Embed Size (px)

Citation preview

DIGITAL COMMERCE TODAY. QUANTUM COMMERCE TOMORROW.

Is your business readyto take the leap?

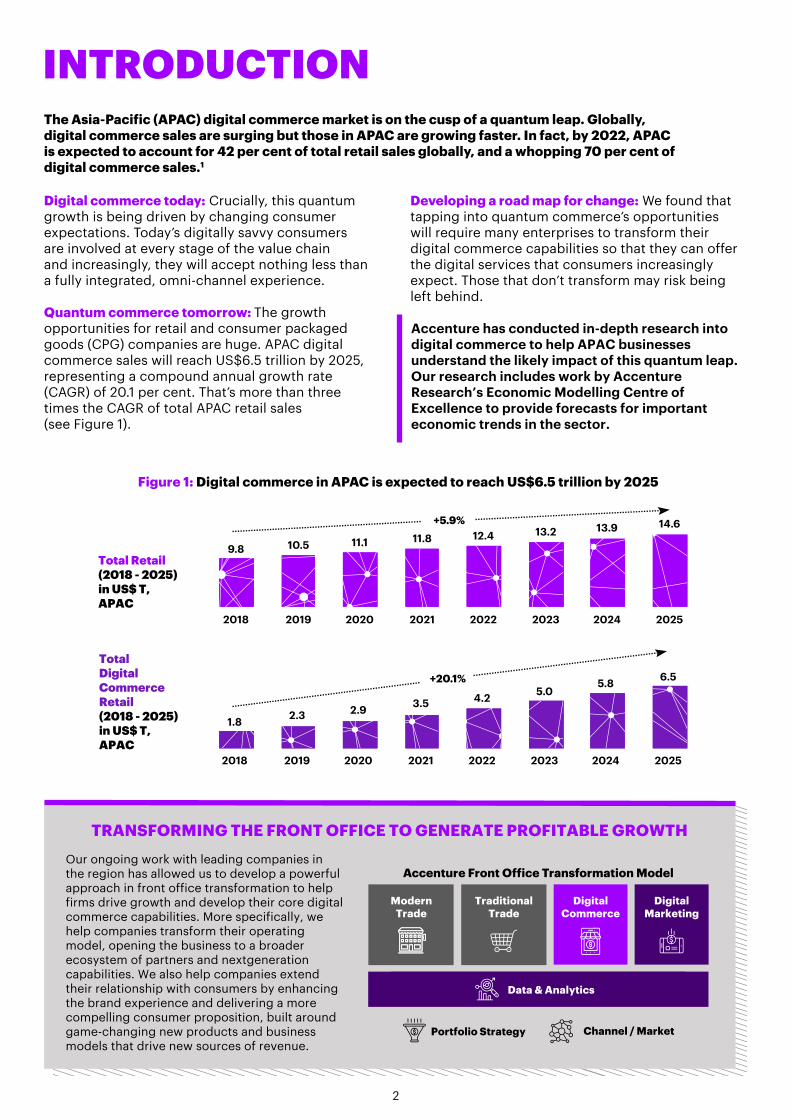

INTRODUCTION

Digital commerce today: Crucially, this quantumgrowth is being driven by changing consumerexpectations. Today’s digitally savvy consumersare involved at every stage of the value chainand increasingly, they will accept nothing less thana fully integrated, omni-channel experience.

Quantum commerce tomorrow: The growthopportunities for retail and consumer packagedgoods (CPG) companies are huge. APAC digitalcommerce sales will reach US$6.5 trillion by 2025,representing a compound annual growth rate(CAGR) of 20.1 per cent. That’s more than threetimes the CAGR of total APAC retail sales(see Figure 1).

Developing a road map for change: We found thattapping into quantum commerce’s opportunitieswill require many enterprises to transform theirdigital commerce capabilities so that they can offerthe digital services that consumers increasinglyexpect. Those that don’t transform may risk beingleft behind.

Accenture has conducted in-depth research into digital commerce to help APAC businesses understand the likely impact of this quantum leap. Our research includes work by AccentureResearch’s Economic Modelling Centre of Excellence to provide forecasts for important economic trends in the sector.

TRANSFORMING THE FRONT OFFICE TO GENERATE PROFITABLE GROWTH

Our ongoing work with leading companies in the region has allowed us to develop a powerful approach in front office transformation to help firms drive growth and develop their core digital commerce capabilities. More specifically, we help companies transform their operating model, opening the business to a broader ecosystem of partners and nextgeneration capabilities. We also help companies extend their relationship with consumers by enhancing the brand experience and delivering a more compelling consumer proposition, built around game-changing new products and business models that drive new sources of revenue.

ModernTrade

TraditionalTrade

DigitalCommerce

DigitalMarketing

Data & Analytics

Portfolio Strategy Channel / Market

Accenture Front Office Transformation Model

Figure 1: Digital commerce in APAC is expected to reach US$6.5 trillion by 2025

Total Retail (2018 - 2025) in US$ T, APAC

Total Digital CommerceRetail (2018 - 2025) in US$ T, APAC

2018 2019 2020 2021 2022 2023 2024 2025

9.8 10.5 11.1 11.8 12.4 13.2 13.9 14.6+5.9%

2018 2019 2020 2021 2022 2023 2024 2025

1.8 2.3 2.9 3.5 4.2 5.05.8 6.5+20.1%

The Asia-Pacific (APAC) digital commerce market is on the cusp of a quantum leap. Globally, digital commerce sales are surging but those in APAC are growing faster. In fact, by 2022, APAC is expected to account for 42 per cent of total retail sales globally, and a whopping 70 per cent of digital commerce sales.1

2

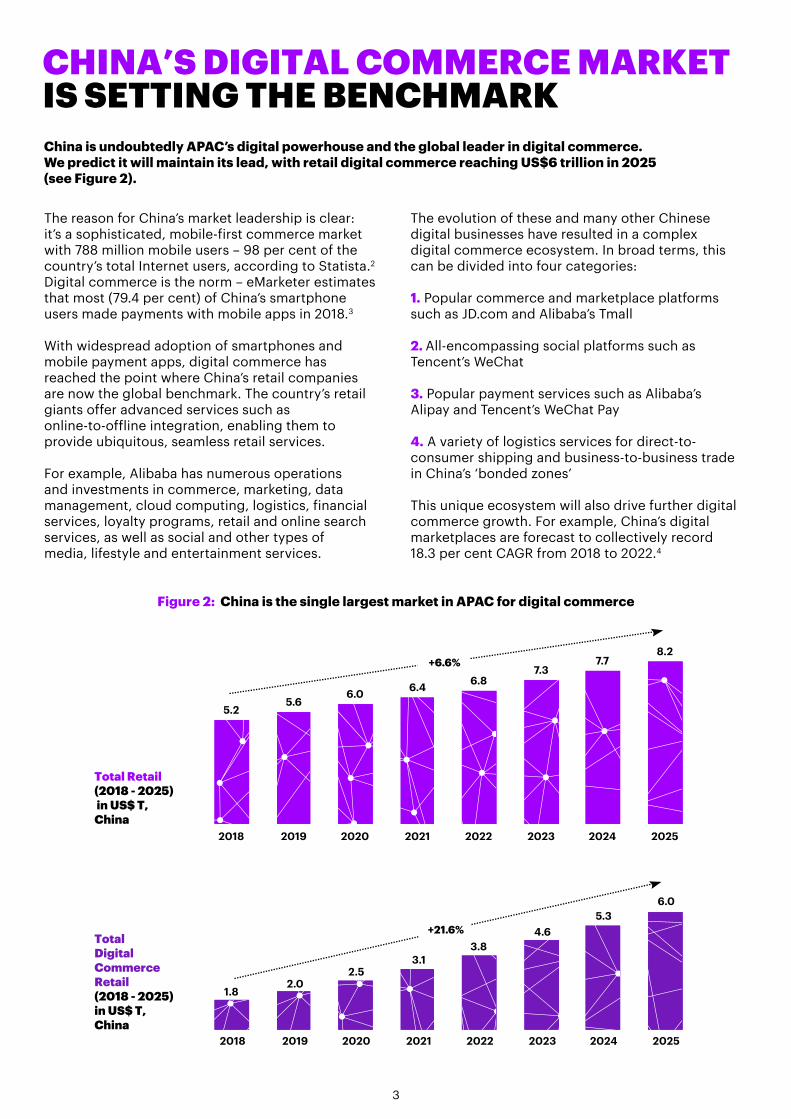

CHINA’S DIGITAL COMMERCE MARKETIS SETTING THE BENCHMARKChina is undoubtedly APAC’s digital powerhouse and the global leader in digital commerce. We predict it will maintain its lead, with retail digital commerce reaching US$6 trillion in 2025 (see Figure 2).

The reason for China’s market leadership is clear:it’s a sophisticated, mobile-first commerce marketwith 788 million mobile users – 98 per cent of thecountry’s total Internet users, according to Statista.2

Digital commerce is the norm – eMarketer estimatesthat most (79.4 per cent) of China’s smartphoneusers made payments with mobile apps in 2018.3

With widespread adoption of smartphones andmobile payment apps, digital commerce hasreached the point where China’s retail companiesare now the global benchmark. The country’s retailgiants offer advanced services such asonline-to-offline integration, enabling them toprovide ubiquitous, seamless retail services.

For example, Alibaba has numerous operationsand investments in commerce, marketing, datamanagement, cloud computing, logistics, financialservices, loyalty programs, retail and online searchservices, as well as social and other types ofmedia, lifestyle and entertainment services.

The evolution of these and many other Chinesedigital businesses have resulted in a complexdigital commerce ecosystem. In broad terms, thiscan be divided into four categories:

1. Popular commerce and marketplace platformssuch as JD.com and Alibaba’s Tmall

2. All-encompassing social platforms such asTencent’s WeChat

3. Popular payment services such as Alibaba’sAlipay and Tencent’s WeChat Pay

4. A variety of logistics services for direct-to-consumer shipping and business-to-business trade in China’s ‘bonded zones’

This unique ecosystem will also drive further digitalcommerce growth. For example, China’s digitalmarketplaces are forecast to collectively record18.3 per cent CAGR from 2018 to 2022.4

Figure 2: China is the single largest market in APAC for digital commerce

Total Digital Commerce Retail (2018 - 2025) in US$ T, China

2018 2019 2020 2021 2022 2023 2024 2025

5.25.6

6.0 6.4 6.87.3

7.78.2

+6.6%

Total Retail (2018 - 2025) in US$ T, China

2018 2019 2020 2021 2022 2023 2024 2025

1.82.0

2.53.1

3.84.6

5.36.0

+21.6%

3

APAC IS POISED FOR A QUANTUM LEAP IN DIGITAL COMMERCEResearch shows that the retail and CPG industries in the rest of APAC look set to follow China’s digital commerce lead, ushering in a quantum leap in growth for the sector across the region. Indeed, Accenture predicts that

Figure 3: ASEAN digital commerce is expected to grow at 3 times of the overall retail growth

Total Digital Commerce Retail (2018 - 2025) in US$ B, ASEAN

2018 2019 2020 2021 2022 2023 2024 2025

880.2 932.3 984.5 1,034.6 1,082.9 1,145.6 1,209.9 1,279.6+5.5%

Total Retail(2018 - 2025) in US$ B, ASEAN

2018 2019 2020 2021 2022 2023 2024 2025

23.5 28.1 33.1 38.5 44.3 51.358.9 67.4+16.3%

• The region’s home to an increasingly connected, expanding urban middle class. While ASEAN remains highly diverse, the number of middle-class households is forecast to more than quadruple to 161 million by 2030.5

• At the same time, hundreds of millions of digitally savvy millennials are now coming into their prime spending years. By one estimate, half of APAC’s population will be aged between 18 and 35 by 2020.6

• APAC’s consumers are also becoming more connected. The region is already home to 55.8 per cent of the world’s Internet users, according to eMarketer. That’s more than 2 billion connected consumers, a figure that is expected to jump to nearly 2.5 billion by 2022.7

• Smartphones are the device of choice for APAC consumers, accounting for 61 per cent of the region’s Internet connections. The GSMA expects that figure to surge to 91 per cent by 2025, when the region will have 3.9 billion smartphones.8

digital commerce in ASEAN will reach US$67.4 billion in sales, representing a CAGR of 16.3 per cent. That’s three times the growth of total retail sales in the region (see Figure 3).

Rest of the world Asia Pacific Note: Inner chart: 2016; Outer chart: 2030

GDP

Shift from“export driven” to

“consumption driven”

CONSUMER EXPENDITURE

URBAN POPULATION

The rise of the “self”and “spend” -

centered consumer

Home to 17 megacities,3 of which are the world’s largest

(Tokyo, Delhi and Shanghai).22 megacities by 2030

POPULATION WITH

INCOME >US$150K

Regions High Net WorthIndividuals (HNWI)wealth would be

>US$42 trillion by 2025

Figure 4: APAC emerges strongly as the new growth frontier

At the same time, governments in the region are seizing the opportunity to contribute to the spread of digitalization through a range of initiatives. The Singapore Government, for example, has launched numerous digital initiatives under its Smart Nation programme – including PayNow, its new real-time payment platform, which is already being used by 1.4 million residents.9 The Indonesian Government also has a number of programmes, including one to create 1,000 high-tech startups by 2020.10

Businesses in APAC are also investing heavily in digital services, a trend that’s set to make a profound impact. International Data Corporation (“IDC”) predicts that by 2021, digital products and services will account for 60 per cent of APAC’s gross domestic product – a tenfold increase from 2017.11

The critical factors fuelling such a leap include a growing consumer base, among other aspects (see Figure 4):

4

THE RETAIL AND CPG CHALLENGE:PREPARE OR PERISH

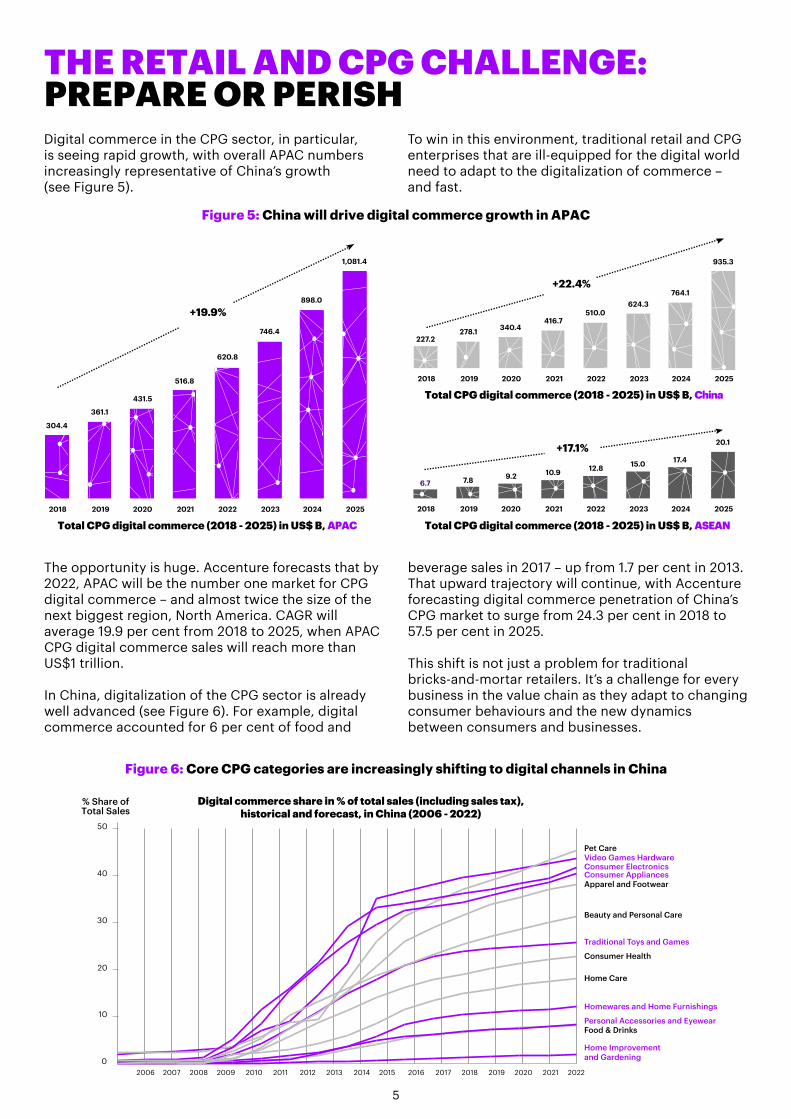

Figure 5: China will drive digital commerce growth in APAC

2018 2019 2020 2021 2022 2023 2024 2025

304.4

361.1

431.5

516.8

620.8

746.4

898.0

1,081.4

+19.9%

Total CPG digital commerce (2018 - 2025) in US$ B, APAC Total CPG digital commerce (2018 - 2025) in US$ B, ASEAN

2018 2019 2020 2021 2022 2023 2024 2025

227.2278.1 340.4

416.7510.0

624.3764.1

935.3

+22.4%

Total CPG digital commerce (2018 - 2025) in US$ B, China

2018 2019 2020 2021 2022 2023 2024 2025

6.7 7.8 9.2 10.9 12.8 15.0 17.4

20.1+17.1%

The opportunity is huge. Accenture forecasts that by 2022, APAC will be the number one market for CPG digital commerce – and almost twice the size of the next biggest region, North America. CAGR will average 19.9 per cent from 2018 to 2025, when APAC CPG digital commerce sales will reach more than US$1 trillion.

In China, digitalization of the CPG sector is already well advanced (see Figure 6). For example, digital commerce accounted for 6 per cent of food and

beverage sales in 2017 – up from 1.7 per cent in 2013.That upward trajectory will continue, with Accenture forecasting digital commerce penetration of China’s CPG market to surge from 24.3 per cent in 2018 to 57.5 per cent in 2025.

This shift is not just a problem for traditional bricks-and-mortar retailers. It’s a challenge for every business in the value chain as they adapt to changing consumer behaviours and the new dynamics between consumers and businesses.

Video Games HardwareConsumer ElectronicsConsumer Appliances

Traditional Toys and Games

Homewares and Home Furnishings

Home Improvementand Gardening

Personal Accessories and Eyewear

Pet Care

Apparel and Footwear

Beauty and Personal Care

Consumer Health

Home Care

Food & Drinks

50

% Share ofTotal Sales

40

30

20

10

0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Digital commerce share in % of total sales (including sales tax),historical and forecast, in China (2006 - 2022)

Figure 6: Core CPG categories are increasingly shifting to digital channels in China

Digital commerce in the CPG sector, in particular, is seeing rapid growth, with overall APAC numbersincreasingly representative of China’s growth (see Figure 5).

To win in this environment, traditional retail and CPG enterprises that are ill-equipped for the digital world need to adapt to the digitalization of commerce – and fast.

5

UNDERSTANDING THEDIGITAL-FIRST CONSUMERThe new breed of digital-first consumers hasunprecedented choice and flexibility in how, when and where they shop. Where once businesses would dictate their product development, marketing, distribution and pricing, that power is now being transferred to consumers.

Digital consumers can easily compare prices and access reviews of products from anywhere in the world. If they find a better-value option or have a bad consumer experience, they can simply move to another brand or supplier.

In addition, consumers are now more involved in allaspects of the value chain (see Figure 7). Social media and intelligent new tools such as chatbots

R&D and Financing

Marketing& Sales

StoreExecutionInnovation Marketing Manufacturing Distribution

CROWDSOURCING,CROWDFUNDING

CONSUMER INSIGHTS

Coca-Cola

Creyate

OPEN INNOVATION,PERSONALIZATION

FlipkartUberRUSH

The DIY SecretsMAKE @ HOME

LAST MILE PARTNERS

MeetupCONTENT,COMMUNITY

Field AgentEtsy

SOCIALCOMMERCE

CONSUMER INTIMACY,CONSUMER AS EMPLOYEE

Operations in Singapore

BrewSmith

PinkPi

MyFit

Figure 7: Consumers are now integrated into all parts of the value chain

are transforming marketing and after-sales support. Consumers also have far greater influence over each other, and they receive rapid responses to their aftersales issues. Clever new social media campaigns allow consumers to participate in tasks traditionally performed by staff – such as naming new products.

Consumers also have greater power over how products are delivered, through disruptive new services such as food delivery apps. They are even actively participating in product development through crowdsourcing and crowdfunding. Coca-Cola, for example, recently used a crowd-funding platform to gauge consumer demand for the premium water brand Valser.

6

IDENTIFYING THE UPSIDE OF DISRUPTIONAll this change is having a huge disruptive effect on traditional businesses. However, the upside for businesses is that this change can greatly accelerate their responsiveness to market changes.

By tracking social networks, for example, businesses can receive immediate feedback on a new product or service, including competitive offerings.

Product development can traditionally take years,requiring extensive research and development, and numerous focus groups. By comparison, Coca-Cola’s Valser crowdfunding campaign took a month.

Digital platforms along with data analytics allow businesses to better engage with consumer

through personalization, such as sending customised offers. This can even extend to bricks-and-mortar stores, using beacon technology. These tiny devices provide location services for indoor navigation and other cloud and mobile apps, greatly enhancing the physical shopping experience.

Crucially, the rise of digital commerce doesn’t mean the end of bricks-and-mortar retailing. However, it could spell the end for companies that remain bogged down with the old ways of doing business.

A DIGITAL ROADMAPFOR CHANGE

Clearly, traditional businesses need to transform – starting with fundamental changes to their business values and models. Businesses need to shift from their traditional supply-led model to a consumer-led one – where consumers are engaged throughout the value chain. Only by making this conscious shift will businesses be able to make the other necessary changes, which include:

• Undergoing a comprehensive digital transformation across the business – from product development to marketing and after-sales support

• Engaging with consumers across the value chain through digital channels and by offering personalised experiences

• Investing heavily in mobile technology – the most vital digital channel in APAC

• Understanding and, where suitable, adopting powerful new digital tools, such as chatbots, artificial intelligence and beacon technology

• Regularly assessing their value offering in comparison with competitors, and improving that offering through pricing changes, new services or other value-adds

• Leveraging the selling power of third-party digital marketplaces, such as Alibaba, JD.com and Amazon.

That’s a lot of change. To achieve it, businesses will need to undertake a challenging journey that’s virtually impossible to complete without a trusted partner with broad and deep digitalization experience and expertise.

7

THE WAY FORWARD:YOUR TRUSTEDPARTNER FORQUANTUM COMMERCEAccenture has that experience and expertise. Specifically, Accenture has a centre of excellence for quantum commerce that can help businesses take the leap into digital commerce and transform their capabilities to thrive and grow.

We can also help your business apply Accenture’s Digital Commerce Control Tower, a comprehensive approach for all digital commerce needs, ranging from supply chain and operations to digital marketing.

8

DigitalCommerce

ValueAssessment

DigitalCommerce

ConsumerExperience

DigitalCommerce

SupplyChain

DigitalCommerce

DemandGeneration

DigitalCommerceOperations

DigitalCommerceTechnology

Enablers

DigitalCommerce

Analytics

ACCENTURE DIGITAL COMMERCE CONTROL TOWER

9

REFERENCES1 eMarketer. Forecasts: eMarketer estimates and historical data; Accenture Research.

2 Forbes (2018, 23 August). China Now Boasts More Than 800 Million Internet Users And 98% Of Them Are Mobile.https://www.forbes.com/sites/niallmccarthy/2018/08/23/china-now-boasts-more-than-800-million-internet-users-and-98-of-them-are-mobileinfographic/#2ac183c47092

3 eMarketer (2018, 17 December). Global Proximity Mobile Payment Users.https://www.emarketer.com/content/global-proximity-mobile-payment-users

4 PlanetRetail (2018, Jan 30). Future Retail Disruption: China STEIP 2018.

5 The Economist Intelligence Unit (2018). ASEAN cities – Stirring the melting pot.

6 Asia House (2017, 6 July). Asian Millennials leading new APAC trends.https://asiahouse.org/millennials-asia-panel/

7 eMarketer (2018, July).

8 GSMA (2018). The Mobile Economy Asia Pacific 2018.https://www.gsma.com/mobileeconomy/asiapacific/

9 Monetary Authority of Singapore (2018, 20 June). E-Payments for Everyone - keynote speech by Mr Ong Ye Kung, Minister for Education and MAS’ Board Member.http://www.mas.gov.sg/News-and-Publications/Speeches-and-Monetary-Policy-Statements/Speeches/2018/EPayments-for-Everyone.aspx

10 The Jakarta Post (2016, 11 November). Indonesia wants to lead the region in e-commerce.https://www.thejakartapost.com/news/2016/11/11/indonesia-wants-to-lead-the-region-in-e-commerce.html

11 Microsoft and IDC (2018, 21 February). Unlocking the Economic Impact of Digital Transformation in Asia Pacific.https://news.microsoft.com/apac/features/digital-transformation/

ABOUT ACCENTURE

ABOUT ACCENTURE RESEARCH

Accenture is a leading global professional services company, providing a broad range of services and solutions in strategy, consulting, digital, technology and operations. Combining unmatched experience and specialized skills across more than 40 industries and all business functions—underpinned by the world’s largest delivery network—Accenture works at the intersection of business and technology to help clients improve their performance and create sustainable value for their stakeholders. With 477,000 people serving clients in more than 120 countries, Accenture drives innovation to improve the way the world works and lives. Visit us at www.accenture.com.

Our extensive research into digital commerce included work by Accenture Research’s Economic Modelling Centre of Excellence, a specialised unit focusing on economic modelling, statistical and econometric analysis and forecasting.For this paper, the Economic Modelling Centre of Excellence provided retail and digital commerce forecasts to 2025 for APAC and selected countries. The forecasts were made using Autoregressive Distributed Lag models and estimates for digital commerce evolution based on the Diffusion of Innovation Model. Accenture’s research included analysis of data from thirdparties, including eMarketer, Euromonitor International, PlanetRetail and Statista.

AUTHORSFabio VacircaSenior Managing Director,Products Operating Group, Asia-Pacific, Africa, Middle East and [email protected]

Mohammed SirajuddeenManaging Director,Digital Commerce Lead,Products Operating Group, [email protected]

Copyright © 2019 Accenture All rights reserved.

Accenture, its logo, and New Applied Now are trademarks of Accenture. Any third-party names or trademarks contained in this document are the property of their respective owners. No sponsorship, endorsement or approval of this content by the owners of such names or trademarks is intended, expressed or implied.