Embed Size (px)

Citation preview

Putting Patients & Providers in ControlPutting Patients & Providers in Control™™

What is a Health Savings What is a Health Savings Account (HSA)?Account (HSA)?

““Medical IRA” Medical IRA” Consumer owns HSA and directs how it is investedConsumer owns HSA and directs how it is invested Contributions to HSA pre-tax; earnings grow tax-freeContributions to HSA pre-tax; earnings grow tax-free High Deductible Health Plan (HDHP) must be set-upHigh Deductible Health Plan (HDHP) must be set-up HDHP plan has a higher deductible limit and HDHP plan has a higher deductible limit and will cost will cost

considerably less than current plansconsiderably less than current plans

HSA TrendsHSA Trends

3 million now ……. 60 million by 20093 million now ……. 60 million by 2009

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009

HSAs Control Runaway CostsHSAs Control Runaway Costs

Cost for Family of Four in IndianaCost for Family of Four in Indiana

0

5000

10000

15000

20000

25000

2005 2006 2007 2008 2009

HM MinimumFundingHM MaximumFundingTraditionalHealth Plan

Traditional PPO Plan – 2005Traditional PPO Plan – 2005– $12,000 PPO premium $12,000 PPO premium

(Assume 15% increase / year)(Assume 15% increase / year)

– Must pay co-paysMust pay co-pays

– Not everything is coveredNot everything is covered

IMPACT AFTER 5 YEARSIMPACT AFTER 5 YEARS

– Premiums paid: Premiums paid: $80,900$80,900

– Plus co-pays in after tax $Plus co-pays in after tax $

– Plus non-covered services in Plus non-covered services in after tax $after tax $

– Money in account: Money in account: $0$0

Why HSAs are the FutureWhy HSAs are the Future

HSA with HDHP Plan – 2005HSA with HDHP Plan – 2005– $4,000 HDHP premium $4,000 HDHP premium

$5,000 HSA contribution $5,000 HSA contribution $1,000 healthcare expenses $1,000 healthcare expenses (Assume 4% increase / year)(Assume 4% increase / year)

IMPACT AFTER 5 YEARSIMPACT AFTER 5 YEARS

– Total checks written: Total checks written: $54,164$54,164

– Money in accountMoney in account: $21,666: $21,666

– Tax shelter benefitTax shelter benefit: $16,250 : $16,250 (Assuming 30% tax rate)(Assuming 30% tax rate)

– Total benefit: $37,915Total benefit: $37,915

Initiated pilot program with HSAs in 2004Initiated pilot program with HSAs in 2004 Both employer & employee costs reducedBoth employer & employee costs reduced Experience so good they will drop other Experience so good they will drop other

optionsoptions HealthMatch could make it even betterHealthMatch could make it even better

Why HSAs are the FutureWhy HSAs are the Future

Experience with HSAsExperience with HSAs

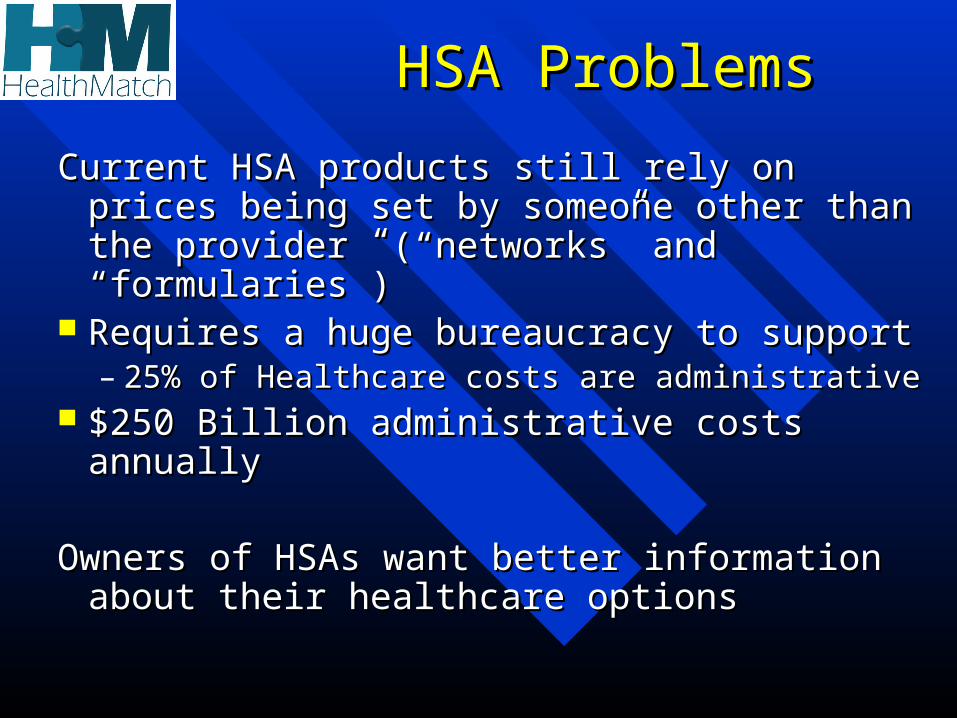

HSA ProblemsHSA Problems

Current HSA products still rely on prices being set Current HSA products still rely on prices being set by someone other than the provider by someone other than the provider (“networks” and “formularies”)(“networks” and “formularies”)

Requires a huge bureaucracy to supportRequires a huge bureaucracy to support– 25% of Healthcare costs are administrative25% of Healthcare costs are administrative

$250 Billion administrative costs annually$250 Billion administrative costs annually

Owners of HSAs want better information about Owners of HSAs want better information about their healthcare options their healthcare options

The HealthMatch SolutionThe HealthMatch Solution

HealthMatch members HealthMatch members shop shop for healthcarefor healthcare– With an HSA, they are spending With an HSA, they are spending their own moneytheir own money

– They shop based on They shop based on price, quality, convenience, service and valueprice, quality, convenience, service and value

HealthMatch provides information consumers HealthMatch provides information consumers have never had beforehave never had before– Members shop for the healthcare they want by product or providerMembers shop for the healthcare they want by product or provider

– Members can shop providers by priceMembers can shop providers by price

– Members can shop providers by consumer feedback ratingsMembers can shop providers by consumer feedback ratings

Intellectual PropertyIntellectual Property

2 patents: comparative healthcare pricing 2 patents: comparative healthcare pricing over the Internet and consumer feedback over the Internet and consumer feedback systemsystem

Provisional Patents granted 1/06Provisional Patents granted 1/06– Atty: Quentin Cantrell, Woodard EmhardtAtty: Quentin Cantrell, Woodard Emhardt

Utility patent filing accepted 7/06Utility patent filing accepted 7/06 Can a provider of consumer driven Can a provider of consumer driven

healthcare with healthcare with competitive pricing competitive pricing avoid avoid using our methods?using our methods?

Our Proprietary AdvantageOur Proprietary Advantage

Each service prompts this rating formEach service prompts this rating form

Allowing HealthMatch to provide information never before available:Allowing HealthMatch to provide information never before available:

Smith and JonesSmith and Jones

Traditional Plan (Smith)

Choose Provider From Network List

Consume “Flat Rate” Healthcare

Hope Service is Covered, Pay Co-Pay

Wait for EOB, Pay Any Remainder

Carrier Keeps Unused Funds

HealthMatch Plan (Jones)

Choose Provider by Comparison Shopping

Consume “Market Priced” Healthcare

Use HealthMatch Debit Card to Pay. TRANSACTION COMPLETE NO PAPERNO CLAIMSNO UNCERTAINTY

Fill out Feedback on Provider

Jones Keeps Unused HSA Funds

Pay $4,000 Premium + $900 fund contr.Pay $12,000 Premium

Provider/Payer Perform 20+ Labor Intensive Steps to Adjudicate Claim

DistributionDistribution

Through traditional network of insurance Through traditional network of insurance brokers and agents (over 30,000)brokers and agents (over 30,000)

HealthMatch has own insurance agency HealthMatch has own insurance agency arm for direct sales (not our prime focus)arm for direct sales (not our prime focus)

Enrollment of Providers will leverage Enrollment of Providers will leverage large groups via existing organizationslarge groups via existing organizations

CompetitionCompetition

Traditional insurers Traditional insurers – Profit from administrative burden - not simple or Profit from administrative burden - not simple or

pleasant for them to changepleasant for them to change– But, they are hedging their betsBut, they are hedging their bets

Other Consumer Driven Health PlansOther Consumer Driven Health Plans– Definity, Lumenos, HealthEquityDefinity, Lumenos, HealthEquity– Lack price transparency, consumer shopping tools Lack price transparency, consumer shopping tools

and market forcesand market forces

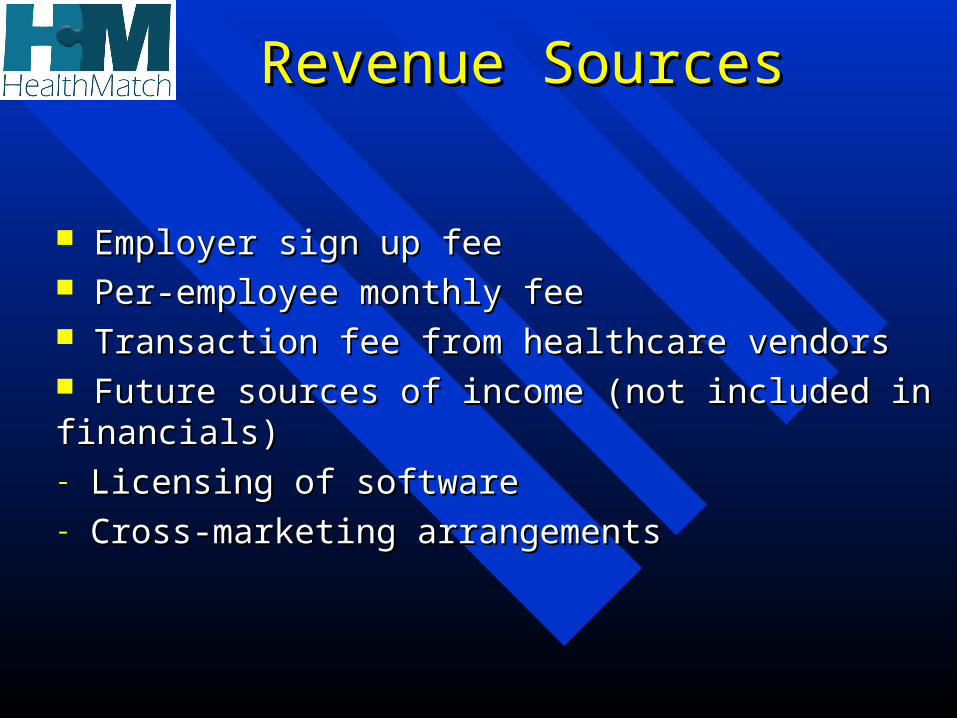

Revenue SourcesRevenue Sources

Employer sign up feeEmployer sign up fee Per-employee monthly feePer-employee monthly fee Transaction fee from healthcare vendorsTransaction fee from healthcare vendors Future sources of income (not included in financials)Future sources of income (not included in financials)- Licensing of softwareLicensing of software- Cross-marketing arrangementsCross-marketing arrangements

Status of DevelopmentStatus of Development

Beta test in Anderson, IN in early 2007Beta test in Anderson, IN in early 2007– We have signed a significant portion of We have signed a significant portion of

Anderson’s primary care providersAnderson’s primary care providers– Now targeting special care physiciansNow targeting special care physicians– Then will target businessesThen will target businesses

SSoftware functional except for consumer feedback oftware functional except for consumer feedback systemsystem

– Feedback system presently being programmedFeedback system presently being programmed

Beta Test ObjectiveBeta Test Objective

Beta test market at 3% share in 3 yearsBeta test market at 3% share in 3 years- yields $4.2 M revenueyields $4.2 M revenue- covers 11,000 memberscovers 11,000 members- provides $2.4 M profitprovides $2.4 M profit- pretax margin is 56.8% pretax margin is 56.8%

Potential market and scalability enormousPotential market and scalability enormous Efficient scaling (think eBay)Efficient scaling (think eBay)

CapitalizationCapitalization

Seeking $1M in new equitySeeking $1M in new equity Represents 48% of Pro-forma equityRepresents 48% of Pro-forma equity Post-Money valuation: $2.1MPost-Money valuation: $2.1M Primary uses of funds: Primary uses of funds:

completion of software and operating expenses completion of software and operating expenses through breakeven (projected for 2Q08)through breakeven (projected for 2Q08)

Indiana Investment Tax CreditIndiana Investment Tax Credit

Entire $1 million is eligible for Indiana Entire $1 million is eligible for Indiana Investment Tax creditInvestment Tax credit

20% of invested amount is a credit against 20% of invested amount is a credit against Indiana Income TaxIndiana Income Tax

Unused balance carries forward for 5 yearsUnused balance carries forward for 5 years $50,000 investment yields $10,000 tax $50,000 investment yields $10,000 tax

credit; net cost = $40,000.credit; net cost = $40,000.

Financial ProjectionsFinancial Projections

(000’s omitted)(000’s omitted)

ActualActual

20052005Pro-FormaPro-Forma

20062006Pro-FormaPro-Forma

20072007Pro-FormaPro-Forma

20082008Pro-FormaPro-Forma

20092009

RevenueRevenue $0$0 $0$0 $311$311 $1,761$1,761 $4,263$4,263

Pretax ProfitPretax Profit ($221)($221) ($367)($367) ($600)($600) $313$313 $2,422$2,422

Net Cash FlowNet Cash Flow $15$15 $552$552 $109$109 $725$725 $709$709

Investment Proceeds +$600K +$400KInvestment Proceeds +$600K +$400K

Deferred Comp +$135K +$424K +$561K -$1.446MDeferred Comp +$135K +$424K +$561K -$1.446M

ROI ROI

PretaxPretax

ProfitProfitPretax Pretax MarginMargin

P/EP/E

WellpointWellpoint $3.9 billion$3.9 billion 8.6%8.6% 17.717.7

United United HealthcareHealthcare $5.1 billion$5.1 billion 11.3%11.3% 19.519.5

HealthMatch HealthMatch ( 3( 3rdrd year ) year )

$2.4 million$2.4 million 56.8%56.8% ????

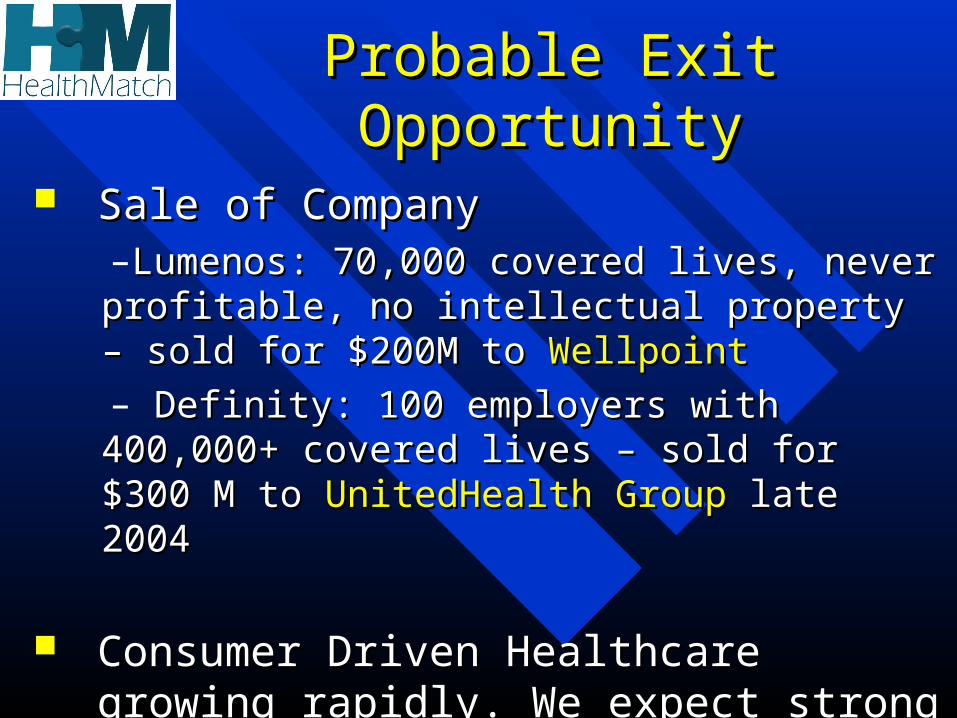

Probable Exit OpportunityProbable Exit Opportunity

Sale of Company Sale of Company –Lumenos: 70,000 covered lives, never profitable, no Lumenos: 70,000 covered lives, never profitable, no intellectual property – sold for $200M to intellectual property – sold for $200M to WellpointWellpoint– Definity: 100 employers with 400,000+ covered lives Definity: 100 employers with 400,000+ covered lives – sold for $300 M to – sold for $300 M to UnitedHealth GroupUnitedHealth Group late 2004 late 2004

Consumer Driven Healthcare growing rapidly. Consumer Driven Healthcare growing rapidly. We expect strong acquisition interest in less than We expect strong acquisition interest in less than 3 years by major players who could leverage 3 years by major players who could leverage HealthMatch to attack industry leadersHealthMatch to attack industry leaders

ContactContact

HealthMatch Solutions, LLCHealthMatch Solutions, LLC2701 Enterprise Drive, Suite 2002701 Enterprise Drive, Suite 200

Anderson, IN 46013Anderson, IN 46013

Ray Snider, CEORay Snider, CEO 317-696-2067 317-696-2067 (Mobile)(Mobile)

Brian Jacobs, MDBrian Jacobs, MD 317-307-0247 317-307-0247 (Pager)(Pager)

Putting Patients & Providers in ControlPutting Patients & Providers in Control™™

Supporting Slides for Q & ASupporting Slides for Q & A

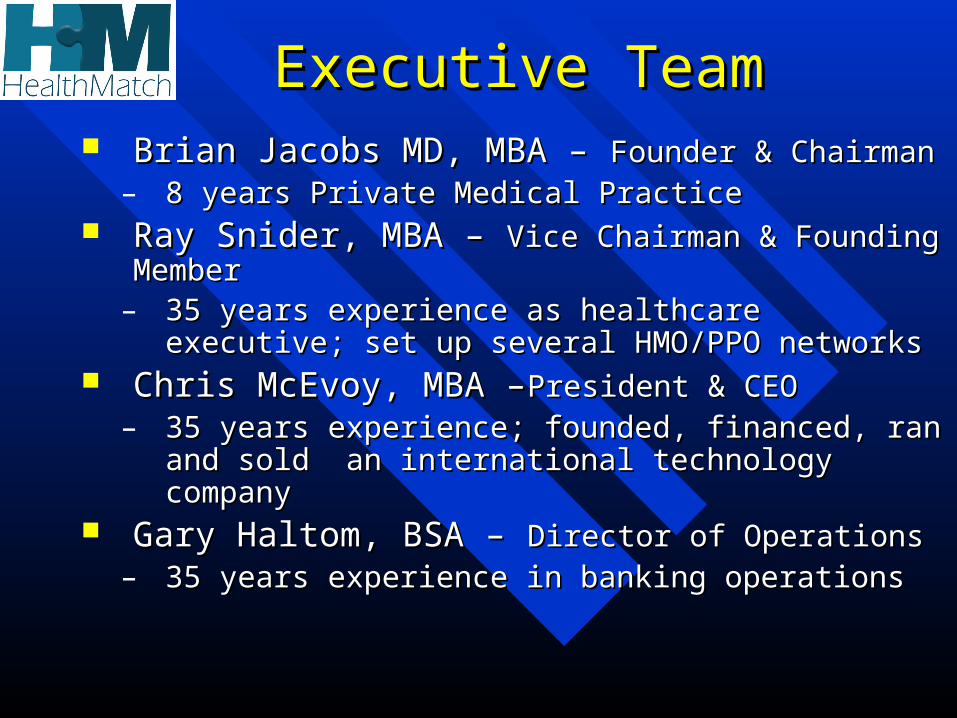

Executive TeamExecutive Team Brian Jacobs MD, MBA – Brian Jacobs MD, MBA – Founder & ChairmanFounder & Chairman

– 8 years Private Medical Practice8 years Private Medical Practice Ray Snider, MBA – Ray Snider, MBA – Vice Chairman & Founding Vice Chairman & Founding

MemberMember– 35 years experience as healthcare executive; set up 35 years experience as healthcare executive; set up

several HMO/PPO networksseveral HMO/PPO networks Chris McEvoy, MBA –Chris McEvoy, MBA –President & CEOPresident & CEO

– 35 years experience; founded, financed, ran and 35 years experience; founded, financed, ran and sold an international technology company sold an international technology company

Gary Haltom, BSA – Gary Haltom, BSA – Director of OperationsDirector of Operations– 35 years experience in banking operations35 years experience in banking operations

HSA ProblemsHSA Problems

We fix this!We fix this!

MilestonesMilestones

Milestones CompletedMilestones Completed

– Phase I Software 2/06Phase I Software 2/06– 11stst Provider Contract 3/06 Provider Contract 3/06– Bank Contract 5/06Bank Contract 5/06– 11stst Hospital system Contract 8/06 Hospital system Contract 8/06– Provisional Patents Granted 1/06Provisional Patents Granted 1/06– Utility Patent Filing Accepted Utility Patent Filing Accepted 7/067/06– First commercial customer 10/06First commercial customer 10/06

Future MilestonesFuture Milestones

– Software completion: 1/07Software completion: 1/07

– Indianapolis launch 7 months Indianapolis launch 7 months after capital raiseafter capital raise

– Breakeven anticipated 18 Breakeven anticipated 18 months after capital raisemonths after capital raise

What is an HSA?What is an HSA?

Example: Family HDHP with $5,000 deductible Example: Family HDHP with $5,000 deductible – Can contribute into HSA the deductible amount of HDHP, in Can contribute into HSA the deductible amount of HDHP, in

this case $5,000 (up to max of $2700 single, $5450 family)this case $5,000 (up to max of $2700 single, $5450 family)

– First $5,000 of medical expenses per year paid from HSAFirst $5,000 of medical expenses per year paid from HSA

– If medical expenses exceed $5,000 deductible, insurance If medical expenses exceed $5,000 deductible, insurance coverage through HDHP kicks incoverage through HDHP kicks in

– While fund is building to maximum, GAP insurance offered to While fund is building to maximum, GAP insurance offered to cover medical expenses that exceed current balance of fundcover medical expenses that exceed current balance of fund

– HSA funds can be used to pay for virtually any medical HSA funds can be used to pay for virtually any medical expense (though some may not count against the deductible)expense (though some may not count against the deductible)

Company Cost TrendsCompany Cost Trends

5.32 5.097.5

-16.26

-26

5.32

10.41

17.92

1.66

-24.35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

2002 2003 2004 2005 2006% increase

Cumulative

Employee Cost TrendsEmployee Cost Trends

3.985.09

12.52

-2.63

-22.39

3.98

9.07

21.59

18.96

-3.43

-25

-20

-15

-10

-5

0

5

10

15

20

25

2002 2003 2004 2005 2006

% increase

Cumulative

MarketsMarkets

Opportunities to market HealthMatch includeOpportunities to market HealthMatch include Complete Benefits SolutionComplete Benefits Solution Providing Support to other HSA VendorsProviding Support to other HSA Vendors

– All HSA vendors would experience administrative cost All HSA vendors would experience administrative cost savings with HealthMatchsavings with HealthMatch

– No claims 94% of the timeNo claims 94% of the time

Direct Support for Consumers using other HSA productsDirect Support for Consumers using other HSA products

Current StatusCurrent Status

Consumers unhappy with current modelConsumers unhappy with current model Employers desperate for changeEmployers desperate for change

– Costs rising faster than the economyCosts rising faster than the economy– Current model cannot be sustainedCurrent model cannot be sustained

Several businesses in central Indiana Several businesses in central Indiana participating in Beta testparticipating in Beta test

Employer AdvantageEmployer Advantage

· Control costs and realize double-digit medical cost savings.

· Can adjust savings by determining contributions to HSAs.

· Consumer-driven health plans restrain health benefit inflation.

Provide even greater savings in subsequent years.

· Experience less hassle and higher employee satisfaction.

· Select high deductible carriers and banking arrangements.

Consumer AdvantageConsumer Advantage- Retains unspent dollars in the HSA for future medical needs.- Retains unspent dollars in the HSA for future medical needs.

- Obtains user-friendly, Internet-based information on price, service, Obtains user-friendly, Internet-based information on price, service, quality, from other members. quality, from other members.

- Select any provider for healthcare services when using funds from Select any provider for healthcare services when using funds from their medical spending accounts.their medical spending accounts.

- Choice of high-deductible Health Insurance coverage.Choice of high-deductible Health Insurance coverage.

- Consumer uses Debit Card to pay for healthcare services.Consumer uses Debit Card to pay for healthcare services.

- Freedom to choose the healthcare they want, yet save money over Freedom to choose the healthcare they want, yet save money over their current traditional plan. their current traditional plan.

Provider AdvantageProvider Advantage

- Choose their own prices in a competitive environment.

- Receive immediate payment directly from the debit card.

- Eliminates slow, laborious, and expensive claims processing.

- Avoids managed care restrictions and reduces administrative costs.

- Does not interfere in the doctor-patient relationship.

- Quick payment through Debit card eliminates bad debt expenses.

Insurance Broker AdvantageInsurance Broker Advantage

- Provides competitive commissions.- Provides competitive commissions.

- Agents improve existing relationships with customers by - Agents improve existing relationships with customers by presenting a new option.presenting a new option.

- Totally new process that provides their customers significant - Totally new process that provides their customers significant savings.savings.

- Helps brokers/agents to attract new customers previously priced - Helps brokers/agents to attract new customers previously priced out of the health insurance market.out of the health insurance market.

THE ENDTHE END