Embed Size (px)

Citation preview

Public Service Loan Public Service Loan ForgivenessForgiveness

NYSFAAA Region 2NYSFAAA Region 2

B.J RevillB.J RevillDirector of Financial AidDirector of Financial Aid

Univ. of RochesterUniv. of RochesterSchool of Medicine and DentistrySchool of Medicine and Dentistry

AgendaAgenda

In-Depth Look at Public Service Loan In-Depth Look at Public Service Loan Forgiveness (PSLF)Forgiveness (PSLF)

Review of Pay as You Earn (PAYE) & Review of Pay as You Earn (PAYE) & Income Based Repayment (IBR)Income Based Repayment (IBR)

How to use an Income Driven How to use an Income Driven Repayment plan in conjunction with Repayment plan in conjunction with PSLFPSLF

Considerations prior to entering Considerations prior to entering repaymentrepayment

Public ServicePublic ServiceLoan Forgiveness ProgramLoan Forgiveness Program

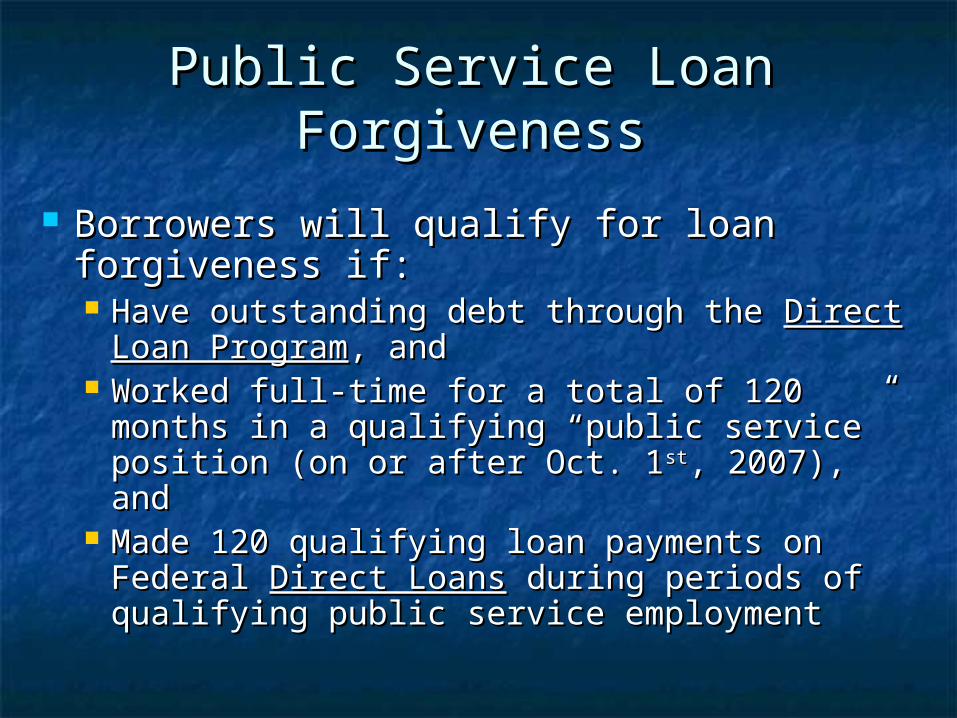

Public Service Loan Public Service Loan ForgivenessForgiveness

Borrowers will qualify for loan Borrowers will qualify for loan forgiveness if:forgiveness if: Have outstanding debt through the Have outstanding debt through the Direct Direct

Loan ProgramLoan Program, and, and Worked full-time for a total of 120 months Worked full-time for a total of 120 months

in a qualifying “public service” position (on in a qualifying “public service” position (on or after Oct. 1or after Oct. 1stst, 2007), and, 2007), and

Made 120 qualifying loan payments on Made 120 qualifying loan payments on Federal Federal Direct LoansDirect Loans during periods of during periods of qualifying public service employmentqualifying public service employment

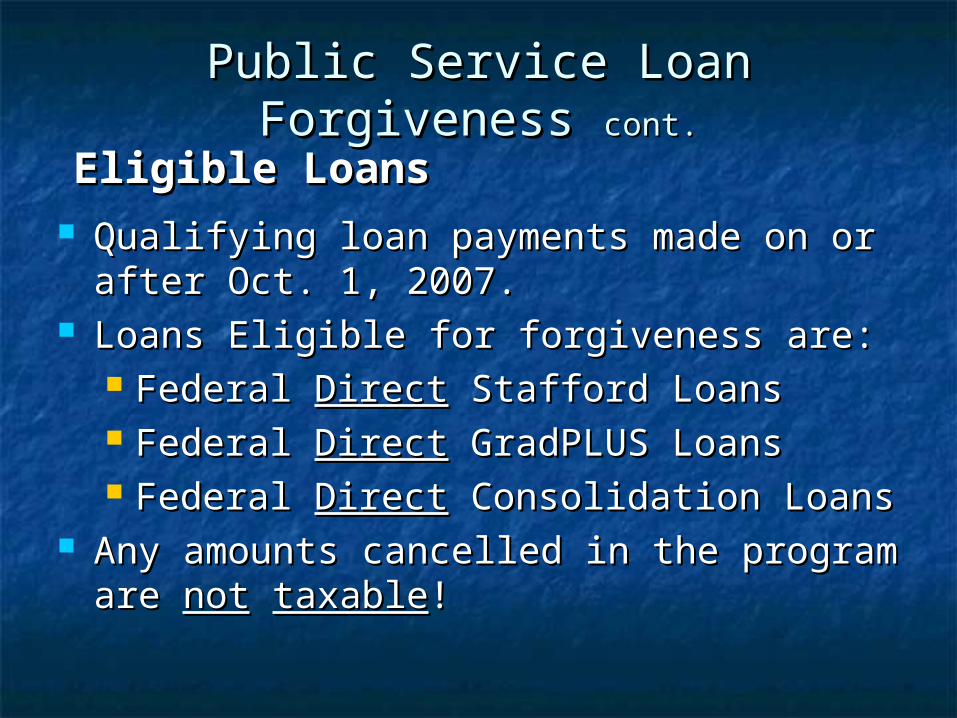

Public Service Loan Forgiveness Public Service Loan Forgiveness cont.cont.

Qualifying loan payments made on or after Qualifying loan payments made on or after Oct. 1, 2007.Oct. 1, 2007.

Loans Eligible for forgiveness are:Loans Eligible for forgiveness are: Federal Federal DirectDirect Stafford Loans Stafford Loans Federal Federal DirectDirect GradPLUS Loans GradPLUS Loans Federal Federal DirectDirect Consolidation Loans Consolidation Loans

Any amounts cancelled in the program are Any amounts cancelled in the program are notnot taxabletaxable!!

Eligible LoansEligible Loans

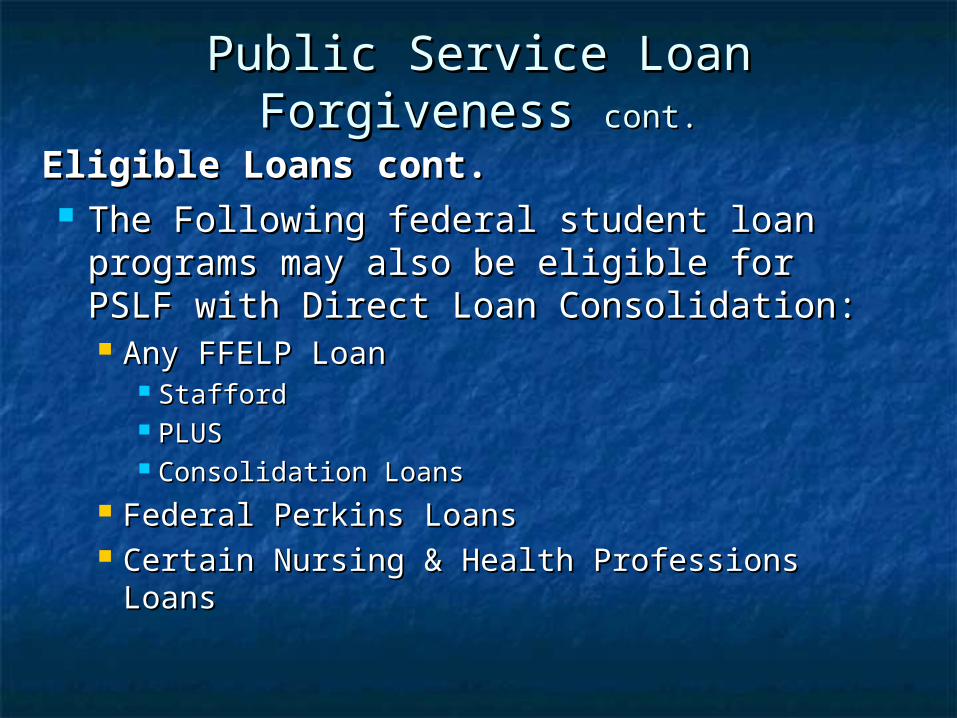

The Following federal student loan The Following federal student loan programs may also be eligible for PSLF programs may also be eligible for PSLF with Direct Loan Consolidation:with Direct Loan Consolidation: Any FFELP LoanAny FFELP Loan

StaffordStafford PLUSPLUS Consolidation LoansConsolidation Loans

Federal Perkins LoansFederal Perkins Loans Certain Nursing & Health Professions LoansCertain Nursing & Health Professions Loans

Public Service Loan Forgiveness Public Service Loan Forgiveness cont.cont.

Eligible Loans cont.Eligible Loans cont.

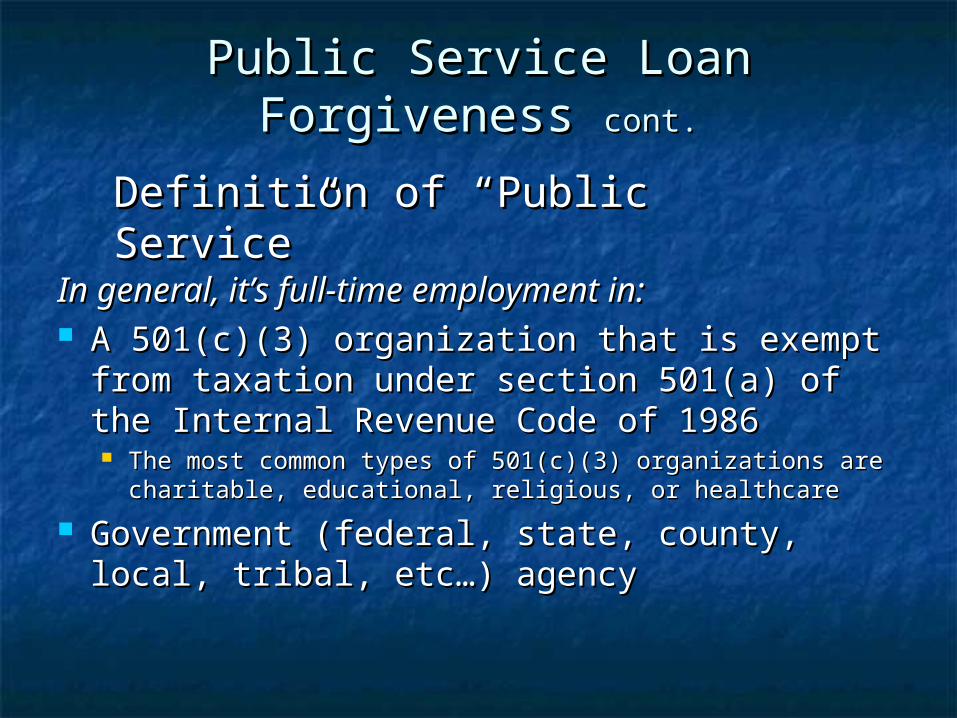

Public Service Loan Forgiveness Public Service Loan Forgiveness cont.cont.

In general, it’s full-time employment in:In general, it’s full-time employment in: A 501(c)(3) organization that is exempt A 501(c)(3) organization that is exempt

from taxation under section 501(a) of the from taxation under section 501(a) of the Internal Revenue Code of 1986Internal Revenue Code of 1986 The most common types of 501(c)(3) organizations are The most common types of 501(c)(3) organizations are

charitable, educational, religious, or healthcare charitable, educational, religious, or healthcare

Government (federal, state, county, local, Government (federal, state, county, local, tribal, etc…) agencytribal, etc…) agency

Definition of “Public Service”Definition of “Public Service”

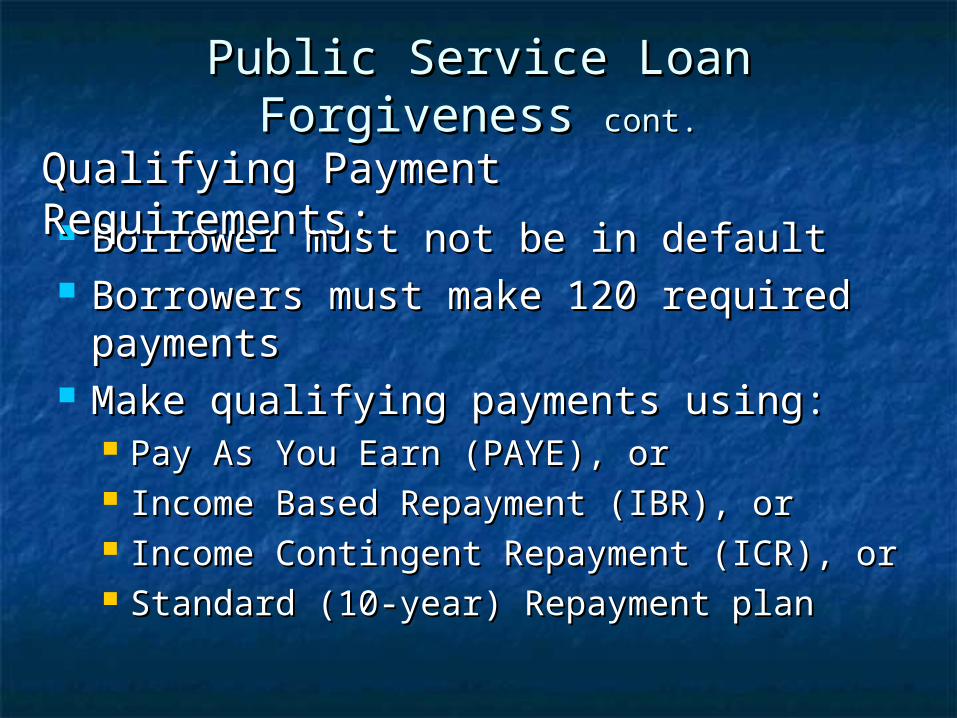

Public Service Loan Forgiveness Public Service Loan Forgiveness cont.cont.

Borrower must not be in defaultBorrower must not be in default Borrowers must make 120 required Borrowers must make 120 required

paymentspayments Make qualifying payments using:Make qualifying payments using:

Pay As You Earn (PAYE), orPay As You Earn (PAYE), or Income Based Repayment (IBR), orIncome Based Repayment (IBR), or Income Contingent Repayment (ICR), orIncome Contingent Repayment (ICR), or Standard (10-year) Repayment planStandard (10-year) Repayment plan

Qualifying Payment Requirements:Qualifying Payment Requirements:

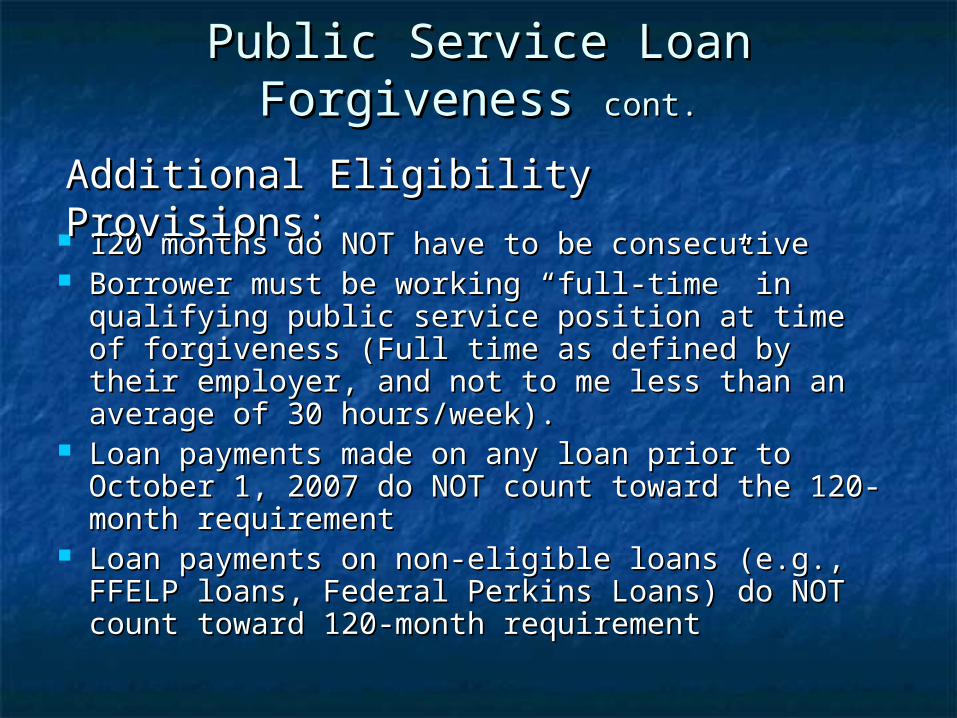

Public Service Loan Forgiveness Public Service Loan Forgiveness cont.cont.

120 months do NOT have to be consecutive120 months do NOT have to be consecutive Borrower must be working “full-time” in qualifying Borrower must be working “full-time” in qualifying

public service position at time of forgiveness (Full public service position at time of forgiveness (Full time as defined by their employer, and not to me time as defined by their employer, and not to me less than an average of 30 hours/week).less than an average of 30 hours/week).

Loan payments made on any loan prior to October Loan payments made on any loan prior to October 1, 2007 do NOT count toward the 120-month 1, 2007 do NOT count toward the 120-month requirementrequirement

Loan payments on non-eligible loans (e.g., FFELP Loan payments on non-eligible loans (e.g., FFELP loans, Federal Perkins Loans) do NOT count loans, Federal Perkins Loans) do NOT count toward 120-month requirementtoward 120-month requirement

Additional Eligibility Provisions:Additional Eligibility Provisions:

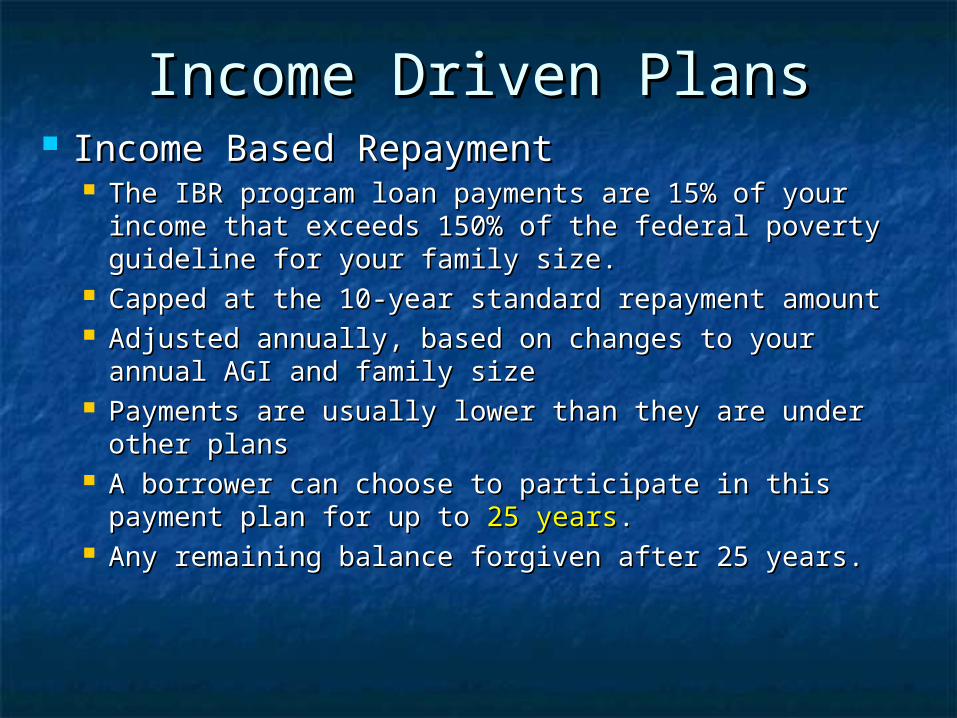

Income Driven PlansIncome Driven Plans Income Based RepaymentIncome Based Repayment

The IBR program loan payments are 15% of your The IBR program loan payments are 15% of your income that exceeds 150% of the federal poverty income that exceeds 150% of the federal poverty guideline for your family size. guideline for your family size.

Capped at the 10-year standard repayment amountCapped at the 10-year standard repayment amount Adjusted annually, based on changes to your annual Adjusted annually, based on changes to your annual

AGI and family sizeAGI and family size Payments are usually lower than they are under other Payments are usually lower than they are under other

plansplans A borrower can choose to participate in this payment A borrower can choose to participate in this payment

plan for up to plan for up to 25 years25 years.. Any remaining balance forgiven after 25 years.Any remaining balance forgiven after 25 years.

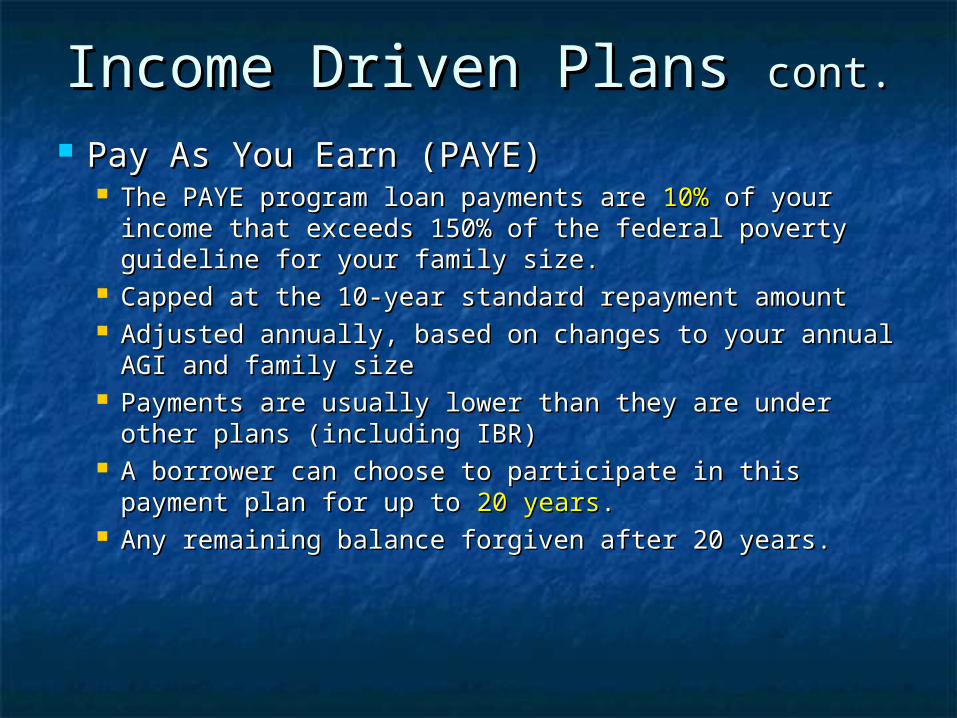

Income Driven Plans Income Driven Plans cont.cont.

Pay As You Earn (PAYE)Pay As You Earn (PAYE) The PAYE program loan payments are The PAYE program loan payments are 10% 10% of your of your

income that exceeds 150% of the federal poverty income that exceeds 150% of the federal poverty guideline for your family size. guideline for your family size.

Capped at the 10-year standard repayment amountCapped at the 10-year standard repayment amount Adjusted annually, based on changes to your annual AGI Adjusted annually, based on changes to your annual AGI

and family sizeand family size Payments are usually lower than they are under other Payments are usually lower than they are under other

plans (including IBR)plans (including IBR) A borrower can choose to participate in this payment A borrower can choose to participate in this payment

plan for up to plan for up to 20 years20 years.. Any remaining balance forgiven after 20 years.Any remaining balance forgiven after 20 years.

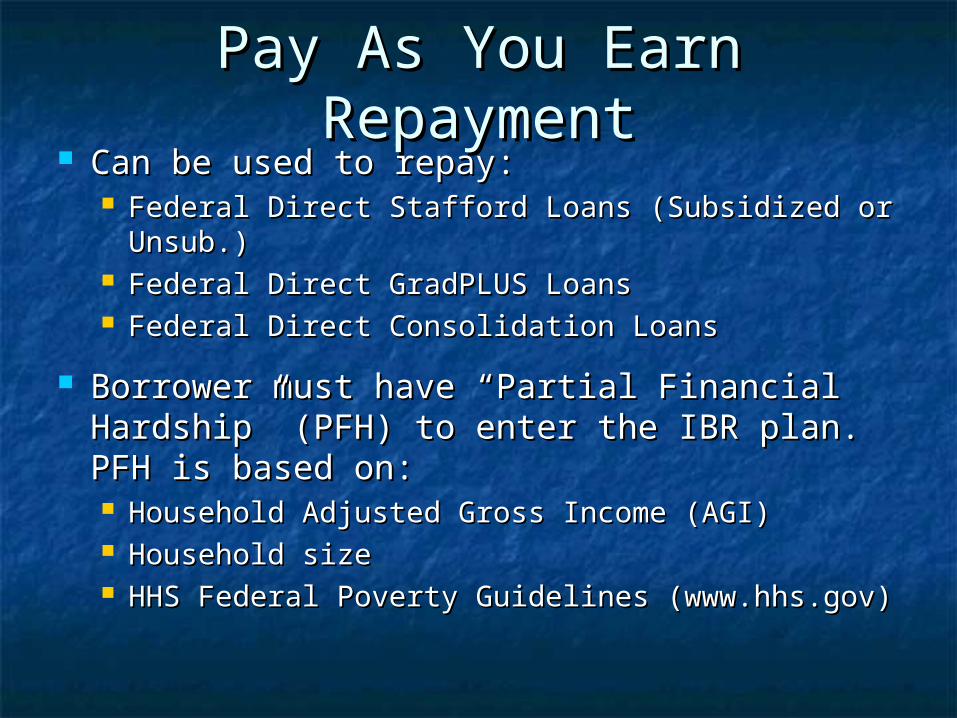

Pay As You Earn RepaymentPay As You Earn Repayment Can be used to repay:Can be used to repay:

Federal Direct Stafford Loans (Subsidized or Federal Direct Stafford Loans (Subsidized or Unsub.)Unsub.)

Federal Direct GradPLUS LoansFederal Direct GradPLUS Loans Federal Direct Consolidation Loans Federal Direct Consolidation Loans

Borrower must have “Partial Financial Borrower must have “Partial Financial Hardship” (PFH) to enter the IBR plan. PFH Hardship” (PFH) to enter the IBR plan. PFH is based on:is based on: Household Adjusted Gross Income (AGI)Household Adjusted Gross Income (AGI) Household sizeHousehold size HHS Federal Poverty Guidelines (www.hhs.gov)HHS Federal Poverty Guidelines (www.hhs.gov)

Pay As You Earn Repayment Pay As You Earn Repayment cont.cont.

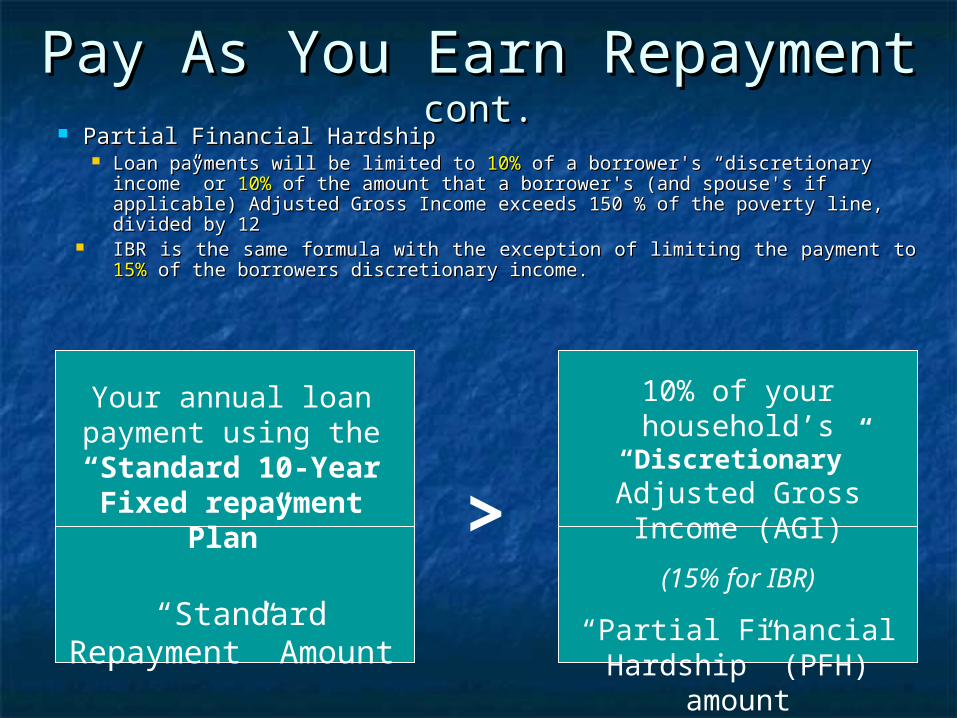

Partial Financial HardshipPartial Financial Hardship Loan payments will be limited to Loan payments will be limited to 10% 10% of a borrower's “discretionary of a borrower's “discretionary

income” or income” or 10% 10% of the amount that a borrower's (and spouse's if applicable) of the amount that a borrower's (and spouse's if applicable) Adjusted Gross Income exceeds 150 % of the poverty line, divided by 12 Adjusted Gross Income exceeds 150 % of the poverty line, divided by 12

IBR is the same formula with the exception of limiting the payment to IBR is the same formula with the exception of limiting the payment to 15% 15% of the borrowers discretionary income. of the borrowers discretionary income.

Your annual loan payment using the

“Standard 10-Year Fixed repayment

Plan”

“Standard Repayment” Amount

10% of your household’s

“Discretionary” Adjusted Gross Income

(AGI)

(15% for IBR)

“Partial Financial Hardship” (PFH)

amount

>

Pay As You Earn Repayment Pay As You Earn Repayment cont.cont.

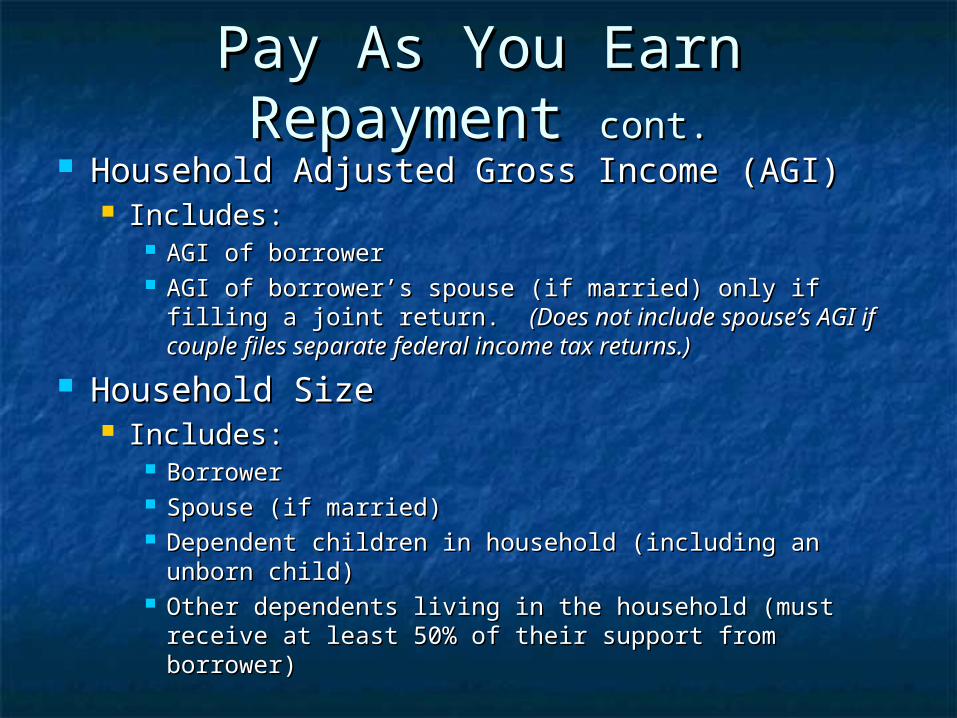

Household Adjusted Gross Income (AGI)Household Adjusted Gross Income (AGI) Includes:Includes:

AGI of borrowerAGI of borrower AGI of borrower’s spouse (if married) only if filling a AGI of borrower’s spouse (if married) only if filling a

joint return. joint return. (Does not include spouse’s AGI if couple (Does not include spouse’s AGI if couple files separate federal income tax returns.)files separate federal income tax returns.)

Household SizeHousehold Size Includes:Includes:

BorrowerBorrower Spouse (if married)Spouse (if married) Dependent children in household (including an Dependent children in household (including an

unborn child)unborn child) Other dependents living in the household (must Other dependents living in the household (must

receive at least 50% of their support from borrower)receive at least 50% of their support from borrower)

Pay As You Earn Repayment Pay As You Earn Repayment cont.cont.

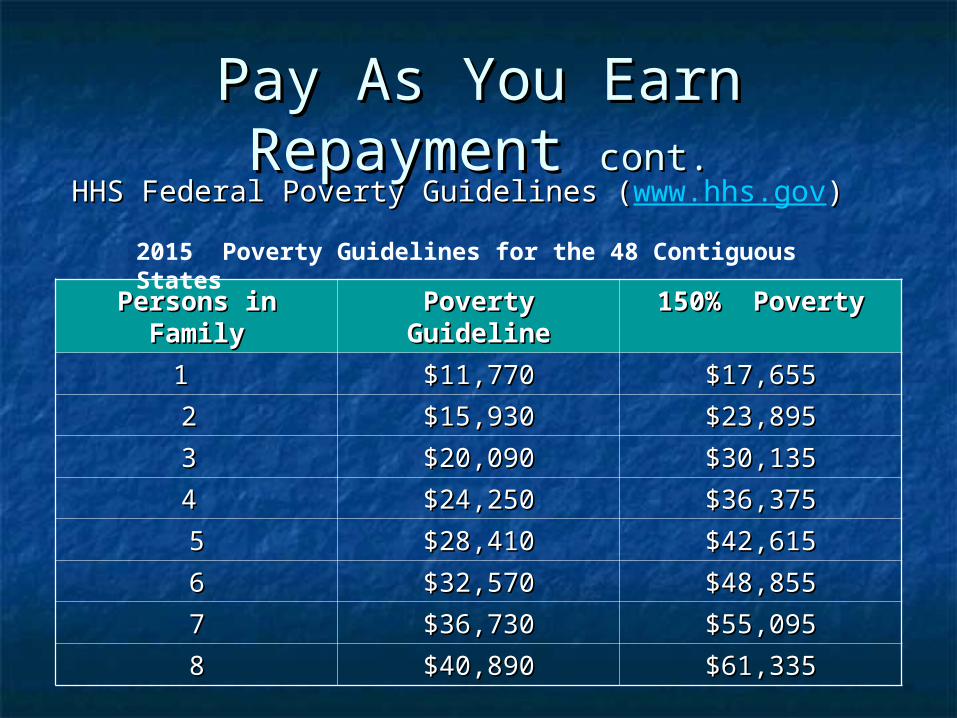

HHS Federal Poverty Guidelines (HHS Federal Poverty Guidelines (www.hhs.gov))

Persons in Persons in FamilyFamily

Poverty Poverty GuidelineGuideline

150% Poverty150% Poverty

1 1 $11,770$11,770 $17,655$17,655

2 2 $15,930$15,930 $23,895$23,895

3 3 $20,090$20,090 $30,135$30,135

4 4 $24,250$24,250 $36,375$36,375

55 $28,410$28,410 $42,615$42,615

66 $32,570$32,570 $48,855$48,855

77 $36,730$36,730 $55,095$55,095

88 $40,890$40,890 $61,335$61,335

2015 Poverty Guidelines for the 48 Contiguous States

Pay As You Earn Repayment Pay As You Earn Repayment cont.cont.

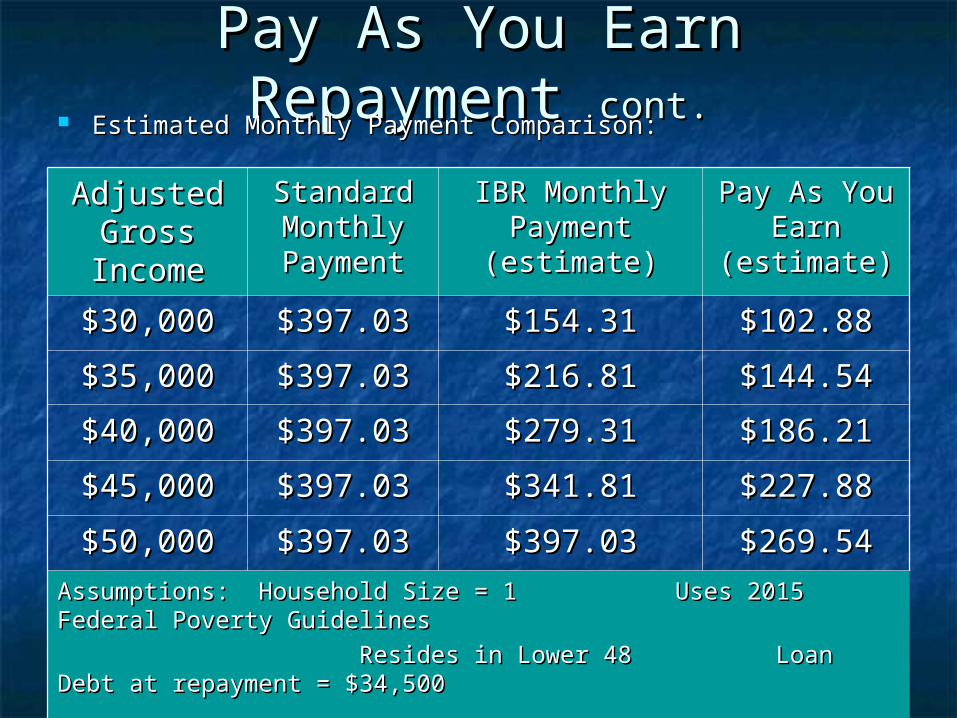

Estimated Monthly Payment Comparison:Estimated Monthly Payment Comparison:

Adjusted Adjusted Gross Gross

IncomeIncome

Standard Standard Monthly Monthly PaymentPayment

IBR Monthly IBR Monthly Payment Payment

(estimate)(estimate)

Pay As You Pay As You Earn Earn

(estimate)(estimate)

$30,000$30,000 $397.03$397.03 $154.31$154.31 $102.88$102.88

$35,000$35,000 $397.03$397.03 $216.81$216.81 $144.54$144.54

$40,000$40,000 $397.03$397.03 $279.31$279.31 $186.21$186.21

$45,000$45,000 $397.03$397.03 $341.81$341.81 $227.88$227.88

$50,000$50,000 $397.03$397.03 $397.03$397.03 $269.54$269.54Assumptions: Household Size = 1 Uses 2015 Federal Poverty Assumptions: Household Size = 1 Uses 2015 Federal Poverty GuidelinesGuidelines

Resides in Lower 48 Loan Debt at repayment = Resides in Lower 48 Loan Debt at repayment = $34,500$34,500

Interest Rate = 6.8%Interest Rate = 6.8%

Pay As You Earn Repayment Pay As You Earn Repayment cont.cont.

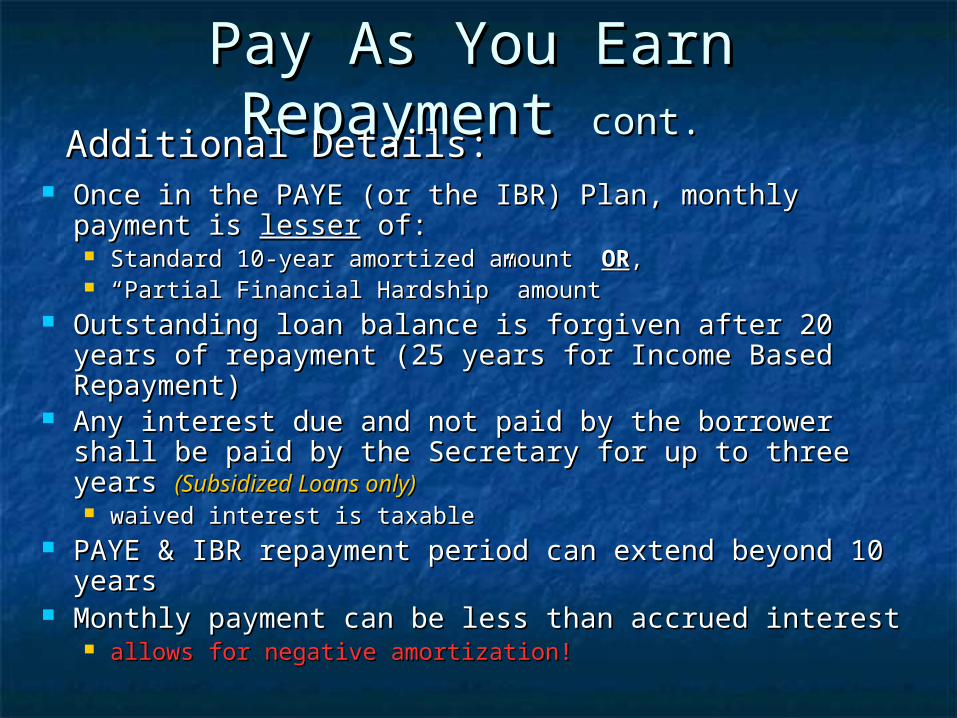

Once in the PAYE (or the IBR) Plan, monthly payment is Once in the PAYE (or the IBR) Plan, monthly payment is lesserlesser of: of: Standard 10-year amortized amount Standard 10-year amortized amount OROR,, ““Partial Financial Hardship” amountPartial Financial Hardship” amount

Outstanding loan balance is forgiven after 20 years of Outstanding loan balance is forgiven after 20 years of repayment (25 years for Income Based Repayment)repayment (25 years for Income Based Repayment)

Any interest due and not paid by the borrower shall be Any interest due and not paid by the borrower shall be paid by the Secretary for up to three years paid by the Secretary for up to three years (Subsidized (Subsidized Loans only)Loans only) waived interest is taxablewaived interest is taxable

PAYE & IBR repayment period can extend beyond 10 PAYE & IBR repayment period can extend beyond 10 yearsyears

Monthly payment can be less than accrued interestMonthly payment can be less than accrued interest allows for negative amortization!allows for negative amortization!

Additional Details:Additional Details:

Pay As You Earn Repayment Pay As You Earn Repayment cont.cont.

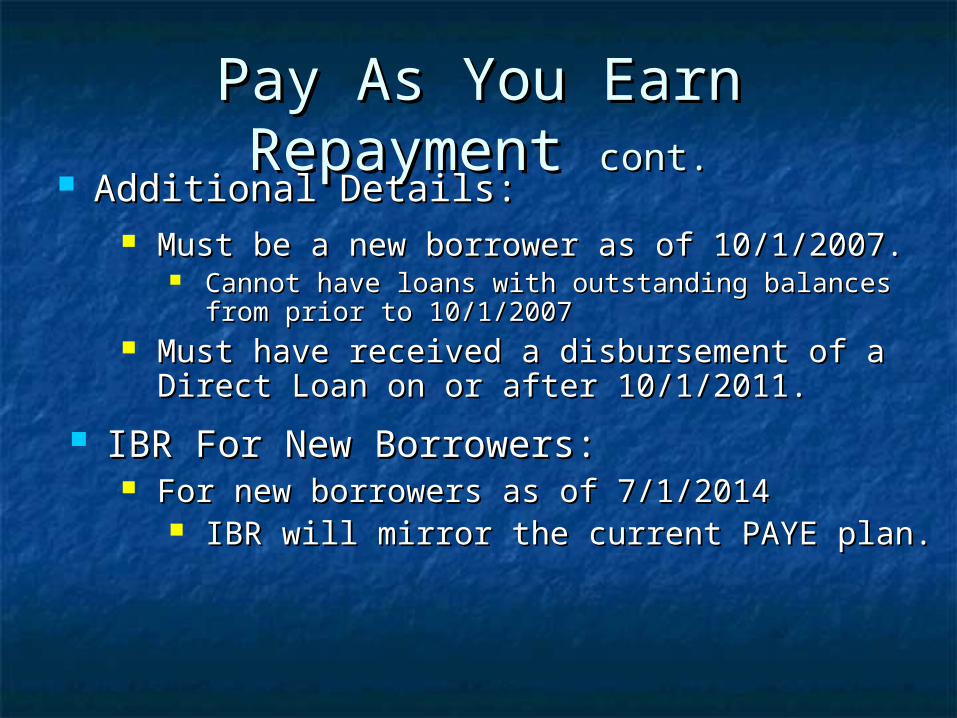

Additional Details:Additional Details: Must be a new borrower as of 10/1/2007.Must be a new borrower as of 10/1/2007.

Cannot have loans with outstanding balances from Cannot have loans with outstanding balances from prior to 10/1/2007 prior to 10/1/2007

Must have received a disbursement of a Direct Must have received a disbursement of a Direct Loan on or after 10/1/2011.Loan on or after 10/1/2011.

IBR For New Borrowers:IBR For New Borrowers: For new borrowers as of 7/1/2014For new borrowers as of 7/1/2014

IBR will mirror the current PAYE plan.IBR will mirror the current PAYE plan.

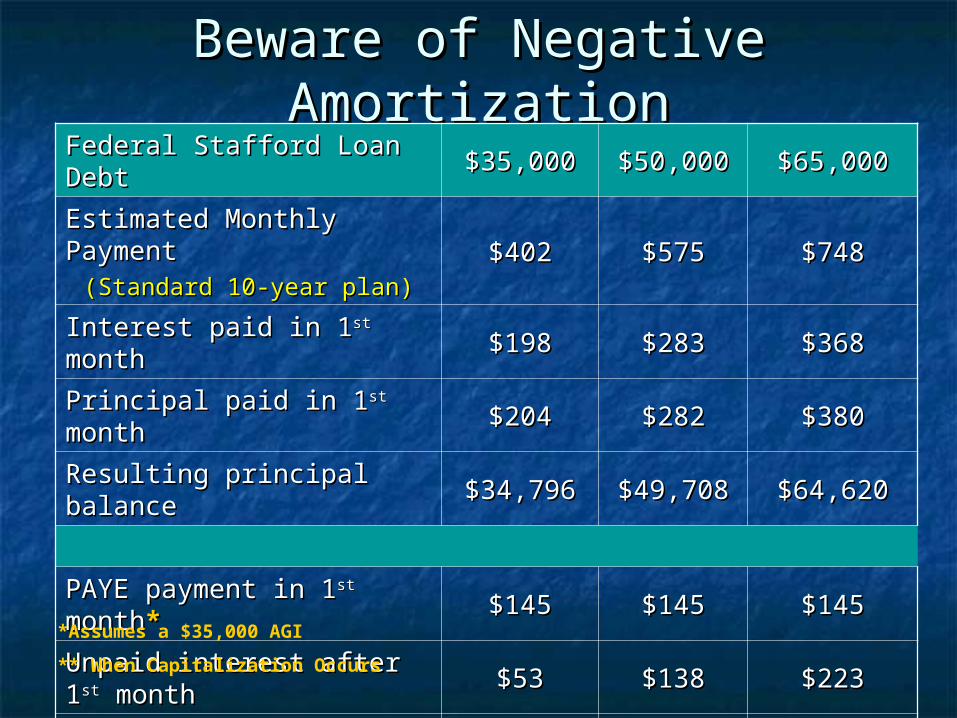

Beware of Negative Beware of Negative AmortizationAmortization

Federal Stafford Loan DebtFederal Stafford Loan Debt $35,000$35,000 $50,000$50,000 $65,000$65,000

Estimated Monthly Estimated Monthly PaymentPayment

(Standard 10-year plan)(Standard 10-year plan)$402$402 $575$575 $748$748

Interest paid in 1Interest paid in 1stst month month $198$198 $283$283 $368$368

Principal paid in 1Principal paid in 1stst month month $204$204 $282$282 $380$380

Resulting principal balanceResulting principal balance $34,796$34,796 $49,708$49,708 $64,620$64,620

PAYE payment in 1PAYE payment in 1stst monthmonth**

$145$145 $145$145 $145$145

Unpaid interest after 1Unpaid interest after 1stst monthmonth $53$53 $138$138 $223$223

Resulting Principal Resulting Principal balancebalance**** $35,053$35,053 $50,138$50,138 $65,223$65,223*Assumes a $35,000 AGI

** When Capitalization Occurs

Pay As You Earn Repayment Pay As You Earn Repayment cont.cont.

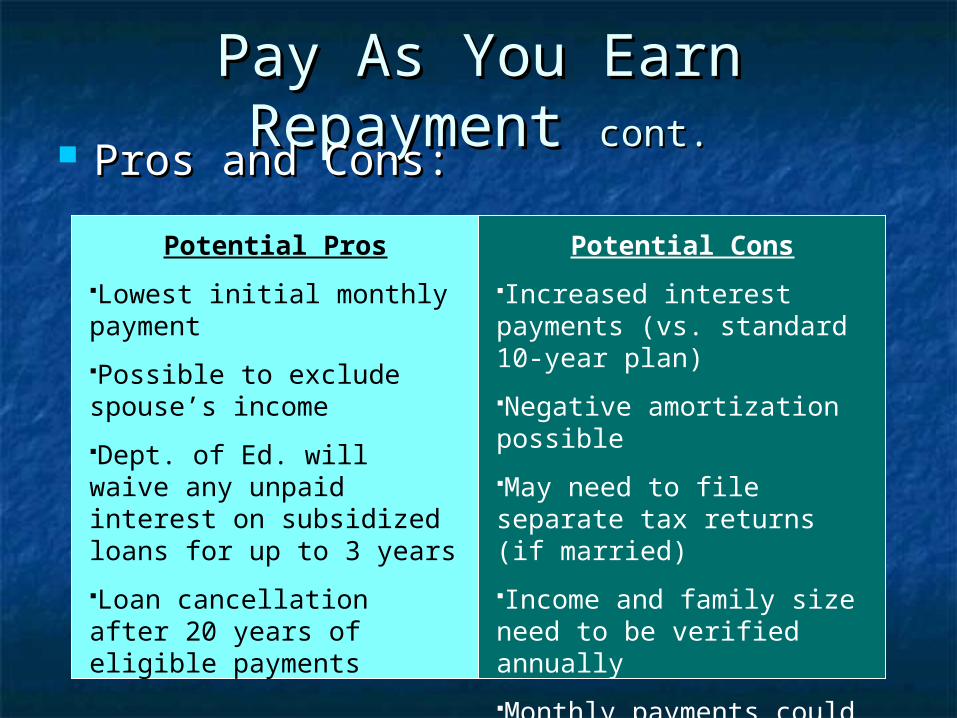

Pros and Cons:Pros and Cons:

Potential Pros

Lowest initial monthly payment

Possible to exclude spouse’s income

Dept. of Ed. will waive any unpaid interest on subsidized loans for up to 3 years

Loan cancellation after 20 years of eligible payments

Potential Cons

Increased interest payments (vs. standard 10-year plan)

Negative amortization possible

May need to file separate tax returns (if married)

Income and family size need to be verified annually

Monthly payments could change each year

Income Driven Plans Income Driven Plans & PSLF & PSLF (Calculations)(Calculations)

Public Service Loan ForgivenessPublic Service Loan Forgiveness contcont..

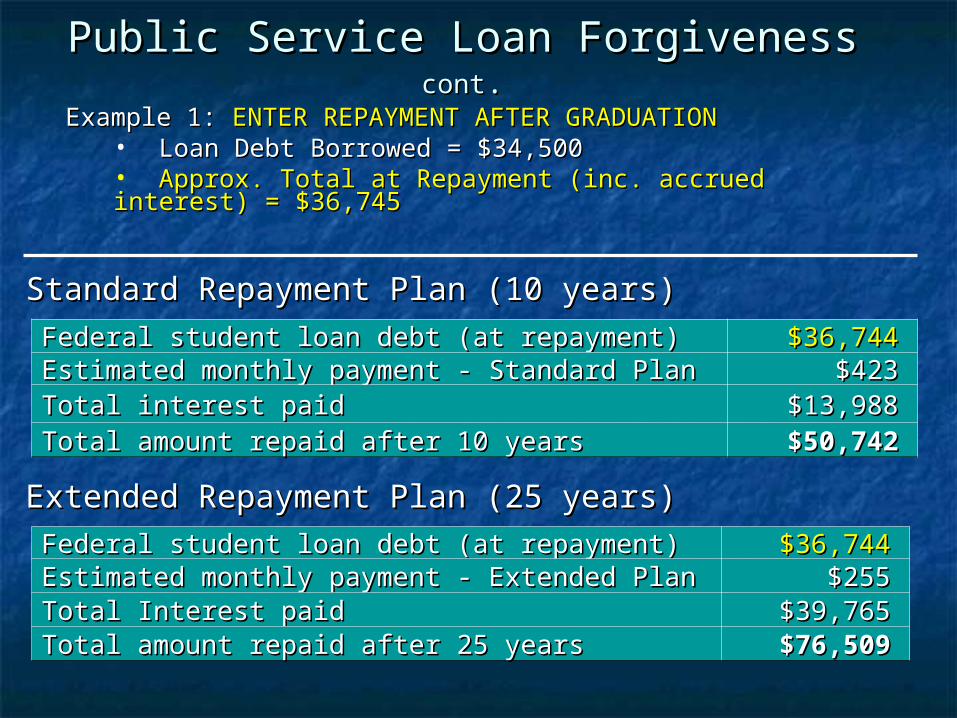

Federal student loan debt (at repayment)Federal student loan debt (at repayment) $36,744$36,744Estimated monthly payment - Standard PlanEstimated monthly payment - Standard Plan $423$423Total interest paidTotal interest paid $13,988$13,988Total amount repaid after 10 yearsTotal amount repaid after 10 years $50,742$50,742

Example 1: Example 1: ENTER REPAYMENT AFTER GRADUATIONENTER REPAYMENT AFTER GRADUATION• Loan Debt Borrowed = $34,500Loan Debt Borrowed = $34,500• Approx. Total at Repayment (inc. accrued interest) = $36,745 Approx. Total at Repayment (inc. accrued interest) = $36,745

Standard Repayment Plan (10 years)Standard Repayment Plan (10 years)

Extended Repayment Plan (25 years)Extended Repayment Plan (25 years)

Federal student loan debt (at repayment)Federal student loan debt (at repayment) $36,744$36,744Estimated monthly payment - Extended PlanEstimated monthly payment - Extended Plan $255$255Total Interest paidTotal Interest paid $39,765$39,765Total amount repaid after 25 yearsTotal amount repaid after 25 years $76,509$76,509

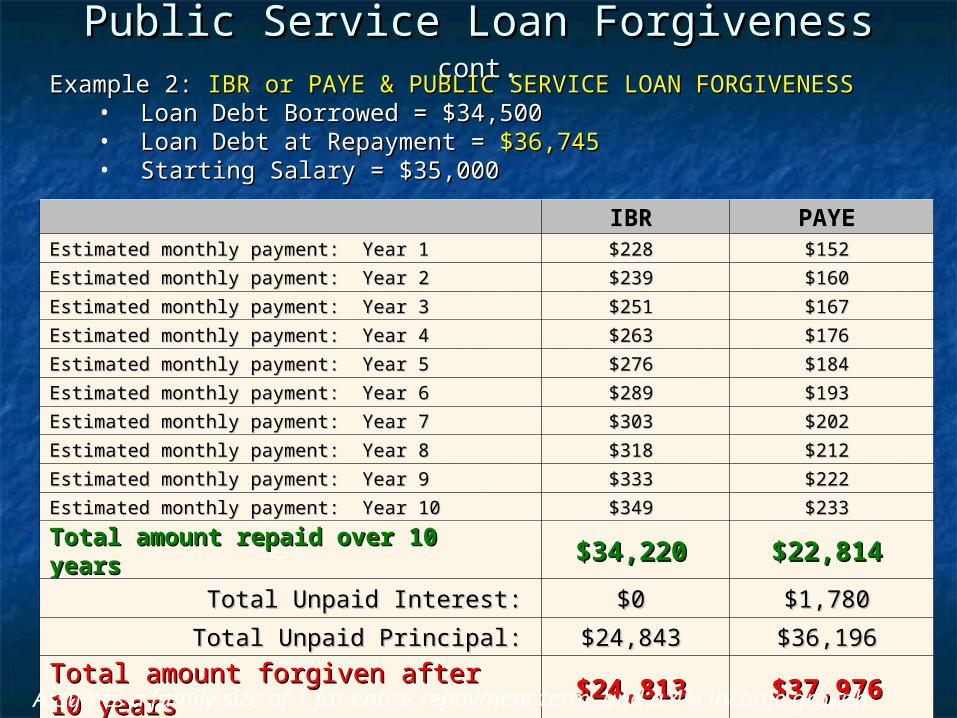

Public Service Loan ForgivenessPublic Service Loan Forgiveness contcont..Example 2: Example 2: IBR or PAYE & PUBLIC SERVICE LOAN FORGIVENESSIBR or PAYE & PUBLIC SERVICE LOAN FORGIVENESS

• Loan Debt Borrowed = $34,500Loan Debt Borrowed = $34,500• Loan Debt at Repayment = Loan Debt at Repayment = $36,745$36,745• Starting Salary = $35,000Starting Salary = $35,000

IBRIBR PAYEPAYEEstimated monthly payment: Year 1Estimated monthly payment: Year 1 $228$228 $152$152

Estimated monthly payment: Year 2Estimated monthly payment: Year 2 $239$239 $160$160

Estimated monthly payment: Year 3Estimated monthly payment: Year 3 $251$251 $167$167

Estimated monthly payment: Year 4Estimated monthly payment: Year 4 $263$263 $176$176

Estimated monthly payment: Year 5Estimated monthly payment: Year 5 $276$276 $184$184

Estimated monthly payment: Year 6Estimated monthly payment: Year 6 $289$289 $193$193

Estimated monthly payment: Year 7Estimated monthly payment: Year 7 $303$303 $202$202

Estimated monthly payment: Year 8Estimated monthly payment: Year 8 $318$318 $212$212

Estimated monthly payment: Year 9Estimated monthly payment: Year 9 $333$333 $222$222

Estimated monthly payment: Year 10Estimated monthly payment: Year 10 $349$349 $233$233

Total amount repaid over 10 yearsTotal amount repaid over 10 years $34,220$34,220 $22,814$22,814Total Unpaid Interest:Total Unpaid Interest: $0$0 $1,780$1,780

Total Unpaid Principal:Total Unpaid Principal: $24,843$24,843 $36,196$36,196

Total amount forgiven after 10 Total amount forgiven after 10 yearsyears $24,813$24,813 $37,976$37,976

Assumes a family size of 1 for entire repayment term, and a 4% income growth.

Public Service Loan Forgiveness Public Service Loan Forgiveness cont.cont.

A few Points to Ponder:A few Points to Ponder: Borrower is required to work full-time in Borrower is required to work full-time in

a qualified public service position for a a qualified public service position for a minimum of 120 months. minimum of 120 months.

Borrower must make qualifying monthly Borrower must make qualifying monthly loan payments during the entire 120 loan payments during the entire 120 month period of public service month period of public service employment.employment.

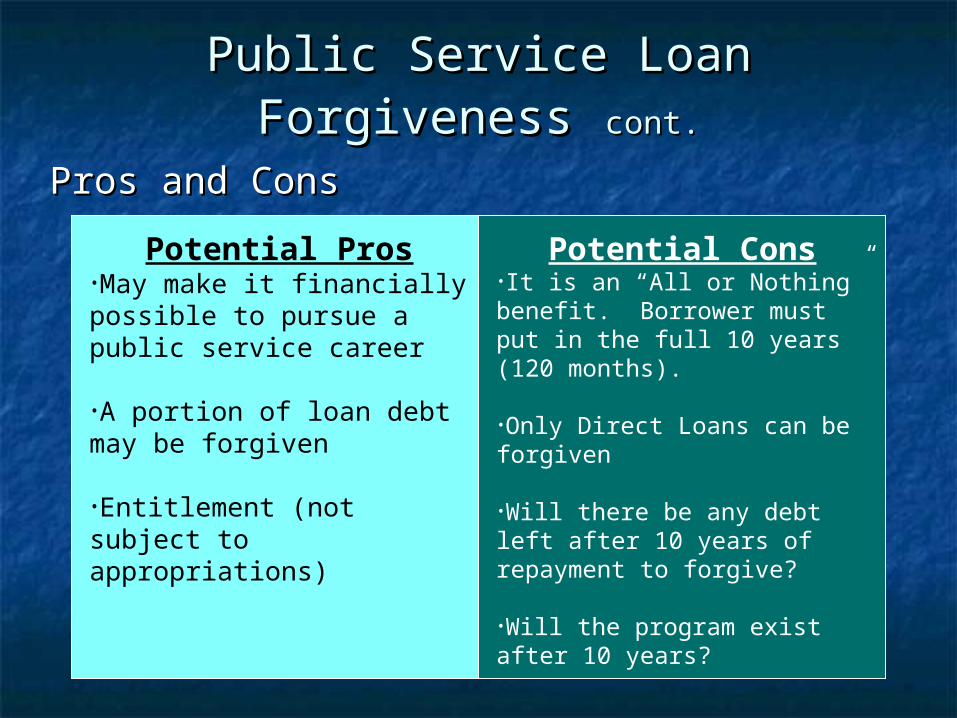

Public Service Loan ForgivenessPublic Service Loan Forgiveness cont.cont.

Pros and ConsPros and Cons

Potential Pros•May make it financially possible to pursue a public service career

•A portion of loan debt may be forgiven

•Entitlement (not subject to appropriations)

Potential Cons•It is an “All or Nothing” benefit. Borrower must put in the full 10 years (120 months).

•Only Direct Loans can be forgiven

•Will there be any debt left after 10 years of repayment to forgive?

•Will the program exist after 10 years?

Public Service Loan ForgivenessPublic Service Loan Forgiveness cont.cont.

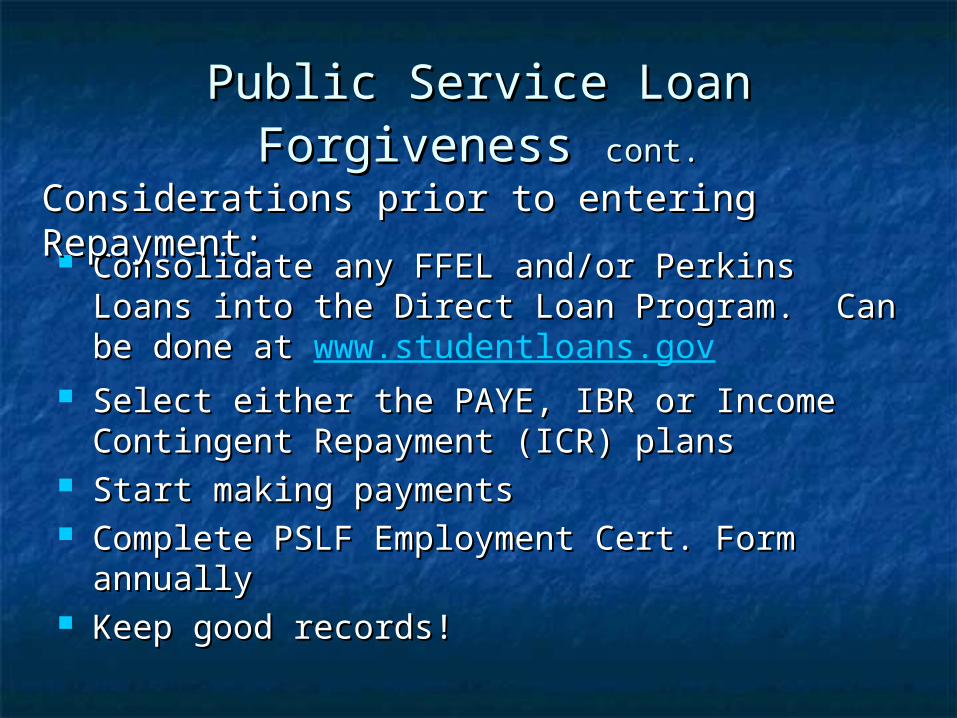

Consolidate any FFEL and/or Perkins Loans Consolidate any FFEL and/or Perkins Loans into the Direct Loan Program. Can be done at into the Direct Loan Program. Can be done at www.studentloans.gov

Select either the PAYE, IBR or Income Select either the PAYE, IBR or Income Contingent Repayment (ICR) plansContingent Repayment (ICR) plans

Start making paymentsStart making payments Complete PSLF Employment Cert. Form Complete PSLF Employment Cert. Form

annuallyannually Keep good records!Keep good records!

Considerations prior to entering Considerations prior to entering Repayment:Repayment:

Public Service Loan ForgivenessPublic Service Loan Forgiveness cont.cont.

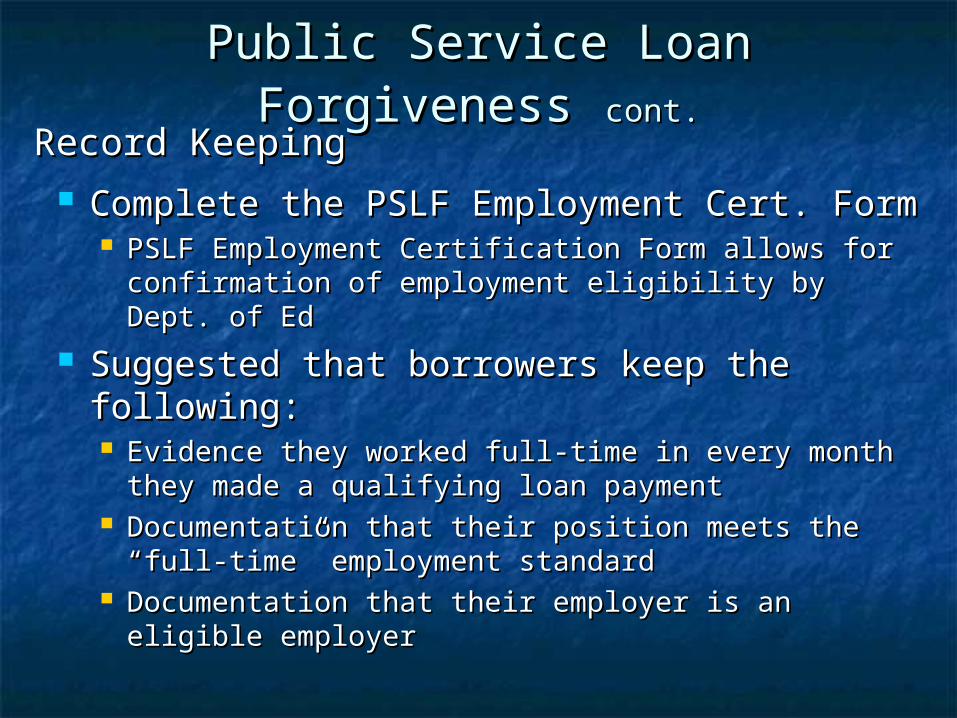

Complete the PSLF Employment Cert. FormComplete the PSLF Employment Cert. Form PSLF Employment Certification Form allows for PSLF Employment Certification Form allows for

confirmation of employment eligibility by Dept. of confirmation of employment eligibility by Dept. of EdEd

Suggested that borrowers keep the Suggested that borrowers keep the following:following: Evidence they worked full-time in every month they Evidence they worked full-time in every month they

made a qualifying loan paymentmade a qualifying loan payment Documentation that their position meets the “full-Documentation that their position meets the “full-

time” employment standardtime” employment standard Documentation that their employer is an eligible Documentation that their employer is an eligible

employeremployer

Record KeepingRecord Keeping

Questions?Questions?