Embed Size (px)

Citation preview

QUICK GUIDE TOCLASSIFICATION OF LEASE TRANSACTIONS

NATIONAL TREASURY

Presenter: SCOA Technical Committee| National Treasury|

Content

2

• Definition of a lease

• Types of lease agreements

• Operating Leases Infrastructure

• Operating Leases Non-Infrastructure

• Classification of payments made in terms of a operating lease and

finance lease

• Frequently asked questions (FAQ)

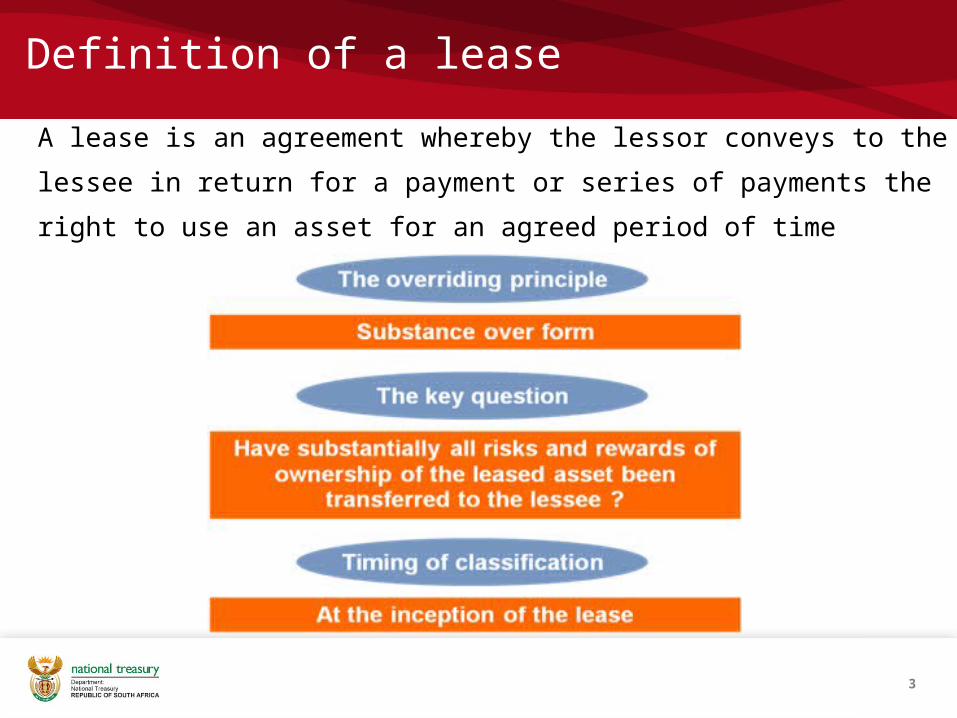

Definition of a lease

3

A lease is an agreement whereby the lessor conveys to the lessee in return

for a payment or series of payments the right to use an asset for an agreed

period of time

4

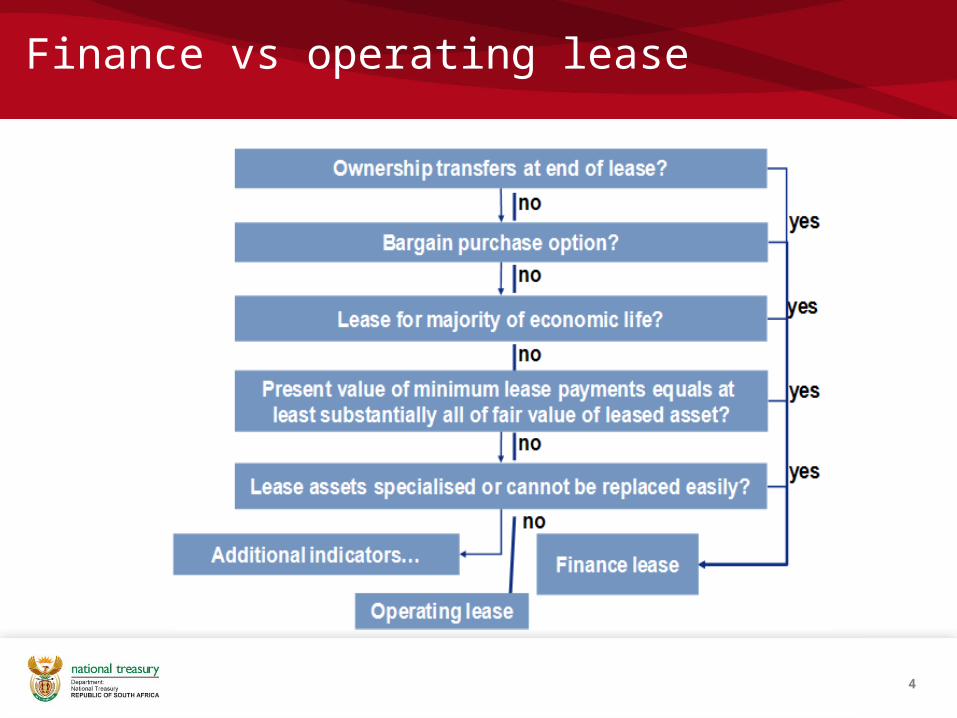

Finance vs operating lease

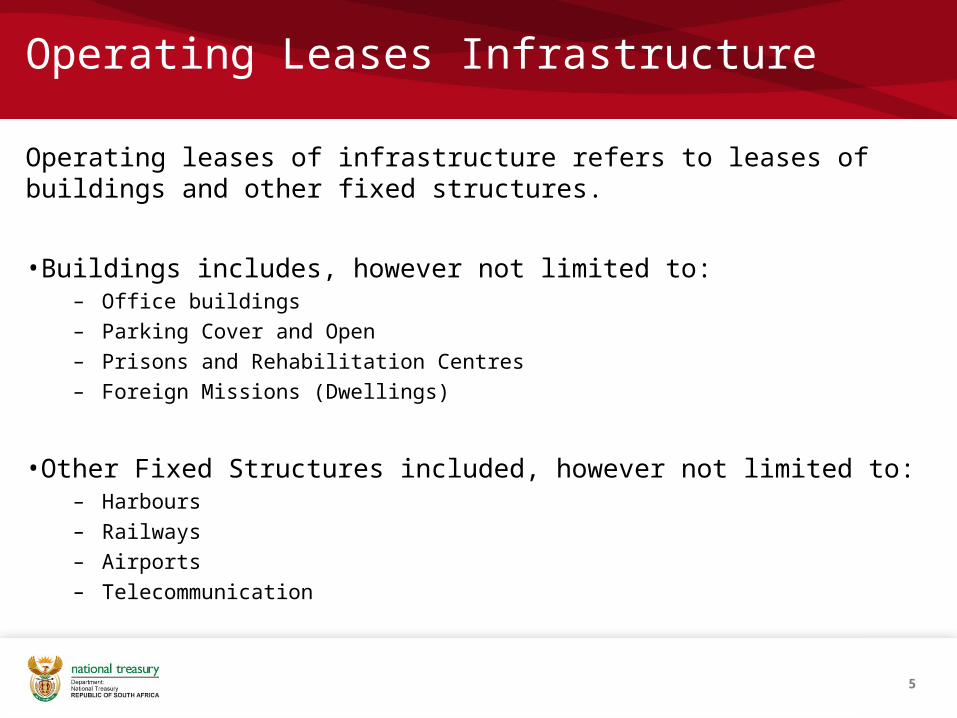

Operating Leases Infrastructure

Operating leases of infrastructure refers to leases of buildings and other fixed structures.

•Buildings includes, however not limited to:– Office buildings– Parking Cover and Open– Prisons and Rehabilitation Centres– Foreign Missions (Dwellings)

•Other Fixed Structures included, however not limited to:– Harbours– Railways– Airports– Telecommunication

5

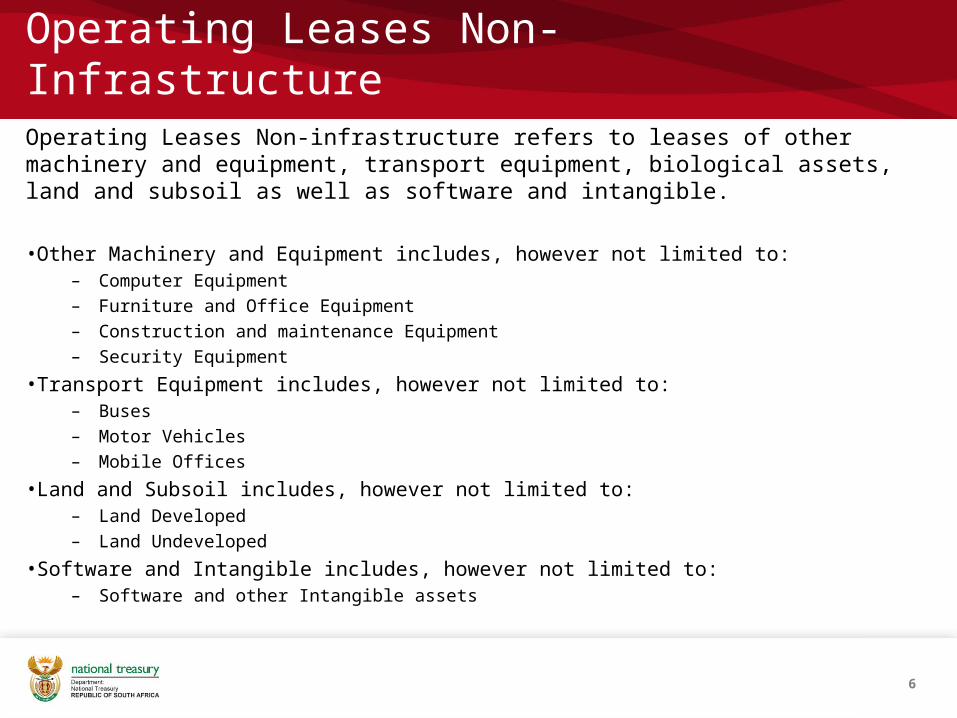

Operating Leases Non-Infrastructure Operating Leases Non-infrastructure refers to leases of other machinery and equipment, transport equipment, biological assets, land and subsoil as well as software and intangible.

•Other Machinery and Equipment includes, however not limited to:– Computer Equipment– Furniture and Office Equipment– Construction and maintenance Equipment– Security Equipment

•Transport Equipment includes, however not limited to:– Buses– Motor Vehicles– Mobile Offices

•Land and Subsoil includes, however not limited to:– Land Developed– Land Undeveloped

•Software and Intangible includes, however not limited to:– Software and other Intangible assets

6

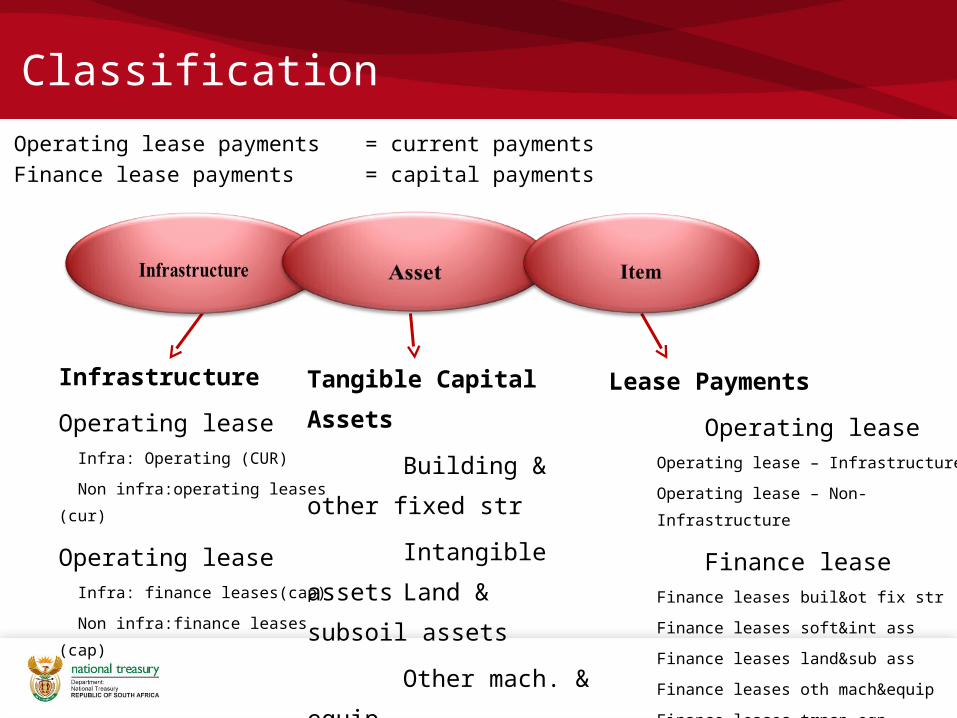

Classification

Operating lease payments = current payments

Finance lease payments = capital payments

Tangible Capital Assets

Building & other

fixed str

Intangible assets

Land & subsoil

assets

Other mach. &

equip

Transport assets

Lease Payments

Operating leaseOperating lease – Infrastructure

Operating lease – Non-Infrastructure

Finance leaseFinance leases buil&ot fix str

Finance leases soft&int ass

Finance leases land&sub ass

Finance leases oth mach&equip

Finance leases trnsp eqp

Infrastructure

Operating lease Infra: Operating (CUR)

Non infra:operating leases (cur)

Operating lease Infra: finance leases(cap)

Non infra:finance leases (cap)

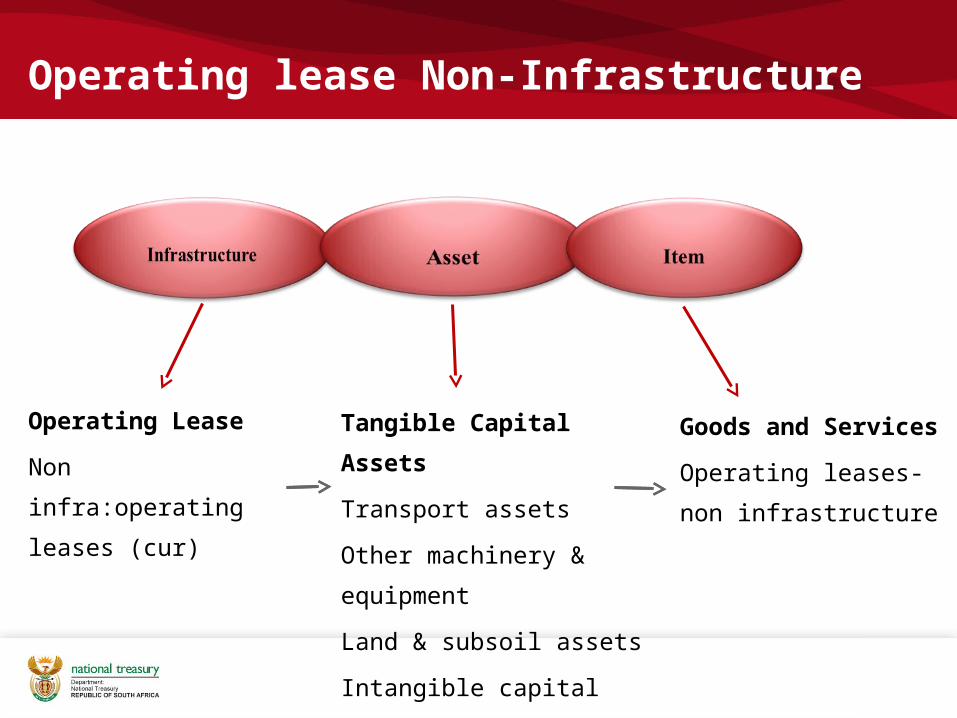

Operating lease Non-Infrastructure

Tangible Capital Assets

Transport assets

Other machinery & equipment

Land & subsoil assets

Intangible capital assets

Goods and Services

Operating leases-non

infrastructure

Operating Lease

Non infra:operating

leases (cur)

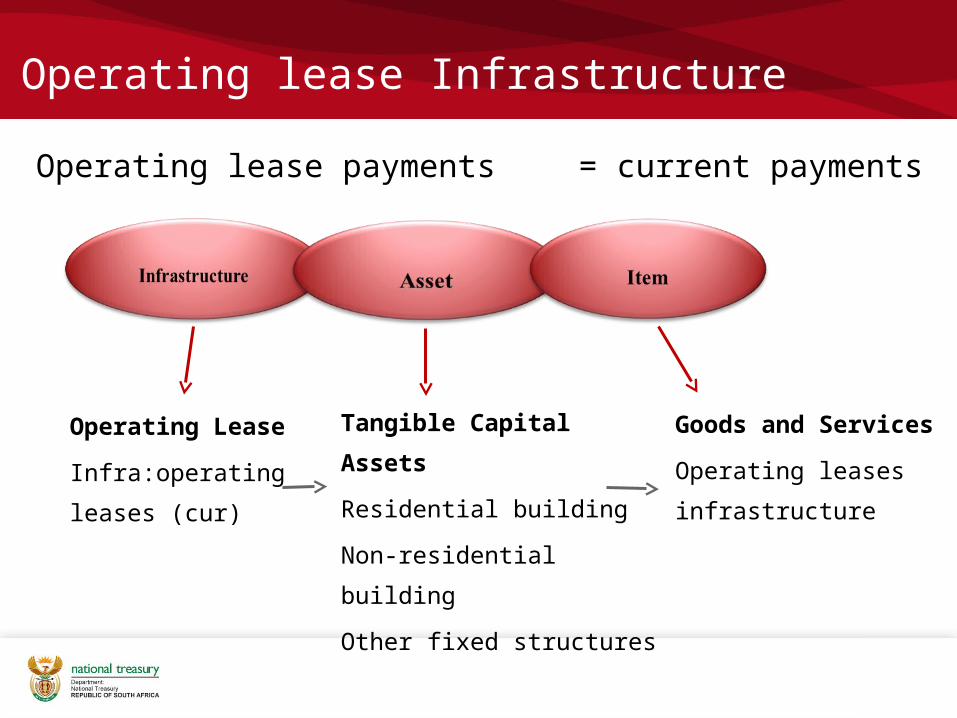

Operating lease Infrastructure

Operating lease payments = current payments

Operating Lease

Infra:operating

leases (cur)

Tangible Capital Assets

Residential building

Non-residential building

Other fixed structures

Goods and Services

Operating leases

infrastructure

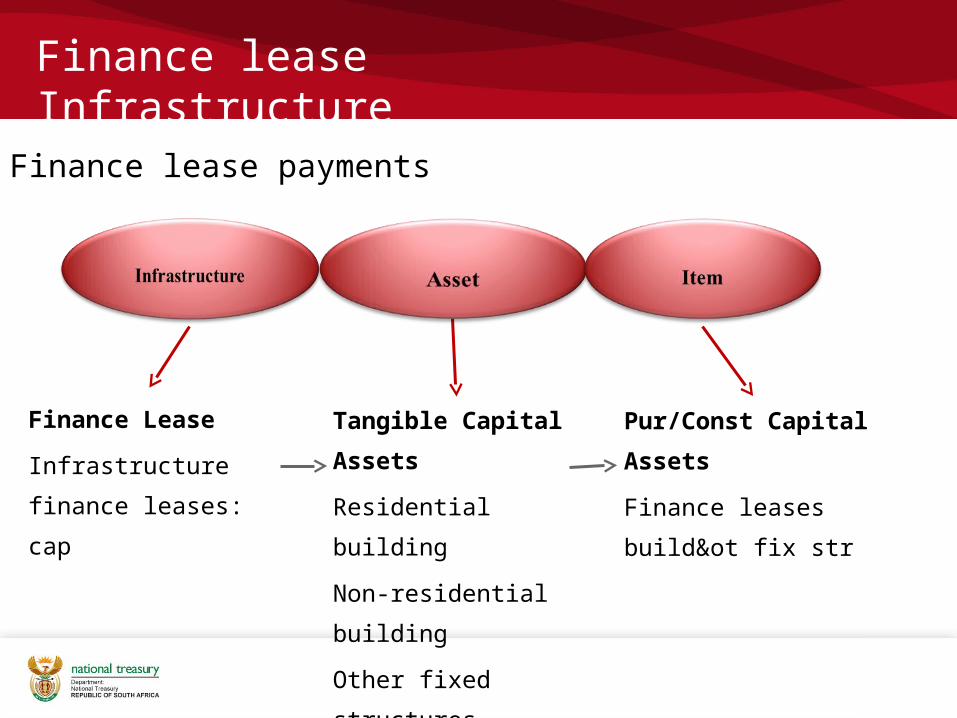

Finance lease Infrastructure

Finance lease payments

Finance Lease

Infrastructure finance

leases: cap

Tangible Capital Assets

Residential building

Non-residential building

Other fixed structures

Pur/Const Capital Assets

Finance leases build&ot fix

str

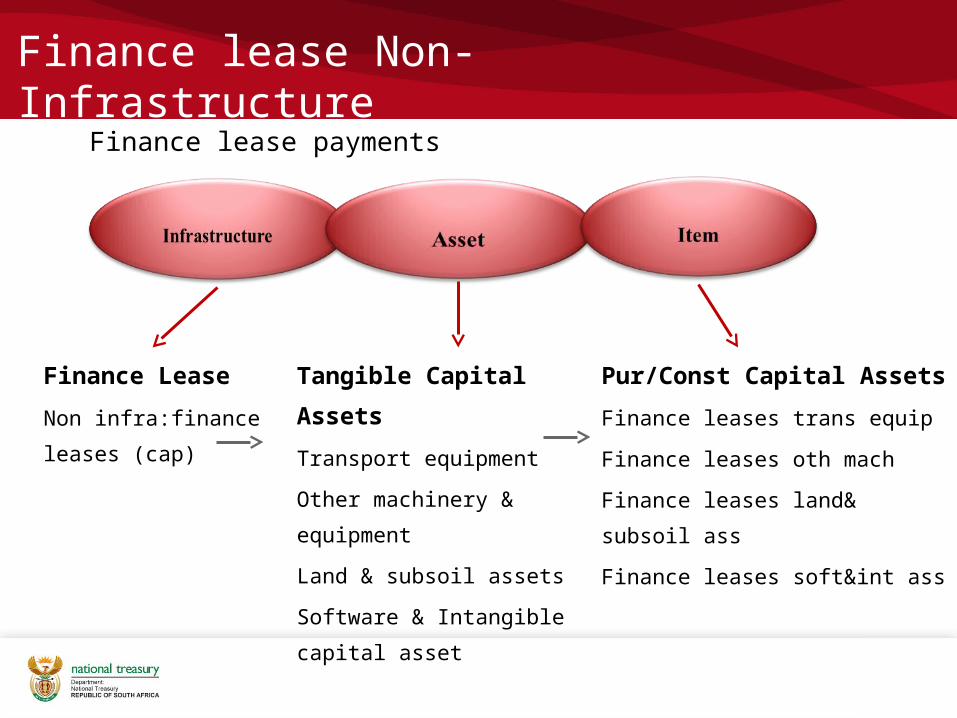

Finance lease Non-Infrastructure

Finance lease payments

Finance Lease

Non infra:finance

leases (cap)

Pur/Const Capital Assets

Finance leases trans equip

Finance leases oth mach

Finance leases land& subsoil ass

Finance leases soft&int ass

Tangible Capital Assets

Transport equipment

Other machinery & equipment

Land & subsoil assets

Software & Intangible capital

asset

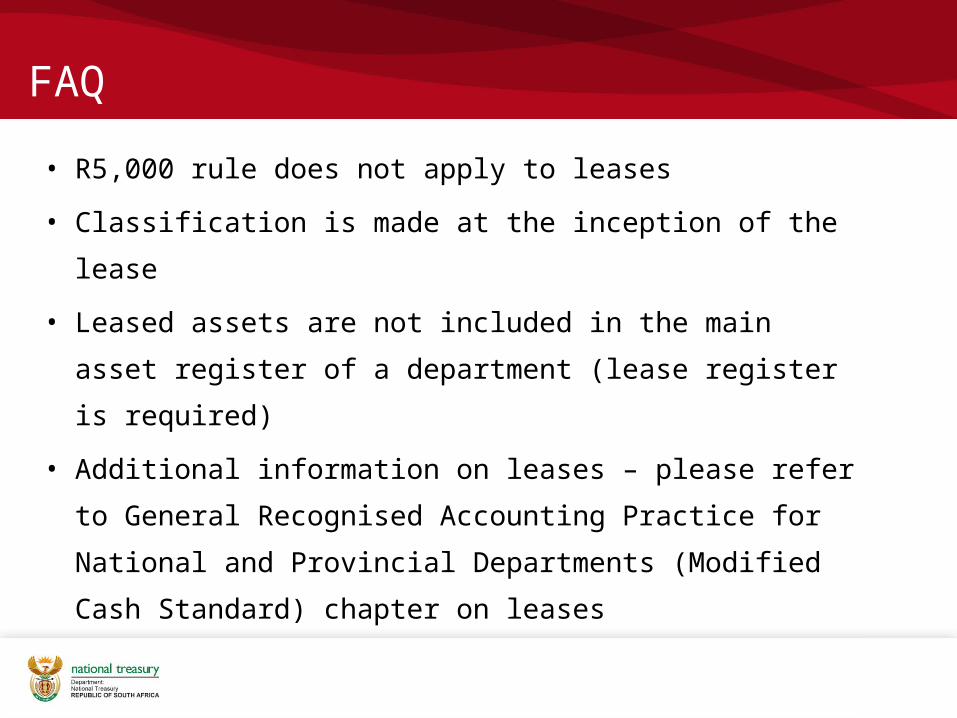

FAQ

• R5,000 rule does not apply to leases

• Classification is made at the inception of the lease

• Leased assets are not included in the main asset

register of a department (lease register is required)

• Additional information on leases – please refer to

General Recognised Accounting Practice for National

and Provincial Departments (Modified Cash Standard)

chapter on leases