Embed Size (px)

Citation preview

Investor Conference CallQ1 2015 Results

April 30, 2015 / Marijn Dekkers, CEO

• Q1 2015 Investor Conference Call • Marijn Dekkers Page 1

DisclaimerThis presentation may contain forward-looking statements based on currentassumptions and forecasts made by Bayer Group or subgroup management.

Various known and unknown risks, uncertainties and other factors could lead tomaterial differences between the actual future results, financial situation,development or performance of the company and the estimates given here.These factors include those discussed in Bayer’s public reports which areavailable on the Bayer website at www.bayer.com.

The company assumes no liability whatsoever to update these forward-lookingstatements or to conform them to future events or developments.

• Q1 2015 Investor Conference Call • Marijn Dekkers Page 2

Page 3

Q1 2015 – Strong Start to the Year

Significant sales and earnings growth in HealthCare

CropScience performance steady in a weaker market environment

MaterialScience posts earnings growth

Portfolio transformation into a pure Life Science company, integration of the acquired businesses and preparations for the flotationof MaterialScience remain on track

Full-year Group Guidance 2015 raised mainly due to Fx

• Q1 2015 Investor Conference Call • Marijn Dekkers

Page 4

EBITin € million

-5%

1,9982,096

Salesin € million% currency & portfolio adj.

+3%

12,11710,555

EBITDAbefore special itemsin € million

+10%

3,0002,738

Core EPSin €

+8%

2.101.95

Q1’15Q1’14 Q1’15Q1’14 Q1’15Q1’14 Q1’15Q1’14

Q1 2015 – Strong Start to the Year

• Q1 2015 Investor Conference Call • Marijn Dekkers

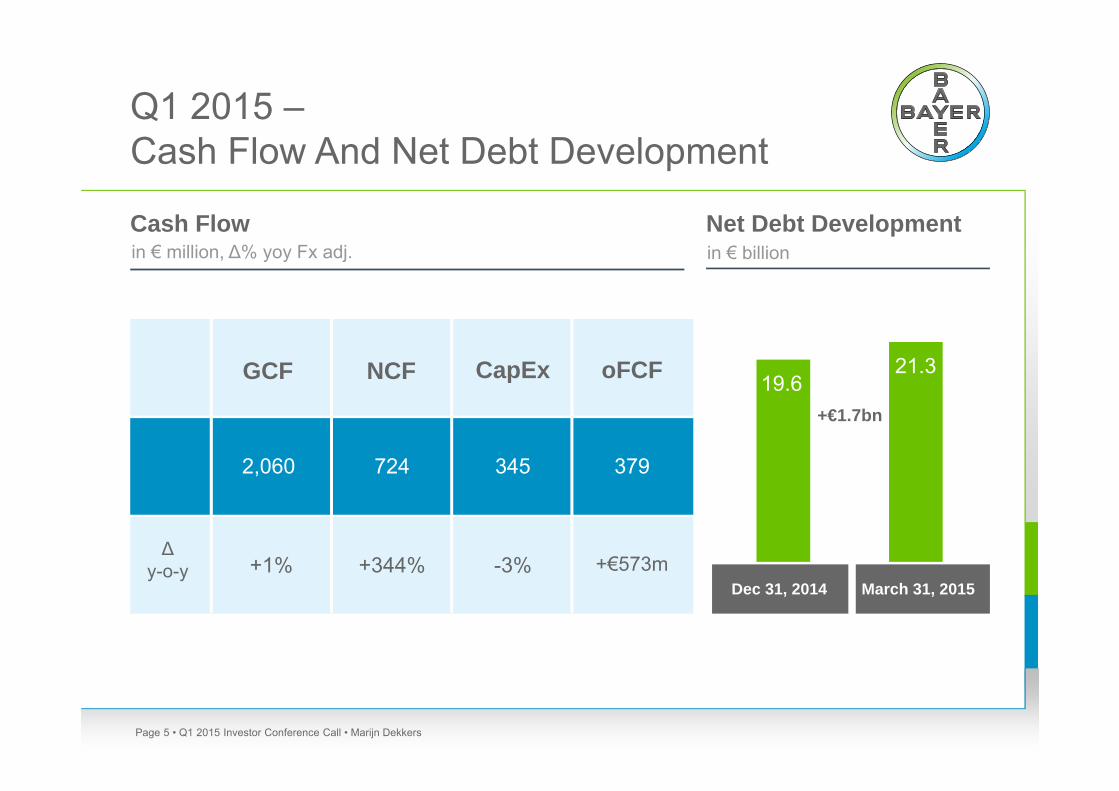

Q1 2015 –Cash Flow And Net Debt Development

Page 5

+€1.7bn

21.3GCF oFCF

2,060

CapEx

345 379

∆y-o-y +1% +€573m

NCF

724

+344% -3%Dec 31, 2014 March 31, 2015

19.6

• Q1 2015 Investor Conference Call • Marijn Dekkers

Cash Flow in € million, ∆% yoy Fx adj.

Net Debt Developmentin € billion

Q1 2015 – HealthCare: All Divisions Generated Strong Growth

Page 6

Pharma+15% (+7%)

ConsumerHealth

42% (+7%)

36%

HealthCare €5,742m; +26% (+7%)

3,2002,542

Price1%

Volume+7%

Fx+8%

Portfolio+11% Q1‘14 Q1‘15

873 988

428 627

+13%

+46%

1,301

1,615 +24%

321 +46%

946

1,185 +25%

625

470

EBITDA EBIT

715 +14%

• Q1 2015 Investor Conference Call • Marijn Dekkers

Salesin € million, ∆% yoy, () = Fx & portf. adj.

Earnings

Q1‘14 Q1‘15

before special items, in € million, ∆% yoy

Q1 2015 – Pharma:Launch Products Drove Growth

Page 7

Launch products

Pharmaceuticals €3,200m; +15% (+7%)

898

Q1‘14 Q1‘15 Q1‘14 Q1‘15

873

988 +13%

625715 +14%

• Q1 2015 Investor Conference Call • Marijn Dekkers

Salesin € million, ∆% yoy, () = Fx & portf. adj.

EBITDA EBIT

Earningsbefore special items, in € million, ∆% yoy

Q1 2015 – Consumer Health:All Businesses with Strong Growth

Page 8

Medical Care+12% (+6%)

ConsumerCare

+69% (+8%)

36%

Consumer Health €2,542m; +42% (+7%)

600

1,556

Q1‘14 Q1‘15 Q1‘14 Q1‘15

428

627 +46%

321

+46%470

• Q1 2015 Investor Conference Call • Marijn Dekkers

Animal Health+17 (+6%)

386

Salesin € million, ∆% yoy, () = Fx & portf. adj.

EBITDA EBIT

Earningsbefore special items, in € million, ∆% yoy

Q1 2015 – CropScience: Steady in Weak Market Environment

Page 9

Crop Protection+3% (-1%)

Environmental Science+22% (+4%)

Seeds+19% (+8%)

CropScience €3,092m; +7% (+1%)

Price+3%

Volume-2%

Fx+5%

Portfolio+1%

2,292

Q1‘14 Q1‘15 Q1‘14 Q1‘15

1,089 1,040 -5% 988 921 -7%

203

597

• Q1 2015 Investor Conference Call • Marijn Dekkers

Salesin € million, ∆% yoy, () = Fx & portf. adj.

EBITDA EBIT

Earningsbefore special items, in € million, ∆% yoy

Q1 2015 – MaterialScience:Lower Raw Material Costs Impacted Sales and Earnings

Page 10**CAS: Coatings, Adhesives, Specialties *** IO: Industrial Operations

CAS**+14% (+5%)

MaterialScience €3,014m; +8% (-2%)

Price-4%

Volume+2%

Fx+10%

Portfolio0%

1,551764

IO***0% (-4%)

Q1‘14 Q1‘15 Q1‘14 Q1‘15

366

424 +16%

221261534

165

• Q1 2015 Investor Conference Call • Marijn Dekkers

Polyurethanes+3% (-7%)

Polycarbonates+16% (+4%)

+18%

Salesin € million, ∆% yoy, () = Fx & portf. adj.

EBITDA EBIT

Earningsbefore special items, in € million, ∆% yoy

Q1 2015 –Full-Year Group Guidance Raised Mainly Due to Fx

Page 11

2014 2015original guidance

2015Update (April) Fx effect

Sales €42.2bnLow-single digit %

increase~€46bn

Low-single digit % increase

€48 - 49bn~ +9%

EBITDAbefore special items

€8.8bn Low-to-mid-teens % increase

High-teens % increase ~ +8%

core EPS €6.02 Low-teens % increase

High-teens % increase ~ +7%

Sales ∆% Fx and portfolio adjusted

Assuming end Q1’15 Fx ratesOutlook depends on specific planning assumptions as detailed in the Annual Report• Q1 2015 Investor Conference Call • Marijn Dekkers

Investor Conference CallQ1 2015 Results

April 30, 2015 / Marijn Dekkers, CEO

• Q1 2015 Investor Conference Call • Marijn Dekkers Page 12