Embed Size (px)

Citation preview

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Investor Presentation

June 2013

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Overview of Gitanjali Group

Owns 8 out of the top 10 diamond jewellery brands in India

Owns key Italian brands and leading retail chain in the US

Brands built over the years through extensive marketing campaigns independently valued at over

US$1bn

Established in 1966, Gitanjali Gems is one of the largest integrated branded jewellery players in

India; Experience of around five decades in the Indian gems and jewellery business

Pioneer in the branded jewellery segment and amongst the first few companies to launch own outlets

to sell branded jewellery in India

Present across the entire value chain from sourcing to manufacturing to retailing

State of the art manufacturing with 3 cutting and polishing facilities and 9 jewellery manufacturing

facilities (235,000 pieces per month) across India and China

Combination of diamonds and gold branded jewellery across various price points

Business model rapidly shifting from C&P1 diamonds to branded jewellery thereby improving

margins and cash flows

Till recently gold price fluctuation was hedged through a gold loan arrangement thereby derisking

any price fluctuation; Recent change in RBI policy on gold loan to have marginal impact for a short

term

Mehul Choksi, Chairman & Managing Director, is an industry veteran and has received several

awards and recognition for his entrepreneurship and innovation

Supported by highly professional experienced management team

Design bank of 0.3mn SKUs, 10,000 active SKUs and 4,000 new active SKUs added every year

Over 360 distributors selling to over 3,000 retailers and 1,100 retail outlets across the formats of own

stores, franchisee and shop in shops across India, US, Japan, China and Middle East

Leading Jewellery Player

Well established Brands

Extensive Design Collection with

Wide Distribution Network

Integrated Player

Highly Attractive Revenue Mix

With Low Commodity Price

Risk

Strong Management

(1): Cut and Polish

1

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Formed JV with ‘D'Damas’

Started jewellery operations

at the manufacturing units

in SEEPZ, Mumbai

IPO of Gitanjali Gems Limited

Acquired Samuel Jewelers Inc, USA for retail

presence in the US

Formed JV Sanghavi Exports for manufacturing

and marketing ‘Sangini’ brand

Acquired the brand ‘Nakshatra’

Acquired the brand ‘Asmi’ from DTC

Gitanjali Gems - Milestones

Source: Company Presentation

Launched India's first branded

jewellery, ‘Gili’, through Gili

India

Incorporated as a limited company

'Gitanjali Gems Private Limited'

Started operations at the manufacturing unit

in Borivali, Mumbai

Acquired assets of DIT Group S.p.A (DIT)

Italy

Acquired minority stake in Verite, a jewellery

retailer in Japan

Acquired brands ‘Nirvana’ and ‘Viola’

Launched Gitanjaligifts.com, for e -commerce

foray

Formed JV to promote brand 'Nakshtra'

1994

1996

2004

2006

2007

2008

2011

2012

1991

1986

2003

Formed Gitanjali Exports for

polished manufacturing and trading 1966

2

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

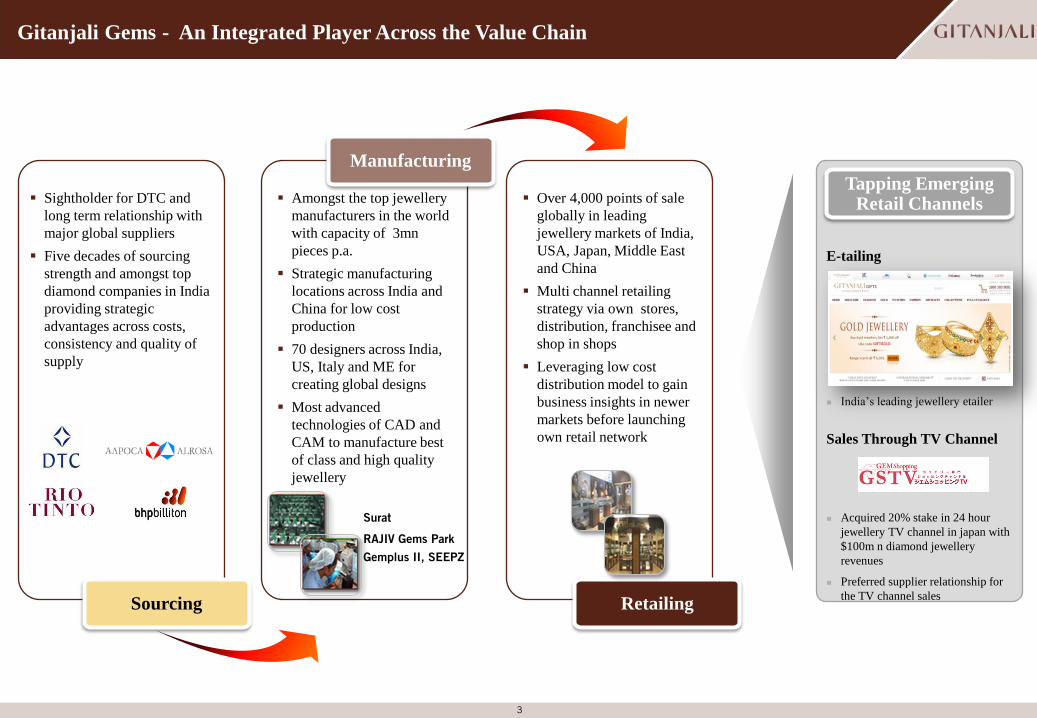

Gitanjali Gems - An Integrated Player Across the Value Chain

Sightholder for DTC and

long term relationship with

major global suppliers

Five decades of sourcing

strength and amongst top

diamond companies in India

providing strategic

advantages across costs,

consistency and quality of

supply

Sourcing

Amongst the top jewellery

manufacturers in the world

with capacity of 3mn

pieces p.a.

Strategic manufacturing

locations across India and

China for low cost

production

70 designers across India,

US, Italy and ME for

creating global designs

Most advanced

technologies of CAD and

CAM to manufacture best

of class and high quality

jewellery

Manufacturing

Over 4,000 points of sale

globally in leading

jewellery markets of India,

USA, Japan, Middle East

and China

Multi channel retailing

strategy via own stores,

distribution, franchisee and

shop in shops

Leveraging low cost

distribution model to gain

business insights in newer

markets before launching

own retail network

Retailing

Surat

RAJIV Gems Park

Gemplus II, SEEPZ

E-tailing

India’s leading jewellery etailer

Sales Through TV Channel

Acquired 20% stake in 24 hour

jewellery TV channel in japan with

$100m n diamond jewellery

revenues

Preferred supplier relationship for

the TV channel sales

Tapping Emerging Retail Channels

3

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Gitanjali Gems - Strategically Present In The Top 5 Global Diamond Jewellery Markets

Middle East

Positioned as leading branded

jeweller from India

Distribution of Indian branded

jewellery to over 50 stores of

Damas, Al-Haseena, Alukkas

India

Pioneers of branded jewellery and

organized jewellery retailing in

India

Pan India presence with over 4,000

points of sale

Japan

Strategic stake in a leading

jewellery retailer with 110 stores in

Japan

20% stake in the largest jewellery

selling TV channel

China

40 SIS in leading departmental

stores under the brand ‘Giantti’

Set up 2 Italian brand stores with

potential to expand European brand

in Chinese market

Europe

5 key Italian brands – Stefan

Hafner, IoSi, Nouvelle Bague,

Porrati and Valente

Access to over 2,000 jewellery

retailers in UK through strategic

acquisition of Alfred Terry

USA

104 retail store chain of Samuels

in the South West

Samules positioned as a top

specialty retailer with focus on

engagement rings and wedding

bands

Leveraging the strong indian

diaspora and appealing to the

locals for its high quality design

4

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

C&P Diamonds

Proportion in revenues has decreased from 80%

at the time of IPO in FY06 to 38% in FY13

Revenues have grown at CAGR of 29% from

FY10 to FY13

Branded Jewellery

Proportion in revenues has been increasing

every year to reach 62% in FY13

Revenues have grown at CAGR of 41% from

FY10 to FY13

Strategic

Shift In

Focus

Revenues

~ INR 16,418 Cr

31%

C&P Diamonds

~ INR 6,211 Cr

14%

Branded Jewellery

~ INR 10,207 Cr

45%

Y-O-Y Growth

Distributors

~ INR 3,958 Cr

Own Stores

~ INR 726 Cr

Franchisee

~ INR 1,630 Cr

SIS

~ INR 895 Cr

Exports

~ INR 3,521 Cr

(10%)

Domestic

~ INR 2,690 Cr

74%

India

~ INR 7,209 Cr

60%

USA Samuels

~ INR 685 Cr

5%

USA Others

~ INR 453 Cr

2%

Middle East

~ INR 900 Cr

39%

Rest of World

~ INR 960 Cr

21%

64%

42%

65%

51%

Gitanjali Gems – Revenue Mix Across Products / Geographies / Distribution Channels

5

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

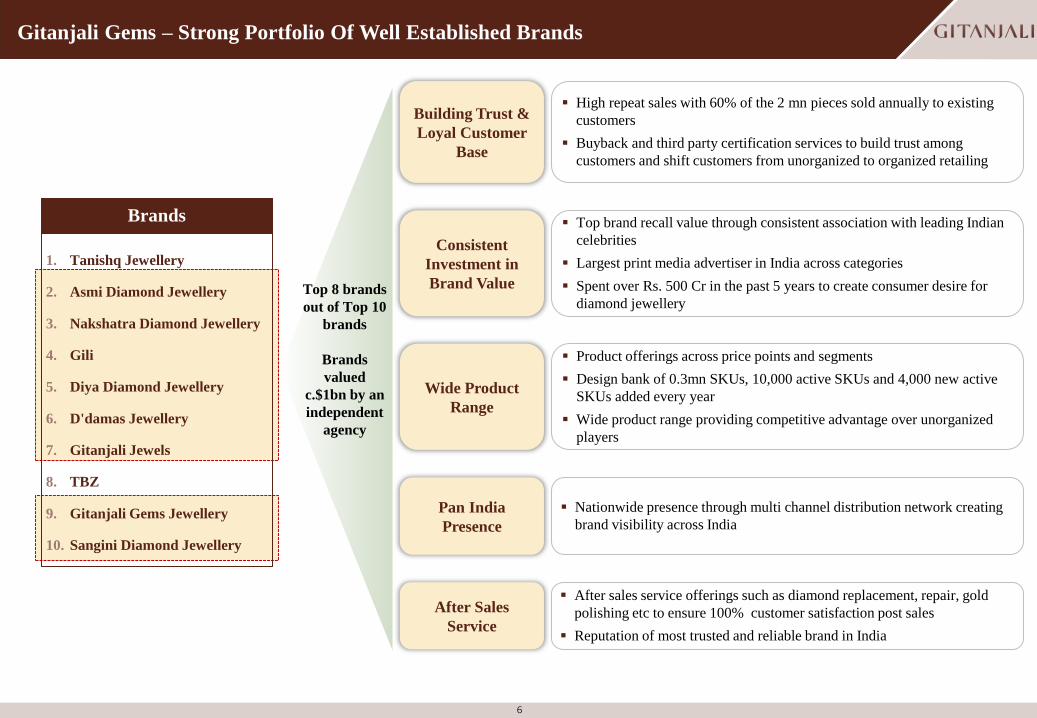

Gitanjali Gems – Strong Portfolio Of Well Established Brands

Brand Positioning of Selected Indian Brands

Selected International Brands

Positioned as easy to wear, highly contemporary and

trendy designer brand at competitive price

High end product offering with presence across product

range including bridal jewellery and evening wear

Premium work wear collection to target customers

including those seeking everyday jewellery

Positioned as easy to wear, highly contemporary and

trendy designer brand at competitive price

Offers traditional classic designs to cater to major gold

jewellery buying occasions

5th largest fine jewellery retail chain in USA

Focus on the mid to upper mid segment .

High end luxury brand

Positioned as brand that combines traditional

skills with a fresh and elegant approach

Produces limited edition jewels with very

strong contemporary designs

[xx]

TBD

TBD

Revenue

Trust FY 10 FY 13

Revenue

Consistent

Investment in

Brand Value

Wide Product

Range

Pan India

Presence

After Sales

Service

Brands

1. Tanishq Jewellery

2. Asmi Diamond Jewellery

3. Nakshatra Diamond Jewellery

4. Gili

5. Diya Diamond Jewellery

6. D'damas Jewellery

7. Gitanjali Jewels

8. TBZ

9. Gitanjali Gems Jewellery

10. Sangini Diamond Jewellery

Top brand recall value through consistent association with leading Indian

celebrities

Largest print media advertiser in India across categories

Spent over Rs. 500 Cr in the past 5 years to create consumer desire for

diamond jewellery

Product offerings across price points and segments

Design bank of 0.3mn SKUs, 10,000 active SKUs and 4,000 new active

SKUs added every year

Wide product range providing competitive advantage over unorganized

players

Nationwide presence through multi channel distribution network creating

brand visibility across India

After sales service offerings such as diamond replacement, repair, gold

polishing etc to ensure 100% customer satisfaction post sales

Reputation of most trusted and reliable brand in India

Top 8 brands

out of Top 10

brands

Brands

valued

c.$1bn by an

independent

agency

Building Trust &

Loyal Customer

Base

High repeat sales with 60% of the 2 mn pieces sold annually to existing

customers

Buyback and third party certification services to build trust among

customers and shift customers from unorganized to organized retailing

6

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Gitanjali Gems – Brands Present Across Price Points to Capture Market Share

Luxury (Primarily Diamond Jewellery)

Mid (Diamond

& Gold

Jewellery)

Low-end (Gold

Jewellery)

High on Fashion

High on Tradition

Transformed key product brand into independent brand retail chains

Specific design signature for each product brand catering to different

consumer preference

Separate brand manager/sales team for each brand category

Product category positioned to compete with traditional jewellers

Mix of diamond, gold, colored stones and pearls to cater to wide

variety of choice to customers

Offers entry points to tier 2 and tier 3 regions with specific focus on

gold jewellery to cater to local demand

Has significant design, quality and price advantage compared to local

jeweller

Has cost plus selling models catering to the traditional method of

selling that helps in acquiring customer from unorganized sector

Key Characteristics of Brands

7

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Gitanjali Gems – Strong PAN India Distribution Network

Growing Own Stores

66 78

90

105 117

165 185

210 233

259

0

50

100

150

200

250

300

50

60

70

80

90

100

110

120

FY09 FY10 FY11 FY12 FY13

Total Area No. of Stores

Started the operations

in [xx]

In short span of [xx] yrs

has grown revenues

from [xx] to [xx]

Leadership position

given very strong brand

recall

Franchisee and Shops-in-Shops

99 138

168 217

274

30 35 42 52 64

160 215

255 319

391 425

470 520

577 643

0

100

200

300

400

500

600

700

0

50

100

150

200

250

300

FY09 FY10 FY11 FY12 FY13

Franchisee Area SIS Area No. of Franchisee No. of SIS

Nationwide presence through multi channel distribution network of

distributors, own stores, franchisee and shop in shops

More than 4,000 sale points with c. 260 own stores makes Gitanjali as the

leading branded jewellery retailer in India

Focus on growth through franchise model well supported by flagship stores to

support premium brand positioning

Plans to penetrate Tier 2 and Tier 3 markets in India primarily through

franchisee route

(Sqft 000s) (Sqft 000s) (No. of Stores) (No. of Stores)

Distribution of Stores Across India

Presence in India

Top 10 States % Stores

Maharashtra 26.1%

Karnataka 11.5%

Delhi 9.6%

West Bengal 6.8%

Uttar Pradesh 6.8%

Andhra Pradesh 6.6%

Gujarat 4.9%

Haryana 4.1%

Madhya Pradesh 3.5%

Punjab 3.5%

Total 83.5%

8

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Gitanjali Gems – History of Highly Successful Acquisitions Across the Globe

Acquired in 2006 for $45mn with an aim to convert the

entire purchases in-house

Turned around the retail chain in 2011, achieved

synergies due to inhouse sourcing and cost optimisation

Nakshtara and Asmi acquired in 2007 and 2008

Operations were smoothly integrated given that brands were operated by Gitanjali in B2B

formats through distribution

Post acquisition revenue of both brands has grown from $20mn in FY06 to $200mn in

FY13by marketing the brands across own stores, franchisees & SIS

Acquired jewellery brands Nirvana and Viola in 2012 to expand its retail network and

increase its market share in the organized retail space

Acquired assets of DIT group in a liquidation process in Italy in 2011

─ Paid c.$10mn on asset based valuation wherein acquired inventory of gold & diamond of

c.$13mn

─ Ownership of popular brands like Stefan Hafner, IOSI, Porrati and Valente

Rationale is to create a bouquet of international brands in RoW and use the distribution

strength to sell Indian brands

Similarly, Indian market moving towards higher luxury brands where these brands are well

positioned

Acquired a minority stake in Verite in 2012 to become a

preferred supplier and gain access to a network of 110

jewellery retail stores

Acquired minority 20% stake in the largest jewellery

selling TV channel to become a preferred supplier in one

of the largest jewellery markets in the world

Acquired Alfred Terry in December 2011 which was

producing innovative diamond jewellery for over 100

years

Has distribution tie ups with over c.2,000 jewellery stores

across Europe

US Japan UK

Italy India

9

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

One of the largest and the fastest growing jewellery markets with similar jewellery tastes, price points and other

cultural aspects as India

Indian brand ambassadors of Gitanjali are extremely popular in the region leading to immediate connect with locals

and large Indian diaspora

Large presence in the region through renowned retail chains like Damas, Alukkas and Al-Haseena offering deep

insight and knowledge for expanding own retail chains

Middle East

Japan is one of the largest diamond jewellery market and provides excellent margins to integrated players. Large

existing proven distribution network in Japan combined with low cost manufacturing capabilities will enable the

next phase of expansion

Existing bouquet of Italian and other international brands helping Gitanjali to aggressively expand in China

Presence in Europe through own design center and distribution presence through well known Italian brands helping

in better understanding of global designs and consumer trends

Rest of World

US being the largest diamond jewellery market with superior margins, is one of the most ambitious markets for

Gitanjali

Existing presence under the brand name Samuels and Rogers (leading retail jewellery chains) with focus on

engagement and wedding bands (price band of US$600)

Integrated business model with strong sourcing, low cost manufacturing capabilities and well established retail

presence has been contributing to increasing market share and profitability

USA

Gitanjali Gems – Significant Presence In World’s Leading Jewellery Markets

10

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Gitanjali Gems – Business Mix Changing towards High Margin Segments

Revenue has increased from

INR 6,527 Cr to INR 16,418 Cr at a

CAGR of 36% from FY10 – FY 13

EBITDA has increased from

INR 440 Cr to INR 1,048 Cr at a

CAGR of 34% whereas Net Income1

has increased from INR 202 Cr to

INR 595 Cr at a CAGR of 43% from

FY10 – FY13

Operating margins have been

increasing over the years though the

marginal drop in EBITDA margins

is due to changing mix of revenues

from sale of diamond jewellery to

gold jewellery

Branded jewellery segment revenues

as a % of total revenues have

increased from 56% in FY10 to 62%

in FY13

Within the branded jewellery

segment, India is the highest

contributor with c. 71% revenue

share

Of the domestic revenues in India,

revenue mix of high margin

franchisee model has increased from

12% to 23% in the last 3 years

Revenue, EBITDA & Net Income Margins Shifting from Non Branded to Branded Jewellery

Geographical Mix of the Branded Jewellery

C&P

Diamond

38%

Intl

Branded

18%

Domestic

Branded

44%

6,527

9,377

12,498

16,418

6.7%

5.8%

6.5%

6.4%

3.1%

3.8% 3.9% 3.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2010 2011 2012 2013Revenue EBITDA % Net Income %

INR cr

C&P

Diamond

44%

Intl

Branded

27%

Domestic

Branded

29%

FY 2010 FY 2013

FY 2010 FY 2013

FY 2013 Operating Margin

Distributors 8.5%

Franchisees 11.3%

Own Stores 10.4%

Shop-in-Shops 9.5%

FY 2013 Operating Margin

Cut & Polish Diamond 2.3%

Intl Branded 7.7%

Domestic Branded 9.3%

68% 55%

10%

10%

12% 23%

10% 12%

0%

20%

40%

60%

80%

100%

FY2010 FY2013

Shop-in-Shops

Franchisees

Own Stores

Distributors

Franchisee

share almost

doubled

Revenue CAGR : 36%

India

71%

US Samuels

7%

US Others

4%

Middle East

9%

Rest of World

9%

(1): Net Income before minority interest

11

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Region

% Total

Jewellery

Contribution

RoCE EBITDA % Margin Revenue

10% 9%

India 51% 71%

12% 4%

17% 7%

10% 9%

FY 2010 FY 2013

US Samuels

US Others

Middle East

Rest Of World

Gitanjali Gems - Geographical Analysis of Branded Jewellery

1,857

7,209

0

4,000

8,000

640 685

550

600

650

700

420

453

400

420

440

460

371

900

0

500

1,000

378

960

0

500

1,000

1,500

Revenue (INR Cr)

Revenue (INR Cr)

Revenue (INR Cr)

Revenue (INR Cr)

Revenue (INR Cr)

10.5% 9.3%

5%

10%

15%

6.6%

5.8%

5%

6%

7%

5.0%

6.6%

0%

4%

8%

5.8%

8.9%

0%

5%

10%

7.0%

8.3%

6%

8%

10%

39.0% 32.0%

0%

25%

50%

9.1% 7.4%

0%

5%

10%

8.4% 8.0%

7%

8%

9%

17.1%

28.3%

0%

10%

20%

30%

FY 2010 FY 2013 FY 2010 FY 2013 FY 2010 FY 2013

(1) ME and ROW RoCE is for Diamond Jewellery

12

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

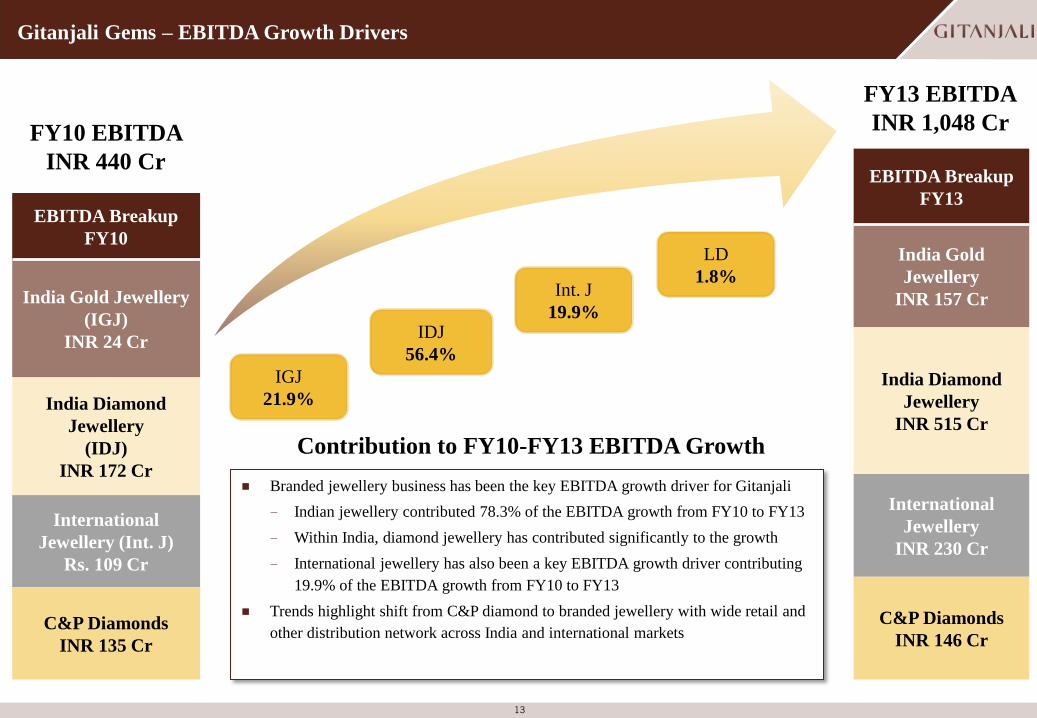

EBITDA Breakup

FY10

India Gold Jewellery

(IGJ)

INR 24 Cr

India Diamond

Jewellery

(IDJ)

INR 172 Cr

International

Jewellery (Int. J)

Rs. 109 Cr

C&P Diamonds

INR 135 Cr

EBITDA Breakup

FY13

India Gold

Jewellery

INR 157 Cr

India Diamond

Jewellery

INR 515 Cr

International

Jewellery

INR 230 Cr

C&P Diamonds

INR 146 Cr

FY10 EBITDA

INR 440 Cr

FY13 EBITDA

INR 1,048 Cr

Int. J

19.9%

IGJ

21.9%

IDJ

56.4%

LD

1.8%

Gitanjali Gems – EBITDA Growth Drivers

Contribution to FY10-FY13 EBITDA Growth

Branded jewellery business has been the key EBITDA growth driver for Gitanjali

− Indian jewellery contributed 78.3% of the EBITDA growth from FY10 to FY13

− Within India, diamond jewellery has contributed significantly to the growth

− International jewellery has also been a key EBITDA growth driver contributing

19.9% of the EBITDA growth from FY10 to FY13

Trends highlight shift from C&P diamond to branded jewellery with wide retail and

other distribution network across India and international markets

13

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

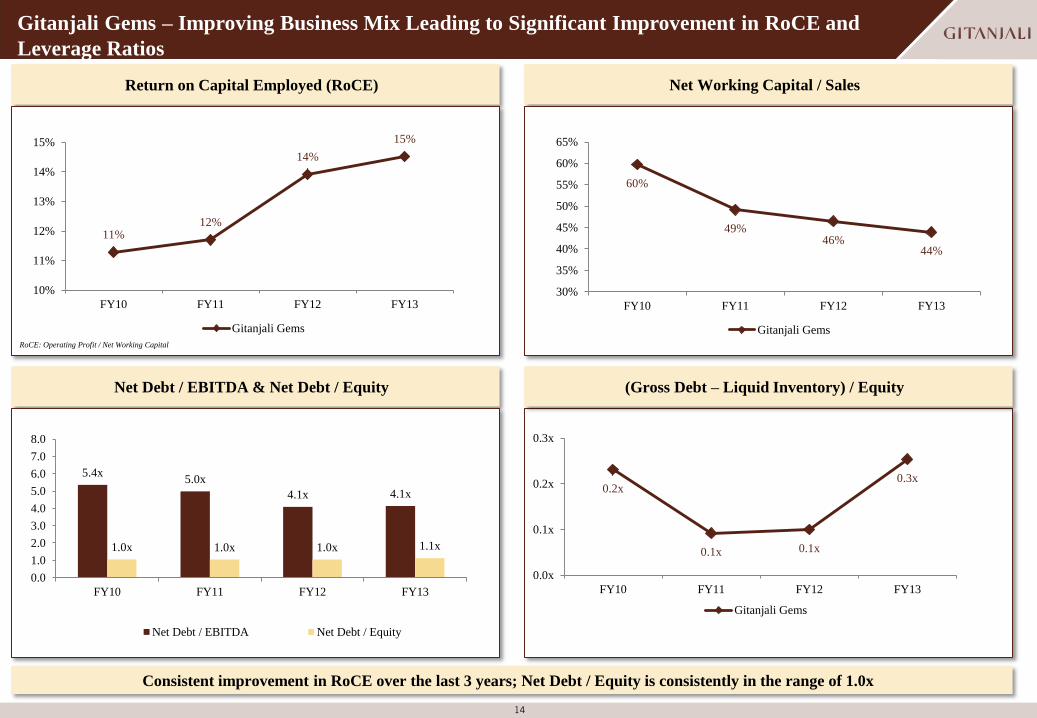

Gitanjali Gems – Improving Business Mix Leading to Significant Improvement in RoCE and

Leverage Ratios

Return on Capital Employed (RoCE) Net Working Capital / Sales

Net Debt / EBITDA & Net Debt / Equity

11% 12%

14%

15%

10%

11%

12%

13%

14%

15%

FY10 FY11 FY12 FY13

Gitanjali Gems

60%

49% 46%

44%

30%

35%

40%

45%

50%

55%

60%

65%

FY10 FY11 FY12 FY13

Gitanjali Gems

5.4x 5.0x

4.1x 4.1x

1.0x 1.0x 1.0x 1.1x

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

FY10 FY11 FY12 FY13

Net Debt / EBITDA Net Debt / Equity

(Gross Debt – Liquid Inventory) / Equity

0.2x

0.1x 0.1x

0.3x

0.0x

0.1x

0.2x

0.3x

FY10 FY11 FY12 FY13

Gitanjali Gems

Consistent improvement in RoCE over the last 3 years; Net Debt / Equity is consistently in the range of 1.0x

RoCE: Operating Profit / Net Working Capital

14

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Gitanjali Gems – Significant Opportunity to Unlock Value

Some of the core investments accounted at book value have appreciated significantly over the years

Currently in the process of unlocking value of historical investments that would generate incremental cash-flows in

the medium term

Land and Building

Inventory Value

Inventory of c.$800mn as of March 31, 2013 mainly consisting of diamond and gold valued at cost

Market value of the inventory significantly higher than the current book value

Unlike other traditional industries, inventory is highly liquid and monetization is possible in a short timeframe

Plus with labor forming less than 5% of the total cost of a finished jewellery, any non-moving inventory can be

recycled without any loss

Brands

Nine brands including Gitanjali, Gili, Nakshatra, Asmi, D’ Damas, Gitanjali Jewels, Maya Gold, Gitanjali Lifestyle

and Shuddhi valued at c.$1bn by a leading UK based agency

Samuels is amongst the leading specialty jewellery retail chain in the US

Brand building expenses incurred annually are not capitalized

None of the brands have been pledged with any lender

15

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Gitanjali Gems – Highly Diversified Board With Proven Corporate Governance Track Record

Board Directors Brief Profile

Mehul Choksi

Chairman

Chairman & Managing Director of the Group

Received many awards and recognition for his entrepreneurship and innovation.

Nominated for “E&Y Entrepreneur of the Year” award (2008)

Sunil Varma

Whole-time Director

Joined the group in 2009

Previously worked with Gemsiam Manufacturing in the finance and operations department

Holds CA, CPA, CFA and MBA

Dhanesh Sheth

Non-Executive Director

Advises company on marketing operations, buying and selling of rough diamonds and other aspects of business development

Joined the board in 1990

Nehal Modi

Non-Executive Director

Has been instrumental in the company’s growth in the USA since 2001

Has been on the board since 2009

Holds a bachelor’s degree in arts (finance and marketing) from Boston University

Sujal Shah

Independent Director

Presently the owner of a SSPA & Co., a chartered accountancy firm

Areas of practice are M&A, restructuring, valuation and due diligence of companies

Has been on the board since 2005

S. Krishnan

Independent Director

Has vast experience in banking, fund management and capital market operations

Held top-level management positions at TAIB Securities, Everest Fund, Aldercrest Trading Limited and First Bank

Has been on the board since 2005

Nitin Potdar

Independent Director

Currently partner at J. Sagar Associates, a leading law firm in India

Specialises in mergers and acquisitions, restructuring of business, asset and share purchase deals, joint ventures and strategic

alliances, domestic and international capital markets, private equity and general corporate advisory

M.S. Sundararajan

Independent Director

Leading banking consultant and economist, part of the visiting faculty at various institutes and was previously the chairman and

managing director of Indian Bank

High Standards of Corporate Governance

1. No major related party transactions

2. No other business interest outside the listed entity by the promoter family

3. Run by a highly professional management team

4. No major litigation or customer or investor complaints pending

16

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Gitanjali Gems – Strong Management Team With Significant Industry Expertise

Name and Role/

Designation Brief Profile

Nishit Mehta

Group President

Joined the Group in 2005

Possesses experience in managing international business in corporate houses

Has been instrumental in establishing the international business of the group

Abhishek Gupta

President

Joined the group in 2008

Heads strategy and business development for the group

Previously worked with JPMorgan Chase and CapGemini

MBA in finance

Kapil Khandelwal

Group CFO

Joined the Group in 2010

Core expertise of financial control, banking, fund raising, M&A and costing

Chartered Accountant and ICWA by qualification

Vijay Agarwal

Vice President and

Head – Secretarial

and Legal

23 years of expertise in legal and secretarial functions such as mergers, restructurings, public issues, private

placement of various securities, joint ventures and intellectual property

Holds a bachelor’s degree in law and is a qualified company secretary

Santosh Srivastava

Head - GJRPL

Joined the Group in 2008 managing the Indian franchisee expansion

Has previous experience of working with the Tata group

Pankhuri Warange

Company Secretary

Responsible for secretarial compliances of the Company

Has over nine years of experience as a company secretary

Holds a bachelor’s degree in law and arts

17

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Strategic Shift from

C&P Diamonds to

Jewellery

Continuous shift from “C&P Diamonds” to “ Branded Jewellery” to cater to the shifting

consumer preference of buying branded jewellery

Advantages of an integrated play, working capital efficiency and consequently higher return

on capital employed

1

Gitanjali Gems - Actionable Future Business Strategy

Comprehensive Mix of

Channels & Categories

Provide wide selection of jewellery across various categories including diamond, gold and

other precious stones

Build a wide distribution across various channels including own stores, 3rd party distribution,

franchisee and shop-in-shops

2

Capturing New

Markets with an

Efficient Distribution

Model

Extending presence in Tier 2 and Tier 3 urban and semi-urban regions to capture the growing

demand and structural shift from unorganized to organized retailing

Entering new markets through asset light franchisee route; thereby de-risking capital and

improving margins

3

International

Expansion

Tapping international markets by leveraging low cost production and high quality

international design capabilities to cater to global consumers

Focus on capturing the growing demand in the top 5 largest jewellery markets globally by

size as well as growth

4

Retail Expansion

Capitalize the in-depth market understanding developed through strong global distribution

network over the years that has helped in creating an efficient retail network

Leverage the above expertise in expanding various retail formats across India and overseas

5

18

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Gitanjali Gems – Implications of the Recent changes in RBI Policy on Gold Loan

Recent RBI policy has prohibited any form of credit on gold imports meant for domestic consumption

− Earlier companies were able to get gold from banks with a 20% margin upfront and also had a window of 6 months to

finalize the price

− Now, companies would have to make 100% payment upfront for the imported gold used for domestic consumption

− The implication of the policy is restricted only to domestic gold jewellery sale and has no impact on domestic diamond

jewellery sale or exports (diamond as well as gold)

Unlike other Indian jewellery companies, Gitanjali is primarily focused on the diamond segment where there are no

changes in the regulatory policy

Inventory required for meeting the domestic gold jewellery revenues is therefore not significant and Gitanjali would be

able to fund the remaining capital required through internal accruals, debt or equity as required

With the revised gold loan policy which requires 100% margin against gold loans, Gitanjali also plans to lessen its

dependence on domestic gold jewellery until the regulatory uncertainty is eliminated thereby reducing its dependence on

gold loan

Separately, in order to hedge the price risk which was earlier available through gold loan, Gitanjali is considering buying

physical gold and simultaneously selling forward contracts thereby completely negating any risk due to price fluctuation

The implication of the drop in gold jewellery revenues will have a very marginal impact on operating profits given

relatively lower margins in gold jewellery as compared to diamond jewllery (key focus area for Gitanjali)

19

Annexure : Historical Performance

20

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Historical Performance – INCOME STATEMENT (CONSOLIDATED)

Particulars FY13 (Audited) FY 12 (Audited) FY 11 (Audited) FY 10 (Audited)

(INR Cr.)

Total Total Total Total

Revenues 16,418.0 12,498.1 9,377.2 6,527.0

Raw material cost 14,116.0 10,671.8 7,992.9 5,525.0

Gross Profit 2,302.1 1,826.4 1,384.4 1,002.0

Operating expenses 1,254.4 1,018.8 844.9 562.4

EBITDA 1,047.7 807.6 539.5 439.6

EBITDA margin (%)

6.4% 6.5% 5.8% 6.7%

Depreciation 36.6 29.5 56.4 44.5

EBIT 1,011.1 778.1 483.1 395.1

EBIT margin (%) 6.2% 6.2% 5.2% 6.1%

Finance Costs 461.3 407.7 221.8 172.4

Other Income 70.8 148.1 103.7 2.6

Exceptional items 0.1 5.1 18.0 0.0

PBT 620.7 523.6 383.0 225.2

PBT Margins (%)

3.8% 4.2% 4.1% 3.5%

Tax 25.5 32.3 26.7 23.2

PAT1 595.2 491.3 356.3 202.0

PAT Margins (%)

3.6% 3.9% 3.8% 3.1%

(1): PAT before minority interest

21

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Historical Performance – BALANCE SHEET (Consolidated)

Particulars FY 13 (Audited) FY 12 (Audited) FY 11 (Audited) FY 10 (Audited)

(INR Cr.) Total Total Total Total

Net operating working capital

Inventories 4,347.3 3,693.6 2,901.3 2,079.1

Inventory days (of COGS) 111 125 131 135

Receivables 7,189.2 5,384.9 4,019.5 3,231.0

Days Receivable (of Sales) 158 155 154 178

Trade Payables and Creditors (4,338.2) (3,292.0) (2,200.1) (1,294.5)

Days Payable (of COGS) (111) (111) (99) (84)

Debt Facility

Long Term Borrowings 687.9 661.2 226.0 506.8

Short Term Borrowings 4,617.4 3,300.0 2,901.3 2,088.0

Gross debt (A) 5,305.3 3,961.1 3,127.4 2,594.8

Cash and cash equivalents (B) 978.4 660.9 443.7 241.7

Net debt (A-B) 4,326.9 3,300.2 2,683.6 2,353.1

Shareholders Equity + Minority Interest 3,832.5 3,168.3 2,579.9 2,244.8

Net debt / Equity ratio 1.13 1.04 1.04 1.05

22

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Disclaimer

This presentation and the accompanying slides (the “Presentation”), which have been prepared by Gitanjali Gems Limited (the “Company”), have been prepared

solely for information purposes and do not constitute any offer, recommendation or invitation to purchase or subscribe for any securities, and shall not form the basis

or be relied on in connection with any contract or binding commitment whatsoever. No offering of securities of the Company will be made except by means of a statutory

offering document containing detailed information about the Company.

This Presentation has been prepared by the Company based on information and data which the Company considers reliable, but the Company makes no representation

or warranty, express or implied, whatsoever, and no reliance shall be placed on, the truth, accuracy, completeness, fairness and reasonableness of the contents of this

Presentation. This Presentation may not be all inclusive and may not contain all of the information that you may consider material. Any liability in respect of the contents

of, or any omission from, this Presentation is expressly excluded.

Certain matters discussed in this Presentation may contain statements regarding the Company’s market opportunity and business prospects that are individually and

collectively forward-looking statements. Such forward-looking statements are not guarantees of future performance and are subject to known and unknown risks,

uncertainties and assumptions that are difficult to predict. These risks and uncertainties include, but are not limited to, the performance of the Indian economy and of the

economies of various international markets, the performance of the gems and jewellery industry in India and world-wide, competition, the company’s ability to

successfully implement its strategy, the Company’s future levels of growth and expansion, technological implementation, changes and advancements, changes in revenue,

income or cash flows, the Company’s market preferences and its exposure to market risks, as well as other risks. The Company’s actual results, levels of activity,

performance or achievements could differ materially and adversely from results expressed in or implied by this Presentation. The Company assumes no obligation to

update any forward-looking information contained in this Presentation. Any forward-looking statements and projections made by third parties included in this

Presentation are not adopted by the Company and the Company is not responsible for such third party statements and projections.

The distribution of this document in certain jurisdictions may be restricted by law and persons into whose possession this presentation comes should inform themselves

about and observe any such restrictions.

23

R 221

G 209

B 205

R 87

G 35

B 22

R 248

G 219

B 145

R 158

G 122

B 111

R 165

G 165

B 165

R 216

G 216

B 216

R 252

G 238

B 204

R 242

G 189

B 53

Thank you

Corporate Office:

3,B Wing, 3rd Floor, Laxmi Towers.

Bandra Kurla Complex.

Mumbai 400 051.

India

Investor contact:

24

![111 ACCY 272 Session 08 Chapter 5 (D,E,F) REDEMPTIONS AND PARTIAL LIQUIDATIONS (2) Text (Lind [6e]), pp. 248-283 Problems, pp. 252-253, 255, 260, 266,](https://img.pdfslide.us/doc/110x75/56649c885503460f949411b1/111-accy-272-session-08-chapter-5-def-redemptions-and-partial-liquidations.jpg)