Embed Size (px)

Citation preview

1

RBC Investor RoadshowNovember 18, 2015

2

Safe Harbor Statements

Forward Looking Statements: This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, Section 21E of the Securities Exchange Act of 1934 and applicable Canadian securities laws conveying management's expectations as to the future based on plans, estimates and projections at the time the Company makes the statements. Forward-looking statements involve inherent risks and uncertainties and the Company cautions you that a number of important factors could cause actual results to differ materially from those contained in any such forward-looking statement. The forward-looking statements contained in this presentation include, but are not limited to, statements related to expected future operating results of the Company, the potential impact the acquisition of DSS Group, Inc. will have on the Company and the estimated synergies resulting from such transaction. The forward-looking statements are based on assumptions regarding management's current plans and estimates. Management believes these assumptions to be reasonable but there is no assurance that they will prove to be accurate. Factors that could cause actual results to differ materially from those described in this presentation include, among others: (1) changes in estimates of future earnings; (2) expected synergies and cost savings are not achieved or achieved at a slower pace than expected; (3) integration problems, delays or other related costs; and (4) unanticipated changes in laws, regulations, or other industry standards affecting the companies. The foregoing list of factors is not exhaustive. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Readers are urged to carefully review and consider the various disclosures, including but not limited to risk factors contained in the Company's Annual Report in the Form 10-K for the year ended January 3, 2015 and its quarterly reports on Form 10-Q, as well as other periodic reports filed with the securities commissions. The Company does not, except as expressly required by applicable law, undertake to update or revise any of these statements in light of new information or future events.

Non-GAAP Measures: The Company routinely supplements its reporting of GAAP measures by utilizing certain non-GAAP measures to separate the impact of certain items from its underlying business results. In this presentation, we use non-GAAP measures such as EBITDA, adjusted EBITDA, adjusted free cash flow and adjusted free cash flow yield and certain ratios using these measures. Since the Company uses these non-GAAP measures in the management of its business, management believes this supplemental information, including on a pro forma basis, is useful to investors for their independent evaluation and understanding of the business. Any non-GAAP financial measures used by the Company are in addition to, and not meant to be considered superior to, or a substitute for, the Company's financial statements prepared in accordance with GAAP. In addition, the non-GAAP financial measures included in this presentation reflects management's judgment of particular items, and may be different from, and therefore may not be comparable to, similarly titled measures reported by other companies. A reconciliation of this non-GAAP measure may be found on www.cott.com.

3

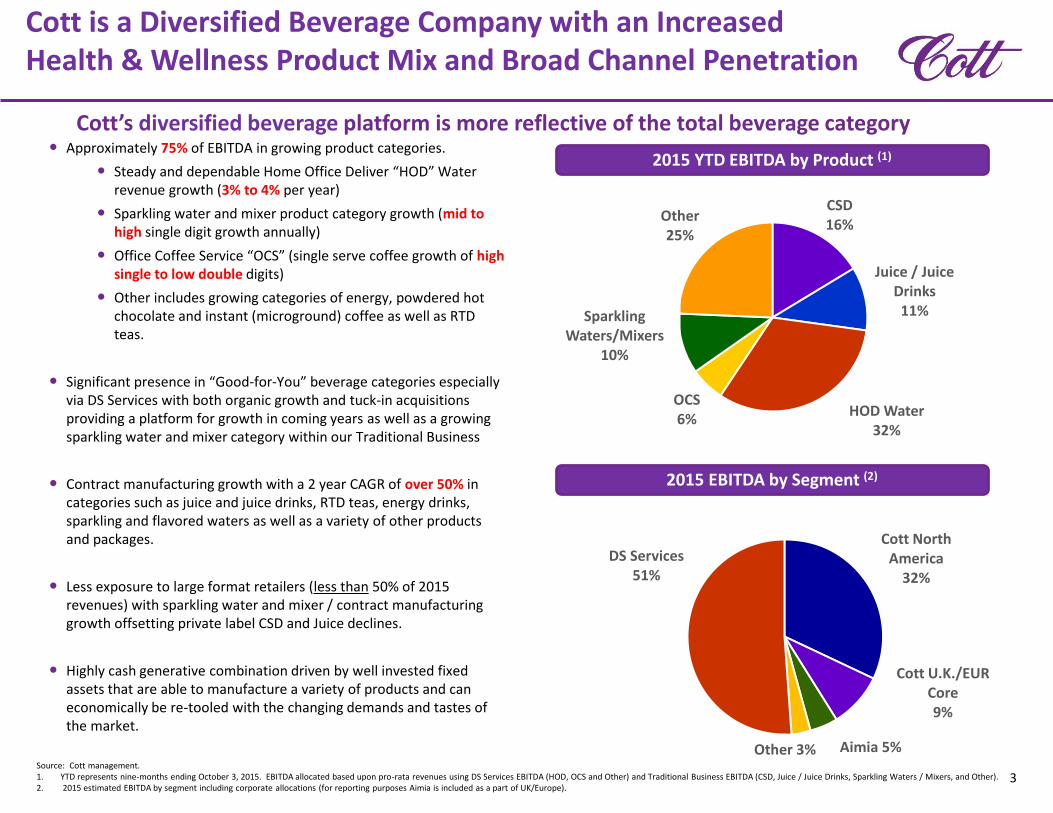

Cott is a Diversified Beverage Company with an Increased Health & Wellness Product Mix and Broad Channel Penetration

2015 YTD EBITDA by Product (1) Approximately 75% of EBITDA in growing product categories.

Steady and dependable Home Office Deliver “HOD” Water revenue growth (3% to 4% per year)

Sparkling water and mixer product category growth (mid to high single digit growth annually)

Office Coffee Service “OCS” (single serve coffee growth of high single to low double digits)

Other includes growing categories of energy, powdered hot chocolate and instant (microground) coffee as well as RTD teas.

Significant presence in “Good-for-You” beverage categories especially via DS Services with both organic growth and tuck-in acquisitions providing a platform for growth in coming years as well as a growing sparkling water and mixer category within our Traditional Business

Contract manufacturing growth with a 2 year CAGR of over 50% in categories such as juice and juice drinks, RTD teas, energy drinks, sparkling and flavored waters as well as a variety of other products and packages.

Less exposure to large format retailers (less than 50% of 2015 revenues) with sparkling water and mixer / contract manufacturing growth offsetting private label CSD and Juice declines.

Highly cash generative combination driven by well invested fixed assets that are able to manufacture a variety of products and can economically be re-tooled with the changing demands and tastes of the market.

Source: Cott management.1. YTD represents nine-months ending October 3, 2015. EBITDA allocated based upon pro-rata revenues using DS Services EBITDA (HOD, OCS and Other) and Traditional Business EBITDA (CSD, Juice / Juice Drinks, Sparkling Waters / Mixers, and Other).2. 2015 estimated EBITDA by segment including corporate allocations (for reporting purposes Aimia is included as a part of UK/Europe).

Cott’s diversified beverage platform is more reflective of the total beverage category

CSD16%

Juice / Juice Drinks11%

HOD Water32%

OCS6%

Sparkling Waters/Mixers

10%

Other25%

2015 EBITDA by Segment (2)

Cott North America

32%

Cott U.K./EUR Core9%

Aimia 5%Other 3%

DS Services51%

4

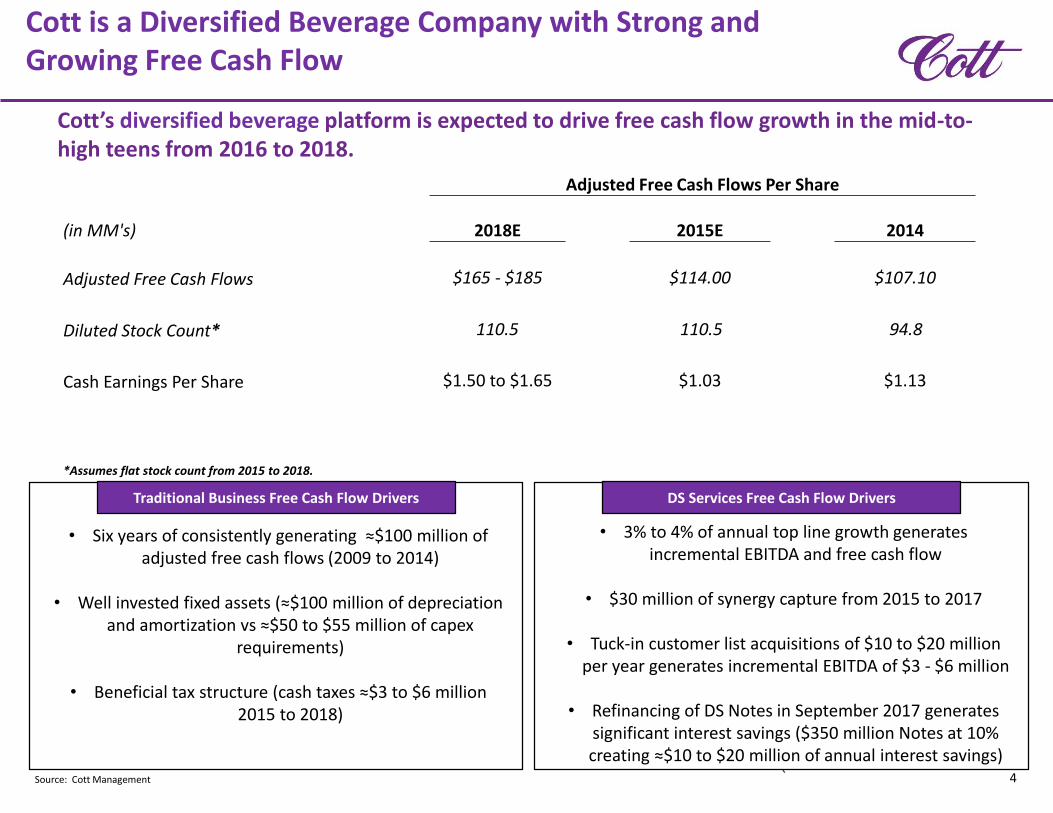

Cott is a Diversified Beverage Company with Strong and Growing Free Cash Flow

Cott’s diversified beverage platform is expected to drive free cash flow growth in the mid-to-high teens from 2016 to 2018.

Adjusted Free Cash Flows Per Share

(in MM's) 2018E 2015E 2014

Adjusted Free Cash Flows $165 - $185 $114.00 $107.10

Diluted Stock Count* 110.5 110.5 94.8

Cash Earnings Per Share $1.50 to $1.65 $1.03 $1.13

*Assumes flat stock count from 2015 to 2018.

Traditional Business Free Cash Flow Drivers

• Six years of consistently generating ≈$100 million of adjusted free cash flows (2009 to 2014)

• Well invested fixed assets (≈$100 million of depreciation and amortization vs ≈$50 to $55 million of capex

requirements)

• Beneficial tax structure (cash taxes ≈$3 to $6 million 2015 to 2018)

DS Services Free Cash Flow Drivers

• 3% to 4% of annual top line growth generates incremental EBITDA and free cash flow

• $30 million of synergy capture from 2015 to 2017

• Tuck-in customer list acquisitions of $10 to $20 million per year generates incremental EBITDA of $3 - $6 million

• Refinancing of DS Notes in September 2017 generates significant interest savings ($350 million Notes at 10% creating ≈$10 to $20 million of annual interest savings)

`Source: Cott Management

5

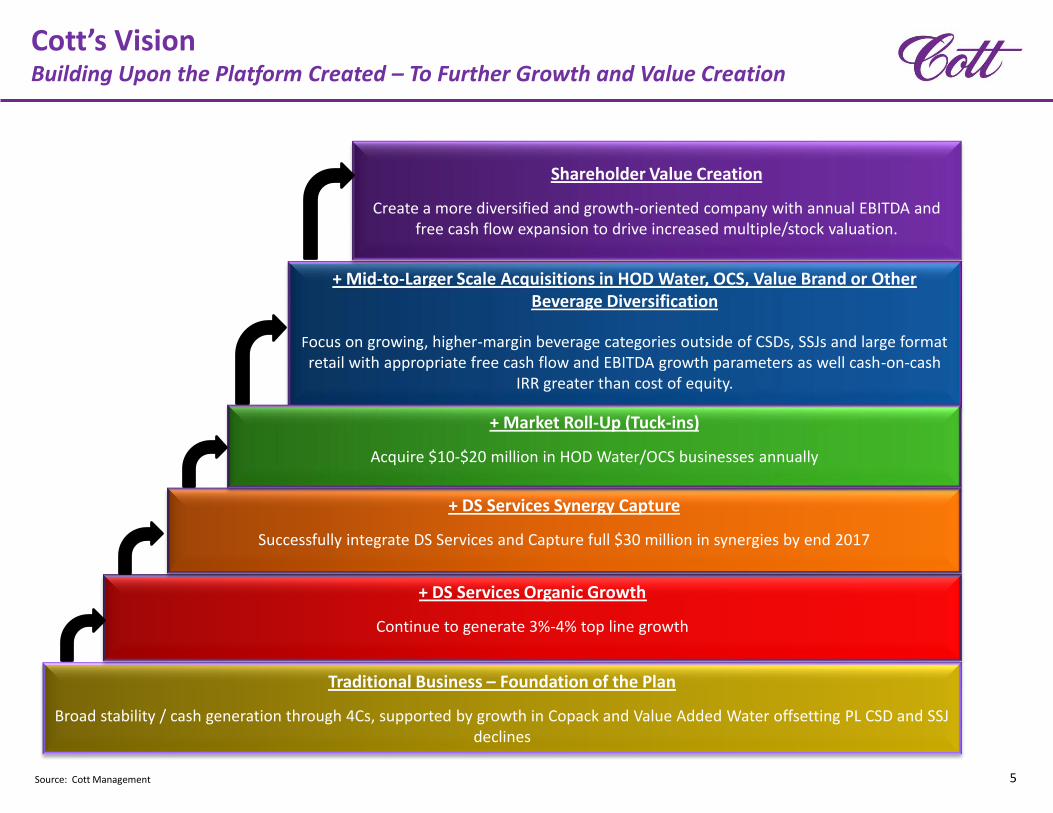

Cott’s VisionBuilding Upon the Platform Created – To Further Growth and Value Creation

Traditional Business – Foundation of the Plan

Broad stability / cash generation through 4Cs, supported by growth in Copack and Value Added Water offsetting PL CSD and SSJ declines

+ DS Services Organic Growth

Continue to generate 3%-4% top line growth

+ Mid-to-Larger Scale Acquisitions in HOD Water, OCS, Value Brand or Other Beverage Diversification

Focus on growing, higher-margin beverage categories outside of CSDs, SSJs and large format retail with appropriate free cash flow and EBITDA growth parameters as well cash-on-cash

IRR greater than cost of equity.

Shareholder Value Creation

Create a more diversified and growth-oriented company with annual EBITDA and free cash flow expansion to drive increased multiple/stock valuation.

+ DS Services Synergy Capture

Successfully integrate DS Services and Capture full $30 million in synergies by end 2017

+ Market Roll-Up (Tuck-ins)

Acquire $10-$20 million in HOD Water/OCS businesses annually

Source: Cott Management

6

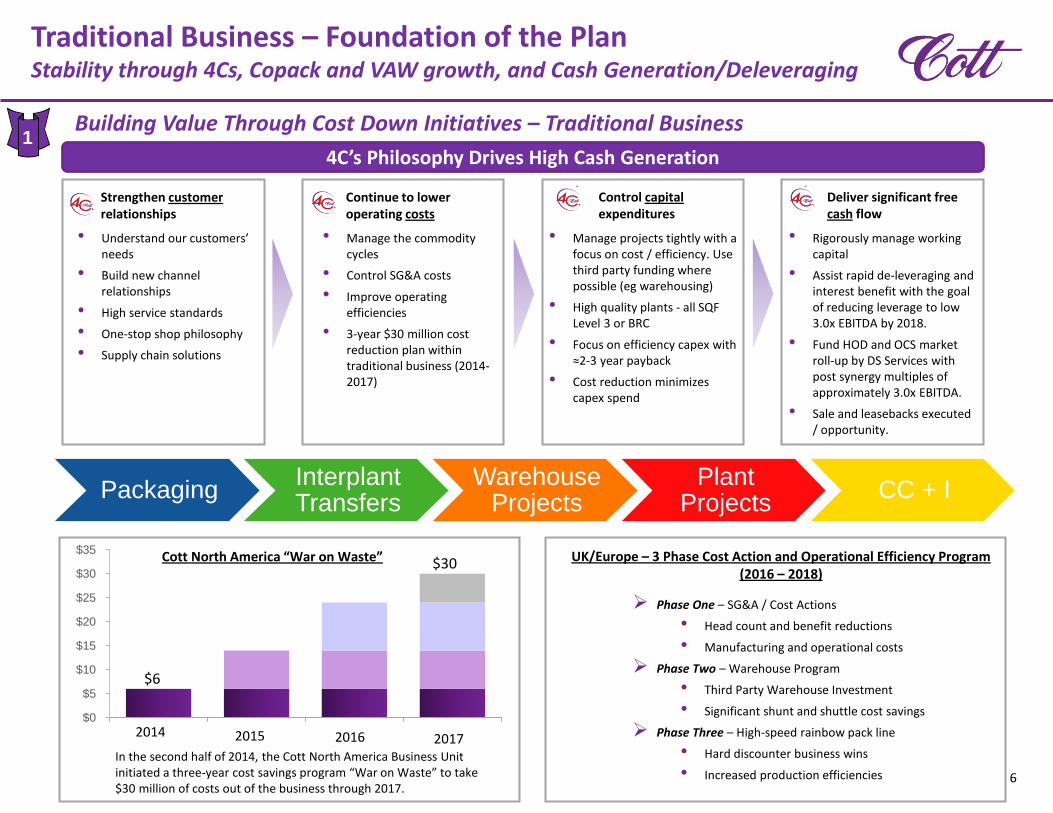

Traditional Business – Foundation of the PlanStability through 4Cs, Copack and VAW growth, and Cash Generation/Deleveraging

Control capitalexpenditures

Deliver significant free cash flow

• Understand our customers’ needs

• Build new channel relationships

• High service standards

• One-stop shop philosophy

• Supply chain solutions

• Manage the commodity cycles

• Control SG&A costs

• Improve operating efficiencies

• 3-year $30 million cost reduction plan within traditional business (2014-2017)

• Manage projects tightly with a focus on cost / efficiency. Use third party funding where possible (eg warehousing)

• High quality plants - all SQF Level 3 or BRC

• Focus on efficiency capex with ≈2-3 year payback

• Cost reduction minimizes capex spend

• Rigorously manage working capital

• Assist rapid de-leveraging and interest benefit with the goal of reducing leverage to low 3.0x EBITDA by 2018.

• Fund HOD and OCS market roll-up by DS Services with post synergy multiples of approximately 3.0x EBITDA.

• Sale and leasebacks executed / opportunity.

Strengthen customerrelationships

Continue to lower operating costs

4C’s Philosophy Drives High Cash Generation

$0

$5

$10

$15

$20

$25

$30

$35

1 2 3 4

$30

$6

2014 2015 2016 2017

Building Value Through Cost Down Initiatives – Traditional Business

PackagingInterplant Transfers

Warehouse Projects

Plant Projects

CC + I

In the second half of 2014, the Cott North America Business Unit initiated a three-year cost savings program “War on Waste” to take $30 million of costs out of the business through 2017.

1

UK/Europe – 3 Phase Cost Action and Operational Efficiency Program (2016 – 2018)

Phase One – SG&A / Cost Actions

• Head count and benefit reductions

• Manufacturing and operational costs

Phase Two – Warehouse Program

• Third Party Warehouse Investment

• Significant shunt and shuttle cost savings

Phase Three – High-speed rainbow pack line

• Hard discounter business wins

• Increased production efficiencies

Cott North America “War on Waste”

7

Traditional Business – Foundation of the PlanStability through 4Cs, Copack and VAW growth, and Cash Generation/Deleveraging

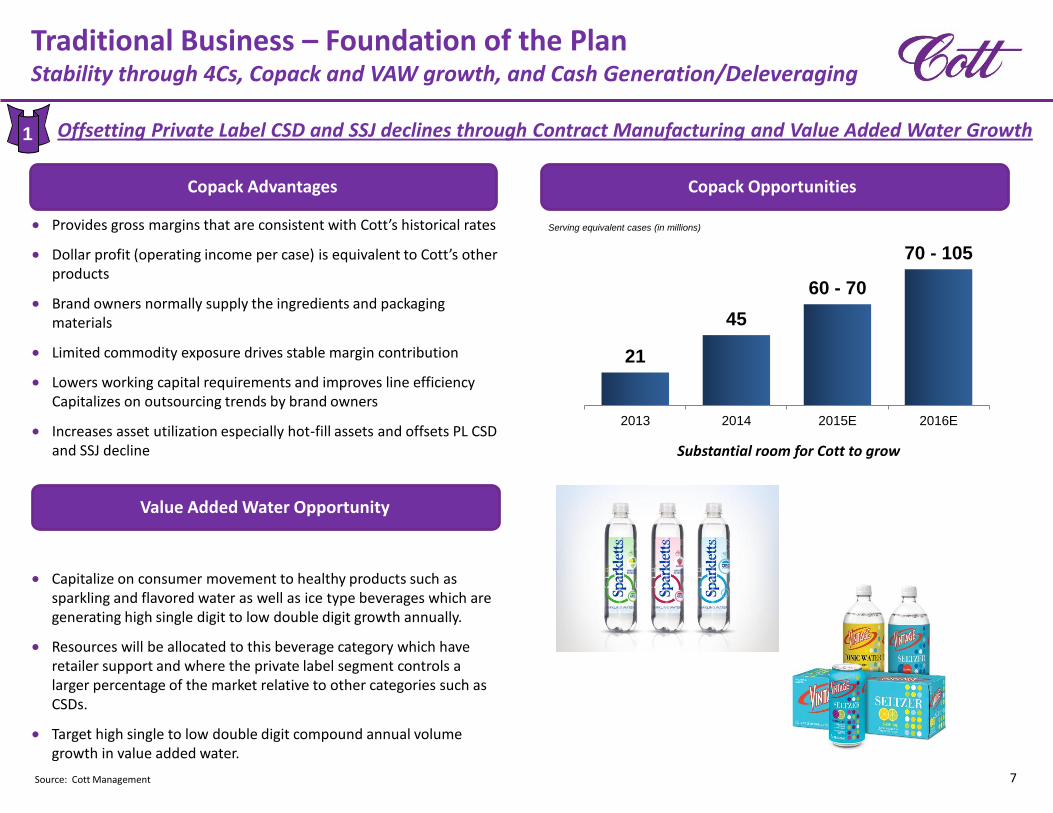

Offsetting Private Label CSD and SSJ declines through Contract Manufacturing and Value Added Water Growth

Copack Opportunities

Provides gross margins that are consistent with Cott’s historical rates

Dollar profit (operating income per case) is equivalent to Cott’s other products

Brand owners normally supply the ingredients and packaging materials

Limited commodity exposure drives stable margin contribution

Lowers working capital requirements and improves line efficiency Capitalizes on outsourcing trends by brand owners

Increases asset utilization especially hot-fill assets and offsets PL CSD and SSJ decline Substantial room for Cott to grow

21

45

60 - 70

70 - 105

2013 2014 2015E 2016E

Serving equivalent cases (in millions)

Copack Advantages

Capitalize on consumer movement to healthy products such as sparkling and flavored water as well as ice type beverages which are generating high single digit to low double digit growth annually.

Resources will be allocated to this beverage category which have retailer support and where the private label segment controls a larger percentage of the market relative to other categories such as CSDs.

Target high single to low double digit compound annual volume growth in value added water.

Value Added Water Opportunity

1

Source: Cott Management

8

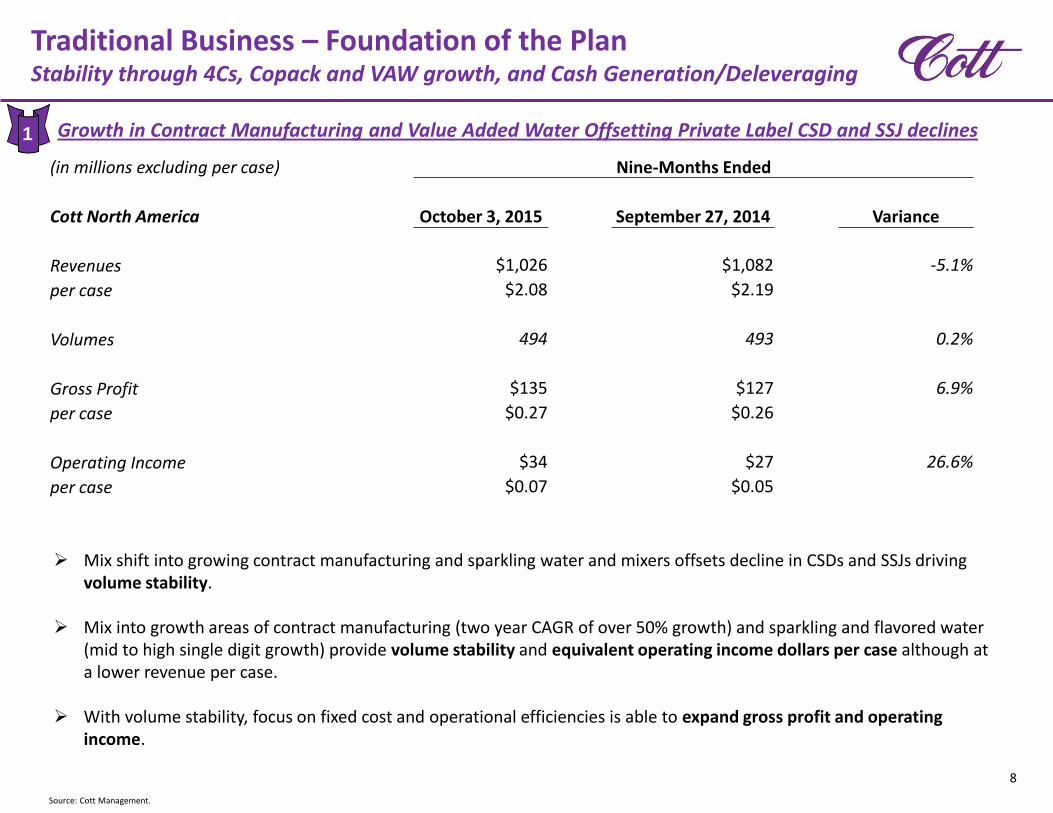

Source: Cott Management.

Mix shift into growing contract manufacturing and sparkling water and mixers offsets decline in CSDs and SSJs driving volume stability.

Mix into growth areas of contract manufacturing (two year CAGR of over 50% growth) and sparkling and flavored water (mid to high single digit growth) provide volume stability and equivalent operating income dollars per case although at a lower revenue per case.

With volume stability, focus on fixed cost and operational efficiencies is able to expand gross profit and operating income.

Traditional Business – Foundation of the PlanStability through 4Cs, Copack and VAW growth, and Cash Generation/Deleveraging

Growth in Contract Manufacturing and Value Added Water Offsetting Private Label CSD and SSJ declines 1

(in millions excluding per case) Nine-Months Ended

Cott North America October 3, 2015 September 27, 2014 Variance

Revenues $1,026 $1,082 -5.1%

per case $2.08 $2.19

Volumes 494 493 0.2%

Gross Profit $135 $127 6.9%

per case $0.27 $0.26

Operating Income $34 $27 26.6%

per case $0.07 $0.05

9

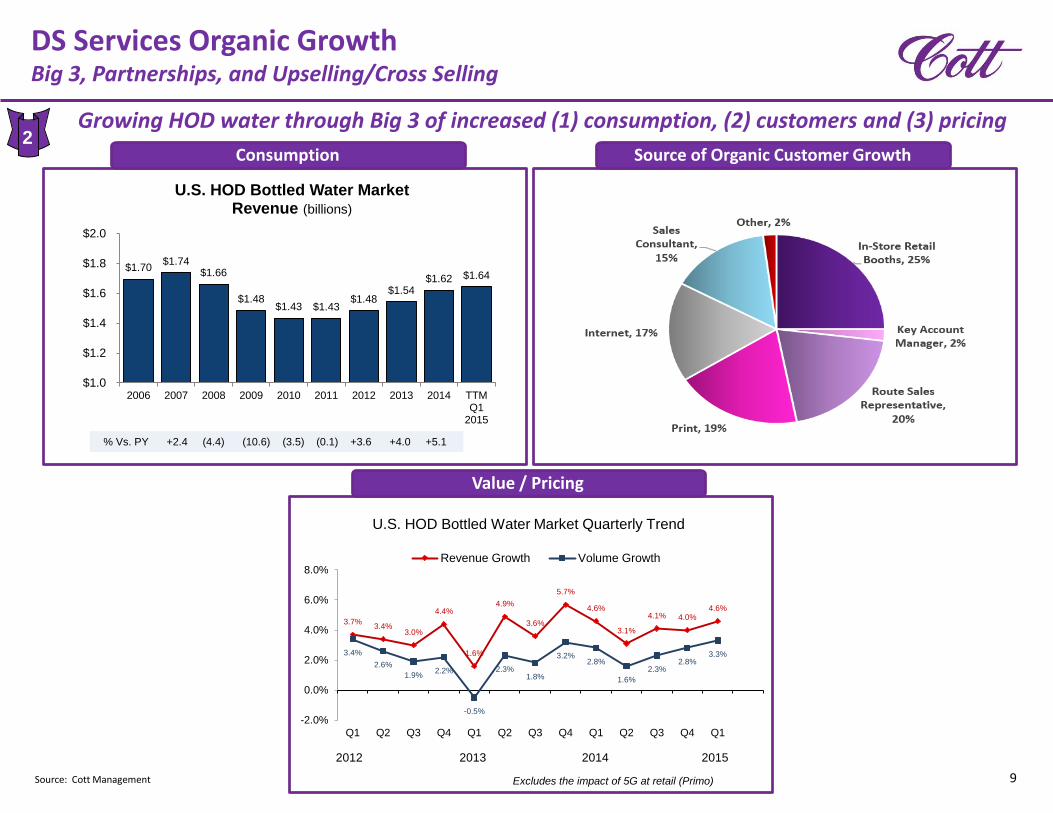

DS Services Organic GrowthBig 3, Partnerships, and Upselling/Cross Selling

Growing HOD water through Big 3 of increased (1) consumption, (2) customers and (3) pricing

$1.70 $1.74

$1.66

$1.48 $1.43 $1.43

$1.48 $1.54

$1.62 $1.64

$1.0

$1.2

$1.4

$1.6

$1.8

$2.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 TTMQ1

2015

U.S. HOD Bottled Water MarketRevenue (billions)

% Vs. PY +2.4 (4.4) (10.6) (3.5) (0.1) +3.6 +4.0 +5.1

3.7%3.4%

3.0%

4.4%

1.6%

4.9%

3.6%

5.7%

4.6%

3.1%

4.1% 4.0%4.6%

3.4%

2.6%

1.9%2.2%

-0.5%

2.3%1.8%

3.2%2.8%

1.6%

2.3%2.8%

3.3%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Revenue Growth Volume Growth

U.S. HOD Bottled Water Market Quarterly Trend

Excludes the impact of 5G at retail (Primo)

2012 2013 2014 2015

Value / Pricing

Consumption Source of Organic Customer Growth2

Source: Cott Management

10

DS Services Organic GrowthBig 3, Partnerships, and Upselling/Cross Selling

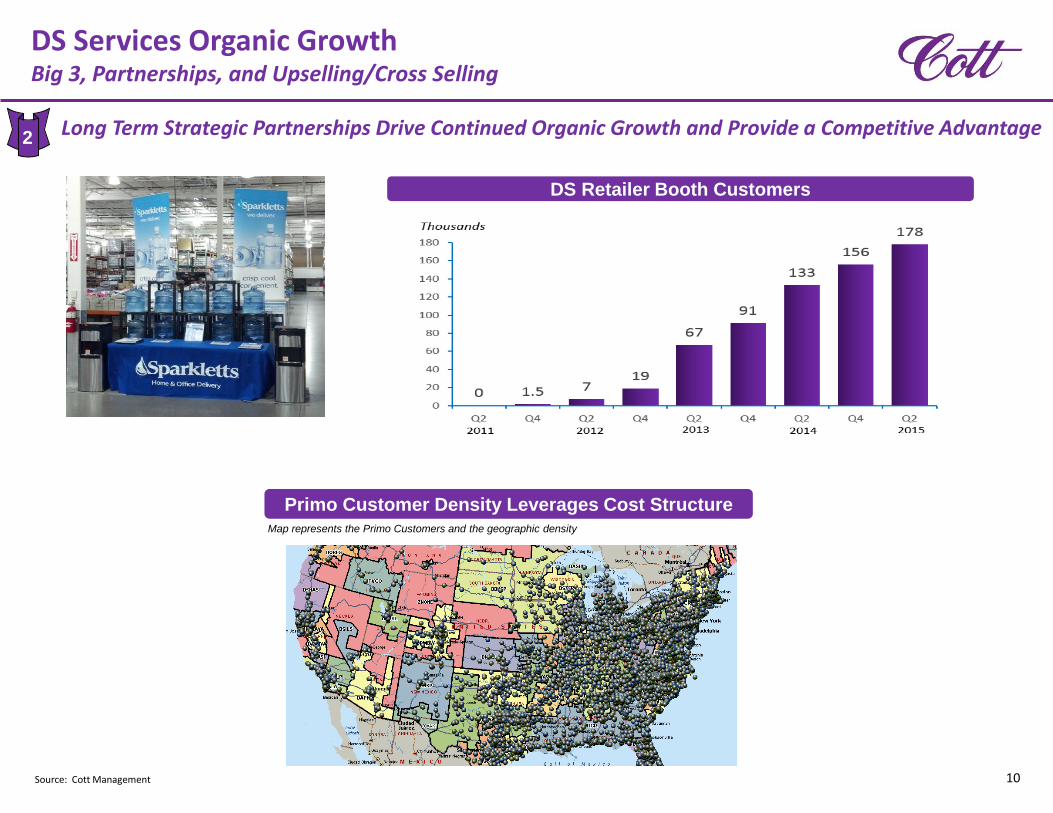

Long Term Strategic Partnerships Drive Continued Organic Growth and Provide a Competitive Advantage

DS Retailer Booth Customers

Map represents the Primo Customers and the geographic density

Primo Customer Density Leverages Cost Structure

2

Source: Cott Management

11

DS Services Organic GrowthBig 3, Partnerships, and Upselling/Cross Selling

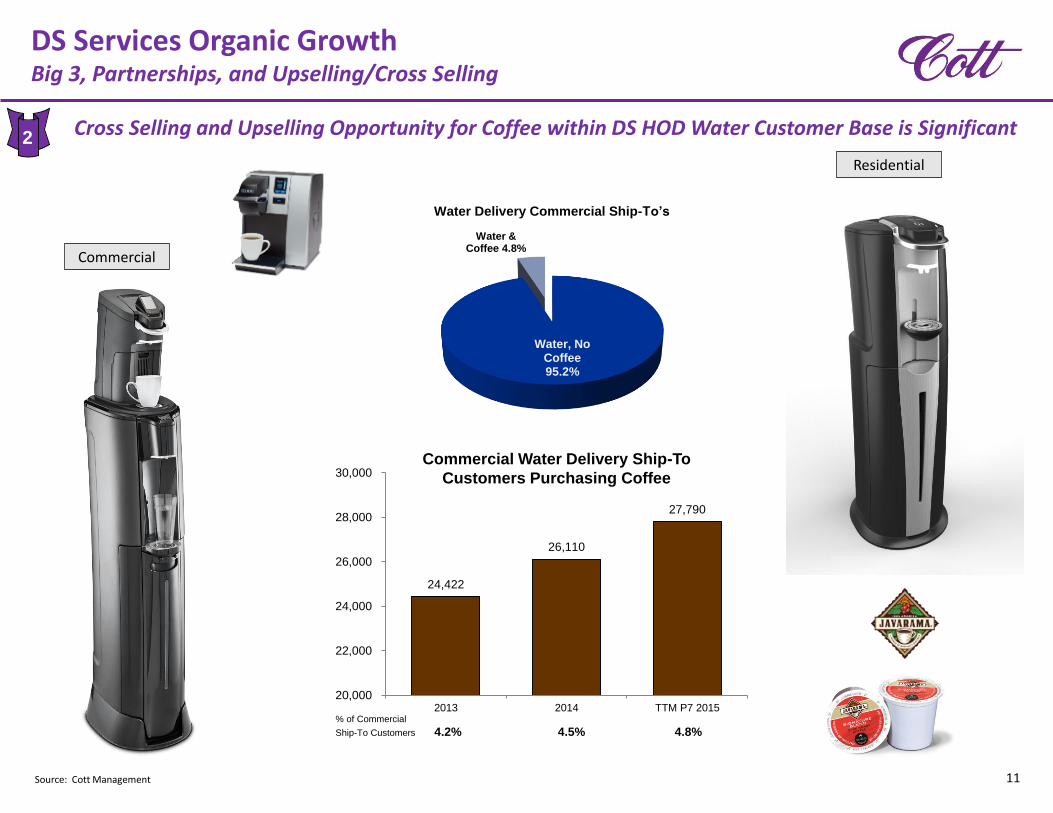

Cross Selling and Upselling Opportunity for Coffee within DS HOD Water Customer Base is Significant

Water, No Coffee95.2%

Water & Coffee 4.8%

Water Delivery Commercial Ship-To’s

Commercial Water Delivery Ship-To

Customers Purchasing Coffee

24,422

26,110

27,790

20,000

22,000

24,000

26,000

28,000

30,000

2013 2014 TTM P7 2015% of Commercial

Ship-To Customers 4.2% 4.5% 4.8%

Commercial

Residential

2

Source: Cott Management

12

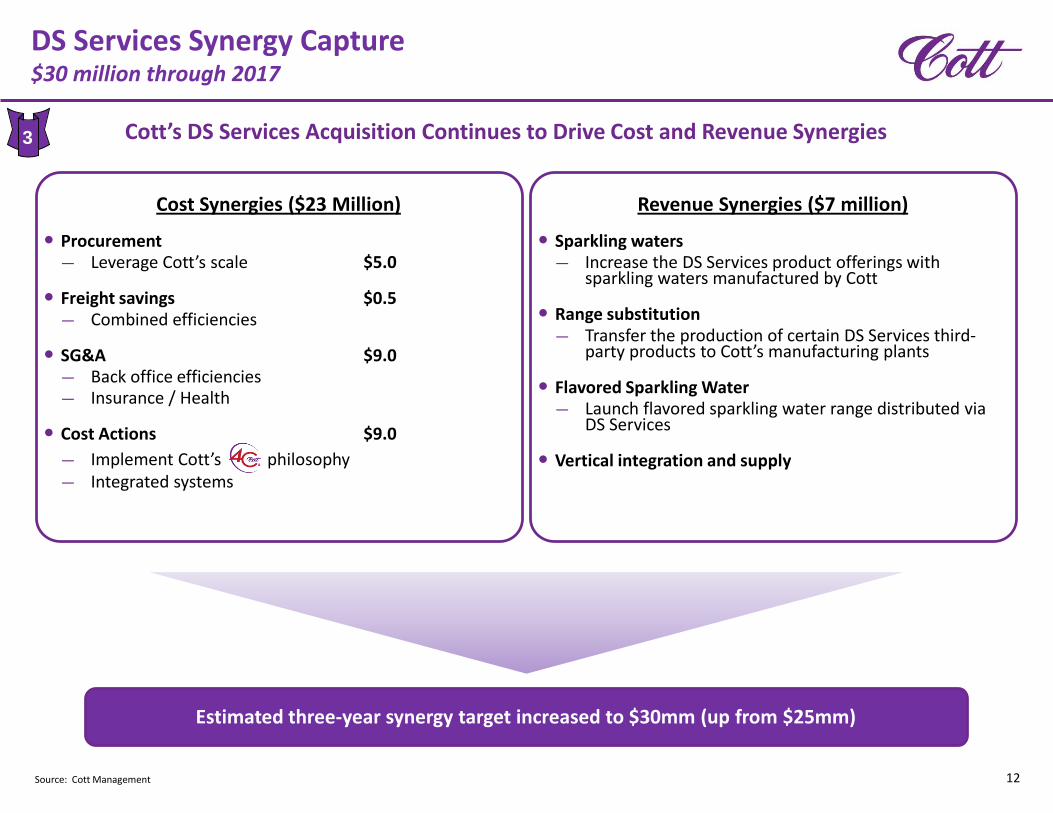

DS Services Synergy Capture$30 million through 2017

Estimated three-year synergy target increased to $30mm (up from $25mm)

Cost Synergies ($23 Million)

Procurement― Leverage Cott’s scale $5.0

Freight savings $0.5― Combined efficiencies

SG&A $9.0― Back office efficiencies― Insurance / Health

Cost Actions $9.0

― Implement Cott’s philosophy― Integrated systems

Revenue Synergies ($7 million)

Sparkling waters ― Increase the DS Services product offerings with

sparkling waters manufactured by Cott

Range substitution― Transfer the production of certain DS Services third-

party products to Cott’s manufacturing plants

Flavored Sparkling Water― Launch flavored sparkling water range distributed via

DS Services

Vertical integration and supply

Cott’s DS Services Acquisition Continues to Drive Cost and Revenue Synergies3

Source: Cott Management

13

DS Services Synergy Capture$30 million through 2017

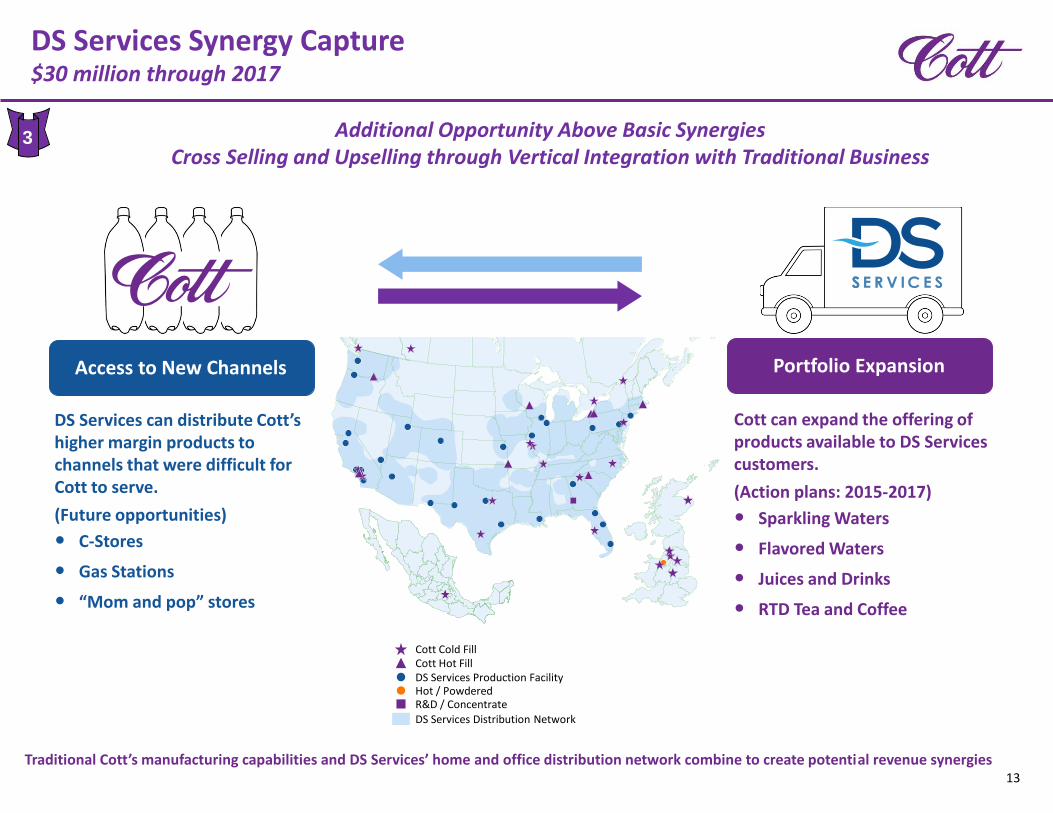

Additional Opportunity Above Basic SynergiesCross Selling and Upselling through Vertical Integration with Traditional Business

Portfolio Expansion

Cott can expand the offering of products available to DS Services customers.

(Action plans: 2015-2017)

Sparkling Waters

Flavored Waters

Juices and Drinks

RTD Tea and Coffee

Traditional Cott’s manufacturing capabilities and DS Services’ home and office distribution network combine to create potential revenue synergies

Access to New Channels

DS Services can distribute Cott’s higher margin products to channels that were difficult for Cott to serve.

(Future opportunities)

C-Stores

Gas Stations

“Mom and pop” stores

Cott Cold Fill

DS Services Production Facility Cott Hot Fill

DS Services Distribution Network

Hot / PowderedR&D / Concentrate

3

14

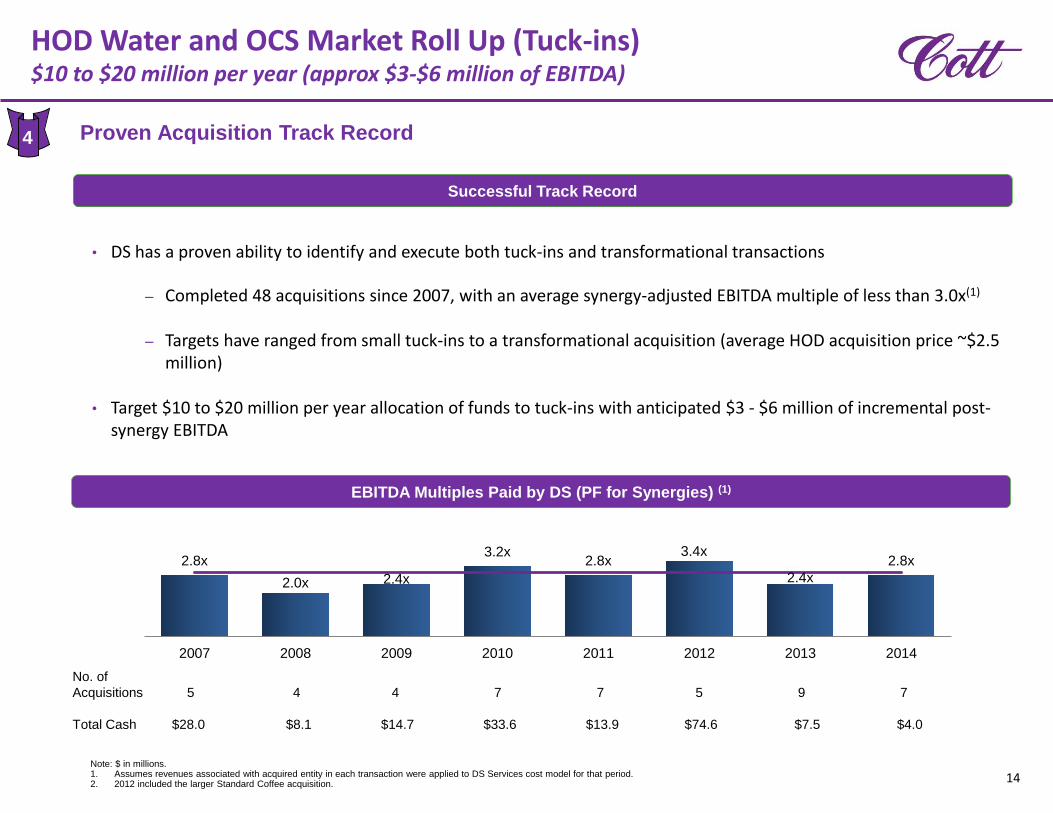

HOD Water and OCS Market Roll Up (Tuck-ins)$10 to $20 million per year (approx $3-$6 million of EBITDA)

Proven Acquisition Track Record

• DS has a proven ability to identify and execute both tuck-ins and transformational transactions

‒ Completed 48 acquisitions since 2007, with an average synergy-adjusted EBITDA multiple of less than 3.0x(1)

‒ Targets have ranged from small tuck-ins to a transformational acquisition (average HOD acquisition price ~$2.5 million)

• Target $10 to $20 million per year allocation of funds to tuck-ins with anticipated $3 - $6 million of incremental post-synergy EBITDA

Successful Track Record

EBITDA Multiples Paid by DS (PF for Synergies) (1)

2.8x

2.0x 2.4x

3.2x2.8x

3.4x

2.4x

2.8x

2007 2008 2009 2010 2011 2012 2013 2014

No. of

Acquisitions 5 4 4 7 7 5 9 7

Total Cash $28.0 $8.1 $14.7 $33.6 $13.9 $74.6 $7.5 $4.0

4

Note: $ in millions.1. Assumes revenues associated with acquired entity in each transaction were applied to DS Services cost model for that period. 2. 2012 included the larger Standard Coffee acquisition.

15

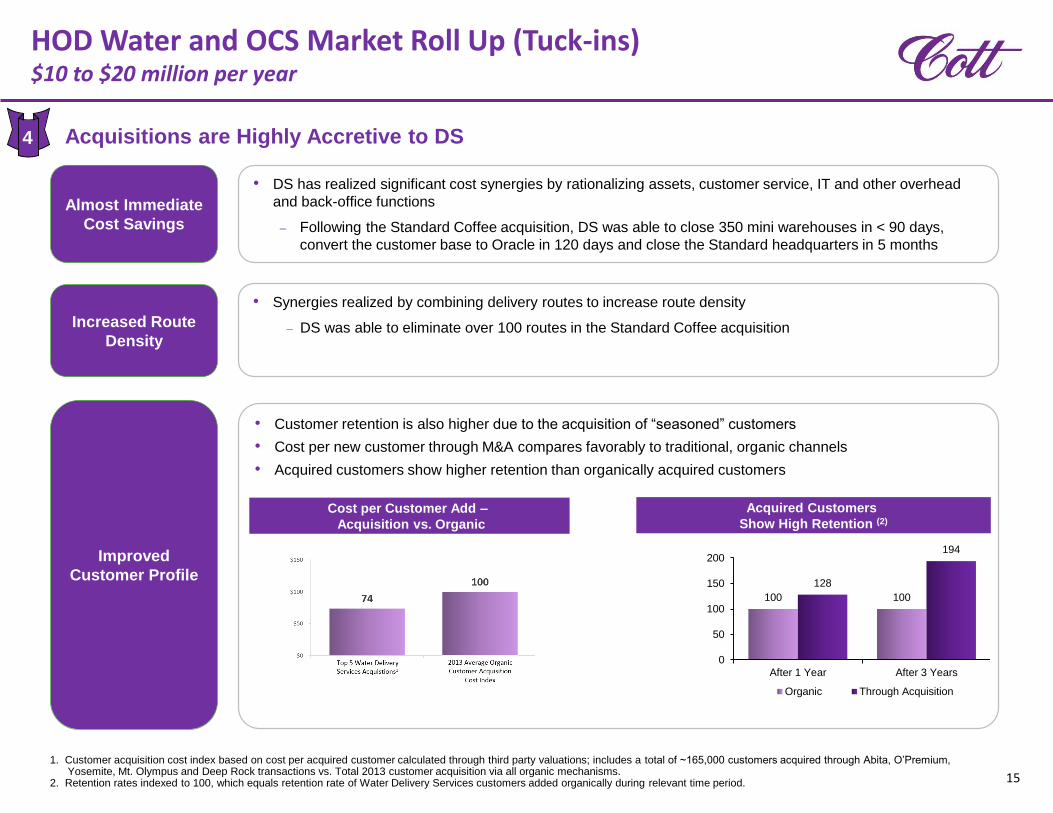

HOD Water and OCS Market Roll Up (Tuck-ins)$10 to $20 million per year

Acquisitions are Highly Accretive to DS

• Customer retention is also higher due to the acquisition of “seasoned” customers

• Cost per new customer through M&A compares favorably to traditional, organic channels

• Acquired customers show higher retention than organically acquired customers

Almost Immediate

Cost Savings

Increased Route

Density

Improved

Customer Profile

• DS has realized significant cost synergies by rationalizing assets, customer service, IT and other overhead

and back-office functions

‒ Following the Standard Coffee acquisition, DS was able to close 350 mini warehouses in < 90 days,

convert the customer base to Oracle in 120 days and close the Standard headquarters in 5 months

• Synergies realized by combining delivery routes to increase route density

‒ DS was able to eliminate over 100 routes in the Standard Coffee acquisition

Acquired Customers

Show High Retention (2)

Cost per Customer Add –

Acquisition vs. Organic

100 100

128

194

0

50

100

150

200

After 1 Year After 3 Years

Organic Through Acquisition

4

1. Customer acquisition cost index based on cost per acquired customer calculated through third party valuations; includes a total of ~165,000 customers acquired through Abita, O’Premium, Yosemite, Mt. Olympus and Deep Rock transactions vs. Total 2013 customer acquisition via all organic mechanisms.

2. Retention rates indexed to 100, which equals retention rate of Water Delivery Services customers added organically during relevant time period.

16

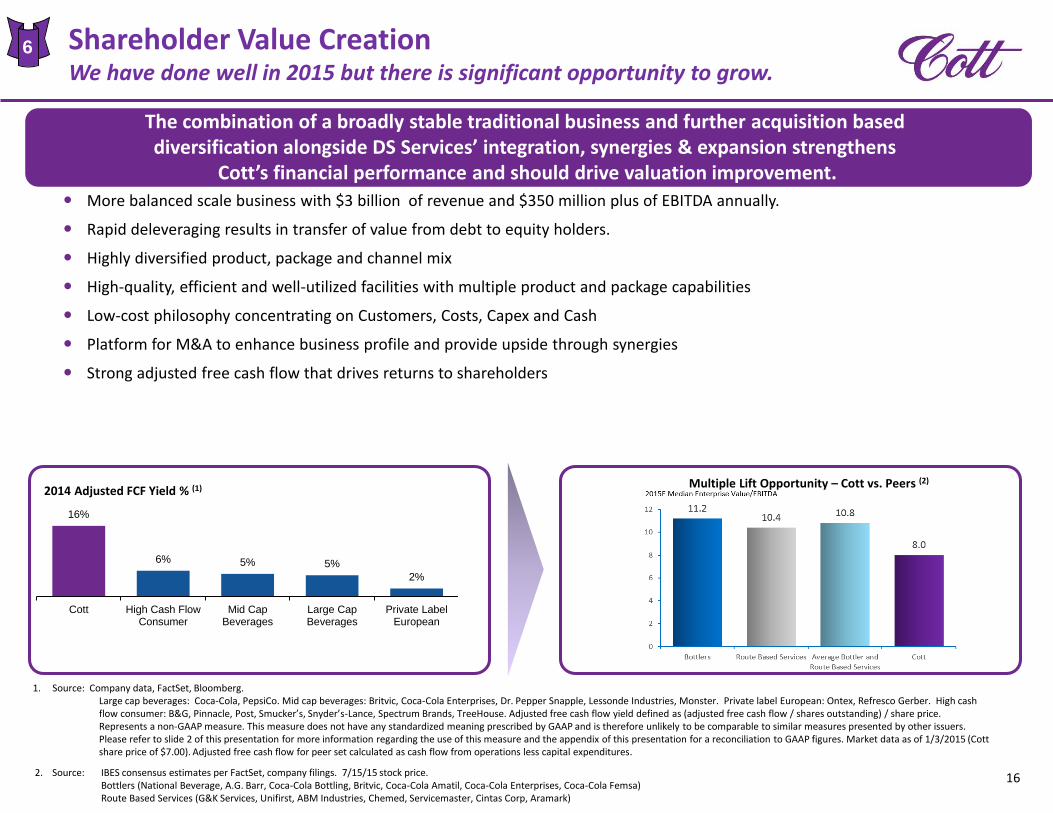

Shareholder Value CreationWe have done well in 2015 but there is significant opportunity to grow.

More balanced scale business with $3 billion of revenue and $350 million plus of EBITDA annually.

Rapid deleveraging results in transfer of value from debt to equity holders.

Highly diversified product, package and channel mix

High-quality, efficient and well-utilized facilities with multiple product and package capabilities

Low-cost philosophy concentrating on Customers, Costs, Capex and Cash

Platform for M&A to enhance business profile and provide upside through synergies

Strong adjusted free cash flow that drives returns to shareholders

The combination of a broadly stable traditional business and further acquisition based diversification alongside DS Services’ integration, synergies & expansion strengthens

Cott’s financial performance and should drive valuation improvement.

6

16%

6% 5% 5%

2%

Cott High Cash FlowConsumer

Mid CapBeverages

Large CapBeverages

Private LabelEuropean

2014 Adjusted FCF Yield % (1)

1. Source: Company data, FactSet, Bloomberg. Large cap beverages: Coca-Cola, PepsiCo. Mid cap beverages: Britvic, Coca-Cola Enterprises, Dr. Pepper Snapple, Lessonde Industries, Monster. Private label European: Ontex, Refresco Gerber. High cash flow consumer: B&G, Pinnacle, Post, Smucker’s, Snyder’s-Lance, Spectrum Brands, TreeHouse. Adjusted free cash flow yield defined as (adjusted free cash flow / shares outstanding) / share price. Represents a non-GAAP measure. This measure does not have any standardized meaning prescribed by GAAP and is therefore unlikely to be comparable to similar measures presented by other issuers. Please refer to slide 2 of this presentation for more information regarding the use of this measure and the appendix of this presentation for a reconciliation to GAAP figures. Market data as of 1/3/2015 (Cott share price of $7.00). Adjusted free cash flow for peer set calculated as cash flow from operations less capital expenditures.

Multiple Lift Opportunity – Cott vs. Peers (2)

2. Source: IBES consensus estimates per FactSet, company filings. 7/15/15 stock price.Bottlers (National Beverage, A.G. Barr, Coca-Cola Bottling, Britvic, Coca-Cola Amatil, Coca-Cola Enterprises, Coca-Cola Femsa)Route Based Services (G&K Services, Unifirst, ABM Industries, Chemed, Servicemaster, Cintas Corp, Aramark)

![FIS for the RBC/RBC Handover...4.2.1.1 The RBC/RBC communication shall be established according to the rules of the underlying RBC-RBC Safe Communication Interface [Subset-098]. Further](https://img.pdfslide.us/doc/110x75/5e331307d520b57b5677b3fa/fis-for-the-rbcrbc-handover-4211-the-rbcrbc-communication-shall-be-established.jpg)