Embed Size (px)

Citation preview

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 84

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

Quality of Information Supplied to Board of

Directors: a Case Study on a Malaysian Higher

Learning Institution

Mohd Yussoff Ibrahim1, Azrai Abdullah2,

Khalidah BT Khalid Ali3 and Abu Bakar Sedek B. Abdul Jamak4 1Mohd Yussoff Ibrahim, Assoc. Prof. Dr. is with the Centre of Postgraduate and Research, Kolej Universiti Insaniah, Alor Setar,

05350 Kedah, Malaysia. (phone: + 604-7323958/4405; Fax :+ 604 -7320164; email:[email protected]) 2Azrai Abdullah, Dr. is with the Department of Management and Humanities, Universiti Teknologi PETRONAS, Bandar Seri

Iskandar, Perak, 31750 Malaysia. (phone: + 605- 3657731/7755; Fax: + 605-3656280; email: [email protected] 3Khalidah Khalid Ali is with the Department of Management and Humanities, Universiti Teknologi PETRONAS, Bandar Seri

Iskandar, Perak, 31750 Malaysia. (phone: + 605-3687737; Fax: + 605-3656280; email: [email protected]) 4Abu Bakar Sedek Bin Abdul Jamak is with the Department of Management and Humanities, Universiti Teknologi PETRONAS,

Bandar Seri Iskandar, Perak, Malaysia. (phone: + 605- 3687764; Fax: + 605-3656280; email: [email protected])

Abstract-- Board of Directors (BOD) of corporations is

responsible for the company’s operational and financial

performance apart from its fiduciary duty to fulfill the needs of

all stakeholders. In executing their responsibilities, Board

members have to make strategic decisions on a broad spectrum

of business issues to survive in today’s challenging global

environment. The efficiency of BOD and effectiveness of their

decisions truly depend on the nature and quality of information

provided by the Management as they are not the implementers

but “overseers” in the management process. Much as the

information and communication technology (ICT) has facilitated

the flow of information in general, the extent, nature and quality

of information provided to BOD have often been in question.

This paper seeks to develop a research tool to measure the

adequacy of the internal reporting system that provides

information to companies’ BOD based on seven dimensions;

Relevant, Integrated, In perspective, Timely, Reliable, Comparable

and Clear. The efficiency and effectiveness of the internal

reporting system are evaluated by measuring the gap between

the levels of satisfaction that directors have on each of the

characteristics with that of the preparers’ perception. The

instruments to measure those constructs were developed and

tested based on a pilot study performed at a Malaysian higher

institution of learning. The result will be used to develop

measurement tools for evaluating the efficiency and effectiveness

of an internal reporting system of corporations.

Index Term-- Board of Directors, Malaysia, management,

quality of information, internal reporting system, efficiency,

effectiveness, level of satisfaction

I. INTRODUCTION

The fiduciary role of Board of Directors (BOD), being

responsible to all its stakeholders, is an important element of

corporate governance (CG). The BOD, among others, is also

responsible for establishing and maintaining internal financial

controls, communicating financial situations internally and

externally, establishing and revising where necessary the

firm’s code of ethics and ethical standards, selecting the

external auditor and establishing different board committees

including the audit committee to ensure good governance

(Stanwick and Stanwick, 2009).

In view of its strategic role and in order to effectively

exercise its responsibilities, the Board sets out the company’s

policies and guidelines, identifies short and long term

objectives and puts procedures into place. It is thus ultimately

accountable for the company’s goals as well as the means to

achieve it. To execute its responsibilities, the Board has to

monitor the performance of the company as well as make

decisions on diverse policy matters.

The efficiency of BOD and effectiveness of its decisions truly

depend on the nature and quality of information provided by

the Management as Board members are not the implementers

but “overseers” in the management process. Much as the

information and communication technology (ICT) has

facilitated the flow of information in general, the extent,

nature and quality of information provided to BOD have often

been in question. Questions have also been raised in literature

on the extent of the Board’s satisfaction on the information

provided to them in carrying out their responsibilities. One

recent example is Chartered Institute of Management

Accountant’s (CIMA) concern regarding the quality of board

reporting practice, which is crucial for good market

performance and sound corporate governance. The issue is

whether the BOD is being provided with the right type of

information to effectively perform its responsibility. The

Board needs information to steer the organization towards

achieving its goals and objectives. At the same time, the Board

members need to limit their exposure to any allegation that

they are not discharging their duties to the shareholders to

uphold their integrity.

This paper reports on a comparative study undertaken to

measure the gap between the satisfaction of directors and that

of the preparers’ perception on the quality of information

provided for making business decisions. The finding from this

research will provide basis for developing an instrument to

measure the quality of information prepared for the

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 85

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

companies’ Board of Directors. It will also provide hindsight

as to the actions necessary for the improvement of the

corporate internal reporting practice.

II. BACKGROUND

One of the main pillars of a nation’s economy is its corporate

governance (CG). The success or failure of a nation’s

economy, in its effort to achieve stable and continuous

economic development rests heavily on the existence and

effectiveness of its corporate governance. Various definitions

have been given to corporate governance. Corporate

governance has been defined as: “…the system of checks and

balances, both internal and external to the companies, which

ensures that companies discharge their accountability to all

their stakeholders and act in a socially responsible way in all

areas of their business activity” (Solomon & Solomon, 2004).

It is also defined as the system by which companies are

directed and controlled (Cadbury, 1992), a means by which

various stakeholders exert control over a corporation by

exercising certain rights as established in the existing legal

and regulatory frameworks as well as corporate bylaws (John

& Senbet,1998). Precisely, the definitions imply that corporate

governance deals with mechanism by which stakeholders or

owners of a company exercise control over management such

that their interests are protected. John and Senbet (1998)

define stakeholders of a company to include equity holders,

creditors and other claimants who supply capital, as well as

other stakeholders such as employees, consumers, suppliers

and the government.

Following the 1997 financial turmoil, Malaysia has developed

a code on corporate governance published in 2000 and revised

in 2007. Specifically, the code aims to set out principles and

best practices on structures and processes that companies may

use in their operation towards achieving the optimal

governance framework (Finance Committee on Corporate

Governance, 2000). With the principles and best practices, the

code aspires to achieve two primary inter-related objectives;

encourage disclosure by providing investors with timely and

relevant information and provide a guide to the Board of

Directors by clarifying their responsibilities and providing

prescriptions to strengthen their control (Najmuddin et al.

2002)

On the responsibilities of Board of Directors, Section D of the

Principles of Corporate Governance states inter-alia that the

Board ‘should present a balanced and understandable

assessment of the company’s position and prospects and

maintain a sound system of internal control’. The Best

Practice section of the Code details out the responsibilities as

follows;

Reviewing and adopting a strategic plan

Overseeing the conduct of the company’s business

Identifying and managing principle risk

Succession planning

Developing and implementing an investors’ relation

programme

Reviewing the integrity of the company’s internal

control

CG literature provides many explanations on the Board of

Director’s responsibilities. Board responsibility (roles) can be

classified into four: monitoring, service, strategy and resource

provision (Daily et al., 2003; Zahra and Pearce, 1989).

According to Lasfer (2004), the Board’s role comprises of

monitoring and advising.

Among the best practices suggested by the Code are related to

the quality of information provided to Board of Directors. The

third principle of corporate governance regarding directors

specifies that ‘the Board should be supplied in a timely

fashion with information in a form and of a quality appropriate

to enable it to discharge its duties’ (Finance Committee on

Corporate Governance, 2000). In the section on Best Practices

in Corporate Governance regarding Board of Directors, item

(xvii) further emphasized on the quality of information

supplied to the Board. ‘The Board should receive information

that is not just historical or bottom line and financial-oriented

but information that goes beyond assessing the quantitative

performance of the enterprise and looks at other performance

factors such as customer satisfaction, product and service

quality, market share, market reaction, environmental

performance..’(ibid. 2000). Hence, the Code does recognize

that it is crucial for the Board of Directors to have access to

quality information that allows them to exercise their duties

effectively. Furthermore, according to CIMA (as cited from

Starovic (2003), a good report should contain all the

information necessary to facilitate decision making at Board

level.

What constitutes quality information? There are various

prescriptions of quality characteristics. As mentioned in the

previous paragraph, the Malaysian Codes of Corporate

Governance defined information quality in terms of the scope

and form of its content. The Board should be provided with

financial and non-financial information that are historical as

well as futuristic. The Institute of Chartered Accountants in

England and Wales (as cited in Starovic, 2003) advocates five

characteristics of quality information as follows: material,

relevant, reliable, comparable and understandable. In contrast,

Metapraxis (as cited in Starovic, 2003) a management

consultancy organization, prescribes quality as having the

following characteristics: accuracy, relevance, timeliness,

clarity, risk assessment, depth and provision. Based on the

above definitions, CIMA (UK) outlined seven characteristics

essential to quality information: relevant, integrated, in

perspective, timely, reliable, comparable and clear (Starovic,

2003).

It is important for the Management to be aware of the

characteristics of information quality preferred by Board of

Directors in order to develop the perceived quality of

information. This is crucial because of the divergent

perceptions of the quality between the preparer and the user of

information (Parasuraman et al., 1985). An organization has to

define quality in accordance with users’ expectations, needs

and wants. Failure to do so will lead to a wasted effort on any

improvement initiative because the Management is not

focusing on the same characteristics preferred by the users. A

supplier of information aiming to provide high-quality

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 86

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

information thus needs to be familiar with the characteristics

of the information that are important to the consumers

(Parasuraman et al., 1988). Mapping all the significant

characteristics of information quality perceived by the Board

members would provide quality measurements and subsequent

quality improvements. The identification and assessment of

these attributes are thus important. However, to the best of our

knowledge, no studies have attempted to evaluate the quality

of information prepared for the Board of Directors and to

assess the gap between preparers’ and the users’ perceptions.

This paper attempts to describe the development of scale to

measure the level of quality of information provided by the

Management to Board of Directors as perceived by the

preparer and the user and to gauge the gap between them.

III. LITERATURE REVIEW

Corporate governance (CG) has become a research area since

early 80s.1 Among the areas focused in CG studies relate to;

Board of Directors, managerial incentives, capital structure,

by-laws and charter provision and internal control system

(Gillan, 2006). According to Gillan (2006) on the subject of

‘Board of Directors’, the focus of the researches is broad,

encompassing board size, structure, compensation,

independence, characteristics and expertise. Some of the

variables linked to the Board in past studies include firm

value, governance choice, investment and financing decisions,

activity of board sub-committee and CEO compensation,

firm’s performance, ownership structure, corporate fraud,

earning restatements and incentive compensation. Sample of

the previous studies (as cited from Gillan, 2006) that relates to

the Board of Directors are; board-size and the independence of

the board from corporate management (Rosenstein and Wyatt,

1990; Yermack, 1996), board activity (Vafeas, 1999), board

structure and activity of board sub-committees (Klein, 1998,

2002; Deli and Gillan, 2000), theoretical aspects of board

structure (Hermalin and Weisbach (1988), Warther (1998),

Adams and Ferreria (2003), Gillette et al. (2003), Harris and

Raviv (2005), and Raheja (2005)), the evolution of board

structure over time, and changes in board structure post-

Sarbanes–Oxley (SOX) (Chhaochharia and Grinstein,

2005a,b; Coles et al. 2005b; and Linck et al. (2005a,b).

There were few research carried out on the information

reported to the Board and information usage by the Board.

The quality of information provided to the Board is crucial to

ensure effectiveness in executing its roles and responsibilities.

Past studies have related the need for information by the

Board to their monitoring and advisory roles. Lorsch and

MacIver (1989) and Noe and Rebello (1997) as cited from

Lasfer (2004) argued that in order to undertake the advisory

role, information should flow from the managers or the CEO

to the Board members. Lasfer (2004) hinted that ‘in normal

circumstances, the monitoring and the advisory role are

1 A quick search using Science Direct (an e-library) in the

field of Art and Humanities, Business, Management and

Accounting, Economics, Econometrics and Finance and Social

Sciences.

complementary because the better the information disclosed,

the better will be the advice and the evaluation’. Past literature

suggested that the effectiveness of the Board depends on the

severity of the firm’s agency conflicts as well as on the

information disclosed by managers (Lasfer, 2004).

However, the information communicated to internal

management has attracted profound interest among

researchers. One aspect that has received strong criticism is

regarding the form of information used in making decision.

Accounting systems have produced numerous measures of

financial performance including costs, revenues and profits.

Each of these financial measures can be calculated at the firm-

wide level or at the segments level. However, there has been

criticism that traditional performance measures motivate

dysfunctional behaviour by causing managers to pay attention

to the ‘wrong’ things (Hirst, 1983).

Several studies have indicated that dysfunctional behaviour

among employees arises from using performance

measurement based on accounting data or the style adopted in

using the data. Hopwood (1972) found that the more the

emphasis given to accounting data in performance

measurement, the higher is the level of dysfunctional

behavior. Otley (1978) tested a similar relationship in a

different environment and found a contradictory result. His

sample included managers of profit centres in one particular

industry whereas Hopwood‘s sample comprised managers of

cost centres in a factory. Hirst (1983) expanded the findings of

Hopwood (1972) and that of Otley (1978) by testing the

relationship in different levels of task uncertainty. The

conclusion arrived is that ‘A medium to high (medium to low)

reliance on accounting performance measures minimizes the

incidence of dysfunctional behavior in situation of low (high)

task uncertainty’.

Many firms now are beginning to place greater emphasis on

non-financial measures such as quality, customer satisfaction,

on-time delivery, innovation measures, and on the attainment

of strategic objectives (Ittner et. al., 1997). Kaplan and Norton

(1992, 1993) have developed the notion of a ‘balanced

scorecard’ in an attempt to provide a multi-dimensional

measure of managerial performance and to capture the value

drivers that have been concealed in the conventional

accounting numbers. A recent study on the nature of the

information communicated internally by Yussoff, Daing and

Krishnan (2008) has found that the emphasis on non-financial

measure by Management in their decision making has positive

relationship with the effectiveness of management control

system. This research measures the impact of quality

information on the effectiveness of the BOD using the board

role performance (Ong & Wan, 2007) as the proxy measure.

Board role performance was defined as ‘board’s ability to

perform its role’ and four critical Board’s roles are

monitoring, service, strategy and resource provision (ibid,

2007).

Research on information quality heavily focused on the

quality of information produced by organizations’

Management Information System (MIS) for particular process

or industry. Examples of these are studies on the impact of

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 87

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

information quality on the order fulfillment process (Forslund,

2007), the export market assistance (Toften & Rustad, 2005)

and the strategic technology planning (Gelle & Karhu, 2003).

The issue focused by these studies relate to the criteria of

information quality for enhancement of the processes or

functions. Apart from that, several studies focused on

development of instrument to measure information quality.

Various dimensions of information quality were identified

either through empirical research (Wang and Strong (1996)

and Zmud, (1978) or from literature review (Jarke and

Vassiliou (1997); Delone and McLean (1992)).

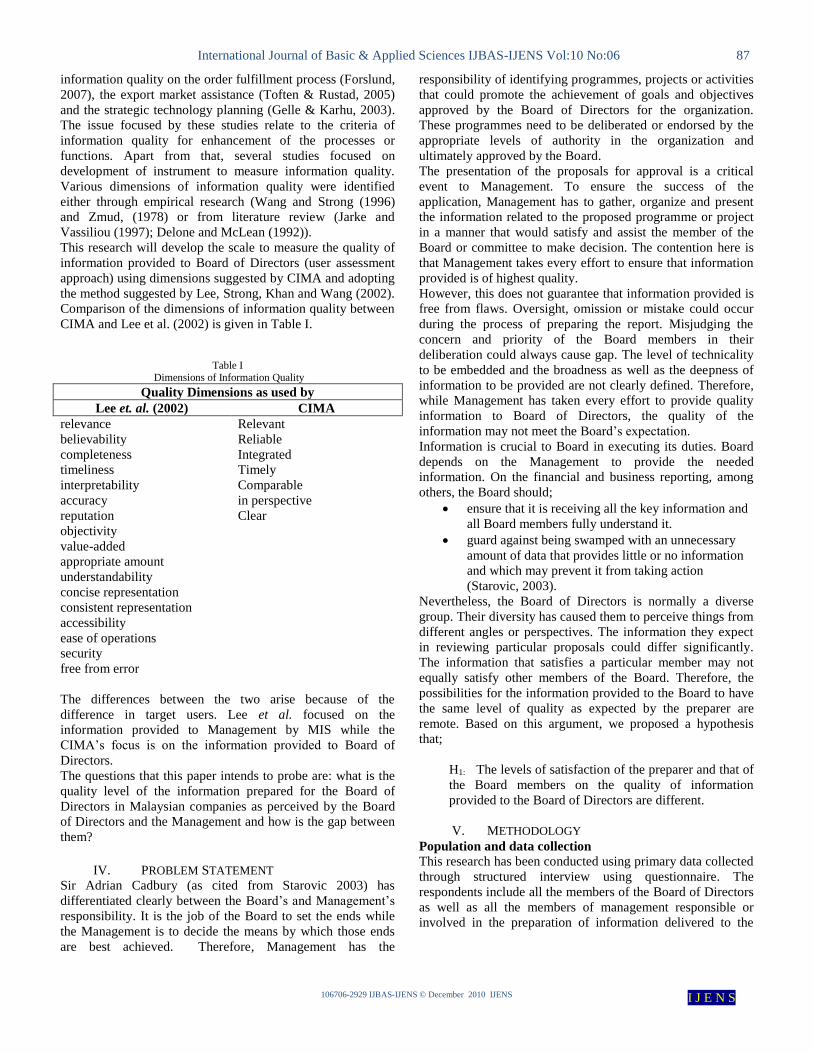

This research will develop the scale to measure the quality of

information provided to Board of Directors (user assessment

approach) using dimensions suggested by CIMA and adopting

the method suggested by Lee, Strong, Khan and Wang (2002).

Comparison of the dimensions of information quality between

CIMA and Lee et al. (2002) is given in Table I.

Table I Dimensions of Information Quality

Quality Dimensions as used by

Lee et. al. (2002) CIMA

relevance Relevant

believability Reliable

completeness Integrated

timeliness Timely

interpretability Comparable

accuracy in perspective

reputation Clear

objectivity

value-added

appropriate amount

understandability

concise representation

consistent representation

accessibility

ease of operations

security

free from error

The differences between the two arise because of the

difference in target users. Lee et al. focused on the

information provided to Management by MIS while the

CIMA’s focus is on the information provided to Board of

Directors.

The questions that this paper intends to probe are: what is the

quality level of the information prepared for the Board of

Directors in Malaysian companies as perceived by the Board

of Directors and the Management and how is the gap between

them?

IV. PROBLEM STATEMENT

Sir Adrian Cadbury (as cited from Starovic 2003) has

differentiated clearly between the Board’s and Management’s

responsibility. It is the job of the Board to set the ends while

the Management is to decide the means by which those ends

are best achieved. Therefore, Management has the

responsibility of identifying programmes, projects or activities

that could promote the achievement of goals and objectives

approved by the Board of Directors for the organization.

These programmes need to be deliberated or endorsed by the

appropriate levels of authority in the organization and

ultimately approved by the Board.

The presentation of the proposals for approval is a critical

event to Management. To ensure the success of the

application, Management has to gather, organize and present

the information related to the proposed programme or project

in a manner that would satisfy and assist the member of the

Board or committee to make decision. The contention here is

that Management takes every effort to ensure that information

provided is of highest quality.

However, this does not guarantee that information provided is

free from flaws. Oversight, omission or mistake could occur

during the process of preparing the report. Misjudging the

concern and priority of the Board members in their

deliberation could always cause gap. The level of technicality

to be embedded and the broadness as well as the deepness of

information to be provided are not clearly defined. Therefore,

while Management has taken every effort to provide quality

information to Board of Directors, the quality of the

information may not meet the Board’s expectation.

Information is crucial to Board in executing its duties. Board

depends on the Management to provide the needed

information. On the financial and business reporting, among

others, the Board should;

ensure that it is receiving all the key information and

all Board members fully understand it.

guard against being swamped with an unnecessary

amount of data that provides little or no information

and which may prevent it from taking action

(Starovic, 2003).

Nevertheless, the Board of Directors is normally a diverse

group. Their diversity has caused them to perceive things from

different angles or perspectives. The information they expect

in reviewing particular proposals could differ significantly.

The information that satisfies a particular member may not

equally satisfy other members of the Board. Therefore, the

possibilities for the information provided to the Board to have

the same level of quality as expected by the preparer are

remote. Based on this argument, we proposed a hypothesis

that;

H1: The levels of satisfaction of the preparer and that of

the Board members on the quality of information

provided to the Board of Directors are different.

V. METHODOLOGY

Population and data collection

This research has been conducted using primary data collected

through structured interview using questionnaire. The

respondents include all the members of the Board of Directors

as well as all the members of management responsible or

involved in the preparation of information delivered to the

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 88

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

Board. Since this is the pilot study and it involves only one

organization, no sampling will be performed.

Research instruments

The data collection process is conducted using questionnaire.

The questionnaire is developed using the principles for the

effective reporting of financial and non-financial reporting to

boards as outlined by CIMA (Starovic 2003). Seven proposed

dimensions of quality information include Relevant,

Integrated, In perspective, Timely, Reliable, Comparable and

Clear. The perceptions of the respondents on the quality levels

of each dimension are gauged using a 5-point Likert Scale.

Followings are discussion on the definition of each dimension

and the related measurements.

Relevant

Relevant is defined as the degree to which something is related

or useful to what is happening or being talked about

(Cambridge Advanced Learner's Dictionary). With respect to

information presented to the Board of Directors, information

is relevant if it is sharply focused and reflects the defined

objective and overall strategy of an organization (Starovic,

2003). With the information, the Board should be able to drill

down and seek further supplementary report if necessary. In

reviewing strategic proposals, Board may need to have

supplementary information to allow exploration of as many

alternatives as possible, necessary for unbiased information to

be made. Besides historical and quantitative data, forecast and

qualitative data are sometimes needed.

The dilemma that Management has to face in preparing the

information are striking the balance between insufficient and

excess information, historical and projected information,

quantitative and qualitative inputs and financial and non-

financial information. Imbalanced information will

unnecessarily burden, confuse and complicate the Board’s

function. To provide a clear definition of what each point

indicates, we develop the following scale to measure the

degree of relevancy.

It is difficult to find a perfect expression that could incorporate

all the concepts that relate to ‘Relevant’. In the questionnaire,

we use the expression ‘related to the decision’ as representing

‘Relevant’. A rating from 1 ‘extremely related’ to 5 ‘not

related’ has also been used as the assessment scale.

Integrated

Ideally information prepared for the Board of Directors should

be Integrated so that the information reported internally and

externally does not contradict. Since the interests of investors

and the directors are congruent, information reported in the

annual report and those supplied to Board of Directors should

be similar except for the degree of details. Therefore,

information needed for both purposes should come from the

same source i.e. the financial accounting system. However, the

additional information needed by Board of Directors may need

to be collected from external sources such as the information

on benchmarking of competitors’ performance. What

influences the integrity characteristic of information? The

assignment of responsibility on internal and external reporting

will determine the level of information integrity. The more it

is focused or concentrated to the financial accounting system,

the more Integrated the information will be.

Some of the aspects that portray the degree of integration that

the information exhibits are as follows:

provide link between activity data and financial

result.

provide sufficient non-financial information.

information received contradict with information

reported externally.

information received and information reported to

outside parties were prepared by same source.

In the questionnaire, we use the terms ‘contradict to’,

‘matches’ and ‘ in-line’ to indicate the degree of integration of

the information prepared for the Board and information

reported externally. The rating used is from 1 to indicate

‘totally contradicts’ to 5 to indicate ‘totally in line’.

In perspective

The information provided to Board of Directors should be In

perspective with reference to time context. It relates to how

the information presented to the Board is categorized by

period. Most of the problems deliberated by the Board are

strategic in nature and have long term perspectives. Having

information about the budget, actual as well as the forecast

would allow the Board to review progress or evaluate

performance of a project or transaction. This provides better

control on the company’s operations and performance.

Among the impressions related to In perspective are;

The information were classified by period

Cumulative position were highlighted

Variances from the budget were adequately explained

Trend and analysis were included

Full-year projections updated

To measure the degree that the information is In perspective,

we ask the respondent to assess the degree that the information

is categorized, from 1 ‘perfectly categorized’ to 5 ‘not

categorized’.

Timely

Information has time value. Information that reaches the

Board after the related decisions have been made has lost its

value no matter how relevant it is. The Board should be given

sufficient time to digest the information. As far as possible,

information should be Timely, i.e. available in parallel with

activities to which it relates (CIMA). The effect of not

providing the information timely is to deny the Board

members information needed to make decision.

Among the phrases related to ‘Timely’ are;

far in advance

in parallel with

information were denied

In the questionnaire, we use the phrases ‘late, timely and

appropriate time’ to differentiate the degree of timeliness of

information from 1 ‘very late’ to 5 ‘at the most appropriate

time’.

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 89

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

Reliable

The information prepared for the Board should be of

sufficiently high reliability to attain their confidence. Reliable

is defined as ‘suitable or fit to be relied on or dependable

(Merriam-Webster). The degree of confidence that the Board

has may come from past experience or the knowledge and

expertise of the Board members themselves.

To measure the degree of reliability of the information

provided to the Board in the questionnaire, we based on the

degree of confidence one has on the information from 1 ‘no

confidence’ to 5 ‘high confidence’.

Clear

Information provided to the Board must be simple and clear to

maximize its value for the Board’s deliberation and decision.

The preparer should avoid using jargon and acronyms when

everyday language is possible. Graph and chart can enhance

the effectiveness of the communication if wisely used. The

information may include financial and non-financial, and both

need to be presented clearly if they are to reflect the

performance of a company. This is especially true for large

organizations with many subsidiaries, where the layers of

management and the number of units/divisions may obscure

the relevant figures and breed a lack of common

understanding of what the key performance drivers are.

(Starovic, 2003)

We use the terms ‘Clear, confusing and distorted’ in the

questionnaire to assess the degree that the information is

clearly presented from 1 ‘very clear’ to 5 ‘very distorted’.

Comparable

To enhance its usefulness, the information provided to the

Board should be compared to some appropriate measure or

value wherever possible. Comparison provides the relative

value of measures and allows users to be aware of the real

situation. The actual financial performance of the company for

example can be compared with the budgeted (planned) or with

‘what should have happened’ or with the future performance.

The extent of and the choice of measure or value used for

comparison are critical in preparing information for the Board

as these would have an impact on the quality of monitoring

practice performed by the Board.

In the questionnaire, we ask the respondents to assess the

quality of measures or values used for comparison in terms of

the appropriateness of the choice using the scale of 1

‘extremely appropriate’ to 5 ‘highly inappropriate’.

The direction (forward or reverse) of the rating in the

questionnaire was randomly distributed. The assessments for

three (3) dimensions (i.e. reliable, integrated and timely) are

forward direction which means ‘5’ carries positive and ‘1’

carries negative meaning and the others are of reverse

direction. This will restrain respondents from entering the

score mechanically.

Analysis

The two objectives of the research are firstly to assess the

quality of the information disseminated to the Board of

Directors as perceived by the Board members and the preparer

and secondly to measure the gap between the Board of

Directors’ and the preparers’ assessment. For the first

objective, descriptive analysis to measure the Means and

Standard Deviation will be performed and T- test will be used

to determine the significance of the differences between the

Board and the preparers on the quality of the information.

Pilot study

In this pilot study, questionnaires were distributed and

administered for the members of the Management Committee

and the Board of Directors of a Malaysian higher institution of

learning. This institution was selected in view of its position

as a corporate entity and its accessibility to the researchers.

Information on the types of decisions made by the Board and

the types of information delivered to them was gathered. The

types of decisions the Board ordinarily makes include:

Approval of the University’s business plans and

annual budgets

Provides advice on the next steps to enhance the

University’s competitive advantage

Deliberates on the Internal Audit Report

Approves the audited financial accounts

Approves the manpower budget

Award, termination and reappointment of contractors

The information provided to the Board includes the following;

University’s business plans and annual budgets

Detail on the yearly objectives of each department

Performance reporting of the whole University

Internal Audit Report

Manpower budget of the University

Infrastructural development

As for the pilot test, the information deliberated by the Board

was classified into three items: Overall policies and

guidelines, Business plan and budget, and Overall

management and performance of the organization. For each

item, the seven characteristics of information quality are being

measured using a 5-point Likert scale. Refer to Appendix 4.

Out of the fourteen members (seven from the Management

group and seven from the Board of Directors), we received 11

responses (seven from the Management group and four from

the Board), which is equivalent to 78 percent response rate.

VI. RESULTS AND FINDINGS

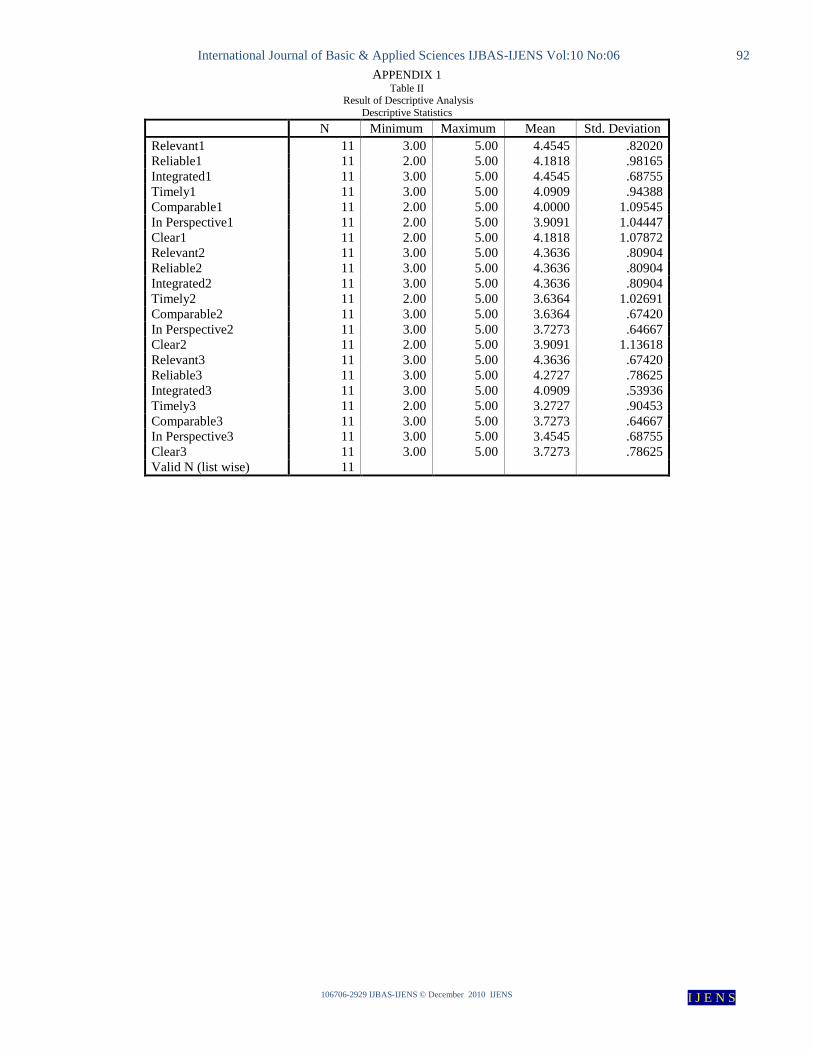

Using the SPSS Version 12, the data is analyzed. Table II (see

Appendix 1) shows the descriptive analysis of the responses.

The mean values of the responses range from the lowest 3.27

for the timeliness of the information related to the ‘Overall

management and performance of the organization’ to the

highest of 4.45 for the degree of relevancy and integrity of the

information related to the ‘Overall policies and guidelines’.

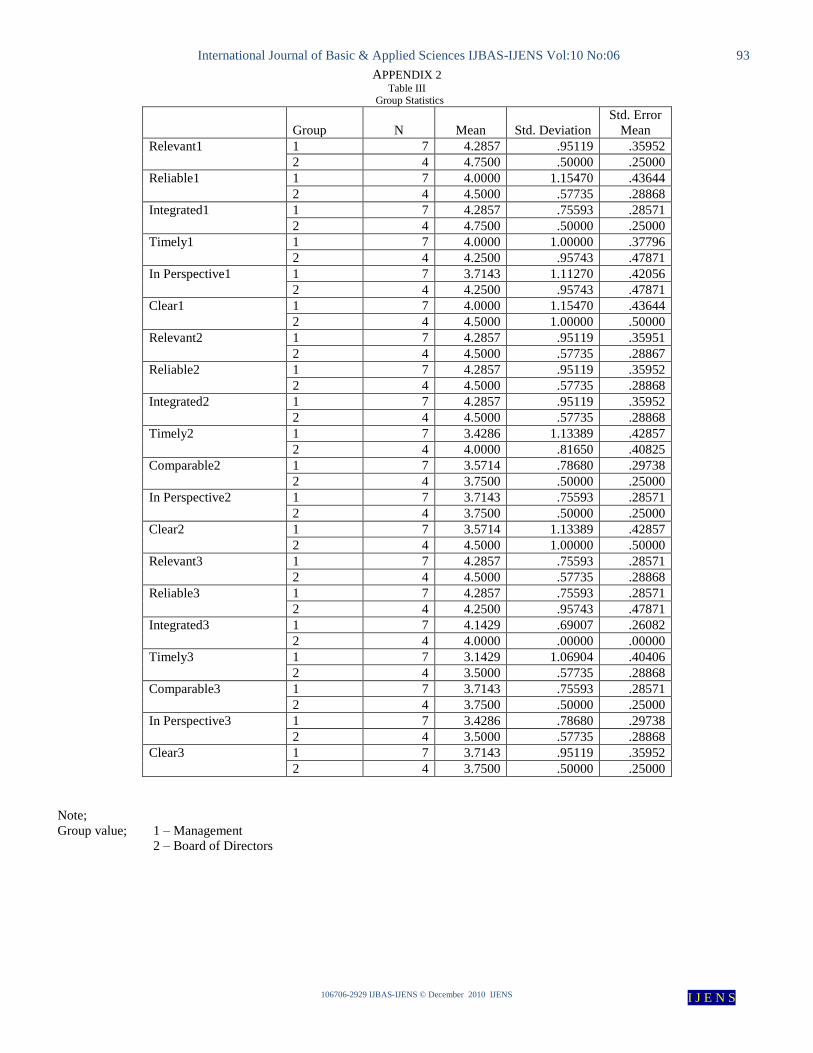

Table III (see Appendix 2) presents result of comparing the

mean scores of the Management (Group 1) and that of the

Board of Directors (Group 2). Comparing the means for each

characteristic of quality, we notice that the differences are

small and difficult to pick the extreme cases.

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 90

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

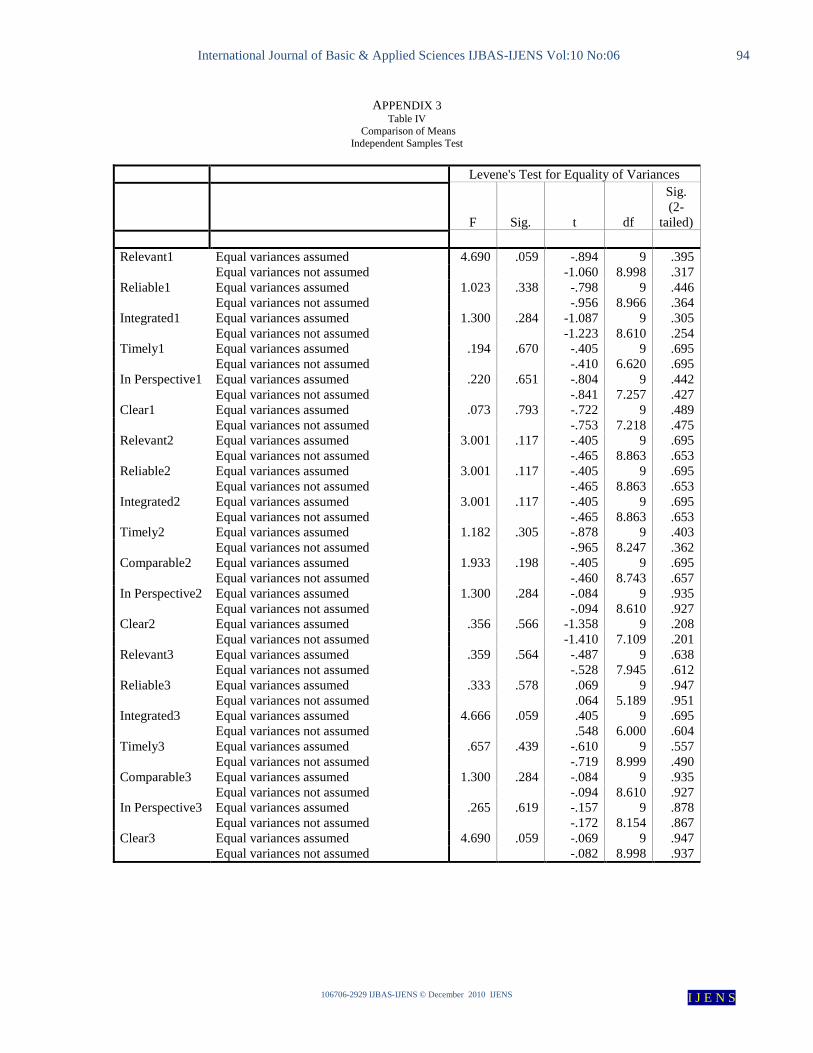

However, using the result of Levene’s test for equality of

variance, the degree of significance for each pair indicates that

there are significant differences between the means of the pair.

Three most significant differences are for the ‘Relevant

of information’ related to ‘Overall policies and guidelines’,

degree of Integrated and Clarity of information related to the

‘Overall management and performance of the organization’.

These are the three areas where the level of satisfaction with

the information quality differs greatly.

However, these three differences are only significant at 90%

confidence level.

VII. DISCUSSION

From the analysis discussed in the previous section, we can

deduce three points. Firstly, the quality of information

provided to Board of Directors is high. Secondly, there is a

convergence of opinion between the Management and BOD

on the above issue. Lastly, the satisfaction of BOD as the user

of the information is higher than that of the Management as

the preparer of that information. Following this, the higher

institution of learning where this research was conducted can

feel assured that Management understands its role and

responsibility with respect to providing of information to

BOD.

Although the scores for all the seven quality dimensions of

information are above average, on closer examination of the

mean scores in Table II, we notice that there is a quality

dimension that persistently scores lower than the rest.

‘Timeliness of the information’ scores lowest among the seven

dimensions in two items while third lowest in another. This

indicates that a possible room for improvement of the

information quality lies in improving the timeliness of the

information.

As mentioned in the introduction, the objective of this pilot

study is to evaluate the suitability of the instrument in

measuring the quality of information. From the descriptive

analysis, variation in the mean scores reflects the instrument’s

capability of capturing variations among respondents. The

five-point Likert scales used do provide reasonable choice to

respondents in deciding the quality level they select for a

given dimension.

Nevertheless, the major problem faced by the researchers is in

the administration of the instrument. It is a big challenge to get

the cooperation of Management as well as the BOD and a

much bigger challenge is in collecting the completed

questionnaires from the respondents. To overcome these

problems, in our future surveys, it is proposed that due

consent of top management of an organization or a group of

organizations be obtained accordingly, and secondly to

administer the data collection on the day of the Board sitting

i.e. when the Board concludes their meeting. This approach

will overcome the problems of collecting the questionnaires

from the respondents, and also the difficulty experienced by

the respondents in answering the questions.

VIII. CONCLUSION

Finally we conclude that the instrument is effective and

efficient in measuring the quality of information provided by

the Management to BOD. We may need to alter some of the

three items of information according to nature of the

organization tested or the order (reverse and forward) of the

questions.

REFERENCES [1] Adams, R., & Ferreria, D. (2003). A Theory of Corporate Boards,

Working Paper. SITE-Stockholm School of Economics.

[2] Cadbury, A. (1992). Report of the Committee on the Financial

Aspect of Corporate Governance, Gee. London. [3] Chhaochharia, V., & Grinstein, Y., (2005a). The Transformation

of US Corporate Boards: 1997–2003. Working Paper. Cornell

University. [4] Chhaochharia, V., & Grinstein, Y., (2005b). Corporate

Governance and Firm Value: The Impact of the 2002 Governance

Rules. Working Paper. Cornell University. [5] Coles, J.L., Daniel, N., & Naveen, L. (2005). Boards: Does One

Size Fit All? Working Paper. Arizona State University.

[6] Cornforth, C. (2001). What makes boards effective? An examination of the relationships between board inputs, structures,

processes and effectiveness in non-profit organizations’ Corporate

Governance: An International Review, Vol. 9 No. 3, pp. 217-27. [7] Daily, C., Dalton, D. & Cannella, A. (2003). Corporate

governance: decades of dialogue and data, Academy of Management Review, Vol. 28 No. 3, pp. 371-82.

[8] Deli, D.N., & Gillan, S.L. (2000). On the demand for independent

and active audit committees. Journal of Corporate Finance 6 (2), 427– 445.

[9] Delone, W.H. & McLean,E.R. (1992). Information systems

success: the quest for the dependent variable, Information systems research 3 (1), pp. 60–95.

[10] Finance Committee on Corporate Governance (2000). Malaysian

Code on Corporate Governance, Securities Commission. [11] Finance Committee on Corporate Governance (2001). Report on

Corporate Governance, Securities Commission.

[12] Forbes, D. and Milliken, F. (1999). ‘‘Cognition and corporate governance: understanding boards of directors as strategic

decision-making groups’’, Academy of Management Review, Vol.

24 No. 3, pp. 489-505. [13] Forslund, H. (2007). Measuring information quality in the order

fulfilment process, International Journal of Quality & Reliability

Management Vol. 24 No. 5, pp. 515-524 [14] Gelle. E. & Karhu. K. (2003) Information quality for strategic

technology planning Industrial Management and Data

Systems,Vol. 103, Issue 8-9, pp 633-643. [15] Gillan, S.L. (2006). Recent development in corporate governance:

an overview. Journal of Corporate Finance, 12 (2006) 381-402

[16] Gillette, A.B., Noe, T.H., & Rebello, M.J. (2003). Corporate board composition, protocols, and voting behavior: experimental

evidence. Journal of Finance 58 (5), 1997–2032

[17] Harris, M., & Raviv, A. (2005). A Theory of Board Control and Size. Working Paper. University of Chicago.

[18] Healy, P.M., & Palepu K.G. (2001). Information asymmetry,

corporate disclosure, and the capital market: A review of the empirical disclosure literature. Journal of Accounting and

Economics 31, 405–440.

[19] Hermalin, B., & Weisbach, M. (1988). The determinants of board composition. Rand Journal of Economics 19 (4), 589–606.

[20] Hirst, M. K. (1983). Reliance on Accounting Performance

Measures, Task Uncertainty, and Dysfunctional Behavior: Some Extensions, Journal of Accounting Research, Autumn, p. 596-605.

[21] Hopwood, A.G. (1972). An Empirical Study of the Role of

Accounting Data in Performance Evaluation. Empirical Research in Accounting, Supplement to Journal of Accounting Research, p.

156-182

[22] Ittner, C., D. Larcker and M. Rajan. (1997). The choice of performance measures in annual bonus contracts. The Accounting

Review (April): 231-255.

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 91

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

[23] Jarke,M. & Vassiliou,Y. (1997). Data warehouse quality: a review

of the DWQ project, Proceedings of the Conference on

Information Quality, Cambridge, MA, , pp. 299–313.

[24] John, K. & Senbet, L.W. (1998). Corporate governance and board

effectiveness. Journal of banking and Finance, 22, 371-403. [25] Kaplan, R., Norton, D. (1992). The balanced scorecard: Measures

that drive performance. The Harvard Business Review, January–

February, 71–79. [26] Kaplan, R., Norton, D. (1993). Putting the balanced scorecard to

work. The Harvard Business Review, September–October, 134–

147. [27] Klein, A. (1998). Firm performance and board committee

structure. Journal of Law and Economics, 137– 165.

[28] Klein, A. (2002). Economic determinants of audit committee independence. Accounting Review 77, 435–452.

[29] Lambert R.A. (2001). Contracting theory and accounting. Journal

of Accounting and Economics, 32, 3–8. [30] Lasfer, M. A. (2004). On the role of the board of directors: the

case of the adoption of Cadbury Recommendations in the

U.K.Corporate Governance, Advances in Financial Economics, Volume 9, 287–326

[31] Lee, Y.W., Strong, D. M., Kahn, B. K., and Wang, R.Y. (2002).

AIMQ: a methodology for information quality assessment. Information & Management 40,133–146

[32] Linck, J.S., Netter, J., & Yang, T. (2005a). The Determinants of

Board Structure. Working Paper. University of Georgia. [33] Linck, J.S., Netter, J., & Yang, T., 2005b. Effects and Unintended

Consequences of the Sarbanes Oxley Act on Corporate Boards. Working Paper. University of Georgia.

[34] Lorsch, J., & MacIver, E. (1989). Pawns or potentates. Boston,

MA: Harvard Business School Press. [35] Ong C.H. & Wan, D. (2008). Three conceptual models of board

role performance. Corporate Governance Vol 8 No. 3 2008, pp.

317-329 [36] Otley, D.T. (1978). Budget Use and Managerial Performance,

Journal of Accounting Research, p. 122-149.

[37] Parasuraman, A., Zeithaml, V.A. and Berry, L.L. (1985), “A conceptual model of service quality and its implications for future

research”, Journal of Marketing, Vol. 49, pp. 41-50.

[38] Parasuraman, A., Zeithaml, V.A. and Berry, L.L. (1988), “SERVQUAL: a multiple-item scale for measuring consumer

perceptions of service quality”, Journal of Retailing, Vol. 64 No.

1, pp. 12-40. [39] Price,R.; Shanks,G. (2005). A semiotic information quality

framework: Development and comparative analysis. Journal of

Information Technology, 2005, 20, 2, 88-102 [40] Raheja, C. (2005). Determinants of board size and composition: a

theory of corporate boards. Journal of Financial and Quantitative

Analysis 40 (2), 283– 306.

[41] Rosenstein, S., & Wyatt, J.G., 1990. Outside directors, board

independence and shareholder wealth. Journal of Financial Economics 26, 175– 191.

[42] Solomon, J. & Solomon A., (2004). Corporate Governance and

Accountability. John Wiley & Sons,Ltd. pp. 14 [43] Stanwick, P.A and Stanwick S.D.(2009), Understanding Business

Ethics, New Jersey; Pearson Education Inc, Prentice Hall

[44] Starovic, Danka. (2003). Performance Reporting to Boards: A Guide to Good Practice, The Chartered Institute of Management

Accountants . Retrieved November 4, 2008, from

http://www2.cimaglobal.com/cps/rde/xbcr/SID-0A82C289- 07A1F0A6/live/perfrpttoboards_techguides_2003.pdf

[45] Toften, K. & Rustad, K., (2005). Attributes of information

qualityof export market assistance: an exploratory study, European Journal of Marketing Vol. 39 No. 5/6, pp. 676-695

[46] Vafeas, N. (1999). Board meeting frequency and firm

performance. Journal of Financial Economics 53 (1), 113–142. [47] Van den Berghe, L. & Baelden, T. (2003). The monitoring role of

the board: one approach does not fit all. Corporate Governance:

An international review vol.13 pt 5 pp.680-690 [48] Wang, R.Y. & Strong, D.M. (1996). Beyond accuracy: what data

quality means to data consumers, Journal of Management

Information Systems 12 (4), pp. 5–34. [49] Warther, V.A. (1998). Board effectiveness and board dissent: a

model of the board’s relationship to management and shareholders.

Journal of Corporate Finance 4, 53– 70. [50] Westphal, J.D. (1999). Collaboration in the boardroom: the

consequences of social ties in the CEO/board relationship, Academy of Management Journal, Vol. 42, pp. 7-24.

[51] Yermack, D. (1996). Higher market valuation of companies with a

small board of directors. Journal of Financial Economics 40 (2), 185–213.

[52] Yussoff I., Daing , N. I., & Subramaniam S.P. (2008). Effect of

emphasis on non-financial indicators on management control system: Malaysian manufacturing experience. Working paper

presented at Global Management Accounting Research

Symposium, UNSW [53] Zahra, S. & Pearce, J (1989). Boards of directors and corporate

financial performance: a review and integrative model. Journal of

Management, Vol. 15 No. 2, pp. 291-334. [54] Zmud R. (1978). Concepts, theories and techniques: an empirical

investigation of the dimensionality of the concept of information,

Decision Sciences 9 (2), pp. 187–195.

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 92

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

APPENDIX 1 Table II

Result of Descriptive Analysis

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Relevant1 11 3.00 5.00 4.4545 .82020

Reliable1 11 2.00 5.00 4.1818 .98165

Integrated1 11 3.00 5.00 4.4545 .68755

Timely1 11 3.00 5.00 4.0909 .94388

Comparable1 11 2.00 5.00 4.0000 1.09545

In Perspective1 11 2.00 5.00 3.9091 1.04447

Clear1 11 2.00 5.00 4.1818 1.07872

Relevant2 11 3.00 5.00 4.3636 .80904

Reliable2 11 3.00 5.00 4.3636 .80904

Integrated2 11 3.00 5.00 4.3636 .80904

Timely2 11 2.00 5.00 3.6364 1.02691

Comparable2 11 3.00 5.00 3.6364 .67420

In Perspective2 11 3.00 5.00 3.7273 .64667

Clear2 11 2.00 5.00 3.9091 1.13618

Relevant3 11 3.00 5.00 4.3636 .67420

Reliable3 11 3.00 5.00 4.2727 .78625

Integrated3 11 3.00 5.00 4.0909 .53936

Timely3 11 2.00 5.00 3.2727 .90453

Comparable3 11 3.00 5.00 3.7273 .64667

In Perspective3 11 3.00 5.00 3.4545 .68755

Clear3 11 3.00 5.00 3.7273 .78625

Valid N (list wise) 11

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 93

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

APPENDIX 2 Table III

Group Statistics

Group N Mean Std. Deviation

Std. Error

Mean

Relevant1 1 7 4.2857 .95119 .35952

2 4 4.7500 .50000 .25000

Reliable1 1 7 4.0000 1.15470 .43644

2 4 4.5000 .57735 .28868

Integrated1 1 7 4.2857 .75593 .28571

2 4 4.7500 .50000 .25000

Timely1 1 7 4.0000 1.00000 .37796

2 4 4.2500 .95743 .47871

In Perspective1 1 7 3.7143 1.11270 .42056

2 4 4.2500 .95743 .47871

Clear1 1 7 4.0000 1.15470 .43644

2 4 4.5000 1.00000 .50000

Relevant2 1 7 4.2857 .95119 .35951

2 4 4.5000 .57735 .28867

Reliable2 1 7 4.2857 .95119 .35952

2 4 4.5000 .57735 .28868

Integrated2 1 7 4.2857 .95119 .35952

2 4 4.5000 .57735 .28868

Timely2 1 7 3.4286 1.13389 .42857

2 4 4.0000 .81650 .40825

Comparable2 1 7 3.5714 .78680 .29738

2 4 3.7500 .50000 .25000

In Perspective2 1 7 3.7143 .75593 .28571

2 4 3.7500 .50000 .25000

Clear2 1 7 3.5714 1.13389 .42857

2 4 4.5000 1.00000 .50000

Relevant3 1 7 4.2857 .75593 .28571

2 4 4.5000 .57735 .28868

Reliable3 1 7 4.2857 .75593 .28571

2 4 4.2500 .95743 .47871

Integrated3 1 7 4.1429 .69007 .26082

2 4 4.0000 .00000 .00000

Timely3 1 7 3.1429 1.06904 .40406

2 4 3.5000 .57735 .28868

Comparable3 1 7 3.7143 .75593 .28571

2 4 3.7500 .50000 .25000

In Perspective3 1 7 3.4286 .78680 .29738

2 4 3.5000 .57735 .28868

Clear3 1 7 3.7143 .95119 .35952

2 4 3.7500 .50000 .25000

Note;

Group value; 1 – Management

2 – Board of Directors

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 94

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

APPENDIX 3 Table IV

Comparison of Means

Independent Samples Test

Levene's Test for Equality of Variances

F Sig. t df

Sig.

(2-

tailed)

Relevant1 Equal variances assumed 4.690 .059 -.894 9 .395

Equal variances not assumed -1.060 8.998 .317

Reliable1 Equal variances assumed 1.023 .338 -.798 9 .446

Equal variances not assumed -.956 8.966 .364

Integrated1 Equal variances assumed 1.300 .284 -1.087 9 .305

Equal variances not assumed -1.223 8.610 .254

Timely1 Equal variances assumed .194 .670 -.405 9 .695

Equal variances not assumed -.410 6.620 .695

In Perspective1 Equal variances assumed .220 .651 -.804 9 .442

Equal variances not assumed -.841 7.257 .427

Clear1 Equal variances assumed .073 .793 -.722 9 .489

Equal variances not assumed -.753 7.218 .475

Relevant2 Equal variances assumed 3.001 .117 -.405 9 .695

Equal variances not assumed -.465 8.863 .653

Reliable2 Equal variances assumed 3.001 .117 -.405 9 .695

Equal variances not assumed -.465 8.863 .653

Integrated2 Equal variances assumed 3.001 .117 -.405 9 .695

Equal variances not assumed -.465 8.863 .653

Timely2 Equal variances assumed 1.182 .305 -.878 9 .403

Equal variances not assumed -.965 8.247 .362

Comparable2 Equal variances assumed 1.933 .198 -.405 9 .695

Equal variances not assumed -.460 8.743 .657

In Perspective2 Equal variances assumed 1.300 .284 -.084 9 .935

Equal variances not assumed -.094 8.610 .927

Clear2 Equal variances assumed .356 .566 -1.358 9 .208

Equal variances not assumed -1.410 7.109 .201

Relevant3 Equal variances assumed .359 .564 -.487 9 .638

Equal variances not assumed -.528 7.945 .612

Reliable3 Equal variances assumed .333 .578 .069 9 .947

Equal variances not assumed .064 5.189 .951

Integrated3 Equal variances assumed 4.666 .059 .405 9 .695

Equal variances not assumed .548 6.000 .604

Timely3 Equal variances assumed .657 .439 -.610 9 .557

Equal variances not assumed -.719 8.999 .490

Comparable3 Equal variances assumed 1.300 .284 -.084 9 .935

Equal variances not assumed -.094 8.610 .927

In Perspective3 Equal variances assumed .265 .619 -.157 9 .878

Equal variances not assumed -.172 8.154 .867

Clear3 Equal variances assumed 4.690 .059 -.069 9 .947

Equal variances not assumed -.082 8.998 .937

International Journal of Basic & Applied Sciences IJBAS-IJENS Vol:10 No:06 95

106706-2929 IJBAS-IJENS © December 2010 IJENS I J E N S

APPENDIX 4

Information related to;

Quality Dimensions

Relevant Reliable Integrated

1. Overall policies and

guidelines1

2. Business Plan and

Budget2

3. Overall management

and performance of

the organization3

Rating What each rating means

1

The information

presented was

extremely related to the

decision.

I have no confidence in

the quality of the

information presented.

The information presented

totally contradicts with

information reported

externally.

2

This information

presented was

substantially related to

the decision.

I have little confidence

in the information

presented.

The information presented

slightly contradicts with

information reported

externally.

3

This information

presented was

moderately related to

the decision.

I have moderate

confidence in the

information presented.

The information presented

matches with information

reported externally.

4

This information

presented was least

related to the decision.

I have sufficient

confidence in the

information presented.

The information presented

is substantially in line

with information reported

externally.

5

This information

presented was not

related to the decision.

I have high confidence

in the information

presented.

This information is

totally in line with

information reported

externally.

Information related to;

Quality Dimensions

Timely Comparable In perspective Clear

1. Overall policies and

guidelines1

2. Business Plan and Budget2

3. Overall management and performance of the

organization3

Rating What each rating means

1

The information presented came very

late.

The comparative data provided was

extremely

appropriate.

The information provided was perfectly

categorized by period.

The information presented was very

clear.

2

The information

presented came a bit

late.

The comparative

data provided was

substantially

appropriate.

The information provided

was substantially well

categorized by period.

The information

presented was

moderately clear.

3

The information

presented came

timely.

The comparative

data provided was

appropriate.

The information provided

was well categorized by period.

The information

presented was clear.

4

The information

presented came quite

timely.

The comparative

data provided was

slightly

inappropriate.

The information provided

was barely categorized

by period.

The information

presented was

confusing.

5

The information

presented came at the

most appropriate

time.

The comparative

data provided was

highly

inappropriate.

The information provided

was not categorized by period.

The information

presented was very

distorted.