Embed Size (px)

Citation preview

Henry C. Newell President and Chief Executive Officer Sherri L. Lemmer Senior Vice President and Chief Financial Officer Perry D. Grueber Director Investor Relations

Q3 2013 Conference Call October 29, 2013

Forward Looking Statements

The matters discussed in this news release concerning the company’s future performance or

anticipated financial results are forward-looking statements and are made pursuant to the safe

harbor provisions of the Private Securities Litigation Reform Act of 1995. Such statements involve

risks and uncertainties which may cause results to differ materially from those set forth in these

statements. Among other things, these risks and uncertainties include the strength of the

economy and demand for paper products, increases in raw material and energy prices,

manufacturing problems at company facilities, and other risks and assumptions described under

“Information Concerning Forward-Looking Statements” in Item 7 and in Item 1A of the company’s

Form 10-K for the year ended December 31, 2012. The company assumes no obligation to update

or supplement forward-looking statements that become untrue because of subsequent events.

Non-GAAP Financial Measures This presentation refers to certain non-U.S. GAAP financial measures. A reconciliation of those

numbers to U.S. GAAP financial measures is provided on the Company's website at:

www.wausaupaper.com/investors.

2 Q3 2013 Earnings Call

Q3 2013 Earnings Call 3

Our First Quarter as a

Tissue Company

Hank Newell President and CEO

Wausau Paper Transformation over the Last Twenty-Four Months

Q3 2013 Earnings Call 4

Strategic Repositioning

• Divested Premium Print & Color Brands

• Divested Timberlands

• Shut Brokaw and Brainerd Operations

• Divested Specialty Paper Business

Tissue Expansion

• Repositioned EcoSoft™ Brand

• Executed Largest Capital Expansion in Company History

• Launched DublNature® Brand (ATMOS)

• Grew Tissue Volume 2-3x Market

Organization

• New CEO, CFO, Tissue SVP & GM

• New Chairman, Five New Board Members

• Reduction & Realignment of Salaried Staffing

• New Enterprise Information Technology Platform

Third Quarter Highlights

• First quarter as Tissue only company

• Case volume up 7.4%, Revenue up 5.6%

• EBITDA margins* continue to expand Q1 7.6% Q2 10.1% Q3 11.5%

• Demonstrated solid progress ramping up and optimizing operations

• Announced policy to return approximately 50% of free cash to shareholders

Q3 2013 Earnings Call 5

* Represents Adjusted EBITDA margins. See Appendix for reconciliation of Adjusted EBITDA margins

Our Near-Term Focus

• Deliver Volume Growth at Target Margins

• Ramp up and Optimize Operations Platform

• Demonstrate Free Cash Flow Growth

• Increase Return of Cash to Shareholders

Q3 2013 Earnings Call 6

Deliver Volume Growth at Target Margins

• +6% volume CAGR is expectation over next 4-5 years

• Strong market acceptance of DublNature® premium products

• ≈46% of our volume “new” as result of EcoSoft™ repositioning and DublNature® premium product launch

• Further product introductions and new proprietary dispenser technology are in near-term pipeline

Q3 2013 Earnings Call 7

Building a Powerful Operational Platform

Major investments completed, now ramping up paper machine and optimizing operations platform:

• New Towel & Tissue machine in Harrodsburg

• Nine converting line retrofits for large scale parent rolls

• Eight premium converting line upgrades

• One new proprietary converting line in startup

• Major shift in distribution scale

Q3 2013 Earnings Call 8

Source of Significant Improvement

Ramping Up the New “ATMOS” Machine

0

10,000

20,000

Q4 12 Q1 13 Q2 13 Q3 13 Q413F

Q4 14Target

Conventional Premium (ATMOS)

Q3 2013 Earnings Call 9

• Flexible asset produces towel & tissue in conventional or ATMOS modes

• Conventional mode achieving cost structure and displacing higher cost purchased parent rolls

• ATMOS mode producing DublNature® premium products and progressing on ramp up curve

• Excellent quality and market acceptance of DublNature® premium products

• ATMOS product qualification • Inventory build

Tons

Realignment & Reduction of Staffing

Q3 2013 Earnings Call 10

569

347

271-195 -27

-76

0

200

400

600

January 2013 PaperDivestiture

BrainerdClosure

Post Paper Realignment/ Reduction

Goal

• 55% corporate, 22% overall salaried staffing reduction (Post Paper); approaching 20% by year end

• Operating functions consolidated in Kentucky; support functions in Wisconsin

• As company delivers growth targeting SG&A as 10-11% of sales; well-below relevant competitors

# A

uth

ori

zed

Sal

arie

d P

osi

tio

ns

22% Reduction

Capital Allocation

• Support organic growth needs to deliver EBITDA and ROCE commitments

• Targeting a leverage ratio of ≈2.5x total Debt / LTM EBITDA

• No major capital expansion in current plan; opportunistic acquisitions focused on capability or geography with strict return criteria

• Return of cash to shareholders through a growing dividend and/or share repurchase is a priority

Q3 2013 Earnings Call 11

4.9x4.3x 3.8x-4.0x

2.1x-2.3x

Q2 13 Q3 13 Q4 13F Q4 14F

Target ≈ 2.5

Total Debt / LTM EBITDA*

≈$10≈$15

≈$25

Maintenance Capital Growth Capital Dispenser Subsidy

2014F Uses of Cash$MM

Guidance * Continuing Operations

FINANCIAL REVIEW

Sherri Lemmer

12 Q3 2013 Earnings Call

2013 Q3 RESULTS

13 Q3 2013 Earnings Call

Financial Overview Sales Volume

Q3 2013 Earnings Call 14

Market growth is estimate based on industry sources and management estimates

Case Growth

2013 • Q4 Target +6% • Full Year +4-5%

2012 • Q4 +4.0% • Full Year +3.3%

Market Growth ≈1.5%

3.77

4.11 4.06 4.09

3.77

4.214.36

Q1 Q2 Q3 Q4 Q1 Q2 Q3

Case Shipments (MM) With % of Strategic Mix

2012 2013

49.2% 48.3% 48.5%

50.1% 47.6% 47.4%

48.4%

+7.4%

$81.9 $88.6 $86.8

$78.2 $87.6

$91.7

$0

$50

$100

$150

Q1 Q2 Q3

2012 2013

Financial Overview Net Sales

Q3 2013 Earnings Call 15

See Appendix for reclassification of Net Sales for Continuing Operations

Net Sales Continuing Operations

• Record Quarterly Sales

• Q3 +5.6% to prior year

• Nine-month Net Sales

• 2013 $257.5MM

• 2012 $257.2MM

($MM)

Financial Overview Adjusted EBITDA

Q3 2013 Earnings Call 16

• 2013 Quarter-over-Quarter Improvement

• +3.6% Sales Volume

• Improved Strategic Mix

• Increased Operating Efficiencies

• Increased Cost in Quarter Related to Realignment and Reduction Efforts

Adjusted EBITDA and EBITDA margin are non-GAAP measures. See Appendix for reconciliation of EBITDA to Adjusted EBITDA

$5.9

$8.8

$10.6 $1.3

$2.9

($2.4)

Q1 Q2 Q3 Deliver Growth

Optimize Operations

Repositioning & Other

($MM)

7.6%

10.1% 11.5%

2013 Adjusted EBITDA and EBITDA Margin Continuing Operations

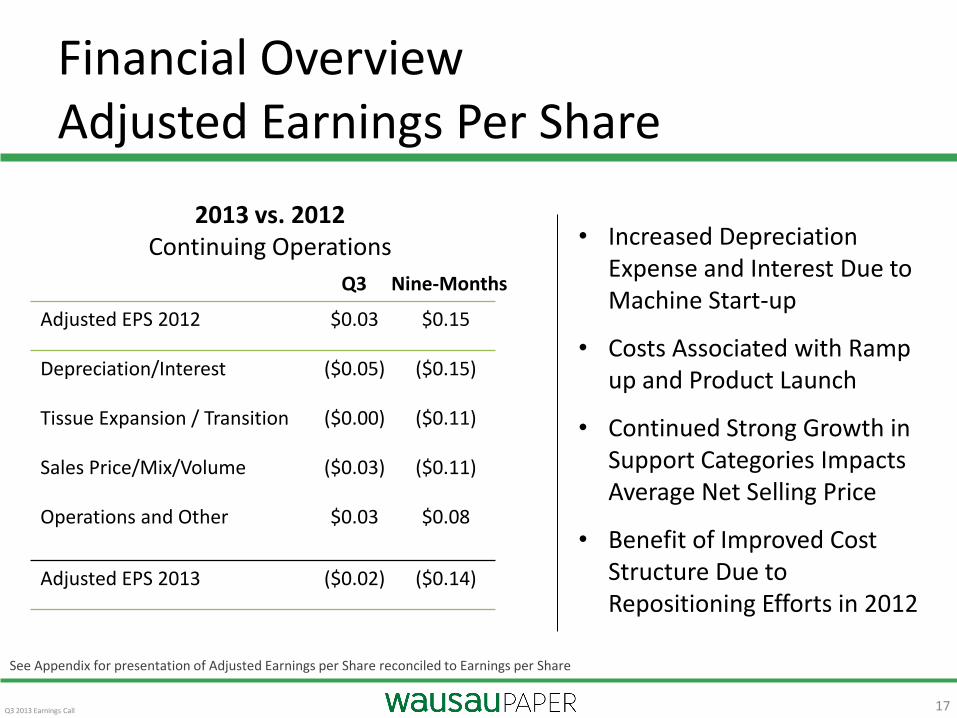

Financial Overview Adjusted Earnings Per Share

Q3 2013 Earnings Call 17

See Appendix for presentation of Adjusted Earnings per Share reconciled to Earnings per Share

2013 vs. 2012 Continuing Operations

Adjusted EPS 2012 $0.03 $0.15

Depreciation/Interest ($0.05) ($0.15)

Tissue Expansion / Transition ($0.00) ($0.11)

Sales Price/Mix/Volume ($0.03) ($0.11)

Operations and Other $0.03 $0.08

Adjusted EPS 2013 ($0.02) ($0.14)

Q3 Nine-Months

• Increased Depreciation Expense and Interest Due to Machine Start-up

• Costs Associated with Ramp up and Product Launch

• Continued Strong Growth in Support Categories Impacts Average Net Selling Price

• Benefit of Improved Cost Structure Due to Repositioning Efforts in 2012

Debt

• Credit Capacity

• $200MM under Unsecured Private Shelf Agreement (First Maturity June 2016)

• $100MM under Unsecured Bank Credit Facility (Expires June 2014)

• Cost Effective Structure

• Current Cost of Debt ≈ 5.1%

18 Q2 2013 Earnings Call

12/31/12 Net Debt* 9/30/13

9/30/13

(1) EBITDA is a non-GAAP measure and represents continuing operations only. See Appendix for reconciliation and presentation of LTM EBITDA (2) This calculation of Total Debt / Capital is not intended to be used for purposes of calculating debt covenant compliance *Net of $25.4MM in cash & cash equivalents

$196

$150$125

Quarterly Debt ($MM)

As of 9/30/13 Total Debt / LTM EBITDA(1) 4.3x Total Debt / Capital(2) 51.7%

Outlook

Q4 2013F Q4 2014F FY 2014F

Case Growth +6% +6% +6%

EBITDA $13-$15MM $20-$24MM $65-$70MM

EBITDA % 14-16% 20-24% 17-19%

Net EPS $0.01-$0.03 $0.10-$0.13 $0.21-$0.28

Q3 2013 Earnings Call 19

Q4 2014F EBITDA* Bridge

Q3 2013 Earnings Call 20

$5.9$8.8

$10.6

$13-$15

$20-$24$2

$2

$6

($2)

Q1 Q2 Q4F Q3 Q4F

PM3 Startup

Initial Launch

Launch & Optimize

2013 2014

Deliver Growth • Volume (Cases) • Strategic Mix

Optimize Operations

Input Costs

($MM)

* EBITDA is a non-GAAP measure and represents continuing operations only. See Appendix for reconciliation of EBITDA to Adjusted EBITDA

2014 First Half Impacts

• Demand Seasonality (Q1)

• Maintenance Outage (Q2)

• Artisan™ Product Trials / Launch

Q3 2013 Earnings Call 21

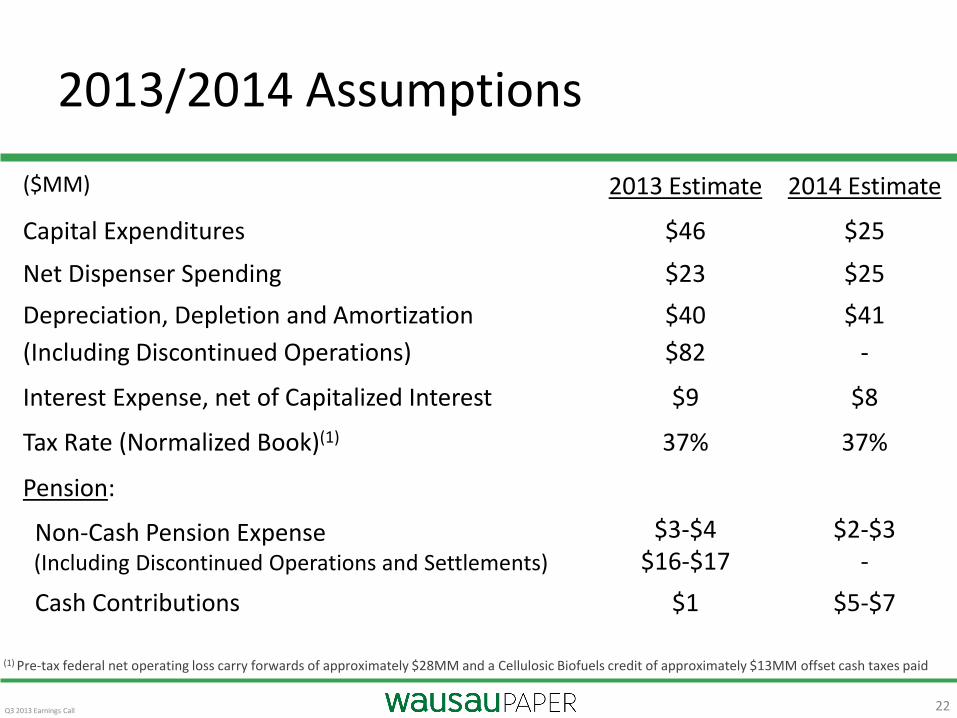

2013/2014 Assumptions

($MM) 2013 Estimate 2014 Estimate

Capital Expenditures $46 $25

Net Dispenser Spending $23 $25

Depreciation, Depletion and Amortization

(Including Discontinued Operations)

$40

$82

$41

-

Interest Expense, net of Capitalized Interest $9 $8

Tax Rate (Normalized Book)(1) 37% 37%

Pension:

Non-Cash Pension Expense (Including Discontinued Operations and Settlements)

$3-$4 $16-$17

$2-$3 -

Cash Contributions $1 $5-$7

22 Q3 2013 Earnings Call

(1) Pre-tax federal net operating loss carry forwards of approximately $28MM and a Cellulosic Biofuels credit of approximately $13MM offset cash taxes paid

Longer-Term View

Q3 2013 Earnings Call 23

• Well-positioned for significant earnings expansion and cash flow growth

• We have previously provided EBITDA guidance of ≈$140MM by 2017. Our outlook has not changed, but any long-term forecast has uncertainties

• Our improvement in earnings and cash flow is a ramp up curve and that improvement will not be in a straight line

• Macro factors such as fiber are expected to be offset by product pricing over time in our long-term outlook, but there will be lags in timing

$0

$25

$50

$75

$100

2013F 2014F Q4 2014FAnnualized

$38-$40

$65-$70

$80-$96

Overall Solid Progress on Path to Achieving our Objectives

Adjusted EBITDA Continuing Operations

($MM)

Summary

• A 100% Tissue company uniquely positioned to grow and deliver value

• Excellent third quarter progress delivering volume growth and margin expansion

• Return of cash to our shareholders is a priority

Q3 2013 Earnings Call 24

Q&A

25 Q3 2013 Earnings Call

26

Upcoming Events: Bank of America US Basic Materials Conference Boston, Massachusetts Wednesday, December 11, 2013 Q4 2013 Earnings Release - Monday, February 10, 2014 Next Investor and Analyst Conference Call - Tuesday, February 11, 2014

9 AM Central / 10 AM Eastern

Q3 2013 Earnings Call

APPENDIX

27 Q3 2013 Earnings Call

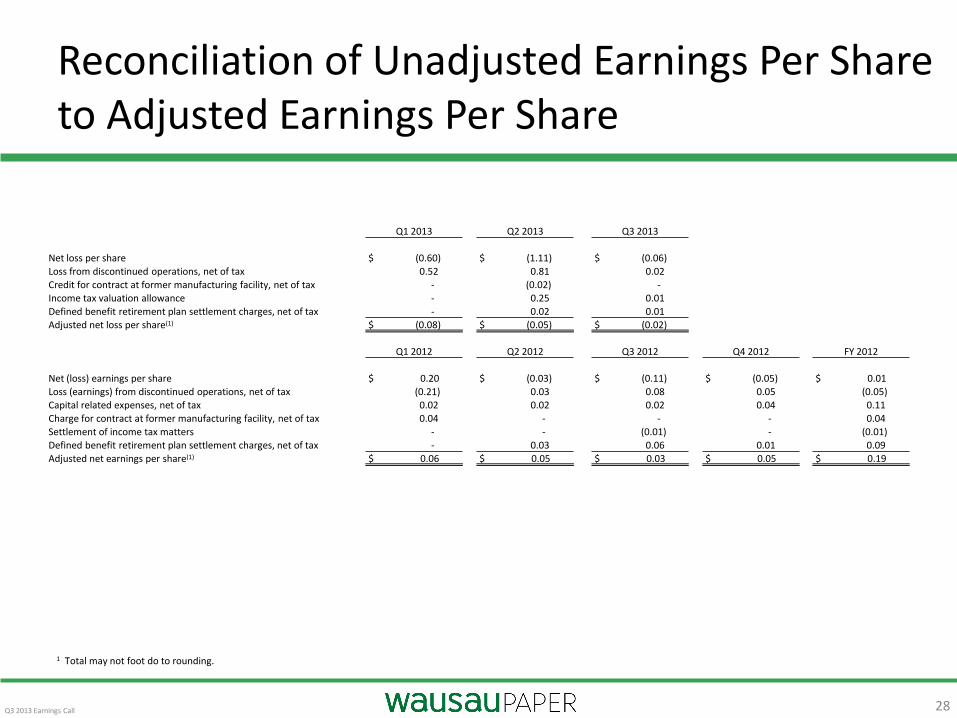

Reconciliation of Unadjusted Earnings Per Share to Adjusted Earnings Per Share

28

1 Total may not foot do to rounding.

Q3 2013 Earnings Call

Q1 2013 Q2 2013 Q3 2013

Net loss per share $ (0.60) $ (1.11) $ (0.06) Loss from discontinued operations, net of tax 0.52 0.81 0.02

Credit for contract at former manufacturing facility, net of tax - (0.02) -

Income tax valuation allowance - 0.25 0.01

Defined benefit retirement plan settlement charges, net of tax - 0.02 0.01 Adjusted net loss per share(1) $ (0.08) $ (0.05) $ (0.02)

Q1 2012 Q2 2012 Q3 2012 Q4 2012 FY 2012

Net (loss) earnings per share $ 0.20 $ (0.03) $ (0.11) $ (0.05) $ 0.01 Loss (earnings) from discontinued operations, net of tax (0.21) 0.03 0.08 0.05 (0.05) Capital related expenses, net of tax 0.02 0.02 0.02 0.04 0.11

Charge for contract at former manufacturing facility, net of tax 0.04 - - - 0.04

Settlement of income tax matters - - (0.01) - (0.01)

Defined benefit retirement plan settlement charges, net of tax - 0.03 0.06 0.01 0.09

Adjusted net earnings per share(1) $ 0.06 $ 0.05 $ 0.03 $ 0.05 $ 0.19

Reconciliation of Unadjusted EBITDA to Adjusted EBITDA

Q3 2013 Earnings Call 29

(in thousands) Q1 2013 Q2 2013 Q3 2013

Net loss $ (29,605) $ (54,826) $ (2,852)

Loss from discontinued operations, net of taxes 25,873 40,231 818

(Credit) provision for income taxes (2,420) 11,255 (132)

Interest expense and other, net 2,343 2,530 1,982

Operating loss (3,809) (810) (184)

Depreciation, depletion, and amortization 9,740 10,032 9,945

EBITDA $ 5,931 $ 9,222 $ 9,761

Net sales $ 78,193 $ 87,623 $ 91,663

EBITDA margin 7.6% 10.5% 10.6%

EBITDA $ 5,931 $ 9,222 $ 9,761

Capital related expenses - - -

Credit for contract at former manufacturing facility - (1,713)

Defined benefit retirement plan settlement charges 0 1,320 801

Adjusted EBITDA $ 5,931 $ 8,829 $ 10,562

Net sales $ 78,193 $ 87,623 $ 91,663

Adjusted EBITDA margin 7.6% 10.1% 11.5%

(in thousands) Q1 2012 Q2 2012 Q3 2012 Q4 2012 FY 2012

Net earnings (loss) $ 9,758 $ (1,315) $ (5,309) $ (2,458) $ 676

(Loss) earnings from discontinued operations, net of taxes (10,251) 1,614 3,708 2,691 (2,236)

(Credit) provision for income taxes (536) 709 (832) (23) (682)

Interest expense and other, net 735 1,000 661 985 3,381

Operating profit (loss) (294) 2,008 (1,772) 1,195 1,139

Depreciation, depletion, and amortization 7,201 7,285 7,410 8,677 30,573

EBITDA $ 6,907 $ 9,293 $ 5,638 $ 9,872 $ 31,712

Net sales $ 81,851 $ 88,559 $ 86,811 $ 86,961 $ 344,182

EBITDA margin 8.4% 10.5% 6.5% 11.4% 9.2%

EBITDA $ 6,907 $ 9,293 $ 5,638 $ 9,872 $ 31,712

Capital related expenses 1,923 1,498 1,947 2,985 8,353

Charge for contract at former manufacturing facility 3,324 - - - 3,324

Defined benefit retirement plan settlement charges - 2,240 4,388 519 7,147

Adjusted EBITDA $ 12,154 $ 13,031 $ 11,973 $ 13,376 $ 50,536

Net sales $ 81,851 $ 88,559 $ 86,811 $ 86,961 $ 344,182

Adjusted EBITDA margin 14.9% 14.7% 13.8% 15.4% 14.7%

Net Sales

30

Net Sales to Net Sales – Continuing Operations

Q1 12 Q2 12 Q3 12 Q4 12 2012 FY Q1 13

Consolidated Net Sales – As Reported $216.2 $ 212.9 $202.2 $190.9 $822.2 $188.0

Net Sales from Discontinued Operations (134.3) (124.3) (115.4) (103.9) (478.0) (109.8)

Consolidated Net Sales – Continuing Operations $81.9 $ 88.6 $86.8 $87.0 $344.2 $78.2

Q3 2013 Earnings Call