Embed Size (px)

Citation preview

Inigo Fraser Jenkins

+44 20 7102 4658

Nomura Global Quantitative Equity Conference in London

+44 20 7102 4658

Quantitative Equity StrategyMay 2011

© Nomura International plc© Nomura International plc

C t tContents

P f f t d l i th t i t Performance of quant models in the current environment

The factor outlook

Four views on current areas of quant development:

1 Is there a case for minimum variance? 1. Is there a case for minimum variance?

2. Improving performance through timing of screening

3. Factor rotation

4 Non-linear interaction factors have been working recently4. Non linear interaction factors have been working recently

1

Source: Nomura Equity Strategy

N Gl b l Q t B h k i d l ti t k tNomura Global Quant Benchmark index relative to market

2 Jan 06 = 100

111

113

Inferno Purgatorio Paradiso??

107

109 equal-weighted relative

asset weighted relative

103

105

99

101

95

97

06 06 06 06 07 07 07 07 08 08 08 08 09 09 09 09 10 10 10 10 -11

-11

-11

Figure shows the performance of equal-weighted and asset-weighted quant fund indices relative to the global market and also the absolute return of the Hedge Fund Research Equity Market Neutral index. Source: Hedge Fund Research, Bloomberg, Nomura Equity Strategy research

Jan-

Apr

-

Jul-

Oct

-

Jan-

Apr

-

Jul-

Oct

-

Jan-

Apr

-

Jul-

Oct

-

Jan-

Apr

-

Jul-

Oct

-

Jan-

Apr

-

Jul-

Oct

-

Jan -

Apr

-

Jul-

2

M t M d lMeta Model

tttttt MomentumGrowthValueCorrelr 4321:

Where Correl is the average pairwise correlation between stocks. Value, Growth and Momentum all refer to th di i f th f t th k t

β s.e. t-statistic

C l i 48 2 11 3 4 3

the dispersion of these factors across the market.

Correlation -48.2 11.3 -4.3

Value -17.1 9.6 -1.8

Growth 2.8 0.4 6.7Growth 2.8 0.4 6.7

Momentum -0.6 0.5 -1.2

Constant -10.6 8.1 -1.3

R2 0.7

3

Source: Nomura Equity Strategy

P di t d t t

35

Predicted quant returns%

20

25

30 Realised 12m FWD Return

Predicted 12m FWD Return

5

10

15

-5

0

5

-15

-10

ay-0

0

ay-0

1

ay-0

2

ay-0

3

ay-0

4

ay-0

5

ay-0

6

ay-0

7

ay-0

8

ay-0

9

ay-1

0

Ma

Ma

Ma

Ma

Ma

Ma

Ma

Ma

Ma

Ma

Ma

The quant proxy for which we are forecasting 12 -month forward return (r) is the Nomura Quant Benchmark . Before 2006, we use a sector-neutral blend of P/E and 12 -month price momentum combined using a simple average approach for the quant proxy. We use a regression based approach to forecast the 12 -month forward returns using average pairwise correlation between global stocks and dispersion of value, growth and momentum as detailed in Quant and Existentialism , 9 October 2010.

Source: Nomura Strategy Research

ANY AUTHORS NAMED ON THIS REPORT ARE RESEARCH ANALYSTS UNLESS OTHERWISE INDICATED.PLEASE SEE ANALYST(S) CERTIFICATION(S) ON SLIDE 2 AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 4. 4

A l ti f t k Gl b l d USAverage correlation of stocks Global and US

0.450.9Correlation Correlation

0.35

0.40

0.7

0.8

0.25

0.30

0.35

0.5

0.6

0.7

0.15

0.20

0.25

0.3

0.4

0.5

0 05

0.10

0.15

0 1

0.2

0.3

75 day mean pair wise

Median 63-day correlation of S&P 500 stocks to the S&P 500 index (LHS)

0.00

0.05

0

0.1

pr-7

2

pr-7

4

pr-7

6

pr-7

8

pr-8

0

pr-8

2

pr-8

4

pr-8

6

pr-8

8

pr-9

0

pr-9

2

pr-9

4

pr-9

6

pr-9

8

pr-0

0

pr-0

2

pr-0

4

pr-0

6

pr-0

8

pr-1

0

75 day mean pair-wise correlation (Global) (RHS)

Global correlation is defined as the mean of all the pairwise correlations between stocks over the prior 75 days. Universe is the 500 largest stocks in the FTSE World index. US correlation is the median 63-Day correlation of S&P 500 Stocks to the S&P 500 Index. Source: Nomura Equity Strategy, Ned Davis

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

Ap

5

A l ti f t k (E )Average correlation of stocks (Europe)

Correlation

0.5

0.6

0.4

0.5

0.3

0 1

0.2

0.0

0.1

00 00 01 01 02 02 03 03 04 04 05 05 06 06 07 07 08 08 09 09 10 10 11

Correlation is defined as the mean of all the pairwise correlations between stocks over the prior 75 days. Universe is the stocks that are in or ever have been in the FTSE World index. Source: Nomura Equity Strategy

Apr

-0

Oct

-0

Apr

-0

Oct

-0

Apr

-0

Oct

-0

Apr

-0

Oct

-0

Apr

-0

Oct

-0

Apr

-0

Oct

-0

Apr

-0

Oct

-0

Apr

-0

Oct

-0

Apr

-0

Oct

-0

Apr

-0

Oct

-0

Apr

-1

Oct

-1

Apr

-1

6

Di i f t d th tDispersion of expected growth rates22

Gap in expected growth, % points

16

18

20

Europe

W ld

12

14

16 World

8

10

12

4

6

2

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Chart shows the cross-sectional dispersion of expected growth rate for each region. This is defined as the median long-term expected growth of high-expected-growth names less the median for low-expected-growth names. The portfolios are defined as the top/bottom quartiles of stocks screened on long-term expected growth and FY0-FY3 expected growth. The universes used are the 300 largest stocks in the FTSE World Europe and the 500 largest companies from the FTSE World index. Portfolios are rebalanced every quarter. Source: IBES, WorldScope, FTSE, Exshare, Nomura Equity Strategy research

7

P/E V l ti f t d thP/E Valuation of expected growth

3.5Ratio

3.0EuropeWorld

2.5World

1.5

2.0

1.0

0.5

an-9

0

an-9

1

an-9

2

an-9

3

an-9

4

an-9

5

an-9

6

an-9

7

an-9

8

an-9

9

an-0

0

an-0

1

an-0

2

an-0

3

an-0

4

an-0

5

an-0

6

an-0

7

an-0

8

an-0

9

an-1

0

an-1

1

Chart shows the P/E ratio of the top/bottom quartiles of stocks screened on long-term expected growth and FY0-FY3 expected growth with stocks selected from the 300 largest stocks in the FTSE World Europe and the 500 largest companies from the FTSE World index every quarter.

Source: IBES, FTSE, Exshare, Nomura Strategy research

Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja J

8

P i /B k l ti f t d thPrice/Book valuation of expected growth

5.0Ratio

4.0

4.5

Europe

3.0

3.5

4.0World

2.0

2.5

3.0

1.0

1.5

2.0

0.5

1.0

an-9

0

an-9

1

an-9

2

an-9

3

an-9

4

an-9

5

an-9

6

an-9

7

an-9

8

an-9

9

an-0

0

an-0

1

an-0

2

an-0

3

an-0

4

an-0

5

an-0

6

an-0

7

an-0

8

an-0

9

an-1

0

an-1

1

Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja Ja

Chart shows the price/book ratio of the top/bottom quartiles of stocks screened on long-term expected growth and FY0-FY3 expected growth with stocks selected from the 300 largest stocks in the FTSE World Europe and the 500 largest companies from the FTSE World index every quarter. Source: IBES, WorldScope, FTSE, Exshare, Nomura Equity Strategy research 9

H d th t t ll di tiHow good are growth measures at actually predicting growth?

Mar 93 = 100

3000

3500 Composite Growth FY0-FY3 Growth

Trailing Earnings Trailing Revenues

Internal Growth Long Term Growth

Mar 93 = 100

2000

2500Expected Growth Price/Book

1500

2000

500

1000

0

Figure shows the ex post one year forward growth for a wide variety of growth factors. This is done by constructing high/low growth portfolios every December on these factors and track the growth in 12 month forward consensus EPS over the subsequent year. We chart the spread in cumulative earnings growth between the high and low growth portfolio which is also the data highlighted in yellow to the right of each sheet. Portfolios are selected from the 500 largest stocks in the FTSE World.Source: IBES, FTSE, WorldScope, Exshare, Nomura Equity Strategy research

10

V l ti f l / llValuation of large/small caps

Ratio

3.00

3.50

PEprice/book

2 00

2.50price/book

1.50

2.00

0.50

1.00

0.00

an-9

0ep

-90

ay-9

1an

-92

ep-9

2ay

-93

an-9

4ep

-94

ay-9

5an

-96

ep-9

6ay

-97

an-9

8ep

-98

ay-9

9an

-00

ep-0

0ay

-01

an-0

2ep

-02

ay-0

3an

-04

ep-0

4ay

-05

an-0

6ep

-06

ay-0

7an

-08

ep-0

8ay

-09

an-1

0ep

-10

Figure shows the relative P/E and price/book of the largest/smallest quartile of stocks selected from the FTSE World Europe index and rebalanced every quarter. Source: FTSE, WorldScope, Exshare, IBES, Nomura Equity Strategy research

Ja Se

M Ja Se

M Ja Se

M Ja Se

M Ja Se

M Ja Se

M J a Se

M Ja Se

M Ja Se

M J a Se

M Ja Se

11

C t T d i Q t A t M tCurrent Trends in Quant Asset Management

Quant Managers are offering wider range of models:Quant Managers are offering wider range of models:

This includes many non-benchmark strategies eg minimum variance

Strategies applied to broader universe: Emerging markets, small caps

Discretion in quant models Discretion in quant models

Looking at alternative ways of using the data that we have already: timing and interaction of factors

Factor rotation approaches

12

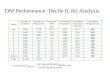

H Mi i V i b i d?Has Minimum Variance been re-priced?Cross-sectional distribution of P/E by volatility decile

18 0 PE Ratio

16 0

17.0

18.0 PE Ratio

Mar-11

Average

Average ex 99-01

14 0

15.0

16.0 Average ex 99 01

13.0

14.0

11.0

12.0

9.0

10.0

1 2 3 4 5 6 7 8 9 10

Figure shows the valuation of volatility deciles defined as the median 12 month forward PE of stocks in each decile screened on trailing 12 months volatility of returns. The universe is the 300largest stocks in the FTSE World Europe index. The portfolios have been rebalanced every quarter. The average valuation is calculated over the period January 1990 – March 2011. Source: Nomura Equity Strategy research 13

H Mi i V i b i d?Has Minimum Variance been re-priced? Slope of cross-sectional regression of P/E for volatility deciles

1.0 Regression Coefficient

0.0

0.5Valuation downward sloping with volatility

-1.0

-0.5

-2.0

-1.5

-3.0

-2.5Valuation upward

sloping with volatility

-3.5

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Figure shows the slope coefficient from a regression of the valuation of volatility deciles on a cross-sectional dummy variable. Valuation is measured as the median observation within the portfolio of consensus 12 monthforward PE. Portfolios have been created by sorting on trailing 12 month realised volatility. A negative coefficient implies that valuation is upward sloping with volatility and vice versa. The universe is the 300 largest stocks inthe FTSE World Europe index. The portfolios have been rebalanced every quarter. Source: Nomura Equity Strategy research 14

F t ffi th thFactor efficacy over the month

There are many managers who use month-end prices forThere are many managers who use month end prices for screening and then implement factor portfolios early in the month

There is evidence that this makes end-month factor t ti d tf li i l t ti l ff ticonstruction and portfolio implementation less effective

In some cases implementing just before the end of the monthIn some cases implementing just before the end of the month can lift performance

15

Source: Nomura Equity Strategy

PE d PBK b l ff ti t th dPE and PBK become less effective at month endEfficacy of factors for 3 month forward stock selection when implemented on day:

2.10

2.30

Price/bookPE

1 70

1.90

2.10

ffici

ent

PE

1 30

1.50

1.70

ssio

n co

ef

0 90

1.10

1.30

Reg

res

0.70

0.90

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31D f th

16Chart shows the regression coefficients of a regression run of 3 month forward returns on factor values screened on a given day of the month. Regressions run 2000-2011 for the 300 largest stocks in the FTSE World Europe index. Source: Nomura Equity Strategy

Day of month

Sh t t l l l ff ti t th dShort term reversal also less effective at month endEfficacy of 1 month reversal factor for 1 month forward stock selection when implemented on day:p y

0 80

1.00

0.60

0.80

effic

ient

0.20

0.40

essi

on C

oe

-0.20

0.00

Reg

re

-0.401 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31

Day of the month

17

y

Chart shows the regression coefficients of a regression run of 1 month forward returns on factor values screened on a given day of the month. Regressions run 2000-2011 for the 300 largest stocks in the FTSE World Europe index. Source: Nomura Equity Strategy

V M i t ti l b l ff ti t th dV + M interaction also becomes less effective at month endEfficacy of factors for 3 month forward stock selection when implemented on day:

2 10

2.30

2.50PBK+12m mtm (3m holding)PE+12m mtm (3m holding)PE+1m reversal (1m holding)

1 70

1.90

2.10 PE+1m reversal (1m holding)

1.30

1.50

1.70

0.90

1.10

0.701 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31

Day of Month

18Chart shows the regression coefficients of a regression run of 3 month forward returns on factor values screened on a given day of the month. Regressions run 2000-2011 for the 300 largest stocks in the FTSE World Europe index. Source: Nomura Equity Strategy

Section Header (used to create Tab s and Table of Contents)

Style selectorStyle selector

Style Ranking

Measure of Long term Measure of Short term

1/21/2

•Value (cheap) Measure of Long term

over reaction

Measure of Short term

under reaction

1/4 1/4

Value (cheap)

•Value (expensive)

•High FCF yield

•Low FCF yield

Hi h G th•High Growth

•Low Growth

•High Profitability

•Low Profitability

P/E of Style relative to

history

Price/Book of Style

relative to history

Style Momentum (12M)

•High Gearing

•Low Gearing

•High Risk

•Low Risk y•High Momentum

•Low Momentum

•Mid/Small Cap

19

P f f lt ti t l l t d l (E )Performance of alternative style selector model (Europe)450May 91= 100

350

400persistenceonly

250

300

150

200 Value + persistence

50

100 Value only

50

May

-91

Jan-

92S

ep-9

2M

ay-9

3Ja

n-94

Sep

-94

May

-95

Jan-

96S

ep-9

6M

ay-9

7Ja

n-98

Sep

-98

May

-99

Jan-

00S

ep-0

0M

ay-0

1Ja

n-02

Sep

-02

May

-03

Jan-

04S

ep-0

4M

ay-0

5Ja

n-06

Sep

-06

May

-07

Jan-

08S

ep-0

8M

ay-0

9Ja

n-10

Sep

-10

Figure shows the relative performance of attractive and unattractive styles according to a range of switching models on a long-short basis. Portfolio holdings g p y g g g g ghave been rebalanced each month. Stocks have been equally weighted within the style portfolio at the beginning of each holding period and styles are equally weighted. Style performance is on a total return, common currency basis. From 2000 a three-day implementation lag is introduced as each rebalancing point to allow for a conservative trading horizon. The investable universe is the 300 largest companies in the FTSE World Europe indexSource: Nomura, WorldScope, FTSE, Exshare 20

M d l d ti f M

This updates our ranking of European styles. We use a value and momentum approach as detailed in European Style Selector 5 June 2009 The model recommends going long styles highlighted at the top of the table and short the styles

Model recommendations for May

Selector , 5 June 2009. The model recommends going long styles highlighted at the top of the table and short the styles highlighted at the bottom.

Current PE Average PE PE (z score) Current PBKAverage Price/Book Momentum Rank on PE Rank on

Price/BookRank on

MomentumOverall Rank : 1/4 A + 1/4 B Final RankCurrent PE Average PE PE (z score) Current PBK PBK (z score) (12m) (A) Price/Book

(B)Momentum

(C)1/4 A + 1/4 B

+ 1/2 CFinal Rank

Low Profitability 12.46 14.63 -0.87 1.42 1.65 -0.53 34.93 4 7 1 3.25 1High FCF Yield 10.67 12.64 -0.84 1.75 2.09 -0.66 33.70 5 5 3 4.00 2High Gearing 12.46 14.11 -0.56 2.18 2.15 0.05 33.84 8 14 2 6.50 3Value (Expensive) 17.22 20.62 -0.53 3.95 4.59 -0.36 31.82 9 10 5 7.25 4High Growth 13.40 16.50 -0.65 2.42 3.82 -1.06 28.42 7 1 11 7.50 5Low Growth 11.21 12.89 -0.75 1.41 1.62 -0.56 28.63 6 6 9 7.50 5Low Gearing 15.57 16.83 -0.31 3.39 3.75 -0.28 32.46 13 11 4 8.00 7Large Cap 11.16 14.08 -0.90 1.80 2.38 -0.83 26.79 3 3 13 8.00 7High Risk 9.34 15.14 -1.18 1.25 2.10 -0.83 26.47 1 2 15 8.25 9Low Momentum 10 53 13 15 -0 92 1 36 1 85 -0 82 26 70 2 4 14 8 50 10Low Momentum 10.53 13.15 -0.92 1.36 1.85 -0.82 26.70 2 4 14 8.50 10Low FCF Yield 13.30 14.69 -0.52 2.45 2.12 0.53 30.74 10 16 6 9.50 11High Profitability 13.90 15.14 -0.36 4.39 4.72 -0.21 29.94 11 13 7 9.50 11High Momentum 14.51 15.54 -0.27 2.33 2.71 -0.41 28.82 14 9 8 9.75 13Value (Cheap) 9.26 9.95 -0.35 1.17 1.35 -0.52 28.40 12 8 12 11.00 14Low Risk 13.55 14.06 -0.23 2.84 2.67 0.32 28.44 15 15 10 12.50 15

Source: Nomura Strategy Research

Mid/Small Cap 12.48 12.73 -0.13 1.47 1.57 -0.22 25.07 16 12 16 15.00 16

21

I t ti f t

A normal multifactor model may select a stock as attractive if it is the cheapest in the

Interaction factor

universe but only attains a mediocre score on other factors.

This could be erroneous if what really matters is the joint score on value and t A l f thi ld bmomentum. An example of this would be:

)(... 21: tititititti MVMVr

If we make the interaction function non-linear, this will give a disproportionate weight

)( ,,,2,1:, tititititti

, g p p gto stocks were the value and momentum signal are aligned.

May help in situations of overcrowding

We use a cubic interaction function to combine factor scores

22

V l dd d f li i t ti f tValue added from non-linear interaction factor

Dec 91 = 100

125 Out of sample

Dec 91 = 100

115

120

110

105

100

Dec

-91

Dec

-92

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

D D D D D D D D D D D D D D D D D D D D

Source: Nomura Equity Strategy research 23

P f f N Gl b l M ltif t M d lPerformance of Nomura Global Multifactor Model

Dec 91 = 100

550

600

650

O t f lReturn, % pa

Annualised monthly volatility

Annualised monthly IR

Live period

450

500

550 Out of sampleWhole Period 9.97 7.14 1.40Jun 04 - Present 4.67 3.96 1.18Dec 92 - Jun 04 12.99 8.28 1.57

Live period

300

350

400

200

250

300

100

150

-91

-92

-93

-94

-95

-96

-97

-98

-99

-00

-01

-02

-03

-04

-05

-06

-07

-08

-09

-10

Out of sample is the period over which the factor coefficients have been constant. Live period is the period over which the stocks selected by the model have been published every month. Source: Nomura Equity Strategy research

24

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-

Dec

-