Embed Size (px)

Citation preview

Public Accounting and GovernanceCourse for doctoral students

25-28 April 2006 in Tartu, Estonia

Public sector accounting and budgetingreforms in Europe

-International Public Sector Accounting

StandardsGiuseppe Grossi

PhD and Associate Professor in Public Management and Accounting

E-mail: [email protected]

Department of Business and Social StudiesSiena University

(website: www.unisi.it)

Agenda

Public sector accounting and budgeting reforms in Europe

IPSAS and IFAC-PSC

Reasons for IPSAS

Background and Current status of StandardsProject

Accounting Principles

Components of Financial Statements

2

Comparative Project

Klaus Lüder/Rowan Jones: Diffusion of accrualaccounting and budgeting in Europe – a cross-countryanalysis

in: Lüder/Jones (eds.), Reforming governmental accountingand budgeting in Europe, Fachverlag Moderne Wirtschaft, Frankfurt/Main 2003

3

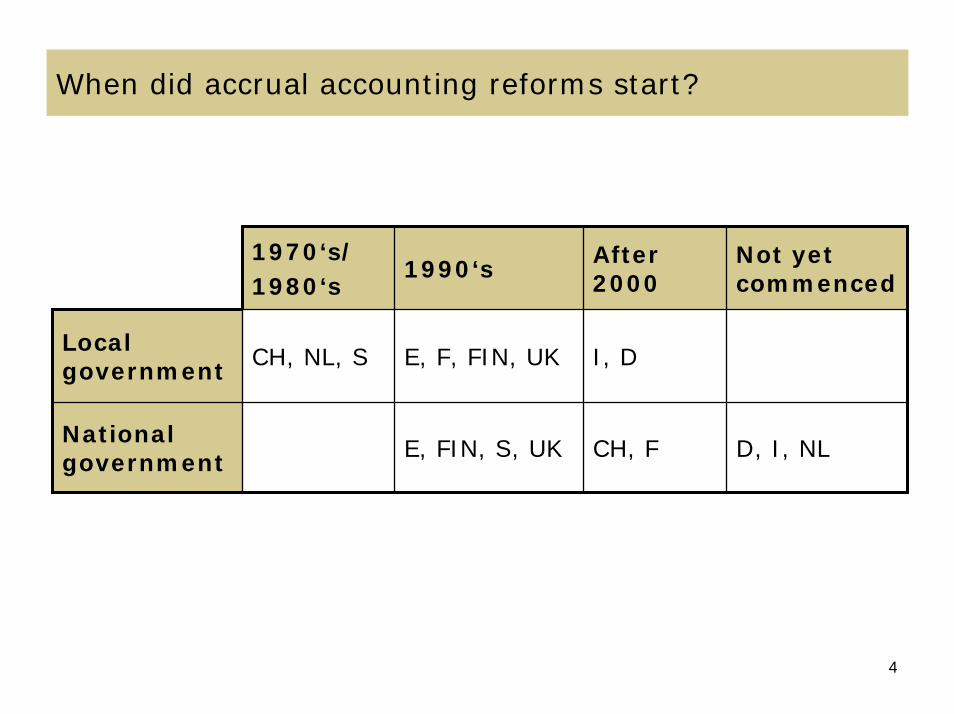

When did accrual accounting reforms start?

1970‘s/1980‘s

1990‘sAfter 2000

Not yetcommenced

Localgovernment CH, NL, S E, F, FIN, UK I, D

National government E, FIN, S, UK CH, F D, I, NL

4

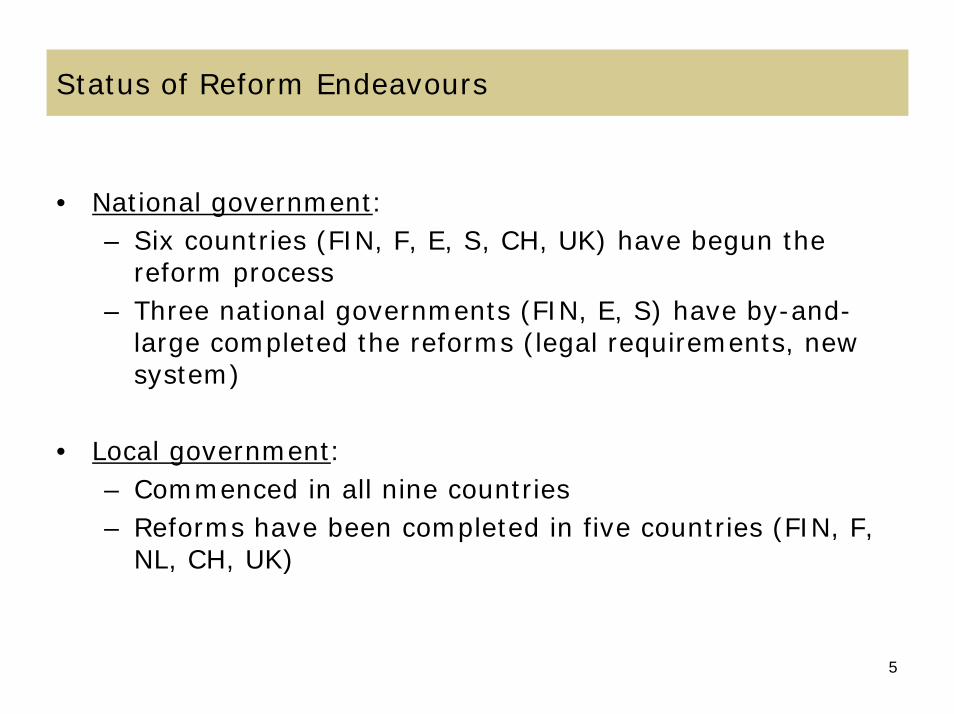

Status of Reform Endeavours

• National government:– Six countries (FIN, F, E, S, CH, UK) have begun the

reform process– Three national governments (FIN, E, S) have by-and-

large completed the reforms (legal requirements, newsystem)

• Local government:– Commenced in all nine countries– Reforms have been completed in five countries (FIN, F,

NL, CH, UK)

5

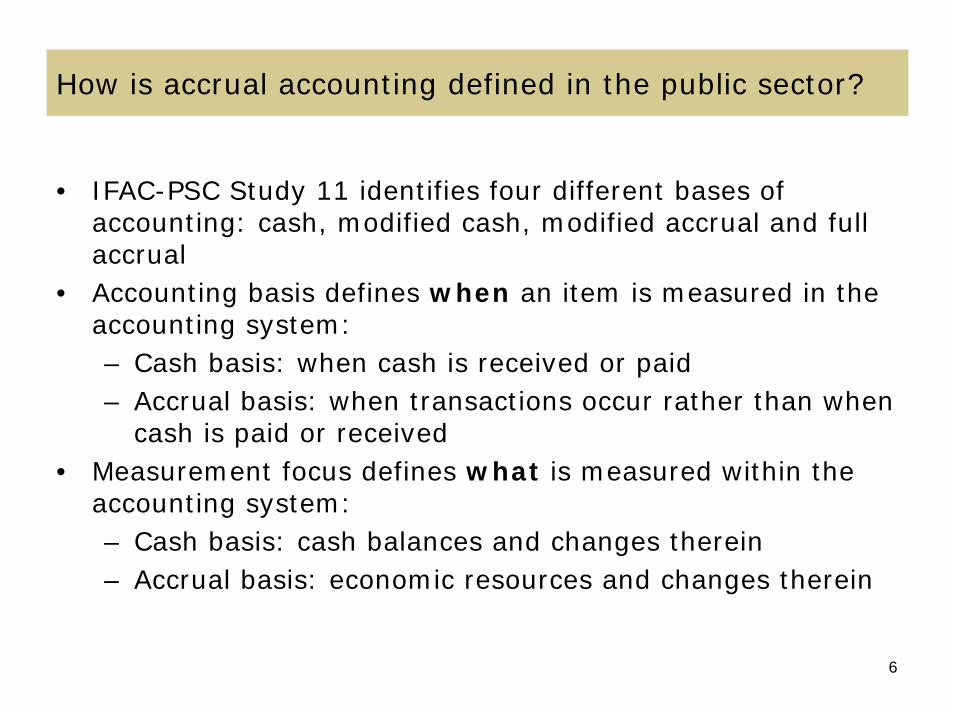

How is accrual accounting defined in the public sector?

• IFAC-PSC Study 11 identifies four different bases of accounting: cash, modified cash, modified accrual and fullaccrual

• Accounting basis defines when an item is measured in theaccounting system:– Cash basis: when cash is received or paid– Accrual basis: when transactions occur rather than when

cash is paid or received• Measurement focus defines what is measured within the

accounting system:– Cash basis: cash balances and changes therein– Accrual basis: economic resources and changes therein

6

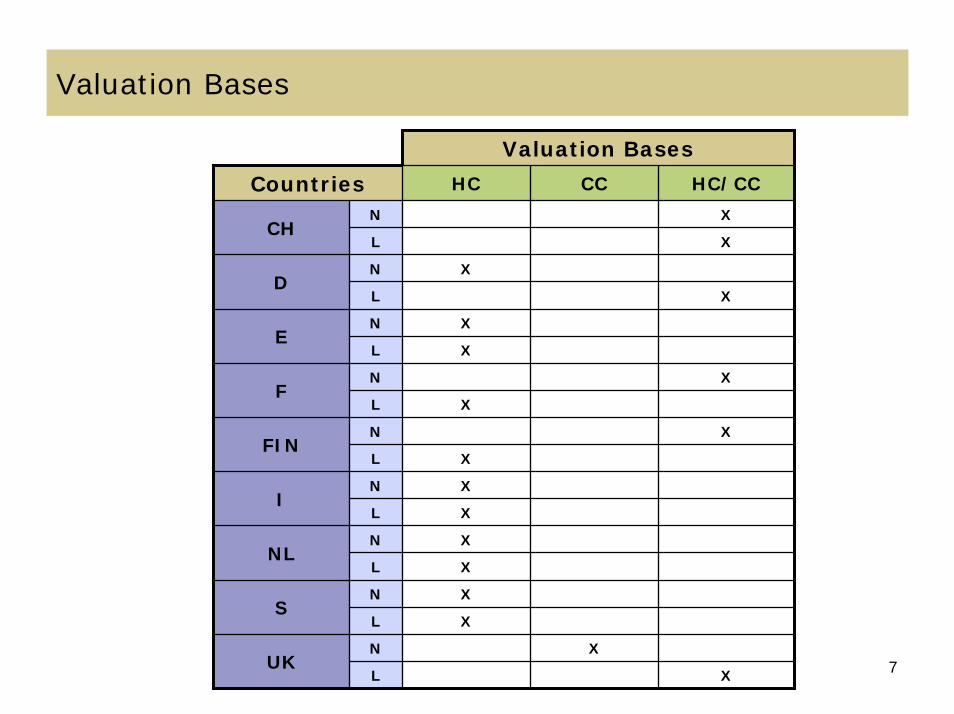

Valuation Bases

Valuation Bases

Countries HC CC HC/CC

N X

L X

N X

L X

N X

L X

N X

L X

N X

L X

N X

L X

N X

L X

N X

L X

N X

L XUK

S

NL

I

FIN

F

E

D

CH

7

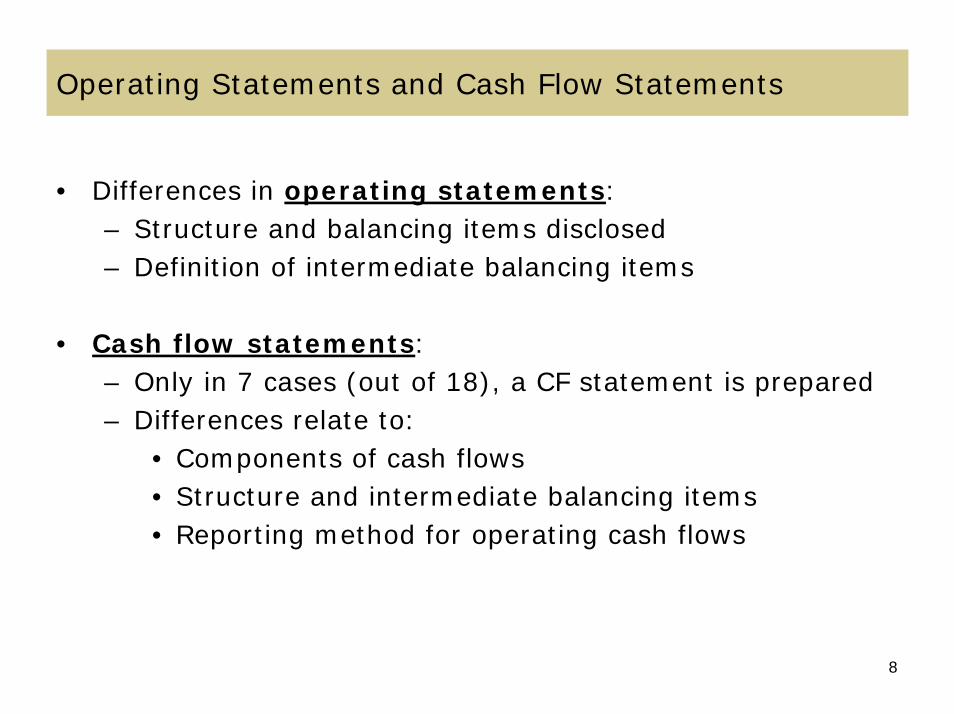

Operating Statements and Cash Flow Statements

• Differences in operating statements:– Structure and balancing items disclosed– Definition of intermediate balancing items

• Cash flow statements:– Only in 7 cases (out of 18), a CF statement is prepared– Differences relate to:

• Components of cash flows• Structure and intermediate balancing items• Reporting method for operating cash flows

8

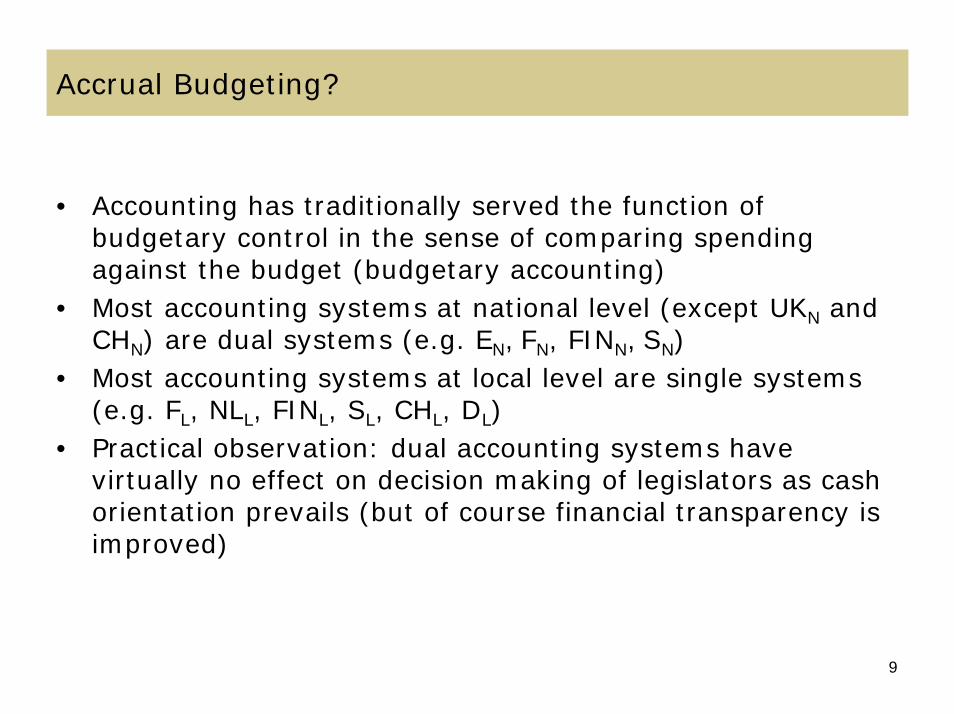

Accrual Budgeting?

• Accounting has traditionally served the function of budgetary control in the sense of comparing spendingagainst the budget (budgetary accounting)

• Most accounting systems at national level (except UKN and CHN) are dual systems (e.g. EN, FN, FINN, SN)

• Most accounting systems at local level are single systems(e.g. FL, NLL, FINL, SL, CHL, DL)

• Practical observation: dual accounting systems havevirtually no effect on decision making of legislators as cash orientation prevails (but of course financial transparency isimproved)

9

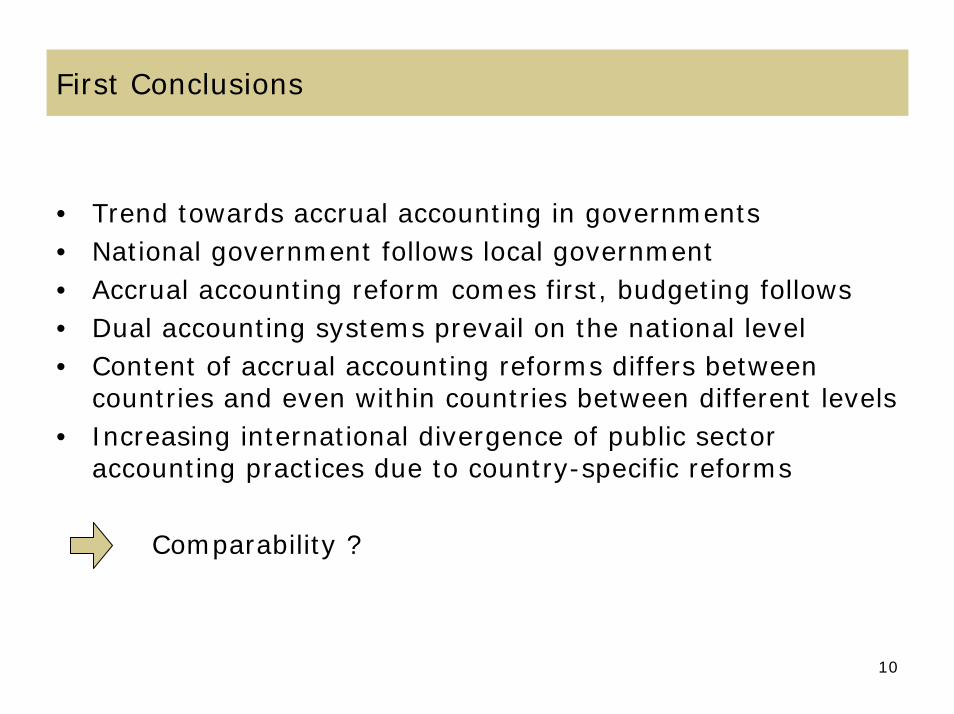

First Conclusions

• Trend towards accrual accounting in governments• National government follows local government• Accrual accounting reform comes first, budgeting follows• Dual accounting systems prevail on the national level• Content of accrual accounting reforms differs between

countries and even within countries between different levels• Increasing international divergence of public sector

accounting practices due to country-specific reforms

Comparability ?

10

Agenda

Public sector accounting and budgeting reforms in Europe

IPSAS and IFAC-PSC

Reasons for IPSAS

Background and Current status of StandardsProject

Accounting Principles

Components of Financial Statements

11

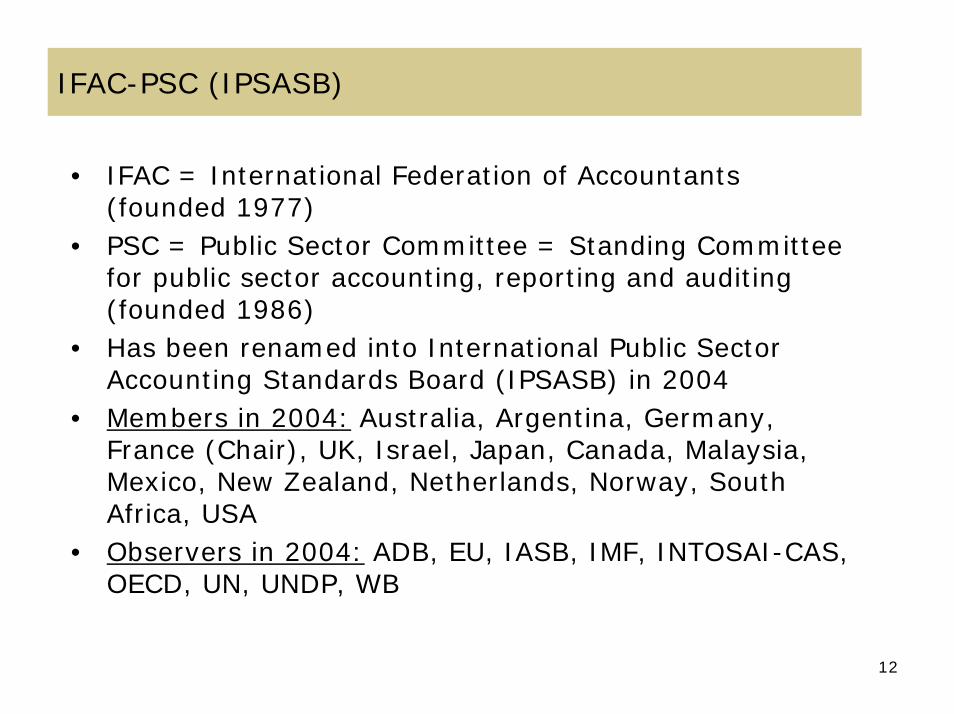

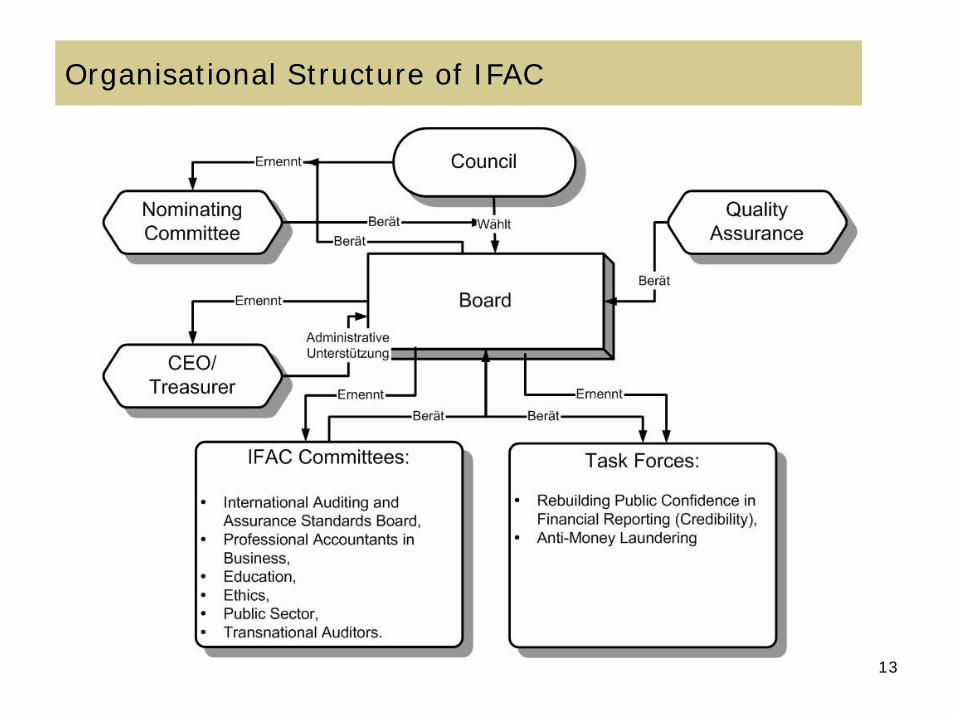

IFAC-PSC (IPSASB)

• IFAC = International Federation of Accountants(founded 1977)

• PSC = Public Sector Committee = Standing Committeefor public sector accounting, reporting and auditing(founded 1986)

• Has been renamed into International Public SectorAccounting Standards Board (IPSASB) in 2004

• Members in 2004: Australia, Argentina, Germany, France (Chair), UK, Israel, Japan, Canada, Malaysia, Mexico, New Zealand, Netherlands, Norway, South Africa, USA

• Observers in 2004: ADB, EU, IASB, IMF, INTOSAI-CAS, OECD, UN, UNDP, WB

12

Organisational Structure of IFAC

13

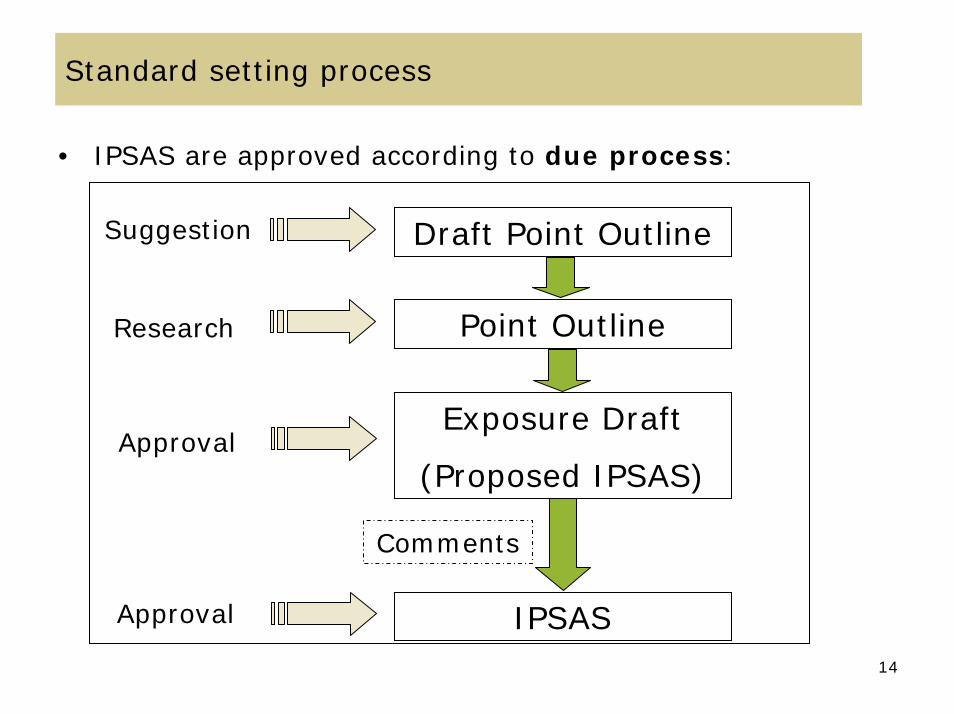

Standard setting process

• IPSAS are approved according to due process:

Draft Point Outline

Point Outline

Exposure Draft

(Proposed IPSAS)

IPSAS

Suggestion

Research

Approval

Approval

Comments

14

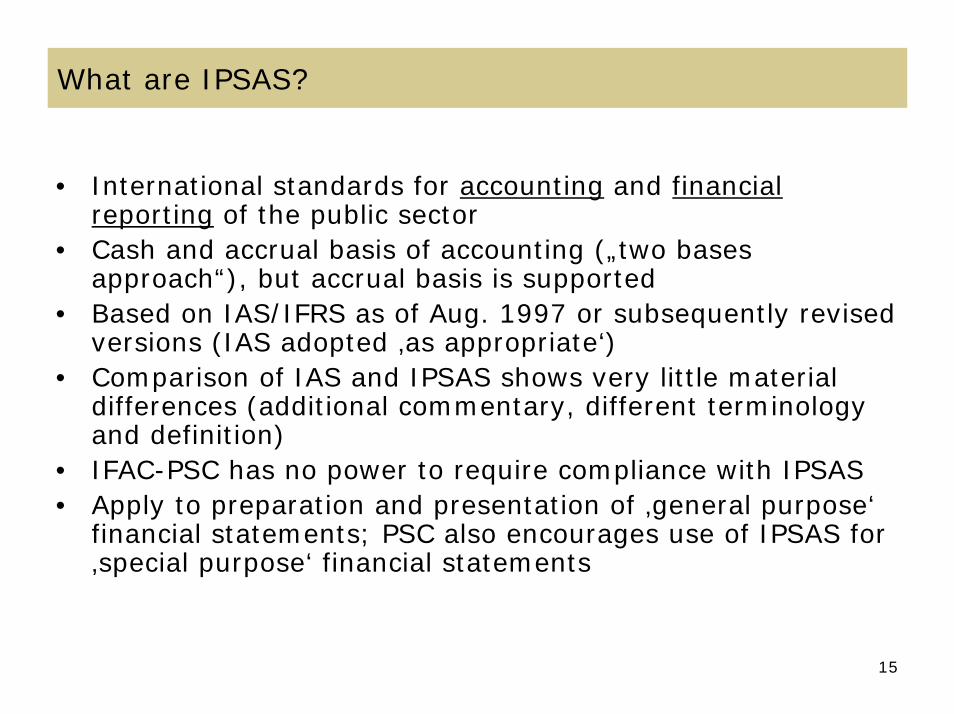

What are IPSAS?

• International standards for accounting and financialreporting of the public sector

• Cash and accrual basis of accounting („two basesapproach“), but accrual basis is supported

• Based on IAS/IFRS as of Aug. 1997 or subsequently revisedversions (IAS adopted ‚as appropriate‘)

• Comparison of IAS and IPSAS shows very little material differences (additional commentary, different terminologyand definition)

• IFAC-PSC has no power to require compliance with IPSAS• Apply to preparation and presentation of ‚general purpose‘

financial statements; PSC also encourages use of IPSAS for‚special purpose‘ financial statements

15

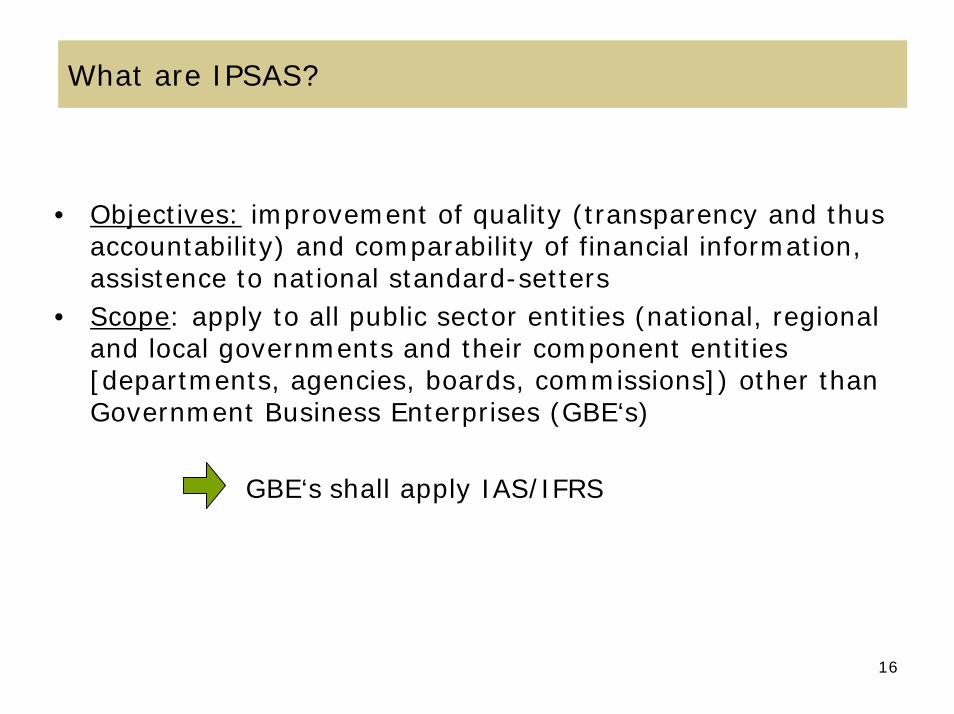

What are IPSAS?

• Objectives: improvement of quality (transparency and thusaccountability) and comparability of financial information, assistence to national standard-setters

• Scope: apply to all public sector entities (national, regional and local governments and their component entities[departments, agencies, boards, commissions]) other thanGovernment Business Enterprises (GBE‘s)

GBE‘s shall apply IAS/IFRS

16

Agenda

Public sector accounting and budgeting reforms in Europe

IPSAS and IFAC-PSC

Reasons for IPSAS

Background and Current status of StandardsProject

Accounting Principles

Components of Financial Statements

17

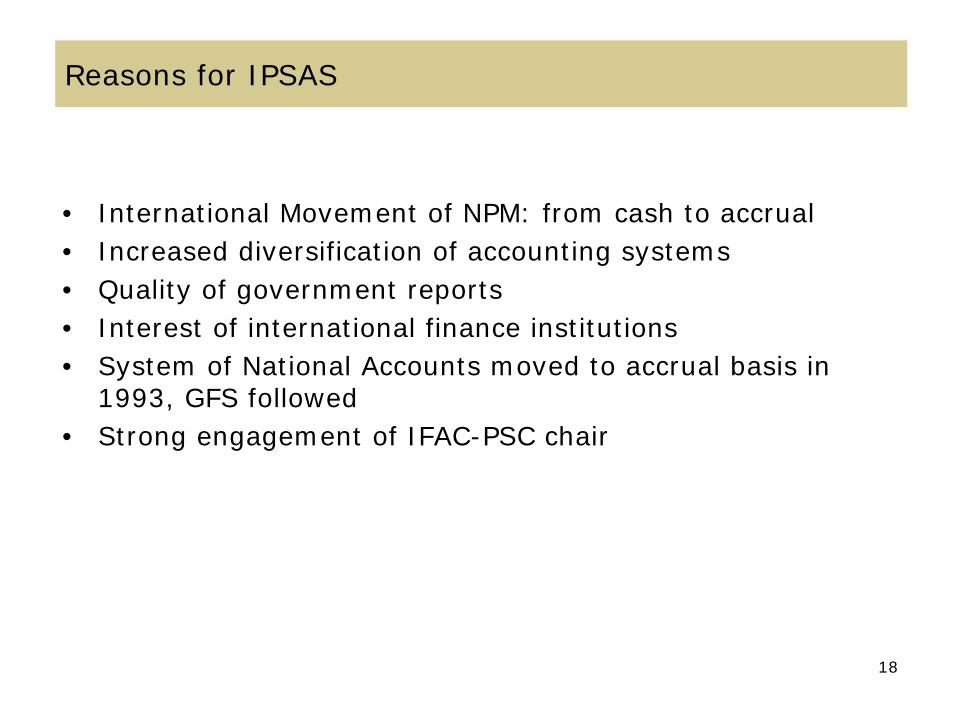

Reasons for IPSAS

• International Movement of NPM: from cash to accrual• Increased diversification of accounting systems• Quality of government reports• Interest of international finance institutions• System of National Accounts moved to accrual basis in

1993, GFS followed• Strong engagement of IFAC-PSC chair

18

Agenda

Public sector accounting and budgeting reforms in Europe

IPSAS and IFAC-PSC

Reasons for IPSAS

Background and Current status of StandardsProject

Accounting Principles

Components of Financial Statements

19

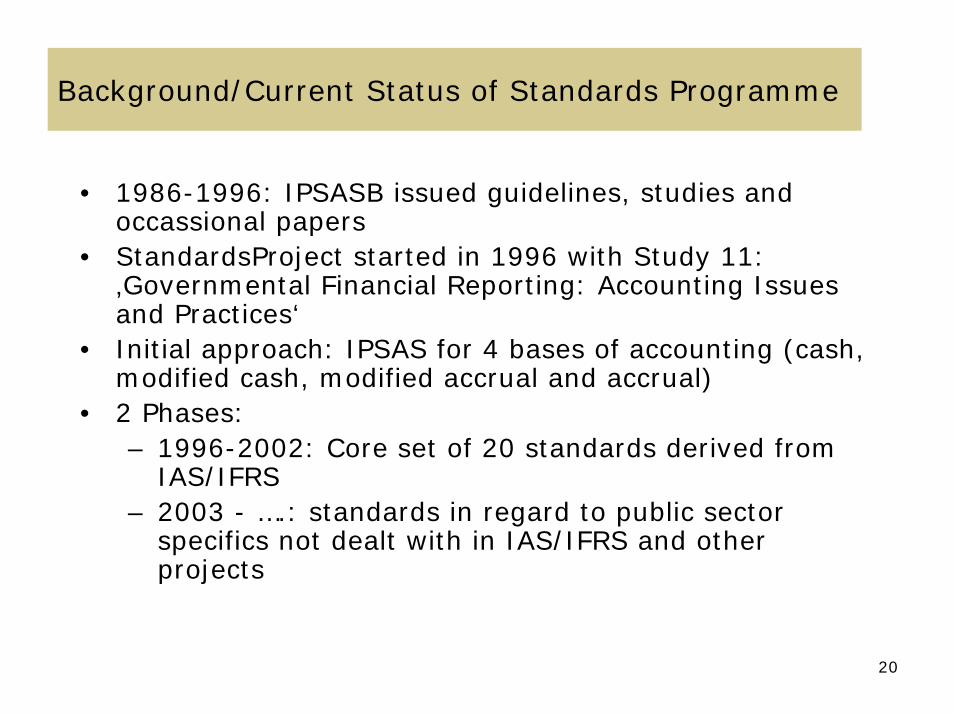

Background/Current Status of Standards Programme

• 1986-1996: IPSASB issued guidelines, studies and occassional papers

• StandardsProject started in 1996 with Study 11: ‚Governmental Financial Reporting: Accounting Issuesand Practices‘

• Initial approach: IPSAS for 4 bases of accounting (cash, modified cash, modified accrual and accrual)

• 2 Phases:– 1996-2002: Core set of 20 standards derived from

IAS/IFRS– 2003 - ….: standards in regard to public sector

specifics not dealt with in IAS/IFRS and otherprojects

20

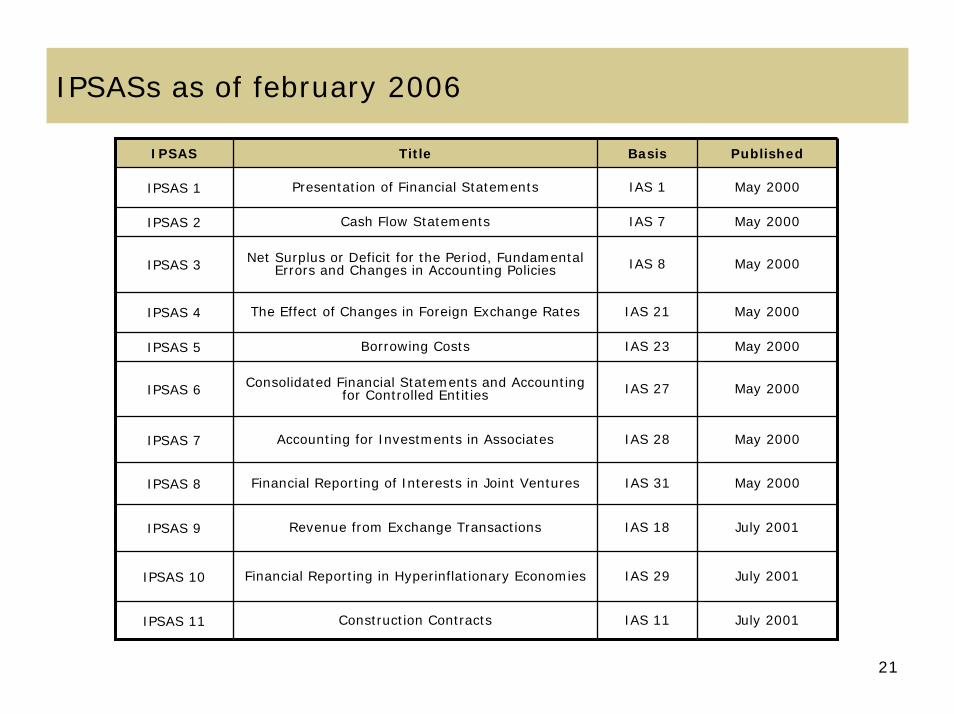

IPSASs as of february 2006

IPSAS Title Basis Published

IPSAS 1 Presentation of Financial Statements IAS 1 May 2000

IPSAS 2 Cash Flow Statements IAS 7 May 2000

IPSAS 3 Net Surplus or Deficit for the Period, Fundamental Errors and Changes in Accounting Policies IAS 8 May 2000

IPSAS 4 The Effect of Changes in Foreign Exchange Rates IAS 21 May 2000

IPSAS 5 Borrowing Costs IAS 23 May 2000

IPSAS 6 Consolidated Financial Statements and Accountingfor Controlled Entities IAS 27 May 2000

IPSAS 7 Accounting for Investments in Associates IAS 28 May 2000

IPSAS 8 Financial Reporting of Interests in Joint Ventures IAS 31 May 2000

IPSAS 9 Revenue from Exchange Transactions IAS 18 July 2001

IPSAS 10 Financial Reporting in Hyperinflationary Economies IAS 29 July 2001

IPSAS 11 Construction Contracts IAS 11 July 2001

21

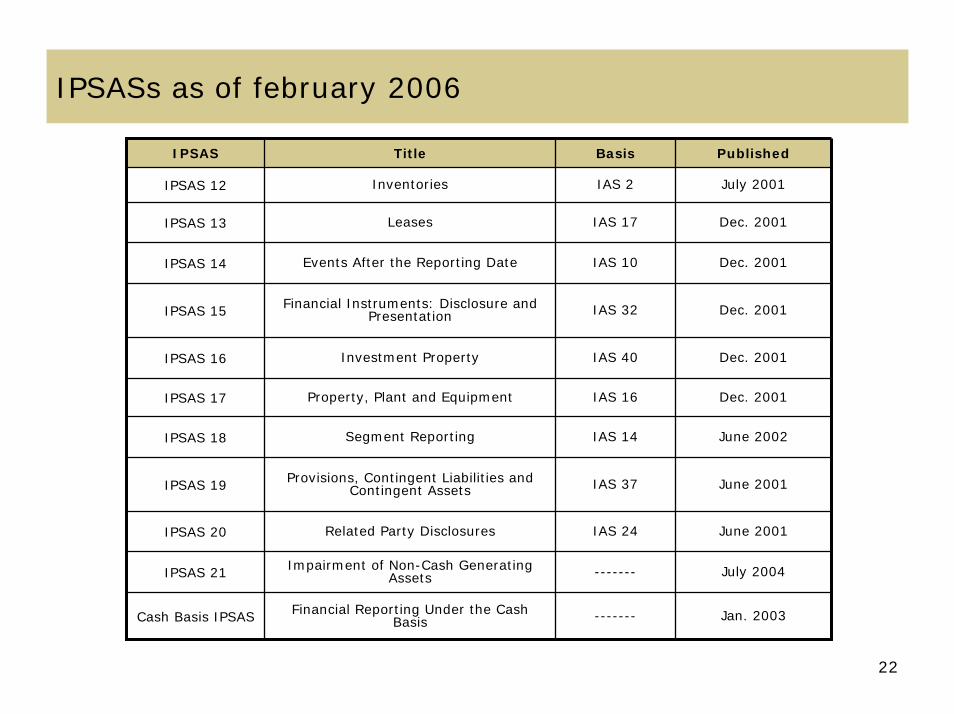

IPSASs as of february 2006

IPSAS Title Basis Published

IPSAS 12 Inventories IAS 2 July 2001

IPSAS 13 Leases IAS 17 Dec. 2001

IPSAS 14 Events After the Reporting Date IAS 10 Dec. 2001

IPSAS 15 Financial Instruments: Disclosure and Presentation IAS 32 Dec. 2001

IPSAS 16 Investment Property IAS 40 Dec. 2001

IPSAS 17 Property, Plant and Equipment IAS 16 Dec. 2001

IPSAS 18 Segment Reporting IAS 14 June 2002

IPSAS 19 Provisions, Contingent Liabilities and Contingent Assets IAS 37 June 2001

IPSAS 20 Related Party Disclosures IAS 24 June 2001

IPSAS 21 Impairment of Non-Cash GeneratingAssets ------- July 2004

Cash Basis IPSAS Financial Reporting Under the Cash Basis ------- Jan. 2003

22

IPSASs as of february 2006

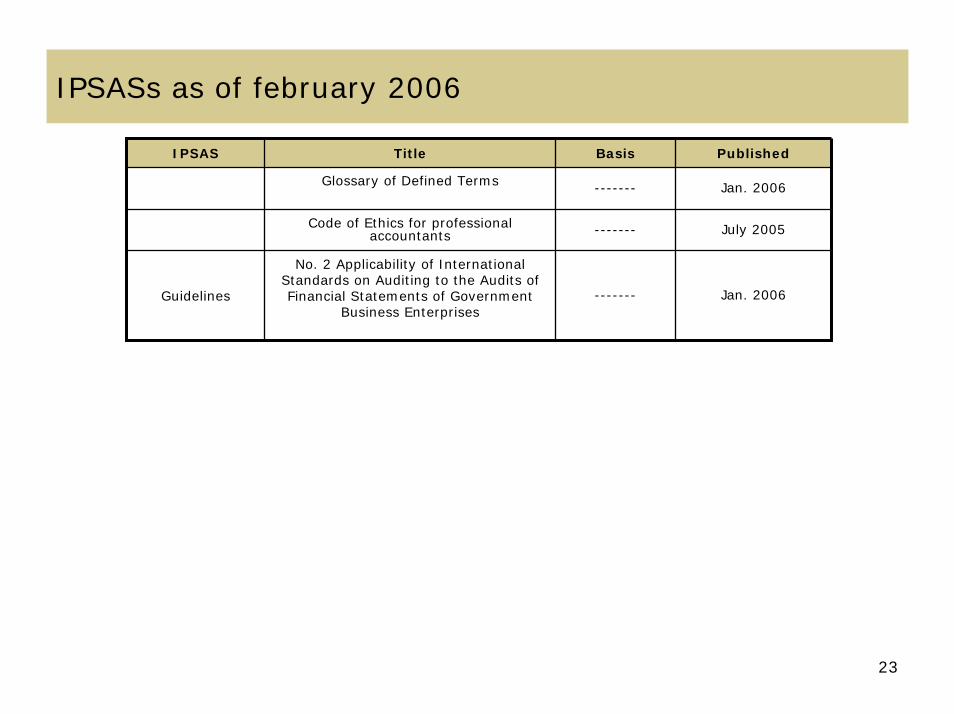

IPSAS Title Basis Published

Glossary of Defined Terms ------- Jan. 2006

Code of Ethics for professionalaccountants ------- July 2005

Guidelines

No. 2 Applicability of InternationalStandards on Auditing to the Audits of Financial Statements of Government

Business Enterprises------- Jan. 2006

23

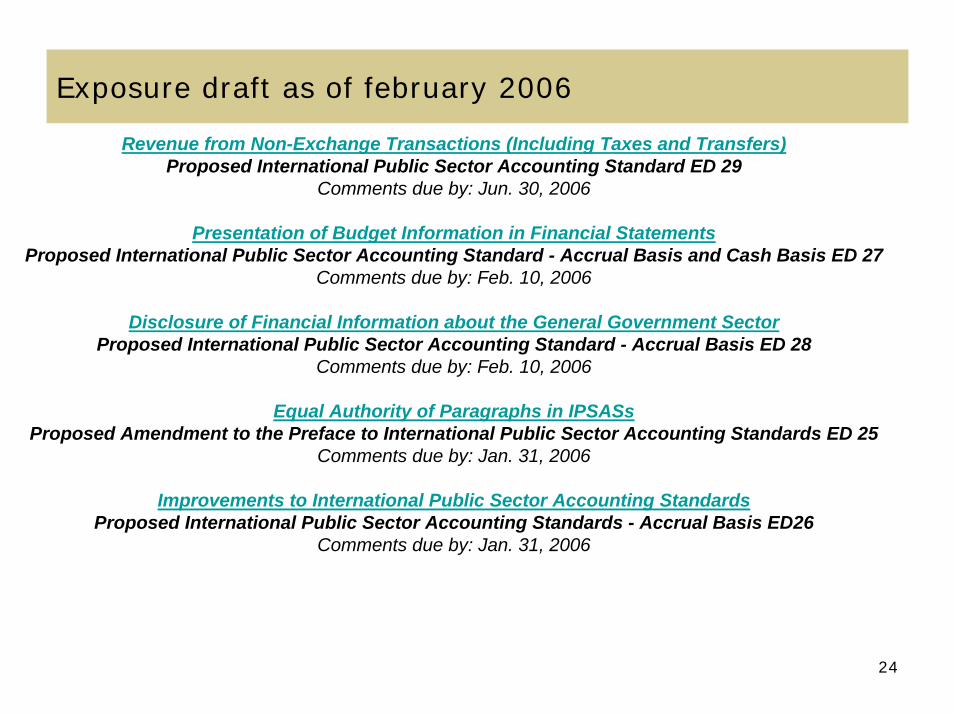

Exposure draft as of february 2006

Revenue from Non-Exchange Transactions (Including Taxes and Transfers)Proposed International Public Sector Accounting Standard ED 29

Comments due by: Jun. 30, 2006

Presentation of Budget Information in Financial StatementsProposed International Public Sector Accounting Standard - Accrual Basis and Cash Basis ED 27

Comments due by: Feb. 10, 2006

Disclosure of Financial Information about the General Government SectorProposed International Public Sector Accounting Standard - Accrual Basis ED 28

Comments due by: Feb. 10, 2006

Equal Authority of Paragraphs in IPSASsProposed Amendment to the Preface to International Public Sector Accounting Standards ED 25

Comments due by: Jan. 31, 2006

Improvements to International Public Sector Accounting StandardsProposed International Public Sector Accounting Standards - Accrual Basis ED26

Comments due by: Jan. 31, 2006

24

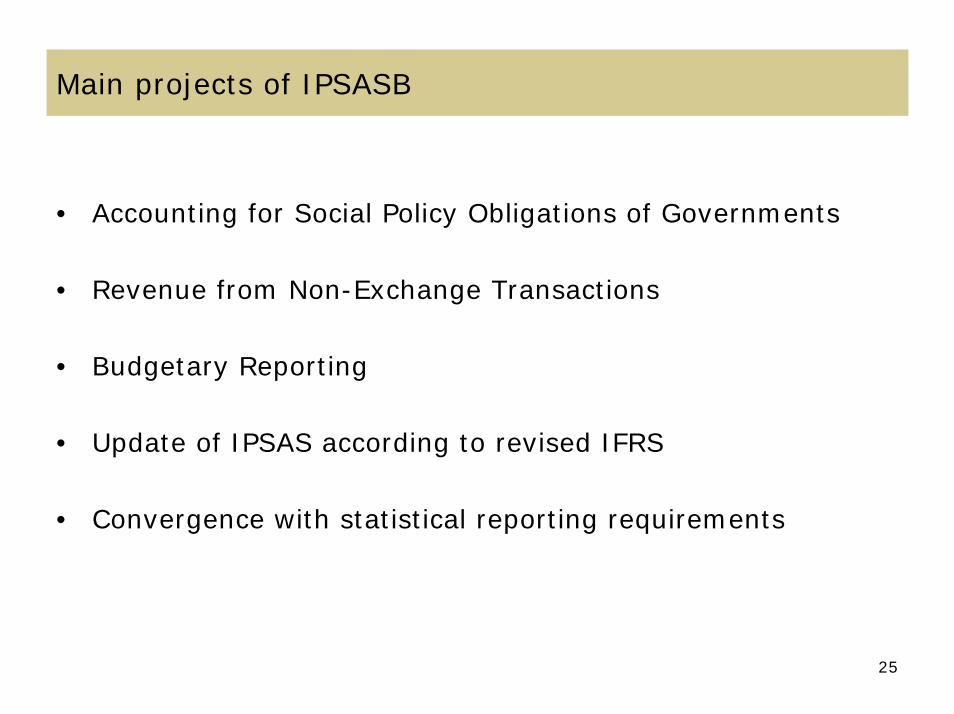

Main projects of IPSASB

• Accounting for Social Policy Obligations of Governments

• Revenue from Non-Exchange Transactions

• Budgetary Reporting

• Update of IPSAS according to revised IFRS

• Convergence with statistical reporting requirements

25

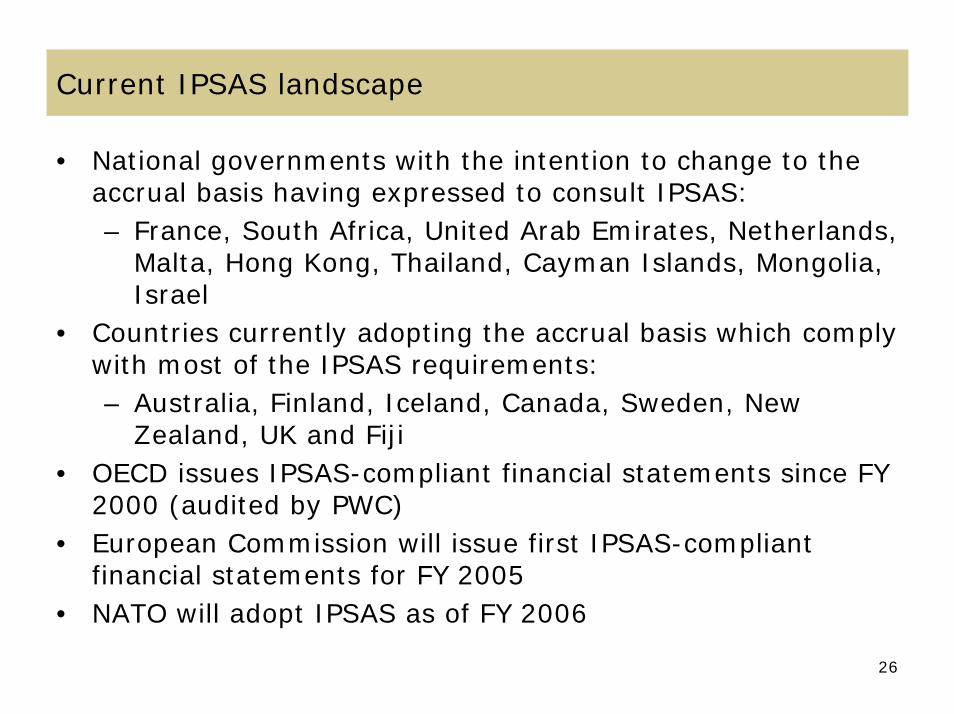

Current IPSAS landscape

• National governments with the intention to change to theaccrual basis having expressed to consult IPSAS:– France, South Africa, United Arab Emirates, Netherlands,

Malta, Hong Kong, Thailand, Cayman Islands, Mongolia, Israel

• Countries currently adopting the accrual basis which complywith most of the IPSAS requirements:– Australia, Finland, Iceland, Canada, Sweden, New

Zealand, UK and Fiji• OECD issues IPSAS-compliant financial statements since FY

2000 (audited by PWC)• European Commission will issue first IPSAS-compliant

financial statements for FY 2005• NATO will adopt IPSAS as of FY 2006

26

Agenda

Public sector accounting and budgeting reforms in Europe

IPSAS and IFAC-PSC

Reasons for IPSAS

Current status of StandardsProject and WorkPlan

Accounting Principles

Components of Financial Statements

27

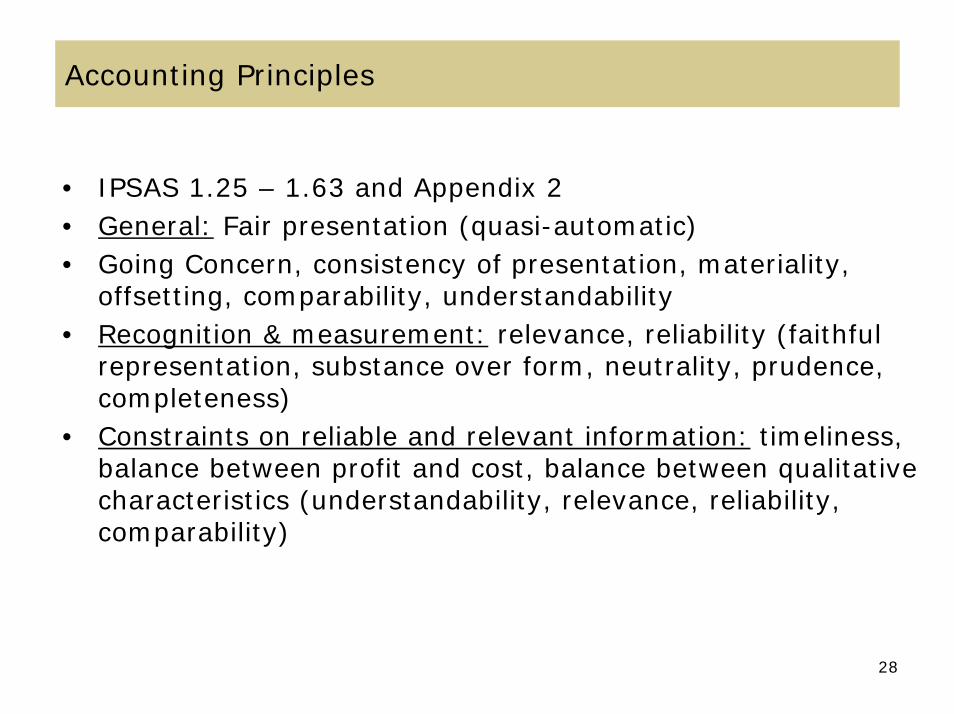

Accounting Principles

• IPSAS 1.25 – 1.63 and Appendix 2• General: Fair presentation (quasi-automatic)• Going Concern, consistency of presentation, materiality,

offsetting, comparability, understandability• Recognition & measurement: relevance, reliability (faithful

representation, substance over form, neutrality, prudence, completeness)

• Constraints on reliable and relevant information: timeliness, balance between profit and cost, balance between qualitative characteristics (understandability, relevance, reliability, comparability)

28

Agenda

Public sector accounting and budgeting reforms in Europe

IPSAS and IFAC-PSC

Reasons for IPSAS

Current status of StandardsProject and WorkPlan

Accounting Principles

Components of Financial Statements

29

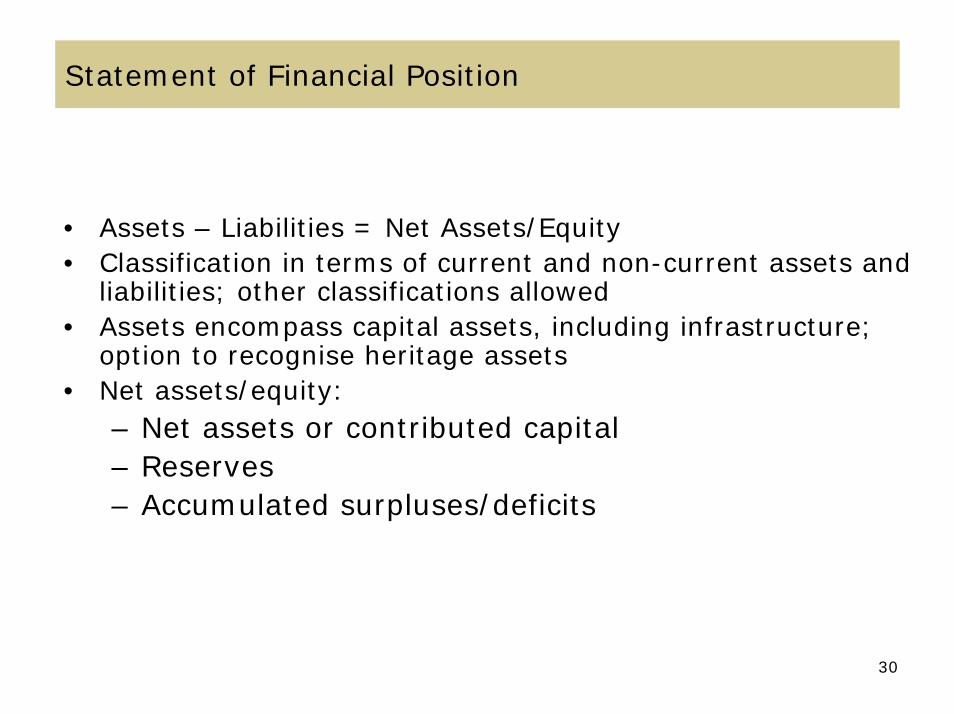

Statement of Financial Position

• Assets – Liabilities = Net Assets/Equity• Classification in terms of current and non-current assets and

liabilities; other classifications allowed• Assets encompass capital assets, including infrastructure;

option to recognise heritage assets• Net assets/equity:

– Net assets or contributed capital– Reserves– Accumulated surpluses/deficits

30

31

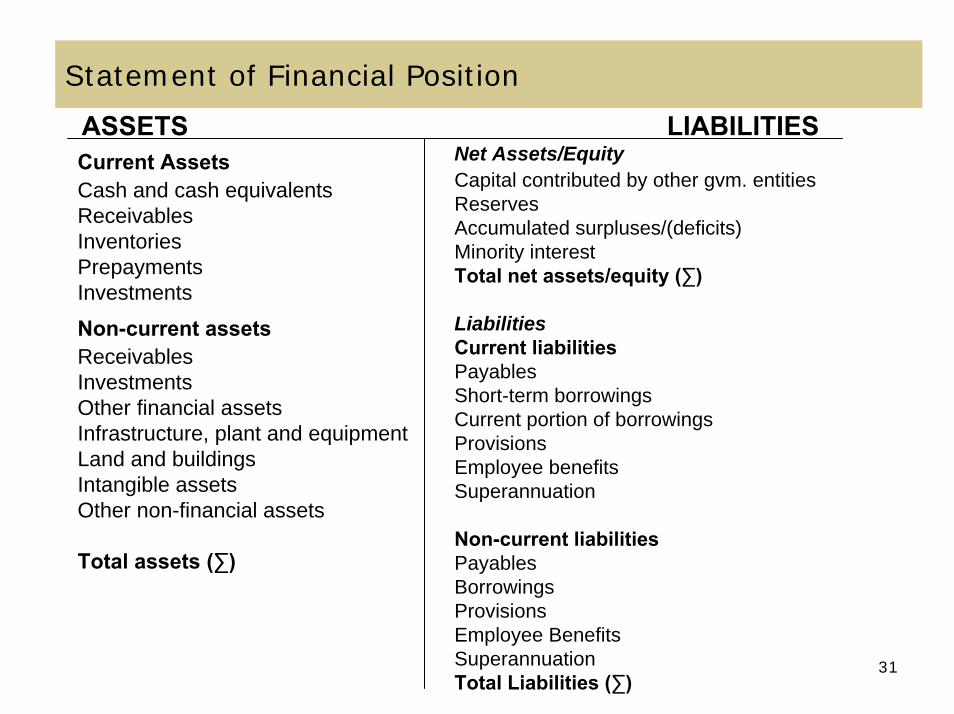

Statement of Financial Position

Current AssetsCash and cash equivalentsReceivablesInventoriesPrepaymentsInvestments

Non-current assetsReceivablesInvestmentsOther financial assetsInfrastructure, plant and equipmentLand and buildingsIntangible assetsOther non-financial assets

Total assets (∑)

ASSETSNet Assets/EquityCapital contributed by other gvm. entitiesReservesAccumulated surpluses/(deficits)Minority interestTotal net assets/equity (∑)

LiabilitiesCurrent liabilitiesPayablesShort-term borrowingsCurrent portion of borrowingsProvisionsEmployee benefitsSuperannuation

Non-current liabilitiesPayablesBorrowingsProvisionsEmployee BenefitsSuperannuationTotal Liabilities (∑)

LIABILITIES

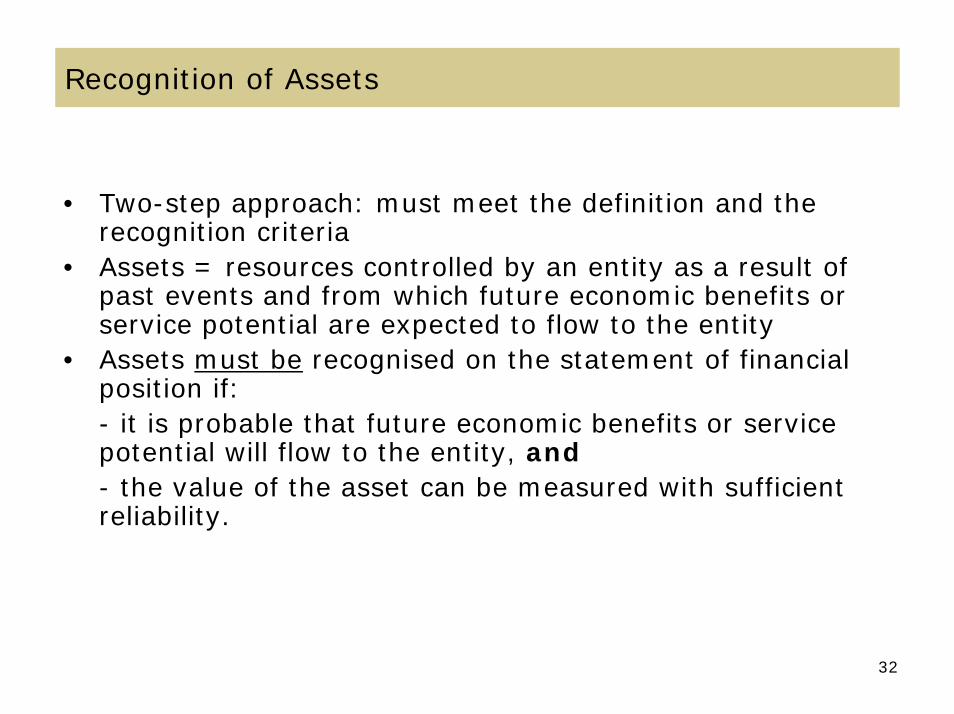

Recognition of Assets

• Two-step approach: must meet the definition and therecognition criteria

• Assets = resources controlled by an entity as a result of past events and from which future economic benefits orservice potential are expected to flow to the entity

• Assets must be recognised on the statement of financialposition if:- it is probable that future economic benefits or servicepotential will flow to the entity, and- the value of the asset can be measured with sufficientreliability.

32

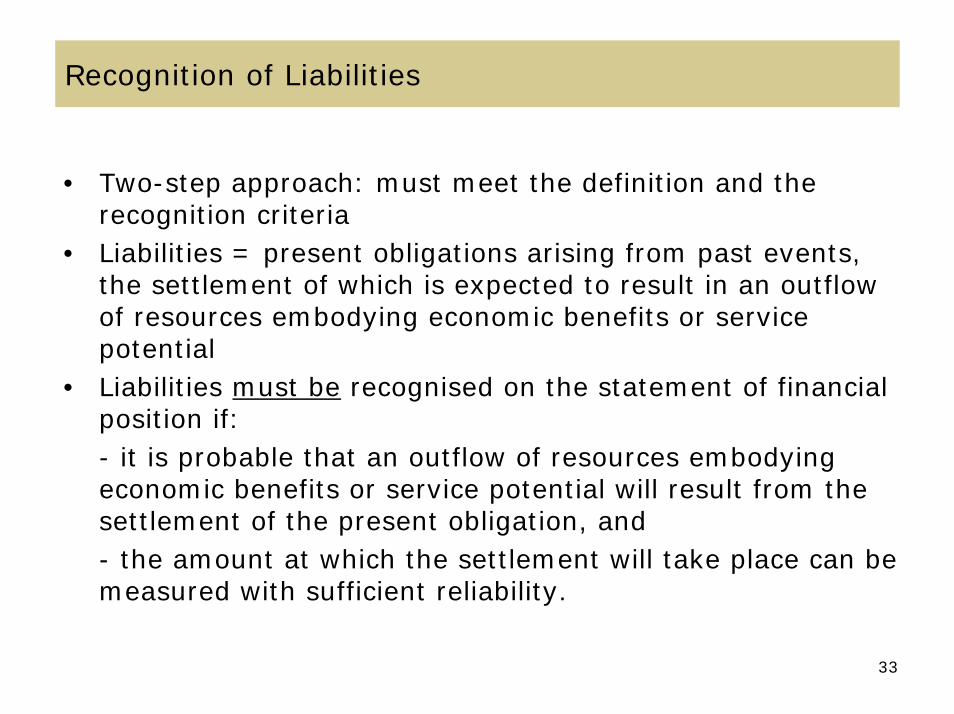

Recognition of Liabilities

• Two-step approach: must meet the definition and therecognition criteria

• Liabilities = present obligations arising from past events, the settlement of which is expected to result in an outflowof resources embodying economic benefits or servicepotential

• Liabilities must be recognised on the statement of financialposition if:- it is probable that an outflow of resources embodyingeconomic benefits or service potential will result from thesettlement of the present obligation, and- the amount at which the settlement will take place can bemeasured with sufficient reliability.

33

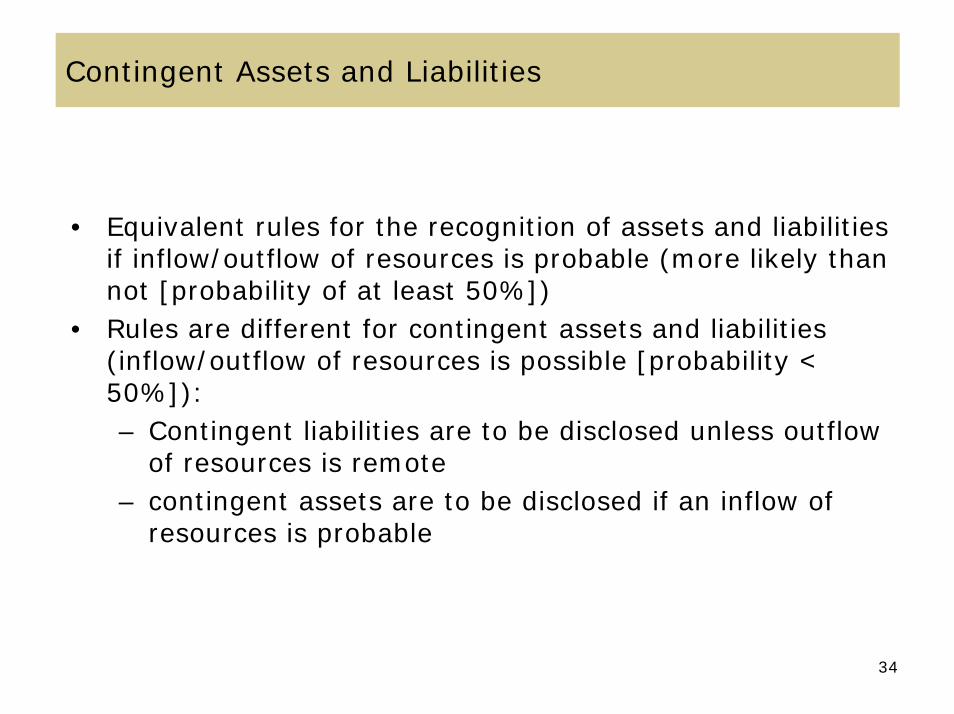

Contingent Assets and Liabilities

• Equivalent rules for the recognition of assets and liabilitiesif inflow/outflow of resources is probable (more likely thannot [probability of at least 50%])

• Rules are different for contingent assets and liabilities(inflow/outflow of resources is possible [probability < 50%]):– Contingent liabilities are to be disclosed unless outflow

of resources is remote– contingent assets are to be disclosed if an inflow of

resources is probable

34

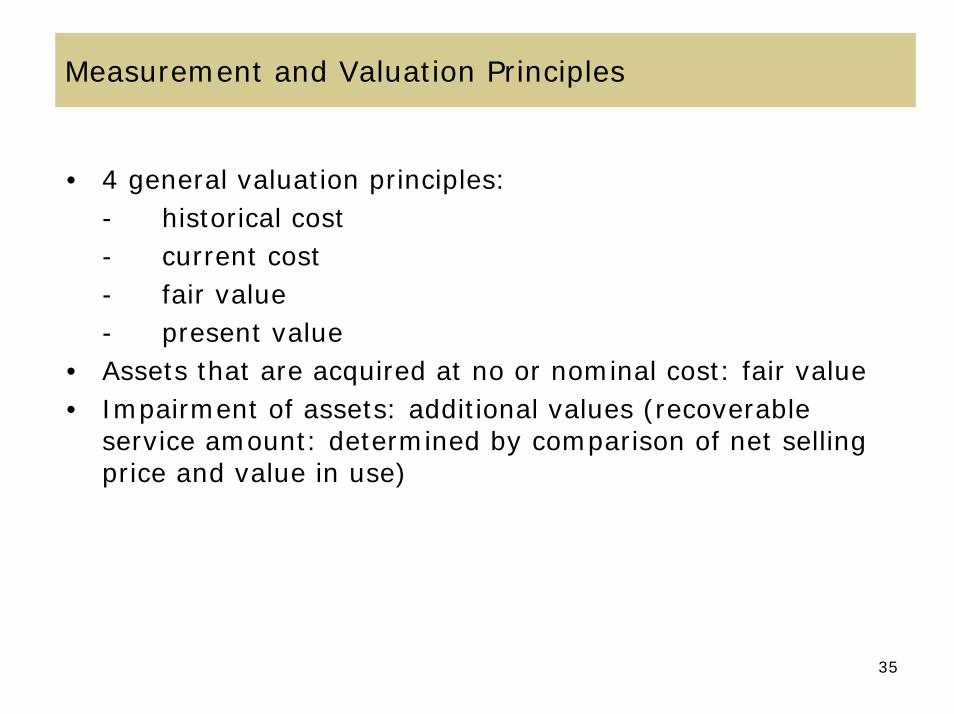

Measurement and Valuation Principles

• 4 general valuation principles:- historical cost- current cost- fair value- present value

• Assets that are acquired at no or nominal cost: fair value• Impairment of assets: additional values (recoverable

service amount: determined by comparison of net sellingprice and value in use)

35

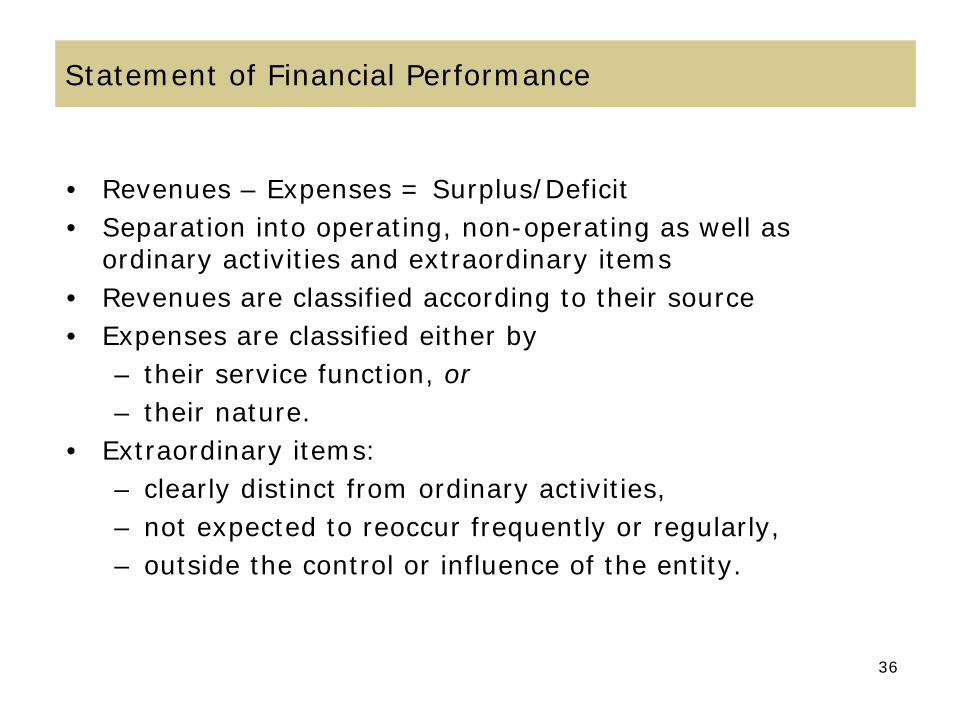

Statement of Financial Performance

• Revenues – Expenses = Surplus/Deficit• Separation into operating, non-operating as well as

ordinary activities and extraordinary items• Revenues are classified according to their source• Expenses are classified either by

– their service function, or– their nature.

• Extraordinary items:– clearly distinct from ordinary activities,– not expected to reoccur frequently or regularly,– outside the control or influence of the entity.

36

37

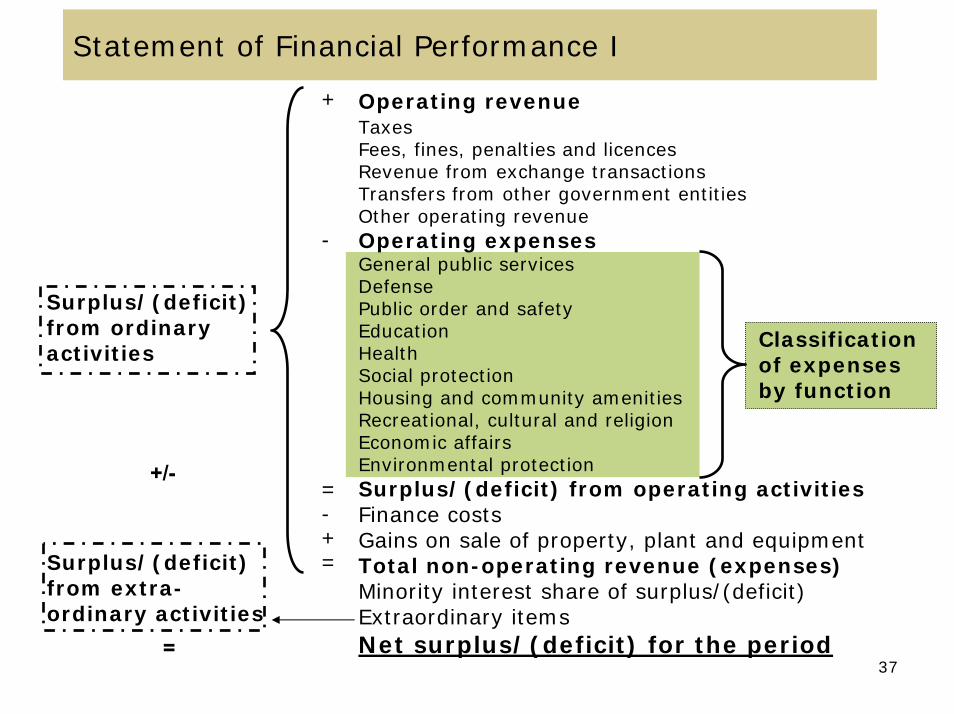

Statement of Financial Performance I

Operating revenueTaxesFees, fines, penalties and licencesRevenue from exchange transactionsTransfers from other government entitiesOther operating revenueOperating expensesGeneral public servicesDefensePublic order and safetyEducationHealthSocial protectionHousing and community amenitiesRecreational, cultural and religionEconomic affairsEnvironmental protectionSurplus/(deficit) from operating activitiesFinance costsGains on sale of property, plant and equipmentTotal non-operating revenue (expenses)Minority interest share of surplus/(deficit)Extraordinary itemsNet surplus/(deficit) for the period

+

-

=-+=

Surplus/(deficit) from ordinaryactivities

Surplus/(deficit) from extra-ordinary activities

+/-

=

Classificationof expensesby function

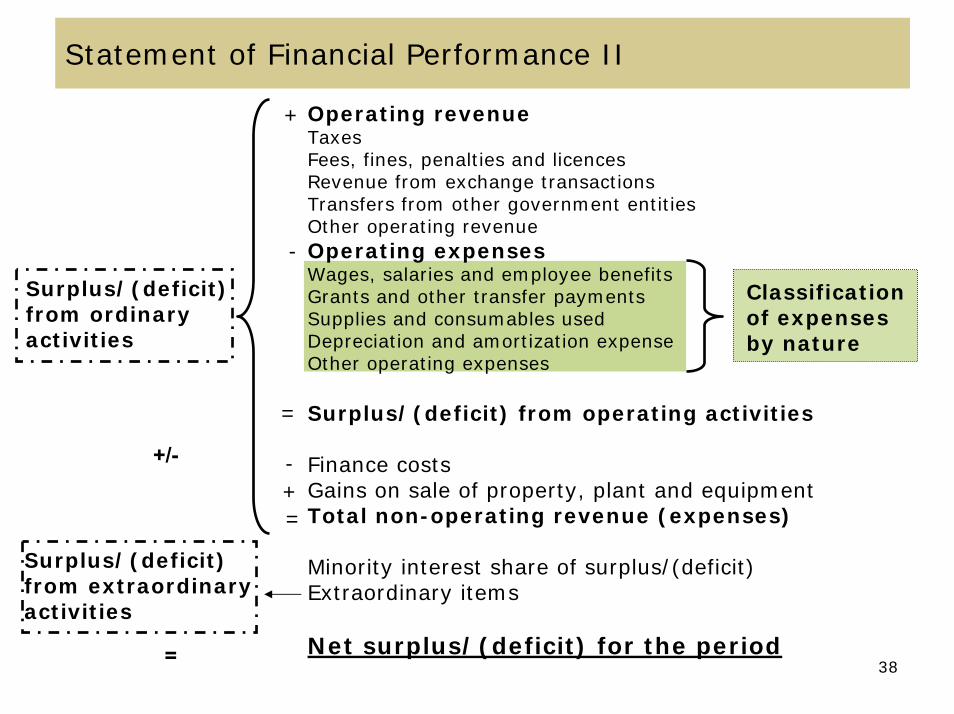

Statement of Financial Performance II

38

Operating revenueTaxesFees, fines, penalties and licencesRevenue from exchange transactionsTransfers from other government entitiesOther operating revenueOperating expensesWages, salaries and employee benefitsGrants and other transfer paymentsSupplies and consumables usedDepreciation and amortization expenseOther operating expenses

Surplus/(deficit) from operating activities

Finance costsGains on sale of property, plant and equipmentTotal non-operating revenue (expenses)

Minority interest share of surplus/(deficit)Extraordinary items

Net surplus/(deficit) for the period

+

Surplus/(deficit) from ordinaryactivities

Surplus/(deficit) from extraordinaryactivities

+/-

=

Classificationof expensesby nature

-

=

-+=

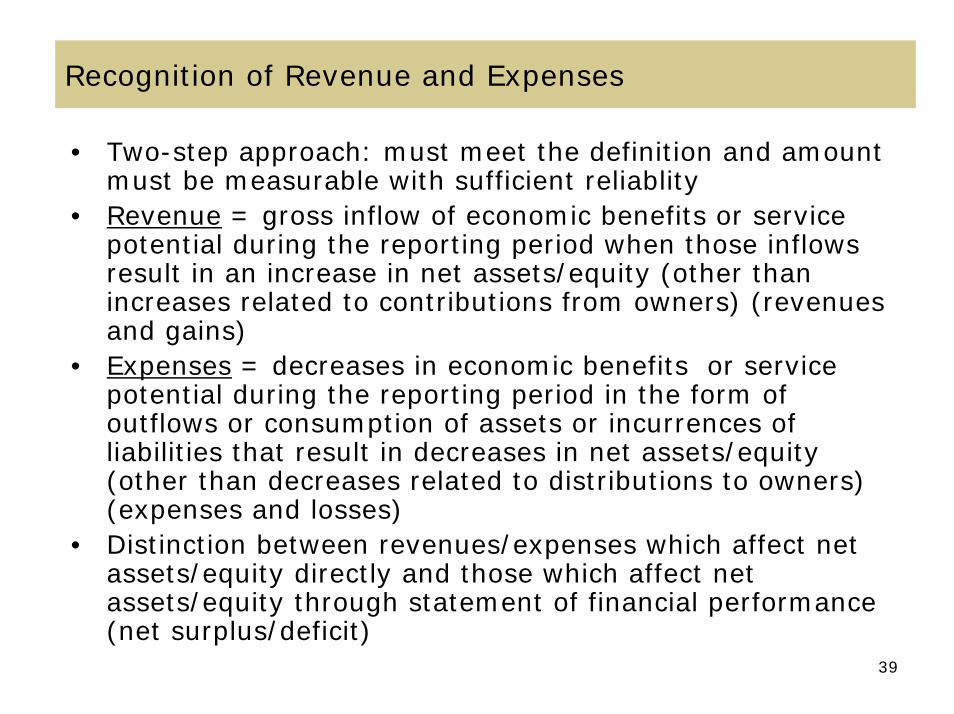

Recognition of Revenue and Expenses

• Two-step approach: must meet the definition and amountmust be measurable with sufficient reliablity

• Revenue = gross inflow of economic benefits or servicepotential during the reporting period when those inflowsresult in an increase in net assets/equity (other thanincreases related to contributions from owners) (revenuesand gains)

• Expenses = decreases in economic benefits or servicepotential during the reporting period in the form of outflows or consumption of assets or incurrences of liabilities that result in decreases in net assets/equity(other than decreases related to distributions to owners) (expenses and losses)

• Distinction between revenues/expenses which affect netassets/equity directly and those which affect netassets/equity through statement of financial performance(net surplus/deficit)

39

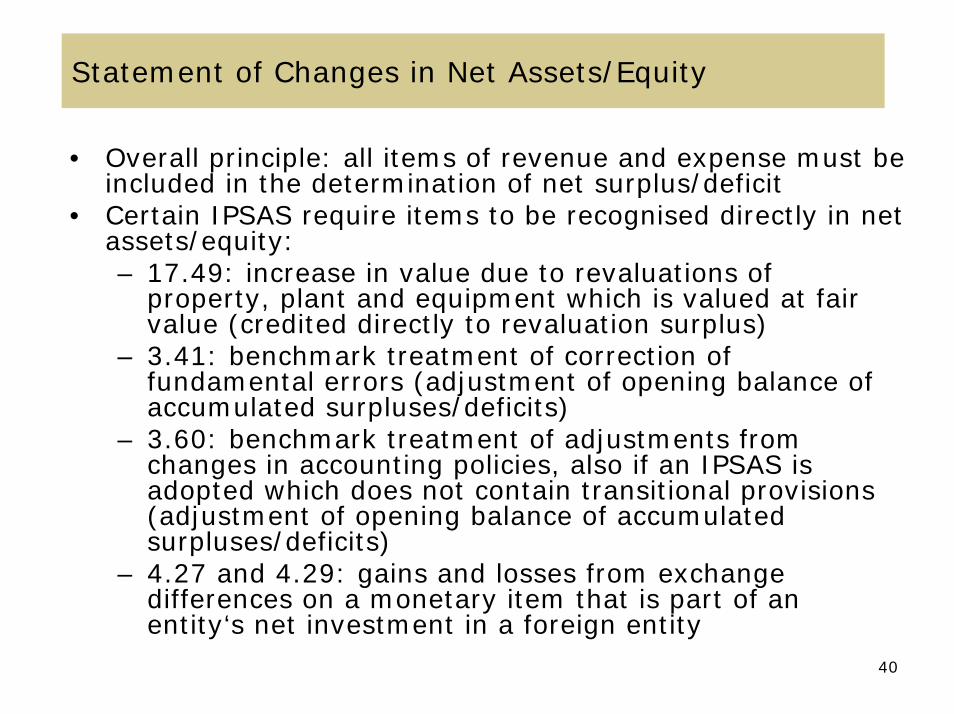

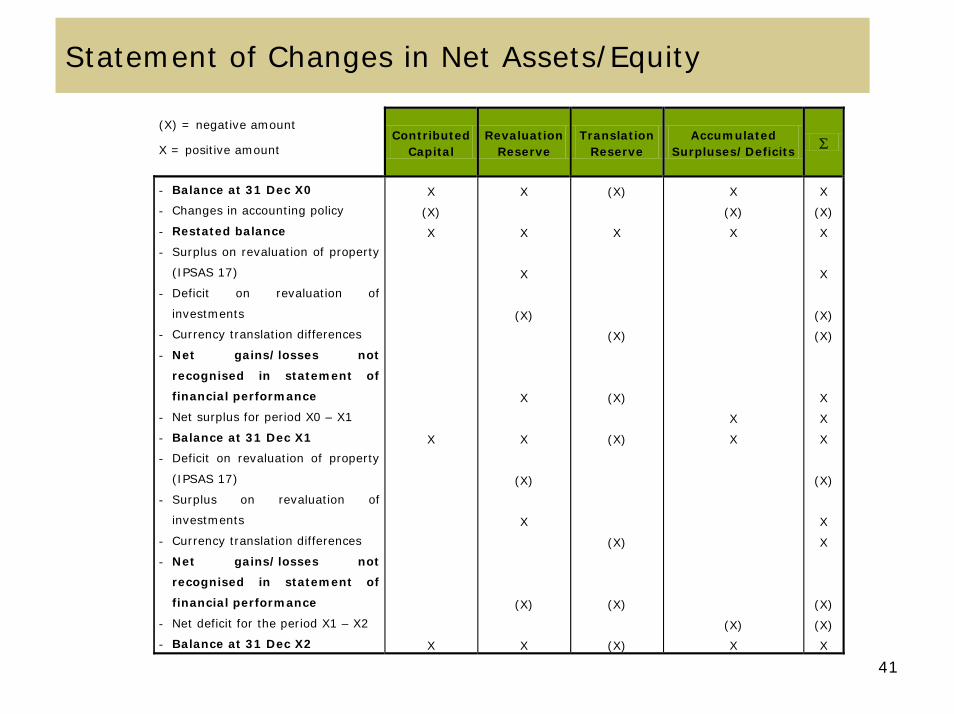

Statement of Changes in Net Assets/Equity

• Overall principle: all items of revenue and expense must beincluded in the determination of net surplus/deficit

• Certain IPSAS require items to be recognised directly in netassets/equity:– 17.49: increase in value due to revaluations of

property, plant and equipment which is valued at fair value (credited directly to revaluation surplus)

– 3.41: benchmark treatment of correction of fundamental errors (adjustment of opening balance of accumulated surpluses/deficits)

– 3.60: benchmark treatment of adjustments fromchanges in accounting policies, also if an IPSAS isadopted which does not contain transitional provisions(adjustment of opening balance of accumulatedsurpluses/deficits)

– 4.27 and 4.29: gains and losses from exchangedifferences on a monetary item that is part of an entity‘s net investment in a foreign entity

40

Statement of Changes in Net Assets/Equity

(X) = negative amount

X = positive amount Contributed

Capital Revaluation

Reserve Translation

Reserve Accumulated

Surpluses/Deficits ∑

- Balance at 31 Dec X0

- Changes in accounting policy

- Restated balance

- Surplus on revaluation of property

(IPSAS 17)

- Deficit on revaluation of

investments

- Currency translation differences

- Net gains/losses not

recognised in statement of

financial performance

- Net surplus for period X0 – X1

- Balance at 31 Dec X1

- Deficit on revaluation of property

(IPSAS 17)

- Surplus on revaluation of

investments

- Currency translation differences

- Net gains/losses not

recognised in statement of

financial performance

- Net deficit for the period X1 – X2

- Balance at 31 Dec X2

X

(X)

X

X

X

X

X

X

(X)

X

X

(X)

X

(X)

X

(X)

X

(X)

(X)

(X)

(X)

(X)

(X)

X

(X)

X

X

X

(X)

X

X

(X)

X

X

(X)

(X)

X

X

X

(X)

X

X

(X)

(X)

X

41

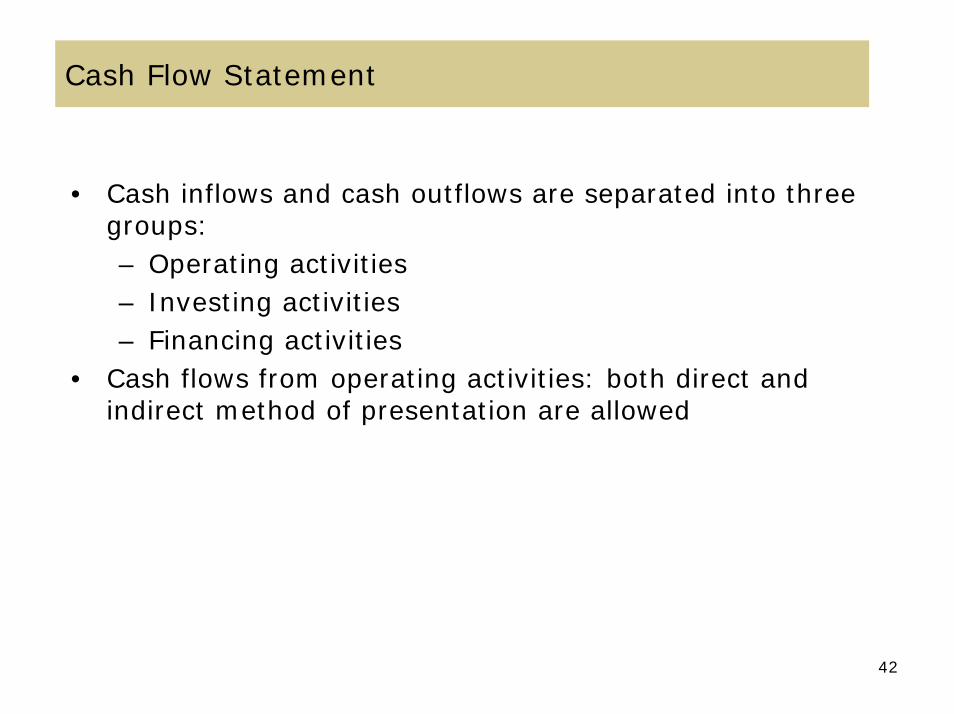

Cash Flow Statement

• Cash inflows and cash outflows are separated into threegroups:– Operating activities– Investing activities– Financing activities

• Cash flows from operating activities: both direct and indirect method of presentation are allowed

42

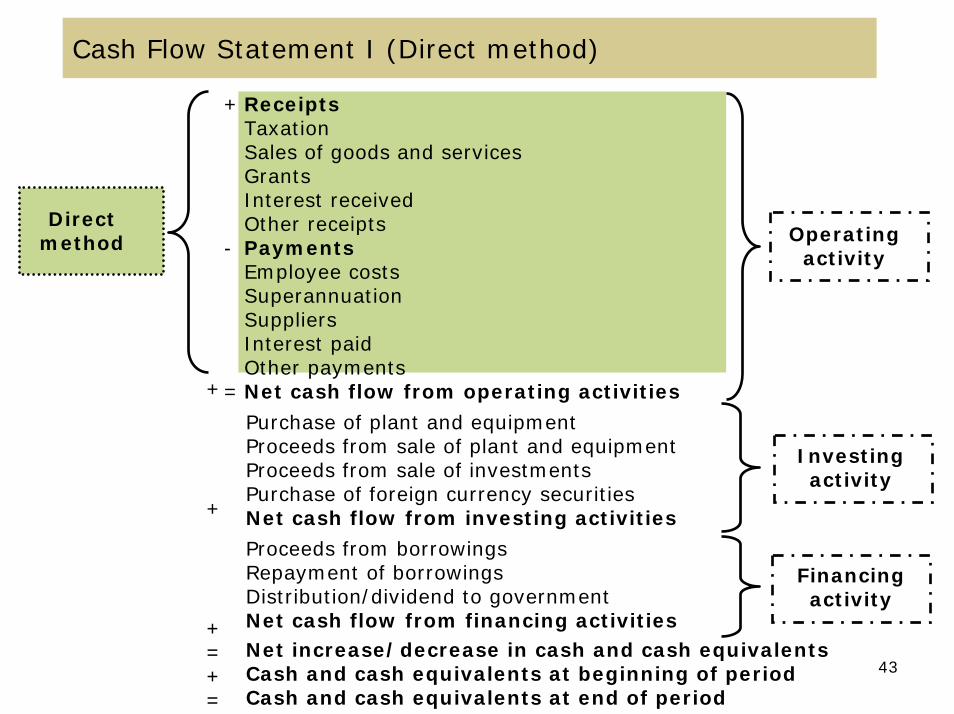

Cash Flow Statement I (Direct method)

43

+

-

=

Operatingactivity

ReceiptsTaxationSales of goods and servicesGrantsInterest receivedOther receiptsPaymentsEmployee costsSuperannuationSuppliersInterest paidOther paymentsNet cash flow from operating activities

Investingactivity

Purchase of plant and equipmentProceeds from sale of plant and equipmentProceeds from sale of investmentsPurchase of foreign currency securitiesNet cash flow from investing activities

Proceeds from borrowingsRepayment of borrowingsDistribution/dividend to governmentNet cash flow from financing activities

Financingactivity

Net increase/decrease in cash and cash equivalentsCash and cash equivalents at beginning of periodCash and cash equivalents at end of period

+

+

+=+=

Directmethod

44

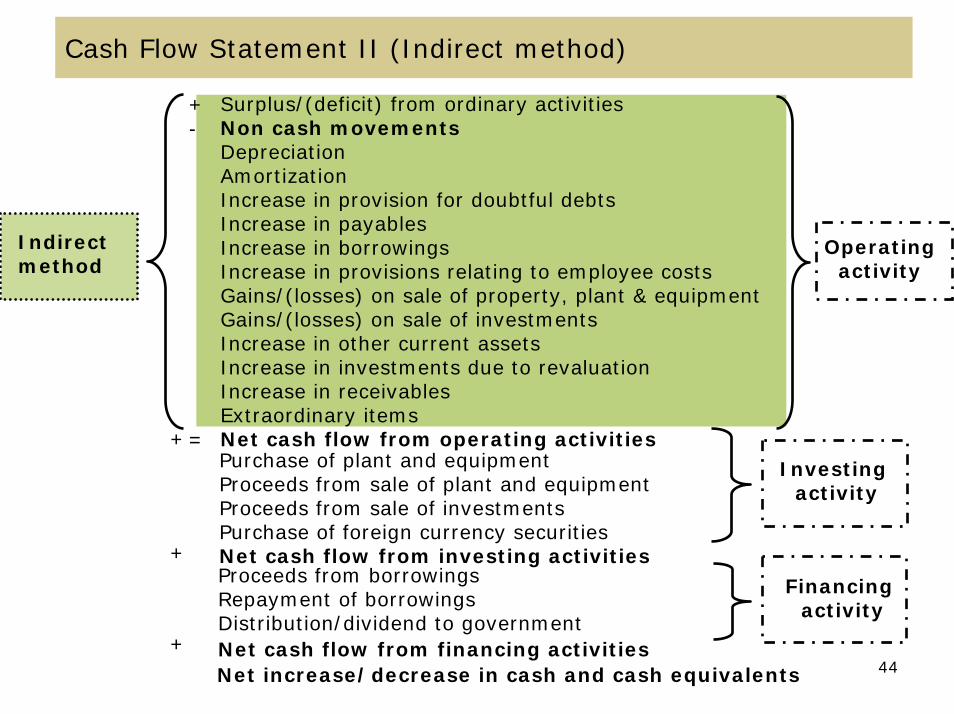

Cash Flow Statement II (Indirect method)

+-

=

Operatingactivity

Surplus/(deficit) from ordinary activitiesNon cash movementsDepreciationAmortizationIncrease in provision for doubtful debtsIncrease in payablesIncrease in borrowingsIncrease in provisions relating to employee costsGains/(losses) on sale of property, plant & equipmentGains/(losses) on sale of investmentsIncrease in other current assetsIncrease in investments due to revaluationIncrease in receivablesExtraordinary itemsNet cash flow from operating activities

Investingactivity

Purchase of plant and equipmentProceeds from sale of plant and equipmentProceeds from sale of investmentsPurchase of foreign currency securitiesNet cash flow from investing activitiesProceeds from borrowingsRepayment of borrowingsDistribution/dividend to governmentNet cash flow from financing activities

Financingactivity

+

+

+

Indirectmethod

Net increase/decrease in cash and cash equivalents

![Budgeting Process [Cost & Management Accounting]](https://img.pdfslide.us/doc/110x75/55a0b1d41a28ab6b5d8b45cf/budgeting-process-cost-management-accounting.jpg)