Embed Size (px)

Citation preview

Q U A R T E R L Y R E P O R T

2017 THIRD QUARTER

2 QUARTERLY REPORT Q3 2017

Contents Highlights 3

Group summary 5

Business areas 6

Other matters 7

Outlook 7

Financial statements 9

Notes to the financial statements 12

Definitions 15

Financial calendar and investor information 16

3 QUARTERLY REPORT Q3 2017

Highlights per third quarter 2017

Hafslund ASA de-listed from Oslo Stock Exchange, de-merger and Hafslund AS established effective 4 August, with main business Hafslund Nett.

Hafslund Marked, Hafslund Varme and Hafslund Produksjon spun off and sold to Fortum, E-CO and the Oslo kommune on 4 August.

Year-to-date EBITDA of NOK 1,124 million and year-to-date profit after tax before discontinued operations of NOK 362 million at end of third quarter.

Solid operations and KILE costs in Q3 on a par with last year.

AMS project progressing well – more than half of 700,000 meters installed.

Net debt of NOK 6.2 billion and net debt/EBITDA ratio of 3.9.

Ytd EBITDA

NOK

1,124 million

Net debt/ EBITDA

3.9

4 QUARTERLY REPORT Q3 2017

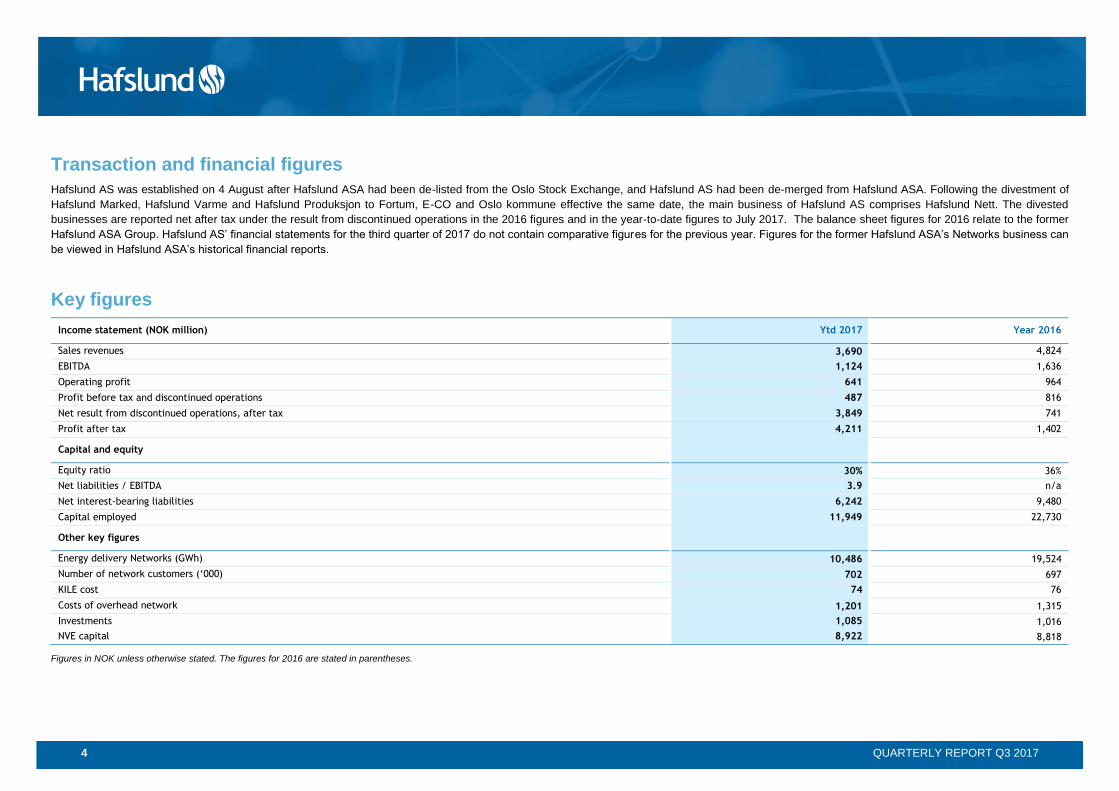

Transaction and financial figures

Hafslund AS was established on 4 August after Hafslund ASA had been de-listed from the Oslo Stock Exchange, and Hafslund AS had been de-merged from Hafslund ASA. Following the divestment of

Hafslund Marked, Hafslund Varme and Hafslund Produksjon to Fortum, E-CO and Oslo kommune effective the same date, the main business of Hafslund AS comprises Hafslund Nett. The divested

businesses are reported net after tax under the result from discontinued operations in the 2016 figures and in the year-to-date figures to July 2017. The balance sheet figures for 2016 relate to the former

Hafslund ASA Group. Hafslund AS’ financial statements for the third quarter of 2017 do not contain comparative figures for the previous year. Figures for the former Hafslund ASA’s Networks business can

be viewed in Hafslund ASA’s historical financial reports.

Key figures

Income statement (NOK million) Ytd 2017 Year 2016

Sales revenues 3,690 4,824

EBITDA 1,124 1,636

Operating profit 641 964

Profit before tax and discontinued operations 487 816

Net result from discontinued operations, after tax 3,849 741

Profit after tax 4,211 1,402

Capital and equity

Equity ratio 30% 36%

Net liabilities / EBITDA 3.9 n/a

Net interest-bearing liabilities 6,242 9,480

Capital employed 11,949 22,730

Other key figures

Energy delivery Networks (GWh) 10,486 19,524

Number of network customers (‘000) 702 697

KILE cost 74 76

Costs of overhead network 1,201 1,315

Investments 1,085 1,016

NVE capital 8,922 8,818

Figures in NOK unless otherwise stated. The figures for 2016 are stated in parentheses.

5 QUARTERLY REPORT Q3 2017

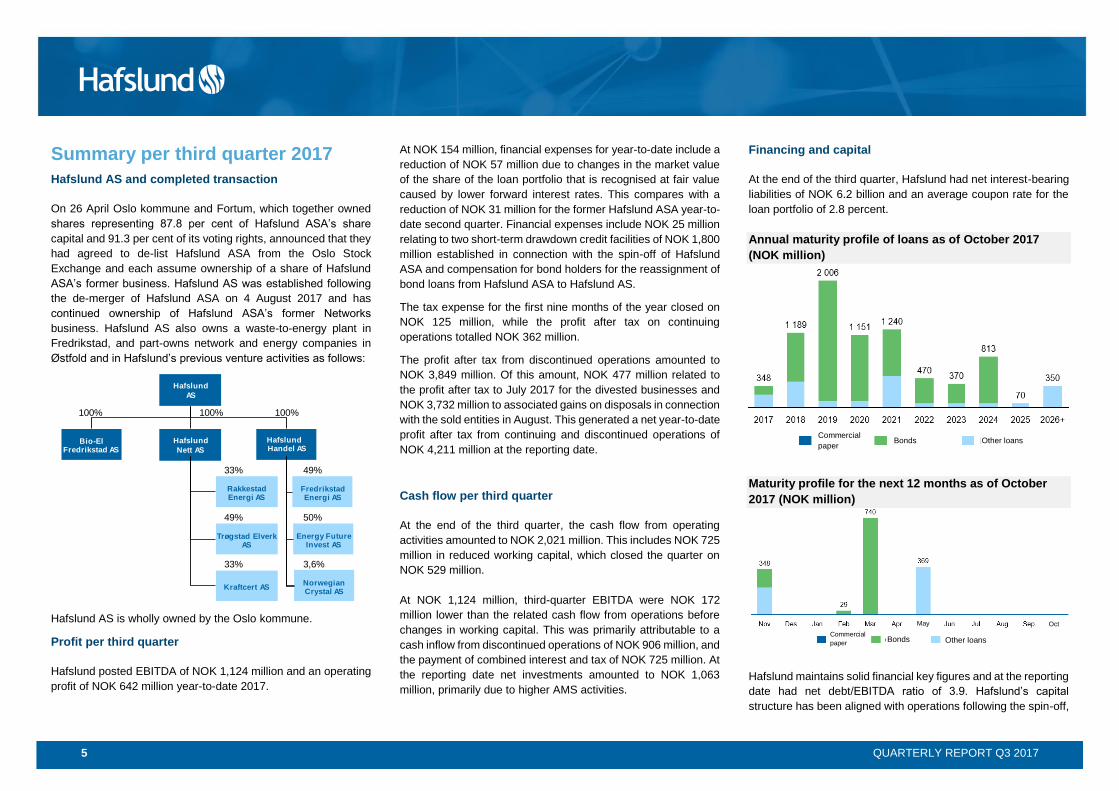

Summary per third quarter 2017

Hafslund AS and completed transaction

On 26 April Oslo kommune and Fortum, which together owned

shares representing 87.8 per cent of Hafslund ASA’s share

capital and 91.3 per cent of its voting rights, announced that they

had agreed to de-list Hafslund ASA from the Oslo Stock

Exchange and each assume ownership of a share of Hafslund

ASA’s former business. Hafslund AS was established following

the de-merger of Hafslund ASA on 4 August 2017 and has

continued ownership of Hafslund ASA’s former Networks

business. Hafslund AS also owns a waste-to-energy plant in

Fredrikstad, and part-owns network and energy companies in

Østfold and in Hafslund’s previous venture activities as follows:

Hafslund AS is wholly owned by the Oslo kommune.

Profit per third quarter

Hafslund posted EBITDA of NOK 1,124 million and an operating

profit of NOK 642 million year-to-date 2017.

At NOK 154 million, financial expenses for year-to-date include a

reduction of NOK 57 million due to changes in the market value

of the share of the loan portfolio that is recognised at fair value

caused by lower forward interest rates. This compares with a

reduction of NOK 31 million for the former Hafslund ASA year-to-

date second quarter. Financial expenses include NOK 25 million

relating to two short-term drawdown credit facilities of NOK 1,800

million established in connection with the spin-off of Hafslund

ASA and compensation for bond holders for the reassignment of

bond loans from Hafslund ASA to Hafslund AS.

The tax expense for the first nine months of the year closed on

NOK 125 million, while the profit after tax on continuing

operations totalled NOK 362 million.

The profit after tax from discontinued operations amounted to

NOK 3,849 million. Of this amount, NOK 477 million related to

the profit after tax to July 2017 for the divested businesses and

NOK 3,732 million to associated gains on disposals in connection

with the sold entities in August. This generated a net year-to-date

profit after tax from continuing and discontinued operations of

NOK 4,211 million at the reporting date.

Cash flow per third quarter

At the end of the third quarter, the cash flow from operating

activities amounted to NOK 2,021 million. This includes NOK 725

million in reduced working capital, which closed the quarter on

NOK 529 million.

At NOK 1,124 million, third-quarter EBITDA were NOK 172

million lower than the related cash flow from operations before

changes in working capital. This was primarily attributable to a

cash inflow from discontinued operations of NOK 906 million, and

the payment of combined interest and tax of NOK 725 million. At

the reporting date net investments amounted to NOK 1,063

million, primarily due to higher AMS activities.

Financing and capital

At the end of the third quarter, Hafslund had net interest-bearing

liabilities of NOK 6.2 billion and an average coupon rate for the

loan portfolio of 2.8 percent.

Annual maturity profile of loans as of October 2017

(NOK million)

Maturity profile for the next 12 months as of October

2017 (NOK million)

Hafslund maintains solid financial key figures and at the reporting

date had net debt/EBITDA ratio of 3.9. Hafslund’s capital

structure has been aligned with operations following the spin-off,

Fredrikstad Energi AS

Energy FutureInvest AS

49%

Norwegian Crystal AS

3,6%

50%

Hafslund

AS

Rakkestad Energi AS

Trøgstad Elverk AS

33%

49%

Kraftcert AS

33%

Hafslund Handel AS

Bio-El Fredrikstad AS

Hafslund

Nett AS

100% 100%100%

Commercial

paper Bonds Other loans

Commercial

paper Bonds Other loans

May Oct

6 QUARTERLY REPORT Q3 2017

with an aim of maintaining a similar credit profile to that of the

former Hafslund ASA. Gross interest-bearing liabilities are

expected to be on a par with net interest-bearing liabilities by the

first half of 2018. Hafslund’s capital requirements will increase

slightly towards the end of 2018, in part due to the completion of

the roll-out of automatic meters (the "AMS project"). The

company’s net-interest bearing liabilities/EBITDA ratio is not

expected in exceed 5.

At the end of the third quarter, Hafslund had cash and cash

equivalents of NOK 2,066 million and a drawdown facility of NOK

500 million that matures in October 2018. Management is

working to establish a new, larger drawdown facility that is

expected to be in place in the fourth quarter of 2017. Hafslund

has a robust financing structure with sufficient liquidity to cover

at least the next 12 months’ maturities.

Networks

Key financial figures

NOK million Q3 17 Q3 16 Ytd 2017 Ytd 2016

Sales revenues 1,110 1,103 3,603 3,400

Gross contribution 688 751 2,128 2,175

EBITDA 386 411 1,160 1,195

Operating profit 224 255 687 748

Energy delivery (GWh) 4,065 3,856 10,486 10,458

Number of customers (‘000)

702 693

Costs of overhead network

361 304 1201 963

Investments 410 254 1,085 605

NVE capital 8,922 8,294

Capital employed 11,694 11,279 11,694 11,279

Networks posted sales revenues of NOK 1,110 million in the

quarter, up NOK 7 million on the comparable prior-year period.

The increase was attributable to a higher volume and network

rental. The energy delivery for the third quarter came in at NOK

4,065 GWh, an increase of five per cent on the previous year.

Combined costs for the overhead network (Statnett) and energy

purchases for network losses amounted to NOK 409 million

(NOK 345 million) in the quarter. The increase primarily relates

to higher costs for the overhead network (Statnett) of NOK 57

million. This generated a gross contribution of NOK 688 million

(NOK 751 million) for the third quarter.

At NOK 302 million, operating expenses for the third quarter were

NOK 38 million lower than the third quarter of 2016. Operating

and maintenance expenses fell by NOK 32 million, of which NOK

20 million relates to customer-initiated work, NOK 3 million to

lower contingency costs, and NOK 9 million to other operating

expenses. Remaining operating expenses decreased by NOK 17

million, primarily due to lower costs for meter reading, invoicing

and revenue collection services for network customers.

Investment contributions rose by NOK 6 million against the

previous year. These contributions have no impact on profit due

to the fact that there is a corresponding increase in income.

Third-quarter EBITDA of NOK 386 million were NOK 25 million

lower than the previous year.

Assuming normal energy demand, planned network tariffs and

forward power prices, as well as planned maintenance and cost

changes, Networks’ operating profit for 2017 is expected to come

in around 15 percent lower than in 2016. This is attributable to

major positive non-recurring effects in 2016 relating to the

purchased networks business in Østfold in 2014.

At the end of 2016, Networks had accumulated surplus income

of NOK 187 million. According the current forecasts,

accumulated surplus income is expected to increase to around

NOK 310 million by the end of 2017. The increase in surplus

income is part due to Hafslund Nett’s desire to maintain the

network rental as stable as possible.

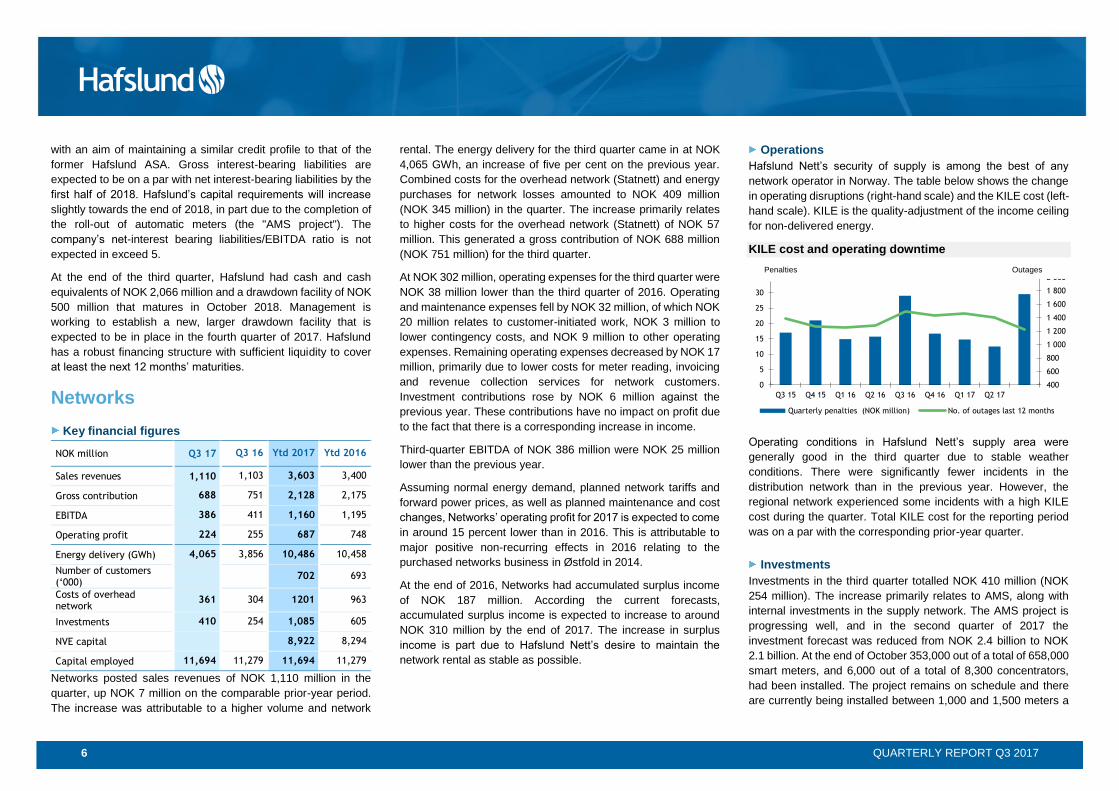

Operations

Hafslund Nett’s security of supply is among the best of any

network operator in Norway. The table below shows the change

in operating disruptions (right-hand scale) and the KILE cost (left-

hand scale). KILE is the quality-adjustment of the income ceiling

for non-delivered energy.

KILE cost and operating downtime

Operating conditions in Hafslund Nett’s supply area were

generally good in the third quarter due to stable weather

conditions. There were significantly fewer incidents in the

distribution network than in the previous year. However, the

regional network experienced some incidents with a high KILE

cost during the quarter. Total KILE cost for the reporting period

was on a par with the corresponding prior-year quarter.

Investments

Investments in the third quarter totalled NOK 410 million (NOK

254 million). The increase primarily relates to AMS, along with

internal investments in the supply network. The AMS project is

progressing well, and in the second quarter of 2017 the

investment forecast was reduced from NOK 2.4 billion to NOK

2.1 billion. At the end of October 353,000 out of a total of 658,000

smart meters, and 6,000 out of a total of 8,300 concentrators,

had been installed. The project remains on schedule and there

are currently being installed between 1,000 and 1,500 meters a

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

0

5

10

15

20

25

30

35

Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17

Quarterly penalties (NOK million) No. of outages last 12 months

OutagesPenalties

7 QUARTERLY REPORT Q3 2017

day. The risk profile is relatively unchanged against the second

quarter. The greatest areas of uncertainty for the project relate to

continuation of the current installment rate, efficient use of IT

support and capacity in the radio-mesh network. At the end of the

third quarter of 2017, Networks had capital employed of NOK

11.7 billion (NOK 11.3 billion).

Other business

NOK million Ytd 2017 Year 2016

Staff functions (62) (48)

Other business 16 (44)

Operating loss Other business (46) (92)

Other business posted a total operating loss of NOK 46 million in

the third quarter. Staff functions, which related to the former

parent company Hafslund ASA until 4 August and subsequently

to the new company Hafslund AS, posted an operating loss of

NOK 62 million for the nine months to 30 September 2017. This

compares to a loss of NOK 27 million at the end of the second

quarter for the former Hafslund ASA. The operating loss for staff

functions includes NOK 29 million in costs relating to the

transaction. Staff functions have been scaled down in the new

company Hafslund AS. Other business comprises Bio-El

Fredrikstad AS, associates and changes in the value of interest-

rate derivatives. The low result in 2016 primarily relates to

impairments in associates and Other business.

Business disposals

In August 2017, Hafslund’s Markets, Heat and Production

business areas were spun off and sold. The income statement

for the first nine months of 2017 has been restated with the

results of discontinued operations shown separately. The

comparative figures for 2016 have been restated accordingly.

See also discussion in Note 2.

Other matters

Settlement of transaction

Profit from discontinued operations is based on the latest

estimated purchase figures per balance sheet date. It is expected

that the final purchase figures and settlement will be completed

in fourth-quarter 2017. Preliminary calculations indicate that

Hafslund's cash holdings will be reduced by approximately NOK

250 million, mainly as a result of tax and working capital

adjustments.

The Board of Directors of Hafslund AS

Hafslund AS’ Board of Directors comprises:

• Hilde Tonne – Chair

• Bente Sollid Storehaug

• Jeanette Iren Moen

• Odd Håkon Hoelsæter

• Bjørn Erik Næss

• Per Orfjell – Employee

representative

• Per Luneborg – Employee

representative

• Tommy Linder –

Employee representative

Bjørn Erik Næss is the Chair of the Audit Committee

Outlook

The transaction agreed with Oslo kommune and Fortum was

implemented on 4 August this year. Hafslund was de-merged,

and Hafslund Marked, Hafslund Varme and Hafslund Produksjon

were sold. The main business of Hafslund now comprises

Hafslund ASA’s former Networks operations. Hafslund Nett,

which owns and operates the bulk of the regional and distribution

network in Akershus, Oslo and Østfold, is Norway’s largest

network operator with 700,000 customers. Ownership of the

regulated network business provides a solid basis for stable and

predictable returns.

In implementing the de-merger, importance was attached to

maintaining deliveries to customers, securing stable and efficient

operations and upholding expertise levels and the performance

of the business areas. Hafslund will deliver Group services to the

divested businesses for a transitional period, and significant work

is being performed to securely embed Hafslund and the divested

businesses with their new owners.

Networks’ long-term earnings are influenced by the business

area’s relative cost efficiency compared with the rest of the

networks industry, interest rate fluctuations and changes in

public regulations. Digitalisation of the value chain and the

customer interface is absolutely critical to achieving efficient

operations and retaining satisfied customers.

Hafslund will ramp up its investments to a yearly average of

around NOK 1.7 billion in 2017 and 2018, compared with a yearly

average of NOK 0.7 billion between 2013 and 2015 and NOK 1

billion in 2016. In addition to ongoing investments in operations

and expansion, the Group’s future investments will be

characterised by investments of NOK 2.1 billion in automatic

meters at all customers and associated new ICT systems.

Hafslund ASA’s debt have been transferred to Hafslund AS, and

will be aligned with the business’ activities and strategy. Hafslund

AS aims to maintain a similar credit profile to that of the former

Hafslund ASA.

Hafslund will continue the previously communicated growth and

improvement initiatives and further develop Hafslund Nett as one

of Norway’s most efficient network operators. Hafslund also

holds a 49 per cent stake in Fredrikstad Energi AS, which has

94,000 customers, and shareholdings in two smaller network

operators. Hafslund will seek out further growth opportunities

both organically and through acquisitions and intend to

participate in any consolidation in the eastern parts of Norway.

Oslo, 27 November 2017

Hafslund AS

Board of Directors

8 QUARTERLY REPORT Q3 2017

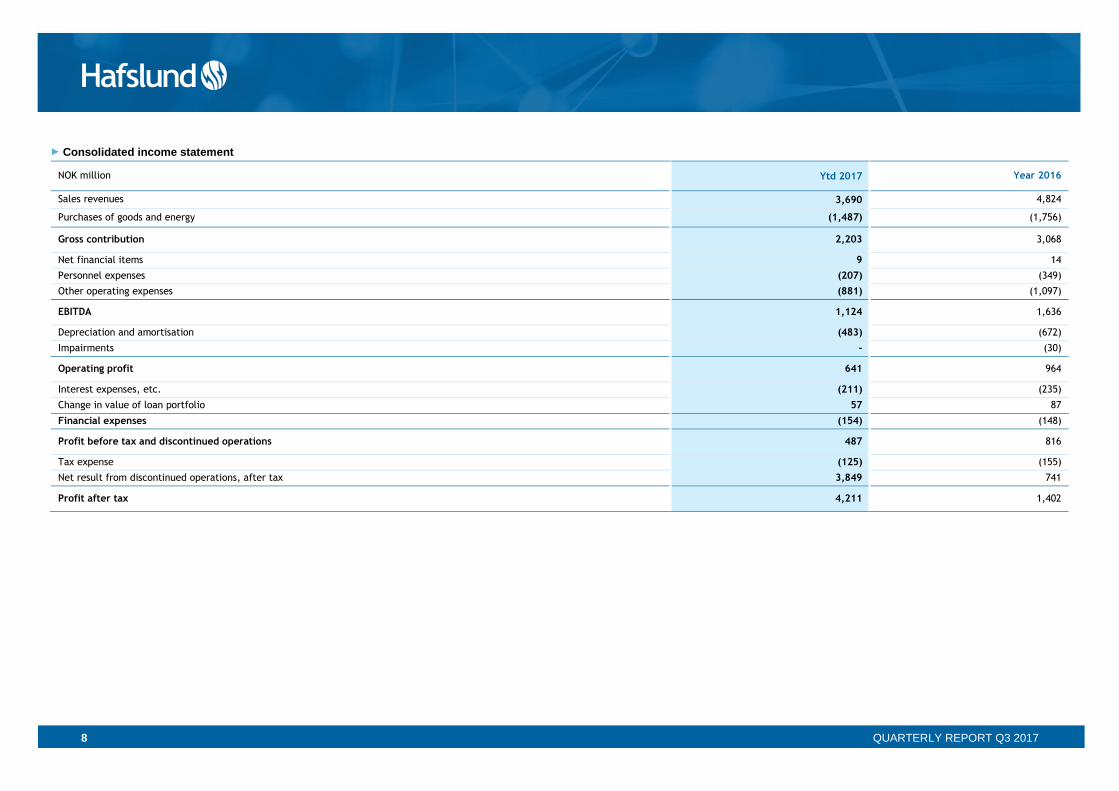

Consolidated income statement

NOK million Ytd 2017 Year 2016

Sales revenues 3,690 4,824

Purchases of goods and energy (1,487) (1,756)

Gross contribution 2,203 3,068

Net financial items 9 14

Personnel expenses (207) (349)

Other operating expenses (881) (1,097)

EBITDA 1,124 1,636

Depreciation and amortisation (483) (672)

Impairments - (30)

Operating profit 641 964

Interest expenses, etc. (211) (235)

Change in value of loan portfolio 57 87

Financial expenses (154) (148)

Profit before tax and discontinued operations 487 816

Tax expense (125) (155)

Net result from discontinued operations, after tax 3,849 741

Profit after tax 4,211 1,402

9 QUARTERLY REPORT Q3 2017

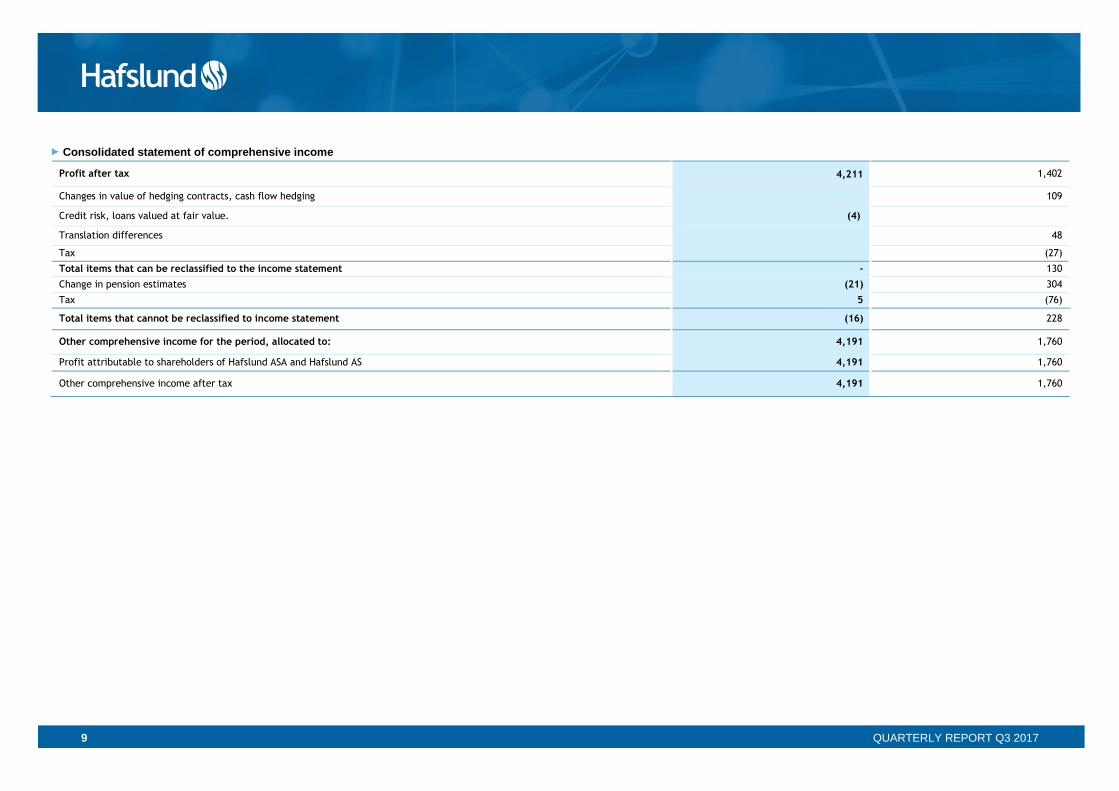

Consolidated statement of comprehensive income

Profit after tax 4,211 1,402

Changes in value of hedging contracts, cash flow hedging 109

Credit risk, loans valued at fair value. (4)

Translation differences 48

Tax (27)

Total items that can be reclassified to the income statement - 130

Change in pension estimates (21) 304

Tax 5 (76)

Total items that cannot be reclassified to income statement (16) 228

Other comprehensive income for the period, allocated to: 4,191 1,760

Profit attributable to shareholders of Hafslund ASA and Hafslund AS 4,191 1,760

Other comprehensive income after tax 4,191 1,760

10 QUARTERLY REPORT Q3 2017

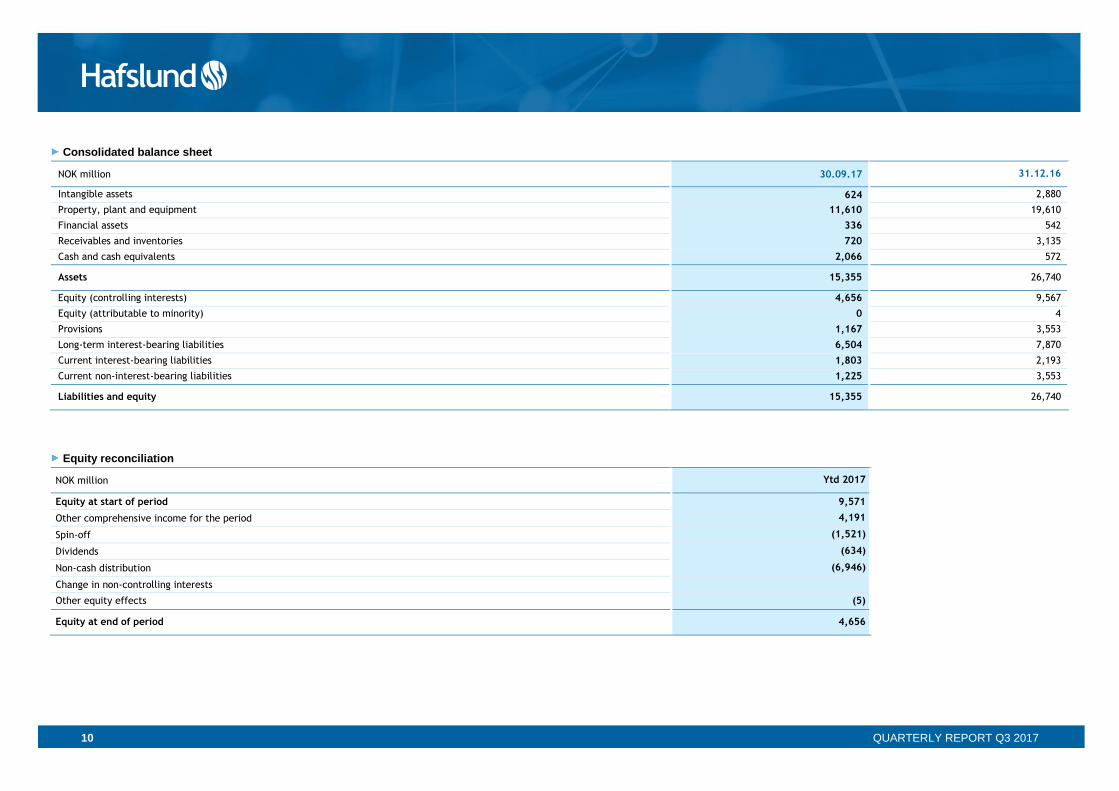

Consolidated balance sheet

NOK million 30.09.17 31.12.16

Intangible assets 624 2,880

Property, plant and equipment 11,610 19,610

Financial assets 336 542

Receivables and inventories 720 3,135

Cash and cash equivalents 2,066 572

Assets 15,355 26,740

Equity (controlling interests) 4,656 9,567

Equity (attributable to minority) 0 4

Provisions 1,167 3,553

Long-term interest-bearing liabilities 6,504 7,870

Current interest-bearing liabilities 1,803 2,193

Current non-interest-bearing liabilities 1,225 3,553

Liabilities and equity 15,355 26,740

Equity reconciliation

NOK million Ytd 2017

Equity at start of period 9,571

Other comprehensive income for the period 4,191

Spin-off (1,521)

Dividends (634)

Non-cash distribution (6,946)

Change in non-controlling interests

Other equity effects (5)

Equity at end of period 4,656

11 QUARTERLY REPORT Q3 2017

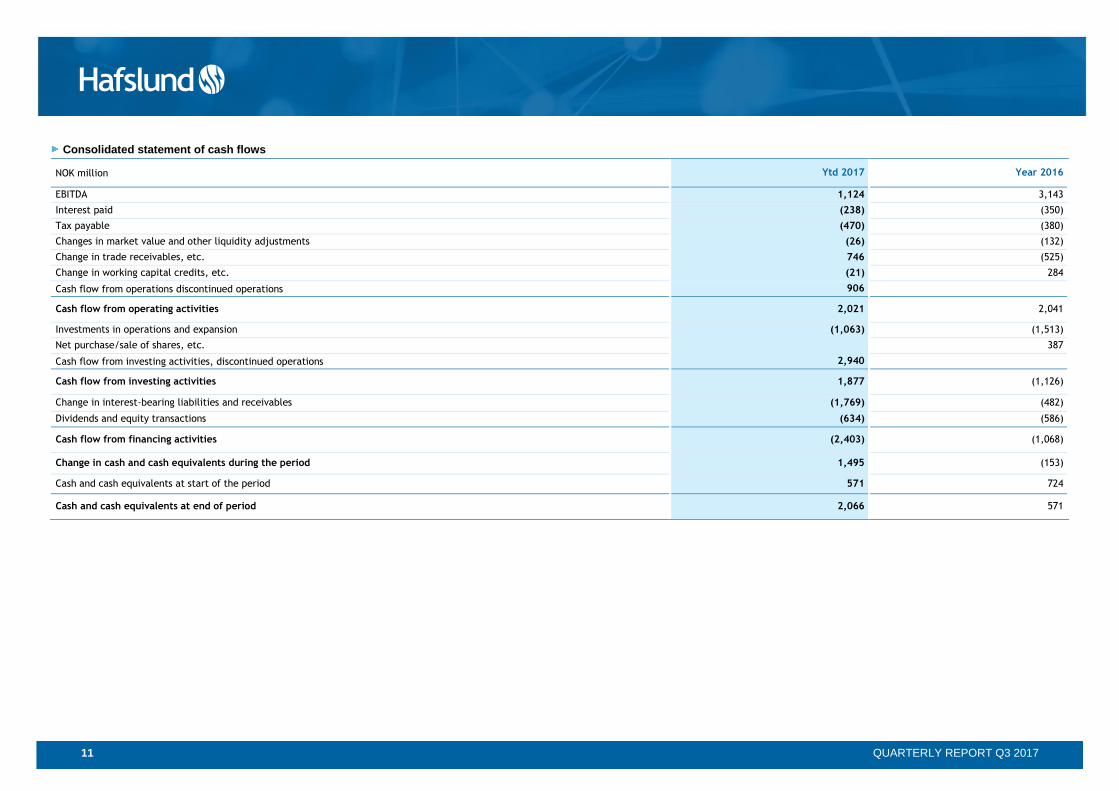

Consolidated statement of cash flows

NOK million Ytd 2017 Year 2016

EBITDA 1,124 3,143

Interest paid (238) (350)

Tax payable (470) (380)

Changes in market value and other liquidity adjustments (26) (132)

Change in trade receivables, etc. 746 (525)

Change in working capital credits, etc. (21) 284

Cash flow from operations discontinued operations 906

Cash flow from operating activities 2,021 2,041

Investments in operations and expansion (1,063) (1,513)

Net purchase/sale of shares, etc. 387

Cash flow from investing activities, discontinued operations 2,940

Cash flow from investing activities 1,877 (1,126)

Change in interest-bearing liabilities and receivables (1,769) (482)

Dividends and equity transactions (634) (586)

Cash flow from financing activities (2,403) (1,068)

Change in cash and cash equivalents during the period 1,495 (153)

Cash and cash equivalents at start of the period 571 724

Cash and cash equivalents at end of period 2,066 571

12 QUARTERLY REPORT Q3 2017

Notes to the financial statements

1) Framework conditions and key accounting policies

The consolidated financial statements for the third quarter of 2017, for the period ending 30

September 2017, have been prepared in accordance with International Financial Reporting

Standards (IFRSs) as adopted by the EU and include Hafslund AS, its subsidiaries and associates.

Financial figures have not been prepared for the third quarter in isolation; however, year-to-date

figures have been prepared as of 30 September 2017 following the completion of the spin-off. This

deviates from the requirements for interim reporting contained in IAS 34. This interim report has not

been audited,

The interim financial statements do not provide the same scope of information as the annual financial

statements and should therefore be viewed in the context of Hafslund ASA’s consolidated financial

statements for 2016. The accounting policies and calculation methods applied in interim reporting

are the same as those described in Note 2 to the consolidated annual financial statements of the

Hafslund ASA Group for 2016, with the exception of IFRS 9 Financial Instruments.

The Group has decided to early-adopt IFRS 9, which replaces IAS 39, and will apply IFRS 9 from 1

January 2017. In accordance with IFRS 9 financial assets are divided into three categories: fair value

through profit or loss; fair value through other comprehensive income; and amortised cost. The

standard deals with the classification, measurement, recognition and de-recognition of financial

assets and liabilities, and introduces new rules for hedge accounting and a new impairment model

for financial assets. The following areas have been affected by IFRS 9:

✓ The standard essentially continues the requirements of IAS 39 for financial liabilities, where the

most significant change relates to use of the fair value option for financial liabilities. In

accordance with IFRS 9 changes in fair value attributable to changes in inherent credit risk are

recognised in other comprehensive income. At the end of the third quarter of 2017, this change

amounted to NOK -4 million.

✓ Impairments attributable to credit risk are now recognised based on expected losses rather than

under previous models where losses must already have been incurred. The new impairment

model has not materially impacted the consolidated figures at the end of the third quarter of

2017.

IFRS 9 will be of less relevance for the residual business following the disposal of Hafslund’s power-

exposed operations. The Group is also working to implement IFRS 15 Revenues from Contracts

with Customers and IFRS 16 Leases. See Note 2 to Hafslund ASA’s consolidated annual financial

statements for 2016.

2) Business disposals

On 3 July 2017, Oslo kommune made a voluntary offering for all the shares in Hafslund ASA

through its wholly owned subsidiary Oslo Energi Holding AS. After the compulsory acquisition of

the shares of minority shareholders, the shares were de-listed from the Oslo Stock Exchange. On

4 August 2017 Hafslund ASA implemented a spin-off pursuant to company law with continuity of

shareholders’ shares and rights, in which all assets, rights and obligations, apart from those

assets, rights and liabilities associated with Hafslund Produksjon, were spun off to the new

company Hafslund AS.

From a company-law perspective Hafslund AS is the acquiring company in the spin-off described

above. However, for consolidated accounting purposes the financial entity represented by the

former Hafslund ASA Group is continued as the reporting entity. Since Hafslund AS acquired three

of four business areas in the spin-off, the consolidated financial statements of Hafslund AS are

deemed to represent a continuation of the former Hafslund ASA Group. Consequently, the values

have not been re-measured in the Hafslund AS Group. The disposal of the power production

segment is recognised in the consolidated financial statements as a reduction in equity as a result

of the spin-off in the statement of changes in equity. The results of the power production business

for the period 1 January 2016 to the spin-off date are recognised under the result from

discontinued operations.

Immediately after the spin-off, Hafslund AS sold 100 percent of the shares in the subsidiary

Hafslund Marked AS and 50 per cent of the shares in the subsidiary Hafslund Varme AS to

Fortum.

The gain on the sale of the shares in Hafslund Market AS is recognised in the consolidated

financial statements as the difference between the carrying amount in the Group and the

consideration received. The results from the Markets segment for the period 1 January 2016 to the

disposal date are recognised in the result from discontinued operations together with the gain.

The sale of 50 per cent of the shares in Hafslund AS is recognised in the consolidated financial

statements as a sell-off with loss of control. The residual shareholding is measured at fair value,

with the resulting upwards revaluation recognised in income. The results from the Heat segment

for the period from 1 January 2016 to the disposal date are recognised in the result from

discontinued operations together with the associated gains.

13 QUARTERLY REPORT Q3 2017

The residual 50 percent shareholding in Hafslund Varme AS, and receivables due from Fortum

following the disposal of the shares in Hafslund Varme AS and Hafslund Marked AS, were

distributed as a non-cash asset to Oslo Energi Holding AS as of 30 September 2017. This

distribution is recognised at fair value in the consolidated financial statements.

The consideration for all the above transactions was measured at fair value and subject to normal

purchase sum calculations. The result from discontinued operations is based on the latest

estimated purchase sum calculations available at the balance sheet date. It is expected that the

final purchase figures and settlement will be completed in fourth-quarter 2017. Preliminary

calculations indicate that Hafslund's cash holdings will be reduced by approximately NOK 250

million, mainly as a result of tax and working capital adjustments.

Result from discontinued operations

NOK million Ytd 2017 2016

Operating revenues 5,428 9,126

Operating expenses (4,660) (7,898)

Net financial items (47) (69)

Profit before tax 721 1,159

Tax expense (244) (418)

Net profit for the period 477 741

Profit after tax 3,372

Result from discontinued operations 3,849 741

3) Networks – income ceiling and income surpluses/shortfalls

Permitted income for the year

Electrical power is distributed via networks, which represent a natural monopoly within the individual

network business’s geographic area. The Norwegian Water Resources and Energy Directorate

(NVE) therefore establishes an income ceiling that represents the maximum income level the

networks businesses are allowed to collect in network rental, and which is intended to provide a

reasonable return on invested capital, and to cover normal operating and maintenance expenses.

The regulated income ceiling, plus re-invoicing of expenses from the overhead network (Statnett)

are referred to as permitted income and established for the year as a whole.

Actual income for the year

Actual income (tariff income) for a network company comprises the tariffs, power output and actually

transmitted energy volumes at any one time in the network company’s supply area. In accordance

with IFRSs, income is recognised in the Networks business based on actual income for the year,

and not permitted income as described above. However, the tariffs, or network rental, are

established based on the premise that over time actual income will correspond to the permitted

income for the Networks business.

Annual income surpluses and shortfalls

Permitted income will normally deviate from actual income for the year due to the effect of the

weather and temperatures on the transmitted volume in the network. If actual income is higher than

permitted income, this results in an income surplus; and if it is lower, in an income deficit. Under

IFRSs, income surpluses and income shortfalls are defined as regulated liabilities or assets that do

not qualify for balance-sheet recognition. This is justified on the grounds that a contract has not been

entered into with a particular customer and therefore the resulting receivable/liability is theoretically

contingent on a future delivery.

At the end of 2016, Networks had an accumulated income surplus of NOK 187 million. According

the available forecasts, accumulated surplus income is expected to increase to around NOK 310

million by the end of 2017. The increase in surplus income is partly due to Hafslund Nett’s desire to

maintain the network rental charge as stable as possible.

4) Interest-bearing loans and interest and currency derivatives

At the end of the third quarter of 2017, the value of the loan portfolio recognised in the balance sheet

amounted to NOK 8,386 million, of which NOK 6,583 million related to long-term liabilities and NOK

1,803 million to current liabilities. The change in the fair value of the loans boosted profits by NOK

51 million in the third quarter, while the change in the fair value of interest rate derivatives reduced

profits by NOK 9 million. Hafslund’s credit spreads narrowed by 30–40 basis points for maturities of

between three months and ten years during the reporting period. The Nibor and swap rates fell by

up to 40 basis points for maturities of up to one year and by 10 to 20 basis points for terms of two to

five years. The interest rates for longer terms remained virtually unchanged. The net effect of the

above was that the market interest rate (including Hafslund’s credit spreads) narrowed by around 60

to 70 basis points for maturities of up to one year and by around 40 basis points for longer maturities.

The change in the fair value of loans is recognised as financial expenses in the income statement,

while any change in the value of interest rate derivatives is recognised as a net financial item in the

operating result.

14 QUARTERLY REPORT Q3 2017

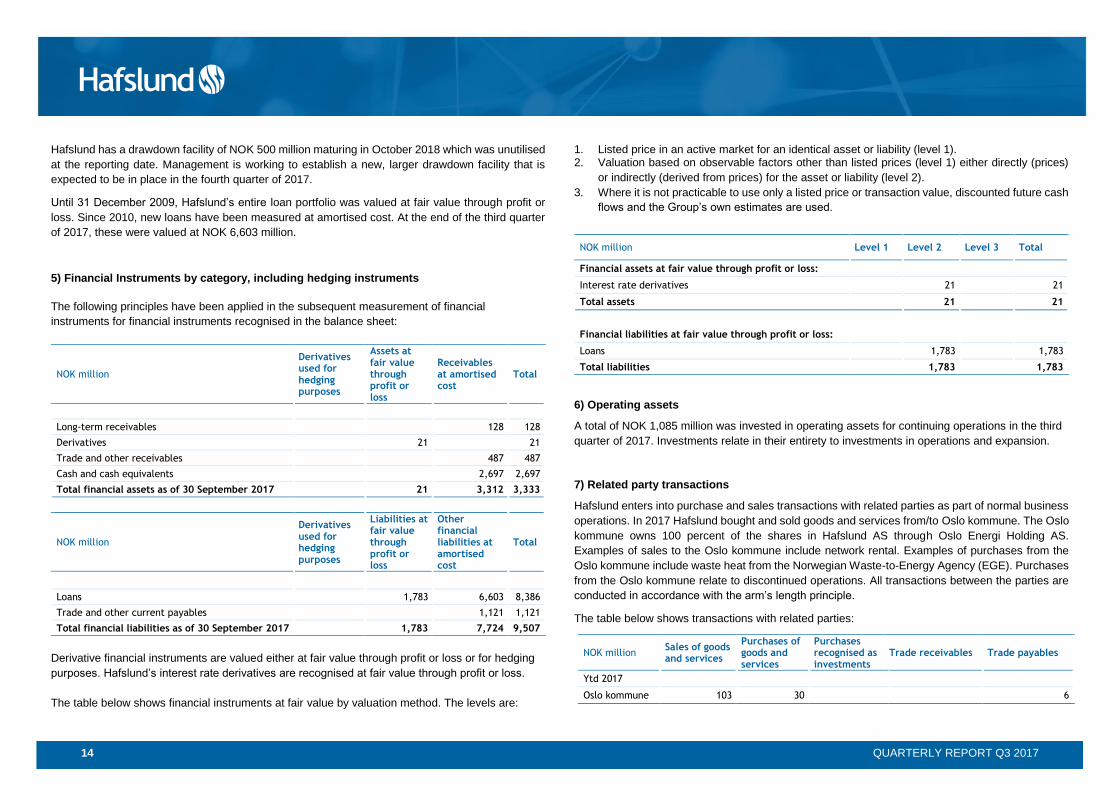

Hafslund has a drawdown facility of NOK 500 million maturing in October 2018 which was unutilised

at the reporting date. Management is working to establish a new, larger drawdown facility that is

expected to be in place in the fourth quarter of 2017.

Until 31 December 2009, Hafslund’s entire loan portfolio was valued at fair value through profit or

loss. Since 2010, new loans have been measured at amortised cost. At the end of the third quarter

of 2017, these were valued at NOK 6,603 million.

5) Financial Instruments by category, including hedging instruments

The following principles have been applied in the subsequent measurement of financial

instruments for financial instruments recognised in the balance sheet:

NOK million

Derivatives used for hedging purposes

Assets at fair value through profit or loss

Receivables at amortised cost

Total

Long-term receivables 128 128

Derivatives 21 21

Trade and other receivables 487 487

Cash and cash equivalents 2,697 2,697

Total financial assets as of 30 September 2017 21 3,312 3,333

NOK million

Derivatives used for hedging purposes

Liabilities at fair value through profit or loss

Other financial liabilities at amortised cost

Total

Loans 1,783 6,603 8,386

Trade and other current payables 1,121 1,121

Total financial liabilities as of 30 September 2017 1,783 7,724 9,507

Derivative financial instruments are valued either at fair value through profit or loss or for hedging

purposes. Hafslund’s interest rate derivatives are recognised at fair value through profit or loss.

The table below shows financial instruments at fair value by valuation method. The levels are:

1. Listed price in an active market for an identical asset or liability (level 1). 2. Valuation based on observable factors other than listed prices (level 1) either directly (prices)

or indirectly (derived from prices) for the asset or liability (level 2).

3. Where it is not practicable to use only a listed price or transaction value, discounted future cash

flows and the Group’s own estimates are used.

NOK million Level 1 Level 2 Level 3 Total

Financial assets at fair value through profit or loss:

Interest rate derivatives 21 21

Total assets 21 21

Financial liabilities at fair value through profit or loss:

Loans 1,783 1,783

Total liabilities 1,783 1,783

6) Operating assets

A total of NOK 1,085 million was invested in operating assets for continuing operations in the third

quarter of 2017. Investments relate in their entirety to investments in operations and expansion.

7) Related party transactions

Hafslund enters into purchase and sales transactions with related parties as part of normal business

operations. In 2017 Hafslund bought and sold goods and services from/to Oslo kommune. The Oslo

kommune owns 100 percent of the shares in Hafslund AS through Oslo Energi Holding AS.

Examples of sales to the Oslo kommune include network rental. Examples of purchases from the

Oslo kommune include waste heat from the Norwegian Waste-to-Energy Agency (EGE). Purchases

from the Oslo kommune relate to discontinued operations. All transactions between the parties are

conducted in accordance with the arm’s length principle.

The table below shows transactions with related parties:

NOK million Sales of goods and services

Purchases of goods and services

Purchases recognised as investments

Trade receivables Trade payables

Ytd 2017

Oslo kommune 103 30 6

15 QUARTERLY REPORT Q3 2017

Definitions

Capital employed Equity + Net interest-bearing liabilities + Net tax positions

NVE capital Finished non-current assets including a fixed percentage add-on for working capital

Equity ratio Equity / Total capital

Net interest-bearing liabilities Interest-bearing liabilities - Interest-bearing receivables and cash equivalents

Liabilities / EBITDA Net interest-bearing liabilities / EBITDA for the last 12 months

16 QUARTERLY REPORT Q3 2017

Financial calendar

1. Fourth Quarter 2017 Report and provisional annual result – 15 February 2018

2. First Quarter 2018 Report – 2 May 2018

3. Second Quarter 2018 Report – 10 July 2018

4. Third Quarter 2018 Report – 24 October 2018

Investor information

1. Information is displayed on Hafslund's website:

o www.hafslund.no

o You can subscribe to stock market notifications via "My page" at www.oslobors.no

2. CFO, Heidi Ulmo,

o Tel.: +47 909 19 325

3. Head of Finance and Investor Relations, Martin S. Lundby

o Tel.: +47 416 14 448

![Jerusalem Quarterly Winter 2011 [in Colonial Shoes -- Notes on the Material Afterlife in Post-Oslo Palestine]](https://img.pdfslide.us/doc/110x75/577d222f1a28ab4e1e96c649/jerusalem-quarterly-winter-2011-in-colonial-shoes-notes-on-the-material.jpg)