Embed Size (px)

Citation preview

ICICI Securities Ltd. | Retail Equity Research

May 22, 2015

Monthly Update

Q4 numbers mixed; M&A hots up… The Q4 numbers declared by some companies under I-direct coverage have portrayed a mixed picture. Ajanta and Cadila continued to provide strong growth traction on expected lines whereas Biocon and Jubilant delivered better-than-expected numbers. Despite currency depreciation in emerging markets and lack of products approvals in the US, Dr Reddy’ managed to register double digit revenue growth (~11% YoY). On the other hand, Lupin and Torrent’s results were impacted by the high base of gCymbalta last year. Unichem continued to deliver a dismal set of numbers. M&A activities intensified during the month with Torrent Pharma acquiring Encore Group’s dermatology arm Zyg Pharma, which owns a USFDA approved plant in Pithampur (Indore), to foray into the US dermatology space. Similarly, Lupin made its maiden entry in the Brazilian market with an acquisition of Brazilian drug firm Medquimica. Strides will be re-entering the Australian market by agreeing with South African major Aspen to acquire the latter’s generic/branded generic portfolio in Australia and Singapore. On the legal front, the Supreme Court has restrained Glenmark from the manufacture and sale of Merck’s anti-diabetes drugs Januvia and Janumet for infringement of patent. In another development, US based retailer Meijer Inc has filed a case against Ranbaxy in the US district court for allegedly manipulating USFDA rules to keep generic drugs of other companies out of the marketplace. In other significant developments, Daiichi Sankyo finally exited Ranbaxy by offloading its entire 8.93% stake (21.4 crore shares) in Sun Pharmaceuticals for ~ | 20430 crore in the open market. Biocon has finally decided to list its research arm Syngene in July 2015. Finally, on the domestic front, the Indian pharmaceutical market (IPM) registered highest ever sales of | 8047 crore (grew 17.2% YoY) in April 2015. The YoY growth was mainly driven by robust YoY volume growth 8.8% (0.3% in April 2014) followed by price hikes – 5.2% (1.7% in April 2014) and new product launches (3.2%). Domestic markets took 24 months to move from | 6000 crore to | 7000 crore whereas it has taken just nine months to breach the | 8000 crore mark. Pharma takes breather after recent run up Pharma stocks are witnessing a brief phase of consolidation after riding the re-rating wave in FY15. The consolidation was warranted as even after re-rating, most pharma stocks were running slightly ahead of valuations. We, however, maintain our long term bullish view on the sector on the back of its structural strength. Strong visibility on the back of a good product basket and a reasonable base business growth continue to attract buying interest in the pharma sector despite premium valuations. US and Indian formulations remain the main growth drivers for the sector on the back of a strong pipeline and incremental product launches. Healthy operating margins, relatively low leverage and strong return ratios are some of the other attributes for most pharma players. Sun Pharma, Lupin and Dr Reddy’s are our top picks from the large cap pharma space whereas Cadila, Aurobindo, Torrent Pharma and Ajanta Pharma are our picks from the midcap pharma space. Near term headwinds for the sector are a slower-than-expected pick-up in USFDA approvals and currency volatility in some of the pharmerging markets.

Health CheckSector View

Outperformer

Index Performance as on May 21, 2015

Return (%) 1M 3M YTD 1Y

CNX 500 1 -3 3 19

Nifty 0 -4 2 16

CNX Pharma 1 7 15 69

Return (%)

Stocks Performance Mcap

Company 1M 3M YTD 1Y 21-May

Sun Pharma.Inds. 2 8 19 70 237111

Lupin -2 1 20 85 77137

Dr Reddy's Labs 2 7 12 58 61883

Cipla 2 -1 7 73 53847

Aurobindo Pharma 0 28 19 119 39580

Cadila Health. 0 10 10 85 35993

Glaxosmit Pharma 0 1 0 26 27197

Glenmark Pharma. 0 14 16 72 24327

Divi's Lab. 2 8 6 43 24284

Torrent Pharma. 3 12 10 97 21111

Apollo Hospitals 3 -3 15 42 18115

Wockhardt -17 -2 42 99 15822

Ajanta Pharma 1 28 49 218 12215

Pfizer -1 12 3 84 10195

Biocon -2 1 5 2 8952

Ipca Labs. 1 -1 -9 -17 8441

Natco Pharma 13 68 53 213 7757

Strides Arcolab 5 29 24 156 7070

Indoco Remedies 5 19 20 163 3457

Jubilant Life 10 6 42 -9 2742

Unichem Labs. -6 -7 -17 4 1827

Return (%)

Mcap: Market cap in | crore

Price movement

50006000700080009000

100001100012000130001400015000

May-14 Aug-14 Nov-14 Feb-15 May-15

4000

6000

8000

10000

12000

CNX Pharma Nifty (RHS)

Research Analyst

Siddhant Khandekar [email protected] Mitesh Shah [email protected]

Nandan Kamat [email protected]

ICICI Securities Ltd. | Retail Equity Research

Page 2

Regulatory approvals

Exhibit 1: Summary of USFDA approvals for March 2015

[5

Company Drug Name Therapeutic Area Innovator company Generic Version of Market SizeAurobindo Pharma Sildenafil Citrate Harmonal Pfizer Revatio US$ 300 millionAurobindo Pharma Atracurium Besylate CNS Hospira Tracrium NAGlenmark Ethinyl Estradiol; Levonorgestrel Contraceptive Wyeth Pharms Alesse US$ 6.4 millionLupin Memantine Hydrochloride CNS Forest Labs Namenda US$ 1.1 billionGlenmark Ethinyl Estradiol; Norethindrone Acetate Contraceptive Warner Chilcott Estrostep US$ 38.6 millionStrides Acrolab Polyetylene Glycol 3350; Potassium Chloride; Sodium Bicarbonate;

Sodium CchlorideColonoscopy Braintree Nulytely US$ 20 million

Aurobindo Pharma Cefixime Antibiotic Lederle Suprax US$ 123 millionNatco Pharma Alprazolam CNS UCB Inc Niravam NALupin Quinine Sulfate Anti-malaria Mutual Pharm Co Inc Qualaquin US$ 31.9 millionSun Pharma Oxymorphone Hydrochloride Pain Endo Pharms Opana US$ 25 millionTorrent Pharma Aripiprazole CNS Otsuka Abilify US$ 7.8 billion

Company Drug Name Therapeutic Area Innovator company Generic Version of Market SizeTorrent Pharma Rosuvastatin Calcium Avascular necrosis IPR Crestor US$ 5 billionLupin Fesoterodine Fumarate Urology Pfizer Toviaz US$ 159 millionGlenmark Calcipotriene Vitamins Leo Pharma Dovonex US$ 92.8 million

Tentative Approvals

CNS: Central Nervous System; CVS: Cardiovascular, NA: Not available; Source: USFDA, ICICIdirect.com Research

Regulatory approvals/IP issues

Dr Reddy’s launches Somazina for stroke patients in India Dr Reddy’s has launched Citicoline’s branded drug Somazina in India, for the treatment of post-stroke patients. The company has partnered with Citicoline for launching this drug in India. Somazina is indicated for improving cognitive function in patients who have suffered from stroke or cerebral infarction, or who have undergone brain surgery or suffered from head injuries. Every year, ~15 lakh people suffer from stroke in India. As per the Global Burden of Disease Study 2013, cerebral stroke is the third leading cause of deaths in India. Lawsuits/court rulings/settlements/USFDA regulations

Case filed against Ranbaxy in US court US based retailer Meijer Inc has filed a case against Ranbaxy in the US district court for alleging anti-trust and other violations for allegedly manipulating USFDA rules to keep generic drugs of other companies out of the marketplace. Supreme Court bars Glenmark from diabetes drug The Supreme Court has restrained Glenmark Pharmaceuticals from the manufacture and sale of Merck’s anti-diabetes drugs Januvia and Janumet for patent infringement. Glenmark sells the medicines under the brand names Zita and Zita-met. The Supreme Court has, however, allowed Glenmark to sell its existing stocks of these drugs in the market. As per MAT April 2015, annual sales of Zita and Zita-met brands were ~| 105 crore (1.5% of FY15 sales). M&As, demergers and JVs

Lupin acquires Brazilian company Lupin has acquired a 100% equity stake in Brazil based Medquimica Industria Farmaceutica for an undisclosed amount. The acquisition marks Lupin’s maiden foray into the Brazilian market. This is the second acquisition in the LatAm market after its acquisition of Laboratorios Grin in Mexico last fiscal. Medquimica is a broad-based pharmaceutical company engaged in development, manufacture and commercialisation of branded generics and over-the-counter (OTC) products. It reported net revenues of around BRL 94 million (US$31 million) in CY14 and has over 550 employees.

ICICI Securities Ltd. | Retail Equity Research

Page 3

Daiichi exits Sun Pharma Daiichi Sankyo has offloaded its entire 8.93% stake (21.4 crore shares) in Sun Pharma in the open market. The company has assigned an indicative price band of | 930.00 and | 1,043.80 per share. In the upper band, the total consideration stands at ~| 22420 crore. The company has cited ‘’perspective of improvement in corporate value’’ as the reason for offloading. Daiichi has taken a significant hit on its books due to a one-time write-down of 46.2 billion yen (~| 2450 crore) related to its investment in Ranbaxy Laboratories. Strides Arcolab to buy Aspen's generic pharma Strides Arcolab has signed definitive agreements with certain wholly-owned subsidiaries of South Africa based Aspen Pharmacare Holdings to acquire a generic pharmaceutical business in Australia together with certain branded pharmaceutical assets. The business, which will operate under the Arrow Pharmaceuticals brand, will sell approximately 140 generic prescription drugs and an extensive range of non-prescription pharmacy products. The acquired products had sales of approximately A$120 million in the past financial year (June 2014) with an EBITDA margin of ~31%. The consideration for the acquisitions will be ~A$ 380 million. The transaction is likely to be financed by a combination of internal accruals and debt financing. Torrent Pharma to acquire Zyg Pharma Torrent Pharmaceuticals has inked an agreement to fully acquire Zyg Pharma for an undisclosed amount. The company is engaged in manufacturing various dermatological formulations like creams, ointments, gels, lotions and solutions. The acquisition is likely to strengthen Torrent’s position in niche dermatological segment, especially in developed markets like the US and Europe. Cipla increases stake in Ugandan company Cipla's wholly owned subsidiary, Cipla (EU) Ltd, UK has entered into a definitive agreement to acquire a 51% stake in Quality Chemicals, Uganda (QCL) from the existing shareholders of QCL. As per the agreement, the consideration works out to US$30 million. QCL was incorporated in 1997 and is engaged in the business of import and distribution of pharmaceutical and consumer products. QCL also holds a 22.05% stake in the company's subsidiary in Uganda, Cipla Quality Chemical Industries (CQCIL). Consequent to this acquisition, Cipla's effective stake (held through its subsidiaries) in CQCIL will increase from the existing 51.05% to 62.30%. Cipla acquires Brazilian company Duomed Cipla has acquired Duomed Produtos Farmaceuticos Ltda. in Brazil at ~| 2.6 crore. The deal has an approval of Brazilian health authority (Anvisa) and other regulatory authorities to import and distribute pharmaceutical products in Brazil. Capex/investments/fund raising

Biocon initiates Syngene listing Biocon’s contract research subsidiary Syngene International Ltd (Syngene) has filed the draft DRHP with Sebi seeking approval for an initial public offering (IPO). This is an offer for sale (OFS) by Biocon of a part of its shareholding in Syngene. Biocon along with its subsidiary Biocon Research (BRL) currently holds an 84.5% equity stake in Syngene. Biocon is offering to sell up to 22 million equity shares of face value of | 10 each, through Syngene’s IPO. Syngene has reported revenues of | 822 crore in FY15.

ICICI Securities Ltd. | Retail Equity Research

Page 4

Glenmark raises | 945 crore via preferential allotment to Temasek Temasek Holdings Pvt Ltd, the investment arm of the Singapore government, has made an investment of | 945 crore in Glenmark through preferential issue (1.08 crore share @ | 875) through its wholly-owned subsidiary Aranda Investments (Mauritius) Pte Ltd. The money will most likely be utilised by the company for debt repayment. Q4FY15 Results

Torrent Pharma - High base impacts result, outlook robust Revenues de-grew 5.8% to YoY to | 1154 crore, on account of a 44% decline in US sales to | 224 crore. EBITDA margins declined 1453 bps to 14% on account of higher employee expenses and other expenditure. EBITDA de-grew 53.7% to | 162 crore. However, adjusted EBITDA (ex-one offs) came in at | 259 crore. Net profit witnessed a YoY reduction of 46.7% to | 130 crore mainly on account of a lower operational performance. Cadila - continues to thrive on superior US growth Revenues grew 16.2% to | 2288.2 crore mainly on the back of 44.3% YoY growth in the US formulations business to | 979 crore. EBITDA margins improved 346 bps to 21.7% while EBITDA grew 38.3% YoY to | 495.9 crore. PAT grew 46.5% YoY to | 350.4 crore boosted mainly by a strong operational performance. Lupin - US slowdown halts growth Revenues de-grew 1.4% YoY to | 3078.2 crore. US sales (45% of net sales) de-grew 6.3% to | 1378 crore on the back of a slowdown in product approvals and pricing pressure. Domestic formulations (22% of net sales) grew 15.2% YoY to | 664 crore. EBITDA margins declined 246 bps to 25.6% mainly on account of a 318 bps YoY increase in employee costs as percentage of sales and higher R&D spend. Net profit declined 1.1% YoY to | 547 crore owing to a decline in EBITDA margins. Jubilant - Pharma performance improves but LSI lags Revenues declined 1.7% YoY to | 1536.5 crore. Revenues in the pharmaceutical business grew 8.2% YoY to | 762.6 crore while life science ingredients (LSI) revenues de-grew 9.6% YoY to | 775.5 crore. EBITDA margins increased ~37 bps YoY to 16.1% mainly on account of lower other expenditure. EBITDA increased 0.7% to | 247.4 crore. Adjusted net profit grew 22.7% YoY to | 76.6 crore on the back of an EBITDA improvement, lower depreciation and finance cost. Dr Reddy’s - Higher R&D, adverse product mix hit margins Revenues grew 11.2% YoY to | 3870.4 crore mainly on account of 15% growth in US formulation sales to | 1715.4 crore. EBITDA margins declined 111 bps YoY to 21.3%. The delta was mainly due to higher R&D spends, change in product mix and currency fluctuation. EBITDA increased 5.7% to | 825.6 crore. Net profit increased 7.7% to | 518.8 crore. The miss was on account of lower operational income and higher finance expenses. Ajanta Pharma - maintains growth tempo Revenues grew 18.6% YoY to | 368.8 crore on the back of higher-than-expected export growth (up 18.9% to | 245 crore). EBITDA margins improved 261 bps YoY to 38.2% while EBITDA increased 27.3% YoY to | 140.7 crore. Adjusted net profit increased 30.3% YoY to | 91.3 crore, driven by a strong operational performance.

ICICI Securities Ltd. | Retail Equity Research

Page 5

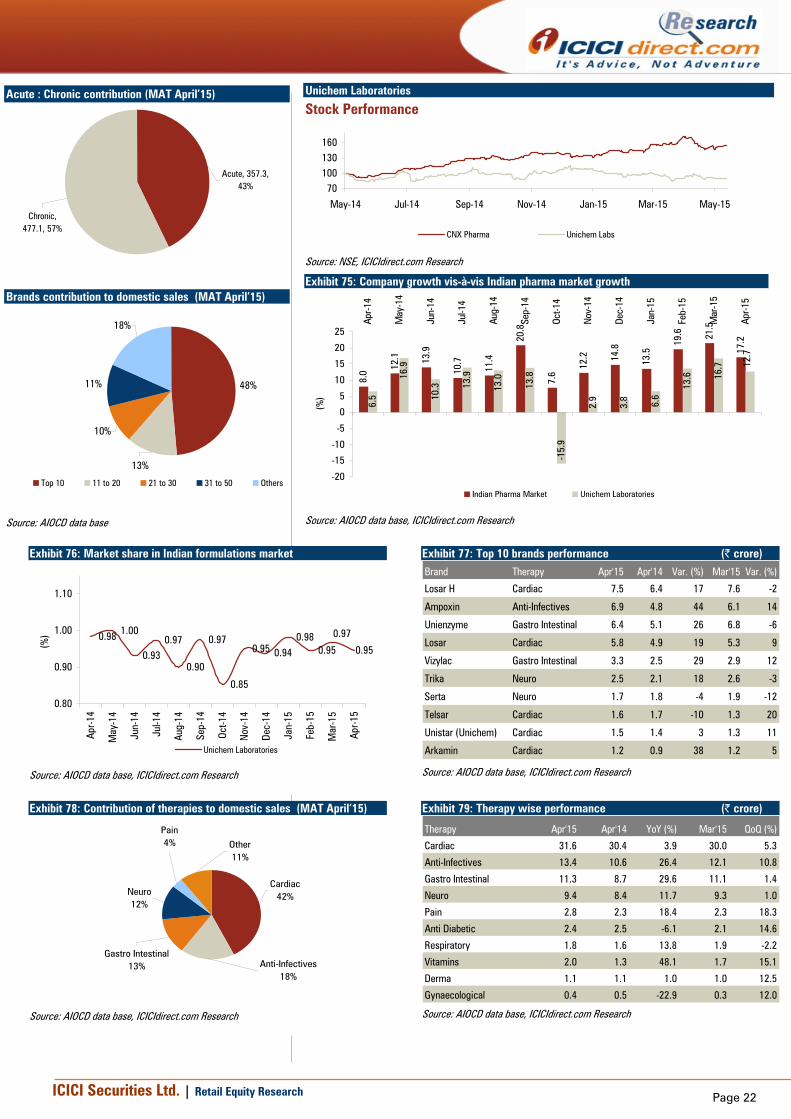

Biocon - Focus shifts to Syngene unlocking Revenues grew ~15% YoY to | 837.3 crore. The growth was driven by ~27% growth in the research segment to | 238 crore and ~11% growth in the biopharma segment to | 489 crore. EBITDA margins contracted 200 bps YoY to 22.1% on higher R&D expenses. EBITDA grew ~5% to | 184.9 crore while adjusted net profit declined 6.2% to | 106.1 crore. Unichem -Another weak quarter; margins plunge further Revenues grew ~5% YoY to | 256 crore mainly due to meagre 3% YoY growth in domestic sales to | 151.1 crore. Exports, on the other hand, grew ~8%. EBITDA margins declined 720 bps to 5.8% due to subdued domestic sales. EBITDA declined ~53% YoY to | 14.8 crore due to a change in the product mix. Net profit witnessed a YoY decline of ~68% to | 9.8 crore owing to a decline in EBITDA margins.

ICICI Securities Ltd. | Retail Equity Research

Page 6

Exhibit 2: Patent litigations in last 12 months

[5

Month Innovator ANDA Filer Brand Name API Used for May-14 Senju Pharmaceuticals Aurobindo Pharma Zymaxid Gatifloxacin ConjunctivitisMay-14 Otsuka Pharmaceutical Co. Alembic Pharma Abilify Aripiprazole SchizophraniaMay-14 Dr Reddy's Labs Purdue Pharmaceutical Product Intermezzo Zolpidem InsomniaMay-14 Otsuka Pharmaceutical Co. Cadila Healthcare Abilify Aripiprazole SchizophraniaMay-14 Otsuka Pharmaceutical Co. Aurobindo Pharma Abilify Aripiprazole SchizophraniaMay-14 AstraZeneca AB Aurobindo Pharma Onlyza Saxagliptin Type 2 DiabetesMay-14 AstraZeneca AB Glenmark Generics Onlyza Saxagliptin Type 2 DiabetesMay-14 AstraZeneca AB Wockhardt Onlyza Saxagliptin Type 2 DiabetesMay-14 Otsuka Pharmaceutical Co. Wockhardt Abilify Aripiprazole SchizophraniaMay-14 Forest Laboratories Inc. Ranbaxy Labs Namenda XR Memantine Alzheimer's diseaseJun-14 AstraZeneca Pharmaceuticals LP Sun Pharma Global FZE; Onglyza Saxagliptin DiabetesJun-14 Bristol-Myers Squibb Co. Aurobindo Pharma Reyataz Atazanavir HIVJun-14 Teva Women's Health Lupin Quartette Levonorgestre ContraceptiveJun-14 Forest Laboratories Inc Aurobindo Pharma Namenda XR Memantine Alzheimer's diseaseJun-14 Senju Pharma Lupin Pharma Inc. Prolensa Bromfenac Ocular InflammationJul-14 Pfizer Inc Aurobindo Pharma Tygacil Tygecycline InfectionJul-14 GlaxoSmithKline LLC Glenmark Generics Inc. Coreg Carvedilol High Blood PressureJul-14 Allos Therapuetics Inc Dr Reddy's Folotyn Pralatrexate LymphomaJul-14 Acorda Therapeutics Inc.; Aurobindo Pharma Ampyara Dalfampridine Multiple SyrosysJul-14 Alcon Pharmaceuticals Ltd. Aurobindo Pharma Vigamox Moxifloxacin Eye InfectionJul-14 Gilead Sciences Inc. Lupin Ltd. Atripla Efavirenz/Emtricitabine/Tenofovir HIVJul-14 AbbVie Inc. Aurobindo Pharma Norvir Ritonavir HIVJul-14 Alkermes Pharma Ltd. Sun Pharmaceuticals Focalin XR Dexmethylphenidate ADHDJul-14 Otsuka Pharma Co. Torrent Pharma Abilify Aripiprazole SchizophreniaJul-14 Astrazeneca AB Cadila Healthcare Nexium Esomeprazole Acid RefluxAug-14 Janssen Products LP Cipla Ltd. Prezista Darunavir HIVAug-14 Forest Labs Lupin Ltd. Namenda Memantine Hydrochloride Alzheimer's diseaseAug-14 Senju Pharma Ltd. Lupin Ltd. Prolensa Bromfenac Ocular InflammationAug-14 Novartis Pharma Dr. Reddy's Labs Gleevec Imatinib Mesylate Organ RejectionSep-14 Millenium Pharmaceuticals Glenmark Pharma Valcade Bortezomib Multiple MylomaSep-14 Teva Pharma Dr. Reddy's Labs Copaxon Glatiramer Acetate Multiple SclerosisSep-14 Reckitt Benckiser LLC Aurobindo Pharma Mucinex Guaifenesin MucusSep-14 Cephalon Inc. Dr. Reddy's Labs Treanda Bendamustine LeukemiaSep-14 Cephalon Inc. Sun Pharma Treanda Bendamustine LeukemiaOct-14 Novartis Pharma Dr. Reddy's Labs Gleevec Imatinib LeukemiaOct-14 Braintree Laboratory Inc. Taro Pharma Suprep Sodium Sulphate Bowel PreparationOct-14 Cephalon Inc. Wockhardt Treanda Bendamustine LeukemiaNov-14 Biomarin Pharma Dr. Reddy's Labs Kuvan Sapropterin Dihydrochloride phenylketonuriaNov-14 Otsuka Pharma Cadila Healthcare Abilify Aripiprazole schizophreniaNov-14 Otsuka Pharma Alembic Pharma Abilify Aripiprazole schizophrenia

Jan-15 iCeutica Lupin Ltd. Zorvolex Diclofenac Anti-Inflammatory

Jan-15 Senju Pharma Lupin Ltd. Prolensa Bromfenac Eye Inflammation

Jan-15 Sheonogi & Co. Aurobindo Pharma Doribax Doripenem Infection

Jan-15 Teva Pharma Dr. Reddy's Labs Copaxone Glatiramer Multiple Sclerosis

Feb-15 Roxane Laboratories Lupin Ltd. Roxane Calcium Acetate CCalcium Acetate Serum phosphorous Reduction

Feb-15 Cephalon Inc. Glenmark Generics Treanda Bendamustine Leukemia

Feb-15 Cephalon Inc. Dr. Reddy's Labs Treanda Bendamustine Leukemia

Mar-15 Otsuka Pharma Indoco Remedies Abilify Aripiprazole Schizophrenia

Apr-15 Sanofi Aventis Dr. Reddy's Labs Jevtana KIT Cabazitaxel Prostate Cancer

Apr-15 Sanofi Aventis Glenmark Jevtana KIT Cabazitaxel Prostate Cancer

Apr-15 Medicis Pharma Taro Pharma Zyclara Imiquimod Actinic Keratoses

Apr-15 Alcon Research Wockhardt Patanol Olopatadine hydrochloride Allergic Conjunctivitis

Apr-15 Janssen Products LP Cipla Prezista Darunavir Anti-Retroviral

Apr-15 Teva Pharma Dr. Reddy's Labs Copaxone Glatiramer Multiple Sclerosis

Apr-15 Eli Lilly Lupin Effient Prasugrel CVS

Apr-15 Horizon Pharma Lupin Pennsaid Diclofenac Osteoporosis

Source: Bloomberg, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 7

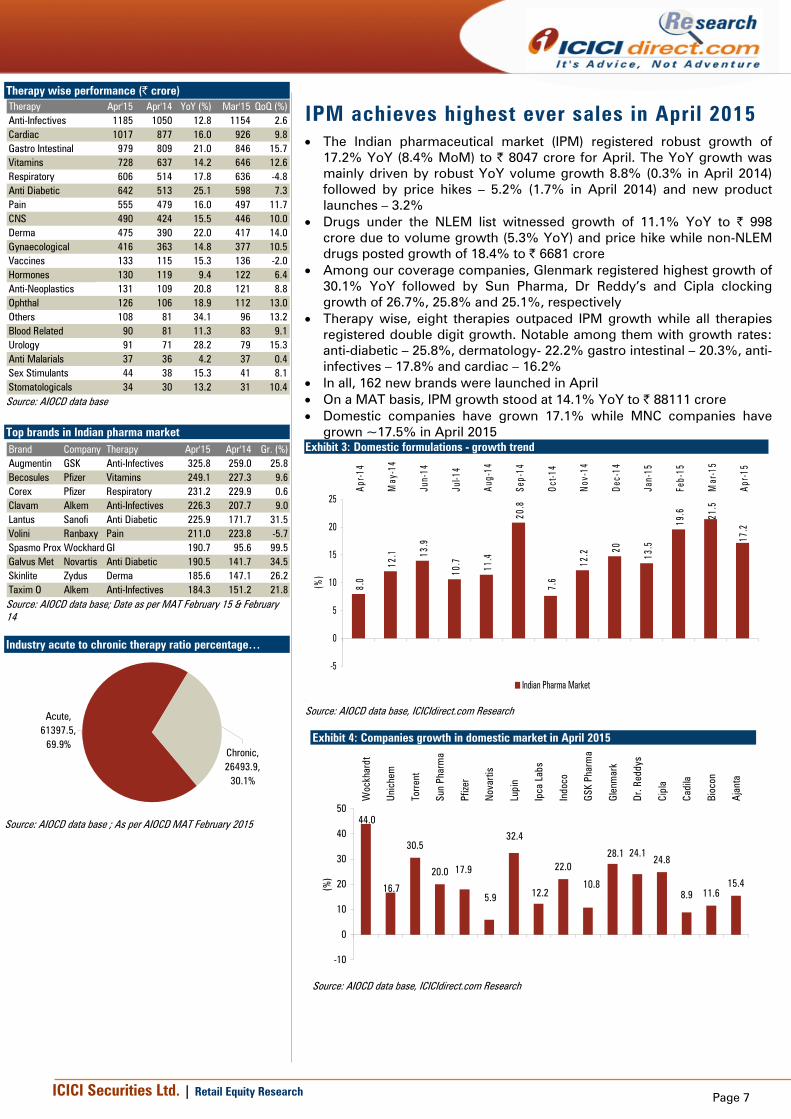

IPM achieves highest ever sales in April 2015 • The Indian pharmaceutical market (IPM) registered robust growth of

17.2% YoY (8.4% MoM) to | 8047 crore for April. The YoY growth was mainly driven by robust YoY volume growth 8.8% (0.3% in April 2014) followed by price hikes – 5.2% (1.7% in April 2014) and new product launches – 3.2%

• Drugs under the NLEM list witnessed growth of 11.1% YoY to | 998 crore due to volume growth (5.3% YoY) and price hike while non-NLEM drugs posted growth of 18.4% to | 6681 crore

• Among our coverage companies, Glenmark registered highest growth of 30.1% YoY followed by Sun Pharma, Dr Reddy’s and Cipla clocking growth of 26.7%, 25.8% and 25.1%, respectively

• Therapy wise, eight therapies outpaced IPM growth while all therapies registered double digit growth. Notable among them with growth rates: anti-diabetic – 25.8%, dermatology- 22.2% gastro intestinal – 20.3%, anti-infectives – 17.8% and cardiac – 16.2%

• In all, 162 new brands were launched in April • On a MAT basis, IPM growth stood at 14.1% YoY to | 88111 crore • Domestic companies have grown 17.1% while MNC companies have

grown ~17.5% in April 2015 Exhibit 3: Domestic formulations - growth trend

8.0

12.1 13

.9

10.7 11

.4

20.8

19.6

7.6

12.2 20

13.5

21.5

17.2

-5

0

5

10

15

20

25

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market [

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 4: Companies growth in domestic market in April 2015

30.5

20.0 22.024.8

11.615.4

44.0

16.7

17.9

5.9

32.4

12.210.8

28.1 24.1

8.9

-10

0

10

20

30

40

50

Woc

khar

dt

Unic

hem

Torr

ent

Sun

Phar

ma

Pfize

r

Nov

artis

Lupi

n

Ipca

Lab

s

Indo

co

GSK

Phar

ma

Glen

mar

k

Dr. R

eddy

s

Cipl

a

Cadi

la

Bioc

on

Ajan

ta

(%)

Source: AIOCD data base, ICICIdirect.com Research

Therapy wise performance (| crore) Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)Anti-Infectives 1185 1050 12.8 1154 2.6Cardiac 1017 877 16.0 926 9.8Gastro Intestinal 979 809 21.0 846 15.7Vitamins 728 637 14.2 646 12.6Respiratory 606 514 17.8 636 -4.8Anti Diabetic 642 513 25.1 598 7.3Pain 555 479 16.0 497 11.7CNS 490 424 15.5 446 10.0Derma 475 390 22.0 417 14.0Gynaecological 416 363 14.8 377 10.5Vaccines 133 115 15.3 136 -2.0Hormones 130 119 9.4 122 6.4Anti-Neoplastics 131 109 20.8 121 8.8Ophthal 126 106 18.9 112 13.0Others 108 81 34.1 96 13.2Blood Related 90 81 11.3 83 9.1Urology 91 71 28.2 79 15.3Anti Malarials 37 36 4.2 37 0.4Sex Stimulants 44 38 15.3 41 8.1Stomatologicals 34 30 13.2 31 10.4

Source: AIOCD data base

Top brands in Indian pharma market Brand Company Therapy Apr'15 Apr'14 Gr. (%)Augmentin GSK Anti-Infectives 325.8 259.0 25.8Becosules Pfizer Vitamins 249.1 227.3 9.6Corex Pfizer Respiratory 231.2 229.9 0.6Clavam Alkem Anti-Infectives 226.3 207.7 9.0Lantus Sanofi Anti Diabetic 225.9 171.7 31.5Volini Ranbaxy Pain 211.0 223.8 -5.7Spasmo Prox Wockhard GI 190.7 95.6 99.5Galvus Met Novartis Anti Diabetic 190.5 141.7 34.5Skinlite Zydus Derma 185.6 147.1 26.2Taxim O Alkem Anti-Infectives 184.3 151.2 21.8

Source: AIOCD data base; Date as per MAT February 15 & February 14 Industry acute to chronic therapy ratio percentage…

Acute, 61397.5,

69.9%Chronic, 26493.9,

30.1%

Source: AIOCD data base ; As per AIOCD MAT February 2015

ICICI Securities Ltd. | Retail Equity Research

Page 8

Sun Pharmaceuticals

Stock Performance

80

125

170

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Sun Pharma

Source: NSE, ICICIdirect.com Research Exhibit 5: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

10.0

16.5 17

.6

15.3

14.4

9.9

9.7

14.9

21.7

13.5 16

.0

20.0

26.7

0

5

10

15

20

25

30

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Sun Pharmaceutical Industries

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 6: Market share in Indian formulations market

5.3

5.5

5.1

5.35.2

4.9

5.4

5.6 5.7

5.9

5.4

5.65.7

4.8

5.0

5.2

5.4

5.6

5.8

6.0

6.2

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Sun Pharmaceutical Industries

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 7: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Gemer Anti Diabetic 12.8 10.2 26 11.6 10

Istamet Anti Diabetic 12.5 7.9 59 11.5 9

Susten Gynaecological 12.3 9.9 24 11.4 8

Pantocid Gastro Intestinal 11.9 9.5 25 11.2 7

Levipil Neuro 11.6 8.3 41 10.7 9

Aztor Cardiac 9.9 7.4 34 8.7 14

Pantocid Dsr Gastro Intestinal 9.8 6.8 44 9.4 5

Montek-Lc Respiratory 6.3 4.6 37 6.5 -3

Glucored Anti Diabetic 6.3 5.7 10 5.7 10

Cardivas Cardiac 6.0 4.6 30 5.3 13

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 8: Contribution of therapies to domestic sales (MAT April’15) z

Neuro 35%

Cardiac23%

Gastro Intestinal19%

Anti Diabetic15%

Gynaecological8%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 9: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Neuro 123.5 95.8 29.0 113.1 9.3

Cardiac 84.9 68.0 24.9 76.0 11.8

Gastro Intestinal 70.2 51.0 37.7 63.2 11.1

Anti Diabetic 55.9 42.5 31.5 50.5 10.8

Gynaecological 28.4 30.1 -5.6 25.8 10.1

Pain 20.4 15.3 32.9 18.0 13.5

Ophthal 20.0 15.4 30.1 17.6 13.7

Respiratory 16.9 14.0 20.4 17.2 -1.8

Vitamins 15.2 10.4 47.1 14.1 8.1

Hormones 9.1 9.0 2.0 7.6 19.9

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 90.4, 28%

Chronic, 231.4, 72%

Brands contribution to domestic sales (MAT April’15)

21%

11%

8%

11%

49%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 9

Ranbaxy Laboratories

Stock Performance

80120160200240

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Ranbaxy

Source: NSE, ICICIdirect.com Research Exhibit 10: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

0.3

4.1

15.0

8.5

10.1

15.9

0.9 10

.7

8.2

8.5

3.8

6.7

6.2

-15

-10

-5

0

5

10

15

20

25

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Ranbaxy Laboratories

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 11: Market share in Indian formulations market

3.56 3.53 3.563.49

3.583.48 3.44

3.67

3.43 3.40

3.13 3.113.23

2.82.93.03.13.23.33.43.53.63.73.8

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Ranbaxy Laboratories

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 12: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Volini Pain 16.9 17.9 -6 15.6 8

Rosuvas Cardiac 12.7 10.2 24 11.5 11

Storvas Cardiac 10.4 8.3 25 9.2 13

Mox Anti-Infectives 9.3 8.1 14 9.4 -1

Sporidex Anti-Infectives 6.1 3.9 53 5.0 21

Moxclav Anti-Infectives 5.5 3.8 44 5.6 -3

Cepodem Anti-Infectives 5.2 4.3 22 5.4 -4

Zanocin Anti-Infectives 4.7 3.6 32 3.7 28

Oframax Anti-Infectives 4.5 2.7 65 4.2 7

Silverex Ionic Derma 3.8 3.4 12 3.0 26

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 13: Contribution of therapies to domestic sales (MAT April’15) z

Anti-Infectives30%

Cardiac15%Pain

12%Derma11%

Vitamins 7%

Other25%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 14: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Anti-Infectives 77.1 66.0 16.8 75.3 2.4

Cardiac 44.5 35.9 23.9 39.5 12.5

Pain 31.8 30.1 5.8 27.3 16.4

Derma 30.2 25.3 19.0 24.5 23.0

Vitamins 6.8 26.9 -74.9 5.3 26.6

Gastro Intestinal 19.2 16.2 18.4 15.0 27.6

Urology 12.9 8.8 46.2 10.4 23.3

Respiratory 8.6 8.5 0.5 8.9 -3.7

Neuro 8.3 9.4 -12.0 6.8 22.0

Anti Diabetic 9.0 6.1 47.3 7.8 15.0

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 2296.5, 76%

Chronic, 711.4, 24%

Brands contribution to domestic sales (MAT April’15)

49%

19%

10%

10%

12%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 10

Cipla

Stock Performance

80

110

140

170

200

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Cipla

Source: NSE, ICICIdirect.com Research

Exhibit 15: Company growth vis-à-vis Indian pharma market growth

8.0 12

.1 13.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

8.3

7.2 12

.4

10.4

15.4

38.8

10.3

8.3 13

.5

13.2

24.0

24.8

25.1

0

5

10

15

20

25

30

35

40

45

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Cipla

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 16: Market share in Indian formulations market

5.0

4.74.6

4.7

4.9

5.4

5.04.9

5.1 5.15.3

5.1

5.3

4.04.24.44.64.85.05.25.45.6

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Cipla

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 17: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Foracort Respiratory 17.5 13.1 33 15.5 13

Budecort Respiratory 13.0 10.1 29 13.3 -2

Seroflo Respiratory 12.5 10.5 19 11.3 11

Asthalin Respiratory 12.1 11.6 4 12.3 -1

Duolin Respiratory 10.6 8.7 22 9.7 9

Aerocort Respiratory 9.8 8.5 16 7.8 25

Azee Anti-Infectives 7.2 5.8 24 7.4 -2

Emeset Gastro Intestinal 6.9 3.9 77 5.3 30

Montair Lc Respiratory 6.7 5.0 33 6.5 2

Dytor Cardiac 6.6 5.1 30 5.7 17

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 18: Contribution of therapies to domestic sales (MAT April’15)

Respiratory30%

Anti-Infectives27%

Cardiac13%

Gastro Intestinal7%

Urology5%

Other18%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 19: Therapy wise performance (| crore)

Therapy Apr '15 Apr'14 YoY (%) Mar '15 QoQ (%)Respiratory 128.9 104.8 23.0 119.8 7.6Anti-Infect ives 109.1 86.7 25.8 96.6 12.9

Cardiac 55.8 44.8 24.7 48.7 14.6Gastro Intestinal 33.0 25.4 29.7 25.9 27.2

Urology 20.6 14.4 43.5 17.8 15.7Neuro 15.6 12.1 29.3 13.6 14.4

Pain 12.6 8.2 54.0 10.4 20.8

Ophthal 10.7 9.6 12.0 8.6 24.7

Derma 9.5 8.7 9.6 8.0 19.0

Vitamins 9.0 8.5 5.6 6.6 37.4

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 2609.7, 59%

Chronic, 1812.6, 41%

Brands contribution to domestic sales (MAT April’15)

25%

12%

9%12%

42%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 11

Dr Reddy’s Laboratories

Stock Performance

70

100

130

160

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15CNX Pharma Dr. Reddys

Source: NSE, ICICIdirect.com Research

Exhibit 20: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

5.0 8.

9

16.0

9.3

15.3 16.6

1.6

9.3 12

.8

12.3 16

.1

24.1 25

.8

-10

0

10

20

30

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Dr. Reddys Laboratories

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 21: Market share in Indian formulations market

2.0

2.12.1

2.1

2.1 2.1

2.0

2.1

2.2

2.12.1

2.2 2.2

1.9

2.0

2.0

2.1

2.1

2.2

2.2

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Dr. Reddys Laboratories

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 22: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Omez Gastro Intestinal 10.3 7.7 33 9.0 15

Omez D Gastro Intestinal 7.1 5.4 32 6.3 13

Econorm Gastro Intestinal 6.1 4.6 34 4.7 29

Nise Pain 5.5 4.6 18 5.1 7

Stamlo Cardiac 5.4 4.5 20 5.1 5

Reditux Anti-Neoplastics 4.8 4.0 22 3.9 23

Mintop Derma 4.6 3.6 29 4.3 7

Grafeel Anti-Neoplastics 4.3 1.1 290 2.9 48

Stamlo Beta Cardiac 4.3 3.8 13 4.5 -5

Razo D Gastro Intestinal 4.2 3.6 17 4.0 5

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 23: Contribution of therapies to domestic sales (MAT April’15)

Gastro Intestinal23%

Cardiac16%

Anti-Neoplastics

11%Anti-Infectives9%

Pain 8%

Other33%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 24: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Gastro Intestinal 40.9 32.1 27.5 35.3 15.8

Cardiac 28.9 23.0 25.4 25.8 11.9

Anti-Neoplastics 21.7 15.7 38.4 18.4 17.8

Anti-Infectives 13.6 9.7 40.4 13.5 0.1

Pain 12.9 11.3 14.1 11.5 12.2

Anti Diabetic 12.6 9.9 27.1 12.5 1.1

Derma 12.1 10.9 10.4 11.5 4.5

Respiratory 7.7 6.5 19.2 9.0 -14.3

Urology 6.5 5.6 16.2 6.4 1.2

Stomatologicals 6.2 5.4 15.3 5.9 6.3

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 1294.4, 70%

Chronic, 565.0, 30%

Brands contribution to domestic sales (MAT April’15)

31%

16%9%

12%

32%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 12

Lupin

Stock Performance

75115155195

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Lupin

Source: NSE, ICICIdirect.com Research

Exhibit 25: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

21.5

20.8 23

.0

13.3

8.5

19.8

10.5 13

.7

18.3

15.0

23.3

3.4

19.6

17.2

0

4

8

12

16

20

24

28

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Lupin

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 26: Market share in Indian formulations market

3.6 3.7 3.7

3.4

3.23.3 3.4 3.4 3.4 3.4

3.23.1

3.2

2.32.52.72.93.13.33.53.73.9

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Lupin

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 27: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Gluconorm-G Anti Diabetic 11.2 11.0 2 9.5 17

Tonact Cardiac 7.9 7.5 5 6.9 13

Budamate Respiratory 6.1 5.4 11 7.2 -16

Ramistar Cardiac 4.3 4.6 -7 3.8 14

Rablet-D Gastro Intestinal 4.2 3.9 8 3.6 16

R-Cinex Anti-Infectives 4.1 4.7 -12 4.3 -4

Rablet Gastro Intestinal 4.1 3.8 6 3.4 20

Esiflo Respiratory 3.5 3.3 6 3.5 -1

Signoflam Pain 3.3 2.7 23 2.7 23

Tazar Anti-Infectives 3.2 3.4 -4 2.9 12

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 28: Contribution of therapies to domestic sales (MAT April’15)

Cardiac25%

Anti-Infectives23%

Respiratory12%

Anti Diabetic10%

Gastro Intestinal8%

Other22%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 29: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Cardiac 65.8 61.7 6.7 56.9 15.7

Anti-Infectives 55.8 60.2 -7.3 51.8 7.9

Respiratory 28.8 27.1 6.4 30.1 -4.3

Anti Diabetic 28.3 26.0 8.8 23.9 18.4

Gastro Intestinal 21.0 19.3 8.6 16.8 24.8

Vitamins 15.6 15.9 -2.1 12.7 23.1

Neuro 12.7 13.2 -3.7 10.9 17.0

Pain 13.1 11.2 17.0 10.6 23.4

Gynaecological 8.0 6.6 19.9 6.2 29.1

Derma 1.6 1.5 9.5 1.4 14.5

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 1554.5, 53%

Chronic, 1398.5, 47%

Brands contribution to domestic sales (MAT April’15)

20%

12%

9%13%

46%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 13

Cadila Healthcare

Stock Performance

5080

110140170200230

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Cadila Healthcare

Source: NSE, ICICIdirect.com Research

Exhibit 30: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7 11

.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

9.7

8.8 11

.2

9.1

8.9

12.0

0.9

7.4

11.6

5.1

5.2

8.9

8.1

0

5

10

15

20

25

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Cadila Healthcare

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 31: Market share in Indian formulations market

4.1

3.9 3.9

3.83.8

3.6

3.7

4.0

3.9 3.9

3.73.7 3.7

3.6

3.8

4.0

4.2

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 32: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Skinlite Derma 16.3 13.4 22 15.6 5

Mifegest Kit Gynaecological 14.6 13.2 11 10.0 47

Atorva Cardiac 10.4 8.8 18 10.4 0

Deriphyllin Respiratory 8.8 8.9 -1 8.8 0

Pantodac Gastro Intestinal 7.8 6.8 15 7.3 6

Amlodac Cardiac 6.1 6.0 1 6.1 -1

Primolut N Gynaecological 5.5 4.4 25 4.4 24

Aten Cardiac 5.3 6.1 -13 6.0 -11

Clopitorva Cardiac 4.5 3.0 49 4.1 11

Dexona Hormones 4.4 5.8 -25 3.3 32

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 33: Contribution of therapies to domestic sales (MAT April’15)

Cardiac18%

Gastro Intestinal14%

Gynaecological12%

Respiratory11%

Derma9%

Other36%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 34: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Cardiac 54.4 49.7 9.4 52.9 2.8

Gastro Intestinal 41.8 39.5 5.7 35.6 17.3

Gynaecological 42.8 36.5 17.2 34.2 24.9

Respiratory 31.8 28.8 10.7 31.7 0.2

Derma 26.1 20.7 26.2 24.3 7.5

Pain 20.4 22.5 -9.5 20.4 -0.2

Anti-Infectives 17.3 19.5 -11.2 15.2 13.3

Vitamins 12.1 10.3 17.4 12.5 -3.0

Anti-Neoplastics 13.7 9.3 48.4 13.1 4.7

Anti Malarials 5.4 4.8 13.0 5.5 -2.5

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 2260.0, 68%

Chronic, 1086.8, 32%

Brands contribution to domestic sales (MAT April’15)

27%

13%

8%11%

41%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 14

GlaxoSmithKline Pharmaceuticals

Stock Performance

80110140170200

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma GSK Pharma

Source: NSE, ICICIdirect.com Research

Exhibit 35: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

-12.

2 -7.0 -4.5

-6.0

1.4

13.0

12.1

5.5

0.8 2.

6 6.6 10

.8 12.9

-15

-10

-5

0

5

10

15

20

25

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Glaxosmithkline Pharmaceuticals

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 36: Market share in Indian formulations market

3.53.6 3.6

3.63.7

3.53.4 3.5 3.4

3.3 3.3

3.4 3.4

3.0

3.2

3.4

3.6

3.8

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Glaxosmithkline Pharmaceuticals

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 37: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Augmentin Anti-Infectives 26.6 20.5 30 30.1 -12

Synflorix Vaccines 15.8 10.3 54 14.4 10

Betnovate C Derma 14.5 7.6 90 10.6 37

Zinetac Gastro Intestinal 14.4 12.6 14 12.3 17

Calpol Pain 13.9 11.7 19 13.4 4

Betnovate N Derma 12.2 9.6 27 9.6 28

Eltroxin Hormones 11.9 11.4 4 10.6 13

Ceftum Anti-Infectives 10.2 10.0 3 10.6 -3

Betnesol Hormones 10.0 5.5 82 9.3 7

T Bact Derma 8.0 7.0 14 6.9 16

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 38: Contribution of therapies to domestic sales (MAT April’15)

Anti-Infectives26%

Derma20%Vaccines

12%

Pain 9%

Vitamins 7%

Other26%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 39: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Anti-Infectives 63.2 63.1 0.1 64.2 -1.6

Derma 61.7 44.5 38.4 50.6 21.9

Vaccines 30.9 27.8 11.3 31.1 -0.5

Pain 24.9 20.6 20.4 21.9 13.3

Vitamins 19.1 18.0 6.0 17.7 7.6

Hormones 22.7 17.9 27.1 20.7 9.6

Respiratory 15.0 13.4 11.7 16.6 -9.6

Gastro Intestinal 17.2 16.4 4.7 14.5 18.6

Cardiac 6.3 7.4 -15.1 6.2 0.7

Ophthal 3.6 3.3 8.2 2.9 21.3

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 2666.9, 87%

Chronic, 401.3, 13%

Brands contribution to domestic sales (MAT April’15)

48%

16%

9%

11%

16%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 15

Wockhardt

Stock Performance

050

100150200250300350400

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Wockhardt

Source: NSE, ICICIdirect.com Research Exhibit 40: Company growth vis-à-vis Indian pharma market growth

8.0 12

.1 13.9

10.7

11.4

20.8

7.6 12

.2 14.8

13.5 19

.6 21.5

17.2

-6.1

-2.4

14.6

-5.1

-5.9

18.0

8.5

5.0

-2.6

19.0

31.2

44.0

27.5

-10

0

10

20

30

40

50

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Wockhardt

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 41: Market share in Indian formulations market

1.171.15

1.09

1.191.24

1.08

1.161.10

1.16

1.37

1.47

1.40

1.28

1.01.11.11.21.21.31.31.41.41.51.5

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Wockhardt

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 42: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Spasmo Proxyvon PluGastro Intestinal 23.4 11.0 113 22.3 5

Practin Vitamins 6.9 5.8 NA 7.1 -2

Biovac V Vaccines 6.1 0.0 #DIV/0! 7.6 -20

Bro Zedex Respiratory 4.5 4.8 -8 5.2 -13

Tryptomer Neuro 4.1 4.0 2 4.0 2

Zedex Respiratory 3.4 3.4 0 3.6 -5

Methycobal Vitamins 3.3 3.2 3 3.0 9

Biovac A Vaccines 3.0 1.4 120 3.3 -10

Ace Proxyvon Pain 2.9 2.4 21 2.5 16

Libotryp Neuro 2.0 1.6 23 1.7 17

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 43: Contribution of therapies to domestic sales (MAT April’15)

Gastro Intestinal19%

Vitamins 17%

Respiratory15%

Derma8%

Anti-Infectives7%

Other34%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 44: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Gastro Intestinal 25.3 12.3 105.9 24.0 5.7

Vitamins 17.0 17.0 0.5 16.1 6.0

Respiratory 13.2 12.6 4.5 15.2 -13.2

Derma 6.9 6.1 12.5 7.6 -9.8

Anti-Infectives 6.1 6.6 -8.3 6.1 -0.1

Neuro 6.8 6.2 9.4 6.3 7.8

Pain 6.1 5.1 18.9 5.9 2.1

Vaccines 9.1 1.5 495.4 11.0 -16.9

Anti Diabetic 5.7 5.0 14.9 5.1 13.2

Hormones 1.8 4.0 -55.6 1.9 -5.4

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 861.4, 80%

Chronic, 215.0, 20%

Brands contribution to domestic sales (MAT April’15)

53%

17%

8%

8%14%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 16

Glenmark Pharmaceuticals

Stock Performance

60

100

140

180

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15CNX Pharma Glenmark

Source: NSE, ICICIdirect.com Research

Exhibit 45: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

11.4 15

.0 18.0

9.9

9.1

27.2

2.6

20.4 21

.5

21.4 24

.2

28.1 30

.1

0

5

10

15

20

25

30

35

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Glenmark Pharmaceuticals

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 46: Market share in Indian formulations market

2.1

1.92.0

2.02.1

2.4

2.1

2.4 2.52.4

2.32.3

2.3

1.9

2.1

2.3

2.5

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Glenmark Pharmaceuticals

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 47: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Telma Cardiac 13.6 11.7 16 12.8 6

Telma H Cardiac 10.8 9.4 15 9.8 10

Ascoril Plus Respiratory 7.9 7.0 13 8.8 -10

Candid-B Derma 7.4 5.9 24 5.6 32

Zitamet Anti Diabetic 6.8 3.2 114 6.2 8

Candid Derma 6.3 4.4 43 5.0 26

Telma Am Cardiac 5.5 4.3 28 4.9 13

Zita(Glenmark) Anti Diabetic 4.9 2.0 146 4.3 13

Candid Mouth Derma 3.3 1.9 67 2.6 27

Milixim Anti-Infectives 3.2 1.7 97 3.0 9

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 48: Contribution of therapies to domestic sales (MAT April’15)

Derma29%

Cardiac23%

Respiratory15%

Anti-Infectives14%

Anti Diabetic8%

Other11%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 49: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Derma 52.3 40.4 29.5 42.7 22.5

Cardiac 43.0 35.3 21.8 38.8 10.8

Respiratory 26.4 20.6 28.5 28.8 -8.1

Anti-Infectives 27.1 18.6 45.4 25.3 6.9

Anti Diabetic 15.9 9.9 60.4 14.8 6.9

Gastro Intestinal 5.1 3.3 56.8 4.2 21.8

Vitamins 4.4 3.3 34.5 3.6 20.7

Pain 4.0 3.5 14.3 3.4 17.5

Gynaecological 3.2 4.3 -25.3 3.1 2.8

Otologicals 2.9 2.4 23.2 2.4 24.3

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 1240.2, 63%

Chronic, 723.3, 37%

Brands contribution to domestic sales (MAT April’15)

37%

13%10%

12%

28%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 17

Torrent Pharmaceuticals

Stock Performance

80

170

260

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Torrent Pharma

Source: NSE, ICICIdirect.com Research

Exhibit 50: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

1.1

4.7

12.2

10.9

8.4

18.5

6.0

23.2

30.7

21.1

30.9

30.5

28.7

0

5

10

15

20

25

30

35

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Torrent Pharmaceuticals

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 51: Market share in Indian formulations market

2.232.20

2.26 2.26

2.11 2.12

2.242.31

2.43

2.362.402.32

2.45

1.9

2.0

2.1

2.2

2.3

2.4

2.5

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Torrent Pharmaceuticals

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 52: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Shelcal Vitamins 19.8 8.7 127 14.7 34

Chymoral Forte Pain 9.9 4.7 113 9.8 1

Nikoran Cardiac 6.8 6.0 14 6.3 8

Dilzem Cardiac 5.7 5.7 0 5.1 12

Nebicard Cardiac 5.1 4.4 17 4.3 20

Azulix-Mf Anti Diabetic 4.7 3.9 20 4.2 12

Nexpro Rd Gastro Intestinal 4.2 3.5 18 4.2 0

Nexpro Gastro Intestinal 4.1 3.3 25 4.1 0

Alprax Neuro 3.4 3.0 12 2.9 16

Rozucor Cardiac 3.4 2.7 27 2.6 31

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 53: Contribution of therapies to domestic sales (MAT April’15)

Cardiac29%

Neuro 16%Gastro Intestinal

16%

Vitamins 14%

Anti-Infectives7%

Other18%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 54: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Cardiac 57.5 49.2 16.9 51.1 12.5

Neuro 31.2 26.4 18.5 27.2 14.8

Gastro Intestinal 29.1 23.6 23.4 26.0 11.9

Vitamins 31.2 17.8 74.9 24.2 29.0

Anti-Infectives 10.5 11.0 -4.5 10.8 -2.6

Pain 14.6 7.7 89.4 13.9 4.9

Anti Diabetic 11.1 9.3 19.6 10.1 9.8

Derma 4.4 3.2 37.6 3.8 15.9

Gynaecological 3.8 2.9 31.6 3.0 26.4

Urology 0.6 0.5 23.2 0.5 27.0

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 1000.0, 50%

Chronic, 1017.4, 50%

Brands contribution to domestic sales (MAT April’15)

32%

14%9%

12%

33%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 18

Ipca Laboratories

Stock Performance

60

120

180

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Ipca

Source: NSE, ICICIdirect.com Research

Exhibit 55: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

2.5

22.2

23.1

15.5

21.4

9.2 13

.0

12.9

28.6

35.9

12.2

16.3

14.5

0

5

10

15

20

25

30

35

40

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Ipca Laboratories

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 56: Market share in Indian formulations market

1.3

1.5 1.51.4 1.5

1.51.4

1.31.2 1.2 1.2 1.2 1.3

1.0

1.2

1.4

1.6

1.8

2.0

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Ipca Laboratories

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 57: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Zerodol Sp Pain 6.7 4.2 59 5.7 18

Hcqs Anti Malarials 5.9 4.1 45 5.1 17

Zerodol P Pain 5.2 4.7 11 4.0 29

Rapither-Ab Anti Malarials 3.4 2.4 43 2.7 25

Folitrax Anti-Neoplastics 2.8 2.2 26 2.3 20

Lariago Anti Malarials 2.6 2.3 16 2.8 -6

Glycinorm M Anti Diabetic 2.3 2.5 -7 2.4 -2

Saaz Gastro Intestinal 2.2 1.2 80 1.8 20

Mmf (Ipca) Anti-Neoplastics 2.1 0.5 295 2.3 -7

Larinate Anti Malarials 2.0 2.3 -12 2.1 -5

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 58: Contribution of therapies to domestic sales (MAT April’15)

Pain 23%

Anti Malarials21%

Cardiac17%

Gastro Intestinal8%

Anti-Infectives7%

Other24%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 59: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Pain 24.8 20.4 21.9 20.8 19.5

Anti Malarials 17.6 16.2 9.1 16.1 9.5

Cardiac 17.8 16.8 6.4 16.4 8.8

Gastro Intestinal 8.8 7.9 11.5 7.2 22.3

Anti-Infectives 6.6 5.9 10.7 6.8 -3.4

Anti Diabetic 4.9 5.3 -6.0 4.8 2.4

Respiratory 3.7 3.5 3.9 4.3 -14.8

Neuro 4.9 3.5 41.9 4.5 10.1

Anti-Neoplastics 4.9 2.7 79.5 4.6 6.4

Derma 2.8 2.6 8.9 2.8 -1.5

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 877.5, 73%

Chronic, 325.6, 27%

Brands contribution to domestic sales (MAT April’15)

36%

15%

11%

13%

25%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 19

Biocon

Stock Performance

6080

100120140160180

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15CNX Pharma Biocon

Source: NSE, ICICIdirect.com Research

Exhibit 60: Company growth vis-à-vis Indian pharma market growth

8.0 12

.1 13.9

10.7

11.4

20.8

7.6

12.2 14

.8 19.6 21

.5

17.226.8

33.8

13.5

43.1

20.3

11.4

31.3

9.8

1.0

7.2

18.8

17.5

11.6

11.5

05

101520253035404550

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Biocon

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 61: Market share in Indian formulations market

0.35

0.37

0.40

0.360.35

0.39

0.37

0.36 0.36

0.38

0.350.34

0.36

0.33

0.34

0.35

0.36

0.37

0.38

0.39

0.40

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Biocon

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 62: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Insugen Anti Diabetic 6.7 5.7 17 6.9 -4

Basalog Anti Diabetic 4.7 3.4 41 4.5 6

Blisto Mf Anti Diabetic 1.7 2.1 -18 1.6 11

Canmab Anti-Neoplastics 1.6 0.2 706 2.0 -22

Erypro Blood Related 1.4 0.9 62 1.2 15

Insugen R Anti Diabetic 1.4 1.1 23 1.3 9

Abraxane Anti-Neoplastics 1.0 1.7 -43 1.3 -29

Insugen N Anti Diabetic 0.9 0.6 41 0.8 13

Abstet Anti-Neoplastics 0.8 0.1 521 0.4 94

Psorid Anti-Neoplastics 0.5 0.2 151 0.4 34

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 63: Contribution of therapies to domestic sales (MAT April’15)

Anti Diabetic59%

Anti-Neoplastics

20%

Cardiac9%

Blood Related4%

Anti-Infectives3%

Other 5%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 64: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Anti Diabetic 16.9 14.8 14.4 16.4 2.7

Anti-Neoplastics 5.0 2.9 69.1 5.1 -1.4

Cardiac 1.9 2.9 -33.9 1.9 3.2

Blood Related 1.4 0.9 61.7 1.2 15.4

Anti-Infectives 0.6 1.3 -54.9 0.7 -18.8

Derma 0.8 0.9 -10.9 0.7 5.6

Others 0.3 0.4 -25.1 0.2 27.1

Vitamins 0.2 0.2 -8.1 0.3 -39.0

Gastro Intestinal 0.1 0.0 299.7 0.0 77.3

Pain 0.0 0.0 -59.7 0.0 42.9

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 90.4, 28%

Chronic, 231.4, 72%

Brands contribution to domestic sales (MAT April’15)

72%

12%

7%

6%

3%

Top 10 11 to 20 21 to 30 31 to 50 Others

ICICI Securities Ltd. | Retail Equity Research

Page 20

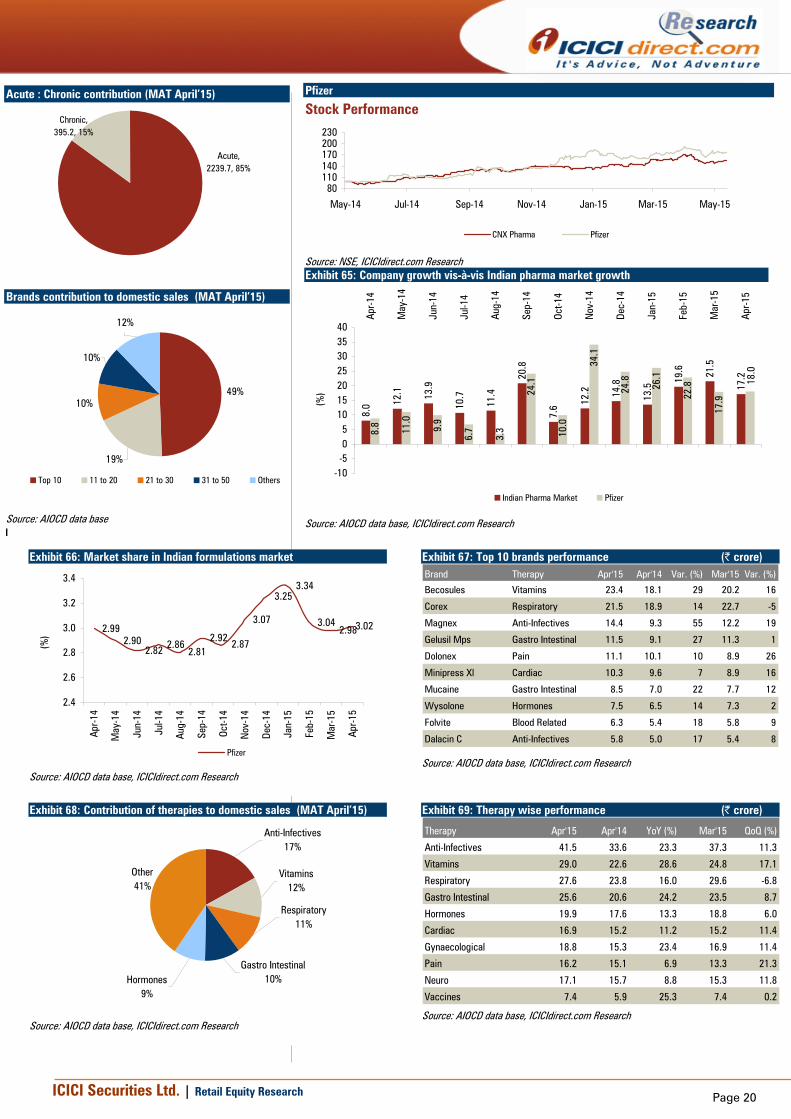

Pfizer

Stock Performance

80110140170200230

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Pfizer

Source: NSE, ICICIdirect.com Research Exhibit 65: Company growth vis-à-vis Indian pharma market growth

8.0 12

.1 13.9

10.7

11.4

20.8

7.6 12

.2 14.8

13.5

19.6 21

.5

17.2

8.8

11.0

9.9

6.7

3.3

24.1

10.0

34.1

24.8

26.1

22.8

17.9

18.0

-10-505

10152025303540

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Pfizer

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 66: Market share in Indian formulations market

2.992.90

2.82 2.862.81

2.922.87

3.07

3.253.34

3.042.983.02

2.4

2.6

2.8

3.0

3.2

3.4

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Pfizer

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 67: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Becosules Vitamins 23.4 18.1 29 20.2 16

Corex Respiratory 21.5 18.9 14 22.7 -5

Magnex Anti-Infectives 14.4 9.3 55 12.2 19

Gelusil Mps Gastro Intestinal 11.5 9.1 27 11.3 1

Dolonex Pain 11.1 10.1 10 8.9 26

Minipress Xl Cardiac 10.3 9.6 7 8.9 16

Mucaine Gastro Intestinal 8.5 7.0 22 7.7 12

Wysolone Hormones 7.5 6.5 14 7.3 2

Folvite Blood Related 6.3 5.4 18 5.8 9

Dalacin C Anti-Infectives 5.8 5.0 17 5.4 8

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 68: Contribution of therapies to domestic sales (MAT April’15)

Anti-Infectives17%

Vitamins 12%

Respiratory11%

Gastro Intestinal10%Hormones

9%

Other41%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 69: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Anti-Infectives 41.5 33.6 23.3 37.3 11.3

Vitamins 29.0 22.6 28.6 24.8 17.1

Respiratory 27.6 23.8 16.0 29.6 -6.8

Gastro Intestinal 25.6 20.6 24.2 23.5 8.7

Hormones 19.9 17.6 13.3 18.8 6.0

Cardiac 16.9 15.2 11.2 15.2 11.4

Gynaecological 18.8 15.3 23.4 16.9 11.4

Pain 16.2 15.1 6.9 13.3 21.3

Neuro 17.1 15.7 8.8 15.3 11.8

Vaccines 7.4 5.9 25.3 7.4 0.2

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 2239.7, 85%

Chronic, 395.2, 15%

Brands contribution to domestic sales (MAT April’15)

49%

19%

10%

10%

12%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base l

ICICI Securities Ltd. | Retail Equity Research

Page 21

Novartis India

Stock Performance

80

130

180

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Novartis India

Source: NSE, ICICIdirect.com Research

Exhibit 70: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

0.1

-0.9

-1.9

-2.4

-0.5

13.4

5.9

5.1 6.

7

2.6 5.

9

-0.1

1.1

-5

0

5

10

15

20

25

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Novartis India

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 71: Market share in Indian formulations market

1.46

1.36 1.35 1.341.30

1.34

1.42

1.32

1.381.34

1.26 1.251.25

1.11.21.21.31.31.41.41.51.5

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Novartis India

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 72: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Galvus Met Anti Diabetic 17.3 14.3 21 16.1 8

Voveran Pain 13.5 11.7 15 9.5 42

Rabipur (Novartis) Vaccines 8.4 8.9 -6 8.6 -3

Galvus Anti Diabetic 8.3 7.8 7 8.0 4

Otrivin Respiratory 5.5 5.0 9 5.8 -5

Tegrital Neuro 4.5 5.7 -21 4.1 9

Regestrone Gynaecological 3.2 3.5 -10 3.9 -19

Methergin Gynaecological 3.0 2.8 7 2.7 12

Genteal Ophthal 2.9 2.4 20 2.7 7

Calcium Sandoz Vitamins 2.1 2.1 2 1.5 41

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 73: Contribution of therapies to domestic sales (MAT April’15)

Anti Diabetic26%

Pain 19%

Respiratory12%

Vitamins 10%

Gynaecological8%

Other25%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 74: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Anti Diabetic 26.4 23.0 14.3 25.1 4.9

Pain 21.1 19.7 6.7 16.4 28.5

Respiratory 9.6 11.3 -14.8 10.6 -9.1

Vitamins 9.5 10.1 -6.0 8.2 15.6

Gynaecological 8.1 8.5 -4.7 8.5 -3.9

Vaccines 8.4 9.1 -7.9 8.7 -3.8

Neuro 7.3 8.7 -16.5 6.7 9.1

Anti-Infectives 4.4 4.1 7.3 3.9 15.1

Ophthal 3.3 2.9 15.7 3.1 8.3

Cardiac 1.1 1.4 -24.3 1.0 4.9

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 752.4, 64%

Chronic, 415.6, 36%

Brands contribution to domestic sales (MAT April’15)

65%

15%

7%

6%7%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 22

Unichem Laboratories

Stock Performance

70100130160

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Unichem Labs

Source: NSE, ICICIdirect.com Research

Exhibit 75: Company growth vis-à-vis Indian pharma market growth

8.0 12

.1 13.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

6.5

16.9

10.3 13

.9

13.0

13.8

-15.

9

2.9

3.8 6.6

13.6 16

.7 12.7

-20

-15

-10

-5

0

5

10

15

20

25

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Unichem Laboratories

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 76: Market share in Indian formulations market

0.98 1.00

0.930.97

0.90

0.97

0.85

0.95 0.940.98

0.95 0.95

0.97

0.80

0.90

1.00

1.10

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Unichem Laboratories

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 77: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Losar H Cardiac 7.5 6.4 17 7.6 -2

Ampoxin Anti-Infectives 6.9 4.8 44 6.1 14

Unienzyme Gastro Intestinal 6.4 5.1 26 6.8 -6

Losar Cardiac 5.8 4.9 19 5.3 9

Vizylac Gastro Intestinal 3.3 2.5 29 2.9 12

Trika Neuro 2.5 2.1 18 2.6 -3

Serta Neuro 1.7 1.8 -4 1.9 -12

Telsar Cardiac 1.6 1.7 -10 1.3 20

Unistar (Unichem) Cardiac 1.5 1.4 3 1.3 11

Arkamin Cardiac 1.2 0.9 38 1.2 5

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 78: Contribution of therapies to domestic sales (MAT April’15)

Cardiac42%

Anti-Infectives18%

Gastro Intestinal13%

Neuro 12%

Pain 4% Other

11%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 79: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Cardiac 31.6 30.4 3.9 30.0 5.3

Anti-Infectives 13.4 10.6 26.4 12.1 10.8

Gastro Intestinal 11.3 8.7 29.6 11.1 1.4

Neuro 9.4 8.4 11.7 9.3 1.0

Pain 2.8 2.3 18.4 2.3 18.3

Anti Diabetic 2.4 2.5 -6.1 2.1 14.6

Respiratory 1.8 1.6 13.8 1.9 -2.2

Vitamins 2.0 1.3 48.1 1.7 15.1

Derma 1.1 1.1 1.0 1.0 12.5

Gynaecological 0.4 0.5 -22.9 0.3 12.0

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 357.3, 43%

Chronic, 477.1, 57%

Brands contribution to domestic sales (MAT April’15)

48%

13%

10%

11%

18%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 23

Indoco Remedies

Stock Performance

80

180

280

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Indoco

Source: NSE, ICICIdirect.com Research

Exhibit 80: Company growth vis-à-vis Indian pharma market growth

8.0

12.1 13

.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

11.7

19.0

19.0

8.5

17.5

34.4

6.1

2.8

4.8

8.6 8.9

18.9

22.0

0

5

10

15

20

25

30

35

40

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indian Pharma Market Indoco Remedies

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 81: Market share in Indian formulations market

0.8

0.70.8 0.8

0.8

0.9

0.8

0.70.7

0.70.8

0.7

0.70.70.70.80.80.80.80.80.90.9

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

(%)

Indoco Remedies

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 82: Top 10 brands performance (| crore) Brand Therapy Apr'15 Apr'14 Var. (%) Mar'15 Var. (%)

Febrex Plus Respiratory 5.8 5.6 3 6.2 -7

Cyclopam Gastro Intestinal 3.5 3.6 -3 3.1 16

Cital Urology 3.2 2.8 12 2.6 20

Sensodent-K Stomatologicals 3.1 3.1 0 3.2 -5

Oxipod Anti-Infectives 2.5 2.3 5 2.5 -2

Atm Anti-Infectives 2.1 1.9 10 2.3 -10

Sensodent-Kf Stomatologicals 1.8 1.4 23 1.8 -2

Cloben G Derma 1.7 1.6 5 1.3 26

Cyclopam Gastro Intestinal 1.7 1.6 4 1.5 12

Sensoform Stomatologicals 1.7 1.6 5 1.8 -8

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 83: Contribution of therapies to domestic sales (MAT April’15) Respiratory

19%

Stomatologicals17%

Anti-Infectives16%

Gastro Intestinal14%

Vitamins 6%

Other28%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 84: Therapy wise performance (| crore)

Therapy Apr'15 Apr'14 YoY (%) Mar'15 QoQ (%)

Respiratory 9.1 9.3 -2.6 11.0 -17.7

Stomatologicals 9.4 8.5 9.8 9.4 -0.5

Anti-Infectives 8.4 8.3 1.3 8.8 -4.3

Gastro Intestinal 7.9 8.3 -3.8 7.1 12.0

Vitamins 3.4 2.6 29.8 3.1 7.7

Urology 3.4 3.0 12.8 2.8 19.6

Pain 2.1 2.5 -14.9 2.1 1.5

Derma 2.3 2.1 7.1 1.9 20.2

Anti Diabetic 1.9 2.2 -13.7 1.9 4.7

Ophthal 2.2 1.9 17.4 1.9 17.4

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (MAT April’15)

Acute, 622.1, 93%

Chronic, 45.2, 7%

Brands contribution to domestic sales (MAT April’15)

48%

17%

8%

10%

17%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 24

Ajanta Pharma

Stock Performance

50100150200250300350400

May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15

CNX Pharma Ajanta

Source: NSE, ICICIdirect.com Research

Exhibit 85: Company growth vis-à-vis Indian pharma market growth

8.0 12

.1 13.9

10.7

11.4

20.8

7.6

12.2 14

.8

13.5

19.6 21

.5

17.2

39.6

44.8

41.5

33.1

45.6

27.5

36.0

23.2

19.9

14.6 16.2

15.4

10.1

05