Embed Size (px)

Citation preview

`

RAK INVESTMENT AUTHORITY

GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS

AND INDEPENDENT AUDITOR’S REPORT

FOR THE YEAR ENDED

DECEMBER 31, 2009

RAK INVESTMENT AUTHORITY

GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS

AND INDEPENDENT AUDITOR’S REPORT

FOR THE YEAR ENDED DECEMBER 31, 2009

Table of Contents

Page Exhibit

Independent Auditor’s Report 1 --

Consolidated Statement of Financial Position 2 A

Consolidated Income Statement 3 B

Consolidated Statement of Comprehensive Income 4 C

Consolidated Statement of Changes in Equity 5 D

Consolidated Cash Flow Statement 6 E

Notes to the Consolidated Financial Statements 7 - 52 --

RAK INVESTMENT AUTHORITY

GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

CONSOLIDATED INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2009

EXHIBIT B

Notes

2009

2008

AED’000 AED’000

(Restated)

Revenue 4.31 & 31 611,719 370,302

Cost of revenue 32 (304,021) (162,359)

________ ________

Gross profit 307,698 207,943

Other income 33 32,827 40,765

Marketing expenses 34 (20,036) (18,716)

Administrative expenses 35 (79,658) (60,286)

Investment income 36 26,635 33,373

Finance costs 37 (61,442) (28,949)

Shares of results of associated companies 14 (b) 58,603 82,013

Loss on disposal of a subsidiary 38 (4,415) (8,800)

Impairment of assets 39 (27,424) (142,670)

Profit from sale of an associate -- 33,189

________ _______

Profit before income tax 232,788 137,862

Income tax (expenses)/benefits 4.32 (3,540) 14,772

_______ ________

PROFIT FOR THE YEAR 229,248 152,634

====== =======

ATTRIBUTABLE TO:

Owner of the parent – Exhibit D 228,852 182,644

Non – controlling interest – Exhibit D 396 (30,010)

________ ________

229,248 152,634

======= =======

The attached notes 1 to 46 form part of these consolidated financial statements.

-3-

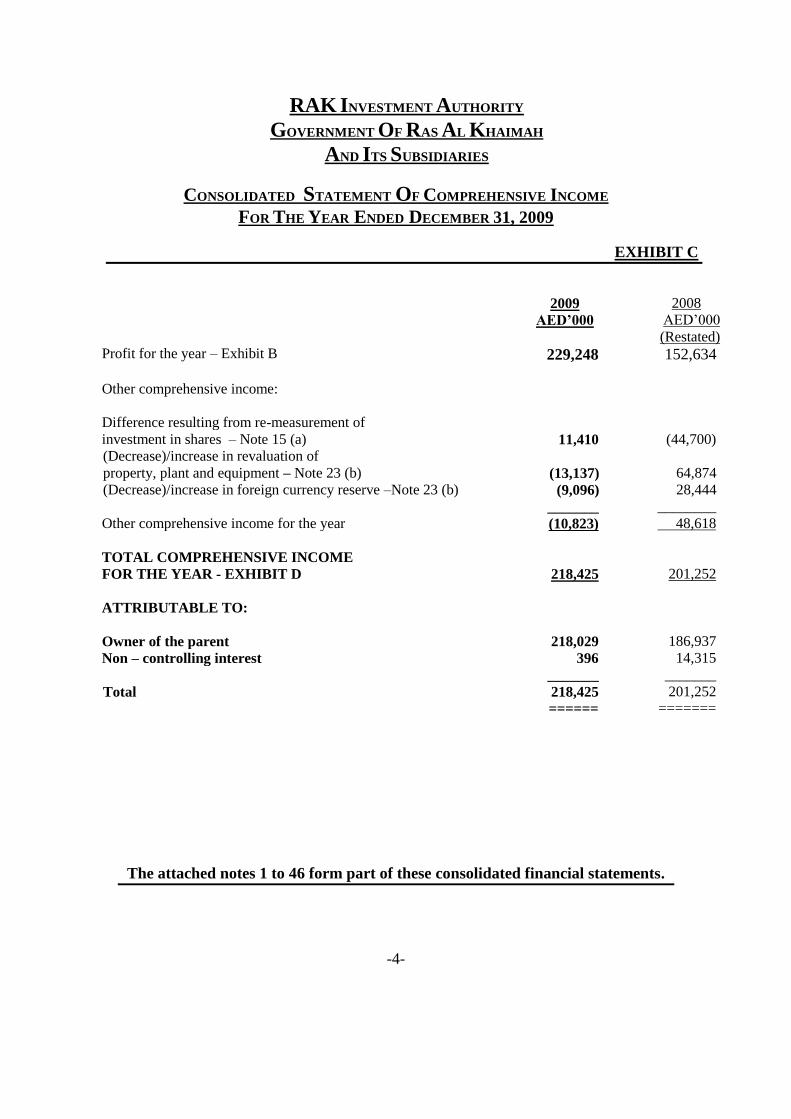

RAK INVESTMENT AUTHORITY

GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED DECEMBER 31, 2009

EXHIBIT C

2009 2008

AED’000 AED’000

(Restated)

Profit for the year – Exhibit B 229,248 152,634

Other comprehensive income:

Difference resulting from re-measurement of

investment in shares – Note 15 (a) 11,410 (44,700)

(Decrease)/increase in revaluation of

property, plant and equipment – Note 23 (b) (13,137) 64,874

(Decrease)/increase in foreign currency reserve –Note 23 (b) (9,096) 28,444

_______ ________

Other comprehensive income for the year (10,823) 48,618

TOTAL COMPREHENSIVE INCOME

FOR THE YEAR - EXHIBIT D

218,425

201,252

ATTRIBUTABLE TO:

Owner of the parent 218,029 186,937

Non – controlling interest 396 14,315

_______ _______

Total 218,425 201,252

====== =======

The attached notes 1 to 46 form part of these consolidated financial statements.

-4-

RAK INVESTMENT AUTHORITY

GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED DECEMBER 31, 2009

EXHIBIT D

Reserves

Cumulative

changes in fair

value of

available-for-

sale investments

Government

current account

Retained

earnings

Total

Non-controlling

interest

Total

equity

AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000

Balance at December 31, 2007 635,794 18,300 -- . 50,428 704,522 (909) 703,613

Profit for the year – Exhibit B -- -- -- 182,644 182,644 (30,010) 152,634

Foreign currency translation reserve – Note 23 (b) 15,907 -- -- -- 15,907 12,537 28,444 Other comprehensive income 33,086 (44,700) -- . -- . (11,614) 31,788 20,174

Total comprehensive income for the year- Exhibit C 48,993 (44,700) -- . 182,644 186,937 14,315 201,252

Net movement in non-controlling interest -- -- -- (50,538) (50,538) 196,575 146,037

Capital reserve against land – Note 6 (b) 262,157 -- -- -- 262,157 -- 262,157

Capital reserve on acquisition of shares – Note 23 (b) 199 -- -- -- 199 -- 199 Net movement in RAK Govt. current account -- -- (65,004) -- (65,004) -- (65,004)

Transferred to RAK Govt. current account -- -- 65,004 (65,004) -- -- --

________ ________ __________ _________ _________ _________ _________

Balance at December 31, 2008 (Restated) – Exhibit A 947,143 (26,400) -- . 117,530 1,038,273 209,981 1,248,254

Profit for the year – Exhibit B -- -- -- 228,852 228,852 396 229,248

Increase in foreign currency translation reserve – Note 23 (b) (9,096) -- -- -- (9,096) -- (9,096) Other comprehensive income (13,137). 11,410 -- . -- . (1,727) --___ (1,727)

Total comprehensive income for the year- Exhibit C (22,233) 11,410 -- . 228,852 218,029 396 218,425

Acquisition of shares from non-controlling interest 44,325 -- -- (34,794) 9,531 (209,796) (200,265)

Addition to minority shareholders’ interest -- -- -- -- -- 500 500

Capital reserve against land – Note 6 (b) 297,700 -- -- -- 297,700 -- 297,700 Transferred to retained earnings (199) -- -- 199 -- -- --

Net movement in RAK Govt. current account -- -- (73,073) -- (73,073) -- (73,073)

Transferred to RAK Govt. current account -- -- 73,073 (73,073) -- -- --

_________ _________ __________ __________ __________ _________ _________

Balance at December 31, 2009 – Exhibit A 1,266,736 (14,990) -- 238,714 1,490,460 1,081 1,491,541

======== ======== ========= ========= ========= ======== ========

____The attached notes 1 to 46 form part of these consolidated financial statements. .

-5-

RAK INVESTMENT AUTHORITY

GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

CONSOLIDATED CASH FLOW STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2009

EXHIBIT E

2009 2008

AED’000 AED’000

Cash Flows from Operating Activities (Restated)

Profit before income tax – Exhibit B 232,788 137,862

Adjustments for:

Depreciation and amortization 34,502 13,833

Impairment loss 27,424 142,670

End of service benefits 407 (194)

Finance costs 61,442 28,949

Investment income (26,635) (33,373)

Interest income (17,065) (4,570)

Gain on disposal of investment property (4) --

Loss from a subsidiary 4,415 8,800

Profit from associates (58,603) (82,013)

Profit on sale of investment in an associate -- (33,189)

Dividend income ___(190) (5,896)

Operating profit before working capital changes 258,481 172,879

Decrease/(Increase) in inventories 2,894 (9,700)

(Increase) in trade and other receivables (49,389) (50,194)

(Decrease)/Increase in advances from customers (118,339) 1,805,264

Increase in trade and other payables 91,286 188,413 _____________ ____________

Net cash generated from operations 184,933 2,106,662

Finance costs paid (55,042) (20,755)

Net cash provided by operating activities 129,891 2,085,907

Cash Flows from Investing Activities

Purchase of land (2,020) (113,919)

Purchase of property, plant and equipment (366,542) (753,581)

Sale of property, plant and equipment 2,356 62,002

Capital work-in-progress (282,244) (287,606)

Goodwill on acquisition of shares in subsidiary (1,778) (85,440)

Land improvement (915) (4,773)

Disposal of investment property 146 (27,519)

Advance to contractors (54,070) (183,414)

Refund from contractors 73,470 --

Purchase of intangible assets (72) (61)

Advances for investment projects (5,940) (488,520)

Trading properties under development (71,889) (1,091,121)

Investments in associates (88,011) (47,048)

Sale proceeds from an associate -- 69,692

Sale proceeds of investment in a subsidiary 6,827 510

Purchase of available-for-sale investments (781) (162,514)

Income from investments in associates 82,732 55,125

Proceeds of available-for-sale investments 500 --

Finance lease receivable -- (76,831)

Investment income 23,056 33,373

Fixed deposits with bank (11,850) --

Dividend received 190 5,916

Interest income 15,984 __ 4,570

Net cash (used) in investing activities (680,851) (3,091,159)

Cash Flows from Financing Activities

Proceeds from unsecured loans 211,649 494,587

Payment of unsecured loans (60,836) (59,706)

Proceeds from medium-term bank loans 701,452 112,720

Payment of medium-term bank loans (86,486) (31,900)

Loans and advances 105,789 (619,911)

Payment of finance lease liabilities (49) 160

Proceeds from short-term borrowings from banks -- 33,969

RAK Government current account (73,073) (65,004)

Non-controlling interests (208,900) 196,575

Net cash provided by financing activities 589,546 61,490

Net increase/(decrease) in cash and cash equivalents 38,586 (943,762)

Net foreign currency translation difference 8,936 (9,490)

Cash and cash equivalents at beginning of the year (Restated) 159,810 1,113,062

CASH AND CASH EQUIVALENTS AT END OF THE YEAR – Notes 4.17 & 22 207,332 159,810

======= ========

The attached notes 1 to 46 form part of these consolidated financial statements.

-6-

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 7 -

1. GENERAL INFORMATION:

RAK Investment Authority, a government owned entity (“the Parent Entity”) was

established by the Government of Ras Al Khaimah, U.A.E. under Emiri Decree No. 2

dated February 1, 2005 issued by H.H. Sheikh Saqr Bin Mohammad Bin Salim Al

Qassimi, Ruler of the Emirate of Ras Al Khaimah. The Parent Entity and its

subsidiaries constitute the Group (“the Group”). The domicile of the Parent Entity is in

Ras Al Khaimah City, Emirate of Ras Al Khaimah, United Arab Emirates.

The principal activities of the Parent Entity are:

1. Attracting investments in industrial sectors in the Emirate of Ras Al

Khaimah.

2. Developing and promoting industrial, tourism & infrastructure activities in

the Emirate of Ras Al Khaimah.

3. Issuing licenses and collecting lease rents from companies registered in Free

Zone and Industrial Zone in the Emirate of Ras Al Khaimah.

4. Investments in various projects.

2. BASIS OF PREPARATION:

2.1 Statement of compliance:

The consolidated financial statements have been prepared in accordance with

International Financial Reporting Standards (“IFRS”).

2.2 Basis of measurement:

The consolidated financial statements have been prepared on a historical cost

basis except for the available-for-sale investments which are measured at fair

value. The method used to measure fair value of available-for-sale investment is

discussed in Note 4.10.

2.3 Functional and presentation currency:

The consolidated financial statements are presented in United Arab Emirates

Dirhams (“AED”), which is the Group‟s functional currency. All financial

information presented in AED have been rounded to the nearest thousand unless

otherwise stated.

2.4 Basis of consolidation:

Subsidiaries are those enterprises controlled by the Parent Entity. Control exists

when the Parent Entity owns directly or indirectly more than 50% of the capital

and has the power, directly or indirectly, to govern the financial and operating

policies of an enterprise so as to obtain benefits from its activities.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 8 -

2. BASIS OF PREPARATION: (continued…)

2.4 Basis of consolidation: (continued…)

The consolidated financial statements incorporate the financial statements of the

Parent Entity and its subsidiaries (“the Group”). The details of the consolidated

subsidiaries are as follows:

Name of

subsidiary

Country of

incorporation

Principal activities

Percentage

of holding

Al Jazeera Farm

Products LLC

UAE Agricultural production

activity and marketing the

same within UAE.

56 %

Al Ghail Power LLC UAE Natural gas based power

generation and supply

99 %

JSC Poti Sea Port Georgia Servicing ships, cargo

handling, dispatching

operations and warehousing.

100 %

Ras Al Khaimah

Investment Authority

Georgia LLC

Georgia Hotel and hospitality as main

activity and real estate

development as other activity

in Georgia.

100 %

RAKIA Georgia Free

Industrial Zone LLC

Georgia Development of Free

Industrial Zone, leasing and

licensing in FIZ

100 %

Yacht Club Port of

Poti LLC

(a subsidiary of JSC

Poti Sea Port)

Georgia

Restaurant and related

activities.

100 %

All intra-group balances, transactions, income and expenses, and profits and losses

resulting from intra-group transactions that are recognized in assets are eliminated in full.

Subsidiaries are consolidated from the date on which control is transferred to the Group

and cease to be consolidated from the date on which control is transferred out of the

Group.

3. ADOPTION OF NEW AND REVISED STANDARDS (Deemed Appropriate):

In the current year, the Group has adopted the new and revised International Financial

Reporting Standards (IFRSs) including the International Accounting Standards (IASs)

and their interpretations that are relevant to its operations and effective for annual

reporting periods beginning on or after January 1, 2009, and the consequential

amendments thereon.

The Group has adopted the following new and amended IFRS and IFRIC interpretations

as of January 1, 2009:

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 9 -

3. ADOPTION OF NEW AND REVISED STANDARDS (Deemed Appropriate): (continued…)

IFRS 3 Business Combinations (Revised) and IAS 27 Consolidated and Separate

Financial Statements (Amended) effective July 1, 2009.

IFRS 7 Financial Instruments : Disclosures effective January 1, 2009

IFRS 8 Operating Segments effective January 1, 2009

IAS 1 Presentation of Financial Statements effective January 1, 2009

IAS 23 Borrowing Costs (Revised) effective January 1, 2009

IAS 40 Investment Property (Amended)

Improvement to IFRS (May 2008) effective January 1, 2009

The adoption of the above standards and interpretations did not have any effect on the

financial performance or position of the Group. However, the adoption of certain

standards and interpretations resulted in certain disclosures in the consolidated financial

statements as follows:

IFRS 3 Business Combination (Revised)

IFRS 3 requires an entity to account each business combination by applying the

acquisition method. Applying the acquisition method requires identifying the

acquirer, determining the acquisition date, recognizing and measuring the

identifiable assets acquired, liabilities assumed and any non-controlling interest in

the acquiree and recognizing and measuring goodwill or gain from a bargain

purchase

IFRS 7 Financial Instruments: Disclosures

The amended standard requires additional disclosure about fair value measurement

and liquidity risk.

IFRS 8 Operating Segments

During the year the Group has adopted IFRS 8 “Operating Segments”, which

requires a „management approach‟ under which segment information is presented on

the same basis as that used for internal reporting purposes. The Group concluded

that the operating segments determined in accordance with IFRS 8 are the same as

the business segments previously identified under IAS 14.

IAS 1 Presentation of Financial Statements

The revised standard separates owner and non-owner changes in equity. The

statement of changes in equity includes only details of transactions with owners,

with non-owner changes in equity presented in a reconciliation of each component

of equity. In addition, the standard introduces the statement of comprehensive

income; it presents all items of recognized income and expense, either in one single

statement, or in two linked statements. The Group has elected to present two

statements.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 10 -

3. ADOPTION OF NEW AND REVISED STANDARDS (Deemed Appropriate): (continued…)

IAS 23 Borrowing Costs (Revised)

A revised IAS 23 Borrowing Cost was issued in March 2007, and becomes effective

for financial years beginning on or after January 1, 2009. The standard has been

revised to require capitalisation of borrowing cost when such costs relate to

qualifying asset. A qualifying asset is an asset that necessarily takes an substantial

period of time to get ready for its intended use or sale. The Group accounting policy

was already in accordance with this revised standard.

IAS 40 Investment Property (Amended)

IAS 40 has been amended to bring within its scope investment under construction.

Consequently such property is measured at fair value when completed investment

properties are measured at fair value. However, the adoption of this amendment did

not have any impact on the financial position of the Group as it uses cost model for

measuring its investment properties.

Improvement to IFRS (May 2008)

In May 2008 and April 2009, the IASB issued various amendments to its standards,

primarily with a view to removing inconsistencies and clarifying wording. There are

separate transitional provisions for each standard. The adoption of May 2008

amendments resulted in changes to accounting policies but did not have any impact

on the financial position or performance of the Group. The impact of April 2009

improvements on the consolidated financial position and performance of the Group

is currently being assessed by the management.

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES:

The accounting policies set out below have been applied consistently to all periods

presented in these consolidated financial statements:

4.1 Land:

Land has been allotted to the Parent Entity by the Government of Ras Al Khaimah

free of cost to set up free zones and industrial zones in the Emirate of Ras Al

Khaimah. Land which is mortgaged is stated as per valuation report of valuer and

has been transferred to capital reserve account and the balance has been stated at

nominal value. Land also includes land acquired by subsidiaries in the country of

their operation.

4.2 Property, plant and equipment:

Property, plant and equipment are stated at cost less accumulated depreciation.

Cost comprises of the purchase price and any other attributable cost of bringing

the assets to its working condition for its intended use as per IAS 16.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 11 -

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (continued…)

4.3 Depreciation:

The Group applies the straight-line method in depreciating its property, plant and

equipment over their estimated useful lives of service. Annual rates of

depreciation used are as follows:

Asset Category Percentage

Building 1 – 10

Plant and machinery 2 – 33.33

Tools and equipment 25

Motor vehicles & transportation equipment 3 – 25

EDP system and office equipment 5 – 50

Furniture and fixtures 5 – 50

4.4 Capital work-in-progress:

Capital work-in-progress is recorded at cost incurred by the Group for the

construction of asset. Allocated cost directly attributable to the construction of

assets are capitalized. The capital work-in-progress is transferred to the

appropriate asset category and depreciated in accordance with the Group‟s policies

when construction of the asset is completed and is available for use.

4.5 Investment properties:

Investment properties are properties held for rental income and capital

appreciation and which is not occupied by the Group or its subsidiaries.

Investment properties in Ras Al Khaimah, UAE are stated at cost, less

accumulated depreciation and provision for impairment, where required. The

investment properties in Georgia are not depreciated until the date of their future

use is determined by the Group‟s management. If any indication exists that

investment properties may be impaired, the Group estimates the recoverable

amount as the higher of value in use and fair value less cost to sell. The carrying

amount of an investment property is written down to its recoverable amount

through consolidated income statement.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 12 -

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (continued…)

4.5 Investment properties: (continued…)

An impairment loss recognised in prior years is reversed if there has been

subsequent changes in the estimates used to determine the assets‟ recoverable

amount.

Subsequent expenditure is capitalised only when it is probable that future

economic benefits associated with it will flow to the Group and cost can be

measured reliably. All other repairs and maintenance costs are expensed when

incurred. If an investment property becomes owner-occupied, it is reclassified to

property, plant and equipment, and its carrying amount at the date of

reclassification becomes its deemed cost to be subsequently depreciated.

The Group charged depreciation on straight-line basis over the useful lives of the

investment properties.

4.6 Goodwill:

Goodwill acquired in a business combination is initially measured at cost being

the excess of the cost of the business combination over the Group‟s interest in the

net fair value of the identifiable assets, liabilities and contingent liabilities.

Following initial recognition, goodwill is measured at cost less any accumulated

impairment losses.

Goodwill is tested for impairment annually and when circumstances indicate that

the carrying value may be impaired.

Impairment is determined for goodwill by assessing the recoverable amount of the

cash-generating units, to which the goodwill is allocated. Where the recoverable

amount of the cash-generating units is less than their carrying amount an

impairment loss is recognized. Impairment losses relating to goodwill cannot be

reversed in future periods. The Group performs its annual impairment test of

goodwill at year end.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 13 -

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (continued…)

4.7 Intangible assets:

The Group policy is to recognize intangible assets initially at cost. Intangible

assets are tested annually for impairment and any estimated reduction in value is

charged to the consolidated income statement for the current year. The Group‟s

intangible assets include computer software licenses.

4.8 Trading properties under development:

Properties in the process of construction or development for the purpose of sale on

completion are classified as trading properties under development. Trading

properties under development are measured at the lower of cost and net realizable

value. Cost of trading properties under development is determined on the basis of

specific identification of their individual costs. The classification of trading

properties under development as current and non-current depends upon the

expected date of their completion.

4.9 Investments in associates:

Investments in associates are accounted for using the equity method depending on

the most recent available financial statements of the associated company.

Any gain or loss resulting from investment in the associated company is

recognized in consolidated income statement for the current year.

4.10 Available-for-sale investments:

Available-for-sale investments are initially recognized at cost being the fair value

of the consideration given. After initial measurement, available-for-sale financial

assets are measured at fair value with unrealized gains or losses recognized

directly in the statement of comprehensive income until the investment is

derecognized or determined to be impaired at which time the cumulative gain or

loss recorded in the statement of changes in equity is recognized in the

consolidated income statement. Reversal of impairment loss is not recognized in

the consolidated income statement.

4.11 Loans and advances:

Loans and advances are stated at amortised cost net of provisions for impairment.

All loans and advances are recognised when cash is disbursed to borrowers.

Expenses incurred in making loans and advances are charged to the consolidated

income statement in the year of disbursing these loans and advances.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 14 -

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (continued…)

4.12 Finance lease:

Leases are classified as finance leases whenever the terms of lease transfer

substantially all the risks and rewards incidental to ownership of an asset to the

lessee. All other leases are classifed as operating leases.

Amounts due from lessees under finance lease are recorded as receivables at the

amount of Groups‟s net investment in the leases. Finance lease income is allocated

to accounting period so as to reflect a constant periodic rate of return on the

Group‟s net investment outstanding in respect of the leases.

4.13 Deferred income tax assets recognition:

The recognized deferred tax asset represents income taxes recoverable through

future deductions from taxable profits and is recorded on the statement of financial

position. Deferred income tax assets are recorded to the extent that realization of

the related tax benefit is probable. The future taxable profits and the amount of tax

benefits that are probable in the future are based on medium term business plan

and cash flow projections prepared by management and extrapolated results

thereafter. The business plan is based on management expectations that are

believed to be reasonable under the circumstances.

4.14 Inventories:

Inventories are stated at lower of actual cost and net realizable value. Cost is

determined on average basis. Finished goods are valued at the lower of average cost

and net realizable value. Cost comprises direct cost of production.

4.15 Trade accounts receivable:

Trade accounts receivable are stated at original invoice amount less provision for any

doubtful or uncollectible amount. An estimate of doubtful debts is made when

collection of the full amount is no longer probable. Bad debts are written-off when

there is no possibility of recovery.

4.16 Postdated cheques received:

Postdated cheques received are recognized and accounted for in the books of account

upon their actual collection.

4.17 Cash and cash equivalents:

Cash represents cash on hand and checking accounts with banks. Cash equivalents

represent all highly liquid investments that are readily convertible into known

amounts of cash which are subject to an insignificant risk of changes in value and

include call deposits and fixed deposits with maturities of three months or less from

the date of placement. Bank overdraft balances (if any) that fluctuate from debit to

credit during the year are deducted from cash and cash equivalents.

4.18 Impairment of financial assets:

Financial assets are assessed for indicators of impairment at each financial statements

date. Financial assets are impaired where there is an objective evidence that, as a

result of one or more events that occurred after the initial recognition of the financial

asset, the estimated future cash flows of the financial asset have been impacted.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 15 -

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (continued…)

4.18 Impairment of financial assets: (continued…)

For certain categories of financial assets, such as trade receivables, assets that are

assessed not to be impaired individually are subsequently assessed for impairment

on a collective basis. Objective evidence of impairment for a portfolio of

receivables could include the Group‟s past experience of collecting payments, an

increase in the number of delayed payments in the portfolio past the average credit

period of 120 days, as well as observable changes in national or local economic

conditions that correlate with default on receivables.

The carrying amount of the financial asset is reduced by the impairment loss

directly for all financial assets with the exception of trade receivables, where the

carrying amount is reduced through the use of an allowance account. When a trade

receivable is considered uncollectible, it is written-off against the allowance

account. Subsequent recoveries of amounts previously written-off are credited to

other income. Changes in the carrying amount of the allowance account are

recognized in the consolidated income statement.

If, in a subsequent period, the amount of the impairment loss decreases and

decrease can be related objectively to an event occurring after the impairment was

recognized, the previously recognized impairment loss is reversed through the

consolidated income statement to the extent that the carrying amount of the

investment at the date the impairment is reversed does not exceed what the

amortized cost would have been had the impairment not been recognized.

Unquoted available-for-sale investments are carried at cost due to the

unpredictable nature of future cash flows and the lack of other suitable methods

for arriving at a reliable fair value.

4.19 Trade and settlement date accounting:

The Group adopts the trade date accounting for the regular way purchase and sale

of various categories of financial assets. Trade date accounting requires

recognition of the financial assets on the date of its acquisition or sale by the

Group.

4.20 Non-controlling interests:

Non-controlling interests represent the portion of profit or loss and net assets not

held by the Group and are presented separately in the consolidated income

statement and within equity in the consolidated statement of financial position,

separately from the Parent Entity‟s equity.

4.21 End of service benefit obligation:

The employees‟ end of service benefit obligation (indemnity) is accounted for non

– UAE national employees on the basis of UAE Federal Labour Law.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 16 -

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (continued…)

4.22 Government grants:

Government grants are recognized at their fair value where there is reasonable

assurance that the grant will be received and all attaching conditions will be

complied with. Government grants whose primary condition is that the Group

should purchase, construct or otherwise acquire non-current assets are recognized

as deferred revenue in the consolidated statement of financial position and

transferred to profit or loss on a systematic and rational basis over the useful lives

of the related assets.

4.23 Medium-term bank loans:

Medium-term bank loans are stated in the consolidated statement of financial

position at the amounts received after deducting the installments paid. The

interests on these loans are at the effective market interest rate which was recorded

in the books of account.

4.24 Leased assets:

Where the Group is a lessee in a lease which transferred substantially all the risks

and rewards incidental to ownership to the Group, the assets leased are capitalised

in property, plant and equipment at the commencement of the lease at the lower of

the fair value of the leased assets and present value of the minimun lease

payments. Each lease payment is allocated between the liabilty and finance

charges, so as to achieve a constant rate on the finance balance outstanding. The

corresponding rental obligations, net of future finance charges, are included in the

borrowings. The interest cost is charged to the statement of comprehensive income

over the lease period using the effective interest method. The assets acquired under

the finance leases are depreciated over their useful lives or the shorter lease term if

the Group is not reasonably certain that it will obtain ownership by the end of the

lease term.

4.25 Loans and borrowings:

After initial recognition, interest bearing loans and borrowings are subsequently

measured at amortized cost using the effective interest rate method. Gains and

losses are recognized in the consolidated income statement when the liabilities are

derecognized as well as through the amortization process.

4.26 Short-term employees’ benefits :

The short-term employees‟ benefits are accounted for on the basis of U.A.E.

Federal Labour Law. The leave obligation thereof is calculated on basic salary

plus house and car allowance of each employee and 30 leave days for each year of

service completed less leave availed.

Air ticket obligation is accounted for individually for eligible employees as per the

terms and conditions of employment contracts. Computation is based on the

quoted market prices currently available to the Group for air tickets to various

destinations of employees‟ native countries.

4.27 Trade accounts payable:

Trade accounts payable are measured at original received invoice amount.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 17 -

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (continued…)

4.28 Provisions:

Provisions are recognized when the Group has a legal or constructive obligation as

a result of past event; it is probable that an outflow of resources will be required to

settle the obligation and the amount can be reliably estimated.

4.29 Borrowing costs:

Borrowing costs directly attributable to the acquisition, construction or production

of qualifying assets, which are assets that necessarily take a substantial period of

time to get ready for their intended use or sale, are added to the cost of those

assets, until such time as the assets are substantially ready for their intended use

or sale.

All other borrowing cost are recognized in consolidated income statement in the

period in which they are incurred.

4.30 Foreign currency translations:

The consolidated financial statements are presented in UAE Dirhams (AED) which

is functional currency of the Parent Entity. Each company in the Group determines

its own functional currency and items included in the financial statements of each

entity are measured using that functional currency.

Transactions in foreign currencies are recorded in the functional currency at the

rate ruling at the date of the transaction. Monetary assets and liabilities

determined in foreign currencies are retranslated at the rate of exchange ruling at

the reporting date. All differences are taken to consolidated income statement.

Any goodwill arising on the acquisition of a foreign operation and any fair value

adjustments to the carrying amounts of assets and liabilities arising on the

acquisition are treated as assets and liabilities of the foreign operation and

translated at closing rate.

As at the reporting date, the assets and liabilities of the subsidiaries with the

functional currencies other than AED are translated into AED at the rate of

exchange ruling at the reporting date and their income statements are translated at

the weighted average exchange rates for the year. These differences arising on

the translation are taken directly to the consolidated statement of comprehensive

income. On disposal of an entity, the deferred cumulative amount recognized in

equity relating to that entity is recognized in the consolidated income statement.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 18 -

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (continued…)

4.31 Revenue recognition:

Revenue is recognized in the consolidated income statement when the amount of

revenue can be measured reliably; it is probable that the economic benefits

associated with the transaction will flow to the Group; and the costs incurred or to

be incurred in respect of the transaction can be measured reliably.

Revenue is generally recognized in the consolidated income statement as

follows:

Income from sale of trading properties are recognized on the basis of transfer of

title deed of the properties.

Visa and licensing income is recognized when these services are provided and

invoices are raised to the clients.

Lease rental income is recognized when lease contract is signed and invoices

are raised according to the terms of the relevant lease.

Interest income is accrued on a timely basis, by reference to the principal

outstanding and effective interest rate applicable.

Revenue of other services is recognized when the services are provided and are

invoiced to the clients.

Revenue of sales is generally recognized upon issuance of sales invoices to

customers.

4.32 Income tax:

Taxation is provided in accordance with the relevant fiscal regulations with the

countries in which the Group operates.

Current tax is the expected tax payable on the taxable income for the year, using

tax rates enacted or substantially enacted at the reporting date, and any

adjustments to the tax payable in respect of prior years.

Income tax relating to items recognized directly in equity is recognized in equity

and not in the consolidated income statement.

Deferred income tax is provided, using the liability method, on all temporary

differences at the reporting date between the tax bases of assets and liabilities and

their carrying amounts.

Deferred income tax assets and liabilities are measured at the tax rates that are

expected to apply to the period when the asset is realized or the liability is settled,

based on laws that have been enacted at the reporting date.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 19 -

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: (continued…)

4.32 Income tax:(continued…) Deferred income tax assets are recognized for all deductible temporary

differences and carry-forward of unused tax assets and tax losses to the extent that

it is probable that taxable profit will be available against which the deductible

temporary differences and carry-forward of unused tax assets and unused tax

losses can be utilized.

The carrying amount of deferred income tax assets is reviewed at each balance

sheet date and reduced to the extent that it is no longer probable that sufficient

taxable profit will be available to allow all or part of the deferred income tax asset

to be utilized.

4.33 Financial instruments:

The Group‟s financial instruments are principally comprised of trade and other

receivables, finance lease receivables, loans and advances, deferred tax assets,

cash and banks, end of service benefits obligation, deferred tax liabilities, Sukuk

payable, medium-term bank loans, finance lease liabilities, unsecured loans,

advances from others, advance from customers, trade and other payables, and

short-term borrowings from banks.

The Group uses different assumptions to estimate the fair value of the financial

instruments. The significant assumptions underlying the estimation of fair value of

financial instruments, include, reference to quoted market prices, estimating the

net realizable value, applying the discounted cash flows approach using current

market interest rate, and other assumptions depending on the management‟s past

experience.

If an objective evidence exists that a financial instrument may be impaired, then

the impairment losses are recognized in the consolidated income statement for the

current year.

5. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES

OF ESTIMATION UNCERTAINTY:

In the application of the Group‟s accounting policies, which are described in Note 4, the

management is required to make judgments, estimates and assumptions about the

carrying amounts of assets and liabilities that are not readily apparent from other sources.

The estimates and associated assumptions are based on historical experience and other

factors that are considered to be relevant. Annual results may differ from these

estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions

to accounting estimates are recognized in the period in which the estimate is revised if

the revision affects only that period, or in the period of the revision and future periods if

the revision affects both current and future periods.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 20 -

5. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES

OF ESTIMATION UNCERTAINTY: (continued…)

Critical judgments in applying accounting policies: In the process of applying the Group‟s accounting policies, the management is of the

opinion that there is no instance of application of judgments which is expected to have

effect on the amounts recognized in the consolidated financial statements:

Investments and other financial assets Financial assets within the scope of IAS 39 Financial Instruments: Recognition and

Measurement (Revised) are classified as either financial assets at fair value through profit

or loss, loans and receivables, or available-for-sale investments, as appropriate. The Group

determines the classification of its financial assets at initial recognition.

Valuation of unquoted equity investments

The available-for-sale investments in unquoted securities are carried at cost due to the

unpredictable nature of future cash flows and lack of other suitable methods for arriving at

a reliable fair value.

Impairment of financial assets

The Group determines whether available-for-sale equity financial assets are impaired when

there has been a significant or prolonged decline in their fair value below cost. This

determination of what is significant or prolonged requires judgment. In making this

judgment and to record whether an impairment occurred, the Group evaluates among other

factors, the normal volatility, the financial health of the investee, industry and sector

performance, changes in technology and operational and financial cash flows.

Key sources of estimation uncertainty:

The following are the key assumptions concerning the future, and other key sources of

estimating uncertainty at the consolidated statement of financial position‟s date:

Business combinations

Accounting for the acquisition of a business requires the allocation of the purchase price to

the various assets and liabilities of the acquired business. For most assets and liabilities, the

purchase price allocation is accomplished by recording the asset or liability at its estimated

fair value. Determining the fair value of assets acquired and liabilities assumed requires

judgment by management and often involves the use of significant estimates and

assumptions, including assumptions with respect to future cash inflows and outflows,

discount rates, the useful lives of licenses and other assets and market multiples. The

Group‟s management uses all available information to make these fair value

determinations.

Impairment of loans, advances and receivables

An estimate of the collectible amount of loans, advances and receivable is made when

collection of the full amount is no longer probable. For individually significant

amounts, this estimation is performed on an individual basis. Amounts which are not

individually significant, but which are past due, are assessed collectively and a

provision applied according to the length of time past due, based on historical recovery

rates. Any difference between the amounts actually collected in future periods and the

amounts expected to be received will be recognized in the consolidated income

statement.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 21 -

5. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES

OF ESTIMATION UNCERTAINTY: (continued…)

Fair value of financial instruments

Where the fair value of financial assets and financial liabilities recorded in the statements

of financial position cannot be derived from active markets, they are determined using

valuation techniques including the discounted cash flows model. The inputs to these

models are taken from observable markets where possible, but where this is not feasible, a

degree of judgment is required in establishing fair values. The judgments include

consideration of inputs such as liquidity risk, credit risk and volatility. Changes in

assumptions about these factors could affect the reported fair value of financial

instruments.

Impairment of non financial assets – impairment testing

The Group‟s impairment testing for non financial assets is based on calculating the

recoverable amount of each cash generating unit or group of cash generating units being

tested. Recoverable amount is the higher of value in use and fair value less costs to sell.

Value in use for relevant cash generating units is derived from projected cash flows as

approved by management and do not include restructuring activities that the group is not

yet committed to or significant future investments that will enhance the asset base of the

cash generating unit being tested. Fair value less cost to sell for relevant cash generating

units is generally derived from discounted cash flow models using market based inputs and

assumptions. Recoverable amount is most sensitive to the price assumptions, foreign

exchange rate assumptions and discount rates used in the cash flow models.

Investments and other financial assets

Available-for-sale investments are treated as impaired when there has been a significant or

prolonged decline in the fair value below cost or where other objective evidence of

impairment exists. The determination of what is “significant” or “prolonged” requires

considerable judgment and includes factors such as normal volatility in share price for

quoted equities and the future cash flows and discount factors for unquoted equities.

Contingencies

By their nature, contingencies will only be resolved when one or more future events occur

or fail to occur. The assessment of probability of occurrence of contingencies inherently

involves the exercise of significant judgment and estimates of the outcome of future

events.

6. LAND:

a) This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Land – Note 6 (b) 1,312,235 1,013,061

Land leveling 25,865 24,950

_________ ________

Total – Exhibit A 1,338,100 1,038,011

======== =======

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 22 -

6. LAND: (continued…)

b) The details of land are as follows:

2008

2009

AED’000

AED‟000

(Restated)

Balance as of January 1 1,013,061 635,794

Additions 2,020 115,110

Revaluations – Note 6 (d) & Exhibit D 297,700 262,157

Foreign currency translation differences (546) --

_________ ________

Total – Note 6 (a) above 1,312,235 1,013,061

======= =======

c) The details of land area and valuation during year 2009 are as follows:

Area Amount

(in Sqr. Mts.) AED’000

Land granted by RAK Government and

value stated as per valuation report of the

independent valuer

21,073,788

1,244,707

Purchased land 18,887 29,815

Land situated in foreign country 3,046,037 37,713

Area of land carrying at nominal value 13,226,525 --

_________ _________

Total 37,365,237 1,312,235

======== ========

d) The off-setting amount of land revaluation is credited to capital reserve.

e) The land as shown in Note 6 (b) above includes cost of land amounting to AED

1,082,204 thousands, with service area 8,546,619 square meters, comprises of

various parcel of land which are presently mortgaged with different banks against

financing of various projects of the Parent Entity.

f) Land amounting to AED 1,312,235 thousands as shown in Note 6 (b) above

includes cost of land acquired by a foreign subsidiary amounting to AED 37,713

thousands and which is mortgaged with a bank against finance facility obtained by

the subsidiary.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

23

7. PROPERTY, PLANT AND EQUIPMENT:

Property, plant and equipment are stated at cost less accumulated depreciation as follows:

Buildings

Plant and

machinery

Tools &

equipment

Motor

vehicles &

transportation

equipment

EDP system &

office equipment

Furniture &

fixtures

Total

AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000

Cost:

At January 1, 2009 498,753 20,155 1,053 48,138 9,605 12,868 590,572

Additions 17,635 363,446 2,548 3,727 2,617 4,419 394,392

Disposals (1,421) (377) -- (312) (877) (96) (3,083)

Transfers from CWIP 16,312 133,934 -- (4,657) 2,068 -- 147,657

Revaluation decrease (23,693) (7,440) -- (1,887) -- -- (33,020)

Foreign currency translation differences (7,159) (163) -- . (671) (111) (285) (8,389)

At December 31, 2009 500,427 509,555 3,601 44,338 13,302 16,906 1,088,129

Accumulated Depreciation:

At January 1, 2009 1,428 3,161 -- 862 5,524 2,602 13,577

Charged for the year 8,107 12,162 231 3,965 1,353 2,196 28,014

Disposals (11) (24) -- (59) (633) -- (727)

Elimination on revaluation (6,037) (2,014) -- (3,653) -- -- (11,704)

Impairment -- -- -- -- -- 845 845

Foreign currency translation differences (20) -- . -- . -- . (18) (17) (55)

At December 31, 2009 3,467 13,285 231 1,115 6,226 5,626 29,950

Carrying Amount:

At December 31, 2008 (Restated) – Exhibit A 497,325 16,994 1,053 47,276 4,081 10,266 576,995

====== ====== ====== ====== ====== ====== =======

At December 31, 2009 – Exhibit A 496,960 496,270 3,370 43,223 7,076 11,280 1,058,179

====== ====== ====== ====== ====== ====== =======

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

24

8. CAPITAL WORK-IN-PROGRESS:

a) The details of capital work-in-progress are as follows:

2008 2009

AED’000

AED‟000

(Restated)

RAKIA Accommodation 115,750 --

Al Hamra Industrial Zone infrastructure 67,956 59,083

Al Hamra Free Zone infrastructure 41,625 24,548

Labour Accommodation 13,685 20,787

Al Ghayl Zone infrastructure 46,681 28,666

RAK Financial City 16,346 12,447

Customs Building 2,407 2,364

Al Hamra Amenity Centre 50,499 66,443

Al Hamra Power Project -- 133,934

Construction in progress in Georgia – Subsidiaries 8,624 4,639

Al Hamra Commercial Centre -- 6,884

Other projects 9,835 1,546

Total – Exhibit A 373,408 361,341

======= ======

b) The movements over capital work-in-progress are as follows:

2008 2009

AED’000

AED‟000

(Restated)

Balance as at January 1 361,341 128,086

Additions during the year 287,516 342,922

Transferred to property, plant and equipment (147,657) (106,198)

Transferred to trading properties (127,725) --

Disposal -- (3,469)

Foreign currency translation difference (67) --

_________ _________

Balance as at December 31 373,408 361,341

========= =========

9. INVESTMENT PROPERTIES:

Investment properties consist of land plots and building acquired by the Group in Ras

Al Khaimah, UAE and Georgia. The Group has not started any development or

construction work over this property and neither determined its future use. As such the

acquired property is regarded as held for capital appreciation. The investment properties

in Ras Al Khaimah are depreciated annually. The investment properties in Georgia are

not depreciated until the date of their future use is determined by the Group

management. The carrying value of investment properties is reviewed for impairment at

each financial statements date. As of December 31, 2009, the fair value of investment

properties was estimated and stated as per valuation report of independent appraiser in

Georgia.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

25

9. INVESTMENT PROPERTIES: (continued…)

The movement over this account is as follows:

Cost: AED’000

At January 1, 2009 33,390

Additions 127,725

Disposal (142)

Foreign currency translation difference (480)

_______

At December 31, 2009 160,493

======

Accumulated impairment

At January 1, 2009 5,871

Charged for the year 6,232

Foreign currency translation difference (85)

_______

At December 31, 2009 12,018

======

Carrying amount:

At December 31, 2008 (Restated) – Exhibit A 27,519

======

At December 31, 2009 – Exhibit A 148,475

======

10. GOODWILL:

Goodwill as shown in Exhibit A represents goodwill recognized on acquisition of a

subsidiary, JSC Poti Sea Port - Georgia. The detail of goodwill calculation is as follows:

2008 2009

AED’000

AED‟000

(Restated)

Percentage of shares held by Parent Entity 100 % 51 %

Amount paid for acquisition of shares 532,657 293,880

Less: Share of net worth in the subsidiary (408,704) (208,440)

________ ________

Net – Exhibit A 123,953 85,440

======= =======

11. OTHER INTANGIBLE ASSETS:

a) Other intangible assets comprise of software license obtained and web page

developed for operational needs.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

26

11. OTHER INTANGIBLE ASSETS: (continued…)

b) Other intangible assets are stated at cost less accumulated amortization as follows:

Total

Cost: AED’000

At January 1, 2009 1,636

Additions 72

Foreign currency translation differences (23)

At December 31, 2009 1,685

====

Accumulated amortization:

At January 1, 2009 455

Amortized during the year 256

Impairment during the year 77

Foreign currency translation differences (9)

At December 31, 2009 779

====

Carrying amount:

At December 31, 2008 (Restated) – Exhibit A 1,181

====

At December 31, 2009 – Exhibit A 906

====

12. TRADING PROPERTIES UNDER DEVELOPMENT:

a) Trading properties under development represent the costs of the following projects:

2008

2009

AED’000

AED‟000

(Restated)

Al Marjan Island – Note 12 (b) 1,043,776 946,912

Dana Island 354,647 357,723

Gateway City 138,672 126,242

RAK Financial City 54,133 50,668

Al Hamra Views 13,521 12,992

Other projects 6,430 4,785

Total – Exhibit A 1,611,179 1,499,322

======= =======

b) The cost of Al Marjan Island amounting to AED 1,043,776 thousands as shown above

includes an amount of AED 101,605 thousands being the capitalized cost of profit on

Sukuk.

c) The movement details of trading properties under development are as follows:

2008

2009

AED’000

AED‟000

(Restated)

Balance at January 1 1,499,322 408,201

Additions of new projects 216,411 765,118

Sale of a parcel of land (131,678) (53,547)

Deferred commission on projects 27,124 379,550

Net – Note 12 (a) above 1,611,179 1,499,322

======= ========

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

27

13. INVESTMENTS IN UNCONSOLIDATED SUBSIDIARIES:

a) Transactions over this account are as follows:

2008

Country of

Incorporation

Legal Form

Percentage of

Holding

2009

AED’000

AED‟000

(Restated)

London International Television Ltd. - Note 13 (b) U.K. LTD 53 11,612 11,612

RAK Power LLC - Note 13 (b) RAK LLC 70 700 700

JSC Poti Sea Port Georgia JSC 100 -- 330,615

__________ ________ _________ ______ _______

Total 12,312 342,927

Beaufort RAK LLC (restated) – Note 13 (c) 29,999 29,999

JSC Poti Sea Port transferred to consolidated subsidiaries

(restated) (refer to Note 10)

--

(293,880)

Transferred to advance for investment in subsidiary

(JSC Poti Sea Port)

--

(36,735)

Subsidiary sold during the year (29,999) --

Provision for impairment of investment in subsidiaries (12,312) (7,347)

_______ _______

Net - Exhibit A -- 34,964

====== ======

b) Impairment for these unconsolidated subsidiaries have been fully provided for during the year 2009.

c) This subsidiary has been disposed off and loss on disposal is recognized during the year.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

- 28 -

14. INVESTMENTS IN ASSOCIATES:

a) This item comprises of the following:

2008

Country of

incorporation

Legal

form

Percentage of

holding

2009

AED’000

AED‟000

(Restated)

Falcon Technologies International LLC U.A.E L.L.C 33 5,822 16,617

ANRAK Aluminium Ltd. – Note 14 (c), (d) India LTD 30 156,165 73,511

Pioneer Cement Industries LLC U.A.E L.L.C. 50 104,380 121,213

Polo RAK Amusement LLC - Note 14 (c) U.A.E L.L.C 25.5 12,716 8,509

Spira International LLC U.A.E L.L.C 20 -- 6,388

RAK Ghani Glass LLC U.A.E L.L.C 20 9,089 6,809

RAK Petropack LLC U.A.E L.L.C 36 2,463 896

RAK Warehouse & Leasing LLC U.A.E L.L.C 50 1,811 2,300

Channel Energy (Poti) Limited – Note 14 (e) Georgia LTD 25 5,351 4,885

Doctranshipment (Poti) Limited – Note 14 (e) Georgia LTD 50 1,355 1,355

EPFL RAKIA LLC – Note 14 (c) U.A.E L.L.C 50 750 -- .

Total – Note 14 (b) 299,902 242,483

Provision for impairment of investments in associates -- (3,800)

_______ _______

Net - Exhibit A 299,902 238,683

====== ======

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

29

14. INVESTMENTS IN ASSOCIATES: (continued…)

b) Movements over these accounts are as follows:

Balance at

Dec. 31,

2008

Additions

Dividend

Received

Profit

/(Loss)

during

the year

Disposed

during

the year

Foreign

currency

translation

difference

Balance at

Dec. 31,

2009

AED’000

(Restated)

AED’000

AED’000

AED’000

AED’000

AED’000

AED’000

Falcon Technologies International L.L.C. 16,617 -- -- (10,795) -- -- 5,822

ANRAK Aluminium Ltd.- Note 14 (c), (d) 73,511 82,654 -- -- -- -- 156,165

Pioneer Cement Industries L.L.C. 121,213 -- (82,688) 65,855 -- -- 104,380

Polo RAK Amusement L.L.C. - Note 14 (c) 8,509 4,207 -- -- -- -- 12,716

Spira International L.L.C. 6,388 -- -- -- (6,388) -- --

RAK Ghani Glass L.L.C. 6,809 -- -- 2,280 -- -- 9,089

RAK Petropack L.L.C. 896 400 -- 1,167 -- -- 2,463

RAK Warehouse & Leasing L.L.C. 2,300 -- -- (489) -- -- 1,811

Channel Energy Limited – Note 14 (e) 4,885 -- -- 541 -- (75) 5,351

Doctranshipment Poti JSC – Note 14 (e) 1,355 -- (44) 44 -- -- 1,355

EPFL RAKIA L.L.C. – Note 14 (c) -- 750 -- -- -- -- 750

________ _______ ________ _______ ________ ______ _______

Total – Note 14 (a) above 242,483 88,011 (82,732) 58,603 (6,388) (75) 299,902

======= ====== ======= ===== ======= ====== ======

c) These associates have not started their commercial activities as of the financial statements date.

d) This associate‟s investment value represent the share of RAK Investment Authority as of the financial statements date.

e) These associates are associates of subsidiary and are located in foreign country.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

30

15. AVAILABLE-FOR-SALE INVESTMENTS:

a) The movements over these investments are as follows:

2008

2009

AED’000

AED‟000

(Restated)

Balance at January 1 214,439 96,125

Purchase during the year 781 162,514

Transferred from advance for investment in projects 7,125 --

Transferred from investment in associates -- 500

Sold during the year (500) --

Difference resulting from re-measurement of

available-for-sale investments – Exhibit C

11,410

(44,700)

Net - Exhibit A 233,255 214,439

======= ======

b) Available-for-sale investments are classified as follows:

2008

2009

AED’000

AED‟000

(Restated)

Quoted investments 60,910 49,500

Unquoted investments 172,345 164,939

Total – Note 15 (a) above 233,255 214,439

====== ======

Unquoted available-for-sale investments are carried at cost due to the

unpredictable nature of future cash flow and lack of other suitable methods for

arriving at a reliable fair value.

c) Available-for-sale investments are classified into the following business segments:

2008

2009

AED’000

AED‟000

(Restated)

Real estate sector 156,737 155,957

Banking sector 60,910 49,500

Airline sector 11,318 4,193

Industrial sector 4,290 4,789

________ _______

Total – Note 15 (a) above 233,255 214,439

======= ======

Investment in banking sector (quoted) amounting to AED 60,910 thousands has

been disposed off during January 2010.

d) Geographical concentration of available-for-sale investments is as follows:

2009

AED’000

2008

AED‟000

(Restated

Within U.A.E. 231,518 213,482

Outside U.A.E. 1,737 957

________ ________

Total – Note 15 (a) above 233,255 214,439

======= =======

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

31

16. ADVANCES FOR INVESTMENT PROJECTS:

a) This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Advances for investment in subsidiaries

– Note 16 ( b)

429,416

488,538

Advances for investment in associates 86,445 85,491

Advances for other investments 44,519 51,644

Total – Exhibit A 560,380 625,673

====== ======

b) Advances for investment in subsidiaries:

This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Advance to RAK Infra Holding Ltd.- Mauritius 257,320 257,320

Advance to RAK Vision Ltd.- Mauritius 146,125 146,960

Advance to JSC Poti Sea Port – Georgia -- 36,735

Advances for other investment in subsidiaries 25,971 47,523

Total – Note 16 (a) above 429,416 488,538

====== ======

17. ADVANCES TO CONTRACTORS:

a) This item consists of the following:

2008

2009

AED’000

AED‟000

(Restated)

Advances for capital work-in-progress

– Note 17 (b)

13,717

109,813

Advances for investment projects – Note 17 (c) 98,289 73,601

_______ _______

Total – Exhibit A 112,006 183,414

====== ======

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

32

17. ADVANCES TO CONTRACTORS: (continued…)

b) Advances for capital work-in-progress:

This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Balance at January 1, 109,813 13,676

Paid during the year 989 109,813

Transferred to capital work-in-progress (5,272) (12,676)

Transferred to property, plant and equipment (6,768) --

Transferred to advance for trading property

and development

(11,575)

--

Advance refunded (73,470) --

Transferred to land --___ (1,000)

Balance at December 31- Note 17 (a) above 13,717 109,813

====== =======

c) Advances for trading properties under development:

This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Balance at January 1 73,601 37,480

Paid during the year 53,081 36,121

Transferred from advance for CWIP 11,575 --

Transferred to trading property under

development

(39,968)

--___

Balance at December 31- Note 17 (a) above 98,289 73,601

====== ======

18. LOANS AND ADVANCES:

a) Loans and advances are classified as follows:

2008

2009

AED’000

AED‟000

(Restated)

Non-curent assets – Note 18 (b) & Exhibit A 625,624 581,162

Current assets – Note 18 (c) & Exhibit A 102,213 263,607

Total 727,837 844,769

======= =======

b) This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Rakeen Development PJSC – Note 18 (d) 283,293 282,433

Dana Executive Air– Note 18 (e) 224,541 185,186

Falcon Techonologies International L.L.C.

– Note 18 (f)

117,790

113,543

Total – Note 18 (a) above 625,624 581,162

======= ======

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

33

18. LOANS AND ADVANCES: (continued…)

c) This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Advance to suppliers 64,560 38,475

Ras Al-Khaimah Ceramics Co. PSC

– Note 18 (g)

26,640

210,410

Polo RAK Amusement L.L.C. – Note 18 (h) 7,000 2,500

Loan to subsidiaries -- 7,643

Advances to others 4,013 4,579

_______ _______

Total – Note 18 (a) above 102,213 263,607

====== ======

d) The loan amounting to AED 283,293 thousands granted to RAKEEN

Development PJSC (RAKEEN) is interest-bearing unsecured loan for an

unspecified repayment period. Also, the Group has 10.88 percentage of holding

amounted to AED 155,000 thousands in RAKEEN‟s capital which is classified

under available-for-sale investments (refer to Note 15).

e) The loan granted to Dana Executive Air amounted to AED 224,541 thousands is

non-interest bearing unsecured loan with an unspecified period.

f) The loan amounting to AED 117,790 thousands was granted to Falcon

Technologies International LLC (FTI), an associate, is interest-bearing

unsecured loan. The repayment of the loan was scheduled to commence during

the year 2009. However, the loan repayment has not yet been commenced and

the management has intended to reschedule the loan. The Group‟s management

believes that the loan due from FTI is fully recoverable.

g) The amount of AED 26,640 thousands owed by RAK Ceramics Co. PSC is

interest-bearing unsecured loan to be fully settled during the year 2010.

h) The amount of AED 7,000 thousands owed by Polo RAK Amusement LLC is

interest bearing unsecured loan and is due to commence during the year 2010.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

34

19. FINANCE LEASE RECEIVABLE:

a) This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Amount receivable under finance lease:

Within one year 23,018 20,585

2 to 5 years 124,872 121,944

Above 5 years 458,873 486,805

Total 606,763 629,334

Less: Unearned finance charges (526,353) (552,503)

Present value of minimum payment

receivable

80,410

76,831

======= ======

b) Maturity-wise detail of finance lease receivable is as follows:

2008

2009

AED’000

AED‟000

(Restated)

Non-current finance lease receivable

– Exhibit A

60,007

57,338

Current finance lease receivable – Exhibit - A 20,403 19,493

Total 80,410 76,831

====== ======

20. INVENTORIES:

This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Spare parts 9,064 9,099

Materials 4,855 7,398

Food and beverages 327 582

Fuel 582 730

Others 185 98

Total – Exhibit A 15,013 17,907

====== =====

21. TRADE AND OTHER RECEIVABLES:

a) This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Trade accounts receivable – Note 21 (b) 83,341 64,135

Due from associates 9,276 315

Other receivables – Note 21 (c) 31,619 13,447

Total – Exhibit A 124,236 77,897

======= ======

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

35

21. TRADE AND OTHER RECEIVABLES (continued…)

b) Trade accounts receivable:

This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Trade accounts receivable 97,833 75,370

Provision for impairment of trade

receivables

(14,492)

(11,235)

Net – Note 21 (a) above 83,341 64,135

====== ======

Trade accounts receivable amounting to AED 97,833 thousands include an

amount of AED 44,492 thousands being due from thirteen clients only, which

constitutes 45% of the total balance thereof.

Unimpaired receivables are expected on the basis of past experiences to be fully

recoverable. It is not the general practice of the Group to obtain collateral over

receivables and vast majority are therefore, unsecured.

Trade receivables are non-interest bearing and are generally 120 days term.

The ageing analysis of trade receivables as of December 31, 2009 is as follows:

Less than

30 days

Between

30 to 90

days

Between

90 to 180

days

More

than 180

days

Neither

past due

nor

impaired

Total

AED’000 AED’000 AED’000 AED’000 AED’000 AED’000

2009 17,701 19,957 15,197 23,999 20,979 97,833

===== ===== ====== ====== ===== =======

2008 2,926 4,955 8,272 12,215 47,002 75,370

===== ====== ====== ===== ===== =======

c) Other receivables:

This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Prepaid expenses 2,492 430

Refundable deposits 1,156 302

Tax/VAT recoverable 18,328 10,940

Advance to suppliers 6,246 1,479

Accrued interest 1,081 --

Sundry receivables 2,316 296

Total – Note 21 (a) above 31,619 13,447

====== =====

d) Postdated cheques amounting to AED 271,231 thousands were received as of

the financial statements date. These cheques will be recognized upon their

actual collection.

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

36

22. CASH AND BANKS:

a) This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Cash on hand and in transit 744 963

Bank checking accounts 46,587 89,047

Demand deposits with banks 6,595 6,222

Fixed deposit with maturity of less

than three months

155,057

63,578

Overdrawn book balances of

bank checking account

(1,651)

--

_______ _______

Cash and cash equivalents – Exhibit E 207,332 159,810

Bank deposit - Note 22 (b) 11,692 --

Guarantee margin deposit with bank 158 -- .

Total - Exhibit A 219,182 159,810

====== =======

b) Bank deposits as shown in Note 22 (a) above represent restricted cash with a bank

situated in Georgia.

c) Location-wise detail of cash and banks is as follows:

2008

2009

AED’000

AED‟000

(Restated)

Within UAE 181,752 122,827

Outside UAE 37,430 36,983

Total – Note 22 (a) above 219,182 159,810

====== ======

RAK INVESTMENT AUTHORITY – GOVERNMENT OF RAS AL KHAIMAH

AND ITS SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2009

37

23. RESERVES:

a) This item comprises of the following:

2008

2009

AED’000

AED‟000

(Restated)

Capital reserve emerged from recognition

of land granted by Govt. of RAK –

(Refer to Notes 6 (c) & (d) )

1,195,651

897,951

Property, plant and equipment

revaluation reserve

51,737

33,086