Embed Size (px)

Citation preview

November 5, 2014

Ramkrishna Forgings Ltd.

… ready to reap benefits

SKP Securities Ltd www.skpmoneywise.com Page 1 of 15

CMP ` 275 Target: ` 372 Initiating Coverage – BUY

Source: BSE India

Company Profile Ramkrishna Forgings Ltd (RKFL), promoted by Mr Mahabir Prasad Jalan, a technopreneur, is a medium sized forging company, having expertise in ring rolling, machined forging and heavy press forging. The Company has presence in M&HCV segments of automotive sector, which contributed about 73% to the total revenue in FY14. RKFL’s current forging capacity of 70,000 MT pa. is utilized in the production of machine forged engine, steering components, gearbox components and axle components such as screw couplings, draw gear assembly, spur gears, synchro rings, wheel hubs, clamps etc. Key Highlights In time capital expenditure – ready to reap benefits:

RKFL is in the midst of capacity expansion at Jamshedpur, with the total capex of ` 6.75 bn by installing four heavy press lines to manufacture front axle beam, stub axle, connecting rod, crankshaft etc.

In the last couple of years, the domestic M&HCV segments witnessed one of its roughest patches in two decades. The global scene was not encouraging either. In such a scenario, it was bold move for RKFL to have set up a new facility, primarily targeted for global markets, to augment its capacity, topline and bottomline with higher margins. Domestic demand has already turned around. The bold decision is likely to pay off soon.

RKFL has been able to secure debt limits of ` 4.6 bn at very attractive rates which is expected to give them a competitive advantage.

The new facility at Jharkhand is developed keeping in view the international export market. RKFL has recently signed a USD 100 mn contract with a global original equipment manufacturer (OEM) for a period of five years.

We expect half of the new capacity to be utilized by FY16 and export contribution of the company is expected to rise to 61% by FY17E from the current 21%.

Topline to grow with a CAGR of 49% during the next three years:

RKFL’s topline has seen sluggish pace CAGR growth of 2.2% between FY11‐14 due to slowdown in the domestic automobile industry, athough exports grew at good pace. Ring rolling and machined forging segment, contributed about 40%, and 51% respectively, during FY14.

Consolidated net topline posted by the company for FY14 was ` 4.4 bn, which we expect to touch ` 14.5 bn by the end of FY17E with a CAGR of 49%, led by revival in domestic automobile industry and higher exports from the new capacity.

Margins to improve with increasing contribution from exports:

EBIDTA margins of the company have remained under pressure between FY12‐14 due to slowdown in domestic auto segment. EBIDTA margin for RKFL was at peak in FY11 at 17% which slid down to 13.6% in FY14. We expect RKFL will be able to expand its EBIDTA margins over 18% by FY17E due to focus on exports which fetch better margins than domestic.

PAT Margins have also declined from 5.4% in FY11 to 1.9% in FY14. We expect that the PAT margin of RKFL to remain in the vicinity of about 6.4% and 5.3% during FY15E & FY16E respectively, as the Company is in expansion mode. With the improvement in economy and decline in interest cost due to repayment of term loan FY16E onwards, we expect PAT margin to touch 7% in FY17E.

Outlook & Recommendation With the new capacity getting operational leading to higher margins from exports and revival in domestic automotive industry, RKFL is set to reap the fruits, the seeds of which were sown two years back. We have valued the stock on the basis of EV/EBIDTA ‐ of 6.5x of FY17E EBIDTA – method of relative valuation. Although the stock has recently witnessed a sharp rise to a 52 week high, we recommend a BUY on the stock with a target price of ` 372/‐ (35% upside) in 18 months.

Key Share DataFace Value (`) 10.0Equity Capital (` mn) 261.0M.Cap (` mn) 7177.352‐wk High/Low (`) 275/65Avg. Daily Vol 9865BSE Code 532527NSE Code RKFORGEReuters Code RKFO.BOBloomberg Code RMKF:IN

Shareholding Pattern (as on Sept 30, 2014)

48%

2%

30%

20%Promoters

FII

DII

Public & Others

Particulars FY14 FY15E FY16E FY17ENet Sales 4372.1 6579.0 11649.9 14499.4Sales Gr. 8.0% 50.5% 77.1% 24.5%EBIDTA 592.8 1072.4 2038.7 2653.4Adj. PAT 84.6 418.2 613.0 1014.5PAT Gr. ‐3.7% 394.5% 46.6% 65.5%EPS (`) 3.2 14.6 21.4 35.4CEPS (`) 12.8 26.5 49.1 60.6

Financials (` mn)

Particulars FY14 FY15E FY16E FY17EInt Cover (x) 1.5 2.2 2.6 4.6P/E (x) 84.9 18.9 12.9 7.8P/BV (x) 2.2 2.0 1.8 1.4P/Cash EPS (x) 21.4 10.4 5.6 4.5M.Cap/Sales (x) 1.6 1.2 0.7 0.5EV/EBIDTA (x) 19.9 14.2 7.6 5.5ROCE (%) 4.3% 6.4% 10.2% 15.8%ROE (%) 2.6% 10.7% 13.7% 18.6%EBIDTM (%) 13.6% 16.3% 17.5% 18.3%NPM (%) 1.9% 6.4% 5.3% 7.0%Debt‐Equity (x) 1.5 1.9 1.7 1.2

Key Ratios

Price Performance RKFL vs BSESMALLCAP

‐50%

0%

50%

100%

150%

200%

250%

300%

Oct‐1

3

Nov

‐13

Dec

‐13

Jan‐

14

Feb‐

14

Mar‐1

4

Apr‐1

4

May‐1

4

Jun‐

14

Jul‐1

4

Aug

‐14

Sep‐

14

Oct‐1

4

RKFL

BSE SMALLCAP

Analysts: Nikhil Saboo Tel No: +91 33 4007 7019; Mobile: +91 93301 86643 e‐mail: [email protected] Vineet P. Agrawal Tel No: +91 22 4922 6006; Mobile: +91 98195 10575 e‐mail: [email protected]

Ramkrishna Forgings Ltd.

SKP Securities Ltd. www.skpmoneywise.com Page 2 of 15

• Forging is a manufacturing process involving shaping of metal using localized compressive forces. Product range includes rough forgings or machine parts like crankshaft, camshaft, connecting rods, shifting fork, steering components, gear box components, crown propeller shafts, front axle beams, rear axle shafts, and railway tires, etc.

• Capacity & Utilization: The forging industry is one of the important industries for the success for automobile, power, and general engineering sectors in India. India’s forging industry, which majorly supplies to auto companies, has a current installed capacity of 3.75 MT per annum with a capacity utilization of about 2.8 MT. Based on installed production capacity and annual sales turnover of these forging units, they can be classified into five categories as shown in the table.

• Structure: The organized sector accounts for 65‐70% of the total forging production in India and rest are unorganized players, who are mainly small and tiny units. These unorganized players mainly cater to job work and replacement markets or tier 3 or tier 4 component manufacturers.

• Highly dependent on automotive sector: The sector is worth ` 250 bn and is highly dependent on automotive sector which contributes to about 70% of the total business. The impact of changes in the Indian automobile industry is directly proportional to the Indian forging industry.

• The (forging) Sector is under stress since 2012 due to slowdown in automotive sector and increasing input costs. The industry players are caught between their suppliers, who are increasing input costs and OEMs who want to keep tight control on costs citing slowdown.

• Slowdown in the automotive industry: With the onset of the slowing industrial growth and weakening investment sentiment across sectors the strong growth phase of the domestic CV segment came to standing halt since the second half of 2011‐12. Production trend of CVs at a glance:

Source: Company & SKP Research

• The overall domestic sales of CV segment also registered de‐growth of 20% from 632,738

vehicles in 2012‐13 to 793,211 vehicles in 2013‐14. Thus, M&HCV segment sales also registered a sharp downfall of 16% during FY14.

• Further Contraction in M&HCV segment in April‐July 2014: Data for this financial year show decline in sales in both the LCV and M&HCV for the entire April‐July period. sales volume for Passenger carriers and goods careers declined by 23% and 4% respectively during the period.

Category 2007‐08 2008‐09 2009‐10 2010‐11 2011‐12 2012‐13 2013‐14

Commercial Vehicles ‐ M&HCV 549006 416870 566608 760735 929136 832649 698864

% Growth ‐‐ ‐24% 36% 34% 22% ‐10% ‐16%

The Industry at a Glance

Scale of Operation Installed Capacity (MT) Units in No.

Very Large Above 75,000 8

Large 30,000‐75,000 15

Medium 12,500‐30,000 32

Small 5,000‐12,500 99

Very Small Upto 5,000 265

Source: Company Annual Report 2014

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 3 of 15

• Economic turnaround underway: For the quarter ended June this year, India’s economy grew at a nine‐quarter high of 5.7%, compared with 4.6% in the previous quarter, driven largely by industry, even as the biggest segment of the services sector — trade, hotels, transport and communications — remained subdued.

• Uptick in August and September 2014 numbers of M&HCV segment: With the signs of revival in the economy, an uptick has been seen in the demand of M&HCV sales in August, though number for busses remained subdued.

• This uptick could be seen as a sign of bottoming out of the downtrend in M&HCV segment. M&HCV data for September was also quite encouraging. The numbers at a glance:

Source: SKP Research

• Normally, the medium commercial vehicles (MCV) segment shows the first sign of growth, while we are now witnessing sales growth in the HCV segment. Logically, this should be followed by smaller‐tonnage vehicles, perhaps with a lag of six‐nine months.

• Entire CV segment to go green by FY16: A proper recovery in the M&HCV space is expected in the last quarter of this financial year, followed by growth in the LCV segment in the first quarter of FY16. Improvements in infrastructure spending and manufacturing activity towards the end of the financial year will translate into an improvement in the commercial vehicle segment. The M&HCV segment will see recovery first, followed by the LCV segment. It is expected the entire segment to witness positive growth post FY15.

• Forging Industry Outlook: We believe that gradual traction in automotive segment, gaining market share from railways with superior highways infrastructure, changing landscape of the logistics industry towards an organized one and stricter implementation of emissions and anti‐overloading norms would continue to support demand for CVs in India.

• Furthermore, growth in the industry would be driven by the improvement in macro conditions on the domestic front, moderation in interest rates, and revival in consumer confidence.

• Revival in the auto industry – specially in CV segment – will be quite positive for RKFL as the CV sales volume and RKFL’s sales volume are closely related to each other, as clearly shown in the adjacent graph.

Sep‐13 Sep‐14 % Change Sep‐13 Sep‐14 % Change

M&HCV 8817 10404 18% 4715 6621 40%

LCV 24393 18539 ‐24% 2517 2572 2%

CV 33210 28943 ‐13% 7232 9193 27%

Sales (No of units)Sales (Tata Motors) Sales (Ashok Leyland)

Source: SKP Research

Aug‐13 Aug‐14 % Change

Passenger Carriers 3613 2682 ‐26%

Goods Career 11855 14273 20%

M&HCV 15468 16955 10%

SalesM&HCV Sales (No. of Units)

‐24%

36% 34%

22%

‐10%

‐16%

11%

25%

32%

17%

‐27%

‐4%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

FY09 FY10 FY11 FY12 FY13 FY14

CV Volume Growth RKFL's Volume Growth

Source: Company & SKP Research

RKFL’s Sales Volume Growth vs CV Volume Growth

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 4 of 15

• An Introduction: Ramkrishna Forgings Ltd (RKFL) commenced operations in November, 1981, promoted by Mr Mahabir Prasad Jalan, headquartered in Kolkata, West Bengal, as an small scale industrial unit, supplying forging items for railways, with the turnover of ` 5‐6 mn per annum.

• Today, the company has expanded its interest in M&HCV segment of automobiles with the turnover of over ` 4 bn. It manufactures forging products ranging from 50‐180 kgs.

• Mr Mahabir Prasad Jalan, Promoter and the Chairman of RKFL, is a B.E. (Hons) in

Mechanical Engineering from BITS, Pilani. He has got an experience of more than 30 years in forging industry.

• Infrastructure: RKFL has 5 state‐of‐the‐art manufacturing facilities in India, of which one is in Liluah, West Bengal and rest is in Jamshedpur, Jharkhand.

• Segments and product portfolio: The Company’s activities can be divided into three product categories namely ring rolling, machine forging and heavy press forging.

• The current capacity (FY14) of RKFL is 70,000 MTPA the break of which is as follows:

Source: Company & SKP Research

• RKFL, with existing facilities, manufactures machine forged engine, steering components , gearbox components and axle components such as screw couplings, draw gear assembly, spur gears, synchro rings, wheel hubs, clamps and so on.

• The Company is in the midst of capacity expansion at Jamshedpur, Jharkhand, which will enhance its capacity to 150,000 MTPA. The new capacity is expected to be fully commissioned by FY16.

• With this expansion, the company’s portfolio will be enhanced by more complex forging components such as crankshaft, camshaft, front axle beam, and connecting rods.

• Industries served: RKFL derives majority of its revenue from automotive sector (M&HCV segment). Apart from automobile industry, the Company also caters to industries like railways and mining. Its products are also exported to countries like USA, Mexico Turkey, Brazil, Europe, etc.

• Marquee Clientele: RKFL caters to domestic as well as international clients. Domestic OEM players served by the company are Tata Motors, Ashok Leyland, SAIL, BHEL, Indian railways and so on, whereas, Meritor, US, HEMA Endustri A.S., Turkey; Sisamax US; etc. are international tier I auto component suppliers served by the company.

FY14 Ring Rolling Forging Heavy Press Capacity 32000 38000 ‐‐Utilization 56% 62% ‐‐

The Company at a Glance

66%74% 70% 70% 65%

52%

10%9%

6% 5%8%

10%

5%4%

3% 6% 6%

6%

8%5%

11% 9% 12%23%

11% 8% 9% 10% 9% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY09 FY10 FY11 FY12 FY13 FY14

Others

Exports

Mining

Railways

Automobile

Industry wise Revenue Mix RKFL

Source: Company & SKP Research

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 5 of 15

Key Products at a Glance: Product Picture Application Industry

Crankshaft

The crankshaft is located in the engine of a vehicle and converts the force created by the engine's pistons moving up and down into a force that moves the wheels in a circular motion so the vehicle can go forward. It is connected to all the pistons in the engine and to the flywheel.

Automotive

Camshaft

A camshaft is a rotating cylindrical shaft used to regulate the injection of vaporized fuel in an internal combustion engine. A camshaft is directly coupled to the crankshaft, so that the valve openings are timed accordingly.

Automotive

Connecting Rod

In a reciprocating piston engine, the connecting rod connects the piston to the crankshaft. Together with the crankshaft, they form a simple mechanism that converts reciprocating motion into rotating motion.

Automotive

Front Axel Beam

Beam axle is a dependent suspension design which is the system of springs, shock absorbers and linkage that connects a vehicle to its wheels and allows relative motion between the two. It keeps vehicles occupants comfortable and reasonably isolated from bumps and vibrations.

Automotive

Rear Axle Shaft

A rear axle shaft is a component of the rear axle housing on a rear‐wheel drive vehicle. Manufactured of solid steel, the rear axle shaft provides the power to the tires to drive the vehicle.

Automotive

Steering Components

Steering is the collection of components, linkages, etc. which allows a vehicle to follow the desired course. A steering mechanism includes – 1) Steering Wheel 2) Steering Column 3)Rack and Pinion 4)Tie rod and 5) Kingpin

Automotive

Stub Axle

A stub axle is one of the two front axles that carry a wheel in a rear drive vehicle. The axle is capable of limited angular movement about the kingpin for steering the vehicle.

Automotive

Screw Coupling Used to connect rolling stock Railways

Draw Gear Assembly Draw gear is the assembly behind the coupling at each end of the rolling stock to take care of the compression and tension forces between wagons of train.

Railways

Source: Company & SKP Research

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 6 of 15

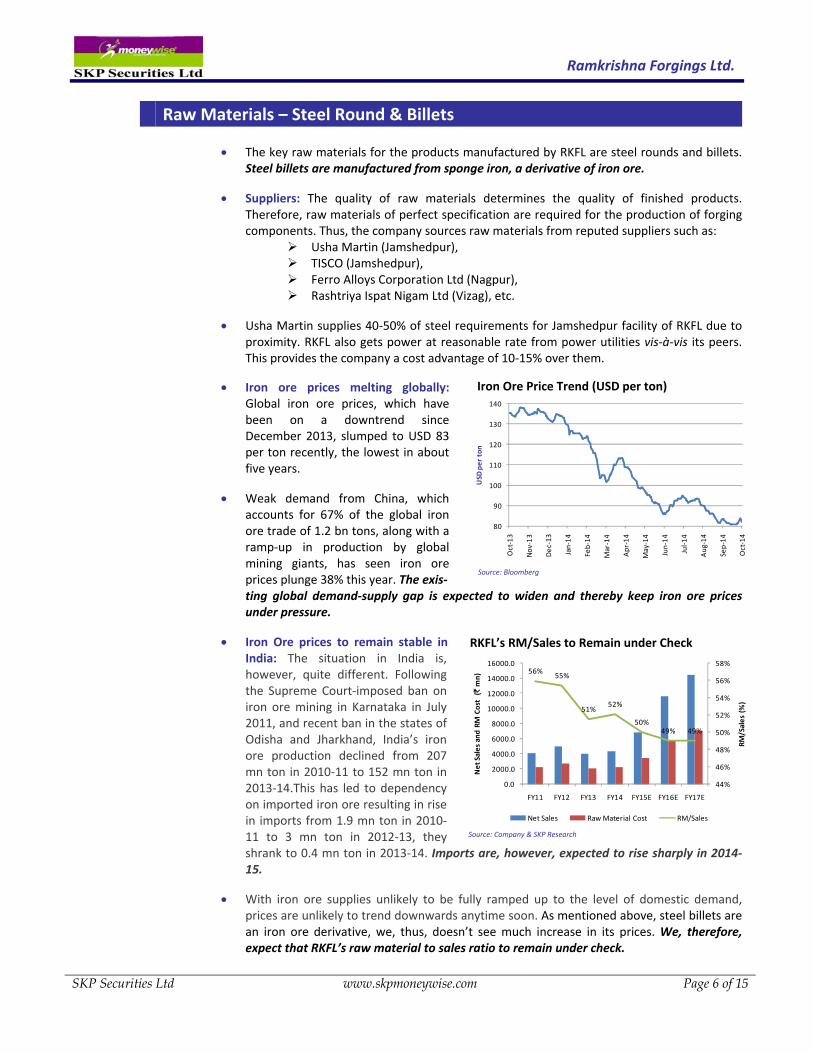

Raw Materials – Steel Round & Billets • The key raw materials for the products manufactured by RKFL are steel rounds and billets.

Steel billets are manufactured from sponge iron, a derivative of iron ore.

• Suppliers: The quality of raw materials determines the quality of finished products. Therefore, raw materials of perfect specification are required for the production of forging components. Thus, the company sources raw materials from reputed suppliers such as:

Usha Martin (Jamshedpur), TISCO (Jamshedpur), Ferro Alloys Corporation Ltd (Nagpur), Rashtriya Ispat Nigam Ltd (Vizag), etc.

• Usha Martin supplies 40‐50% of steel requirements for Jamshedpur facility of RKFL due to

proximity. RKFL also gets power at reasonable rate from power utilities vis‐à‐vis its peers. This provides the company a cost advantage of 10‐15% over them.

• Iron ore prices melting globally: Global iron ore prices, which have been on a downtrend since December 2013, slumped to USD 83 per ton recently, the lowest in about five years.

• Weak demand from China, which accounts for 67% of the global iron ore trade of 1.2 bn tons, along with a ramp‐up in production by global mining giants, has seen iron ore prices plunge 38% this year. The exis‐ ting global demand‐supply gap is expected to widen and thereby keep iron ore prices under pressure.

• Iron Ore prices to remain stable in India: The situation in India is, however, quite different. Following the Supreme Court‐imposed ban on iron ore mining in Karnataka in July 2011, and recent ban in the states of Odisha and Jharkhand, India’s iron ore production declined from 207 mn ton in 2010‐11 to 152 mn ton in 2013‐14.This has led to dependency on imported iron ore resulting in rise in imports from 1.9 mn ton in 2010‐11 to 3 mn ton in 2012‐13, they shrank to 0.4 mn ton in 2013‐14. Imports are, however, expected to rise sharply in 2014‐15.

• With iron ore supplies unlikely to be fully ramped up to the level of domestic demand, prices are unlikely to trend downwards anytime soon. As mentioned above, steel billets are an iron ore derivative, we, thus, doesn’t see much increase in its prices. We, therefore, expect that RKFL’s raw material to sales ratio to remain under check.

Iron Ore Price Trend (USD per ton)

Source: Bloomberg

80

90

100

110

120

130

140

Oct‐1

3

Nov

‐13

Dec

‐13

Jan‐

14

Feb‐

14

Mar‐1

4

Apr‐1

4

May‐1

4

Jun‐

14

Jul‐1

4

Aug

‐14

Sep‐

14

Oct‐1

4

USD

per

ton

56% 55%

51%52%

50%49% 49%

44%

46%

48%

50%

52%

54%

56%

58%

0.0

2000.0

4000.0

6000.0

8000.0

10000.0

12000.0

14000.0

16000.0

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

RM/S

ales

(%

)

Net

Sal

es a

nd R

M C

ost

(`m

n)

Net Sales Raw Material Cost RM/Sales

Source: Company & SKP Research

RKFL’s RM/Sales to Remain under Check

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 7 of 15

Global Forex and Travel Ltd

• Global Forex and Travel Ltd (GFTL), a wholly owned subsidiary of RKFL acquired in December 2012, is expected to generate revenue of ` 120‐140 mn during FY15E with the EBIDTA of ` 80‐100 mn.

• Global Forex and Travels Limited is engaged in the business of travel and travel related

services provided to the public at large both national and international. The company is a member of IATA and is entitled to sell the tickets and book flights on various airlines operating in and out of India. The Company is also entitled to use the present Galileo system of reservation of tickets and is entitled to sell such tickets to the public.

• As GFTL is not a material subsidiary of RKFL, it will not have material impact on the

valuations of the company. Conscious of the fact that its an unrelated diversification, we expect the company management to divest this business going forward. We have not included GFTL in our forecasted numbers.

Investment Rationale

1. In time capital expenditure – ready to reap the benefits:

• Expansion Plan: RKFL is in the midst of capacity expansion plan, at Jamshedpur, Jharkhand,

with the total capex of ` 6.75 bn, building four heavy press lines .

• This expansion will increase the existing capacity (70,000 MT) of RKFL to 150,000 MT. The plants are expected to be completed by March 2015. Out of the four press lines, two are already commissioned. The Company’s Expansion plan at a glance:

Source: Company and SKP Research

• RKFL has decided to invest in expensive technology and manufacture more value‐added

products two years ago, at a time when the Indian M&HCV industry entered its roughest patch in two decades. With the demand environment has given the indications of revival in M&HCV segment, in August and September 2014, the bold decision has begun to pay off.

• The new facility to manufacture majorly modern forging products such as front axle beam, stub axle, connecting rod and crankshaft, etc. These products fetch better margins than the products manufactured from the existing facilities.

• Financing: RKFL has been able to secure debt of ` 4.6 bn at attractive rates, which, in itself is a competitive advantage. Rest of the project is funded through equities. Financing by the company at a glance:

Heavy Press Capex (` mn) Date of Commissioning 3150 Tons July 20144500 Tons July 20146300 Tons March 201512500 Tons 1,750 March 2015Total 6,750

5,000

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 8 of 15

Source: Company and SKP Research

• Export Oriented Facility – Already tied up with one of the leading international OEM: The

new facility at Jharkhand under development will cater to international export markets.

• RKFL has recently signed a USD 100 mn contract with a global original equipment manufacturer (OEM) in Latin America for a period of five years. We expect half of the capacity of its new facility to be utilized by FY16E.

• With the new capacity expected to be in place by the end of FY15E, we expect the share of

exports to spike to about 61% to its total net revenues, from less than a fourth at present, within the next three years.

RKFL’s Domestic Sales vs. Exports

• The company is in advanced talks to clinch another big contract from two global OEM. Both

the OEMs have already completed the audit of RKFL plants.

• RKFL is ready to reap the benefits: RKFL will be ready to reap the gains of its bold decision, by FY16E, of capacity modernization cum augmentation with the tie‐ups for the capacity in place.

Debt Funding Currency Amount (currency mn)

Exim Bank INR 1000

IFC USD 14

DBS Bank USD 10

LBBW EURO 18.3SBI INR 700

Equity Funding Instrument Amount (` mn)

IFC (Jan 2013) Equity Shares 275

Wayzata II Indian Ocean (April 2013) Equity Shares 494

Promoter Group Share Warrants 680

Internal Accruals Internal Cash 601Total Equity Funding 2050

88%79%

63%

44% 39%

12%21%

37%

56% 61%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15E FY16E FY17E

Reve

nue

Cont

ribu

tion

(%

)

Domestic Exports

Source: The Company & SKP Research

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 9 of 15

2. Topline to grow with a CAGR of 49% during the next three years:

• Net Topline: RKFL’s topline has seen sluggish pace CAGR growth of 2.2% between FY11‐14 due to slowdown in automobile industry, during the period, in India, though exports grew by good pace. Ring rolling and forging segment contributed about 40%, and 51% respectively, during FY14.

• Net topline posted by the company for FY14 was ` 4.4 bn, which we expect to touch ` 14.5 bn by the end of FY17E with a CAGR of 49%, led by revival in domestic automobile industry and higher exports.

• Exports: As mentioned elsewhere in the report, RKFL is putting heavy press line capacity to meet global export demand. Keeping this in view the Company has already tied up with one of the major international OEM, in Latin America and the company is in advanced talks with two other international OEMs for capacity tie‐up. Such tie‐ups will help improving exports of the company. With these tie‐ups in place, we expect the capacity utilization from the new facility to reach 50% and 70% in FY16E and FY17E respectively. Exports (Gross) have grown with a CAGR of 25% between FY11‐15E and we further expect it to grow at a CAGR of 113%.

• Domestic Sales: Domestic Sales for the company has seen a CAGR de‐growth of 2% during FY11‐14 due to de‐growth in the years FY13 and FY14 by 23% and 2% respectively on the back of slowdown in automotive industry.

• With the indication of revival of M&HCV segment sales in August and September 2014, we expect that the domestic sales for RKFL to grow with a CAGR of 18% during FY14‐17E, though we feel that the domestic growth in FY17 will be at moderate pace as we expect the ring rolling capacity of the company to reach at optimum utilization level.

Source: The Company & SKP Research

Source: The Company & SKP Research

Source: The Company & SKP Research

4096

.9

5012

.6

4049

.7

4372

.1

6579

.0 1164

9.9

1449

9.4

0

2000

4000

6000

8000

10000

12000

14000

16000

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Ove

rall

Net

Rev

enue

s (`

mn)

Overall Revenue

463.8 428.6 501.0907.6

2406.1

6498.9

8795.3

0.0

1000.0

2000.0

3000.0

4000.0

5000.0

6000.0

7000.0

8000.0

9000.0

10000.0

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Expo

rt (`

mn)

3633

.1

4584

.1

3548

.8

3464

.5

4172

.8

5151

.0

5704

.1

34%

26%

‐23%

‐2%

20%23%

11%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

0

1000

2000

3000

4000

5000

6000

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

% G

row

th

Dom

esti

c Sa

les

(`m

n)

Domestic Sales Growth %

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 10 of 15

3. Margins to improve with increasing contribution from exports: • EBIDTA margins of the company have remained under pressure between FY12‐14 due to

slowdown in domestic auto segment. EBIDTA margin for RKFL was at peak in FY11 at 17% which slid down to 13.6% in FY14. During the period, industry players were caught between its suppliers, who are increasing cost and OEM, who want to keep tight control on costs citing slow down. Though, the EBIDTA Margin moved northwards to 15.6% in H1FY15.

• We expect RKFL will be able to expand its EBIDTA margins beyond 18% by FY17E due to‐ Focus on exports which fetch better margins than domestic margins.

As mentioned earlier contribution from exports are expected to increase to 61% of the total gross revenue from the present 21%.

Revival in domestic automotive sector. The Indian automotive sector was at decline since second half of FY12. M&HCV segment has shown signs of revival in August and September 2014. We expect that industry will be out of red by FY16, thus fetching better margins.

• PAT Margins also declined from 5.4% in FY11 to 1.9% in FY14 which has improved to 7.8% in H1FY15, which includes exceptional items worth ` 110.8 mn.

• We expect that the PAT margin of RKFL to remain in the vicinity of about 2% during FY15E as the Company is in expansion mode. The assets worth ` 6.75 bn will be capitalized in its balance sheet during the year, thus, resulting in to higher depreciation. Depreciation will also remain high on existing fixed assets due to revised depreciation rate on fixed assets w.e.f. April 1, 2014, as per the useful life specified in Schedule II of the Companies Act, 2013. Furthermore, we expect term loan to increase during the year due to the above mentioned capex which will further pressurize PAT.

• With the improvement in economy and decline in interest cost, due to repayment of term loan FY16E onwards, we expect PAT margin to touch 7% in FY17E.

• Margins of the company at a glance:

EBIDTA & EBIDTM PAT & PATM

ROE & ROCE D/E & Interest Coverage Source: Company & SKP Research

With the improvement in margins ROE and ROCE to improve to about 19% and 16% respectively in FY17E from the current 3% and 4%. With the repayment of term loans D/E and interest coverage to improve to 1.2x and 4.6x respectively by FY17E from the current 1.5x each.

Export orders enjoys better margins than the domestic orders, thus, result in higher EBIDTM and PATM

693.

2

809.

4

552.

0

592.

8

1072

.4

2038

.7 2653

.4

17%16%

14% 14%

16%18%

18%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

500

1000

1500

2000

2500

3000

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

PAT

Mar

gin

(%)

EBID

TA (`

mn)

220.6 242.9

87.8 84.6

418.2

613.0

1014.5

5.4%4.8%

2.2% 1.9%

6.4%

5.3%7.0%

0%

1%

2%

3%

4%

5%

6%

7%

8%

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

PAT

Mar

gin

(%)

PAT

(`m

n)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

ROE (%) ROCE (%)

1.10.8 0.9

1.5

1.91.7

1.2

2.9 2.9

1.6 1.5

2.22.6

4.6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

D/E (x) Interest Coverage (x)

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 11 of 15

4. Strong Clientele: • RKFL is the preferred supplier for OEM’s like Tata Motors, Ashoka Leyland, Eicher etc

and is also a global supplier for CV majors like Meritor, US; HEMA Endustri A.S., Turkey; Sisamex, Mexico; AxleTech International, US; and so on. About 30‐40% of the production in existing facility at Jamshedpur goes to Tata Motors.

• RKFL has tied up with some the biggest vendors (tier–I) in Latin America and post

commencement of new plant it is expected to significantly increase its exports in Latin America and USA. Exports contributed 21% in FY14.

• BHEL, SAIL and Indian Railways are their clients in general engineering, steel and

railways segment respectively. BEML is another marquee client of RKFL under earth moving segment.

• Some key Clients of RKFL:

Domestic Clients

International Clients

Source: Company & SKP Research

Key Concerns

1. Volatile Dollar Rupee Rate: With the full commissioning of Heavy press line facility at Jamshedpur, the exposure of exports to the total revenues of RKFL is going to increase. Any unfavorable USD –Indian rupee movement may put negative impact on the results of the company.

2. Price volatility of steel: Steel billets and steel rounds are the key raw material for the company, which is highly price volatile. Any adverse movement in the prices may put negative impact on the margins of the company.

3. Prolonged slowdown in domestic automotive sector: Though the domestic automotive market has given the sign of bottoming out, but, if the slowdown prolonged, may again put negative impact on the margins of the company.

4. Rise in power Cost: Currently, RKFL is getting electricity at cheaper rate than its peers. In light of cancellation coal blocks by Supreme Court, any rise in the power cost, may put negative impact on the margins of the company.

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 12 of 15

Source: Company

Note for Exceptional Items during H1FY15

Particulars Rs mn

Keyman Insurance Surrender ‐ Q2FY15 29.20

Profit on sale of office Premises ‐ Q2FY15 45.43

Profit on sale of Shares ‐ Q1FY15 36.14

Total Exceptional Items 110.77 Source: Company

Particulars Q2 FY15 Q2 FY14 % Change Q1FY14 % Change H1FY15 H1FY14 % ChangeNet Sales 1626.2 969.2 67.8% 1231.9 32.0% 2858.0 2053.7 39.2%Raw Material Consumed 813.8 483.0 68.5% 628.4 29.5% 1442.2 1098.7 31.3%% to Sales 50.0% 49.8% ‐‐ 51.0% ‐‐ 50.5% 53.5% ‐‐Employee Expenses 102.2 74.9 36.5% 89.08 14.7% 191.3 146.0 31.0%Fuel Cost 136.6 103.0 32.6% 134.0 2.0% 270.5 219.4 23.3%Other Expenses 305.5 182.0 67.9% 201.8 51.4% 507.2 343.9 47.5%TOTAL EXPENDITURE 1358.0 842.8 61.1% 1053.2 28.9% 2411.3 1808.0 33.4%EBIDTA 268.1 126.4 112.2% 178.6 50.1% 446.8 245.7 81.9%EBIDTA Margin 16.5% 13.0% ‐‐ 14.5% ‐‐ 15.6% 12.0% ‐‐Depreciation 75.2 60.1 25.0% 68.0 10.6% 143.2 118.3 21.1%EBIT 192.9 66.2 191.4% 110.7 74.3% 303.6 127.4 138.3%EBIT Margin 11.9% 6.8% ‐‐ 9.0% ‐‐ 10.6% 6.2% ‐‐Interest 71.5 49.0 46.0% 64.2 11.3% 135.7 90.0 50.8%Other Income 7.7 5.8 31.0% 39.1 ‐80.4% 10.6 8.8 20.4%Exceptional Items ‐74.6 0.0 ‐‐ 0.0 ‐‐ ‐110.8 0.0 ‐‐Forex Difference 0.0 0.0 ‐‐ 0.0 ‐‐ 0.0 0.0 ‐‐Tax 38.6 8.4 361.8% 26.5 45.4% 65.1 16.3 63.2%Extraordinary Items 0.0 0.0 ‐‐ 0.0 ‐‐ 0.0 0.0 ‐‐Prior period taxes written bk. 0.0 0.0 ‐‐ 0.0 ‐‐ 0.0 0.0 ‐‐Minority Interest 0.0 0.0 ‐‐ 0.0 ‐‐ 0.0 0.0 ‐‐Share of Associate Company 0.0 0.0 ‐‐ 0.0 ‐‐ 0.0 0.0 ‐‐Reported Profit After Tax 165.1 14.7 1021.8% 59.0 179.8% 224.2 29.9 648.7%PAT Margin 10.2% 1.5% ‐‐ 4.8% 112.0% 7.8% 1.5% ‐‐Diluted EPS (`) 6.0 0.6 920.3% 2.3 166.4% 8.4 1.2 597.5%

Q2FY15 & H1FY15 Standalone Results at a Glance (` mn)

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 13 of 15

Valuation

With the new capacity getting operational leading to higher margins from exports and revival in domestic automotive industry, RKFL is set to reap the fruits, the seeds of which were sown two years back.

We have valued the stock on the basis of EV/EBIDTA ‐ of 6.5x of FY17E EBIDTA – method of relative valuation. We recommend BUY rating on the stock with a target price of ` 372/‐ (35% upside) in 18 months.

EV/EBIDTA FY17E EBIDTA (` mn) 2653.4 Est EV/EBIDTA (x) 6.5

EV (` mn) 17247.0 Debt (` mn) 6750.0 Cash (` mn) 159.0

Shareholders' Value (` mn) 10656.0 O/s Shares (mn Shares in FY17E) 28.7

Fair Value (` per share) 371.7

CMP (`) 275.0

Return (%) 35.2% Source: SKP Research

One Year Forward Looking P/E Band One Year Forward Looking EV/EBIDTA Band

Source: SKP Research

Peers Comparison

Source: Bloomberg Consensus and SKP Research

0

100

200

300

400

500

600

700

800

900

Apr‐1

0

Jul‐1

0

Oct‐1

0

Jan‐

11

Apr‐1

1

Jul‐1

1

Oct‐1

1

Jan‐

12

Apr‐1

2

Jul‐1

2

Oct‐1

2

Jan‐

13

Apr‐1

3

Jul‐1

3

Oct‐1

3

Jan‐

14

Apr‐1

4

Jul‐1

4

Oct‐1

4

Close Price 10 20 30 40 50 60

0

2000

4000

6000

8000

10000

12000

14000

Apr‐1

0

Jul‐1

0

Oct‐1

0

Jan‐

11

Apr‐1

1

Jul‐1

1

Oct‐1

1

Jan‐

12

Apr‐1

2

Jul‐1

2

Oct‐1

2

Jan‐

13

Apr‐1

3

Jul‐1

3

Oct‐1

3

Jan‐

14

Apr‐1

4

Jul‐1

4

Oct‐1

4

3 6 9 12 15 EV

FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17E FY14 FY15E FY16E FY17EBharat Forge Ltd 35.5 29.9 22.4 17.9 3.1 2.8 2.4 2.0 19.5 15.2 12.4 10.5 29.7 20.7 16.2 13.5 7.0 6.0 4.9 4.0Amtek Auto Ltd 6.4 3.9 3.1 ‐‐ 1.7 0.7 0.7 ‐‐ 6.7 3.6 3.1 ‐‐ 9.4 5.2 4.5 ‐‐ 0.6 0.5 0.4 ‐‐RKFL 84.9 18.9 12.9 7.8 2.7 2.3 1.3 1.0 19.9 14.2 7.6 5.5 34.6 20.8 12.4 7.5 2.2 2.0 1.8 1.4

PlayersEV/EBIT (x)P/E (x) EV/Sales (x) EV/EBIDTA (x) P/B (x)

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 14 of 15

Income Statement FY14 FY15E FY16E FY17E Balance Sheet FY14 FY15E FY16E FY17E

Net Operating Income 4372.1 6579.0 11649.9 14499.4 Equity Capital 261.0 286.7 286.7 286.7

Operating Expenditure 3779.3 5506.6 9611.2 11846.0 Share Warrants 65.4 0.0 0.0 0.0

EBIDTA 592.8 1072.4 2038.7 2653.4 Reserves 2890.8 3621.2 4200.6 5181.6

Depreciation 250.7 342.8 794.9 723.3 Net Worth 3217.2 3907.9 4487.3 5468.3

EBIT 342.1 729.6 1243.9 1930.0 Loan Funds 4793.8 7502.2 7700.0 6750.0

Other Income 16.1 29.6 23.3 29.0 Deferred Tax Liab. 291.9 291.9 291.9 291.9

Interest 228.8 333.8 481.3 421.9 Total Liabilities 8303.0 11701.9 12479.2 12510.2

Exceptional Items 0.0 ‐110.7 0.0 0.0 Net Block 2424.7 8831.9 8037.1 7313.7

EBT after Exceptional Items 129.4 536.1 785.9 1537.2 Capital WIP 3470.4 0.0 0.0 0.0

Tax 44.8 117.9 172.9 522.6 Investment 1.1 1.1 1.1 1.1

Minority Interest 0.0 0.0 0.0 0.0 Net Current Assets 2406.8 2868.9 4441.1 5195.4

PAT 84.6 418.2 613.0 1014.5 Total Assets 8303.0 11701.9 12479.2 12510.2

EPS (`) 3.2 14.6 21.4 35.4

Cash Flow Statement FY14 FY15E FY16E FY17E Ratios FY14 FY15E FY16E FY17E

PBT 129.4 536.1 785.9 1537.2 Valuation ratios (x)

P/E 84.9 18.9 12.9 7.8

P/Cash EPS 21.4 10.4 5.6 4.5

Net change in WC, Tax, Int ‐371.0 ‐522.9 ‐1786.0 ‐1286.9 P/BV 2.2 2.0 1.8 1.4

EV/EBIDTA 19.9 14.2 7.6 5.5

EV/Sales 2.7 2.3 1.3 1.0

Capital Expenditure ‐2907.9 ‐3279.6 0.0 0.0 Earning Ratios (%)

EBIDTAM 13.6% 16.3% 17.5% 18.3%

OPM 7.8% 11.1% 10.7% 13.3%

NPM 1.9% 6.4% 5.3% 7.0%

ROE 2.6% 10.7% 13.7% 18.6%

ROCE 4.3% 6.4% 10.2% 15.8%

B/S Ratios

Current ratio (x) 2.2 1.9 1.8 1.8

D/E (x) 1.5 1.9 1.7 1.2

Opening Cash Balance 38.3 152.7 209.9 168.9 Debtor Days 93.1 90.5 82.8 87.2

Creditor Days 72.1 79.3 79.7 86.3

Inventory Days 139.5 124.1 120.3 125.8

Closing Cash Balance 152.7 209.9 168.9 159.0 FA/Turnover (x) 1.8 0.7 1.4 2.0

Cash flow from Financing Activities 2789.2 2647.0 ‐317.0 ‐1405.4

Investments, Sales of FA, Dividend received and others 35.5 0.0 0.0 0.0

Cash balance of acquired subsidiaries 0.0 0.0 0.0 0.0

Add: Depreciation, Interest & Other Exppenditure 439.1 676.6 1276.1 1145.2

Net Increase/Decrease in Cash & Cash equivalents 114.4 57.2 ‐40.9 ‐10.0

Cash Flow from Operating Activities 197.5 689.8 276.0 1395.4

Cash flow investing Activities ‐2872.4 ‐3279.6 0.0 0.0

Financials (` mn)

Source: Company & SKP Research

Ramkrishna Forgings Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 15 of 15

Notes:

The above analysis and data are based on last available prices and not official closing rates. SKP Research is also available on Bloomberg, Thomson First Call & Investext Myiris, Moneycontrol, Tickerplant and ISI Securities.

DISCLAIMER: This document has been issued by SKP Securities Ltd (SKP), a stock broker registered with and regulated by Securities & Exchange Board of India, for the information of its clients/potential clients and business associates/affiliates only and is for private circulation only, disseminated and available electronically and in printed form. Additional information on recommended securities may be made available on request. This document is supplied to you solely for your information and no matter contained herein may be reproduced, reprinted, sold, copied in whole or in part, redistributed or passed on, directly or indirectly, to any other person for any purpose, in India or into any other country without prior written consent of SKP. The distribution of this document in other jurisdictions may be strictly restricted and/ or prohibited by law, and persons into whose possession this document comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition. If you are dissatisfied with the contents of this complimentary document or with the terms of this Disclaimer, your sole and exclusive remedy is to stop using the document and SKP shall not be responsible and/ or liable in any manner. Neither this document nor the information or any opinion expressed therein should be construed as an investment advice or offer to anybody to acquire, subscribe, purchase, sell, dispose of, retain any securities or derivatives related to such securities or an offer to sell or the solicitation of an offer to purchase or subscribe for any investment or as an official endorsement of any investment. Any recommendation or view or opinion expressed on investments in this document is not intended to constitute investment advice and should not be intended or treated as a substitute for necessary review or validation or any professional advice. The views expressed in this document are those of the analyst which are subject to change and do not represent to be an authority on the subject. SKP may or may not subscribe to any and/ or all the views expressed herein. It is the endeavor of SKP to ensure that the analyst(s) use current, reliable, comprehensive information and obtain such information from sources, which the analyst(s) believes to be reliable. However, such information may not have been independently verified by SKP or the analyst(s). The information, opinions and views contained within this document are based upon publicly available information, considered reliable at the time of publication, which are subject to change from time to time without any prior notice. The Document may be updated anytime without any prior notice to anybody. SKP makes no guarantee, representation or warranty, express or implied; and accepts no responsibility or liability as to the accuracy or completeness or correctness of the information in this Report. SKP, its Directors, affiliates and employees do not accept any liability whatsoever, direct or indirect, that may arise from the use of the information or recommendations herein. Please note that past performance is not necessarily a guide to evaluate future performance. SKP or its affiliates, may, from time to time render advisory and other services to companies being referred to in this document and receive compensation for the same. SKP and/or its affiliates, directors and employees may trade for their own account or may also perform or seek to perform investment banking or underwriting services for or relating to those companies and may also be represented in the supervisory board or on any other committee of those companies or may sell or buy any securities or make any investment, which may be contrary to or inconsistent with this document. This document should be read and relied upon at the sole discretion and risk of the reader. The value of any investment made at your discretion based on this document or income there from may be affected by changes in economic, financial and/ or political factors and may go down as well as up and you may not get back the full or the expected amount invested. Some securities and/ or investments involve substantial risk and are not suitable for all investors. Neither SKP nor its affiliates or their directors, employees, agents or representatives/associates, shall be responsible or liable in any manner, directly or indirectly, for information, views or opinions expressed in this document or the contents or any errors or discrepancies herein or for any decisions or actions taken in reliance on the document or inability to use or access our service or this document or for any loss or damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits or any loss or damage that may arise from or in connection with the use of or reliance on this document or inability to use or access our service or this document.

SKP Securities LtdContacts Research Sales Mumbai Kolkata Mumbai KolkataPhone 022 4922 6006 033 4007 7000 022 4922 6000 033 4007 7400Fax 022 4922 6066 033 4007 7007 022 4922 6066 033 4007 7007E‐mail

[email protected] [email protected] [email protected]

Member: NSE BSE NSDL CDSL NCDEX* MCX* MCX‐SX FPSB *Group Entities INB/INF: 230707532, BSE INB: 010707538, CDSL IN‐DP‐CDSL‐132‐2000, DPID: 021800, NSDL IN‐DP‐NSDL: 222‐2001, DP ID: IN302646, ARN: 0006, NCDEX: 00715, MCX: 31705, MCX‐SX: INE 260707532

Equities Derivatives Commodities Currency Demat Services Mutual Funds Insurance Financial Planning Online Trading

Page 15of 15