Embed Size (px)

Citation preview

woodmac.com Trusted Intelligence

Horacio Cuenca, Research Director, Upstream Latin America

Quantifying the Decommissioning Opportunity

A redevelopment story

2

woodmac.com

2

woodmac.com

5 bnbbl of additional oil

could be recovered from

the Campos basin

if recovery factors were

raised to US GoM or North

Sea levels

3

woodmac.com

2717 964

469

7372 1395

991

0%

20%

40%

60%

80%

100%

Campos Gulf of Mexico North Sea

WM Reserves (mmbbl) Remaining Oil in Place (mmbbl) Target

Analogues in the US Gulf of Mexico and North Sea have recovery factors of at least 30%

The average recovery factors is 15% in Campos shelf carbonates, 26% in shelf turbidites and 23% in deepwater turbidites

542 50 1533

3158 116 2656

0%

20%

40%

60%

80%

100%

Campos US Gulfof Mexico

NorthSea

Recovery

facto

r (%

)

2717 964 469

7372 1395 991

0%

20%

40%

60%

80%

100%

Campos US Gulf ofMexico

North Sea

15360 6559 398

50843 15608 886

0%

20%

40%

60%

80%

100%

Campos US Gulf ofMexico

North Sea

30% 30%

32%

8 3 3 19 98 3 21 127 1

Porosity

°API

Permeability

(mD)

Source: Wood Mackenzie Petroview, ANP, BOEM, Norwegian Petroleum Directorate

# Fields analyzed

20%-35%

20°- 35°

400

20%-35%

20°-35°

5,000

20%-35%

15°-35°

5,000

Shelf-carbonate plays (Water

depth <400m)

Shelf-turbidite plays (Water

depth <400m)

Deepwater-turbidite plays

(Water depth >400m)

Includes fields in the three regions with available information that fit the criteria. Fields were classified by their primary reservoir.

The target recovery factors are set at the lowest between US Gulf of Mexico and the North Sea.

How much higher can Campos basin recovery factors go?

4

woodmac.com

The largest Campos fields have seen lower drilling density

Infill drilling opportunities exist to increase recovery factors

Source: Wood Mackenzie Petroview, ANP

Field recovery factor vs development wells/km² of licensed area and

0%

10%

20%

30%

40%

50%

60%

70%

80%

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0

Re

co

ve

ry f

ac

tor

(%)

Drilling density (# dev wells per km²)

Other Campos basin fields Case studies before redevelopment Case studies after redevelopment

Marlim

Roncador

Polvo

Lack of drilling driving lower recovery factors

Bubble sizes represent original oil-in-place volumes

Redevelopment plans in Marlim,

Polvo and Roncador:

43 new wells will add 1.5 billion

barrels of reserves

5

woodmac.com

0 3 6 9 12 15

0

5

10

15

20

25

0 3 6 9 12 15

0

2

4

6

8

Well

Co

un

t

0.00

0.05

0.10

0.15

0.20

0.25

1976 1986 1996 2006 2016

Dri

llin

g d

en

sit

y (

de

v w

ells

pe

r k

m²)

<400m 400-1500m >1500m

New acreage

awarded in Campos

basin shallow

waters (Round 9)

2011-13: First

oil from Santos

basin pre-salt

Chasing the next frontier

Unparalleled productivity of pre-salt wells has attracted most of Petrobras investment capacity. Drilling activity in the Campos basin has fallen to historical lows

Source: Wood Mackenzie Petroview, ANP

1987/88: Albacora’s

first oil, the first in

deep waters

0 10 20 30 40

0

40

80

120

160

Well

Co

un

t

0 10 20 30 40

0

5

10

15

20

25

30Pre-salt (Campos and

Santos) Campos deepwater

turbidites

Campos shelf

turbidites

Campos shelf

carbonates

Campos basin drilling density by depth Distribution of well peak rates per play

Campos basin historical development

* Only wells with first oil in Jan/2006 or later

Well peak rate (‘000 b/d) Well peak rate (‘000 b/d)

6

woodmac.com

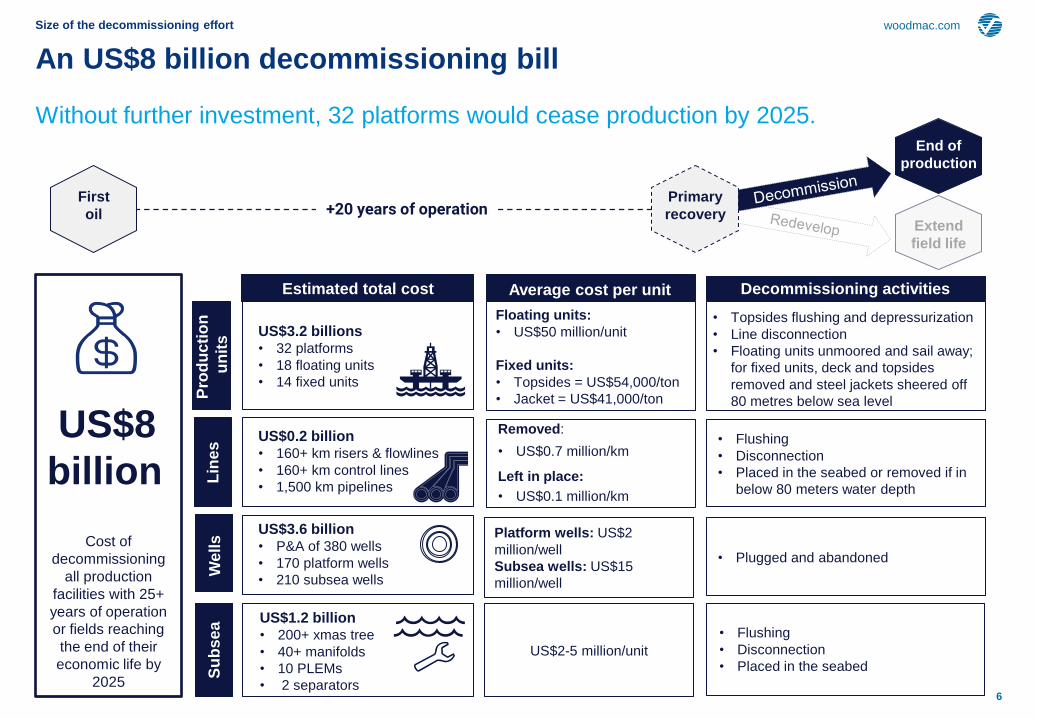

An US$8 billion decommissioning bill

Without further investment, 32 platforms would cease production by 2025.

First

oil

Primary

recovery Extend

field life

+20 years of operation

End of

production

Size of the decommissioning effort

US$8

billion*

Floating units:

• US$50 million/unit

Fixed units:

• Topsides = US$54,000/ton

• Jacket = US$41,000/ton

• Topsides flushing and depressurization

• Line disconnection

• Floating units unmoored and sail away;

for fixed units, deck and topsides

removed and steel jackets sheered off

80 metres below sea level

US$3.2 billions • 32 platforms

• 18 floating units

• 14 fixed units

Platform wells: US$2

million/well

Subsea wells: US$15

million/well

US$2-5 million/unit

US$0.2 billion • 160+ km risers & flowlines

• 160+ km control lines

• 1,500 km pipelines

US$3.6 billion • P&A of 380 wells

• 170 platform wells

• 210 subsea wells

• Flushing

• Disconnection

• Placed in the seabed or removed if in

below 80 meters water depth

• Plugged and abandoned

• Flushing

• Disconnection

• Placed in the seabed

US$1.2 billion • 200+ xmas tree

• 40+ manifolds

• 10 PLEMs

• 2 separators

Removed:

• US$0.7 million/km

Left in place:

• US$0.1 million/km

Pro

du

cti

on

un

its

L

ine

s

We

lls

S

ub

se

a

Cost of

decommissioning

all production

facilities with 25+

years of operation

or fields reaching

the end of their

economic life by

2025

Decommissioning activities Average cost per unit Estimated total cost

7

woodmac.com

Or you can redevelop.

Petrobras and Equinor will extend the field life of Roncador by eight years, recover an incremental 500 mmboe and generate US$1.6 billion of value.

Source: Wood Mackenzie GEM, Asset Phase functionality

0

200

400

600

800

1000

1200

1400

1600

1800

2000

0

50

100

150

200

250

300

350

400

1994 1999 2004 2009 2014 2019 2024 2029 2034

Ca

pit

al c

os

ts, U

S$

millio

n

Oil p

rod

uc

tio

n, '0

00

b/d

Base production Incremental production Base capex Incremental capex

Roncador production and capex

• 20 new production

wells over 5 years

• US$2.1 billion total

investment

FID: 2019

Start-up: 2020

Case study #1 – there are plenty of infill drilling opportunities in the basin

Capital receipt of US$1

billion in 2016 related

to the sale and lease

back agreement of the

FPSO P-52

+5 points of recovery factor

• 4D seismic

• infill drilling

8

woodmac.com

Campos basin platforms by years of operation Most production units in shallow water have

operated for more than 30 years.

» Investment needed to revamp ageing fixed

platforms. Upgrades would require an assessment

of structural integrity and associated costs to extend

its service life.

Majority of units operating in deep water are

less than 10 - 20 years old and could have

production extended until 2030 through the

connection of new wells.

Revamping topsides would also enhance

production and reduce opex. Debottlenecking

water treatment infrastructure would free spare

oil processing capacity and improve water

injection.

In Marlim, shrinking the number and the size of

operating platforms will also contribute to opex

reductions of US$8/boe.

Deepwater fields have newer platforms with a remaining 10 to 15 years of service life; these fields would be easier to redevelop

Most shallow-water platforms have been in service for 30+ years and structural integrity would need to be assessed before investment is committed

Source: Wood Mackenzie

0

5

10

15

20

25

30

less than5

5 to 15 15 to 25 25 to 35 35 to 45

Nu

mb

er

of

pro

du

cti

on

un

its

Number of years in operation

Floating units Fixed units

Case study #2 – ageing facilities may require substitution

9

woodmac.com

0

10

20

30

40

50

60

70

80

0

100

200

300

400

500

600

700

1991 1995 1999 2003 2007 2011 2015 2019 2023 2027 2031 2035O

pe

x/b

oe

(U

S$

/bo

e)

Pro

du

cti

on

('0

00

bo

e/d

)

Redevelopment phase production Current phase production

Production W/O Redevelopment Current Opex/boe

Redevelopment Opex/boe

Marlim: A leaner fleet and higher production to reduce opex by 30%

Redevelopment extends Marlim’s life by ten years with a secondary 140,000 boe/d production peak and an incremental NPV10 of US$1.5 billion

Source: Wood Mackenzie GEM, Asset Phase functionality

In 2023, the last FPSO

onstream (180,000 b/d)

of the current phase

produces only 5,000 b/d

440 mmboe

added

• 100+ wells shut in

• 40 wells reconnected

• 10 new wells drilled

(US$2.7 billion capex)

Marlim production and operational cost

• 100+ wells shut down

• 30 wells reconnected

• 10 new wells drilled

(US$2.7 bi capex*)

Production infrastructure

before and after redevelopment

388

150

172

2

707

730

780

9

Gasprocessing

capacity(mmcfd)

Oil processingcapacity (kb/d)

Fixed opex(US$ M/year)

# platforms

Current Redevelopment

Current production

Case study #2 – ageing facilities may require substitution

Opex from US$26/boe

in 2018 to US$18/boe

in 2023

10

woodmac.com

0

20

40

60

80

100

120

140

0

5

10

15

20

25

Op

ex/b

oe

(U

S$

/bo

e)

Pro

du

ctio

n (

'00

0 b

oe

/d)

Incremental production

Base production

Legacy production enabled by redevelopment

Opex/boe

Polvo’s opex fell 62% through operational efficiencies and contract renegotiations after a smaller operator took operatorship

Royalty reduction could incentivize incremental investment. In Polvo, the reduction would pay for 70% of the redevelopment capex

Source: Wood Mackenzie GEM, Asset Phase functionality

Renegotiation of contracts at the bottom of the market and low Brent prices

Replacement of service providers and suppliers

3 new wells

+ 6,000 b/d by 2019

with additional

US$60MM D&C

capex

Post 2018

Polvo production and operational costs

Taking over the operation during the oil price

crash helped PetroRio in the cost reduction

Since 2013...

40% reduction in FPSO lease cost

62% reduction of general costs

Royalty rate

reduction to 5% enables incremental

production and collection of US$44

million in royalty

+ 15

mmboe in

reserves

Postponement of US$51 million in

decommissioning cost to 2023

Case study #3 – what are the opportunities for smaller companies?

11

woodmac.com

Investing the same US$8 billion in the redevelopment of mature fields can add 500 mmboe of incremental reserves by 2025

The 10 fields facing the highest decommissioning cost could postpone cessation production to the 2030s

First

oil

Primary

recovery Extend

field life

+20 years of operation

End of

production

Two options: decommission or redevelop?

To develop our upside

scenario, we have used the

Upstream Data Tool to screen

Campos basin fields under the

selected criteria:

• Recovery factors under 30%

• Production facilities with

remaining service life of more

than 10 years

The fields were then ranked

by their abandonment spend

from 2018 to 2025 and we

added investment until the

US$8 billion limit was reached

Incremental

production by

2025

Additional royalty

collected through

2025

Up to 12 wells

drilled per year

and related subsea

equipment

installed

Extra positions

maintained open

from 2018 to 2025

Investment of

US$8 billion

230,000 boe/d US$3.0 billion

30,000 jobs 60 new wells

Potential fields to redevelop Incremental results versus decommissioning scenario

12

woodmac.com

0

1

1

2

2

2010 2013 2016 2019 2022 2025 2028

millio

n b

oe

/d

The extra investment in redevelopment could generate 30,000 more jobs through 2025 than the abandonment alternative, while delaying US$4.8 billion of decommissioning costs

Source: Wood Mackenzie GEM, IBP

Redevelopment could add 230,000 boe/d if getting started by 2019

Campos basin production Investment

Incremental results

Base Future projects

0

2

4

6

8

10

2010 2013 2016 2019 2022 2025 2028

US

$ b

illio

n

Redevelopment (ongoing) Redevelopment (potential)

13

woodmac.com

Horacio Cuenca

Upstream Research Director, Latin America

Biography Connect with Horacio

Horacio Cuenca is Wood Mackenzie’s Southern Cone Upstream Research Director, based in

Rio de Janeiro. Horacio works as a content leader for research efforts in Latin America,

shaping Wood Mackenzie's Southern Cone regional perspective within the global upstream

team.

Horacio is responsible for maintaining and growing Wood Mackenzie’s analytical coverage in

Argentina, Brazil and Bolivia, developing junior analysts and representing Wood Mackenzie's

views in regional industry events.

Prior to joining Wood Mackenzie in 2013, Horacio worked seven years for IHS CERA’s

Energy and Natural Resources Consulting Practice in London, focused on upstream new

ventures advisory services. Horacio has ample experience using quantitative analysis to

understand the impact of fiscal regime parameters on project and portfolio value, and key

technical decisions made under uncertainty. Prior to that Horacio worked for Petroecuador

and independent operators in Ecuador.

Horacio holds a BA in Corporate Finance and a Masters Degree in Petroleum Economy from

Scuola Superiore Enrico Mattei in Milan, Italy.

+55 21 993 006 806

+55 21 3550 7700

@WMHoracio

14

woodmac.com

Americas +1 713 470 1700

Asia Pacific +65 6518 0888

Europe +44 131 243 4477

Wood Mackenzie Client Helpdesk

Contacts

Pedro Camarota (Rio de Janeiro) T +55 21 3550 7702

Wood Mackenzie Relationship Manager

Research Director, Upstream Latin America

Horacio Cuenca (Rio de Janeiro) T +55 21 3550 7705

15

woodmac.com

Disclaimer

Strictly Private & Confidential

These materials, including any updates to them, are published by and remain subject to the copyright of the Wood Mackenzie group

("Wood Mackenzie"), and are made available to clients of Wood Mackenzie under terms agreed between Wood Mackenzie and those

clients. The use of these materials is governed by the terms and conditions of the agreement under which they were provided. The

content and conclusions contained are confidential and may not be disclosed to any other person without Wood Mackenzie's prior

written permission. Wood Mackenzie makes no warranty or representation about the accuracy or completeness of the information

and data contained in these materials, which are provided 'as is'. The opinions expressed in these materials are those of Wood

Mackenzie, and nothing contained in them constitutes an offer to buy or to sell securities, or investment advice. Wood Mackenzie's

products do not provide a comprehensive analysis of the financial position or prospects of any company or entity and nothing in any

such product should be taken as comment regarding the value of the securities of any entity. If, notwithstanding the foregoing, you or

any other person relies upon these materials in any way, Wood Mackenzie does not accept, and hereby disclaims to the extent

permitted by law, all liability for any loss and damage suffered arising in connection with such reliance.

Copyright © 2018, Wood Mackenzie Limited. All rights reserved. Wood Mackenzie is a Verisk business.

Wood Mackenzie™, a Verisk business, is a trusted intelligence provider, empowering decision-makers with unique insight on the world’s natural resources. We are a leading research and consultancy business for the global energy, power and

renewables, subsurface, chemicals, and metals and mining industries. For more information visit: woodmac.com

WOOD MACKENZIE is a trademark of Wood Mackenzie Limited and is the subject of trademark registrations and/or

applications in the European Community, the USA and other countries around the world.

Europe

Americas

Asia Pacific

Website

+44 131 243 4400

+1 713 470 1600

+65 6518 0800

www.woodmac.com