Embed Size (px)

Citation preview

Quarterly reporton the Spanisheconomy

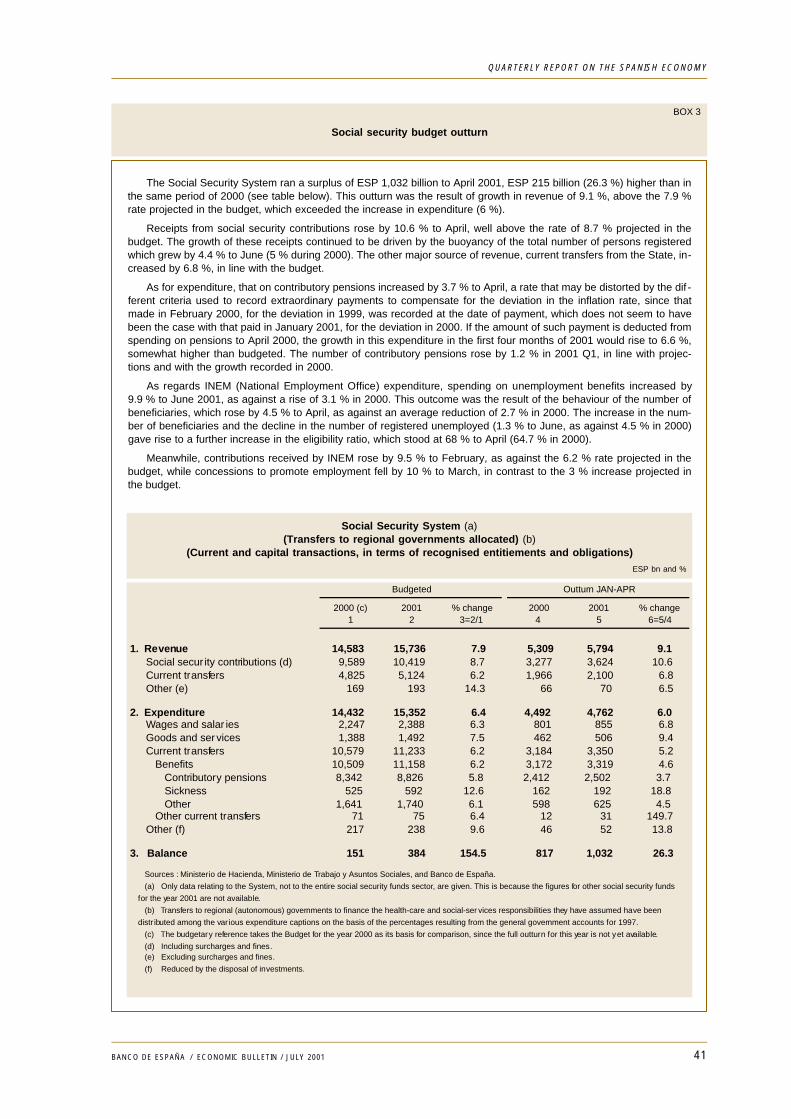

1. Overview

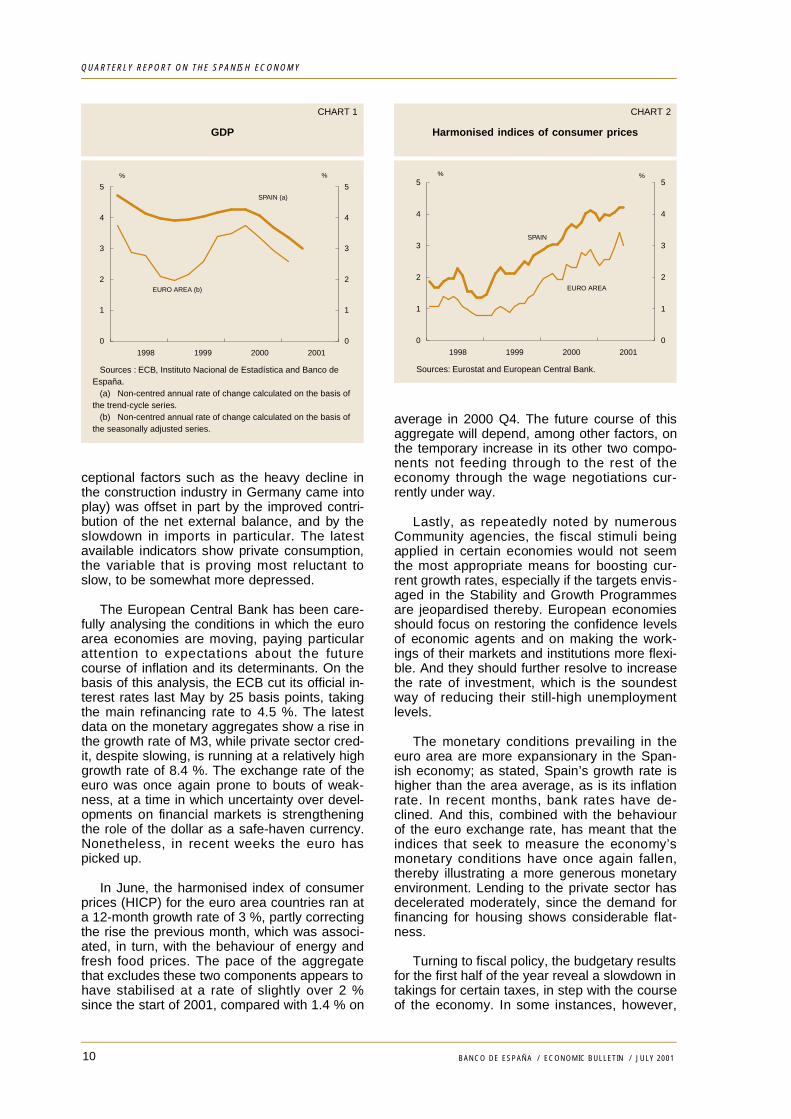

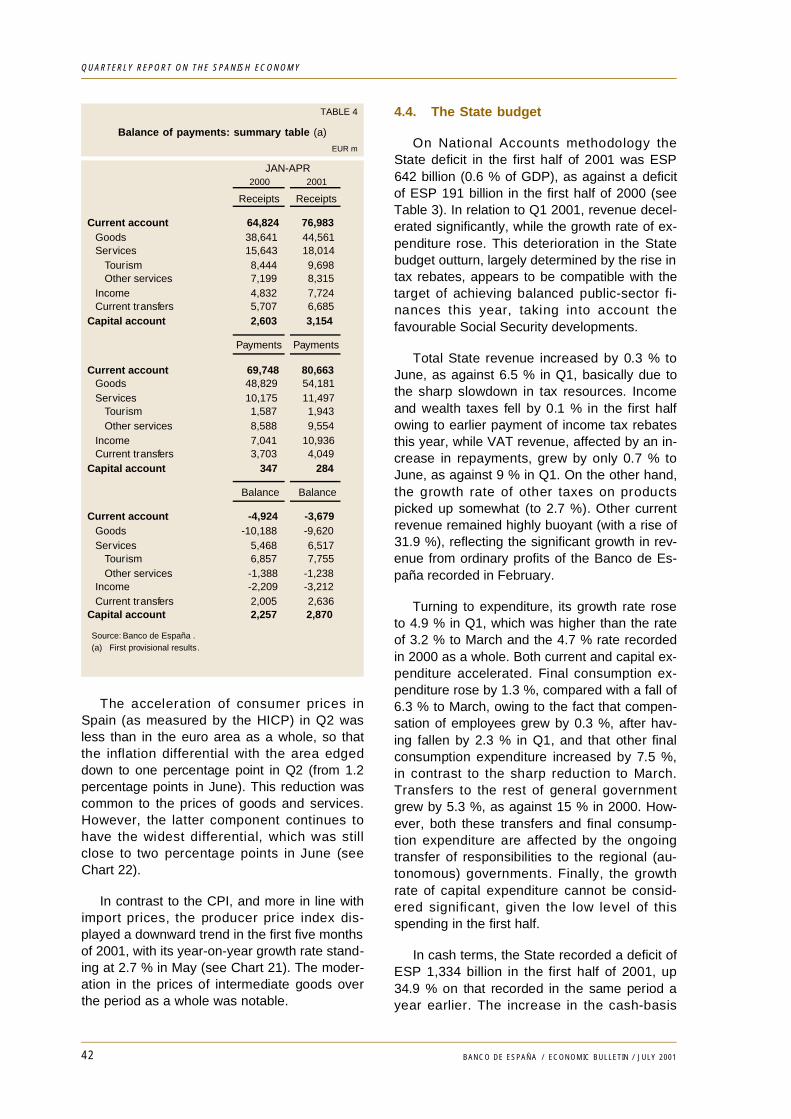

The international economic outlook has con-tinued to worsen during the year 2001. The onlyindication of a future correction in price growthrates in numerous economies and of an allevia-tion of contractionary trends is the lessening oftension on the oil market that appears to havetaken hold. Against this background, the growthrate of the Spanish economy has declined, butits real year-on-year GDP growth rate apprecia-bly exceeds that of most of its trading partners.

Specifically, the Spanish economy’s realGDP growth in 2001 Q2 was estimated at 3 %,four-tenths of a percentage point down on theprovisional figure released by INE for the firstthree months of the year. There have been nosignificant changes in the patterns that have de-termined this outcome: a gradual slowdown indomestic demand, tending to stabilise at a realrate of around 2.5 %, and a positive contributionof net external demand to GDP growth. Em-ployment growth is slowing, but remains no-table. And the expected and foreseeable de-cline in the inflation rate, the differential ofwhich with the euro area countries is fluctuatingat slightly over one percentage point, has notyet come about. It would appear that the morecontained pace of economic activity, affectingabove all the industrial sectors and capitalgoods investment decisions, will not jeopardisethe envisaged target of balanced public fi-nances at the end of the year.

Recent indicators of the US economy do notpresage a rapid recovery. Following the 25 ba-sis points cut in the federal funds target rate lastJune to 3.75 %, the markets expect fresh inter-est rate cuts in the coming months. It is expect-ed that this, combined with the scheduled fiscalmeasures (some of which back-dated), will pro-vide the necessary stimulus for a turnaround ineconomic activity. The slackness of growth hasso far been based more on investment and ex-ports than on consumption, which has remainedmore buoyant. The ongoing stagnation in Japanhas boosted the contractionary effect exertedby the US situation on other areas of the worldeconomy. Growth prospects have also been ad-versely influenced by the impact of the Argen-tinean crisis in Latin America and the vulnerabil-ity of other south-east Asian and eastern Euro-pean economies to the greater instability of fi-nancial markets.

The European economies have been affect-ed by this unfavourable environment, but torather differing degrees depending on their ini-tial exposure to developments in the crisis-rid-den markets. Real GDP growth in the euro areaas a whole during Q2 is expected to be lowerthan in Q1 (2.6 %). In the latter quarter, thesluggishness of domestic demand (where ex-

9BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

ceptional factors such as the heavy decline inthe construction industry in Germany came intoplay) was offset in part by the improved contri-bution of the net external balance, and by theslowdown in imports in particular. The latestavailable indicators show private consumption,the variable that is proving most reluctant toslow, to be somewhat more depressed.

The European Central Bank has been care-fully analysing the conditions in which the euroarea economies are moving, paying particularattention to expectations about the futurecourse of inflation and its determinants. On thebasis of this analysis, the ECB cut its official in-terest rates last May by 25 basis points, takingthe main refinancing rate to 4.5 %. The latestdata on the monetary aggregates show a rise inthe growth rate of M3, while private sector cred-it, despite slowing, is running at a relatively highgrowth rate of 8.4 %. The exchange rate of theeuro was once again prone to bouts of weak-ness, at a time in which uncertainty over devel-opments on financial markets is strengtheningthe role of the dollar as a safe-haven currency.Nonetheless, in recent weeks the euro haspicked up.

In June, the harmonised index of consumerprices (HICP) for the euro area countries ran ata 12-month growth rate of 3 %, partly correctingthe rise the previous month, which was associ-ated, in turn, with the behaviour of energy andfresh food prices. The pace of the aggregatethat excludes these two components appears tohave stabilised at a rate of slightly over 2 %since the start of 2001, compared with 1.4 % on

average in 2000 Q4. The future course of thisaggregate will depend, among other factors, onthe temporary increase in its other two compo-nents not feeding through to the rest of theeconomy through the wage negotiations cur-rently under way.

Lastly, as repeatedly noted by numerousCommunity agencies, the fiscal stimuli beingapplied in certain economies would not seemthe most appropriate means for boosting cur-rent growth rates, especially if the targets envis-aged in the Stability and Growth Programmesare jeopardised thereby. European economiesshould focus on restoring the confidence levelsof economic agents and on making the work-ings of their markets and institutions more flexi-ble. And they should further resolve to increasethe rate of investment, which is the soundestway of reducing their still-high unemploymentlevels.

The monetary conditions prevailing in theeuro area are more expansionary in the Span-ish economy; as stated, Spain’s growth rate ishigher than the area average, as is its inflationrate. In recent months, bank rates have de-clined. And this, combined with the behaviourof the euro exchange rate, has meant that theindices that seek to measure the economy’smonetary conditions have once again fallen,thereby illustrating a more generous monetaryenvironment. Lending to the private sector hasdecelerated moderately, since the demand forfinancing for housing shows considerable flat-n e s s .

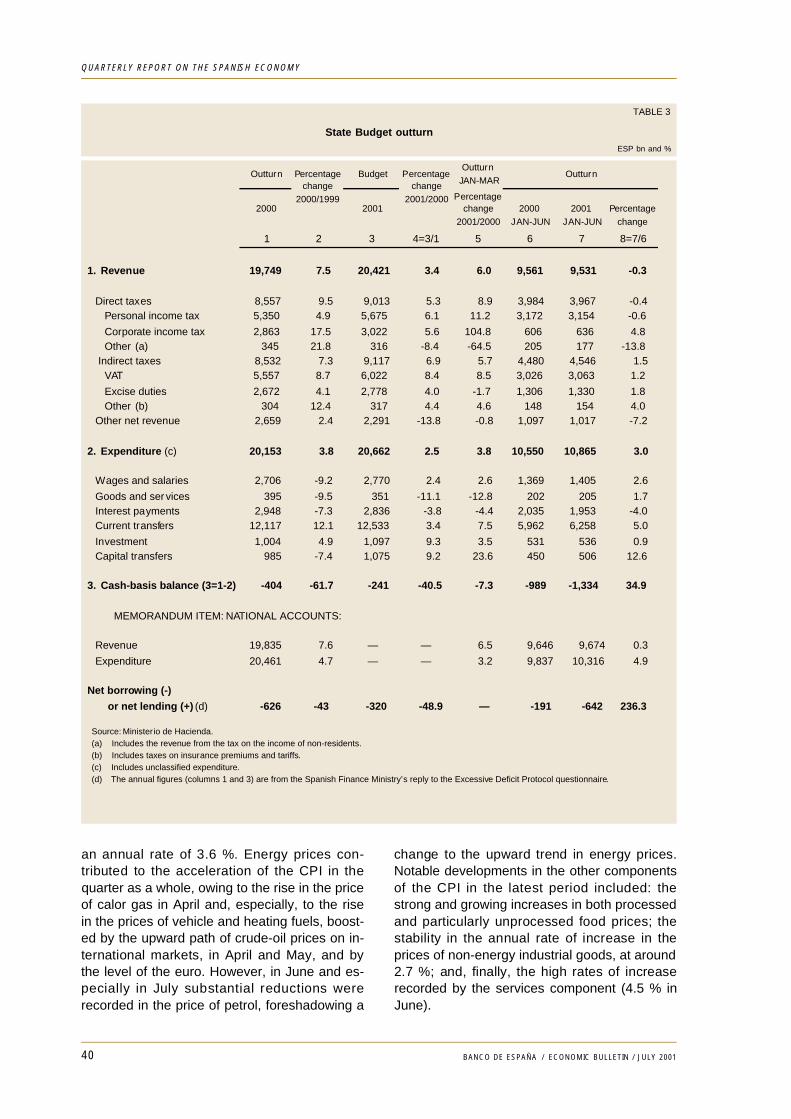

Turning to fiscal policy, the budgetary resultsfor the first half of the year reveal a slowdown intakings for certain taxes, in step with the courseof the economy. In some instances, however,

10

CHART 1

GDP

CHART 2

Harmonised indices of consumer prices

Sources : ECB, Instituto Nacional de Estadística and Banco de España. (a) Non-centred annual rate of change calculated on the basis of the trend-cycle series. (b) Non-centred annual rate of change calculated on the basis of the seasonally adjusted series.

0

1

2

3

4

5

1998 1999 2000 2001

0

1

2

3

4

5% %

SPAIN (a)

EURO AREA (b)

0

1

2

3

4

5

1998 1999 2000 2001

0

1

2

3

4

5% %

SPAIN

EURO AREA

Sources: Eurostat and European Central Bank.

QUARTERLY REPORT ON THE SPANISH ECONOMY

BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

they are the outcome of specific factors whichwill be corrected in the coming months. Such isthe case of the bringing forward of personal in-come tax refunds for excess tax paid in the year2000. Expenditure is broadly running to plan,and budgetary forecasts are expected to be metat the end of the year, assisted by the mostfavourable results in the social security ac-counts.

Against the international background andwithin the framework established by macroeco-nomic policies, the Spanish economy has sus-tained a high though diminishing real growthrate during the first half of the current year ledessentially by exports and investment in theconstruction sector. The slowdown in consumerspending has moderated and, in relative terms,has held at a more sustained pace, while in-vestment in capital goods has been the compo-nent most marked by the change in expecta-tions.

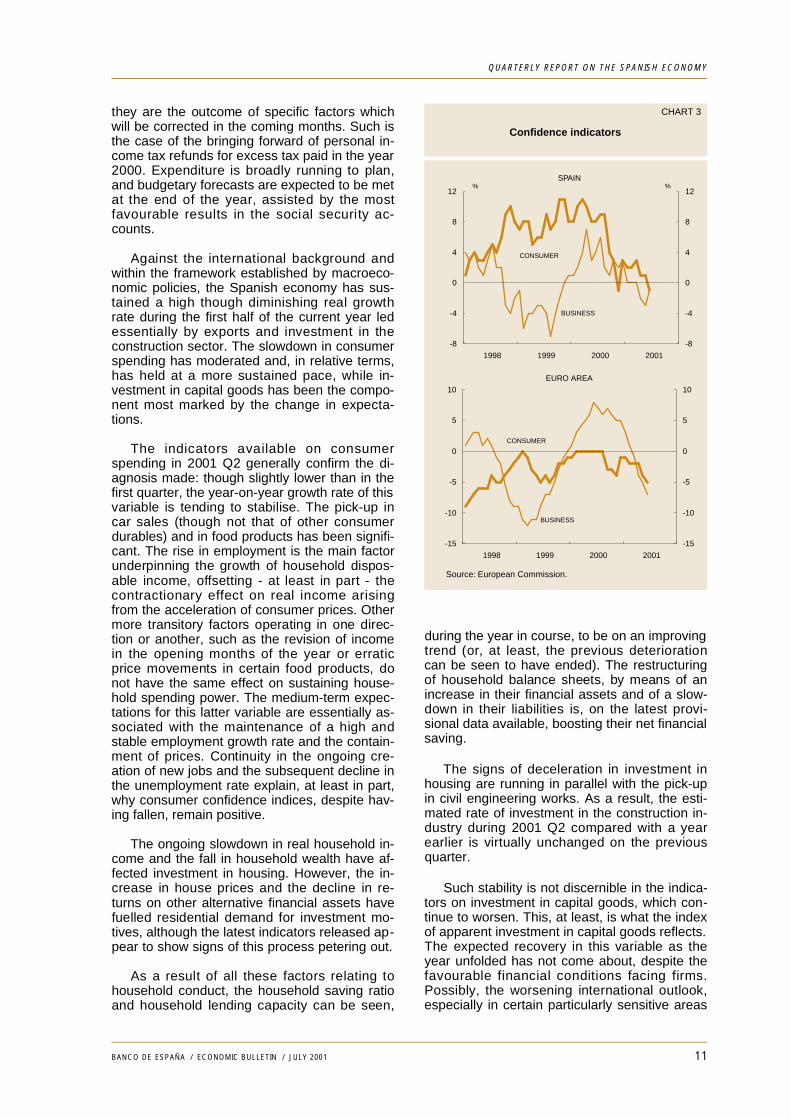

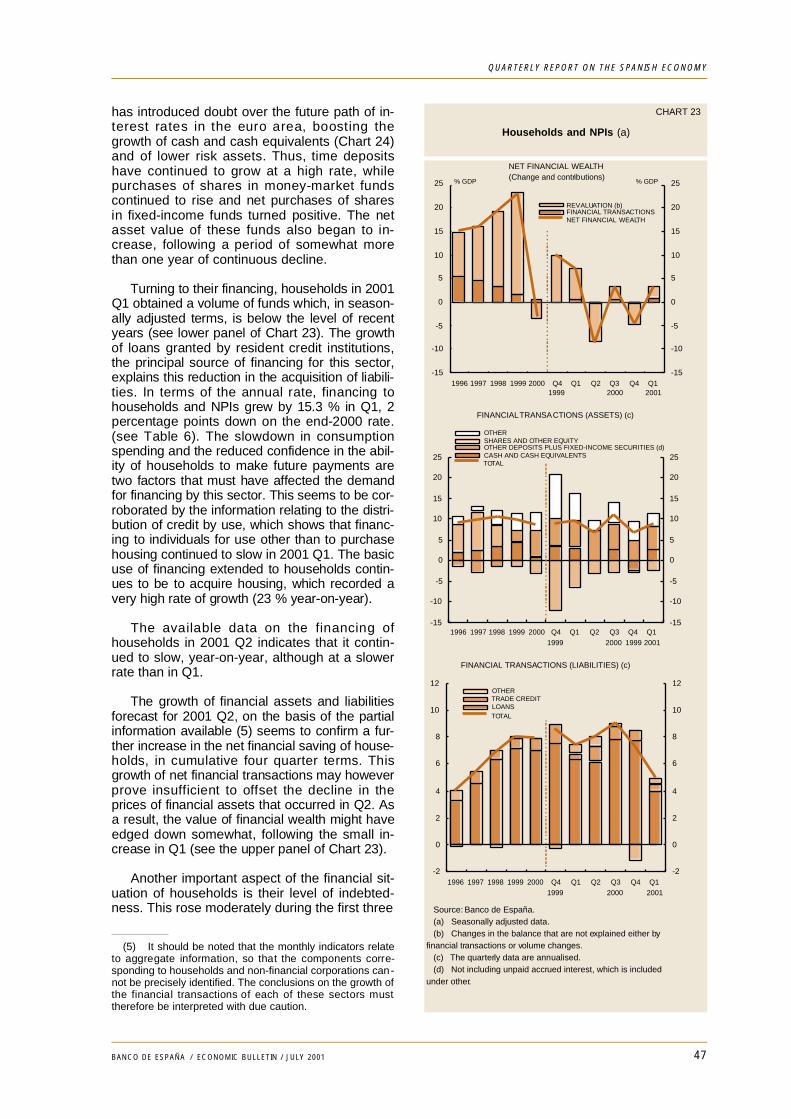

The indicators available on consumerspending in 2001 Q2 generally confirm the di-agnosis made: though slightly lower than in thefirst quarter, the year-on-year growth rate of thisvariable is tending to stabilise. The pick-up incar sales (though not that of other consumerdurables) and in food products has been signifi-cant. The rise in employment is the main factorunderpinning the growth of household dispos-able income, offsetting - at least in part - thecontractionary effect on real income arisingfrom the acceleration of consumer prices. Othermore transitory factors operating in one direc-tion or another, such as the revision of incomein the opening months of the year or erraticprice movements in certain food products, donot have the same effect on sustaining house-hold spending power. The medium-term expec-tations for this latter variable are essentially as-sociated with the maintenance of a high andstable employment growth rate and the contain-ment of prices. Continuity in the ongoing cre-ation of new jobs and the subsequent decline inthe unemployment rate explain, at least in part,why consumer confidence indices, despite hav-ing fallen, remain positive.

The ongoing slowdown in real household in-come and the fall in household wealth have af-fected investment in housing. However, the in-crease in house prices and the decline in re-turns on other alternative financial assets havefuelled residential demand for investment mo-tives, although the latest indicators released ap-pear to show signs of this process petering out.

As a result of all these factors relating tohousehold conduct, the household saving ratioand household lending capacity can be seen,

during the year in course, to be on an improvingtrend (or, at least, the previous deteriorationcan be seen to have ended). The restructuringof household balance sheets, by means of anincrease in their financial assets and of a slow-down in their liabilities is, on the latest provi-sional data available, boosting their net financialsaving.

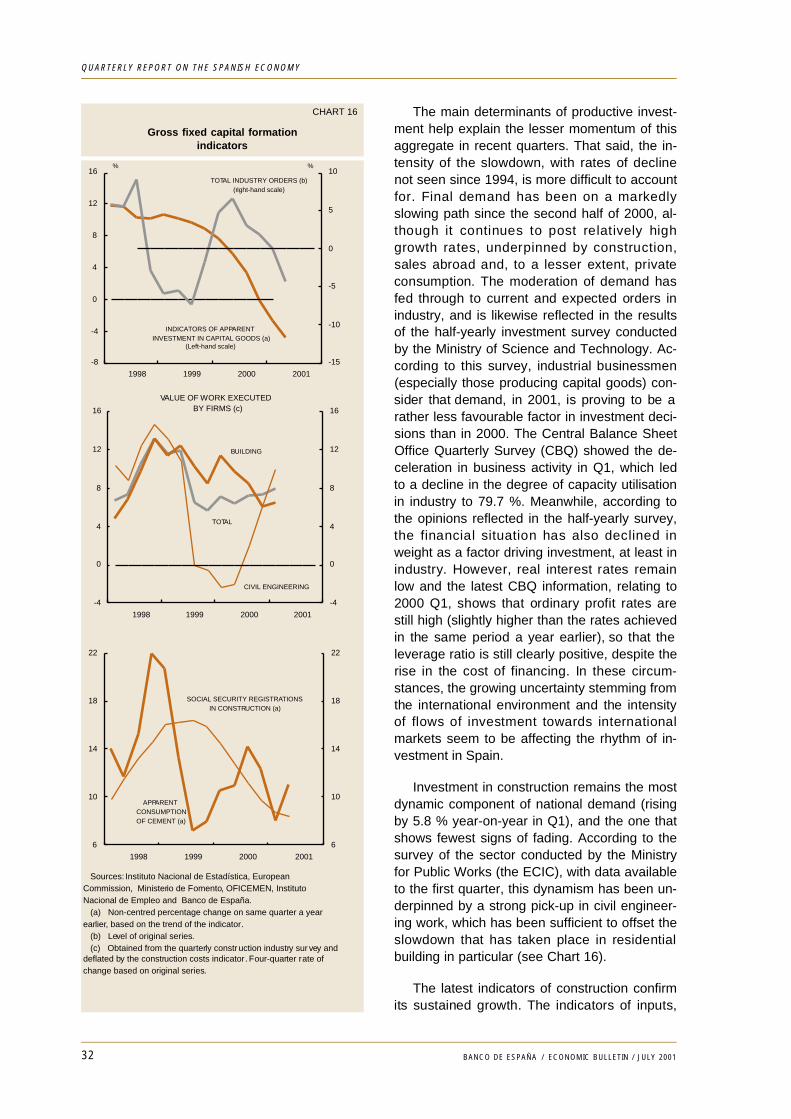

The signs of deceleration in investment inhousing are running in parallel with the pick-upin civil engineering works. As a result, the esti-mated rate of investment in the construction in-dustry during 2001 Q2 compared with a yearearlier is virtually unchanged on the previousquarter.

Such stability is not discernible in the indica-tors on investment in capital goods, which con-tinue to worsen. This, at least, is what the indexof apparent investment in capital goods reflects.The expected recovery in this variable as theyear unfolded has not come about, despite thefavourable financial conditions facing firms.Possibly, the worsening international outlook,especially in certain particularly sensitive areas

CHART 3

Confidence indicators

-8

-4

0

4

8

12

1998 1999 2000 2001

-8

-4

0

4

8

12

SPAIN% %

CONSUMER

BUSINESS

Source: European Commission.

-15

-10

-5

0

5

10

1998 1999 2000 2001

-15

-10

-5

0

5

10EURO AREA

BUSINESS

CONSUMER

QUARTERLY REPORT ON THE SPANISH ECONOMY

BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001 11

for Spanish companies, has put the start of thisprocess on hold.

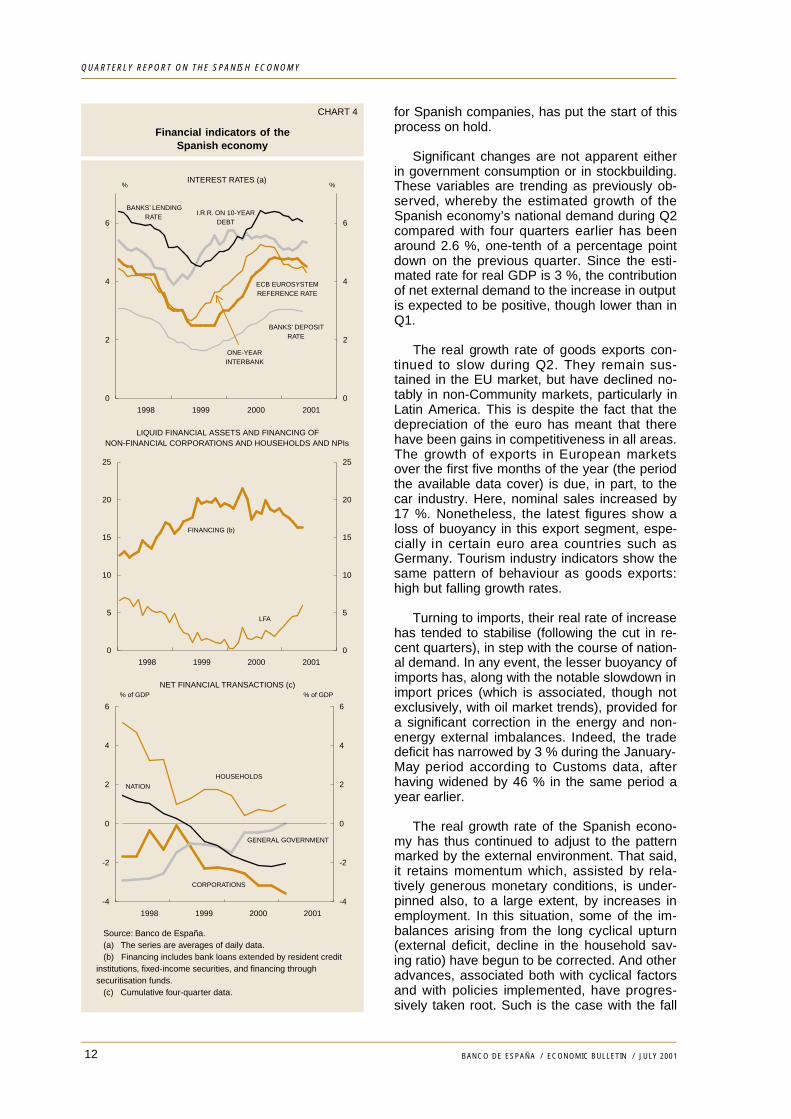

Significant changes are not apparent eitherin government consumption or in stockbuilding.These variables are trending as previously ob-served, whereby the estimated growth of theSpanish economy’s national demand during Q2compared with four quarters earlier has beenaround 2.6 %, one-tenth of a percentage pointdown on the previous quarter. Since the esti-mated rate for real GDP is 3 %, the contributionof net external demand to the increase in outputis expected to be positive, though lower than inQ1.

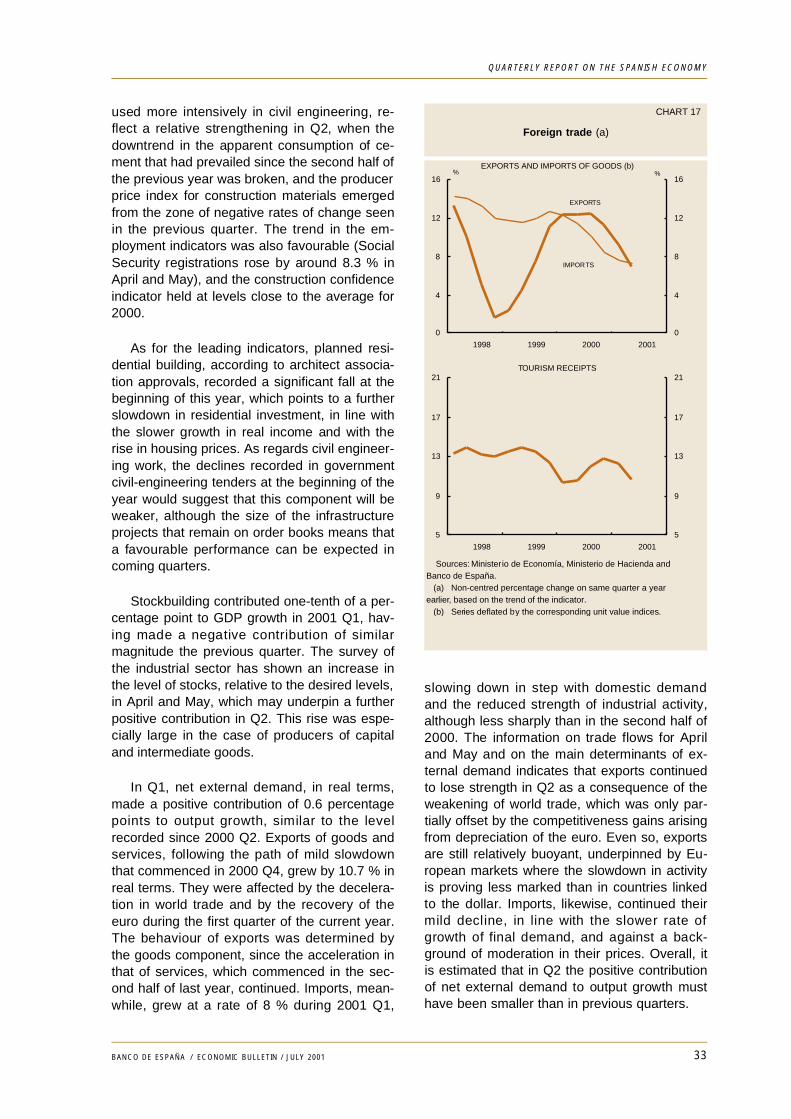

The real growth rate of goods exports con-tinued to slow during Q2. They remain sus-tained in the EU market, but have declined no-tably in non-Community markets, particularly inLatin America. This is despite the fact that thedepreciation of the euro has meant that therehave been gains in competitiveness in all areas.The growth of exports in European marketsover the first five months of the year (the periodthe available data cover) is due, in part, to thecar industry. Here, nominal sales increased by17 %. Nonetheless, the latest figures show aloss of buoyancy in this export segment, espe-cially in certain euro area countries such asGermany. Tourism industry indicators show thesame pattern of behaviour as goods exports:high but falling growth rates.

Turning to imports, their real rate of increasehas tended to stabilise (following the cut in re-cent quarters), in step with the course of nation-al demand. In any event, the lesser buoyancy ofimports has, along with the notable slowdown inimport prices (which is associated, though notexclusively, with oil market trends), provided fora significant correction in the energy and non-energy external imbalances. Indeed, the tradedeficit has narrowed by 3 % during the January-May period according to Customs data, afterhaving widened by 46 % in the same period ayear earlier.

The real growth rate of the Spanish econo-my has thus continued to adjust to the patternmarked by the external environment. That said,it retains momentum which, assisted by rela-tively generous monetary conditions, is under-pinned also, to a large extent, by increases inemployment. In this situation, some of the im-balances arising from the long cyclical upturn(external deficit, decline in the household sav-ing ratio) have begun to be corrected. And otheradvances, associated both with cyclical factorsand with policies implemented, have progres-sively taken root. Such is the case with the fall

12

CHART 4

Financial indicators of theSpanish economy

0

2

4

6

1998 1999 2000 2001

0

2

4

6

INTEREST RATES (a)%

ECB EUROSYSTEMREFERENCE RATE

ONE-YEAR INTERBANK

I.R.R. ON 10-YEARDEBT

BANKS’ LENDINGRATE

%

BANKS’ DEPOSITRATE

0

5

10

15

20

25

1998 1999 2000 2001

0

5

10

15

20

25

LIQUID FINANCIAL ASSETS AND FINANCING OFNON-FINANCIAL CORPORATIONS AND HOUSEHOLDS AND NPIs

FINANCING (b)

LFA

Source: Banco de España. (a) The series are averages of daily data. (b) Financing includes bank loans extended by resident credit institutions, fixed-income securities, and financing through securitisation funds. (c) Cumulative four-quarter data.

-4

-2

0

2

4

6

1998 1999 2000 2001

-4

-2

0

2

4

6

NET FINANCIAL TRANSACTIONS (c)% of GDP

NATION

% of GDP

HOUSEHOLDS

CORPORATIONS

GENERAL GOVERNMENT

QUARTERLY REPORT ON THE SPANISH ECONOMY

BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

in the unemployment rate and the headwaymade towards sound public finances.

The inflation rate, approximated by the be-haviour of the consumer price index (CPI) or bythe harmonised index of consumer prices(HICP), shows greater reluctance to slow, how-ever. This is partly because pressures on oilmarkets have persisted for longer than expect-ed and because of the rise in certain foodprices. Yet this inertia is also due to the storingup of inflationary pressures in certain productivesectors over recent years as a result of persis-tently high demand growth rates and the imper-fections of certain markets. Indeed, the lessvariable CPI components, namely services andnon-energy industrial goods, are maintaininghigh growth rates and persistent differentialswith the euro area countries. Temporary priceincreases have already begun to be strippedout (energy products are a case in point), butthis process must spread to the other CPI com-ponents so that the Spanish economy may re-sume a path of stability.

In this connection, a containment of labourcost growth dynamics and an improvement inthe efficiency of certain markets, where thegrowth of business margins is considerable,must be brought about. Wage increases duringthe current year are running high as a result ofthe combination of inflation-adjustment clauses

and wage bargaining where past - temporary -price increases are being built in. This curtailsthe dynamics of wage restraint that have char-acterised the recent upturn in the Spanisheconomy and that have been a key factor in therise in job creation capacity in recent years.

This process has proven most unevenacross the various productive branches, sincethe least competitive industries may passthrough labour cost increases to prices, retain-ing or even widening their operating margins.By contrast, the sectors most exposed to com-petition cannot do this, since the resulting loss-es in competitiveness would ultimately cancelout their growth capacity. In fact, the increase inbusiness surpluses in the economy as a whole,according to the latest available figures, areconcentrated essentially in the construction andenergy industries and in certain servicesbranches, but not in many industrial activities.

The desirability of improving the workings ofmarkets and containing the growth of labourcosts is thus based on the need to retain a pat-tern of job creation conducive to growth and in-vestment in the most dynamic and efficient in-dustries. Through gains in competitiveness, thiswill further enable the Spanish economy to con-tinue its process of real convergence, even un-der the less favourable conditions of the currentinternational environment.

13BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

2. The externalenvironment of the euroarea

The latest information on the external envi-ronment of the euro area shows, for 2001 Q2, areduction in the growth of the world economy.This is concurrent with the slowdown in theUnited States, deepening economic stagnationin Japan and a sharp decline in the growth ofmany emerging economies (especially in south-east Asia and, to a lesser extent, in Latin Amer-ica). Growth forecasts for 2001 have thus beenscaled back across the board and, although un-certainty over these forecasts remains high,there appear to be more downside than upsiderisks.

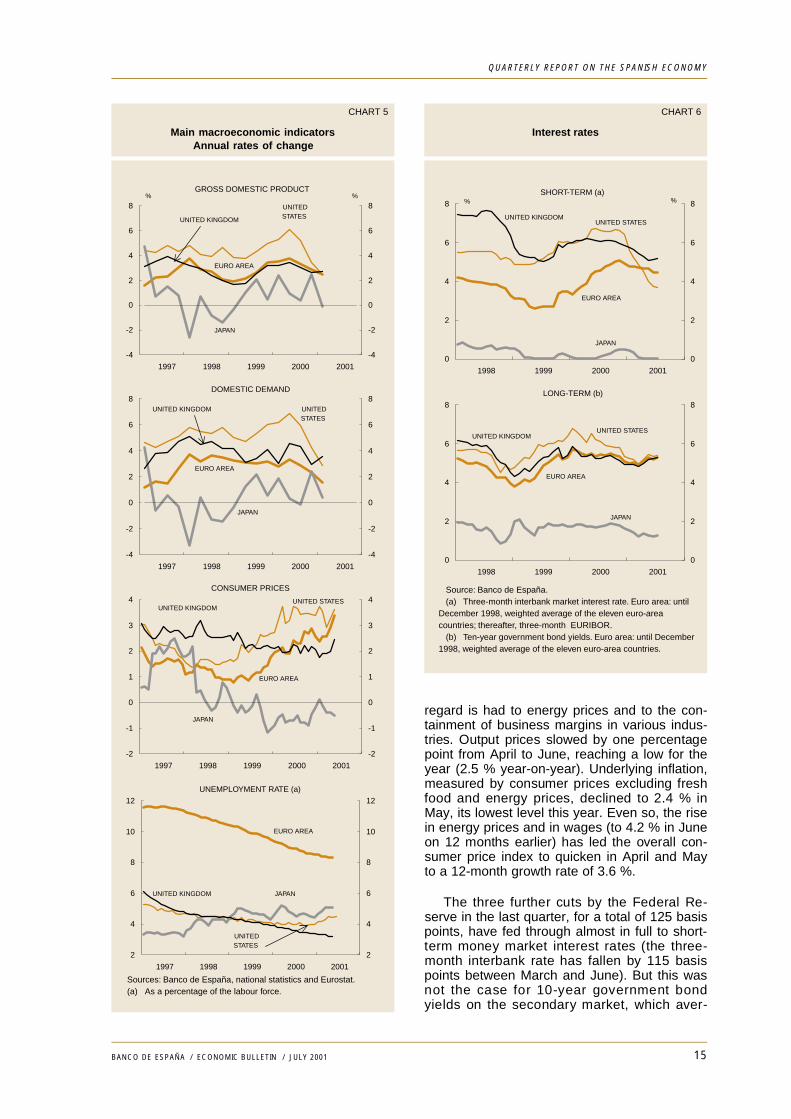

Inflation moderated slightly in most coun-tries, helped by the recent stabilisation of ener-gy prices. In the United States, the Federal Re-serve made three further official interest ratecuts during Q2 (making a total of six since thestart of the year), lowering the federal fundsrate to 3.75 %. In Japan, monetary policy hasbeen made more expansionary following thechange in strategy in March towards a bank re-serves target.

The revised US National Accounts data forQ1 showed annual ised quarterly growth of0.3 % for GDP. They also evidenced a less un-favourable performance by domestic demandthan initially expected, thanks to the resilienceof private consumption (whose quarterly growthwas revised upwards by one-tenth of a point to0.8 %). Private investment (especially that inthe capital goods and new technologies sec-tors) and exports evidenced the greatest weak-ness. The Q2 indicators generally show the per-sistence of sluggish economic activity, althoughthere are differing signals. Despite the factindustrial output posted fresh falls in Q2 com-pared with a year earlier, the NAPM index im-proved slightly in relation to the previous quar-ter. Private consumption remained fairly firm,judging by the positive year-on-year figures forretail sales throughout the quarter, the reduc-tion in the personal savings ratio as a percent-age of disposable income in the period to Mayand the improvement in the consumer confi-dence indicator in May and June. However, thelabour market continued to worsen, as seen inthe quarter-on-quarter fall in non-farm employ-ment and the rise in the unemployment rate to4.5 % in June. Investment demand improvedslightly in May, although it continued to run at avery negative rate in year-on-year terms.Across the various industries, orders continuedto be cut heavily in the new technologies sec-tors, as did earnings expectations, while con-struction industry indicators exhibited a positivetrend in April and May.

Inflation, despite the increase in the overallindex, gave relatively less cause for concern if

14 BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

regard is had to energy prices and to the con-tainment of business margins in various indus-tries. Output prices slowed by one percentagepoint from April to June, reaching a low for theyear (2.5 % year-on-year). Underlying inflation,measured by consumer prices excluding freshfood and energy prices, declined to 2.4 % inMay, its lowest level this year. Even so, the risein energy prices and in wages (to 4.2 % in Juneon 12 months earlier) has led the overall con-sumer price index to quicken in April and Mayto a 12-month growth rate of 3.6 %.

The three further cuts by the Federal Re-serve in the last quarter, for a total of 125 basispoints, have fed through almost in full to short-term money market interest rates (the three-month interbank rate has fallen by 115 basispoints between March and June). But this wasnot the case for 10-year government bondyields on the secondary market, which aver-

15BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

CHART 5

Main macroeconomic indicatorsAnnual rates of change

CHART 6

Interest rates

Sources: Banco de España, national statistics and Eurostat. (a) As a percentage of the labour force.

-2

-1

0

1

2

3

4

1997 1998 1999 2000 2001

-2

-1

0

1

2

3

4CONSUMER PRICES

EURO AREA

UNITED STATES

JAPAN

UNITED KINGDOM

2

4

6

8

10

12

1997 1998 1999 2000 2001

2

4

6

8

10

12UNEMPLOYMENT RATE (a)

EURO AREA

UNITED STATES

JAPANUNITED KINGDOM

-4

-2

0

2

4

6

8

1997 1998 1999 2000 2001

-4

-2

0

2

4

6

8UNITED KINGDOM UNITED

STATES

EURO AREA

JAPAN

DOMESTIC DEMAND

-4

-2

0

2

4

6

8

1997 1998 1999 2000 2001

-4

-2

0

2

4

6

8UNITED STATES

JAPAN

EURO AREA

UNITED KINGDOM

%%GROSS DOMESTIC PRODUCT

0

2

4

6

8

1998 1999 2000 2001

0

2

4

6

8

UNITED STATES

EURO AREA

JAPAN

UNITED KINGDOM

LONG-TERM (b)

0

2

4

6

8

1998 1999 2000 2001

0

2

4

6

8SHORT-TERM (a)

EURO AREA

UNITED STATES

JAPAN

UNITED KINGDOM

% %

Source: Banco de España. (a) Three-month interbank market interest rate. Euro area: until December 1998, weighted average of the eleven euro-area countries; thereafter, three-month EURIBOR. (b) Ten-year government bond yields. Euro area: until December 1998, weighted average of the eleven euro-area countries.

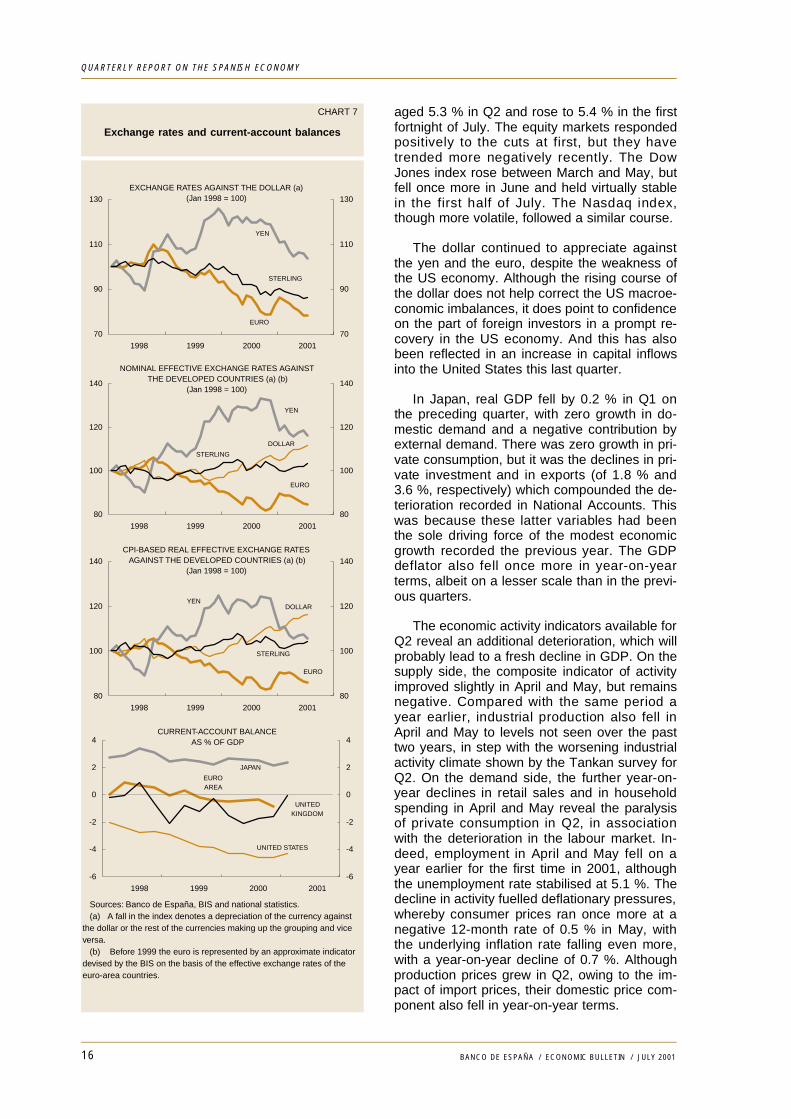

aged 5.3 % in Q2 and rose to 5.4 % in the firstfortnight of July. The equity markets respondedpositively to the cuts at first, but they havetrended more negatively recently. The DowJones index rose between March and May, butfell once more in June and held virtually stablein the first half of July. The Nasdaq index,though more volatile, followed a similar course.

The dollar continued to appreciate againstthe yen and the euro, despite the weakness ofthe US economy. Although the rising course ofthe dollar does not help correct the US macroe-conomic imbalances, it does point to confidenceon the part of foreign investors in a prompt re-covery in the US economy. And this has alsobeen reflected in an increase in capital inflowsinto the United States this last quarter.

In Japan, real GDP fell by 0.2 % in Q1 onthe preceding quarter, with zero growth in do-mestic demand and a negative contribution byexternal demand. There was zero growth in pri-vate consumption, but it was the declines in pri-vate investment and in exports (of 1.8 % and3.6 %, respectively) which compounded the de-terioration recorded in National Accounts. Thiswas because these latter variables had beenthe sole driving force of the modest economicgrowth recorded the previous year. The GDPdeflator also fell once more in year-on-yearterms, albeit on a lesser scale than in the previ-ous quarters.

The economic activity indicators available forQ2 reveal an additional deterioration, which willprobably lead to a fresh decline in GDP. On thesupply side, the composite indicator of activityimproved slightly in April and May, but remainsnegative. Compared with the same period ayear earlier, industrial production also fell inApril and May to levels not seen over the pasttwo years, in step with the worsening industrialactivity climate shown by the Tankan survey forQ2. On the demand side, the further year-on-year declines in retail sales and in householdspending in April and May reveal the paralysisof private consumption in Q2, in associationwith the deterioration in the labour market. In-deed, employment in April and May fell on ayear earlier for the first time in 2001, althoughthe unemployment rate stabilised at 5.1 %. Thedecline in activity fuelled deflationary pressures,whereby consumer prices ran once more at anegative 12-month rate of 0.5 % in May, withthe underlying inflation rate falling even more,with a year-on-year decline of 0.7 %. Althoughproduction prices grew in Q2, owing to the im-pact of import prices, their domestic price com-ponent also fell in year-on-year terms.

16 BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

CHART 7

Exchange rates and current-account balances

80

100

120

140

1998 1999 2000 2001

80

100

120

140

NOMINAL EFFECTIVE EXCHANGE RATES AGAINSTTHE DEVELOPED COUNTRIES (a) (b)

(Jan 1998 = 100)

DOLLAR

EURO

STERLING

YEN

70

90

110

130

1998 1999 2000 2001

70

90

110

130

YEN

EURO

STERLING

EXCHANGE RATES AGAINST THE DOLLAR (a)(Jan 1998 = 100)

80

100

120

140

1998 1999 2000 2001

80

100

120

140CPI-BASED REAL EFFECTIVE EXCHANGE RATES

AGAINST THE DEVELOPED COUNTRIES (a) (b)(Jan 1998 = 100)

DOLLAR

EURO

YEN

STERLING

-6

-4

-2

0

2

4

1998 1999 2000 2001

-6

-4

-2

0

2

4CURRENT-ACCOUNT BALANCE

AS % OF GDP

UNITED KINGDOM

JAPAN

UNITED STATES

EURO AREA

Sources: Banco de España, BIS and national statistics. (a) A fall in the index denotes a depreciation of the currency against the dollar or the rest of the currencies making up the grouping and vice versa. (b) Before 1999 the euro is represented by an approximate indicator devised by the BIS on the basis of the effective exchange rates of the euro-area countries.

Despite the falling trend of the yen againstthe dollar (which was interrupted only in Mayand which stepped up in the first half of July,taking the Japanese currency to an annual low),exports continued to fall due to the weakness offoreign demand. In the period to May this year,the trade and current-account surpluses werecut substantially.

Turning to monetary policy, the strategy initi-ated in March by the Bank of Japan to expandthe monetary base held short-term market inter-est rates at levels very close to zero and slightlyraised the year-on-year growth of the moneysupply (to 3.1 % in June, from 2.6 % in March).But it has not managed to extricate Japan fromdeflation, which was its implicit aim, and 10-year bond yields on the secondary market havenot picked up, having stabilised rather at 1.3 %.And nor has a bigger fall in private sector creditbeen averted (down 2.7 % in May on 12 monthsearlier). The equity market saw a rise in theNikkei index of 11 % in April, following the intro-duction of the new quantitative monetary policy.But it moved once more onto a clearly decliningtrend from May as the deterioration in the eco-nomic situation was confirmed.

In the EU countries not belonging to the euroarea, the United Kingdom saw an appreciableslowdown in economic activity during 2001 Q2,following growth of 2.7 % in Q1. Manufacturingoutput in particular declined in both April andMay on a year earlier. Since June, the slow-down in activity has spread to services, judgingby the reduction in the year-on-year growth ofretail sales and orders in this industry. The un-employment rate stabilised at 3.2 % in April andMay. In these two months inflation quickened,with the 12-month growth rate of the index mea-suring consumer prices rising to 2.4 % in May(from 1.9 % in March). This contributed to theBank of England not cutting rates, despite theeconomic slowdown. Market interest rates heldvirtually stable in the short term, while 10-yearbond yields on the secondary market rose mod-erately. The equity market has been on a fallingtrend since April.

The south-east Asian economies, exceptChina, proved particularly vulnerable to theslowdown in the growth of their external de-mand as from the beginning of the year (espe-

cially in the high technology industries, in whichmany of these countries have specialised), andthe process accelerated substantially duringQ2. Following the progressive decline in the ex-ports of most of these countries, and despitethe practically across-the-board depreciation oftheir currencies against the dollar, the pace ofactivity in the region diminished continuously.That has given rise to a marked and gener-alised downward revision of their growth fore-casts for the current year. Conversely, econom-ic growth in China during the first half of theyear (despite moderating exports) ran at almost8 % year-on-year, a similar rate to that recordedin the second half of last year. Against thisbackground, most of the countries in the regiontended to adopt looser monetary and -especial-ly- fiscal policies to counter slowing growth.

The slowdown in economic activity in LatinAmerica brought about slightly negative GDPgrowth in quarter-on-quarter terms in the areaas a whole. And judging by the data availablefor virtually all the economies in the area, thistrend appeared to accelerate in Q2. A key de-velopment is the exacerbation of the financialcrisis in Argentina following three years of re-cession. The Argentine public finances haveworsened substantially and there has beengrowing external fragility during the course ofQ2. The effects of this financial turbulence havespread discernibly to a good number of SouthAmerican economies, despite their differingoverall and financial circumstances. Brazil hasbeen most affected by the Argentine crisis, andits currency has depreciated sharply (21 %against the dollar so far this year to end-July).The response of the Brazilian authorities was toraise interest rates and step up intervention onthe foreign exchange markets. Chile, too, de-spite the prior soundness of its macroeconomicmagnitudes, is in an increasingly weak position,though it retains considerable scope for eco-nomic policy action in the short run. Finally,Mexico exhibited a marked dichotomy betweenthe current weakness of its domestic economicactivity (more affected than the above-men-tioned economies by the US slowdown) and thebuoyancy of its foreign investment inflows in re-cent months. Such inflows, unlike in most of thearea’s economies, have caused its currency toappreciate in the year to date.

17BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

3. The euro area and themonetary policy of theEuropean Central Bank

The latest data on economic developmentsin the euro area point to a slight reduction in thepace of GDP in 2001 Q2, thereby prolongingthe trend observed in the preceding quarters.The slowdown in activity has essentially comeabout due to the weakness of external demandand to the adverse real effects of two concur-rent supply shocks, namely the rise in oil pricesand the crisis in the food industry. The inflation-ary situation has been affected by these shocksand by the sizeable cumulative depreciation ofthe euro. Against this background, the ECB hasmaintained a cautious stance, based on a thor-ough evaluation of the real and monetary situa-tion and, in particular, of the economy’s infla-tionary outlook. The evaluation of these factorsled it to cut official interest rates moderately inmid-May by 25 basis points to 4.5 %.

3.1. Economic developments

According to the second National Accountsestimate, euro area GDP posted quarter-on-quarter growth of 0.6 % in 2001 Q1, a similarrate to the previous quarter. Taking a slightlylonger view, the rate of expansion of economicactivity can be seen to have lost steam; afterhaving averaged growth of around 3.5 % duringthe first half of 2000 on a year earlier, the ratedropped to 2.6 % in 2001 Q1, a similar figure tothat recorded in mid-1999 (see Chart 8).

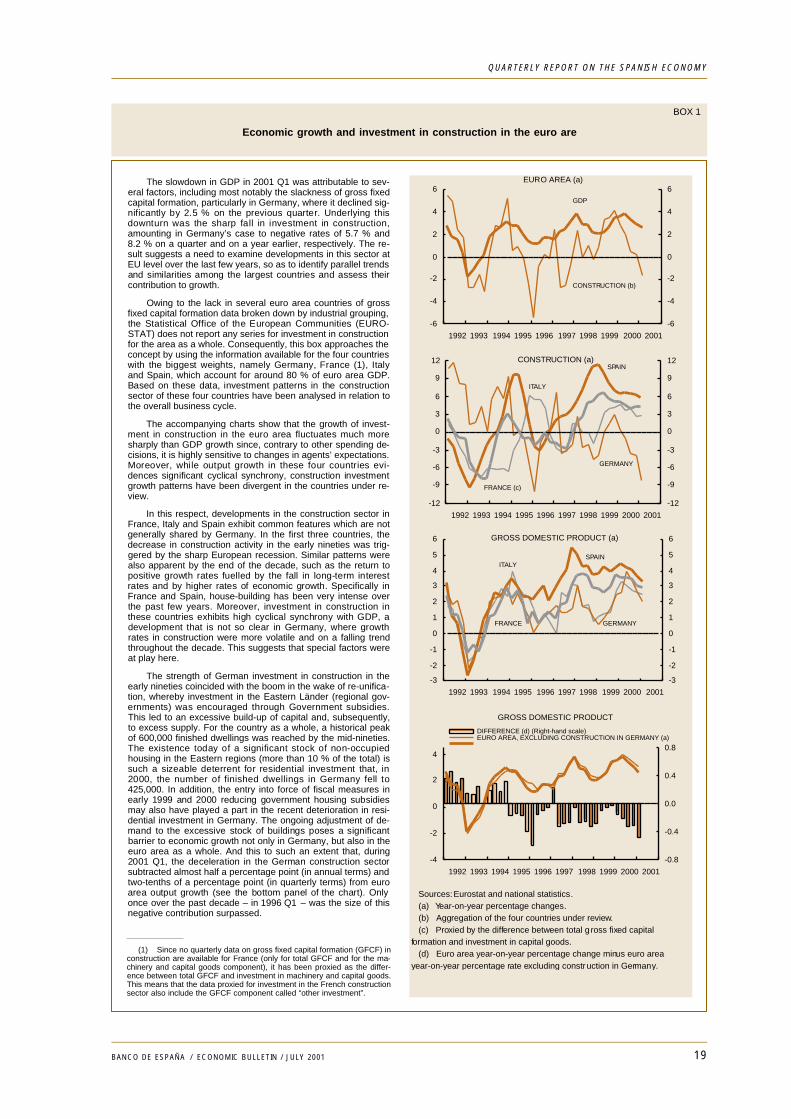

Underlying the stability of the quarterlygrowth rate of GDP is, however, a significantslowdown in final demand. This derives bothfrom the sluggishness of domestic demand andfrom exports, meaning the main driving force ofGDP growth is the notable containment of im-ports. The loss of momentum of final demandhas come about due to the erosion of real in-come caused by price increases and the slack-ness of foreign demand. And neither the contin-uing relative generosity of monetary and finan-cial conditions (which will be analysed ingreater detail in the following section) nor theexpansionary effects of the fiscal reforms ap-plied in certain countries have been able tocounter these factors. In Q1 this year privateconsumption grew by 0.4 %, one percentagepoint up on the previous quarter but less vigor-ous than in the first half of the year 2000. Gov-ernment consumption remained the most buoy-ant domestic demand component, though it wasless robust in Q1, having followed a slightlyslowing course since the second half of 2000.Gross fixed capital formation shrank notably (byalmost half a percentage point compared withthe previous quarter) due largely to the slack-ness of demand and to the favourable perfor-mance of construction investment in Germany(see Box 1). Finally, the marked 1.2 % decline

18 BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

19BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

BOX 1

Economic growth and investment in construction in the euro are

The slowdown in GDP in 2001 Q1 was attributable to sev-eral factors, including most notably the slackness of gross fixedcapital formation, particularly in Germany, where it declined sig-nificantly by 2.5 % on the previous quarter. Underlying thisdownturn was the sharp fall in investment in construction,amounting in Germany’s case to negative rates of 5.7 % and8.2 % on a quarter and on a year earlier, respectively. The re-sult suggests a need to examine developments in this sector atEU level over the last few years, so as to identify parallel trendsand similarities among the largest countries and assess theircontribution to growth.

Owing to the lack in several euro area countries of grossfixed capital formation data broken down by industrial grouping,the Statistical Office of the European Communities (EURO-STAT) does not report any series for investment in constructionfor the area as a whole. Consequently, this box approaches theconcept by using the information available for the four countrieswith the biggest weights, namely Germany, France (1), Italyand Spain, which account for around 80 % of euro area GDP.Based on these data, investment patterns in the constructionsector of these four countries have been analysed in relation tothe overall business cycle.

The accompanying charts show that the growth of invest-ment in construction in the euro area fluctuates much moresharply than GDP growth since, contrary to other spending de-cisions, it is highly sensitive to changes in agents’ expectations.Moreover, while output growth in these four countries evi-dences significant cyclical synchrony, construction investmentgrowth patterns have been divergent in the countries under re-view.

In this respect, developments in the construction sector inFrance, Italy and Spain exhibit common features which are notgenerally shared by Germany. In the first three countries, thedecrease in construction activity in the early nineties was trig-gered by the sharp European recession. Similar patterns werealso apparent by the end of the decade, such as the return topositive growth rates fuelled by the fall in long-term interestrates and by higher rates of economic growth. Specifically inFrance and Spain, house-building has been very intense overthe past few years. Moreover, investment in construction inthese countries exhibits high cyclical synchrony with GDP, adevelopment that is not so clear in Germany, where growthrates in construction were more volatile and on a falling trendthroughout the decade. This suggests that special factors wereat play here.

The strength of German investment in construction in theearly nineties coincided with the boom in the wake of re-unifica-tion, whereby investment in the Eastern Länder (regional gov-ernments) was encouraged through Government subsidies.This led to an excessive build-up of capital and, subsequently,to excess supply. For the country as a whole, a historical peakof 600,000 finished dwellings was reached by the mid-nineties.The existence today of a significant stock of non-occupiedhousing in the Eastern regions (more than 10 % of the total) issuch a sizeable deterrent for residential investment that, in2000, the number of finished dwellings in Germany fell to425,000. In addition, the entry into force of fiscal measures inearly 1999 and 2000 reducing government housing subsidiesmay also have played a part in the recent deterioration in resi-dential investment in Germany. The ongoing adjustment of de-mand to the excessive stock of buildings poses a significantbarrier to economic growth not only in Germany, but also in theeuro area as a whole. And this to such an extent that, during2001 Q1, the deceleration in the German construction sectorsubtracted almost half a percentage point (in annual terms) andtwo-tenths of a percentage point (in quarterly terms) from euroarea output growth (see the bottom panel of the chart). Onlyonce over the past decade – in 1996 Q1 – was the size of thisnegative contribution surpassed.

-6

-4

-2

0

2

4

6

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

-6

-4

-2

0

2

4

6EURO AREA (a)

CONSTRUCTION (b)

GDP

Sources: Eurostat and national statistics. (a) Year-on-year percentage changes. (b) Aggregation of the four countries under review. (c) Proxied by the difference between total g ross fixed capitalformation and investment in capital goods. (d) Euro area year-on-year percentage change minus euro areayear-on-year percentage rate excluding construction in Germany.

-12

-9

-6

-3

0

3

6

9

12

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

-12

-9

-6

-3

0

3

6

9

12

ITALY

CONSTRUCTION (a)

GERMANY

SPAIN

FRANCE (c)

-4

-2

0

2

4

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

-0.8

-0.4

0.0

0.4

0.8

DIFFERENCE (d) (Right-hand scale) EURO AREA, EXCLUDING CONSTRUCTION IN GERMANY (a)

GROSS DOMESTIC PRODUCT

-3

-2

-1

0

1

2

3

4

5

6

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

-3

-2

-1

0

1

2

3

4

5

6

ITALY

GROSS DOMESTIC PRODUCT (a)

GERMANY

SPAIN

FRANCE

(1) Since no quarterly data on gross fixed capital formation (GFCF) inconstruction are available for France (only for total GFCF and for the ma-chinery and capital goods component), it has been proxied as the differ-ence between total GFCF and investment in machinery and capital goods.This means that the data proxied for investment in the French constructionsector also include the GFCF component called “other investment”.

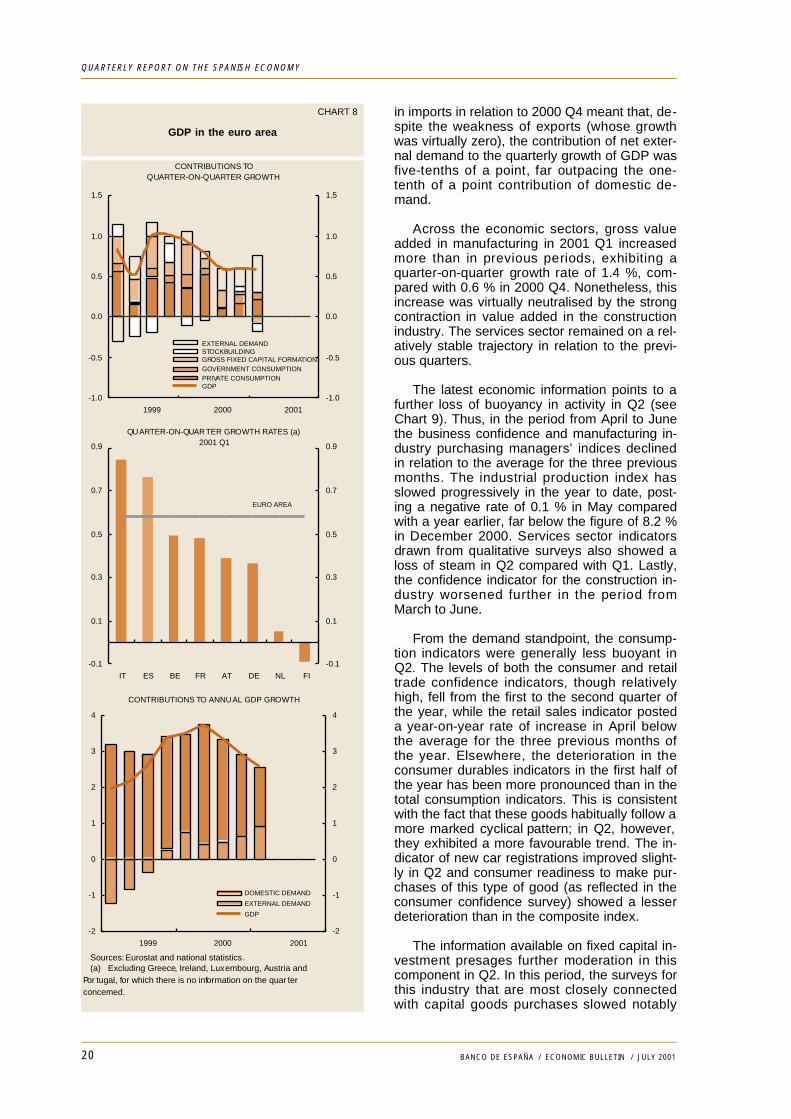

in imports in relation to 2000 Q4 meant that, de-spite the weakness of exports (whose growthwas virtually zero), the contribution of net exter-nal demand to the quarterly growth of GDP wasfive-tenths of a point, far outpacing the one-tenth of a point contribution of domestic de-mand.

Across the economic sectors, gross valueadded in manufacturing in 2001 Q1 increasedmore than in previous periods, exhibiting aquarter-on-quarter growth rate of 1.4 %, com-pared with 0.6 % in 2000 Q4. Nonetheless, thisincrease was virtually neutralised by the strongcontraction in value added in the constructionindustry. The services sector remained on a rel-atively stable trajectory in relation to the previ-ous quarters.

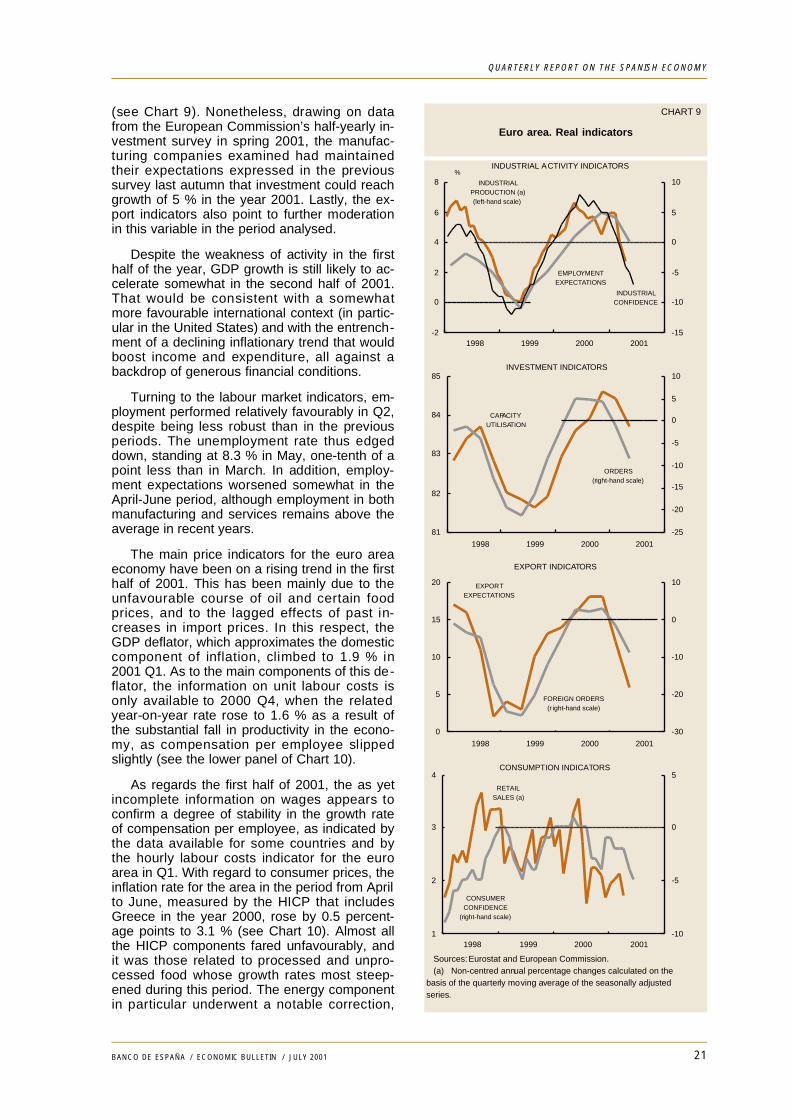

The latest economic information points to afurther loss of buoyancy in activity in Q2 (seeChart 9). Thus, in the period from April to Junethe business confidence and manufacturing in-dustry purchasing managers’ indices declinedin relation to the average for the three previousmonths. The industrial production index hasslowed progressively in the year to date, post-ing a negative rate of 0.1 % in May comparedwith a year earlier, far below the figure of 8.2 %in December 2000. Services sector indicatorsdrawn from qualitative surveys also showed aloss of steam in Q2 compared with Q1. Lastly,the confidence indicator for the construction in-dustry worsened further in the period fromMarch to June.

From the demand standpoint, the consump-tion indicators were generally less buoyant inQ2. The levels of both the consumer and retailtrade confidence indicators, though relativelyhigh, fell from the first to the second quarter ofthe year, while the retail sales indicator posteda year-on-year rate of increase in April belowthe average for the three previous months ofthe year. Elsewhere, the deterioration in theconsumer durables indicators in the first half ofthe year has been more pronounced than in thetotal consumption indicators. This is consistentwith the fact that these goods habitually follow amore marked cyclical pattern; in Q2, however,they exhibited a more favourable trend. The in-dicator of new car registrations improved slight-ly in Q2 and consumer readiness to make pur-chases of this type of good (as reflected in theconsumer confidence survey) showed a lesserdeterioration than in the composite index.

The information available on fixed capital in-vestment presages further moderation in thiscomponent in Q2. In this period, the surveys forthis industry that are most closely connectedwith capital goods purchases slowed notably

20 BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

CHART 8

GDP in the euro area

-0.1

0.1

0.3

0.5

0.7

0.9

IT ES BE FR AT DE NL FI

-0.1

0.1

0.3

0.5

0.7

0.9

QUARTER-ON-QUARTER GROWTH RATES (a)2001 Q1

EURO AREA

Sources: Eurostat and national statistics. (a) Excluding Greece, Ireland, Luxembourg, Austria andPor tugal, for which there is no information on the quar terconcerned.

-2

-1

0

1

2

3

4

1999 2000 2001

-2

-1

0

1

2

3

4

DOMESTIC DEMAND

EXTERNAL DEMAND

GDP

CONTRIBUTIONS TO ANNUAL GDP GROWTH

-1.0

-0.5

0.0

0.5

1.0

1.5

1999 2000 2001

-1.0

-0.5

0.0

0.5

1.0

1.5

EXTERNAL DEMAND STOCKBUILDING GROSS FIXED CAPITAL FORMATION. GOVERNMENT CONSUMPTION PRIVATE CONSUMPTION GDP

CONTRIBUTIONS TOQUARTER-ON-QUARTER GROWTH

21BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

(see Chart 9). Nonetheless, drawing on datafrom the European Commission’s half-yearly in-vestment survey in spring 2001, the manufac-turing companies examined had maintainedtheir expectations expressed in the previoussurvey last autumn that investment could reachgrowth of 5 % in the year 2001. Lastly, the ex-port indicators also point to further moderationin this variable in the period analysed.

Despite the weakness of activity in the firsthalf of the year, GDP growth is still likely to ac-celerate somewhat in the second half of 2001.That would be consistent with a somewhatmore favourable international context (in partic-ular in the United States) and with the entrench-ment of a declining inflationary trend that wouldboost income and expenditure, all against abackdrop of generous financial conditions.

Turning to the labour market indicators, em-ployment performed relatively favourably in Q2,despite being less robust than in the previousperiods. The unemployment rate thus edgeddown, standing at 8.3 % in May, one-tenth of apoint less than in March. In addition, employ-ment expectations worsened somewhat in theApril-June period, although employment in bothmanufacturing and services remains above theaverage in recent years.

The main price indicators for the euro areaeconomy have been on a rising trend in the firsthalf of 2001. This has been mainly due to theunfavourable course of oil and certain foodprices, and to the lagged effects of past in-creases in import prices. In this respect, theGDP deflator, which approximates the domesticcomponent of inflation, climbed to 1.9 % in2001 Q1. As to the main components of this de-flator, the information on unit labour costs isonly available to 2000 Q4, when the relatedyear-on-year rate rose to 1.6 % as a result ofthe substantial fall in productivity in the econo-my, as compensation per employee slippedslightly (see the lower panel of Chart 10).

As regards the first half of 2001, the as yetincomplete information on wages appears toconfirm a degree of stability in the growth rateof compensation per employee, as indicated bythe data available for some countries and bythe hourly labour costs indicator for the euroarea in Q1. With regard to consumer prices, theinflation rate for the area in the period from Aprilto June, measured by the HICP that includesGreece in the year 2000, rose by 0.5 percent-age points to 3.1 % (see Chart 10). Almost allthe HICP components fared unfavourably, andit was those related to processed and unpro-cessed food whose growth rates most steep-ened during this period. The energy componentin particular underwent a notable correction,

CHART 9

Euro area. Real indicators

81

82

83

84

85

1998 1999 2000 2001

-25

-20

-15

-10

-5

0

5

10

CAPACITYUTILISATION

ORDERS(right-hand scale)

INVESTMENT INDICATORS

Sources: Eurostat and European Commission. (a) Non-centred annual percentage changes calculated on thebasis of the quarterly moving average of the seasonally adjustedseries.

0

5

10

15

20

1998 1999 2000 2001

-30

-20

-10

0

10

FOREIGN ORDERS(r ight-hand scale)

EXPORTEXPECTATIONS

EXPORT INDICATORS

1

2

3

4

1998 1999 2000 2001-10

-5

0

5

CONSUMERCONFIDENCE

(right-hand scale)

RETAILSALES (a)

CONSUMPTION INDICATORS

-2

0

2

4

6

8

1998 1999 2000 2001-15

-10

-5

0

5

10

INDUSTRIAL ACTIVITY INDICATORS

EMPLOYMENTEXPECTATIONS

INDUSTRIALPRODUCTION (a)(left-hand scale)

INDUSTRIALCONFIDENCE

%

22 BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

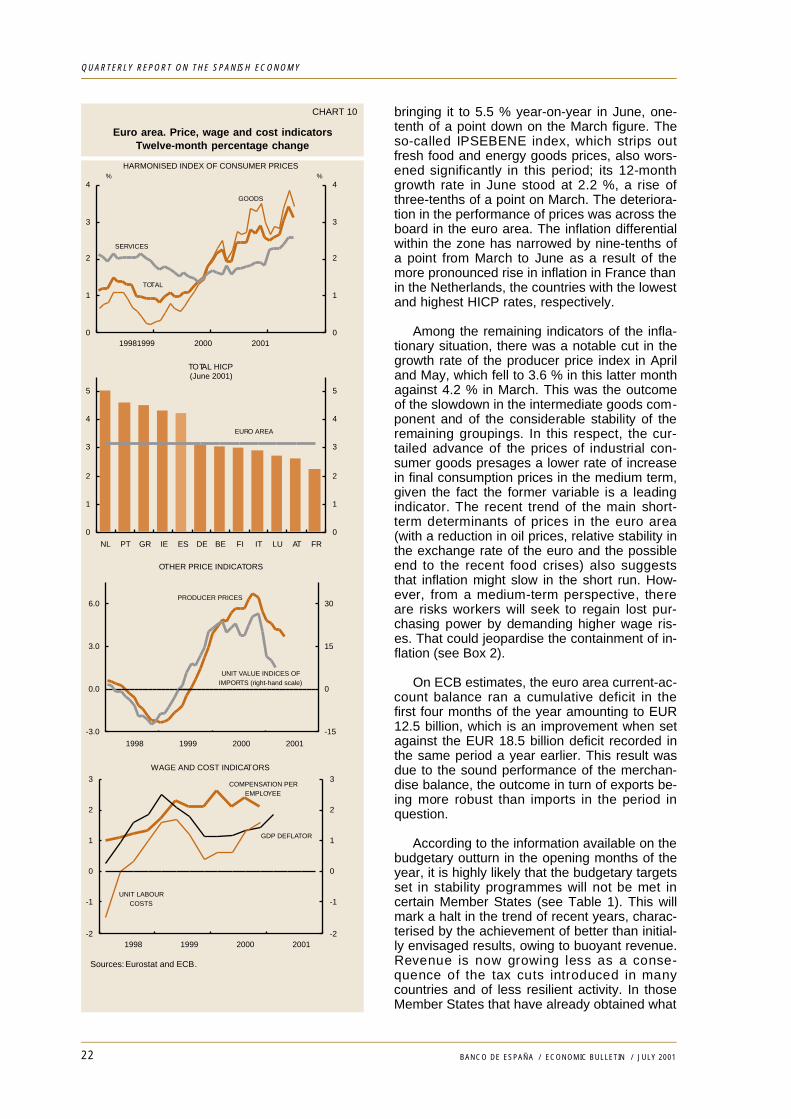

bringing it to 5.5 % year-on-year in June, one-tenth of a point down on the March figure. Theso-called IPSEBENE index, which strips outfresh food and energy goods prices, also wors-ened significantly in this period; its 12-monthgrowth rate in June stood at 2.2 %, a rise ofthree-tenths of a point on March. The deteriora-tion in the performance of prices was across theboard in the euro area. The inflation differentialwithin the zone has narrowed by nine-tenths ofa point from March to June as a result of themore pronounced rise in inflation in France thanin the Netherlands, the countries with the lowestand highest HICP rates, respectively.

Among the remaining indicators of the infla-tionary situation, there was a notable cut in thegrowth rate of the producer price index in Apriland May, which fell to 3.6 % in this latter monthagainst 4.2 % in March. This was the outcomeof the slowdown in the intermediate goods com-ponent and of the considerable stability of theremaining groupings. In this respect, the cur-tailed advance of the prices of industrial con-sumer goods presages a lower rate of increasein final consumption prices in the medium term,given the fact the former variable is a leadingindicator. The recent trend of the main short-term determinants of prices in the euro area(with a reduction in oil prices, relative stability inthe exchange rate of the euro and the possibleend to the recent food crises) also suggeststhat inflation might slow in the short run. How-ever, from a medium-term perspective, thereare risks workers will seek to regain lost pur-chasing power by demanding higher wage ris-es. That could jeopardise the containment of in-flation (see Box 2).

On ECB estimates, the euro area current-ac-count balance ran a cumulative deficit in thefirst four months of the year amounting to EUR12.5 billion, which is an improvement when setagainst the EUR 18.5 billion deficit recorded inthe same period a year earlier. This result wasdue to the sound performance of the merchan-dise balance, the outcome in turn of exports be-ing more robust than imports in the period inquestion.

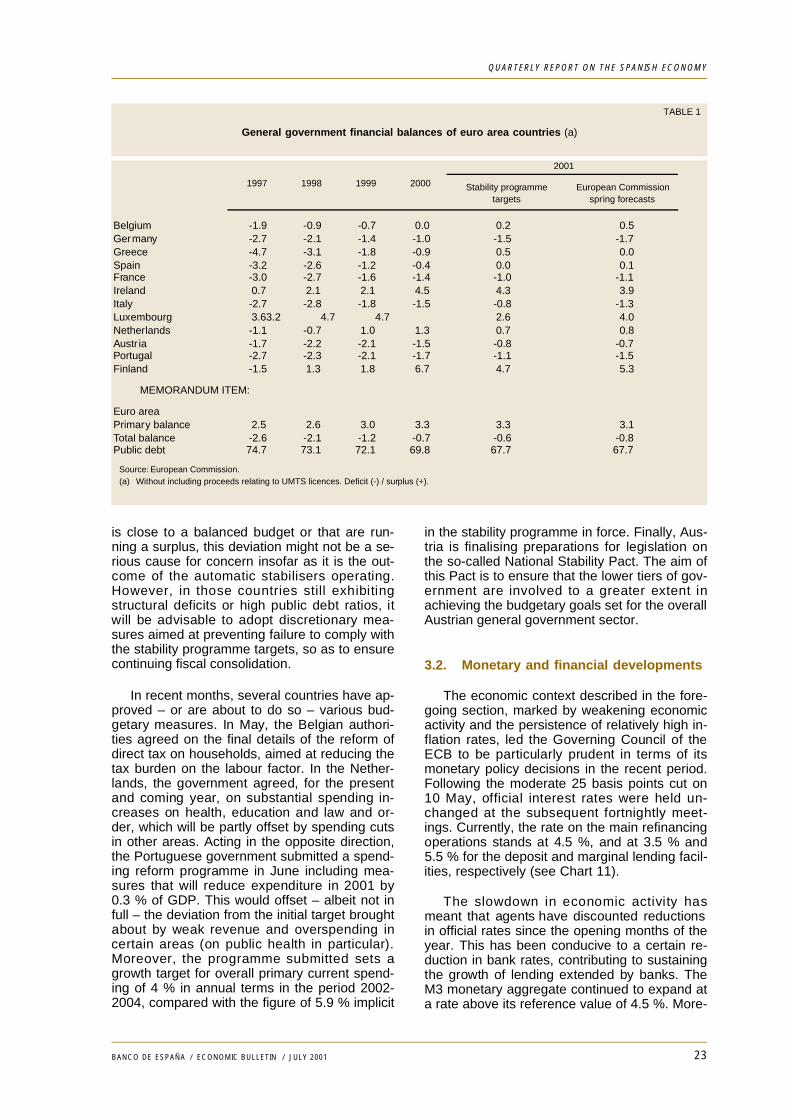

According to the information available on thebudgetary outturn in the opening months of theyear, it is highly likely that the budgetary targetsset in stability programmes will not be met incertain Member States (see Table 1). This willmark a halt in the trend of recent years, charac-terised by the achievement of better than initial-ly envisaged results, owing to buoyant revenue.Revenue is now growing less as a conse-quence of the tax cuts introduced in manycountries and of less resilient activity. In thoseMember States that have already obtained what

CHART 10

Euro area. Price, wage and cost indicatorsTwelve-month percentage change

Sources: Eurostat and ECB.

0

1

2

3

4

1998 1999 2000 20010

1

2

3

4

HARMONISED INDEX OF CONSUMER PRICES%

TOTAL

GOODS

SERVICES

%

0

1

2

3

4

5

NL PT GR IE ES DE BE FI IT LU AT FR

0

1

2

3

4

5

TOTAL HICP(June 2001)

EURO AREA

-3.0

0.0

3.0

6.0

1998 1999 2000 2001

-15

0

15

30

UNIT VALUE INDICES OFIMPORTS (right-hand scale)

OTHER PRICE INDICATORS

PRODUCER PRICES

-2

-1

0

1

2

3

1998 1999 2000 2001-2

-1

0

1

2

3

UNIT LABOURCOSTS

COMPENSATION PEREMPLOYEE

GDP DEFLATOR

WAGE AND COST INDICATORS

23BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

is close to a balanced budget or that are run-ning a surplus, this deviation might not be a se-rious cause for concern insofar as it is the out-come of the automatic stabilisers operating.However, in those countries still exhibitingstructural deficits or high public debt ratios, itwill be advisable to adopt discretionary mea-sures aimed at preventing failure to comply withthe stability programme targets, so as to ensurecontinuing fiscal consolidation.

In recent months, several countries have ap-proved – or are about to do so – various bud-getary measures. In May, the Belgian authori-ties agreed on the final details of the reform ofdirect tax on households, aimed at reducing thetax burden on the labour factor. In the Nether-lands, the government agreed, for the presentand coming year, on substantial spending in-creases on health, education and law and or-der, which will be partly offset by spending cutsin other areas. Acting in the opposite direction,the Portuguese government submitted a spend-ing reform programme in June including mea-sures that will reduce expenditure in 2001 by0.3 % of GDP. This would offset – albeit not infull – the deviation from the initial target broughtabout by weak revenue and overspending incertain areas (on public health in particular).Moreover, the programme submitted sets agrowth target for overall primary current spend-ing of 4 % in annual terms in the period 2002-2004, compared with the figure of 5.9 % implicit

in the stability programme in force. Finally, Aus-tria is finalising preparations for legislation onthe so-called National Stability Pact. The aim ofthis Pact is to ensure that the lower tiers of gov-ernment are involved to a greater extent inachieving the budgetary goals set for the overallAustrian general government sector.

3.2. Monetary and financial developments

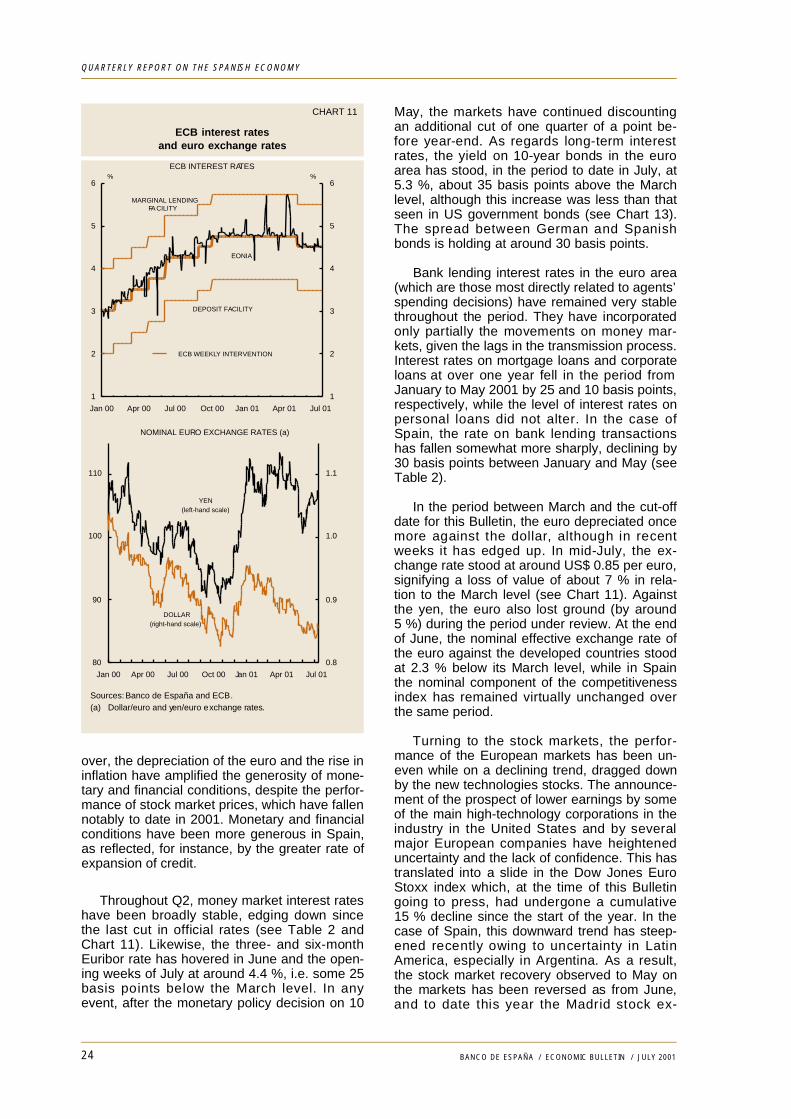

The economic context described in the fore-going section, marked by weakening economicactivity and the persistence of relatively high in-flation rates, led the Governing Council of theECB to be particularly prudent in terms of itsmonetary policy decisions in the recent period.Following the moderate 25 basis points cut on10 May, official interest rates were held un-changed at the subsequent fortnightly meet-ings. Currently, the rate on the main refinancingoperations stands at 4.5 %, and at 3.5 % and5.5 % for the deposit and marginal lending facil-ities, respectively (see Chart 11).

The slowdown in economic activity hasmeant that agents have discounted reductionsin official rates since the opening months of theyear. This has been conducive to a certain re-duction in bank rates, contributing to sustainingthe growth of lending extended by banks. TheM3 monetary aggregate continued to expand ata rate above its reference value of 4.5 %. More-

TABLE 1

General government financial balances of euro area countries (a)

Belgium -1.9 -0.9 -0.7 0.0 0.2 0.5Germany -2.7 -2.1 -1.4 -1.0 -1.5 -1.7Greece -4.7 -3.1 -1.8 -0.9 0.5 0.0Spain -3.2 -2.6 -1.2 -0.4 0.0 0.1France -3.0 -2.7 -1.6 -1.4 -1.0 -1.1Ireland 0.7 2.1 2.1 4.5 4.3 3.9Italy -2.7 -2.8 -1.8 -1.5 -0.8 -1.3Luxembourg 3.6 3.2 4.7 4.7 2.6 4.0Netherlands -1.1 -0.7 1.0 1.3 0.7 0.8Austr ia -1.7 -2.2 -2.1 -1.5 -0.8 -0.7Portugal -2.7 -2.3 -2.1 -1.7 -1.1 -1.5Finland -1.5 1.3 1.8 6.7 4.7 5.3

MEMORANDUM ITEM:

Euro areaPrimary balance 2.5 2.6 3.0 3.3 3.3 3.1Total balance -2.6 -2.1 -1.2 -0.7 -0.6 -0.8Public debt 74.7 73.1 72.1 69.8 67.7 67.7

2001

Stability programmetargets

European Commissionspring forecasts

1997 1998 1999 2000

Source: European Commission. (a) Without including proceeds relating to UMTS licences. Deficit (-) / surplus (+).

24 BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

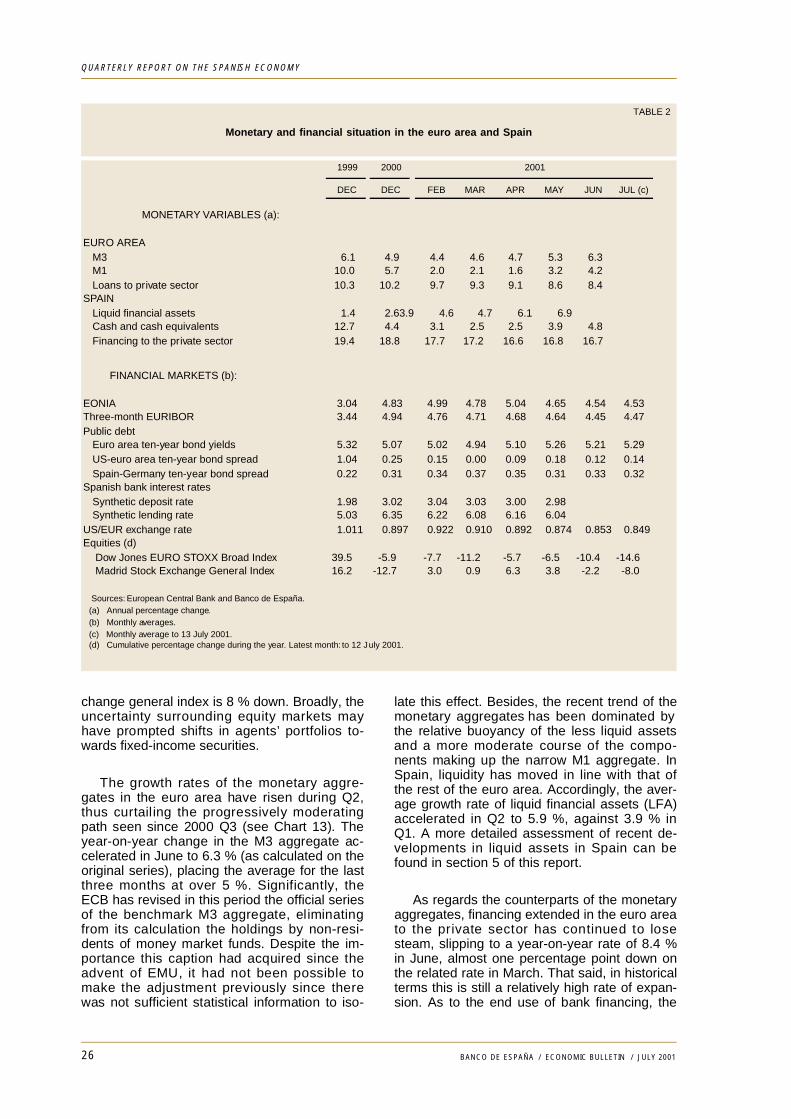

over, the depreciation of the euro and the rise ininflation have amplified the generosity of mone-tary and financial conditions, despite the perfor-mance of stock market prices, which have fallennotably to date in 2001. Monetary and financialconditions have been more generous in Spain,as reflected, for instance, by the greater rate ofexpansion of credit.

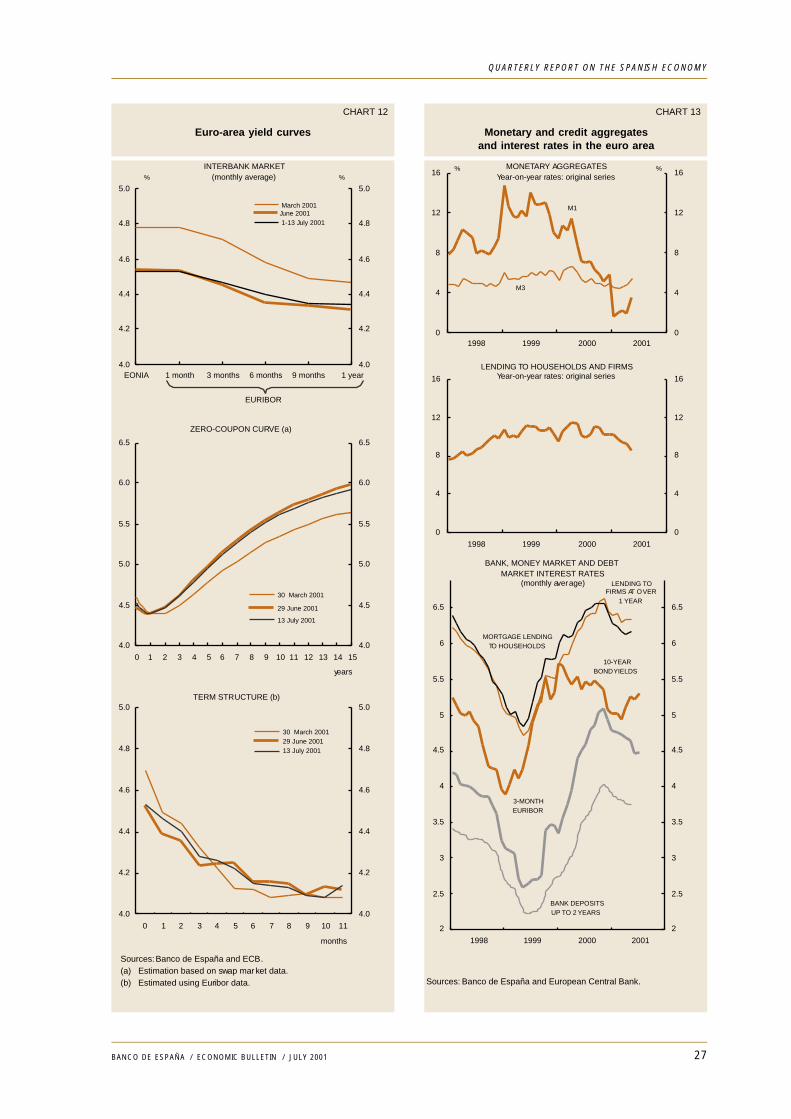

Throughout Q2, money market interest rateshave been broadly stable, edging down sincethe last cut in official rates (see Table 2 andChart 11). Likewise, the three- and six-monthEuribor rate has hovered in June and the open-ing weeks of July at around 4.4 %, i.e. some 25basis points below the March level. In anyevent, after the monetary policy decision on 10

May, the markets have continued discountingan additional cut of one quarter of a point be-fore year-end. As regards long-term interestrates, the yield on 10-year bonds in the euroarea has stood, in the period to date in July, at5.3 %, about 35 basis points above the Marchlevel, although this increase was less than thatseen in US government bonds (see Chart 13).The spread between German and Spanishbonds is holding at around 30 basis points.

Bank lending interest rates in the euro area(which are those most directly related to agents’spending decisions) have remained very stablethroughout the period. They have incorporatedonly partially the movements on money mar-kets, given the lags in the transmission process.Interest rates on mortgage loans and corporateloans at over one year fell in the period fromJanuary to May 2001 by 25 and 10 basis points,respectively, while the level of interest rates onpersonal loans did not alter. In the case ofSpain, the rate on bank lending transactionshas fallen somewhat more sharply, declining by30 basis points between January and May (seeTable 2).

In the period between March and the cut-offdate for this Bulletin, the euro depreciated oncemore against the dollar, although in recentweeks it has edged up. In mid-July, the ex-change rate stood at around US$ 0.85 per euro,signifying a loss of value of about 7 % in rela-tion to the March level (see Chart 11). Againstthe yen, the euro also lost ground (by around5 %) during the period under review. At the endof June, the nominal effective exchange rate ofthe euro against the developed countries stoodat 2.3 % below its March level, while in Spainthe nominal component of the competitivenessindex has remained virtually unchanged overthe same period.

Turning to the stock markets, the perfor-mance of the European markets has been un-even while on a declining trend, dragged downby the new technologies stocks. The announce-ment of the prospect of lower earnings by someof the main high-technology corporations in theindustry in the United States and by severalmajor European companies have heighteneduncertainty and the lack of confidence. This hastranslated into a slide in the Dow Jones EuroStoxx index which, at the time of this Bulletingoing to press, had undergone a cumulative15 % decline since the start of the year. In thecase of Spain, this downward trend has steep-ened recently owing to uncertainty in LatinAmerica, especially in Argentina. As a result,the stock market recovery observed to May onthe markets has been reversed as from June,and to date this year the Madrid stock ex-

CHART 11

ECB interest ratesand euro exchange rates

1

2

3

4

5

6

Jan 00 Apr 00 Jul 00 Oct 00 Jan 01 Apr 01 Jul 01

1

2

3

4

5

6

DEPOSIT FACILITY

MARGINAL LENDINGFACILITY

% %

ECB INTEREST RATES

EONIA

ECB WEEKLY INTERVENTION

Sources: Banco de España and ECB. (a) Dollar/euro and yen/euro exchange rates.

80

90

100

110

Jan 00 Apr 00 Jul 00 Oct 00 Jan 01 Apr 01 Jul 01

0.8

0.9

1.0

1.1

YEN(left-hand scale)

DOLLAR(right-hand scale)

NOMINAL EURO EXCHANGE RATES (a)

25BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

BOX 2

Surveys and inflation expectations in the euro area

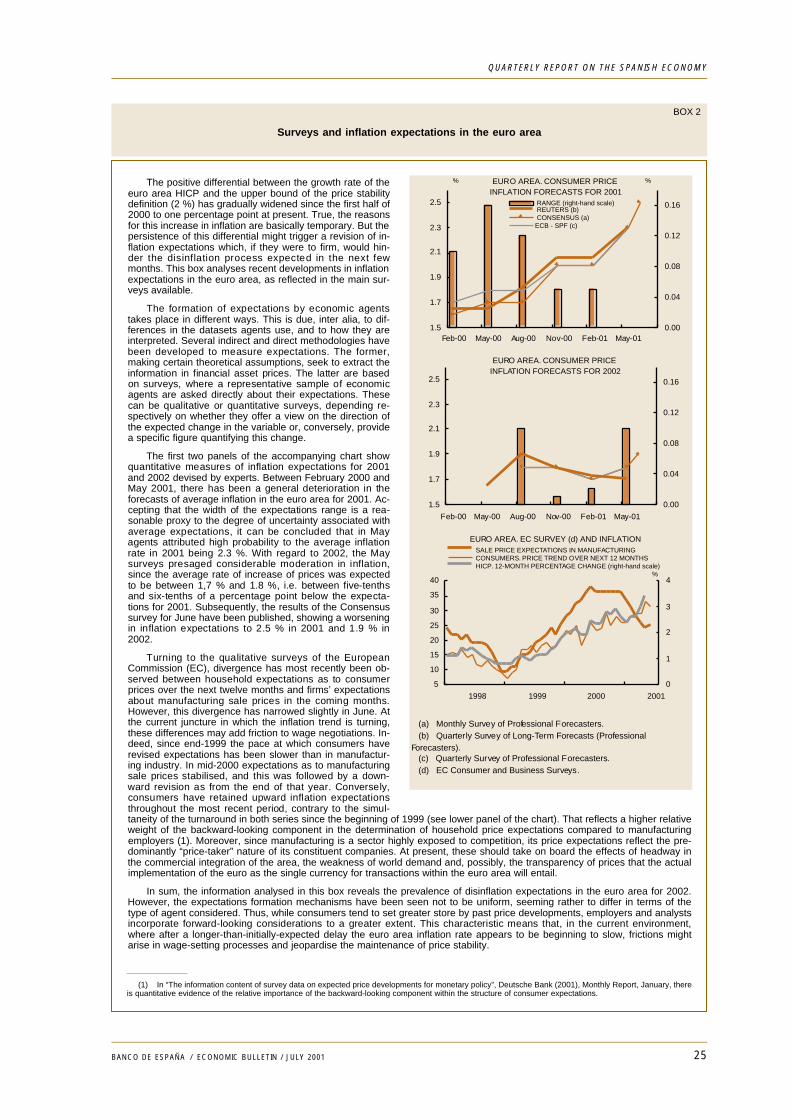

The positive differential between the growth rate of theeuro area HICP and the upper bound of the price stabilitydefinition (2 %) has gradually widened since the first half of2000 to one percentage point at present. True, the reasonsfor this increase in inflation are basically temporary. But thepersistence of this differential might trigger a revision of in-flation expectations which, if they were to firm, would hin-der the disinflation process expected in the next fewmonths. This box analyses recent developments in inflationexpectations in the euro area, as reflected in the main sur-veys available.

The formation of expectations by economic agentstakes place in different ways. This is due, inter alia, to dif-ferences in the datasets agents use, and to how they areinterpreted. Several indirect and direct methodologies havebeen developed to measure expectations. The former,making certain theoretical assumptions, seek to extract theinformation in financial asset prices. The latter are basedon surveys, where a representative sample of economicagents are asked directly about their expectations. Thesecan be qualitative or quantitative surveys, depending re-spectively on whether they offer a view on the direction ofthe expected change in the variable or, conversely, providea specific figure quantifying this change.

The first two panels of the accompanying chart showquantitative measures of inflation expectations for 2001and 2002 devised by experts. Between February 2000 andMay 2001, there has been a general deterioration in theforecasts of average inflation in the euro area for 2001. Ac-cepting that the width of the expectations range is a rea-sonable proxy to the degree of uncertainty associated withaverage expectations, it can be concluded that in Mayagents attributed high probability to the average inflationrate in 2001 being 2.3 %. With regard to 2002, the Maysurveys presaged considerable moderation in inflation,since the average rate of increase of prices was expectedto be between 1,7 % and 1.8 %, i.e. between five-tenthsand six-tenths of a percentage point below the expecta-tions for 2001. Subsequently, the results of the Consensussurvey for June have been published, showing a worseningin inflation expectations to 2.5 % in 2001 and 1.9 % in2002.

Turning to the qualitative surveys of the EuropeanCommission (EC), divergence has most recently been ob-served between household expectations as to consumerprices over the next twelve months and firms’ expectationsabout manufacturing sale prices in the coming months.However, this divergence has narrowed slightly in June. Atthe current juncture in which the inflation trend is turning,these differences may add friction to wage negotiations. In-deed, since end-1999 the pace at which consumers haverevised expectations has been slower than in manufactur-ing industry. In mid-2000 expectations as to manufacturingsale prices stabilised, and this was followed by a down-ward revision as from the end of that year. Conversely,consumers have retained upward inflation expectationsthroughout the most recent period, contrary to the simul-taneity of the turnaround in both series since the beginning of 1999 (see lower panel of the chart). That reflects a higher relativeweight of the backward-looking component in the determination of household price expectations compared to manufacturingemployers (1). Moreover, since manufacturing is a sector highly exposed to competition, its price expectations reflect the pre-dominantly “price-taker” nature of its constituent companies. At present, these should take on board the effects of headway inthe commercial integration of the area, the weakness of world demand and, possibly, the transparency of prices that the actualimplementation of the euro as the single currency for transactions within the euro area will entail.

In sum, the information analysed in this box reveals the prevalence of disinflation expectations in the euro area for 2002.However, the expectations formation mechanisms have been seen not to be uniform, seeming rather to differ in terms of thetype of agent considered. Thus, while consumers tend to set greater store by past price developments, employers and analystsincorporate forward-looking considerations to a greater extent. This characteristic means that, in the current environment,where after a longer-than-initially-expected delay the euro area inflation rate appears to be beginning to slow, frictions mightarise in wage-setting processes and jeopardise the maintenance of price stability.

1.5

1.7

1.9

2.1

2.3

2.5

Feb-00 May-00 Aug-00 Nov-00 Feb-01 May-010.00

0.04

0.08

0.12

0.16 RANGE (right-hand scale) REUTERS (b) CONSENSUS (a)ECB - SPF (c)

% %EURO AREA. CONSUMER PRICEINFLATION FORECASTS FOR 2001

(a) Monthly Survey of Professional Forecasters. (b) Quarterly Survey of Long-Term Forecasts (ProfessionalForecasters). (c) Quarterly Survey of Professional Forecasters. (d) EC Consumer and Business Surveys.

1.5

1.7

1.9

2.1

2.3

2.5

Feb-00 May-00 Aug-00 Nov-00 Feb-01 May-01

0.00

0.04

0.08

0.12

0.16

EURO AREA. CONSUMER PRICEINFLATION FORECASTS FOR 2002

5

10

15

20

25

30

35

40

1998 1999 2000 2001

0

1

2

3

4

SALE PRICE EXPECTATIONS IN MANUFACTURING CONSUMERS. PRICE TREND OVER NEXT 12 MONTHS HICP. 12-MONTH PERCENTAGE CHANGE (right-hand scale)

EURO AREA. EC SURVEY (d) AND INFLATION

%

(1) In “The information content of survey data on expected price developments for monetary policy”, Deutsche Bank (2001), Monthly Report, January, thereis quantitative evidence of the relative importance of the backward-looking component within the structure of consumer expectations.

26 BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

change general index is 8 % down. Broadly, theuncertainty surrounding equity markets mayhave prompted shifts in agents’ portfolios to-wards fixed-income securities.

The growth rates of the monetary aggre-gates in the euro area have risen during Q2,thus curtailing the progressively moderatingpath seen since 2000 Q3 (see Chart 13). Theyear-on-year change in the M3 aggregate ac-celerated in June to 6.3 % (as calculated on theoriginal series), placing the average for the lastthree months at over 5 %. Significantly, theECB has revised in this period the official seriesof the benchmark M3 aggregate, eliminatingfrom its calculation the holdings by non-resi-dents of money market funds. Despite the im-portance this caption had acquired since theadvent of EMU, it had not been possible tomake the adjustment previously since therewas not sufficient statistical information to iso-

late this effect. Besides, the recent trend of themonetary aggregates has been dominated bythe relative buoyancy of the less liquid assetsand a more moderate course of the compo-nents making up the narrow M1 aggregate. InSpain, liquidity has moved in line with that ofthe rest of the euro area. Accordingly, the aver-age growth rate of liquid financial assets (LFA)accelerated in Q2 to 5.9 %, against 3.9 % inQ1. A more detailed assessment of recent de-velopments in liquid assets in Spain can befound in section 5 of this report.

As regards the counterparts of the monetaryaggregates, financing extended in the euro areato the private sector has continued to losesteam, slipping to a year-on-year rate of 8.4 %in June, almost one percentage point down onthe related rate in March. That said, in historicalterms this is still a relatively high rate of expan-sion. As to the end use of bank financing, the

TABLE 2

Monetary and financial situation in the euro area and Spain

1999 2000

DEC DEC FEB MAR APR MAY JUN JUL (c)

MONETARY VARIABLES (a):

EURO AREAM3 6.1 4.9 4.4 4.6 4.7 5.3 6.3M1 10.0 5.7 2.0 2.1 1.6 3.2 4.2Loans to private sector 10.3 10.2 9.7 9.3 9.1 8.6 8.4

SPAINLiquid financial assets 1.4 2.6 3.9 4.6 4.7 6.1 6.9Cash and cash equivalents 12.7 4.4 3.1 2.5 2.5 3.9 4.8Financing to the private sector 19.4 18.8 17.7 17.2 16.6 16.8 16.7

FINANCIAL MARKETS (b):

EONIA 3.04 4.83 4.99 4.78 5.04 4.65 4.54 4.53Three-month EURIBOR 3.44 4.94 4.76 4.71 4.68 4.64 4.45 4.47Public debt

Euro area ten-year bond yields 5.32 5.07 5.02 4.94 5.10 5.26 5.21 5.29US-euro area ten-year bond spread 1.04 0.25 0.15 0.00 0.09 0.18 0.12 0.14Spain-Germany ten-year bond spread 0.22 0.31 0.34 0.37 0.35 0.31 0.33 0.32

Spanish bank interest ratesSynthetic deposit rate 1.98 3.02 3.04 3.03 3.00 2.98Synthetic lending rate 5.03 6.35 6.22 6.08 6.16 6.04

US/EUR exchange rate 1.011 0.897 0.922 0.910 0.892 0.874 0.853 0.849Equities (d)

Dow Jones EURO STOXX Broad Index 39.5 -5.9 -7.7 -11.2 -5.7 -6.5 -10.4 -14.6 Madrid Stock Exchange General Index 16.2 -12.7 3.0 0.9 6.3 3.8 -2.2 -8.0

2001

Sources: European Central Bank and Banco de España. (a) Annual percentage change. (b) Monthly averages. (c) Monthly average to 13 July 2001. (d) Cumulative percentage change during the year. Latest month: to 12 July 2001.

27BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

CHART 12

Euro-area yield curves

Sources: Banco de España and ECB. (a) Estimation based on swap market data. (b) Estimated using Euribor data.

4.0

4.5

5.0

5.5

6.0

6.5

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

4.0

4.5

5.0

5.5

6.0

6.5

30 March 2001

29 June 2001

13 July 2001

years

ZERO-COUPON CURVE (a)

4.0

4.2

4.4

4.6

4.8

5.0

EONIA 1 month 3 months 6 months 9 months 1 year4.0

4.2

4.4

4.6

4.8

5.0

March 2001June 2001 1-13 July 2001

INTERBANK MARKET(monthly average)

EURIBOR

% %

4.0

4.2

4.4

4.6

4.8

5.0

0 1 2 3 4 5 6 7 8 9 10 11

4.0

4.2

4.4

4.6

4.8

5.0

30 March 2001 29 June 2001 13 July 2001

TERM STRUCTURE (b)

months

CHART 13

Monetary and credit aggregatesand interest rates in the euro area

0

4

8

12

16

1998 1999 2000 20010

4

8

12

16

M1

MONETARY AGGREGATESYear-on-year rates: original series

M3

% %

Sources: Banco de España and European Central Bank.

0

4

8

12

16

1998 1999 2000 2001

0

4

8

12

16

LENDING TO HOUSEHOLDS AND FIRMSYear-on-year rates: original series

2

2.5

3

3.5

4

4.5

5

5.5

6

6.5

1998 1999 2000 2001

2

2.5

3

3.5

4

4.5

5

5.5

6

6.5

BANK, MONEY MARKET AND DEBTMARKET INTEREST RATES

(monthly average)

3-MONTHEURIBOR

MORTGAGE LENDINGTO HOUSEHOLDS

LENDING TOFIRMS AT OVER

1 YEAR

BANK DEPOSITSUP TO 2 YEARS

10-YEARBOND YIELDS

28 BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

information available for Q1 indicates that it ishouseholds which have most contributed totempering lending, the consumer segment ofwhich has proven intense. In any event, itshould be recalled that there are sources of fi-nancing other than bank lending, such as cor-porate financing via fixed-income issues, whichis progressively acquiring considerable impor-

tance. In the case of Spain, the growth of fi-nancing to non-financial corporations andhouseholds and non-profit institutions is beingcontained to some degree, although the associ-ated rates of expansion are still high at 16 %year-on-year. Section 5 offers a more exhaus-tive evaluation of the financing of these eco-nomic sectors.

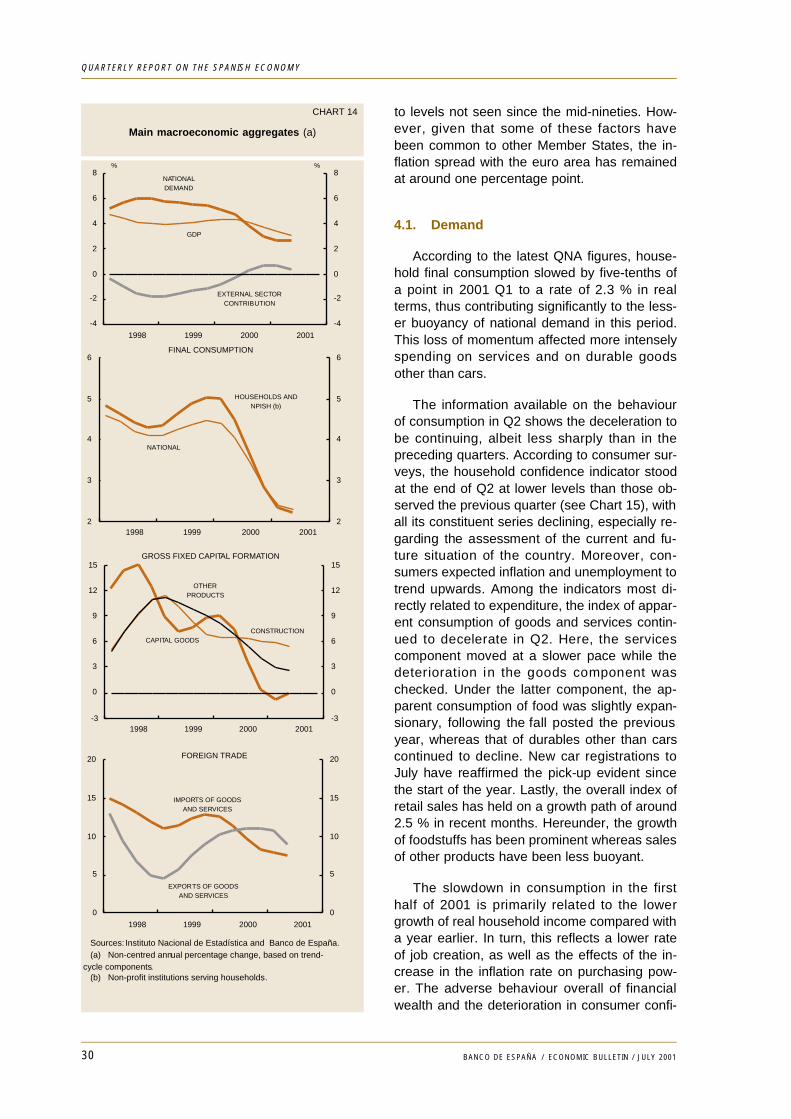

4. The Spanish economy On QNA estimates, GDP remained in 2001Q1 on the decelerating path initiated in the sec-ond half of the previous year, posting a realgrowth rate of 3.4 % (1) on a year earlier, three-tenths of a point less than the previous quarter(see Chart 14). This profile was determined bythe slowdown in the main components of na-tional demand, both private consumption andgross fixed capital formation, placing the year-on-year rate of change of this aggregate at2.7 %. The contribution of net external demandto GDP growth, for its part, held at the higherlevel reached the previous quarter (0.6 percent-age point). The short-term economic informa-tion available for 2001 Q2 points to a moderateand further slowdown in national demand to arate of around 2.5 %, and a somewhat less pos-itive contribution by the external sector, the re-sult of weaker exports. Overall, GDP is estimat-ed to have held on a slowing path in 2001 Q2,and its year-on-year rate to have fallen to 3 %.

All the productive branches saw a lesseningof the pace of activity during Q1, in line with fi-nal demand. The loss of momentum was sharp-er in the industrial and energy branches, asthese were affected by a less favourable inter-national background and by the weakening ofthe investment climate, a pattern that has con-tinued into Q2. Apart from in market services,the slowdown in activity did not pass through infull to employment, giving rise to a fresh fall inthe rate of increase of apparent labour produc-tivity. Compensation per employee in the mar-ket economy increased by a similar amount tothat at the end of last year (3.7 %), contributingto a slight rise in unit labour costs in this groupof activities.

As early as last year, wage increases beganto incorporate, in part, the upward effects on theinflation rate derived from oil price rises andfrom the successive crises besetting the foodindustry. This process has continued into thecurrent year. Against this backdrop, where freshdirect upward effects on prices (stemming fromchanges in the market for certain meat prod-ucts) have combined with the effects derivedfrom higher wage and intermediate costs, the12-month growth rate of the CPI has risen anew

29BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

(1) Unless otherwise indicated, the growth rates of theQNA series mentioned in this section refer to trend-cycleseries.

to levels not seen since the mid-nineties. How-ever, given that some of these factors havebeen common to other Member States, the in-flation spread with the euro area has remainedat around one percentage point.

4.1. Demand

According to the latest QNA figures, house-hold final consumption slowed by five-tenths ofa point in 2001 Q1 to a rate of 2.3 % in realterms, thus contributing significantly to the less-er buoyancy of national demand in this period.This loss of momentum affected more intenselyspending on services and on durable goodsother than cars.

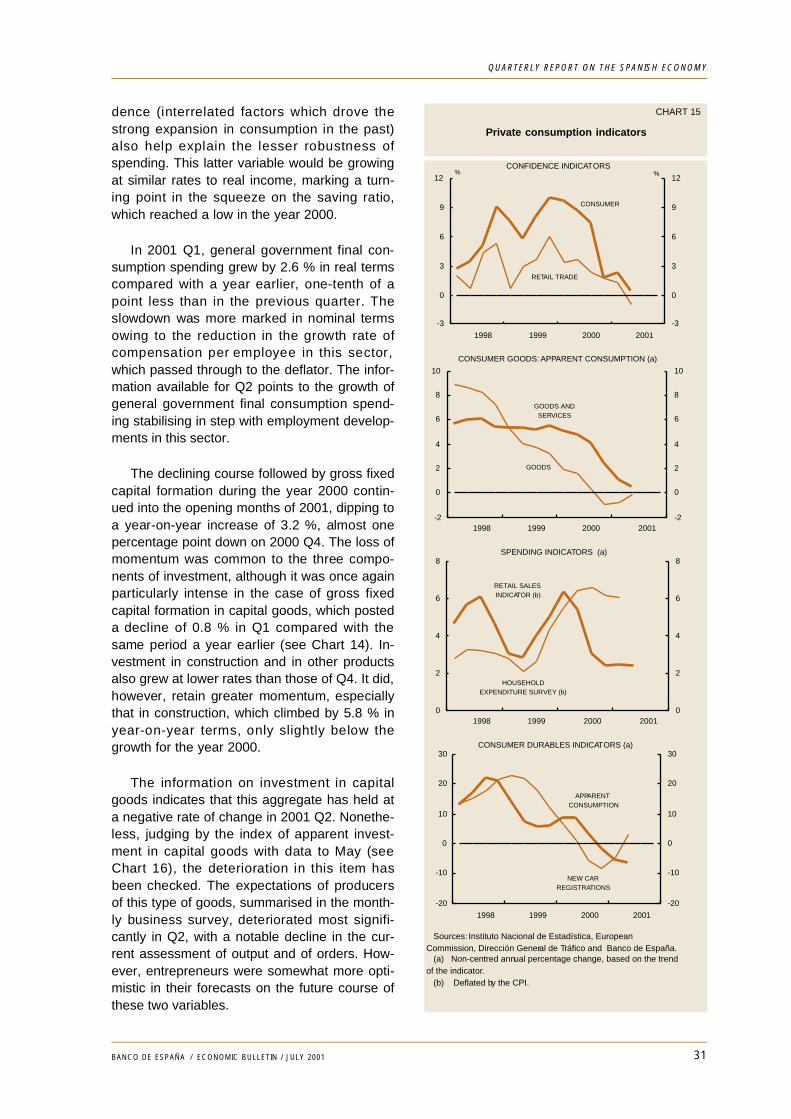

The information available on the behaviourof consumption in Q2 shows the deceleration tobe continuing, albeit less sharply than in thepreceding quarters. According to consumer sur-veys, the household confidence indicator stoodat the end of Q2 at lower levels than those ob-served the previous quarter (see Chart 15), withall its constituent series declining, especially re-garding the assessment of the current and fu-ture situation of the country. Moreover, con-sumers expected inflation and unemployment totrend upwards. Among the indicators most di-rectly related to expenditure, the index of appar-ent consumption of goods and services contin-ued to decelerate in Q2. Here, the servicescomponent moved at a slower pace while thedeterioration in the goods component waschecked. Under the latter component, the ap-parent consumption of food was slightly expan-sionary, following the fall posted the previousyear, whereas that of durables other than carscontinued to decline. New car registrations toJuly have reaffirmed the pick-up evident sincethe start of the year. Lastly, the overall index ofretail sales has held on a growth path of around2.5 % in recent months. Hereunder, the growthof foodstuffs has been prominent whereas salesof other products have been less buoyant.

The slowdown in consumption in the firsthalf of 2001 is primarily related to the lowergrowth of real household income compared witha year earlier. In turn, this reflects a lower rateof job creation, as well as the effects of the in-crease in the inflation rate on purchasing pow-er. The adverse behaviour overall of financialwealth and the deterioration in consumer confi-

30 BANCO DE ESPAÑA / ECONOMIC BULLETIN / JULY 2001

QUARTERLY REPORT ON THE SPANISH ECONOMY

CHART 14

Main macroeconomic aggregates (a)

-4

-2

0

2

4

6

8

1998 1999 2000 2001

-4

-2

0

2

4

6

8NATIONALDEMAND

%

EXTERNAL SECTORCONTRIBUTION

GDP

%

2

3

4

5

6

1998 1999 2000 20012

3

4

5

6

HOUSEHOLDS ANDNPISH (b)

FINAL CONSUMPTION

NATIONAL

-3

0

3

6

9

12

15

1998 1999 2000 2001-3

0

3

6

9

12

15

CONSTRUCTION

GROSS FIXED CAPITAL FORMATION

CAPITAL GOODS

OTHERPRODUCTS

0

5

10

15

20

1998 1999 2000 2001

0

5

10

15

20

EXPORTS OF GOODSAND SERVICES

FOREIGN TRADE

IMPORTS OF GOODSAND SERVICES

Sources: Instituto Nacional de Estadística and Banco de España. (a) Non-centred annual percentage change, based on trend-cycle components. (b) Non-profit institutions serving households.

dence (interrelated factors which drove thestrong expansion in consumption in the past)also help explain the lesser robustness ofspending. This latter variable would be growingat similar rates to real income, marking a turn-ing point in the squeeze on the saving ratio,which reached a low in the year 2000.

In 2001 Q1, general government final con-sumption spending grew by 2.6 % in real termscompared with a year earlier, one-tenth of apoint less than in the previous quarter. Theslowdown was more marked in nominal termsowing to the reduction in the growth rate ofcompensation per employee in this sector,which passed through to the deflator. The infor-mation available for Q2 points to the growth ofgeneral government final consumption spend-ing stabilising in step with employment develop-ments in this sector.

The declining course followed by gross fixedcapital formation during the year 2000 contin-ued into the opening months of 2001, dipping toa year-on-year increase of 3.2 %, almost onepercentage point down on 2000 Q4. The loss ofmomentum was common to the three compo-nents of investment, although it was once againparticularly intense in the case of gross fixedcapital formation in capital goods, which posteda decline of 0.8 % in Q1 compared with thesame period a year earlier (see Chart 14). In-vestment in construction and in other productsalso grew at lower rates than those of Q4. It did,however, retain greater momentum, especiallythat in construction, which climbed by 5.8 % inyear-on-year terms, only slightly below thegrowth for the year 2000.