-

Corporate Directing: governing,strategising and leading in

action*

Annie Pye**

This paper elaborates the concept of corporate directing,

integrating the processes ofgoverning, strategising and leading by

which small groups of people effectively runorganisations. If

governing and strategising are the warp and weft of this fabric,

then leadingis the textural imprint that is created through the

enacting of corporate directing. Based ontwo ESRC-funded research

projects (19879 and 19982000), it offers data on which thisconcept

is based, drawn from large UK plcs (e.g. Prudential, Marks &

Spencer) and selectedinstitutional investors (e.g. Hermes, Philips

and Drew).

Keywords: Corporate governance, leadership, corporate directing,

executive directors, non-executive directors

Introduction

T his paper introduces the concept ofcorporate directing, which

is taken to bean integrative process of governing, strategis-ing

and leading by which directors enact theirroles in large

organisations. Although thephrase has been used in other work

relatingto this project, this is the first formal attemptto develop

and articulate the concept with awider academic and practitioner

audience.

Divided into three main sections, the paperbegins by outlining

the background andcontext to the research project upon whichthese

ideas are based. It does not includelengthy consideration of

methodology andmethods as these have been well documentedelsewhere

(Pye, 2001). However, this sectionsets the scene to the project and

then looksmore closely at each of the dimensions ofdirecting:

governing, strategising and leading.The emphasis is retained upon

process ratherthan practice because it is common for

allorganisations now to claim they have soundgovernance practices,

but it is only throughthe doing of governing, i.e. how they

actuallydo their practice, that it is brought about. Eachof these

sub-themes considers something ofthe relevant literature as well as

illustrations

from practice upon which these themes aredeveloped.

This is then followed by a discussionsection, which looks more

closely at some ofthe difficulties of the concept of

corporatedirecting. It raises a number of unresolvedquestions,

which highlight some of the ob-stacles to developing a clear

understanding ofthis subject. For instance, directors are

heldindividually responsible for their actions inlaw, yet their

decisions are usually made ina collective forum called the board,

and itis a well-known fact that people sometimesact differently in

groups compared to theirindividual actions. There is also an

arrayof power issues that underpin corporatedirecting, including

the power of investorsto define the acceptability of directors

ex-planations of corporate performance; thepower of the Chairman to

determine theeffectiveness of other directors and NEDs

inparticular; and the power of the Triumvirate(Chairman, Chief

Executive and FinanceDirector) to shape what happens at this

level.Not surprisingly, with continuing efforts toencourage open

and transparent governance,there appears to remain a strong

principle oftrust that underpins the enacting of

corporatedirecting.

* This paper was presented atthe 4th International Confer-ence

on Corporate Governanceand Direction, 1517 October2001, at the

Centre for BoardEffectiveness, Henley Manage-ment College.**

Address for correspondence:School of Management, Uni-versity of

Bath, Bath BA2 7AY,UK. Tel: 01225 386128;

E-mail:[email protected]

CORPORATE DIRECTING 153

# Blackwell Publishers Ltd 2002. 108 Cowley Road, Oxford OX4

1JF, UKand 350 Main Street, Malden, MA 02148, USA. Volume 10 Number

3 July 2002

-

Corporate directing: research contextand model

The idea that top management is somehowdifferent to other

management has beenaround for a long time. The work of Ham-brick

and Mason (1984) in particular, iden-tified and distinguished

characteristics andvalues of these higher echelons (see alsoNadler

and Tushman, 1990; Tichy and Charan,1995; Finkelstein and Hambrick,

1996). Thegeneral view is that not only are they differentto other

managers, but also that they make adifference to their

organisations. So with this,our thinking went (in 1986, when we

firstinitiated this project), perhaps it means thereare different

competencies which are char-acteristic of effective top managers.

Hence in19879, we studied chairmen, chief execu-tives (CEs) and

board members in 12 largeUK plcs to explore this question.1 We

quicklyfound, however, that no matter how care-fully one seeks to

describe the competenciesof individuals, it is actually their

effect ina collective dynamic (i.e. a small group ofpeople engaged

in continuous, purposiveaction) that leads to the attribution of

effec-tiveness being given (or not) by others to

theirperformance.

So we began to look more closely at howsmall groups of directors

ran large organisa-tions and the variety was considerable: e.g.

atHanson, two central directors supported by aselect group of key

people created a verytightly driven financial management system;at

Glynwed, the shared ambition of boardmembers was that of becoming

the lowest-cost producer; while at Lucas, they were aim-ing to be

one of the top three in their keymarkets; and so on. What was

consistent toall, however, was that they had a strategicambition

and engaged in continuous andconsistent communication (largely

within,but also outside, their organisations) abouthow it was they

were collectively going toachieve that ambition and beyond

(Manghamand Pye, 1991).

Some ten years later, in 19982000, I returnedboth to former

contributors and to their organ-isations to ask once again, how do

you run alarge organisation?2 And while there are somesimilarities

in terms of the previous projectfindings, there are also many

differences interms of how they conduct their roles,

includ-ing:

(i) in 19879, no one talked of corporategovernance, whereas now

most contri-butors raise this subject of their ownvolition,

implying greater awareness ofand sensitivity to such issues;

(ii) relationships with major shareholdershave changed

considerably across thedecade and directors now see accountingfor

their strategic direction as crucial inthis context; and

(iii) the role of director, both executive andnon-executive, is

felt to be more criticallyunder the spotlight.

Hence, this paper draws together these threethemes of governing,

strategising and leadingtogether into the concept of corporate

direct-ing.

As often confounds organisational behav-iour scholars, life does

not happen in neatlylabelled boxes: this is the prerogative of

aca-demic analysts. That is, in neither study havedirectors been

able to distinguish betweentheir behaviour in terms of, for

instance,doing a bit of managing and a bit of leading instead, as

we described it in the first study,they simply do managing (Mangham

andPye, 1991). However, my current data set isnot best reflected as

the doing of managing,as directors horizons seem to have

changedconsiderably, and to call it the doing ofleading would also

only give a partial viewof what it is they do. Hence, my recent

find-ings lead me to propose a new concept calledcorporate

directing to describe the enactingof governing, strategising and

leading byorganisation directors.

Each of these key components of directorsaction is worthy of an

entire book on its own:indeed, many business schools run

wholecourses on each one. However, it is arguedhere that these

themes are highly interrelatedand interwoven, with each influencing

andbeing influenced by the others in the processof corporate

directing. Indeed, one mightconsider governing and strategising to

com-prise the warp and the weft of a fabric in adynamic and

complementary tension, withleading both in terms of its enactment

andits perception by others creating the texturethat is shaped

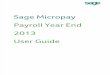

through the threads (see Figure1 below). This interweaving is a

continuous,forever-evolving and changing process, hence,it is

important to focus on the integratedthemes of governing,

strategising and lead-ing, rather than the more static and

stablenotions of governance, strategy and leader-ship.

This fabric metaphor is a useful one at thisstage as one may

have several differentthreads (influences of strategising, for

in-stance) that interweave the material, andtexture and pattern

(leading) can change.However, like all good metaphors, it is

onlyone way of seeing and may preclude otherways of seeing (Morgan,

1986). Hence the

CORPORATE GOVERNANCE154

Volume 10 Number 3 July 2002 # Blackwell Publishers Ltd 2002

-

discussion section of this paper goes on toexplore corporate

directing beyond thesebasic themes and identifies some of

thetensions that underlie it.

One aspect that is particularly difficult toarticulate is a

tension between the analysis ofindividual and collective (board)

actions. Thatis, according to law, directors are held to

beindividually accountable (and are paid in-dividually), but their

actions at board levelare clearly part of a collective and, as is

wellknown in the study of organisational behav-iour, people acting

together may do thingsthat they would never do alone (Myers,

1994).For this reason, I argue that corporate direct-ing is a

relational concept, known only throughrelationships with others

which are dynamicrather than additive. So rather than addingthe

individual abilities of each director on aboard to calculate the

total capability of thatgroup, it is argued instead that a board

maybe greater (and sometimes less) than the sumof its parts.

Contributors themselves have offeredmany observations of

differences betweentheir own and others boards in their

ex-perience, as well as the relationships and

emergent board culture in each case thateffectively provide

directions for action.While this re-emphasises that corporate

direct-ing is a collective process, it also illustrateshow three

individuals, in particular thechairman, CE and finance director

(FD) andtheir relationships (or sometimes partner-ships) stand out

as key to shaping and de-fining board culture, which has

significantimpact on board effectiveness. However,corporate

directing is known through morethan just board behaviour and

includes allaspects of directors communications, bothexplicit and

implicit, as well as inside andoutside their organisation, in the

process ofshaping their organisations future.

Governing

Governing has always been an important partof the directors

role, but during the courseof the last decade, it has commanded

evengreater attention. One reason for this, as Quelch(2000) notes,

is that in that time, organisationsthemselves have grown

significantly in econ-omic influence:

Basic warp and weft governing and strategising processes:

From: http://www.millo.dk/images/bckgrnds/examples.html

Enacted through leading, bringing colour and unique form to

corporate directing:

From:

http://needlepoint.about.com/library/pics/jacquard-top.jpg?once=true&

Figure 1: The process of corporate directing

CORPORATE DIRECTING 155

# Blackwell Publishers Ltd 2002 Volume 10 Number 3 July 2002

-

. . . it is true that 50 of the top 100 economiesin the world

are multinational corporations,not countries. An increasing amount

ofpower is in the hands of a relatively smallnumber of business

people who answeronly to their globally dispersed share-holders.

(Quelch, 2000)

While politicians are seen to be accountable totheir

electorates, directors are (in theory, atleast) accountable to

shareholders. However,this line of accountability has been called

intoquestion on numerous occasions in the lastdecade, including the

Maxwell Pension Fundscandal, Polly Peck and Barings Bank dis-asters

and more recently, apparent irregu-larities at TransTech and

Tomkins and thecollapse of Independent Insurance. TheCadbury

Committee was established in 1992(followed by Greenbury, Hampel and

Turn-bull Committees), to develop a code of goodpractice with

regards to governance and,indeed, the Combined Code of Practice

wasadopted by the Stock Exchange in 1998.

The Combined Code (1998) was generallywelcomed by contributors

to my study,although many felt this had led to a degreeof box

ticking to ensure that the board haddone the right things. For

some, this had hada detrimental effect on the role of the

nonexecutive director (NED), where it now tookup the greater part

of their time. For thisreason, I wish to distinguish between

govern-ance and governing: governance impliessomething static and a

box that can be ticked,whereas governing implies a social

processand collective phenomenon, i.e. done withand through

relationships with other people.Corporate governance is often

identifiedthrough indicators such as board compo-sition, committee

structure, executive com-pensation schemes and risk

assessmentprocedures etc., which offer a snapshot viewof governance

practice rather than the dy-namic process of governing. To

exploregoverning, i.e. how governance is enacted,means unravelling

the complex network ofrelationships amongst those who comprisethe

body (board and/or organisation) whosepractice is being observed as

well as relation-ships with outsiders who observe andcomment on

this organisations governance,e.g. investors analysts and major

share-holders, PIRC,3 customers, regulators etc.

This distinction between practice and pro-cess is brought into

sharp focus when oneconsiders new governance, the phrasecurrently

being promulgated by Pricewater-houseCoopers to describe the

growing bodyof issues such as intangibles, stakeholderdialogue,

reputation, customer service and

sustainability, which are not covered by thetraditional

umbrella. It is argued here thatnew governance is not very

different to oldgovernance (i.e. executive compensation andboard

composition) to the extent that bothsets of indicators are

concerned with ensuringthat companies are open and transparentabout

what they do.

However, some might argue that suchopenness can be

self-defeating: that you mayactually get more criticism for trying

to bemore transparent, as Shell have complainedrecently (Delfgauuw,

cited in Bingham, 2001),while those who stay quiet avoid

attention.This illustrates the key point in appreciatingthe process

of governing, which is that thereare two sides to this

relationship. It is notsimply enough to say that companies haveto

widen their reporting function to include,for instance, corporate

social responsibilityand the like, but they must actively manage

theinformation flow in ways that are credible andinformative. The

other side of this, though,in terms of both old and new

governanceis the demands this process then makes ofinvestors how do

they use the flood ofinformation now emerging from companies?

because the record of many institutions ofmaking judgements on even

old govern-ance issues is far from perfect.

In a presentation to the PIRC Annual Con-ference (2001), Reuters

Company Secretary,Rosemary Martin, made a scathing attack

oninvestors inability to think outside the tickbox. She explained

how Reuters had beencriticised for having offices in

politicallyunstable parts of the globe, such as Venezuela,Bosnia

and Cuba etc., and hence scored badlyon governance indices as a

consequence. Butas she pointed out, as the vehicle for promot-ing

freedom of speech in such countries, theywould be denying their

entire raison detre ifthey didnt have offices in such places! So,

sheargued, investors must think outside theirboxes. To this end,

she also explained howshe had recently launched an

innovativedirectors training programme across theReuters group. But

in response, investorsand analysts seemed barely interested in

suchmatters: they apparently preferred to evaluateReuters based

around the issues on theirvoting template and director training

does notscore highly.

So if, as a recent report by McKinsey claimedwas the case, three

quarters of (200) institu-tional investors (surveyed) said board

prac-tices were at least as important as financialperformance when

evaluating investments(Dickson, 2000), one would somehow expectthem

to be more interested in and attuned tothis kind of detail. But it

seems that generally

CORPORATE GOVERNANCE156

Volume 10 Number 3 July 2002 # Blackwell Publishers Ltd 2002

-

they are not, at the moment, at least. There is,of course, great

danger in talking of investorsas if they comprise a homogenous

group: theyare all different, depending on the style of fundsunder

management. However, what theseillustrations show is that actively

managingthese relationships is a key part of

governing.Paradoxically, while there is public pressure(e.g. PIRC,

CalPERS, Corporate Library) foropen governance, much of it seems to

happenoffstage or backstage behind closed doors oraway from public

record (Pye, 2001). As mydata illustrate and Golding (2001)

confirms,these meetings are a routine expectationamongst fund

managers who not only wantto understand the strategy being

pursued,they also need to make a judgement on man-agements ability

to achieve that strategy(Golding, 2001, p. 170). This leads on to

thenext theme in my model.

Strategising

If governing is about ensuring the legal dutiesand liabilities

of directors are met effectivelyand accountably, then strategising

providesthe reason for why these duties and liabilitiesexist in the

first place: that is, without visionand strategy, there is no need

for existencein the sense that there would be no futuredirection

for the organisation. Hence, strate-gising the process of

developing the futuredirection of an organisation provides

anotherimportant thread to corporate directing.

Strategic focus is the contemporary mantraamongst directors in

my sample, althoughtwo did suggest it may be current

businessfashion. However, the consistency with whichthis phrase was

used in my data suggests thatstrategic focus is a very powerful

framingdevice for strategic decision making, giving aclear

illustration of the shifting power andinfluence of institutional

investors. For example,two organisations (Avon Rubber and

Glynwed)had shed their original founding businessduring the last

decade to focus on what wasnow identified as core business.

Likewise, thetwo conglomerates in effect re-invented them-selves as

a focused engineer (Invensys-BTRand Siebe) and an aggregates

company(Hanson). Both these cases show how strate-gising must

resonate with the wider organis-ation environment: that is, no

matter howcapable and skilful, for example, the Hansonsenior

management are at implementing theirstrategy of tight financial

control (Goold andCampbell, 1990) and regardless of the con-tinuing

stream of individually and relativelysuccessful acquisitions, if

the market isunsure about the future, then the share

price falls together with most measures ofshareholder value.

Hence, the link betweenstrategic focus and shareholder value also

hasto be accounted for to the outside (investor)world.

Strategising refers here to the process bywhich directors go

about shaping the direc-tion, future, vision etc. of the

organisation.This day-to-day work of practitioners in-cludes both

the routine and the exceptional(i.e. intentionally structured

agency) and con-duct towards particular strategic goals

ordirection. Importantly though, not all direc-tors or boards are

uniformly involved in thestrategising process, nor is their

involvementconsistent over time: that is, in times of crisis,a

board is likely to be very closely involvedin formulating strategy,

whereas in non-crisistimes it may simply receive and

debateexecutive proposals. Either way, however,this collective of

executive and non-executivedirectors (i.e. board) shapes the future

direc-tion of the organisation.

The Institute of Directors Standards for theBoard document

describes this key part of thepurpose of the board as setting

strategy,whereas Stiles and Taylor (2001, p. 31) describeit as to

set the context of strategy. Based onmy research, the notion of

strategising seemsmore appropriate, because it is certainly thecase

that rarely are these boards actually theoriginators or formulators

of strategy: indeed,as we found with the first research project,. .

. it is not so much whether or not you havesomething called

strategy which is important. . . what really matters is that if by

commu-nicating that your organisation has a strategy,this helps to

focus peoples minds and actionsand to define meaning, then strategy

may be ahelpful construct (Pye, 1995, p. 457). Thuswe concluded at

the time that it is the theprocess of communicating and the

collectiveoutcome of that talk which is important, notthe label

that you give to it (p. 457).

Likewise, here I find that the process ofcommunicating (amongst

board membersand with others, inside and outside theorganisation)

and the collective outcome ofthat talk is important in terms of

shapingfuture direction. For this reason, adopting aprocess notion

of strategising a continuousprocess, shaping the organisations

future seems more reflective of my data than theidea of strategy,

which somehow has acuriously retrospective aspect to it a

theoryabout the past and current success of the firm.One FD summed

this up very neatly:

I can think of, at the moment, at least threebig moves we could

make, all of which wecould argue into our strategy but they

CORPORATE DIRECTING 157

# Blackwell Publishers Ltd 2002 Volume 10 Number 3 July 2002

-

would take us into different strategicdirections . . . I think a

lot of strategy isretrospective. There are certain things whichfit

logically and until youve made the bigmove . . . the speed at which

weve got tochange size means we cant do it organic-ally, so weve

got to do it by acquisition,merger, . . . And in that sense, its

goingto be not only what we want but whatwere able to achieve. And

thats why . . .actually if you a look at a lot of large com-panies,

their strategy develops retrospec-tively. (Finance Director,

italicised emphasisadded)

So how do directors decide their organis-ations strategic

direction? Undoubtedly, thisis primarily shaped by executive

directors,although NEDs were also seen by some tohave a role to

play. Several were quitedismissive of the strategy awayday: a

goodbonding exercise and opportunity to talk topeople off the daily

premises, but not the bestway to develop corporate strategy. This

mayhardly be surprising when one considersfrom ones own personal

experience thatoften the most influential conversations, orthe

discussions that make you think a littledifferently or ask

questions of something, areusually those that take place outside

ofmeetings (although this is troublesome froman open governance

point of view). So away-day bonding may be important for

thesesocial reasons, but as far as formal strategyis concerned, for

some it seems that little ofsignificant strategic value appears to

comeout of them.

Again though, this further emphasises theneed to consider the

strategising processrather than simply the strategy. Perhapsthe

most important conclusion to be drawnfrom their comments, however,

is that, call itstrategy or vision or whatever, almost alldirectors

agreed that what is crucial is not somuch the words on paper (i.e.

about having astrategy) but the process of dialogue and debateby

which these words are brought into action.Naturally, the

organisations strategy docu-ment must have key words in it that

explainto anyone what the business is about andwhere it is going,

but the process by whichthose ideas were generated and debated,

ideaslistened to and discussed, peoples contri-butions respected

and reflected upon, i.e.strategising process, is much more

importantthan the final document.

And here again, there is an interestingdimension from the

investors point of view,which is that they seem to pay scant

attentionto the process by which strategy is generated,but simply

want to know that the board has

one. Yet, how managers generate their strategicthinking and

agree a direction has a hugeamount to do with quality of outcome

andhow effectively they are able to implement it.In my research, it

seems that investors rarelypay attention to this detail, although

they areinterested in the managers themselves.

Leading

The way governing and strategising are viewedin practice

underpins the third dimension inmy model: leading. Leadership is

reflectedin just about everything an organisation does,not just in

what the executive team does,although there is still a curious

assumptionthat the further up the organisation you go,the more

leadership you do. And somehow,the assumption goes, this kind of

leadershipis different from other kinds of leadership asyou might

find elsewhere usually lowerdown in an organisation. Bearing in

mindthe original question with which we began,what is important

about leadership at thislevel that might distinguish it from

otherkinds of leadership?

If you could actually define what youmeant by (other kinds of)

leadership, it mightmake it a bit easier to answer this

question!Generally, it is taken to mean leadershipperformed by

those in a director role, whichis then differentiated between

executive andnon-executive directors. But the root of theword to

lead has an interesting derivation,which refers to a road, a

journey, to go to, totravel ahead:

To lead:to guide with reference to action oropinion;to bring by

persuasion or counsel to orinto a condition;to conduct by argument

or representa-tion to a conclusion;to induce to do something. (Said

both ofpersons and motives, circumstances,evidence, etc.) (OED on

line)

And contributors would agree with this, butwould also take a

slightly more pragmaticline to the extent that they think

thingsthrough, not necessarily to a conclusion,but instead, to a

decision, which impliesfurther action (see Mangham and Pye, 1991,p.

20). In essence, their role is to lead the way,but it is not so

easy to articulate how they dothis.

For instance, it is easy to become side-tracked into focusing on

the people andindividual leaders involved, which then leadsone to

altercast others into a non-leading

CORPORATE GOVERNANCE158

Volume 10 Number 3 July 2002 # Blackwell Publishers Ltd 2002

-

position. Yet boards illustrate a collection ofleaders who are

together enacting collectiveleadership, even if one person, i.e.

the CE,ultimately stands more clearly identified inthis process

than any others, as primus interpares. When put like this, it is

hardly sur-prising that traditional views of leadershipappear more

appealing, as it is much simplerto rely on an inspiring and

energising figure-head than to try to identify shared or

collectiveleadership. For example, motivation, align-ment, cohesion

and the ability to focus fol-lowers on goals, values and visions

are thecentral features of good leadership (Kotter,1988) is somehow

more palpable than aprocess of transformative change where

theethics of individuals are integrated into themores of a

community as a means of evolu-tionary social development (Barker,

2001).

From my data, it is clear that leading at thislevel happens

through communication as wellas through a host of organisational

processeswhich support particular strategic initiatives.That is,

while leading is usually thought ofthrough face-to-face social

influence, there aremultiple ways in which organisational

struc-tures and systems influence the actions peopletake and the

direction in which the collectivegoes. Interestingly,

characteristic of somedirectors in my sample is an appreciation

ofthe limits to their influence that is, they mayhave a broad

corporate overview from thedirecting point of view, but as far as

theinfectious quality of their executive leader-ship is concerned,

most of them are awarethat they can really only inspire those

rela-tively close to them. It is not impossible todeepen their

influence and many do sothrough spending a lot of time on the

road.A different illustration is the case of Sir PeterDavis in a

series of TV advertisements runby Prudential in 1996. He was newly

in postand took an essentially risky step to front theTV

advertisements, which effectively apolo-gised for pensions

mis-selling and committedPrudential to changing culture in the

processof redressing the situation. In his view, thiswas a very

effective means of powerfullyreaching all Prudential employees and

show-ing that this was a real and total culturechange for everyone,

rather more traditionalmeans such as training programmes and

in-house communications within Prudential. Italso did much to

repair their reputation withtheir customers.

It is easy to say that directors should begood communicators,

but this is a nonsensephrase that may disguise the more

importantability to relate to people: that is, they aregood at

talking and listening to people as wellas being able to walk the

talk. In addition, it is

not a quality that can be applied globally toall in my sample,

as some are less influentialthan others in leading in this way. An

alter-native analysis suggests that they are good atconsistently

explaining their organising,something which they do all of the

time, ineverything they do. Hence, while most effec-tive CEs and

some chairmen are visible,perhaps more important for directors as

awhole is that they are strongly connected totheir organisations

and beyond, developingrelationships and rapport with people

acrossthe field.

Discussion

The concept of corporate directing describesthe integrative

process of governing, strate-gising and leading in action, i.e. the

enactingof directors roles both individually andcollectively. It is

a relational concept, onlyknown and brought about through

otherpeople, and includes all aspects of directorssymbolic actions.

Pfeffer (1981) describedmanagement as symbolic action: it is

arguedhere that directing is symbolic (en)acting.

However, there are several tensions under-lying this concept,

which will be outlined inthis discussion.

(i) With different director roles, does eachkind of role

occupant demonstrate a dif-ferent kind of directing? For instance,

isCE directing different to that performedby the FD, the chairman,

the non-executive or the senior non-executive?In principle, I would

argue from my datathat the answer is no: it is a generic termthat

describes the integrative process ofgoverning, strategising and

leading atthis level of organising. In practice, yes,observers

undoubtedly find ways ofdifferentiating between the functionand

performance of different individualsand (board) groups (Pye, 2000a;

Stilesand Taylor, 2001) and indeed, investorshave quite distinct

views on their ex-pectations of CEs as opposed to FDs asopposed to

senior NEDs, as opposed tochairmen etc. Importantly, these

differ-ences also change over time such that, onoccasions, a NED

may be more involvedin strategy formulation than at othertimes.

(ii) This then leads one to consider whethereach director must

perform well in allthree of these dimensions or is it simplythe

case that collectively, as a board, theymust perform well across

these three di-mensions? And how might one know

CORPORATE DIRECTING 159

# Blackwell Publishers Ltd 2002 Volume 10 Number 3 July 2002

-

the difference? Herein lies a very inter-esting research

challenge. Intuitively,one would argue that equanimity of

in-dividual contribution is neither possiblenor necessary; however,

practically (andtheoretically), it is then a very big stepup to

evaluate the collective achievementof all three combined aspects of

direct-ing.

(iii) This leads to perhaps the key tensionunderlying the

concept of corporatedirecting, which is the relationship be-tween

individual and collective. Direc-tors always say that each member

oftheir board has to be an effective playerand that everyone must

pull their weightetc., although it is always the case thatwhen

members of a group work together,there is rarely total equality of

input orability: as Jay (1980) pointed out in hisanalysis of

Belbins work, nobodysperfect but a team can be. Yet legally,each

directors performance is accountedfor individually: they are held

to beaccountable for their own individualactions and indeed, are

paid based onindividual performance. So in this case,if there is a

weak link, in theory at least,this person would be highlighted

andpresumably helped to leave if the weak-ness was seriously

undermining boardperformance. Yet the weakest link inpractice seems

to be an inability toaccount for the relationship betweenindividual

and collective action.

(iv) So how does one then account for thedifferences between

boards, even whenperhaps some of the directors are thesame?

Certainly, in one case, a verysenior NED with experience in

manydifferent boards illustrated one boardwhere he was a very

effective andpowerful player and the company per-formed very well

and another, where thecompany performed very badly and thewhole

board appeared less than effectivein the face of a powerful CE. So,

indi-vidually, this NED had taken his un-doubted skill sets and

high professionalstandards to both boards and the out-come had been

very different. So as faras inputs to the board are concerned,

heremains the same person (individual)throughout, yet in terms of

effectivenessof the collectives, the situations arealmost

incomparable. One might saythat this is simply because of

differentorganisations in different industry sec-tors at a

particular time in their corporatehistories. However, the key point

here isthat regardless of the individual input(s)

to any board, there are a host of con-tingency factors which

mean that the waythings are done in each board, i.e. theboard

culture, is very different.

(v) There are a host of power implicationsin this discussion,

including questionsabout the power of board culture, thepower of

investor influence and theenacting of both individual and

collec-tive power and influence to shapecorporate outcomes. It is

proposed herethat the emergent board culture dependsvery largely on

the chairman, CE andFD and their relationships whicheffectively

provides directions for ac-tion. The aphorism of the chairmanruns

the board and the CE runs thecompany is often used to sum up

theirparts, to which I would add that the FDalso ensures that the

numbers add up.4

Effective relationships between theseplayers do not seem to

depend on whereyou draw the lines between them, solong as each

party understands andagrees where it is. Although it is hardto

access this point, my data seem toevidence a series of partnerships

under-pinning their doing of corporate direct-ing: that is,

partnerships betweenchairman and CE, CE and FD and tosome extent,

chairman and FD.

Importantly though, how they actuallydevelop these partnerships

is different ineach board case. In some cases, the combina-tion can

be very powerful, described by oneNED as impregnable. Consequently,

enact-ing the NED role and NED effectiveness inthis process depends

significantly on thechairman and also the CE. Hence, boardculture

differs in each case, but as Petersand Watermans (1982) search for

excel-lence revealed, it is impossible to define anideal culture,

particularly where the tone andtenor of relationships amongst board

mem-bers influences conduct and relationshipsboth inside and, in a

much wider field,outside board meetings.

The power of investor influence is alsodifficult to ascertain

and, where directlyquestioned, most contributors said investorsdid

not act as a ghost at the bargaining(board) table. However, it is

impossible toidentify the extent to which investor meetingshave

influenced thinking and informationprior to any board meeting or

discussion,although it seems most likely that thishappens. Hence,

investors power is palpablygreater than in 1989, but the extent to

whichit can be evaluated in corporate directingremains unclear

(Pye, 2001).

CORPORATE GOVERNANCE160

Volume 10 Number 3 July 2002 # Blackwell Publishers Ltd 2002

-

A director of a company must in any givencase

(a) act in a way he decides, in goodfaith, would be most likely

to pro-mote the success of the company forthe benefit of its

members aswhole . . . and

(b) in deciding what would be mostlikely to promote that

success, takeaccount in good faith of all thematerial factors that

it is practicablein the circumstances for him toidentify.

This is taken from the statement of generalprinciples by which

directors are bound inCompany Law, following lengthy debatethrough

the recent Company Law Review.However, I can find no similar

statementreferring to board conduct, even though it isa well-known

fact that people in groups dothings that would be unthinkable when

actingalone. This in part reflects the different powerto influence

played out by different actorsin different situations and is

something thatseems to remain relatively unexplored inboard

contexts.

Given the above observations, I concludethat trust is a critical

element that facilitatesboard relationships, both inside an

organisa-tion (Stiles and Taylor, 2001) and with outsideinterest

groups, including the wider society.Within the board context,

director relation-ships seem characterised by respect, which inturn

may lead to trust. However, these arequalities that are earned such

that subsequentreturn on earning trust can be considerable,although

it does occasionally need reapprais-ing in order to avoid

complacency. Forexample, much attention is paid to ensuringdirector

independence (e.g. Hermes website)as a means of heightening

trustworthiness.Yet it is concluded here that independenceis an

impossible ideal in this arena, where thenetwork of relationships

over time is verydense and where things are only made tohappen

through ones relationships with in-fluential others (Pye, 2000b)

and where eventhe most independent NEDs are still depen-dent on the

chairman and key executives forinformation, the very lifeblood of

their role.

Conclusions

There is much more to running a largeorganisation effectively

than either tickingthe boxes of corporate governance or devel-oping

strategic direction or demonstratingdynamic leadership. Each board

and organis-ation in my sample is unique in how it runs

its affairs, a uniqueness that changes with timeand people. This

paper offers some work-in-progress findings that draw together

someaspects of this process and proposes theconcept of corporate

directing.

It is argued here that corporate directing isa valuable way to

conceptualise the processesof governing, strategising and leading

bywhich small groups of people effectivelyrun organisations.

Governing and strategis-ing can be considered as the warp and weft

ofthe corporate directing fabric to which thenotion of leading is

interwoven to create thetextural imprint that defines the fabric:

henceeach weave and fabric is different. The em-phasis is on the

continuous process of enact-ing their roles in which it is almost

impossibleto distinguish between doing a bit of govern-ing, a bit

of strategising or a bit of leading:instead, they do directing.

Hence, corporate directing is described as arelational concept,

known through and iden-tified by other people. It is also symbolic

inconduct and consequence: through all aspectsof their behaviour,

both individual andcollective, directors are seen to

communicatetheir organising (Mangham and Pye, 1991),shaping a

collective appreciation of corporatedirection. Given that much of

their time isspent developing relationships outsidetheir

organisations and that the power todefine the acceptability of

corporate explana-tions of performance now seems to lie outsidethe

organisation, this also includes relation-ships with investors,

analysts and others,as well as with other board members

andorganisational members. It is important toremember that there

are two sides to theserelationships: hence where openness

andtransparency in governance is consideredimportant, it holds

implications for bothparties to the relationships and not

simplycorporate directors.

Challenging questions still remain, whichinclude: the difficulty

of teasing out therelationship between individual and collec-tive

action and how this might be known andevaluated; differences in the

power to influ-ence the enacting of corporate directing; andthe

importance of trust in an era of opennessand transparency in the

conduct of corporatelife. As one contributor pointed out, if

thechairman and/or CE and/or FD connive todo wrong things, then it

is very difficult foranyone (and non executives in particular)

tofind out what is going on. Hence, the roles ofchairman and CE are

of particular importanceto the enacting of corporate directing, as

theformal focal point of this higher echelon isthe board, where the

chairman and CE have apowerful influence on shaping board

culture

CORPORATE DIRECTING 161

# Blackwell Publishers Ltd 2002 Volume 10 Number 3 July 2002

-

and the way things (including governing,strategising and

leading) are done.

Notes

1. This project was funded in 19879 by theEconomic and Social

Research Council, undergrant number WF 2925 0020 and involved46

interviews conducted with board membersat Avon Rubber, Beazer, BTR,

Coats Viyella,Glynwed, Hanson, Lucas, Marks & Spencer,Metal

Box, Prudential, Reckitt & Colman andTSB.

2. The author is grateful to ESRC for theircontinued funding of

this work, under grantnumber R 000236868. This paper is based

ondata generated from 25 interviews with pre-vious contributors; 35

interviews with currentboard members in Avon, Beazer, Coats

Viyella,Glynwed, Hanson, LloydsTSB, Marks & Spen-cer,

Prudential, Reckitt & Colman and ScottishPower; and interviews

with chief executivesat (or similar) Hermes, Gartmore,

Liontrust,Merrill Lynch and Philips and Drew.

3. Pensions and Investment Research Consul-tants, an influential

pressure group that ad-vocates greater transparency in

governance.

4. One FD described his felt need to tell the storyof the

accounts, in order ensure that othersshared the same interpretation

as he made. Inaddition, Golding (2001) makes the point thatearnings

figures are easily and frequentlymanipulated. Hence, there is also

consider-able power in this role.

References

Barker, R. A. (2001) The Nature of Leadership,Human Relations,

54, 469494.

Bingham (2001) Editorial, Governance, 191, 2.Combined Code of

Practice (1998) London: Gee and

Co.Dickson, M. (2000) Measuring where Capital is

Created and Destroyed, FT, November 2000,vii.

Finkelstein, S. and Hambrick, D. C. (1996) StrategicLeadership:

Top Executives and their Effects onOrganizations. Minneapolis: West

Publishing.

Golding, T. (2001) The City: Inside the Great Expecta-tion

Machine. London: FT Prentice Hall.

Goold, M. and Campbell, A. (1990) Strategies andStyles. Oxford:

Blackwell.

Hambrick, D. C. and Mason, P. A. (1984) UpperEchelons: the

Organization as a Reflection of itsTop Managers, Academy of

Management Review, 9,193206.

Jay, A. (1980) Nobodys Perfect but a Team can be,Observer

Magazine, 20 April 1980, 2637.

Kotter, J. (1988) The Leadership Factor. NY: FreePress.

Mangham, I. L. and Pye, A. J. (1991) The Doing ofManaging.

Oxford: Blackwell.

Morgan, G. (1986) Images of Organization. London:Sage.

Myers, D. G. (1994) Exploring Social Psychology. NY:McGraw

Hill.

Nadler, D. A. and Tushman, M. L. (1990) Beyondthe Charismatic

Leader: Leadership and Organ-izational Change, California

Management Review,32, 7797.

Peters, T. and Waterman, R. W. (1982) In Search ofExcellence.

London: Harper Collins.

Pfeffer, J. (1981) Management as symbolic action.In L. L.

Cummings and B. M. Staw (eds) Researchin Organizational Behavior,

vol. 3: 152. London:JAI Press.

Pye, A. J. (1995) Strategy through Dialogue andDoing, Management

Learning, 26(4), 445462.

Pye, A. J. (2000a) Changing Scenes, In, From andOutside the

Board Room: UK Corporate Govern-ance in Practice from 1989 to 1999,

CorporateGovernance, 8(4), 335346.

Pye, A. J. (2000b) Board Members, Fund Managersand the Power of

Social Capital: Making Sense ofChanging Explanations from 1989 to

1999. Paperpresented to the British Academy of Manage-ment Annual

Conference, Edinburgh.

Pye, A. J. (2001) Corporate Boards, Investors andtheir

Relationships: Accounts of Accountabilityand Corporate Governing in

Action, CorporateGovernance, 9, 186195.

Quelch, J. (2000) Meet Britains Real Rulers: theFirst Men of the

Footsie, Independent on Sunday,5 March, i.

Stiles, P. and Taylor, B. (2001) Boards at Work: HowDirectors

View their Roles and Responsibilities.Oxford: Oxford University

Press.

Tichy, N. M. and Charan, R. (1995) The CEO asCoach, Harvard

Business Review, 2, 6978.

Annie Pye is a Senior Lecturer in Manage-ment at the University

of Bath, School ofManagement. She was funded by ESRC in19982000 to

repeat her 19879 study of chiefexecutives, chairmen and board

members inlarge UK organisations, e.g. Prudential,Marks &

Spencer, Hanson, etc. Her empiricalwork and writing relates to

strategy, leader-ship, structure, culture, top teams,

corporategovernance and social capital: perhaps bestsummed up by

the phrase sensemaking.She wrote The Doing of Managing with

IainMangham and publishes in a range of journals,including

Organization Science, Journal of Man-agement Inquiry and Corporate

Governance.

CORPORATE GOVERNANCE162

Volume 10 Number 3 July 2002 # Blackwell Publishers Ltd 2002

-

Copyright of Corporate Governance: An International Review is

the property of Wiley-Blackwell and itscontent may not be copied or

emailed to multiple sites or posted to a listserv without the

copyright holder'sexpress written permission. However, users may

print, download, or email articles for individual use.