Embed Size (px)

DESCRIPTION

• This household report is one of ten super category reports designed to show high-level comparison and analysis for retail markets across major countries in Europe.• This report contains data gathered from around Europe. This market was split into the following categories: air fresheners, dishwashing, household cleaners, shoe cleaners,cleaning supplies, insecticides, fabric detergents, fabric enhancers and paper disposables.• The report highlights key metrics such as total sales figures, market trends, categoryshares, winners and losers for Europe and for individual countries.• The data has been sourced from IRI retail databases and Eurostat, the statistical branch of administration for the European Commission.• The countries included in the report are: France, Germany, Italy, the Netherlands, Spain and the United Kingdom (U.K.).

Citation preview

PULSE REPORT

IRI Pulse Report Household

Welcome to the Pulse Q3 2013 edition for household. We hope you

find it useful. Please do not hesitate to contact us if you have any

questions or comments at [email protected].

Q3 2013

IRIworldwide.eu

PULSE REPORT

About the Report

2

• This household report is one of ten super category reports designed to show high-level

comparison and analysis for retail markets across major countries in Europe.

• This report contains data gathered from around Europe. This market was split into the

following categories: air fresheners, dishwashing, household cleaners, shoe cleaners,

cleaning supplies, insecticides, fabric detergents, fabric enhancers and paper disposables.

• The report highlights key metrics such as total sales figures, market trends, category

shares, winners and losers for Europe and for individual countries.

• The data has been sourced from IRI retail databases and Eurostat, the statistical branch of

administration for the European Commission.

• The countries included in the report are: France, Germany, Italy, the Netherlands, Spain

and the United Kingdom (U.K.).

• The market channels used for each country in this report are as follows:

Country Channels used

UK Hypermarkets, supermarkets, drug stores and impulse outlets

ESHypermarkets, supermarkets, hard discounters, and drug stores, including the Canary Islands

DE Hypermarkets, supermarkets, hard discounters and drug stores

NL Hypermarkets, supermarkets, hard discounters and drug stores

ITHypermarkets, supermarkets, small self service, hard discounters and drug stores

FR Hypermarkets and supermarkets

• For analytical purposes, the data sourced from available retail databases has been

consolidated to provide consistent results. However, for some countries it was not possible

to source data pertaining to certain categories. When this occurred, it has been documented

in the notes section found at the end of the report.

PULSE REPORT

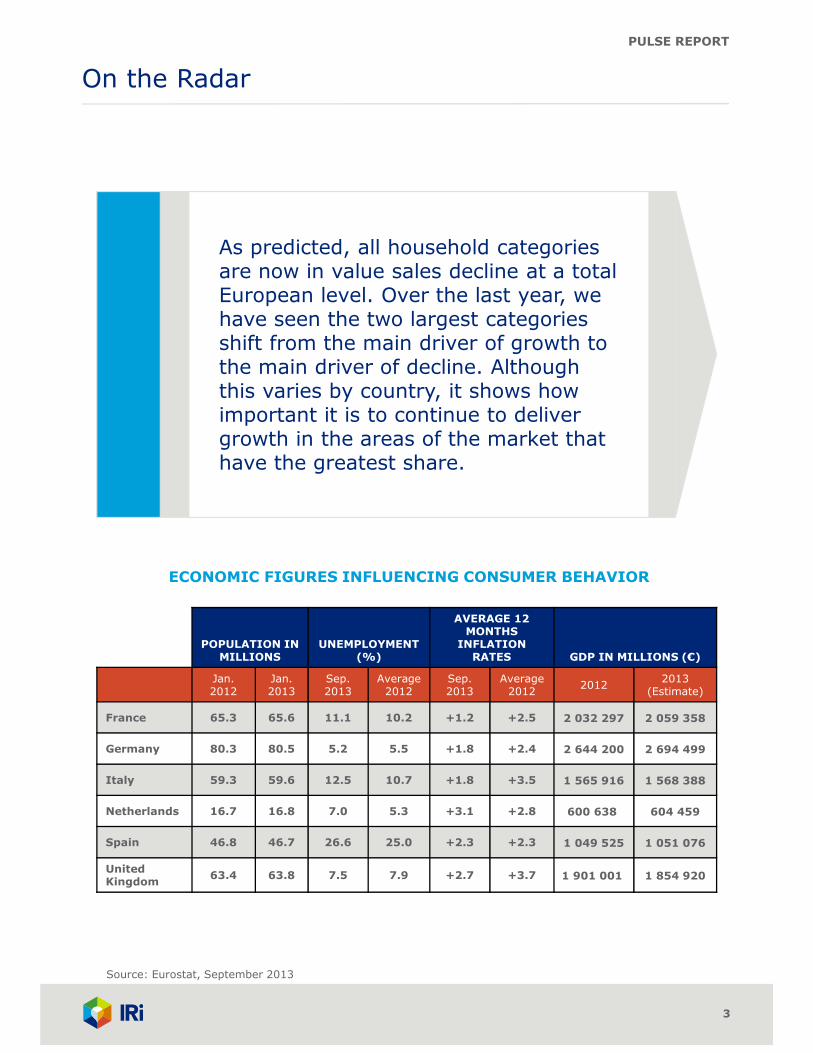

On the Radar

3

ECONOMIC FIGURES INFLUENCING CONSUMER BEHAVIOR

Source: Eurostat, September 2013

As predicted, all household categories are now in value sales decline at a total European level. Over the last year, we have seen the two largest categories shift from the main driver of growth to the main driver of decline. Although this varies by country, it shows how important it is to continue to deliver growth in the areas of the market that have the greatest share.

POPULATION IN MILLIONS

UNEMPLOYMENT (%)

AVERAGE 12 MONTHS

INFLATION RATES GDP IN MILLIONS (€)

Jan. 2012

Jan.2013

Sep. 2013

Average 2012

Sep. 2013

Average 2012

20122013

(Estimate)

France 65.3 65.6 11.1 10.2 +1.2 +2.5 2 032 297 2 059 358

Germany 80.3 80.5 5.2 5.5 +1.8 +2.4 2 644 200 2 694 499

Italy 59.3 59.6 12.5 10.7 +1.8 +3.5 1 565 916 1 568 388

Netherlands 16.7 16.8 7.0 5.3 +3.1 +2.8 600 638 604 459

Spain 46.8 46.7 26.6 25.0 +2.3 +2.3 1 049 525 1 051 076

United Kingdom

63.4 63.8 7.5 7.9 +2.7 +3.7 1 901 001 1 854 920

PULSE REPORT

1 230 1 250 1 232 1 245 1 209 1 224

1 008 1 037 966 951 995 1 020

274 274 261 271 264 265

1 483 1 5191 405 1 398 1 433 1 451

1 630 1 6571 636 1 668 1 611 1 660

1 385 1 4711 388 1 401 1 381

1 496

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

01-juil.-12 01-oct.-12 30-déc.-12 31-mars-13 30-juin-13 29-sept.-13

Mil

lio

ns

Period Ending

France

Germany

Italy

Netherlands

Spain

UK

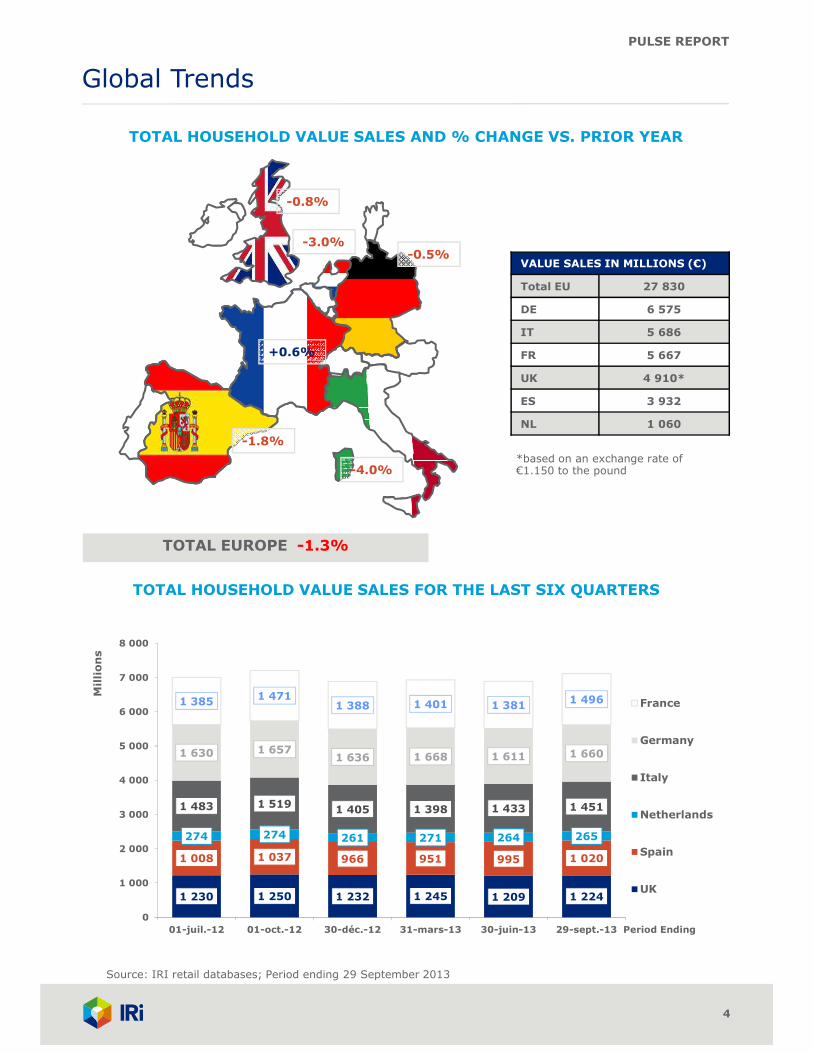

Global Trends

4

TOTAL EUROPE -1.3%

-4.0%

-0.5%

-0.8%

VALUE SALES IN MILLIONS (€)

Total EU 27 830

DE 6 575

IT 5 686

FR 5 667

UK 4 910*

ES 3 932

NL 1 060

TOTAL HOUSEHOLD VALUE SALES AND % CHANGE VS. PRIOR YEAR

*based on an exchange rate of €1.150 to the pound

-1.8%

+0.6%

-3.0%

TOTAL HOUSEHOLD VALUE SALES FOR THE LAST SIX QUARTERS

Source: IRI retail databases; Period ending 29 September 2013

PULSE REPORT

2 674

8 483

4 167

5 875

2 836

-1.6 -0.6 -1.3 -0.9 -0.7

Paper

Dis

posable

s

Fabri

c

Dete

rgents

Household

Cle

aners

Dis

hw

ash

Fabri

c

Enhancers

Mil

lio

ns

Total € Sales % € vs. YA

15.0%

9.6%

5.9%

30.5%

0.5%

1.8%

5.3%

21.1%

10.2%

Paper Disposables Fabric Detergents Household Cleaners

Dishwash Fabric Enhancers Air Fresheners

Cleaning Supplies Insecticides Shoe Cleaners

Europe

5

5 875

4 167

2 836

1 6531 478

514 150

8 483

2 674

Eu

ros,

in M

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

Europe includes: France, Germany, Italy, Netherlands, Spain and United Kingdom

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change vs. year ago

Source: IRI retail databases; Period ending 29 September 2013

KEY TRENDS

• France is now the only country in Europe

to grow household sales, although

Germany and the U.K. declined at a slower

rate than the European total. However, all

countries have grown versus the previous

quarter.

• Sales are down -1.3% versus the prior

year with none of the household categories

in growth at a total European level. Fabric

detergents was previously one of the main

growth areas, but this has had a dramatic

turnaround and is now the category with

the largest decline. This is followed by

paper disposables, again a category which

has historically driven the growth of the

household market.

• These two categories should act as a

warning to any category – within the space

of a few months, the largest area of

growth can become the largest area of

decline.

PULSE REPORT

Europe

6

CATEGORY INSIGHTS

• Fabric detergents is now the largest area of decline at a European level. Although France,

Germany and the U.K. have growth, there are significant declines in Italy and Spain which

have driven this trend. Powder, which is in significant decline in Spain and the U.K., seems to

drive this. Other formats are unable to achieve the levels of growth needed to offset this

decline.

• Paper disposables continues to decline as France and Spain are unable to cover for the losses

seen in the U.K. and Italy. The U.K. decline is driven by private label in the soft sector, whilst

Italy declines across all sectors except napkins and wipes.

• Household cleaners are in decline in all countries with the exception of Germany. The

majority of the decline is seen in Italy, where all sectors are now in decline.

• Air fresheners are in decline across every European country. Although this is not the top five

in terms of share of household, this wide decline brings it into the bottom 5 performing

categories.

Europe includes: France, Germany, Italy, Netherlands, Spain and the United Kingdom

Source: IRI retail databases; Period ending 29 September 2013

TOP LOSERS: VALUE SALES CHANGE VS. YR. AGO (€)

TOP WINNERS: VALUE SALES CHANGE VS. YR. AGO (€)

0 0 0 0 0 0 0

Millions

- 38,7

- 42,7

- 54,7

- 96,1

- 78,9

-120 -100 -80 -60 -40 -20 0

AirFresheners

CleaningSupplies

HouseholdCleaners

PaperDisposables

FabricDetergents

.

Millions

PULSE REPORT

542

1 492

813

1 280

607

0.6 2.2-0.8 1.5 1.5

Paper

Dis

posable

s

Fabri

c

Dete

rgents

Household

Cle

aners

Dis

hw

ash

Fabri

c

Enhancers

Mil

lio

ns

Total € Sales % € vs. YA

France

7

KEY TRENDS

• France is the only country in Europe to

register growth on household products,

growing 0.6% in value sales versus a

decline of 1.3% for Europe.

• But, France’s growth rate is slowing down

quarter by quarter.

• Also, FMCG as a whole is now far more

dynamic than household products , with

1.7% growth in Q3 2013.

• Household growth mainly comes from

“essential” categories, which include paper

disposables, fabric detergents and

dishwashing.

Eu

ros,

in M

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

Source: IRI retail databases; Period ending 29 September 2013

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change vs. year ago

14.3%

9.6%

7.8%

26.3%

0.6%

2.3%

5.8%

22.6%

10.7%

Paper Disposables Fabric Detergents Household Cleaners

Dishwash Fabric Enhancers Cleaning Supplies

Air Fresheners Insecticides Shoe Cleaners

1 280

813

607

441

329

130

34

1 492

542

PULSE REPORT

France

8

TOP LOSERS: VALUE SALES CHANGE VS. YR. AGO (€)

TOP WINNERS: VALUE SALES CHANGE VS. YR. AGO (€)

Source: IRI retail databases; Period ending 29 September 2013

Millions

CATEGORY INSIGHTS

• Fabric detergents, the second largest category on household products, is now only the fourth

contributor to growth. Value sales only grew by 0.6% versus around 5% in 2012. The strong

increase of the capsules segment is not sufficient to offset regression of all other product

forms.

The economic context now seems to be weighing on the category’s health. Moreover, during

the last two or three years, fabric was benefiting from liquid compaction, but it seems that

now consumers are using the correct dose.

• Paper disposables and dishwashing grew mainly through promotional sales increases.

• Household cleaners still suffer from the structural decline of categories such as floor care and

bleach.

22,7

13,2

7,8

7,8

0,9

0 5 10 15 20 25

PaperDisposables

Dishwash

FabricEnhancers

FabricDetergents

ShoeCleaners

- 1,7

- 3,1

- 6,4

- 4,9

-8 -6 -4 -2 0

Insecticides

AirFresheners

CleaningSupplies

HouseholdCleaners

.

Millions

PULSE REPORT

589

2 221

990

1 380

698

0.4 -0.7 0.6-0.7 0.1

Paper

Dis

posable

s

Fabri

c

Dete

rgents

Household

Cle

aners

Dis

hw

ash

Fabri

c

Enhancers

Mil

lio

ns

Total € Sales % € vs. YA

Germany

9

KEY TRENDS

• The household market experienced a slight

decline, driven by losses in the paper

disposable and air freshener categories.

• Although promotions contributed to more

than 21% of total sales, there has been a

dip in promotional sales growth which is a

reason for the category decline.

• Hypermarkets remain the major channel

with positive growth. The major sub-

channels are 1500-2499 square meter

(sqm) and 2500-4999 sqm with significant

growth.

• Although other drug stores contributed to

more than 50% of the sales of drug stores

and show an overall positive development,

they are unable to compensate for the

bankruptcy of Schlecker.

• Discounters have shown positive

development with growth from both hard

and soft discounters. Growth in household

cleaners and fabric detergent categories led

to the sales boost.

Eu

ros,

in M

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

TOP 5 CATEGORIES: EVOLUTIONValue sales (€) and % change vs. year ago

Source: IRI retail databases; Period ending 29 September 2013

15.1%

9.0%

5.6%

33.8%

0.4%

1.1%3.5%

21.0%

10.6%

Paper Disposables Fabric Detergents Household Cleaners

Dishwash Fabric Enhancers Air Fresheners

Cleaning Supplies Insecticides Shoe Cleaners

1 380

990

698

367 229

27

2 221

589

75

PULSE REPORT

Germany

10

CATEGORY INSIGHTS

• Household cleaners lead the category driven by value growth of toilet bowl cleaner/stones in

all channels except for drug stores. Major channels with positive development are

discounters and hypermarkets, together contributing to approximately 62% of market share

fueled by higher promotions. The overall volume decline of the category is majorly due to

losses in drug stores. Private label holds around 30% of share with a flat growth rate, but

faced losses in drug stores.

• Fabric detergents continue to grow, mainly driven by the value growth in all purpose

washing detergents. Hypermarket is the major channel with over 40% of market share,

showing a stable growth rate with a promotion sales boost. Hard discounters also play a

major role in pumping up sales growth and masking the losses from drug stores. Private

label holds around 22% of market share, but shows a slight decline, mainly driven by losses

in drug stores.

• Fabric enhancers show stable development driven by positive growth in the fabric softeners

category. Hypermarket is the major channel. Private label has an 18% share, but showed a

dip in sales with losses in both drug stores and hypermarkets.

• Due to heavy losses in the major categories toilet paper and paper napkins, paper

disposables showed a huge decline. Losses in drug stores pulled down the overall sales

growth. Hard discounters also declined, adding to the losses.

• Cleaning supplies also showed decline driven by losses in drugstores and discounters.

Although hypermarkets showed slight positive growth, they were unable to offset the losses.

Private label is the major manufacturer with approximately 64% of market share, but is also

declining.

TOP LOSERS: VALUE SALES CHANGE VS. YR. AGO (€)

TOP WINNERS: VALUE SALES CHANGE VS. YR. AGO (€)

Source: IRI retail databases; Period ending 29 September 2013

Millions

5.6

5.6

0.4

0 1 2 3 4 5 6

HouseholdCleaners

FabricDetergents

FabricEnhancers

- 2,4

- 5,0

- 9,9

- 16,0

- 10,5

-20 -15 -10 -5 0

Insecticides

Dishwash

AirFresheners

CleaningSupplies

PaperDisposables

.Millions

PULSE REPORT

556

1 609

9791 071

568

-5.3 -4.9 -3.3 -2.9 -2.7

Paper

Dis

posable

s

Fabri

c

Dete

rgents

Household

Cle

aners

Fabri

c

Enhancers

Dis

hw

ash

Mil

lio

ns

Total € Sales % € vs. YA

Italy

11

KEY TRENDS

• The Italian macro-economical scenario is

more and more in recession. Consumption

still decreased in value and in volume as

well, unemployment increased and the GDP

forecast for 2014 is weakly positive.

• Inflation is quite stable compared to

previous levels, but there will be higher

prices due to increasing taxes. Both retailers

and manufacturers are competing more and

more on a price and promotional basis.

• The general downturn is affecting both

private labels and branded products in every

segment of FMCG.

Eu

ros,

in M

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

Source: IRI retail databases; Period ending 29 September 2013

TOP 5 CATEGORIES: EVOLUTIONValue sales (€) and % change vs. year ago

17.2%

9.8%

8.2%

28.3%

0.7%3.1%

3.8%

18.8%

10.0%

Paper Disposables Fabric Detergents Household Cleaners

Fabric Enhancers Dishwash Cleaning Supplies

Air Fresheners Insecticides Shoe Cleaners

1 071 979

568 467

217 178

42

1 609

556

PULSE REPORT

Italy

12

CATEGORY INSIGHTS

• Compared to food and beverage, household categories are even more negative in volume

and value in the year 2012, but there was a weak recovery in the first 9 months of 2013.

Drug stores and discounters are still positive.

• Every important market for household cleaning was very negative and for the first time there

were no positive categories.

• Among the top 5 household categories, every one is deeply decreasing. Only dishwashing

had a decrease lower than 3.0%. Auto dish washing was not as negative as hand dish

washing.

• In fabric detergents, only machine washing decreased less than average in value and

increased in volume, thanks to high promotions in terms of price reduction and special

packaging with special offers.

• Paper disposable, the biggest market of household, is still negative and every segment is

strongly decreasing. Only napkins and wipes were positive in volume.

• Fabric enhancers were one of the top negative markets. Softeners, the biggest market of the

segment, decreased less, as there was heavy investment by top companies in terms of

assortment and promotions, while the second biggest market, laundry additives, decreased

over 7%.

• Among other households categories, only continuous air fresheners increased.

• Private labels confirmed their growth in every grocery market, even if the economic

downturn is affecting private label as well.

TOP LOSERS: VALUE SALES CHANGE VS. YR. AGO (€)

TOP WINNERS: VALUE SALES CHANGE VS. YR. AGO (€)

Source: IRI retail databases; Period ending 29 September 2013

Millions

0 0 0 0 0 0 0

- 21,0

- 29,5

- 33,2

- 59,4

- 47,5

-80 -60 -40 -20 0

CleaningSupplies

FabricEnhancers

HouseholdCleaners

PaperDisposables

FabricDetergents

.Millions

PULSE REPORT

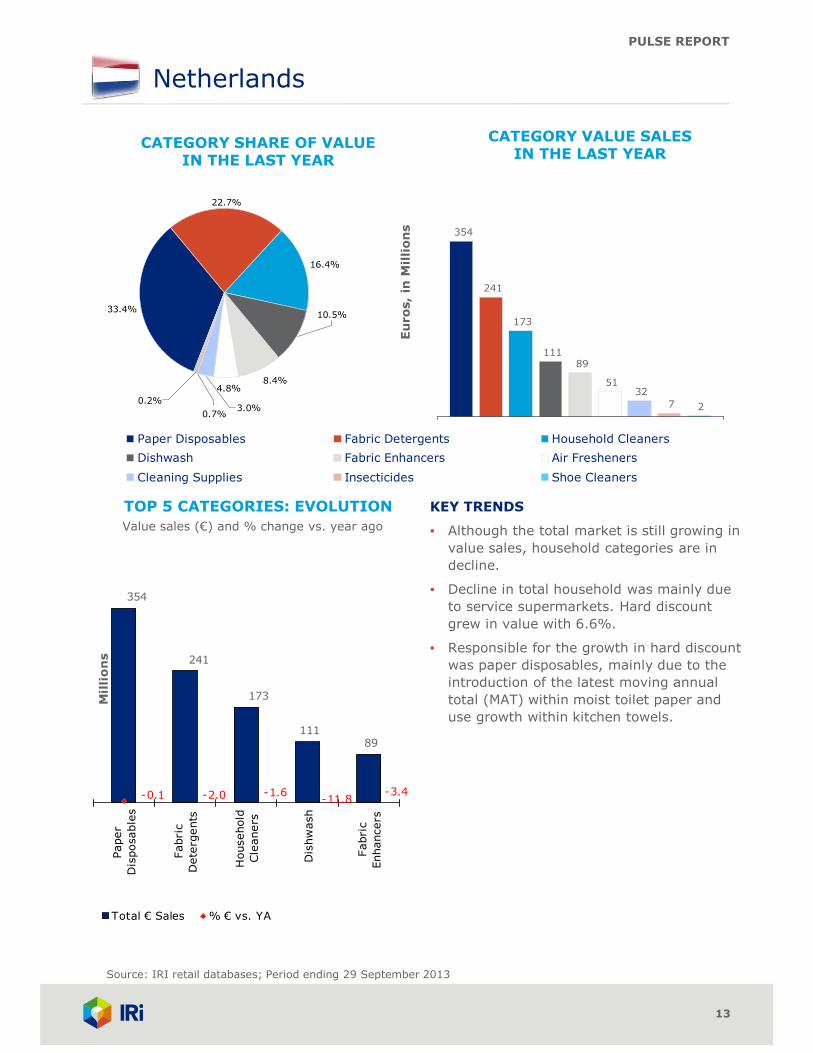

Netherlands

13

Eu

ros,

in M

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change vs. year ago

Source: IRI retail databases; Period ending 29 September 2013

16.4%

8.4%4.8%

33.4%

0.2%

0.7%3.0%

22.7%

10.5%

Paper Disposables Fabric Detergents Household Cleaners

Dishwash Fabric Enhancers Air Fresheners

Cleaning Supplies Insecticides Shoe Cleaners

241

173

111

51 32

7 2

354

89

89

354

173

241

111

-2.0 -11.8 -1.6 -0.1 -3.4

Paper

Dis

posable

s

Fabri

c

Dete

rgents

Household

Cle

aners

Dis

hw

ash

Fabri

c

Enhancers

Mil

lio

ns

Total € Sales % € vs. YA

KEY TRENDS

• Although the total market is still growing in

value sales, household categories are in

decline.

• Decline in total household was mainly due

to service supermarkets. Hard discount

grew in value with 6.6%.

• Responsible for the growth in hard discount

was paper disposables, mainly due to the

introduction of the latest moving annual

total (MAT) within moist toilet paper and

use growth within kitchen towels.

PULSE REPORT

Netherlands

14

TOP LOSERS: VALUE SALES CHANGE VS. YR. AGO (€)

TOP WINNERS: VALUE SALES CHANGE VS. YR. AGO (€)

Source: IRI retail databases; Period ending 29 September 2013

Millions

0 0 0 0 0 0 0

- 2,9

- 3,1

- 3,5

- 14,9

- 5,0

-20 -15 -10 -5 0

HouseholdCleaners

FabricEnhancers

AirFresheners

FabricDetergents

Dishwash

.

Millions

CATEGORY INSIGHTS

• Paper disposables had slight growth in Euro sales within both drug stores and hard discount.

Service supermarkets are trying to get share back with a high promotional pressure. Until

now, this has not been successful. Service supermarkets were the only group in decline. Only

volume growth for paper disposables for hard discount, mainly due to the introduction of the

latest MAT within moist toilet paper and moist tissues.

• Total detergents are under pressure, but showed a high increase within drug stores both in

value and volume. Promotional sales are driving the positive drug stores’ sales. The growth in

drug stores has had a negative impact on the sales in supermarkets.

• Dishwashing products declined in growth again. After a long period of high promotional sales,

promotional pressure is declining within both drug stores and supermarkets. Also, hard

discount gained territory from supermarkets and drug stores.

• Air freshener volume declined within supermarkets, drug stores and hard discount. Although

hard discount showed an increase in value, this is by far not enough for total market growth.

PULSE REPORT

355

1 189

594

785

374

-5.5 -1.2 -2.3 0.9 0.3

Paper

Dis

posable

s

Fabri

c

Dete

rgents

Household

Cle

aners

Fabri

c

Enhancers

Dis

hw

ash

Mil

lio

ns

Total € Sales % € vs. YA

Spain

15

KEY TRENDS

• The FMCG market had a positive trend in

2013 with 0.5% growth, but demand was

still negative. Only fresh products had a

flat demand. The rest of the sectors,

including food, beverages, household,

perfumeries and baby, declined, with

household declining at the fastest rate.

• Even though the household sector is falling

in demand and value in total this year,

there are still channels where the trend is

positive. Not only big supermarkets, but

small supermarkets saw a flat trend.

Proximity stores are over performing.

• In an unusual trend, private label

performed worse than the household

market and only grew in medium

supermarkets. Manufacturer brands are

decreasing too, but less so than private

label.

Eu

ros,

in M

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change vs. year ago

Source: IRI retail databases; Period ending 29 September 2013

15.1%

9.0%

6.6%

30.2%

0.4%

2.6%

6.6%

20.0%

9.5%

Paper Disposables Fabric Detergents Household Cleaners

Fabric Enhancers Dishwash Cleaning Supplies

Air Fresheners Insecticides Shoe Cleaners

785

594

374

258 258

102

16

1 189

355

PULSE REPORT

Spain

16

CATEGORY INSIGHTS

• All segments are growing in paper disposable. However, the tendency in volume is negative,

so the price increase would explain the value growth. In the toilet paper sector, the growth of

big packs is driving up the category.

• Dishwashing is growing because of hand dishwashing products. Within this sector, the

concentrated products are growing ahead of the category, particularly for private label in big

supermarkets.

• Powder decreased in the detergent category and hand detergents and delicate detergents

pulled down the category as well. Also, promotional levels have decreased slightly.

• Air fresheners are decreasing due to lost sales in all of the segments, except automatic air

fresheners. This is one of the most injured categories in household. Even private label is

decreasing and only the new launches in automatic air fresheners contributed to growth.

• Household cleaners decreased in specific cleaners and private label. Manufacturer brands

decreased, but less. No segment saw a positive trend, only a few small segments remained

flat.

TOP LOSERS: VALUE SALES CHANGE VS. YR. AGO (€)

TOP WINNERS: VALUE SALES CHANGE VS. YR. AGO (€)

Source: IRI retail databases; Period ending 29 September 2013

Millions

10,4

1,1

0 2 4 6 8 10 12

PaperDisposables

Dishwash

- 4,7

- 5,0

- 8,2

- 46,1

- 14,0

-50 -40 -30 -20 -10 0

FabricEnhancers

CleaningSupplies

AirFresheners

HouseholdCleaners

FabricDetergents

.Millions

PULSE REPORT

508

1 619

618

1 118

513

0.11.9-0.6 -2.9 0.6

Paper

Dis

posable

s

Fabri

c

Dete

rgents

Household

Cle

aners

Fabri

c

Enhancers

Dis

hw

ash

Mil

lio

ns

Total € Sales % € vs. YA

United Kingdom

17

KEY TRENDS

• The U.K. is ahead of the European market

growth rate, but in decline (-0.8% versus

-1.3%) with the sales growth rate falling

behind Germany as well as France. Value

sales were up versus last quarter.

• Paper disposables drove the decline whilst

household cleaners and air fresheners are

now in decline. Of the five largest

categories, fabric enhancers grew at the

fastest rate and delivered the most

absolute growth.

• We have started to see more new product

development in household categories this

quarter, which may enable some

categories to remain in growth. Many of

these come at a premium, so it will be

interesting to see how volume performs

over the next quarter.

Eu

ros,

in M

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change vs. year ago

Source: IRI retail databases; Period ending 29 September 2013

12.6%

10.3%

8.8%

33.0%

0.4%

0.6% 1.0%

22.8%

10.4%

Paper Disposables Fabric Detergents Household Cleaners

Fabric Enhancers Dishwash Air Fresheners

Cleaning Supplies Shoe Cleaners Insecticides

1 118

618 513

432

51 31 20

1 619

508

PULSE REPORT

United Kingdom

18

CATEGORY INSIGHTS

• Fabric enhancers drove growth this quarter more than the other categories combined.

Concentrated conditioners are the largest part of the market and the source of growth with

Unilever and P&G driving this at the expense of private label.

• Dishwashing product growth was driven by the machine sector, with hand now in decline

after a long period of growth. Machine growth came from private label, which was also the

area of decline for the hand sector. Overall, category growth came from more effective

promotions and at higher promoted prices.

• Fabric detergents are still positive, but no longer driving household growth. Main wash is

now in decline, driven by P&G powder, but there was some growth in liquid formats following

new product development. Growth came from the wash treatment sector, where, again,

powder was the source of decline whilst capsules grew.

• Household cleaners are now in decline after a lengthy period of growth. This was driven by

toilet rim blocks across most manufacturers, whilst bleach has seen value growth from price

increases.

• Paper disposables are now in heavy decline and are the key reason for the overall household

decline in the U.K. This is driven by price declines in the soft sector, as this has not driven

sufficient volume to cover for the loss in value. The soft sector decline is driven by private

label and Kimberly Clark.

Source: IRI retail databases; Period ending 29 September 2013

TOP LOSERS: VALUE SALES CHANGE VS. YR. AGO (€)

TOP WINNERS: VALUE SALES CHANGE VS. YR. AGO (€)

Millions

9,8

3,3

1,2

1,2

0,1

0 2 4 6 8 10 12

FabricEnhancers

Dishwash

CleaningSupplies

FabricDetergents

Insecticides

- 3.3

- 0.1

- 48.0

- 3.7

-60 -50 -40 -30 -20 -10 0

Shoe Cleaners

AirFresheners

HouseholdCleaners

PaperDisposables

.Millions

PULSE REPORT

Final Notes

19

Notes on Category Definitions for Countries

Due to the diverse products found in individual countries across this market, it was necessary

to consolidate the available data into the categories in this report. In some cases, it wasn’t

always possible to align products across all 6 countries, hence the need to highlight any

anomalies in the report. Those exceptions are listed below:

Shoe cleaners

• The Germany and France data in this report includes leather cleaning products.

Tools

• The U.K. data in this report only contains rubber gloves for this category.

• The Germany data in this report does not include mops, brushes or rubber gloves.

Fabric enhancers

• The U.K. data in this report does not include stain remover or fabric bleach products.

• The Italy data in this report does not include tumble dry enhancers.

• The Spain data in this report does not include anti-lime scale for laundry, tumble dry

enhancer or fabric storage products.

Paper disposables

• The France data in this report does not include wet wipes.

• The U.K. data in this report does not include paper napkins.

PULSE REPORT

Resources

20

About IRI. IRI is a leader in delivering powerful market and shopper information, predictive analysis and the foresight

that leads to action. We go beyond the data to ignite extraordinary growth for our clients in the CPG, retail and over-

the-counter healthcare industries by pinpointing what matters and illuminating how it can impact their businesses

across sales and marketing. Move your business forward at IRIworldwide.eu

Arlington Square, Downshire Way, Bracknell, Berkshire RG12 1WA, Tel +44 (0) 1344 746000

Copyright © 2013 Information Resources, Inc. (IRI). All rights reserved. IRI, the IRI logo and the names of IRI products and services

referenced herein are either trademarks or registered trademarks of IRI. All other trademarks are the property of their respective owners.

FOR MORE INFORMATION

Please contact Sam Cialis, Senior Insight Manager,

IRI at [email protected] or

+44 1344 747910 with questions or comments about this report.

To gain insight into opportunities across specific categories, segments, channels or retailers,

contact your IRI client service representative regarding custom analyses leveraging the

following resources:

• IRI InfoScan Census® is a syndicated retail tracking service that enables manufacturers

and retailers to acquire industry insights used to make better business decisions. IRI

InfoScan Census utilizes the data that IRI collects from grocery, drug, and mass

merchandise retailers to provide the most comprehensive and accurate syndicated data

offering in the FMCG sector. With access to accurate, granular detail by category, geography,

measure, and time period, clients have the tools needed to develop marketing and sales

strategies based on product performance, distribution, and promotion responsiveness. All

data about household comes from IRI InfoScan Census®.

• IRI Consulting provides strategic insights and advice, leveraging a variety of data sources,

predictive analytics, enabling technologies, and business analyses to help FMCG

manufacturers and retailers address significant sales and marketing issues effectively.