Embed Size (px)

Citation preview

Putting confidence atyour fingertips

Financial Reporting UpdateMarch 2015

New for June 2015

Applicable for the first time

• Accounting for levies

• Offsetting financial instruments

• Annual improvements

IFRIC agenda decisions

Available for early adoption

• AASB 9 Financial instruments

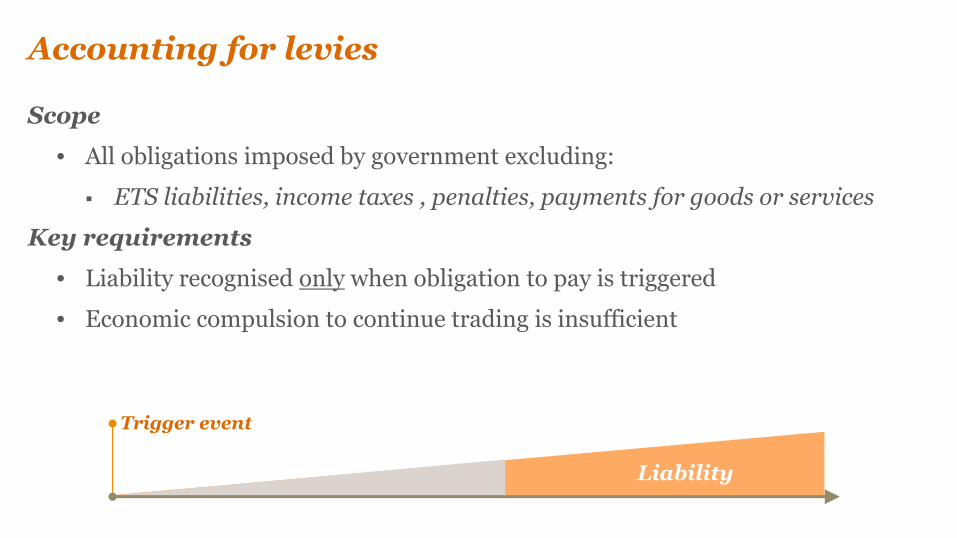

Accounting for levies

Scope

• All obligations imposed by government excluding:

ETS liabilities, income taxes , penalties, payments for goods or services

Key requirements

• Liability recognised only when obligation to pay is triggered

• Economic compulsion to continue trading is insufficient

Liability

Trigger event

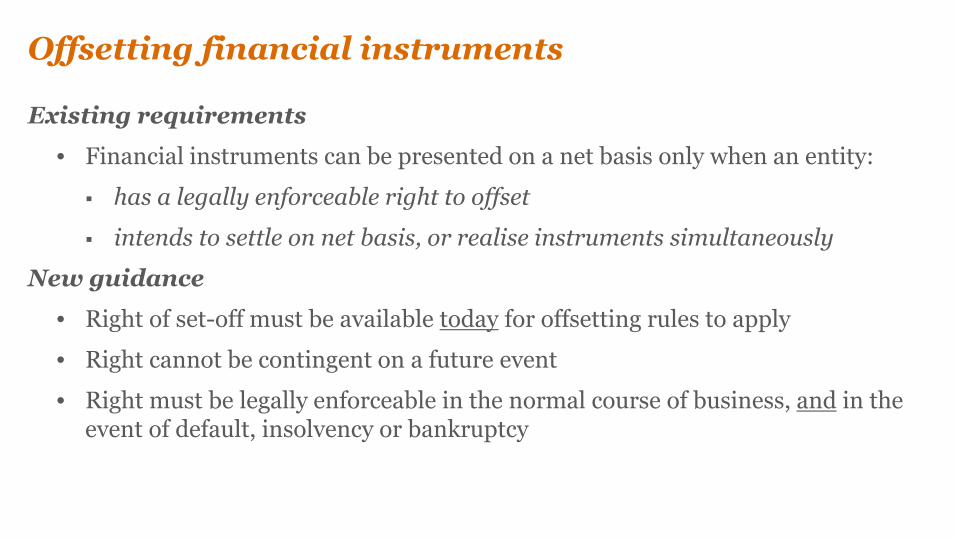

Offsetting financial instruments

Existing requirements

• Financial instruments can be presented on a net basis only when an entity:

has a legally enforceable right to offset

intends to settle on net basis, or realise instruments simultaneously

New guidance

• Right of set-off must be available today for offsetting rules to apply

• Right cannot be contingent on a future event

• Right must be legally enforceable in the normal course of business, and in theevent of default, insolvency or bankruptcy

Annual improvements

Contingent consideration

• All non-equity contingent consideration to be measured at fair value throughprofit or loss

Related parties

• Related parties include an entity that provides KMP services to the reportingentity

Investment property

• Acquisition of an investment property may fall within the scope of a businesscombination

Operating segments

• Disclose judgements made in aggregating multiple segments

IFRIC agenda decisions

• Significant judgments in a going concernassessment

• Income taxes

• Joint arrangements

AASB 9 Financial instruments

Key considerations

• Early adopters are taking advantage of favourable hedging rules

• Classification rules for financial assets may also be beneficial

• Must be adopted in its entirety

• Mandatory for years beginning on or after 1 January 2018

01

02

03

Classification& Measurement

Expected CreditLosses

Hedging

AASB 9

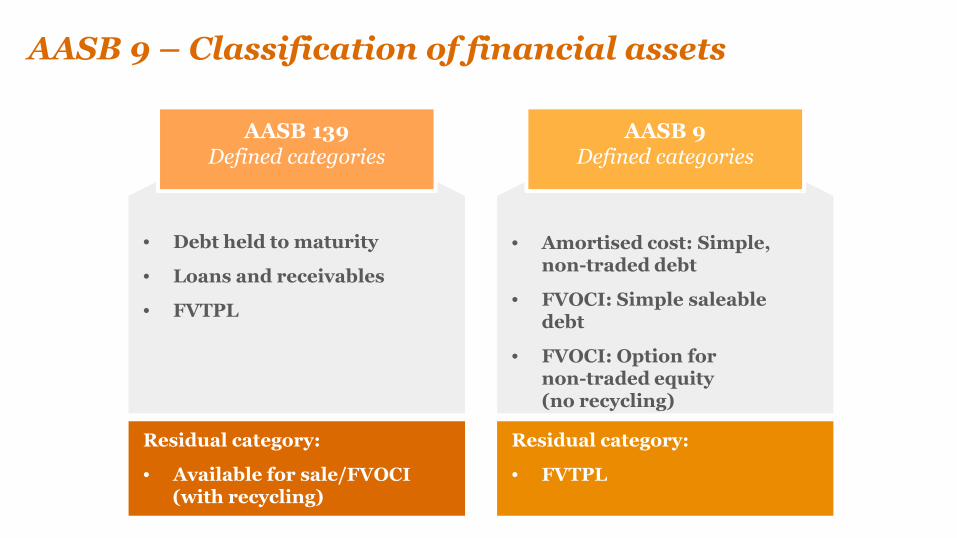

AASB 9 – Classification of financial assets

AASB 139Defined categories

• Debt held to maturity

• Loans and receivables

• FVTPL

AASB 9Defined categories

• Amortised cost: Simple,non-traded debt

• FVOCI: Simple saleabledebt

• FVOCI: Option fornon-traded equity(no recycling)

Residual category:

• FVTPL

Residual category:

• Available for sale/FVOCI(with recycling)

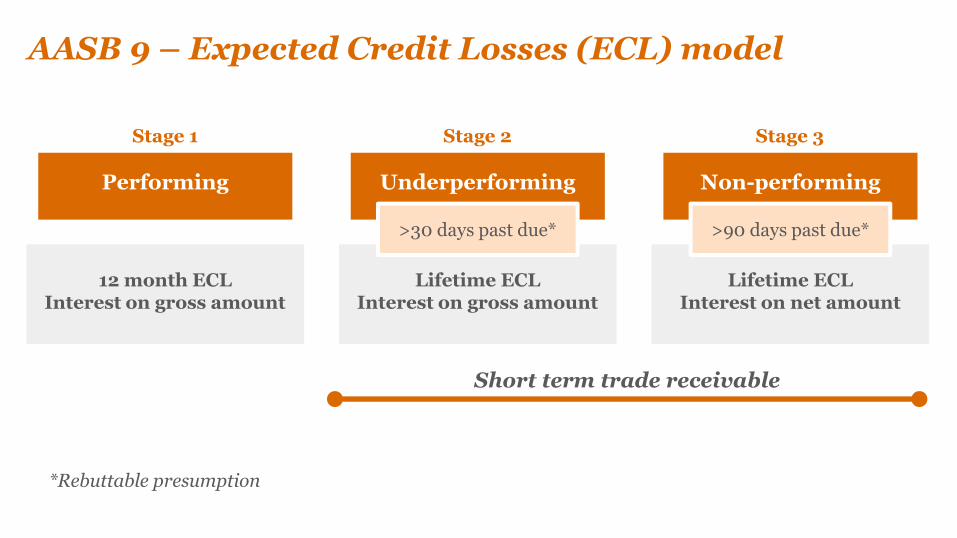

AASB 9 – Expected Credit Losses (ECL) model

Performing

12 month ECLInterest on gross amount

Underperforming

Lifetime ECLInterest on gross amount

>30 days past due*

Non-performing

Lifetime ECLInterest on net amount

>90 days past due*

Stage 1 Stage 2 Stage 3

Short term trade receivable

*Rebuttable presumption

AASB 9 – Hedging

The good news…

• Effectiveness is simpler to prove

• Hedge accounting reflects risk management objectives:

A net exposure can be hedged (net of USD purchases /sales)

More items are eligible for hedge accounting such as:

- Components of non-financial items

- Aggregated items

• Change in the way time value, forward points and currency basis arerecognised will reduce volatility in earnings

AASB 9 – Hedging

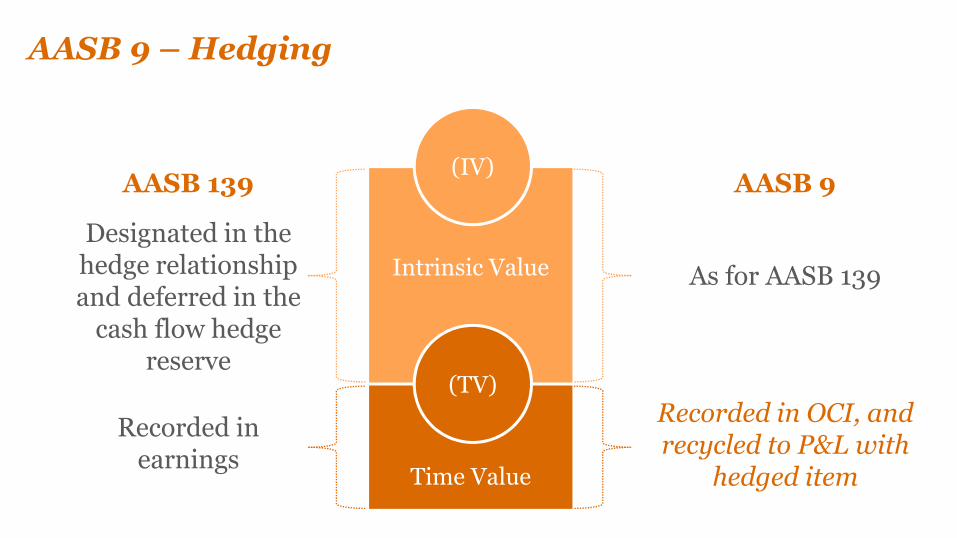

Intrinsic Value

Time Value

(IV)

(TV)

AASB 139 AASB 9

Recorded inearnings

Designated in thehedge relationshipand deferred in the

cash flow hedgereserve

Recorded in OCI, andrecycled to P&L with

hedged item

As for AASB 139

AASB 9 – Hedging

But be aware of...

• New requirement to discount forecast transactions

• Updated hedge documentation requirements

• Additional disclosure requirements – will mean incremental effort

Revenue

Topics

• What market activity are we seeing?

• Overview of the model

• What are the potential impacts?

• What will transition look like?

What marketactivity are weseeing? High impact

industries Deals space

New or renewed long-term contracts Audit Committees

Managementteams

ASICexpectations

Overview of the model – a new way of thinking

• More guidance on complex areas

• Effective date 1 January 2017

Step 1Identify thecontract

Step 2Separateperformanceobligations

Step 3Determinetransactionprice

Step 4Allocatetransactionprice

Step 5Recogniserevenue

What are the potential impacts?

• Separating obligations

• Variable consideration

• Licences of intellectual property (IP)

• Point in time versus over time

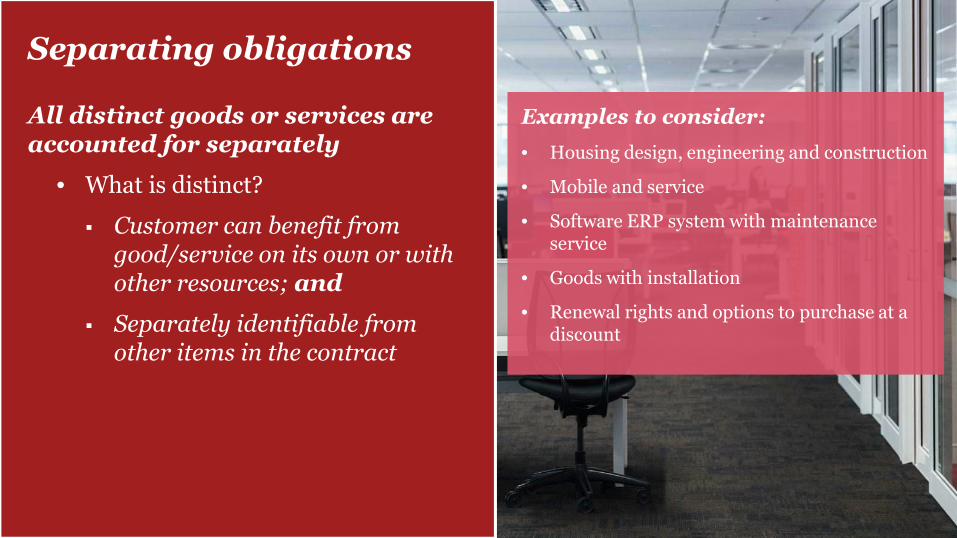

Separating obligations

All distinct goods or services areaccounted for separately

• What is distinct?

Customer can benefit fromgood/service on its own or withother resources; and

Separately identifiable fromother items in the contract

Examples to consider:

• Housing design, engineering and construction

• Mobile and service

• Software ERP system with maintenanceservice

• Goods with installation

• Renewal rights and options to purchase at adiscount

AASB 15 – required torecognise the minimum

amount which is nothighly probable of

significant risk of reversal

Currentaccounting

defers revenuethat varies

Currentaccountingestimates

considerationthat varies

Variable consideration

Examples

• Rebates and returns

• Royalties

• Performance fees

• Contract bonus / success fees

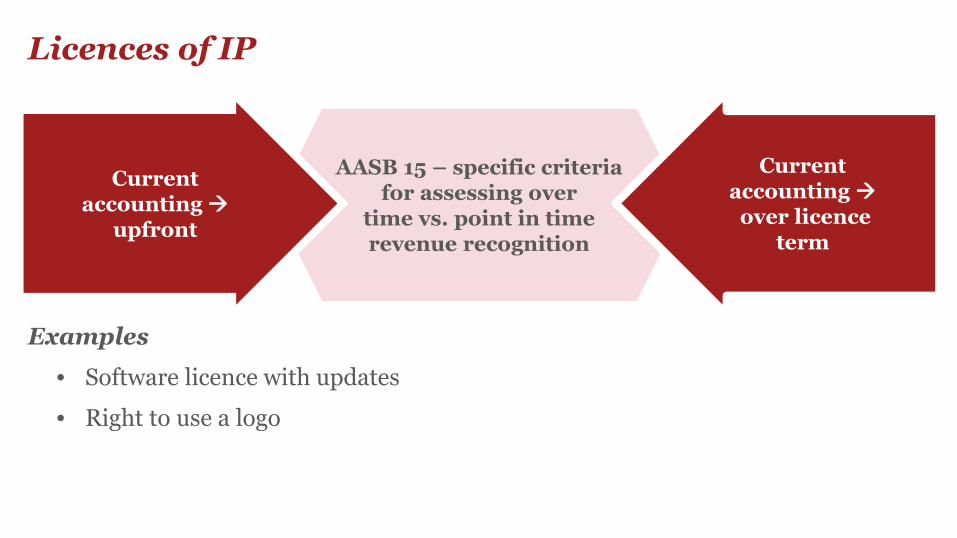

AASB 15 – specific criteriafor assessing over

time vs. point in timerevenue recognition

Currentaccounting

upfront

Currentaccounting

over licenceterm

Licences of IP

Examples

• Software licence with updates

• Right to use a logo

Point in time versus over time

Ov

er

tim

e Po

int

intim

eCustomer receives benefits as performed/

another would not need to re-performe.g. cleaning service, shipping

No

Yes

Yes

Yes

No

Create/enhance an asset customer controlse.g. house on customer land

Does not create asset w/alternative useAND right to payment for work to datee.g. customer specific manufacturing

No

Right to payment forasset

Legal title to asset

Customer hasaccepted the asset

Physical possessionof the asset

Customer hassignificant risks andrewards

Point in timeversus over time

If criteria not met, controltransfers at a point in timebased on followingindicators:

PwC

2016 2017

Effective date = 1 January 2017

NEWGAAP

NEWGAAP

Cumulative effect at 1 January 2016

Impact

• Double revenue or lostrevenue between 2015 and2016

It depends.

Option 1 –Full retrospective

OLD GAAPNEWGAAP

Cumulativeeffect at

1 January 2017

DiscloseOld GAAP

Option 2 –Prospective

• Double revenue or lostrevenue between 2016 and2017

What will transition look like?

Resources

A practical guide: 2014 Revenue from contracts with customers

In depth: Revenue standard is final – A comprehensive look at the newrevenue model (by industry)

Trends inreporting

Trends in reporting

• IASB disclosure project

• Streamlined financial reports

• Remuneration reports

• ASX corporate governance guidelines

• Special purpose financial reports

• Audit reports

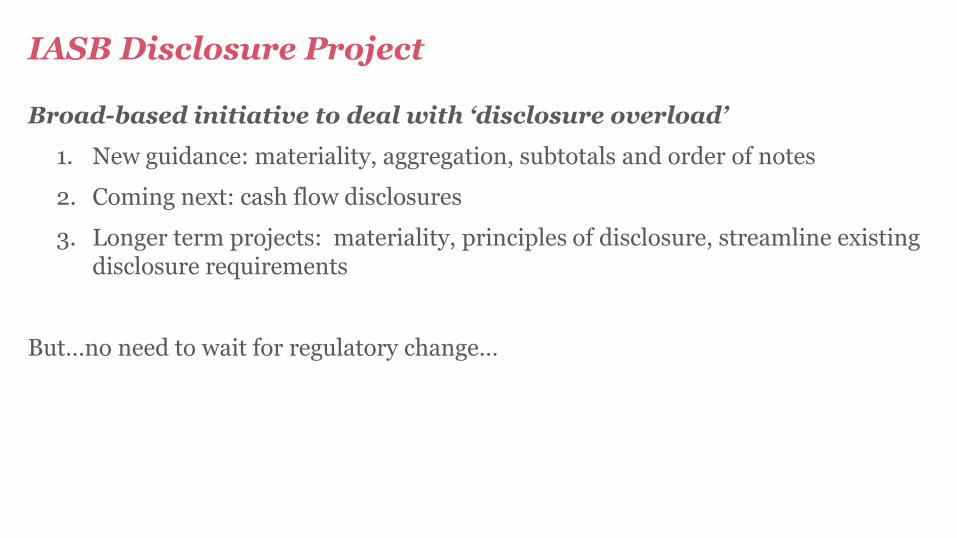

Broad-based initiative to deal with ‘disclosure overload’

1. New guidance: materiality, aggregation, subtotals and order of notes

2. Coming next: cash flow disclosures

3. Longer term projects: materiality, principles of disclosure, streamline existingdisclosure requirements

But…no need to wait for regulatory change…

IASB Disclosure Project

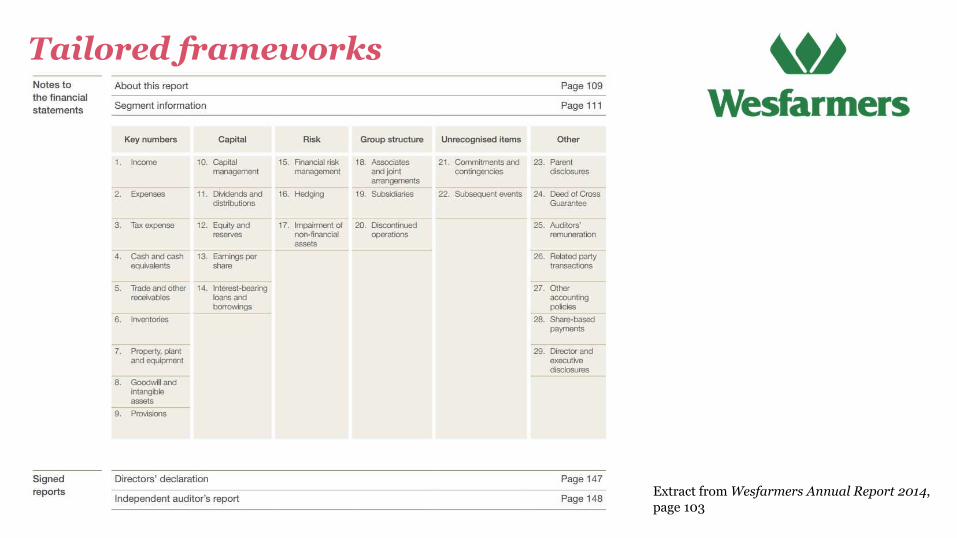

Streamlined financial reports

45%

Streamlining the Wesfarmers financial report reducedthe volume of the report by:

Our work with Wesfarmers

Tailored frameworks

Extract from Wesfarmers Annual Report 2014,page 103

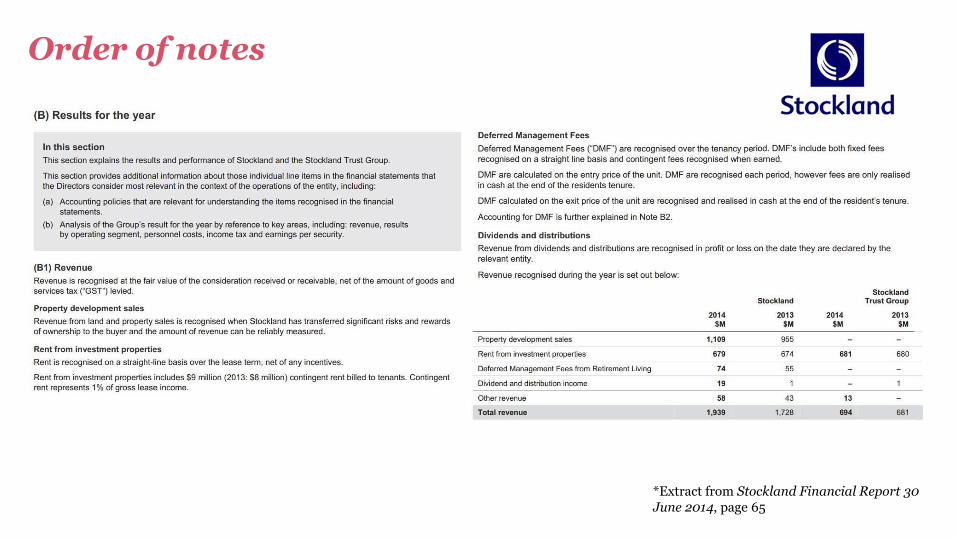

Order of notes

*Extract from Stockland Financial Report 30June 2014, page 65

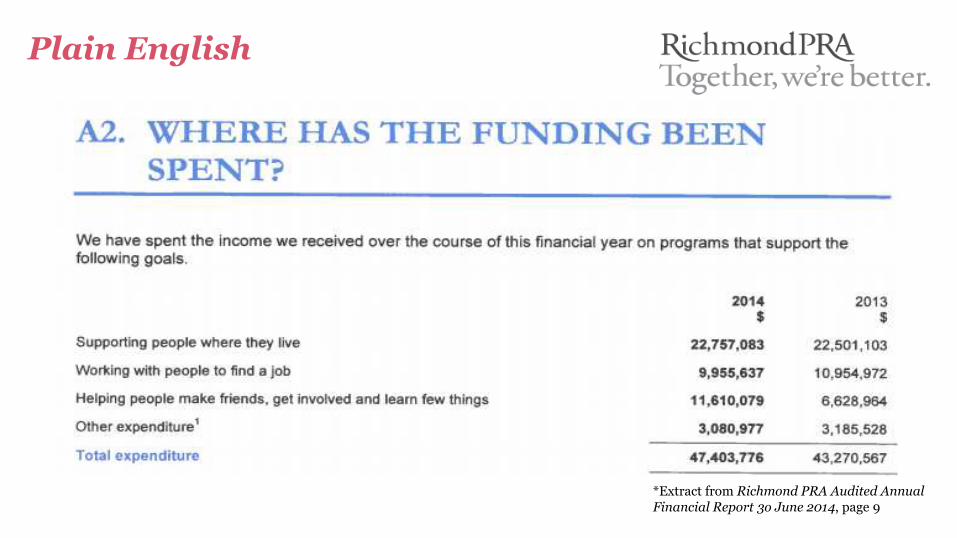

Plain English

*Extract from Richmond PRA Audited AnnualFinancial Report 3o June 2014, page 9

Removed

• PPE movements where no actual movements occurred during the year

• Defined benefit plan disclosures where plans are no longer material

• Accounting policies that don’t apply to the entity

Moved

• Trivial balances moved into other assets and other liabilities

Immaterial or trivial disclosures

Visual design & digital functionality

Extract from Transpacific Annual Report 2014,page 67

Next step to streamlining: remuneration reports

14%of annual

report

21pages

Average:

39pages

Longest:

98

Largest no. offootnotes:

20tables

30glossary

terms

It is not unusual for the statutoryremuneration reports…to belargely impenetrable to the layreader

(Chartered Secretaries Australia)

* Based on disclosures for the 35 largest ASX companies in 2013

What could you do today?

• Logical framework and order

• Plain English

• Visual design

Legislative changeneeded…but there could besome quick wins

ASX corporate governanceprinciples

• New 3rd edition applies for 30 June 2015

• Disclosures can now be provided online

• AASB report on reporting entity concept and special purpose financial reports

• Continuing discussion and debate

• Treasury may reconsider reporting thresholds in the future

• Entities considering IPOs may be reporting entities

Special purpose financial reports

New insightful audit reports

New audit report standards issued by IAASB

• Likely to be adopted in Australia for 2016

Significant changes:

• Insight – key audit matters

New insightful audit reports

Extract from Unilever Annual Report andAccounts 2013, page 88

New audit report standards issued by IAASB

• Likely to be adopted in Australia for 2016

Significant changes:

• Insight – key audit matters

• Transparency – auditor independence and name of partner

• Readability – restructuring content, moving boilerplate disclosures online

New insightful audit reports

The IAASB is moving to make audit reports moreinformative and insightful

What are you thinking ofdoing to enhance yourfinancial report this year?

Thank you for joining us

Financial Reporting UpdateMarch 2015

© 2015 PricewaterhouseCoopers. All rights reserved.PwC refers to the Australian member firm, and may sometimes refer to the PwC network.Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

![freedom at your fingertips one-click! at your fingertips · PDF fileat your fingertips freedom Sign up for online bill pay [Financial Institution Name] at your fingertips freedom Sign](https://img.pdfslide.us/doc/110x75/5a7122a07f8b9ac0538c9b67/freedom-at-your-fingertips-one-click-at-your-fingertips-nbsppdf-fileat.jpg)