Embed Size (px)

Citation preview

BUY IT TO TRY IT Nita Rollins, PhD, Director of Thought Leadership & Cultural Insights

BUY IT TO TRY IT Executive Summary

Purchase Assessment Increasingly Happens After the BuyConsumers have always returned goods that weren’t to their liking, but

generally, these returns were unintentional and caused inconvenience

and extra cost. Returns these days are another matter. Due to various

behavioral, cultural and industry changes, they’re on the rise: As much

as a third of all Internet sales are returned, according to retail consultancy

Kurt Salmon, and that percentage ticks higher during the holiday season.

Delving into the return phenomenon a bit, we find many consumers

are intentionally and habitually recreating the store experience at

home, where they’re free to assess the purchase at their leisure before

fully committing—and (in most cases) return what doesn’t work while

suffering little to no downside.

Though it’s never quite this simplistic, the consumer’s continued

quest for ways to compensate for the lack of materiality in ecommerce

transactions has a great deal to do with the new conditional purchase

journey and its accompanying trend, Buy It To Try It. The latter clusters

together a growing number of consumer behaviors and retail practices

with one thing in common: ecommerce purchase consideration activities

take place after the transaction. Because the retailers innovating in this

space are quite diverse, from VC-backed start-up to ecommerce titan,

the impact of Buy It To Try will be broadly felt. Three retail practices

in particular—planned over-ordering or home try-on; subscription

shopping; and personal e-stylists—address consumers’ long-standing

and culturally evolved needs to increase shopping pleasure, decrease

online shopping risk, and last but certainly not least, have more

meaningful relationships with the brands they patronize. This nexus of

commerce platform innovations will gradually influence the relationship

all retailers have with their consumers.

BU

Y

IT

TO

T

RY

IT

BU

Y

IT

TO

T

RY

IT

Consumer Entitlement, Risk Aversion Behind Conditional Buying Just where did today’s conditional buying come from and how can we account

for its momentum? Consumers’ heightened awareness of their value to retailers

in a low-loyalty, price-transparent market has undoubtedly led to a sense of

entitlement regarding perks for their patronage. Moreover, the consumer’s

perception of what constitutes a good brand relationship has radically changed.

Edelman’s latest Brandshare study shows that 87% of people want meaningful

interactions with brands, but only 17% think brands are actually delivering

today. This perception of one-sidedness has emboldened consumers to look

for more—more service responsiveness, more social responsibility, and, yes,

more perks, whether tied to loyalty programs or not—from the next brand, if

they’re not satisfied with the first.

Conditional buying and purchase return behaviors also come from

ratcheted-up risk aversion on the part of a digitally savvier and permanently

value-oriented consumer in the US. As author of a study of returns in the

Journal of Marketing, Amanda Bower says: “The really dominant driving

characteristic is how much do I regret having spent $7 on return shipping in

the past, and is it really worth it to risk paying that money again in the future?

In contrast, free returns are similar to the saying, ‘What would you do if you

knew you couldn’t fail?’”

BU

Y

IT

TO

T

RY

IT

a job decreases, the younger the employee. Culturally speaking, we’re definitely

having a grazing moment in the US, at least among those in the middle to upper

ends of the socioeconomic spectrum. The pressure to get it right—the first time

and for good—is dissipated, and the freedom to experiment, to have a short-

term, low-cost experience of everything from shared cars to vacation homes has

clearly crept into the three ecommerce approaches we’re discussing below.

Three Retail Innovations Disrupting the Traditional Purchase JourneyBeyond the cultural and behavioral drivers of the Buy It To Try It trend, it has

been given steam by increasingly lenient merchandise return policies and three

ecommerce innovations breathing new life into the purchase journey: planned

over-ordering, subscription shopping, and personal e-stylist. Though differing

in their respective details, they share one key ingredient: asking for a financial

commitment of some sort before further purchase assessment—and the

pleasure that generally accompanies it—can happen. Myriad values are created

from these ecommerce practices: the consumer’s costs associated with returns

approach zero, recurrent revenue for the retailer is locked in, data on consumer

preferences becomes highly reliable (and household profit becomes the goal

rather than square meter profit, according to the Boston Consulting Group), and

brand loyalty and customer lifetime value increase.

Shopping as Entertainment, Sharing Economy Drivers As WellThere are cultural forces at work here as well. First, an Urban Land Institute 2013 report on Gen Y found that half the men and 70% of the women consider

shopping a form of entertainment. “They are researching products, comparing

prices, envisioning how clothing or accessories would look on them, or

responding to flash sales or coupon offers.” The study also found that 45%

of respondents spend at least an hour each day on retail-oriented sites, and

among those spending over two hours, men are more engaged than women.

Consumerism as entertainment is not confined to millennials, of course;

shopping as a leisure activity is widespread. Today’s consumers’ continuous

partial shopping makes them experts at gaming the system, which is a source

of pride to many.

Somewhat at odds with consumerism as entertainment, conditional buying is

more mysteriously tied to the burgeoning sharing economy, where leasing or

renting as a semi-permanent deferral of both the decision to buy and the onus

of ownership have taken shape. Many digitally enabled dating rituals today

have the same noncommittal ethos, and the average number of years spent at

BU

Y

IT

TO

T

RY

IT

Boomerang Purchases Are Big Business Purchase returns are very, very big business. Retail analysis firm IHL

Group’s recent study pegs global retail returns as a $642.6 billion

loss. Studies find that handling each returned item costs online

sellers between $6 and $18, and the cost of restocking merchandise

is sometimes recouped via a handling fee but not always, draining

revenue by 4% a year on average. In aggregate, manufacturers and

retailers spend more than $100 billion annually on return-related logistics. Not infrequently, with liberal return windows, the item

is no longer on-trend, which is particularly tough for style-related

categories like fashion/textiles/shoe retailers, 48% of whom have a

return rate between 25-50%, according to a university study. (And a

full 13% of customers order online without intending to purchase.)

Nick Robertson, former chief executive of online fashion retailer

Asos, once said a 1% fall in returns would immediately add $16

million to the company’s bottom line. (Robertson also said their

return rate is around 30%.)

To make matters more costly, return fraud cost US stores a whopping

$10.9 billion in 2014—$3.6 billion just during the holiday season,

according to NRF’s 2014 Return Fraud Survey. The survey indicates

a full 92.7% of retailers have experienced the return of stolen

merchandise, which electronic receipts have made easier to do.

There is also the problem of “wardrobing”—returns of merchandise

the consumer only intended to wear once—which Bloomingdale’s and other

higher-end stores now combat with conspicuous tags that when removed means

the item is a keeper. (Single-use purchases happen in electronics too: Best Buy

staffers talk about the Super Bowl returnees, who are in line with their repacked

flat screens the day after the big event.)

New Rules of the Road 1. Buying is inherently conditional.

2. Some Subscription Shopping and Personal Stylist commerce

models rely upon discovery post purchase.

3. Over-ordering to try different styles or sizes also moves product

assessment to post-purchase.

4. Keeping one/some and returning one/some items is frequently the

real moment of purchase, and often the trigger for another.

5. The automated setup of curation and replenishment subscription

commerce models means the next purchase is in the bag.

HOW “BUY IT TO TRY IT” SHAPES A PURCHASE JOURNEY

Discover

Assess

Buy Keep Return Buy

Membership or multiple Items

Recurrent Purchases Online, Unplanned Purchases In-Store

BU

Y

IT

TO

T

RY

IT

at companies where consumers had to pay for shipping on returns. Second,

returns in-store, which 62% of consumers prefer to make, enable some stores

to experience up to 17% comps due to sales credit from selling e-commerce–

only SKUs brought into the store through returns, according to Kurt Salmon.

Third, and perhaps most obviously, returns in-store mean footfall.

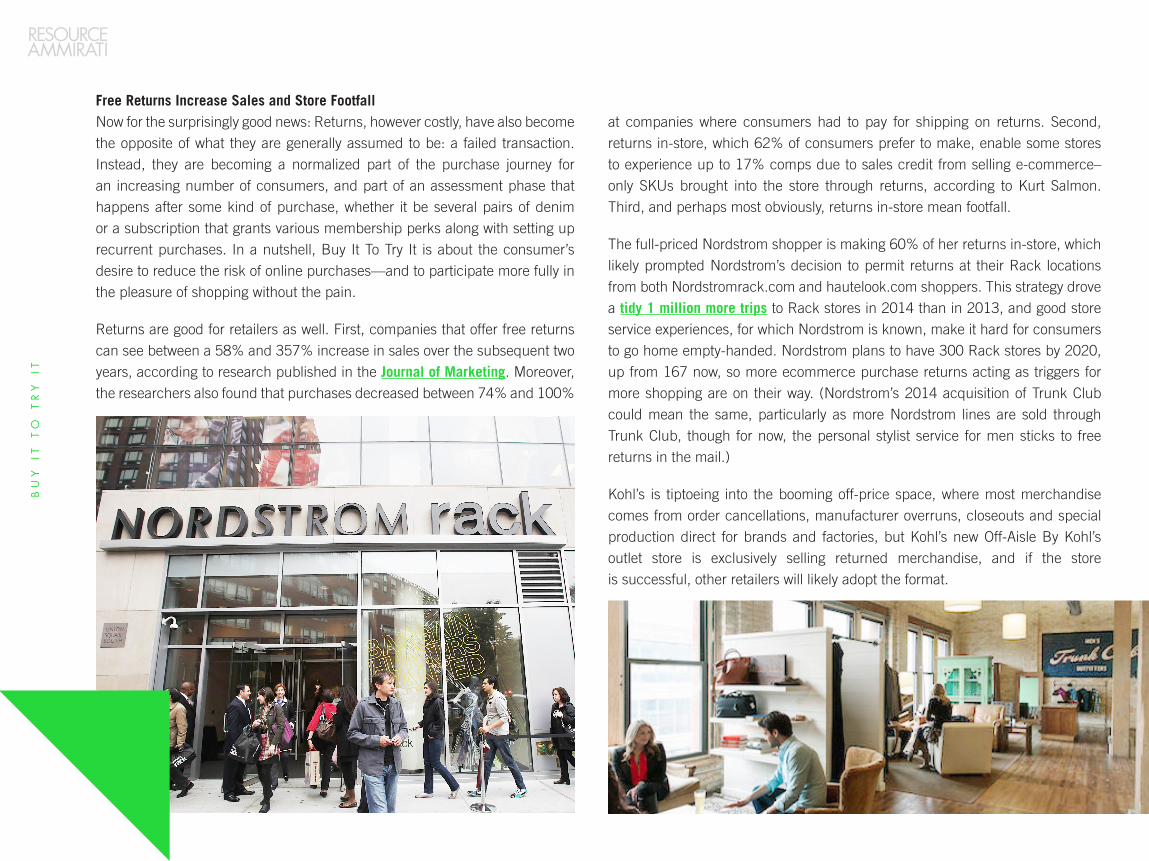

The full-priced Nordstrom shopper is making 60% of her returns in-store, which

likely prompted Nordstrom’s decision to permit returns at their Rack locations

from both Nordstromrack.com and hautelook.com shoppers. This strategy drove

a tidy 1 million more trips to Rack stores in 2014 than in 2013, and good store

service experiences, for which Nordstrom is known, make it hard for consumers

to go home empty-handed. Nordstrom plans to have 300 Rack stores by 2020,

up from 167 now, so more ecommerce purchase returns acting as triggers for

more shopping are on their way. (Nordstrom’s 2014 acquisition of Trunk Club

could mean the same, particularly as more Nordstrom lines are sold through

Trunk Club, though for now, the personal stylist service for men sticks to free

returns in the mail.)

Kohl’s is tiptoeing into the booming off-price space, where most merchandise

comes from order cancellations, manufacturer overruns, closeouts and special

production direct for brands and factories, but Kohl’s new Off-Aisle By Kohl’s

outlet store is exclusively selling returned merchandise, and if the store

is successful, other retailers will likely adopt the format.

Free Returns Increase Sales and Store FootfallNow for the surprisingly good news: Returns, however costly, have also become

the opposite of what they are generally assumed to be: a failed transaction.

Instead, they are becoming a normalized part of the purchase journey for

an increasing number of consumers, and part of an assessment phase that

happens after some kind of purchase, whether it be several pairs of denim

or a subscription that grants various membership perks along with setting up

recurrent purchases. In a nutshell, Buy It To Try It is about the consumer’s

desire to reduce the risk of online purchases—and to participate more fully in

the pleasure of shopping without the pain.

Returns are good for retailers as well. First, companies that offer free returns

can see between a 58% and 357% increase in sales over the subsequent two

years, according to research published in the Journal of Marketing. Moreover,

the researchers also found that purchases decreased between 74% and 100%

BU

Y

IT

TO

T

RY

IT

Consumers and Retailers Embrace Generous Return Policies Routinely over-ordering more than one color or size of an item or

more items than the consumer reasonably expects to keep, and

fully expecting free returns to be part of every shopping experience:

these might seem like consumer behaviors and cavalier attitudes

confined to product categories where fit and style are factors. In

fact, a 2012 UK study by Fits.me (a provider of virtual fitting room

technology) found that 41% of the 1,000 study participants bought

clothing in multiple sizes and returned those that didn’t fit.

It’s easy to assume these behaviors and attitudes typify extreme

shoppers—some of whom are high value, others just addicted to

the process of shopping and can be serial returners—and busy

moms, confirmed to buy multiple sizes for their kids by recent

Resource/Ammirati research. It would also seem likely this behavior

is common to the luxury category. McKinsey reports that a full 90%

of American consumers expect a convenient return policy and free shipping from

their digital luxury experience. But ComScore and UPS’s 3rd annual Pulse of the Online Shopper™ Study finds these behaviors are quite widespread: 82% of

study respondents—shoppers of all categories—said they would complete the

purchase if they could return the item to a store or have free return shipping, and

66% said they view a retailer’s return policy before making a purchase.

Finally, in its 2015 Future of Retail Study, Walker Sands found that free returns

are now the “No. 2 incentive for getting consumers to shop online more,” ranking

higher than one-day shipping. Given its importance, how many retailers have

institutionalized free and convenient returns? Of the Top 40 online retailers

studied by StellaService Analysts, 25% always provided free returns, and 60%

provided a prepaid return label in Q4 2014. (This included retailers who charged

for the label, as well as those who do not include the label in the box itself.)

BU

Y

IT

TO

T

RY

IT

Longer Return Windows and the Endowment EffectOf course, consumers don’t merely consider the cost of the return;

they look at the return window as well. For instance, there is no time

limit on returns at Bath & Body Works, Macy’s, Bloomingdale’s and

Nordstrom (Rack customers have 90 days). Zappos and Kohl’s give

customers 365 days, and Target gives 90 days, though REDcard

holders enjoy 30 extra days and private-label purchases now have a

full-year return window. These are a few of the retailers with the most

generous return policies, though the trend toward longer periods is

undeniable. What is counterintuitive to marketers is that the longer

the return window, generally the fewer the returns. This can be

attributable to the “endowment effect,” the human tendency to

overvalue something just because we own it (also called divestiture

aversion and status quo bias). The longer that dress hangs on the

closet door, the more it seems like it’s ours already, hence valuable,

so why not keep it?

Three Ecommerce Approaches Invigorating Retail 1. Planned Over-Ordering, better known as Home Try-On

Zappos has always been a big proponent of the home try-on experience,

openly encouraging consumers to order more than one size of shoes,

leading to a 35% return rate—and a startling 50% for their most profitable

customers, who order more expensive lines. Many luxury apparel retailers

routinely send two sizes to customers, and Rent the Runway tells shoppers

uncertain about size and fit, “When in doubt, size up [for free].”

Despite some retailer skepticism (though this is changing), studies show

that if the return process is relatively hassle-free, she becomes a higher

value customer over time, demonstrating greater brand loyalty and more

risk-taking with higher-margin purchases. Warby Parker has perhaps done

more than any other retailer to popularize the Buy It To Try It trend, given

its five pairs/five days/free shipping and free returns setup, a deceptively

simple, non-subscription consumer experience of a disruptive retail

model currently valued at $1.2 billion. Though social responsibility and

undercutting eyewear behemoth Luxottica with more affordable frames

have as much to do with Warby Parker’s early success as their home try-on

experience that bakes spectacle returns into a winning formula, it is the

latter that has permeated the shopping zeitgeist.

For online apparel-shopping men of Mott & Bow, a purchase of one pair

of pants automatically comes with another, and the wrong fit is shipped

back for free.

For a product notoriously hard to fit, True & Co offers a five-bra collection

for trying on at home, with a 30-day free return window.

What’s notable about these examples is that the consumer is the beneficiary

of what used to be a luxury experience, and this is where one is tempted

to talk (as many have) in terms of the Uber-ization of online shopping

amenities—the shopping equivalent of chauffeured cars for the masses.

BU

Y

IT

TO

T

RY

IT

BU

Y

IT

TO

T

RY

IT

Three Ecommerce Approaches Invigorating Retail 2. Subscription Shopping

The so-called subscription economy, aka “subcom,” is hard to miss these days,

and although flameouts are fairly common—Shoedazzle, Swag of the Month,

Fourth and Grand, Lollihop, to name but a few—the subcom market is worth

around $3 billion. Gartner Group estimated that by the end of 2015, 35%

of Global 2000 companies would generate revenue via subscription-based

services and revenue models. Of total American household consumption,

goods have decreased by 10% over the past two decades, while services

have increased, and the subcom approach simply surrounds products with

service, reports The Economist, unlike many flash sale retailers, the supernova

ecommerce model of five years ago that put less emphasis on service and

relationship-building.

Dynamic PricingA variation on the subcom model, heretofore focused on convenience

or discovery, the recently launched Jet.com claims to offer the lowest prices on

the web for an annual $49 fee. Though positioning itself as an Amazon rival,

it actually has something critical in common with Amazon: dynamic pricing.

Amazon’s Subscribe and Save ensures the more a shopper buys, the more

she saves, up to a 15% discount, but Amazon’s real algorithm-based dynamic

pricing is a behind-the-scenes practice. Jet.com’s version is coming out of the

closet in real time as a potent add-to-bag tactic on overdrive. The site explains:

“As you shop, we show you the items that bring costs down when bought together.

Choose those items and watch your savings get bigger and

bigger.” Jet says on top of prices 10% to 15% cheaper than

elsewhere online, prices drop even further if shoppers pay

with debit instead of credit or agree to wait for different

items to be shipped in the same package. As for those

pesky returns, there is a 3% discount if a member

agrees upfront not to return any item in the order.

Putting consumers on a plan to receive goods at certain intervals (every month,

every other, etc.) is essentially another way to incentivize consumers to meet

spending thresholds for certain service perks or promotions, with the basket

size or spending threshold spread out over time. It’s not as easy as it seems,

however; churn can be murderous, retailers must have a handle on calculating

CLTV (customer lifetime value) and even today’s forerunners like Dollar Shave

Club struggle to achieve profitability.

BU

Y

IT

TO

T

RY

IT

Some subscription ecommerce models are replenishment-oriented, like

Amazon’s Subscribe and save, Target Subscriptions and P&G’s Venus Direct,

a Resource/Ammirati client, focused on reducing “cognitive load” by increasing

the convenience of shopping for items that are low consideration, and repeated

at fairly regular intervals. The benefit to Amazon and Target is some guarantee of

continuous revenue, as well as improved warehousing and stock management.

Even consumer goods replenishment itself can be disrupted, however: Boxed, the

mobile app that sells wholesale bulky goods like the kind sold at Costco or Sam’s

Club, doesn’t require a long-term commitment of any kind, nor a membership

fee, and is competing for the shopping habits of mainly millennials and Gen Xers

simply by offering a better mobile app experience while the wholesale giants

sleep on the mobile app job.

BU

Y

IT

TO

T

RY

IT

Though there is overlap, the other subscription companies that are part of the Buy

It To Try It trend focus on product discovery, e.g., curated product mixes, some

expert-led, some consumer survey/profile-based, most a blend of the two. These

are a clear way for consumers to “buy” via subscription in order to try the product

before, in many cases, eventually trading up to a full-size product or buying

more of the same, more of that wine or those dog treats. How many subscription

sampling consumers trade up to a full size or increase the frequency of their

deliveries (if this is permitted)? A full 50% of the monthly samples Birchbox mails

are purchased by their consumers in full size on the site, in no small part because

Birchbox, a Resource/Ammirati client, matches a consumer profile with others

like it using affinity analysis, thereby packing boxes likelier to appeal. Kicked

off in 2010, Birchbox generated over $125 million in 2014, and encourages

trading up by offering Birchbox points for shopping, referring friends and giving

feedback on the five monthly samples.

Reviewers of Popsugar’s Must Have Box claim to have purchased many of the

products they “discovered,” and the “Special Edition” boxes, which quickly sell

out, can cost as much as $250. (TRYMBL, a failed start-up, had an interesting

business model: invitation-only members were to be selected based on their

likeliness to follow beauty product sampling with purchase.) Eco-friendly food

curation company Conscious Box also incentivizes consumers to write product

reviews to earn points toward a future purchase like a full-size product. Among

the conscientious army of beauty box bloggers, the issue of companies sending

closeout or discontinued items has surfaced precisely because many subscribers

expect to be able to buy the (full-sized) product if they so choose.

A FULL 50% OF THE MONTHLY SAMPLES BIRCHBOX MAILS ARE PURCHASED BY THEIR CONSUMERS IN FULL SIZE ON THE SITE.

BU

Y

IT

TO

T

RY

IT

Boxycharm, which achieved 4000% growth in less than two

years, and charges $21 per month for products equaling over

$100 (verifiable, thanks to the price/product list it sends), has

broken precedent with most sampling boxes, sending full and

“luxury-sized” products each month because it enables the company

to truly act as curator (of the products it buys), rather than having

to work with a dwindling supply of free beauty samples, already

small enough in Asia to have virtually killed the beauty sample

box trend there.

Still, “deluxe” or so-called luxury sizes can be purchased in full size,

and Boxycharm subscribers receive 450 loyalty charms every three

months, redeemable for additional full-size and luxury-size beauty

items of the member’s choice.

BU

Y

IT

TO

T

RY

IT

Suffice it say, there are endless subcom variations. Meundies.com is a kind of

underwear of the month club, and membership buys personalized choices at

special pricing (up to 33% savings), in addition to free shipping and returns.

Members have the option of skipping a month or putting their membership on

pause during the first five days of each month.

The clever monthly subscription company Turntable Kitchen sends subscribers

a “pairings box” with a custom-mixed vinyl record featuring favorite and up-and-

coming bands; three seasonal, themed recipes; one to two premium ingredients;

and suggested pairing and tasting notes. There is no trading up here, though

the value of the limited edition pressing of new music is stressed, and digital

downloads of the music is password protected, for subscribers only.

BU

Y

IT

TO

T

RY

IT

Currently valued at $2 billion after only three years, Blue Apron’s meal kit delivery

options ask consumers to commit to a two-person plan with three meals per week

or a family plan with a choice of two or four meals per week—with the option to

cancel anytime. The recently introduced mobile app lets consumers exert more

control over the “try” half of the trend by making changes to recipe selections

and deliveries, and the app facilitates more buying of items such as sea salt

and salad spinners from the Blue Apron marketplace as well—particularly those

featured in the video tutorials.

What retailers must bear in mind if considering subscription shopping is that the

consumer feels they are in a relationship with the retailer that surpasses the one

they have without a membership. Blue Apron’s mobile app lets home chefs add

animated “steam” to their dishes for more sharing fun on Facebook, Instagram

or Twitter—deepening the sense of belonging to the Blue Apron movement.

Some consumers have quit their favorite beauty box companies when they

abandoned the subscription model precisely because the latter makes them

feel as if they’re part of a club and they’re being sent a gift, not just a delivery,

and, ideally, that the retailer is truly getting to know them better based on their

monthly feedback and data analytics. Also, agreements must be crystal clear.

Justfab, on track to be a $500 million company this year, got off to a rocky start

due to consumer confusion and dismay over the checkout process that initially

made it much easier to be signed up for the monthly subscription service than

not (thereby surprising many early customers when they were charged for the

month’s delivery because they hadn’t opted out by the 5th of the month). News

media subscriptions often automatically renew annually, a convenience to some,

a Mafia-like membership perk to others.

Logistics SubscriptionsThis ecommerce innovation is the odd man out, as it’s focused not on deepening

a relationship with any one retailer, but rather on taking the financial cost out

of conditional buying anywhere on the web. Sprouting up in the same crevice

that fast or same-day delivery companies have flourished, these companies

cover the return journey and give the Big Two, UPS and FedEx, a bit of healthy

competition, a good thing according to Rent the Runway CEO Jennifer Hyamor.

At the last SXSW, she lamented increasingly expensive delivery services and

said, “The delivery [industry] needs to be completely ripped up and totally

recreated.” Enter ShopRunner, which offers both free shipping and returns for

a $79 a year subscription (though it’s free for American Express cardholders),

but covers only 100 or so brands. Return Saver, from the same company that

gave us Freeshipping.com ($13 a month for roughly 1,000 online stores), lets

you make as many FedEx ground returns (under 50 pounds) as you would like

to any retailer for $49 per year.

BU

Y

IT

TO

T

RY

IT

3. Personal E-Stylists A blend of subscription shopping and home try-on businesses, online personal

stylist retailers are replicating, in a way, one of apparel retailing’s oldest practices.

Historically, a service amenity of higher end department stores or reserved

for celebrities, it has been transformed by the democratizing and dataization

(yes, a word) of the web. Of the three Buy It To Try It ecommerce models,

this one takes relationship-building the furthest, quite simply because, as

retail analyst Marshal Cohen says, “What the customer is interested in is what

comes before and after the transaction—they want help making purchases

in a personal way.” Cohen also says personal-shopping sales account for

about 10% of a store’s fashion business, a percentage the e-stylist cottage

industry aims to raise by mixing art and science, or, more precisely, mixing

personal merchandisers, buyers and stylists’ judgments with data analytics.

Bombfell, billing itself as men’s “stylist-picked clothes delivered,” explains in

its FAQ section that technology is used to surface recommendations for each

consumer based on fit and style, but that a “human stylist (the sort with years

of experience working in production, design and merchandising in men’s

fashion) has the final say.” Before you can say structural unemployment for

stylists thanks to algorithms and data mining, Keaton Row pairs consumers

with everyday fashionistas who apply to work on commission for the company

and can get better over time through dashboards, lookbooks and live chat with

their clients. And through the Marie Claire Masters of Style Program, a short-

term media partner, exceptional Keaton Row stylists were provided styling

tips by the magazine, allowing them to attract an even wider customer base.

Everywear, still in beta, taps founder and former Lucky editor-in-chief Brandon

Holley’s network of professional fashion stylists, and puts recommendations

in the context of a closet review, (information which is then licensed to stores),

a patently great way to decrease returns. So far, out of every 100 customers,

30 make a (full-priced) purchase.

BU

Y

IT

TO

T

RY

IT

B

UY

IT

T

O

TR

Y

IT

The JustFab survey, like many on these e-stylist sites, can seem like a blunt,

impersonal instrument for determining personal style: the consumer is presented

nothing but high heels for “girls’ night out,” but what if you’re going to the movies

(I ask myself)?

Behind the scenes, though, CEO Adam Goldenberg told the Wall Street Journal that they crunch data constantly, scoring customers on their likelihood to make

purchases within the next month based on how frequently they visit the site,

the number of items they have on their wish list, household income and other

attributes. This enables JustFab to keep the right merchandise in the right

amount in stock, and to refine the “personalized boutiques” of “hand-picked”

items each month.

Not surprisingly, the magic bullet for these e-stylist businesses is almost always

free returns, but incentives to keep the merchandise are strong: 70% of Stitch

Fix customers order a second box within 90 days, egged on perhaps by the 25%

discount they earn if they keep all five items.

And higher-end Tog+Porter charges a $50 styling fee on the first two “TogBoxes,”

but if the consumer keeps four or more items, the fee is applied toward the

clothing. Plus, there is a short seven-day return window, after which a 7%

restocking fee applies. In a smart practice that undoubtedly reduces returns,

Bombfell, the men’s retailer, sends a preview email that lets consumers edit or

cancel the assortment for 48 hours.

BU

Y

IT

TO

T

RY

IT

The e-stylist leader for menswear, a segment growing faster than

women’s, is Trunk Club, which Nordstrom purchased in 2014,

thereby providing the e-stylist with all the benefits of a brick and

mortar partner, such as access to Nordstrom’s larger supply chains

and infrastructure, including its UPS contract, which helps it cuts

costs. Trunk Club customers are provided access to Nordstrom’s

tailors to make adjustments to their clothes. In turn, Nordstrom

acquires new customers via Trunk Club, and gets increased foot

traffic as customers visit stores to return or exchange Trunk Club

purchases. With no stylist or subscription fees, not to mention a

Trunk Club for women in beta, Nordstrom is signaling clearly that it

will invest what it takes to develop more personal(ized) brick-and-

click relationships with its consumers.

Media/magazines are another potent partner for e-stylist companies,

the stylist in this case being the magazine’s editorial content and

its style writers/bloggers, as in the Thrillest.com/JackThreads.com

merger. Speaking to Fortune back in 2013, Thrillest Media Group

CEO Dan Lerer boasted: “This is going to be the new model all

media outlets follow online. Why would you want people to read

about something at your site and then go somewhere else to buy it?”

His aim has been for each of TMG’s sites to sell, in an online store,

merchandise that closely aligns with its content.

Apparently agreeing with Lerer’s vision, Time Inc. recently announced

a strategic investment in Keaton Row in order to expand its fashion

and beauty network. According to Evelyn Webster, executive vice

president of Time Inc.: “Our fashion brands, including InStyle and

People Stylewatch, are highly transactional. Keaton Row’s peer-to-

peer social commerce model matches our sensibility and will open

up an array of e-commerce opportunities.”

BU

Y

IT

TO

T

RY

IT

Conclusion: Why Buy It To Try It MattersAs retailers’ return policies have become more critical to consumers’ decisions

to buy, retailers have dealt with the risk of online shopping in other ways as

well: by vastly improving their decision support with customer reviews, editorial

fit tips and size guides, fit technology like Clothes Horse and avatar-based

Fits.me, how-to guides (QVC decreased returns with instructional videos on

gadgets like beauty tools and vacuum cleaners), better product visualization, a

record or “closet” of past purchases so favorites and sizes can be referenced, in

short, a wide-ranging panoply of techniques designed to take the unforeseeable

out of the process. But despite these improvements, returns are inevitable, and

from these lemons have come the lemonade of three novel ecommerce models:

home try-on, subscription shopping, and e-stylist.

Resource/Ammirati’s VP of Omni-Commerce Klay Huddleston says: “We are

seeing an ecommerce industry begin to innovate with new models because of the

omni investments they’ve made in three key areas: distribution centers and supply

chain systems designed for omni-channel fulfillment, ecommerce platforms that

support personalized experiences across device, and CRM systems that support

a single view of the customer.”

These innovative ecommerce models don’t focus merely on the back half of

the purchase funnel. They’ve found ways to unshackle the purchase journey

from a transaction mentality and think more experientially—fostering a more

collaborative experience with the customer, allowing for more opportunities for

service excellence that, ultimately, leads to more loyalty and more favorable and

reliable conversion rates. Moreover, once consumer habits are locked in due to

the value-add of these ecommerce models, it becomes harder for competitors to

penetrate the service line of defense a retailer has erected around their products.

The never-ending race to keep the services meaningful, however, cannot be

underestimated. One day, free shipping and free returns, the next day, some

equivalent, perhaps, of Amazon Prime value-adds like streaming content and

cloud storage.

BU

Y

IT

TO

T

RY

IT

What’s Next for Conditional Buying?Consumer awareness of planned obsolescence is growing, thanks

to Apple’s hugely successful Trade-In Program (which now includes

non-Apple smartphones and PCs), among others. Consequently,

the consumer practice of buying products that, after a period of

time, will retain trade-in value or resale marketplace value is gaining

ground. Neiman Marcus and Saks recently partnered with luxury

consignment e-merchant TheRealReal to capture some of the value

of this practice, offering gift cards for the consignment of luxury

goods—plus an extra 10% added to their payout at Neiman Marcus.

TheRealReal CEO and founder Julie Wainwright told Fortune that

by boosting the value of secondhand luxury goods in this manner,

shoppers see more value in buying them firsthand from these

department stores. Watch for more of these resale partnerships in

the returns economy.

Dr. Nita Rollins

Director of Thought Leadership & Cultural Insights

CONTACT US

Contact name goes here with informationLorem ipsum dolor sit amet, consectetur adipiscing elit. Quisque nec mi sit amet

lectus vestibulum congue. Nam sollicitudin convallis vulputate. Donec eget

consectetur lacus, sed pretium ex.

RESOURCEAMMIRATI.COM