Embed Size (px)

Citation preview

Rail Costing and Regulation: The Uniform Rail Costing System

Wesley W. Wilson and Frank A. Wolak University of Oregon Stanford University

Motivation • Staggers Act significantly expanded pricing discretion

of railroads – Complete pricing freedom for movements deemed to be

“effectively competitive” – Freedom to negotiate contract rates subject to constraint

that contract does not harm common carrier service – Tariff rates can be subject to regulatory review if they are

set by a “market dominant” shipper • Staggers Act and preceding legislation set two major

goals for new regime – Protect captive shippers from excessive prices – Ensure revenue adequacy necessary for long-term

financial viability of railroads

Motivation • “Variable cost” of shipment calculated using

Uniform Rail Costing System (URCS) is a major input to meeting both of these goals – Input to market dominance test – Input to determining excessive prices

• URCS “variable cost” is computed using 15 accounting-based cost activities by allocating a portion of the total costs for each category to each shipment based on a variability ratio of each activity – Predicted percent of activity-specific costs that vary

with output of activity

Motivation • Implication--URCS “variable cost” of a shipment is

an “allocated cost” concept that bears little relation to railroad costs caused by shipment – Incremental cost of shipment

• Ratio of revenue for shipment (R) to URCS “variable cost” (VC) is used as a basis for determining market dominance of shipment

• R/VC greater than 180 percent is necessary for shipper to have possibility for regulatory relief from STB

Purpose of Paper • Evaluate current approach employed by STB to

provide rate relief to shippers subject to market dominance – Assess economic foundation for using URCS “variable

cost” as basis for allowing shipper access to regulatory relief process

• Evaluate economic foundation for using URCS ‘variable cost” to determine a reasonable price

• Discuss market efficiency consequences of using URCS to set maximum reasonable price for a shipment

• Evaluate need for continued collection and production of railroad cost data

Outline of Presentation

• Background on railroad industry post-Staggers • Review of Staggers Act mandate and how it is

implemented by STB • Describe of basic features of URCS procedure • Present simplified model of railroad costs and

pricing – Determining incremental cost of shipment – Setting profit-maximizing shipment prices

• Need for and use of railroad cost data going forward

Background • Partial deregulation of railroads to place greater

reliance on the market mechanisms to set rates • Staggers Act was intended to “[strip] away needless

and costly regulation in favor of marketplace forces wherever possible” (Carter 1980).

• Rate regulatory oversight was significantly changed – No price regulation for shipments deemed “competitive”

by STB – Negotiated contracts between shipper and railroads

allowed – Regulation only over movements where a rail carrier was

deemed market dominant • Eased and streamlined merger reviews and rail line

abandonments and sales reviews

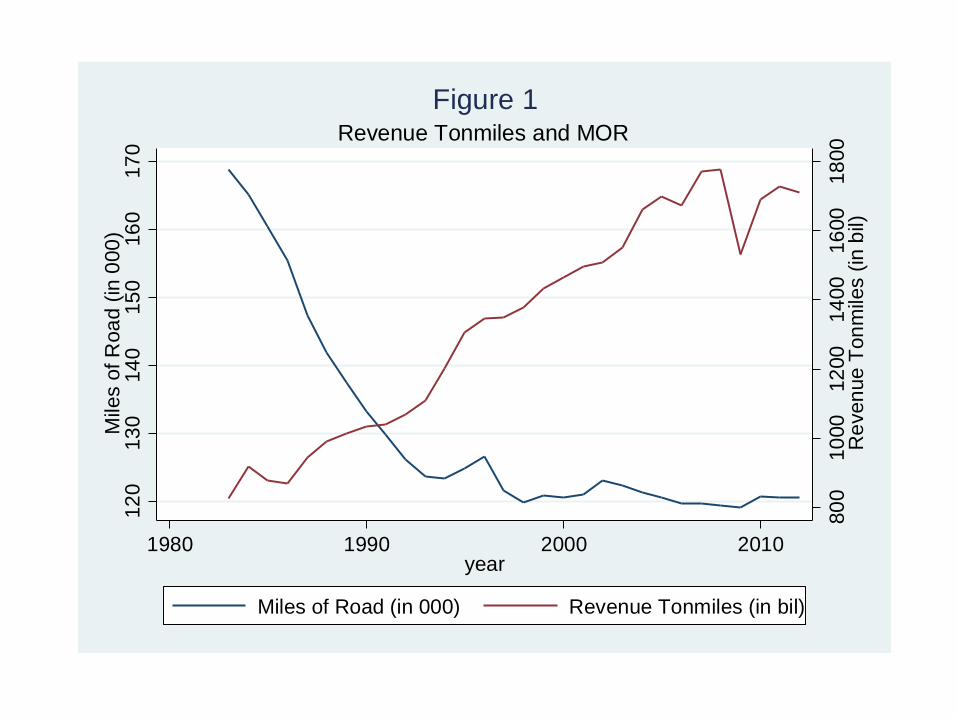

Background • Dramatic changes post-Staggers Act

– A massive consolidation movement (from 40 Class I carriers to 7, most through mergers)

– Reduction in rates from 6.46 cents/ton-mile in 1980 to 3.29 cents/ton-mile in 2013 (2009$)

– Reduction in size of network held by Class I carriers from 164,822 miles in 1980 to 95,391 in 2013.

– Increases in average length of haul from 615 to 973 miles

Background

– Many shippers now have only one railroad option and many face high prices for rail shipments

– Some shippers cannot negotiate “reasonably priced” contracts with railroad

– Rail networks are smaller but they are moving significantly more tonnage over the network.

• Allocation to higher-priced traffic • Service issues • Network congestion

800

1000

1200

1400

1600

1800

Rev

enue

Ton

mile

s (in

bil)

120

130

140

150

160

170

Mile

s of

Roa

d (in

000

)

1980 1990 2000 2010year

Miles of Road (in 000) Revenue Tonmiles (in bil)

Revenue Tonmiles and MORFigure 1

02

46

8

1980 1990 2000 2010year

rel_mor rel_rtm

Average Revenue Tonmiles and Miles of Road (relative to 1983)Figure 3

500

600

700

800

900

Ave

rage

Len

gth

of H

aul

1980 1990 2000 2010year

Average Length of HaulFigure 4

2025

3035

4045

wei

ghte

d_ut

1980 1990 2000 2010year

Unit Train PercentageFigure 5

STB Regulatory Oversight Process

STB Regulatory Oversight • Contract rates are not subject to regulatory review (some

limited review of agricultural commodity contracts). • Some car types/commodities exempted because STB has

determine these shipments have competitive alternative • Remaining rates, “tariff” rates, are subject to regulatory

review for reasonableness if provider of movement is deemed “market dominant” – Market dominance means that R/VC>180 percent and there is a lack

of competitive options (intramodal and intermodal). – Notably if R/VC<180, the rate is not market dominant and the finding

cannot be rebutted.

• VC of a movement is calculated using URCS

Rate Reasonableness Process • If market dominance is found by STB, then the level of rate

can be scrutinized by three alternatives – SAC (Stand-Alone Cost)

• Seeks to determine the lowest cost at which a hypothetical, efficiently operating carrier could provide service.

• Docket 715: “the rate at issue cannot be higher than the rate a hypothetical efficient railroad would need to charge to serve the complaining shipper while fully covering all of its costs, including a reasonable return on investment. In other words, we judge the challenged rate against a simulated competitive rate a captive shipper would enjoy if a competitive transportation market existed.”

– Pittman (2010) documents significant time and financial costs of this procedure ($5 million) and argues that its application to the railroad industry is inappropriate

– Shippers complain SAC process is too complex and expensive

Rate Reasonableness Process • Simplified SAC:

– Limits evidence that can be submitted to streamline process

– Find the replacement cost of the existing facilities used to serve the captive shipper and the return on investment a hypothetical railroad would require to replicate those facilities

– $5 million limitation on relief from excessive rates that a shipper can collect

Rate Reasonableness • Three benchmark: An examination of three

benchmarks are used to evaluate the reasonableness of the rate. – 1. The average markup above VC that a carrier would

need to charge all of its potentially captive traffic (i.e., those with ratios greater than 180 percent) to recover all of its non-variable costs;

– 2. The average markup above variable costs that a carrier receives on its captive traffic (R/VC) greater than 180 percent); and

– 3. The average markup assessed on other potentially captive traffic involving the same or a similar commodity moving similar distances

• $1 million cap on relief that shipper can receive

Rate Regulation and URCS

• URCS is used to – Determine jurisdiction of the STB to initiate

rate review process – Determine the reasonableness of rates

using all three tests • SAC • Simplified-SAC • Three benchmarks

Uniform Railroad Costing System

URCS

• Adopted in 1989 after years of development • Replaced Rail Form A which was introduced in

1939. • It is the STB’s general costing program • Used by STB to compute “variable cost” (VC)

of a shipment

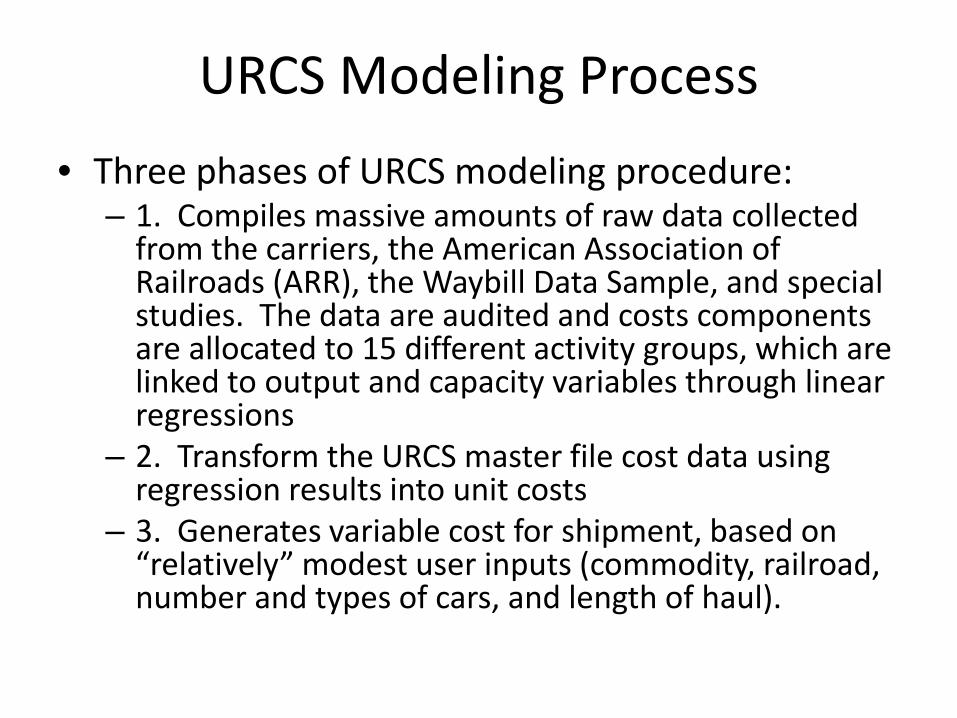

URCS Modeling Process • Three phases of URCS modeling procedure:

– 1. Compiles massive amounts of raw data collected from the carriers, the American Association of Railroads (ARR), the Waybill Data Sample, and special studies. The data are audited and costs components are allocated to 15 different activity groups, which are linked to output and capacity variables through linear regressions

– 2. Transform the URCS master file cost data using regression results into unit costs

– 3. Generates variable cost for shipment, based on “relatively” modest user inputs (commodity, railroad, number and types of cars, and length of haul).

URCS Modeling Process

• Activity groups are defined in terms of similarities of costs, judgements and generally accepted accounting practices.

• The calculation of URCS “variable costs” – Rhodes and Westbook (1986): “… shipment variable

costs are weighted averages of total costs from individual cost categories that comport with cost categories defined in railroad accounting practices.”

– The weights used to compute VC are proportional to the variability ratios of each activity

• Variability ratio = Fraction of total costs that activity-level regression predicts are “variable”

URCS Properties • No reason to expect that this VC has any relationship to

the incremental cost of the rail movement (cost caused by movement) in the sense defined by Panzer (1989) – IC(qj|Q-j) = C(qj,Q-j) – C(0.Q-j),

• Q-j is the (J-1)-dimensional vector of tonnages associated with the other J-1 movements by the railroad

• C(qj*,Q-j*) is total cost of railroad producing the J-dimensional output vector (qj*,Q-j*’)’.

• Note: A profit-maximizing railroad would not price below average incremental cost of providing shipment – Doing so would imply a reduction in railroad’s profits

URCS Properties • Christensen Associates (2009) found

– 22 percent of ton-miles have R/VC values less than 100 (2000-2001)

– 29 percent of ton-miles have R/VC values less than 100 (2005-6)

• Findings are not surprising given that URCS shipment VCs are based on arbitrary accounting-based cost allocation methodology – Different allocated cost methodologies would yield

different frequencies of violation of this “rational pricing” constraint

– Different cost allocation methodologies will produce different sets of shipments violating R/VC > 180 test

Other Properties of URCS • URCS methodology does not account for any input

substitution in production in response to changes in level of output

• URCS costs are based on linear relationship between activity-level measures of cost and output – Greatly simplifies, but is likely to be inconsistent with how rail

costs are actually incurred (Griliches, 1988) • Activity-level relationship approach to cost allocation does

not allow for economies density in providing rail service • Christensen Associates (2009) also found that R/VC

relationships are only weakly correlated with measures of competition they construct.

Other Properties of URCS • URCS uses information for special studies

conducted in the 1930s • Some of the activity-level cost/output

relationships did not produce sensible regression results and were assigned an ad hoc default variability ratio

• Conclusion—URCS measure of “variable cost” of shipment based on arbitrary cost allocation rules that are likely to be unrelated to causally related costs of shipment that determine shipment price

Profit-Maximizing Pricing • Profit-maximizing multi-product firm (railroad) serving independent

demands sets prices for each of J (j=1,2,…,J) goods (shipments) to satisfy – (P(j) – MC(j))/P(j) = -1/η(j) – P(j) is price of jth good (shipment) – MC(j) = ∂C(qj,Q-j)/∂qj is marginal cost of jth good (shipment) – η(j) is own-price elasticity of demand for jth good (depends on

competition railroad faces from competitors for jth shipment) • Implications of profit-maximizing pricing

– Prices can differ across shipments for same origin and destination pair, depending on differences in marginal costs and demand elasticities for shipments

– Markups, (P(j) – MC(j))/P(j), can differ across shipments for same origin and destination pairs depending on elasticity of demand for shipment

The Usefulness of Cost Information • Large portions of total cost of railroad do not vary

with tonnages or even its composition – Railroads therefore must price above average

incremental costs on most if not all shipments to recover total costs

• Even perfect estimate of railroad cost function, C(qj,Q-j), would not solve the problem of what constitutes an unreasonable rate for shipper – Just changes problem from setting “minimal excessive

price” to that of setting “minimal excessive markup”

Challenge of Setting Maximum Markups • Setting a single maximum markup for all

shipments would likely produce significant shipper and railroad welfare losses – Total welfare maximizing prices subject to zero

economic profit constraint (Ramsey Prices) set markups inversely related to demand elasticities (similar to profit-maximizing firm)

– (P(j) – MC(j))/P(j) = -λ/η(j) where 0< λ< 1 • This logic argues for focusing regulatory process

on setting maximum price for shipments, based on shipment characteristics, rather than maximum markup for shipment

Should STB Collect Cost Information? • Strong reasons to discontinue to use of URCS to

determine excessive prices and set regulated prices • STB still needs railroad cost and output data to meet

other aspects of its regulatory mandate – Re-focus data collection efforts to serve these goals

• Areas where cost data is needed – Service quality regulation – Infrastructure adequacy – Operating and maintenance adequacy – Safety effort and expenditure adequacy

• Cost and output data can be used to benchmark railroads to enhance ability of STB to achieve these regulatory mandates

Conclusions • URCS “variable costs” are the result of an arbitrary cost

allocation mechanism that bears little relation to cost constructs that determine pricing decisions of profit-maximizing railroad

• Estimates of railroad cost function only changes regulatory challenge from setting maximum price to setting maximum markup over “economically relevant” measure of cost (marginal cost) of shipment

• Focusing on setting maximum price avoids needs to perform massively complex task of estimating railroad’s cost function

• Cost data collection process should be streamlined to focus on where cost data is needed to meet STB’s regulatory mandate

Questions/Comments?

![[vc 1037 - listing.archiviolocation.com · [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM [vc 1037] ARCHIVIOLOCATION.COM. archivio location](https://img.pdfslide.us/doc/110x75/5fcd99d1df347e1ae154645c/vc-1037-vc-1037-archiviolocationcom-vc-1037-archiviolocationcom-vc-1037.jpg)