Embed Size (px)

Citation preview

23rd Annual Investment Conference amp Luncheon

William Larkin Jr Portfolio Manager

Cabot Money Management Inc

216 Essex Street Salem Massachusetts 01970

800-888-6468 eCabotcom

Trouble with the Bubble

Bond Bubble

Part I

Analyzing Our Current Situation

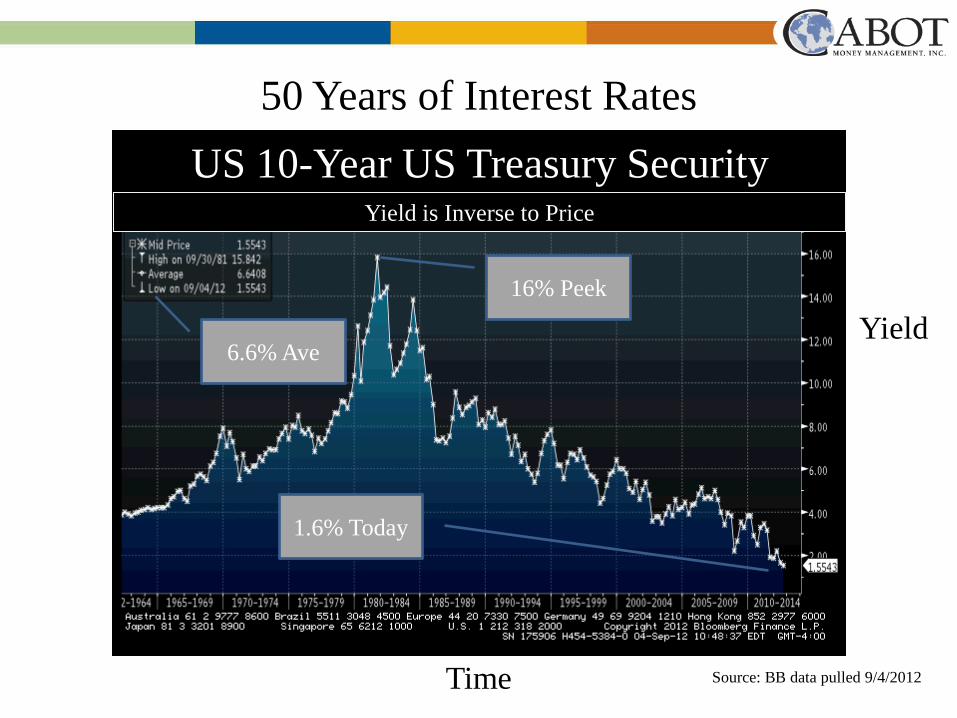

US 10-Year US Treasury Security

Yield

Time

Yield is Inverse to Price

16 Peek

16 Today

Source BB data pulled 942012

50 Years of Interest Rates

66 Ave

Our Interconnected Financial Systems

Debt Bubble

Housing

3

Market Uncertainty Feeds Fear

House Bubble Burst Crisis-Averting Maneuvers Banking Crisis

US Debt Purchases

1 2

4

5

Cheapening the Value of Money

3

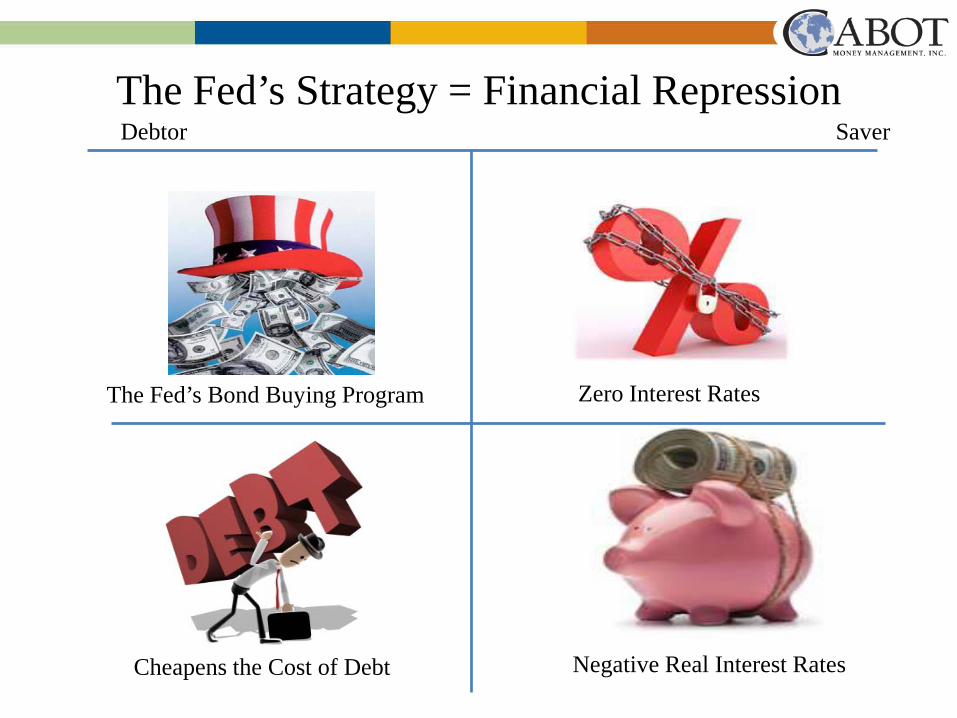

The Fedrsquos Strategy = Financial Repression

The Fedrsquos Bond Buying Program

Cheapens the Cost of Debt Negative Real Interest Rates

Zero Interest Rates

Debtor Saver

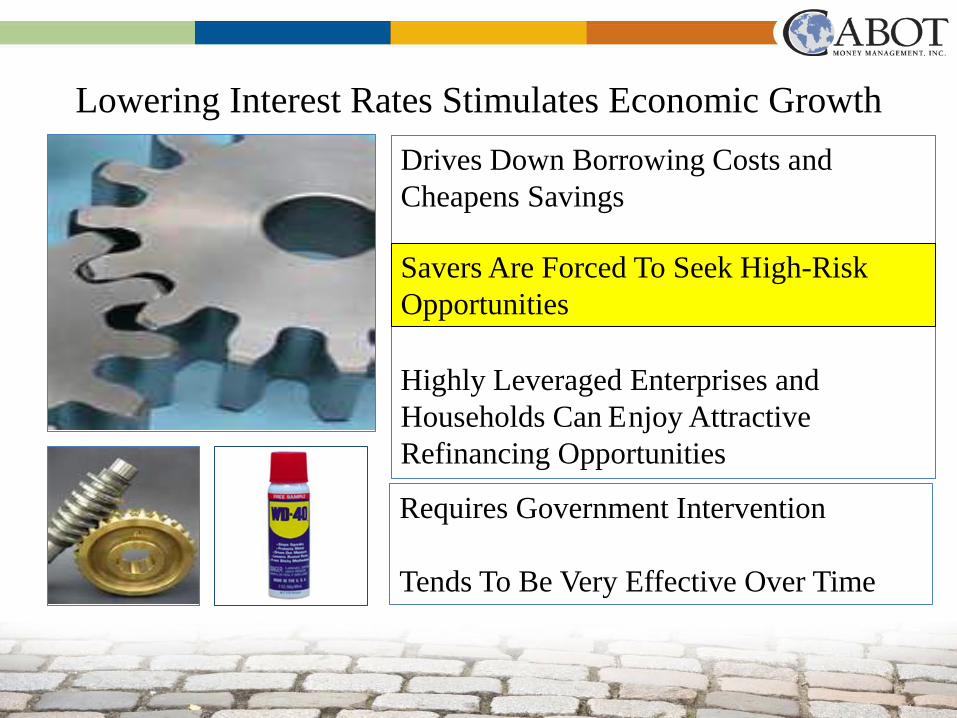

Lowering Interest Rates Stimulates Economic Growth Drives Down Borrowing Costs and Cheapens Savings Highly Leveraged Enterprises and Households Can Enjoy Attractive Refinancing Opportunities

Requires Government Intervention Tends To Be Very Effective Over Time

Savers Are Forced To Seek High-Risk Opportunities

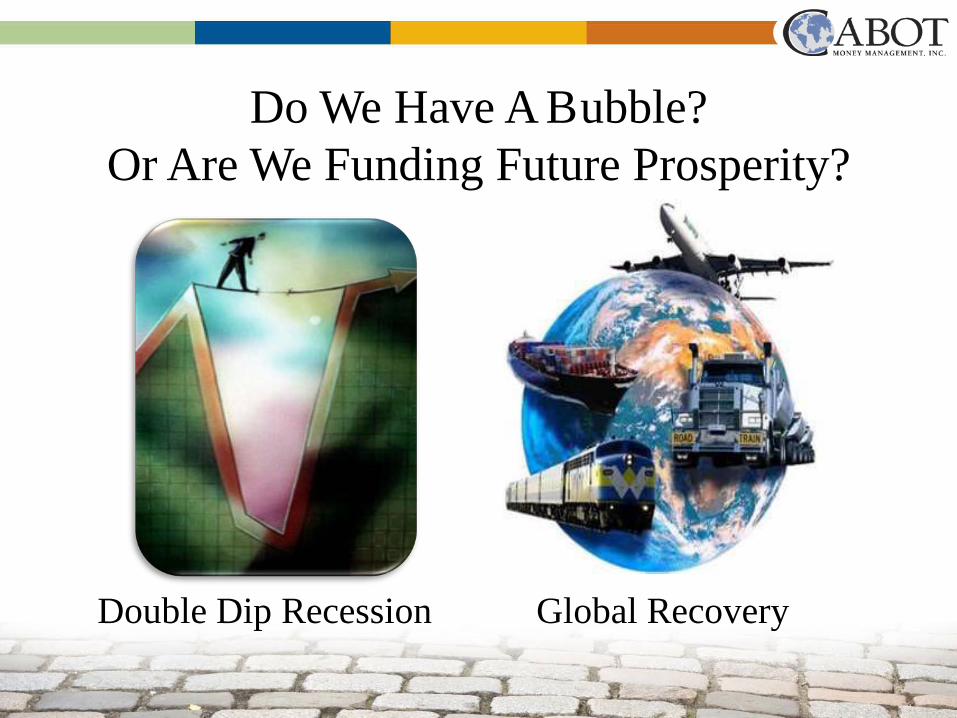

Do We Have A Bubble Or Are We Funding Future Prosperity

Double Dip Recession Global Recovery

Part II ndash Explaining the Low Rate Environment

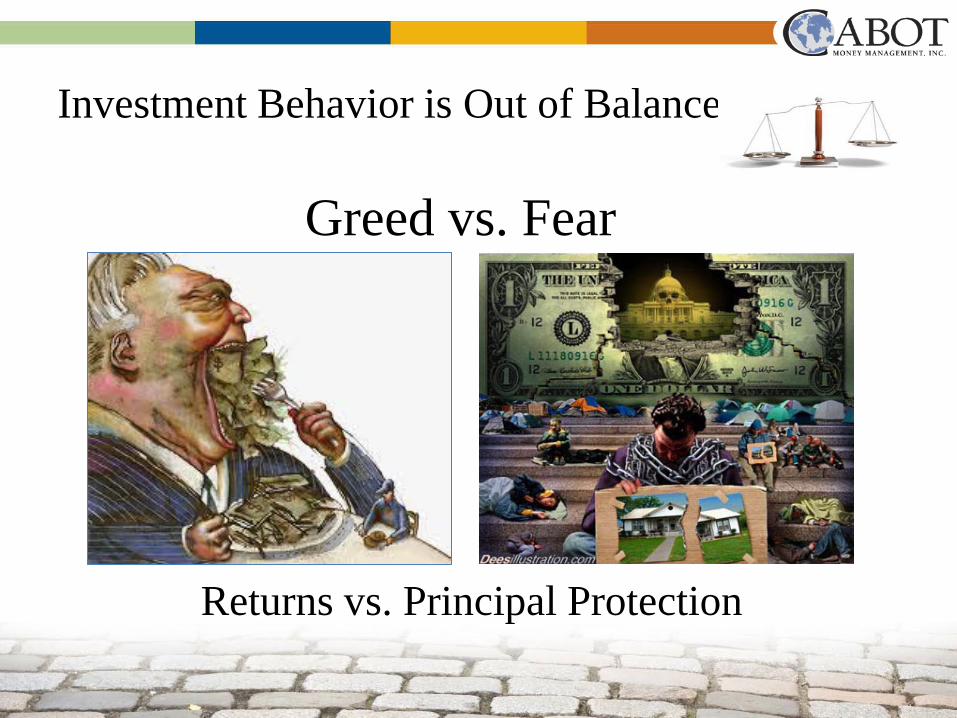

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

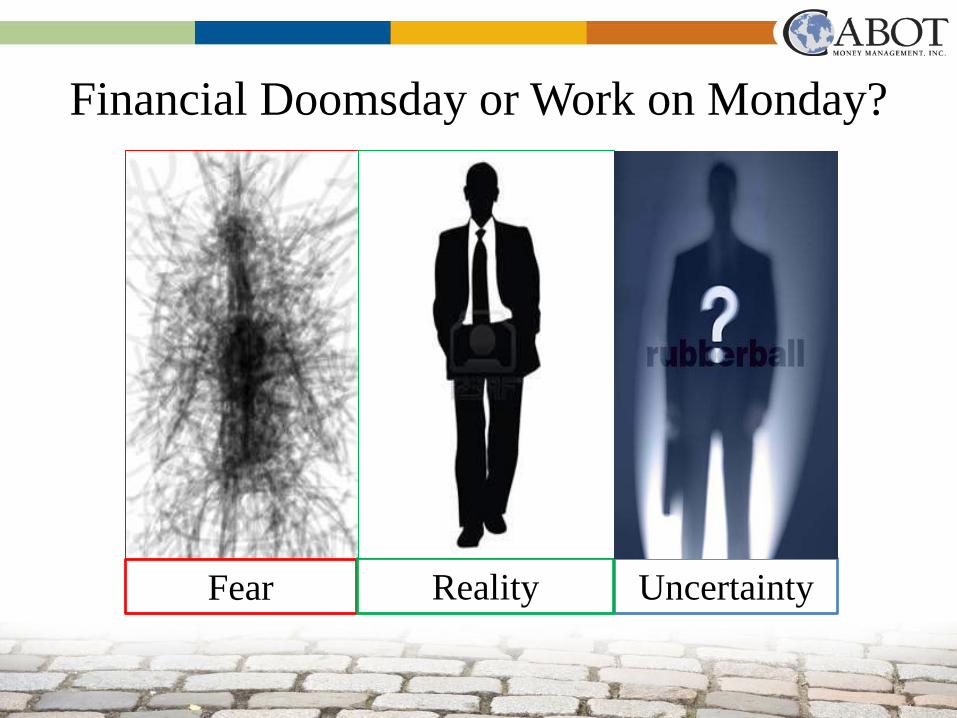

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

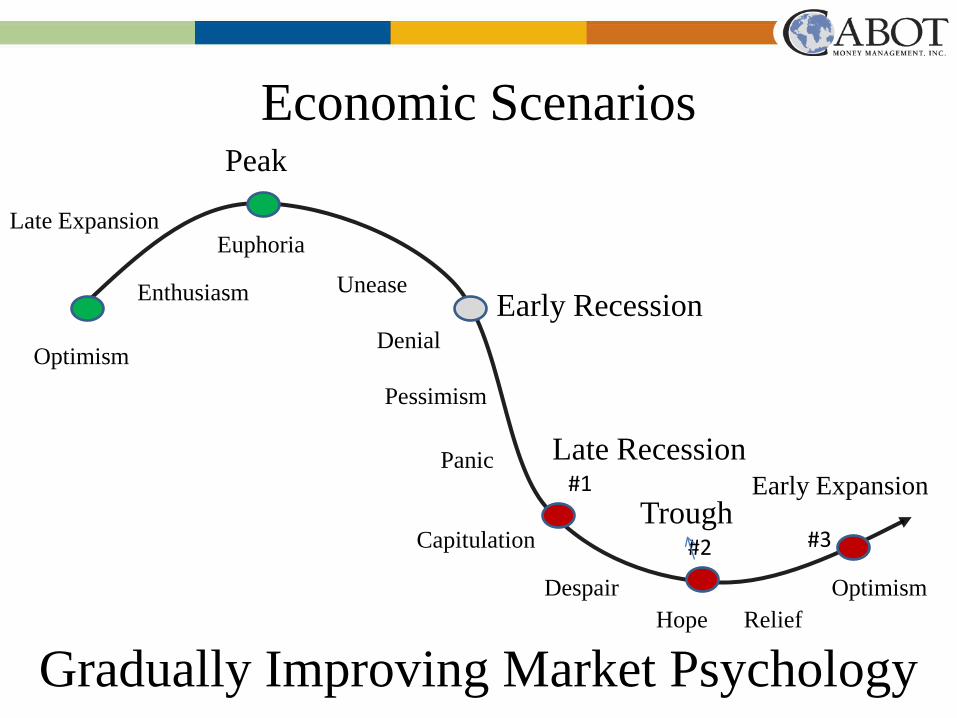

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

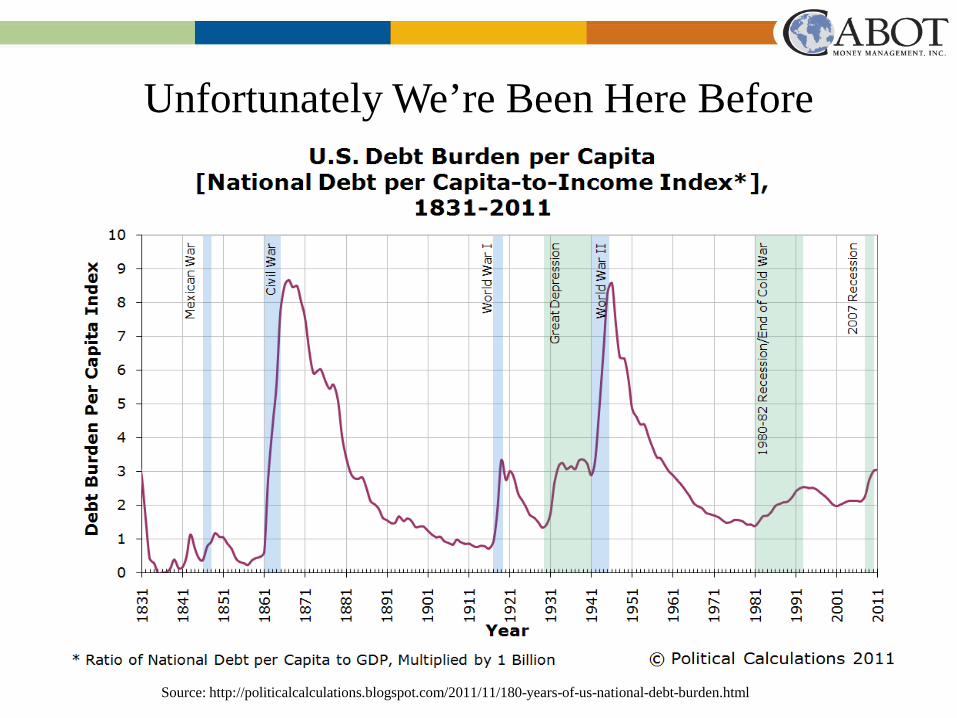

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

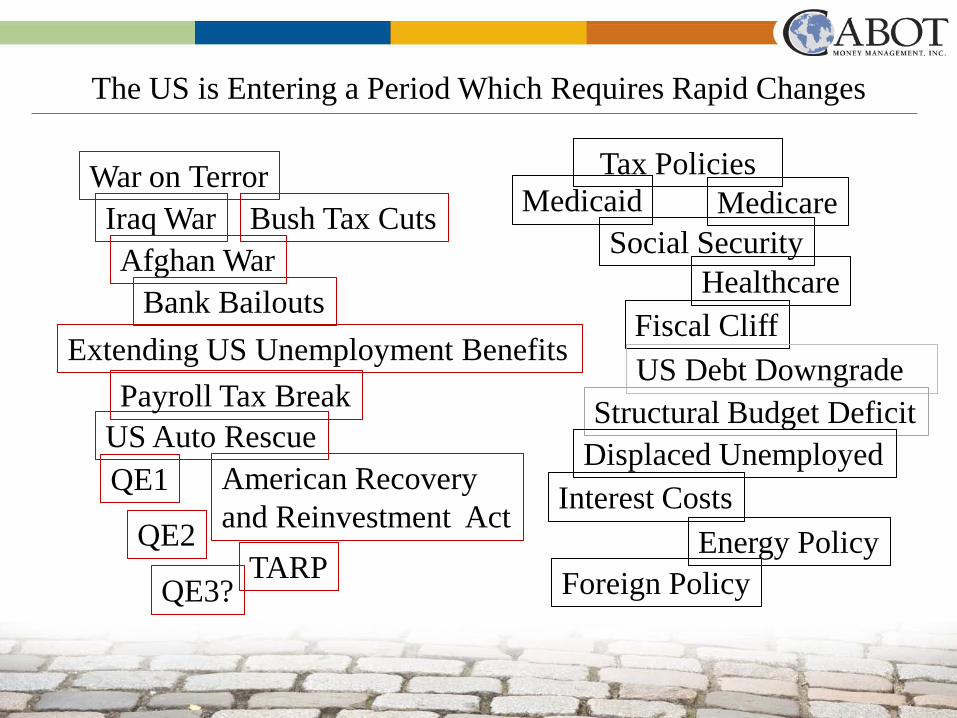

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

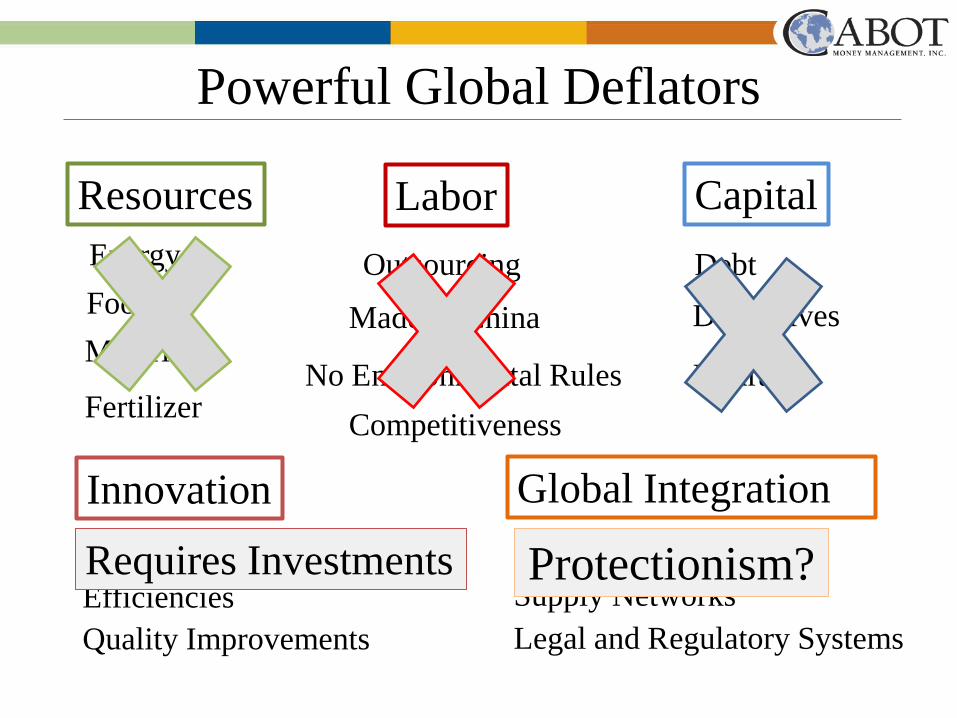

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

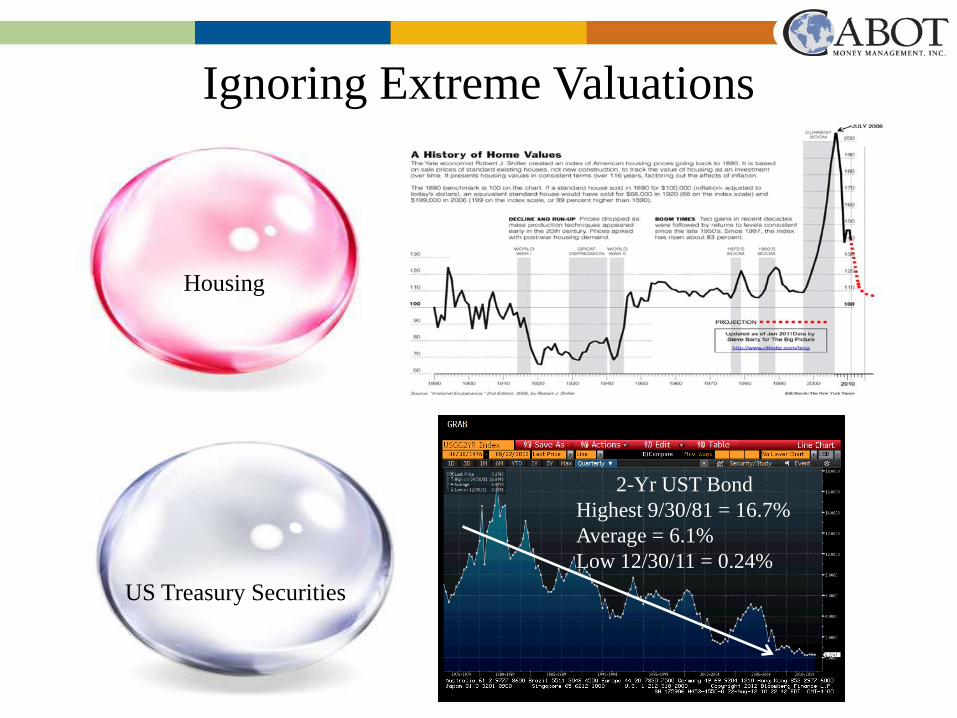

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

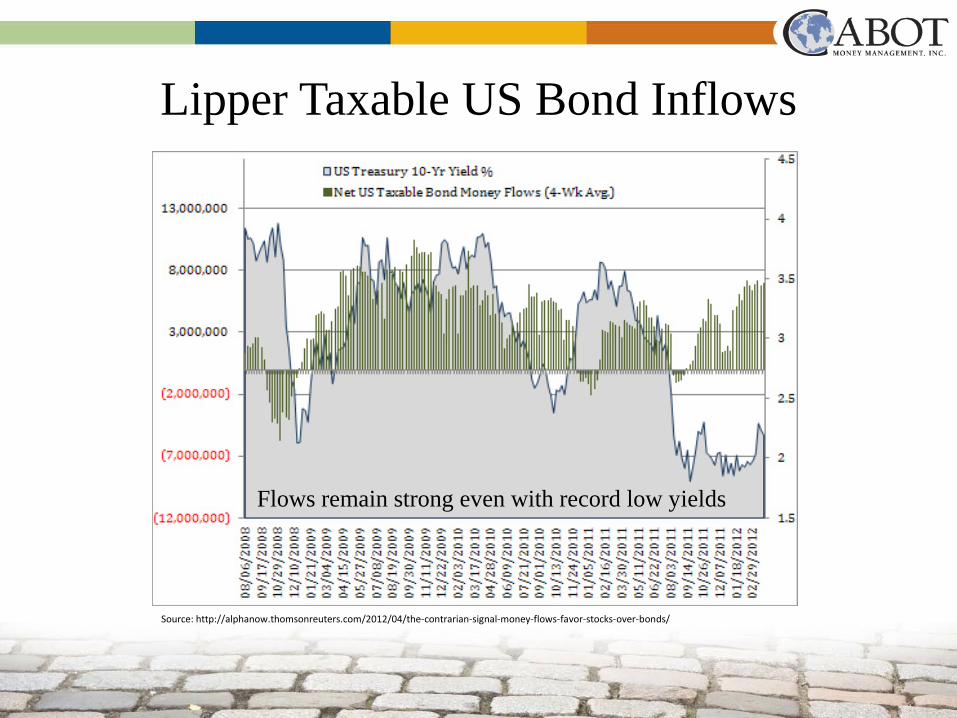

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

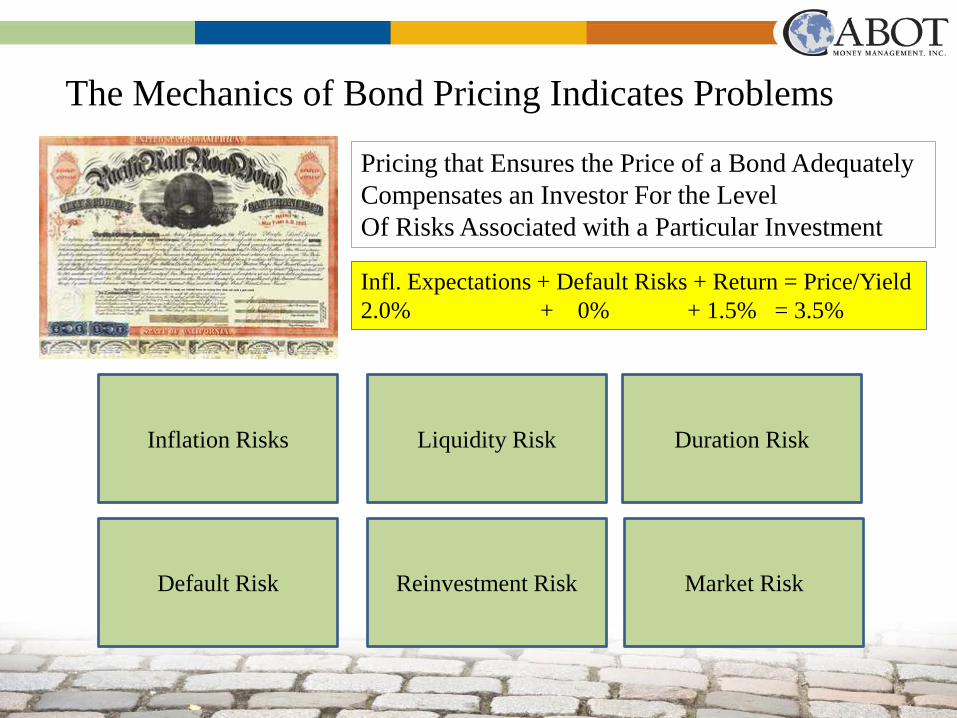

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

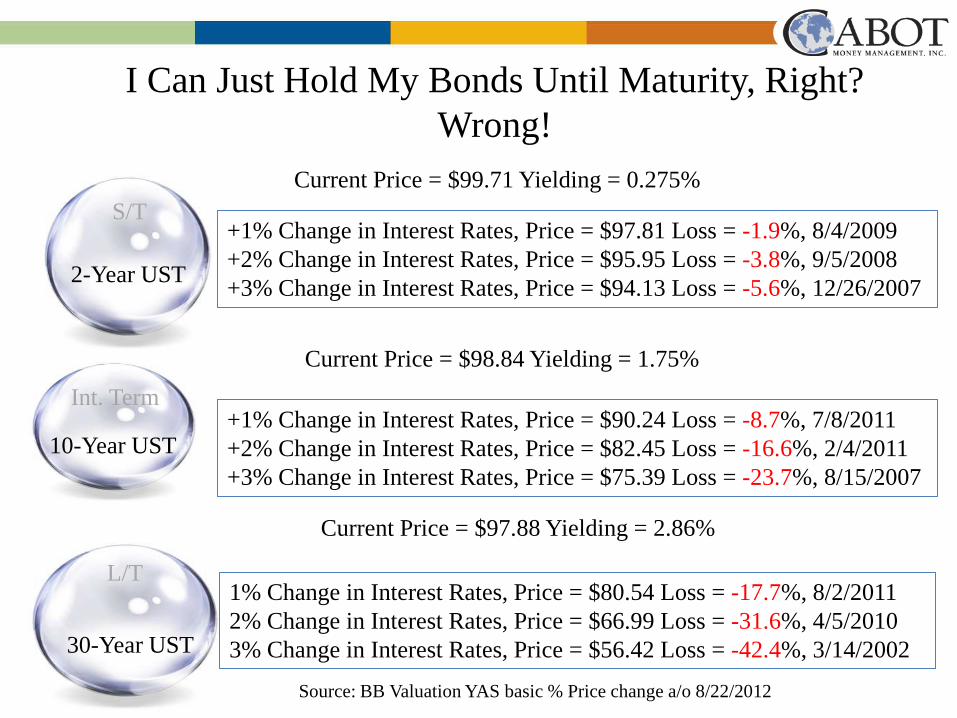

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

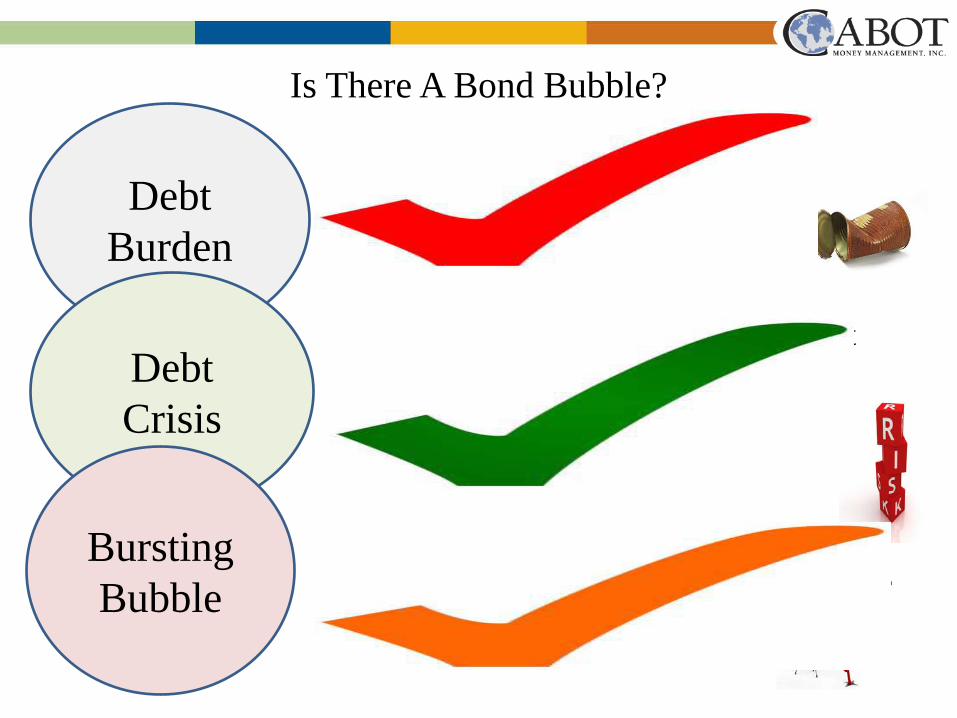

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

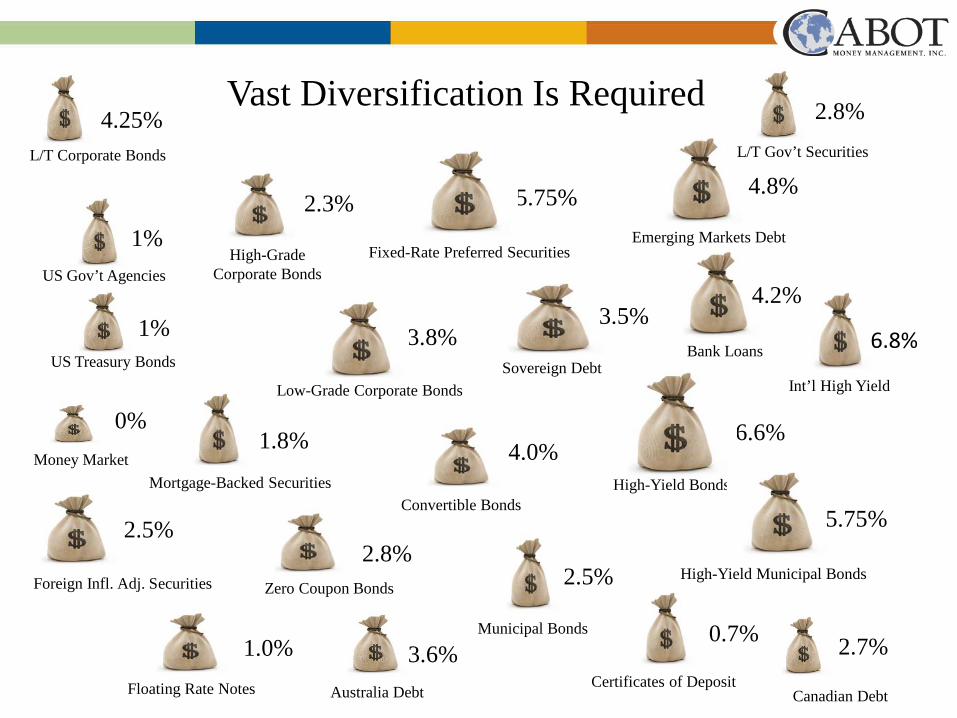

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

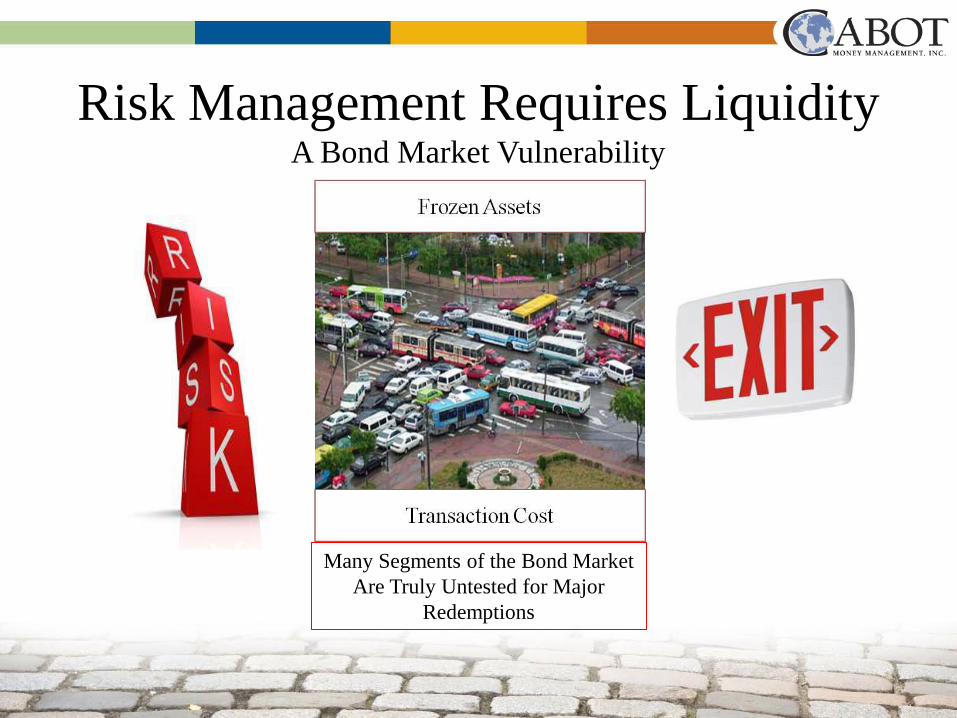

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

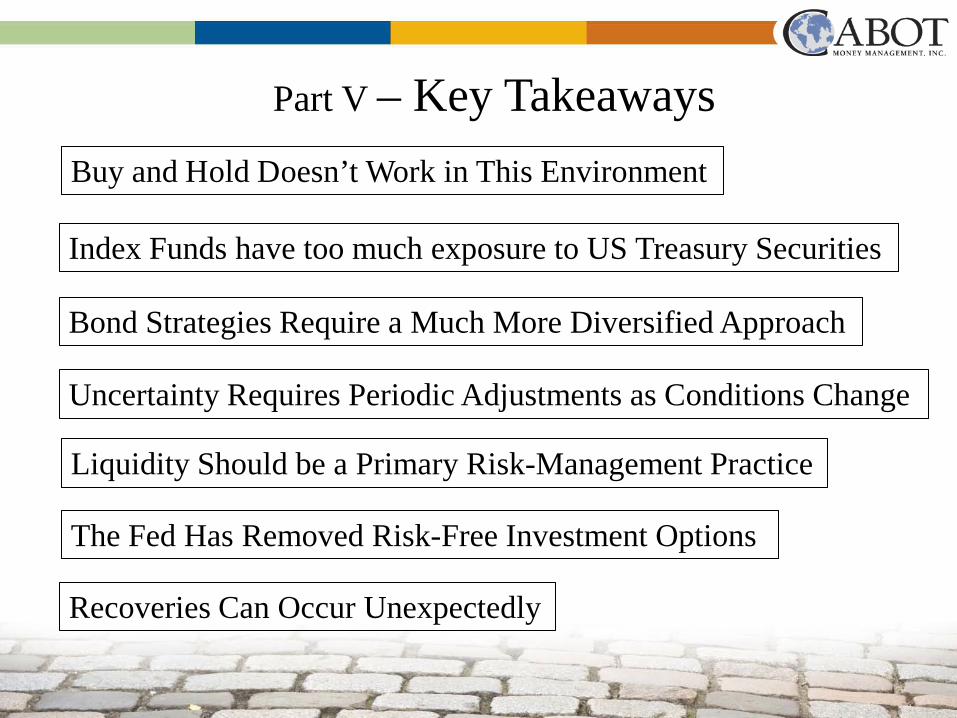

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

William Larkin Jr Portfolio Manager

Cabot Money Management Inc

216 Essex Street Salem Massachusetts 01970

800-888-6468 eCabotcom

Trouble with the Bubble

Bond Bubble

Part I

Analyzing Our Current Situation

US 10-Year US Treasury Security

Yield

Time

Yield is Inverse to Price

16 Peek

16 Today

Source BB data pulled 942012

50 Years of Interest Rates

66 Ave

Our Interconnected Financial Systems

Debt Bubble

Housing

3

Market Uncertainty Feeds Fear

House Bubble Burst Crisis-Averting Maneuvers Banking Crisis

US Debt Purchases

1 2

4

5

Cheapening the Value of Money

3

The Fedrsquos Strategy = Financial Repression

The Fedrsquos Bond Buying Program

Cheapens the Cost of Debt Negative Real Interest Rates

Zero Interest Rates

Debtor Saver

Lowering Interest Rates Stimulates Economic Growth Drives Down Borrowing Costs and Cheapens Savings Highly Leveraged Enterprises and Households Can Enjoy Attractive Refinancing Opportunities

Requires Government Intervention Tends To Be Very Effective Over Time

Savers Are Forced To Seek High-Risk Opportunities

Do We Have A Bubble Or Are We Funding Future Prosperity

Double Dip Recession Global Recovery

Part II ndash Explaining the Low Rate Environment

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

Bond Bubble

Part I

Analyzing Our Current Situation

US 10-Year US Treasury Security

Yield

Time

Yield is Inverse to Price

16 Peek

16 Today

Source BB data pulled 942012

50 Years of Interest Rates

66 Ave

Our Interconnected Financial Systems

Debt Bubble

Housing

3

Market Uncertainty Feeds Fear

House Bubble Burst Crisis-Averting Maneuvers Banking Crisis

US Debt Purchases

1 2

4

5

Cheapening the Value of Money

3

The Fedrsquos Strategy = Financial Repression

The Fedrsquos Bond Buying Program

Cheapens the Cost of Debt Negative Real Interest Rates

Zero Interest Rates

Debtor Saver

Lowering Interest Rates Stimulates Economic Growth Drives Down Borrowing Costs and Cheapens Savings Highly Leveraged Enterprises and Households Can Enjoy Attractive Refinancing Opportunities

Requires Government Intervention Tends To Be Very Effective Over Time

Savers Are Forced To Seek High-Risk Opportunities

Do We Have A Bubble Or Are We Funding Future Prosperity

Double Dip Recession Global Recovery

Part II ndash Explaining the Low Rate Environment

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

Part I

Analyzing Our Current Situation

US 10-Year US Treasury Security

Yield

Time

Yield is Inverse to Price

16 Peek

16 Today

Source BB data pulled 942012

50 Years of Interest Rates

66 Ave

Our Interconnected Financial Systems

Debt Bubble

Housing

3

Market Uncertainty Feeds Fear

House Bubble Burst Crisis-Averting Maneuvers Banking Crisis

US Debt Purchases

1 2

4

5

Cheapening the Value of Money

3

The Fedrsquos Strategy = Financial Repression

The Fedrsquos Bond Buying Program

Cheapens the Cost of Debt Negative Real Interest Rates

Zero Interest Rates

Debtor Saver

Lowering Interest Rates Stimulates Economic Growth Drives Down Borrowing Costs and Cheapens Savings Highly Leveraged Enterprises and Households Can Enjoy Attractive Refinancing Opportunities

Requires Government Intervention Tends To Be Very Effective Over Time

Savers Are Forced To Seek High-Risk Opportunities

Do We Have A Bubble Or Are We Funding Future Prosperity

Double Dip Recession Global Recovery

Part II ndash Explaining the Low Rate Environment

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

US 10-Year US Treasury Security

Yield

Time

Yield is Inverse to Price

16 Peek

16 Today

Source BB data pulled 942012

50 Years of Interest Rates

66 Ave

Our Interconnected Financial Systems

Debt Bubble

Housing

3

Market Uncertainty Feeds Fear

House Bubble Burst Crisis-Averting Maneuvers Banking Crisis

US Debt Purchases

1 2

4

5

Cheapening the Value of Money

3

The Fedrsquos Strategy = Financial Repression

The Fedrsquos Bond Buying Program

Cheapens the Cost of Debt Negative Real Interest Rates

Zero Interest Rates

Debtor Saver

Lowering Interest Rates Stimulates Economic Growth Drives Down Borrowing Costs and Cheapens Savings Highly Leveraged Enterprises and Households Can Enjoy Attractive Refinancing Opportunities

Requires Government Intervention Tends To Be Very Effective Over Time

Savers Are Forced To Seek High-Risk Opportunities

Do We Have A Bubble Or Are We Funding Future Prosperity

Double Dip Recession Global Recovery

Part II ndash Explaining the Low Rate Environment

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

Our Interconnected Financial Systems

Debt Bubble

Housing

3

Market Uncertainty Feeds Fear

House Bubble Burst Crisis-Averting Maneuvers Banking Crisis

US Debt Purchases

1 2

4

5

Cheapening the Value of Money

3

The Fedrsquos Strategy = Financial Repression

The Fedrsquos Bond Buying Program

Cheapens the Cost of Debt Negative Real Interest Rates

Zero Interest Rates

Debtor Saver

Lowering Interest Rates Stimulates Economic Growth Drives Down Borrowing Costs and Cheapens Savings Highly Leveraged Enterprises and Households Can Enjoy Attractive Refinancing Opportunities

Requires Government Intervention Tends To Be Very Effective Over Time

Savers Are Forced To Seek High-Risk Opportunities

Do We Have A Bubble Or Are We Funding Future Prosperity

Double Dip Recession Global Recovery

Part II ndash Explaining the Low Rate Environment

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

The Fedrsquos Strategy = Financial Repression

The Fedrsquos Bond Buying Program

Cheapens the Cost of Debt Negative Real Interest Rates

Zero Interest Rates

Debtor Saver

Lowering Interest Rates Stimulates Economic Growth Drives Down Borrowing Costs and Cheapens Savings Highly Leveraged Enterprises and Households Can Enjoy Attractive Refinancing Opportunities

Requires Government Intervention Tends To Be Very Effective Over Time

Savers Are Forced To Seek High-Risk Opportunities

Do We Have A Bubble Or Are We Funding Future Prosperity

Double Dip Recession Global Recovery

Part II ndash Explaining the Low Rate Environment

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

Lowering Interest Rates Stimulates Economic Growth Drives Down Borrowing Costs and Cheapens Savings Highly Leveraged Enterprises and Households Can Enjoy Attractive Refinancing Opportunities

Requires Government Intervention Tends To Be Very Effective Over Time

Savers Are Forced To Seek High-Risk Opportunities

Do We Have A Bubble Or Are We Funding Future Prosperity

Double Dip Recession Global Recovery

Part II ndash Explaining the Low Rate Environment

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

Do We Have A Bubble Or Are We Funding Future Prosperity

Double Dip Recession Global Recovery

Part II ndash Explaining the Low Rate Environment

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

Part II ndash Explaining the Low Rate Environment

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

Investment Behavior is Out of Balance

Greed vs Fear

Returns vs Principal Protection

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

Financial Doomsday or Work on Monday

Fear Uncertainty Reality

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance

Made In China

No Environmental Rules Competitiveness

Innovation Product Development Efficiencies Quality Improvements

Global Integration Trade Supply Networks Legal and Regulatory Systems

Protectionism Requires Investments

Ignoring Extreme Valuations

Housing

US Treasury Securities

2-Yr UST Bond Highest 93081 = 167 Average = 61 Low 123011 = 024

Lipper Taxable US Bond Inflows

Source httpalphanowthomsonreuterscom201204the-contrarian-signal-money-flows-favor-stocks-over-bonds

Flows remain strong even with record low yields

The Mechanics of Bond Pricing Indicates Problems

Inflation Risks

Default Risk

Liquidity Risk

Reinvestment Risk

Duration Risk

Market Risk

Pricing that Ensures the Price of a Bond Adequately Compensates an Investor For the Level Of Risks Associated with a Particular Investment

Infl Expectations + Default Risks + Return = PriceYield 20 + 0 + 15 = 35

I Can Just Hold My Bonds Until Maturity Right Wrong

Current Price = $9971 Yielding = 0275

Current Price = $9884 Yielding = 175

Current Price = $9788 Yielding = 286

+1 Change in Interest Rates Price = $9781 Loss = -19 842009 +2 Change in Interest Rates Price = $9595 Loss = -38 952008 +3 Change in Interest Rates Price = $9413 Loss = -56 12262007

+1 Change in Interest Rates Price = $9024 Loss = -87 782011 +2 Change in Interest Rates Price = $8245 Loss = -166 242011 +3 Change in Interest Rates Price = $7539 Loss = -237 8152007

1 Change in Interest Rates Price = $8054 Loss = -177 822011 2 Change in Interest Rates Price = $6699 Loss = -316 452010 3 Change in Interest Rates Price = $5642 Loss = -424 3142002

2-Year UST

10-Year UST

30-Year UST

Source BB Valuation YAS basic Price change ao 8222012

ST

Int Term

LT

Is There A Bond Bubble

The debt burden grows out of control and fiscal solutions fail to develop

The market comes to the conclusion that the debt has become unsustainable and demands a much higher return to offset growing risks

Bond yields rise causing harm to current holders that do not properly understand their potential loses

Debt Burden

Debt Crisis

Bursting Bubble

Part IV Investment Solutions

Active Management Passive Indexing

Price Insensitive Opportunistic

Vast Diversification Is Required

66

48 575

38

23

18

1

1

0 40

25

Money Market

US Treasury Bonds

US Govrsquot Agencies

Municipal Bonds

Mortgage-Backed Securities

High-Grade Corporate Bonds

Low-Grade Corporate Bonds

Fixed-Rate Preferred Securities

Sovereign Debt

Emerging Markets Debt

Bank Loans

High-Yield Bonds Convertible Bonds

Foreign Infl Adj Securities

25

High-Yield Municipal Bonds

575

Zero Coupon Bonds

28

Floating Rate Notes

10 Certificates of Deposit

07

Australia Debt

36 Canadian Debt

27

LT Corporate Bonds

425 LT Govrsquot Securities

28

35 42

Intrsquol High Yield

68

Risk Management Requires Liquidity

Many Segments of the Bond Market Are Truly Untested for Major

Redemptions

A Bond Market Vulnerability

The Biggest Risk Is Taking No Risk

Credit Risk

Broaden Exposure

Duration Risk

3 Strategy Options

Default Risk

Global Opportunities Extend Maturities

Buy and Hold Doesnrsquot Work in This Environment

Index Funds have too much exposure to US Treasury Securities

Part V ndash Key Takeaways

Bond Strategies Require a Much More Diversified Approach

Uncertainty Requires Periodic Adjustments as Conditions Change

Liquidity Should be a Primary Risk-Management Practice

The Fed Has Removed Risk-Free Investment Options

Recoveries Can Occur Unexpectedly

Questions

23rd Annual Investment Conference amp Luncheon

Peak

Trough

Early Recession

Late Recession Early Expansion 1

2 3

Gradually Improving Market Psychology

Late Expansion

Optimism

Enthusiasm

Euphoria

Unease

Denial

Pessimism

Panic

Capitulation

Despair Hope Relief

Optimism

Economic Scenarios

Part III - Analyze The Current Situation

Source httppoliticalcalculationsblogspotcom201111180-years-of-us-national-debt-burdenhtml

Unfortunately Wersquore Been Here Before

War on Terror Iraq War Afghan War

Bank Bailouts Extending US Unemployment Benefits

US Auto Rescue QE1

QE2

Payroll Tax Break

QE3

Tax Policies

Fiscal Cliff

Medicare Medicaid Social Security

Healthcare

US Debt Downgrade Structural Budget Deficit

Displaced Unemployed Interest Costs

Energy Policy

Bush Tax Cuts

American Recovery and Reinvestment Act

Foreign Policy

The US is Entering a Period Which Requires Rapid Changes

TARP

A Unique Macro Environment Banking Capital Markets

LaborWork Design Technology

Multi-National Companies

Supply Chain

Interest Rates

Transportation

Energy

Powerful Global Deflators

Energy

Resources Labor

Food Materials

Fertilizer

Capital Outsourcing Debt

Derivatives

Insurance