Embed Size (px)

Citation preview

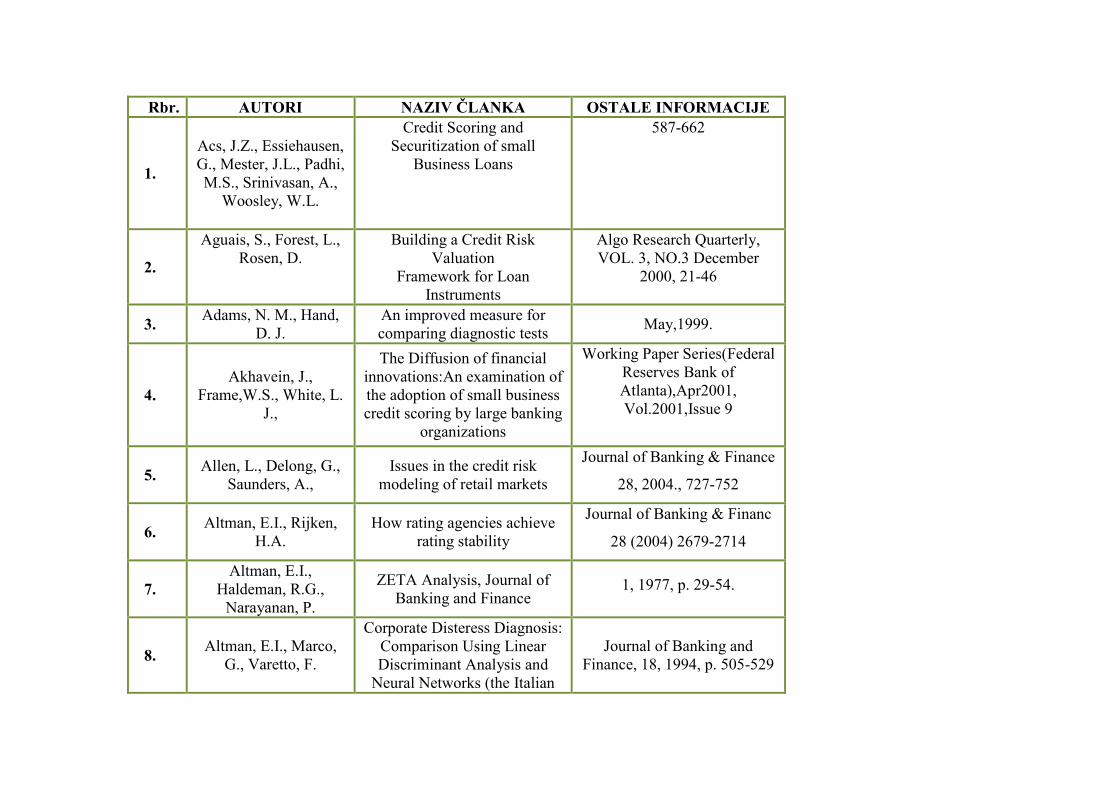

Rbr. AUTORI NAZIV ČLANKA OSTALE INFORMACIJE

1.

Acs, J.Z., Essiehausen, G., Mester, J.L., Padhi, M.S., Srinivasan, A.,

Woosley, W.L.

Credit Scoring and Securitization of small

Business Loans

587-662

2.

Aguais, S., Forest, L., Rosen, D.

Building a Credit Risk Valuation

Framework for Loan Instruments

Algo Research Quarterly, VOL. 3, NO.3 December

2000, 21-46

3. Adams, N. M., Hand,

D. J. An improved measure for comparing diagnostic tests May,1999.

4.

Akhavein, J., Frame,W.S., White, L.

J.,

The Diffusion of financial innovations:An examination of the adoption of small business credit scoring by large banking

organizations

Working Paper Series(Federal Reserves Bank of Atlanta),Apr2001, Vol.2001,Issue 9

5. Allen, L., Delong, G.,

Saunders, A., Issues in the credit risk

modeling of retail markets

Journal of Banking & Finance

28, 2004., 727-752

6. Altman, E.I., Rijken,

H.A. How rating agencies achieve

rating stability

Journal of Banking & Financ

28 (2004) 2679-2714

7.

Altman, E.I., Haldeman, R.G.,

Narayanan, P.

ZETA Analysis, Journal of Banking and Finance

1, 1977, p. 29-54.

8. Altman, E.I., Marco,

G., Varetto, F.

Corporate Disteress Diagnosis: Comparison Using Linear Discriminant Analysis and

Neural Networks (the Italian

Journal of Banking and Finance, 18, 1994, p. 505-529

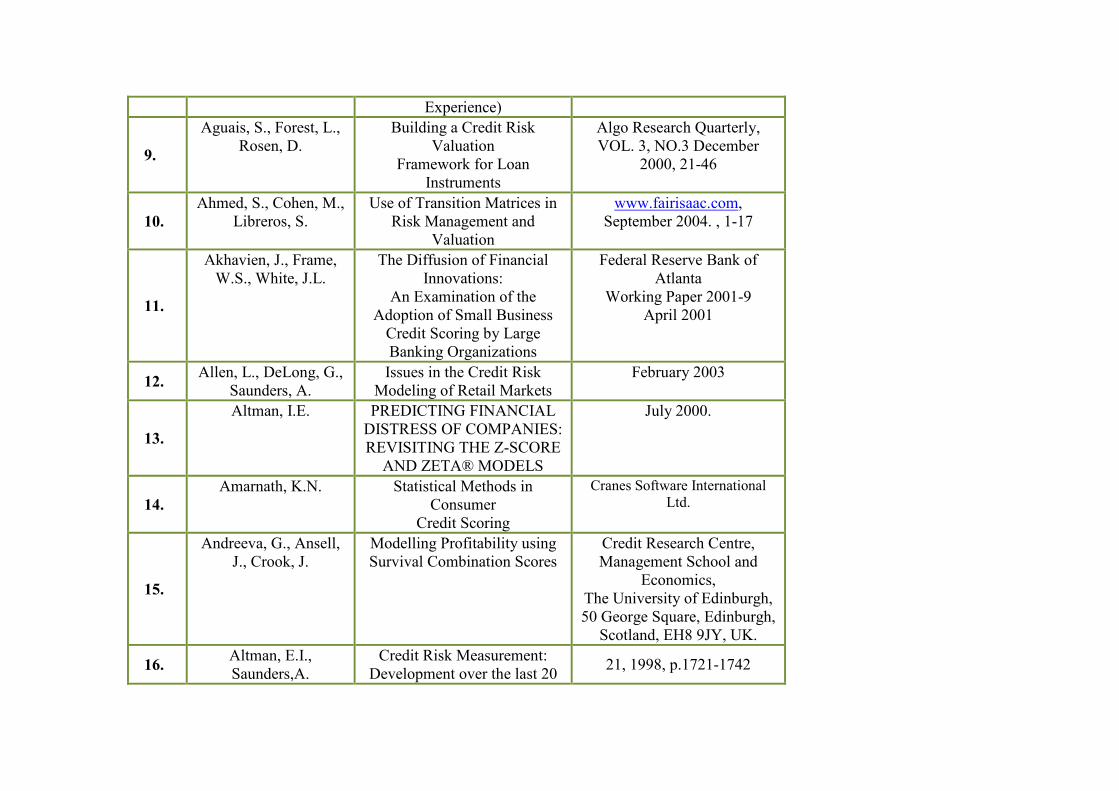

Experience)

9.

Aguais, S., Forest, L., Rosen, D.

Building a Credit Risk Valuation

Framework for Loan Instruments

Algo Research Quarterly, VOL. 3, NO.3 December

2000, 21-46

10.

Ahmed, S., Cohen, M., Libreros, S.

Use of Transition Matrices in Risk Management and

Valuation

www.fairisaac.com, September 2004. , 1-17

11.

Akhavien, J., Frame, W.S., White, J.L.

The Diffusion of Financial Innovations:

An Examination of the Adoption of Small Business

Credit Scoring by Large Banking Organizations

Federal Reserve Bank of Atlanta

Working Paper 2001-9 April 2001

12. Allen, L., DeLong, G.,

Saunders, A. Issues in the Credit Risk

Modeling of Retail Markets February 2003

13.

Altman, I.E. PREDICTING FINANCIAL DISTRESS OF COMPANIES: REVISITING THE Z-SCORE

AND ZETA® MODELS

July 2000.

14.

Amarnath, K.N. Statistical Methods in Consumer

Credit Scoring

Cranes Software International Ltd.

15.

Andreeva, G., Ansell, J., Crook, J.

Modelling Profitability using Survival Combination Scores

Credit Research Centre, Management School and

Economics, The University of Edinburgh, 50 George Square, Edinburgh,

Scotland, EH8 9JY, UK.

16. Altman, E.I., Saunders,A.

Credit Risk Measurement: Development over the last 20 21, 1998, p.1721-1742

Years, Journal of Banking and Finance

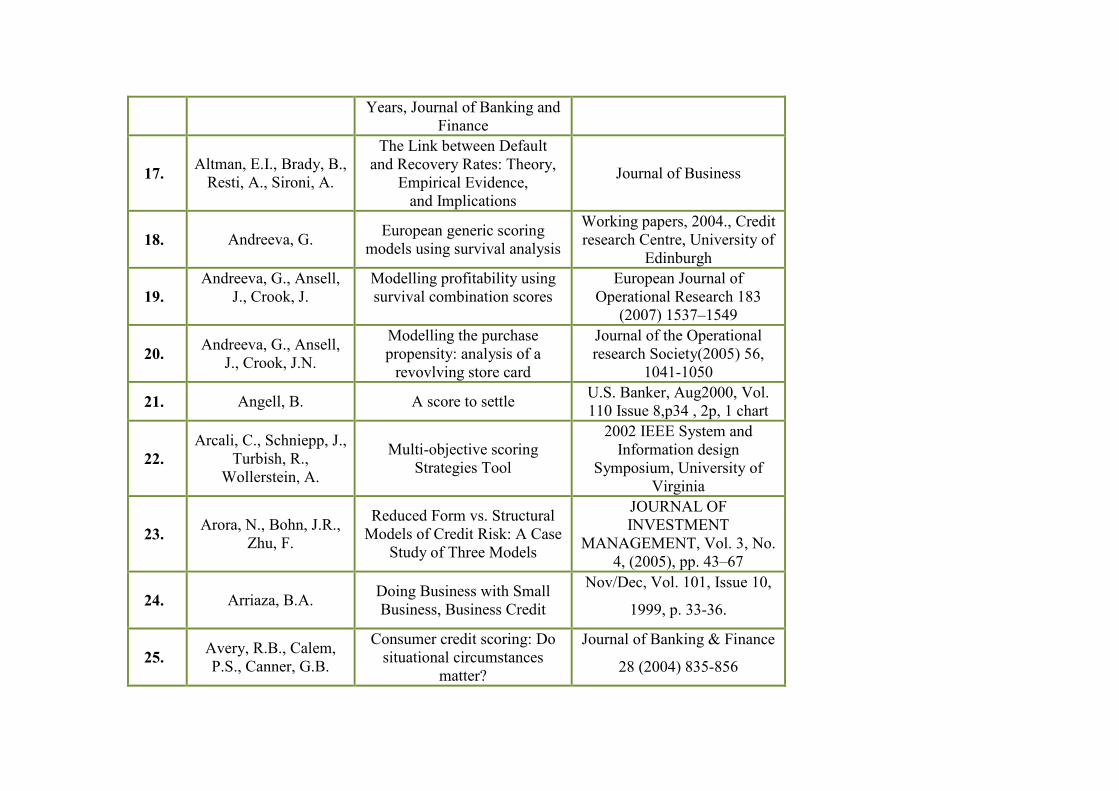

17. Altman, E.I., Brady, B.,

Resti, A., Sironi, A.

The Link between Default and Recovery Rates: Theory,

Empirical Evidence, and Implications

Journal of Business

18. Andreeva, G. European generic scoring models using survival analysis

Working papers, 2004., Credit research Centre, University of

Edinburgh

19.

Andreeva, G., Ansell, J., Crook, J.

Modelling profitability using survival combination scores

European Journal of Operational Research 183

(2007) 1537–1549

20. Andreeva, G., Ansell,

J., Crook, J.N.

Modelling the purchase propensity: analysis of a

revovlving store card

Journal of the Operational research Society(2005) 56,

1041-1050

21. Angell, B. A score to settle U.S. Banker, Aug2000, Vol. 110 Issue 8,p34 , 2p, 1 chart

22.

Arcali, C., Schniepp, J., Turbish, R.,

Wollerstein, A.

Multi-objective scoring Strategies Tool

2002 IEEE System and Information design

Symposium, University of Virginia

23. Arora, N., Bohn, J.R.,

Zhu, F.

Reduced Form vs. Structural Models of Credit Risk: A Case

Study of Three Models

JOURNAL OF INVESTMENT

MANAGEMENT, Vol. 3, No. 4, (2005), pp. 43–67

24. Arriaza, B.A. Doing Business with Small Business, Business Credit

Nov/Dec, Vol. 101, Issue 10,

1999, p. 33-36.

25. Avery, R.B., Calem, P.S., Canner, G.B.

Consumer credit scoring: Do situational circumstances

matter?

Journal of Banking & Finance

28 (2004) 835-856

26.

Avery, R.B., Bostic, R.W., Calem, P.S.,

Canner, G.B.

Credit scoring: Statistical Issues and Evidence from

Credit-bureau files, Real Estate Economics

Vol. 28, Issue 3, 2000, p. 523-547

27.

Baesens, B., De Backer, M., Setiono,

R., Vanthienen, J.

BUILDING INTELLIGENT CREDIT SCORING SYSTEMS USING

DECISION TABLES

ICEIS 2003 - Arti_cial Intelligence and Decision Support Systems, 19-25

28.

Baesens, B., Dedene, G., Derrig, A.R.,

Viaene, S.

A Comparison of State-of-the-Art Classification Techniques

for Expert Automobile Insurance Claim Frand

Detection

The Jurnal of Risk and Insurance, 2002, Vol.69, No.

3, 373-421

29.

Baesens, B., Files, C.M., Mues, C., Vanthienen, J.

Decision diagrams in machine learning: an empirical study on real-life credit-risk data

Expert Systems with Applications 27 (2004) 257–

264

30. Badiru, A.B., Sieger,

D.B.

Neural network as a simulation metamodel in economic analysis of risky projects

Europian Journal of Operational Research 105

(1998) 130-142.

31.

Baesens, B., Van Gestel, T., Stepanova,

M., Vanthienen, J.

Neural Network Survival Analysisi for Personal Loan

Data

Journal of the Operational Research Society (2005) 56,

1089-1098

32. Baljkas, S., Prester, J. Primjena teorije očekivanog

izbora na management projektnih rizika

Suvremeno poduzetništvo 11/2003.

33. Banasik, J., Crook, J. Credit scoring, augmentation and lean models

Journal of the Operational Research Society (2005) 56,

1072-1081.

34. Banasik, J., Crook, J.,

Thomas, L.C. Not if but when will borrowers

default

Journal of the Operational Research Society (1999) 50,

1185-1190

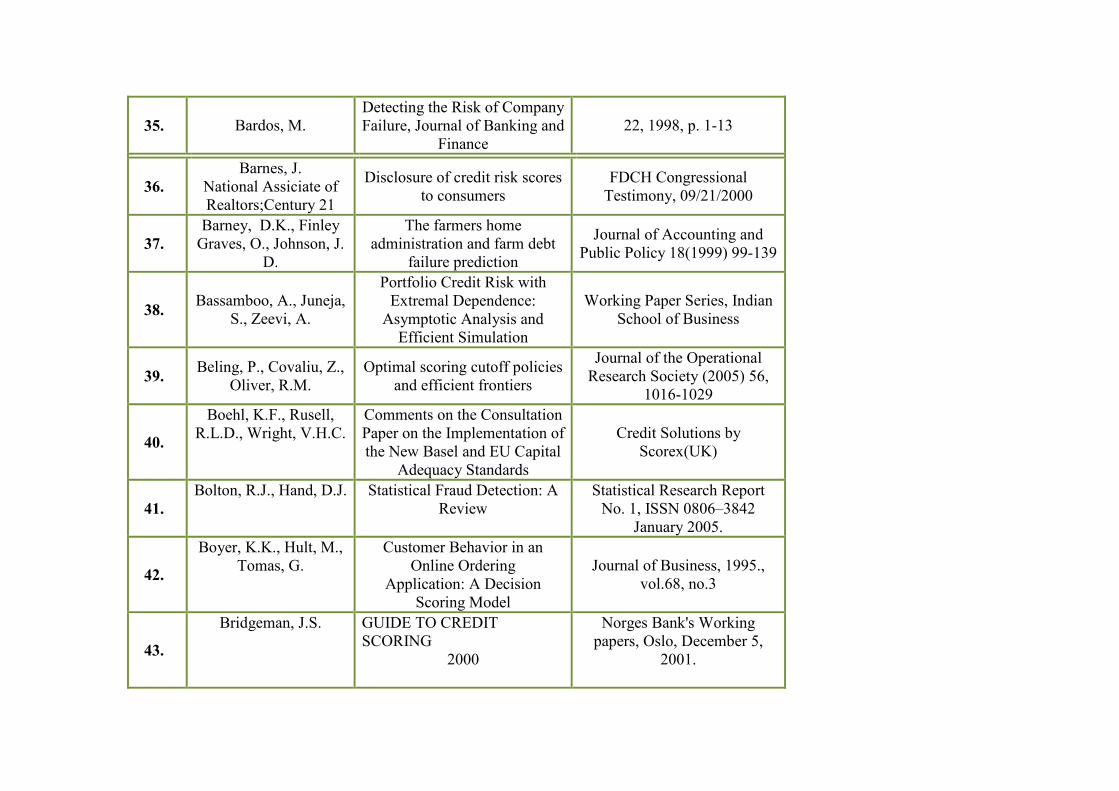

35. Bardos, M. Detecting the Risk of Company Failure, Journal of Banking and

Finance 22, 1998, p. 1-13

36.

Barnes, J. National Assiciate of Realtors;Century 21

Disclosure of credit risk scores to consumers

FDCH Congressional Testimony, 09/21/2000

37.

Barney, D.K., Finley Graves, O., Johnson, J.

D.

The farmers home administration and farm debt

failure prediction

Journal of Accounting and Public Policy 18(1999) 99-139

38. Bassamboo, A., Juneja,

S., Zeevi, A.

Portfolio Credit Risk with Extremal Dependence:

Asymptotic Analysis and Efficient Simulation

Working Paper Series, Indian School of Business

39. Beling, P., Covaliu, Z.,

Oliver, R.M. Optimal scoring cutoff policies

and efficient frontiers

Journal of the Operational Research Society (2005) 56,

1016-1029

40.

Boehl, K.F., Rusell, R.L.D., Wright, V.H.C.

Comments on the Consultation Paper on the Implementation of the New Basel and EU Capital

Adequacy Standards

Credit Solutions by Scorex(UK)

41.

Bolton, R.J., Hand, D.J. Statistical Fraud Detection: A Review

Statistical Research Report No. 1, ISSN 0806–3842

January 2005.

42.

Boyer, K.K., Hult, M., Tomas, G.

Customer Behavior in an Online Ordering

Application: A Decision Scoring Model

Journal of Business, 1995., vol.68, no.3

43.

Bridgeman, J.S. GUIDE TO CREDIT SCORING

2000

Norges Bank's Working papers, Oslo, December 5,

2001.

44.

Bugera, V., Konno, H., Uryasev,S.

Credit Cards Scoring with Quadratic Utility Functions

International Journal of Bank Marketing, Vol. 13 No. 5,

1995, pp. 31-36

45.

Bugera, V., Konno, H., Uryasev,S.

Credit Cards Scoring with Quadratic Utility Functions

ERIM Report Series Research in Management, ERS-2001-

11-LIS, February 2001.

46.

Bunn, P., Redwood, V. Company accounts based modelling of business failures

and the implications for financial stability

Journal of banking & Finance xxx (2005) xxx-xxx

47. Burns, P., Ody, C. Validation of Consumer

Credit Risk Models Journal of Econometrics 40 (1989) 3-14,North-Holland

48. Brennan, P.J. Profitability Scoring Comes of Age, Bank Management Vol. 69, No. 9, 1993, p. 58-60.

49. Brill, J. The Importance of credit

scoring models in improving cash flow and collections

Business Credit, Jan98, Vol.100 Issue 1, p16, 2p.

50. Bunn, D. W. Empirical Bayes Procedure for the Credit Granting Decision Vol. 1, No. 1

51.

Bugera, V., Konno, H., Uryasev,S.

Credit Cards Scoring with Quadratic Utility Functions

Risk Management and Financial Engineering Lab

Center for Applied Optimization

Department of Industrial and Systems Engineering University of Florida,

Gainesville, FL, 32611 Date: January, 15, 2002

52.

Bugera, V., Konno, H., Uryasev,S.

Credit Cards Scoring with Quadratic Utility Functions

JOURNAL OF MULTI-CRITERIA DECISION

ANALYSIS

J. Multi-Crit. Decis. Anal. 11: 197–211 (2002)

Published online in Wiley InterScience

(www.interscience.wiley.com) DOI: 10.1002/mcda.327

53.

Bunn, P., Redwood, V. Company accounts based modelling of business failures

and the implications for financial stability

© Bank of England 2003 ISSN 1368-5562

54. Burns, P., Ody, C. Validation of Consumer

Credit Risk Models www.philadelphiafed.org/pcc

55. Butler, P., Durkin, M. Relationship intermediaries:

business advisers in the small firm-bank relationship

MCB International Journal of Bankong Marketing, Vol 16

,Issue 1.

56.

Caire, D. Building Credit Scorecards for Small Business Lending in

Developing Markets

Bannock Consulting November 2004

57.

Charalambous, C., Chariton, A.,

Neophyton, E.

Predicting Corporate Failure: Empirical Evidence for the UK

This version September 2000

58.

Chinchilli, M.V., King, T.S.

A generalized concordance correlation coe(cient for

continuous and categorical data

STATISTICS IN MEDICINE Statist. Med. 2001; 20:2131–2147 (DOI: 10.1002/sim.845)

59.

CIB Bank Ltd. Managing credit products with the exploitation of SAS Credit Scoring

solution

A case study for in-house credit scoring model development in CIB

60. Capponi, A., Cvitanić

J. Credit Risk Modeling with

Misreporting and Submitted to Management

Science

Incomplete Information manuscript

61. Claessens, S., Krahnen,

J., Lang, W.W. The Basel II Reform and Retail

Credit Markets Journal of Financial Services Research 28:1/2/3 5–13, 2005

62. Chatterjee, S., Corbae,

D., Rios-Rull, J.V.

Credit Scoring and Competitive Pricing of Default

Risk 2004.

63. Chatzky, J.S. Keeping Score Money;Mar2003, Vol. 32 Issue 3, p142, 1p, 2c

64. Chen, G.G., Ǻstebro, T. Bound and Collapse Bayesian Reject Inference When Data are Missing not at Random

Septembre, 2003.

65. Chen, M.C., Huang,

S.H.

Credit scoring and rejected instances ressigning through

evolutionary computation techniques

Expert Systems with Applications 24 (2003) 433-

441

66. Cheng, R.H.C., McKee,

S.

Ima Journal of mathematics applied in business and

industry

Volume 11 Number 2 March 2000

67. Chi, L.C., Tang T.C. Prediction: Application of

Logit Analysis in Export Credit Risks

Australian Journal of Management, Vol. 31, No. 1

June 2006.

68. Coffman, J., Introducing Scoring to Micro and Small Business Lending Partner, C&T International

69. Cowan, C. D., Cowan,

A. M.

A Survey Based Assessment of Financial

Institution Use of Credit Scoring for

Small Business Lending

Small Business Research Summary, 2006. [62] pages. Under contract SBAH-04-Q-

002

70. Cowling, M., Westhead, P.

Bank lending decisions and small firms: does size matter

Enterpreneurial Behaviour& Reserch, Vol. 2, 1996, pp. 52-

68

71. Cressy, R.C.

Credit rationing or entrepreneurial risk aversion? An alternative explanation for

the evans And Jovanovic finding

Economics Letters 66 (2000)

235-240.

72. Cressy, R.C. Debt Rescheduling versus Bankruptcy: The Creditor's

Decision Problem

Journal of Business Finance &

Accounting, 23(8), October

1996, 0306-686X

73.

Caire, D. Building Credit Scorecards for Small Business Lending in

Developing Markets

Bannock Consulting November 2004

74.

Charalambous, C., Chariton, A.,

Neophyton, E.

Predicting Corporate Failure: Empirical Evidence for the UK

This version September 2000

75.

Chinchilli, M.V., King, T.S.

A generalized concordance correlation coe(cient for

continuous and categorical data

STATISTICS IN MEDICINE Statist. Med. 2001; 20:2131–2147 (DOI: 10.1002/sim.845)

76.

CIB Bank Ltd. Managing credit products with the exploitation of SAS Credit Scoring

solution

A case study for in-house credit scoring model development in CIB

77. Crook, J., Banasik, J. Does Reject Inference Really Improve the Performance of Application Scoring Models

Working Paper Series No.

02/3

78. Čaklogović, L., Šego,

V. Potential method applied on

exact data

Operational Research

Proceedings KOI2002,237-

248

79. Dakovic, R., Czado, C.,

Berg, D. Bankruptcy prediction in

Norway: a comparison study

Statistical Research Report No. 4, ISSN 0806–3842 June

2007.

80. Davidson, S. Recent Research on Trends in Small Business Bank Lending

Community Banker, Vol.9, Issue 9, 200, p.40-41.

81. Davis, K.T. Credit Scoring Software: A Brief Look

Business Credit, Feb99, Vol. 101 Issue 2, p32, 3p

82. Dennis, W. L. Fair lending and credit scoring Mortgage Banking, Nov95, Vol.56 Issue 2,p55, 4p

83. De Noni, I., Lorenzon,

A., Orsi, L.

Measuring and Managing Credit Risk in SMEs: a

Quantitative and Qualitative Rating Model

Department of Economics, Business Administration and Statistics, Faculty of Political Science, University of Milan

84.

Desai, V.S., Crook, J.N., Overstreet Jr.,

G.A.

A comparasion of neural networks and linear scoring models in the credit union

environment

European Journal of Operational Research 95

(1996) 24-37

85.

Desai, V.S., Conway, D.G., Crook, J.N.,

Overstreet Jr., G.A.

Credit-scoring models in the credit-union enviroment using neural networks and genetic

algorithms

IMA Journal of Mathematics Applied in Business &

Industry (1997) 8, 323-346

86. Dey, S., Mumy, G. Determinants of Borrowing Limits on Credit Cards

Bank of Canada Working Paper 2005-7, March 2005.

87. Dickens, M., Keppler,

B. SUMMARY ON CREDIT APPLICATION SCORING

The PA Consulting Group

88.

Dimitrios, V., Georgios, A.,

Konstantinos, S.

RiskRisk--Based Pricing (RBP) Using Bayesian

Statistics: How to Market RBP in the Context of New Credit

Card CustomersCard

Athens University of Economics and Business

Customers

89. Domowitz, I., Sartain,

R.L. Determinants of the Consumer

Bankruptcy Decision

The Journal of Finance, Vol. 54, No. 1 (Feb., 1999), 403-

420.

90. Duffie, D., Saita, L.,

Wang, K.

Multi-period corporate default prediction with stochastic

covariates

Journal of Financial Economics 83 (2007) 635–665

91. Dunn, L.F., Kim, T. An Empirical Investigation of Credit Card Default August, 1999.

92. Dunis, C.L., Wiliams,

M.

Modelling and Trading the EUR/USD Exchange Rate: Do

Neural Network Models Perform Better?

February 2002

93.

Emmer, S., Tasche, D. Calculating credit risk capital charges with

the one-factor model

Volume 7/ Number 2, Winter 2005 URL:

www.thejournalofrisk.com 85-101

94.

Evangelopoulos, N. Dana Mining A Special Presentation for BCIS 4660

95. EXPERIAN Solving the mystery of credit

scoring models www.experian.com

96.

EXPERIAN LGD Scoring Overview Description, methods and

application

Decision Support Solutions LGD Scoring Overview 2002 Experian-Scorex

97.

Dvořáček, J., Sousedíková, R., Domaracká, L.

Industrial enterprises bankruptcy forecasting

METALURGIJA 47 (2008) 1, 33-36

98. Emel, A.B., Oral, M., Reisman, A., Yolalan,

A credit scoring approach for the commercial banking sector

Socio-Economic Planning Sciences 37 (2003) 103-123

R.

99. Evans, P., Flannery,

M.J., West, K.D. Journal of Money,Credit and

Banking Department of Economics,The

Ohio State University,1945. 100. Fair, I. LiquidCredit Decision engine LiquidCredit

101. Fair, I. Banks making credit too easy Business Courier, 11/27/98, Vol. 15 Issues 32

102. Fair, I. Credit Scoring in small

Business lending: Bane or Blessing?

Financel Update, Apr-Jun99, Vol. 12 Issue 2,pl,3p,1c

103. Fair, Isaac „Demystifies“ FICO Scores

104. Falbo, P. Credit-Scoring by Enlarged Discriminant Models

Omega Int.J. of Mgmt Sci., Vol.19 , No 4 pp. 275-289,

1991.

105. Feelders, A.J. Credit scoring and Reject Inference With Mixture

Models

International Journal of Intelligent System in

Accounting, Finance & Management 9, 1-8 (2000)

106. Feldman,R.

Small Business Loans, Small Banks and a Big Change in Technology Called Credit

Scoring

Region, Sep97, Vol. 11, Issue 3, p.18-24.

107. Fletcher, M. Decision making by Scottish bank managers

International Journal of Entrepreneurial Behaviour & Reserch, Vol. 1 No. 2, 1995

pp. 37-53.

108. Foglia, A., Laviola, S.,

Marullo Reedtz, P.

Multiple banking relationships and the fragility of corporate

borrowers

Journal of Banking & Finance 22 (1998) 1441-1456.

109. Freshbach, D.,

Schwinn, P. A Tactiacal Approach to Credit

Scores Mortgage Banking, Feb99, Vol.59 Issue 5, p46, 6p 8

graphs, 1map, 1c

110. Freer, J. Big Break from big banks South Florida Business journal , 03/14/97, Vol. 17 Issue 30,

p21, 2p, 1 cartoon.

111. Friedland, M. Credit scoring digs into data Credit World, May/Jun96, Vol. 84 Issue 5, p19, 5p

112. FairIsaac Understanding Your Credit

Score FairIsaac

113. FairIsaac Credit Scoring 101 Federal Trade Commission

July 22,1999

114.

Feelders, A.J. Credit Scoring and Reject Inference With Mixture

Models

Copyright Ó 2000 John Wiley & Sons, Ltd. Received 8

October 1999

115. Friedland, M. In any language, credit grantors say yes to scoring

Credit World , Sep/oct93, Vol. 82 Issue 1, p13, 4p

116. Galindo, J., Tamayo, P.

Credit Risk Assessment Using Statistical and Machine

Learning: Basic Methodology and Risk Modeling

Applications

Computational Economics, 15, 2000, p. 107-143.

117. Gallinger,G. W.

A Framework for Financial Statement Analysis Part 5:Prediction of Financial

Distress

Business Credit; Sep2000, Vol.102 Issue 8,p30, 4p, 3

charts

118. Gao, L., Zhou, C., Gao,

H. B., Shi, Y. R.

Credit Scoring Model Based on Neural Network with Particle

Swarm Optimization

National Basic Research Program of China,

No.2004CB719405 and the National Natural Science Foundation of China, No.

50305008. 119. Gayler, R. W. Comment: Classifier Statistical Science

Technology and the Illusion of Progress—Credit

Scoring

2006, Vol. 21, No. 1, 19–23

120. Gibson, M.S.

Measuring Counterparty Credit Exposure to a Margined

Counterparty

Finance and Economics Discussion Series, Divisions of Research & Statistics and

Monetary Affairs Federal Reserve Board,

Washington, D.C.

121. Giesecke, K. Default and Information Journal of Economic

Dynamics and Control, forthcoming

122. Glasserman, P., Kang, W., Shahabuddin, P

Large deviations in multifactor portfolio credit risk

Mathematical Finance, Vol. 17, No. 3 (July 2007), 345–

379

123. Gloy, B.A. Agricultural Finance Markets in Transition

Department of Applied Economics and Management,

College of Agriculture and Life Sciences

Cornell University, Ithaca, New York, 14853-7801

124. Gothe, P. Credit bureau point scoring sheds light on shades of gray

Credit world, May/Jun90, Vol.78 Issue 5, p 26, 4p

125. Gray, D.F., Merton,

R.C., Bodie, Z.

The Contingent Claims Approach to Measuring

Sovereign Risk

JOURNAL OF INVESTMENT

MANAGEMENT, Vol. 5, No. 4, (2007), pp. 5–28

126. Greene, W. Sample selection in credit-scoring models

Japan and World economy 10(1998) 299-316

127. Grieb, T., Hegji, C., Macroeconomic Factors, Journal of Economics and

Jones, S.T. Consumer Behavior, and Bankcard Default Rates

Finance, Vol. 25, No.3, 2001.

128. Guillen, M., Artis, M. Count Data Models for a credit scoring system

Third Meeting on the European Conference Series Quantitative Economics and

Econometrics on Econometrics of Duration,

Count and Transition Models. Paris,December, 10-11, 1992

129.

Glen, J.J. Dichotomous Categorical Variable Formation in

Mathematical Programming Discriminant

Analysis Models

Naval Research Logistics,

Vol. 51 (2004) 576-596

130.

Glennon D. Issues in Credit Scoring Risk Analysis Division Economics Department

The Office of the Comptroller of the Currency

131.

Glossner, P. Calculating Basel II Risk Parameters

for a Portfolio of Retail Loans

Mathematical Finance 12th of April, 2003

132.

Global Financial Markets

International Finance Corporation

Making Small Business Finance Profitable

Challenges and Opportunities for Financial Institutions

133.

Glossner, P. Calculating Basel II Risk Parameters

for a Portfolio of Retail Loans

Mathematical Finance 12th of April, 2003

134.

Grenne, W.H. A Statistical Model for Credit Scoring

Department of Economics Stern School of Business

New York University

100 Trinity Place New York, NY 10006

April 8, 1992

135.

Gupta, N.D.J., Smith, A.K.

Neural networks in business: techniques and applications for

the operations researcher

Computers & Operations Research 27 (2000)

1023}1044

136. Habal, H. Credit scoring questioned as minority loan criterion

American Banker, 12/03/98, Vol.163 Issue 230, p12 , 1/2p,

1bw

137. Hackbarth, D., Miao,

J., Morellec, E.

Capital structure, credit risk, and

macroeconomic conditions

Journal of Financial Economics 82 (2006) 519–550

138. Hamerle, A., Rösch, D. Misspecified Copulas in Credit

Risk Models:How Good is Gaussian?

Journal of Risk 8 (1), 2005, pp. 41-58

139.

Hamerle, A., Knapp, M., Liebig, T., Wildenauer, N.

Incorporating prediction and estimation risk in point-in-time

credit portfolio models

Discussion Paper Series 2: Banking and

Financial Studies, No 13/2005

140. Hancock, S. Developing a more accurate and efficient scorecard

Credit Control, 1999, Vol.20 Issue 8, p10, 6p

141. Hand, D.J. Marginal classifier

improvement and reality Imperial College London

May 2004.

142.

Hand, D.J. Good Practice in

Retail Credit Scorecard Assessment

Imperial College London September, 2003

143. Hand, D.J. Good practice in retail credit scorecard assessment

Journal of the Operational Research Society (2005) 56,

1109-1117

144. Hand, D.J. New uses of Statistics in Retail Banking

American Journal of Mathematical and

management Sciences

145. Hand, D.J., Heneley,

W.E.

Statistical Classification Methods in Consumer Credit

Scoring:a Review

J.R. Statistical Society A (1997), 160, Part 3, pp. 523-

541.

146. Hand, D.J., Kelly, M.G. Lookahead scorecards for new fixed term credit products

Journal of the Operational research Society, 52, 989-996.

147. Hand, D.J., Till, R. J.

A simple generalisation of the area under the ROC curve for multiple class classification

problems

Machine Learning, 45, 171-186.

148.

Hand, D. J., McConway, K.J., Stanghellini, E.

Graphical models of applicants for credit

IMA Journal of Mathematics Applied in Bussines &

Industry (1997) 8 , 143 - 155

149. Hand, D. J., Adams, N.

M.

Defining attributes for scorecard construction in credit

scoring

Journal of Applied Statistics, Vol. 27, No. 5, 2000, 527 -

540

150. Hanson, S., Pesaran,

M.H., Schuermann, T. Scope for Credit Risk

Diversification

IEPR WORKING PAPER 05.18, INSTITUTE OF ECONOMIC POLICY

RESEARCH, UNIVERSITY OF SOUTHERN CALIFORNIA

151. Hardle, W., Mammen,

E., Muller, M.

Testing Parametric versus Semiparametric Modeling in Generalized Linear Models

June 9,1998

152. Harney, K.R. Fannie Mae Issues New Rules

for Lenders Using Credit Scores

San Antonio Business Journal, Vol. 11, No. 8, 1997, p. 10b-

11b.

153. He, Y., Kamath, R.,

Meier, H. H.

An empirical evaluation of bankruptcy prediction models for small firms: An over-the-

Academy of Accounting and Financial Studies Journal,

Volume 9, Number 1, 2005.

counter market experience

154. Healy, T.J. The new science of borrowing Behaviour

Mortgage Banking, Feb98, Vol. 58 Issue 5 , p27, 7p, 2 charts, 1 diagram, 7 graphs

155. Henley, W.E., Hand,

D.J.

A k-nearest-neighbour classifier for assessing consumer credit risk

The Statistician (1996) 45. No. 1 pp 77-95

156. Henry, J. AmeriCredit secret: Credit scoring

Automotive News,=7/27/98, Vol.72 Issue 5777, p24, 3/5p,

1c.

157.

Hilbers, P., Otker-Robe, I., Pazarbasioglu,

C., Johnsen, G.

Assessing and Managing Rapid Credit Growth and the Role of

Supervisory and Prudential Policies

IMF Working Paper, Monetary and Financial

Systems Department

158. Hsieh, N. C. An integrated data mining and behavioral scoring model for

analyzing bank customers

Expert System with Applications 27 (2004) 623-

633

159. Hsieh, N. C. Hybrid mining approach in the design of credit scoring models

Expert System with Applications 28 (20059 655-

665

160. Huang, C.L., Chen, M.C., Wang, C.J.

Credit scoring with a data mining approach based on support vector machines

Expert Systems with Applications xxx (2006) xxx–

xxx

161. Huang, J.J., Tzeng,

G.H., Ong, C.S.

Two-stage genetic programming (2SGP)

for the credit scoring model

Applied Mathematics and Computation xxx (2005) xxx–

xxx

162.

Hansen, E., Pullen, A., Zattler, M.

Benefiting from Basel II Turning uncertainty to market

advantage

IBM Business Consulting Services

July 2003

163. Hanson, S.,

Schuermann, T. Federal Reserve Bank of New

York Staff Report no. 190

July 2004

Staff Reports

164.

Hayden, E. Are Credit Scoring Models Sensitive With Respect to

Default Definitions? Evidence from the

Austrian Market

February 2003

165.

Hoch, P. Academy Curriculum 2004

Your partner for the training

YOUneed

MasterCard International

166. Holton, G.A. Defining Risk 19-25, F.A.J. Vol.60, No.6,

2004.

167. Honohan, P. Risk management and the costs

of the banking crisis http://ner.sagepub.com

168. Hull, J., White, A. Valuing Credit Derivatives Using an Implied Copula

Approach

Journal of Derivatives, Fall 2006

169. Jacobson, T., Roszbach, K.

Bank lending policy, credit scoring and Value at Risk 30 July 1998

170. Jayagopal, B. Applying Data Mining

Techniques to Credit Scoring Amadeus Software Limited

VIEWS 2004

171. Jayagopal, B. Applying dana MIning

Techniques to Credit Scoring Amadeus Software Limited

172.

Jacobson, T., Linde, J., Roszbach, K.

Credit risk vs. capital requirements under Basel II:

are SME loans and retail credit really different?

Sveriges Riksbank

173.

Jones, D., Mingo, J., Gray, B., Wilson, T.C., Nishiguchi, K., Kawai,

Credit Risk Modeling Summary of Presentation

H., Sazaki, T.

174. Jorion, P., Zhang, G.

Good and Bad Credit Contagion:

Evidence from Credit Default Swaps

Forthcoming, Journal of Financial Economics

175. Jost, A. Neural Networks Credit World, Vol. 81, No. 4, 1993, p. 26-35

176. Kapliński, O. Usefulness and credibility of

scoring methods in construction industry

Journal of Civil Engineering and Management, 2008, 14(1):

21–28

177.

Kaynak, E., Kucukemiroglu, O.,

Ozmen, A.

Correlates of credit card acceptance and usage in an

advanced developing Middle Eastern country

Journal of Services Marketing Vol.9, No. 4, 1995, pp. 52-63.

178. Kealhofer, S. Quantifying Credit Risk II: Debt Valuation

Financial Analysts Journal, January 2003.

179.

Kelly, M.G., Hand, D.J. Credit Scoring with Uncertain

Class Definition

IMA Journal of Mathematics Applied in Business &

Industry, 10, 1999, p. 331-345.

180. Kiefer, N.M., Larson,

C.E.

Specification and Informational Issues in Credit

Scoring CAE Working Paper #06-11

181. Kim, J., Kim, K. Loss Given Default Modelling under the Asymptotic Single

Risk Factor Assumption

MPRA Paper No. 860, posted 07. November 2007 / 01:21

182. Kim, Y. S., Sohn, S. Y. Managing loan customers

using misclassification patterns of credit scoring model

www.elsevier.com , 2003.

183. Kim, H., Gu, Z. Predicting Restaurant

Bankruptcy: A Logit Model in Comparison with a

Journal of Hospitality & Tourism Research, Vol. 30, No. 4, November 2006, 474-

Discriminant Model 493

184. Korn, D.J. Learn how your credit rating can get you credit easier and

faster Black Enterprise August 1998.

185. Kovačević, J. Analiza kreditne sposobnosti Ekonomski analitičar, Zagreb,1992, p. 44-54.

186. Kovačević, J. Prilog analizi kreditne sposobnosti

Financijska praksa 15, 1991, p. 23-42.

187. Kumar, A., Motwani, J. Reengineering the lending

procedure for small businesses:a case study

Volume 48 Number 1 1999 pp 6-12.

188.

Karp, A.H. USING LOGISTIC REGRESSION TO PREDICT CUSTOMER RETENTION

Sierra Information Services, Inc.

San Francisco, California USA

189.

Kiss, F. CREDIT SCORING PROCESSES FROM A

KNOWLEDGE MANAGEMENT PERSPECTIVE

PERIODICA POLYTECHNICA SER. SOC. MAN. SCI. VOL. 11, NO. 1,

PP. 95–110 (2003)

190.

Kofman,J. THE BENEFITS OF BASEL II AND THE PATH TO

IMPROVED FINANCIAL PERFORMANCE

REVISED: JANUARY 14, 2004

191. Komorad, K. On Credit Scoring Estimation Berlin, December 18, 2002

192.

Kreidler, M. Effect of Credit Scoring on Auto Insurance

Underwriting and Pricing

January 2003

193.

Krieger, S. Directly Optimizing the Area under the ROC Curve in Credit Scoring Models:

Selection and Best Linear

LMU, June 17, 2004

Combination of Predictor Variables

194. Latković, M. Upravljanje rizicima:

Identifikacija, mjerenje i kontrola

Financijska teorija i praksa 26 (2) str. 463-477, 2002.

195. Lee,W.A. Fair, Isaac Web Site Offering Explanation of Credit Scores

American Banker, Vol.165, Issue 219, 2000, p.7-9.

196. Lee, T.S., Chiu, C.C.,

Lu, C.J., Chen, I.F. Credit scoring using the hybrid neural discriminant technique

Expert Systems with Applications 23 (2002) 245-

254

197. Leonard, K.J. Empirical Bayes analysis of the

commercial loan evaluation process

Volume 18, Issue 4 , 9 November 1993 , Pages 289-

296

198. Leonard, K.J. The Development of credit

scoring quality measures for consumer credit applications

International Journal of credit scoring quality measures for consumer credit applications

199. Leonard, K.J. Information systems and

benchmarking in the credit scoring industry

BQM&T 3,1

200. Leung, W.K., Lai, K.K. Improving the quality of the credit authorization approach

International Journal of Service Industry Management, Vol. 12, No. 4, 2001, pp. 328-

341.

201. Li, H. G., Hand, D. J., Direct versus Indirect Credit Scoring Classifications December 2001.

202. Lim, M.K., Sohn, S.Y. Cluster-based dynamic scoring model

Expert System with Applications 32 (2007) 427-

431

203. Lin, Y. Improvement on behavior

scores by dual-model scoring system

International Journal of Information Technology &

Decision Making, Vol. 1, No.

1 (2002) 153-164

204. Liu, Y. New Issues in Credit Scoring Application Arbeitsbericht Nr. 16/2001

205.

Lai, K.K. Credit Granting: Challenges

and Solution Approaches

Faculty of Business

City University of Hong Kong December 2003

206.

Laitinen, K.E. Predicting a corporate credit analyst’s risk estimate by logistic and linear models

International Review of Financial Analysis 8:2 (1999) 97–121

207.

Langeheine, R., Rost, J. A Guide through Latent Structure Models for

Categorical Data

Chapter 1, 13-37

208.

Leonard, J.K., Sheather, S.J.

The Development of Delinquency and Collection

Credit Bureau Scores

SCORE

209.

Leonard, J.K. The Development of Delinquency and Collection

Credit Bureau Scores

Credit scoring quality

measures, November 1993., 79-85

210. Lien Y-L., Liu, Y-L.,

Liu, W., Tsaih, R. Credit scoring system for small

business loans Decision Support Systems xx

(2003) xxx– xxx

211. Lotz, C., Schlogl, L. Default risk in a market model Journal of Banking & Finance 24 (2000) 301-327

212. Madeira, S.C., Oliveira, A.L., Conceição, C.S.

A Data Mining Approach to credit Risk Evaluation and

Behaviour Scoring

EPIA 2003, LNAI 2902,pp.184-188, 2003.

213. Malhotra, R., Malhotra,

D.H. Evaluating consumer loans

using neural networks Omega 1 (2003) 83 - 96

214. Mann, R.J. The Role of Secured Credit in Small-Business Lending

The Georgtown Law Journal, Vol.86, Num.1, October, 1997,

p. 1-44.

215. Mitchell, J., Van Roy,

P.

Failure prediction models : performance, disagreements, and internal rating systems

NBB WORKING PAPER No. 123 - DECEMBER 2007

216. Morns, R. Credit scoring and small business loans

Federal Reserve Bank of Minneapolis Spring 1997.

217. Morrison, J.S. Preparing for Basel II: Part 4 The RMA Journal, July/August 2004

218.

Marinopoulos, J. Credit Scoring Development and Methods

Head of Retail Decision Model

13/11/2008

219.

Matsatsinis, F.N. CCAS: An Intelligent Decision Support Systemfor

Credit Card Assessment

JOURNAL OF MULTI-CRITERIA DECISION

ANALYSIS J. Multi-Crit. Decis. Anal. 11:

213–235 (2002)

220.

McDonough, W.J. 4th Annual Risk Management Convention and Exhibition & the GARP Financial Risk

Manager of the Year Awards

GARP, FEBRUARY 1O – 13, 2003 MILLENNIUM

BROADWAY, NEW YORK

221.

Mester, J.L. What’s the Point of Credit Scoring?

BUSINESS REVIEW SEPTEMBER/OCTOBER

1997

222.

Mikulčić, D. Value at Risk ( Rizičnost vrijednosti)

Teorija i primjena na meñunarodni portfelj

instrumenata s fiksnim prihodom

Hrvatska narodna banka, P – 7, kolovoz 2001.

223. Musto, D., Souleles, A Portfolio View of Consumer March 16, 2005

S.N. Credit*

224. N.A.

D&B DecisionMaker Now available Via Internet,

Customized credit decision tool translates information into uniform actinable decision

Business Wire, 03/20/2000

225. N.A. Credit Scoring Models should be revised for Internet Card

offers

Philips Business Information Highlights 04/06/2000

226. Noe,J. Credit Scoring, America's Community Banker

Aug97, Vol.6, Issue 8, p. 29-36.

227. Noh, H.J., Roh, T.H.,

Han, I.

Prognostic personal credit risk model considering censored

information

Expert system with Applications 28 (2005) 753-

762

228. Ochs, J.R., Parkinson,

K.L. Credit Managers Talk

Technology Business Credit, Vol. 101, No.

1, 1999, p. 54-57.

229. OCC Bulletin Risk Modeling Model Validation

May 30, 2000

230.

Olszak, M.C., Ziemba, E.

Business Intelligence Systems in the Holistic Infrastructure

Development Supporting Decision-Making

in Organisations

Interdisciplinary Journal of Information, Knowledge, and Management Volume 1, 2006,

47-58

231.

Ozdemir, O. EXAMINING CREDIT DEFAULT RISK: AN EMPIRICAL STUDY ON

CONSUMER CREDIT CLIENTS

Yeditepe University Levent Boran, Koçbank

232. Ong, C.S., Huang, J.J.,

Tzeng, G.H. Building credit scoring models

using genetic programming Expert System with

Applications 29, (2005) 41-47 233. Ozden G., Wallace W. Classifying delinquent Interantional Journal of

A. customers for credit collections: an application of

probabilistic inductive learning

Human-Computer Studies, Volume 42, Issue 6, June

1995, p.633-646.

234. Padhi, M.S., Woosley, L. W., Srinivasan, A.

Credit Scoring and Small Business Lending in Low-and

Moderate-income Communities

Federal Reserve Bank of Atlanta

235. Peek, J., Rosengren,

E.S. The Evolution of Bank

Lending to Small Business

New England Economic Review, Mar/Apr 1998, p. 27-

37.

236.

Pesaran, M.H., Schuermann, T.,

Treutler, B.J., Weiner, S.M.

Macroeconomic Dynamics and Credit Risk: A Global

Perspective

Journal of Money, Credit and Banking, April, 2005

237. Piramuthu,S. Financial Credit-risk

Evaluation with Neural and Nerofuzzy Systems

European Journal of Operational Research, 112,

1999, p.310-312

238. Prajago, D.I., Sohal,

A.S.

The relationship between organization strategy, total quality management and

organization performance-the mediating role of TQM

European Journal of Operational Research 168

(2006) 35-50

239.

Paper, W., Rashid, A. CREDIT SCORING Smart Decisions for Challenging Times

Copyright ©2003 Magnum Communications, Limited,

August 6,2003

240.

Pluto, K., Tasche, D. Estimating Probabilities of Default for Low Default

Portfolios

July 28, 2005

241.

Pritchard, J. Implementing Basel II in the Norwich and

Peterborough Building Society

Journal of Financial Regulation and Compliance,

Vol. 12, No. 3,2004, pp. 240–

247# Henry Stewart Publications, 1358–1988

242.

Saita,F. MEASURING RISK-ADJUSTED

PERFORMANCES FOR CREDIT RISK

Working Paper N. 89/03 March 2003

243.

SAS SAS® Credit Scoring for Telecommunications

A component of SAS® Telecommunications Intelligence Solutions

www.sas.com

244.

SAS SAS® Credit Scoring for Banking

Faster, cheaper, more flexible scoring for confident decisions

www.sas.com

245.

Savillo, J. Behavior Scoring for Collections

12th Annual Credit Card Collections Conference Oct 15 - Oct 17, 2003

246.

Scallan, G. BAD DEBT PROJECTION MODELS

An Overview of Modeling Approaches

February 1998 - v1.1, Score plus

247. Scheper, P. FICO Scoring 101 www.LoanLinkOC.com

248.

Schumann, M. New Issues in Credit Scoring Application

Georg-August-Universität Göttingen Institut für

Wirtschaftsinformatik

249.

Schumann, M. A framework of data mining application

process for credit scoring

Georg-August-Universität Göttingen Institut für

Wirtschaftsinformatik

250.

Schumann, M. The evaluation of classification models for credit scoring

Georg-August-Universität Göttingen Institut für

Wirtschaftsinformatik

251.

SCOREPLUS, Scallan, G.

Credit Scoring, Modelling and Data Issues

What should scoring do?

Pinners’ Hall - London 19 October 2001

252.

Sobehart, R.J., Keenan, S.C., Stein, M.R.

Benchmarking Quantitative Default Risk

Models: A Validation Methodology

Moody’s Rating Methodology, March 2000

253. SOLID Partners Finance SOLID Partners, Keyrus

Group 254. Star Card Star Card Asset Soft

255.

Stanghellini, E. Monitoring the Behaviour of Credit

Card Holders with Graphical Chain

Models

Journal of Business Finance & Accounting, 30(9) & (10),

Nov./Dec. 2003, 0306-686X, 1423-1435

256.

Stein, P. Making Small Business Finance Profitable

The Importance of Credit Information and Credit Scoring

in Small Business Lending

Global Financial Markets Group

Bangkok, December 3, 2001

257.

Strategic Consultancy Partnership

Monaco

New Basel Capital Accord Survey

Are Retail Banks prepared to meet the

requirements for the Internal Rating

2002 Scorex

Based approach?

258. Sinnock. B. Fair Issac Site Offers credit Score Details

National Mortgage News, 11/06/2000, Vol. 25 Issue

8,p6, 1/5p.

259. Sobehart, J., Keenan, S. Measuring default accurately Credit Risk special report, March 2001.

260. Sohn, S. Y., Moon, T.

H., Kim, S. Improved technology scoring

model for credit guarantee fund www.elsevier.com , 2005.

261. Sohn, S. Y., Shin, H.W. Reject inference in credit

operations based on survival analysis

Expert System with Applications xx(2005) 1-4

262. Somerville, M.T. Scoring and the Small Business Lender

Commercial Lending Review, Vol. 12, Issue 3, 1997, p. 62-

65.

263.

Sookhanaphibarn, K., Polsiri, P., Choensawat,

W., Lin, F. C.

Application of Neural Networks to Business

Bankruptcy Analysis in Thailand

International Journal of Computational Intelligence Research, ISSN 0973-1873

Vol.3, No.1 (2007), pp. 91–96

264. Stern, L. Learning the Score Newsweek, Vol.136, Issue 20, 2000, p. 92-94.

265. Stanghellin, E. A discrete variable chain graph for applicants for credit

Appl. Statist. (1999) 48. Part 2, pp. 239 - 251

266. Sun, L.

A re-evaluation of auditors’ opinions versus statistical

models in bankruptcy prediction

Springer Science + Business Media, Published online: 15

November 2006

267. Swicegood, P., Clark,

J.A.

Off-site Monitoring System for Predicting Bank

Underperformance: A Comparison of Neural

Networks, Discriminant

International Journal of Intelligent Systems in

Accounting, Finance & Management 10, 169-186

(2001)

Analysis, and Professional Human Judgment

268. Tarashev, N.A. An Empirical Evaluation of Structural Credit Risk Models BIS Working Papers, No 179

269. Taylor, I., McCoy-Pinderhughes, P. Credit Scoring gets an 'A' Balck Enterprise, Nov2000,

Vol. 31, p57, 2/3p.

270. Thomas, L. C.

A survey of credit and behavioural scoring:

forecasting financial risk of lending to consumers

International Journal of Forecasting 16 (2000) 149-172

271. Thomas, L. C., Ho, J.,

Scherer, W.T.

Time will tell: Behavioural scoring and the dynamics

consumer credit assessment

IMA Journal of Management Mathematics (20019 12, 89-

103

272. Thomas, L. C., Oliver,

R.W., Hand, D.J.

A Survey the issues in Consumer Credit Modelling

Research

Journal of the Operational Research Society (2005) 56,

1006-1015

273. Tierney, M.F., Truglio,

P.M.

Case Study: How Fleet Bank Uses Credit Scoring for Small

Businesses

Commercial Lending Review, Vol. 12, Issue 4, 1997, p. 47-

49. 274. Timmons, H. The Craks in credit scoring Academic Search Premier

275. Tintor, J. Potraživanja, kreditna sposobnost i zarada

Poslovna analiza i upravljanje, Zagreb, 1996, p. 3-8.

276. Tsaih, R., Liu, Y.J., Liu, W., Lien, Y. L.

Credit scoring system for small business loans

Decision Support System 38 (2004) 91-99

277.

Thomas, L.C. Consumer Credit Modelling: Context and Current Issues

School of Management, University of Southampton,

Southampton, UK

278.

Thomas, L.C., Jung, M.K., Thomas, S.D.,

Wu, J.

MODELING CONSUMER ACCEPTANCE

PROBABILITIES

School of Management, University of Southampton,

Southampton, UK,SO17 1BJ, UK

Department of Informational Statistics, Kyungsung

University, Busan 608-736,South Korea

279.

Topping, S. City University of Hong Kong Professional Seminar on

Latest Perspective on Basel II

Hong Kong Monetary Authority

19 July 2004

280.

Van den Poer, D., Verstraeten, G.

The Impact of Sample Bias on Consumer Credit

Scoring Performance and Profitability

Department of Marketing, Ghent University,

Hoveniersberg 24, 9000 Ghent, Belgium

281.

Van den Poel, D. Data Mining for Customer Relationship

Management

Ghent University, Dept. of Marketing, Belgium

282. Vasicek, A.Q. Credit Valuation KMV, March 22, 1984

283.

Vogelgesang, U. Microfinance in Times of Crisis: The Effects of Competition, Rising

Indebtedness, and Economic Crisis on Repayment Behavior

World Development Vol. 31, No. 12, pp. 2085–2114, 2003

284. Van Order, R. Modeling the Credit Risk of Mortgage Loans: A Primer

Ross School of Business Working Paper Series,

Working Paper No. 1086, January 2007

285. Varetto, F. Genetic algorithms

applications in the analysis of insolvency risk

Journal of Banking & Finance 22 (1998) 1421-1439.

286.

Van den Poer, D., Verstraeten, G.

The Impact of Sample Bias on Consumer Credit

Scoring Performance and Profitability

Department of Marketing, Ghent University,

Hoveniersberg 24, 9000 Ghent, Belgium

287.

Van den Poel, D. Data Mining for Customer Relationship

Management

Ghent University, Dept. of Marketing, Belgium

288. Vasicek, A.Q. Credit Valuation KMV, March 22, 1984

289.

Vogelgesang, U. Microfinance in Times of Crisis: The Effects of Competition, Rising

Indebtedness, and Economic Crisis on Repayment Behavior

World Development Vol. 31, No. 12, pp. 2085–2114, 2003

290. Verstraeten, G., Van

den poel, D. The Impact of Sample Bias on

Consumer Credit Scoring Working Paper, 3/2004.

291.

Whittaker, J., Whitehead, C, Souers,

M.

The neglog transformation and quantile regression

for the analysis of a large credit scoring database

Appl. Statist. (2005) 54, Part 5, pp. 863–878

292. Wagner, C. A credit decision making and risk monitoring tool

Credit Risk international, January 2003.

293. Weiss, L. A., Capkun,

V.

The Impact of Incorporating the Cost of Errors into

Bankruptcy Prediction Models 14th March 2005.

294. West, D. Neural network credit scoring models

Computers & Operations Research 27 (2000) 1131-1152

295. West, D., Dellana, S.,

Qian, J.

Neural network ensemble strategies for nfinancial

decision applications

Computers & Operations Research 32 (2005) 2543-2559

296. Whiteman, L. Banks Say One-on-One Beats Credit Scoring Models

American Banker, 10/08/98, Vol.163 Issue 193, p13 , 1/4p.

297. Wilkinson, K. Lenders want to know your score before granting loans

New Orleans CityBusiness, 05/22/2000, Vol.20 Issue 48,

p29, 3p, 1bw 298. Worthington, S., A new relationship marketing International Journal of Bank

Horne, S. model and its application in the affinity credit card market

Marketing 1671 (1998) 39-44

299. Yin,W., Devaney,

Sharon, a.

A Comparison of Two Credit Scoring Models: Commercial versus Consumer Education

Consumer Interests Annual, 1999 Issue 45, p136, 1p

300. Zadnik Stirn, L.

Multivariate and multi-criteria methods for selection and evaluation of sustainable development investment

project's decicions

Operational Research Proceedings KOI 2002, 261-

273

301. Zeitun, R., Tian, G.,

Keen, S.

Default Probability for the Jordanian Companies: A Test

of Cash Flow Theory

International Research Journal of Finance and Economics,

ISSN 1450-2887 Issue 8 (2007)

![Tehničke Informacije - Tehnicke informacije.pdf · EcoPole Tehničke Informacije EcoPole Asortiman Proizvoda Specifikacije EP180 EP225 EP300 Dužina [m] Težina [kg] Maks. opterećenje](https://img.pdfslide.us/doc/110x75/5ecf6b9e1a8329501b59beff/tehnike-informacije-tehnicke-informacijepdf-ecopole-tehnike-informacije.jpg)