Embed Size (px)

Citation preview

03.05.2011 | www.gtai.com 1

©Chri

s S

chm

idt

- is

tockphoto

PV Germany:

New Investment Opportunities with Grid Parity

Tobias Homann

Taipei, May 2011

03.05.2011 | www.gtai.com 2

Executive Summary

Germany is the world‟s leading PV market with 17.2 GWp of cumulated

PV Power and 7.4 GWp of newly installations in 2010. It will remain the

largest market for the next years.

Customers in largest segment favor “Made in Germany” quality.

The German PV cluster has a unique concentration of manufacturers,

suppliers, project developers and R&D institutes. It offers easy access

to know-how and existing infrastructure.

Experience of engineering companies and local authorities enables fast

realization of manufacturing projects.

Significant investment opportunities exist at all stages of the value

chain and in all technologies.

GTAI supports you to become part of the world‟s leading PV cluster.

03.05.2011 | www.gtai.com 3

I. Germany Trade & Invest

II. The German PV Policy & Market

III. The German PV Industry

IV. Advantages of Germany as an Investment Location

03.05.2011 | www.gtai.com 4

www.gtai.com

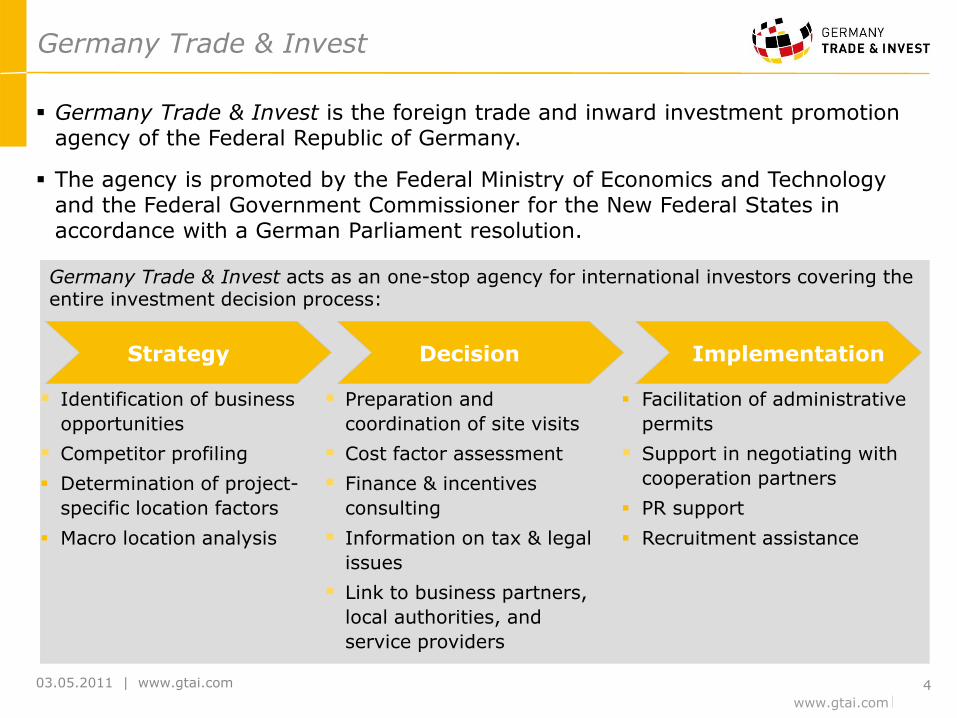

Germany Trade & Invest is the foreign trade and inward investment promotion agency of the Federal Republic of Germany.

The agency is promoted by the Federal Ministry of Economics and Technology and the Federal Government Commissioner for the New Federal States in accordance with a German Parliament resolution.

Germany Trade & Invest

Germany Trade & Invest acts as an one-stop agency for international investors covering the entire investment decision process:

Preparation and

coordination of site visits

Cost factor assessment

Finance & incentives

consulting

Information on tax & legal

issues

Link to business partners,

local authorities, and

service providers

Facilitation of administrative

permits

Support in negotiating with

cooperation partners

PR support

Recruitment assistance

Implementation Decision Strategy

Identification of business

opportunities

Competitor profiling

Determination of project-

specific location factors

Macro location analysis

03.05.2011 | www.gtai.com 5

Example: Milestones of a PV manufacturing project

European location analysis (long list)

Detailed site evaluation

Initial site visits

Re-evaluation of site analysis

(short list)

In-depth site visit (LOIs)

Incentive comparison

Detailed incentives

assessment

Incentive calculation

Approval of incentives

Incentives application

Negotiation of incentives

(LOI)

Meeting with financing partners

Negotiation of Conditions

(Term Sheet)

Building and Environmental

permit

Discussion about

infrastructure upgrades

Detailed site matrix

(plot analysis)

Meeting with engineering companies

Start of construction

Utility prices and reliability comparison

LOIs for utility supply

Discussion of utility

requirements

Site Decision. MoU

Advice on financial structure

Financial agreement

Site Selection

Incentives

Financing

Utilities

Engineering

Months (est.): 0 2 4 6 8 T

The Role of Germany Trade & Invest

Germany Trade & Invest closely supports the project team throughout

the investment decision making process

03.05.2011 | www.gtai.com 6

The Role of Germany Trade & Invest – Success Stories

*) As planned by company 1) Current number of employees 2) GTAI support: from start of project to construction

Germany Trade & Invest has successfully supported some of the most

renowned PV companies in their location decisions

Size and Type of Facility*

Invest-ment

Volume*

446 MWp Module Factory (CdTe)

€ 275 Mil.

100 MWp Integrated

Factory (Ribbon-

Si)

€ 180 Mil.

500 MWp Module Factory (CIGS)

€ 25 Mil.

120 MWp Module Factory (CIS)

€ 210 Mil.

120 MWp Module Factory

(a-Si/µc-Si)

€ 95 Mil.

80 MWp Cell

Factory (c-Si)

€ 50 Mil.

180 MWp Module Factory (a-Si/a-

Si)

€ 140 Mil.

Job creation1 650 1200 50 200 240 160 170

Time-frame2

June 2005 –

June 2006

Sept 2004 –

July 2005

July 2005 –

Mar 2007

Jan 2006 –

May 2007

July 2006 –

June 2007

July 2006 –

Aug 2007

Oct 2007 –

Aug 2008

Country of Origin

USA Norway

USA USA France Norway Canada UAE

120 MWp Module Factory

(a-Si/µc-Si)

€ 95 Mil.

80 MWp Cell

Factory (c-Si)

€ 50 Mil.

180 MWp Module Factory (a-Si/a-

Si)

€ 140 Mil.

240 160 170

July 2006 –

June 2007

July 2006 –

Aug 2007

Oct 2007 –

Aug 2008

Norway Canada UAE Norway

PV Glass Processing

Factory

€ 24 Mil.

65*

Nov 2007 –

Oct 2009

Norway

PV Glass Processing

Factory

€ 24 Mil.

65*

Nov 2007 –

Oct 2009

Norway

100 MWp Cell

Factory (c-Si)

€ 42 Mil.

160*

Dec 2008 –

Feb 2010

Norway

100 MWp Cell

Factory (c-Si)

€ 42 Mil.

160*

Dec 2008 –

Feb 2010

03.05.2011 | www.gtai.com 7

I. Germany Trade & Invest

II. The German PV Policy & Market

III. The German PV Industry

IV. Advantages of Germany as an Investment Location

03.05.2011 | www.gtai.com 8

The German PV Market

Germany is the world‟s leading PV market

Turnover (incl. exports) € 12.22 bn

Number of jobs 107,800

German PV Market 20102

German PV Industry 20103

New PV Installations 2010 in MWp1

Sources: 1) Solarbuzz estimates March 2011 2) Preliminary numbers by Federal Network Agency March 2011 3) ZSW estimates March 2011

Total 18.2 GWp

Newly installed PV power 7.4 GWp

Investments in new installations3 € 19.5 bn

Total installed PV power 17.2 GWp

Germany

7,644 (42%)

Italy

3,822

Other

Europe 3,276

USA

910

Japan

910

Rest of

World 1,638

03.05.2011 | www.gtai.com 9

Source: Federal Network Agency 2011

Installations in January 2011 grew 20% compared to January 2010

Installed PV capacity by month [in MWp]

The German PV Market: Comparison by Month

3 16 55 115 150

206 307 291

327 378

497

1,461

222 163

331

454

573

2,109

663

363

654

341 360

1,174

266

0

500

1.000

1.500

2.000

2.5002009: 3.8 GWp

2010: 7.4 GWp

2011

03.05.2011 | www.gtai.com 10

3,845

6,900 5,500

4,300 4,515 4,650

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

2009 2010e 2011e 2012e 2013e 2014e

Germany Italy France

Spain Greece Rest of Europe

Source: Bank Sarasin, Nov. 2010

The German PV Market

Annual PV installations [MWp] in Germany will exceed those in other

main markets for years to come:

USA Asia Europe

5,720

10,620

9,833 9,525

10,951

12,374

Latest forecasts for annual installations in Germany in 2011:

10.5 GWp (Photon Consulting, Feb. 2011) 8.2 GWp (Solarbuzz, Feb. 2011) 7.2 GWp (HIS iSupply, March 2011) 7 GWp (Bloomberg NEF, Feb. 2011)

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

2009 2011e 2013e

China Japan India Rest of Asia

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

2009 2011e 2013e

7 GWp (EuPD, Feb. 2011) 5.8 GWp (Deutsche Bank, Feb. 2011) 5-6 GWp (Jefferies & Company, Jan. 2011) 4.5 GWp (Barclays Capital, Feb. 2011)

03.05.2011 | www.gtai.com 11

Fixed feed-in tariff for 20 years

Tariff level depends on the type of electricity generation, the first year of plant operation, and the plant‟s capacity.

Electricity grid operators are obligated to make it a priority to purchase and transmit electricity from renewable energy sources.

The cost benefits are apportioned to all grid system operators across the country and passed on by them to electricity customers

No market cap

FiT degression enforces yearly price reductions

Very unbureaucratic initiating process

Transparent (public register) and reliant

The Renewable Energy Sources Act (EEG)

Source: BMU 2010

EEG has proven to be highly efficient:

High installation volume as adequate ROI ensured

Drives down costs as tariffs lowered

… copied by 52 countries worldwide

EEG: the major market driver, since year 2000

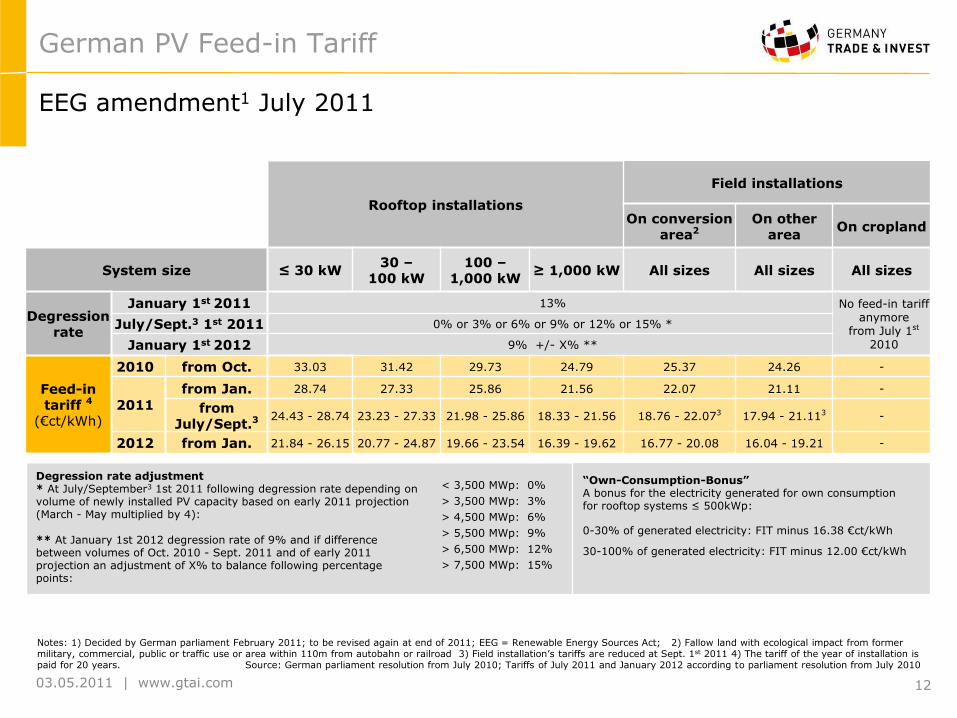

03.05.2011 | www.gtai.com 12

Rooftop installations

Field installations

On conversion area2

On other area

On cropland

System size ≤ 30 kW 30 –

100 kW 100 –

1,000 kW ≥ 1,000 kW All sizes All sizes All sizes

Degression rate

January 1st 2011 13% No feed-in tariff anymore

from July 1st 2010

July/Sept.3 1st 2011 0% or 3% or 6% or 9% or 12% or 15% *

January 1st 2012 9% +/- X% **

Feed-in tariff 4

(€ct/kWh)

2010 from Oct. 33.03 31.42 29.73 24.79 25.37 24.26 -

2011

from Jan. 28.74 27.33 25.86 21.56 22.07 21.11 -

from July/Sept.3

24.43 - 28.74 23.23 - 27.33 21.98 - 25.86 18.33 - 21.56 18.76 - 22.073 17.94 - 21.113 -

2012 from Jan. 21.84 - 26.15 20.77 - 24.87 19.66 - 23.54 16.39 - 19.62 16.77 - 20.08 16.04 - 19.21 -

Notes: 1) Decided by German parliament February 2011; to be revised again at end of 2011; EEG = Renewable Energy Sources Act; 2) Fallow land with ecological impact from former military, commercial, public or traffic use or area within 110m from autobahn or railroad 3) Field installation‟s tariffs are reduced at Sept. 1st 2011 4) The tariff of the year of installation is paid for 20 years. Source: German parliament resolution from July 2010; Tariffs of July 2011 and January 2012 according to parliament resolution from July 2010

EEG amendment1 July 2011

German PV Feed-in Tariff

Degression rate adjustment * At July/September3 1st 2011 following degression rate depending on volume of newly installed PV capacity based on early 2011 projection (March - May multiplied by 4): ** At January 1st 2012 degression rate of 9% and if difference between volumes of Oct. 2010 - Sept. 2011 and of early 2011 projection an adjustment of X% to balance following percentage points:

< 3,500 MWp: 0%

> 3,500 MWp: 3%

> 4,500 MWp: 6%

> 5,500 MWp: 9%

> 6,500 MWp: 12%

> 7,500 MWp: 15%

“Own-Consumption-Bonus” A bonus for the electricity generated for own consumption for rooftop systems ≤ 500kWp:

0-30% of generated electricity: FIT minus 16.38 €ct/kWh

30-100% of generated electricity: FIT minus 12.00 €ct/kWh

03.05.2011 | www.gtai.com 13

1,10

1,30

1,50

1,70

1,90

2,10

2,30

2,50

2,70

2,90

3,10

3,30

3,50

3,70

3,90

4,10

4,30

4,50

4,70

4,90

0,10

0,15

0,20

0,25

0,30

0,35

0,40

0,45

0,50

0,55

2007 2008 2009 2010 2011 2012

Maxim

um

Syste

m P

ric

e f

or 6

% R

OI*

[EU

R/

Wp

]

FIT

/ L

CO

E

[EU

R/

kW

h] Prognosis

Prognosis

Average System Price (100 kWp RT) RT < 100 kWp

RT 100 – 1,000 kWp

RT > 1000 kWp Min./Max Degression RT

Field Installations Min./Max Degression Field Price of Electricity (< 5,000 kWh/a)**

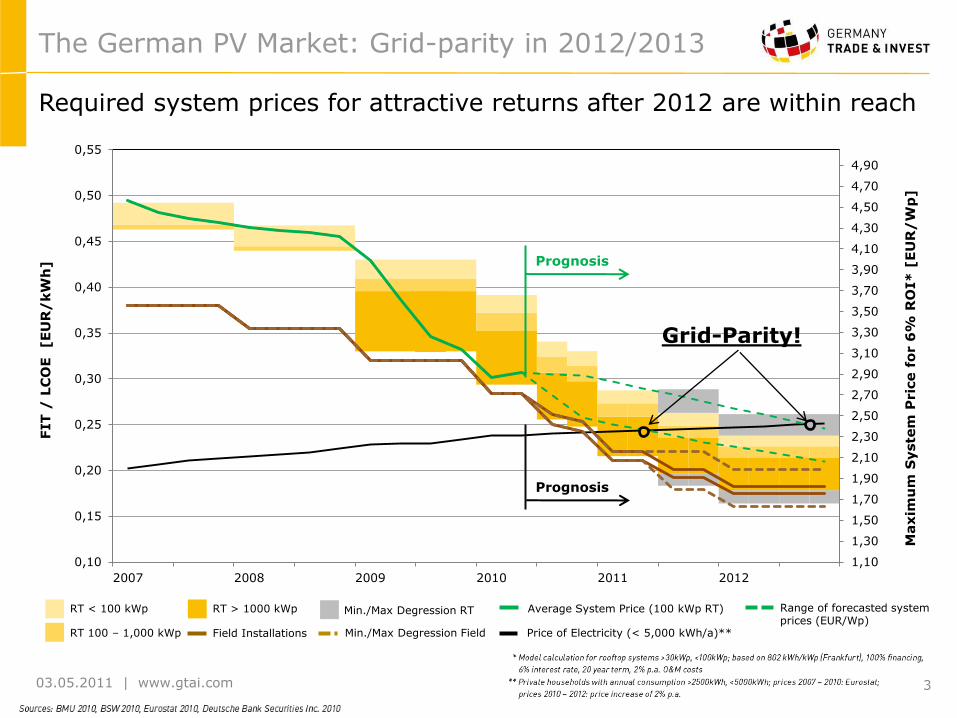

Grid-Parity!

Required system prices for attractive returns after 2012 are within reach

The German PV Market: Grid-parity in 2012/2013

Range of forecasted system prices (EUR/Wp)

03.05.2011 | www.gtai.com 14

The Principle of the „Own-Consumption Bonus“

Wattage

Time of day

0h 3h 6h 9h 12h 15h 18h 21h 24h

Feed-in tariff: 28.74 to 26.24 €ct/kWh1

„Own-Consumption-Bonus“: 15.43 to 9.86 €ct/kWh2

PLUS cost savings

Energy from grid: Costs ~ 22 €ct/kWh3

Funding through feed-in tariff system AND cost savings on grid energy:

Rooftop systems ≤ 500kWp may generate income of > 37 €ct/kWh in 2011

500 kWp max. PV Energy

Energy Demand

„Inhouse“ consumption of PV Energy

Notes: 1) Depending on size of system according to feed-in tariff classification (example based on FIT before July 2011) | 2) Applicable for rooftop systems ≤ 500kWp only | 3) Depending on electricity retail price of respective utility company. Source: German parliament resolution from July 2010

03.05.2011 | www.gtai.com 14

03.05.2011 | www.gtai.com 15

Installed capacity in 2010

Source: Federal Network Agency 2011; Images: Solarwatt, BP, Geosol Note: Figures do not sum to 100%, because of rounding

Systems up to 30kWp are dominating the market, with systems below

10kWp accounting for 43% of the total number of installations

The German PV Market: Installations per Segment

Up to 30kWp 30 - 100kWp 100kWp – 1MWp Over 1MWp

Number of PV systems installed in 2010

TOTAL: 7.4 GWp

35%

23%

23%

19%

84% 13%

3%

0.2%

TOTAL: 249,845

installations

0

5.000

10.000

15.000

20.000

25.000

< 1

kW

p

1 k

Wp

2 k

Wp

3 k

Wp

4 k

Wp

5 k

Wp

6 k

Wp

7 k

Wp

8 k

Wp

9 k

Wp

10 k

Wp

11 k

Wp

12 k

Wp

13 k

Wp

14 k

Wp

15 k

Wp

16 k

Wp

17 k

Wp

18 k

Wp

19 k

Wp

20 k

Wp

21 k

Wp

22 k

Wp

23 k

Wp

24 k

Wp

25 k

Wp

26 k

Wp

27 k

Wp

28 k

Wp

29 k

Wp

30 k

Wp

03.05.2011 | www.gtai.com 16

17.6%

23.8%

50.2%

31.2%

45.1%

37.7%

33.3%

19.4%

7.7%

17.9%

11.7%

Premium Medium class low price No product class assignable

The German PV Market: Customer Preference

Buying decision - Premium modules favored

Source: 1) Sonne Wind & Wärme 1/2011: survey among 25 PV wholesalers, 2010 forecasted; 2) EuPD Research 2009: survey among 202 system owners

36.0%

31.8%

32.2%

30.9%

23.8%

27.8%

8.0%

9.5%

2010

2009

Private Commercial Farmers Others

4.4% Private users

Commercial customers

Farmers

Largest segment: Private users1

Private users favor premium modules²

03.05.2011 | www.gtai.com 17

The German PV Market: Further Characteristics

Image: Sharp

Image: BP

Image: ‚Geosol Image: ‚Geosol

Regional distribution of newly installed

capacity 20101

The German PV market is far from saturation

Others <1%

Sources: 1) Federal Network Agency 2011; 2) IEA 2004; 3) BSW 2011

Market size: Over 201,000 ha of PV-

suitable residential rooftops2

Market growth potential: A potential

rooftop PV capacity of at least 120 GWp.

Experience: More than 860,000 PV

systems have already been installed.3

A mature sales structure: Highly

experienced system integrators and

project developers facilitate easy market

entry and enable rapid market growth for

module manufacturers. Bavaria 33% Baden-

Württemberg 13%

Rheinland-Pfalz 5%

Hessen 5%

Thuringia 2%

Saxony 3%

Saxony-Anhalt 4% North Rhine-

Westphalia 12%

Niedersachsen 11%

Schleswig- Holstein

5% Mecklenburg- Vorpommern

2% Hamburg

Berlin

Brandenburg 5%

Saarland

Bremen

03.05.2011 | www.gtai.com 18

FiTs of major European PV markets

The European Feed-in Tariffs 2011

Sources: BMU 2011 and countries„ respective energy acts 2010/2011 Feed-in tariffs subject to change; *Exchange rate (USD-Euro) from 19.01.2011

UK • Tariff between €0.33 and €0.47/kWh

depending on type and size • Contract duration: 25 years

Belgium: System of green certificates Tariffs vary according to region Min. €0.15/kWh: e.g. Flanders:

€0.45/kWh (contract duration 20 years)

France: Tariffs: €0.58/kWh (rooftop ≤3kWp),

€0.37-0.51/kWh (rooftop >3kWp depending on type of building), €0.276-0.352/kWh (ground-mounted >250kWp), depending on location

Special support in overseas departments Contract duration: 20 years

Portugal Tariff between €0.35 and €0.55/kWh

depending on size/type Contract duration: 15 years or

21GWh/MW Cap: 150MWp (ground-mounted) and

50MW (BIPV)

Spain Tariffs: €0.298/kWh (rooftop ≤20kWp),

€0.209/kWh (rooftop >20kWp), €0.138/kWh (ground-mounted)

Power plant limit size: Rooftop 2MWp; ground-mounted 10MWp

Contract duration: 25 years Cap: 481 MWp (2010); 2011 cap tba

Czech Republic: Tariffs: €0.305/kWh (<30kWp),

€0.236/kWh (30-100kWp), €0.22/kWh (>100kWp)

Solar tax: 26-28% (2011-2013) Contract duration: 20 years Italy Tariff between €0.346 and €0.47/kWh

depending on size/type 2% degression rate per year Contract duration: 20 years Cap :1,200MWp Bulgaria: Tariff s: €0.41/kWh (≤5kW),

€0.37/kWh (>5kW) Contract duration: 25 years Greece: Tariff of €0.55/kWh (rooftop ≤10 kWp) Degression of 5% p.a. 2012-2019 Tariff of €0.37-0.47/kWh depending on

size and location Contract duration: 20 years, linked to

inflation

Turkey* Tariff of €0.01/kWh for 10 years Bonus between €0.02-0.18/kWh for

locally produced components Cap: 600MWp until end of 2013

Germany: Tariff between €0.21 and €0.28/kWh

depending on type/size Quick application process Contract duration: 20 years No cap

03.05.2011 | www.gtai.com 19

I. Germany Trade & Invest

II. The German PV Policy & Market

III. The German PV Industry

IV. Advantages of Germany as an Investment Location

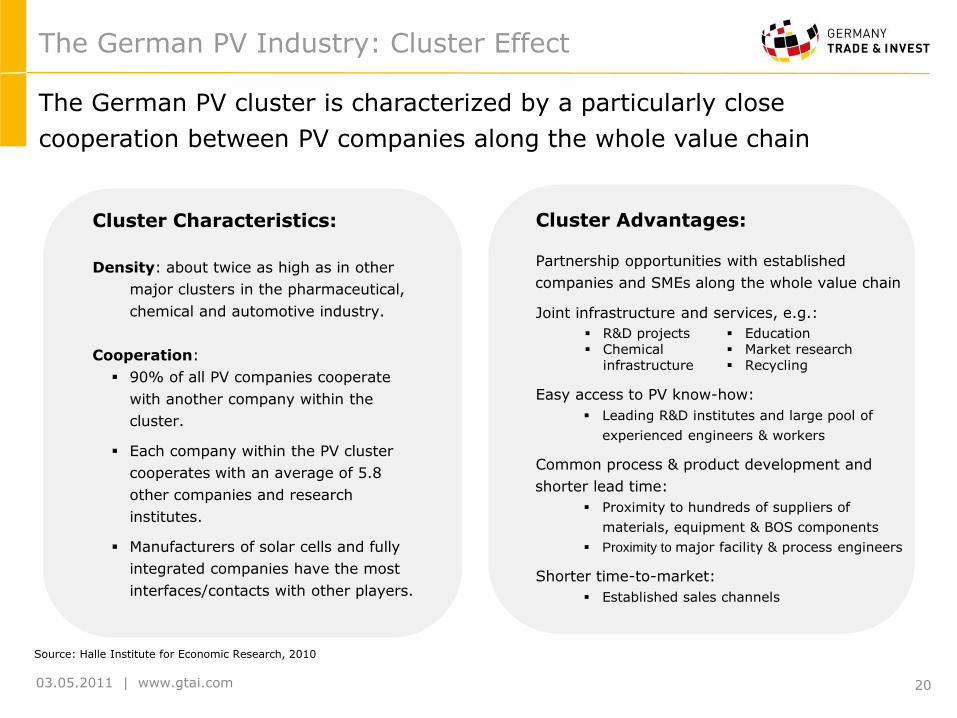

03.05.2011 | www.gtai.com 20

Cluster Advantages:

Partnership opportunities with established

companies and SMEs along the whole value chain

Joint infrastructure and services, e.g.:

Easy access to PV know-how:

Leading R&D institutes and large pool of

experienced engineers & workers

Common process & product development and

shorter lead time:

Proximity to hundreds of suppliers of

materials, equipment & BOS components

Proximity to major facility & process engineers

Shorter time-to-market:

Established sales channels

Cluster Characteristics:

Density: about twice as high as in other

major clusters in the pharmaceutical,

chemical and automotive industry.

Cooperation:

90% of all PV companies cooperate

with another company within the

cluster.

Each company within the PV cluster

cooperates with an average of 5.8

other companies and research

institutes.

Manufacturers of solar cells and fully

integrated companies have the most

interfaces/contacts with other players.

The German PV Industry: Cluster Effect

Source: Halle Institute for Economic Research, 2010

The German PV cluster is characterized by a particularly close

cooperation between PV companies along the whole value chain

R&D projects Chemical

infrastructure

Education Market research Recycling

03.05.2011 | www.gtai.com 21

Germany hosts the world‟s largest PV cluster: (I) Companies in wafer-based technologies

1)Planned / under construction 2)Total number of employees at respective location

The German PV Industry

Source: Germany Trade & Invest, Information provided by the respective company, February 2011

Germany

Value Chain No. Companies Selected Locations Capacity

2011 [MWp] Empl. ²

Silicon 01 Wacker Chemie Burghausen, Nünchritz 33,000t 1766

02 PV Crystalox Solar Silicon Bitterfeld-Wolfen 1,800t 115

03 Joint Solar Silicon Rheinfelden 850t n/a

04 Schmid Pilot Production Spreewitz1 150t 90

Wafer 05 PV Crystalox Erfurt 400 145

06 SCHOTT Solar Wafer Jena 300 400

Cell 07 Q-Cells Bitterfeld-Wolfen 500 1300

08 SCHOTT Solar Alzenau 305 520

09 ITS Innotech Solar Halle 135 36

10 Sunways Konstanz, Arnstadt 116 350

11 Solland Solar Cells Aachen 110 275

12 ARISE Technologies Bischofswerda, Gelsenkirchen 85 160

13 Systaic Heilbronn - 40

Module 14 CENTROSOLAR Wismar 350 700

15 aleo solar (Bosch) Prenzlau 280 801

16 SOLON Berlin, Greifswald 251 470

17 SOLARWATT Dresden 240 470

18 Solar-Fabrik Freiburg 210 350

19 Scheuten Solar Technology Gelsenkirchen 20 270

20 Heckert Solar Chemnitz 180 205

21 ALGATEC Solar Prösen, Großräschen 130 233

22 asola Erfurt 45 120

23 Antaris JuraWatt Neumarkt 40 45

24 solarnova Wedel 25 40

25 alfasolar Hannover 20 85

26 arinna Berlin 20 50

27 GSS Korbußen 20 44

28 Webasto Solar Landsberg/Lech 20 40

29 Solarbau Süd Großbettlingen 15 43

30 Sunware Duisburg < 1 20

31 Sunovation Klingenberg < 1 5

32 Q-mo solar Teltow < 1 5

33 Wulfmeier Solar Bielefeld < 1 5

34 Q-Cells Bitterfeld-Wolfen1 - 1300

Fully Integrated

35 SolarWorld Freiberg 1000/250/550 990

36 Bosch Solar Energy Arnstadt 400/430/n/a1 1500

(Wafer/Cell/ Module)

37 Conergy Frankfurt (Oder) 200/250/250 700

38 Sovello Bitterfeld-Wolfen 180/180/180 1200

CPV 39 Concentrix Solar Freiburg 25 80

Stuttgart

Munich

Hamburg

Düsseldorf

Berlin

Dresden

Frankfurt

Leipzig

16

05

01

07

15

02

03

04

06

08

11

10

13

17

14

18

22

27

24

16

10

01

22

31

11

21

26

33

20

09

36

38

35

37

25

12

19

30

39

24

32

34

29

21

TSMC-Centrosolar

03.05.2011 | www.gtai.com 22

Germany hosts the world‟s largest PV cluster: (II) Companies in thin-film & other technologies

The German PV Industry

1)Planned / under construction 2)Total number of employees at respective location

Source: Germany Trade & Invest, Information provided by the respective company, February 2011

Value Chain

No. Companies Selected Locations Capacity 2011

[MWp] Empl.²

Thin Film

40 Schüco TF Großröhrsdorf 110 150

41 Masdar PV Ichtershausen 75 270

42 Malibu (Schüco) Osterweddingen 45 120

a-Si 43 Inventux Berlin 40 200

a-Si/μc-Si 44 Bosch Thin Film Erfurt 40 195

45 SCHOTT Solar Thin Film Jena 35 200

46 EPV SOLAR Senftenberg 30 110

47 Wilms Gruppe Bitterfeld-Wolfen 25 79

48 CENTROSOLAR Paderborn 6.5 10

49 Solibro (Q-Cells) Bitterfeld-Wolfen 135 500

50 AVANCIS Torgau 120 223

51 Nanosolar Luckenwalde 120 77

52 Sulfurcell Berlin 35 250

CIS 53 Global Solar Berlin 35 100

CIGS 54 Würth Solar Schwäbisch Hall 30 280

CIGSSe 55 Bosch Solar CIS Tech Brandenburg 30 150

56 Odersun Frankfurt (Oder), Fürstenwalde 25 330

57 Solarion Leipzig Pilot 50

58 CIS Solartechnik Bremerhaven Pilot 25

59 PVflex Solar Fürstenwalde Pilot 20

60 First Solar Frankfurt (Oder) 447 600

CdTe 61 Calyxo (Q-Cells) Bitterfeld-Wolfen 25 140

62 ANTEC Solar Arnstadt1 n/a n/a

Poly-Si 63 CSG Solar Bitterfeld-Wolfen - 44

GaAs 64 Azur Space Solar Power Heilbronn 250 135

OPV 65 heliatek Dresden1 - 55

PV & Thermal

66 Solarzentrum Allgäu Altdorf-Biessenhofen 2 100

67 solarhybrid Markranstädt n/a 50

68 Grammer Solar Amberg n/a 45

69 Heli Solar Blankenburg1 n/a 5

Leipzig 55

Germany

Stuttgart

Munich

Hamburg

Düsseldorf

Berlin

Dresden

Frankfurt

54 64

58

65

42

62 44

41 45

57

61 63 49 46

40

60 56

59 51

52

55

43 53

69

67

66

68

48

56 47

50

Walsin Lihwa -Solarion

03.05.2011 | www.gtai.com 23

Collaborating with first-class PV research ensures a sustainable edge

The German PV R&D Institutes

Si feedstock

Wafer based cell technology

Thin film technology

Organic cell technology

Process & production technology

Systems

17 26

36

43

32

35

14

21

42 34

This list is not intended to be exhaustive.

Source: Germany Trade & Invest, September 2009

Nr . Institute Location Activities

1 Fraunhofer Center for Silicon Photovoltaics (CSP ) Halle

2 Fraunhofer Institute of Integrated Systems and Device Technology (IISB),

Erlangen Crystal Growth Laboratory

3 Fraunhofer Technology Center for Semiconducter Materials (THM) Freiberg

4 Institute of Crystal Growth (IKZ) Berlin

5 Fraunhofer Institute for Solar Energy Systems (ISE) Freiburg

6 Freiberg University of Mining and Technology, Institute for Experimental Physics Freiberg

7 International Solar Energy Research Center (ISC-Konstanz) Konstanz

8 University of Konstanz - Dept. of Physics, Section Photovoltaics Konstanz

9 Fraunhofer Institute for Solar Energy Systems (ISE) Freiburg

10 Institute for Solar Energy Research (ISFH) Hameln

11 Bavarian Center for Applied Energy Research (ZAE) Erlangen

12 CeNIDE - Center for Nanointegration, University of Duisburg-Essen Duisburg, Essen

13 CISLAB - Institute of Solid-State Physics, University of Jena Jena

14 Technical University of Ilmenau, Dept. for Experimental Physics Ilmenau

15 University of Technology Darmstadt, Dept. for Material Sciences Darmstadt

16 PV Competence Centre Berlin (PVCOMB), Helmholtz Centre Berlin Berlin

17 Justus-Liebig University of Gießen, Institute of Physics Gießen

18 Institute for Solar Technologies (IST-Frankfurt) Frankfurt (Oder)

19 Next Energy - EWE Research Centre for Energy Technology, University of Oldenburg Oldenburg

20 University of Oldenburg, Institute of Physics Oldenburg

21 University of Stuttgart, Institute of Physical Electronics (IPE) Stuttgart

22 Institute of Photonic Technology (IPHT) Jena

23 Institute of Photovoltaics, Research Centre Jülich (IPV) Jülich

24 Centre for Solar Energy and Hydrogen Research Baden-Württemberg (ZSW) Stuttgart, Widderstall

25 CeNS - Center for NanoScience, Ludwig-Maximilians-University Munich Munich

26 Department of Physics, University of Technology Munich Munich

27 Fraunhofer Institute for Applied Polymer Research (IAP) Potsdam

28 Fraunhofer Institute for Photonic Mircosystems Dresden

29 Light Technology Institute, Karlsruhe Institute of Technology (KIT) Karlsruhe

30 Technical University Dresden, Institute for Applied Photo Physics (IAPP) Dresden

31 University of Hannover, Institute of Physical Chemistry and Electrochemistry (PCI) Hannover

32 University of Potsdam, Institute for Physics and Astronomy Potsdam

33 University of Würzburg, Institute of Experminental Physics VI Würzburg

34 Thuringian Institute of Textile and Plastics Research (TITK) Rudolstadt

35 Center for Organic Materials and Electronics Devices (COMEDD) Dresden

36 Fraunhofer Institute for Electron Beam and Plasma Technology (FEP) Dresden

37 Fraunhofer Institute for Laser Technology (ILT) Aachen

38 Fraunhofer Institute for Production Technology and Automation (IPA) Stuttgart

39 Fraunhofer Institute for Silicate Research, (ISC-Würzburg) Würzburg

40 Fraunhofer-Institute for Surface Engineering and Thin Films (IST-Braunschweig) Braunschweig

41 Fraunhofer Institute for Material and Beam Technology (IWS) Dresden

42 KIT - Karlsruhe Institute of Technology Karlsruhe

43 Institute for Plastics Technologies & Recycling (IKTR) Weißandt-Gölzau

44 Laser Zentrum Hannover (LZH) Hannover

45 Photovoltaic Institute Berlin (PI-Berlin) Berlin

46 Institute for Microsensorics (CIS), Solar Centre Erfurt

47 Chair for Thermodynamics, University of Technology Munich Munich

48 Institut für Solare Energieversorgungstechnik (IWES) Kassel

41

27

28

29

33

Stuttgart

Munich

Hanover

Düsseldorf

Bremen

Berlin

Dresden

Frankfurt

1 1

2

4

6

7

8 7

9

10

15

16

15

17

20

21

22 23 23

9

10

11

11

24

14

16

20

21

9

31

11

356

16

38

39

7

40

41

45

46

24 24

9

48

10

32

3

19

25

26

47

14

12 12

13

5

03.05.2011 | www.gtai.com 24

Proximity to leading PV equipment companies accelerates production ramp-up (I)

1)Total number of employees at respective location This list is not intended to be exhaustive.

Source: Germany Trade & Invest, Information provided by the respective company, August 2010

The German PV Equipment Industry

Equipment No. Companies Selected Locations Empl.1

Silicon 01 centrotherm SiTec Blaubeuren 150 - Equipment 02 Decker Berching 50

03 G+R GreenTech Regenstauf 200

04 PVA TePla Wettenberg, Jena 300

05 STANGL Semiconductor Equipment Fürstenfeldbrück 170

Ingot/Wafer 06 ALD Vacuum Technologies Hanau 365 - Equipment 07 Centrotherm SiTec Blaubeuren 150

08 Elma Singen 190

09 G&N Erlangen 33 10 Herbert Arnold Weilburg 190

11 HK Präzisionstechnik Obernburg 40

12 KUKA Systems Augsburg 1200 13 LOG-O-MATIC Mainaschaff 20 14 PVA TePla Wettenberg, Jena 300

15 RENA Gütenbach, Berg, Herrenberg 1150

16 Schmid Freudenstadt, Niedereschach 750

17 STANGL Semiconductor Equipment Fürstenfeldbrück 170

Cell 18 centrotherm photovoltaics group Blaubeuren 1500

- Turnkey Lines

19 Roth & Rau Hohenstein-Ernstthal 500 20 Schmid Freudenstadt, Niedereschach 750

21 SINGULUS TECHNOLOGIES Kahl 270

Cell 22 centrotherm thermal solutions Blaubeuren 470

- Thermal Equipment

23 ATV TECHNOLOGIE Vaterstetten 24 24 Rehm Thermal Systems Blaubeuren 170

Cell 25 Decker Berching 50 - Wet Chemistry

26 LOTUS Systems Gutmadingen 90

27 Ramgraber Hofolding b. Brunnthal 45

28 RENA Gütenbach, Berg, Herrenberg 1150

29 Schmid Freudenstadt 550 30 STANGL Semiconductor Equipment Fürstenfeldbrück 170

Cell 31 Applied Materials Alzenau 540 - Anti-reflective 32 centrotherm photovoltaics group Blaubeuren 1500 Coating 33 Roth & Rau Hohenstein-Ernstthal 500

34 Schmid Freudenstadt 550 35 SINGULUS TECHNOLOGIES Kahl 270

36 VON ARDENNE Anlagentechnik Dresden 570 Cell 37 ASYS Automatisierungssysteme Dornstadt 400

- Screen Printers

38 JRT Photovoltaics Malterdingen 80 39 Manz Automation Reutlingen 400

40 THIEME Teningen 350 Module 41 ACI-ecotech Zimmern ob Rottweil 100

- Turnkey 42 ATS Automation Tooling Systems Munich 80 Lines 43 Böhm-Solar Equipment Technology Zella-Mehlis 200

44 Bürkle Freudenstadt, Rietberg 140

45 centrotherm photovoltaics group Blaubeuren 1500

46 JVG Thoma Freystadt 40 47 KUKA Systems Augsburg 1200

48 MAG Göppingen 320 49 Maschinenbau GEROLD Nettetal 50

50 REIS ROBOTICS Obernburg 830 51 Schmid Freudenstadt, Niedereschach 750 52 Teamtechnik Freiberg am Neckar 350 Module 53 Böhm-Solar Equipment Technology Zella-Mehlis 200

- Stringers, 54 Bürkle Freudenstadt, Rietberg 140

Laminators 55 IMA Automation Berlin Berlin 56

56 JVG Thoma Freystadt 40 57 Meier Solar Solutions Bocholt, Roßla 110 58 REIS ROBOTICS Obernburg 830 59 Robust Remscheid 80 60 Schmid Niedereschach 200 61 SOMONT Umkirch 100 62 Spaleck/ SPALECK-STEVENS InnoTech Bocholt 240

63 Teamtechnik Freiberg am Neckar 350 64 USK Karl Utz Sondermaschinen Limbach-Oberfrohna 230

Stuttgart

Munich

Düsseldorf

Berlin

Dresden

Hamburg

Frankfurt

01

03 02

04

04

05

17 30

08

09

10

11

12

13

14 14

15

15

19 33

16 20

24

23

22

25

26 27 28

28

31

32

18

37 38

39

40

41

44

44

47

50

48 34

52

60

36

63

59

58

59

06

21

35

57

61

54

55

29

64

42

43

45

46

53

54

55

56

51

62

Germany

07

49

03.05.2011 | www.gtai.com 25

Proximity to leading PV equipment companies accelerates production ramp-up(II)

The German PV Equipment Industry

1)Total number of employees at respective location 2)SLS shares employees with USK, No. 55

This list is not intended to be exhaustive.

Source: Germany Trade & Invest Information provided by the respective company, August 2010

Equipment No. Companies Selected Locations Empl.1

Thin Film - Turnkey Lines

65 Bürkle Freudenstadt, Rietberg-Mastholte 140 66 centrotherm photovoltaics group Blaubeuren, Dresden 1500

67 LEYBOLD OPTICS Alzenau, Dresden 380

68 Manz Automation Reutlingen 400 69 Roth & Rau Hohenstein-Ernstthal 500

Thin Film - Vacuum Deposition

70 Aixtron Herzogenrath 450

71 Applied Materials Alzenau 540

72 FHR Anlagenbau Ottendorf-Okrilla 170

73 LEYBOLD OPTICS Alzenau, Dresden 380

74 VON ARDENNE Anlagentechnik Dresden 570

Automation 75 ACI-ecotec Zimmern ob Rottweil 100

76 AMB Automation Langweid 50

77 ASYS Automatisierungssysteme Dornstadt 400

78 ATMsse Singen 50

79 ATS Automation Tooling Systems Munich 80

80 Baumann Amberg 210

81 Bürkle Freudenstadt, Rietberg-Mastholte 140

82 Grenzebach Hamlar 1500

83 IMA Automation Berlin Berlin 56

84 Jonas & Redmann Photovoltaics Berlin 650

85 JRT Photovoltaics Malterdingen 80

86 KUKA Systems Augsburg 1200

87 MAG Göppingen 320

88 Manz Automation Reutlingen 400

89 Maschinenbau GEROLD Nettetal 50

90 MiniTec Maschinenbau Waldmohr 170

91 Mondragon Assembly Stockach 20

92 Olbricht Hamminkeln-Brünen 30

93 REIS ROBOTICS Obernburg 800

94 RENA Gütenbach, Gutmadingen, Berg 1150

95 Rommel Ehingen 100

96 Schiller Automation Sonnenbühl-Genkingen 264 97 Schmalz Glatten 420

98 Schmid Niedereschach 200

99 SLS Solar Line Saxony Limbach-Oberfrohna 20² Laser Processing 100 3D-Micromac Chemnitz 70

101 4JET Ahlsdorf 30

102 ASYS Automatisierungssysteme Dornstadt 400

103 InnoLas Krailling 80

104 Jenoptik Automatisierungstechnik Jena 200

105 LPKF SolarQuipment Suhl-Friedberg 50

106 MAG Göppingen 320

107 Manz Automation Reutlingen 400

108 Rofin Starnberg, Hamburg, Günding 1600 109 Schmid Schwetzingen 60

Stuttgart

Munich

Düsseldorf

Berlin

Dresden

Hamburg

Frankfurt

75

76 75

78

79

80

82

83

84

85 83

89

90

91

92

93

94

95

96 98

99 100

103

108

108

107

88

102

84

94

101

100

97

71

65

66

64

67

67

66

69

70

73

73

72 74

101

Germany

65

81

81

68

108

109

102

03.05.2011 | www.gtai.com 26

I. Germany Trade & Invest

II. The German PV Policy & Market

III. The German PV Industry

IV. Advantages of Germany as an Investment Location

03.05.2011 | www.gtai.com 27

PV Manufacturing in Germany

Germany offers unique advantages - especially for module manufacturing

Higher selling prices

”Made in Germany“ premium brand: easier access to private customers (>35% market share and growing)

Direct link to customer (e.g. ”transparent factory“ concept) satisfying more differentiated markets (e.g. BIPV)

Distinction against competitors at home

Shorter time to market

Short reaction time, just-in-time delivery, optimized supply chain - especially in volatile market

Close proximity to other European markets

Optimized costs

Less transportation costs

Reduced long-term transport inventories

Moderate production costs, cash grants of up to 50% available

Lowered risks

Reduced price risks

Eurozone: single currency means no exchange rate risk

Potential trade barriers eliminated

Lobby power

Many partners

Access to large local supplier base for materials (e.g. glass)

Cooperation with utilities, test houses, banks, insurances, system integrators, proj. developers, R&D institutes

03.05.2011 | www.gtai.com 28

Incentives available to investment projects in Germany

German Incentives Overview

Germany offers different incentive packages to reimburse the

expenditures of an investment project

Incentives

Reducing Operating Costs

R&D Incentives Labor-Related

Incentives

Training Support

Recruitment Support

Grants

Silent / Direct Partnership

Loans

Wage Subsidies

State Investment

Grant

Cash Incentives Reduced Interest

Loans Public

Guarantees

KfW Loans (National Level)

Investment Allowance

State Development

Banks

Combined State/ Federal

Reducing Investment Costs

Up to 50 %

03.05.2011 | www.gtai.com 29

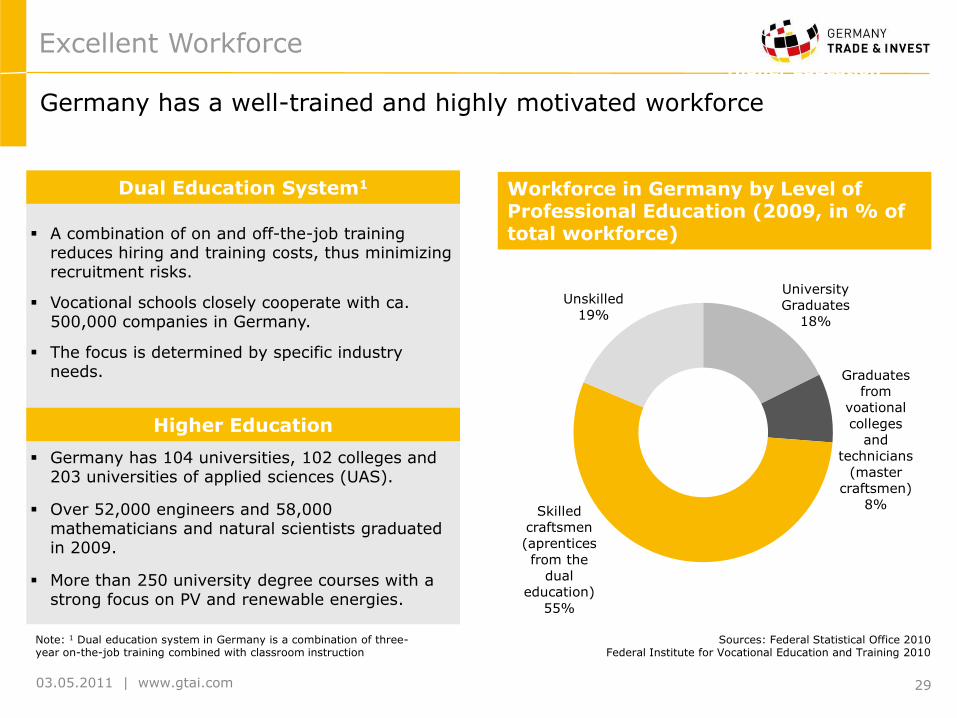

Excellent Workforce

Germany has a well-trained and highly motivated workforce

Higher Education

University

Graduates

18%

Graduates

from

voational

colleges

and

technicians

(master

craftsmen)

8% Skilled

craftsmen

(aprentices

from the

dual

education)

55%

Unskilled

19%

Excellent Workforce

Germany has 104 universities, 102 colleges and 203 universities of applied sciences (UAS).

Over 52,000 engineers and 58,000 mathematicians and natural scientists graduated in 2009.

More than 250 university degree courses with a strong focus on PV and renewable energies.

A combination of on and off-the-job training reduces hiring and training costs, thus minimizing recruitment risks.

Vocational schools closely cooperate with ca. 500,000 companies in Germany.

The focus is determined by specific industry needs.

Higher Education

Dual Education System1

Sources: Federal Statistical Office 2010 Federal Institute for Vocational Education and Training 2010

Workforce in Germany by Level of Professional Education (2009, in % of total workforce)

Note: 1 Dual education system in Germany is a combination of three-year on-the-job training combined with classroom instruction

03.05.2011 | www.gtai.com 30

The labor cost increase in Germany is the lowest in Europe

German Labor Market

Growth of Labor Costs 2001-2009 (yr. average growth | % of total economy)¹

Average gross monthly earnings Western and Eastern Germany2

2,652 2,718

2,806 2,889

2,954 3,009

3,060 3,134

3,213 3,248

1,929 1,982

2,077 2,141

2,191 2,239

2,279 2,344

2,431 2,486

1.500

1.700

1.900

2.100

2.300

2.500

2.700

2.900

3.100

3.300

3.500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Western Germany Eastern Germany

9.1

7.9

7.4

6.9

4.6

4.2

3.5

3.4

3.0

1.9

0 2 4 6 8 10

Hungary

Slovak Republic

Czech Republic

Poland

Spain

UK

Netherlands

EU-27

France

Germany

Note: 1) No data available for USA and Japan 2) In industry and service sector excluding bonuses in €/month Sources: Eurostat 2010, German Federal Statistics Office 2010

03.05.2011 | www.gtai.com 31

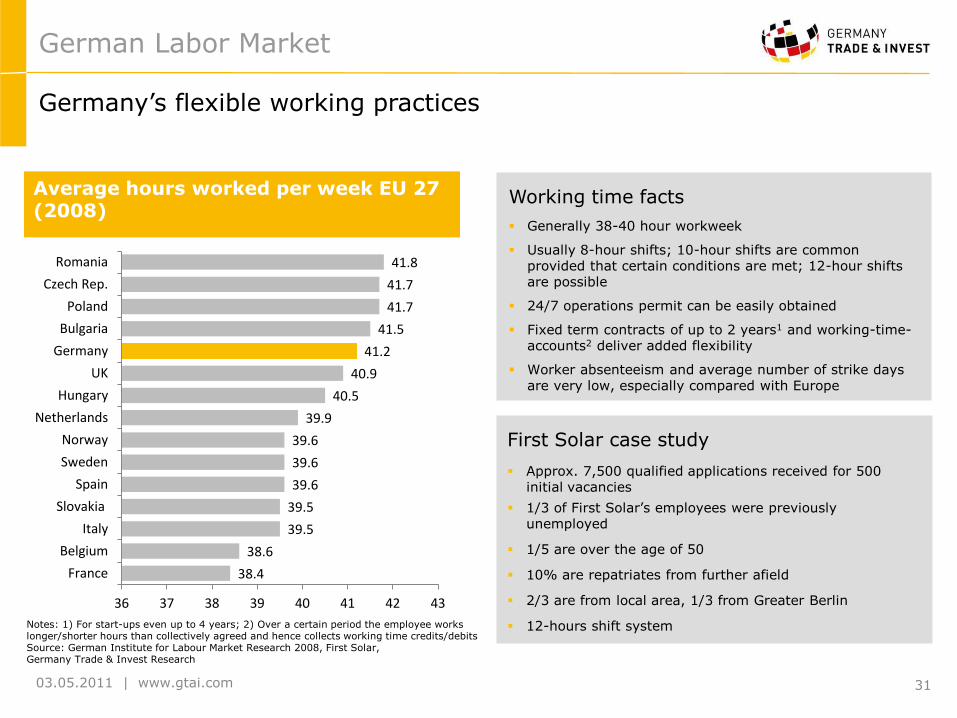

German Labor Market

Germany‟s flexible working practices

Notes: 1) For start-ups even up to 4 years; 2) Over a certain period the employee works longer/shorter hours than collectively agreed and hence collects working time credits/debits Source: German Institute for Labour Market Research 2008, First Solar, Germany Trade & Invest Research

Working time facts

Generally 38-40 hour workweek

Usually 8-hour shifts; 10-hour shifts are common provided that certain conditions are met; 12-hour shifts are possible

24/7 operations permit can be easily obtained

Fixed term contracts of up to 2 years1 and working-time-accounts2 deliver added flexibility

Worker absenteeism and average number of strike days are very low, especially compared with Europe

First Solar case study

Approx. 7,500 qualified applications received for 500 initial vacancies

1/3 of First Solar‟s employees were previously unemployed

1/5 are over the age of 50

10% are repatriates from further afield

2/3 are from local area, 1/3 from Greater Berlin

12-hours shift system

Average hours worked per week EU 27 (2008)

38.4

38.6

39.5

39.5

39.6

39.6

39.6

39.9

40.5

40.9

41.2

41.5

41.7

41.7

41.8

36 37 38 39 40 41 42 43

France

Belgium

Italy

Slovakia

Spain

Sweden

Norway

Netherlands

Hungary

UK

Germany

Bulgaria

Poland

Czech Rep.

Romania

03.05.2011 | www.gtai.com 32

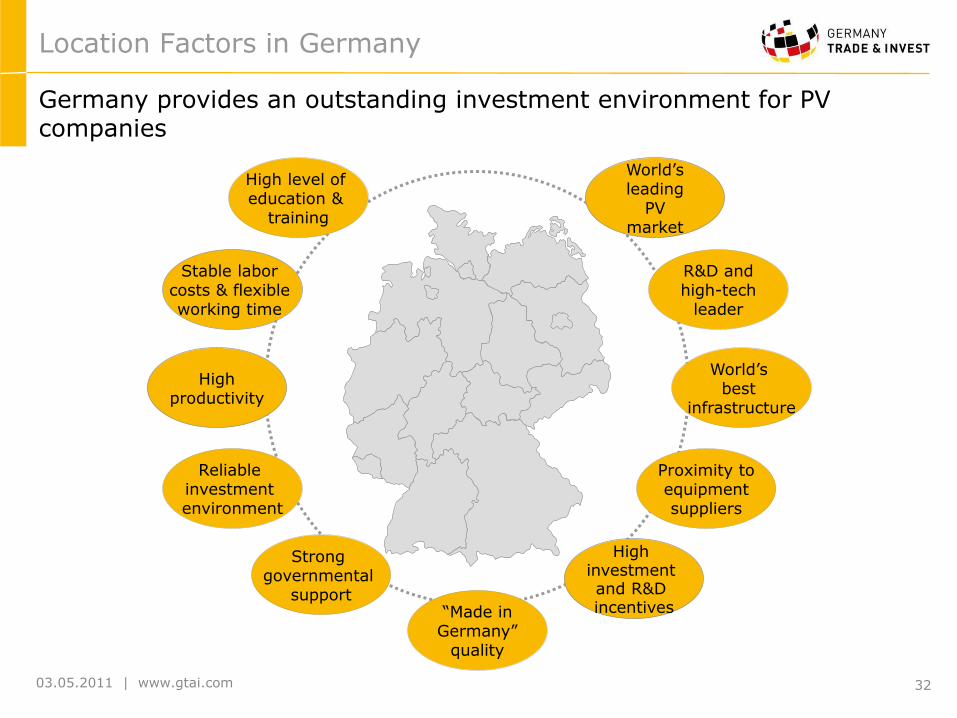

World‟s leading

PV market

High level of education &

training

R&D and high-tech

leader

“Made in Germany”

quality

Reliable investment environment

World‟s best

infrastructure

Stable labor costs & flexible working time

High investment and R&D incentives

High productivity

Proximity to equipment suppliers

Location Factors in Germany

Germany provides an outstanding investment environment for PV companies

Strong governmental

support

03.05.2011 | www.gtai.com 33

Testimonials

Why foreign PV companies invested in Germany:

03.05.2011 | www.gtai.com 34

Germany Trade & Invest

Foreign Trade and Inward Investment Promotion Agency

Germany Trade & Invest

© 2011 Germany Trade & Invest All information provided by Germany Trade & Invest has been put together with the utmost care. However we assume no liability for the accuracy of the information provided.

Contact for PV investments

Germany Trade & Invest Mr. Thomas Grigoleit Director Renewable Energies & Resources Friedrichstraße 60 10117 Berlin Germany

T. +49 30 200 099-224 F. +49 30 200 099-111

Germany Trade & Invest Ms. Anne Bräutigam Manager Photovoltaics Friedrichstraße 60 10117 Berlin Germany T. +49 30 200 099-228 F. +49 30 200 099-111

Germany Trade & Invest Mr. Tobias Homann Senior Manager Photovoltaics Friedrichstraße 60 10117 Berlin Germany T. +49 30 200 099-391 F. +49 30 200 099-111

San Francisco Office Ms. Angelika Geiger Director One Embarcadero Center Suite 1060 San Francisco, 94111, CA USA T.: +1 (415) 248-1246 F.: +1 (415) 627-9169 [email protected]

Tokyo Office Mr. Iwami Asakawa Japan Representative Sanbancho KS Bldg. 5F 2-4 102-0075 Sanbancho, Chiyoda-ku,Tokyo, Japan T.: +81 3 5275 2072 F.: +81 3 5275 2012 [email protected]

New York Office Mr. Claus Habermeier Director 75 Broad Street, 21st Floor New York, 10004, NY USA T.: +1 (212) 584-9715 F.: +1 (212) 262-6449 [email protected]

Beijing Office Mr. Markus Hempel China Representative Unit 0811, Landmark Tower II 8 North Dongsanhuan Road Chaoyang District, Beijing 100004 T. +86 (10) 6539 6725 F. +86 (10) 6590 6167 [email protected]

Germany Trade & Invest Mr. Tobias Rothacher Manager Photovoltaics Friedrichstraße 60 10117 Berlin Germany T. +49 30 200 099-225 F. +49 30 200 099-111