Embed Size (px)

Citation preview

Q1 report

2012-05-02 Q1 report 1

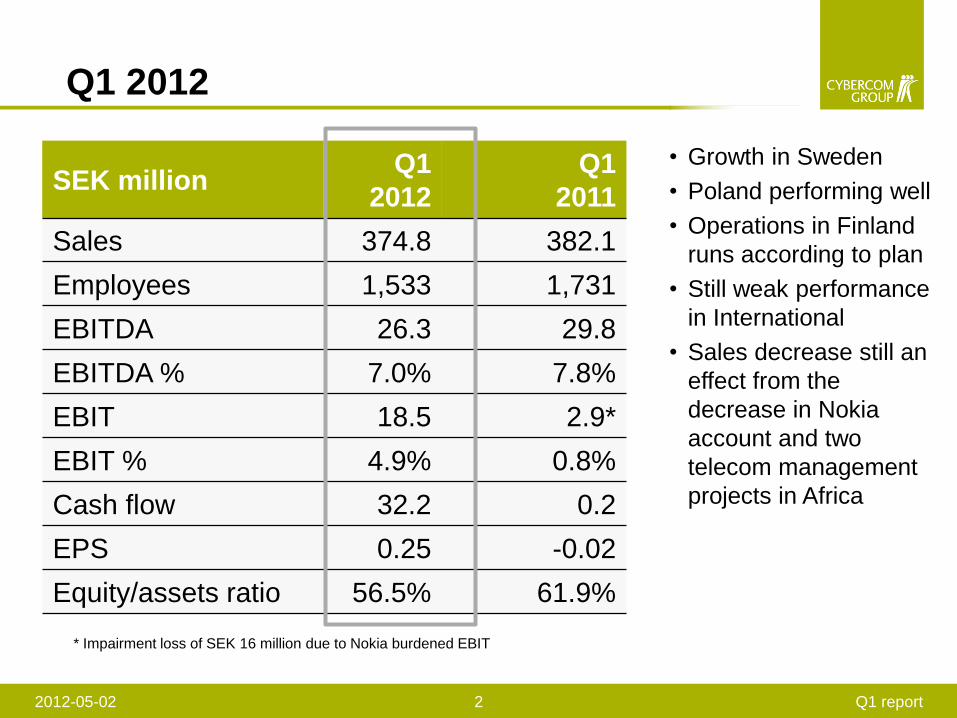

• Growth in Sweden

• Poland performing well

• Operations in Finland

runs according to plan

• Still weak performance

in International

• Sales decrease still an

effect from the

decrease in Nokia

account and two

telecom management

projects in Africa

Q1 2012

2012-05-02 Q1 report 2

SEK million Q1

2012

Q1

2011

Sales 374.8 382.1

Employees 1,533 1,731

EBITDA 26.3 29.8

EBITDA % 7.0% 7.8%

EBIT 18.5 2.9*

EBIT % 4.9% 0.8%

Cash flow 32.2 0.2

EPS 0.25 -0.02

Equity/assets ratio 56.5% 61.9%

* Impairment loss of SEK 16 million due to Nokia burdened EBIT

Sales & EBITDA RTM

2012-05-02 Q1 report 3

• Need to intensify efforts to become more efficient

– Integration of operations still not good enough

– Global structure and delivery capacity need to be optimised to

better benefit from the company's business model

• Need to invest in our employees and our culture

– More focused and effective sales

– Strengthen profitability through controlled skills development

• Change internal focus to external focus

• Further analysis ongoing

CEO initial findings

2012-05-02 Q1 report 4

Sales highlights in Q1

2012-05-02 Q1 report 5

• Cybercom chosen industry expert partner by

Ericsson to develop services and products for the

automotive industry

• An SEK 20 million order over one year for

verification of hardware in mobile services

• Four years contract for the Finnish National Board

of Education

• The ten largest clients 47% (45) of sales

• The biggest client 11% (13) of sales

• Framework-agreement clients 52% (61)

• Turnkey assignments 38% (45)

• Major clients – Alma Media Group, Ericsson, H&M, Millicom, MTV, SAAB

AB, Sony, ST Ericsson, TeliaSonera, and Volvo.

40%

24%

20%

5%3%

4% 4%

Telecom 40% (46%)

Industry 24% (20%)

Public sector 20% (17%)

Media 5% (5%)

Banking & Finance 3% (4%)

Retail 4% (3%)

Other 4% (6%)

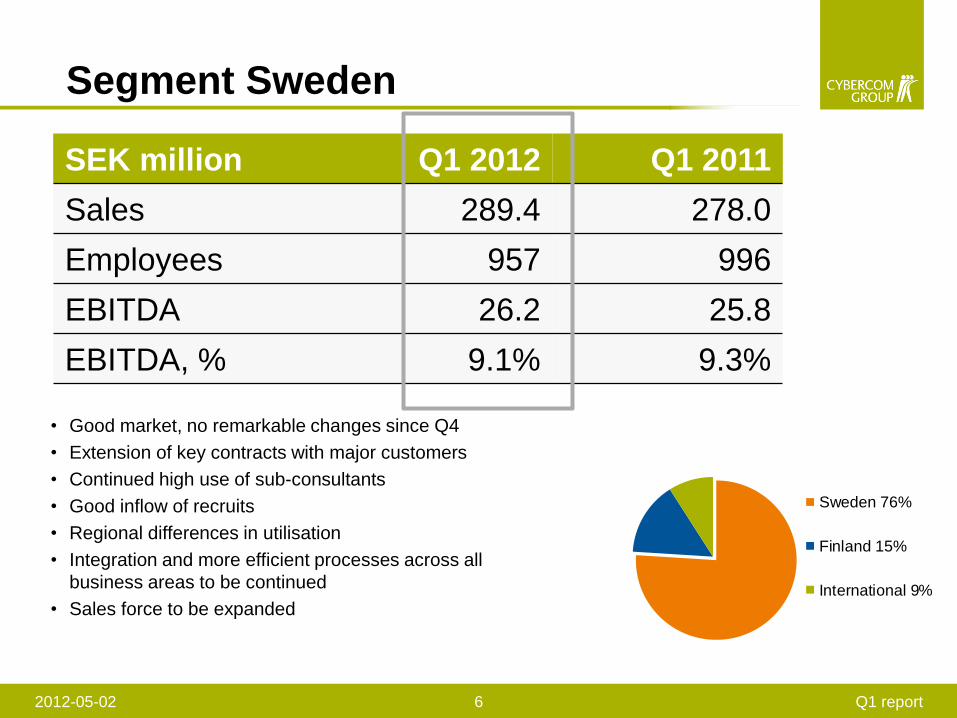

Segment Sweden

2012-05-02 Q1 report 6

• Good market, no remarkable changes since Q4

• Extension of key contracts with major customers

• Continued high use of sub-consultants

• Good inflow of recruits

• Regional differences in utilisation

• Integration and more efficient processes across all

business areas to be continued

• Sales force to be expanded

SEK million Q1 2012 Q1 2011

Sales 289.4 278.0

Employees 957 996

EBITDA 26.2 25.8

EBITDA, % 9.1% 9.3%

Sweden 76%

Finland 15%

International 9%

• Operation developed according to plan

• Decrease in sales due to 2011 downsizing from Nokia

assignment

• Business climate is still somewhat uncertain

• More inroads in the public sector

• Growth in industry and media

• Step by step working towards the recovery of earlier levels

of profit and sales

Segment Finland

2012-05-02 Q1 report 7

SEK million Q1 2012 Q1 2011

Sales 56.0 71.1

Employees 273 463

EBITDA 4.9 7.1

EBITDA, % 8.8% 10.0%

Sweden 76%

Finland 15%

International 9%

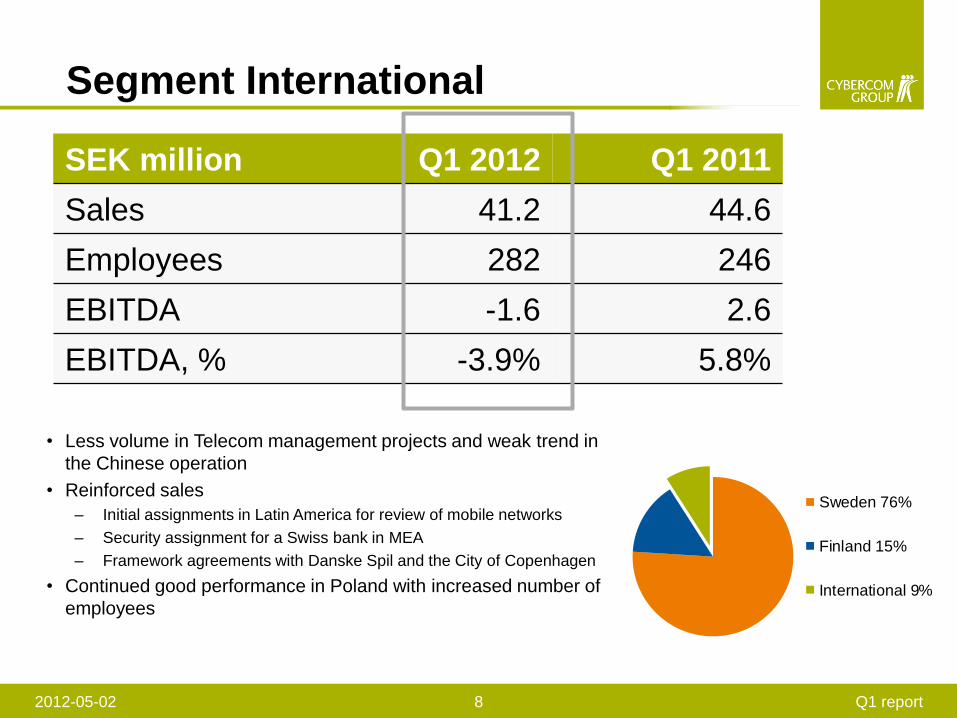

• Less volume in Telecom management projects and weak trend in

the Chinese operation

• Reinforced sales

– Initial assignments in Latin America for review of mobile networks

– Security assignment for a Swiss bank in MEA

– Framework agreements with Danske Spil and the City of Copenhagen

• Continued good performance in Poland with increased number of

employees

Segment International

2012-05-02 Q1 report 8

SEK million Q1 2012 Q1 2011

Sales 41.2 44.6

Employees 282 246

EBITDA -1.6 2.6

EBITDA, % -3.9% 5.8%

Sweden 76%

Finland 15%

International 9%

• The Nordic IT services market was worth €18,3 billion in

2010 and is expected to grow to €21,1 billion in 2015,

representing an annual growth of around 3%. Swedish IT

market is double the size of other Nordic countries.

• Competition is becoming increasingly global – Indian and

other offshore-based international players are gaining share.

The local players do not differentiate well from each other.

• IT market is shaped by a set of megatrends. Key trends

include commoditization and virtualization of IT, and the

increasing connectedness of the people, organizations,

devices and systems through pervasive IP. This trend is also

known as “the connected world” or “the internet of things”.

Nordic IT market overview

2012-05-02 9 Q1 report

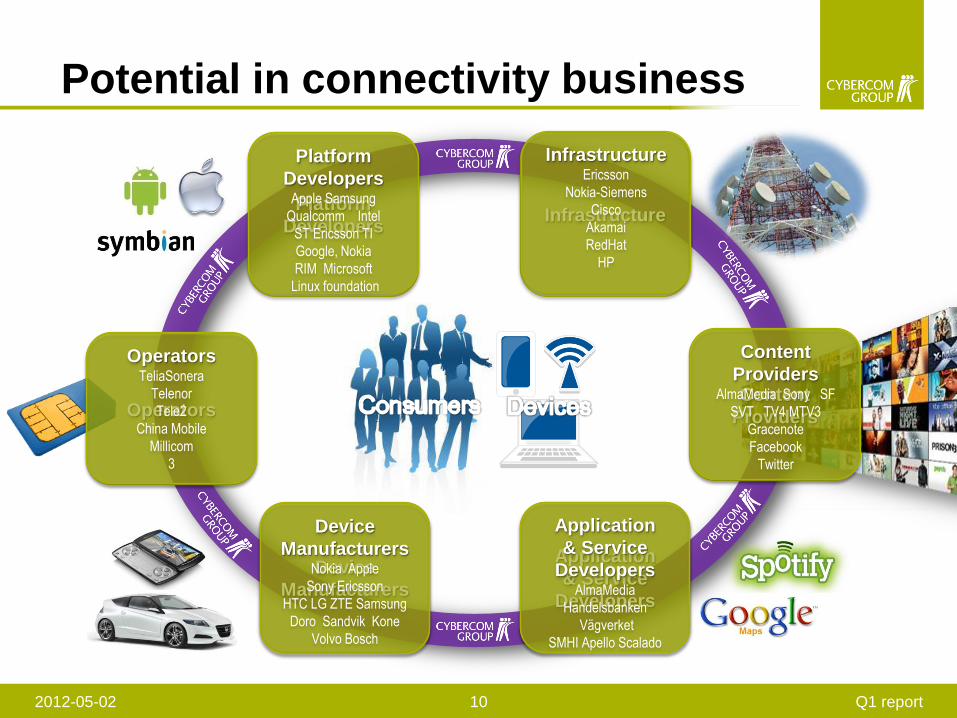

Potential in connectivity business

2012-05-02 10

Operators

Device

Manufacturers

Platform

Developers

Application

& Service

Developers

Content

Providers

Infrastructure

Operators TeliaSonera

Telenor

Tele2

China Mobile

Millicom

3

Platform

Developers Apple Samsung

Qualcomm Intel

ST Ericsson TI

Google, Nokia

RIM Microsoft

Linux foundation

Infrastructure Ericsson

Nokia-Siemens

Cisco

Akamai

RedHat

HP

Content

Providers AlmaMedia Sony SF

SVT TV4 MTV3

Gracenote

Application

& Service

Developers AlmaMedia

Handelsbanken

Vägverket

SMHI Apello Scalado

Device

Manufacturers Nokia Apple

Sony Ericsson

HTC LG ZTE Samsung

Doro Sandvik Kone

Volvo Bosch

Q1 report

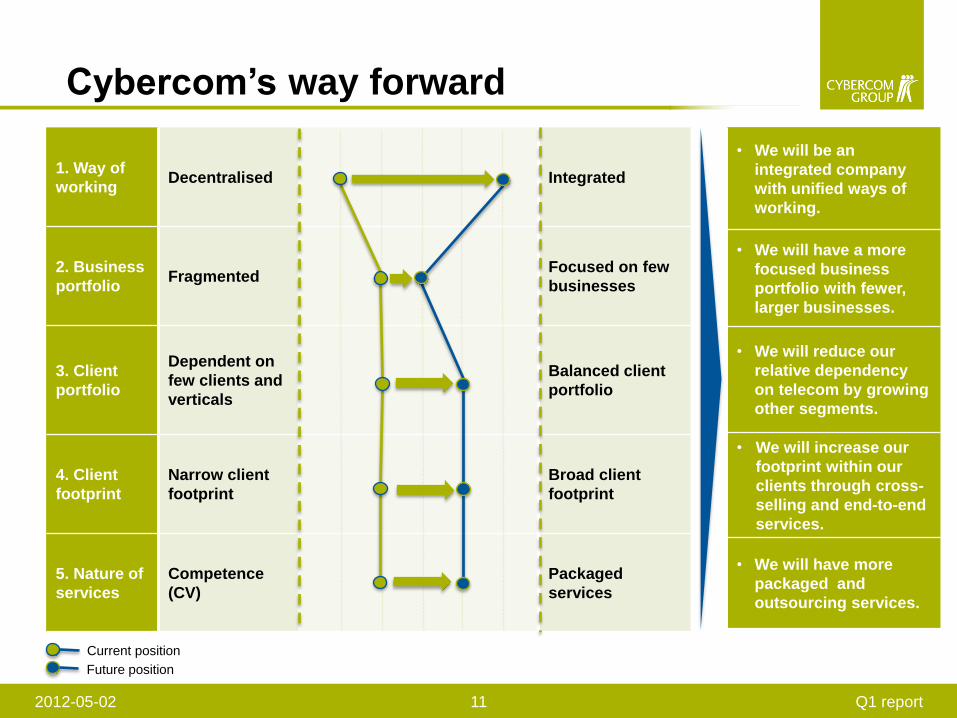

Cybercom’s way forward

11

1. Way of

working Decentralised Integrated

2. Business

portfolio Fragmented

Focused on few

businesses

3. Client

portfolio

Dependent on

few clients and

verticals

Balanced client

portfolio

4. Client

footprint

Narrow client

footprint

Broad client

footprint

5. Nature of

services

Competence

(CV)

Packaged

services

Current position

Future position

• We will be an

integrated company

with unified ways of

working.

• We will have a more

focused business

portfolio with fewer,

larger businesses.

• We will reduce our

relative dependency

on telecom by growing

other segments.

• We will increase our

footprint within our

clients through cross-

selling and end-to-end

services.

• We will have more

packaged and

outsourcing services.

2012-05-02 Q1 report

• Analysis of group structure and organisation

• Clients and new sales

• Optimisation of global delivery capacity

Focus coming quarter

2012-05-02 Q1 report 12

• New CFO starts June 1, 2012

• MBA from the Stockholm School of Economics

• Experience

– Logica: CFO of Logica Sweden

– WM-data: business controller and head of IR

and group treasury within the group

– SEB, Lexicon and the Swegro group

• Board member at Rusforest AB, listed on

NASDAQ OMX First North

CFO Camilla Öberg

2012-05-02 Q1 report 13

2012-05-02 Q1 report 14