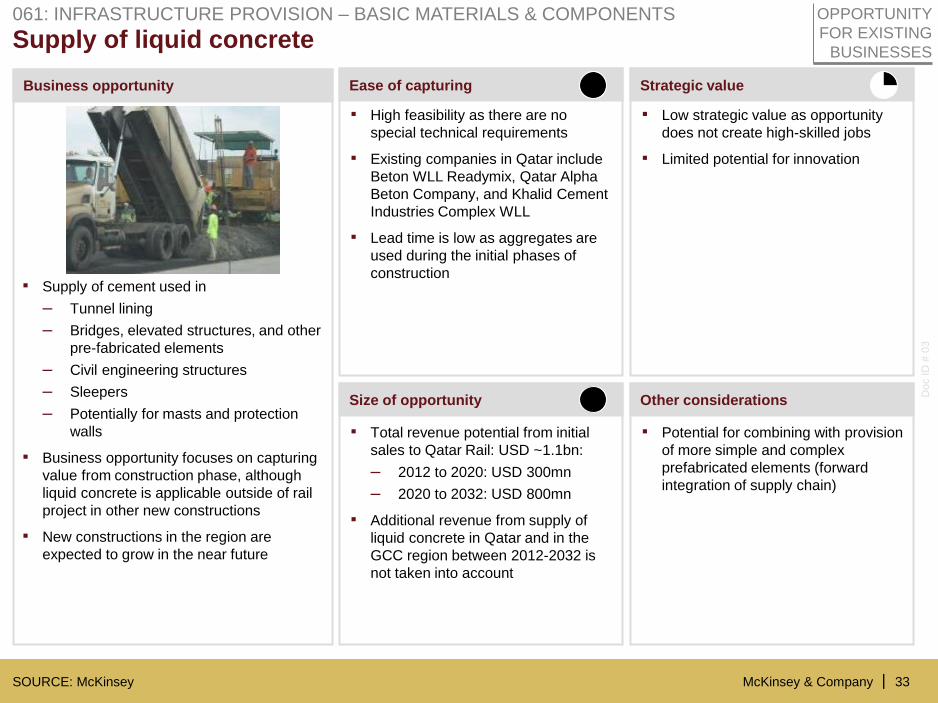

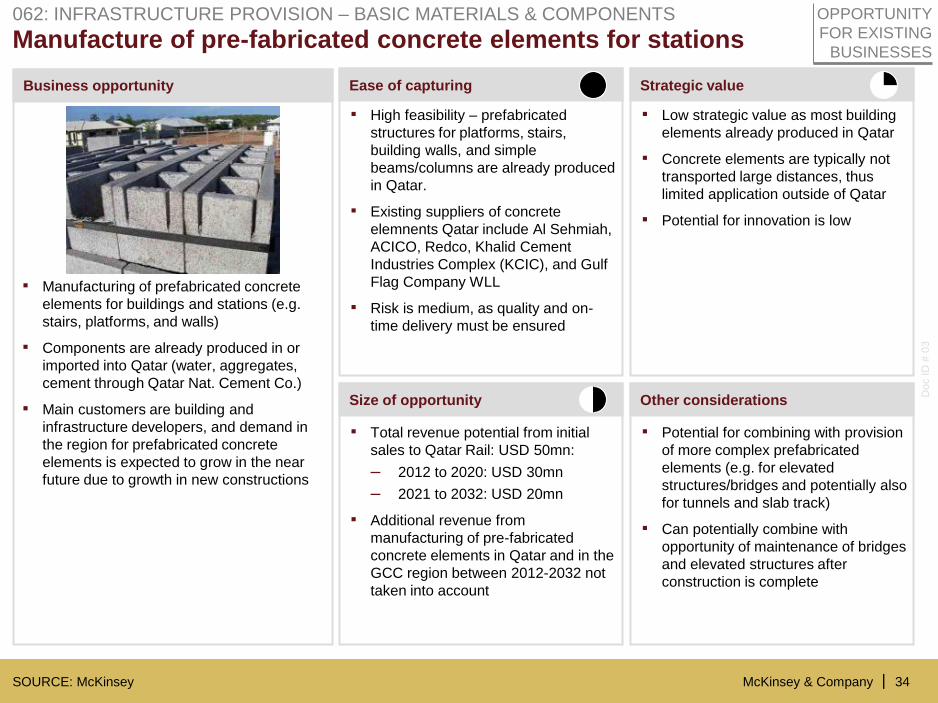

Embed Size (px)

Citation preview

Doc. No.: P000-SPM-EMT-RPT-00003 Rev. 1.0 05/11/13 Printed copy is uncontrolled and only valid at the time of printing. Always refer to the electronic copy as the latest version.

Qatar Rail

Business Opportunities

Information Booklet

Qatar Rail – Business Opportunities Information Booklet

Doc. No.: P000-SPM-EMT-RPT-00003 Rev. 1.0 05/11/13 ii Printed copy is uncontrolled and only valid at the time of printing. Always refer to the electronic copy as the latest version.

Table of contents

1 Introduction ......................................................................................................................... 1

1.1 General ................................................................................................................................................................... 1

1.1.1 Business Opportunity Profiles .............................................................................................................................. 1

1.1.2 Review by Qatar Rail ............................................................................................................................................. 1

1.1.3 Input by Qatar Rail Contractors ........................................................................................................................... 1

1.2 Investment Laws .................................................................................................................................................. 2

Appendices

Appendix A Qatar Rail Civil Engineering Contractors Potential Business Opportunities – Top Priorities

Appendix B McKinsey Report

Qatar Rail – Business Opportunities Information Booklet

Doc. No.: P000-SPM-EMT-RPT-00003 Rev. 1.0 05/11/13 1 Printed copy is uncontrolled and only valid at the time of printing. Always refer to the electronic copy as the latest version.

1 Introduction

1.1 General

This booklet provides potential investors with information about the work that has been

done to date by Qatar Rail, its partners, consultants and contractors in relation to future

business opportunities arising from implementation of the Qatar Rail program.

1.1.1 Business Opportunity Profiles

In order to assess the potential for new business opportunities that construction of the

railway program could generate Qatar Rail, in association with its partner Qatar

Development Bank appointed McKinsey & Company to carry out a comprehensive

investigation.

McKinsey reported in July 2012 by issuing a compilation of potential opportunities

complete with information about ease of capture, strategic value and size for each

opportunity across a range of disciplines. The McKinsey & Company report ‘Provision of

Business Analysis Services for Qatar Railways Company’ is contained in Appendix A.

1.1.2 Review by Qatar Rail

In May 2013 a review of the McKinsey report was carried out by Qatar Rail with assistance

from their strategic consultants and project managers. The outcome of the review was to

accept the McKinsey report and to add a number of further opportunities. In addition a

study was carried out to investigate the way in which the opportunities were spread along

the Qatar Rail implementation timeline.

1.1.3 Input by Qatar Rail Contractors

Following a successful procurement process Qatar Rail appointed the first four engineering

contractors whose scope is to design, build and complete the sub-surface parts of the Metro

including tunnels, stations, building services and architectural works. Each of the

contractors was asked to review the opportunities and to advise which ones held a potential

for future investment. They were also asked to indicate five ‘top priorities’ where they

considered the potential for return to be greatest.

The result of the contractors’ consideration and identification of their top priorities is

tabulated in Appendix A. Indicative values have been included where these are known. The

values are generally those that were reported by McKinsey in their report.

Qatar Rail – Business Opportunities Information Booklet

Doc. No.: P000-SPM-EMT-RPT-00003 Rev. 1.0 05/11/13 2 Printed copy is uncontrolled and only valid at the time of printing. Always refer to the electronic copy as the latest version.

1.2 Investment Laws

The Qatar Ministry of Business and Trade highlights, on their website, a number of

Investment Laws to which foreign investor shall abide. These can be found through the

following link:

http://www.investinqatar.com.qa/English/ForeignInvestor/Pages/Investmentlaws.aspx

The relevant Laws are as follows:

Law No.2 of the year 2005 on the amendment of some provisions of Law No.13 of the year 2000 on Organization of Foreign Capital Investment in the economic activities

Law No.5 of the year 2005 on Protection of Secrets of Trade

Law No.7 of 2002: Law on the protection of copyright and neighbouring rights

Law No.8 of 2002 on Organization of Business of Commercial

Law No.9 of 2002: Law on Trademarks, Commercial Indications, Trade names, Geographical Indications and Industrial Designs

Law No.13 of 2000: Qatar's Investment Law Regulating the investment of foreign capital in economic activities

Law No.30 of the year 2004 Regulating Control of Accounts

Decree Law No.31 of the year 2004 on Amendment of some provisions of Law No.13 of the year 2000 on Organization of Foreign Capital Investment in Economic Activities

Qatar Rail – Business Opportunities Information Booklet

Doc. No.: P000-SPM-EMT-RPT-00003 Rev. 1.0 05/11/13 A-1 Printed copy is uncontrolled and only valid at the time of printing. Always refer to the electronic copy as the latest version.

Appendix A

Qatar Rail Civil Engineering Contractors Potential Business Opportunities Top Priorities

Appendix A Qatar Rail Civil Engineering Contractors Potential Business Opportunities Top Priorities

Ref. Potential

Opportunity Description Timeline

Indicative

Value

(US$ millions)

Indicative

Quantity

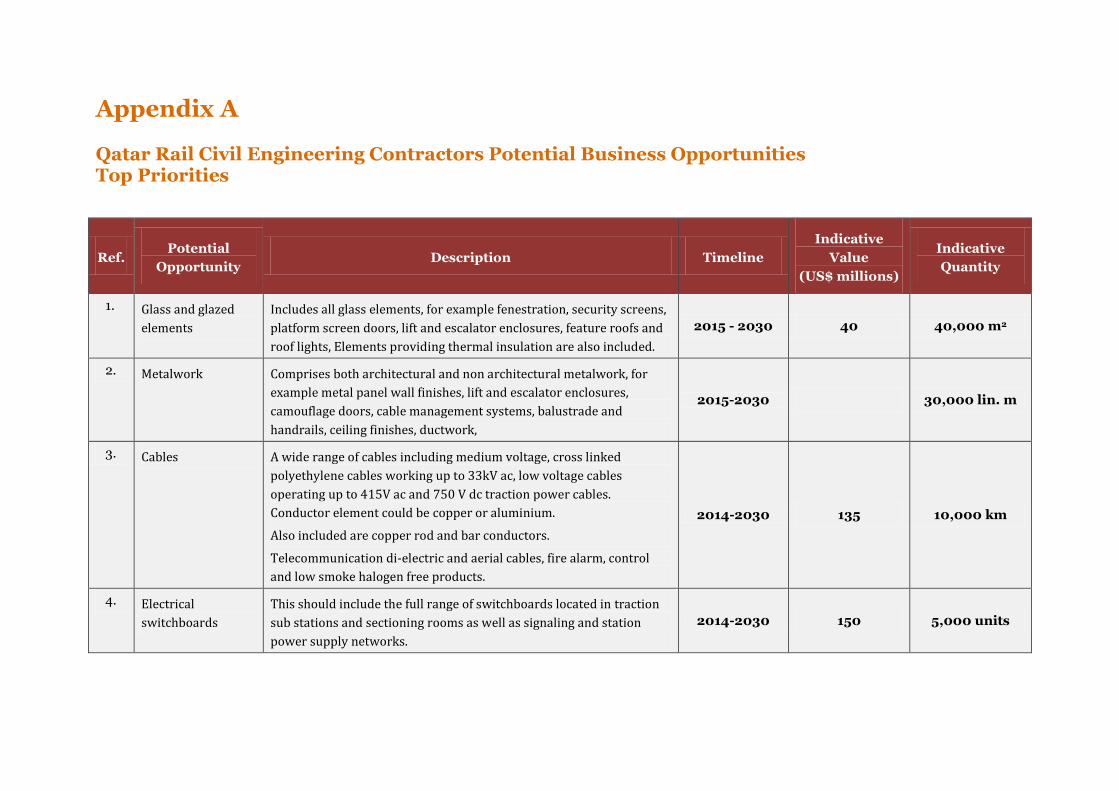

1. Glass and glazed

elements

Includes all glass elements, for example fenestration, security screens,

platform screen doors, lift and escalator enclosures, feature roofs and

roof lights, Elements providing thermal insulation are also included.

2015 - 2030 40 40,000 m2

2. Metalwork Comprises both architectural and non architectural metalwork, for

example metal panel wall finishes, lift and escalator enclosures,

camouflage doors, cable management systems, balustrade and

handrails, ceiling finishes, ductwork,

2015-2030 30,000 lin. m

3. Cables A wide range of cables including medium voltage, cross linked

polyethylene cables working up to 33kV ac, low voltage cables

operating up to 415V ac and 750 V dc traction power cables.

Conductor element could be copper or aluminium.

Also included are copper rod and bar conductors.

Telecommunication di-electric and aerial cables, fire alarm, control

and low smoke halogen free products.

2014-2030 135 10,000 km

4. Electrical

switchboards

This should include the full range of switchboards located in traction

sub stations and sectioning rooms as well as signaling and station

power supply networks.

2014-2030 150 5,000 units

Ref. Potential

Opportunity Description Timeline

Indicative

Value

(US$ millions)

Indicative

Quantity

5. Fire rated doors Fire rated doors will be used in all front and back of house locations.

There will be a variety of ratings. Standardisation across the system is

a desirable objective.

17,000 units

6. Personal protective

equipment

This includes a range or personal items in the first instance worn by

operatives in the civil engineering discipline. There will be demand for

more specialized items as railway systems installation progresses and

an ongoing demand during the operational and maintenance life of the

railway.

2013-2030 30,000

personnel

7. Energy efficient

lighting

installations and

consumables

Lighting installations and fittings that meet the objectives of energy

efficiency and reasonable systemwide uniformity provide opportunity

for local product and consumable design development and

manufacture.

2015-2030 145 200,000 units

8. Environmental

testing and

commissioning

Environmental testing and commissioning is likely to involve

significant service industry input rather than being goods based. Such

industry is likely to require back up from laboratories and testing

houses.

2015-2030

9. Communications

display equipment

Such display equipment will occur across the network. Some will be

integrated and interlocked with the signaling system. Other

equipment will be less specialized although still forming a part of a

communications system. Equipment is likely to comprise electronic

components, wiring, illumination, display screen and physical

containment

2016-2030 3 5,000 units

Ref. Potential

Opportunity Description Timeline

Indicative

Value

(US$ millions)

Indicative

Quantity

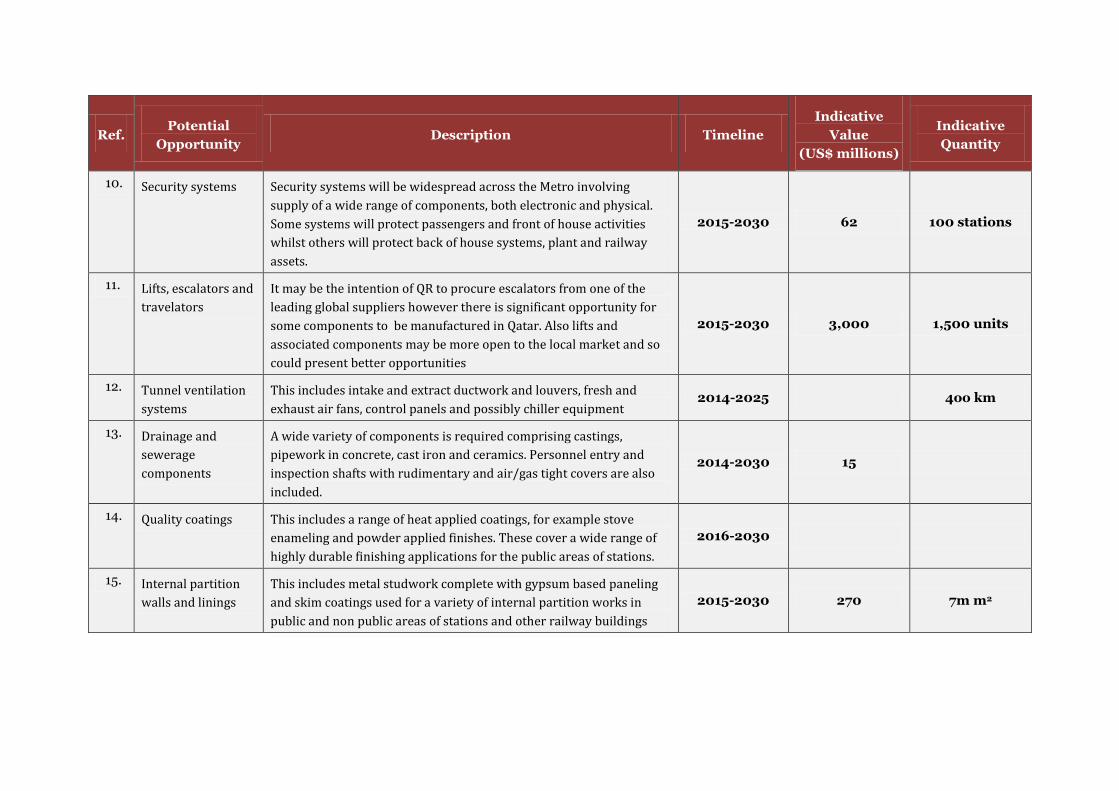

10. Security systems Security systems will be widespread across the Metro involving

supply of a wide range of components, both electronic and physical.

Some systems will protect passengers and front of house activities

whilst others will protect back of house systems, plant and railway

assets.

2015-2030 62 100 stations

11. Lifts, escalators and

travelators

It may be the intention of QR to procure escalators from one of the

leading global suppliers however there is significant opportunity for

some components to be manufactured in Qatar. Also lifts and

associated components may be more open to the local market and so

could present better opportunities

2015-2030 3,000 1,500 units

12. Tunnel ventilation

systems

This includes intake and extract ductwork and louvers, fresh and

exhaust air fans, control panels and possibly chiller equipment 2014-2025 4oo km

13. Drainage and

sewerage

components

A wide variety of components is required comprising castings,

pipework in concrete, cast iron and ceramics. Personnel entry and

inspection shafts with rudimentary and air/gas tight covers are also

included.

2014-2030 15

14. Quality coatings This includes a range of heat applied coatings, for example stove

enameling and powder applied finishes. These cover a wide range of

highly durable finishing applications for the public areas of stations.

2016-2030

15. Internal partition

walls and linings

This includes metal studwork complete with gypsum based paneling

and skim coatings used for a variety of internal partition works in

public and non public areas of stations and other railway buildings

2015-2030 270 7m m2

Ref. Potential

Opportunity Description Timeline

Indicative

Value

(US$ millions)

Indicative

Quantity

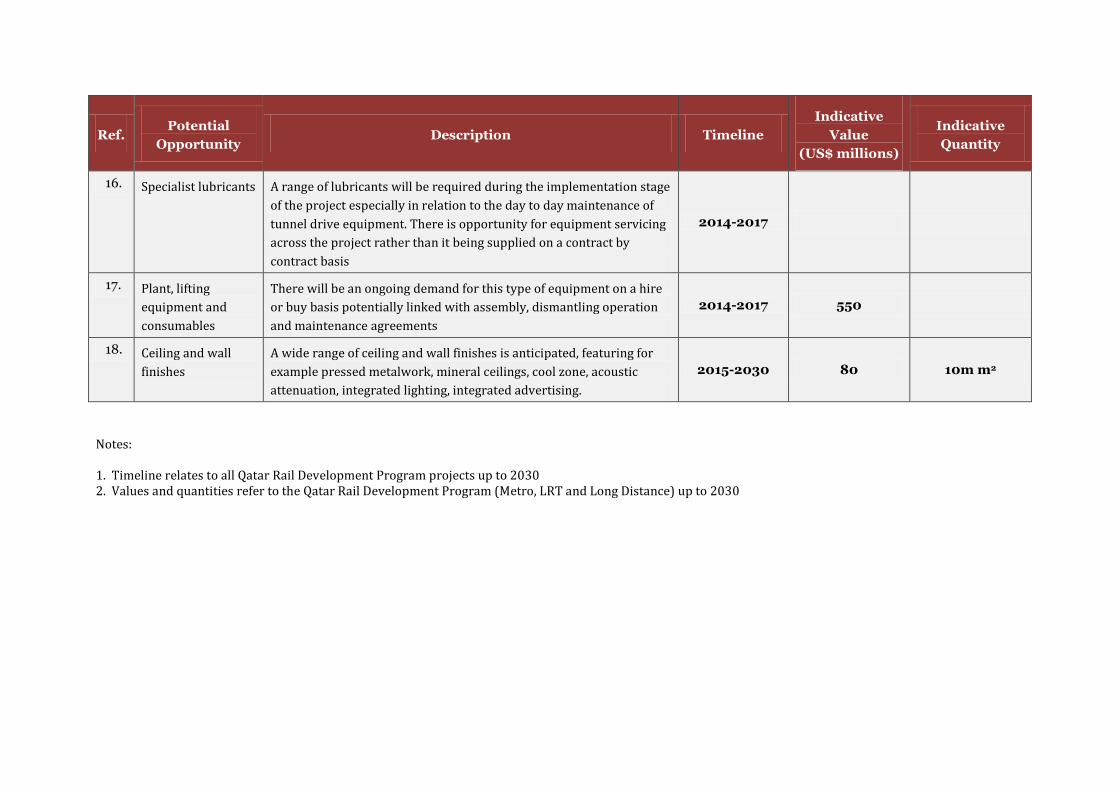

16. Specialist lubricants A range of lubricants will be required during the implementation stage

of the project especially in relation to the day to day maintenance of

tunnel drive equipment. There is opportunity for equipment servicing

across the project rather than it being supplied on a contract by

contract basis

2014-2017

17. Plant, lifting

equipment and

consumables

There will be an ongoing demand for this type of equipment on a hire

or buy basis potentially linked with assembly, dismantling operation

and maintenance agreements

2014-2017 550

18. Ceiling and wall

finishes

A wide range of ceiling and wall finishes is anticipated, featuring for

example pressed metalwork, mineral ceilings, cool zone, acoustic

attenuation, integrated lighting, integrated advertising.

2015-2030 80 10m m2

Notes: 1. Timeline relates to all Qatar Rail Development Program projects up to 2030 2. Values and quantities refer to the Qatar Rail Development Program (Metro, LRT and Long Distance) up to 2030

Qatar Rail – Business Opportunities Information Booklet

Doc. No.: P000-SPM-EMT-RPT-00003 Rev. 1.0 05/11/13 B-1 Printed copy is uncontrolled and only valid at the time of printing. Always refer to the electronic copy as the latest version.

Appendix B

McKinsey Report

Doc ID

# 0

3

Provision of Business Analysis

Services for Qatar Railways

Company

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company is strictly prohibited

Business opportunity profiles

Doha, July 31, 2012

McKinsey & Company |

Doc ID

# 0

3

2

Contents

▪ Prioritized opportunities

– Infrastructure provision

– Infrastructure operations

– Rolling stock provision

– Transport operations

– Other opportunities

▪ Filtered out opportunities

▪ Appendix – Potential additional opportunities

McKinsey & Company |

Doc ID

# 0

3

3

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

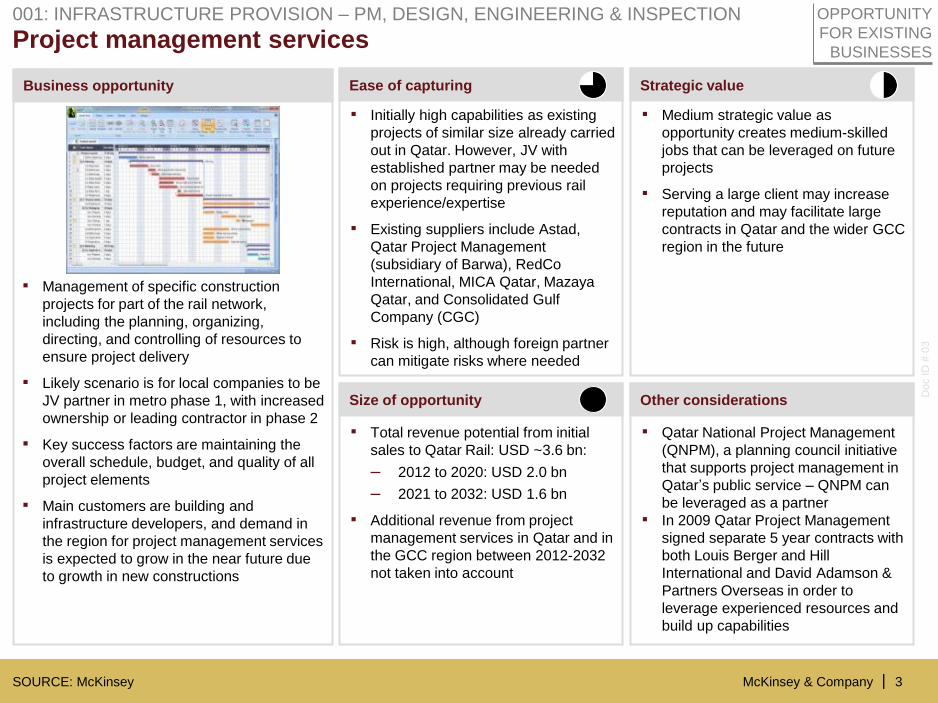

Project management services 001: INFRASTRUCTURE PROVISION – PM, DESIGN, ENGINEERING & INSPECTION

▪ Initially high capabilities as existing

projects of similar size already carried

out in Qatar. However, JV with

established partner may be needed

on projects requiring previous rail

experience/expertise

▪ Existing suppliers include Astad,

Qatar Project Management

(subsidiary of Barwa), RedCo

International, MICA Qatar, Mazaya

Qatar, and Consolidated Gulf

Company (CGC)

▪ Risk is high, although foreign partner

can mitigate risks where needed

▪ Medium strategic value as

opportunity creates medium-skilled

jobs that can be leveraged on future

projects

▪ Serving a large client may increase

reputation and may facilitate large

contracts in Qatar and the wider GCC

region in the future

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~3.6 bn:

– 2012 to 2020: USD 2.0 bn

– 2021 to 2032: USD 1.6 bn

▪ Additional revenue from project

management services in Qatar and in

the GCC region between 2012-2032

not taken into account

▪ Qatar National Project Management

(QNPM), a planning council initiative

that supports project management in

Qatar’s public service – QNPM can

be leveraged as a partner

▪ In 2009 Qatar Project Management

signed separate 5 year contracts with

both Louis Berger and Hill

International and David Adamson &

Partners Overseas in order to

leverage experienced resources and

build up capabilities

▪ Management of specific construction

projects for part of the rail network,

including the planning, organizing,

directing, and controlling of resources to

ensure project delivery

▪ Likely scenario is for local companies to be

JV partner in metro phase 1, with increased

ownership or leading contractor in phase 2

▪ Key success factors are maintaining the

overall schedule, budget, and quality of all

project elements

▪ Main customers are building and

infrastructure developers, and demand in

the region for project management services

is expected to grow in the near future due

to growth in new constructions

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

4

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

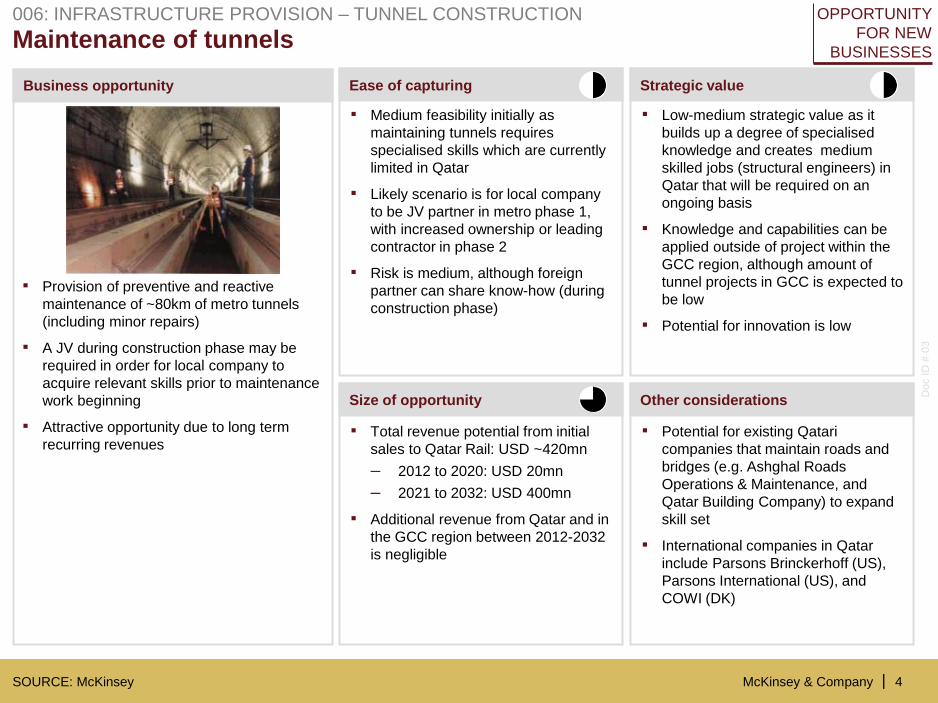

Maintenance of tunnels 006: INFRASTRUCTURE PROVISION – TUNNEL CONSTRUCTION

▪ Medium feasibility initially as

maintaining tunnels requires

specialised skills which are currently

limited in Qatar

▪ Likely scenario is for local company

to be JV partner in metro phase 1,

with increased ownership or leading

contractor in phase 2

▪ Risk is medium, although foreign

partner can share know-how (during

construction phase)

▪ Low-medium strategic value as it

builds up a degree of specialised

knowledge and creates medium

skilled jobs (structural engineers) in

Qatar that will be required on an

ongoing basis

▪ Knowledge and capabilities can be

applied outside of project within the

GCC region, although amount of

tunnel projects in GCC is expected to

be low

▪ Potential for innovation is low

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~420mn

– 2012 to 2020: USD 20mn

– 2021 to 2032: USD 400mn

▪ Additional revenue from Qatar and in

the GCC region between 2012-2032

is negligible

▪ Provision of preventive and reactive

maintenance of ~80km of metro tunnels

(including minor repairs)

▪ A JV during construction phase may be

required in order for local company to

acquire relevant skills prior to maintenance

work beginning

▪ Attractive opportunity due to long term

recurring revenues ▪ Potential for existing Qatari

companies that maintain roads and

bridges (e.g. Ashghal Roads

Operations & Maintenance, and

Qatar Building Company) to expand

skill set

▪ International companies in Qatar

include Parsons Brinckerhoff (US),

Parsons International (US), and

COWI (DK)

OPPORTUNITY

FOR NEW

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

5

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

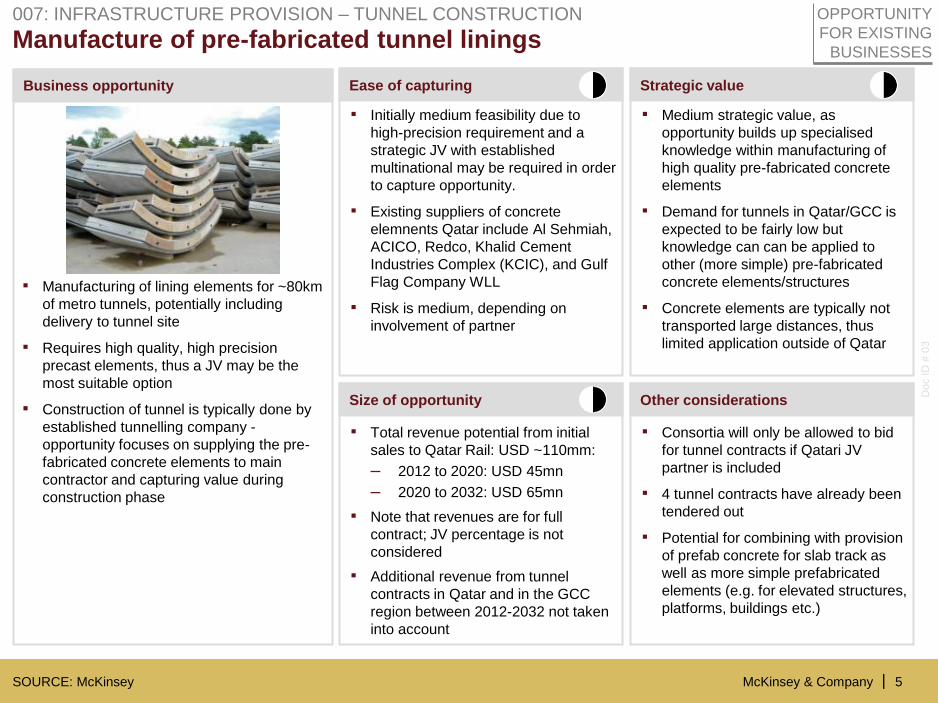

Manufacture of pre-fabricated tunnel linings 007: INFRASTRUCTURE PROVISION – TUNNEL CONSTRUCTION

▪ Initially medium feasibility due to

high-precision requirement and a

strategic JV with established

multinational may be required in order

to capture opportunity.

▪ Existing suppliers of concrete

elemnents Qatar include Al Sehmiah,

ACICO, Redco, Khalid Cement

Industries Complex (KCIC), and Gulf

Flag Company WLL

▪ Risk is medium, depending on

involvement of partner

▪ Medium strategic value, as

opportunity builds up specialised

knowledge within manufacturing of

high quality pre-fabricated concrete

elements

▪ Demand for tunnels in Qatar/GCC is

expected to be fairly low but

knowledge can can be applied to

other (more simple) pre-fabricated

concrete elements/structures

▪ Concrete elements are typically not

transported large distances, thus

limited application outside of Qatar

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~110mm:

– 2012 to 2020: USD 45mn

– 2020 to 2032: USD 65mn

▪ Note that revenues are for full

contract; JV percentage is not

considered

▪ Additional revenue from tunnel

contracts in Qatar and in the GCC

region between 2012-2032 not taken

into account

▪ Consortia will only be allowed to bid

for tunnel contracts if Qatari JV

partner is included

▪ 4 tunnel contracts have already been

tendered out

▪ Potential for combining with provision

of prefab concrete for slab track as

well as more simple prefabricated

elements (e.g. for elevated structures,

platforms, buildings etc.)

▪ Manufacturing of lining elements for ~80km

of metro tunnels, potentially including

delivery to tunnel site

▪ Requires high quality, high precision

precast elements, thus a JV may be the

most suitable option

▪ Construction of tunnel is typically done by

established tunnelling company -

opportunity focuses on supplying the pre-

fabricated concrete elements to main

contractor and capturing value during

construction phase

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

6

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

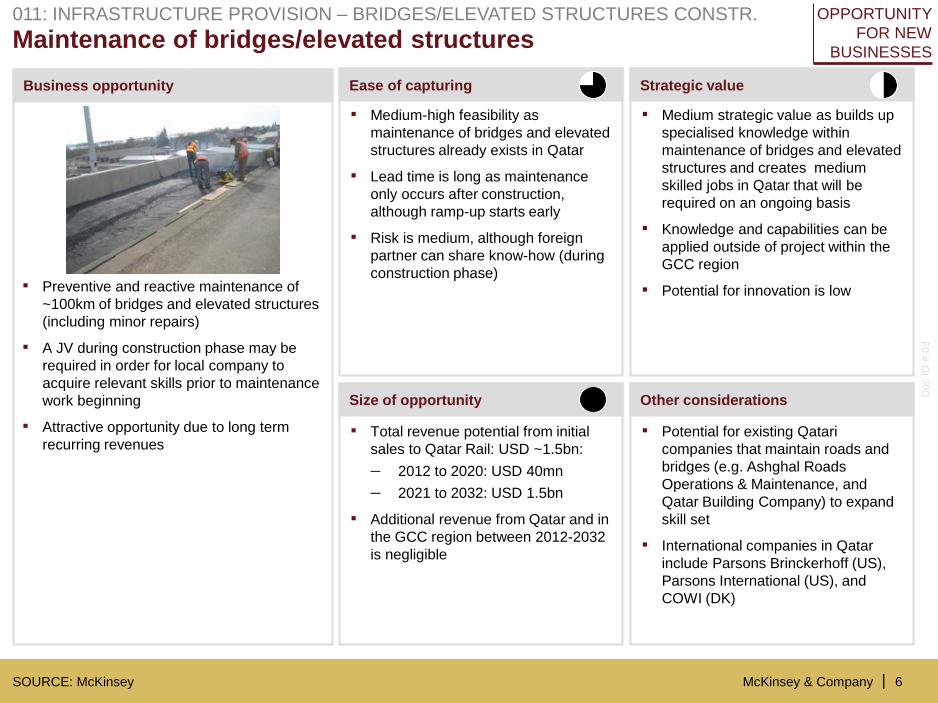

Maintenance of bridges/elevated structures 011: INFRASTRUCTURE PROVISION – BRIDGES/ELEVATED STRUCTURES CONSTR.

▪ Medium-high feasibility as

maintenance of bridges and elevated

structures already exists in Qatar

▪ Lead time is long as maintenance

only occurs after construction,

although ramp-up starts early

▪ Risk is medium, although foreign

partner can share know-how (during

construction phase)

▪ Medium strategic value as builds up

specialised knowledge within

maintenance of bridges and elevated

structures and creates medium

skilled jobs in Qatar that will be

required on an ongoing basis

▪ Knowledge and capabilities can be

applied outside of project within the

GCC region

▪ Potential for innovation is low

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~1.5bn:

– 2012 to 2020: USD 40mn

– 2021 to 2032: USD 1.5bn

▪ Additional revenue from Qatar and in

the GCC region between 2012-2032

is negligible

▪ Potential for existing Qatari

companies that maintain roads and

bridges (e.g. Ashghal Roads

Operations & Maintenance, and

Qatar Building Company) to expand

skill set

▪ International companies in Qatar

include Parsons Brinckerhoff (US),

Parsons International (US), and

COWI (DK)

▪ Preventive and reactive maintenance of

~100km of bridges and elevated structures

(including minor repairs)

▪ A JV during construction phase may be

required in order for local company to

acquire relevant skills prior to maintenance

work beginning

▪ Attractive opportunity due to long term

recurring revenues

OPPORTUNITY

FOR NEW

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

7

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

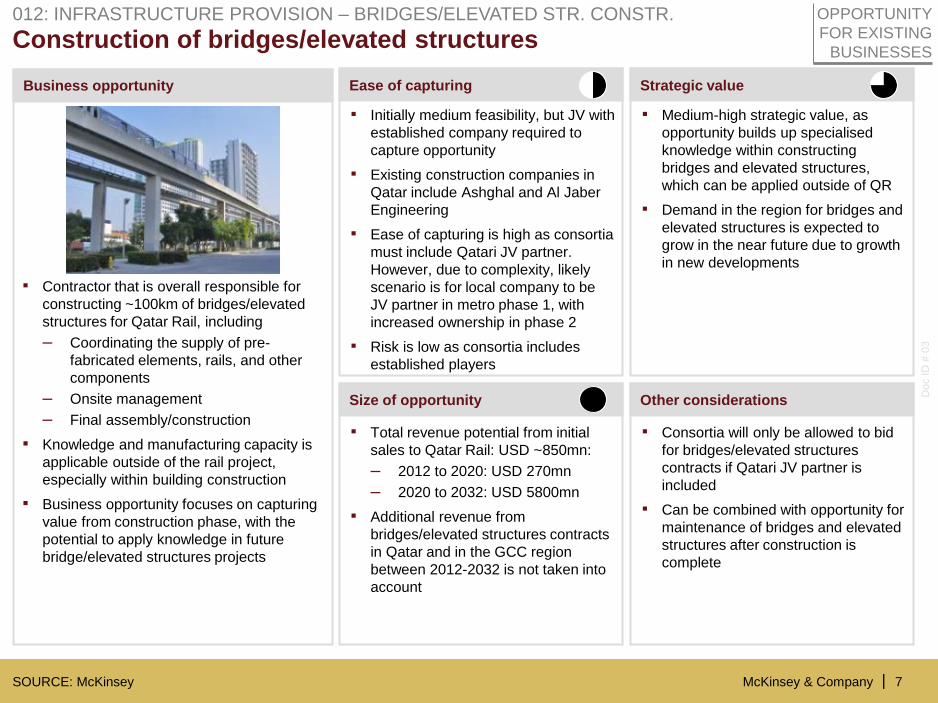

Construction of bridges/elevated structures 012: INFRASTRUCTURE PROVISION – BRIDGES/ELEVATED STR. CONSTR.

▪ Initially medium feasibility, but JV with

established company required to

capture opportunity

▪ Existing construction companies in

Qatar include Ashghal and Al Jaber

Engineering

▪ Ease of capturing is high as consortia

must include Qatari JV partner.

However, due to complexity, likely

scenario is for local company to be

JV partner in metro phase 1, with

increased ownership in phase 2

▪ Risk is low as consortia includes

established players

▪ Medium-high strategic value, as

opportunity builds up specialised

knowledge within constructing

bridges and elevated structures,

which can be applied outside of QR

▪ Demand in the region for bridges and

elevated structures is expected to

grow in the near future due to growth

in new developments

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~850mn:

– 2012 to 2020: USD 270mn

– 2020 to 2032: USD 5800mn

▪ Additional revenue from

bridges/elevated structures contracts

in Qatar and in the GCC region

between 2012-2032 is not taken into

account

▪ Consortia will only be allowed to bid

for bridges/elevated structures

contracts if Qatari JV partner is

included

▪ Can be combined with opportunity for

maintenance of bridges and elevated

structures after construction is

complete

▪ Contractor that is overall responsible for

constructing ~100km of bridges/elevated

structures for Qatar Rail, including

– Coordinating the supply of pre-

fabricated elements, rails, and other

components

– Onsite management

– Final assembly/construction

▪ Knowledge and manufacturing capacity is

applicable outside of the rail project,

especially within building construction

▪ Business opportunity focuses on capturing

value from construction phase, with the

potential to apply knowledge in future

bridge/elevated structures projects

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

8

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

Lead contractor services

▪ Initially high capabilities as existing

projects of similar size already carried

out in Qatar. However, JV with

established partner may be needed

on constructions with complex

designs and/or short timelines

▪ Existing suppliers of construction

management services include Al

Jaber, Redco Group, and Construct

International

▪ Risk is medium, as delay of station

construction could postpone the

operations of the rail system

▪ Medium strategic value as

opportunity creates medium-skilled

jobs that can be leveraged on future

constructions (managing

large/complex constructions for Qatar

Rail will build credibility for future

projects)

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~840mn:

– 2012 to 2020: USD 460mn

– 2021 to 2032: USD 380mn

▪ Additional revenue from construction

management services in Qatar and in

the GCC region between 2012-2032

not taken into account

▪ Will potentially work together with

construction site logistics company,

unless lead contractor can provide

service in-house

▪ Management of specific construction sites

of the rail network, including the overall

material flow, safety, and management of

sub-contractors to ensure successful

construction completion

▪ Key success factors are maintaining the

overall schedule, budget, and quality of all

construction elements

▪ Main customers are building and

infrastructure developers, and demand in

the region for construction management

services is expected to grow in the near

future due to growth in new constructions

OPPORTUNITY

FOR EXISTING

BUSINESSES

014: INFRASTRUCTURE PROVISION – CIVIL ENGINEERING

McKinsey & Company |

Doc ID

# 0

3

9

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

Provision of earth work services 015: INFRASTRUCTURE PROVISION – CIVIL ENGINEERING

▪ High feasibility as earth works is

already done in Qatar and there are

low technical requirements

▪ If the required capacity is available,

opportunity could be captured quickly

▪ Lead time is low as earthworks is the

first phase of building construction

▪ Low strategic value as opportunity

does not create high-skilled jobs

▪ Limited potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~970mn:

– 2012 to 2020: USD 570mn

– 2020 to 2032: USD 400mn

▪ Additional revenue from provision of

earth work services in Qatar and in

the GCC region between 2012-2032

is not taken into account

▪ Moved earth will be used to construct

New Doha International Airport

▪ On-site provision of earth work services for

buildings, including

– Coordinating the necessary equipment

and machinery

– Excavating the earth and unformed

rock

– Disposing of excavated the materials

▪ Business opportunity focuses on capturing

value from construction phase, although

service is applicable outside of rail project

in other new constructions

▪ New constructions in the region are

expected to grow in the near future

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

10

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

Construction of deep foundations 016: INFRASTRUCTURE PROVISION – CIVIL ENGINEERING

▪ High feasibility as provision of deep

foundations is already done in Qatar

and there are low technical

requirements

▪ Lead time is low as provision of deep

foundations is in the early stages of

building construction

▪ Some knowledge can be obtained

from partnering with established

multinational, but limited strategic

value as opportunity does not create

high-skilled jobs

▪ Low potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~480mn:

– 2012 to 2020: USD 280mn

– 2020 to 2032: USD 200mn

▪ Additional revenue from provision of

deep foundations for buildings in

Qatar and in the GCC region between

2012-2032 is not taken into account

▪ Potential to integrate with

manufacturing and trucking of

elements for deep foundations

▪ Construction of deep foundations for

buildings, including

– Coordinating the supply of necessary

equipment, machinery, and materials,

– Driving down prefabricated piles into

the ground using a pile driver to

construct the foundation of the

buildings

▪ Business opportunity focuses on capturing

value from construction phase, although

deep foundations are applicable outside of

rail project in other new constructions

▪ New constructions in the region are

expected to grow in the near future

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

11

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

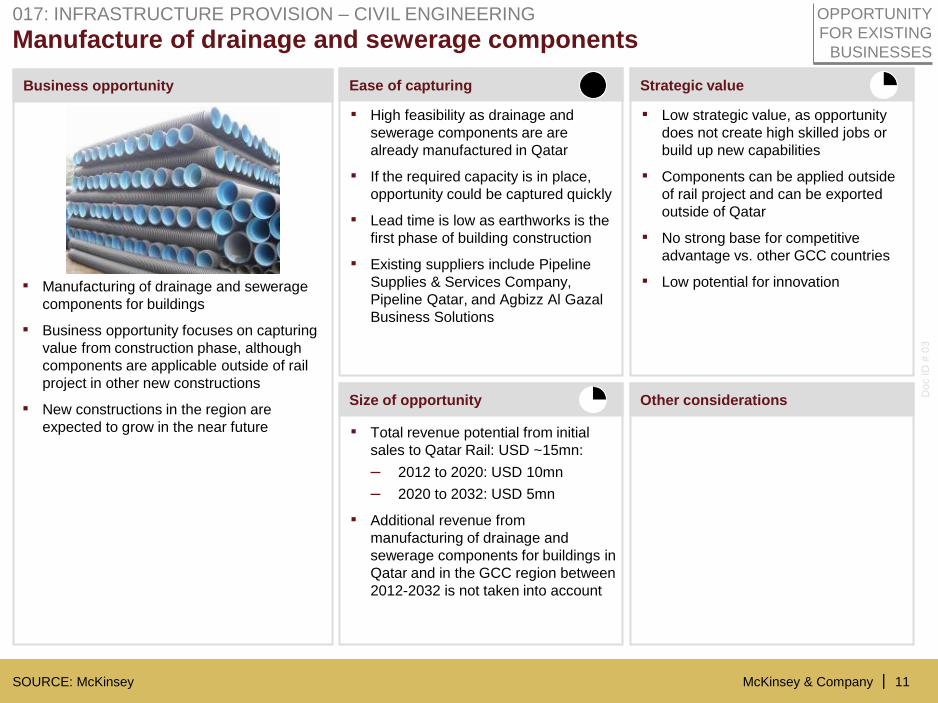

Manufacture of drainage and sewerage components 017: INFRASTRUCTURE PROVISION – CIVIL ENGINEERING

▪ Low strategic value, as opportunity

does not create high skilled jobs or

build up new capabilities

▪ Components can be applied outside

of rail project and can be exported

outside of Qatar

▪ No strong base for competitive

advantage vs. other GCC countries

▪ Low potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~15mn:

– 2012 to 2020: USD 10mn

– 2020 to 2032: USD 5mn

▪ Additional revenue from

manufacturing of drainage and

sewerage components for buildings in

Qatar and in the GCC region between

2012-2032 is not taken into account

▪ Manufacturing of drainage and sewerage

components for buildings

▪ Business opportunity focuses on capturing

value from construction phase, although

components are applicable outside of rail

project in other new constructions

▪ New constructions in the region are

expected to grow in the near future

▪ High feasibility as drainage and

sewerage components are are

already manufactured in Qatar

▪ If the required capacity is in place,

opportunity could be captured quickly

▪ Lead time is low as earthworks is the

first phase of building construction

▪ Existing suppliers include Pipeline

Supplies & Services Company,

Pipeline Qatar, and Agbizz Al Gazal

Business Solutions

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

12

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

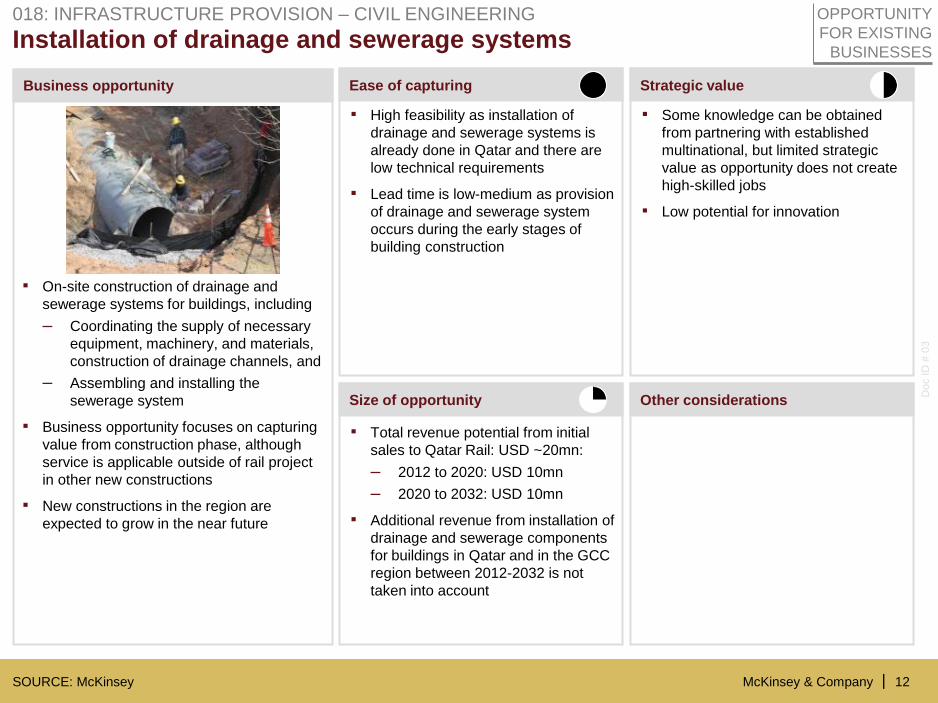

Installation of drainage and sewerage systems 018: INFRASTRUCTURE PROVISION – CIVIL ENGINEERING

▪ High feasibility as installation of

drainage and sewerage systems is

already done in Qatar and there are

low technical requirements

▪ Lead time is low-medium as provision

of drainage and sewerage system

occurs during the early stages of

building construction

▪ Some knowledge can be obtained

from partnering with established

multinational, but limited strategic

value as opportunity does not create

high-skilled jobs

▪ Low potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~20mn:

– 2012 to 2020: USD 10mn

– 2020 to 2032: USD 10mn

▪ Additional revenue from installation of

drainage and sewerage components

for buildings in Qatar and in the GCC

region between 2012-2032 is not

taken into account

▪ On-site construction of drainage and

sewerage systems for buildings, including

– Coordinating the supply of necessary

equipment, machinery, and materials,

construction of drainage channels, and

– Assembling and installing the

sewerage system

▪ Business opportunity focuses on capturing

value from construction phase, although

service is applicable outside of rail project

in other new constructions

▪ New constructions in the region are

expected to grow in the near future

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

13

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

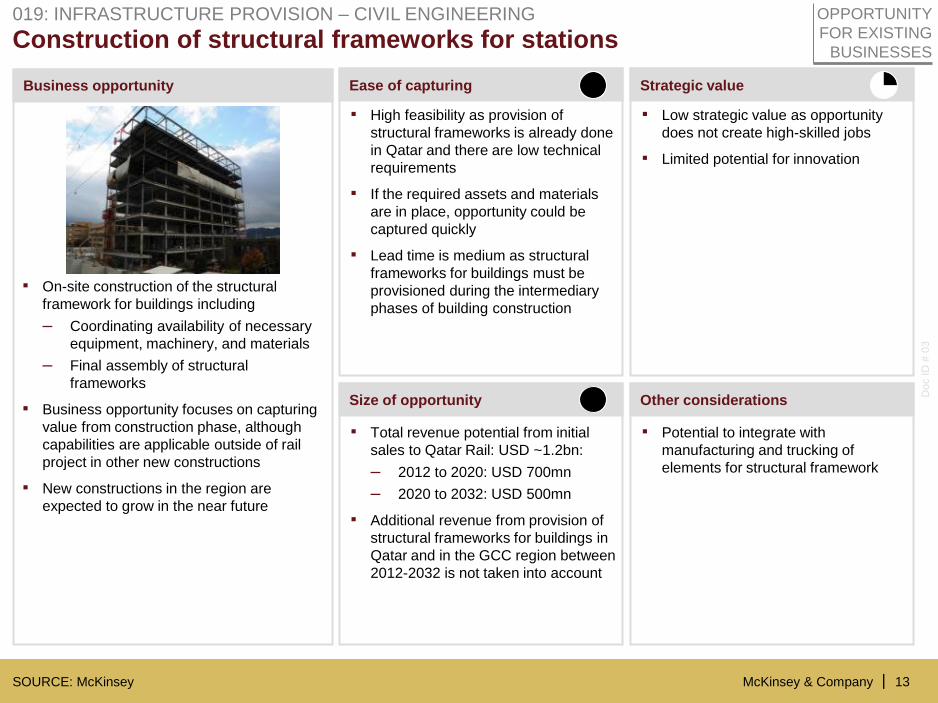

Construction of structural frameworks for stations 019: INFRASTRUCTURE PROVISION – CIVIL ENGINEERING

▪ High feasibility as provision of

structural frameworks is already done

in Qatar and there are low technical

requirements

▪ If the required assets and materials

are in place, opportunity could be

captured quickly

▪ Lead time is medium as structural

frameworks for buildings must be

provisioned during the intermediary

phases of building construction

▪ Low strategic value as opportunity

does not create high-skilled jobs

▪ Limited potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~1.2bn:

– 2012 to 2020: USD 700mn

– 2020 to 2032: USD 500mn

▪ Additional revenue from provision of

structural frameworks for buildings in

Qatar and in the GCC region between

2012-2032 is not taken into account

▪ Potential to integrate with

manufacturing and trucking of

elements for structural framework

▪ On-site construction of the structural

framework for buildings including

– Coordinating availability of necessary

equipment, machinery, and materials

– Final assembly of structural

frameworks

▪ Business opportunity focuses on capturing

value from construction phase, although

capabilities are applicable outside of rail

project in other new constructions

▪ New constructions in the region are

expected to grow in the near future

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

14

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

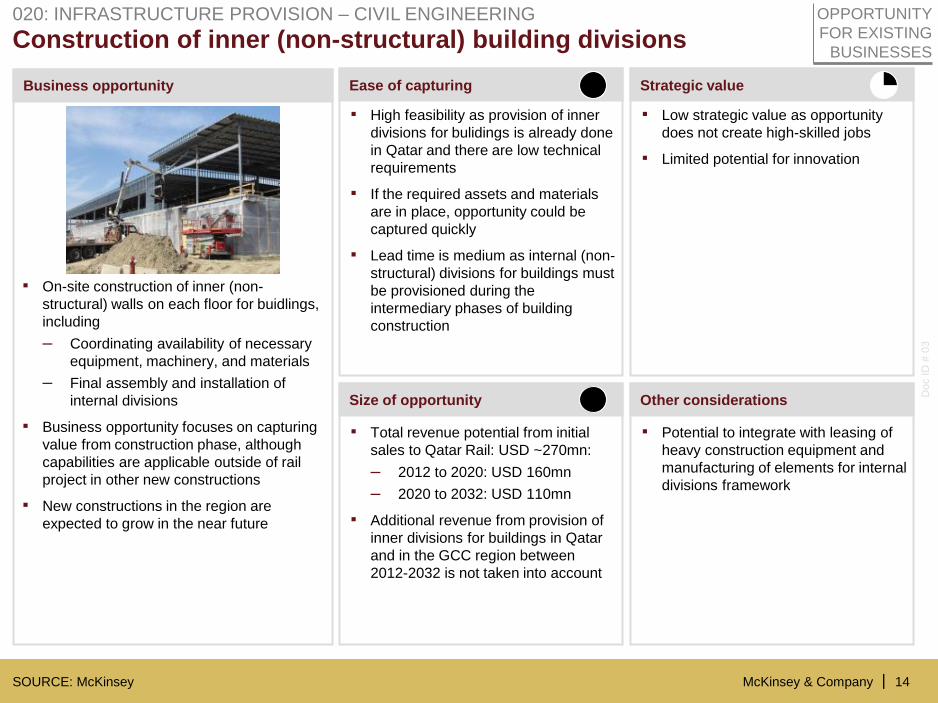

Construction of inner (non-structural) building divisions 020: INFRASTRUCTURE PROVISION – CIVIL ENGINEERING

▪ High feasibility as provision of inner

divisions for bulidings is already done

in Qatar and there are low technical

requirements

▪ If the required assets and materials

are in place, opportunity could be

captured quickly

▪ Lead time is medium as internal (non-

structural) divisions for buildings must

be provisioned during the

intermediary phases of building

construction

▪ Low strategic value as opportunity

does not create high-skilled jobs

▪ Limited potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~270mn:

– 2012 to 2020: USD 160mn

– 2020 to 2032: USD 110mn

▪ Additional revenue from provision of

inner divisions for buildings in Qatar

and in the GCC region between

2012-2032 is not taken into account

▪ Potential to integrate with leasing of

heavy construction equipment and

manufacturing of elements for internal

divisions framework

▪ On-site construction of inner (non-

structural) walls on each floor for buidlings,

including

– Coordinating availability of necessary

equipment, machinery, and materials

– Final assembly and installation of

internal divisions

▪ Business opportunity focuses on capturing

value from construction phase, although

capabilities are applicable outside of rail

project in other new constructions

▪ New constructions in the region are

expected to grow in the near future

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

15

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

Construction of structural frameworks for workshops 021: INFRASTRUCTURE PROVISION – CIVIL ENGINEERING

▪ High feasibility as there are no

special technical requirements

▪ If the required assets and materials

are in place, opportunity could be

captured quickly

▪ Lead time is medium as structural

frameworks for buildings must be

provisioned during the intermediary

phases of building construction

▪ Low strategic value as opportunity

does not create high-skilled jobs

▪ Limited potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~75mn:

– 2012 to 2020: USD 30mn

– 2020 to 2032: USD 45mn

▪ Additional revenue from construction

of workshops for rolling stock

maintenance in Qatar and in the GCC

region between 2012-2032 is not

taken into account

▪ Potential to integrate with leasing of

heavy construction equipment and

manufacturing of elements for

structural framework

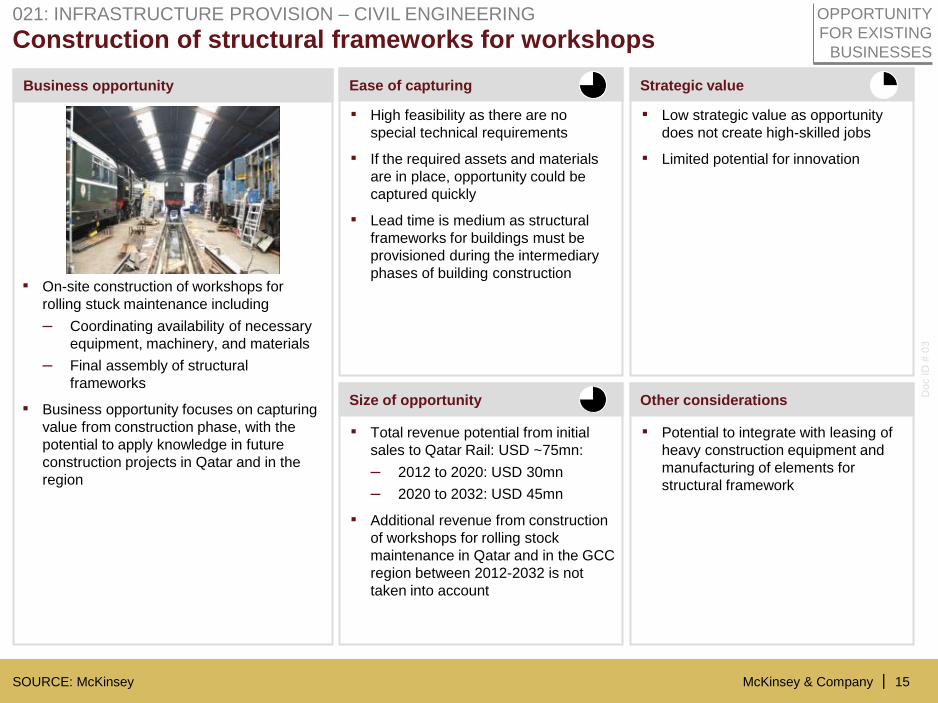

▪ On-site construction of workshops for

rolling stuck maintenance including

– Coordinating availability of necessary

equipment, machinery, and materials

– Final assembly of structural

frameworks

▪ Business opportunity focuses on capturing

value from construction phase, with the

potential to apply knowledge in future

construction projects in Qatar and in the

region

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

16

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

Building inspection services (during construction) 022: INFRASTRUCTURE PROVISION – CIVIL ENGINEERING

▪ High feasibility as service is currently

already provided in Doha

▪ Existing suppliers already existing

Shaheen Engineering, Enermes

Engineering, and Confidence

Engineering

▪ Low strategic value, as opportunity

does not create additional high-skilled

jobs

▪ Applicable outside of rail project in

other new constructions

▪ Low ability to export service outside

of Qatar

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~10mn:

– 2012 to 2020: USD 5mn

– 2020 to 2032: USD 5mn

▪ Additional revenue from provision of

building inspection services in Qatar

and in the GCC region between

2012-2032 is not taken into account

▪ Once construction is complete, there

will be a handover of building

inspection services to station facilities

management company

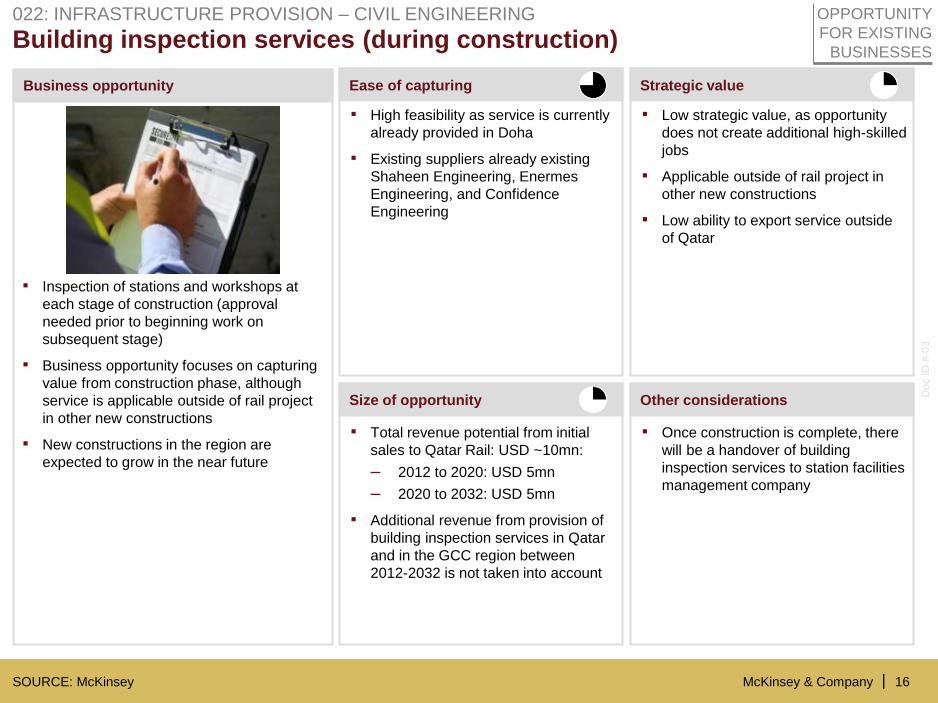

▪ Inspection of stations and workshops at

each stage of construction (approval

needed prior to beginning work on

subsequent stage)

▪ Business opportunity focuses on capturing

value from construction phase, although

service is applicable outside of rail project

in other new constructions

▪ New constructions in the region are

expected to grow in the near future

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

17

Manufacture of pre-fabricated steel grids 024: INFRASTRUCTURE PROVISION – BASIC MATERIALS

▪ Feasible:

– Major input (construction steel)

can be sourced in Qatar – Several smart rebar companies

actually license their software,

including Bamtec from Haussler

Innovation ▪ Initial tests can be run on lower-risk

infrastructure construction, including

stations, platforms

▪ Would require a ramp-up of 9-18

months ▪ Low risk as Qatar rail can fall back on

conventional steel rebar suppliers if

required

▪ Creation of sustainable business in

construction industry with value

added jobs, such as structural

engineers, software engineers

▪ Supports region’s fast-growth

construction sector needs

▪ Potential for steel cluster, including

steel rebar and components

manufacturing

– Opportunity to strengthen/develop

Qatar’s current steel

manufacturing capability

▪ Creates knowledge-based jobs for

expert welders, CAD designers,

quality engineers

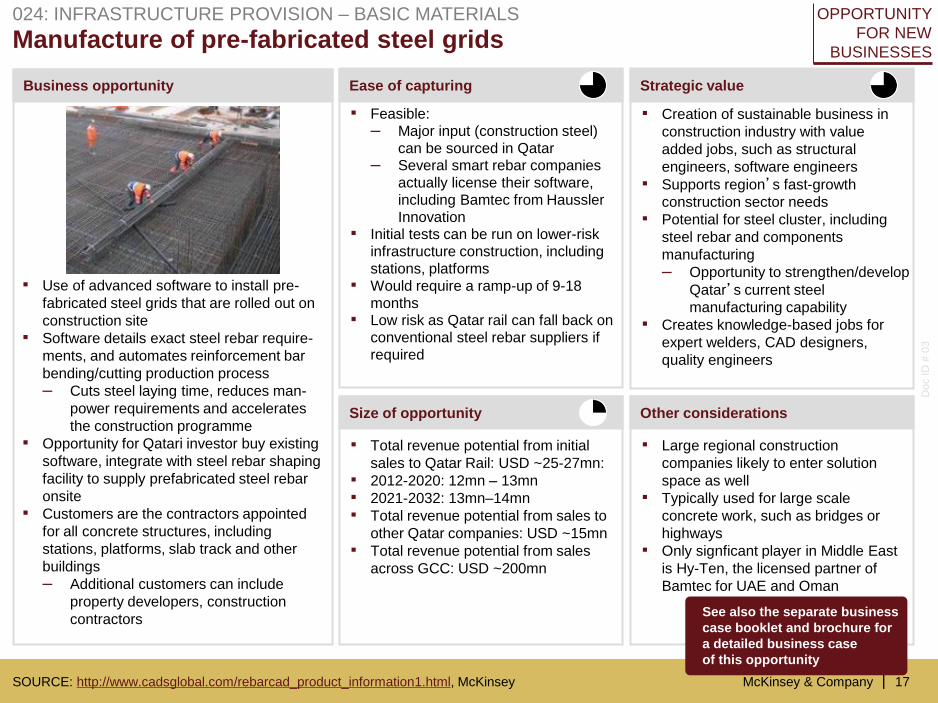

▪ Use of advanced software to install pre-

fabricated steel grids that are rolled out on

construction site

▪ Software details exact steel rebar require-

ments, and automates reinforcement bar

bending/cutting production process

– Cuts steel laying time, reduces man-

power requirements and accelerates

the construction programme

▪ Opportunity for Qatari investor buy existing

software, integrate with steel rebar shaping

facility to supply prefabricated steel rebar

onsite

▪ Customers are the contractors appointed

for all concrete structures, including

stations, platforms, slab track and other

buildings

– Additional customers can include

property developers, construction

contractors

Business opportunity Ease of capturing Strategic value

SOURCE: http://www.cadsglobal.com/rebarcad_product_information1.html, McKinsey

▪ Large regional construction

companies likely to enter solution

space as well

▪ Typically used for large scale

concrete work, such as bridges or

highways

▪ Only signficant player in Middle East

is Hy-Ten, the licensed partner of

Bamtec for UAE and Oman

Size of opportunity Other considerations

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~25-27mn:

▪ 2012-2020: 12mn – 13mn

▪ 2021-2032: 13mn–14mn

▪ Total revenue potential from sales to

other Qatar companies: USD ~15mn

▪ Total revenue potential from sales

across GCC: USD ~200mn

OPPORTUNITY

FOR NEW

BUSINESSES

See also the separate business

case booklet and brochure for

a detailed business case

of this opportunity

McKinsey & Company |

Doc ID

# 0

3

18

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

Maintenance of track infrastructure 025: INFRASTRUCTURE PROVISION – RAIL INFRASTRUCTURE CONSTRUCTION

▪ Medium feasibility initially as

maintaining the rail infrastructure

requires special skills and machinery

which are currently not available in

the country

▪ Potentially entering the market

through JV with established player

(e.g. international construction

company which has a proven

experience in this field) and ramp up

capabilities during first years

▪ Low risk as numerous established

companies can provide service if

required

▪ High strategic value as it is an

ongoing opportunity with highly

skilled jobs

▪ Some potential outside Qatar given

that superstructure has to be

maintained frequently and machinery

can be used across countries, e.g.

grinding, ballast tempering

▪ Potential for innovation is low –

mainly defined by technology built in

at construction phase

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~285mn:

– 2012 to 2020: USD 15mn

– 2021 to 2032: USD 270mn

▪ Additional revenue from Qatar and in

the GCC region between 2012-2032

is not taken into account

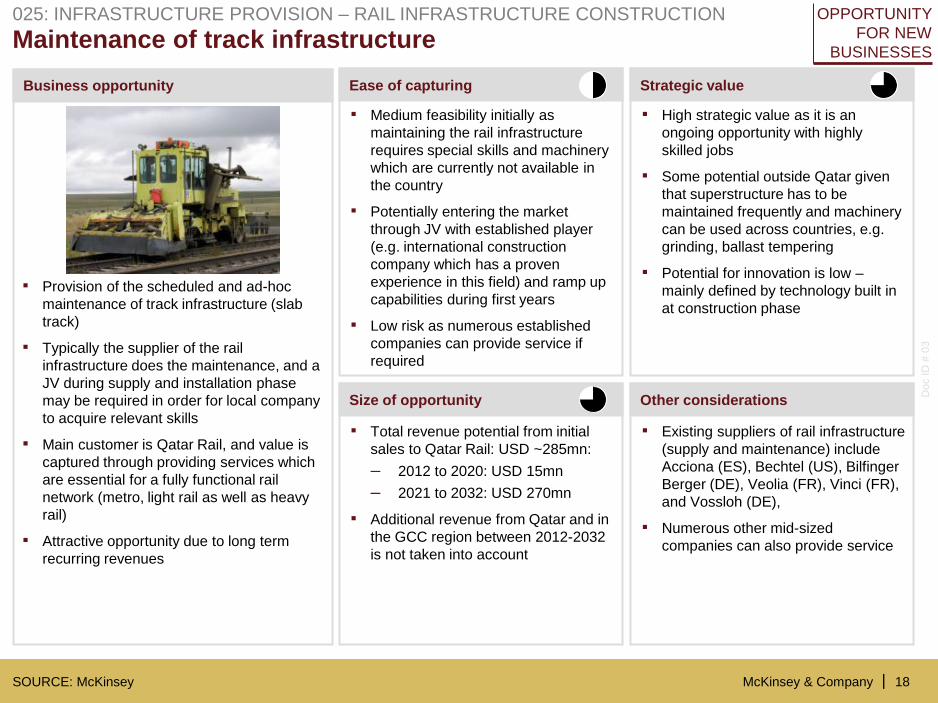

▪ Provision of the scheduled and ad-hoc

maintenance of track infrastructure (slab

track)

▪ Typically the supplier of the rail

infrastructure does the maintenance, and a

JV during supply and installation phase

may be required in order for local company

to acquire relevant skills

▪ Main customer is Qatar Rail, and value is

captured through providing services which

are essential for a fully functional rail

network (metro, light rail as well as heavy

rail)

▪ Attractive opportunity due to long term

recurring revenues

▪ Existing suppliers of rail infrastructure

(supply and maintenance) include

Acciona (ES), Bechtel (US), Bilfinger

Berger (DE), Veolia (FR), Vinci (FR),

and Vossloh (DE),

▪ Numerous other mid-sized

companies can also provide service

OPPORTUNITY

FOR NEW

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

19

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

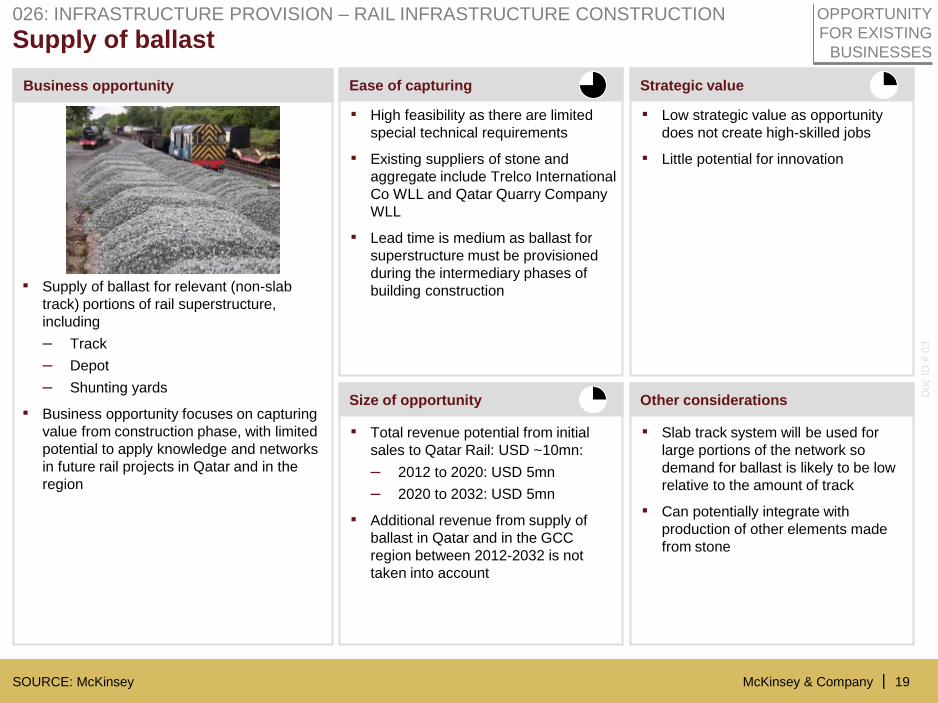

Supply of ballast 026: INFRASTRUCTURE PROVISION – RAIL INFRASTRUCTURE CONSTRUCTION

▪ High feasibility as there are limited

special technical requirements

▪ Existing suppliers of stone and

aggregate include Trelco International

Co WLL and Qatar Quarry Company

WLL

▪ Lead time is medium as ballast for

superstructure must be provisioned

during the intermediary phases of

building construction

▪ Low strategic value as opportunity

does not create high-skilled jobs

▪ Little potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~10mn:

– 2012 to 2020: USD 5mn

– 2020 to 2032: USD 5mn

▪ Additional revenue from supply of

ballast in Qatar and in the GCC

region between 2012-2032 is not

taken into account

▪ Slab track system will be used for

large portions of the network so

demand for ballast is likely to be low

relative to the amount of track

▪ Can potentially integrate with

production of other elements made

from stone

▪ Supply of ballast for relevant (non-slab

track) portions of rail superstructure,

including

– Track

– Depot

– Shunting yards

▪ Business opportunity focuses on capturing

value from construction phase, with limited

potential to apply knowledge and networks

in future rail projects in Qatar and in the

region

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

20

Size of opportunity Other considerations

Business opportunity Ease of capturing Strategic value

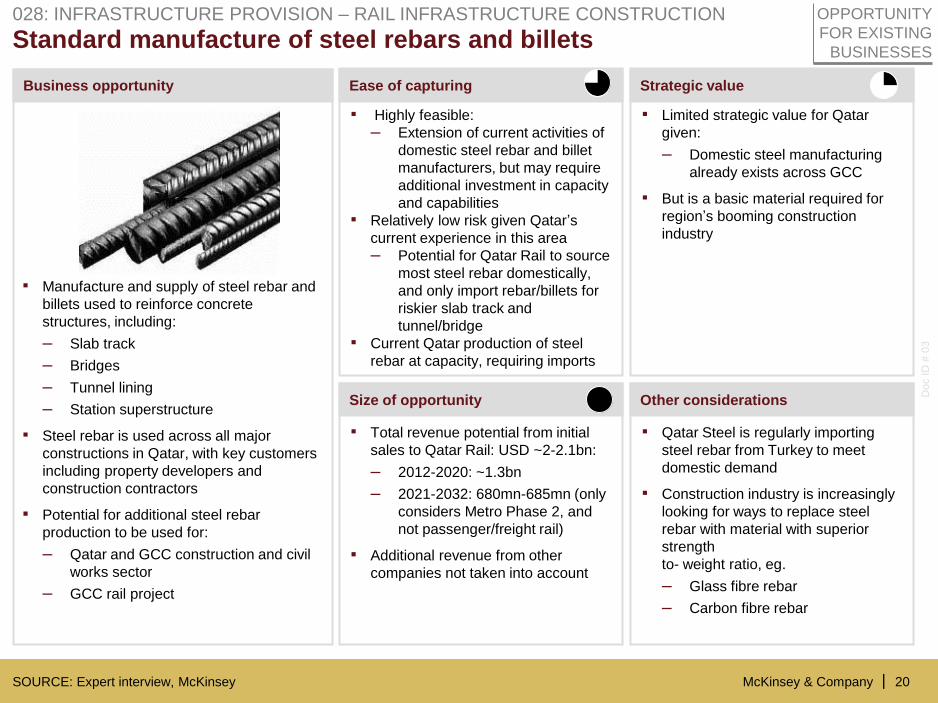

Standard manufacture of steel rebars and billets 028: INFRASTRUCTURE PROVISION – RAIL INFRASTRUCTURE CONSTRUCTION

▪ Highly feasible:

– Extension of current activities of

domestic steel rebar and billet

manufacturers, but may require

additional investment in capacity

and capabilities

▪ Relatively low risk given Qatar’s

current experience in this area

– Potential for Qatar Rail to source

most steel rebar domestically,

and only import rebar/billets for

riskier slab track and

tunnel/bridge

▪ Current Qatar production of steel

rebar at capacity, requiring imports

▪ Limited strategic value for Qatar

given:

– Domestic steel manufacturing

already exists across GCC

▪ But is a basic material required for

region’s booming construction

industry

▪ Manufacture and supply of steel rebar and

billets used to reinforce concrete

structures, including:

– Slab track

– Bridges

– Tunnel lining

– Station superstructure

▪ Steel rebar is used across all major

constructions in Qatar, with key customers

including property developers and

construction contractors

▪ Potential for additional steel rebar

production to be used for:

– Qatar and GCC construction and civil

works sector

– GCC rail project

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~2-2.1bn:

– 2012-2020: ~1.3bn

– 2021-2032: 680mn-685mn (only

considers Metro Phase 2, and

not passenger/freight rail)

▪ Additional revenue from other

companies not taken into account

▪ Qatar Steel is regularly importing

steel rebar from Turkey to meet

domestic demand

▪ Construction industry is increasingly

looking for ways to replace steel

rebar with material with superior

strength

to- weight ratio, eg.

– Glass fibre rebar

– Carbon fibre rebar

SOURCE: Expert interview, McKinsey

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

21

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

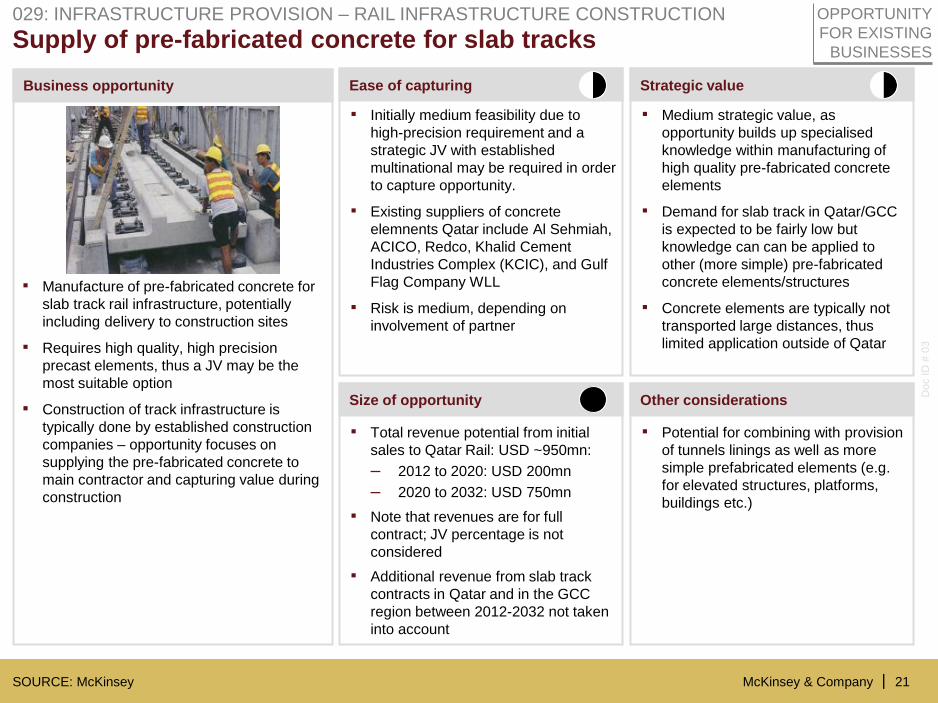

Supply of pre-fabricated concrete for slab tracks

▪ Initially medium feasibility due to

high-precision requirement and a

strategic JV with established

multinational may be required in order

to capture opportunity.

▪ Existing suppliers of concrete

elemnents Qatar include Al Sehmiah,

ACICO, Redco, Khalid Cement

Industries Complex (KCIC), and Gulf

Flag Company WLL

▪ Risk is medium, depending on

involvement of partner

▪ Medium strategic value, as

opportunity builds up specialised

knowledge within manufacturing of

high quality pre-fabricated concrete

elements

▪ Demand for slab track in Qatar/GCC

is expected to be fairly low but

knowledge can can be applied to

other (more simple) pre-fabricated

concrete elements/structures

▪ Concrete elements are typically not

transported large distances, thus

limited application outside of Qatar

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~950mn:

– 2012 to 2020: USD 200mn

– 2020 to 2032: USD 750mn

▪ Note that revenues are for full

contract; JV percentage is not

considered

▪ Additional revenue from slab track

contracts in Qatar and in the GCC

region between 2012-2032 not taken

into account

▪ Potential for combining with provision

of tunnels linings as well as more

simple prefabricated elements (e.g.

for elevated structures, platforms,

buildings etc.)

▪ Manufacture of pre-fabricated concrete for

slab track rail infrastructure, potentially

including delivery to construction sites

▪ Requires high quality, high precision

precast elements, thus a JV may be the

most suitable option

▪ Construction of track infrastructure is

typically done by established construction

companies – opportunity focuses on

supplying the pre-fabricated concrete to

main contractor and capturing value during

construction

OPPORTUNITY

FOR EXISTING

BUSINESSES

029: INFRASTRUCTURE PROVISION – RAIL INFRASTRUCTURE CONSTRUCTION

McKinsey & Company |

Doc ID

# 0

3

22

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

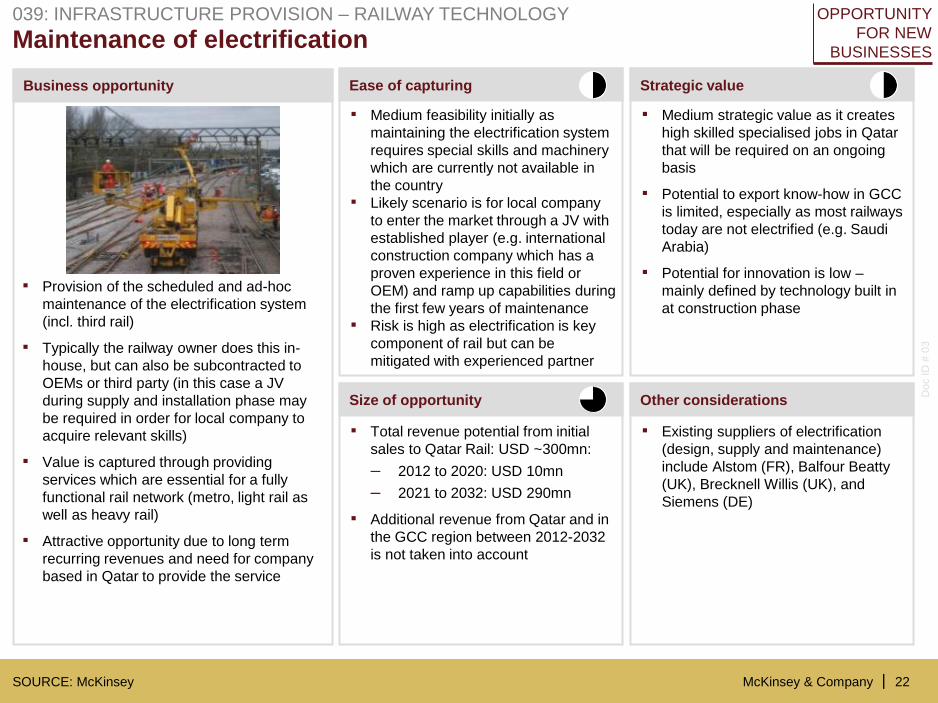

Maintenance of electrification 039: INFRASTRUCTURE PROVISION – RAILWAY TECHNOLOGY

▪ Medium feasibility initially as

maintaining the electrification system

requires special skills and machinery

which are currently not available in

the country

▪ Likely scenario is for local company

to enter the market through a JV with

established player (e.g. international

construction company which has a

proven experience in this field or

OEM) and ramp up capabilities during

the first few years of maintenance

▪ Risk is high as electrification is key

component of rail but can be

mitigated with experienced partner

▪ Medium strategic value as it creates

high skilled specialised jobs in Qatar

that will be required on an ongoing

basis

▪ Potential to export know-how in GCC

is limited, especially as most railways

today are not electrified (e.g. Saudi

Arabia)

▪ Potential for innovation is low –

mainly defined by technology built in

at construction phase

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~300mn:

– 2012 to 2020: USD 10mn

– 2021 to 2032: USD 290mn

▪ Additional revenue from Qatar and in

the GCC region between 2012-2032

is not taken into account

▪ Existing suppliers of electrification

(design, supply and maintenance)

include Alstom (FR), Balfour Beatty

(UK), Brecknell Willis (UK), and

Siemens (DE)

▪ Provision of the scheduled and ad-hoc

maintenance of the electrification system

(incl. third rail)

▪ Typically the railway owner does this in-

house, but can also be subcontracted to

OEMs or third party (in this case a JV

during supply and installation phase may

be required in order for local company to

acquire relevant skills)

▪ Value is captured through providing

services which are essential for a fully

functional rail network (metro, light rail as

well as heavy rail)

▪ Attractive opportunity due to long term

recurring revenues and need for company

based in Qatar to provide the service

OPPORTUNITY

FOR NEW

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

23

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

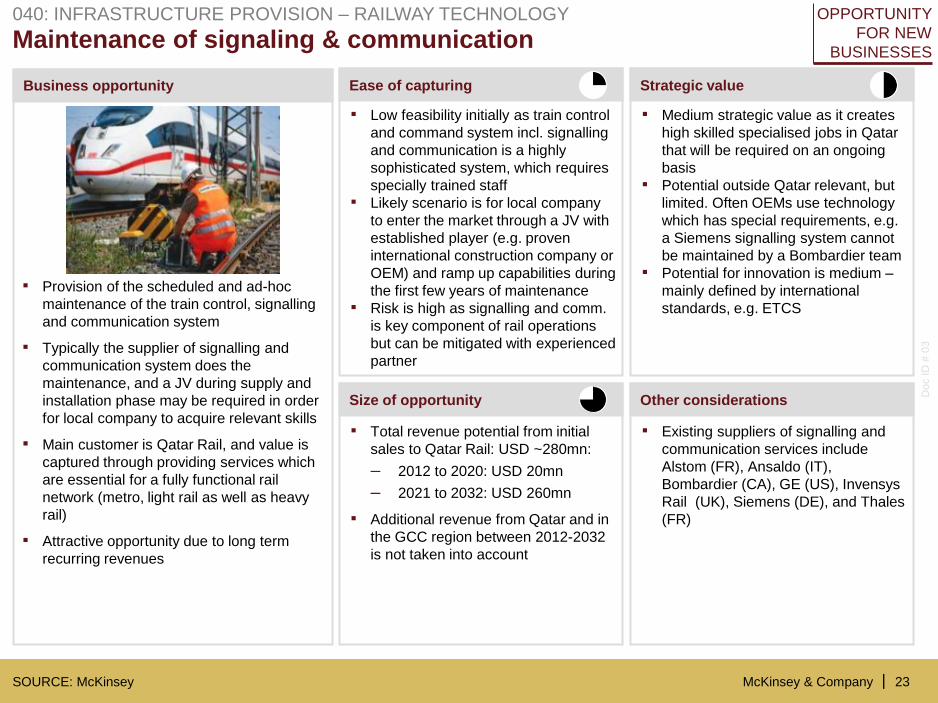

Maintenance of signaling & communication 040: INFRASTRUCTURE PROVISION – RAILWAY TECHNOLOGY

▪ Low feasibility initially as train control

and command system incl. signalling

and communication is a highly

sophisticated system, which requires

specially trained staff

▪ Likely scenario is for local company

to enter the market through a JV with

established player (e.g. proven

international construction company or

OEM) and ramp up capabilities during

the first few years of maintenance

▪ Risk is high as signalling and comm.

is key component of rail operations

but can be mitigated with experienced

partner

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~280mn:

– 2012 to 2020: USD 20mn

– 2021 to 2032: USD 260mn

▪ Additional revenue from Qatar and in

the GCC region between 2012-2032

is not taken into account

▪ Existing suppliers of signalling and

communication services include

Alstom (FR), Ansaldo (IT),

Bombardier (CA), GE (US), Invensys

Rail (UK), Siemens (DE), and Thales

(FR)

▪ Medium strategic value as it creates

high skilled specialised jobs in Qatar

that will be required on an ongoing

basis

▪ Potential outside Qatar relevant, but

limited. Often OEMs use technology

which has special requirements, e.g.

a Siemens signalling system cannot

be maintained by a Bombardier team

▪ Potential for innovation is medium –

mainly defined by international

standards, e.g. ETCS

▪ Provision of the scheduled and ad-hoc

maintenance of the train control, signalling

and communication system

▪ Typically the supplier of signalling and

communication system does the

maintenance, and a JV during supply and

installation phase may be required in order

for local company to acquire relevant skills

▪ Main customer is Qatar Rail, and value is

captured through providing services which

are essential for a fully functional rail

network (metro, light rail as well as heavy

rail)

▪ Attractive opportunity due to long term

recurring revenues

OPPORTUNITY

FOR NEW

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

24

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

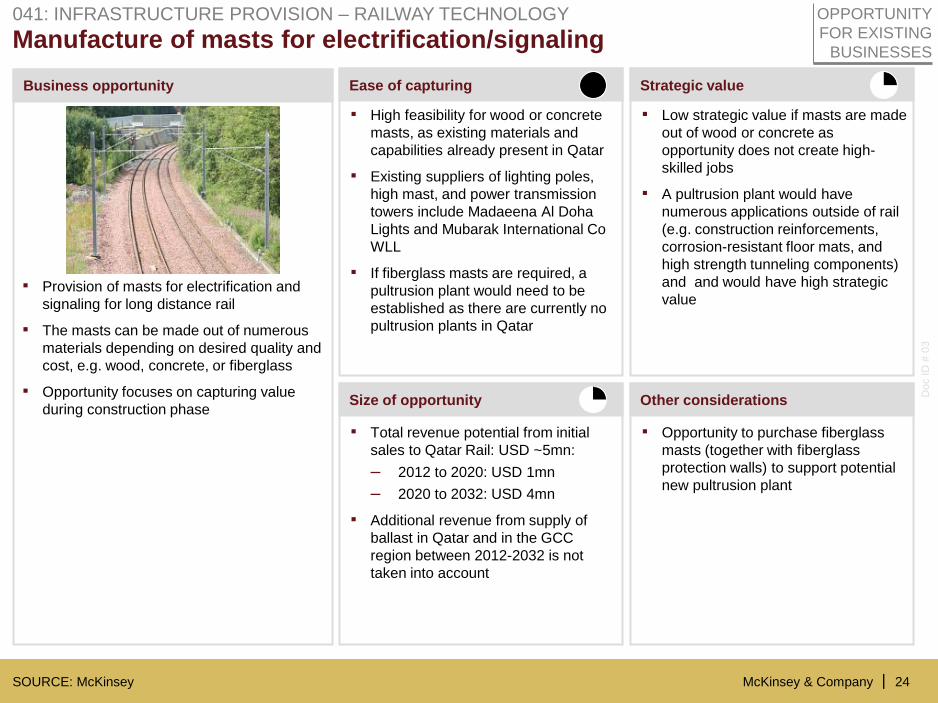

Manufacture of masts for electrification/signaling 041: INFRASTRUCTURE PROVISION – RAILWAY TECHNOLOGY

▪ High feasibility for wood or concrete

masts, as existing materials and

capabilities already present in Qatar

▪ Existing suppliers of lighting poles,

high mast, and power transmission

towers include Madaeena Al Doha

Lights and Mubarak International Co

WLL

▪ If fiberglass masts are required, a

pultrusion plant would need to be

established as there are currently no

pultrusion plants in Qatar

▪ Low strategic value if masts are made

out of wood or concrete as

opportunity does not create high-

skilled jobs

▪ A pultrusion plant would have

numerous applications outside of rail

(e.g. construction reinforcements,

corrosion-resistant floor mats, and

high strength tunneling components)

and and would have high strategic

value

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~5mn:

– 2012 to 2020: USD 1mn

– 2020 to 2032: USD 4mn

▪ Additional revenue from supply of

ballast in Qatar and in the GCC

region between 2012-2032 is not

taken into account

▪ Provision of masts for electrification and

signaling for long distance rail

▪ The masts can be made out of numerous

materials depending on desired quality and

cost, e.g. wood, concrete, or fiberglass

▪ Opportunity focuses on capturing value

during construction phase

▪ Opportunity to purchase fiberglass

masts (together with fiberglass

protection walls) to support potential

new pultrusion plant

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

25

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

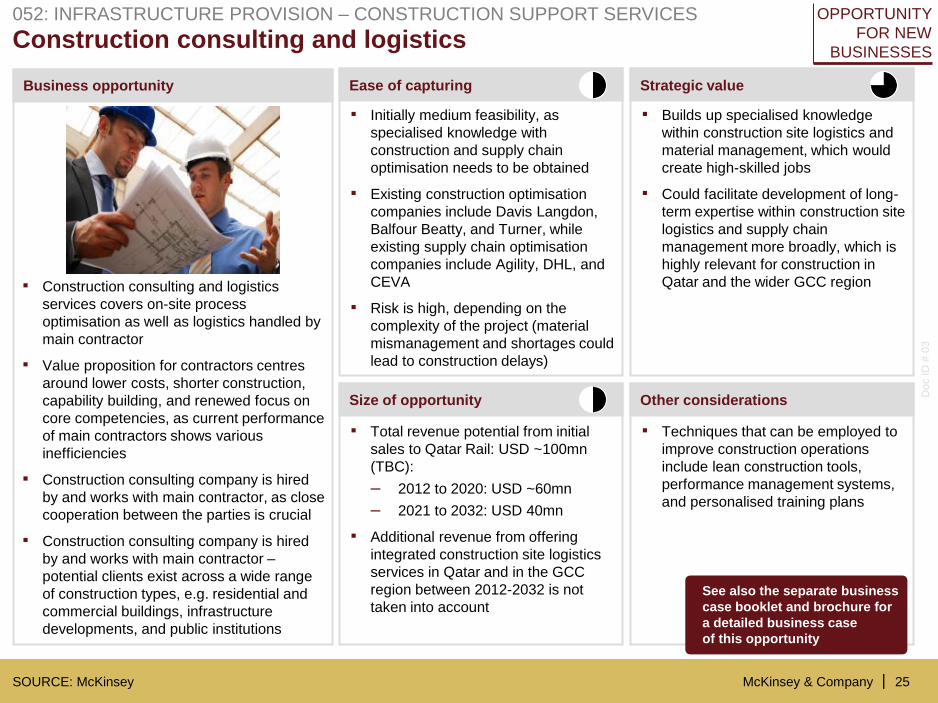

Construction consulting and logistics 052: INFRASTRUCTURE PROVISION – CONSTRUCTION SUPPORT SERVICES

▪ Initially medium feasibility, as

specialised knowledge with

construction and supply chain

optimisation needs to be obtained

▪ Existing construction optimisation

companies include Davis Langdon,

Balfour Beatty, and Turner, while

existing supply chain optimisation

companies include Agility, DHL, and

CEVA

▪ Risk is high, depending on the

complexity of the project (material

mismanagement and shortages could

lead to construction delays)

▪ Builds up specialised knowledge

within construction site logistics and

material management, which would

create high-skilled jobs

▪ Could facilitate development of long-

term expertise within construction site

logistics and supply chain

management more broadly, which is

highly relevant for construction in

Qatar and the wider GCC region

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~100mn

(TBC):

– 2012 to 2020: USD ~60mn

– 2021 to 2032: USD 40mn

▪ Additional revenue from offering

integrated construction site logistics

services in Qatar and in the GCC

region between 2012-2032 is not

taken into account

▪ Techniques that can be employed to

improve construction operations

include lean construction tools,

performance management systems,

and personalised training plans

▪ Construction consulting and logistics

services covers on-site process

optimisation as well as logistics handled by

main contractor

▪ Value proposition for contractors centres

around lower costs, shorter construction,

capability building, and renewed focus on

core competencies, as current performance

of main contractors shows various

inefficiencies

▪ Construction consulting company is hired

by and works with main contractor, as close

cooperation between the parties is crucial

▪ Construction consulting company is hired

by and works with main contractor –

potential clients exist across a wide range

of construction types, e.g. residential and

commercial buildings, infrastructure

developments, and public institutions

OPPORTUNITY

FOR NEW

BUSINESSES

See also the separate business

case booklet and brochure for

a detailed business case

of this opportunity

McKinsey & Company |

Doc ID

# 0

3

26

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey, Qatcom.com, ameinfo, Barwa

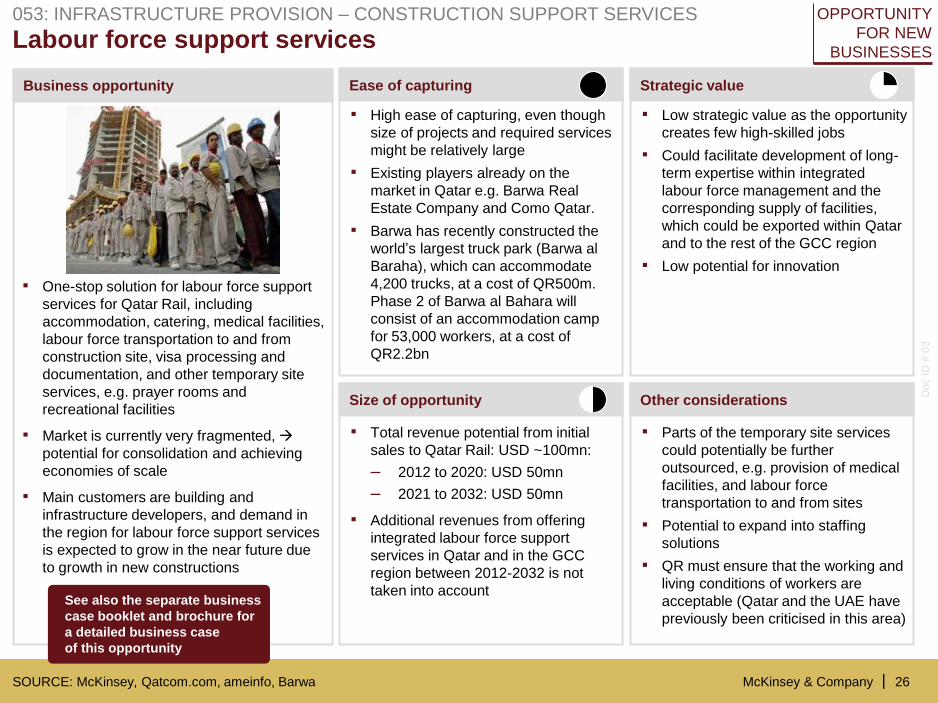

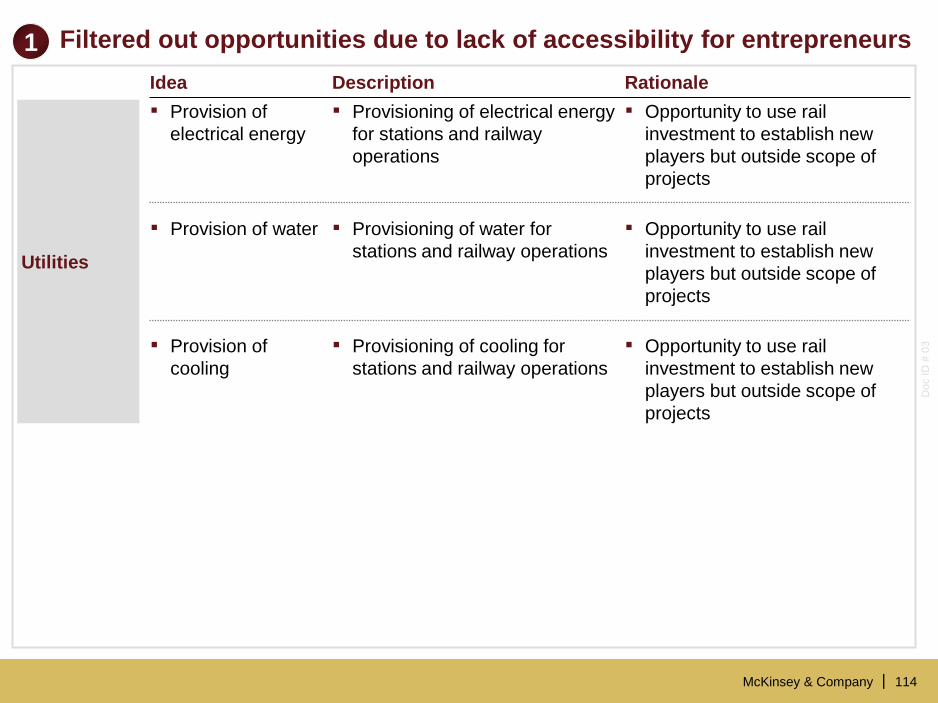

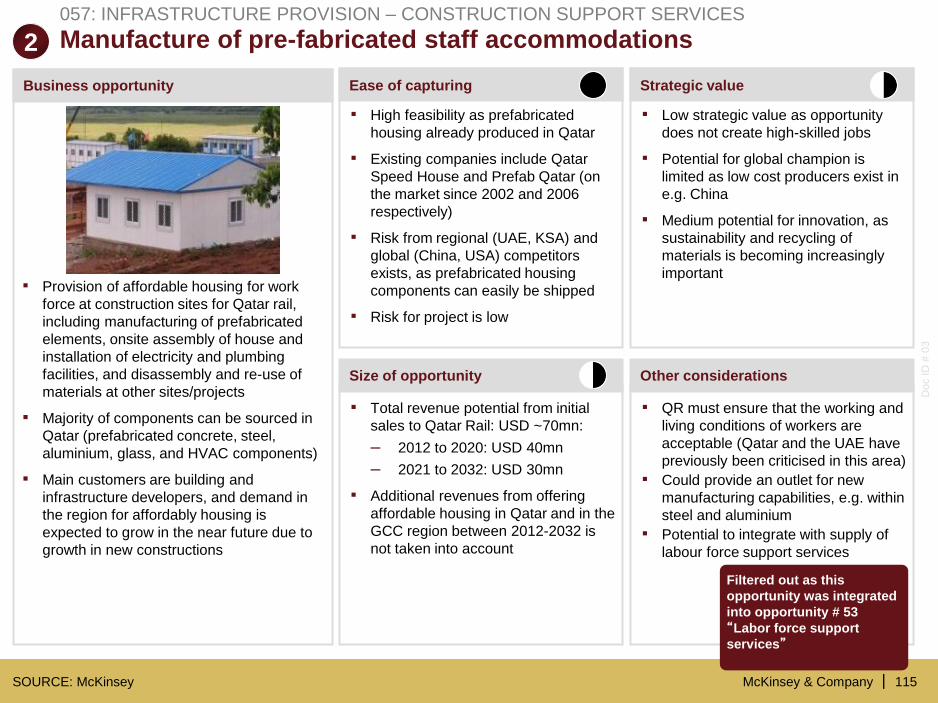

Labour force support services 053: INFRASTRUCTURE PROVISION – CONSTRUCTION SUPPORT SERVICES

▪ High ease of capturing, even though

size of projects and required services

might be relatively large

▪ Existing players already on the

market in Qatar e.g. Barwa Real

Estate Company and Como Qatar.

▪ Barwa has recently constructed the

world’s largest truck park (Barwa al

Baraha), which can accommodate

4,200 trucks, at a cost of QR500m.

Phase 2 of Barwa al Bahara will

consist of an accommodation camp

for 53,000 workers, at a cost of

QR2.2bn

▪ Low strategic value as the opportunity

creates few high-skilled jobs

▪ Could facilitate development of long-

term expertise within integrated

labour force management and the

corresponding supply of facilities,

which could be exported within Qatar

and to the rest of the GCC region

▪ Low potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~100mn:

– 2012 to 2020: USD 50mn

– 2021 to 2032: USD 50mn

▪ Additional revenues from offering

integrated labour force support

services in Qatar and in the GCC

region between 2012-2032 is not

taken into account

▪ Parts of the temporary site services

could potentially be further

outsourced, e.g. provision of medical

facilities, and labour force

transportation to and from sites

▪ Potential to expand into staffing

solutions

▪ QR must ensure that the working and

living conditions of workers are

acceptable (Qatar and the UAE have

previously been criticised in this area)

▪ One-stop solution for labour force support

services for Qatar Rail, including

accommodation, catering, medical facilities,

labour force transportation to and from

construction site, visa processing and

documentation, and other temporary site

services, e.g. prayer rooms and

recreational facilities

▪ Market is currently very fragmented,

potential for consolidation and achieving

economies of scale

▪ Main customers are building and

infrastructure developers, and demand in

the region for labour force support services

is expected to grow in the near future due

to growth in new constructions

OPPORTUNITY

FOR NEW

BUSINESSES

See also the separate business

case booklet and brochure for

a detailed business case

of this opportunity

McKinsey & Company |

Doc ID

# 0

3

27

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

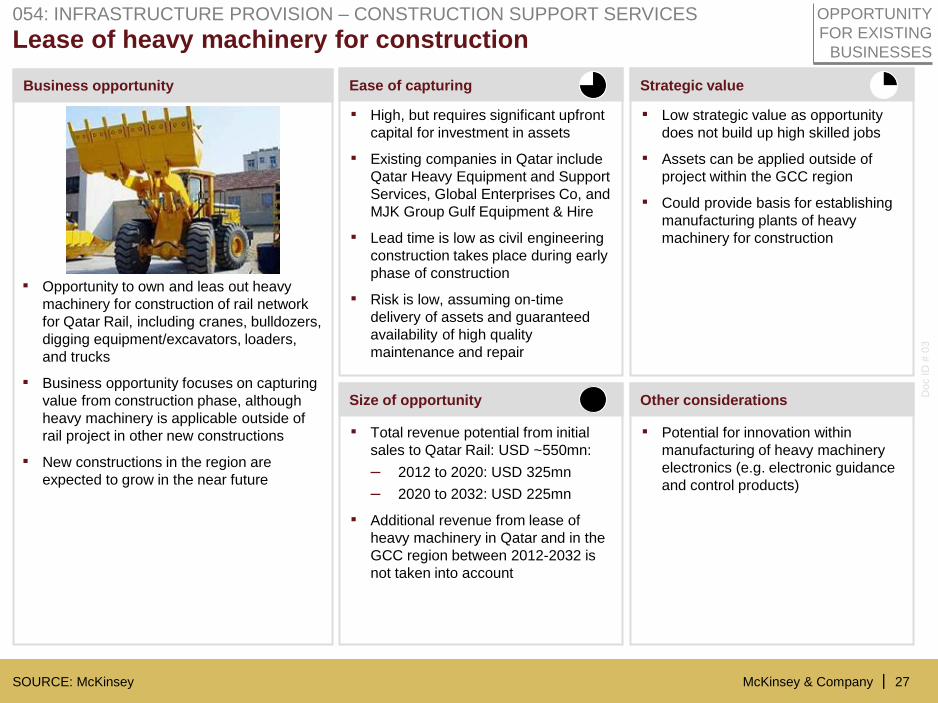

Lease of heavy machinery for construction 054: INFRASTRUCTURE PROVISION – CONSTRUCTION SUPPORT SERVICES

▪ High, but requires significant upfront

capital for investment in assets

▪ Existing companies in Qatar include

Qatar Heavy Equipment and Support

Services, Global Enterprises Co, and

MJK Group Gulf Equipment & Hire

▪ Lead time is low as civil engineering

construction takes place during early

phase of construction

▪ Risk is low, assuming on-time

delivery of assets and guaranteed

availability of high quality

maintenance and repair

▪ Low strategic value as opportunity

does not build up high skilled jobs

▪ Assets can be applied outside of

project within the GCC region

▪ Could provide basis for establishing

manufacturing plants of heavy

machinery for construction

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~550mn:

– 2012 to 2020: USD 325mn

– 2020 to 2032: USD 225mn

▪ Additional revenue from lease of

heavy machinery in Qatar and in the

GCC region between 2012-2032 is

not taken into account

▪ Potential for innovation within

manufacturing of heavy machinery

electronics (e.g. electronic guidance

and control products)

▪ Opportunity to own and leas out heavy

machinery for construction of rail network

for Qatar Rail, including cranes, bulldozers,

digging equipment/excavators, loaders,

and trucks

▪ Business opportunity focuses on capturing

value from construction phase, although

heavy machinery is applicable outside of

rail project in other new constructions

▪ New constructions in the region are

expected to grow in the near future

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

28

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

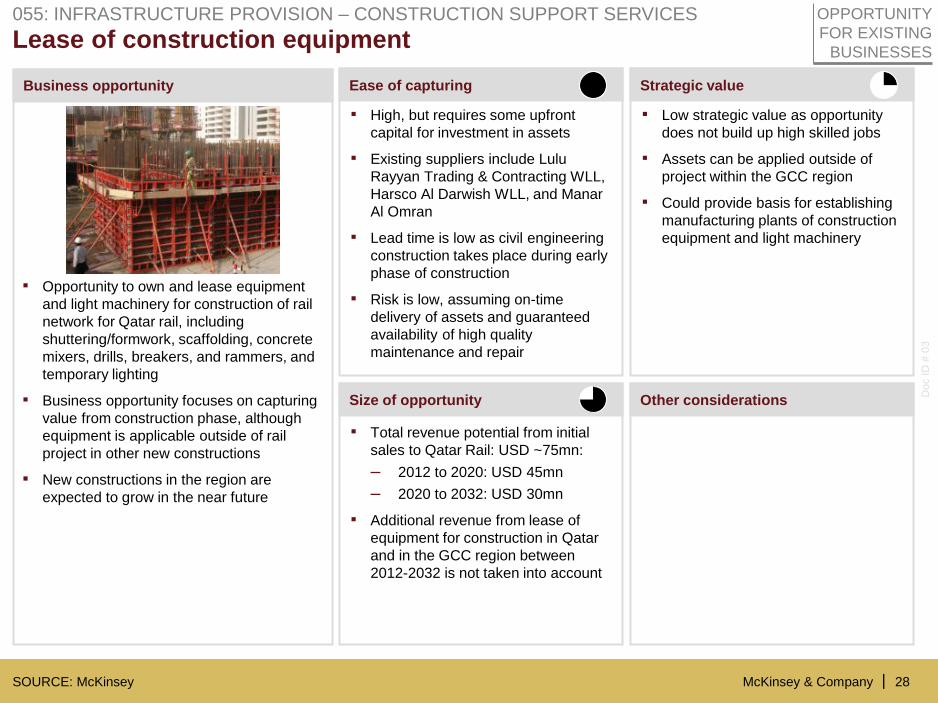

Lease of construction equipment 055: INFRASTRUCTURE PROVISION – CONSTRUCTION SUPPORT SERVICES

▪ High, but requires some upfront

capital for investment in assets

▪ Existing suppliers include Lulu

Rayyan Trading & Contracting WLL,

Harsco Al Darwish WLL, and Manar

Al Omran

▪ Lead time is low as civil engineering

construction takes place during early

phase of construction

▪ Risk is low, assuming on-time

delivery of assets and guaranteed

availability of high quality

maintenance and repair

▪ Low strategic value as opportunity

does not build up high skilled jobs

▪ Assets can be applied outside of

project within the GCC region

▪ Could provide basis for establishing

manufacturing plants of construction

equipment and light machinery

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~75mn:

– 2012 to 2020: USD 45mn

– 2020 to 2032: USD 30mn

▪ Additional revenue from lease of

equipment for construction in Qatar

and in the GCC region between

2012-2032 is not taken into account

▪ Opportunity to own and lease equipment

and light machinery for construction of rail

network for Qatar rail, including

shuttering/formwork, scaffolding, concrete

mixers, drills, breakers, and rammers, and

temporary lighting

▪ Business opportunity focuses on capturing

value from construction phase, although

equipment is applicable outside of rail

project in other new constructions

▪ New constructions in the region are

expected to grow in the near future

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

29

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

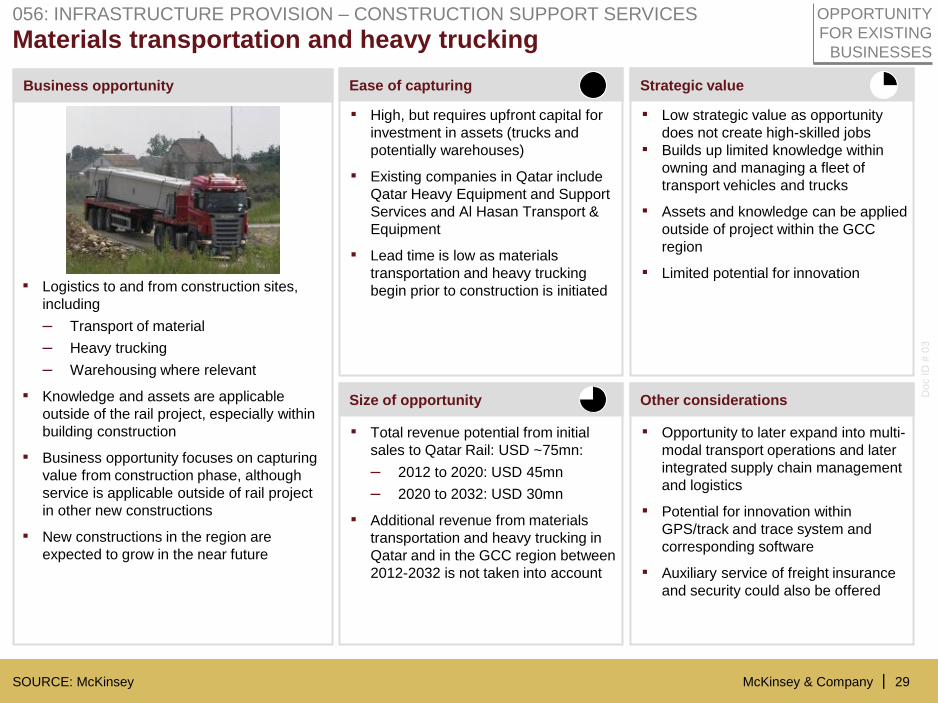

Materials transportation and heavy trucking 056: INFRASTRUCTURE PROVISION – CONSTRUCTION SUPPORT SERVICES

▪ High, but requires upfront capital for

investment in assets (trucks and

potentially warehouses)

▪ Existing companies in Qatar include

Qatar Heavy Equipment and Support

Services and Al Hasan Transport &

Equipment

▪ Lead time is low as materials

transportation and heavy trucking

begin prior to construction is initiated

▪ Low strategic value as opportunity

does not create high-skilled jobs

▪ Builds up limited knowledge within

owning and managing a fleet of

transport vehicles and trucks

▪ Assets and knowledge can be applied

outside of project within the GCC

region

▪ Limited potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~75mn:

– 2012 to 2020: USD 45mn

– 2020 to 2032: USD 30mn

▪ Additional revenue from materials

transportation and heavy trucking in

Qatar and in the GCC region between

2012-2032 is not taken into account

▪ Opportunity to later expand into multi-

modal transport operations and later

integrated supply chain management

and logistics

▪ Potential for innovation within

GPS/track and trace system and

corresponding software

▪ Auxiliary service of freight insurance

and security could also be offered

▪ Logistics to and from construction sites,

including

– Transport of material

– Heavy trucking

– Warehousing where relevant

▪ Knowledge and assets are applicable

outside of the rail project, especially within

building construction

▪ Business opportunity focuses on capturing

value from construction phase, although

service is applicable outside of rail project

in other new constructions

▪ New constructions in the region are

expected to grow in the near future

OPPORTUNITY

FOR EXISTING

BUSINESSES

McKinsey & Company |

Doc ID

# 0

3

30

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

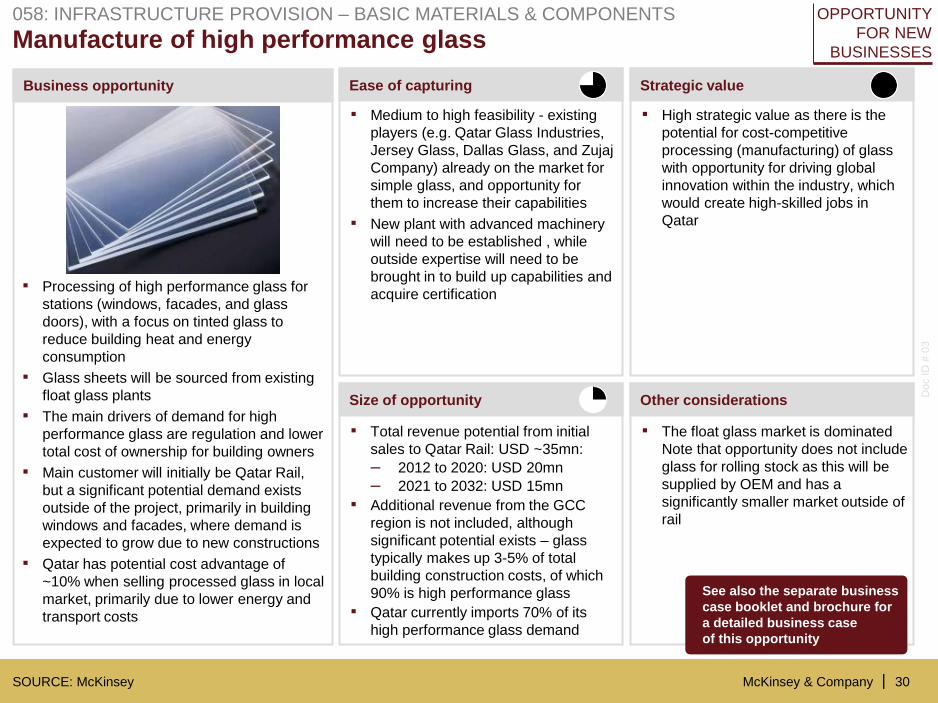

Manufacture of high performance glass 058: INFRASTRUCTURE PROVISION – BASIC MATERIALS & COMPONENTS

▪ Processing of high performance glass for

stations (windows, facades, and glass

doors), with a focus on tinted glass to

reduce building heat and energy

consumption

▪ Glass sheets will be sourced from existing

float glass plants

▪ The main drivers of demand for high

performance glass are regulation and lower

total cost of ownership for building owners

▪ Main customer will initially be Qatar Rail,

but a significant potential demand exists

outside of the project, primarily in building

windows and facades, where demand is

expected to grow due to new constructions

▪ Qatar has potential cost advantage of

~10% when selling processed glass in local

market, primarily due to lower energy and

transport costs

▪ Medium to high feasibility - existing

players (e.g. Qatar Glass Industries,

Jersey Glass, Dallas Glass, and Zujaj

Company) already on the market for

simple glass, and opportunity for

them to increase their capabilities

▪ New plant with advanced machinery

will need to be established , while

outside expertise will need to be

brought in to build up capabilities and

acquire certification

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~35mn:

– 2012 to 2020: USD 20mn

– 2021 to 2032: USD 15mn

▪ Additional revenue from the GCC

region is not included, although

significant potential exists – glass

typically makes up 3-5% of total

building construction costs, of which

90% is high performance glass

▪ Qatar currently imports 70% of its

high performance glass demand

▪ The float glass market is dominated

Note that opportunity does not include

glass for rolling stock as this will be

supplied by OEM and has a

significantly smaller market outside of

rail

▪ High strategic value as there is the

potential for cost-competitive

processing (manufacturing) of glass

with opportunity for driving global

innovation within the industry, which

would create high-skilled jobs in

Qatar

OPPORTUNITY

FOR NEW

BUSINESSES

See also the separate business

case booklet and brochure for

a detailed business case

of this opportunity

McKinsey & Company |

Doc ID

# 0

3

31

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

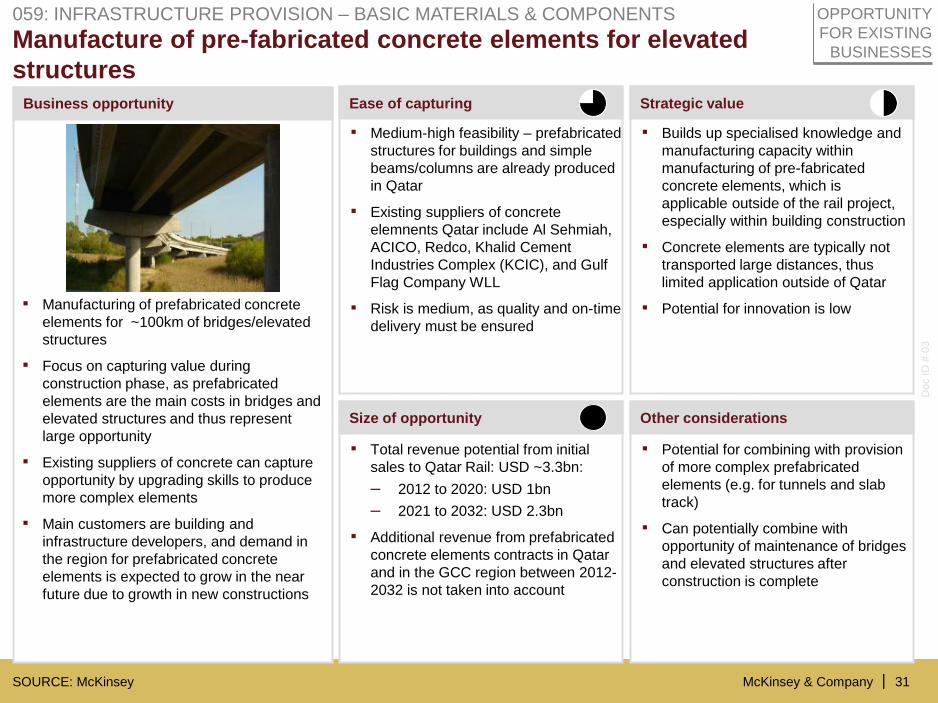

Manufacture of pre-fabricated concrete elements for elevated

structures

▪ Builds up specialised knowledge and

manufacturing capacity within

manufacturing of pre-fabricated

concrete elements, which is

applicable outside of the rail project,

especially within building construction

▪ Concrete elements are typically not

transported large distances, thus

limited application outside of Qatar

▪ Potential for innovation is low

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~3.3bn:

– 2012 to 2020: USD 1bn

– 2021 to 2032: USD 2.3bn

▪ Additional revenue from prefabricated

concrete elements contracts in Qatar

and in the GCC region between 2012-

2032 is not taken into account

▪ Potential for combining with provision

of more complex prefabricated

elements (e.g. for tunnels and slab

track)

▪ Can potentially combine with

opportunity of maintenance of bridges

and elevated structures after

construction is complete

▪ Manufacturing of prefabricated concrete

elements for ~100km of bridges/elevated

structures

▪ Focus on capturing value during

construction phase, as prefabricated

elements are the main costs in bridges and

elevated structures and thus represent

large opportunity

▪ Existing suppliers of concrete can capture

opportunity by upgrading skills to produce

more complex elements

▪ Main customers are building and

infrastructure developers, and demand in

the region for prefabricated concrete

elements is expected to grow in the near

future due to growth in new constructions

▪ Medium-high feasibility – prefabricated

structures for buildings and simple

beams/columns are already produced

in Qatar

▪ Existing suppliers of concrete

elemnents Qatar include Al Sehmiah,

ACICO, Redco, Khalid Cement

Industries Complex (KCIC), and Gulf

Flag Company WLL

▪ Risk is medium, as quality and on-time

delivery must be ensured

OPPORTUNITY

FOR EXISTING

BUSINESSES

059: INFRASTRUCTURE PROVISION – BASIC MATERIALS & COMPONENTS

McKinsey & Company |

Doc ID

# 0

3

32

Business opportunity Ease of capturing Strategic value

Size of opportunity Other considerations

SOURCE: McKinsey

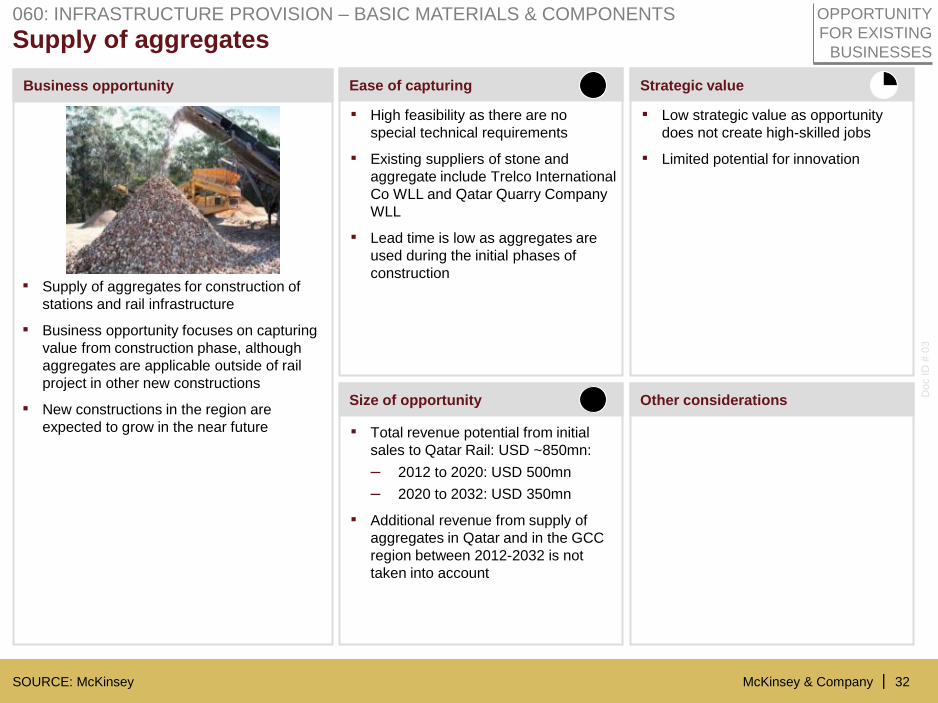

Supply of aggregates 060: INFRASTRUCTURE PROVISION – BASIC MATERIALS & COMPONENTS

▪ High feasibility as there are no

special technical requirements

▪ Existing suppliers of stone and

aggregate include Trelco International

Co WLL and Qatar Quarry Company

WLL

▪ Lead time is low as aggregates are

used during the initial phases of

construction

▪ Low strategic value as opportunity

does not create high-skilled jobs

▪ Limited potential for innovation

▪ Total revenue potential from initial

sales to Qatar Rail: USD ~850mn:

– 2012 to 2020: USD 500mn

– 2020 to 2032: USD 350mn

▪ Additional revenue from supply of

aggregates in Qatar and in the GCC

region between 2012-2032 is not

taken into account