Embed Size (px)

Citation preview

Q3 2017 Business Result

Q3 2017 business result is prepared for investors’ consideration only before

completion of independent auditors’ review. Therefore, parts of contents on this

material could be changeable during independent auditors’ review.

1

Contents

I. YTD Q3 2017 Review

II. Market analysis

III. Performance analysis

IV. Financials

- Income Statement

V. Way Forward

2

• Steady SUV market growth in domestic

and overseas market

- Domestic market

· Total market : + 1.5%

· SUV market : +2.9% due to SUV-B & E

segment growth

- Overseas market

· Growth in Europe & China

• Strengthening competition in domestic

and overseas market

- Domestic market

· Two new models’ launch of competitors in

SUV-B market

- Overseas market

· Intensified competition to emerging markets

YTD Q3 2017 Review

SYMC

vehicle sales

• Total vehicle sales decrease : 4.5%

- Dom. : +8.0% with steady sales increase

- Exp. : -29.0% with continued sluggish sales

· However, gradual vehicle sales increase

due to G4 Rexton export in Aug.

· Q3 2017 : +41.9% vs. Q2 2017

• G4 Rexton vehicle sales

- Vehicle sales increase after launch in May

- Total : 6,235 units in Q3 2017

(+100.5% vs. Rexton in Q3 2016)

- Dom. : 4,572 units in Q3 2017

(+313.4% vs. Rexton in Q3 2016)

• Tivoli vehicle sales

- Dom. (YTD Q3 2017) : +3.9% (yoy)

· Modest vehicle sales growth in spite of

new competitors

Market

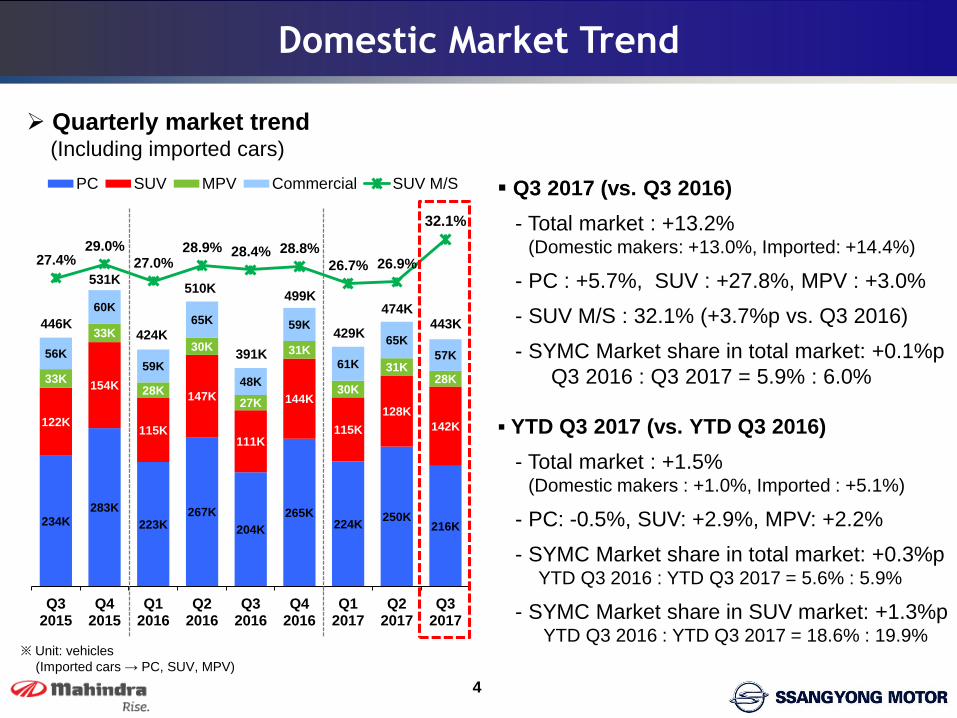

Quarterly market trend(Including imported cars)

Domestic Market Trend

4

234K283K

223K267K

204K

265K224K

250K216K

122K

154K

115K

147K

111K

144K

115K

128K

142K

33K

33K

28K

30K

27K

31K

30K

31K28K

56K

60K

59K

65K

48K

59K

61K

65K

57K

27.4%29.0%

27.0%28.9% 28.4% 28.8%

26.7% 26.9%

32.1%

Q32015

Q42015

Q12016

Q22016

Q32016

Q42016

Q12017

Q22017

Q32017

PC SUV MPV Commercial SUV M/S Q3 2017 (vs. Q3 2016)

- Total market : +13.2%(Domestic makers: +13.0%, Imported: +14.4%)

- PC : +5.7%, SUV : +27.8%, MPV : +3.0%

- SUV M/S : 32.1% (+3.7%p vs. Q3 2016)

- SYMC Market share in total market: +0.1%p

Q3 2016 : Q3 2017 = 5.9% : 6.0%

※ Unit: vehicles

(Imported cars → PC, SUV, MPV)

446K

531K

424K

510K

391K

499K

429K

474K

YTD Q3 2017 (vs. YTD Q3 2016)

- Total market : +1.5%(Domestic makers : +1.0%, Imported : +5.1%)

- PC: -0.5%, SUV: +2.9%, MPV: +2.2%

- SYMC Market share in total market: +0.3%pYTD Q3 2016 : YTD Q3 2017 = 5.6% : 5.9%

- SYMC Market share in SUV market: +1.3%pYTD Q3 2016 : YTD Q3 2017 = 18.6% : 19.9%

443K

0

50

100

150

200

250

300

350

YTD Q3 2016 YTD Q3 2017

22K 29K

125K 118K

87K 71K

71K 98K

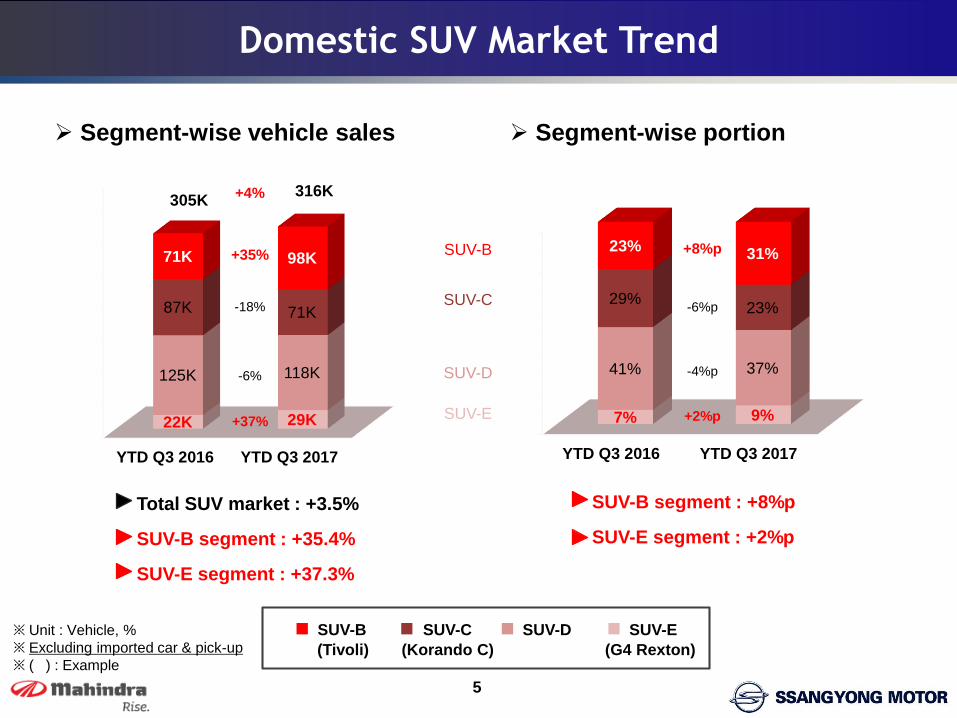

Domestic SUV Market Trend

5

※ Unit : Vehicle, %

※ Excluding imported car & pick-up

※ ( ) : Example

Segment-wise vehicle sales

SUV-B SUV-C SUV-D SUV-E

Total SUV market : +3.5%

SUV-B segment : +35.4%

SUV-E segment : +37.3%

305K316K

(Tivoli) (Korando C) (G4 Rexton)

-6%

+37%

-18%

+4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

YTD Q3 2016 YTD Q3 2017

7% 9%

41% 37%

29%23%

23%31%

Segment-wise portion

SUV-B segment : +8%p

SUV-E segment : +2%p

-4%p

+2%p

-6%p

+8%p+35% SUV-B

SUV-C

SUV-D

SUV-E

Overseas Market Trend

6

Others

※ Unit : Vehicle

※ Source : Automotive News, Makrlines

※ Excluding commercial vehicles

※ ( ) : SUV portion out of total market

Europe (28 Countries)

6,399K

6,388K

2,847K

2,463K

914K

945K

Jan.~Aug.2017

Jan.~Aug.2016

China

Russia

10,063K

10,470K

- Total market : +4.0%

- SUV market : +15.6%

7,101K

7,273K

5,990K

5,067K

1,323K

1,562K

Jan.~Aug.2017

Jan.~Aug.2016

- Total market : +2.6%

- SUV market : +18.2%

482K

471K

400K

329K

26K

25K

Jan.~Aug.2017

Jan.~Aug.2016

- Total market : +9.6%

- SUV market : +21.3%

PC SUV MPVOthers

(US Pick-up)

895K

981K

14,596K

14,978K

(24.5%)

(27.2%)

(36.8%)

(40.7%)

(34.7%)

(40.0%)

4,119K

4,687K

4,671K

4,439K

1,805K

1,742K

Jan.~Aug.2017

Jan.~Aug.2016

USA

11,359K

11,034K

(42.3%)

(39.1%)

- Total market : -2.9%

- SUV market : +5.2%

SYMC Sales Volume in Q3 2017

7

23,233 26,378

13,873 9,928

Q3 2016 Q3 2017

37,106 36,306

-28%

+14%

-2%

(37%)

(63%)

(27%)

(73%)

Sales volume decrease

- Total Sales : -800 units (-2%)

· Domestic : +3,145 units (+14%)

· Export : -3,945 units (-28%)

Domestic portion increase : +10%p

- Q3 2016 : Q3 2017 = 63% : 73%

G4 Rexton

- A leading SUV model in domestic SUV-E segment

(Market share of 47% in Q3 2017)

- Q3 2017 Total 6,235 units : +100% (vs. Q3 2016)Domestic Export

※ Unit: vehicle (including CKD)

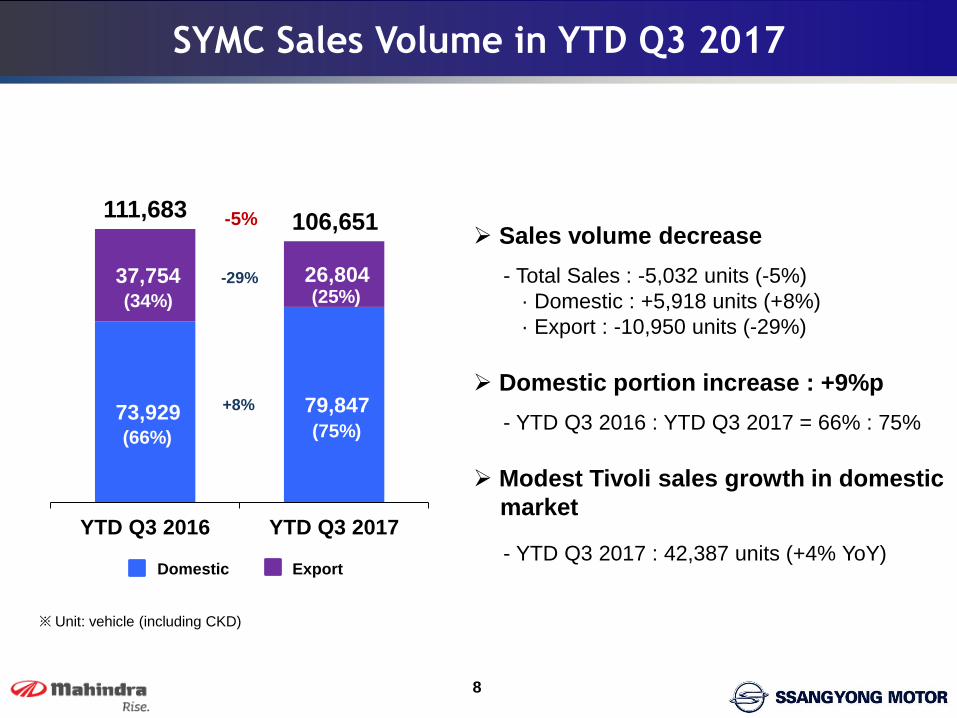

SYMC Sales Volume in YTD Q3 2017

8

73,929 79,847

37,754 26,804

YTD Q3 2016 YTD Q3 2017

111,683106,651

-29%

+8%

-5%

※ Unit: vehicle (including CKD)

(34%)

(66%)

(25%)

(75%)

Sales volume decrease

- Total Sales : -5,032 units (-5%)

· Domestic : +5,918 units (+8%)

· Export : -10,950 units (-29%)

Domestic portion increase : +9%p

- YTD Q3 2016 : YTD Q3 2017 = 66% : 75%

Modest Tivoli sales growth in domestic

market

- YTD Q3 2017 : 42,387 units (+4% YoY)Domestic Export

Region-wise Export Portion in YTD Q3 2017

W. Europe

Asia Pacific

※ % out of export sales volume

(Including CKD)

Others

South America

44%

49%

9%5%

21%26%

20%

26%

YTD Q3

2016

YTD Q3

2017

YTD Q3

2016

YTD Q3

2017

YTD Q3

2016YTD Q3

2017

YTD Q3

2016

YTD Q3

2017

※ Including: China

9

※ Others: ME, AF, E. Europe

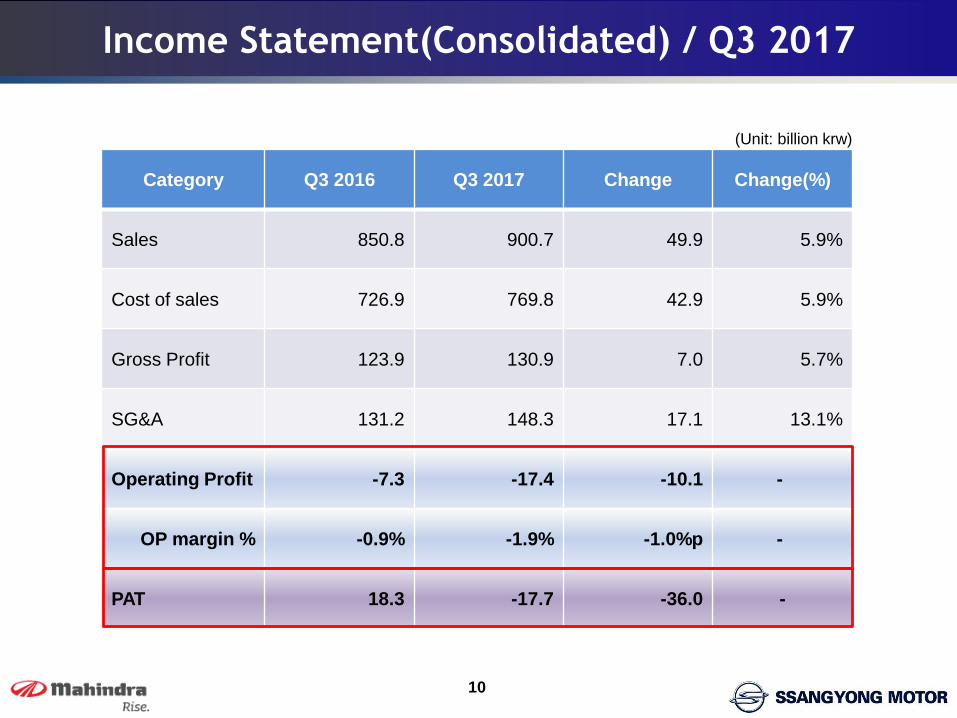

Income Statement(Consolidated) / Q3 2017

Category Q3 2016 Q3 2017 Change Change(%)

Sales 850.8 900.7 49.9 5.9%

Cost of sales 726.9 769.8 42.9 5.9%

Gross Profit 123.9 130.9 7.0 5.7%

SG&A 131.2 148.3 17.1 13.1%

Operating Profit -7.3 -17.4 -10.1 -

OP margin % -0.9% -1.9% -1.0%p -

PAT 18.3 -17.7 -36.0 -

(Unit: billion krw)

10

Operating Costs / Q3 2017

Q3 2016 Q3 2017

+0.1%p

Cost of sales (%) SG&A expense (%)

15.4%

16.5%

※ (Cost of Sales/Sales)*100 ※ (SG&A expenses/Sales)*100

Q3 2016 Q3 2017

11

85.4% 85.5%

+1.1%p

Income Statement(Consolidated) / YTD Q3 2017

Category YTD Q3 2016 YTD Q3 2017 Change Change(%)

Sales 2,627.9 2,592.5 -35.4 -1.3%

Cost of sales 2,196.4 2,198.1 1.7 0.1%

Gross Profit 431.5 394.4 -37.1 -8.6%

SG&A 411.5 434.0 22.5 5.5%

Operating Profit 20.0 -39.5 -59.5 -

OP margin % 0.8% -1.5% -2.3%p -

PAT 38.7 -35.6 -74.3 -

(Unit: billion krw)

12

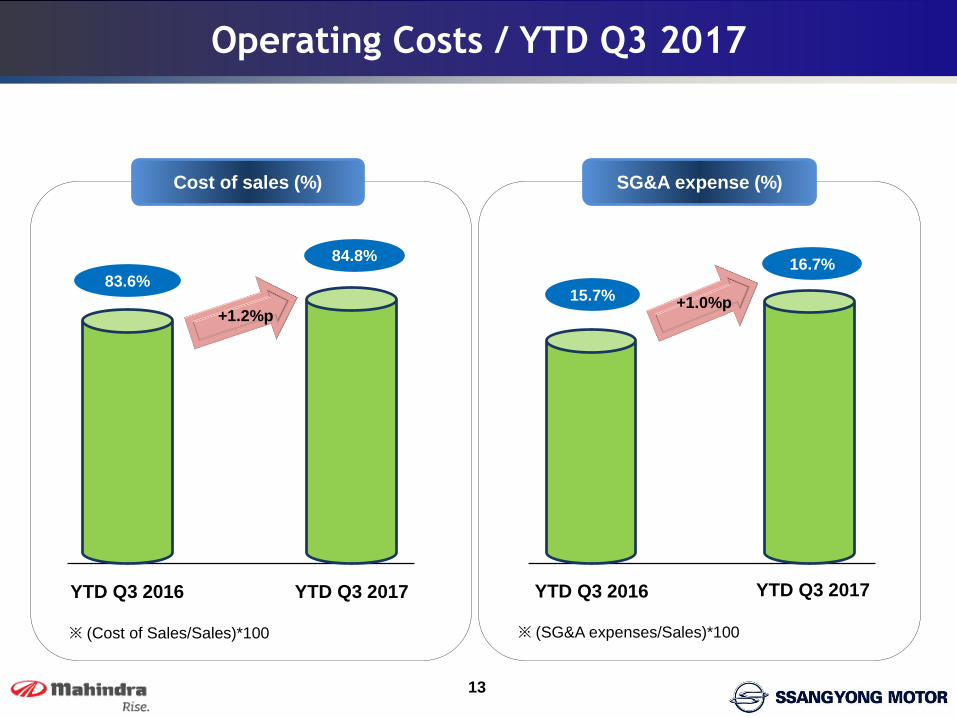

Operating Costs / YTD Q3 2017

YTD Q3 2016 YTD Q3 2017

Cost of sales (%) SG&A expense (%)

15.7%

16.7%

※ (Cost of Sales/Sales)*100 ※ (SG&A expenses/Sales)*100

YTD Q3 2016 YTD Q3 2017

13

83.6%

84.8%

+1.2%p+1.0%p

14

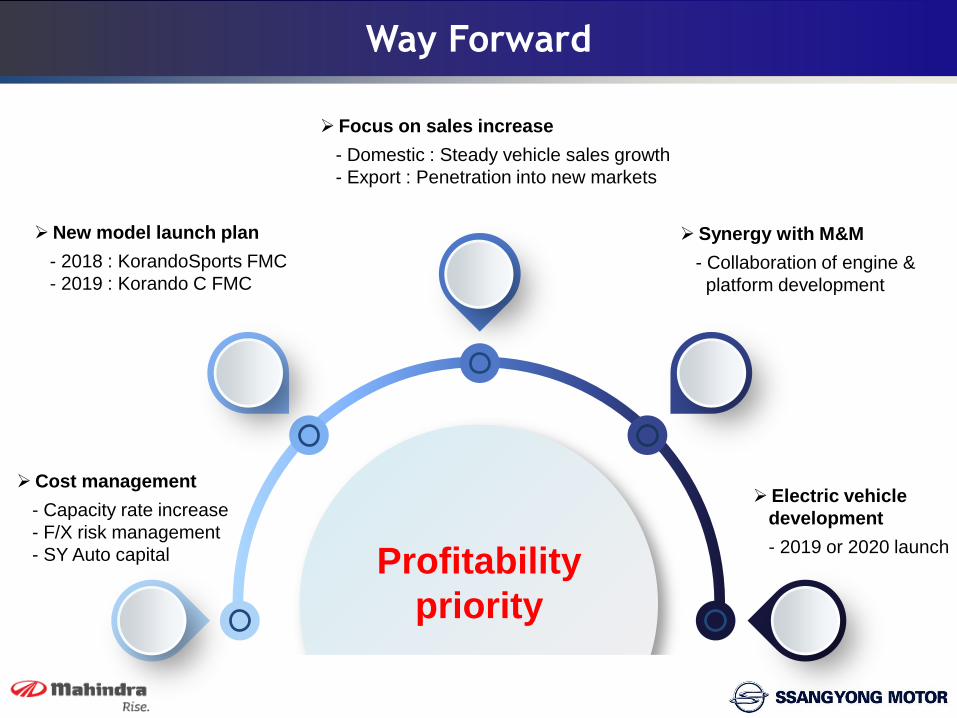

Way Forward

Profitability

priority

Cost management

- Capacity rate increase

- F/X risk management

- SY Auto capital

New model launch plan

- 2018 : KorandoSports FMC

- 2019 : Korando C FMC

Focus on sales increase

- Domestic : Steady vehicle sales growth

- Export : Penetration into new markets

Synergy with M&M

- Collaboration of engine &

platform development

Electric vehicle

development

- 2019 or 2020 launch

![Announces Standalone Q3 results & Limited Review Report for the Quarter ended December 31, 2015 [Result]](https://img.pdfslide.us/doc/110x75/577ca5d61a28abea748bab92/announces-standalone-q3-results-limited-review-report-for-the-quarter-ended.jpg)

![Announces Q3 Results (Standalone) for the Quarter ended December 31, 2015 [Result]](https://img.pdfslide.us/doc/110x75/577c87b61a28abe054c4d771/announces-q3-results-standalone-for-the-quarter-ended-december-31-2015-result.jpg)

![Information Update on the Unaudited Financial Results Q3 2015-16 [Result]](https://img.pdfslide.us/doc/110x75/577ca59a1a28abea748b99ce/information-update-on-the-unaudited-financial-results-q3-2015-16-result.jpg)

![Announces Q3 results [Result]](https://img.pdfslide.us/doc/110x75/577ca58e1a28abea748b9591/announces-q3-results-result.jpg)

![Announces Q3 results & Limited Review Report for the quarter ended December 31, 2015 [Result]](https://img.pdfslide.us/doc/110x75/577ca61e1a28abea748bc3ff/announces-q3-results-limited-review-report-for-the-quarter-ended-december.jpg)