Embed Size (px)

Citation preview

energy.gov/sunshotNREL/PR-6A20-67246

Q2/Q3 2016 Solar Industry Update

David Feldman, NREL Daniel Boff, DOE Robert Margolis, NREL

October 11, 2016

energy.gov/sunshot

Executive Summary

2

• The United States installed 4.0 GWDC in H1 2016, a 47% increase from H1 2015 – 29.9 GWDC totalthrough H1 2016.

– While the top five states in H1 2016 are established markets, many new large markets areemerging, with 14 states installing more than 50 MW in H1 2016, including Utah, Georgia, andSouth Carolina.

– Emerging business practices are driving more solar deployment, such as Community Solar,Corporate PPA’s, and PURPA contracts.

• Analysts estimate that between 61 GW and 74 GW of PV will be installed globally in 2016 (53 GWwere installed in 2015).

– China installed 20 GW in H1 2016 in large part due to scheduled FiT change in H2 2016.• In Q2 2016, residential installation costs (excluding SG&A) for three of the leading firms in the

United States ranged from $2.07/W to $2.27/W.• After several years of relatively flat pricing, modules and components have begun a period of rapid

price declines.– Analysts have reported a significant drop in module pricing since July 2016, with module

quotes between $0.40/W–$0.50/W in the second half of 2016 and still falling – some in theindustry have seen quotes well below $0.40/W for 2017 delivery.

• Nine publically traded PV companies shipped a total of 9 GW in Q2 2016.– This is 12% more than Q1 2016 and 48% more than Q2 2015.

• U.S. module and cell manufacturers had the largest six months of production ever, caused in part byU.S. tariffs in place on Chinese modules and cells, and by a growing U.S. market.

– However, U.S. manufacturers may encounter increased competition due to the downwardmodule price pressure and the expansion of manufacturing capacityin countries not subject to U.S. tariffs.

energy.gov/sunshot

Agenda

3

• Global Deployment • U.S. Deployment • U.S. Pricing • Global Manufacturing • Component Pricing • Market Activity • Tax Credit Availability

energy.gov/sunshot

0

20

40

60

80

100

120

2011 2012 2013 2014 2015 2016P 2017P 2018P 2019P 2020P

PV A

nnua

l Ins

talla

tions

(GW

DC) Europe

ROWIndiaJapanChinaU.S.

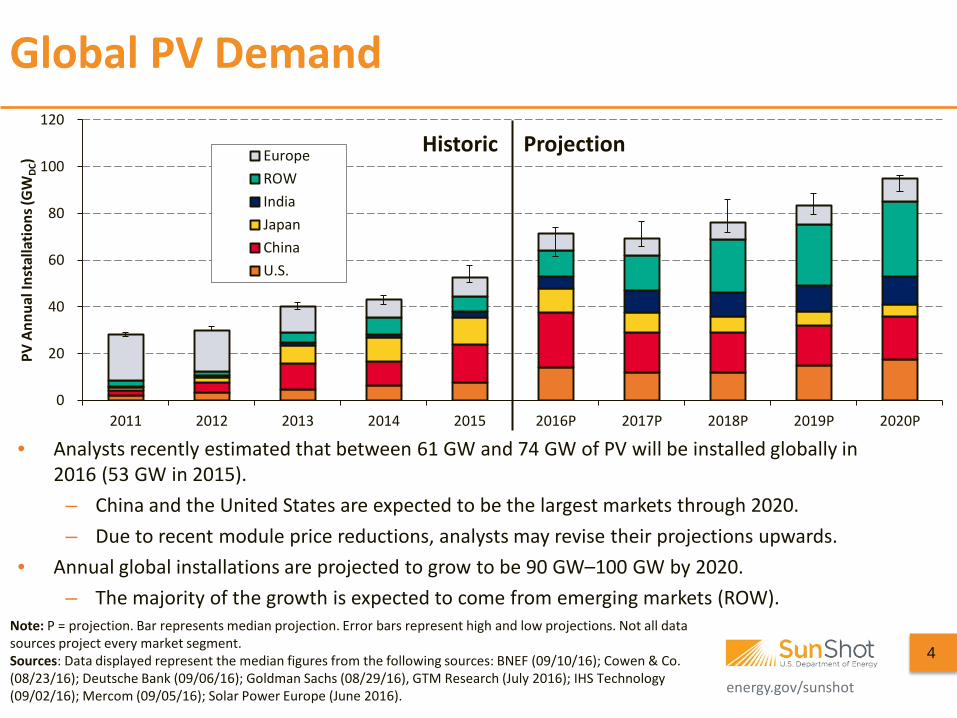

Global PV Demand

Historic Projection

• Analysts recently estimated that between 61 GW and 74 GW of PV will be installed globally in 2016 (53 GW in 2015).

– China and the United States are expected to be the largest markets through 2020. – Due to recent module price reductions, analysts may revise their projections upwards.

• Annual global installations are projected to grow to be 90 GW–100 GW by 2020. – The majority of the growth is expected to come from emerging markets (ROW).

4

Note: P = projection. Bar represents median projection. Error bars represent high and low projections. Not all data sources project every market segment. Sources: Data displayed represent the median figures from the following sources: BNEF (09/10/16); Cowen & Co. (08/23/16); Deutsche Bank (09/06/16); Goldman Sachs (08/29/16), GTM Research (July 2016); IHS Technology (09/02/16); Mercom (09/05/16); Solar Power Europe (June 2016).

energy.gov/sunshot

05

1015202530

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

China India Japan USA

Annu

al In

stal

latio

ns (G

W)

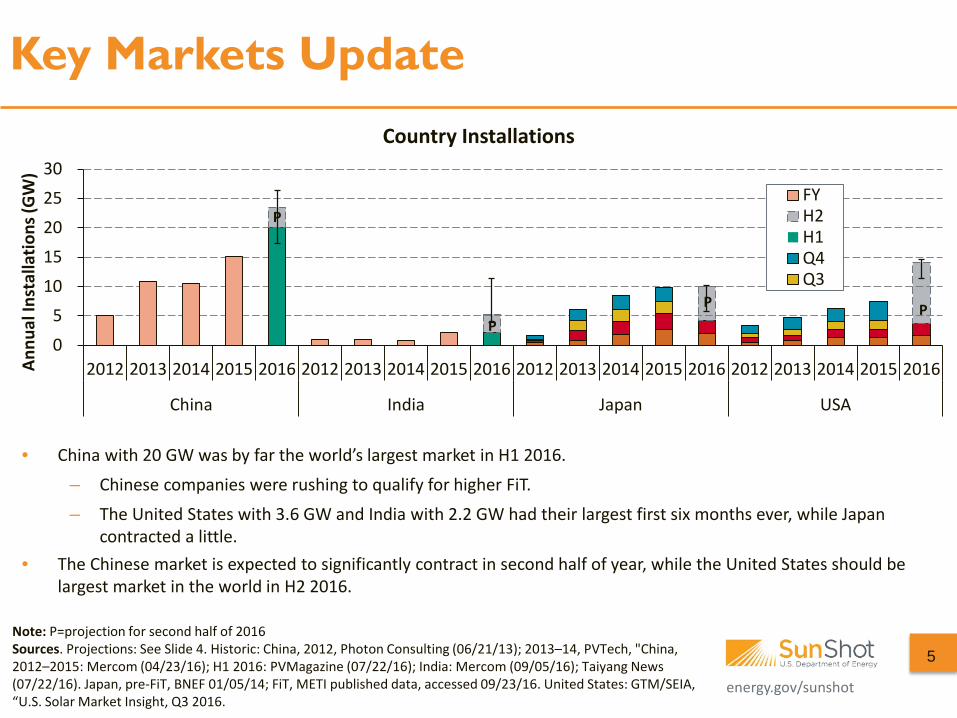

Country Installations

FYH2H1Q4Q3

Key Markets Update

Note: P=projection for second half of 2016 Sources. Projections: See Slide 4. Historic: China, 2012, Photon Consulting (06/21/13); 2013–14, PVTech, "China, 2012–2015: Mercom (04/23/16); H1 2016: PVMagazine (07/22/16); India: Mercom (09/05/16); Taiyang News (07/22/16). Japan, pre-FiT, BNEF 01/05/14; FiT, METI published data, accessed 09/23/16. United States: GTM/SEIA, “U.S. Solar Market Insight, Q3 2016.

5

• China with 20 GW was by far the world’s largest market in H1 2016.

– Chinese companies were rushing to qualify for higher FiT.

– The United States with 3.6 GW and India with 2.2 GW had their largest first six months ever, while Japan contracted a little.

• The Chinese market is expected to significantly contract in second half of year, while the United States should be largest market in the world in H2 2016.

P

P P P

energy.gov/sunshot

U.S.

Spain

Australia

6

Morocco Middle East

India

China

Chile

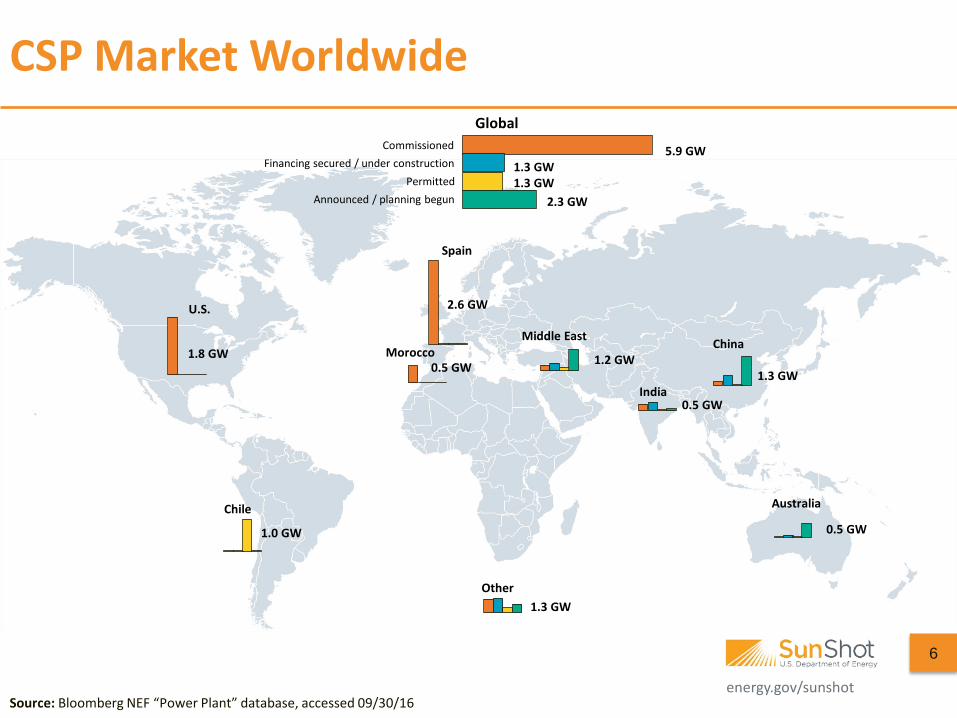

Global

Other

Commissioned Financing secured / under construction

Permitted Announced / planning begun

5.9 GW 1.3 GW 1.3 GW

2.3 GW

1.8 GW

1.0 GW

2.6 GW

0.5 GW 1.2 GW

0.5 GW

1.3 GW

0.5 GW

1.3 GW

Source: Bloomberg NEF “Power Plant” database, accessed 09/30/16

CSP Market Worldwide

energy.gov/sunshot

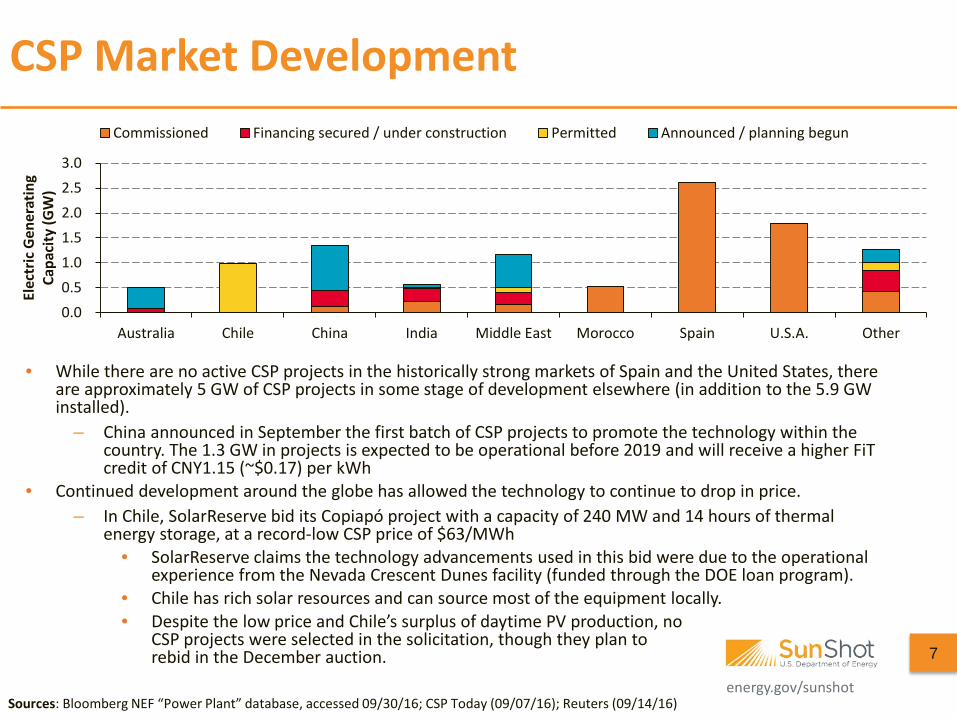

• While there are no active CSP projects in the historically strong markets of Spain and the United States, there are approximately 5 GW of CSP projects in some stage of development elsewhere (in addition to the 5.9 GW installed).

– China announced in September the first batch of CSP projects to promote the technology within the country. The 1.3 GW in projects is expected to be operational before 2019 and will receive a higher FiT credit of CNY1.15 (~$0.17) per kWh

• Continued development around the globe has allowed the technology to continue to drop in price. – In Chile, SolarReserve bid its Copiapó project with a capacity of 240 MW and 14 hours of thermal

energy storage, at a record-low CSP price of $63/MWh • SolarReserve claims the technology advancements used in this bid were due to the operational

experience from the Nevada Crescent Dunes facility (funded through the DOE loan program). • Chile has rich solar resources and can source most of the equipment locally. • Despite the low price and Chile’s surplus of daytime PV production, no

CSP projects were selected in the solicitation, though they plan to rebid in the December auction.

Sources: Bloomberg NEF “Power Plant” database, accessed 09/30/16; CSP Today (09/07/16); Reuters (09/14/16)

0.00.51.01.52.02.53.0

Australia Chile China India Middle East Morocco Spain U.S.A. Other

Elec

tric

Gen

erat

ing

Capa

city

(GW

)

Commissioned Financing secured / under construction Permitted Announced / planning begun

CSP Market Development

7

energy.gov/sunshot

Agenda

8

• Global Deployment • U.S. Deployment • U.S. Pricing • Global Manufacturing • Component Pricing • Market Activity • Tax Credit Availability

energy.gov/sunshot

0.8 1.2 2.2 2.6 2.9 3.3 3.7 3.8 5.0 1.0 1.1

1.3 1.7 1.9 2.0 3.0 3.5

3.2

3.0 4.0

4.4

8.8 6.3 6.3

8.0 8.7

9.6

0

5

10

15

20

25

2013 2014 2015 2016P 2017P 2018P 2019P 2020P 2021P

PV A

nnua

l Ins

talla

tions

(GW

DC)

Utility-scaleNon-Res.Residential

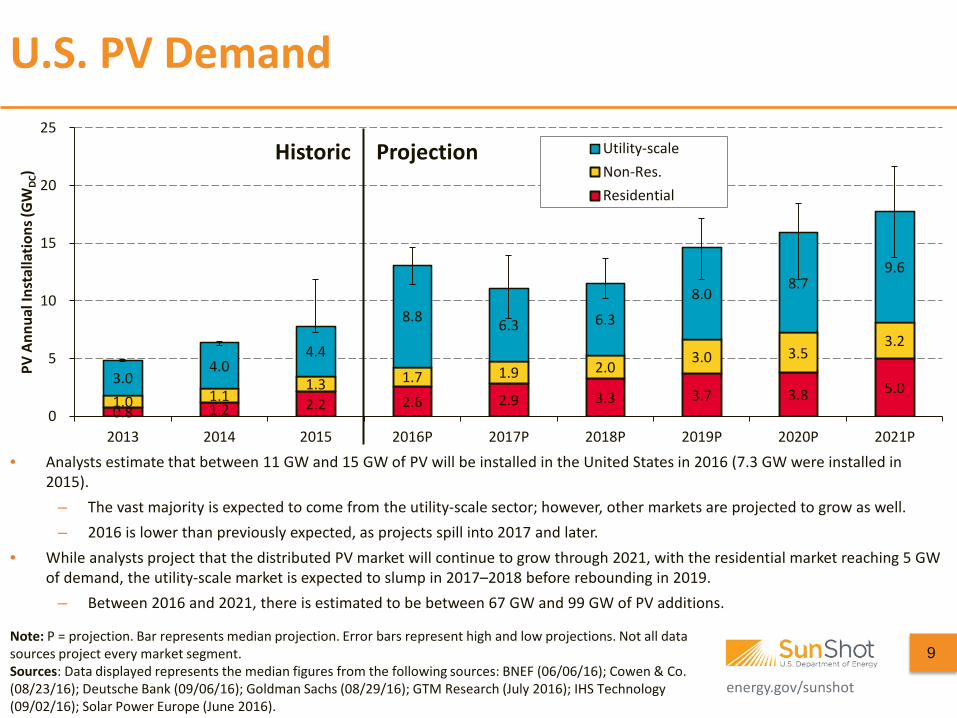

U.S. PV Demand

Historic Projection

• Analysts estimate that between 11 GW and 15 GW of PV will be installed in the United States in 2016 (7.3 GW were installed in 2015).

– The vast majority is expected to come from the utility-scale sector; however, other markets are projected to grow as well. – 2016 is lower than previously expected, as projects spill into 2017 and later.

• While analysts project that the distributed PV market will continue to grow through 2021, with the residential market reaching 5 GW of demand, the utility-scale market is expected to slump in 2017–2018 before rebounding in 2019.

– Between 2016 and 2021, there is estimated to be between 67 GW and 99 GW of PV additions.

9 Note: P = projection. Bar represents median projection. Error bars represent high and low projections. Not all data sources project every market segment. Sources: Data displayed represents the median figures from the following sources: BNEF (06/06/16); Cowen & Co. (08/23/16); Deutsche Bank (09/06/16); Goldman Sachs (08/29/16); GTM Research (July 2016); IHS Technology (09/02/16); Solar Power Europe (June 2016).

energy.gov/sunshot

U.S. Installation Breakdown

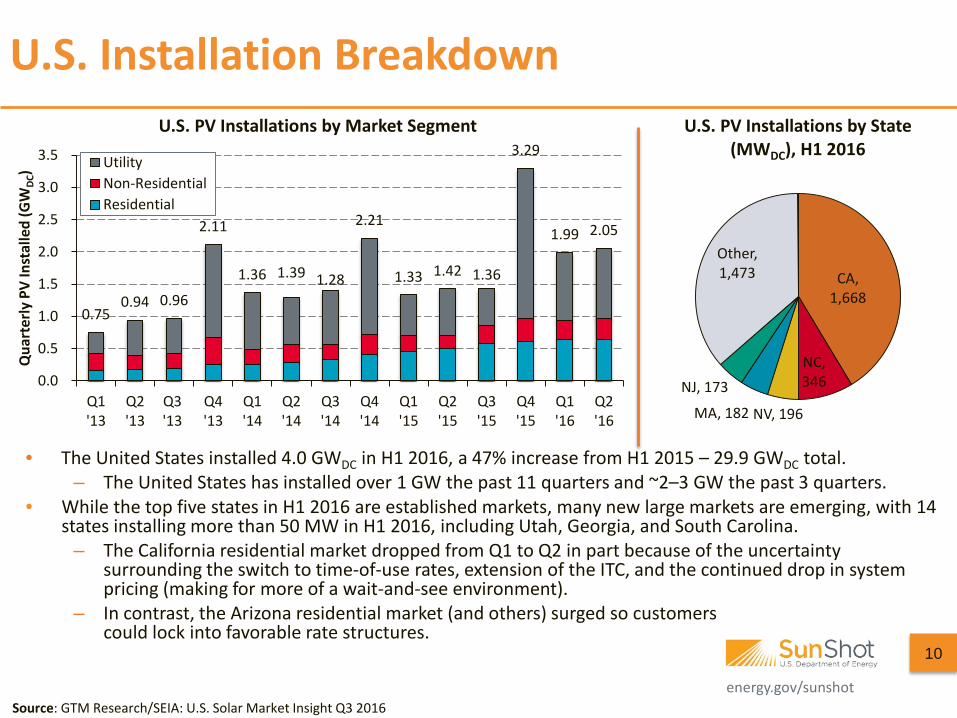

• The United States installed 4.0 GWDC in H1 2016, a 47% increase from H1 2015 – 29.9 GWDC total. – The United States has installed over 1 GW the past 11 quarters and ~2–3 GW the past 3 quarters.

• While the top five states in H1 2016 are established markets, many new large markets are emerging, with 14 states installing more than 50 MW in H1 2016, including Utah, Georgia, and South Carolina.

– The California residential market dropped from Q1 to Q2 in part because of the uncertainty surrounding the switch to time-of-use rates, extension of the ITC, and the continued drop in system pricing (making for more of a wait-and-see environment).

– In contrast, the Arizona residential market (and others) surged so customers could lock into favorable rate structures.

10

Source: GTM Research/SEIA: U.S. Solar Market Insight Q3 2016

0.75 0.94 0.96

2.11

1.36 1.39 1.28

2.21

1.33 1.42 1.36

3.29

1.99 2.05

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Q1'15

Q2'15

Q3'15

Q4'15

Q1'16

Q2'16

Qua

rter

ly P

V In

stal

led

(GW

DC)

U.S. PV Installations by Market Segment

UtilityNon-ResidentialResidential

CA, 1,668

NC, 346

NV, 196 MA, 182

NJ, 173

Other, 1,473

U.S. PV Installations by State (MWDC), H1 2016

energy.gov/sunshot

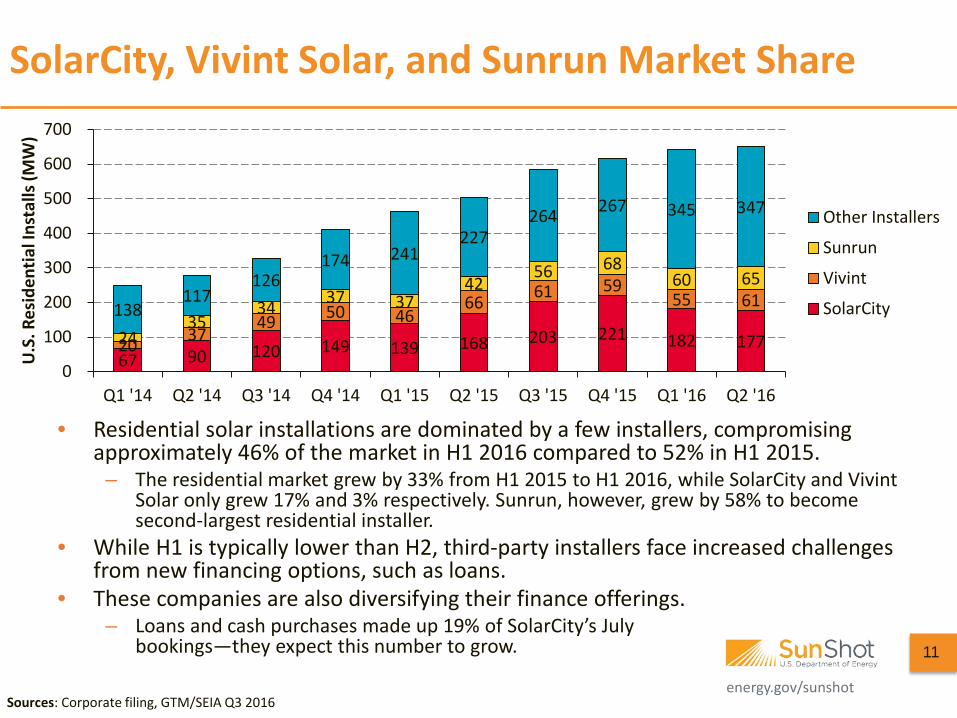

• Residential solar installations are dominated by a few installers, compromising approximately 46% of the market in H1 2016 compared to 52% in H1 2015.

– The residential market grew by 33% from H1 2015 to H1 2016, while SolarCity and Vivint Solar only grew 17% and 3% respectively. Sunrun, however, grew by 58% to become second-largest residential installer.

• While H1 is typically lower than H2, third-party installers face increased challenges from new financing options, such as loans.

• These companies are also diversifying their finance offerings. – Loans and cash purchases made up 19% of SolarCity’s July

bookings—they expect this number to grow.

SolarCity, Vivint Solar, and Sunrun Market Share

Sources: Corporate filing, GTM/SEIA Q3 2016

11

67 90 120 149 139 168 203 221 182 177 20 37 49 50 46

66 61 59 55 61

24 35

34 37 37 42

56 68 60 65

138 117

126 174 241

227 264 267 345 347

0

100

200

300

400

500

600

700

Q1 '14 Q2 '14 Q3 '14 Q4 '14 Q1 '15 Q2 '15 Q3 '15 Q4 '15 Q1 '16 Q2 '16

U.S

. Res

iden

tial I

nsta

lls (M

W)

Other Installers

Sunrun

Vivint

SolarCity

energy.gov/sunshot energy.gov/sunshot

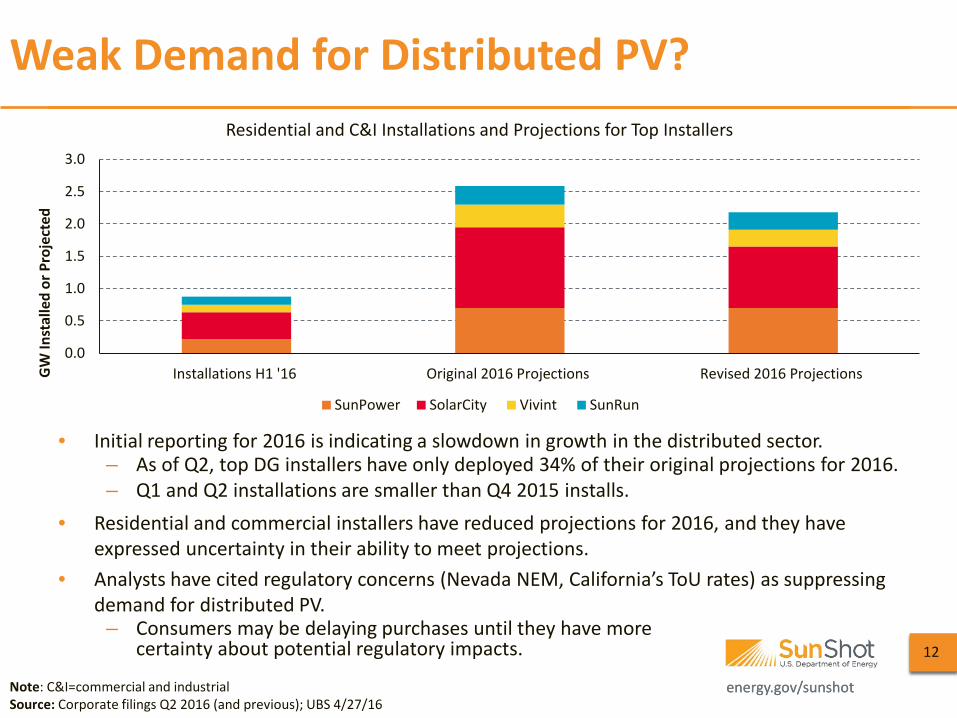

• Initial reporting for 2016 is indicating a slowdown in growth in the distributed sector. – As of Q2, top DG installers have only deployed 34% of their original projections for 2016. – Q1 and Q2 installations are smaller than Q4 2015 installs.

• Residential and commercial installers have reduced projections for 2016, and they have expressed uncertainty in their ability to meet projections.

• Analysts have cited regulatory concerns (Nevada NEM, California’s ToU rates) as suppressing demand for distributed PV.

– Consumers may be delaying purchases until they have more certainty about potential regulatory impacts.

Weak Demand for Distributed PV?

Note: C&I=commercial and industrial Source: Corporate filings Q2 2016 (and previous); UBS 4/27/16

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Installations H1 '16 Original 2016 Projections Revised 2016 ProjectionsGW

Inst

alle

d or

Pro

ject

ed

Residential and C&I Installations and Projections for Top Installers

SunPower SolarCity Vivint SunRun

12

energy.gov/sunshot

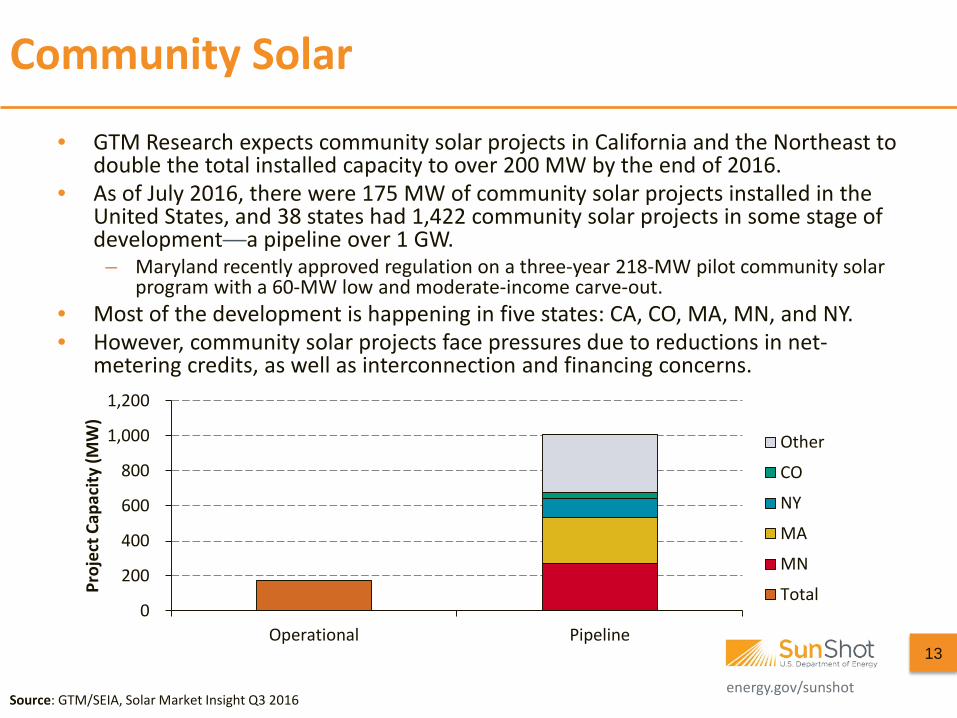

Community Solar

• GTM Research expects community solar projects in California and the Northeast to double the total installed capacity to over 200 MW by the end of 2016.

• As of July 2016, there were 175 MW of community solar projects installed in the United States, and 38 states had 1,422 community solar projects in some stage of development—a pipeline over 1 GW.

– Maryland recently approved regulation on a three-year 218-MW pilot community solar program with a 60-MW low and moderate-income carve-out.

• Most of the development is happening in five states: CA, CO, MA, MN, and NY. • However, community solar projects face pressures due to reductions in net-

metering credits, as well as interconnection and financing concerns.

Source: GTM/SEIA, Solar Market Insight Q3 2016

13

0

200

400

600

800

1,000

1,200

Operational Pipeline

Proj

ect C

apac

ity (M

W)

Other

CO

NY

MA

MN

Total

energy.gov/sunshot

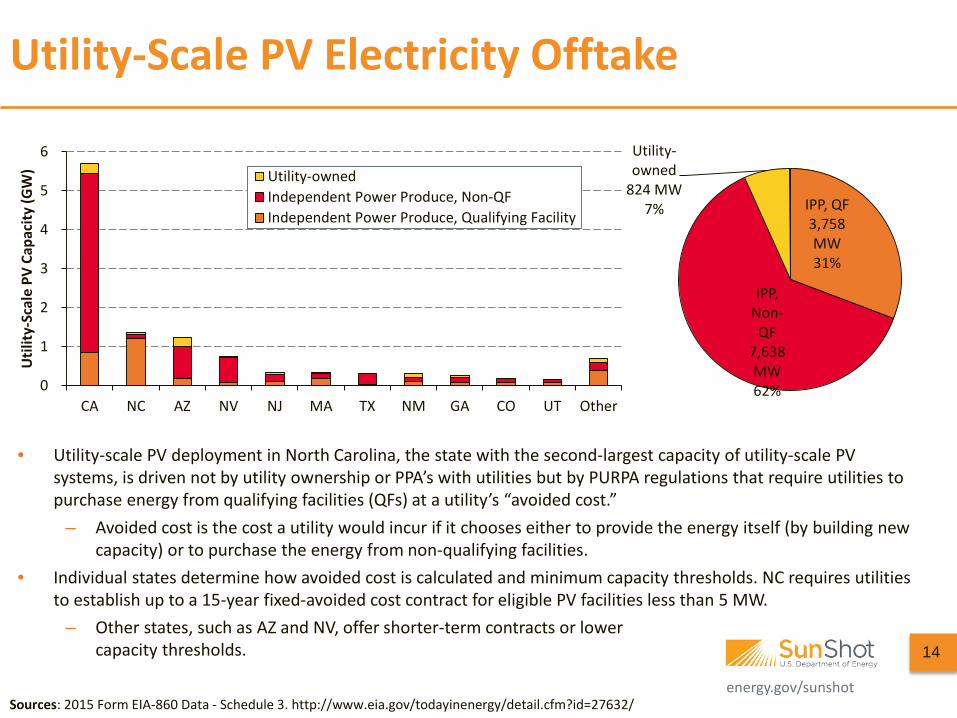

Utility-Scale PV Electricity Offtake

• Utility-scale PV deployment in North Carolina, the state with the second-largest capacity of utility-scale PV systems, is driven not by utility ownership or PPA’s with utilities but by PURPA regulations that require utilities to purchase energy from qualifying facilities (QFs) at a utility’s “avoided cost.”

– Avoided cost is the cost a utility would incur if it chooses either to provide the energy itself (by building new capacity) or to purchase the energy from non-qualifying facilities.

• Individual states determine how avoided cost is calculated and minimum capacity thresholds. NC requires utilities to establish up to a 15-year fixed-avoided cost contract for eligible PV facilities less than 5 MW.

– Other states, such as AZ and NV, offer shorter-term contracts or lower capacity thresholds.

Sources: 2015 Form EIA-860 Data - Schedule 3. http://www.eia.gov/todayinenergy/detail.cfm?id=27632/

0

1

2

3

4

5

6

CA NC AZ NV NJ MA TX NM GA CO UT Other

Util

ity-S

cale

PV

Capa

city

(GW

) Utility-ownedIndependent Power Produce, Non-QFIndependent Power Produce, Qualifying Facility

IPP, QF 3,758 MW 31%

IPP, Non-QF

7,638 MW 62%

Utility-owned

824 MW 7%

14

energy.gov/sunshot

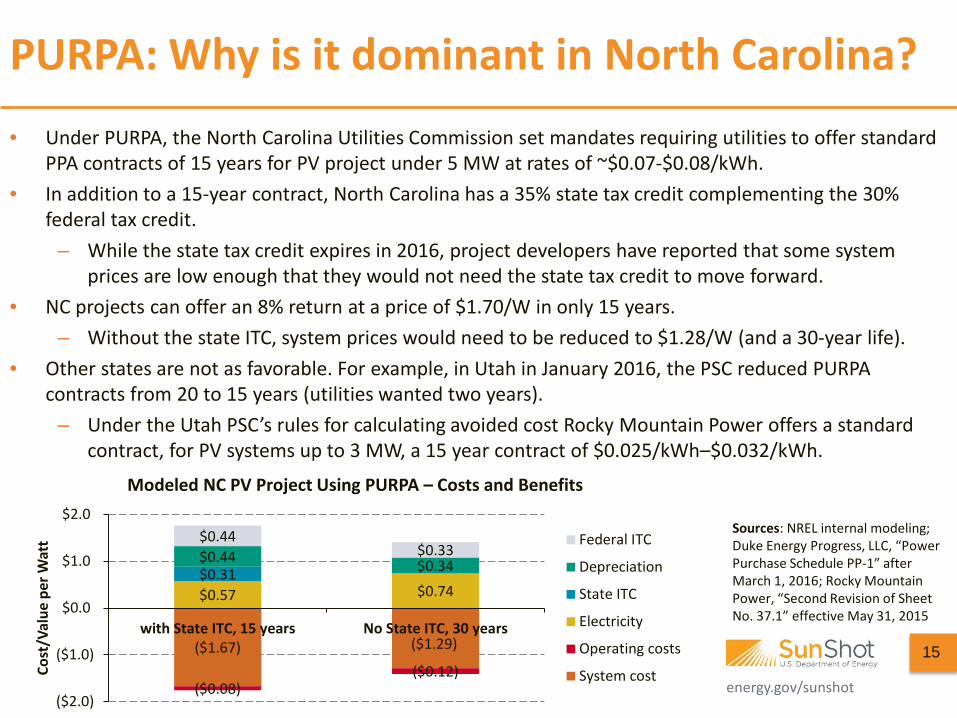

PURPA: Why is it dominant in North Carolina? • Under PURPA, the North Carolina Utilities Commission set mandates requiring utilities to offer standard

PPA contracts of 15 years for PV project under 5 MW at rates of ~$0.07-$0.08/kWh. • In addition to a 15-year contract, North Carolina has a 35% state tax credit complementing the 30%

federal tax credit. – While the state tax credit expires in 2016, project developers have reported that some system

prices are low enough that they would not need the state tax credit to move forward. • NC projects can offer an 8% return at a price of $1.70/W in only 15 years.

– Without the state ITC, system prices would need to be reduced to $1.28/W (and a 30-year life). • Other states are not as favorable. For example, in Utah in January 2016, the PSC reduced PURPA

contracts from 20 to 15 years (utilities wanted two years). – Under the Utah PSC’s rules for calculating avoided cost Rocky Mountain Power offers a standard

contract, for PV systems up to 3 MW, a 15 year contract of $0.025/kWh–$0.032/kWh.

($1.67) ($1.29)

($0.08) ($0.12)

$0.57 $0.74 $0.31 $0.44 $0.34

$0.44 $0.33

($2.0)

($1.0)

$0.0

$1.0

$2.0

with State ITC, 15 years No State ITC, 30 years

Cost

/Val

ue p

er W

att

Modeled NC PV Project Using PURPA – Costs and Benefits

Federal ITC

Depreciation

State ITC

Electricity

Operating costs

System cost15

Sources: NREL internal modeling; Duke Energy Progress, LLC, “Power Purchase Schedule PP-1” after March 1, 2016; Rocky Mountain Power, “Second Revision of Sheet No. 37.1” effective May 31, 2015

energy.gov/sunshot

PURPA and Renewable Energy Deployment More Broadly

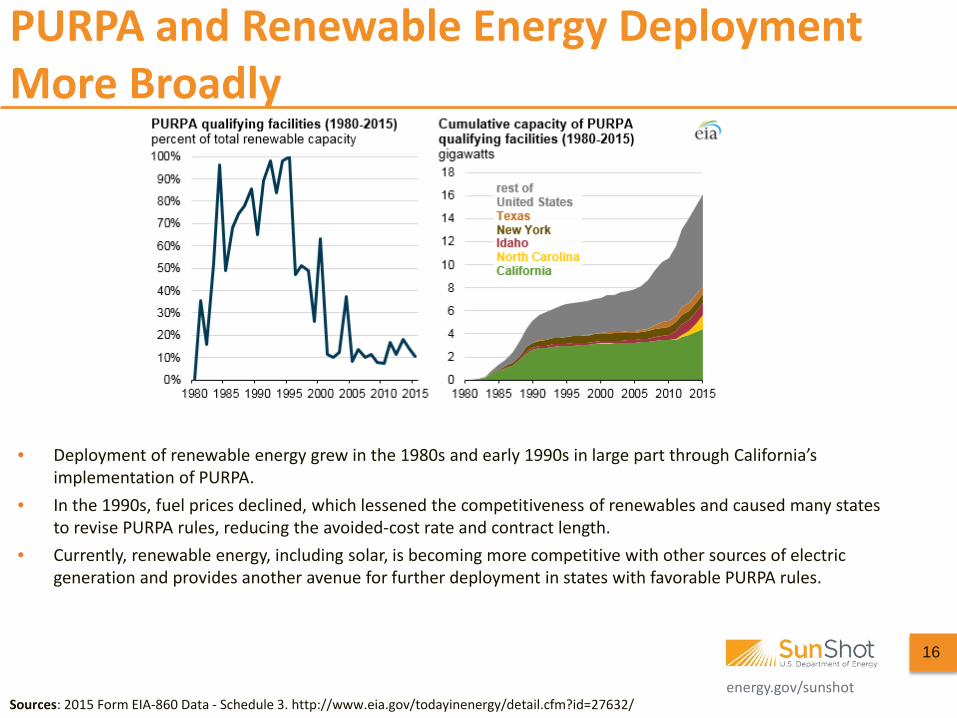

• Deployment of renewable energy grew in the 1980s and early 1990s in large part through California’s implementation of PURPA.

• In the 1990s, fuel prices declined, which lessened the competitiveness of renewables and caused many states to revise PURPA rules, reducing the avoided-cost rate and contract length.

• Currently, renewable energy, including solar, is becoming more competitive with other sources of electric generation and provides another avenue for further deployment in states with favorable PURPA rules.

16

Sources: 2015 Form EIA-860 Data - Schedule 3. http://www.eia.gov/todayinenergy/detail.cfm?id=27632/

energy.gov/sunshot

• Most electricity customers in the United States buy electricity from the same utilities that provide transmission and distribution services.

• In deregulated states, such as many parts of the Northeast, utilities are, for the most part, not permitted to own generating assets.

– Although customers have the option to procure electricity from alternative electric suppliers (such as green power options), customer typically use the default option, having their regulated utility procure energy.

• Community choice aggregation (CCA) has emerged as an alternative energy procurement strategy for municipalities/regions with state-enabling legislation. CCA allows local governments to aggregate electricity demand and procure electricity from alternative suppliers on behalf of residential and, in some cases, commercial customers. Local utilities remain responsible for transmission, distribution, and billing services.

Community Choice Aggregation Procurement

Sources: Pacific Energy Advisors, “Community Choice Aggregation: Enabling Retail Choice Within California’s Electric Power Sector”; UBS conference call, September 9, 2016; O’Shaughnessy, E., J. Heeter, and C. Liu. 2016. Status and Trends in the United States Voluntary Green Power Market (2015 Data). Forthcoming. Golden, CO: National Renewable Energy Laboratory

– Many CCAs procure renewable energy in excess of their RPS requirements (including some local solar).

– In 2015, community choice aggregators sold about 7.4 million MWh of renewable energy to about 1.9 million customers.

– Opt-out policies are common and result in much higher participation (80%–90%) than opt-in programs (~2%, such as the case for green power purchase options).

– A fee is paid by CCA customers to exit their existing utility.

CCA enabling legislation

17

energy.gov/sunshot

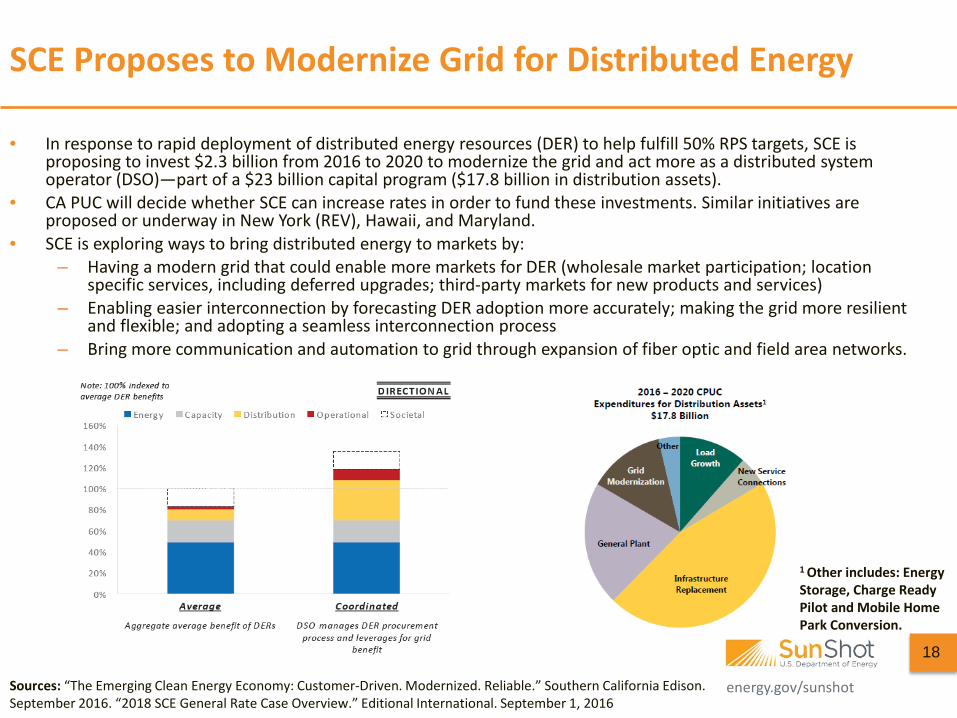

• In response to rapid deployment of distributed energy resources (DER) to help fulfill 50% RPS targets, SCE is proposing to invest $2.3 billion from 2016 to 2020 to modernize the grid and act more as a distributed system operator (DSO)—part of a $23 billion capital program ($17.8 billion in distribution assets).

• CA PUC will decide whether SCE can increase rates in order to fund these investments. Similar initiatives are proposed or underway in New York (REV), Hawaii, and Maryland.

• SCE is exploring ways to bring distributed energy to markets by: – Having a modern grid that could enable more markets for DER (wholesale market participation; location

specific services, including deferred upgrades; third-party markets for new products and services) – Enabling easier interconnection by forecasting DER adoption more accurately; making the grid more resilient

and flexible; and adopting a seamless interconnection process – Bring more communication and automation to grid through expansion of fiber optic and field area networks.

SCE Proposes to Modernize Grid for Distributed Energy

Sources: “The Emerging Clean Energy Economy: Customer-Driven. Modernized. Reliable.” Southern California Edison. September 2016. “2018 SCE General Rate Case Overview.” Editional International. September 1, 2016

18

1 Other includes: Energy Storage, Charge Ready Pilot and Mobile Home Park Conversion.

energy.gov/sunshot

Current Status

Budget Distributed Energy Market Participation

Smart Meter Upgrades

Other

California (SCE)

Rate-case proposal $2.3 Billion Yes Smart meters already required in CA

Hawaii (HECO)

Phase one completed in 2014; Phase 2 docket filed April 2016

$340 Million No Yes Primarily focused on smart meters and grid equipment upgrades

Maryland Request for Comments

$500,000 (for initial study)

Valuation for PV and Storage

Yes Key outcomes are similar to REV goals; initial studies financed by Pepco merger

New York REV underway $5 billion (NY Clean Energy Fund)

Yes No

Grid Modernization around the States

SCE 2018 Rate Case; NY PSC Case14-M-0101; Hawaii PUC Docket No. 2016-0087; Maryland PUC 9/26/16

19

energy.gov/sunshot

U.S. Electric Storage Capacity, June 2016

0

5

10

15

20

25

0

50

100

150

200

250

300

350

400

450

CSP with storage Batteries Gas w. compressedair storage

Flywheels Hydro pumpedstorage

U.S

. Gen

erat

ing

Capa

city

, Pum

ped

Stor

age

(GW

)

U.S

. Gen

erat

ing

Capa

city

, Sto

rage

(MW

)

Source: EIA “Electric Power Monthly,” Table 6.1. Electric Generating Summer Capacity Changes (MW), May 2016 to June 2016

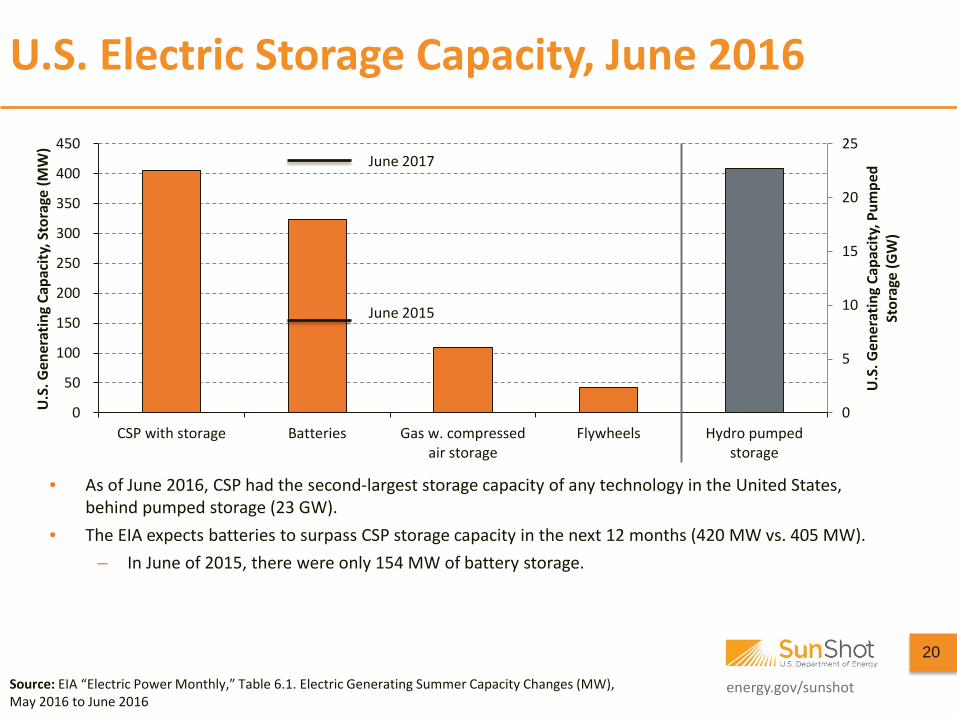

• As of June 2016, CSP had the second-largest storage capacity of any technology in the United States, behind pumped storage (23 GW).

• The EIA expects batteries to surpass CSP storage capacity in the next 12 months (420 MW vs. 405 MW). – In June of 2015, there were only 154 MW of battery storage.

June 2017

20

June 2015

energy.gov/sunshot

Agenda

21

• Global Deployment • U.S. Deployment • U.S. Pricing • Global Manufacturing • Component Pricing • Market Activity • Tax Credit Availability

energy.gov/sunshot

$-

$1

$2

$3

$4

$5

$6

$7

$8

$-

$1

$2

$3

$4

$5

$6

$7

$8

H1 '10 H2 '10 H1 '11 H2 '11 H1 '12 H2 '12 H1 '13 H2 '13 H1 '14 H2 '14 H1 '15 H2 '15 H1 '16

Aver

age

Repo

rted

Sys

tem

Pric

e ($

/W)

Median System Price 20 Percentile 80 Percentile

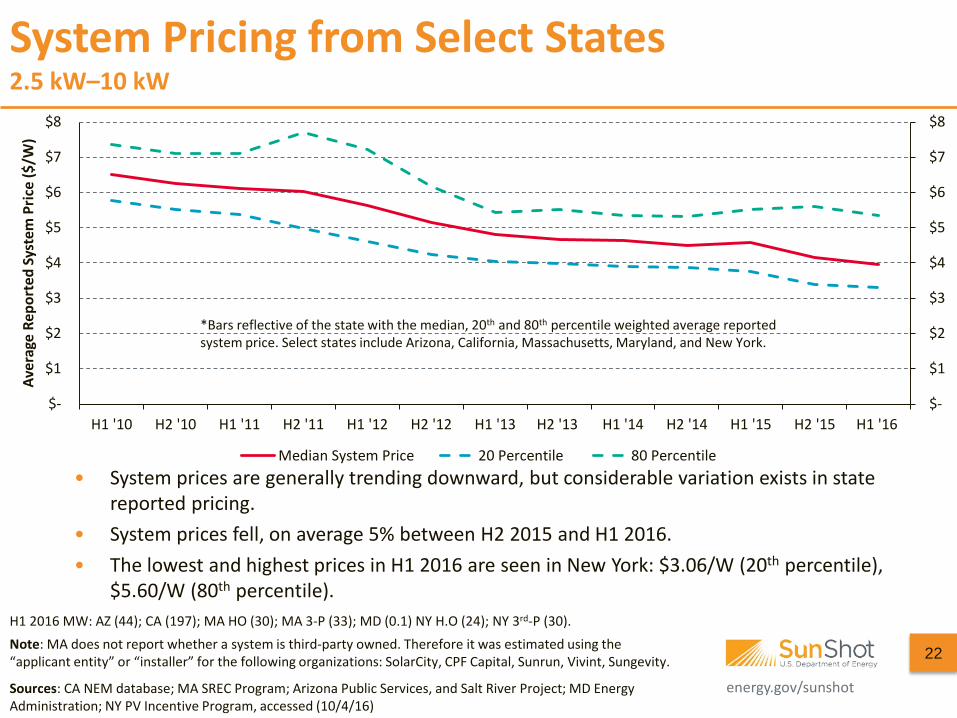

System Pricing from Select States 2.5 kW–10 kW

22

• System prices are generally trending downward, but considerable variation exists in state reported pricing.

• System prices fell, on average 5% between H2 2015 and H1 2016. • The lowest and highest prices in H1 2016 are seen in New York: $3.06/W (20th percentile),

$5.60/W (80th percentile). H1 2016 MW: AZ (44); CA (197); MA HO (30); MA 3-P (33); MD (0.1) NY H.O (24); NY 3rd-P (30). Note: MA does not report whether a system is third-party owned. Therefore it was estimated using the “applicant entity” or “installer” for the following organizations: SolarCity, CPF Capital, Sunrun, Vivint, Sungevity.

Sources: CA NEM database; MA SREC Program; Arizona Public Services, and Salt River Project; MD Energy Administration; NY PV Incentive Program, accessed (10/4/16)

*Bars reflective of the state with the median, 20th and 80th percentile weighted average reported system price. Select states include Arizona, California, Massachusetts, Maryland, and New York.

energy.gov/sunshot

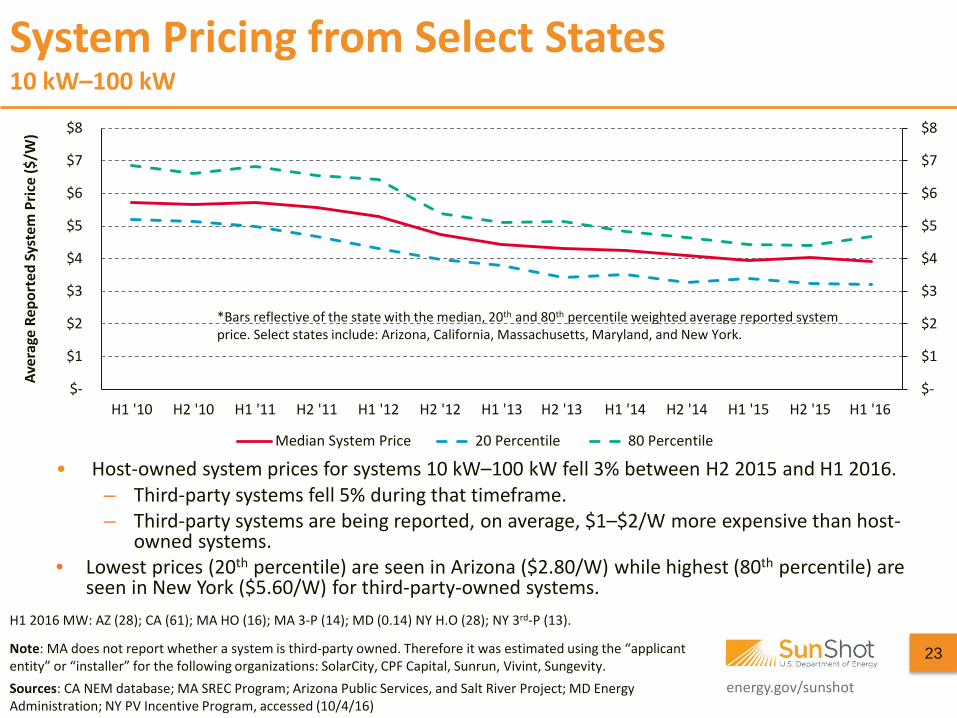

System Pricing from Select States 10 kW–100 kW

23 Note: MA does not report whether a system is third-party owned. Therefore it was estimated using the “applicant entity” or “installer” for the following organizations: SolarCity, CPF Capital, Sunrun, Vivint, Sungevity.

• Host-owned system prices for systems 10 kW–100 kW fell 3% between H2 2015 and H1 2016. – Third-party systems fell 5% during that timeframe. – Third-party systems are being reported, on average, $1–$2/W more expensive than host-

owned systems. • Lowest prices (20th percentile) are seen in Arizona ($2.80/W) while highest (80th percentile) are

seen in New York ($5.60/W) for third-party-owned systems. H1 2016 MW: AZ (28); CA (61); MA HO (16); MA 3-P (14); MD (0.14) NY H.O (28); NY 3rd-P (13).

Sources: CA NEM database; MA SREC Program; Arizona Public Services, and Salt River Project; MD Energy Administration; NY PV Incentive Program, accessed (10/4/16)

*Bars reflective of the state with the median, 20th and 80th percentile weighted average reported system price. Select states include: Arizona, California, Massachusetts, Maryland, and New York.

$-

$1

$2

$3

$4

$5

$6

$7

$8

$-

$1

$2

$3

$4

$5

$6

$7

$8

H1 '10 H2 '10 H1 '11 H2 '11 H1 '12 H2 '12 H1 '13 H2 '13 H1 '14 H2 '14 H1 '15 H2 '15 H1 '16

Aver

age

Repo

rted

Sys

tem

Pric

e ($

/W)

Median System Price 20 Percentile 80 Percentile

energy.gov/sunshot

$2.13 $2.07 $2.56 $2.27

$0.56 $0.71 $0.78 $0.25 $0.27

$0.33 $0.57

$0.94

$0.0$0.5$1.0$1.5$2.0$2.5$3.0$3.5$4.0$4.5$5.0

VivintSolar

SolarCity SunrunAvg.

SunrunBuilt

Inst

alle

d Co

st ($

/W)

Q1 2016

Net Value

G&A

Sales

Installation

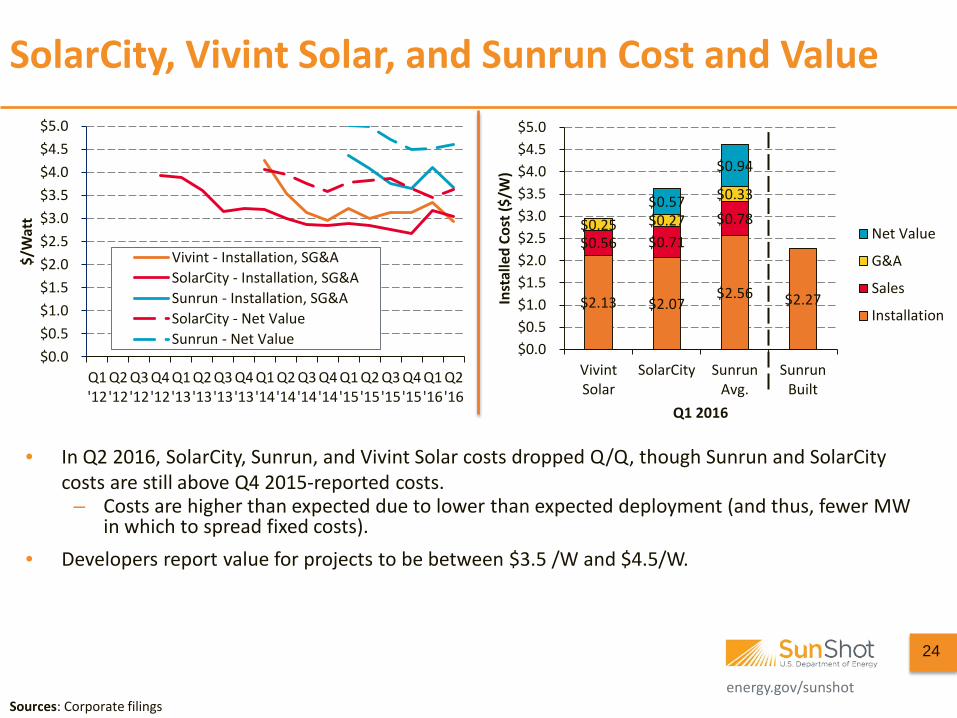

• In Q2 2016, SolarCity, Sunrun, and Vivint Solar costs dropped Q/Q, though Sunrun and SolarCity costs are still above Q4 2015-reported costs.

– Costs are higher than expected due to lower than expected deployment (and thus, fewer MW in which to spread fixed costs).

• Developers report value for projects to be between $3.5 /W and $4.5/W.

SolarCity, Vivint Solar, and Sunrun Cost and Value

Sources: Corporate filings

24

$0.0$0.5$1.0$1.5$2.0$2.5$3.0$3.5$4.0$4.5$5.0

Q1'12

Q2'12

Q3'12

Q4'12

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Q1'15

Q2'15

Q3'15

Q4'15

Q1'16

Q2'16

$/W

att

Vivint - Installation, SG&ASolarCity - Installation, SG&ASunrun - Installation, SG&ASolarCity - Net ValueSunrun - Net Value

energy.gov/sunshot

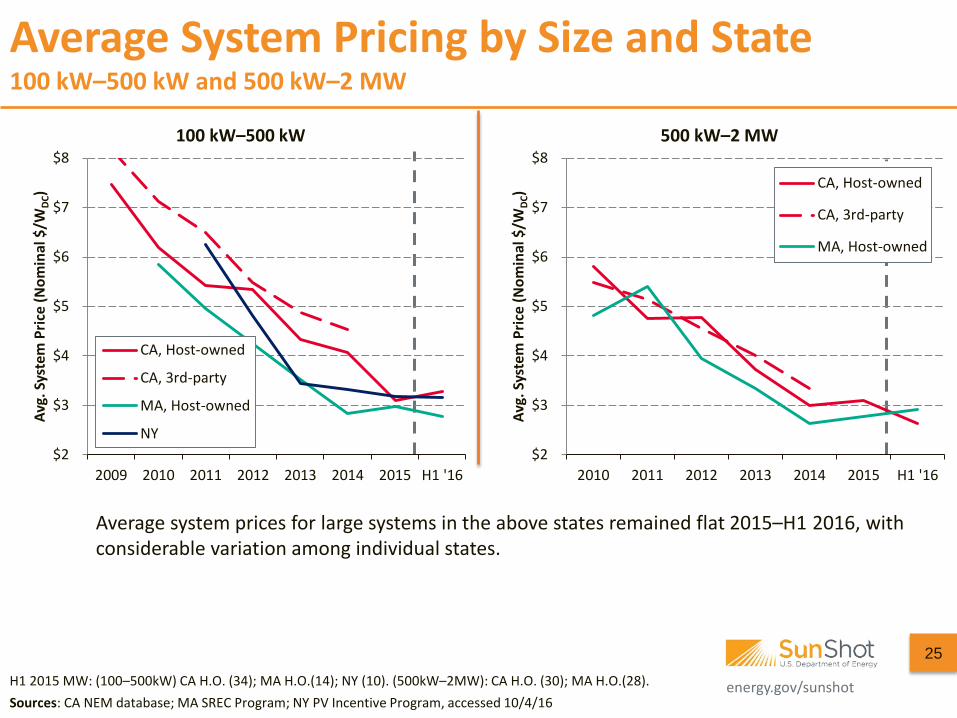

Average System Pricing by Size and State 100 kW–500 kW and 500 kW–2 MW

25

H1 2015 MW: (100–500kW) CA H.O. (34); MA H.O.(14); NY (10). (500kW–2MW): CA H.O. (30); MA H.O.(28).

Average system prices for large systems in the above states remained flat 2015–H1 2016, with considerable variation among individual states.

Sources: CA NEM database; MA SREC Program; NY PV Incentive Program, accessed 10/4/16

$2

$3

$4

$5

$6

$7

$8

2009 2010 2011 2012 2013 2014 2015 H1 '16

Avg.

Sys

tem

Pric

e (N

omin

al $

/WDC

)

100 kW–500 kW

CA, Host-owned

CA, 3rd-party

MA, Host-owned

NY$2

$3

$4

$5

$6

$7

$8

2010 2011 2012 2013 2014 2015 H1 '16

Avg.

Sys

tem

Pric

e (N

omin

al $

/WDC

)

500 kW–2 MW

CA, Host-owned

CA, 3rd-party

MA, Host-owned

energy.gov/sunshot

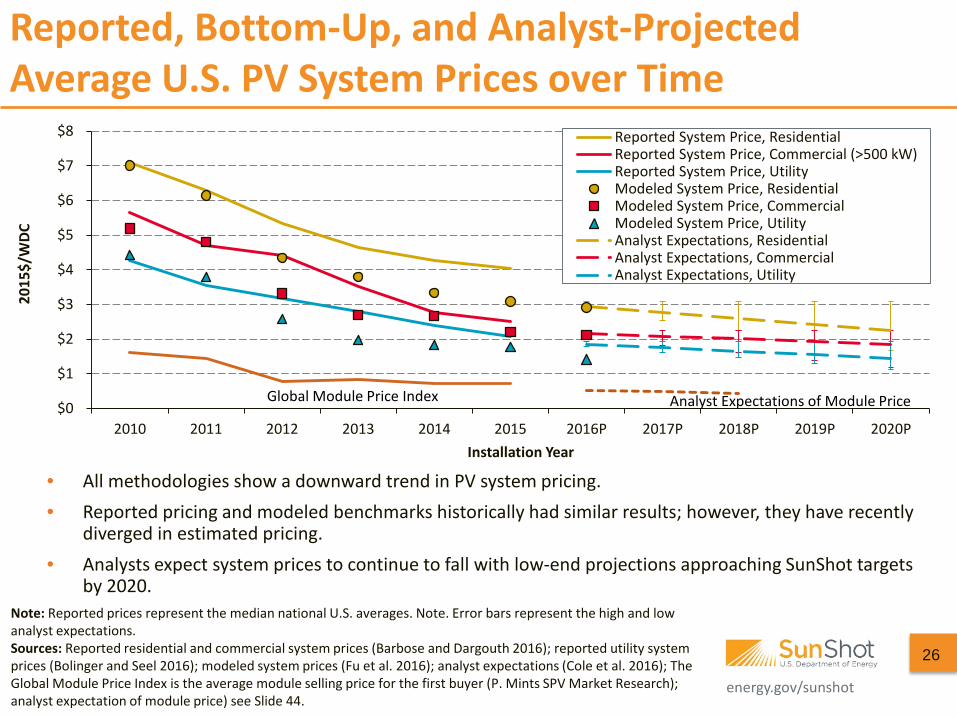

Reported, Bottom-Up, and Analyst-Projected Average U.S. PV System Prices over Time

Note: Reported prices represent the median national U.S. averages. Note. Error bars represent the high and low analyst expectations. Sources: Reported residential and commercial system prices (Barbose and Dargouth 2016); reported utility system prices (Bolinger and Seel 2016); modeled system prices (Fu et al. 2016); analyst expectations (Cole et al. 2016); The Global Module Price Index is the average module selling price for the first buyer (P. Mints SPV Market Research); analyst expectation of module price) see Slide 44.

26

• All methodologies show a downward trend in PV system pricing. • Reported pricing and modeled benchmarks historically had similar results; however, they have recently

diverged in estimated pricing. • Analysts expect system prices to continue to fall with low-end projections approaching SunShot targets

by 2020.

$0

$1

$2

$3

$4

$5

$6

$7

$8

2010 2011 2012 2013 2014 2015 2016P 2017P 2018P 2019P 2020P

2015

$/W

DC

Installation Year

Reported System Price, ResidentialReported System Price, Commercial (>500 kW)Reported System Price, UtilityModeled System Price, ResidentialModeled System Price, CommercialModeled System Price, UtilityAnalyst Expectations, ResidentialAnalyst Expectations, CommercialAnalyst Expectations, Utility

Analyst Expectations of Module Price Global Module Price Index

energy.gov/sunshot

$3.0 $3.5

$3.1 $4.1

$2.1 $2.1 $2.2 $2.5 $3.5

$3.0 $3.0

$1.6 $1.6 $1.6 $1.4 $1.8 $1.9 $2.1

$0$1$2$3$4$5$6

BNEF

GTM

/SEI

A

NRE

L

LBN

L

Ener

gySa

ge

Pet.-

Dean

BNEF

GTM

/SEI

A

NRE

L

LBN

L (>

500k

W)

LBN

L (≤

500k

W)

Ener

gySa

ge

SolS

yste

ms

(≤50

0 kW

)

SolS

yste

ms (

500

kW -

2 M

W)

BNEF

(1-A

xis)

BNEF

(Fix

ed)

GTM

/SEI

A (1

-Axi

s)

GTM

/SEI

A (F

ixed

)

NRE

L (1

-Axi

s)

NRE

L (F

ixed

)

LBN

L

Modeled Reported Quote Modeled Reported Quote Modeled Reported

Residential Non-Residential Utility-scale

Syst

em P

rice

(201

5 $/

WDC

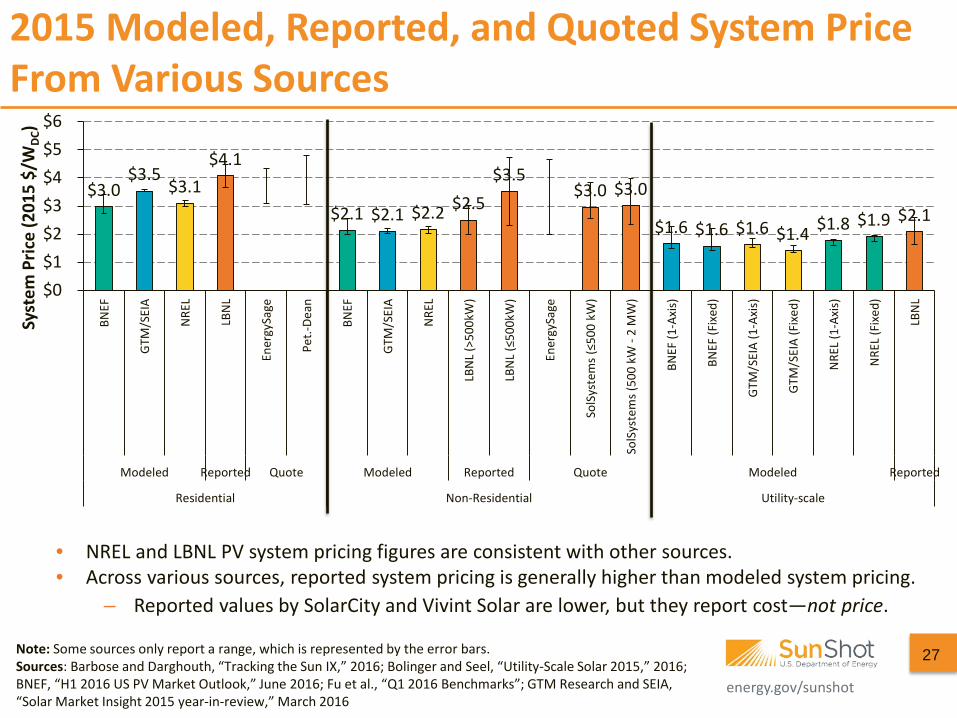

) 2015 Modeled, Reported, and Quoted System Price From Various Sources

27

• NREL and LBNL PV system pricing figures are consistent with other sources. • Across various sources, reported system pricing is generally higher than modeled system pricing.

– Reported values by SolarCity and Vivint Solar are lower, but they report cost—not price.

Note: Some sources only report a range, which is represented by the error bars. Sources: Barbose and Darghouth, “Tracking the Sun IX,” 2016; Bolinger and Seel, “Utility-Scale Solar 2015,” 2016; BNEF, “H1 2016 US PV Market Outlook,” June 2016; Fu et al., “Q1 2016 Benchmarks”; GTM Research and SEIA, “Solar Market Insight 2015 year-in-review,” March 2016

energy.gov/sunshot

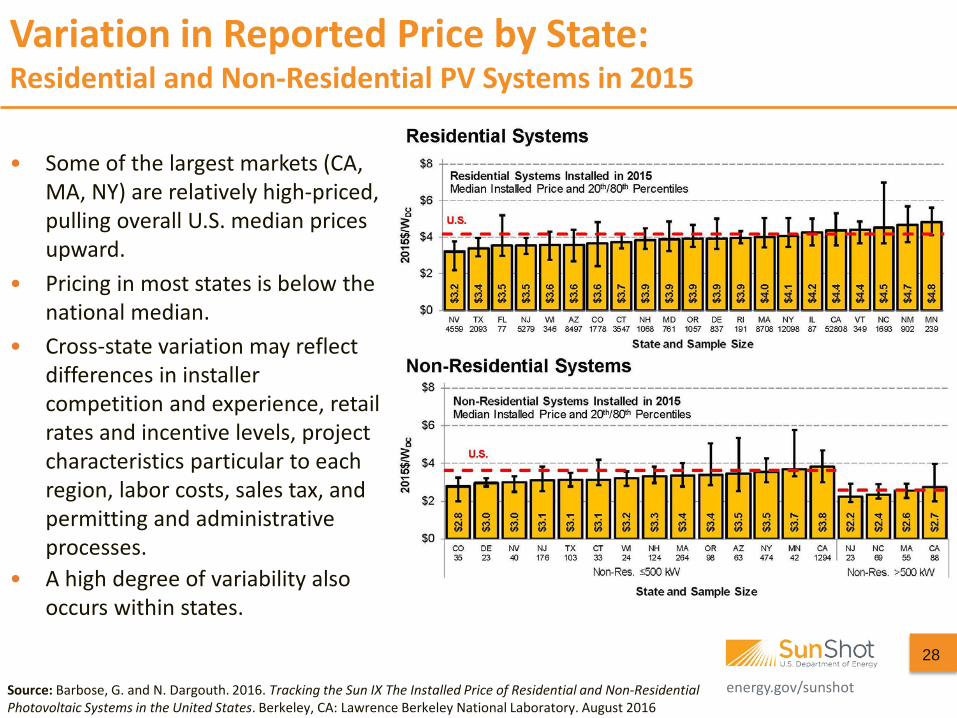

Variation in Reported Price by State: Residential and Non-Residential PV Systems in 2015

• Some of the largest markets (CA, MA, NY) are relatively high-priced, pulling overall U.S. median prices upward.

• Pricing in most states is below the national median.

• Cross-state variation may reflect differences in installer competition and experience, retail rates and incentive levels, project characteristics particular to each region, labor costs, sales tax, and permitting and administrative processes.

• A high degree of variability also occurs within states.

Source: Barbose, G. and N. Dargouth. 2016. Tracking the Sun IX The Installed Price of Residential and Non-Residential Photovoltaic Systems in the United States. Berkeley, CA: Lawrence Berkeley National Laboratory. August 2016

28

energy.gov/sunshot

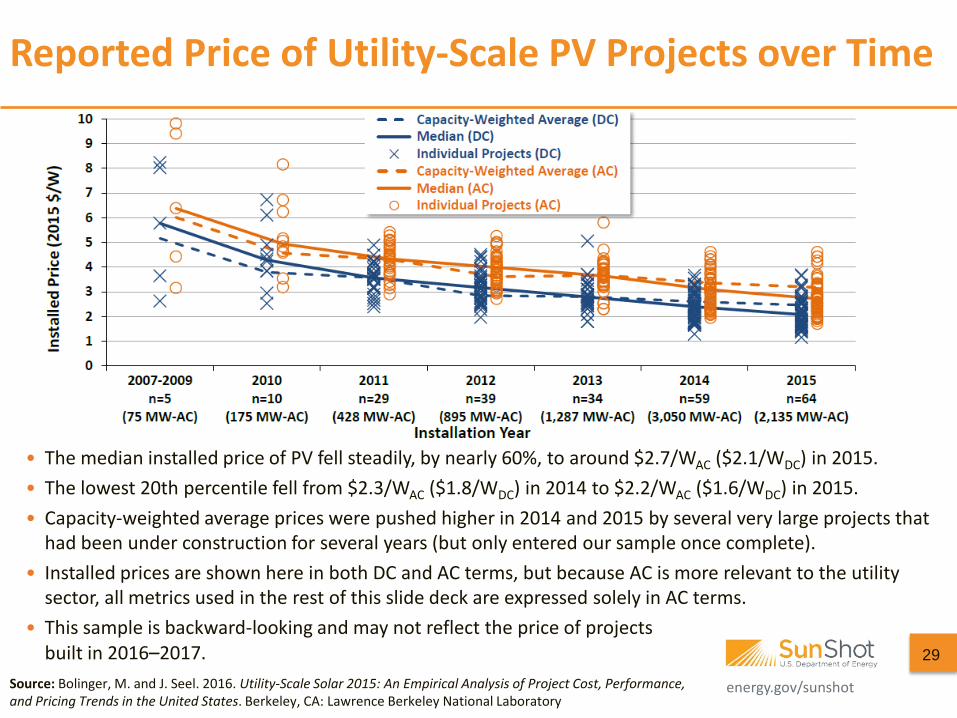

Reported Price of Utility-Scale PV Projects over Time

• The median installed price of PV fell steadily, by nearly 60%, to around $2.7/WAC ($2.1/WDC) in 2015. • The lowest 20th percentile fell from $2.3/WAC ($1.8/WDC) in 2014 to $2.2/WAC ($1.6/WDC) in 2015. • Capacity-weighted average prices were pushed higher in 2014 and 2015 by several very large projects that

had been under construction for several years (but only entered our sample once complete). • Installed prices are shown here in both DC and AC terms, but because AC is more relevant to the utility

sector, all metrics used in the rest of this slide deck are expressed solely in AC terms. • This sample is backward-looking and may not reflect the price of projects

built in 2016–2017. 29

Source: Bolinger, M. and J. Seel. 2016. Utility-Scale Solar 2015: An Empirical Analysis of Project Cost, Performance, and Pricing Trends in the United States. Berkeley, CA: Lawrence Berkeley National Laboratory

energy.gov/sunshot

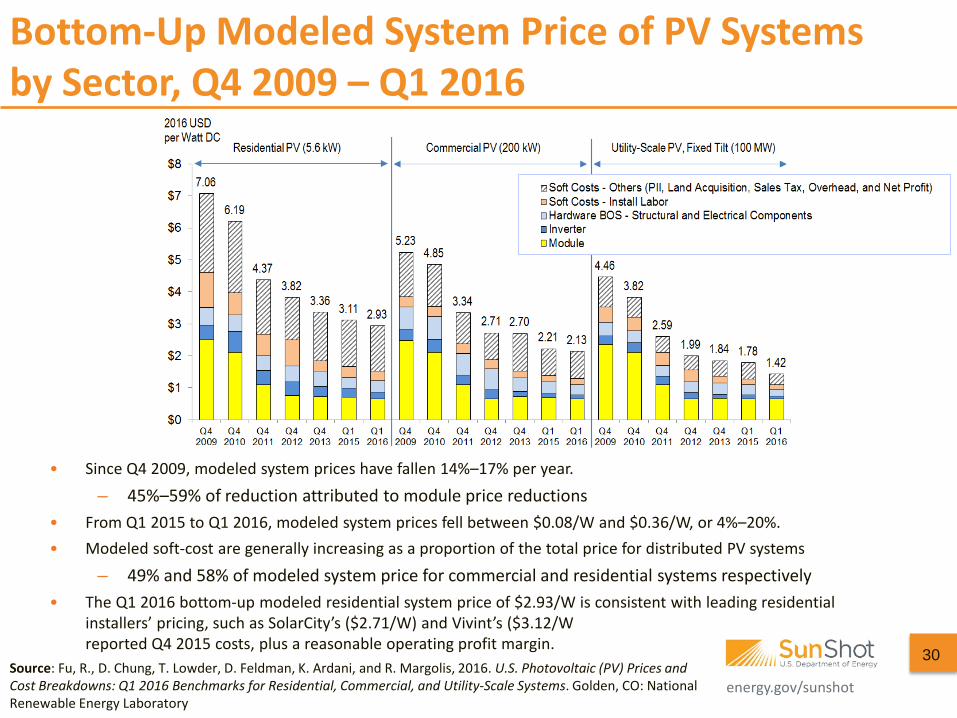

Bottom-Up Modeled System Price of PV Systems by Sector, Q4 2009 – Q1 2016

Source: Fu, R., D. Chung, T. Lowder, D. Feldman, K. Ardani, and R. Margolis, 2016. U.S. Photovoltaic (PV) Prices and Cost Breakdowns: Q1 2016 Benchmarks for Residential, Commercial, and Utility-Scale Systems. Golden, CO: National Renewable Energy Laboratory

• Since Q4 2009, modeled system prices have fallen 14%–17% per year.

– 45%–59% of reduction attributed to module price reductions • From Q1 2015 to Q1 2016, modeled system prices fell between $0.08/W and $0.36/W, or 4%–20%. • Modeled soft-cost are generally increasing as a proportion of the total price for distributed PV systems

– 49% and 58% of modeled system price for commercial and residential systems respectively • The Q1 2016 bottom-up modeled residential system price of $2.93/W is consistent with leading residential

installers’ pricing, such as SolarCity’s ($2.71/W) and Vivint’s ($3.12/W reported Q4 2015 costs, plus a reasonable operating profit margin.

30

energy.gov/sunshot

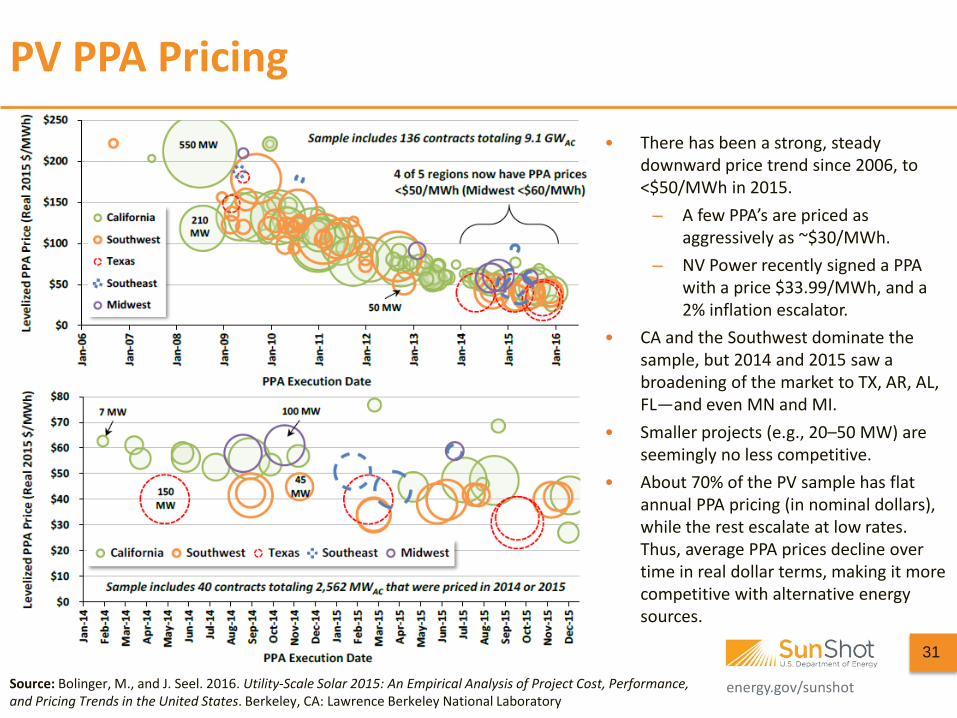

PV PPA Pricing

• There has been a strong, steady downward price trend since 2006, to <$50/MWh in 2015.

– A few PPA’s are priced as aggressively as ~$30/MWh.

– NV Power recently signed a PPA with a price $33.99/MWh, and a 2% inflation escalator.

• CA and the Southwest dominate the sample, but 2014 and 2015 saw a broadening of the market to TX, AR, AL, FL—and even MN and MI.

• Smaller projects (e.g., 20–50 MW) are seemingly no less competitive.

• About 70% of the PV sample has flat annual PPA pricing (in nominal dollars), while the rest escalate at low rates. Thus, average PPA prices decline over time in real dollar terms, making it more competitive with alternative energy sources.

Source: Bolinger, M., and J. Seel. 2016. Utility-Scale Solar 2015: An Empirical Analysis of Project Cost, Performance, and Pricing Trends in the United States. Berkeley, CA: Lawrence Berkeley National Laboratory

31

energy.gov/sunshot

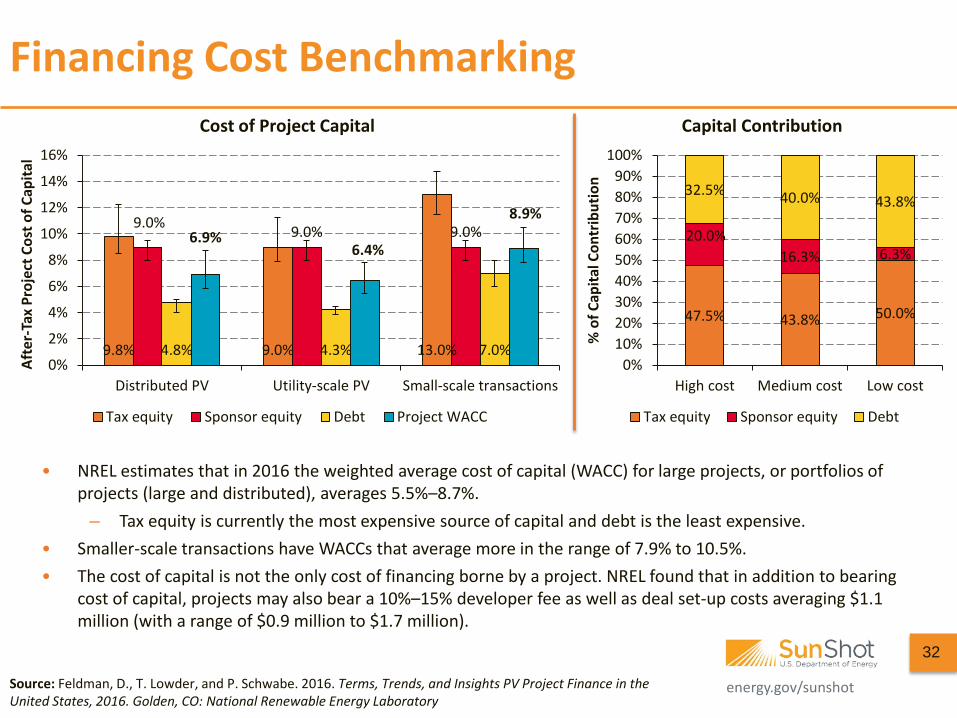

Financing Cost Benchmarking

• NREL estimates that in 2016 the weighted average cost of capital (WACC) for large projects, or portfolios of projects (large and distributed), averages 5.5%–8.7%.

– Tax equity is currently the most expensive source of capital and debt is the least expensive. • Smaller-scale transactions have WACCs that average more in the range of 7.9% to 10.5%. • The cost of capital is not the only cost of financing borne by a project. NREL found that in addition to bearing

cost of capital, projects may also bear a 10%–15% developer fee as well as deal set-up costs averaging $1.1 million (with a range of $0.9 million to $1.7 million).

Source: Feldman, D., T. Lowder, and P. Schwabe. 2016. Terms, Trends, and Insights PV Project Finance in the United States, 2016. Golden, CO: National Renewable Energy Laboratory

9.8% 9.0% 13.0%

9.0% 9.0% 9.0%

4.8% 4.3% 7.0%

6.9% 6.4%

8.9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Distributed PV Utility-scale PV Small-scale transactions

Afte

r-Ta

x Pr

ojec

t Cos

t of C

apita

l

Cost of Project Capital

Tax equity Sponsor equity Debt Project WACC

47.5% 43.8% 50.0%

20.0% 16.3% 6.3%

32.5% 40.0% 43.8%

0%10%20%30%40%50%60%70%80%90%

100%

High cost Medium cost Low cost

% o

f Cap

ital C

ontr

ibut

ion

Capital Contribution

Tax equity Sponsor equity Debt

32

energy.gov/sunshot

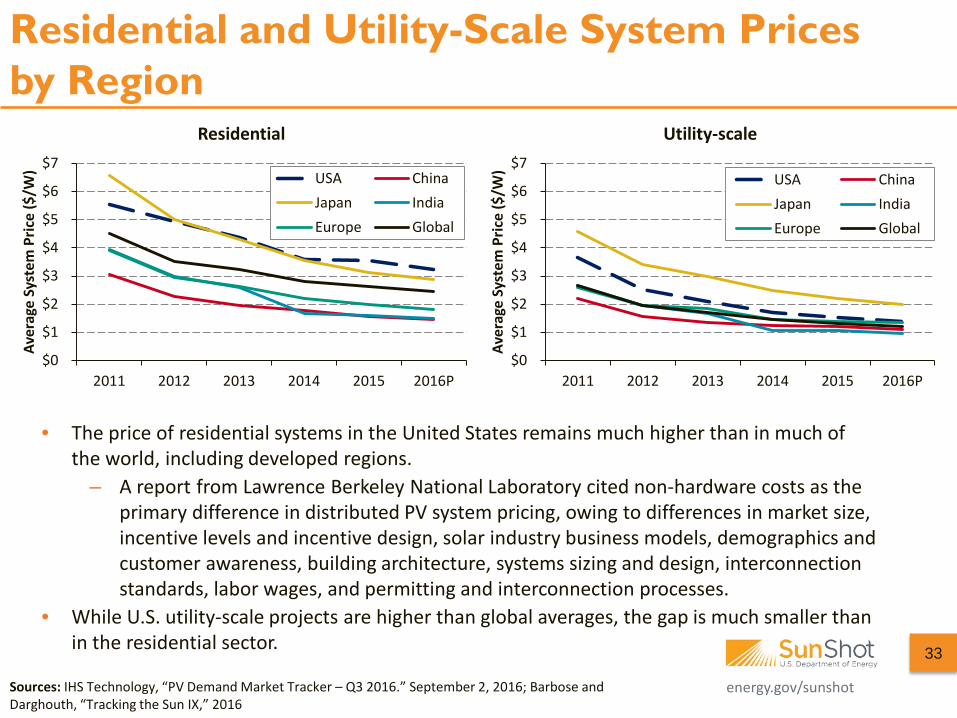

Residential and Utility-Scale System Prices by Region

33

• The price of residential systems in the United States remains much higher than in much of the world, including developed regions.

– A report from Lawrence Berkeley National Laboratory cited non-hardware costs as the primary difference in distributed PV system pricing, owing to differences in market size, incentive levels and incentive design, solar industry business models, demographics and customer awareness, building architecture, systems sizing and design, interconnection standards, labor wages, and permitting and interconnection processes.

• While U.S. utility-scale projects are higher than global averages, the gap is much smaller than in the residential sector.

Sources: IHS Technology, “PV Demand Market Tracker – Q3 2016.” September 2, 2016; Barbose and Darghouth, “Tracking the Sun IX,” 2016

$0

$1

$2

$3

$4

$5

$6

$7

2011 2012 2013 2014 2015 2016P

Aver

age

Syst

em P

rice

($/W

)

Residential

USA ChinaJapan IndiaEurope Global

$0

$1

$2

$3

$4

$5

$6

$7

2011 2012 2013 2014 2015 2016P

Aver

age

Syst

em P

rice

($/W

)

Utility-scale

USA ChinaJapan IndiaEurope Global

energy.gov/sunshot

Agenda

34

• Global Deployment • U.S. Deployment • U.S. Pricing • Global Manufacturing • Component Pricing • Market Activity • Tax Credit Availability

energy.gov/sunshot

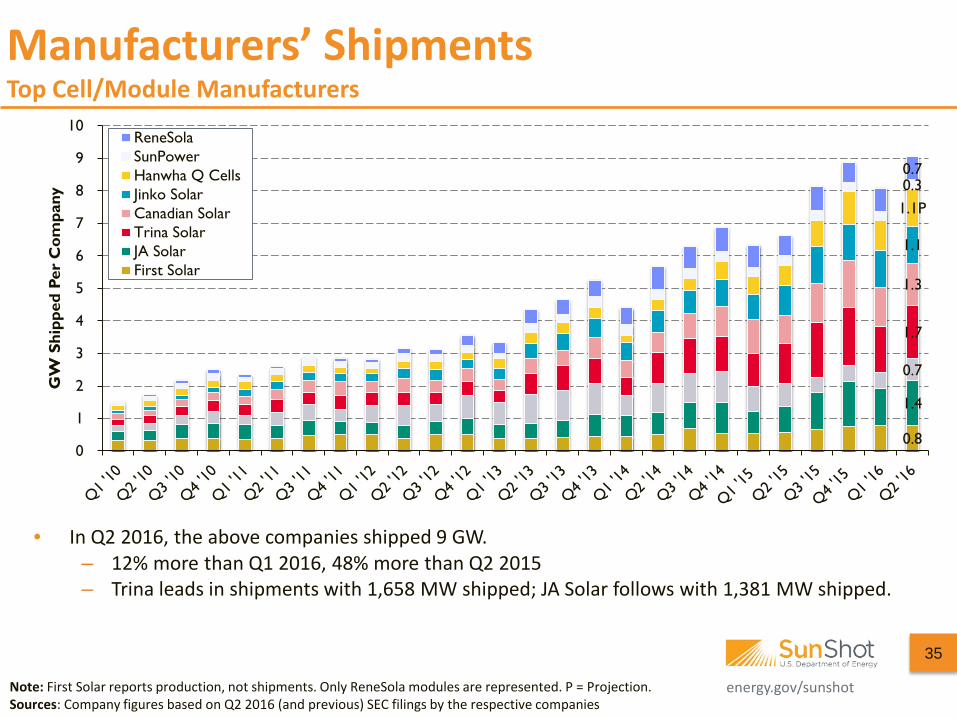

35

Note: First Solar reports production, not shipments. Only ReneSola modules are represented. P = Projection. Sources: Company figures based on Q2 2016 (and previous) SEC filings by the respective companies

Manufacturers’ Shipments Top Cell/Module Manufacturers

• In Q2 2016, the above companies shipped 9 GW. – 12% more than Q1 2016, 48% more than Q2 2015 – Trina leads in shipments with 1,658 MW shipped; JA Solar follows with 1,381 MW shipped.

0.8

1.4

0.7

1.7

1.3

1.1

1.1P 0.3 0.7

0

1

2

3

4

5

6

7

8

9

10

GW

Shi

pped

Per

Com

pany

ReneSolaSunPowerHanwha Q CellsJinko SolarCanadian SolarTrina SolarJA SolarFirst Solar

energy.gov/sunshot energy.gov/sunshot

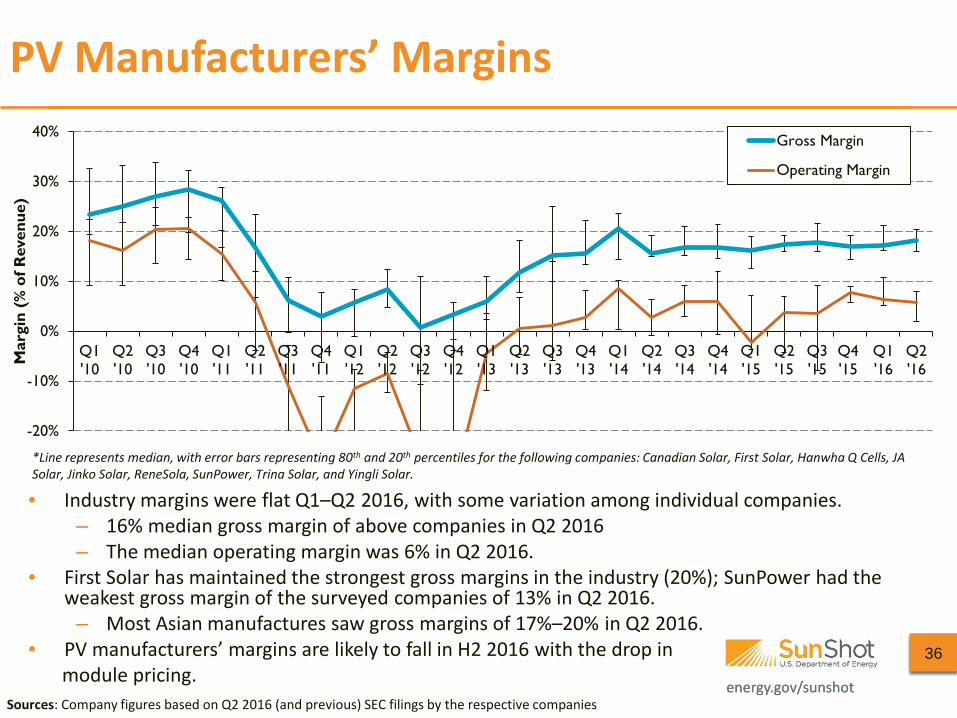

PV Manufacturers’ Margins

• Industry margins were flat Q1–Q2 2016, with some variation among individual companies. – 16% median gross margin of above companies in Q2 2016 – The median operating margin was 6% in Q2 2016.

• First Solar has maintained the strongest gross margins in the industry (20%); SunPower had the weakest gross margin of the surveyed companies of 13% in Q2 2016.

– Most Asian manufactures saw gross margins of 17%–20% in Q2 2016. • PV manufacturers’ margins are likely to fall in H2 2016 with the drop in module pricing.

36

Sources: Company figures based on Q2 2016 (and previous) SEC filings by the respective companies

*Line represents median, with error bars representing 80th and 20th percentiles for the following companies: Canadian Solar, First Solar, Hanwha Q Cells, JA Solar, Jinko Solar, ReneSola, SunPower, Trina Solar, and Yingli Solar.

-20%

-10%

0%

10%

20%

30%

40%

Q1'10

Q2'10

Q3'10

Q4'10

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

Q2'12

Q3'12

Q4'12

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Q1'15

Q2'15

Q3'15

Q4'15

Q1'16

Q2'16

Mar

gin

(% o

f Rev

enue

)

Gross Margin

Operating Margin

energy.gov/sunshot energy.gov/sunshot

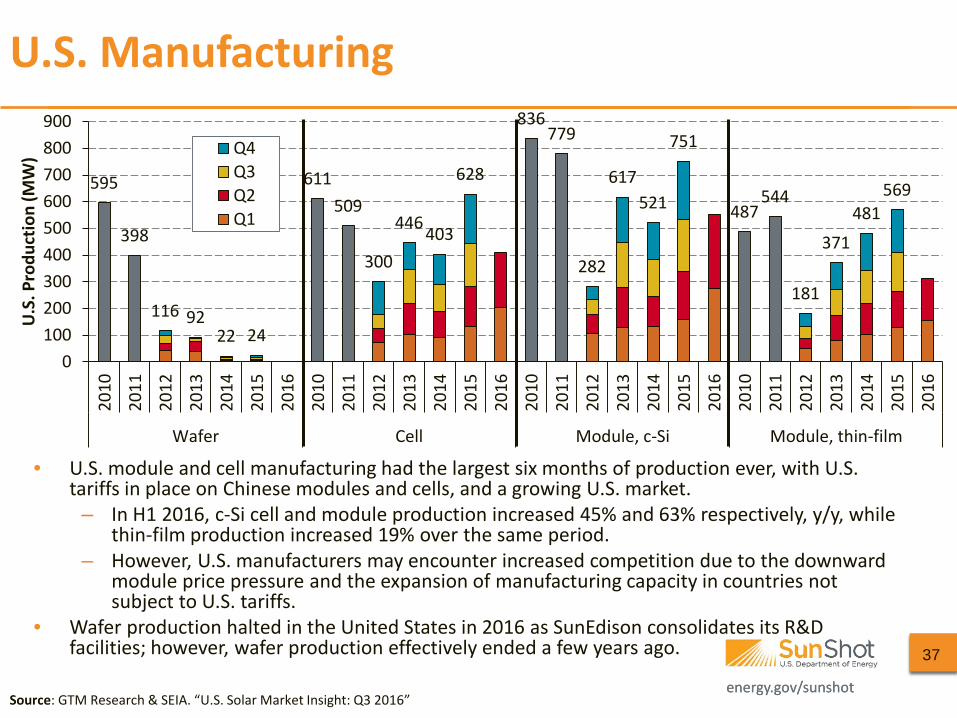

• U.S. module and cell manufacturing had the largest six months of production ever, with U.S. tariffs in place on Chinese modules and cells, and a growing U.S. market.

– In H1 2016, c-Si cell and module production increased 45% and 63% respectively, y/y, while thin-film production increased 19% over the same period.

– However, U.S. manufacturers may encounter increased competition due to the downward module price pressure and the expansion of manufacturing capacity in countries not subject to U.S. tariffs.

• Wafer production halted in the United States in 2016 as SunEdison consolidates its R&D facilities; however, wafer production effectively ended a few years ago.

U.S. Manufacturing

37

Source: GTM Research & SEIA. “U.S. Solar Market Insight: Q3 2016”

595

398

116 92 22 24

611 509

300

446 403

628

836 779

282

617 521

751

487 544

181

371 481

569

0100200300400500600700800900

2010

2011

2012

2013

2014

2015

2016

2010

2011

2012

2013

2014

2015

2016

2010

2011

2012

2013

2014

2015

2016

2010

2011

2012

2013

2014

2015

2016

Wafer Cell Module, c-Si Module, thin-film

U.S

. Pro

duct

ion

(MW

) Q4Q3Q2Q1

energy.gov/sunshot energy.gov/sunshot

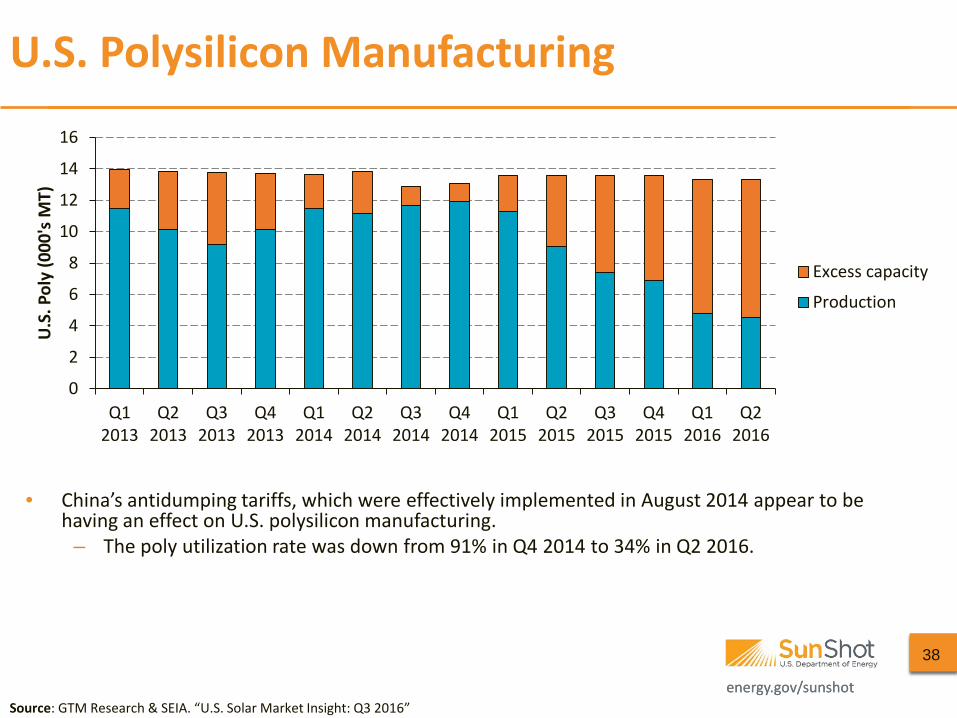

• China’s antidumping tariffs, which were effectively implemented in August 2014 appear to be having an effect on U.S. polysilicon manufacturing.

– The poly utilization rate was down from 91% in Q4 2014 to 34% in Q2 2016.

U.S. Polysilicon Manufacturing

38

Source: GTM Research & SEIA. “U.S. Solar Market Insight: Q3 2016”

0

2

4

6

8

10

12

14

16

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

U.S

. Pol

y (0

00's

MT)

Excess capacity

Production

energy.gov/sunshot

Agenda

39

• Global Deployment • U.S. Deployment • U.S. Pricing • Global Manufacturing • Component Pricing • Market Activity • Tax Credit Availability

energy.gov/sunshot energy.gov/sunshot

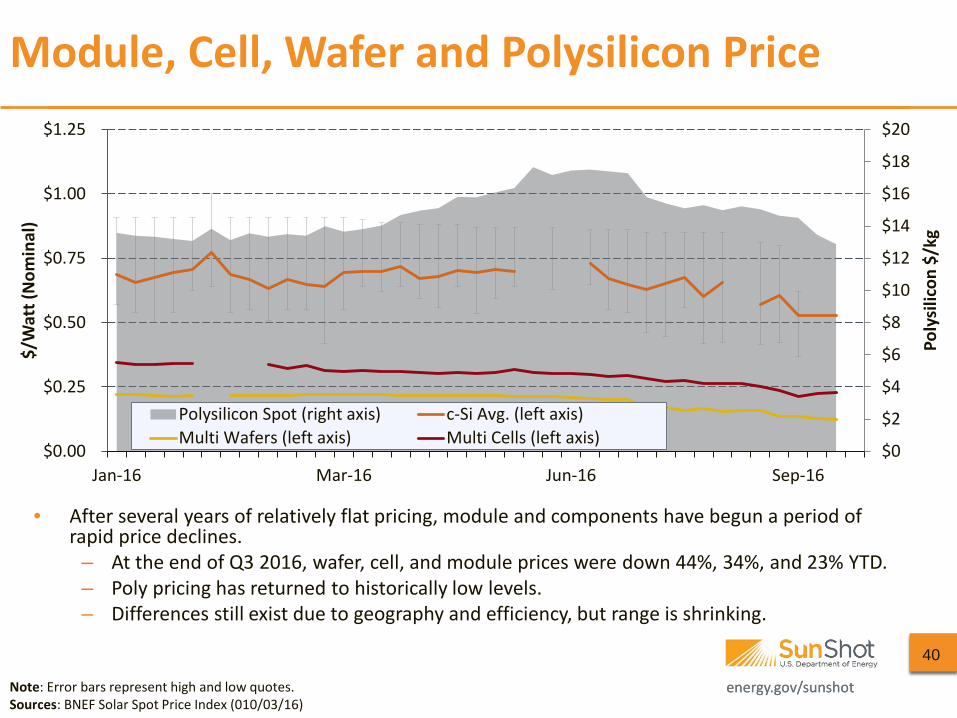

• After several years of relatively flat pricing, module and components have begun a period of rapid price declines.

– At the end of Q3 2016, wafer, cell, and module prices were down 44%, 34%, and 23% YTD. – Poly pricing has returned to historically low levels. – Differences still exist due to geography and efficiency, but range is shrinking.

Module, Cell, Wafer and Polysilicon Price

40

Note: Error bars represent high and low quotes. Sources: BNEF Solar Spot Price Index (010/03/16)

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

$0.00

$0.25

$0.50

$0.75

$1.00

$1.25

Jan-16 Mar-16 Jun-16 Sep-16

Poly

silic

on $

/kg

$/W

att (

Nom

inal

)

Polysilicon Spot (right axis) c-Si Avg. (left axis)Multi Wafers (left axis) Multi Cells (left axis)

energy.gov/sunshot

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

($5)

($4)

($3)

($2)

($1)

$0

$1

$2

$3

$4

$5

Q1 '07 Q1 '08 Q1 '09 Q1 '10 Q1 '11 Q1 '12 Q1 '13 Q1 '14 Q1 '15 Q1 '16

% R

educ

tion

in m

odul

e A

SP, Q

/Q

$/W

att

(Nom

inal

)

% reduction in ASP, Q/Q

c-Si module ASP

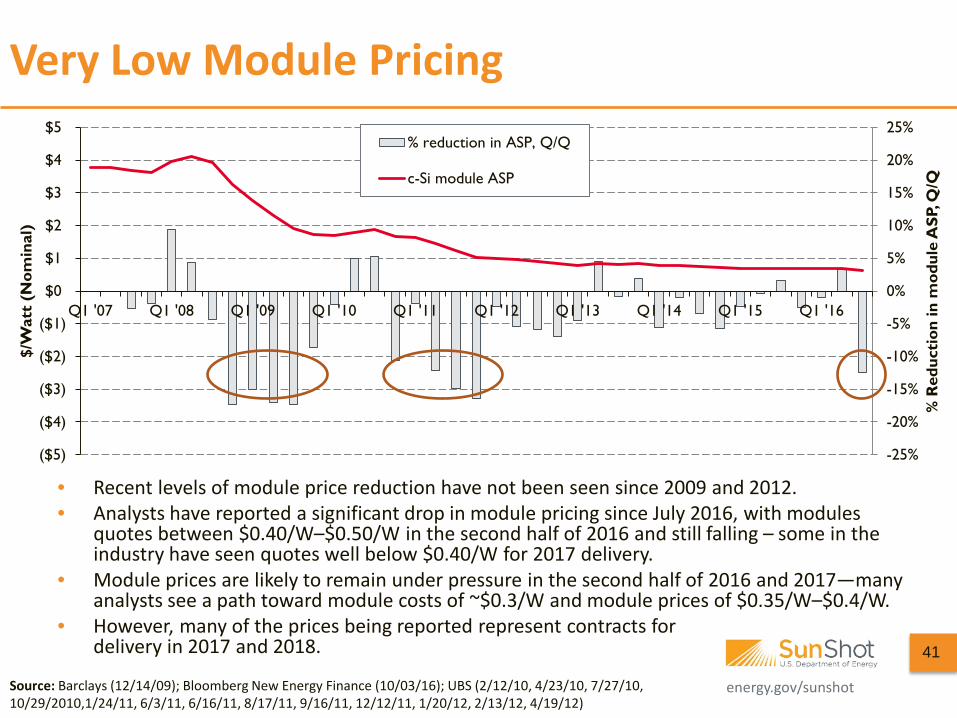

• Recent levels of module price reduction have not been seen since 2009 and 2012. • Analysts have reported a significant drop in module pricing since July 2016, with modules

quotes between $0.40/W–$0.50/W in the second half of 2016 and still falling – some in the industry have seen quotes well below $0.40/W for 2017 delivery.

• Module prices are likely to remain under pressure in the second half of 2016 and 2017—many analysts see a path toward module costs of ~$0.3/W and module prices of $0.35/W–$0.4/W.

• However, many of the prices being reported represent contracts for delivery in 2017 and 2018.

Very Low Module Pricing

Source: Barclays (12/14/09); Bloomberg New Energy Finance (10/03/16); UBS (2/12/10, 4/23/10, 7/27/10, 10/29/2010,1/24/11, 6/3/11, 6/16/11, 8/17/11, 9/16/11, 12/12/11, 1/20/12, 2/13/12, 4/19/12)

41

energy.gov/sunshot

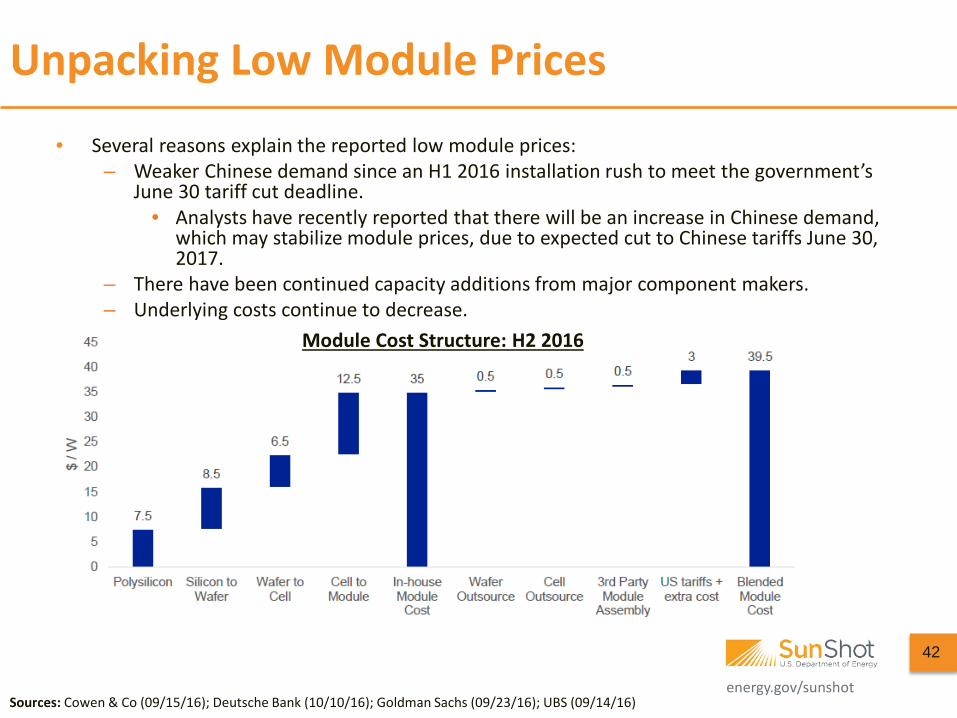

• Several reasons explain the reported low module prices: – Weaker Chinese demand since an H1 2016 installation rush to meet the government’s

June 30 tariff cut deadline. • Analysts have recently reported that there will be an increase in Chinese demand,

which may stabilize module prices, due to expected cut to Chinese tariffs June 30, 2017.

– There have been continued capacity additions from major component makers. – Underlying costs continue to decrease.

Unpacking Low Module Prices

Sources: Cowen & Co (09/15/16); Deutsche Bank (10/10/16); Goldman Sachs (09/23/16); UBS (09/14/16)

Module Cost Structure: H2 2016

42

energy.gov/sunshot

PV Manufacturers’ Cost

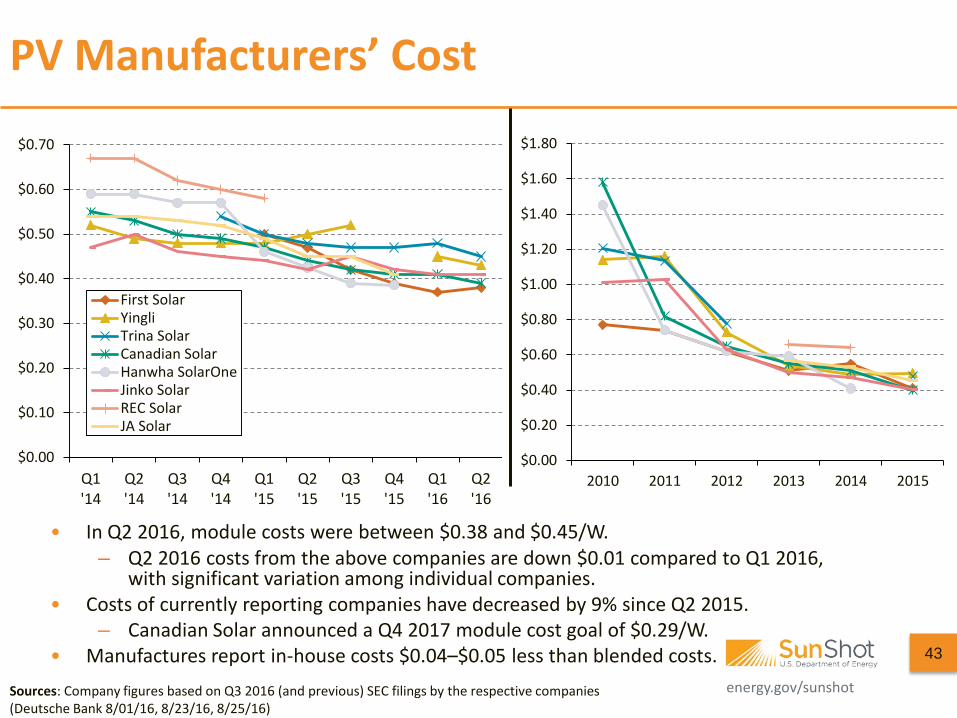

• In Q2 2016, module costs were between $0.38 and $0.45/W. – Q2 2016 costs from the above companies are down $0.01 compared to Q1 2016,

with significant variation among individual companies. • Costs of currently reporting companies have decreased by 9% since Q2 2015.

– Canadian Solar announced a Q4 2017 module cost goal of $0.29/W. • Manufactures report in-house costs $0.04–$0.05 less than blended costs. 43

Sources: Company figures based on Q3 2016 (and previous) SEC filings by the respective companies (Deutsche Bank 8/01/16, 8/23/16, 8/25/16)

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

2010 2011 2012 2013 2014 2015$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

Q1'14

Q2'14

Q3'14

Q4'14

Q1'15

Q2'15

Q3'15

Q4'15

Q1'16

Q2'16

First SolarYingliTrina SolarCanadian SolarHanwha SolarOneJinko SolarREC SolarJA Solar

energy.gov/sunshot

Near-Term Module Price/Cost Projections

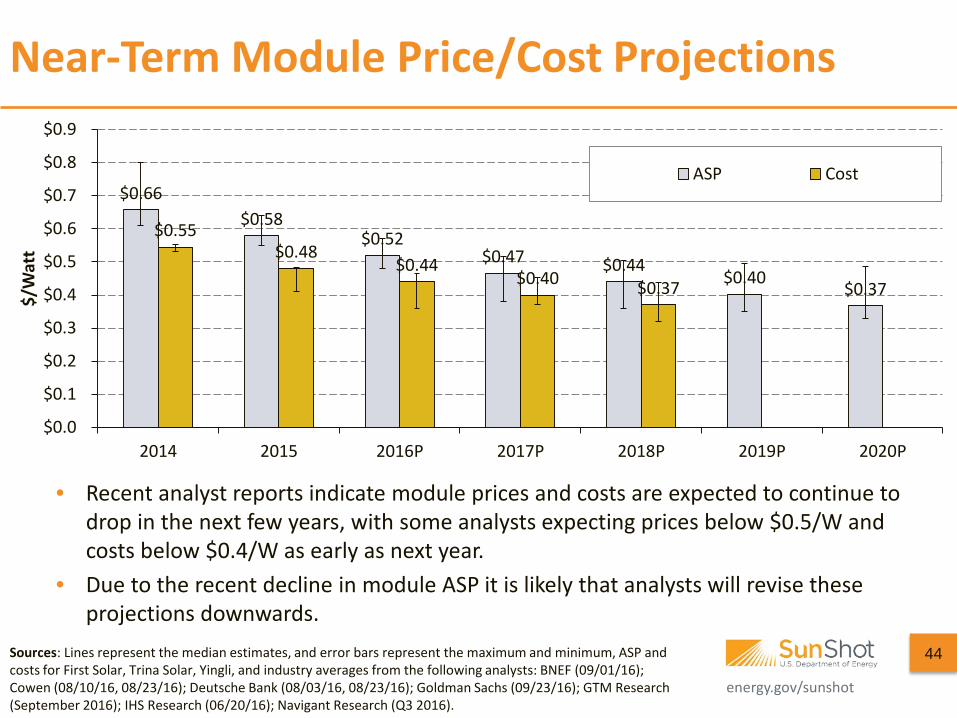

44 Sources: Lines represent the median estimates, and error bars represent the maximum and minimum, ASP and costs for First Solar, Trina Solar, Yingli, and industry averages from the following analysts: BNEF (09/01/16); Cowen (08/10/16, 08/23/16); Deutsche Bank (08/03/16, 08/23/16); Goldman Sachs (09/23/16); GTM Research (September 2016); IHS Research (06/20/16); Navigant Research (Q3 2016).

• Recent analyst reports indicate module prices and costs are expected to continue to drop in the next few years, with some analysts expecting prices below $0.5/W and costs below $0.4/W as early as next year.

• Due to the recent decline in module ASP it is likely that analysts will revise these projections downwards.

$0.66 $0.58

$0.52 $0.47 $0.44

$0.40 $0.37

$0.55 $0.48

$0.44 $0.40 $0.37

$0.0

$0.1

$0.2

$0.3

$0.4

$0.5

$0.6

$0.7

$0.8

$0.9

2014 2015 2016P 2017P 2018P 2019P 2020P

$/W

att

ASP Cost

energy.gov/sunshot

Inverter Pricing

45

Source: GTM/SEIA “Solar Market Insight Q3 2016”

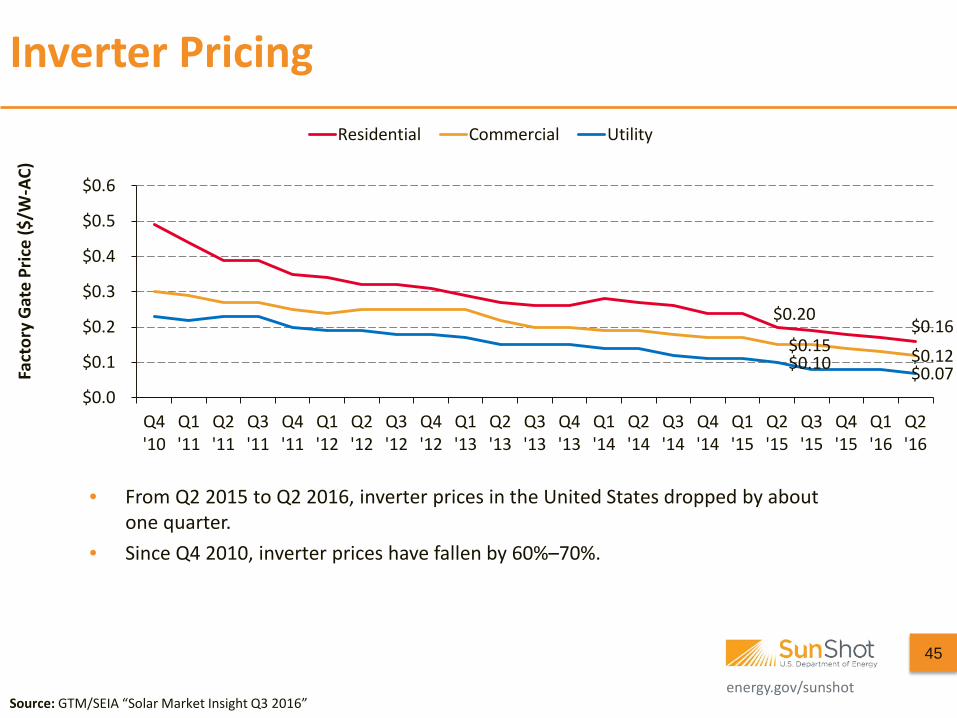

• From Q2 2015 to Q2 2016, inverter prices in the United States dropped by about one quarter.

• Since Q4 2010, inverter prices have fallen by 60%–70%.

$0.20 $0.16

$0.15 $0.12 $0.10 $0.07 $0.0

$0.1

$0.2

$0.3

$0.4

$0.5

$0.6

Q4'10

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

Q2'12

Q3'12

Q4'12

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Q1'15

Q2'15

Q3'15

Q4'15

Q1'16

Q2'16

Fact

ory

Gat

e Pr

ice

($/W

-AC)

Residential Commercial Utility

energy.gov/sunshot

Enphase Microinverters and SolarEdge DC Optimized Inverter Systems

46

Sources: Enphase/SolarEdge public filings; Cowen (05/03/16)

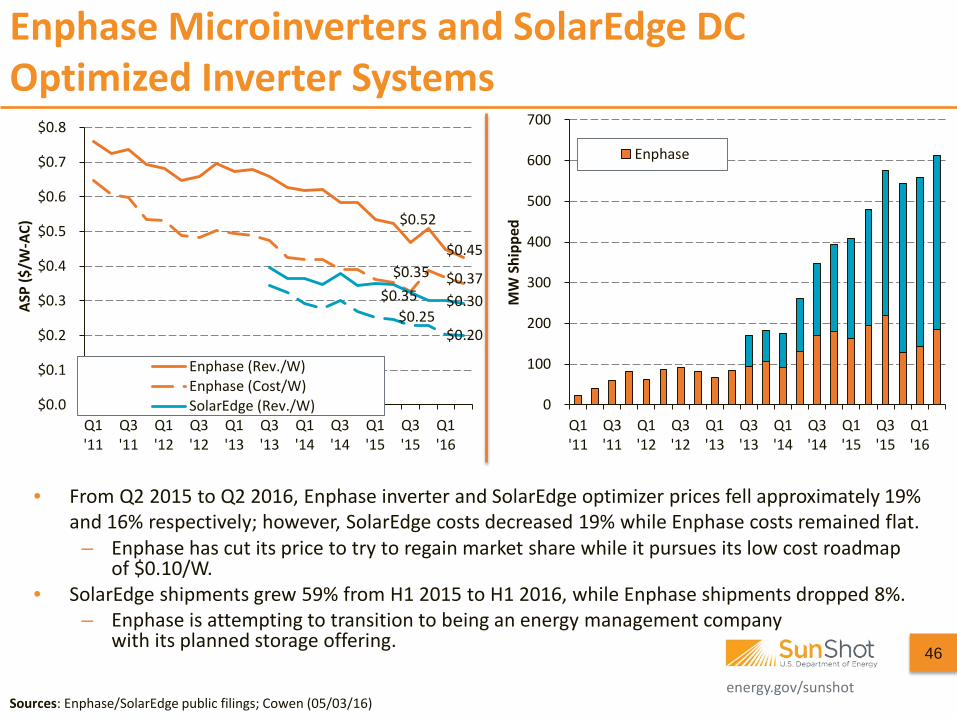

• From Q2 2015 to Q2 2016, Enphase inverter and SolarEdge optimizer prices fell approximately 19% and 16% respectively; however, SolarEdge costs decreased 19% while Enphase costs remained flat.

– Enphase has cut its price to try to regain market share while it pursues its low cost roadmap of $0.10/W.

• SolarEdge shipments grew 59% from H1 2015 to H1 2016, while Enphase shipments dropped 8%. – Enphase is attempting to transition to being an energy management company

with its planned storage offering.

0

100

200

300

400

500

600

700

Q1'11

Q3'11

Q1'12

Q3'12

Q1'13

Q3'13

Q1'14

Q3'14

Q1'15

Q3'15

Q1'16

MW

Shi

pped

Enphase

$0.52

$0.45 $0.35 $0.37

$0.35 $0.30 $0.25

$0.20

$0.0

$0.1

$0.2

$0.3

$0.4

$0.5

$0.6

$0.7

$0.8

Q1'11

Q3'11

Q1'12

Q3'12

Q1'13

Q3'13

Q1'14

Q3'14

Q1'15

Q3'15

Q1'16

ASP

($/W

-AC)

Enphase (Rev./W)Enphase (Cost/W)SolarEdge (Rev./W)

energy.gov/sunshot

Agenda

47

• Global Deployment • U.S. Deployment • U.S. Pricing • Global Manufacturing • Component Pricing • Market Activity • Tax Credit Availability

energy.gov/sunshot

SREC Markets

Source: Blog, SRECTrade, www.srectrade.com (accessed Sept ember 30, 2016)

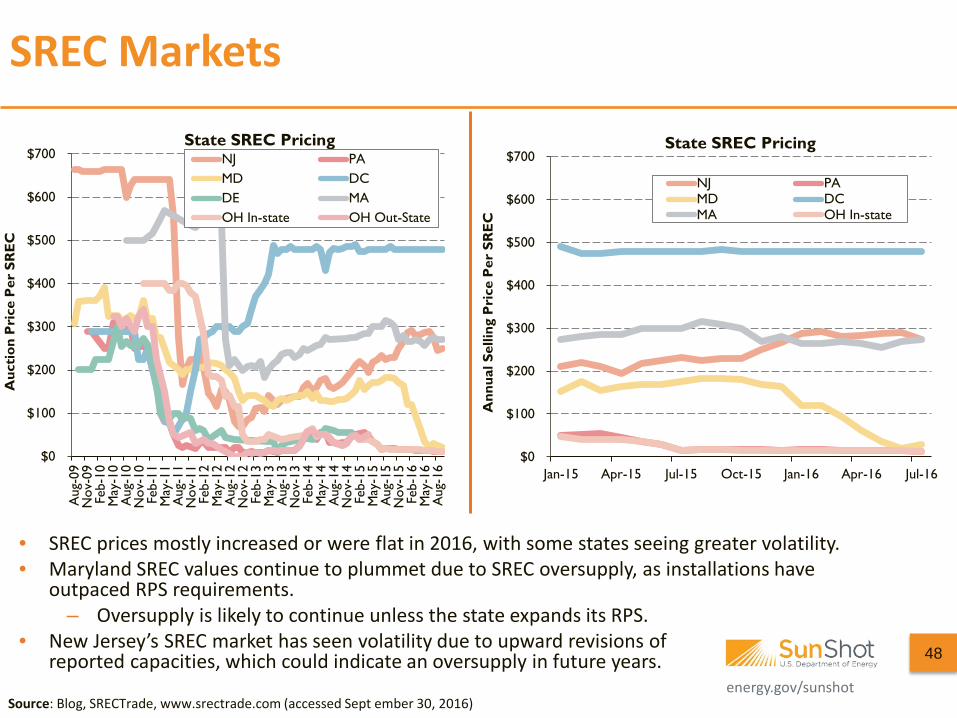

• SREC prices mostly increased or were flat in 2016, with some states seeing greater volatility. • Maryland SREC values continue to plummet due to SREC oversupply, as installations have

outpaced RPS requirements. – Oversupply is likely to continue unless the state expands its RPS.

• New Jersey’s SREC market has seen volatility due to upward revisions of reported capacities, which could indicate an oversupply in future years.

48

$0

$100

$200

$300

$400

$500

$600

$700

Aug

-09

Nov

-09

Feb-

10M

ay-1

0A

ug-1

0N

ov-1

0Fe

b-11

May

-11

Aug

-11

Nov

-11

Feb-

12M

ay-1

2A

ug-1

2N

ov-1

2Fe

b-13

May

-13

Aug

-13

Nov

-13

Feb-

14M

ay-1

4A

ug-1

4N

ov-1

4Fe

b-15

May

-15

Aug

-15

Nov

-15

Feb-

16M

ay-1

6A

ug-1

6

Auc

tion

Pri

ce P

er S

RE

C

State SREC Pricing NJ PAMD DCDE MAOH In-state OH Out-State

$0

$100

$200

$300

$400

$500

$600

$700

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16A

nnua

l Sel

ling

Pri

ce P

er S

RE

C

State SREC Pricing

NJ PAMD DCMA OH In-state

energy.gov/sunshot

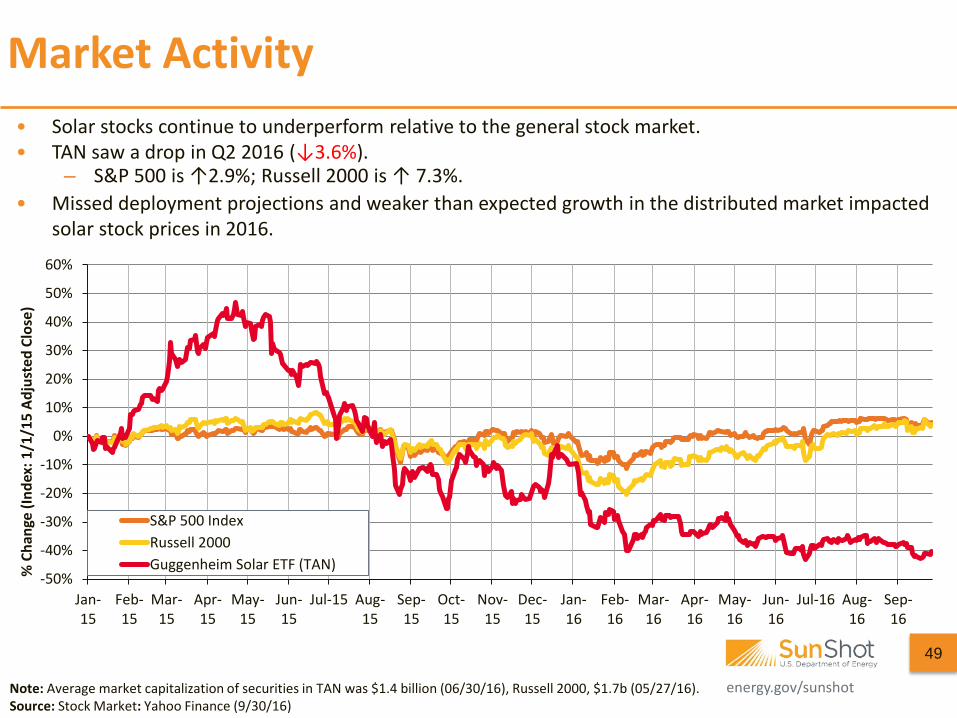

Market Activity • Solar stocks continue to underperform relative to the general stock market. • TAN saw a drop in Q2 2016 (↓3.6%).

– S&P 500 is ↑2.9%; Russell 2000 is ↑ 7.3%. • Missed deployment projections and weaker than expected growth in the distributed market impacted

solar stock prices in 2016.

Note: Average market capitalization of securities in TAN was $1.4 billion (06/30/16), Russell 2000, $1.7b (05/27/16). Source: Stock Market: Yahoo Finance (9/30/16)

49

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-15 Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16 Aug-16

Sep-16

% C

hang

e (In

dex:

1/1

/15

Adju

sted

Clo

se)

S&P 500 IndexRussell 2000Guggenheim Solar ETF (TAN)

energy.gov/sunshot

Agenda

50

• Global Deployment • U.S. Deployment • U.S. Pricing • Global Manufacturing • Component Pricing • Market Activity • Tax Credit Availability

energy.gov/sunshot

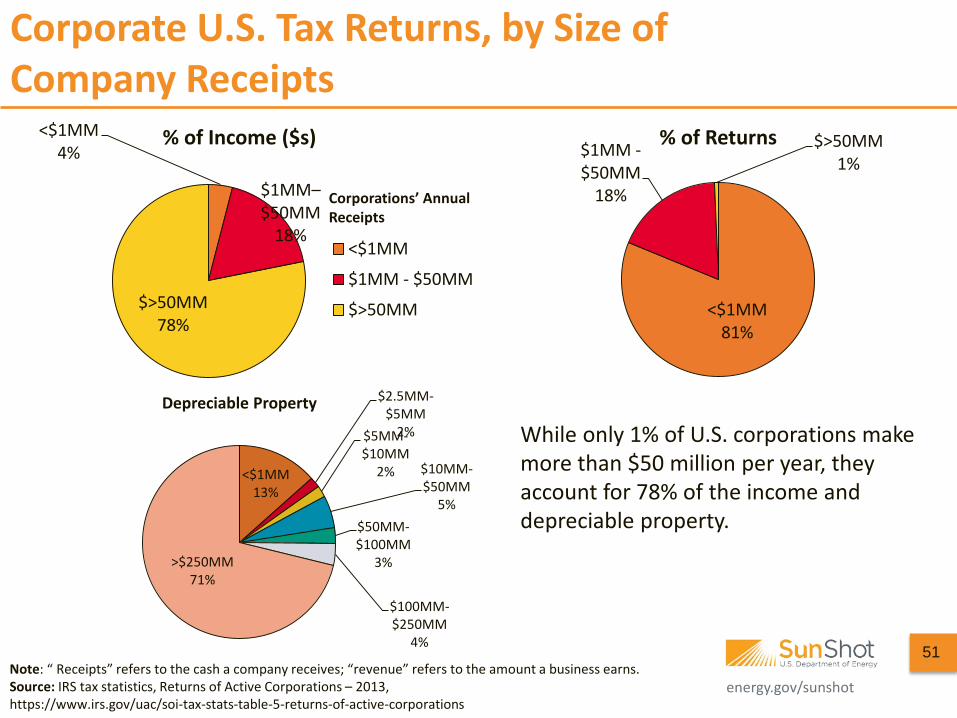

Corporate U.S. Tax Returns, by Size of Company Receipts

<$1MM 81%

$1MM - $50MM

18%

$>50MM 1%

% of Returns <$1MM 4%

$1MM–$50MM

18%

$>50MM 78%

% of Income ($s)

<$1MM

$1MM - $50MM

$>50MM

Corporations’ Annual Receipts

While only 1% of U.S. corporations make more than $50 million per year, they account for 78% of the income and depreciable property.

Note: “ Receipts” refers to the cash a company receives; “revenue” refers to the amount a business earns. Source: IRS tax statistics, Returns of Active Corporations – 2013, https://www.irs.gov/uac/soi-tax-stats-table-5-returns-of-active-corporations

<$1MM 13%

$2.5MM-$5MM

2% $5MM-$10MM

2% $10MM-$50MM

5% $50MM-$100MM

3%

$100MM-$250MM

4%

>$250MM 71%

Depreciable Property

51

energy.gov/sunshot

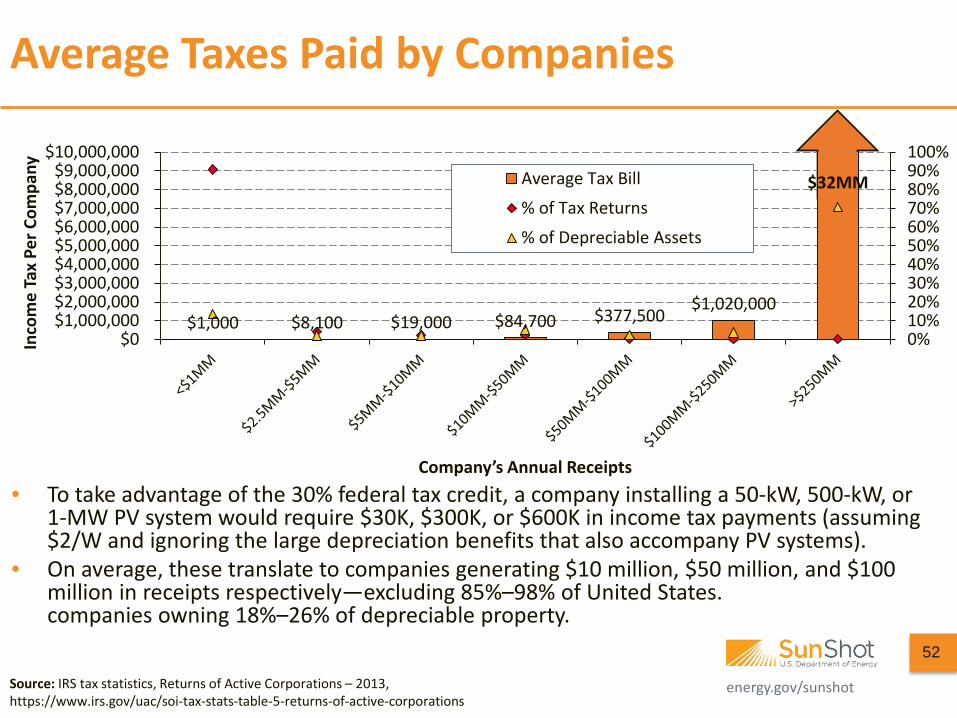

$1,000 $8,100 $19,000 $84,700 $377,500 $1,020,000

0%10%20%30%40%50%60%70%80%90%100%

$0$1,000,000$2,000,000$3,000,000$4,000,000$5,000,000$6,000,000$7,000,000$8,000,000$9,000,000

$10,000,000

Inco

me

Tax

Per C

ompa

ny

Company’s Annual Receipts

Average Tax Bill

% of Tax Returns

% of Depreciable Assets

Average Taxes Paid by Companies

• To take advantage of the 30% federal tax credit, a company installing a 50-kW, 500-kW, or 1-MW PV system would require $30K, $300K, or $600K in income tax payments (assuming $2/W and ignoring the large depreciation benefits that also accompany PV systems).

• On average, these translate to companies generating $10 million, $50 million, and $100 million in receipts respectively—excluding 85%–98% of United States. companies owning 18%–26% of depreciable property.

Source: IRS tax statistics, Returns of Active Corporations – 2013, https://www.irs.gov/uac/soi-tax-stats-table-5-returns-of-active-corporations

$32MM

52

energy.gov/sunshot

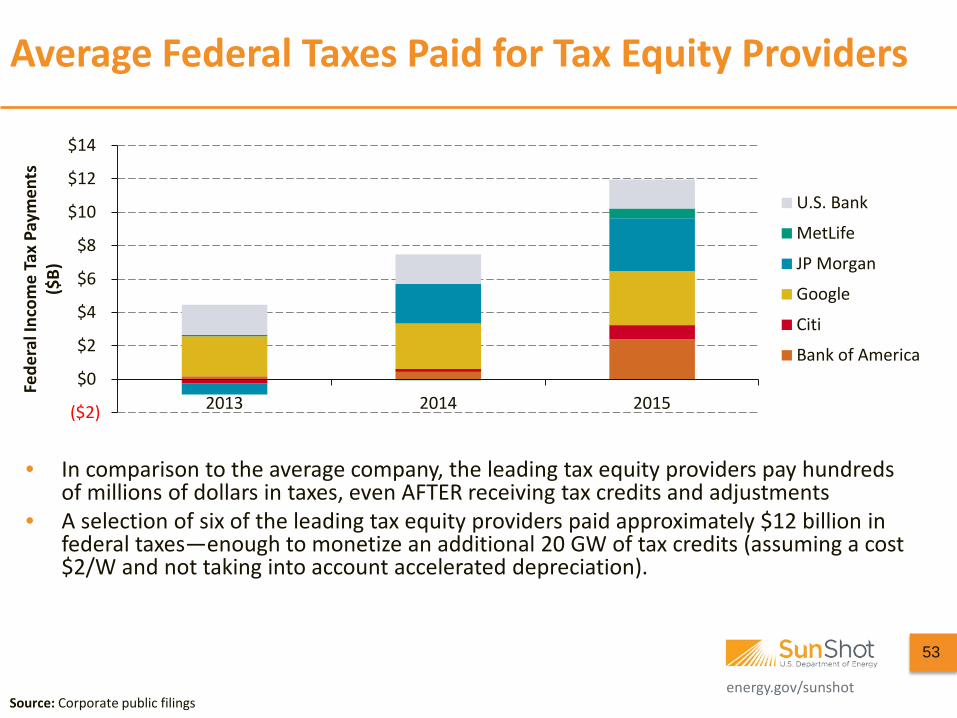

Average Federal Taxes Paid for Tax Equity Providers

• In comparison to the average company, the leading tax equity providers pay hundreds of millions of dollars in taxes, even AFTER receiving tax credits and adjustments

• A selection of six of the leading tax equity providers paid approximately $12 billion in federal taxes—enough to monetize an additional 20 GW of tax credits (assuming a cost $2/W and not taking into account accelerated depreciation).

Source: Corporate public filings

($2)

$0

$2

$4

$6

$8

$10

$12

$14

2013 2014 2015

Fede

ral I

ncom

e Ta

x Pa

ymen

ts

($B)

U.S. Bank

MetLife

JP Morgan

Citi

Bank of America

53

energy.gov/sunshot

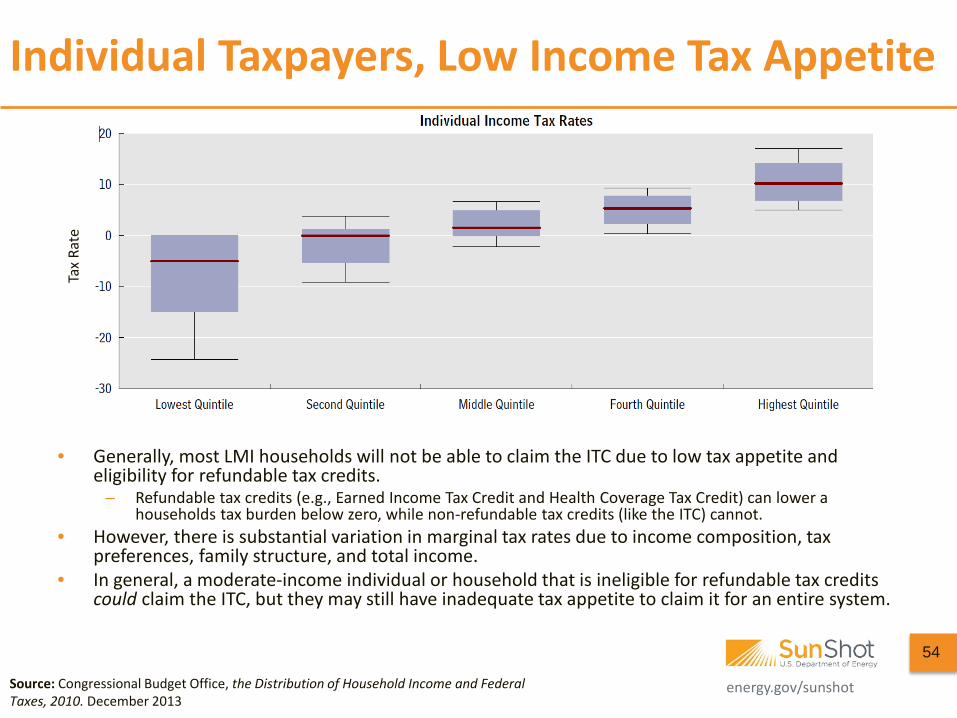

Individual Taxpayers, Low Income Tax Appetite

• Generally, most LMI households will not be able to claim the ITC due to low tax appetite and eligibility for refundable tax credits.

– Refundable tax credits (e.g., Earned Income Tax Credit and Health Coverage Tax Credit) can lower a households tax burden below zero, while non-refundable tax credits (like the ITC) cannot.

• However, there is substantial variation in marginal tax rates due to income composition, tax preferences, family structure, and total income.

• In general, a moderate-income individual or household that is ineligible for refundable tax credits could claim the ITC, but they may still have inadequate tax appetite to claim it for an entire system.

Source: Congressional Budget Office, the Distribution of Household Income and Federal Taxes, 2010. December 2013

54

Tax

Rate

energy.gov/sunshot

Average Taxes Paid by Individuals

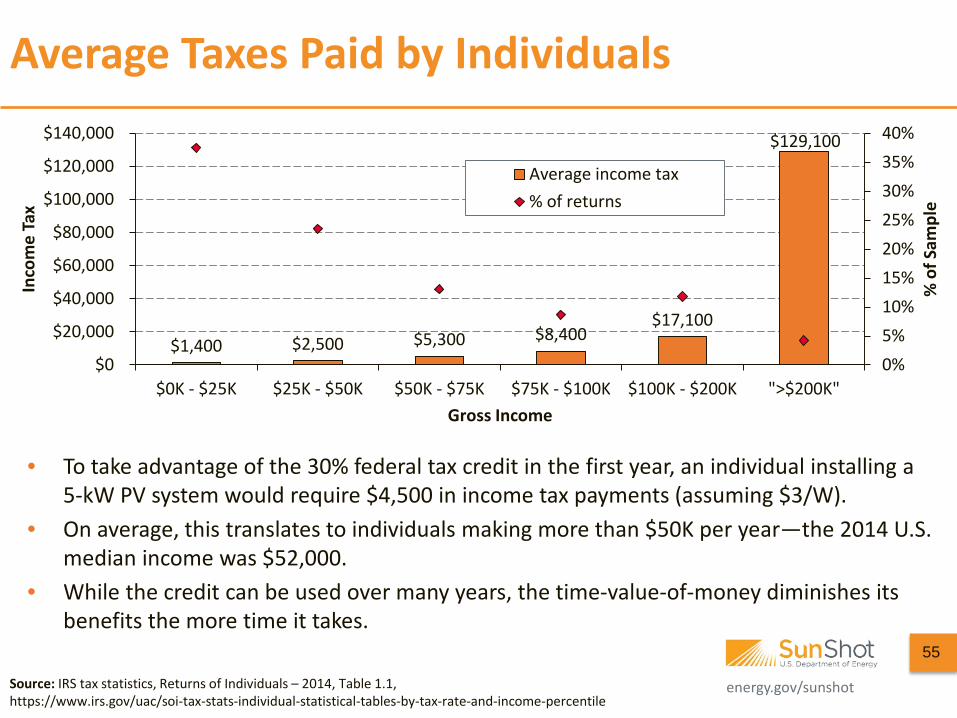

• To take advantage of the 30% federal tax credit in the first year, an individual installing a 5-kW PV system would require $4,500 in income tax payments (assuming $3/W).

• On average, this translates to individuals making more than $50K per year—the 2014 U.S. median income was $52,000.

• While the credit can be used over many years, the time-value-of-money diminishes its benefits the more time it takes.

Source: IRS tax statistics, Returns of Individuals – 2014, Table 1.1, https://www.irs.gov/uac/soi-tax-stats-individual-statistical-tables-by-tax-rate-and-income-percentile

55

$1,400 $2,500 $5,300 $8,400 $17,100

$129,100

0%5%10%15%20%25%30%35%40%

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$0K - $25K $25K - $50K $50K - $75K $75K - $100K $100K - $200K ">$200K"

% o

f Sam

ple

Inco

me

Tax

Gross Income

Average income tax% of returns

energy.gov/sunshot

David Feldman Senior Financial Analyst

National Renewable Energy Laboratory 202-488-2231

Daniel Boff Junior Energy Analyst

Contractor to the United States Department of Energy 202-287-1904

Robert Margolis Senior Analyst

National Renewable Energy Laboratory 202-488-2222

Thank You

The authors are highly indebted to the following individuals for their insights and contributions to this brief: Jenny Chase, BNEF; Jenny Heeter, NREL; Shayle Kann, GTM Research; Jeffrey Logan, NREL; Mike Meshek, NREL; David Mooney, NREL; Nathan Serota, BNEF; Edward Settle, NREL; MJ Shiao, GTM Research; Scott Stephens, NRG Energy, Inc.; Edurne Zoco, IHS

energy.gov/sunshot energy.gov/sunshot

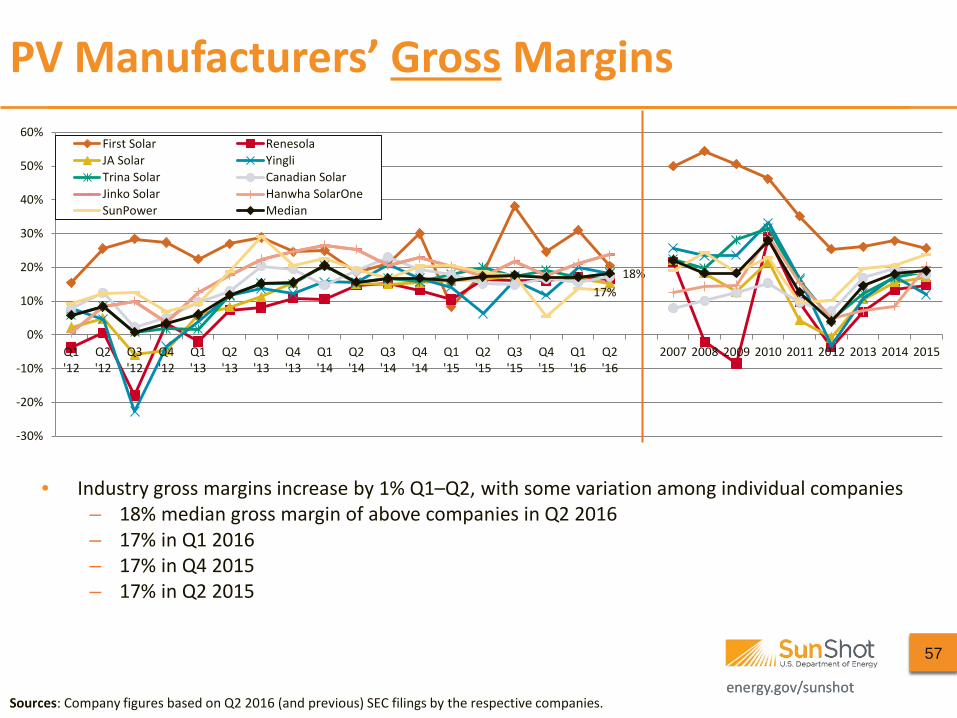

17% 18%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Q1'12

Q2'12

Q3'12

Q4'12

Q1'13

Q2'13

Q3'13

Q4'13

Q1'14

Q2'14

Q3'14

Q4'14

Q1'15

Q2'15

Q3'15

Q4'15

Q1'16

Q2'16

2007 2008 2009 2010 2011 2012 2013 2014 2015

First Solar RenesolaJA Solar YingliTrina Solar Canadian SolarJinko Solar Hanwha SolarOneSunPower Median

PV Manufacturers’ Gross Margins

Sources: Company figures based on Q2 2016 (and previous) SEC filings by the respective companies.

• Industry gross margins increase by 1% Q1–Q2, with some variation among individual companies – 18% median gross margin of above companies in Q2 2016 – 17% in Q1 2016 – 17% in Q4 2015 – 17% in Q2 2015

57

energy.gov/sunshot energy.gov/sunshot Sources: Company figures based on Q2 2016 (and previous) SEC filings by the surveyed companies.

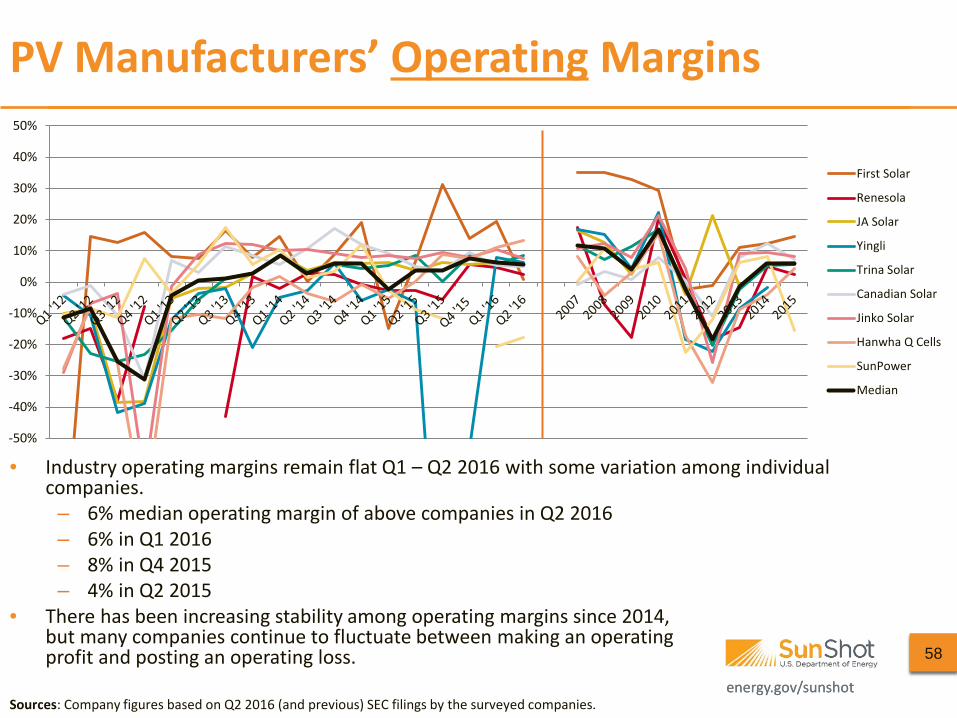

PV Manufacturers’ Operating Margins

• Industry operating margins remain flat Q1 – Q2 2016 with some variation among individual companies.

– 6% median operating margin of above companies in Q2 2016 – 6% in Q1 2016 – 8% in Q4 2015 – 4% in Q2 2015

• There has been increasing stability among operating margins since 2014, but many companies continue to fluctuate between making an operating profit and posting an operating loss. 58

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

First Solar

Renesola

JA Solar

Yingli

Trina Solar

Canadian Solar

Jinko Solar

Hanwha Q Cells

SunPower

Median

energy.gov/sunshot energy.gov/sunshot Sources: Company figures based on Q2 2016 (and previous) SEC filings by the surveyed companies.

List of Acronyms and Abbreviations

• ASP average selling price • kW kilowatt • kWh kilowatt-hour • LMI low-to-moderate income • MM million • MW megawatt • PPA power purchase agreement • PURPA Public Utility Regulatory Policies Act • Q/Q quarter over quarter • ROW rest of world • SREC solar renewable energy certificates • ToU time of use • W watt • WACC weighted average cost of capital • y/y year over year • YTD year to date

59