50%

29%

42%

0%

14%

29% 29%

50%

7%

Average number of business days toissue NAV? (Non-Core Fund)

Non-Core fund − Preliminary NAV

Non-Core fund − Final NAV

0%

10%

20%

30%

40%

50%

Less than2 weeks

Over 2 weeksto 1 month

Over 1 month3 months

More than 3 months

6%

11%

17%

39%

21%

Who is responsible for Fund performance measurement?

Controller/Internal finance teamOthersInvestment teamExternal fund administratorInvestor relations teamHead office (for MNCs not based in Asia)

6%

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

32

This benchmarking survey was primarily carried out between June and october 2017 and comprised the following steps:

SURVEY APPROACh AND METhODOLOgY

Survey approach•TheprofessionalstandardscommitteeofANREV

together with PwC have determined a set of 57 questionstocoveroperationsinthenon-listedreal estate industry. The questions are based on PwC/ANREV real estate industry experience and by looking at similar surveys covering asset management organisations, then tailoring for real estate funds where applicable.

•67realestatefundmanagerswereinvitedbyANREV to participate in the survey. survey was conducted between July and August 2017 on a secure online platform (“Qualtrics”).

Report methodology•20realestatefundmanagersparticipatedin

the survey. PwC extracted and analysed the responses, looking for results which could provide insights for readers.

•Whereapplicable,furthercomparisonsweremade to similar surveys in order to search formeaningfulanalysisortrends.Datawasstratified where results differed by categories of organization (e.g. headcount, AUM, location of head office).

•ThesteeringcommitteefromANREVwereinvited to review the overall results and assess which were meaningful to include within the report.

PwC ANREV REAl EsTATE BENChMARkiNG sURVEy NoVEMBER 2017

33

PwC’s Real Estate practice assists real estate investment advisers, investment trusts, public and private investors, corporations, and management funds in developing strategies, evaluating acquisitions and dispositions; and appraising and valuing real estate. its global network of dedicated real estate professionals enables it to assemble for its clients the most qualified and appropriate team of specialists in the areas of capital markets, systems analysis and implementation, research, accounting, and tax.

PwC has offices in 157 countries and more than 208,000 people globally, and is among the leading professional services networks in the world.

SPONSORINg ORgANISATIONS

Global and Regional Real Estate Contacts:

Craig hughesGlobal Real Estate leaderlondon, United [email protected]

Paul WaltersAsia-PacificRealEstateAssuranceleaderhong kong, [email protected]

k.k. SoAsia-PacificRealEstateLeaderhong kong, [email protected]

PwC hong kongPaul Waltersstanley TamAlisonIp,JonathanKimandDaisyIp

ANREV is the Asian Association for investors in Non-listedRealEstateVehiclesLimited.ANREVisanot-for-profitorganisationdrivenbyinstitutionalinvestorsinAsiannon-listedpropertyfunds.our aim is to serve as a platform for investors who guide the association’s strategy. ANREV’s agenda is driven by its members, in particular institutional investors, and is focused on improving transparency and accessibility through market information, professionalism and best practice. Fund managers, investment banks and advisors provide support in addressing key issues facing theAsiannon-listedrealestatefundmarkets.ANREV now has 200 member companies from 18 countries.

ANREV Contributors:

AmélieDelaunay,Director,ResearchandProfessionalstandards, ANREV

ANREV Survey Sub-Committee:Justin Armstrong, Randy Caenen, Charmaine Cheuk, Eric lechat and Andrew Read

AsiAN AssoCiATioN FoR iNVEsToRs INNON-LISTEDREALESTATEVEHICLES

602,6/FDinaHouse,RuttonjeeCentre,11DuddellStreet,Central,hong kong

T +852 3108 2723E [email protected]