Embed Size (px)

Citation preview

RECENT AMENDMENTS IN COMPANIES ACT 2013

COMPANIES ACT 2013 SO FAR The Companies Act 2013 got assent of the

President of the country on 29th August, 2013.

The Companies Act, 2013 Published in the Official Gazette of India. The Act consists of 29 chapters, 470 Sections with 7 Schedules

98 Sections of the Act were notified and made applicable by the Ministry of Corporate Affairs on 12th September, 2013

Section 135 (Corporate Social Responsibility) was notified on 27th February, 2014

CONTD….

Further 183 sections of the Act were notified on 26th March’ 2014 and made applicable from 1st April, 2014

A total of 283 sections are notified as of date.

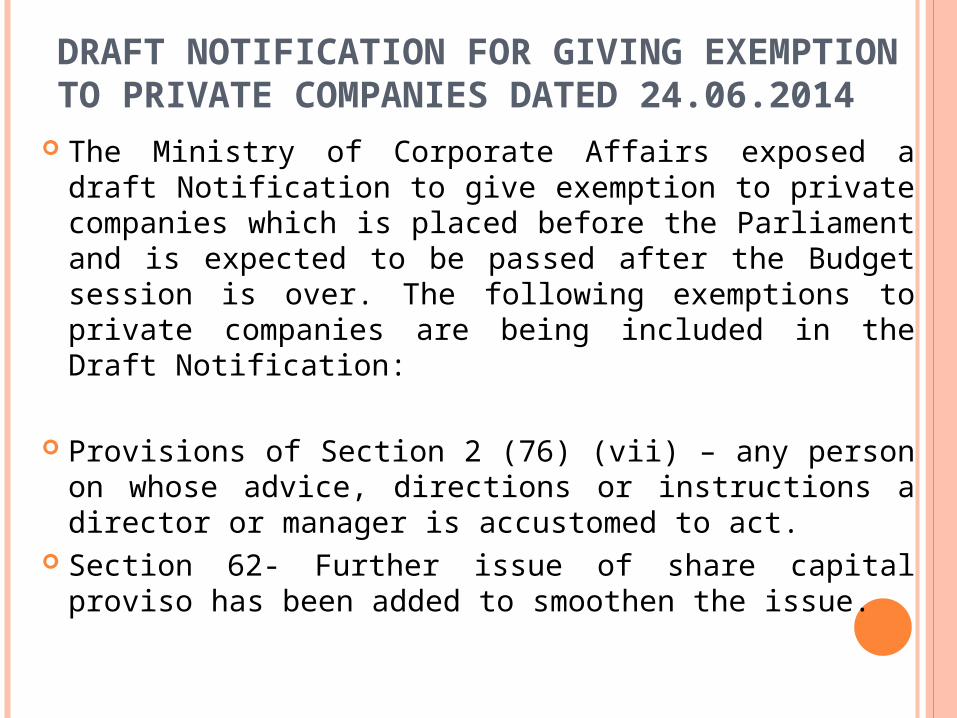

DRAFT NOTIFICATION FOR GIVING EXEMPTION TO PRIVATE COMPANIES DATED 24.06.2014

The Ministry of Corporate Affairs exposed a draft Notification to give exemption to private companies which is placed before the Parliament and is expected to be passed after the Budget session is over. The following exemptions to private companies are being included in the Draft Notification:

Provisions of Section 2 (76) (vii) – any person on whose advice, directions or instructions a director or manager is accustomed to act.

Section 62- Further issue of share capital proviso has been added to smoothen the issue.

CONTD… Section 73 (2) related to acceptance of

deposits- shall apply to private company from its members monies not exceeding 100% of the aggregate paid up share capital and reserves

Cap on number of audits (Section 141 (3) (g)) Provisions of Section 160- relating to Right of

persons other than retiring directors to stand for directorship

Provisions of Section 180- relating to Restrictions on powers of Board.

Provisions of Section 162- relating to Appointment of directors to be voted individually.

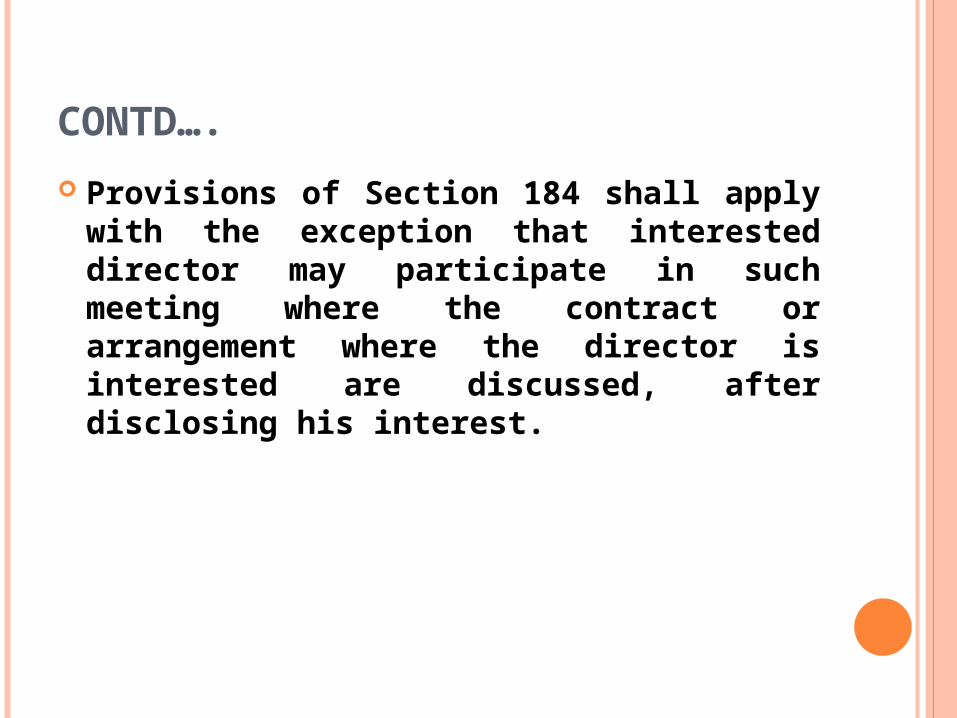

CONTD….

Provisions of Section 184 shall apply with the exception that interested director may participate in such meeting where the contract or arrangement where the director is interested are discussed, after disclosing his interest.

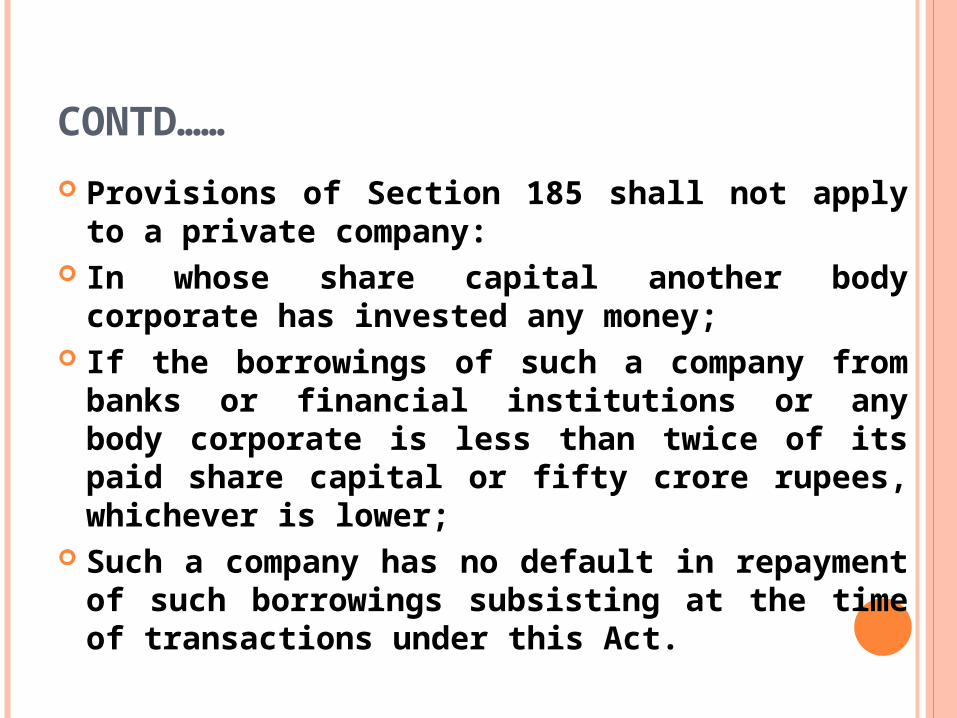

CONTD……

Provisions of Section 185 shall not apply to a private company:

In whose share capital another body corporate has invested any money;

If the borrowings of such a company from banks or financial institutions or any body corporate is less than twice of its paid share capital or fifty crore rupees, whichever is lower;

Such a company has no default in repayment of such borrowings subsisting at the time of transactions under this Act.

CONTD….

Second proviso to Section 188- Related party Transaction-

Provided further that no member of the company shall vote on such resolution, to approve any contract or arrangement which may be entered into by the company, if such a member is a related party.

DEFINITION OF SECTION 2 (76)- RELATED PARTY

Section 470 invoked by (Companies Removal of Difficulties) Fifth Order, 2014 dated 09.07.2014 for Removal of difficulty.

The word “AND” has been inserted in place of ‘OR’

OPTION TO USE DIFFERENT USEFUL LIFE

MCA vide its Notification dated 29.08.2014 has provided for justification for taking different useful life.

(i) The useful life of an asset shall not ordinarily be different from the useful life specified in Part C and the residual value of an asset shall not be more than five per cent. Of the original cost of the asset:

Provided that where a company adopts a useful life different from what is specified in Part C or uses a residual value different from the limit specified above, the financial statements shall disclose such difference and provide justification in this behalf duly supported by technical advice".

REPORTING ON INTERNAL FINANCIAL CONTROL U/S 143 (3) (I)

Ministry of Corporate Affairs has amended Rules vide Amendment dated 14.10.2014 for Chapter 10 (Audit and Auditors) of the Companies Act, 2013 and Reporting on Internal Financial Control u/s 143 (3) (i) of the Companies Act, 2013 has been deferred for one year i.e., upto 31.03.2015. The auditor shall report on the existence of adequate internal financial control and its operational effectiveness for the financial years on or after 01.04.2015.

The auditor may voluntarily report for the year from 01.04.2014 to 31.03.2015.

EXEMPTION FROM PREPARATION OF CONSOLIDATED FINANCIAL STATEMENT Ministry of Corporate Affairs has amended Rules vide

Amendment dated 14.10.2014 for Chapter 9 (Accounts of Companies) of the Companies Act, 2013 and Exemption has been provided from preparation of Consolidated Financial Statement by an Intermediate wholly owned subsidiary, other than a wholly owned subsidiary whose immediate parent is incorporated outside India.

Further, any company that does not have subsidiary but have one or more associates and joint ventures is not required to prepare Consolidated Financial Statements for the current financial year ending on 31.03.2015.

COMPANIES AMENDMENT BILL 2014

Companies Amendment Bill 2014 was passed by the Lok Sabha and is pending before the Rajya Sabha. Following are the sections that have been included in the Companies Amendment Bill, 2014:

Requirement of Minimum capital by a private company and public company would be prescribed in the Rules.

Common Seal is now option. Punishment for contravention of Section 73 or

Section 76 related to acceptance of deposits in contravention of the provisions- Fine of Rs. 1 crore to Rs. 10 crore.

CONTD…. Resolutions and Agreements to be filed

(Section 117)- Prohibits public inspection of Board Resolution filed with the Registrar.

Declaration of Dividend (Section 123)- Includes provision for writing off past losses/ depreciation before declaring dividend for the year.

Financial Statement, Board's report, etc. (Section 134)- Incorporates enabling provisions to prescribe that the fraud that the auditor reports to the Audit Committee or the Board, the same shall be reported in the Board's Report;

CONTD…

Powers and Duties of Auditors and Auditing Standards- Reporting of Fraud by an Auditor (Section 143 (12))- Incorporates enabling provisions to prescribe thresholds beyond which fraud shall be reported to the Central Government (below the threshold, it will be reported to the Audit Committee).

Audit Committee (Section 177)- Provides

provision empowering Audit Committee to give omnibus approvals for related party transactions on annual basis

CONTD…. Loan to Directors, etc. (Section 185)- Exemption

to be provided to the following transactions- any loan made by a holding company to its wholly owned subsidiary company or any guarantee given or security provided by a holding company in respect of any loan made to its wholly owned subsidiary company; or

any guarantee given or security provided by a holding company in respect of loan made by any bank or financial institution to its subsidiary company:

Provided that the loans made under clauses (c) and (d) are utilised by the subsidiary company for its principal business activities.

CONTD….

Related Party Transactions (Section 188)- Replaces 'special resolution' with 'resolution' for approval of related party transactions by non-related shareholders.

Also, Exempts related party transactions between holding companies and wholly owned subsidiaries (WOS) from the requirement of approval of non-related shareholders‘

Investigation into affairs of company by Serious Fraud Investigation Office (Section 212)- Provides for bail restrictions to apply only for offence relating to fraud u/s 447, other offences are bailable

AMENDMENTS IN SECTION 186

Ministry of Corporate Affairs has issued Companies Removal of Difficulty Order, 2015 dated 13th February, 2015 for addressing the following issue:

1. Regarding qualifying criteria to become small company, Now to become a small company both the criteria of paid up share capital and turnover are required to be met.2. Providing exemption to a banking company or an insurance company or a housing finance company for making acquisition of securities in its ordinary course of business as per Section 186 (11) (b)

MCA vide Circular dated 03.03.2015 has issued a Clarification relating to filing of e-form DIR-I1 & DIR-12 under the Companies Act, 2013.

MCA vide Circular dated 10.03.2015 has issued a Clarification with regard to section 185 and 186 of the Companies Act, 2013 - loans and advances to employees

AMOUNTS RECEIVED BY PRIVATE COMPANIES PRIOR TO 01.04.2014 ARE EXEMPT

MCA issued a Circular dated 30.03.2015 and clarified that amounts received by private companies from their members, directors or their relatives prior to 01.04.2014 shall not be treated as deposits under the Companies Act 2013 and Companies (Acceptance of Deposits) Rules, 2014 subject to the condition that relevant private company shall disclose, in the notes to its financial statement for the financial year commencing on or after 1st April, 2014 the figure of such amounts and the accounting head in which such amounts have been shown in the financial statement.

AMENDMENTS

MCA has amended Rules of Chapter V dated 31.03.2015 for returning share application money pending allotment by 1st June, 2015 and Companies may accept deposits without deposit insurance contract till 31.03.2016

Every eligible company shall obtain, at least once in a year, credit rating for deposits accepted by it in the manner specified herein below and a copy of the rating shall be sent to the Registrar of companies.

CLARIFICATION REGARDING LOANS AND ADVANCES TO EMPLOYEES

MCA vide Circular dated 09.04.2015 has issued a Clarification under sub-section (7) of section 186 of the Companies Act, 2013- Loans and/or advances made by the companies to their employees, other than the managing or whole time directors (which is governed by section 185) are not governed by the requirements of section 186 of the Companies Act, 2013. This clarification will be applicable if such loans/advances to employees are in accordance with the conditions of service applicable to employees and are also in accordance with the remuneration policy, in cases where such policy is required to be formulated

CLARIFICATION WITH REGARD TO PAYMENT OF MANAGERIAL PERSON

MCA vide Circular dated 10.04.2015 has issued a Circular related to Remuneration to managerial person under Schedule XIII of the Companies Act, 1956 - Clarification with regard to payment for period.- Managerial person appointed as per Schedule XIII of the companies Act 1956 may continue to receive remuneration as per the provisions of Schedule XIII of the companies Act 1956 for the remaining period of tenure which falls after 01.04.2014

COMPANIES AUDITOR’S REPORT ORDER 2015

MCA vide Removal of difficulty order dated 10th April, 2015 has issued Companies Removal of Difficulty Order, 2015 and prescribed for the following points:

It shall apply to every company including a foreign company as defined in clause (42) of section 2 of the Companies Act, 2013 (18 of 2013) [hereinafter referred to as the Companies Act, except - (i) a banking company as defined in clause (c) of section 5 of the Banking Regulation Act, 1949 (10 of 1949); (ii) an insurance company as defined under the Insurance Act,1938 (4 of 1938):

CONTD….

(iii) a company licensed to operate under section 8 of the Companies Act; (iv) a One Person Company as defined under clause (62) of section 2 of the Companies Act and a small company as defined under clause (85) of section 2 of the Companies Act; and (v) a private limited company with a paid up capital and reserves not more than rupees fifty lakh and which does not have loan outstanding exceeding rupees twenty five lakh from any bank or financial institution and does not have a turnover exceeding rupees five crore at any point of time during the financial year.

CONTD..

Every report made by the auditor under section 143 of the Companies Act, on the accounts of every company examined by him to which this Order applies for the financial year commencing on or after 1st April, 2014, shall contain the matters specified in paragraphs 3 and 4.

MATTERS TO BE INCLUDED IN THE AUDITOR'S REPORT

The auditor's report on the account of a company to which this Order applies shall include a statement on the following matters, namely:- (i) (a) whether the company is maintaining proper records showing full particulars, including quantitative details and situation of fixed assets;

(b) whether these fixed assets have been physically verified by the management at reasonable intervals; whether any material discrepancies were noticed on such verification and if so, whether the same have been properly dealt with in the books of account;

CONTD..

(ii) (a) whether physical verification of inventory has been conducted at reasonable intervals by the management;

(b) are the procedures of physical verification or inventory followed by the management reasonable and adequate in relation to the size of the company and the nature of its business. If not, the inadequacies in such procedures should be reported;

(c) whether the company is maintaining proper records of inventory and whether any material discrepancies were noticed on physical verification and if so, whether the same have been properly dealt with in the books of account;

CONTD… (iii) whether the company has granted any loans,

secured or unsecured to companies, firms or other parties covered in the register maintained under section 189 of the Companies Act. If so, (a) whether receipt of the principal amount and interest are also regular; and (b) if overdue amount is more than rupees one lakh, whether reasonable steps have been taken by the company for recovery of the principal and interest;

(iv) is there an adequate internal control system commensurate with the size of the company and the nature of its business, for the purchase of inventory and fixed assets and for the sale of goods and services. Whether there is a continuing failure to correct major weaknesses in internal control system..

CONTD…. (v) in case the company has accepted deposits,

whether the directives issued by the Reserve Bank of India and the provisions of sections 73 to 76 or any other relevant provisions of the Companies Act and the rules framed there under, where applicable, have been complied with? If not, the nature of contraventions should be stated; If an order has been passed by Company Law Board or National Company Law Tribunal or Reserve Bank of India or any court or any other tribunal, whether the same has been complied with or not?

(vi) where maintenance of cost records Government under sub-section (1) of section been specified by the Central of the Companies Act, whether has 148 such accounts and records have been made and maintained:

CONTD…. (vii) (a) is the company regular in depositing

undisputed statutory dues including provident fund, employees‘ state insurance, income-tax, sales-tax, wealth tax, service tax, duty of customs, duty of excise, value added taxes, cess and any other statutory dues with the appropriate authorities and ii not, the extent of the arrears of outstanding statutory dues as at the last day of the financial year concerned for a period of more than six months from the date they became payable, shall be indicated by the auditor.

(b) in case dues of income tax or sales tax or wealth tax or service tax or duty of customs or duty of excise or value added tax or cess have not been deposited on account of any dispute, then the amounts involved and the forum where dispute is pending shall be mentioned.

CONTD… (A mere representation to the concerned

Department shall not constitute a dispute). (c) whether the amount required to be transferred

to investor education and protection fund in accordance with the relevant provisions of the Companies Act, 1956 (1 of 1956) and rules made thereunder has been transferred to such fund within time.

(viii) whether in case of a company which has been registered for a period not less than five years, its accumulated losses at the end of the financial year are not less than fifty per cent of its net worth and whether it has incurred cash losses in such financial year and in the immediately preceding financial year;

CONTD… (ix) whether the company has defaulted in

repayment of dues to a financial institution or bank or debenture holders? If yes, the period and amount of default to be reported:

(x) whether the company has given any guarantee for loans taken by others from bank or financial institutions, the terms and conditions whereof are prejudicial to the interest of the company;

(xi) whether term loans were applied for the purpose for which the loans were obtained;

(xii) whether any fraud on or by the company has been noticed or reported during the year; If yes, the nature and the amount involved is to be indicated

CONTD….

Reasons to be stated for unfavourable or qualified answers.-

(1) Where, in the auditor's report, the answer to any of the questions referred to in paragraph 3 is unfavourable or qualified, the auditor's report shall also state the reasons for such unfavourable or qualified answer, as the case may be.

(2) Where the auditor is unable to express any opinion in answer to a particular question, his report shall indicate such fact together with the reasons why it is not possible for him to give an answer to such question.

THANK YOU