Embed Size (px)

Citation preview

Q2 Financial Presentation 2017

DOF ASA

2DOF ASA – Q2 presentation 2017

Highlights Group

DOF ASA – Q2 presentation 2017 3

➢ Improved utilisation compared to Q1 (72%)

➢ Skandi Buzios on-hire 8 years with Petrobras in April

➢ Skandi Vinland delivered and on-hire 10-years with Husky Energy in Canada in July

➢ Delivery of a new vessel on management, Skandi Bergen in July

➢ New contract awards securing strong backlog for 2nd half 2017 (70%)

All numbers based on management reporting

Operational EBITDA Q2 MNOK 671 (excl hedge accounting)

Highlights

DOF ASA – Q2 presentation 2017

Total of 4 006 employees• Subsea employees 1 288

• Supply employees 2 718

Positioned globally✓ Head office in Norway

✓ Operating from 6 continents

✓ 20 offices near key O&G markets

✓ 69 vessels globally

Our vessels and subsea equipment*▪ Subsea 31

▪ AHTS 21

▪ PSV 17

▪ Total fleet 69

▪ ROV / AUV 71

DOF ASA, a global player

25 billion backlog

Approx 4 000 employees

69 vessels*

44

* Per August 2017 and included one hired-in vessel

DOF ASA – Q2 presentation 2017

Positioned to deliver

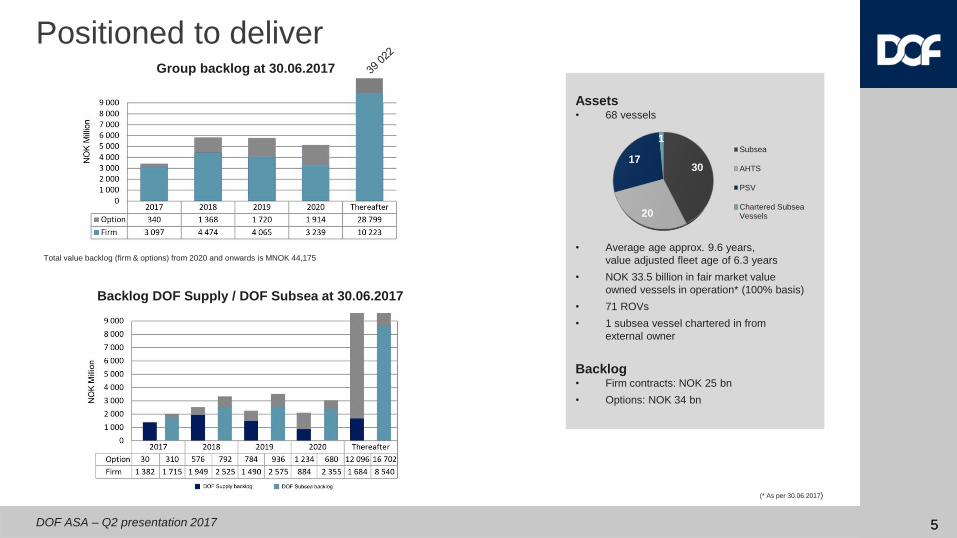

Assets• 68 vessels

• Average age approx. 9.6 years,

value adjusted fleet age of 6.3 years

• NOK 33.5 billion in fair market value

owned vessels in operation* (100% basis)

• 71 ROVs

• 1 subsea vessel chartered in from

external owner

Backlog• Firm contracts: NOK 25 bn

• Options: NOK 34 bn

Total value backlog (firm & options) from 2020 and onwards is MNOK 44,175

30

20

17

1Subsea

AHTS

PSV

Chartered SubseaVessels

55

Backlog DOF Supply / DOF Subsea at 30.06.2017

(* As per 30.06.2017)

Group backlog at 30.06.2017

DOF ASA – Q2 presentation 2017

DOF Supply - New contracts & vessels

6

New contracts in the North Sea

➢ Skandi Flora (PSV) awarded a 5-yr contract commencing in Q3

➢ Skandi Mongstad (PSV) awarded a 5-yr contract commencing in Q4

➢ Skandi Vega (AHTS) 1-yr extension from May

Contract in Brazil

➢ Skandi Admiral awarded a 1-yr contract with Petrobras in Brazil with start up in June

Vessels added to the fleet

➢ Skandi Hera (AHTS), on management from Feb, operating in the North Sea spot market

➢ Skandi Darwin (Subsea), on management from Feb, completed a conversion as IRM

vessel in August. Committed to DOF Subsea to serve their contract with Shell at the

Prelude field in Australia

➢ Skandi Bergen (AHTS), on management from July, in transit from Asia Pacific

DOF ASA – Q2 presentation 2017

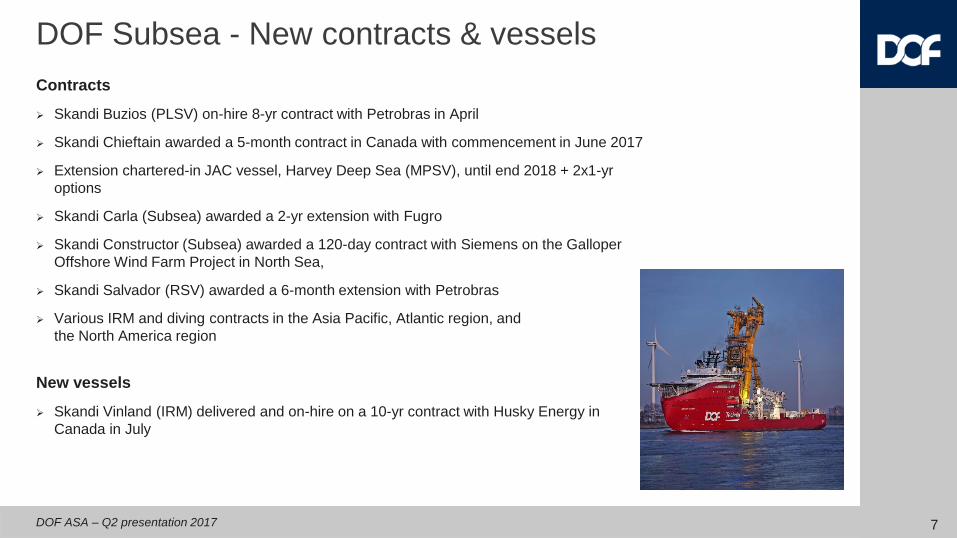

DOF Subsea - New contracts & vessels

7

Contracts

➢ Skandi Buzios (PLSV) on-hire 8-yr contract with Petrobras in April

➢ Skandi Chieftain awarded a 5-month contract in Canada with commencement in June 2017

➢ Extension chartered-in JAC vessel, Harvey Deep Sea (MPSV), until end 2018 + 2x1-yr

options

➢ Skandi Carla (Subsea) awarded a 2-yr extension with Fugro

➢ Skandi Constructor (Subsea) awarded a 120-day contract with Siemens on the Galloper

Offshore Wind Farm Project in North Sea,

➢ Skandi Salvador (RSV) awarded a 6-month extension with Petrobras

➢ Various IRM and diving contracts in the Asia Pacific, Atlantic region, and

the North America region

New vessels

➢ Skandi Vinland (IRM) delivered and on-hire on a 10-yr contract with Husky Energy in

Canada in July

DOF ASA – Q2 presentation 2017 8

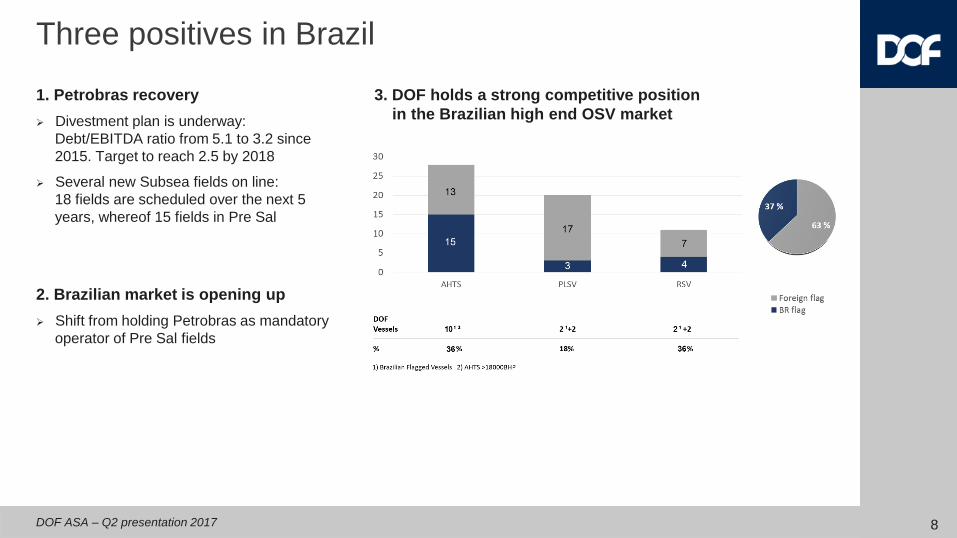

Three positives in Brazil

1. Petrobras recovery

➢ Divestment plan is underway:

Debt/EBITDA ratio from 5.1 to 3.2 since

2015. Target to reach 2.5 by 2018

➢ Several new Subsea fields on line:

18 fields are scheduled over the next 5

years, whereof 15 fields in Pre Sal

2. Brazilian market is opening up

➢ Shift from holding Petrobras as mandatory

operator of Pre Sal fields

3. DOF holds a strong competitive position

in the Brazilian high end OSV market

9DOF ASA – Q2 presentation 2017

FinancialsManagement Reporting

DOF ASA – Q2 presentation 2017 10

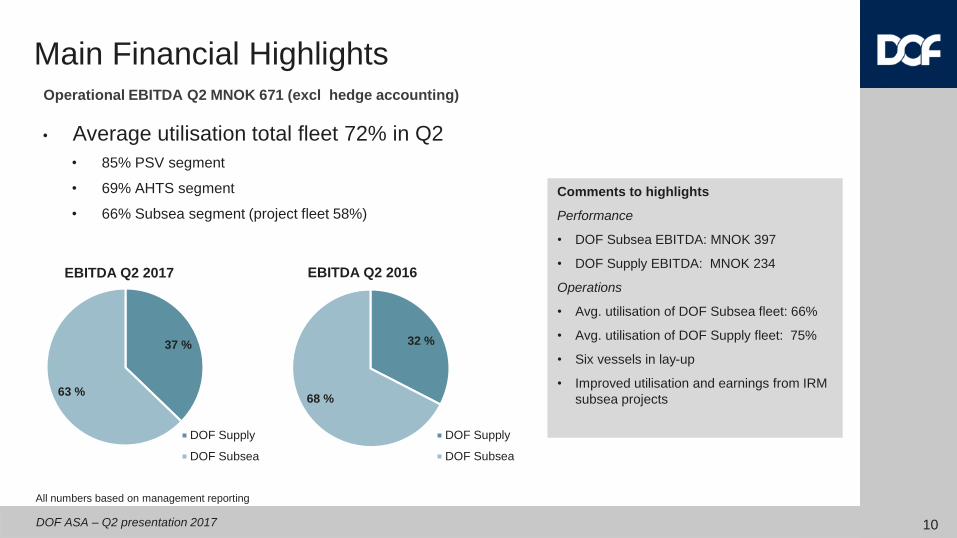

• Average utilisation total fleet 72% in Q2

• 85% PSV segment

• 69% AHTS segment

• 66% Subsea segment (project fleet 58%)

All numbers based on management reporting

Operational EBITDA Q2 MNOK 671 (excl hedge accounting)

Main Financial Highlights

Comments to highlights

Performance

• DOF Subsea EBITDA: MNOK 397

• DOF Supply EBITDA: MNOK 234

Operations

• Avg. utilisation of DOF Subsea fleet: 66%

• Avg. utilisation of DOF Supply fleet: 75%

• Six vessels in lay-up

• Improved utilisation and earnings from IRM

subsea projects

37 %

63 %

EBITDA Q2 2017

DOF Supply

DOF Subsea

32 %

68 %

EBITDA Q2 2016

DOF Supply

DOF Subsea

DOF ASA – Q2 presentation 2017

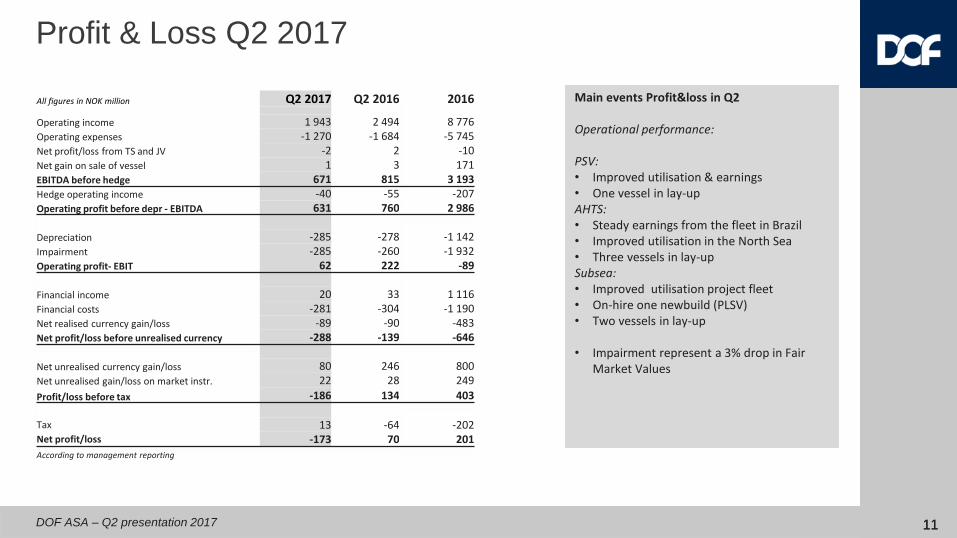

Profit & Loss Q2 2017

Main events Profit&loss in Q2

Operational performance:

PSV:• Improved utilisation & earnings• One vessel in lay-up AHTS:• Steady earnings from the fleet in Brazil• Improved utilisation in the North Sea• Three vessels in lay-upSubsea:• Improved utilisation project fleet• On-hire one newbuild (PLSV)• Two vessels in lay-up

• Impairment represent a 3% drop in Fair Market Values

All figures in NOK million Q2 2017 Q2 2016 2016

Operating income 1 943 2 494 8 776 Operating expenses -1 270 -1 684 -5 745 Net profit/loss from TS and JV -2 2 -10 Net gain on sale of vessel 1 3 171 EBITDA before hedge 671 815 3 193 Hedge operating income -40 -55 -207 Operating profit before depr - EBITDA 631 760 2 986

Depreciation -285 -278 -1 142 Impairment -285 -260 -1 932 Operating profit- EBIT 62 222 -89

Financial income 20 33 1 116 Financial costs -281 -304 -1 190 Net realised currency gain/loss -89 -90 -483 Net profit/loss before unrealised currency -288 -139 -646

Net unrealised currency gain/loss 80 246 800 Net unrealised gain/loss on market instr. 22 28 249

Profit/loss before tax -186 134 403

Tax 13 -64 -202 Net profit/loss -173 70 201

According to management reporting

1111

DOF ASA – Q2 presentation 2017

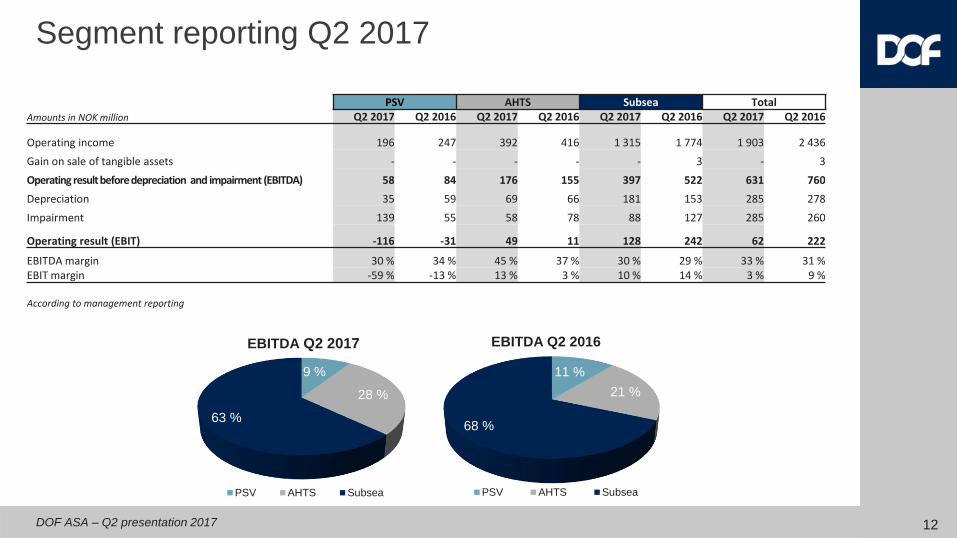

Segment reporting Q2 2017

PSV AHTS Subsea TotalAmounts in NOK million Q2 2017 Q2 2016 Q2 2017 Q2 2016 Q2 2017 Q2 2016 Q2 2017 Q2 2016

Operating income 196 247 392 416 1 315 1 774 1 903 2 436

Gain on sale of tangible assets - - - - - 3 - 3

Operating result before depreciation and impairment (EBITDA) 58 84 176 155 397 522 631 760

Depreciation 35 59 69 66 181 153 285 278

Impairment 139 55 58 78 88 127 285 260

Operating result (EBIT) -116 -31 49 11 128 242 62 222

EBITDA margin 30 % 34 % 45 % 37 % 30 % 29 % 33 % 31 %EBIT margin -59 % -13 % 13 % 3 % 10 % 14 % 3 % 9 %

According to management reporting

12

9 %

28 %

63 %

EBITDA Q2 2017

PSV AHTS Subsea

11 %

21 %

68 %

EBITDA Q2 2016

PSV AHTS Subsea

DOF ASA – Q2 presentation 2017

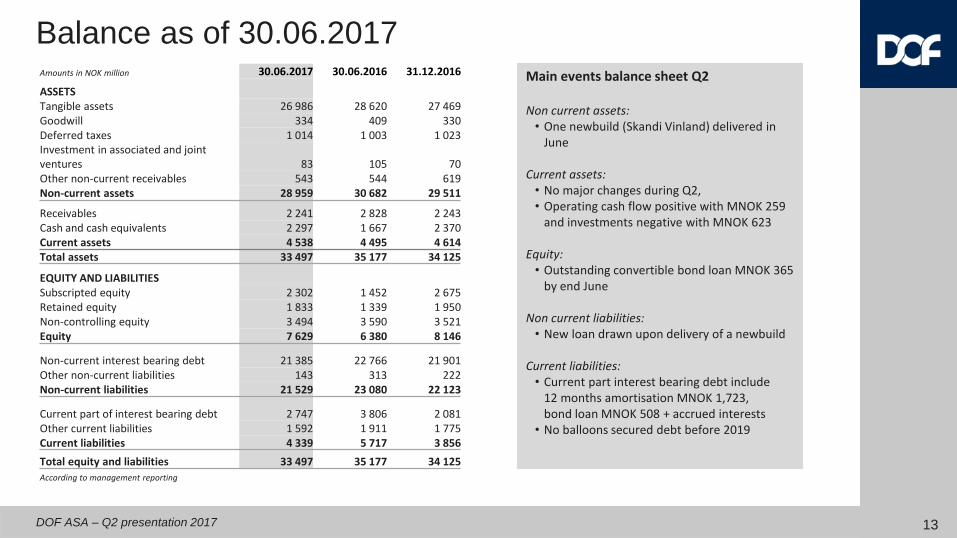

Balance as of 30.06.2017Main events balance sheet Q2

Non current assets:• One newbuild (Skandi Vinland) delivered in

June

Current assets:• No major changes during Q2, • Operating cash flow positive with MNOK 259

and investments negative with MNOK 623

Equity:• Outstanding convertible bond loan MNOK 365

by end June

Non current liabilities:• New loan drawn upon delivery of a newbuild

Current liabilities:• Current part interest bearing debt include

12 months amortisation MNOK 1,723, bond loan MNOK 508 + accrued interests

• No balloons secured debt before 2019

Amounts in NOK million 30.06.2017 30.06.2016 31.12.2016

ASSETSTangible assets 26 986 28 620 27 469Goodwill 334 409 330Deferred taxes 1 014 1 003 1 023Investment in associated and joint ventures 83 105 70Other non-current receivables 543 544 619Non-current assets 28 959 30 682 29 511

Receivables 2 241 2 828 2 243Cash and cash equivalents 2 297 1 667 2 370Current assets 4 538 4 495 4 614Total assets 33 497 35 177 34 125

EQUITY AND LIABILITIESSubscripted equity 2 302 1 452 2 675Retained equity 1 833 1 339 1 950Non-controlling equity 3 494 3 590 3 521Equity 7 629 6 380 8 146

Non-current interest bearing debt 21 385 22 766 21 901Other non-current liabilities 143 313 222Non-current liabilities 21 529 23 080 22 123

Current part of interest bearing debt 2 747 3 806 2 081Other current liabilities 1 592 1 911 1 775Current liabilities 4 339 5 717 3 856

Total equity and liabilities 33 497 35 177 34 125

According to management reporting

13

14DOF ASA – Q2 presentation 2017

DOF Subsea

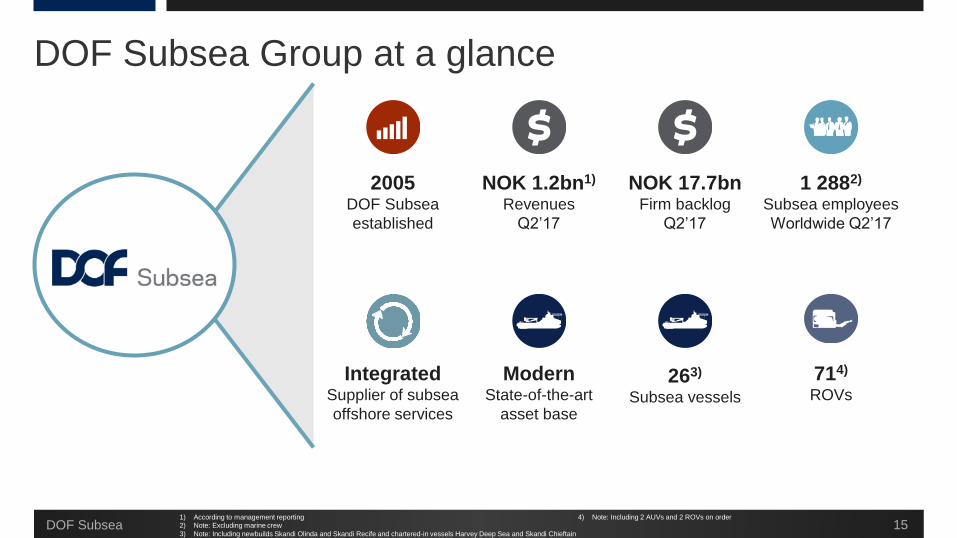

DOF Subsea Group at a glance

15

2005DOF Subsea

established

NOK 1.2bn1)

Revenues

Q2’17

1 2882)

Subsea employees

Worldwide Q2’17

NOK 17.7bnFirm backlog

Q2’17

263)

Subsea vessels

714)

ROVs

ModernState-of-the-art

asset base

IntegratedSupplier of subsea

offshore services

1) According to management reporting

2) Note: Excluding marine crew

3) Note: Including newbuilds Skandi Olinda and Skandi Recife and chartered-in vessels Harvey Deep Sea and Skandi Chieftain

4) Note: Including 2 AUVs and 2 ROVs on order

DOF Subsea

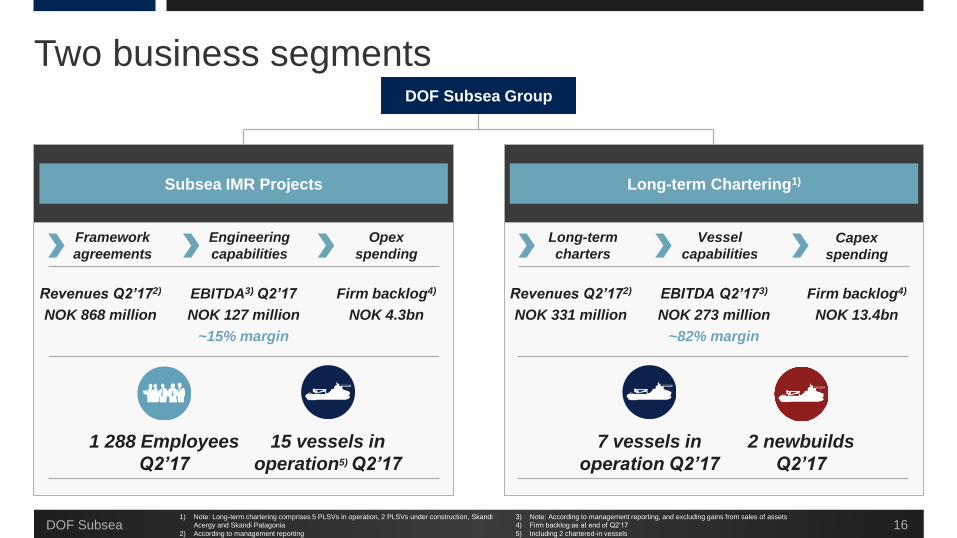

Two business segments

DOF Subsea 16

DOF Subsea Group

Long-term Chartering1)

Revenues Q2’172)

NOK 331 million

EBITDA Q2’173)

NOK 273 million

~82% margin

Firm backlog4)

NOK 13.4bn

1) Note: Long-term chartering comprises 5 PLSVs in operation, 2 PLSVs under construction, Skandi

Acergy and Skandi Patagonia

2) According to management reporting

3) Note: According to management reporting, and excluding gains from sales of assets

4) Firm backlog as at end of Q2’17

5) Including 2 chartered-in vessels

2 newbuilds

Q2’17

7 vessels in

operation Q2’17

Long-term

charters

Vessel

capabilitiesCapex

spending

Subsea IMR Projects

Revenues Q2’172)

NOK 868 million

EBITDA3) Q2’17

NOK 127 million

~15% margin

Firm backlog4)

NOK 4.3bn

1 288 Employees

Q2’17

15 vessels in

operation5) Q2’17

Engineering

capabilities

Framework

agreements

Opex

spending

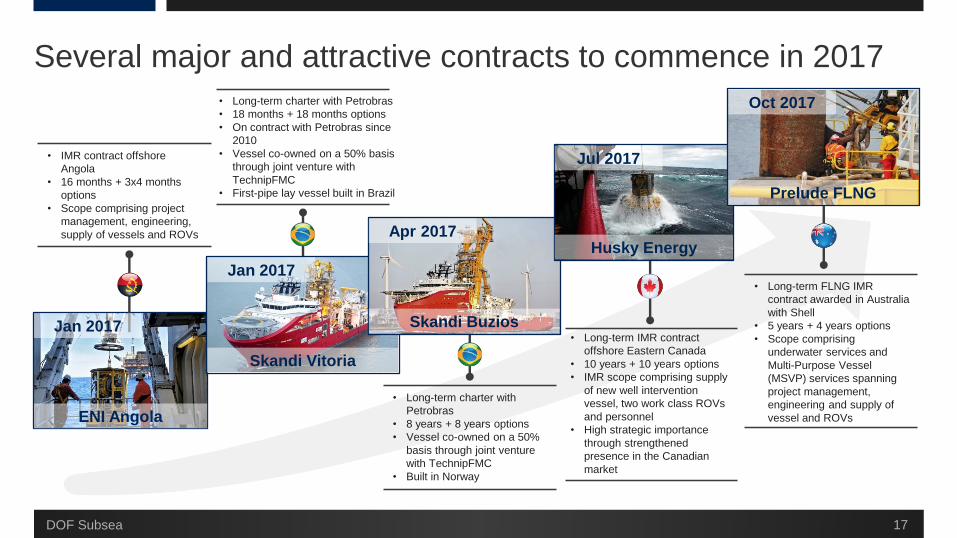

Several major and attractive contracts to commence in 2017

17

ENI Angola

Jan 2017

• IMR contract offshore

Angola

• 16 months + 3x4 months

options

• Scope comprising project

management, engineering,

supply of vessels and ROVs

• Long-term charter with Petrobras

• 18 months + 18 months options

• On contract with Petrobras since

2010

• Vessel co-owned on a 50% basis

through joint venture with

TechnipFMC

• First-pipe lay vessel built in Brazil

• Long-term charter with

Petrobras

• 8 years + 8 years options

• Vessel co-owned on a 50%

basis through joint venture

with TechnipFMC

• Built in Norway

• Long-term IMR contract

offshore Eastern Canada

• 10 years + 10 years options

• IMR scope comprising supply

of new well intervention

vessel, two work class ROVs

and personnel

• High strategic importance

through strengthened

presence in the Canadian

market

• Long-term FLNG IMR

contract awarded in Australia

with Shell

• 5 years + 4 years options

• Scope comprising

underwater services and

Multi-Purpose Vessel

(MSVP) services spanning

project management,

engineering and supply of

vessel and ROVs

Skandi Vitoria

Jan 2017

Skandi Buzios

Apr 2017Husky Energy

Jul 2017

Prelude FLNG

Oct 2017

DOF Subsea

Selected contracts in backlog

18

Location Client Scope Commencement Duration

Angola ENI Angola IMR 2017 16 months + 12 months

Eastern Canada Husky Energy IMR 2017 10 years + 10 years

Prelude Australia Shell Australia IMR 2017 5 years + 4 years

Brazil Petrobras Inspection 2016 1 year + 1 year

Gorgon, Janz and Wheatstone Chevron Australia IMR 2015 3 years + 2 years

Malampaya Shell Philippines IMR 2014 7 years + 3 years

Brazil Petrobras IMR 2012 6 years + 4 years

Brazil Petrobras IMR 2011 6.5 years + 4 years

North Sea Conoco PhillipsIMR

2011 8 years + 13 years

Subsea IMR Projects

North America

Gradually built up the

region, becoming a top

three supplier of IMR

services in the GoM

Brazil

Strong position being one

of the major suppliers of

IMR services

North Sea / Atlantic

Leading supplier of

mooring services in the

North Sea and West

Africa

Asia Pacific

Leading supplier of IMR

services in the region

DOF Subsea

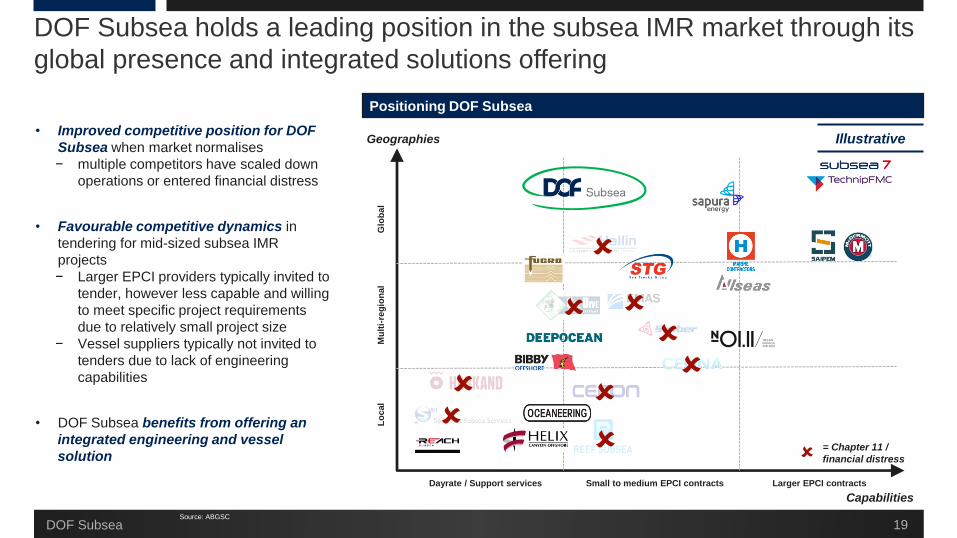

DOF Subsea holds a leading position in the subsea IMR market through its

global presence and integrated solutions offering

19

Positioning DOF Subsea

• Improved competitive position for DOF

Subsea when market normalises

− multiple competitors have scaled down

operations or entered financial distress

• Favourable competitive dynamics in

tendering for mid-sized subsea IMR

projects

− Larger EPCI providers typically invited to

tender, however less capable and willing

to meet specific project requirements

due to relatively small project size

− Vessel suppliers typically not invited to

tenders due to lack of engineering

capabilities

• DOF Subsea benefits from offering an

integrated engineering and vessel

solution

Lo

cal

Mu

lti-

reg

ion

al

Glo

ba

l

Dayrate / Support services Small to medium EPCI contracts Larger EPCI contracts

Source: ABGSC

= Chapter 11 /

financial distress

Geographies

Capabilities

Illustrative

DOF Subsea

DOF ASA – Q2 presentation 2017

No change in guidance for 2017 (MNOK 2 400 – MNOK 2 800)

New vessels added to the fleet from 2nd half 2017

Strong back-log for 2nd half 2017 (70%)

Two remaining newbuild to be delivered in 2018 and 2019 are committed on firm

contracts

Markets continues to be challenging

Outlook

20

Thank youPresented by

Mons Aase - CEO

Hilde Drønen - CFO

DOF ASA – Q2 presentation 2017

DISCLAIMER

This presentation by DOF ASA designed to provide a high level overview of aspects of the operations of the DOF ASA Group.

The material set out in the presentation is current as at 23 August 2017.

This presentation contains forward-looking statements relating to operations of the DOF ASA Group that are based on management’s owncurrent expectations, estimates and projections about matters relevant to DOF ASA‘s future financial performance. Words such as “likely”,“aims”, “looking forward”, “potential”, “anticipates”, “expects”, “predicts”, “plans”, “targets”, “believes” and “estimates” and similarexpressions are intended to identify forward-looking statements.

References in the presentation to assumptions, estimates and outcomes and forward-looking statements about assumptions, estimatesand outcomes, which are based on internal business data and external sources, are uncertain given the nature of the industry, businessrisks, and other factors. Also, they may be affected by internal and external factors that may have a material effect on future businessperformance and results.

No assurance or guarantee is, or should be taken to be, given in relation to the future business performance or results of the DOF ASAGroup or the likelihood that the assumptions, estimates or outcomes will be achieved.

While management has taken every effort to ensure the accuracy of the material in the presentation, the presentation is provided forinformation only. DOF ASA , its officers and management exclude and disclaim any liability in respect of anything done in reliance on thepresentation.

All forward-looking statements made in this presentation are based on information presently available to management and DOF ASAassumes no obligation to update any forward looking- statements. Nothing in this presentation constitutes investment advice and thispresentation shall not constitute an offer to sell or the solicitation of any offer to buy any securities or otherwise engage in any investmentactivity.

You should make your own enquiries and take your own advice (including financial and legal advice) before making an investment in thecompany's shares or in making a decision to hold or sell your shares.

22