Embed Size (px)

Citation preview

CBRE RESEARCH

PUGET SOUND

FLEXIBLE OFFICE SPACE GUIDE

2 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

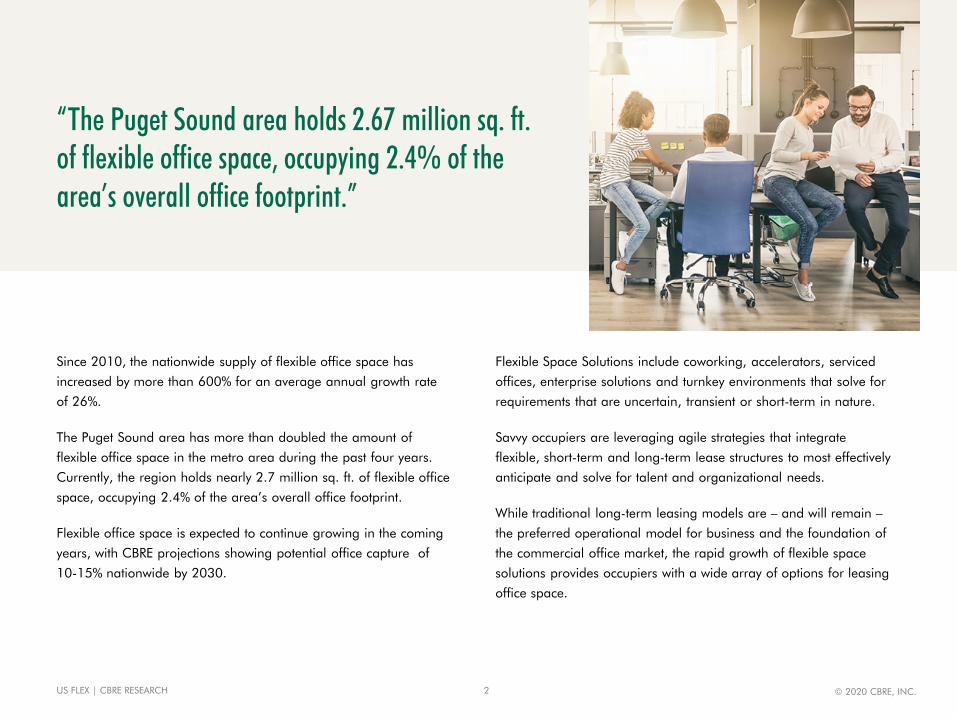

Since 2010, the nationwide supply of flexible office space has

increased by more than 600% for an average annual growth rate

of 26%.

The Puget Sound area has more than doubled the amount of

flexible office space in the metro area during the past four years.

Currently, the region holds nearly 2.7 million sq. ft. of flexible office

space, occupying 2.4% of the area’s overall office footprint.

Flexible office space is expected to continue growing in the coming

years, with CBRE projections showing potential office capture of

10-15% nationwide by 2030.

Flexible Space Solutions include coworking, accelerators, serviced

offices, enterprise solutions and turnkey environments that solve for

requirements that are uncertain, transient or short-term in nature.

Savvy occupiers are leveraging agile strategies that integrate

flexible, short-term and long-term lease structures to most effectively

anticipate and solve for talent and organizational needs.

While traditional long-term leasing models are – and will remain –

the preferred operational model for business and the foundation of

the commercial office market, the rapid growth of flexible space

solutions provides occupiers with a wide array of options for leasing

office space.

“The Puget Sound area holds 2.67 million sq. ft. of flexible office space, occupying 2.4% of the area’s overall office footprint.”

3 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

0.43

0.720.89 0.98

1.20

1.92

2.67

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2013 2014 2015 2016 2017 2018 2019

Milli

ons (

Sq. F

t.)

Flexible office occupancy in the Puget Sound has increased in velocity

dramatically in the last few years, with the amount of space more than

tripling between 2015 and 2019, to 2.67 million sq. ft. Thirty-nine

different flexible office providers operate in the region, and come in a

wide variety, including both local and national, as well as niche providers

that focus on a specific industry or group of people.

Source: CBRE Research, Q1 2020.

FIGURE 1: SEATTLE METRO ANNUAL FLEXIBLE OFFICE OCCUPANCY

27Local

providers 12National or international

providers

6Providers with

a niche purpose 6

Accelerator/ Incubator1

Non-profit

4 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

0.0 0.4 0.8 1.2 1.6 2.0

Downtown

Eastside

Close-In

Tacoma

Southend

Northend

2019 2018

0.0 0.5 1.0 1.5 2.0

WeWork

Regus

Spaces

Industrious

Galvanize

Novel

Impact Hub

All Others

2019 2018

PROVIDER SHARE SUBMARKET SHARE

Downtown 39%

FLEXIBLE OFFICE SPACE AS %

OF CURRENT TOTAL OFPUGET SOUND OFFICE

MARKET

2.4%

FIGURE 2: PROVIDER AND SUBMARKET SHARE OF TOTAL PUGET SOUND FLEXIBLE OFFICE SPACE

12.9%FLEXIBLE OFFICE

SPACE AS %OF 2019 PUGET SOUND

NEW OFFICE LEASES

Sq. Ft. Leased (Millions)Sq. Ft. Leased (Millions)

+76%

0%

+265%

+22%

0%

+38%

+31%

+70%

+373%

+70%

0%

Source: CBRE Research, Q1 2020.

5 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

6 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

$25

$30

$35

$40

$45

$50

$55

$60

0100200300400500600700800

Avg.

Class

A As

king R

ent (

Dot)

Thou

sand

s Sq.

Ft. (

Bar)

Source: CBRE Research, Q1 2020.

67%27%

6%

Class A Class B Class C

Flexible space in the Puget Sound has clustered in

dense submarkets with premium office space as

operators have increasingly shifted towards large,

Class A buildings in downtown submarkets.

Class A buildings have accounted for 85% of new

flexible space leased since 2018, up from 57% in

2016.

Seattle CBD, Denny Regrade and Bellevue CBD

combine for almost 60% of the Puget Sound’s

flexible space inventory with 1.56 million sq. ft.

FIGURE 3: FLEXIBLE DISTRICT BREAKDOWN

FIGURE 4: FLEXIBLE OFFICE BY BUILDING CLASS

2.7 MSF

Source: CBRE Research, Q1 2020.

7 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

0.00.10.20.30.40.50.60.70.80.91.01.11.21.31.4

2013 2014 2015 2016 2017 2018 2019

Milli

ons (

Sq. F

t.)

Under 25% 25%-50% 50%-75% 75%-100%

0.00.10.20.30.40.50.60.70.80.91.0

2013 2014 2015 2016 2017 2018 2019

Milli

ons (

Sq. F

t.)

Under 25K Sq. Ft. 25K-50K Sq. Ft. 50K-75K Sq. Ft. 75K+ Sq. Ft.

FIGURE 5: FLEXIBLE OFFICE SPACE BY SIZE

National flexible space providers have been a major

force in the Puget Sound office market since 2015.

These companies have contributed to large-block

vacancy compression, accounting for 87% of flex leases

of 75,000 sq. ft. or larger.

Large-scale leases were non-existent in 2015 but have

flooded the market in recent years. Leases 75,000 sq. ft.

and larger now account for over 33% of the leased flex

space.

The appetite for large buildings in urban centers has

kept pace with the increase in block size. The

percentage of space leased on a building-to-building

bases has notably contracted, even as the average lease

size has grown almost 50% since 2016.

FIGURE 6: FLEXIBLE OFFICE SPACE SHARE OF BUILDING (Sq. Ft.)

Source: CBRE Research, Q1 2020.

8 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2013 2014 2015 2016 2017 2018 2019

Millio

n (S

q. Ft.

)

Enterprise Tenants All Other Tenants

Tech-savvy entrepreneurs and startups still buoy

demand for flexible space. Large corporations—also

known as enterprise tenants—have increased their

flexible space footprint in recent years.

Flex space occupied by enterprise tenants has grown

to nearly one quarter of total flex leases in the area.

The growth of these tenants will continue to be a

driver of Puget Sound flex trends going forward.

Enterprise tenants have a particularly sizeable

footprint in the Bellevue CBD and Denny Regrade,

representing over 50% of flex space occupancy in

each of those submarkets.

FIGURE 7: ENTERPRISE TENANT SHARE OF FLEXIBLE OFFICE SPACE

0 200,000 400,000 600,000 800,000 1,000,000

Under 25K Sq. Ft.

25K-50K Sq. Ft.

50K-75K Sq. Ft.

75K+ Sq. Ft.

Enterprise Tenants All Other Tenants

FIGURE 8: ENTERPRISE TENANT SHARE OF FLEXIBLE OFFICE SPACE BY SIZE RANGE OF LOCATION

Note: “Enterprise Tenants” defined as established users occupying over 100,000 sq. ft. of traditional office space in the Puget Sound Area.Source: CBRE Research, Q1 2020.

9 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

Hines Securities

Onni Group

Clarion Partners

Nuveen Real Estate

Beacon Capital Partners

Martin Selig Real Estate

The Blackstone Group

Kemper Development

Hudson Pacific Properties

Schnitzer West

Top-10 Flexible Space Building Owners

FIGURE 9: TOP BUILDING OWNERS WITH FLEXIBLE SPACE OCCUPANTS

Note: Owners listed in alphabetical order. Source: CBRE Research Q1 2020

“Over 50 different building owners lease to flexible space providers in the Puget Sound. No single owner is over-exposed, though the top 10 building owners with flexible space tenants account for 54% of all flexible office in Puget Sound”

10 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

Though CBRE projects flexible office to grow at a slower pace nationally, the fundamentals of the Puget Sound’s economic environment make a strong case for this sector’s continued viability.

Limited office supply and pent-up demand has tilted the market to be more landlord favorable. Vacancy is at 20-year low and asking rents continue to rise sparking competition for urban office space and leaving very little room in the direct lease market for the optionality that flexible space provides.

Venture capital investment in Puget Sound tech startups broke $1 billion dollars in 2019, more than double the level three years prior. These new, rapidly growing companies are key tenants for flexible office providers that can uniquely accommodate their changing needs.

Large enterprise tenants have begun to appreciate the shorter terms that flexible space providers offer in recent years. Whether this trend continues will likely depend on the ability of these providers to manage and amenitize office space in ways that continue to anticipate organizational needs and add value.

Despite WeWork’s command of the current market, the region continues to diversify. Seven new flexible space operators entered the market in 2019, with at least two more confirmed for 2020. New flexible office provider requirements have already topped 525,000 sq. ft. going into 2020.

“Though CBRE projects flexible office to grow at a slower pace nationally, the fundamentals of the Puget Sound’s economic environment make a strong case for this sector’s continued viability.”

11 © 2020 CBRE, INC.US FLEX | CBRE RESEARCH

John Miller

Senior Managing Director

Pacific Northwest Region

+1 206 292 6102

Nolan Watson

Senior Research Analyst

Pacific Northwest Region

+1 206 292 6121

Carolyn Davis

Research Manager

Seattle Area Research

+1 206 292 6098

Julie Whelan

Senior Director of Research

Head of Americas Occupier Thought Leadership

+1 617 912 5229

Anne Marie Fall

Sales Director

Seattle Area

+1 303 628 1743

Lexi Russell

Research Director

Mountain-Northwest Region

+1 415 772 0272

CONTACTS

To learn more about CBRE Research or to download our reports, visit cbre.com/research.

Additional U.S. research produced by CBRE Research can be found at www.cbre.us/research.

CBRE’S AGILE REAL ESTATE KNOWLEDGE HUB

A one-stop shop to help you better understand what agility—from coworking to flexible space to shared workplaces to optimized portfolios—means for real estate strategies and the opportunities to leverage new models and ideas.

Visit cbre.com/agile

Disclaimer: Information contained herein, including projections, has been obtained from sources believed to be reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to confirm independently its accuracy and completeness. This information is presented exclusively for use by CBRE clients and professionals and all rights to the material are reserved and cannot be reproduced without prior written permission of CBRE.