Embed Size (px)

Citation preview

QUANTIFYING SUBPRIME

CONSUMER PSYCHOLOGY

Implications for Operational Strategy

October 25, 2012

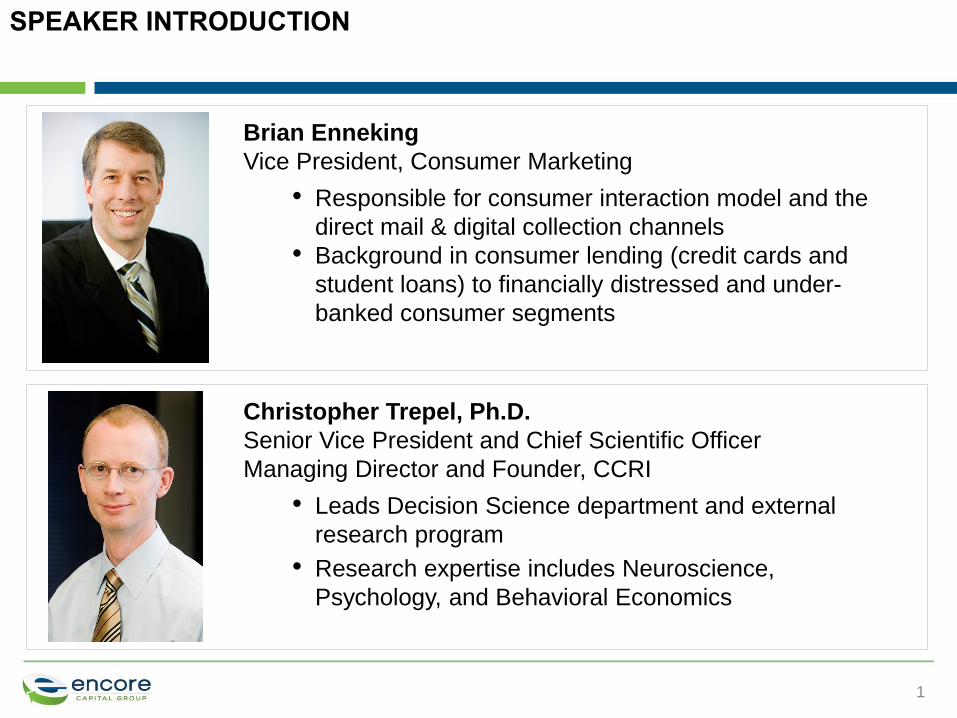

SPEAKER INTRODUCTION

1

Brian Enneking

Vice President, Consumer Marketing

• Responsible for consumer interaction model and the

direct mail & digital collection channels

• Background in consumer lending (credit cards and

student loans) to financially distressed and under-

banked consumer segments

Christopher Trepel, Ph.D.

Senior Vice President and Chief Scientific Officer

Managing Director and Founder, CCRI

• Leads Decision Science department and external

research program

• Research expertise includes Neuroscience,

Psychology, and Behavioral Economics

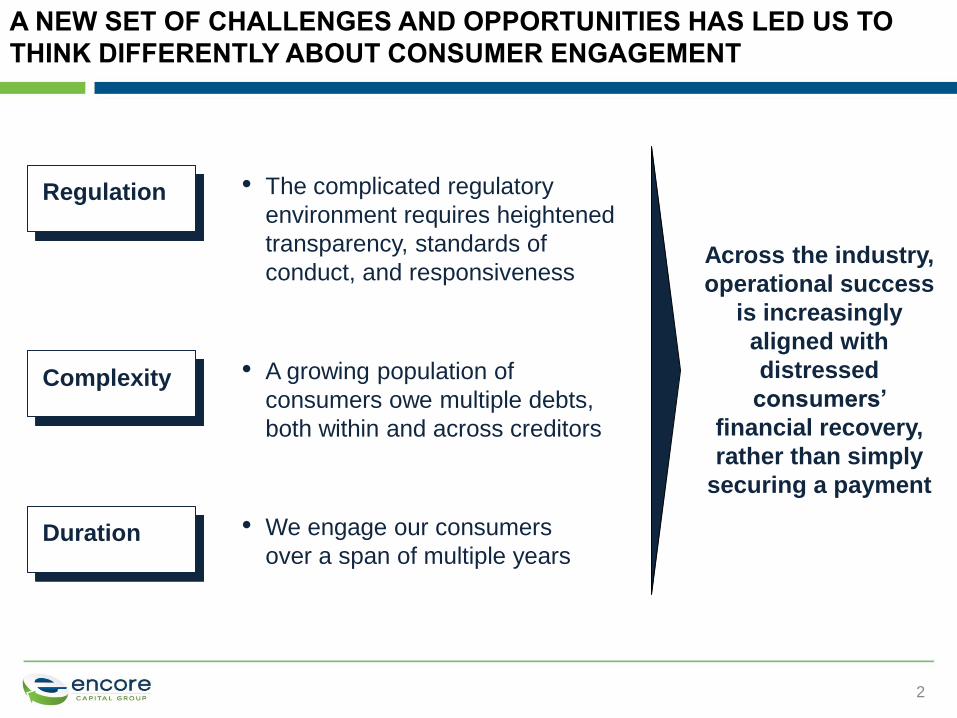

A NEW SET OF CHALLENGES AND OPPORTUNITIES HAS LED US TO

THINK DIFFERENTLY ABOUT CONSUMER ENGAGEMENT

2

• The complicated regulatory

environment requires heightened

transparency, standards of

conduct, and responsiveness

Regulation

• A growing population of

consumers owe multiple debts,

both within and across creditors

Complexity

• We engage our consumers

over a span of multiple years Duration

Across the industry,

operational success

is increasingly

aligned with

distressed

consumers’

financial recovery,

rather than simply

securing a payment

OUR OPERATIONAL STRATEGY AIMS TO UNDERSTAND AND

ACCOMMODATE OUR CONSUMERS‟ FINANCIAL LIVES

3

Start

End with

payment

While traditional consumer interaction

models focus on securing repayment…

Recovery

and

growth

Systematically

resolve

obligations Engage

and

discuss

Measure

and

understand

Promote

repayment

…our approach more closely aligns with

distressed consumers’ needs and goals

WE ARE FOCUSING OUR ENERGY IN THREE SPECIFIC AREAS

4

WE ARE ENGAGING MORE EFFECTIVELY WITH CONSUMERS BY

ASKING IMPORTANT QUESTIONS ABOUT THEIR CIRCUMSTANCES

What can we do to

ethically promote

repayment

behavior?

How do consumers

prioritize their

spending and

saving options?

When do we nudge

consumers using

behavioral

economics?

Conduct research to

understand financially

stressed consumers’

financial decision-making

Promote financial literacy

and recovery through a

tailored suite of products

and services

Integrate experimental

psychology and behavioral

finance with operational

strategy

5

OUR RESEARCH PIPELINE IS ROBUST AND FOCUSED ON BOTH

TRADITIONAL AND NOVEL PROGRAMS

Program Concept Planning

Pilot

Study

Full

Study Application Focus

Consumer

parametrics

• Scientific understanding

of consumer decision

triggers and biases

Model

enhancement

• Describe consumer

trajectories to enhance

operational strategies

Settlement

economics

• Supply and demand

factors that shape

repayment behavior

Information

mapping

• Combining data sets to

reveal new variable

inter-relationships

Debiasing

platforms

• Develop new tools to

improve consumer

decision-making

Credit

availability

• Understand the effect of

collections on credit

availability and repayment

6

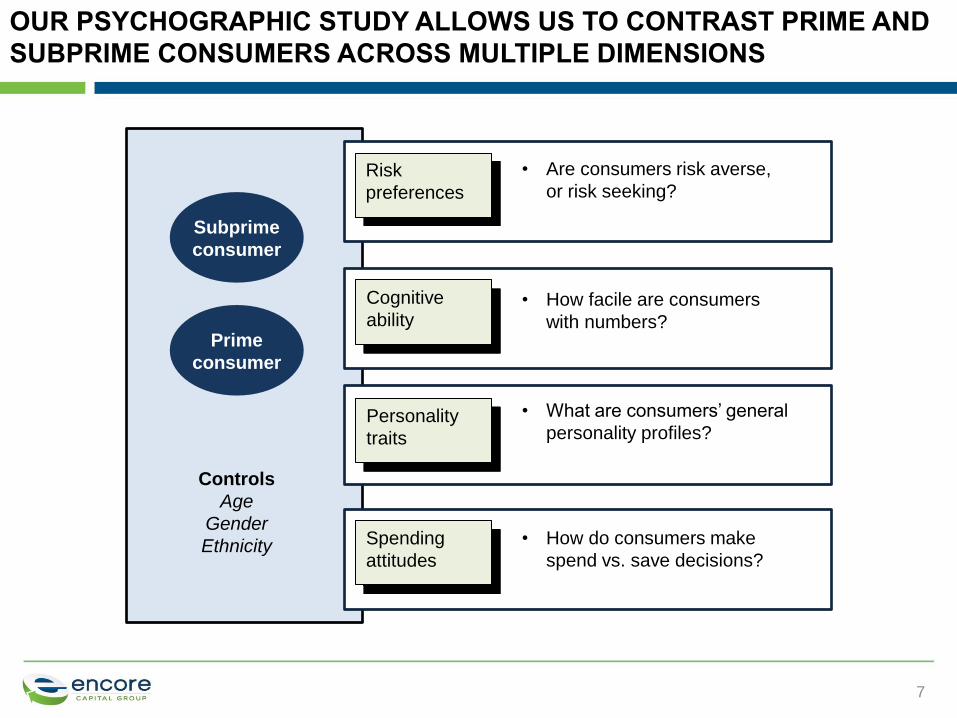

OUR PSYCHOGRAPHIC STUDY ALLOWS US TO CONTRAST PRIME AND

SUBPRIME CONSUMERS ACROSS MULTIPLE DIMENSIONS

7

Subprime

consumer

Prime

consumer

Controls

Age

Gender

Ethnicity

Risk

preferences

• Are consumers risk averse,

or risk seeking?

Cognitive

ability • How facile are consumers

with numbers?

• What are consumers’ general

personality profiles? Personality

traits

Spending

attitudes

• How do consumers make

spend vs. save decisions?

OUR PARTICIPANTS WERE GENERALLY REPRESENTATIVE OF THE

U.S. POPULATION

8

Caucasian Hispanic AfricanAmerican

Asian Other

50.1

61.5

24.3

15.4 13.2 12.5

6.5 4.8 5.9 5.8

Ethnicity of study participants compared to general U.S population

(%) CCRI study

(n=461)

2010 U.S.

census

PRIME CONSUMERS ARE MORE CLOSELY CONNECTED TO THEIR

CREDIT WORTHINESS THAN SUBPRIME CONSUMERS

9

Correct Incorrect

93%

7%

Prime consumers’ self-estimated

credit quality

Correct Incorrect

50% 50%

Subprime consumers’ self-

estimated credit quality

In contrast to prime consumers, subprime consumers

appear to be guessing about their credit worthiness

Spendthrift – Tightwad Scale1

measures the “pain of paying”

10

SPENDING MONEY APPEARS TO BE MORE PAINFUL FOR PRIME

CONSUMERS THAN FOR SUBPRIME CONSUMERS

Controlling for age, gender

and ethnicity, we were able

to differentiate prime and

subprime consumers2

Prime

“Tightwad”

bias

Subprime

“Spendthrift”

bias

People interpret the

decision to spend

money differently

The pain of paying is

not felt equally by all

Pain of

paying is

intense

“Tightwads”

Pain of

paying is

weak

“Spendthrifts”

(1) Rick et al. (2008) Tightwads and spendthrifts. Journal of Consumer Research, 34, 767-782; (2) χ2(1) = 10.14, p<0.01

11

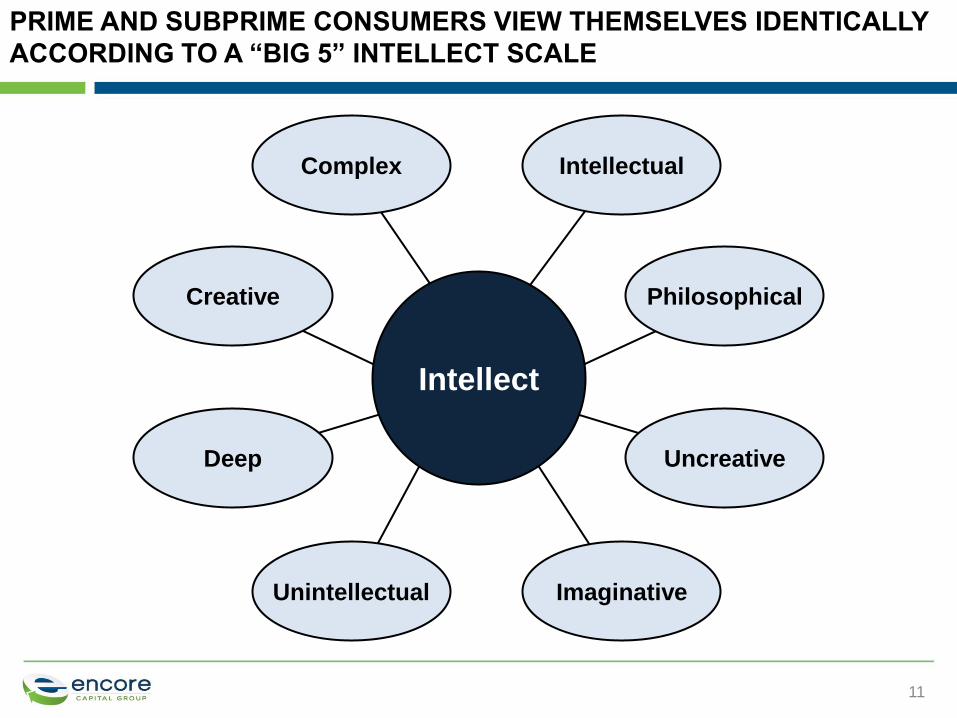

PRIME AND SUBPRIME CONSUMERS VIEW THEMSELVES IDENTICALLY

ACCORDING TO A “BIG 5” INTELLECT SCALE

Complex

Creative

Deep

Imaginative

Intellectual

Philosophical

Uncreative

Unintellectual

Intellect

CAPTURING CONSUMERS‟ SELF-PERCEPTIONS IS IMPORTANT AND

YIELDS VALUE

12

Operational

implications

Hypothesis 1:

“Aspirational”

Consumers are

projecting their

future desired state

• Custom marketing

creative

• Adjusted tone

• Products

‒ Financial

renewal

‒ Education

Hypothesis 2:

“Prestige”

Consumers prefer

a prime-like

interaction model

• Custom marketing

creative

• Adjusted tone

• Workgroup

structure

• Rewards program

• Complete self-

service portal

Champion sequences

A C C C

A D C D

B C C D

Test creatives

A B

C D

E F

PRIMARY FIELD RESEARCH, AND BEHAVIORAL ECONOMICS THEORY,

ARE MORE STRONGLY INFLUENCING OUR MARKETING PRACTICES

13

• Primary field

research

• Academic theory

• Competitive shop

• Operational focus

groups

• Marketing

expertise

• Experimental

refinement

Concept sources

REVISED VALIDATION LETTERS, FOCUSED ON ESTABLISHING

CREDIBILITY, HAVE INCREASED CONSUMER RESPONSIVENESS

14

• Customer-centered

communications flow

– “Your account has a

new home”

– Full account details

– What to expect

– How to access our

Consumer Bill of Rights

– How to contact us

– A request to update

contact information

• Focus on transparency,

honesty, and clarity

• lift in unit yield

(versus control) +20%

ABC%

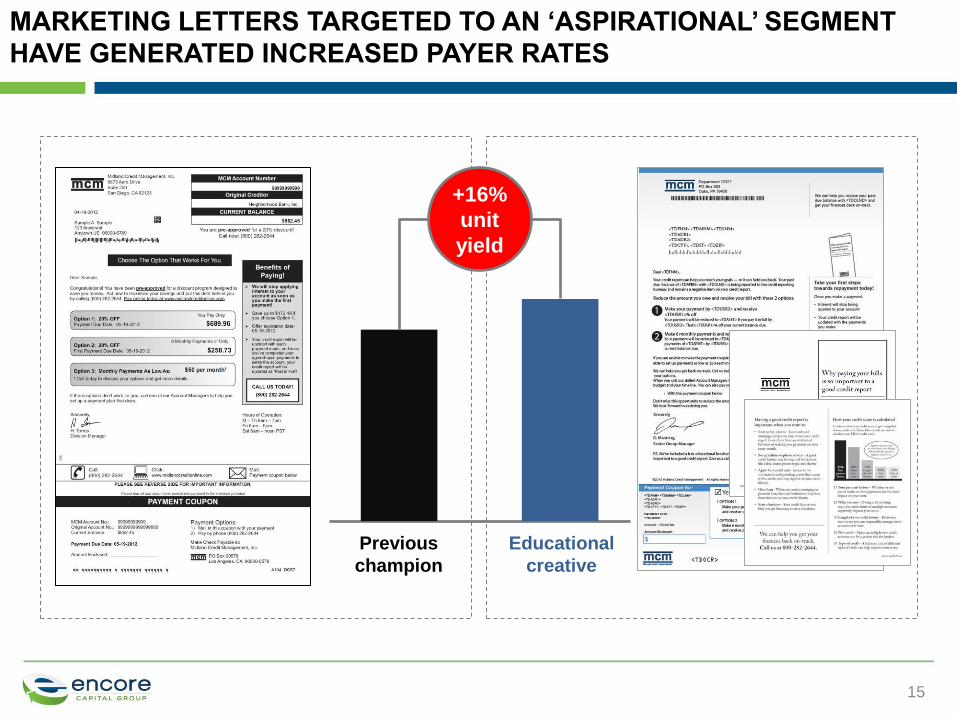

MARKETING LETTERS TARGETED TO AN „ASPIRATIONAL‟ SEGMENT

HAVE GENERATED INCREASED PAYER RATES

15

+16%

unit

yield

Previous

champion

Educational

creative

WE ARE ACTIVELY PROMOTING TOOLS AND RESOURCES THAT

ASSIST CONSUMERS WITH THEIR FINANCIAL RECOVERY

16

FUTURE ENHANCEMENTS WILL STEM FROM SOPHISTICATED

SEGMENTATION SCHEMES AND THE APPLICATION OF UNIQUE DATA

17

Marketing

creatives

derived through

rigorous testing

Segmentation

strategies

grounded in

experimental

field work

Sourcing and

application of

consumer and

macroeconomic

data

Focus on

consumer

interaction

model to drive

lasting recovery

![Knowledge is Power: Consumer Education and the Subprime ... · foreclosures are attributable to subprime mortgages.14 It is estimated that ―[a]t least one out of five subprime loans](https://img.pdfslide.us/doc/110x75/5f0abd137e708231d42d19ec/knowledge-is-power-consumer-education-and-the-subprime-foreclosures-are-attributable.jpg)