Embed Size (px)

Citation preview

Rational speculative bubblesin MENA stock markets

Jung-Suk YuSchool of Urban Planning & Real Estate Studies, Dankook University,

Gyeonggi-do, South Korea, and

M. Kabir HassanDepartment of Economics and Finance, University of New Orleans,

New Orleans, Louisiana, USA

Abstract

Purpose – The purpose of this paper is to examine the existence of rational speculative bubbles inthe Middle East and North African (MENA) stock markets.

Design/methodology/approach – To complement shortcomings of the traditional bubble tests,such as unit root tests and cointegration tests, mainly relying on expectations of future steams ofdividends, the authors employ fractional integration tests and duration dependence tests.

Findings – Despite recent extreme fluctuations of MENA stock markets, fractional integration testsbuilt on autoregressive fractionally integrated moving average models do not support the possibilityof bubbles in the MENA stock markets. Similarly, duration dependence tests based on nonparametricNelson-Aalen hazard functions not only reject the existence of bubbles but also support equality ofhazard functions between domestic and the US-based investors without regard to the rapid financialliberalization and integration in the MENA stock markets.

Originality/value – The reliable results of bubble tests of the MENA stock markets providedomestic and international investors as well as policy makers with invaluable benchmark to betterunderstand the irregular and highly fluctuating stock market behaviors of the MENA stock marketscompared to other developed and emerging stock markets. For domestic and international investors,the formal analysis of MENA stock markets behavior including rational speculative bubbles will helpthem in their portfolio decisions and hedging purposes. Similarly, the empirical results of bubble testsin the paper will be also helpful to policymakers in MENA countries to take actions to improve thefunctioning of these dynamic markets.

Keywords Economic growth, Stock markets, Middle East, North Africa

Paper type Research paper

1. IntroductionReal economic growth rate across the Middle East and North African (MENA) regionaveraged 5.8 percent in 2008, creating benign prospects for most MENA countries inthe region. The Qatar is expected to be the MENA’s fastest growing economy in 2009,with GDP rising by 7.56 percent following its 9.93 percent expansion in 2008. In March2006, Abu Dhabi Commercial Bank launched the first Swiss franc (Sfr)-denominatedFRN for a Middle Eastern bank, with a Sfrs 300 million five-year deal led by BNP

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1086-7376.htm

This paper is a revised version of a working paper titled in “Rational speculative bubbles: anempirical investigation of the Middle East and North African (MENA) stock markets”co-authored by Jung-Suk Yu and M. Kabir Hassan at the University of New Orleans(www.business.uno.edu/econ/workingpapers/2006WP/12-MENA_Bubbles_UNO2007.pdf).The authors would also like to thank anonymous referees for helpful comments on earlier drafts.

Rationalspeculative

bubbles

247

Studies in Economics and FinanceVol. 27 No. 3, 2010

pp. 247-264q Emerald Group Publishing Limited

1086-7376DOI 10.1108/10867371011060054

Paribas which was placed entirely with Swiss accounts for the purpose of riskdiversification from the US dollar deals (EuroWeek, 2006).

While the current state of the economies of the MENA region suggests thateconomic growth will continue to be solid, one may argue that the 10-79 percentincreases in the monthly stock price index returns for most MENA regions were asymptom of persistent deviations of stock prices from the market fundamentals calledrational speculative bubbles, fads, sunspots, or self-fulfilling prophecies as observed inNASDAQ (between November 1998 and March 2000) and Chinese stock market (fromJuly 1994 till June 2001). However, the no-bubble hypothesis cannot be rejected easily ifnonobservable fundamental variables, such as investor rational expectations andmarket sentiment, are the cause of the rapid and sharp divergence of indexes fromfundamental values in the MENA stock markets.

Therefore, for policy-making decisions and international portfolio diversificationpurposes, it is very important to identify whether rational speculative bubbles exist inthe MENA stock market. For example, Chan et al. (2003) explicate that if rationalbubbles are not present, then it is only necessary to take control of the marketfundamentals in conducting monetary policy. Otherwise, positive policy action will beneeded to control expectations from the bubble path.

However, regardless of capital market growth potentials, sizes and rapid financialliberalization in the MENA countries, information on the MENA stock markets tointernational and domestic investors who is seeking portfolio diversification for hedgingpurposes is generally less available than in other financial markets. In the similar vein,despite the potential benefits of portfolio diversification in emerging markets in generaland MENA countries in particular, there is a lack of research and relatively much lessis known about the existence of rational speculative bubbles of MENA stock markets.

For developed and other emerging markets, most previous studies (Brooks andKatsaris, 2003; Chang et al., 2007; Gurkaynak, 2008, among others) have applied bubbletests for integer orders of integration to the log dividend yield or have tested for integercointegration between stock dividends and prices. However, in this paper, tocomplement and overcome well-known shortcomings of the traditional bubble tests,such as unit root tests and cointegration tests, mainly relying on expectations of futuresteams of dividends, we employ newer approaches – fractional integration tests andduration dependence tests – to investigate the evidence of rational speculative bubblesin the MENA stock markets.

For fractional integration tests relying on autoregressive fractionally integratedmoving average (ARFIMA) models, Cunado et al. (2007) test for the presence of rationalbubbles in the Standard & Poor’s (S&P) 500 stock market index by means of amethodology based on fractional processes. Koustas and Serletis (2005) also indicate thatthe notion of fractional integration allows more flexible modeling of the low frequencydynamics of stock prices, dividends, and their equilibrium relationship, while allowingsignificant deviations from equilibrium in the short run. They yield robust rejections ofthe null hypothesis of rational bubbles based on tests for fractional integration andconclude that a fractionally integrated dividend yield is inconsistent with rationalbubbles in annual SP500 composite stock market index from 1871 through 2000.

In addition, many financial researchers have supported duration dependence testsbased on survival analysis in many distinct academic contexts (McQueen and Thorley,1994; Cochran and DeFina, 1996; Chan et al., 1998; Cameron and Hall, 2003; Tudela, 2004;

SEF27,3

248

Buehler et al., 2006; Zhang, 2008; Ali et al., 2009). Traditionally, researchers havepreferred fitting parametric hazard functions such as log-logistic, exponential, Weibull,and Gompertz specifications along with semiparametric tests based on Cox regressionmodel. However, we find that nonparametric hazard functions have much bettersmall-sample properties and are more intuitive to interpret whether hazard functions isdecreasing or increasing. Therefore, we estimate nonparametric Nelson-Aalensmoothed hazard functions together with traditional parametric and semiparametrichazard specifications to investigate duration dependence in runs of positive excessreturns of the MENA stock markets because we have relative small sizes of samples tofit parametric hazard functions. We firmly believe that our approach to plotnonparametric smoothed hazard functions is more reliable to obtain the robustempirical results of duration dependence tests to identify the existence of bubbles in theMENA stock markets.

We summarize the main results as follows. Despite recent extreme fluctuations ofMENA stock markets, we do not find strong evidence of rational speculative bubbles inthe perspective of both domestic and the US-based investors. Fractional integrationtests built on ARFIMA models do not support the possibility of bubbles in the MENAstock markets. Similarly, duration dependence tests derived from nonparametricNelson-Aalen hazard functions strongly reject the existence of bubbles. In addition, itseems that domestic and the US-based investors do not observe rational speculativebubbles in the MENA region, evidenced by the statistically identical hazard functionsacross them, although MENA countries have recently experienced the rapid financialliberalization and integrations with developed countries.

The organization of the paper is the following. In Section 2, provide sample selectioncriteria and descriptive statistics on the MENA stock markets data. Section 3 pointsout empirical challenges of traditional econometric tests to detect rational speculativebubbles. Section 4, describe the newer approaches of rational speculative bubbleidentification. Section 5 analyzes the empirical results. Section 6 concludes the paper.

2. Data and descriptive statistics2.1 Data and sample selection criteriaTo investigate whether rational speculative bubbles exist or not in the MENA region, wecollect monthly S&P/International Finance Corporation Global (IFCG) price indexes ofthe eight MENA stock markets of Bahrain (1999:01-2003:03), Egypt (1996:01-2003:03),Jordan (1979:01-2003:03), Morocco (1996:01-2003:03), Israel (1997:01-2003:03), Oman(1999:01-2003:03), Saudi Arabia (1998:01-2003:03), and Turkey (1987:01-2003:03). Allstock indexes are expressed in local currencies and the US dollar denomination toexamine both domestic and the US-based investors’ perspectives. Then, we computemonthly simple returns rather than continuous compounded returns obtained by logdifferences to perform duration dependence tests to examine the existence of rationalspeculative bubbles in the MENA stock markets.

In addition, reliable dividend yields data are essential to perform formaleconometric bubble tests such as fractional integration tests. Therefore, we considerslightly different sample periods of dividend yields for MENA region from those ofS&P/IFCG price indexes: Bahrain (2000:01-2003:03), Egypt (1996:12-2003:03), Jordan(1984:12-2003:03), Morocco (1996:12-2003:03), Israel (1997:11-2003:03), Oman (2000:01-2003:03), Saudi Arabia (1998:11-2003:03), and Turkey (1987:11-2003:03).

Rationalspeculative

bubbles

249

The source of data is the Emerging Markets Data Base published by S&P’s. Webelieve that S&P/IFCG price indexes are more suitable for our study since they reflectadjusted share price changes and represents stock market performance without takinginto account of restrictions on foreign investors from the domestic investor perspective.According to S&P/IFCG index stock selection guidelines, all of MENA stocks includedin S&P/IFCG indexes must be actively traded and target market share should consist of60-75 percent of total market capitalization. Of course, they should be well-diversifiedacross different industries. Therefore, S&P/IFCG Indexes are intended to representthe performance of the most active stocks in their respective stock markets and to bethe broadest possible indicator of market movements.

2.2 Descriptive statisticsIn Table I, we report descriptive statistics of monthly index returns for eight MENAstock markets. During our sample periods, most of the MENA stock marketsexperienced severe stock markets fluctuations. For the domestic investors’ perspective,Egypt and Turkey are somewhat extreme, evidenced by 7.4 and 19.64 percent ofstandard deviations. Maximum and minimum monthly returns for Egypt and Turkeyare 26.14 percent (79.33 percent) and 211.98 percent (239.27 percent), respectively.Similarly, for the US-based investors’ perspective, Israel and Turkey have the highestuncertainty in their monthly stock market movements among others. Maximum andminimum monthly returns for Israel and Turkey are 14.53 percent (71.29 percent)and 219.07 percent (240.66 percent), respectively.

We also find that except Morocco, Israel, and Saudi Arabia, monthly indexreturns for the MENA stock markets are far from normally distributed with positive ornegative skewness and leptokurtosis as we can see from significant Jarque-Berastatistics. Especially, although Israel suffered the largest fluctuations on marketmovements for the perspective of the US investors, it seems that those volatilities didnot contribute to leptokurtosis, evidenced by the lowest excess kurtosis value (2.7206)and insignificant Jarque-Bera statistics (3.0571). Therefore, maximum and minimumvalues of Israel might be considered outliers since they cannot be representatives ofnormal market movements of Israel.

In Figure 1, we illustrate theoretical quantile-quantile (QQ) plots for the MENA stockmarkets for the perspective of the US-based investors. Although some of countriesinclude significant numbers of outliers in QQ plots, they might result from temporary orspurious shocks not directly related with bubbles, evidenced by insignificant values ofthe Ljung-Box portmanteau test statistics for 12 autocorrelations, Q(12), except Morocco.Therefore, we should be equipped with further formal econometric tests to detect theexistence of bubbles in those rapidly growing MENA stock markets for various practicaland academic reasons such as investments, portfolio diversifications, riskmanagements, and monetary policy and regulation purposes.

3. Empirical challenges of traditional bubble testsAccording to theories of bubbles (Brooks and Katsaris, 2003; Kirman and Teyssiere,2005; Cunado et al., 2007), the actual MENA stock market indexes deviate from thefundamental values if Bubblet . 0. In this case, the markets indexes are called to haverational speculative bubbles:

SEF27,3

250

Bah

rain

Eg

yp

tJo

rdan

Mor

occo

Isra

elO

man

Sau

di

Ara

bia

Tu

rkey

Sam

ple

per

iod

s19

99:0

1-2

003:

0319

96:0

1-2

003:

0319

79:0

1-2

003:

0319

96:0

1-2

003:

0319

97:0

1-2

003:

0319

99:0

1-2

003:

0319

98:0

1-2

003:

0319

87:0

1-2

003:

03P

anel

A:

Dom

esti

cin

vest

ors’

pers

pect

ive

Mea

n2

0.00

362

0.00

250.

0076

0.00

710.

0096

0.00

050.

0052

0.06

16M

edia

n2

0.00

312

0.01

222

0.00

110.

0030

0.01

232

0.02

370.

0028

0.02

63M

axim

um

0.10

850.

2614

0.18

190.

1513

0.14

720.

1889

0.10

460.

7933

Min

imu

m2

0.11

242

0.11

982

0.12

882

0.10

732

0.16

772

0.11

842

0.12

592

0.39

27S

D0.

0361

0.07

480.

0446

0.04

800.

0674

0.06

590.

0447

0.19

64S

kew

nes

s0.

1406

1.02

580.

9979

0.54

982

0.41

491.

0975

20.

2123

1.01

56K

urt

osis

5.35

724.

2276

4.97

253.

2317

2.87

754.

1264

3.39

814.

6300

Q(1

2)0.

0810

20.

0140

0.00

400.

2130

0.05

202

0.13

100.

0190

20.

0350

(0.2

960)

(0.5

160)

(0.8

620)

(0.0

050)

(0.8

740)

(0.2

070)

(0.7

640)

(0.5

060)

Jarq

ue-

Ber

a11

.974

920

.721

495

.477

84.

5777

2.19

8912

.934

80.

8890

55.1

115

(0.0

025)

(0.0

000)

(0.0

000)

(0.1

014)

(0.3

331)

(0.0

016)

(0.6

411)

(0.0

000)

Panel

B:

US

-base

din

vest

ors’

pers

pect

ive

Mea

n2

0.00

362

0.00

860.

0046

0.00

540.

0054

0.00

050.

0052

0.02

26M

edia

n2

0.00

342

0.01

832

0.00

140.

0040

0.01

132

0.02

370.

0027

20.

0087

Max

imu

m0.

1087

0.25

880.

1637

0.15

820.

1453

0.18

890.

1052

0.71

29M

inim

um

20.

1121

20.

1262

20.

1288

20.

0980

20.

1907

20.

1184

20.

1260

20.

4066

SD

0.03

600.

0730

0.04

550.

0493

0.07

640.

0659

0.04

470.

1994

Sk

ewn

ess

0.14

771.

0476

0.62

090.

3040

20.

4744

1.09

842

0.21

140.

8369

Ku

rtos

is5.

3561

4.48

094.

4293

2.97

342.

7206

4.12

833.

4014

4.11

87Q

(12)

0.08

102

0.00

900.

0030

0.17

000.

1330

20.

1310

0.01

902

0.04

80(0

.304

0)(0

.287

0)(0

.788

0)(0

.042

0)(0

.870

0)(0

.209

0)(0

.765

0)(0

.491

0)Ja

rqu

e-B

era

11.9

813

23.8

642

43.4

703

1.34

263.

0571

12.9

605

0.89

1932

.932

8(0

.002

5)(0

.000

0)(0

.000

0)(0

.511

0)(0

.216

9)(0

.001

5)(0

.640

2)(0

.000

0)

Notes:

Th

eta

ble

des

crib

esd

escr

ipti

ve

stat

isti

csof

the

eig

ht

ME

NA

stoc

km

ark

etm

onth

lyin

dex

retu

rns;

the

Q(1

2)is

the

Lju

ng

-Box

por

tman

teau

test

stat

isti

cfo

r12

auto

corr

elat

ion

s;th

ep-

val

ues

are

rep

orte

din

par

anth

eses

Table I.Descriptive statistics of

monthly index returns forthe MENA countries

Rationalspeculative

bubbles

251

Figure 1.Theoretical QQ plots forthe MENA stock markets(the US-based investors’perspective)

–4–3–2–101234

–0.1

2–0

.08

–0.0

40.

000.

040.

080.

12

Bah

rain

Normal quantile

–3–2–101234

–0.2

–0.1

0.0

0.1

0.2

0.3

Egy

pt

–4–3–2–101234

–0.1

5–0

.10

–0.0

50.

000.

050.

100.

150.

20

Jord

an

–3–2–101234

–0.1

5–0

.10

–0.0

50.

000.

050.

100.

150.

20

Mor

occo

–3–2–10123

–0.2

0–0

.15

–0.1

0–0

.05

0.00

0.05

0.10

0.15

Isra

el

Normal quantile

–3–2–101234

–0.1

5–0

.10

–0.0

50.

000.

050.

100.

150.

20

Om

an

–3–2–10123

–0.1

5–0

.10

–0.0

50.

000.

050.

100.

15

Saud

i ara

bia

–3–2–101234

–0.6

–0.4

–0.2

0.0

0.2

0.4

0.6

0.8

Tur

key

SEF27,3

252

MENAat ¼ MENAf

t þ Bubblet þ mt

¼X1k¼1

1

ð1 þ i ÞkEtðDivtþkÞ þ

EtðBubbletþ1Þ

ð1 þ i Þþ mt

ð1Þ

where MENAat is the actual index of the MENA stock markets considered in time t, Divt

is the dividend at period t, MENAft is the fundamental value of the index in time t, i is

the market discount rate, Eð · Þ is the mathematical expectation operator, and mt is anidentically and independently distributed (i.i.d.) stochastic process. Bubblet is the valueof the bubble component in time t and it is entirely consistent with rationalexpectations and the time path of expected returns.

However, previous studies on empirical tests to detect rational speculative bubblesconcentrating on developed and emerging stock markets still remain inconclusive.Therefore, many financial economists have tried to explain the main sources of thecontroversy on the tests of bubbles detection. For example, Blanchard (1979) explainsthat speculative bubbles may take all kinds of shapes and their fundamentals may bestochastic. Kaizoji (2000) argues that bubbles and crashes come from the collectivecrowd behavior of many interacting agents. In theory, although an asset’s fundamentalvalue can be obtained by discounting the asset’s future earnings stream, the difficultiesin estimating the earnings stream and in proper discounting make the identification ofbubbles empirically challenging (Chen, 2001). Gurkaynak (2008) surveys the formaleconometric tests of asset price bubbles and concludes that we cannot distinguishbubbles from time-varying or regime-switching fundamentals.

More importantly, many researchers have also reported that it is very difficult todetect rational speculative bubbles precisely using traditional econometric tests, suchas unit root tests and cointegration tests, mainly relying on expectations of futuresteams of dividends especially in small samples. For example, Taylor and Peel (1998)point out that although rational speculative bubbles imply noncointegration of index orstock prices and dividends, the traditional cointegration tests are subject to sizedistortion or specification error especially in small samples. Owing to these undesirableproperties of cointegration tests, they apply the robust noncointegration test withmuch smaller size distortion and good power characteristics to a long run of the US realstock price and dividend data, then reject the bubbles hypothesis on the US data. Morerecently, using SP 500 log dividend yields, Koustas and Serletis (2005) show thataugmented Dickey-Fuller and Phillips-Perron unit-root tests are unable to reject a unitroot in the price-dividend ratios (dividend yields), which suggests the lack of acointegrating relationship between stock prices and dividends. Therefore, in thefollowing section, we briefly summarize the general idea of newer approaches toidentify rational speculative bubbles in the MENA stock markets.

4. Newer econometric tests to identify rational speculative bubbles4.1 Fractional integration testsTo be consistent with recent study (Cunado et al., 2005; Koustas and Serletis, 2005), weemploy ARFIMA model for bubble detections of a univariate time series of log(dividend yields). With a fractional integration parameter d, the ARFIMA ( p, d, q) iswritten as:

Rationalspeculative

bubbles

253

FðLÞð1 2 LÞdð yt 2 mtÞ ¼ QðLÞ1t ð2Þ

and the fractional differencing operator, ð1 2 LÞd , is defined by:

ð1 2 LÞd ¼ 1 2 dL 2dð1 2 d Þ

2!L 2 2

dð1 2 d Þð2 2 d Þ

3!L 3 2 . . . ð3Þ

where, yt is log (dividend yields), mt is the mean of dividend yields and L is the lagoperator, Lkyt ¼ yt2k:

FðLÞ ¼ 1 2Xp

i¼1

fiLi andQðLÞ ¼ 1 þ

Xq

i¼1

uiLi

represent stationary AR and MA polynomial in the lag operation L. The p and q areintegers, but d is real values, respectively. Furthermore, we assume 1t , N ð0;s 2Þ.The ARFIMA ( p, d, q) models nests the more familiar autoregressive movingaverage (ARMA) (or “Box-Jenkins”) (when d ¼ 0) or autoregressive integrated movingaverage (when d is a positive integer) models as special cases. The ARMA part of themodel is also assumed invertible and stationary, which means that all roots ofFðLÞ ¼ 0 and QðLÞ ¼ 0 are outside the unit circle.

We check the log dividend yield for a fractional exponent in the differencing processusing the exact maximum likelihood (EML) since the unit-root and cointegration testsallow for only integer orders of integration. We also calculate the standard errors by theinverse of the Hessian, estimated by Broyden, Fletcher, Goldfarb, and Shanno algorithmto judge the significance of estimated parameter values. Fractionally integrated longmemory processes are different from both stationary, I ð0Þ, and unit-root processes, I ð1Þ,in that they are persistent but are also mean reverting. In addition, if rational speculativebubbles are present in the MENA stock markets, the fractional integrating parameter oflog dividend yields, d, should not be statistically equal to zero.

4.2 Duration dependence testsAs Cochran and DeFina (1996) point out, hazard functions are appropriate to examineduration dependence since they specify the probability that a particular state will endconditional on the time, which has been spent in the state. On the other hand,traditional time series approaches, such as cointegration tests and unit root testsprovide no information concerning the probability that a run will end or that deviationsfrom the mean will be completely dissipated although they can be useful in identifyingmean-reverting components in monthly returns of the MENA stock markets.

Therefore, first, we parameterize hazard functions to be consistent with traditionalapproaches (McQueen and Thorley, 1994; Chan et al., 1998, among others) along withsemiparametric Cox regression model for bubble identification. Then, second, we alsoperform bubble tests by plotting nonparametric Nelson-Aalen smoothed hazardfunctions, rather than by directly estimating parameterized hazard functions to considerthe relative small sample sizes of the MENA stock markets (For more technical details,Cleves et al., 2004).

4.2.1 Bubble tests based on semiparametric Cox proportional and parametric hazardsmodels. We estimate the following semiparametric Cox proportional hazards toidentify rational speculative bubbles in the perspective of domestic and the US-basedinvestors:

SEF27,3

254

Cox hiðtjCurrencyÞ ¼ h0ðtÞexp{b · Currency} ð4Þ

where h0ðtÞ is the base-line hazard at time t and b is a unknown parameter to estimate.The variable Currency is a dummy variable with values 1 or 0; it equals 1 in the case oflocal currency denomination and 0 otherwise. By definition, exp{b · Currency}is calledthe hazard ratio. In the semiparametric Cox proportional hazards models, the baselinehazard, h0ðtÞ, is given no particular parameterization and, in fact, is left unestimated.

We can also think of a variety of parametric hazard functions specificationsdepending on the expected shapes of hazard functions by making reasonableassumptions about the shape of the baseline hazard, h0ðtÞ. For example, theexponential model is the simplest of parametric hazard models because it assumes thatthe baseline hazard is constant:

Exponential hiðtjCurrencyÞ ¼ expðb0 þ b1 · CurrencyÞ ð5Þ

Similarly, the Weibull regression in the proportional hazard model can provide avariety of monotonically increasing or decreasing shapes of the hazard function, andtheir shape is determined by the estimated parameter p:

Weibull hiðtjCurrencyÞ ¼ pt p21expðb0 þ b1 · CurrencyÞ ð6Þ

Note that when p ¼ 1, the hazard is constant, and thus, the Weibull model reduces tothe exponential model. For other values of p, the Weibull hazard is not constant; it ismonotone decreasing when p , 1 and monotone increasing when p . 1. The Weibullis suitable for modeling data that exhibits monotone hazard rates.

The Gompertz distribution is an old distribution that has been extensively usedby medical researchers and biologists modeling mortality data. This distribution issuitable for modeling data with monotone hazard rates that either increase or decreaseexponentially with time, and the ancillary parameter g controls the shape of thebaseline hazard:

Gompertz hiðtjCurrencyÞ ¼ expðgtÞ expðb0 þ b1 · CurrencyÞ ð7Þ

If g is positive, the hazard function increases with time; if g is negative, the hazarddecreases with time; if g ¼ 0, the hazard function is expðb0Þ for all t, which is to saythat it reduces to the hazard from the exponential model. As such, we estimateparameter values and hazard ratios in each semiparametric and parametric hazardspecification to decide whether different currency denominations make shifts on thebubble identifications between domestic and the US-based investors.

4.2.2 Bubble tests based on the nonparametric Nelson-Aalen hazard functions. Wealso perform bubble tests by plotting an estimate of the hazard function, hðtÞ, by takingthe steps of the Nelson-Aalen cumulative hazard and smoothing them with a Gaussiankernel smoother, rather than by directly estimating parameterized hazard functions toconsider the relative small sample sizes of the MENA stock markets. The estimatednonparametric Nelson-Aalen hazard is calculated as a kernel smooth of the estimatedhazard contributions as obtained by sample hazard rates. The sample hazard rates,hi ¼ ðNiÞ=ðMi þ NiÞ, represents the conditional probability that a run ends at i, giventhat it lasts until i, where Ni is the count of runs of length i and Mi is the count of runswith a length greater than i.

Rationalspeculative

bubbles

255

The cumulative Nelson-Aalen estimator is defined as:

H ðtÞ ¼

Z t

0

hðuÞdu ð8Þ

where hð · Þ is the hazard function. The following nonparametric Nelson-Aalenestimator of cumulative hazard function, HðtÞ, has much better small-sampleproperties than corresponding parameterized ones:

HðtÞ ¼jjtj#t

X dj

nj

ð9Þ

where nj is the number at risk at time tj, dj is the number of failures at time tj, and thesum is over all distinct failure times less than or equal to t. For each observed run endstime tj, the estimated hazard contribution, DHðtjÞ, can be obtained by:

DHðtjÞ ¼ HðtjÞ2 Hðtj21Þ ð10Þ

Therefore, we can estimate the hazard functions with:

hðtÞ ¼ b21XD

j¼1

Kt 2 tj

b

� �DHðtjÞ ð11Þ

for some symmetric Gaussian density function (the kernel) and bandwidth b, thesummation is over the D times at which run ends occur.

In any case, the null hypothesis (H0) of no duration dependence implies that theprobability of a run ending is independent of the prior returns or that positive andnegative abnormal returns are random. The alternative hypothesis (H1) of durationdependence suggests that the probability of a positive run ending should have adecreasing function of the run length. Therefore, if bubbles are detected, the samplehazard rates should decrease as the run length increases (see McQueen and Thorley(1994) and Chan et al. (1998) for further detailed explanations on duration dependencetests to detect rational speculative bubbles).

5. ResultsSince rational speculative bubbles must be persistent to survive several months oryears until market crashes, we should observe statistically significant positiveautocorrelations, skewness, and leptokurtosis due to excess returns during bubbleperiods if bubbles exist in the MENA stock markets. In our study, although summarystatistics show excess kurtosis and positive or negative skewness evidenced bysignificant Jarque-Bera statistics for Morocco, Israel, and Saudi Arabia, many otherfactors not directly related with bubbles can affect market returns. Therefore, the muchcare should be taken to associate higher moments of market returns with thepossibility of rational speculative bubbles. However, unlike Jarque-Bera normalitytests, most MENA stock markets do not show significant positive autocorrelationsexcept Morocco based on the Ljung-Box Portmanteau tests statistics for12 autocorrelations, Q(12), supporting no bubbles to some degree in the MENAstock markets.

SEF27,3

256

The results of these autocorrelation tests question whether the MENA stockmarkets really experienced rational speculative bubbles during our sample periodseven though they suffered a lot of extreme positive or negative monthly returns. AsKoustas and Serletis (2005) insightfully points out, rational speculative bubbles mustbe continually expanding and persistent in order to survive since stock buyers will paya price higher than that suggested by the fundamentals if they believe that someoneelse will subsequently pay an even higher price. Therefore, statistically significantpositive autocorrelations among monthly returns are prerequisite for rationalspeculative bubbles to be present in the MENA stock markets.

The estimation results of fractional integration tests via EML methods in Panel A ofTable II for log dividend yields of the MENA stock markets strongly support theresults of the Ljung-Box autocorrelations tests statistics shown in Table I. We also testwhether fractional integrating parameter ðdÞ is statistically 0 (no unit root) or 1 (unitroot) by performing linear restriction tests in Panel B of Table II. Unlike previousstudies (e.g. Brooks and Katsaris, 2003; Gurkaynak, 2008, among others) that havetested for integer orders of integration, we are able to obtain robust rejections of a unitroot in the log dividend yield from the linear restriction tests. Therefore, we confirmthat fractional integrating parameters of log dividend yields, d, are not statisticallydifferent from zero and reveal no bubbles based on ARFIMA approaches, implyingstationarity of log dividend yields.

In recent study, Koustas and Serletis (2005) also report similar empirical findings asours using SP500 log dividend yields in that they also find the possibility of bubblesbased on unit root tests, but they reject null hypothesis of bubbles based on ARFIMAmethods. They clarify that fractional integration tests are robust to the choice ofparametric estimator of the fractional differencing parameter and data frequency, andbootstrap inference fully supports the estimation results. Therefore, our results of thefractional integration tests are inconsistent with rational speculative bubbles in theMENA stock markets.

In Panel A of Table II, the parameters, f and u, are the estimators of the first orderAR(1), and MA(1), processes in ARFIMA (1, d, 1) models, respectively. To check modeladequacy, we also tabulate residual tests for normality, autoregressive conditionalheteroskedasticity (ARCH) effects, and serial correlations (Portmanteau tests) in PanelC of Table II along with the p-values in parantheses.

For the MENA markets, we can reject the null hypothesis of normality of residualsexcept Morocco and Israel even after the ARFIMA fitting, which suggests usingalternative fatter-tailed distributions such as skewed t-distribution and generalizederror distribution rather than simply assuming normal distributions. For ARCH tests,it appears that ARFIMA settings are well-suited to fit residuals in all of the MENAstock markets even though we assume constant volatility rather than time-varyinggeneralized autoregressive conditional heteroskedasticity-families for the convenience.For Portmanteau tests, it is likely that our ARFIMA (1, d, 1) model successfullycaptures the serial correlations of residuals except Israel. However, although furthercomplexity of model setups considering alternative fatter-tailed distributions andhigher orders of AR or MA processes might improve the overall fits of our ARFIMAmodels, we do not believe that these additional computational efforts will change ourmain results of fractional cointegration tests to detect bubbles in the MENA stockmarkets.

Rationalspeculative

bubbles

257

Bah

rain

Eg

yp

tJo

rdan

Mor

occo

Isra

elO

man

Sau

di

Ara

bia

Tu

rkey

Sam

ple

per

iod

s20

00M

01-2

003M

0319

96M

12-2

003M

0319

84M

12-2

003M

0319

96M

12-2

003M

0319

97M

11-2

003M

0320

00M

01-2

003M

0319

98M

11-2

003M

0319

87M

11-2

003M

03P

anel

A:

Para

met

eres

tim

ate

sd

20.

9975

20.

0624

0.06

932

0.08

082

0.18

992

0.05

472

0.16

072

0.31

02(0

.202

0)(0

.848

0)(0

.829

0)(0

.853

0)(0

.382

0)(0

.879

0)(0

.695

0)(0

.448

0)A

R1(f

)0.

8368

0.84

490.

8084

0.81

040.

9724

0.83

880.

8967

0.86

37(0

.042

0)(0

.000

0)(0

.000

0)(0

.002

0)(0

.000

0)(0

.000

0)(0

.000

0)(0

.000

0)M

A1(u

)0.

1094

0.39

352

0.00

890.

3353

0.18

502

0.04

310.

0446

0.07

79(0

.777

0)(0

.063

0)(0

.974

0)(0

.168

0)(0

.550

0)(0

.883

0)(0

.901

0)(0

.814

0)P

anel

B:

Tes

tsfo

rlin

ear

rest

rict

ion

d¼

01.

6873

0.03

700.

0475

0.03

490.

7831

0.02

340.

1560

0.58

80(0

.194

0)(0

.847

4)(0

.827

3)(0

.851

6)(0

.376

2)(0

.878

3)(0

.692

8)(0

.443

2)d¼

16.

7659

10.7

321

8.57

206.

2570

30.7

339

8.69

358.

1384

10.4

895

(0.0

093)

(0.0

011)

(0.0

034)

(0.0

124)

(0.0

000)

(0.0

032)

(0.0

043)

(0.0

012)

Panel

C:

Res

idualte

sts

for

mod

eladeq

uacy

Nor

mal

ity

17.3

540

47.2

560

38.2

540

4.19

132.

6637

7.47

1133

.522

012

.653

0(0

.000

2)(0

.000

0)(0

.000

0)(0

.123

0)(0

.264

0)(0

.023

9)(0

.000

0)(0

.001

8)A

RC

H0.

0458

0.05

630.

2528

0.22

750.

4366

3.14

170.

0149

1.74

92(0

.831

7)(0

.813

8)(0

.618

3)(0

.636

4)(0

.513

2)(0

.085

3)(0

.903

3)(0

.194

8)P

ortm

ante

au0.

6899

2.63

762.

5505

0.94

408.

4031

1.49

011.

8141

0.82

78(0

.875

6)(0

.450

9)(0

.466

2)(0

.814

8)(0

.038

4)(0

.684

6)(0

.611

9)(0

.842

8)

Notes:

Th

eta

ble

rep

orts

the

esti

mat

ion

resu

lts

offr

acti

onal

inte

gra

tion

test

sv

iaE

ML

met

hod

s;w

eal

sote

stif

frac

tion

alin

teg

rati

ng

par

amet

er(d

)is

stat

isti

call

y0

(no

un

itro

ot)

or1

(un

itro

ot)

by

per

form

ing

lin

ear

rest

rict

ion

test

s;th

ep

aram

eter

s,f

andu

,are

the

esti

mat

ors

ofth

efi

rst

ord

erA

R(1

)an

dM

A(1

)pro

cess

esin

AR

FIM

A(1

,d,1

)mod

els;

toch

eck

mod

elad

equ

acy

,we

also

tab

ula

tere

sid

ual

test

sfo

rn

orm

alit

y,A

RC

Hef

fect

s,an

dse

rial

corr

elat

ion

s(P

ortm

ante

aute

sts)

;th

ep-

val

ues

are

rep

orte

din

par

anth

eses

Table II.Fractional integrationbubble tests in the MENAstock markets

SEF27,3

258

In Table III, to perform duration dependence tests, we compute the actual number ofpositive runs (sequences of excess returns of the same sign) for monthly positive excessindex returns during our sample periods for the perspectives of both domestic and theUS-based investors. We find the longest positive runs (ten months) in Egypt (sampleperiod: 1996:01-2003:03), next 8 months for Bahrain (sample period: 1999:01-2003:03). Allof the MENA countries experience at least five-month positive runs for monthly positiveexcess index returns during our sample periods. However, it seems that those numbersof positive runs are too short, transient, and spurious to be considered as bubbles.

For example, before the worst market crash like Black Thursday (October 24, 1929),the bull markets lasted about 63 months. The presence of a positive and increasingbubble premium continued about 18 months before the crash of Black Monday(October 19, 1987). When the NASDAQ index of technology stocks in the US peaked,the market tripled in value between November 1998 and March 2000 (17 months). Morerecently, the Chinese stock market index had risen 700 percent, propelled by china’sdouble-digit growth rates and surging corporate profitability from July 1994 till June2001 (84 months).

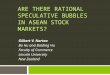

As we can also find from Figure 2, none of the nonparametric smoothed hazardfunctions is monotonically decreasing, implying no bubbles in the MENA stockmarkets. Even though the nonparametric Nelson-Aalen smoothed hazard functionshave different values of hazard rates except Bahrain, Oman, and Saudi Arabia,depending on the types of currency denominations, we observe that Jordan, Morocco,Israel, Saudi Arabia, and Turkey generally show increasing hazard functions, which arenot acceptable if bubbles exist in those markets. Bahrain, Egypt, and Oman also showdistinct patterns, which are not completely consistent with bubbles. Nonparametricsmoothed hazard functions initially increase then decrease.

In Table IV, we provide the comprehensive test results for equality of hazardfunctions between domestic and the US-based investors. Panel A and B of Table IVshows the estimation results of hazard ratios, expðbÞ, of semiparametric Cox andparametric proportional hazards models, respectively, when the currencies are US dollardenominated. It seems that the hazard ratios are insensitive to model specifications,such as Cox, Exponential, Weibull, and Gompertz models. In addition, all of hazard ratesare not only very close to 1 but also statistically insignificant, implying that currencydenominations do not make any difference for bubble identification for the MENA stockmarkets. We also obtain nonparametric statistical test results supporting the equality ofhazard functions between domestic and the US-based investors from log-rank,Wilcoxon, Tarone-Ware, and Peto-Peto tests in Panel C of Table IV. Therefore, we do notfind any statistically significant evidence of bubbles from both fractional integrationtests and duration dependence tests for all of the eight MENA stock markets.

6. ConclusionsWhen we consider sizable market capitalizations and the degree of liberalization in theMENA countries, we believe that the reliable results of bubble tests of the MENA stockmarkets could provide domestic and international investors as well as policy makerswith invaluable benchmark to better understand the irregular and highly fluctuatingstock market behaviors of the MENA stock markets compared to other developed andemerging stock markets. For domestic and international investors, the formal analysisof MENA stock markets behavior including rational speculative bubbles will help

Rationalspeculative

bubbles

259

Bah

rain

Eg

yp

tJo

rdan

Mor

occo

Isra

elO

man

Sau

di

Ara

bia

Tu

rkey

Pos

itiv

eru

ns

Len

gth

Cou

nt

Len

gth

Cou

nt

Len

gth

Cou

nt

Len

gth

Cou

nt

Len

gth

Cou

nt

Len

gth

Cou

nt

Len

gth

Cou

nt

Len

gth

Cou

nt

Panel

A:

Dom

esti

cin

vest

ors’

pers

pect

ive

16

18

139

111

110

17

16

129

23

25

216

21

27

22

24

211

31

31

33

34

32

31

41

38

41

51

43

41

41

51

51

51

81

101

51

52

51

71

62

Tot

al12

1664

1921

1113

49P

anel

B:

US

-base

din

vest

ors’

pers

pect

ive

16

110

138

112

110

17

16

127

23

25

217

22

29

22

24

211

31

31

38

32

31

31

41

37

41

41

43

42

41

51

51

42

81

101

52

51

51

71

51

61

71

Tot

al12

1869

2022

1113

48

Notes:

Th

eta

ble

rep

orts

the

resu

lts

ofd

ura

tion

dep

end

ence

test

sto

det

ect

the

pos

sib

ilit

yof

rati

onal

spec

ula

tiv

eb

ub

ble

s;fo

rth

isp

urp

ose,

we

com

pu

teth

eac

tual

nu

mb

erof

pos

itiv

eru

ns

for

mon

thly

pos

itiv

eex

cess

ind

exre

turn

sfo

rth

ep

ersp

ecti

ves

ofd

omes

tic

(Pan

elA

)an

dth

eU

S-b

ased

(Pan

elB

)in

ves

tors

;a

run

isd

efin

edas

ase

qu

ence

ofex

cess

retu

rns

ofth

esa

me

sig

n

Table III.Duration dependencebubbles tests in theMENA stock markets

SEF27,3

260

Figure 2.Nonparametric

Nelson-Aalen smoothedhazard functions

0.1

0.2

0.3

0.4

0.5

Haz

ard

rate

s

0.1

0.2

0.3

0.4

Haz

ard

rate

s

0 2 4 6 8

Run length

Bahrain

0 2 4 6 8 10

Run length

Egypt

0.3

0.4

0.5

0.6

0.7

Haz

ard

rate

s

1 2 3 4 5 6

Run length

Jordan

0.3

0.35

0.4

0.45

0.5

0.55

Haz

ard

rate

s

0 2 4 6 8

Run Length

Morocco

US-based investors

Local investors

0.35

0.4

0.45

0.5

0.55

0.6

Haz

ard

rate

s

1 2 3 4 5

Run length

Israel

0.38

0.4

0.42

0.44

0.46

Haz

ard

rate

s

1 2 3 4 5

Run length

Oman

0.26

0.28

0.3

0.32

0.34

0.36

Haz

ard

rate

s

0 2 4 6 8Run length

Saudi arabia

0.4

0.5

0.6

0.7

Haz

ard

rate

s

1 2 3 4 5Run length

Turkey

US-based investors

Local Investors

Rationalspeculative

bubbles

261

them in their portfolio decisions and hedging purposes. Similarly, the empirical resultsof bubble tests in this paper will be also helpful to policymakers in MENA countries totake actions to improve the functioning of these dynamic markets.

For this purpose, we extended the speculative bubble literature to the MENA stockmarkets in the perspectives of domestic and the US-based investors. This paper hasemployed fractional integration techniques and duration dependence tests based on theARFIMA models and nonparametric Nelson-Aalen smoothed hazard functions in theMENA stock markets. In this study, we do not find any strong evidence of rationalspeculative bubbles in the MENA stock markets without regard to local currency andthe US dollar denominations. Fractional integration tests do not support the possibilityof rational speculative bubbles in the MENA stock markets, evidenced by thestatistically zero fractional integrating parameter values of log dividend yields.Similarly, duration dependence tests strongly reject the existence of bubbles as well,supported by nondecreasing nonparametric Nelson-Aalen smoothed hazard functions.These test results to identify rational speculative bubbles in MENA region do not differbetween domestic and the US-based investors.

References

Ali, N., Nassir, A., Hassan, T. and Abidin, S. (2009), “Stock overreaction and financial bubbles:evidence from Malaysia”, Journal of Money, Investment and Banking, Vol. 11, pp. 90-101.

Blanchard, O.J. (1979), “Speculative bubbles, crashes and rational expectations”, EconomicsLetters, Vol. 3, pp. 387-9.

Bahrain Egypt Jordan Morocco Israel Oman Saudi Arabia Turkey

Panel A: Semiparametric tests based on Cox regression modelCox 1.0000 0.9544 1.0437 1.0298 0.9875 1.0000 1.0000 1.0586

(1.0000) (0.8910) (0.8060) (0.9280) (0.9670) (1.0000) (1.0000) (0.7800)Panel B: Parametric tests for proportional hazards modelsExponential 1.0000 0.9356 1.0551 1.0230 0.9790 1.0000 1.0000 1.0591

(1.0000) (0.8450) (0.7570) (0.9430) (0.9450) (1.0000) (1.0000) (0.2800)Weibull 1.0000 0.9166 1.0626 1.0772 0.9482 1.0000 1.0000 1.1404

(1.0000) (0.7980) (0.7260) (0.8170) (0.8620) (1.0000) (1.0000) (0.5180)Gompertz 1.0000 0.9356 1.0406 1.0928 0.9572 1.0000 1.0000 1.1276

(1.0000) (0.8450) (0.8190) (0.7840) (0.8860) (1.0000) (1.0000) (0.5550)Panel C: Nonparametric tests for equality of hazard functionsLog-rank 0.0000 0.0400 0.1400 0.0200 0.0000 0.0000 0.0000 0.2000

(1.0000) (0.8394) (0.7087) (0.8976) (0.9514) (1.0000) (1.0000) (0.6585)Wilcoxon 0.0000 0.0400 0.5700 0.0100 0.0000 0.0000 0.0000 0.1500

(1.0000) (0.8422) (0.4518) (0.9246) (0.9685) (1.0000) (1.0000) (0.7004)Tarone-Ware 0.0000 0.0400 0.4500 0.0000 0.0000 0.0000 0.0000 0.1900

(1.0000) (0.8347) (0.5009) (0.9809) (0.9452) (1.0000) (1.0000) (0.6613)Peto-Peto 0.0000 0.0400 0.5200 0.300 0.0000 0.0000 0.0000 0.1300

(1.0000) (0.8488) (0.4701) (0.8736) (0.9650) (1.0000) (1.0000) (0.7229)

Notes: This table provides hazard ratios in each of semiparametric (Panel A) and parametric (Panel B)hazard specifications to decide whether different currency denominations make shifts on the bubbleidentifications between domestic and the US-based investors; we also provide test results for equalityof hazard functions (Panel C) between domestic and the US-based investors; the p-values are reportedin parantheses

Table IV.Tests for equality ofhazard functions betweendomestic and theUS-based investors

SEF27,3

262

Brooks, C. and Katsaris, A. (2003), “Rational speculative bubbles: an empirical investigation ofthe London stock exchange”, Bulletin of Economic Research, Vol. 55, pp. 319-46.

Buehler, S., Kaiser, C. and Jaeger, F. (2006), “Merge or fail? The determinants of mergers andbankruptcies in Switzerland, 1995-2000”, Economics Letters, Vol. 90, pp. 88-95.

Cameron, A.C. and Hall, A.D. (2003), “A survival analysis of Australian equity mutual funds”,Australian Journal of Management, Vol. 28, pp. 209-26.

Chan, H.L., Lee, S.K. and Woo, K.Y. (2003), “An empirical investigation of price and exchangerate bubbles during the interwar European hyperinflations”, International Review ofEconomics and Finance, Vol. 12, pp. 327-44.

Chan, K., McQueen, G. and Thorley, S. (1998), “Are there rational speculative bubbles in Asianstock markets?”, Pacific-Basin Finance Journal, Vol. 6, pp. 125-51.

Chang, T., Chiu, C. and Nieh, C. (2007), “Rational bubbles in the US stock market? Furtherevidence from a nonparametric cointegration test”, Applied Economics Letters, Vol. 14,pp. 517-21.

Chen, N.K. (2001), “Asset price fluctuations in Taiwan: evidence from stock and real estate prices1973 to 1992”, Journal of Asian Economics, Vol. 12, pp. 215-32.

Cleves, M.A., Gould, W.W. and Gutierrez, R.G. (2004), An Introduction to Survival Analysis UsingSTATA, Revised ed., Stata Press, College Station, TX.

Cochran, S.J. and DeFina, R.H. (1996), “Predictability in real exchange rates: evidence fromparametric hazard models”, International Review of Economics and Finance, Vol. 5,pp. 125-47.

Cunado, J., Gil-Alana, L.A. and Gracia, F.P. (2005), “A test for rational bubbles in the NASDAQstock index: a fractionally integrated approach”, Journal of Banking & Finance, Vol. 29,pp. 2633-54.

Cunado, J., Gil-Alana, L.A. and Gracia, F.P. (2007), “Testing for stock market bubbles usingnonlinear models and fractional integration”, Applied Financial Economics, Vol. 17,pp. 1313-21.

Gurkaynak, R.S. (2008), “Econometric tests of asset price bubbles: taking stock”, Journal ofEconomic Surveys, Vol. 22, pp. 166-86.

Kaizoji, T. (2000), “Speculative bubbles and crashes in stock markets: an interacting-agent modelof speculative activity”, Physica A: Statistical Mechanics and its Applications, Vol. 287,pp. 493-506.

Kirman, A. and Teyssiere, G. (2005), “Testing for bubbles and change-points”, Journal ofEconomic Dynamics and Control, Vol. 29, pp. 765-99.

Koustas, Z. and Serletis, A. (2005), “Rational bubbles or persistent deviations from marketfundamentals?”, Journal of Banking & Finance, Vol. 29, pp. 2523-39.

McQueen, G. and Thorley, S. (1994), “Bubbles, stock returns, and duration dependence”, Journalof Financial and Quantitative Analysis, Vol. 29, pp. 379-401.

Taylor, M.P. and Peel, D.A. (1998), “Periodically collapsing stock price bubbles: a robust test”,Economics Letters, Vol. 61, pp. 221-8.

Tudela, M. (2004), “Explaining currency crises: a duration model approach”, Journal ofInternational Money and Finance, Vol. 23, pp. 799-816.

Zhang, B. (2008), “Duration dependence test for rational bubbles in Chinese stock market”,Applied Economics Letters, Vol. 15, pp. 635-9.

Rationalspeculative

bubbles

263

Further reading

Moore, P. (2006), “Middle eastern capital markets”, Euroweek, pp. 45-50.

Yu, Jung-Suk and Kabir Hassan, M. (2006), “Rational speculative bubbles: an empiricalinvestigation of the Middle East and North African (MENA) stock markets”, Working PaperNo. 388, Economic Research Forum, Dokki.

Corresponding authorM. Kabir Hassan can be contacted at: [email protected]

SEF27,3

264

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints