Embed Size (px)

Citation preview

RAO UES Reform: The Final Stage

Anatoly Chubais Chief Executive Officer

RAO “UES of Russia”

April 6-13, 2005New York, London

2

RAO “UES of Russia” today

Reform: company transformation and market development

Conclusions

Table of Contents

1. RAO “UES of Russia” today

4

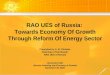

Russia: 4th Largest Power Producer in the world

3 993

1 6401 088 889

601 597 567 555 384 345

0

1 000

2 000

3 000

4 000

5 000

US

Ch

ina

Ja

pa

n

Ru

ss

ia

Ca

na

da

Ind

ia

Ge

rma

ny

Fra

nc

e

UK

Bra

zil

24.9% 10.2% 6.8% 5.5% 3.7% 3.7% 3.5% 3.5% 2.4% 2.1%%

Of World Total

Source: IEA

TWh

RAO “UES of Russia” today

5

RAO “UES of Russia”Leading role in Russia’s electricity industry

Installed capacityRAO: 156m kW

Heat generationRAO: 469m Gcal

RAO “UES of Russia” Other

4%

96%68%

32%28%

72%

Length of transmission linesRAO: 2,497 thousand km

RAO “UES of Russia” today

6

RAO “UES Russia”1999 - 2004 RAO “UES of Russia” financial performance

8,015

10,508

13,273

15,840

20,141

406

1,853 1,8762,819

4,2353,309

(365)

18

1,383 1,101 916 483

16,349

5.1%

20.2%21.0%

17.8%

14.1%

17.6%

(1,000)

1,000

3,000

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

21,000

1999 2000 2001 2002 2003 9M 2004

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Revenues EBITDA Net Income EBITDA Margin

Source: IAS Group financial results(1) Excludes doubtful debtors expense(2) As reported

US$m

RAO “UES of Russia” today

(2)(1)

7

During the last two years shares of RAO “UES of Russia”outperformed broader RTS index by 40%

RAO “UES of Russia”Market capitalization dynamics

1.04.2005

0.0

3.0

6.0

9.0

12.0

15.0

UES RTS Rebased1.04.2003

Market Cap, US$bn

RAO “UES of Russia” today

+128.4%

+88.6%

Source: Factset

8

7.1x 7.1x 7.0x6.3x

5.1x

4.0x3.7x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

Endesa

E.O

n

CE

Z

Enel

Cem

ig

RA

O U

ES

Ele

ctr

obra

s

RAO “UES of Russia”Relative valuation

2005 EV/EBITDA

1,942

1,631

1,287

1,003

478410

134

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Enel

E.O

n

Endesa

CE

Z

Cem

ig

Ele

ctr

obra

s

RA

O U

ES

$/k

W

EV/Installed capacity, $/kW

Average: 5.8x

Average: 984$/kW

RAO “UES of Russia” today

Sources: Brokers’ Estimates, Bloomberg, companies reporting

2. Reform: company transformation and market development

10

2005

2006

2007

Finish is in sight

FINISH

11

Competitive sectors

Monopolies

RAO “UES of Russia”Reform basics

Free price-setting Stimulating

market entry

Market rules

Regulated tariffs

Securing equal access to grids

Establishing market infrastructure

Generation Sales

Transmission Distribution Dispatching

Reform Basics: Separation of Monopoly and Competitive Sectors

Company transformation and market development

12

Legislative base of reforms: Key legislation, 2001-2004

July 2001 – Government Decree №526 «On reform of

Russia’s power sector»

March 2003:Five laws on power sector reform signed by President Putinand entered into force (main– №35-FZ «On the power sector»)

Governmental decrees

and orders

December 2004: Meeting of

Russian government. Key decision

made: preparation

for the unbundling of

RAO «UES of Russia»

to be completed

in 2006

Company transformation and market development

13

RussianFederation

MinorityShareholders

of the Parent Company

IndependentRegionalEnergos:

Irkutskenergo

Tatenergo

Bashkirenergo

RosEnergoAtom

10 NuclearPlants

Company transformation and market development

Pre-reform Sector Structure

Generation

Transmission &

Distribution Grids

Sales

73 Regional Energos High Voltage

Grid+

GridService

Central Dispatch

32 FederalPower Plants

52% 48%

RAO UES

14

Target sector model

Private shareholders

Government

Monopolies

FGC

(Transmission)

<25%

>75%

Competitive Generation

Other generating companies

On the base of independentRegional Energos

Nuclear power generating company

Hydro GenCo (1)

Wholesale GenCos (6)

Territorial

GenCos (14)

51-60% <48% 75-85%

49-40% 25-15%>52%

System operator

<25%

>75%

IDC

(Distribution) (4)

<48%

>52%

Competitivemarket

FGC – Federal Grid CompanyIDC – Inter-regional distribution grid company

Company transformation and market development

15

• Unbundling completed and Regional GenCos registered in 35 regions• Unbundling continues in 25 regions

Regional Energos

Other assets: Grid, Dispatch, Sales, etc.

Generation Assets (Regional GenCos)

Territorial GenCos

6 of 14 registered

HydroGenCo

Formation of new generation companies

Target Private Shareholder Stake: >50% Target Government Stake: >50%

* Some of the assets contributed from Regional Energos

Federal Power Plants

Company transformation and market development

• Capacity ranges from 0.6 GW to 10.5 GW• Annual sales ranges from US$100m to US$1300m

• Average capacity at 9 GW• Average annual sales at US$600m

6 of 6 registered

Wholesale GenCos

•Capacity of 22 GW•Annual sales at US$700m

Registered

16

Transition Market (2006 - 2008)

Status Quo (Nov 2003 – 2005)

Market Progression

List of participants (buyers and sellers) established by the government

Regulator or RAO UES matches buyers and sellers

Tariffs are regulated

Regulated bi-lateral (vesting) contracts introduced (for the next 3-5 years)

Initial electricity volume of 85% of total electricity volumes and decreasing

Regulated Market

Competitive Market (5 – 15%)

Free market segment trading 5 – 15% of electricity volumes

Self regulating trading floor - ATS

Price cap set by the Regulated Market

Voluntary for generators and purchasers

No price cap

Vesting Contracts

Free Market(from 2009)

Full liberalization

Fully Regulated Market(prior to Nov 2003)

List of participants (buyers and sellers) established by the government

Regulator or RAO UES matches buyers and sellers

Tariffs are regulated

Regulated Market

Competitive Market (≥15%)(Spot)

Free marketRegulated Market

Company transformation and market development

Competitive Market

17

The Reform ProcessFinishing line in sight

Company transformation and market development

2005 2006 2007 2008

Launch of vesting contracts and competitive market (spot) Competitive Market (5 – 15%)

Wholesale GenCos Formation

Territorial GenCos Formation

Private majority Wholesale GenCos

Private majority Territorial GenCos

RAO UES unbundling

3. Conclusions

19

Currently/During Transition (2005-2006)

Pro-rata distribution among shareholders brings about transparency and fairness

Entry point into concrete Wholesale

and/or Territorial GenCos along defined and transparent route

Substantial future valuation upside

Valuation parameters

more certain since market signals are in place

Ownership/control

profile of government or industrial group clarified

Relatively smaller and less liquid entities

Valuation risk due to lack of market signals

Valuation upside likely to be lower than through earlier investments

Post RAO UES Unbundling (2007-2008)

RAO UES/Regional GenCos/ Federal Plants Wholesale and Territorial GenCos

Pros

Cons

Vehicles

Investing in Russian Power Sector: Investment Vehicles and Timing

Conclusions

20

Potential Investor Concerns Do We Share?

No Government willingness/commitment to support the company transformation

No

No willingness of the Government to exit generation and consolidate control over monopolies business (FGC, SO, Hydro GenCo)

Partially

No transparency/fairness of corporate procedures during the restructuring

No

No Government commitment to the electricity market liberalization

Partially

Reform’s final stage: Lower risk investmentConclusions

21

Reform of RAO “UES Russia”On a Corporate Mission…

… ensure a sustained GROWTH OF THE VALUE of its shares and the shares of the companies that will be established in the course of restructuring

RAO “UES of Russia” is committed to…

Conclusions

through a successful implementation of the reform…

… and increased efficiency and transparency of its operations as well as the operations of the companies established in the restructuring process

22

Conclusions

Russian Power Sector: Key advantage for investors

2005-2006: From the swamp to the firm ground

Today, electric power assets are deep in the non-market environment ...

… By the end of 2006 they will be available amid competitive market conditions.