Embed Size (px)

Citation preview

08/08/2021

1

Mergers & Acquisitions

Rational for Spin off

• Its leads to enhanced focus, & reduced organizational complexity,

control loss & avoid negative Synergy.

• Eliminate Conglomerate discount the parent may have suffered

as diversified company.

• Increase transparency of both parents & the spun off business to

the stock market. Through separate financial reports of the two

firms to current shareholders

• Create new shareholder interest & allow access to new capital

Rational for Spin off

08/08/2021

2

• Allow shareholders increase flexibility in their portfolio decisions.

• Allow firm to create more efficient capital structures for constituent

business in conformity with the economic of those business.

Equity Crave off

• An equity crave off is the sale of minority or Majority voting control in

subsidiary by its parents to outside Investors.

• Parents use an equity carve out to test the waters & when the first

carve out is well received conduct further stages of the divesture

08/08/2021

3

Motives for Equity Crave off

• Increase the focus of the firm

• Improve autonomy of component business

• Improve the managerial incentive structure byrelating management performance directly toshareholder value

• It is not complete separation but partialdivestment

• Minimise the conglomerate discount throughthis enhanced visibility & increase information

M & A

08/08/2021

4

Date: September 2005

Price: $2.6B

When eBay’s leaders acquired VoIP business Skype for $2.6 billion

in 2005, the thinking was that enhanced communications

technology would help buyers and sellers better connect.

The outcome was less than spectacular, though, with few eBay

users (buyers, sellers, or shippers) having any real reason to

communicate in any way besides email.

eBay also changed the management team in charge of Skype a

reported four times during its four years with the e-commerce site,

before selling off 65% of the company to Silver Lake, Andreessen

Horowitz, and the Canada Pension Plan Investment Board in 2009

for $1.9 billion.

Daimler-Benz and Chrysler

Date: November 12, 1998

Price: $36B

Combining two of the biggest names in the car world in 1998 seemed like a sure

thing. Daimler bet heavily on the union, paying $36 billion to merge with Chrysler.

But leadership changes quickly created issues for the merged company. The

retirement of Chrysler CEO Bob Eaton led to Daimler taking majority control, and

soon after, other high-ranking Chrysler executives, including the president and vice-

chair, were forced out.

With Daimler in full control, it immediately began pouring resources into Chrysler,

but language and cultural differences and misjudged product launches saw Chrysler

losing market share quickly. A recession and continued poor sales spelled the end

of this once-promising union. In 2007, Daimler sold off 80% of Chrysler to Cerberus

Capital Management for $7 billion.

08/08/2021

5

• What went right or potential to success

• i. In 1998 when the merger happened, it displayed powerfuldemonstration of the globalization of the world economy.

• ii. Before the merger, Chrysler and Daimler-Benz wereessentially regional producers — Chrysler with the third-largestmarket share in North America, Daimler-Benz controlling theluxury market in Europe.

• The size of the conglomeration was huge. Largest industrial company in Germany, and in Europe as a whole with one of the biggest American corporations, creating a transnational giant with a work force of 410,000 and an annual output of over $130 billion.

• The fifth largest automaker wrt the number of

vehicles produced, ranking after GM, Ford, Toyota

and Volkswagen.

• If DaimlerChrysler were a country, it would rank 37th

in the world in terms of Gross Domestic Product, just

behind Austria, but well ahead of six other members

of the European Union — Greece, Portugal, Norway,

Denmark, Finland and Ireland.

• Daimler-Chrysler deal involved two highly profitable

companies, with combined net earnings of $5.7

billion in 1997.

08/08/2021

6

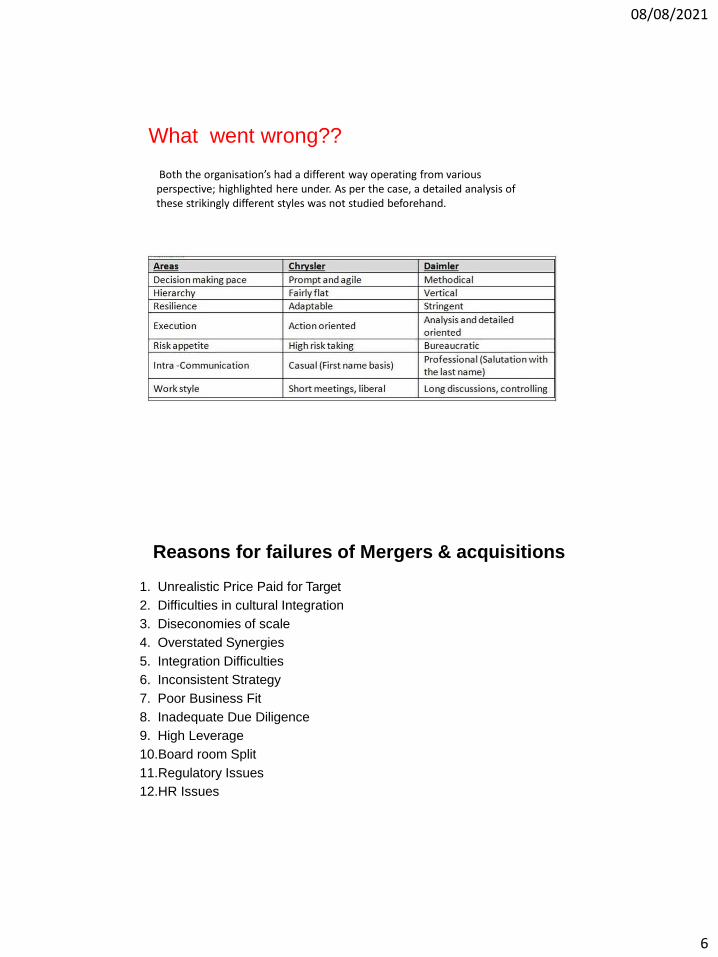

What went wrong??

Both the organisation’s had a different way operating from various perspective; highlighted here under. As per the case, a detailed analysis of these strikingly different styles was not studied beforehand.

Reasons for failures of Mergers & acquisitions

1. Unrealistic Price Paid for Target

2. Difficulties in cultural Integration

3. Diseconomies of scale

4. Overstated Synergies

5. Integration Difficulties

6. Inconsistent Strategy

7. Poor Business Fit

8. Inadequate Due Diligence

9. High Leverage

10.Board room Split

11.Regulatory Issues

12.HR Issues

08/08/2021

7

Unrealistic Price Paid for Target

The process of M&A involves valuation of the target

company and paying a price for taking over the

assets of the company.

Quite often, one finds that the price paid to the

target company is much more that what should

have been paid.

While the shareholders of the target company stand

benefited the shareholders of the acquirer end up on

the loosing side.

Difficulties in cultural Integration

Every merger involves combining of two or moredifferent entities.

These entities reflect corporate cultures, styles ofleadership, differing employee expectations andfunctional differences.

If the merger is implemented in a way that does notdeal sensitively with the companies’ people and theirdifferent corporate cultures, the process may turn outto be disaster.

08/08/2021

8

Diseconomies of scale

• Opposite of economies of scale

• Diffusion of control

• Complexities of monitoring

• Ineffectiveness of communications

Overstated Synergies

• Mergers and acquisitions are looked upon as an

important instrument of creating synergies

through increased revenue, reduced costs,

reduction in net working capital and

improvement in the investment intensity.

Overestimation of these can lead to failure of

mergers

08/08/2021

9

Integration Difficulties

Companies very often face integration difficulties, i.e.the combined entity has to adapt to a new set ofchallengers given the changed circumstances.

To do this, the company prepares plans tointegrate the operations of the combining entities.

If the information available on related issues isinadequate or inaccurate integration becomesdifficult.

Inconsistent Strategy

Mergers and acquisitions that are driven by

sound business strategies are the ones that

succeed.

Entities that fail to assess the strategic benefits

of mergers face failure. It is therefore important

to understand the strategic intent.

08/08/2021

10

Poor Business Fit

Inconsistent Strategy services of the merging entities

do not naturally fit into the acquirer’s overall business

plan. This delays efficient and effective integration

and causes failure.

High Leverage

One of the most crucial elements of an effective

acquisition strategy is planning how one intents

to finance the deal through an ideal capital

structure.

The acquirer may decide to acquire the target

through cash. To pay the price of acquisition, the

acquirer may borrow heavily from the market.

08/08/2021

11

Boardroom Split

• When a merger is planned, it is crucial to

evaluate the composition of the boardroom and

compatibility of the directors.

• Specific personality clashes between executive

in the two companies are also very common.

This may prove to be a major problem, slowing

down or preventing integration of the entries.

Regulatory Issues• The entire process of merger requires legal approvals.

• If any of the stakeholders are not in favour of the

merger, they might create legal obstacles and slow

down the entire process.

• This results in regulatory delays and increase the risk

of deterioration of the business.

• While evaluating a merger proposal, care should be

taken to ensure that regulatory hassles do not crop up.

08/08/2021

12

HR Issues

A merger or acquisition is identified with job

losses, restructuring and the imposition of a

new corporate culture and identity.

This can create uncertainty, anxiety and

resentment among the company’s employees.

These HR issue are crucial to the success of

M&As

Question 01

Firm “A “going to take over firm “B”

Firm “A” estimated that combined entity will have synergy benefit of Rs. 3000 forever.

i) If Firm “B” is will to acquire for Rs 27 per share cash what is the NPV of the merger.

ii) What will the price per share of the merged firm after above (i)

(iii) What is the Merger premium

(iv) Suppose Firm “B” is agreeable to merger by an exchange of stock, if “A” offers three of itsshares for every one of “B” Shares. What will be MPS of merge firm

(v) What is the NPV of the merger assuming the conditions in (iv)

(vi) What is the best for firm B, what is the exchange ratio to B, theshareholders are indifferent between two options

Firm A Firm B

Shares outstanding 1,500 900

MPS Rs.34 Rs. 24

08/08/2021

13

M & A

Defensive tactics against

hostile takeover

Hostile Takeover?

08/08/2021

14

What is a Hostile Takeover?

A hostile takeover, in mergers and acquisitions (M&A), is

the acquisition of a company (called the target company)

by the other company (called the acquirer) by going directly

to the target company’s shareholders (a tender offer) or

through a proxy vote. The difference between a hostile and

friendly takeover is that in a hostile takeover, the target

company’s board of directors do not approve of the

transaction.

Hostile takeover bid tactics

01.Tender offer to the company's shareholders.

A tender offer is a bid to buy a controlling share of the target's stock at a

fixed price. The price is usually set above the current market price in order

to allow the sellers a premium as added incentive to sell their shares.

02. proxy fight

replace board members who are not in favor of the takeover with new

board members who would vote for the takeover. This is done by

convincing shareholders that a change is management is needed and that

the board members who would be appointed by the would-be acquirer are

just what the doctor ordered.

08/08/2021

15

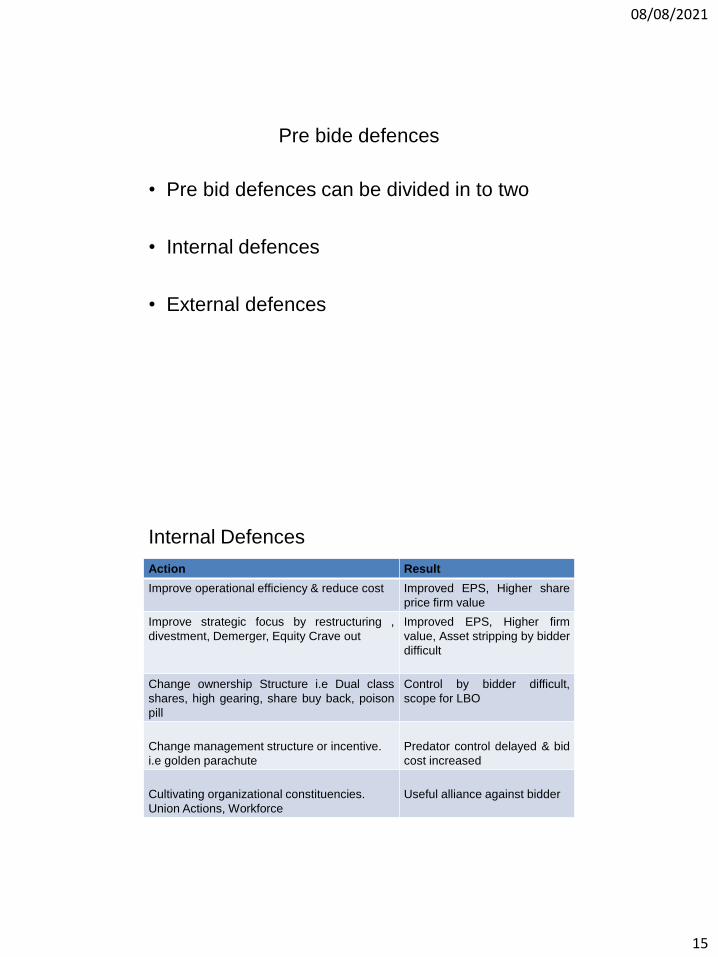

Pre bide defences

• Pre bid defences can be divided in to two

• Internal defences

• External defences

Internal Defences

Action Result

Improve operational efficiency & reduce cost Improved EPS, Higher share

price firm value

Improve strategic focus by restructuring ,

divestment, Demerger, Equity Crave out

Improved EPS, Higher firm

value, Asset stripping by bidder

difficult

Change ownership Structure i.e Dual class

shares, high gearing, share buy back, poison

pill

Control by bidder difficult,

scope for LBO

Change management structure or incentive.

i.e golden parachute

Predator control delayed & bid

cost increased

Cultivating organizational constituencies.

Union Actions, Workforce

Useful alliance against bidder

08/08/2021

16

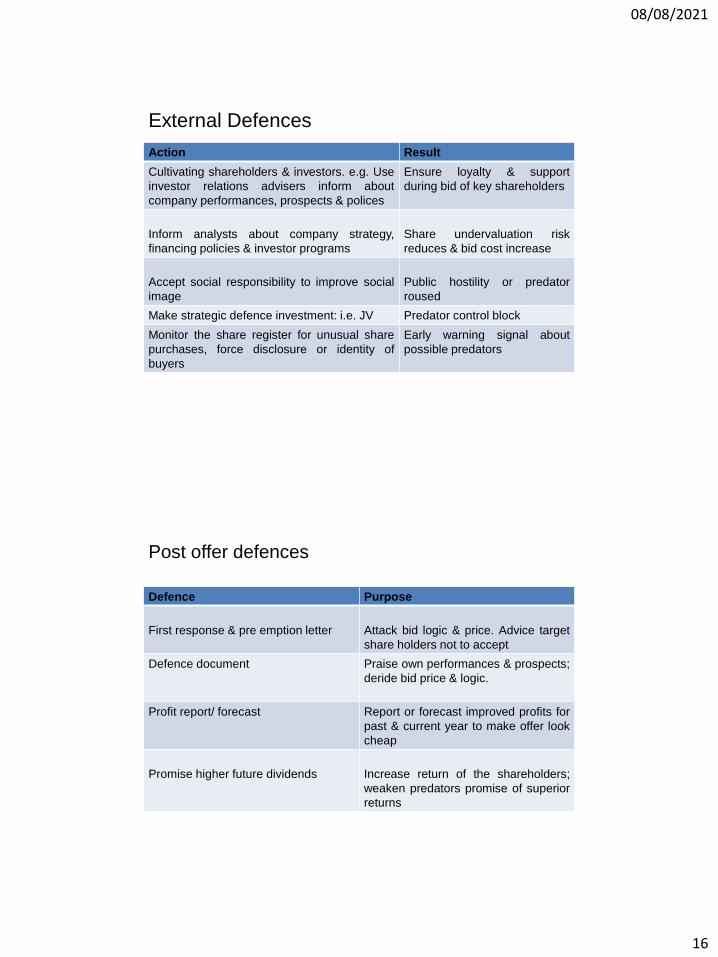

External Defences

Action Result

Cultivating shareholders & investors. e.g. Use

investor relations advisers inform about

company performances, prospects & polices

Ensure loyalty & support

during bid of key shareholders

Inform analysts about company strategy,

financing policies & investor programs

Share undervaluation risk

reduces & bid cost increase

Accept social responsibility to improve social

image

Public hostility or predator

roused

Make strategic defence investment: i.e. JV Predator control block

Monitor the share register for unusual share

purchases, force disclosure or identity of

buyers

Early warning signal about

possible predators

Post offer defences

Defence Purpose

First response & pre emption letter Attack bid logic & price. Advice target

share holders not to accept

Defence document Praise own performances & prospects;

deride bid price & logic.

Profit report/ forecast Report or forecast improved profits for

past & current year to make offer look

cheap

Promise higher future dividends Increase return of the shareholders;

weaken predators promise of superior

returns

08/08/2021

17

Post offer defences

Defence Purpose

Asset revaluation Revalue properties, intangible assets

& brands

Regulatory appeal Lobby antitrust/ regulatory authorities

to block bid

Share support campaign Look for white knight or white squire

Acquisition or divestment Buy a business to make target bigger

or incompatible with bidder, sell crown

jewels, organise management buy out

Unions/ workforce Enlist to lobby regulators or politicians

& attack bidders plans for target

Customers/ Suppliers Enlist to lobby antitrust authorities

Defensive Tactics • Target firm managers frequently resist take over attempts

• Corporate takeovers can sometimes hostile one business acquires control over a public company against the consent of existing management or its board of directors. ( Hostile takeover)

Defenses against a Hostile Takeover

01. Poison pill:

Making the stocks of the target company less attractive by allowing currentshareholders of the target company purchase shares at a discount. It willincrease the number of shares the acquirer company needs to obtain.

08/08/2021

18

There are two types of poison pills:

i. A “flip-in” permits shareholders, except for the acquirer, to purchase

additional shares at a discount. This provides investors with instantaneous

profits. Using this type of poison pill also dilutes shares held by the acquiring

company, making the takeover attempt more expensive and more difficult.

ii. A “flip-over” enables stockholders to purchase the acquirer’s shares after

the merger at a discounted rate. For example, a shareholder may gain the

right to buy the stock of its acquirer, in subsequent mergers, at a two-for-one

rate.

2.Crown jewels defense:

Selling the most valuable parts of the company in the event of a

hostile takeover. It will make the target company less attractive and

deter a hostile takeover.

3. Golden parachute:

An employment contract that guarantees extensive benefits to key

management if they were removed from the company.

4. Pac-Man defense:

The target company purchasing shares of the acquiring company and

attempting a takeover of their own.

08/08/2021

19

5. Greenmail

Greenmail is the practice of buying a voting stake in a company with the threat ofa hostile takeover to force the target company to buy back the stake at apremium. In the area of mergers and acquisitions, the greenmail payment ismade in an attempt to stop the takeover bid. The target company is forced torepurchase the stock at a substantial premium to the takeover.

6. White knight & while square

A white squire is an individual or company that buys a large enough stake in thetarget company to prevent that company from being taken over by a blackknight. In other words, a white squire purchases enough shares in a targetcompany to prevent a hostile takeover.

White knight vs while square

purchases a majority stake in the company while a white squire purchases aminority stake in the company. Therefore, in a white-squire situation, the targetcompany is able to remain independent.

What is a White Knight?

08/08/2021

20

• A white knight is a company or an individual that

acquires a target company that is close to being

taken over by a black knight. A white knight

takeover is the preferred option to a hostile

takeover by the black knight as white knights

make a ‘friendly acquisition‘ by generally

preserving the current management team, making

better acquisition terms, and maintaining the core

business operations.

White Squire

08/08/2021

21

What is a White Squire?

A white squire is an individual or company that

buys a large enough stake in the target company

to prevent that company from being taken over by

a black knight. In other words, a white squire

purchases enough shares in a target company to

prevent a hostile takeover

Example of a White Squire1. Company A receives a bid offer from Company B.

In finance, Company A would be called the “Target Company” and

Company B would be called the “acquirer Company.

• 2. Company A rejects the offer from Company B

• 3. Despite the rejection of their offer, Company B proceeds with a

tender offer (purchasing shares of Company A at a premium

price) to acquire a controlling interest in Company A.

By continuing to pursue an acquisition despite getting their offer

declined by Company A, Company B would be attempting a hostile

takeover of Company A. Company B would be referred to as a black

knight.

• 4. A friendly investor sees the hostile takeover attempt by Company B and

decides to step in and help Company A. The friendly investor purchases

shares in Company A to prevent them from being acquired by Company

B.

08/08/2021

22

Incentives for the White Squire

A white squire is used to help the target company prevent a hostile takeover.

The target company must incentivize the white squire to stand on its side of the

target and not end up selling its shares to the black knight (thus aiding the

hostile takeover attempt).

White Squire vs. White Knight

• A white squire and a white knight are similar in thatboth are involved in preventing a hostile takeoverattempt. However, the differentiating point is that awhite knight purchases a majority interest while awhite squire purchases a partial interest in the targetcompany.

• White squires are preferred over white knights. A whiteknight purchases a majority stake in the companywhile a white squire purchases a minority stake in thecompany. Therefore, in a white-squire situation, thetarget company is able to remain independent.

08/08/2021

23

Due Diligence

What is Due Diligence

• Due diligence is a process of verification, investigation, oraudit of a potential deal or investment opportunity to confirmall facts, financial information, and to verify anything else thatwas brought up during an M&A deal or investment process.

• Due diligence refers to the research done before entering intoan agreement or a financial transaction with another party.

• Due diligence can also refer to the investigation a sellerperforms on a buyer that might include whether the buyer hasadequate resources to complete the purchase.

08/08/2021

24

• To investigate into the Affairs of Business as a prudent business person

• To confirm all material facts related to the Business

• To assess the Risks and Opportunities of a proposed transaction.

• To reduce the Risk of post-transaction unpleasant surprises

• To confirm that the business is what it appears.

Why Due Diligence is Important for M&A….??

47

From a buyer’s perspective

Due diligence allows the buyer to feel more comfortable that his or herexpectations regarding the transaction are correct. In mergers andacquisitions (M&A), purchasing a business without doing due diligencesubstantially increases the risk to the purchaser.

From a seller’s perspective

Due diligence is conducted to provide the purchaser with trust. However,due diligence may also benefit the seller, as going through the rigorousfinancial examination may, in fact, reveal that the fair market value of theseller is more than what was initially thought to be the case. Therefore, it isnot uncommon for sellers to prepare due diligence reports themselves priorto potential transactions.

08/08/2021

25

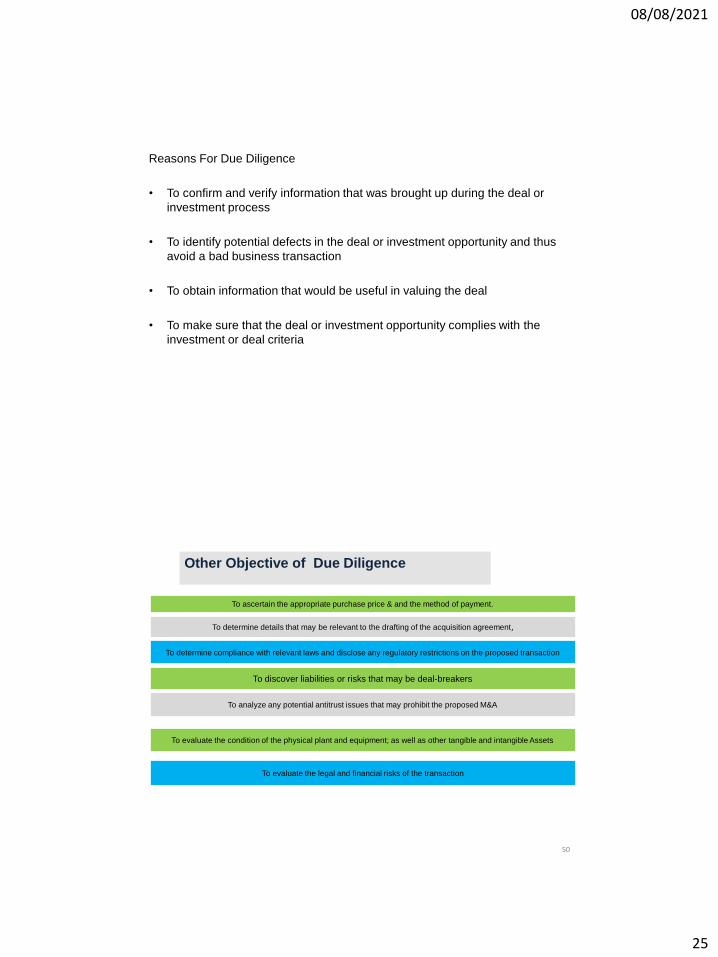

Reasons For Due Diligence

• To confirm and verify information that was brought up during the deal or

investment process

• To identify potential defects in the deal or investment opportunity and thus

avoid a bad business transaction

• To obtain information that would be useful in valuing the deal

• To make sure that the deal or investment opportunity complies with the

investment or deal criteria

Other Objective of Due Diligence

To determine compliance with relevant laws and disclose any regulatory restrictions on the proposed transaction

To evaluate the condition of the physical plant and equipment; as well as other tangible and intangible Assets

To ascertain the appropriate purchase price & and the method of payment.

To determine details that may be relevant to the drafting of the acquisition agreement,

To discover liabilities or risks that may be deal-breakers

To analyze any potential antitrust issues that may prohibit the proposed M&A

To evaluate the legal and financial risks of the transaction

50

08/08/2021

26

Due Diligence Activities in an M&A Transaction

• Target Company Overview

• Financials

• Technology/Patents

• Strategic Fit

• Target Customer Base

• Management/Workforce

• Legal Issues

• Information Technology

• Corporate Matters

• Environmental Issues

Types of due diligence

Accounting due diligence

▪ Review of financial statements and management accounts

▪ Review of significant accounting policies and

▪ compliance with relevant Generally Accepted AccountingPrinciples (GAAP)

▪ Historical revenue and cost trends

▪ Consistency between historical results, versus budget and forecast

▪ Historical and anticipated capital expenditure and working capitallevels

▪ Review of debt covenants and terms of other debt-like instruments

08/08/2021

27

Financial due diligence

• Basis for future business plan

• Valuation

• Deal financing

• Market dynamics and customer attractiveness

• Industry structure and dynamics

• Distribution channel dynamics

• Business plan review

• Quality of assets

Tax due diligence

• Assessment of tax impact arising from “change in control”

• Assessment of historical tax exposures

• Identifying tax saving opportunities

• Assessment of current tax position

08/08/2021

28

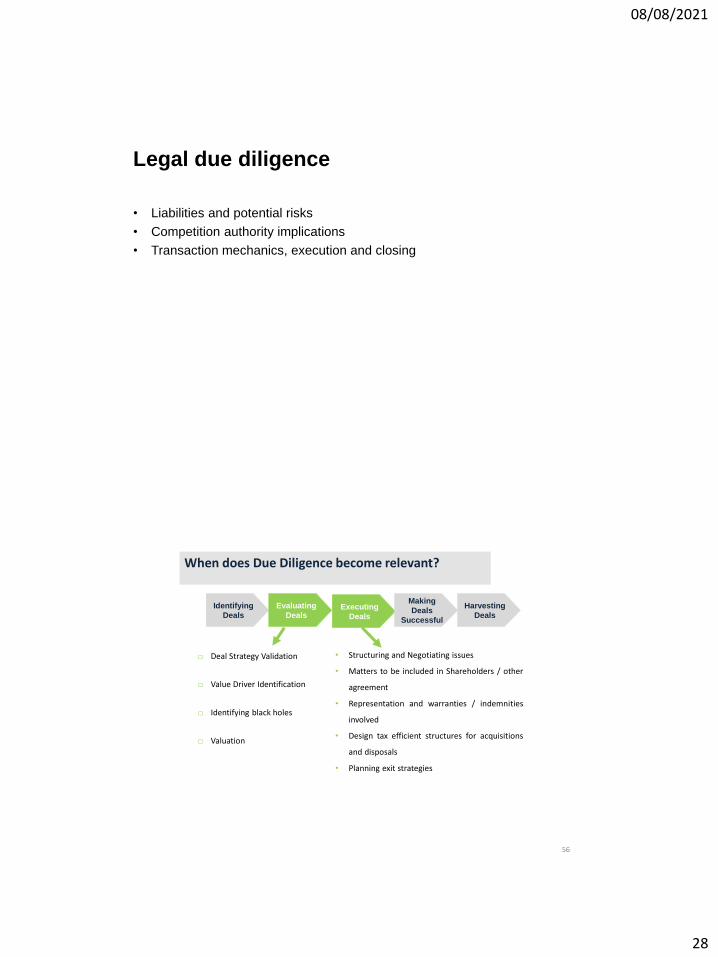

Legal due diligence

• Liabilities and potential risks

• Competition authority implications

• Transaction mechanics, execution and closing

Deal Strategy Validation

Value Driver Identification

Identifying black holes

Valuation

Identifying

Deals

Evaluating

DealsExecuting

Deals

Making

Deals

Successful

Harvesting

Deals

• Structuring and Negotiating issues

• Matters to be included in Shareholders / other

agreement

• Representation and warranties / indemnities

involved

• Design tax efficient structures for acquisitions

and disposals

• Planning exit strategies

When does Due Diligence become relevant?

56

![Rational, unirational and stably rational varietiespirutka/survey.pdf · could be rational (resp. stably rational, resp. retract rational) [30, p.282]. Unirational nonrational varieties](https://img.pdfslide.us/doc/110x75/5f8fad2d18211140cf6c6b61/rational-unirational-and-stably-rational-varieties-pirutka-could-be-rational.jpg)