Embed Size (px)

Citation preview

Now that the stockmarket has comeback somewhat,

with some companies’stock prices rising whileothers have lowered orremained low, there hasbeen increased activityin mergers and acquisi-tions (M&As). Formany companies, this isan opportunity to lookat a merger or acquisi-tion as a quick means toenhance their finan-cials. However, pickingup a bargain in the marketplaceand thinking how much better youcan run that company could leadto disaster—if you don’t assureyourself that such an M&A oppor-tunity is really suitable for yourfirm and blends well with yourcompany. Remember the ill-fatedTime Warner and AOL merger—have we learned anything fromthis? Try to curb your short-termthinking that only looks toward anincrease in sales, net profits, cashflow, and possibly stock price,rather than longer-term growth.

A BIASED VIEW FROM THE TOP

Most mergers and acquisi-tions are engineered from the

top—and interestingly, it isthose at the top (and theirinvestment advisors) who makeout best from the merger oracquisition in the form of cashin their pockets, employee buy-outs, equity positions, options,and sweetheart employmentcontracts. Is it any wonder thatthese individuals continue tohype the benefits of any pro-posed merger or acquisition tomanagement, employees, share-holders, and other stakeholders?We have seen too many mergersgreatly benefit the money peo-ple (the rich get richer) whileresulting in downsizing middlemanagement (and some topmanagement) and operations

personnel throughconsolidations andoutsourcing those jobsto cheaper labor out-side of the country.So, prior to that finaldecision as to whetherto merge or acquire,proper due diligencerequires not only sub-stantiating the finan-cial numbers, but alsoensuring that there is aproper fit througheffective comparisontechniques.

THE CONCEPT OF SYNERGY

In the context of mergingtwo companies of similar butdivergent attributes, synergy canbe defined as “the possibilitythat the merger of these two indi-vidual companies will produce acombined operation of greaterproductivity and efficiency.”Many times, those in favor of themerger, usually top managementand investment advisors, will sellthe merits of the merger on thebasis of positive synergy. Howev-er, in reality, prior to the mergerthere is no definite way in whichto foresee the differences androadblocks that might get in the

Now that the stock market has recovered a bit,merger and acquisition (M&A) activity hasincreased. Many companies view M&A as a quickway to enhance their financials. But think beforeyou leap—is the candidate company really a goodfit? Or might a merger end in disaster, like theTime Warner/AOL debacle? Is short-term financ-ing overruling good business judgment?

The author takes a sobering look at some ofthe hype surrounding M&A and shows how youcan decide if this is really the right move for yourfirm. © 2007 Wiley Periodicals, Inc.

Rob Reider

Questioning M&A

featu

reartic

le

13

© 2007 Wiley Periodicals, Inc.Published online in Wiley InterScience (www.interscience.wiley.com).DOI 10.1002/jcaf.20271

way of such synergy. Top man-agement usually sees the positiveincreased contribution to salesand net income and the decreaseof costs through the reductionand elimination of duplicatefunctions. Postmerger resultsusually produce less-than-expect-ed sales and net income increasesas well as fewer decreases incosts—sometimes even morecosts. While the concept of syn-ergy encompasses enhancedvalue to the combined entities(especially stock price), reducedcosts through consolidation andreduction of certain operations,reduced overall investment, andthe combining of resources, itvery rarely meets premerger

expectations. By comparingmajor attributes and philosophiesand operating practices of thetwo companies, those directingthe merger are able to make amore informed decision and beprepared by knowing whichchanges should be made andwhat constraints exist.

WHY MERGE OR ACQUIRE

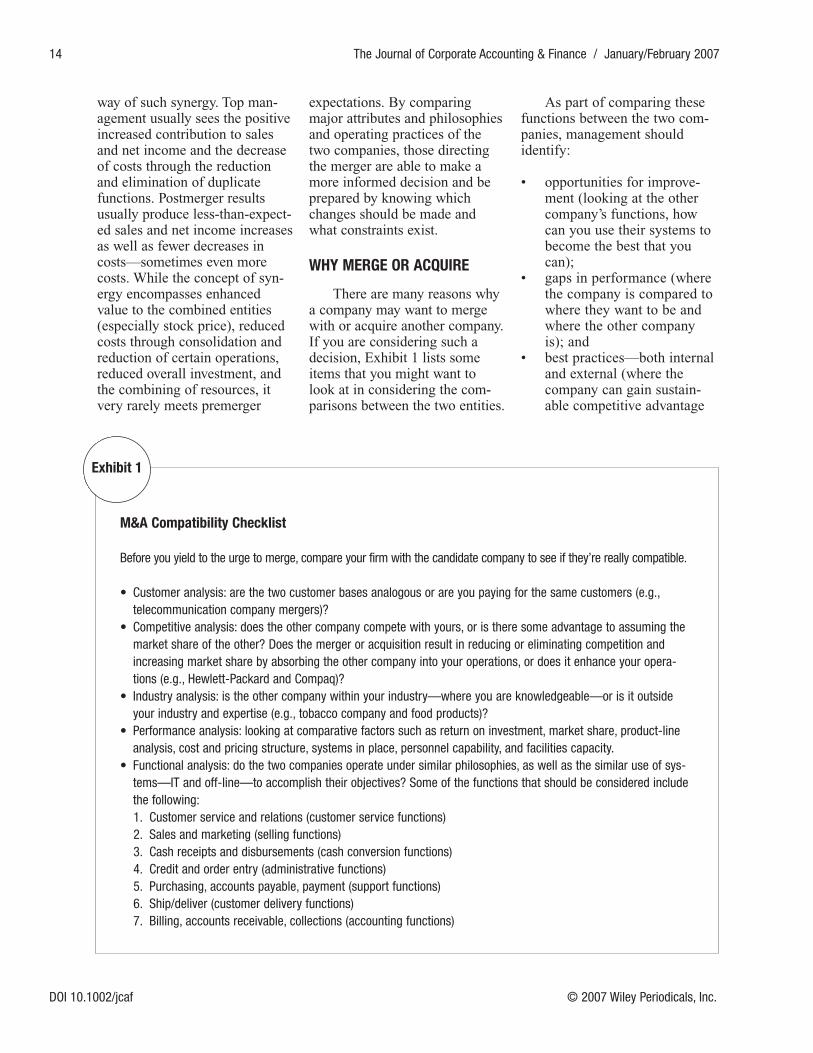

There are many reasons whya company may want to mergewith or acquire another company.If you are considering such adecision, Exhibit 1 lists someitems that you might want tolook at in considering the com-parisons between the two entities.

As part of comparing thesefunctions between the two com-panies, management shouldidentify:

• opportunities for improve-ment (looking at the othercompany’s functions, howcan you use their systems tobecome the best that youcan);

• gaps in performance (wherethe company is compared towhere they want to be andwhere the other companyis); and

• best practices—both internaland external (where thecompany can gain sustain-able competitive advantage

14 The Journal of Corporate Accounting & Finance / January/February 2007

DOI 10.1002/jcaf © 2007 Wiley Periodicals, Inc.

M&A Compatibility Checklist

Before you yield to the urge to merge, compare your firm with the candidate company to see if they’re really compatible.

• Customer analysis: are the two customer bases analogous or are you paying for the same customers (e.g.,telecommunication company mergers)?

• Competitive analysis: does the other company compete with yours, or is there some advantage to assuming themarket share of the other? Does the merger or acquisition result in reducing or eliminating competition andincreasing market share by absorbing the other company into your operations, or does it enhance your opera-tions (e.g., Hewlett-Packard and Compaq)?

• Industry analysis: is the other company within your industry—where you are knowledgeable—or is it outsideyour industry and expertise (e.g., tobacco company and food products)?

• Performance analysis: looking at comparative factors such as return on investment, market share, product-lineanalysis, cost and pricing structure, systems in place, personnel capability, and facilities capacity.

• Functional analysis: do the two companies operate under similar philosophies, as well as the similar use of sys-tems—IT and off-line—to accomplish their objectives? Some of the functions that should be considered includethe following:1. Customer service and relations (customer service functions)2. Sales and marketing (selling functions)3. Cash receipts and disbursements (cash conversion functions)4. Credit and order entry (administrative functions)5. Purchasing, accounts payable, payment (support functions)6. Ship/deliver (customer delivery functions)7. Billing, accounts receivable, collections (accounting functions)

Exhibit 1

through practices of theother company).

Merging with or acquiringanother company can accom-plish numeric growth and opera-tional improvements—or youcan do it by acquiring a divisionof another company, a specificoperation (e.g., research anddevelopment, data processing), aproduct line or product (e.g., afood company acquiring a com-plementary product), and so on.Such acquisitions should be con-sidered using the concept ofleverage. That is, the resultantreturn on investment shouldexceed the cost of the invest-ment. For instance, if thecost of the capital to makethe acquisition is 6 percent,then the expected (and real)return on the investmentshould be sufficientlygreater than 6 percent (e.g.,over 10 percent) to coverthe potential risk involved.Obtaining organizational growththrough acquisition is not alwayspositive, as the company may beacquiring another’s problems ormay lack the expertise to takefull advantage of the acquisition.

COMPARING STRATEGIES FORDOING BUSINESS

Every business, whether itstates it or not, has a predomi-nant strategy for conducting itsbusiness or a business segmentof its operations, and for achiev-ing competitive advantage overits competitors. These strategiesof the companies considering amerger or an acquisition shouldcomplement each other, and notbe at cross purposes. Some ofthese strategies include:

• differentiation as to suchthings as quality, brandname/recognition, customer

orientation, loyal customerbase, patent protection, tech-nical superiority, distribution,and product-line breadth;

• focus as to product lines andproducts, markets, geograph-ic areas, and customer;

• preemption—that is, a spe-cial niche—as to service,product, production meth-ods, innovation, distribution,supply systems, and cus-tomer loyalty; and

• low-cost advantage, whichcould include no-frills prod-ucts, product design, rawmaterial source control,locations, cost

containment/low overhead,and low-cost culture.

Each of these strategies canbe applied to the entire organiza-tion, a distinct product line, aspecific product, a division ordepartment of the company, andso on. For each strategy, theremay be one or more organiza-tional goals. These goals arethen looked at for best practiceimplementation to achieve andhopefully exceed the competi-tion. For example, a differentia-tion strategy of “quality” mightinclude the following aspects:

• immediate order entry intoproduction schedule onreceipt of customer order;

• vendor delivery of materialsneeded at time of productionrequirements;

• entry into production atscheduled time to ensure

completion for deliverytime;

• minimal time spent in pro-duction per schedule;

• no excess materials, rejects,rework, scrap, productiondelays, and so on;

• production completed ontime with total quality andcorrect quantity;

• shipping of order to cus-tomer on time by the rightmethod;

• billing at time of shipment(or before)—accurate andcomplete; and

• collection from the customerin a timely manner (at time ofshipment/receipt if possible).

SOME BASIC BUSINESSPRINCIPLES

Each company differsin the way it conducts itsbusiness. To ensure a com-patible merger or acquisi-tion, it is best that each

company embraces the samebasic business principles. It issometimes extremely difficult tochange a merged or acquiredcompany to your way of thinkingafter the merger or acquisitionhas gone into effect. It is mucheasier and safer to compare twocompanies’ basic business prin-ciples on the front end to ensurecompatibility.

Each organization must deter-mine the basic principles uponwhich it conducts its operations.These principles then become thefoundation upon which the organ-ization bases its desirable operat-ing practices. Examples of suchbusiness principles include thoselisted in Exhibit 2.

ORGANIZATIONAL CONCERNSAND COMPARISONS

There seems to be an organi-zational trend toward empire

The Journal of Corporate Accounting & Finance / January/February 2007 15

© 2007 Wiley Periodicals, Inc. DOI 10.1002/jcaf

To ensure a compatible merger oracquisition, it is best that each com-pany embraces the same basic busi-ness principles.

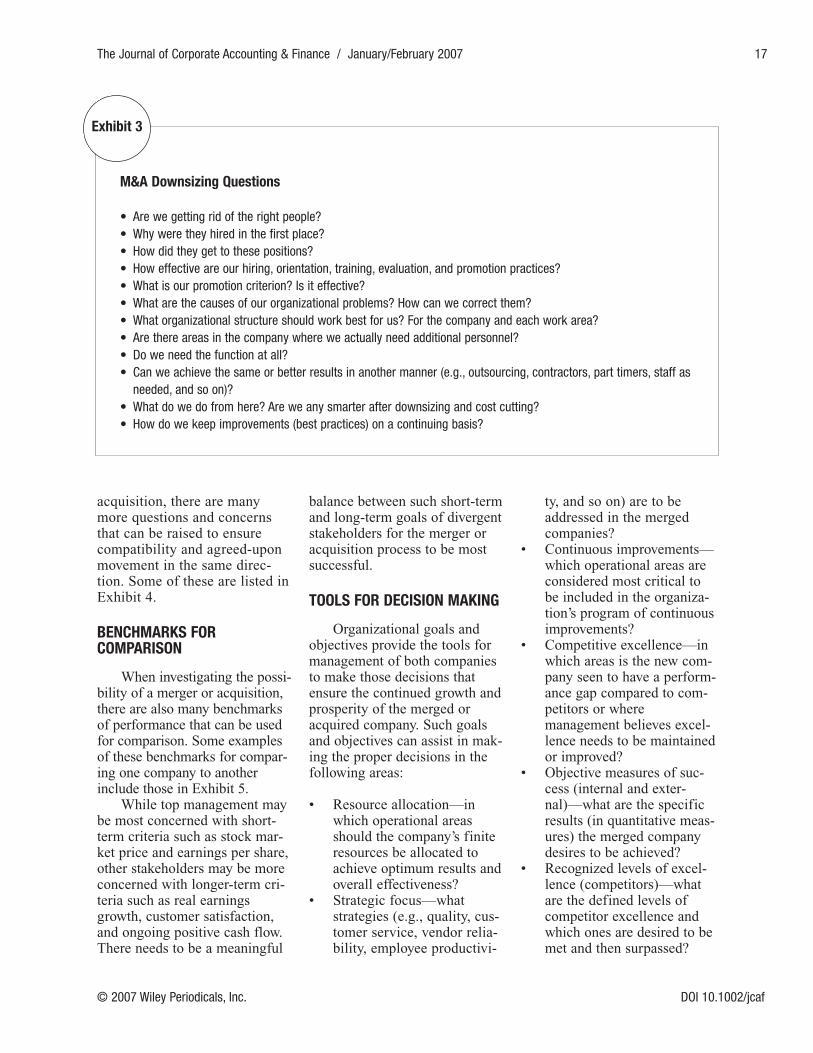

building, particularly from thetop, and the power and controlthat comes with it. Even withpresent-day movements towardsuch things as downsizing,restructuring, reengineering, andso on with its emphasis on get-ting by with less people andresources, those in power aretrying to hold onto unnecessaryempires of people and budget-allocated resources. While amanager is quite agreeable aboutreducing another manager’sempire, there is considerableresistance when it comes toreducing the size of his or herown area. In many instances,even with these quick and short-term remedies at people reduc-tions, there still remain individu-als and layers of organizationalhierarchy that are unnecessary(non-value-added).

By analyzing and compar-ing the two companies’ con-

cepts for organization on thefront end, prior to the merger oracquisition, you can assist bothcompanies in identifying theircritical problem areas, and thenin treating the cause of theproblem and not merely thesymptom of the problem. Withsensible business principles asthe hallmark of the company’soperations, both companies canbe clear as to the direction forpositive movement and avoidmerely improving poor prac-tices. Clear business principlesthat make sense to all levels ofthe organization allow the twocompanies to identify anddevelop proper and compatibleorganizational structures. In thismanner, everyone in the organi-zation is moving in the samedesired direction.

Many organizations havedeveloped systems that they con-sider helpful, such as planning,

budgeting, compensation, report-ing, and cost control. But thesesystems, rather than being help-ful, may result in the building upof unnecessary staff andresources characterized by multi-tiered organization levels andexcessive budgets and expendi-tures. As an example, whilesome companies are reducingstaff size through downsizingand cost cutting, they are hiringnew employees at the same time.When either company reducesstaff size, as a by-product of themerger or acquisition that allowsfor cost economies throughreducing and eliminating dupli-cation of efforts, are they askingthe right questions, such as thosein Exhibit 3?

MORE QUESTIONS TO ASK

In comparing two compa-nies interested in a merger or

16 The Journal of Corporate Accounting & Finance / January/February 2007

DOI 10.1002/jcaf © 2007 Wiley Periodicals, Inc.

Are There Shared Basic Business Principles?

Do both M&A companies embrace the same basic business principles? Here are some examples:

• Produce the best-quality product at the least-possible cost.• Set selling prices realistically, so as to sell the entire product that can be produced within the constraints of the

production facilities.• Build trusting relationships with critical vendors; keeping them in business is keeping the company in business.• The company is in the customer service and cash conversion businesses.• Don’t spend a dollar that doesn’t need to be spent; a dollar not spent is a dollar to the bottom line. Control costs

effectively; there is more to be made here than increased sales.• Manage the company; do not let it manage the managers. Provide guidance and direction, not crises.• Identify the company’s customers and develop marketing and sales plans with the customers in mind. Produce

for the company’s customers, not for inventory. Serve the customers, not sell them.• Don’t hire employees unless they are absolutely needed, and only when they multiply the company’s effective-

ness so that the company makes more from using them than if the company didn’t use them.• Keep property, plant, and equipment to the minimum necessary to maintain customer demand.• Plan for the realistic, but develop contingency plans for the positively unexpected.

Exhibit 2

acquisition, there are manymore questions and concernsthat can be raised to ensurecompatibility and agreed-uponmovement in the same direc-tion. Some of these are listed inExhibit 4.

BENCHMARKS FORCOMPARISON

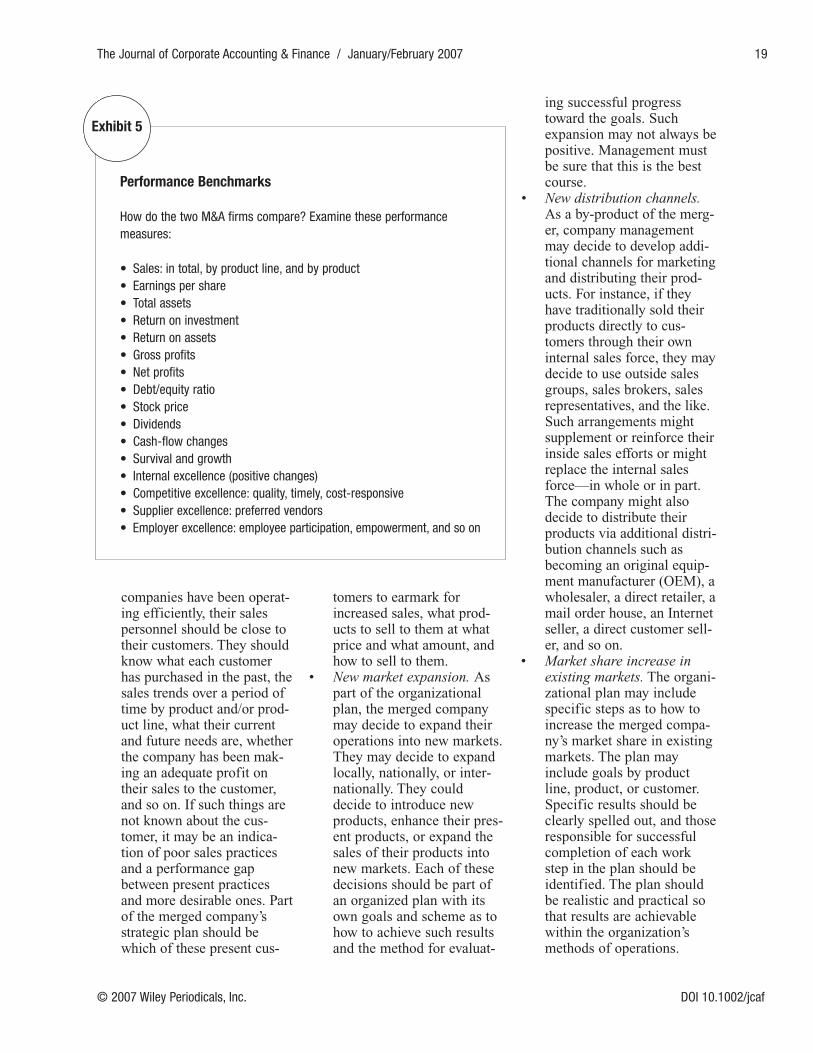

When investigating the possi-bility of a merger or acquisition,there are also many benchmarksof performance that can be usedfor comparison. Some examplesof these benchmarks for compar-ing one company to anotherinclude those in Exhibit 5.

While top management maybe most concerned with short-term criteria such as stock mar-ket price and earnings per share,other stakeholders may be moreconcerned with longer-term cri-teria such as real earningsgrowth, customer satisfaction,and ongoing positive cash flow.There needs to be a meaningful

balance between such short-termand long-term goals of divergentstakeholders for the merger oracquisition process to be mostsuccessful.

TOOLS FOR DECISION MAKING

Organizational goals andobjectives provide the tools formanagement of both companiesto make those decisions thatensure the continued growth andprosperity of the merged oracquired company. Such goalsand objectives can assist in mak-ing the proper decisions in thefollowing areas:

• Resource allocation—inwhich operational areasshould the company’s finiteresources be allocated toachieve optimum results andoverall effectiveness?

• Strategic focus—whatstrategies (e.g., quality, cus-tomer service, vendor relia-bility, employee productivi-

ty, and so on) are to beaddressed in the mergedcompanies?

• Continuous improvements—which operational areas areconsidered most critical tobe included in the organiza-tion’s program of continuousimprovements?

• Competitive excellence—inwhich areas is the new com-pany seen to have a perform-ance gap compared to com-petitors or wheremanagement believes excel-lence needs to be maintainedor improved?

• Objective measures of suc-cess (internal and exter-nal)—what are the specificresults (in quantitative meas-ures) the merged companydesires to be achieved?

• Recognized levels of excel-lence (competitors)—whatare the defined levels ofcompetitor excellence andwhich ones are desired to bemet and then surpassed?

The Journal of Corporate Accounting & Finance / January/February 2007 17

© 2007 Wiley Periodicals, Inc. DOI 10.1002/jcaf

M&A Downsizing Questions

• Are we getting rid of the right people?• Why were they hired in the first place?• How did they get to these positions?• How effective are our hiring, orientation, training, evaluation, and promotion practices?• What is our promotion criterion? Is it effective?• What are the causes of our organizational problems? How can we correct them?• What organizational structure should work best for us? For the company and each work area?• Are there areas in the company where we actually need additional personnel?• Do we need the function at all?• Can we achieve the same or better results in another manner (e.g., outsourcing, contractors, part timers, staff as

needed, and so on)?• What do we do from here? Are we any smarter after downsizing and cost cutting?• How do we keep improvements (best practices) on a continuing basis?

Exhibit 3

ORGANIZATIONAL GROWTH

There are numerous criteriaand areas that the merged organ-ization may choose to implementin their program of synergisticimprovements that lead towardorganizational growth. Some ofthese include the following:

• Cost reductions. Manytimes, costs can be reducedor eliminated without anyappreciable diminishment ofthe organization’s efficiencyor effectiveness—these costreductions should be aggres-sively pursued. Other times,management is strictly look-ing at short-term cost reduc-tions to puff up the compa-ny’s profitability to justifythe merger—these costreductions should be avoidedas they typically only pro-

duce short-term gain forlong-term pain. Rememberthe principle that a dollar ofcost reduction produces adollar increase to the bot-tom-line net profits—but usethis principle effectively.

• Price increases. Companymanagement, due to theirincrease in market share andreduction of competition,may decide at any time toincrease the prices chargedto customers for their goodsand services. Such priceincreases may be justified inthe marketplace (and part ofa strategic plan) or just man-agement’s desire to increaserevenues (hoping everythingelse stays the same). In thissituation, a dollar increase inrevenues will not produce adollar increase in net profits.The best that can be

achieved is the net profitmargin of this additional sale(sales dollars less costs = netprofit per sale). It is possibleif the costs of this additionalsale exceed the revenuesgenerated that each addition-al sale results in a decreasein the bottom line. In addi-tion, such price increasesmay create additional exter-nal competition that maycause less sales or increasedcosts to make each sale.

• Sales volume increases. Partof the merged company’sstrategic plan may be toincrease the level of sales tocustomers—both present andpotential customers. It is usu-ally easier to increase salesvolumes with the mergedcompany’s present customersthan to continually prospectfor new customers. If both

18 The Journal of Corporate Accounting & Finance / January/February 2007

DOI 10.1002/jcaf © 2007 Wiley Periodicals, Inc.

More Compatibility Questions to Ask

• Organizational mission: why is the organization in existence, which products or services will it provide, who areits customers, what does it desire to provide to each of its customers, what are the basic business principlesupon which it will operate, and so on.

• Organizational goals and objectives: what are the overall results desired to be achieved, directions to be movedtoward (increase, decrease, status quo), definitions of desired best practices, critical areas for improvements,and so on.

• Stakeholders’ concerns: owners, shareholders, vendors, customers, employees, management, and so on.• Environmental issues: economy (international, national, local), competitors, political, consumers, legislative, and so on.• Organizational requirements: personnel (hiring, training, downsizing, transferability), facilities (increase, decrease,

combine), equipment (production, data processing), systems (production, management, administrative), and so on.• Control and reporting systems: identification of key operating indicators (e.g., sales by product/product line, on-

time deliveries), evaluative criteria (e.g., each late delivery), reporting format (e.g., real time on line, daily sum-mary), and follow-up procedures.

• Resource requirements: personnel, facilities, equipment, funding, earnings, outside assistance, cash flow, sys-tems, and so on.

• Market assessment: by product, by product line, by customer, by competitor, existing products, changes required,potential products, and so on.

Exhibit 4

companies have been operat-ing efficiently, their salespersonnel should be close totheir customers. They shouldknow what each customerhas purchased in the past, thesales trends over a period oftime by product and/or prod-uct line, what their currentand future needs are, whetherthe company has been mak-ing an adequate profit ontheir sales to the customer,and so on. If such things arenot known about the cus-tomer, it may be an indica-tion of poor sales practicesand a performance gapbetween present practicesand more desirable ones. Partof the merged company’sstrategic plan should bewhich of these present cus-

tomers to earmark forincreased sales, what prod-ucts to sell to them at whatprice and what amount, andhow to sell to them.

• New market expansion. Aspart of the organizationalplan, the merged companymay decide to expand theiroperations into new markets.They may decide to expandlocally, nationally, or inter-nationally. They coulddecide to introduce newproducts, enhance their pres-ent products, or expand thesales of their products intonew markets. Each of thesedecisions should be part ofan organized plan with itsown goals and scheme as tohow to achieve such resultsand the method for evaluat-

ing successful progresstoward the goals. Suchexpansion may not always bepositive. Management mustbe sure that this is the bestcourse.

• New distribution channels.As a by-product of the merg-er, company managementmay decide to develop addi-tional channels for marketingand distributing their prod-ucts. For instance, if theyhave traditionally sold theirproducts directly to cus-tomers through their owninternal sales force, they maydecide to use outside salesgroups, sales brokers, salesrepresentatives, and the like.Such arrangements mightsupplement or reinforce theirinside sales efforts or mightreplace the internal salesforce—in whole or in part.The company might alsodecide to distribute theirproducts via additional distri-bution channels such asbecoming an original equip-ment manufacturer (OEM), awholesaler, a direct retailer, amail order house, an Internetseller, a direct customer sell-er, and so on.

• Market share increase inexisting markets. The organi-zational plan may includespecific steps as to how toincrease the merged compa-ny’s market share in existingmarkets. The plan mayinclude goals by productline, product, or customer.Specific results should beclearly spelled out, and thoseresponsible for successfulcompletion of each workstep in the plan should beidentified. The plan shouldbe realistic and practical sothat results are achievablewithin the organization’smethods of operations.

The Journal of Corporate Accounting & Finance / January/February 2007 19

© 2007 Wiley Periodicals, Inc. DOI 10.1002/jcaf

Performance Benchmarks

How do the two M&A firms compare? Examine these performancemeasures:

• Sales: in total, by product line, and by product• Earnings per share• Total assets• Return on investment• Return on assets• Gross profits• Net profits• Debt/equity ratio• Stock price• Dividends• Cash-flow changes• Survival and growth• Internal excellence (positive changes)• Competitive excellence: quality, timely, cost-responsive• Supplier excellence: preferred vendors• Employer excellence: employee participation, empowerment, and so on

Exhibit 5

• Sell or close a losing opera-tion or location. Sometimesan operation (product line,product, customer, etc.) or aplant or office location isdeemed to be too costly inrelation to the value (incomeor cost saving) added to thecompany. With the properinformation, company man-agement can arrive at theproper decision to retrench.Without such an adequateinformation base, manage-ment may come to the oppo-site conclusion—that is, toallocate more resources intothe operation or location. Inthis instance, managementwould be more than likelyallocating additionalexpenditures to a los-ing proposition. Theobject of retrenchmentis normally to reduceoverall expenses whileincreasing netincome—that is, thebottom line. However,retrenchment will alsodecrease gross sales orincome that may not bedesirable to all of the stake-holders (e.g., owners orshareholders).

• New product or servicedevelopment. Merged com-pany management maydecide that the best methodfor achieving organizationalgrowth or reaching a specif-ic goal is to develop a newproduct or service. To dothis effectively, the companyshould have a real vision oftheir marketplace, theirexisting products, their cus-tomers’ requirements, thedesired need for the newproduct, its effect on existingproducts, and so on. Thedecision to develop and mar-ket a new product should bebased on integrated deci-

sions between the company’smajor functions such assales, marketing, engineer-ing, manufacturing, account-ing, and so on.

• Efficiency or productivityimprovements. The ability toeither operate more effi-ciently at less cost orincrease productivity at thesame (or less) cost may alsobe a workable approach toreaching the merged compa-ny’s organizational growthgoals. A dollar of cost saved(all other factors remainingthe same) will produce anadditional dollar of earningsto the bottom line. Increas-ing productivity produces

more of the product or serv-ice at relatively the samecost, resulting in fewer costsper product or service pro-duced. Both of theseapproaches can be imple-mented and controlled byinternal management andoperations personnel.

There is usually more tobe gained in the bottom linethrough cost efficiencies andproductivity improvementsthan through the variousmethods of revenue or salesenhancements discussedabove. Remember that a dol-lar in sales increase does notadd a dollar to the bottomline, only the incrementalamount of net income gener-ated by the additional sale,which could be a loss.

• Non-value-added activitieseliminated. Functions or

activities that produce novalue added to the productor service should be elimi-nated. As part of the mergeror acquisition, such func-tions or activities should beidentified. Company man-agement should be able toidentify those areas identi-fied for elimination. Forinstance, they may identifyall unnecessary quality con-trol inspections or the prepa-ration of purchase orders. Orthey may identify the desir-ability of eliminating anentire function such as rawmaterial storekeeping orcredit and collections.

• Making employees responsi-ble—for meeting companyexpectations and resultsthrough motivating self-dis-ciplined behavior. With aneffective monitoring sys-tem, this eliminates theneed for management per-sonnel to exist mainly forpolicing and controlling

these individuals with mini-mal value-added activities.Use of operating systemsthat make sense to the work-ers (where they have hadinput in developing suchsystems) who use them with-in a working together atmos-phere (rather than a workingfor atmosphere) willincrease productivity to theextent that fewer employeesoverall are needed. The trickis to not bring on unneces-sary personnel as the compa-ny grows, so that the compa-ny is never in a position tohave to cut back drastically.Many times, a companypenalizes the individualsbeing downsized or laid offfor something out of theircontrol. Effective overseeinghelps to keep the mergedcompany in focus regarding

20 The Journal of Corporate Accounting & Finance / January/February 2007

DOI 10.1002/jcaf © 2007 Wiley Periodicals, Inc.

The decision to develop and marketa new product should be based onintegrated decisions between thecompany’s major functions…

the types and levels of per-sonnel required at any time.

• Organizational structurerevisions. There are manytechniques for building anorganization structure thatare not dependent on thetypical top to bottom mili-tary model that is based onpolicing and controllingthose reporting to each high-er level. Some other tech-niques for organizationalstructure include participa-tive management, sharedmanagement, team manage-ment, self-motivated disci-plined behavior (no manag-er), coaching and facilitativesupports, and so on. There isno right answer for all situa-tions. The merged companymust learn to use a combina-tion of these techniques asthey fit the particular situa-tion. The comparisonprocess allows the mergedcompany to achieve the bestorganizational structureoverall as well as withineach function and activity.Proper management andeffective business principlesemphasize controllingresults, not people; fixingthe cause, not the blame; anddoing the right job right, notjust doing the job right.

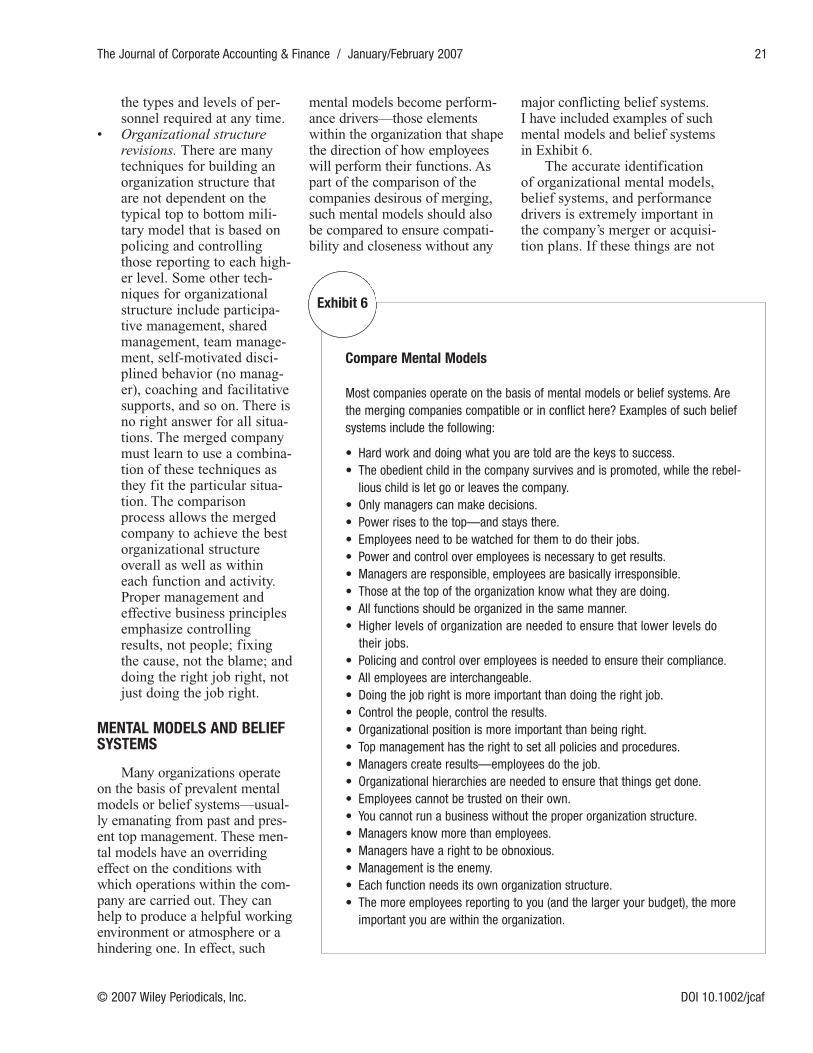

MENTAL MODELS AND BELIEFSYSTEMS

Many organizations operateon the basis of prevalent mentalmodels or belief systems—usual-ly emanating from past and pres-ent top management. These men-tal models have an overridingeffect on the conditions withwhich operations within the com-pany are carried out. They canhelp to produce a helpful workingenvironment or atmosphere or ahindering one. In effect, such

mental models become perform-ance drivers—those elementswithin the organization that shapethe direction of how employeeswill perform their functions. Aspart of the comparison of thecompanies desirous of merging,such mental models should alsobe compared to ensure compati-bility and closeness without any

major conflicting belief systems.I have included examples of suchmental models and belief systemsin Exhibit 6.

The accurate identificationof organizational mental models,belief systems, and performancedrivers is extremely important inthe company’s merger or acquisi-tion plans. If these things are not

The Journal of Corporate Accounting & Finance / January/February 2007 21

© 2007 Wiley Periodicals, Inc. DOI 10.1002/jcaf

Compare Mental Models

Most companies operate on the basis of mental models or belief systems. Arethe merging companies compatible or in conflict here? Examples of such beliefsystems include the following:

• Hard work and doing what you are told are the keys to success.• The obedient child in the company survives and is promoted, while the rebel-

lious child is let go or leaves the company.• Only managers can make decisions.• Power rises to the top—and stays there.• Employees need to be watched for them to do their jobs.• Power and control over employees is necessary to get results.• Managers are responsible, employees are basically irresponsible.• Those at the top of the organization know what they are doing.• All functions should be organized in the same manner.• Higher levels of organization are needed to ensure that lower levels do

their jobs.• Policing and control over employees is needed to ensure their compliance.• All employees are interchangeable.• Doing the job right is more important than doing the right job.• Control the people, control the results.• Organizational position is more important than being right.• Top management has the right to set all policies and procedures.• Managers create results—employees do the job.• Organizational hierarchies are needed to ensure that things get done.• Employees cannot be trusted on their own.• You cannot run a business without the proper organization structure.• Managers know more than employees.• Managers have a right to be obnoxious.• Management is the enemy.• Each function needs its own organization structure.• The more employees reporting to you (and the larger your budget), the more

important you are within the organization.

Exhibit 6

22 The Journal of Corporate Accounting & Finance / January/February 2007

DOI 10.1002/jcaf © 2007 Wiley Periodicals, Inc.

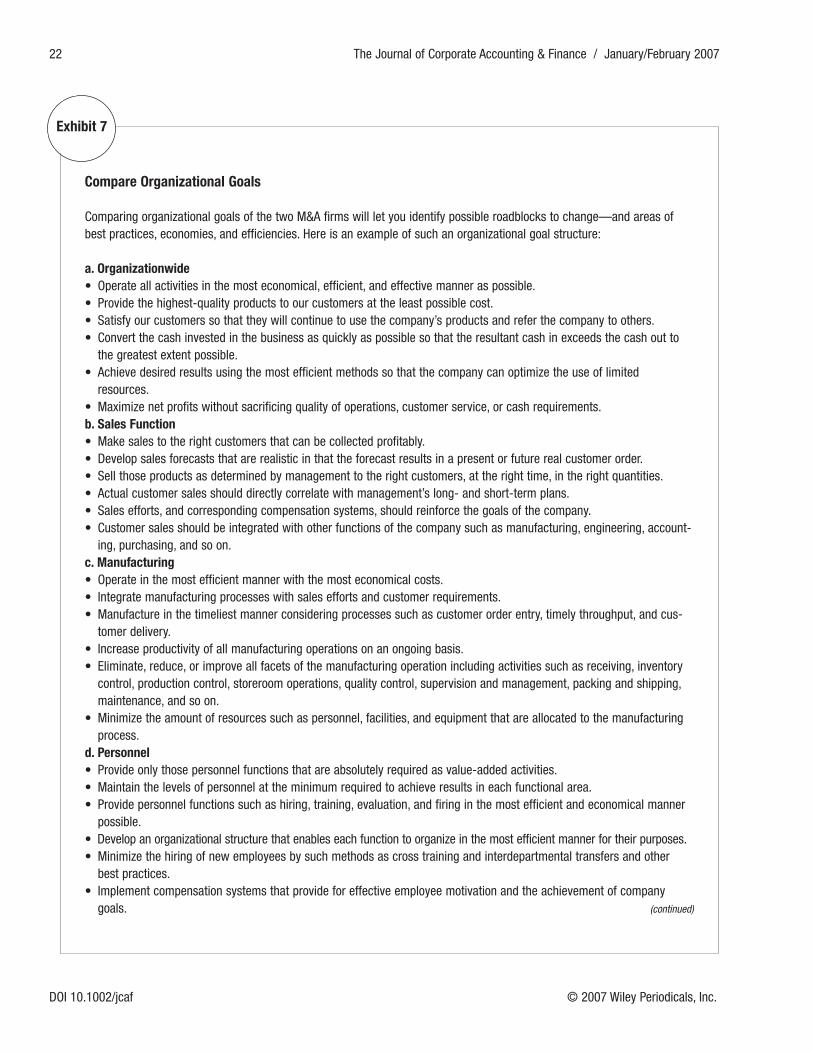

Compare Organizational Goals

Comparing organizational goals of the two M&A firms will let you identify possible roadblocks to change—and areas ofbest practices, economies, and efficiencies. Here is an example of such an organizational goal structure:

a. Organizationwide • Operate all activities in the most economical, efficient, and effective manner as possible.• Provide the highest-quality products to our customers at the least possible cost.• Satisfy our customers so that they will continue to use the company’s products and refer the company to others.• Convert the cash invested in the business as quickly as possible so that the resultant cash in exceeds the cash out to

the greatest extent possible.• Achieve desired results using the most efficient methods so that the company can optimize the use of limited

resources.• Maximize net profits without sacrificing quality of operations, customer service, or cash requirements.b. Sales Function• Make sales to the right customers that can be collected profitably.• Develop sales forecasts that are realistic in that the forecast results in a present or future real customer order.• Sell those products as determined by management to the right customers, at the right time, in the right quantities.• Actual customer sales should directly correlate with management’s long- and short-term plans.• Sales efforts, and corresponding compensation systems, should reinforce the goals of the company.• Customer sales should be integrated with other functions of the company such as manufacturing, engineering, account-

ing, purchasing, and so on.c. Manufacturing• Operate in the most efficient manner with the most economical costs.• Integrate manufacturing processes with sales efforts and customer requirements.• Manufacture in the timeliest manner considering processes such as customer order entry, timely throughput, and cus-

tomer delivery.• Increase productivity of all manufacturing operations on an ongoing basis.• Eliminate, reduce, or improve all facets of the manufacturing operation including activities such as receiving, inventory

control, production control, storeroom operations, quality control, supervision and management, packing and shipping,maintenance, and so on.

• Minimize the amount of resources such as personnel, facilities, and equipment that are allocated to the manufacturingprocess.

d. Personnel• Provide only those personnel functions that are absolutely required as value-added activities.• Maintain the levels of personnel at the minimum required to achieve results in each functional area.• Provide personnel functions such as hiring, training, evaluation, and firing in the most efficient and economical manner

possible.• Develop an organizational structure that enables each function to organize in the most efficient manner for their purposes.• Minimize the hiring of new employees by such methods as cross training and interdepartmental transfers and other

best practices.• Implement compensation systems that provide for effective employee motivation and the achievement of company

goals. (continued)

Exhibit 7

changed to bring them into clos-er agreement, such practices willcontinue grossly affecting over-all company results.

ORGANIZATIONAL GOALSEXAMPLE

As previously discussed, thefirst step in successful compari-son of two different companiesdesiring to merge is to defineeach company’s organizationalgoals as related to their reasonsfor existence, basic business prin-ciples, mental models, belief sys-tems, performance drivers, and soon. These organizational goalsencompass the organization as anentity as well as its major func-tions. Such a comparison allowsthe two companies to identifytheir similarities, differences, andconstraints that might cause road-

blocks to change, and areas ofbest practices, economies, andefficiencies. An example of suchan organizational goal structure isgiven in Exhibit 7.

MAKE THE COMPARISONS!

The development of suchorganizational goals provides thebasis upon which to compare andevaluate the two companies’ cur-rent practices, identify criticalproblem areas, analyze detailedoperations, identify best practices,and implement corrective solu-tions in a program of continuousimprovements. Without the defi-nition and communication of suchorganizational goals, the mergedcompany’s efforts may only suc-ceed in developing best practicesfor functions and activities that inthemselves are bad practices. This

should not be an effort to improvebad practices but to develop pro-cedures that bring best practicesinto the organization. Throughthis process, operating functionsand activities are evaluated as totheir necessity as related to theachievement of organizationalgoals and objectives. If it is decid-ed that a function or activity is notnecessary, then it should be elimi-nated. If it is needed, then itshould be considered for improve-ment looking for the best presentpractice and then continually ana-lyzed in the company’s programof continuous improvements.Through this process, the compa-ny starts to develop itself as alearning organization, with eachindividual responsible for himselfor herself and the activities theyare responsible for achievingresults.

The Journal of Corporate Accounting & Finance / January/February 2007 23

© 2007 Wiley Periodicals, Inc. DOI 10.1002/jcaf

Compare Organizational Goals (continued)

e. Purchasing• Purchase only those items where economies can be gained through a system of central purchasing.• Implement direct-purchase systems for those items that do not need to be processed by the purchasing function such

as low-dollar purchases and repetitive purchases.• Simplify systems so that the cost of purchasing is the lowest possible.• Effectively negotiate with vendors so that the company obtains the right materials at the right time at the right quality at

the right price.• Maintain a vendor analysis system so that vendor performance can be objectively evaluated.• Develop effective computerized techniques that provide for economic processing, adequate controls, and reliability.f. Accounting• Analyze each of the accounting functions and related activities—such as accounts receivable, accounts payable, pay-

roll, budgeting, and general ledger—as to their necessity.• Operate each of the accounting functions in the most economical manner.• Implement effective procedures that result in the accounting functions becoming more analytical than mechanical.• Develop computerized procedures that integrate accounting purposes with operating requirements.• Develop reporting systems that provide management with the necessary operating data and indicators that can be gen-

erated from accounting data.• Eliminate or reduce all accounting operations that are unnecessary or provide no value-added incentives.

Exhibit 7

24 The Journal of Corporate Accounting & Finance / January/February 2007

DOI 10.1002/jcaf © 2007 Wiley Periodicals, Inc.

Rob Reider, CPA, MBA, PhD, is the president of Reider Associates, a management and organizational con-sulting firm he founded in 1976, which is located in Santa Fe, New Mexico. Prior to starting Reider Asso-ciates, Dr. Reider was a manager in the Management Consulting Department of Peat, Marwick (now KPMG)in Philadelphia. Dr. Reider has been a consultant to numerous large, medium, and small businesses of alltypes in both the private and public sectors. He is the course author and sought-after discussion leaderand presenter for more than 20 different seminars that are conducted nationally for various organizationsand associations. He has conducted more than 1,000 such seminars throughout the country and hasreceived the American Institute of Certified Public Accountants Outstanding Discussion Leader of the Yearaward. He is also the author or coauthor of the following books published by John Wiley & Sons:

• Operational Review: Maximum Results at Efficient Costs (text and workbook);• Benchmarking Strategies: A Tool for Profit Improvement; • Improving the Economy, Efficiency, and Effectiveness of Not-for-Profits; and• Managing Cash Flow: An Operational Focus (coauthor with Peter B. Heyler)

Dr. Reider is also the author of the recently released novel Road to Oblivion: The Footpath Back Home, anovel of discovery that looks at life after being downsized. For more information about Rob Reider and hisconsulting firm, visit the Reider Associates Web site at http://www.reiderassociates.com or e-mail him [email protected].