Embed Size (px)

Citation preview

PUBLIC HEARINGS ON LIQUID FUELS CHARTER

TRANSNET’S PRESENTATION TO THE PORTFOLIO COMMITTEE ON ENERGY AND THE SELECT COMMITTEE ON ECONOMIC DEVELOPMENT

15 SEPTEMBER 2010

AGENDA

BACKGROUND

ROLE OF TRANSNET IN FUEL SUPPLY AND LOGISTICS

EMPLOYMENT EQUITY

PROCUREMENT AND BROAD-BASED BLACK ECONOMIC EMPOWERMENT

ACCESS TO FACILITIES

WAYFORWARD

1

2

BACKGROUND

Transnet Limited (Transnet”) through its divisions Transnet National Ports Authority

(“TNPA”), Transnet Pipelines (“TPL”) and Transnet Freight Rail (“TFR”) is involved in

the handling (imports/exports), storage and transportation of petroleum products

throughout South Africa. Extensive transportation of fuel is however, also done by

road transport not controlled by Transnet.

Transnet’s involvement in the transportation of fuel is mainly in the C-zone area of

South Africa which sells more than 70% of all fuel used in the country.

The logistics and supply of fuel is complex and involves many role players:

SA Oil Industry (as producers/suppliers or importers of the fuel);

TNPA as owner and manager of eight commercial ports in South Africa;

TPL and TFR as transporters of petroleum products into the inland market;

Transporters including road haulage and coastal shipping;

Depot storage facilities; and

Customers in the form of oil companies.

BOTSWANA

Mossel Bay

FREE - STATE

SaldanhaBay

Cape Town

LESOTHO

WESTERNCAPE

Port Elizabeth

NAMIBIA

ZIMBABWE

Richards Bay

Durban

KWAZULU /NATAL

SishenMine

MOZAMBIQUE

MAPUTOSWAZILAND

Waterberg

MPUMALANGA

Beira

EXISTING GAS PIPELINEEXISTING PIPELINES (TRANSNET PIPELINES)

Kendal

ANORTHERNCAPE

EASTERNCAPE

BA

Sasolburg

Johannesburg

Secunda

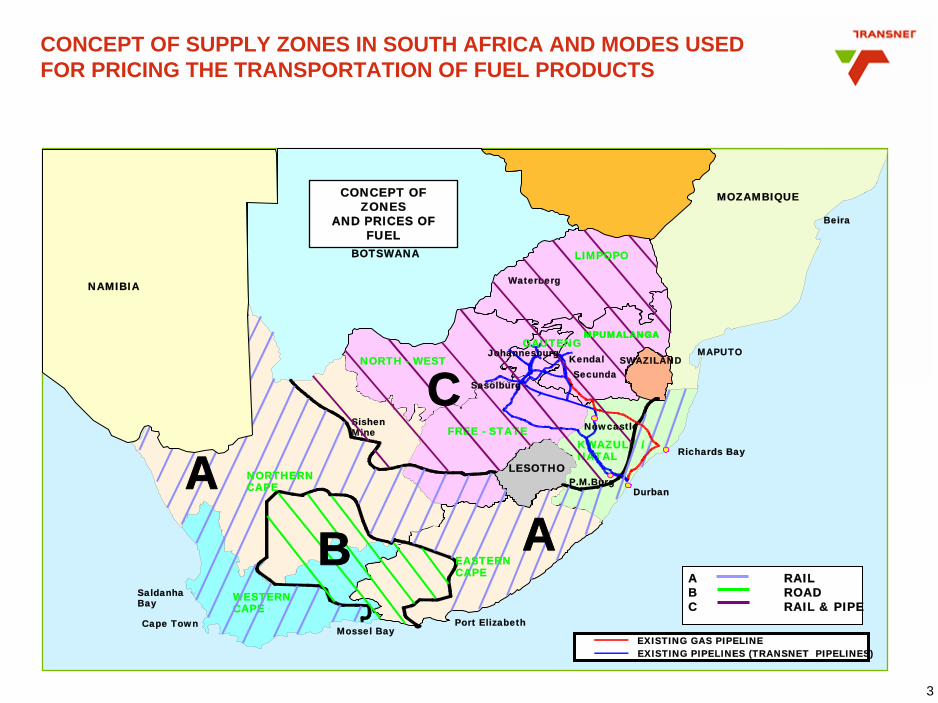

A RAILB ROADC RAIL & PIPE

GAUTENGMPUMALANGA

NORTH - WEST

CP.M.Burg

Newcastle

CONCEPT OF ZONES

AND PRICES OF FUEL

NAMIBIA

LIMPOPO

CONCEPT OF SUPPLY ZONES IN SOUTH AFRICA AND MODES USED FOR PRICING THE TRANSPORTATION OF FUEL PRODUCTS

3

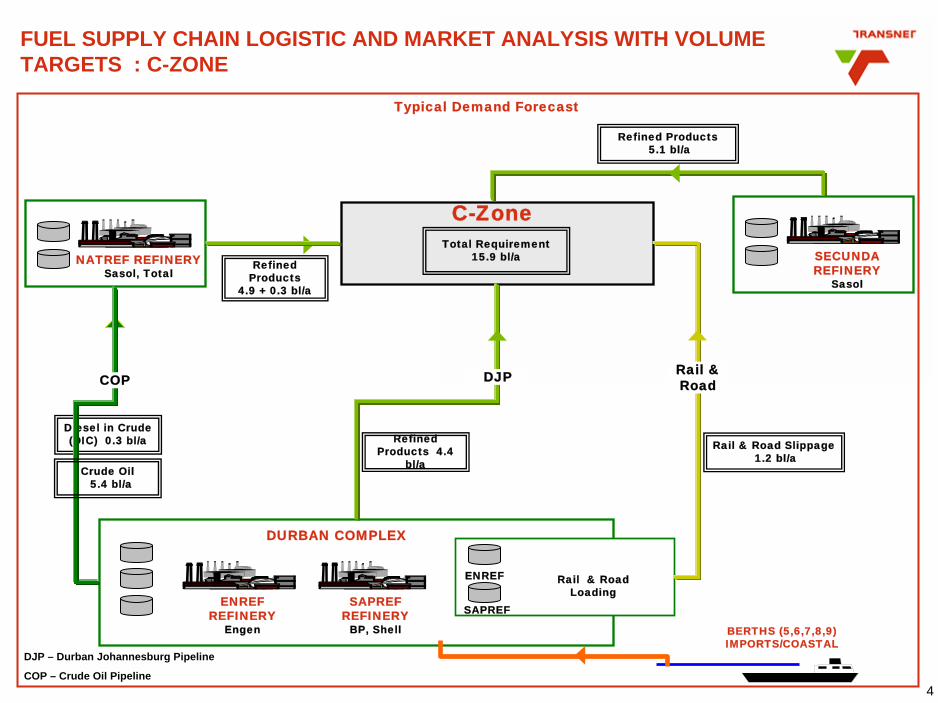

FUEL SUPPLY CHAIN LOGISTIC AND MARKET ANALYSIS WITH VOLUME TARGETS : C-ZONE

Typical Demand Forecast

C-Zone

ENREF REFINERY

Engen

DURBAN COMPLEX

ENREF

SAPREF

Rail & Road Loading

BERTHS (5,6,7,8,9)IMPORTS/COASTAL

Total Requirement15.9 bl/a

Rail & Road Slippage1.2 bl/a

Refined Products

4.9 + 0.3 bl/a

SAPREF REFINERY

BP, Shell

Refined Products 4.4

bl/a

Diesel in Crude (DIC) 0.3 bl/a

DJP

SECUNDA REFINERY

Sasol

NATREF REFINERYSasol, Total

Crude Oil5.4 bl/a

COPRail & Road

Refined Products5.1 bl/a

DJP – Durban Johannesburg Pipeline

COP – Crude Oil Pipeline4

5

LIQUID FUELS CHARTER

Transnet supports policy objectives for sustainable presence, ownership or control by

historically disadvantaged South Africans on all facets of the liquid fuels industry as stated in

the Energy Policy White Paper.

Transnet has endeavoured to make a meaningful contribution in the following areas of the

Liquid Fuels Charter:

Skills development;

Employment Equity;

Procurement; and

Access to facilities.

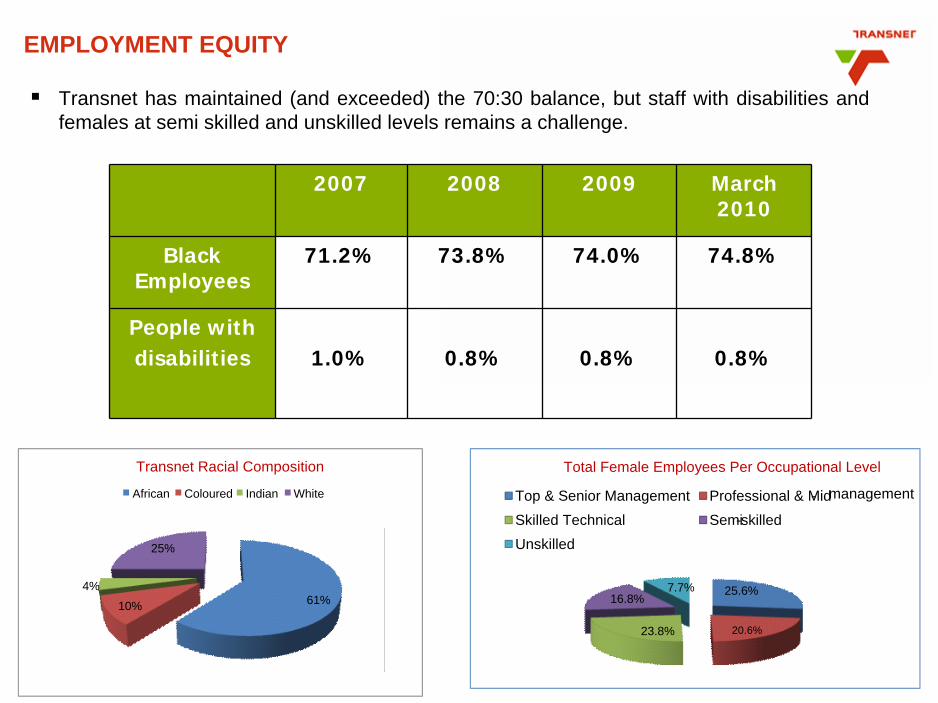

EMPLOYMENT EQUITY

2007 2008 2009 March 2010

Black Employees

71.2% 73.8% 74.0% 74.8%

People with disabilities 1.0% 0.8% 0.8% 0.8%

61%10%

4%

25%

Transnet Racial Composition

African Coloured Indian White

25.6%

20.6%23.8%

16.8%7.7%

Total Female Employees Per Occupational Level

Top & Senior Management Professional & Mid- management

Skilled Technical Semi-skilled Unskilled

Transnet has maintained (and exceeded) the 70:30 balance, but staff with disabilities and females at semi skilled and unskilled levels remains a challenge.

7

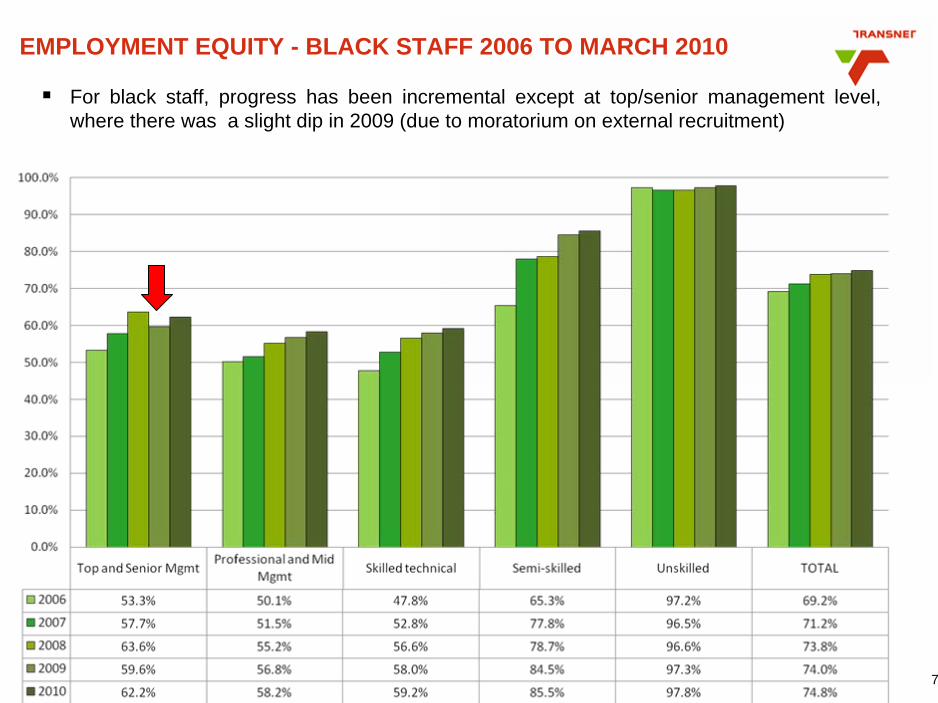

EMPLOYMENT EQUITY - BLACK STAFF 2006 TO MARCH 2010

For black staff, progress has been incremental except at top/senior management level, where there was a slight dip in 2009 (due to moratorium on external recruitment)

8

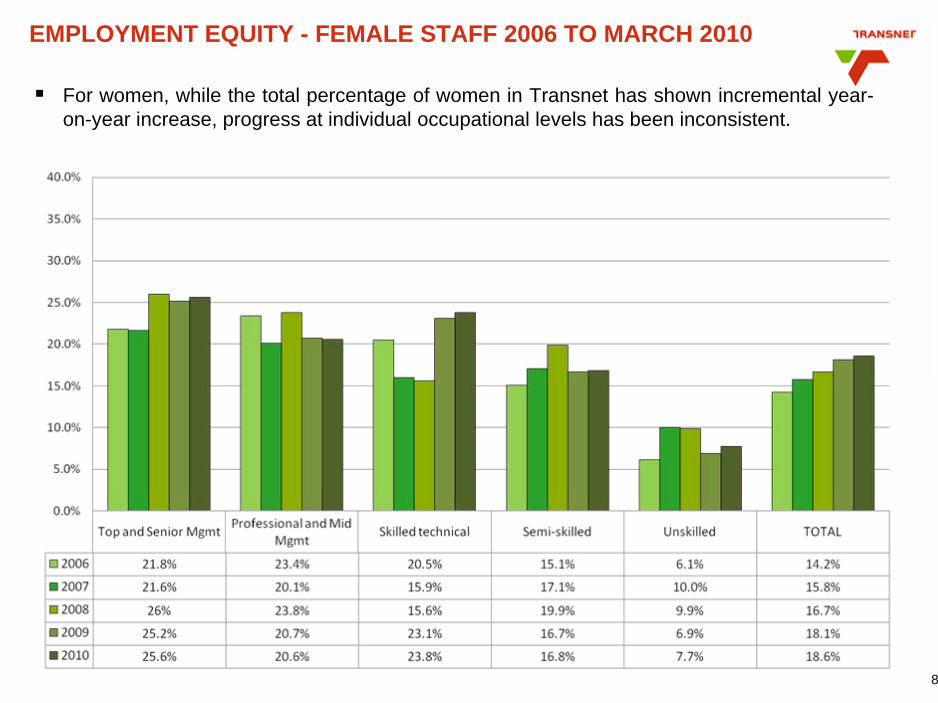

EMPLOYMENT EQUITY - FEMALE STAFF 2006 TO MARCH 2010

For women, while the total percentage of women in Transnet has shown incremental year-on-year increase, progress at individual occupational levels has been inconsistent.

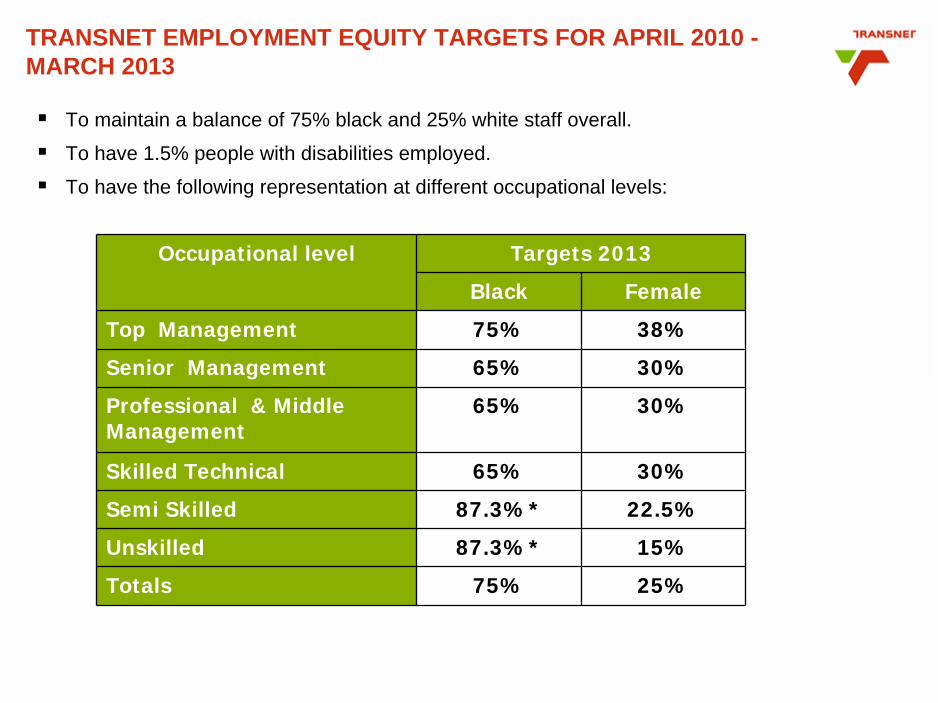

TRANSNET EMPLOYMENT EQUITY TARGETS FOR APRIL 2010 - MARCH 2013

To maintain a balance of 75% black and 25% white staff overall.

To have 1.5% people with disabilities employed.

To have the following representation at different occupational levels:

Occupational level Targets 2013

Black Female

Top Management 75% 38%

Senior Management 65% 30%

Professional & Middle Management

65% 30%

Skilled Technical 65% 30%

Semi Skilled 87.3%* 22.5%

Unskilled 87.3%* 15%

Totals 75% 25%

10

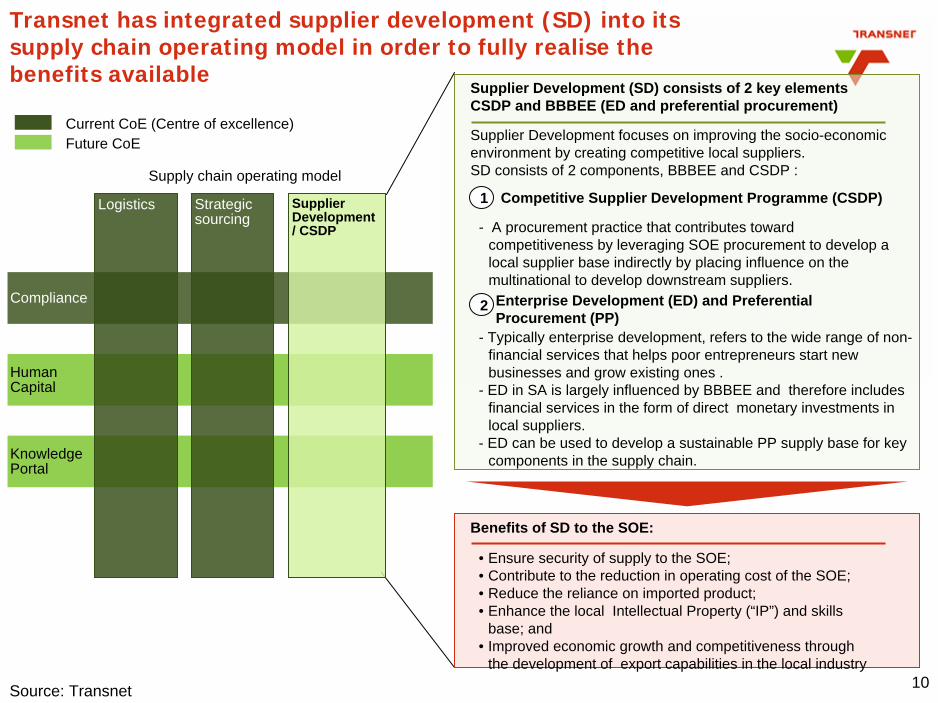

- A procurement practice that contributes toward competitiveness by leveraging SOE procurement to develop a local supplier base indirectly by placing influence on the multinational to develop downstream suppliers.

Compliance

Human Capital

Knowledge Portal

Supplier Development / CSDP

Logistics Strategic sourcing

Supplier Development (SD) consists of 2 key elements CSDP and BBBEE (ED and preferential procurement)

1

2

Supplier Development focuses on improving the socio-economic environment by creating competitive local suppliers. SD consists of 2 components, BBBEE and CSDP :

Enterprise Development (ED) and Preferential Procurement (PP)

Competitive Supplier Development Programme (CSDP)

Benefits of SD to the SOE:

- Typically enterprise development, refers to the wide range of non- financial services that helps poor entrepreneurs start new businesses and grow existing ones .

- ED in SA is largely influenced by BBBEE and therefore includes financial services in the form of direct monetary investments in local suppliers.

- ED can be used to develop a sustainable PP supply base for key components in the supply chain.

• Ensure security of supply to the SOE;• Contribute to the reduction in operating cost of the SOE;• Reduce the reliance on imported product;• Enhance the local Intellectual Property (“IP”) and skills

base; and• Improved economic growth and competitiveness through

the development of export capabilities in the local industry

Future CoECurrent CoE (Centre of excellence)

Source: Transnet

Transnet has integrated supplier development (SD) into its supply chain operating model in order to fully realise the benefits available

Supply chain operating model

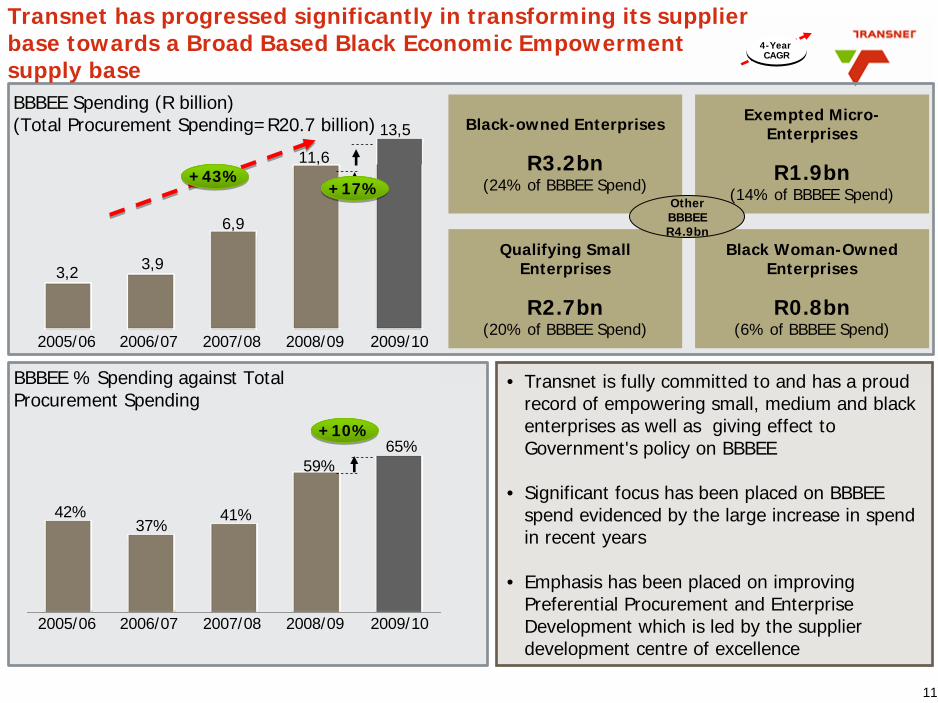

Transnet has progressed significantly in transforming its supplier base towards a Broad Based Black Economic Empowerment supply base

11

65%59%

41%37%

42%

+10%+10%

BBBEE % Spending against Total Procurement Spending

BBBEE Spending (R billion)(Total Procurement Spending=R20.7 billion) 13,5

11,6

6,9

3,93,2

+17%+17%+43%+43%

• Transnet is fully committed to and has a proud record of empowering small, medium and black enterprises as well as giving effect to Government's policy on BBBEE

• Significant focus has been placed on BBBEE spend evidenced by the large increase in spend in recent years

• Emphasis has been placed on improving Preferential Procurement and Enterprise Development which is led by the supplier development centre of excellence

4-Year CAGR

4-Year CAGR

2009/102008/092007/082006/072005/06

2009/102008/092007/082006/072005/06

Black-owned Enterprises

R3.2bn (24% of BBBEE Spend)

Black Woman-Owned Enterprises

R0.8bn (6% of BBBEE Spend)

Qualifying Small Enterprises

R2.7bn (20% of BBBEE Spend)

Exempted Micro- Enterprises

R1.9bn (14% of BBBEE Spend)Other

BBBEER4.9bn

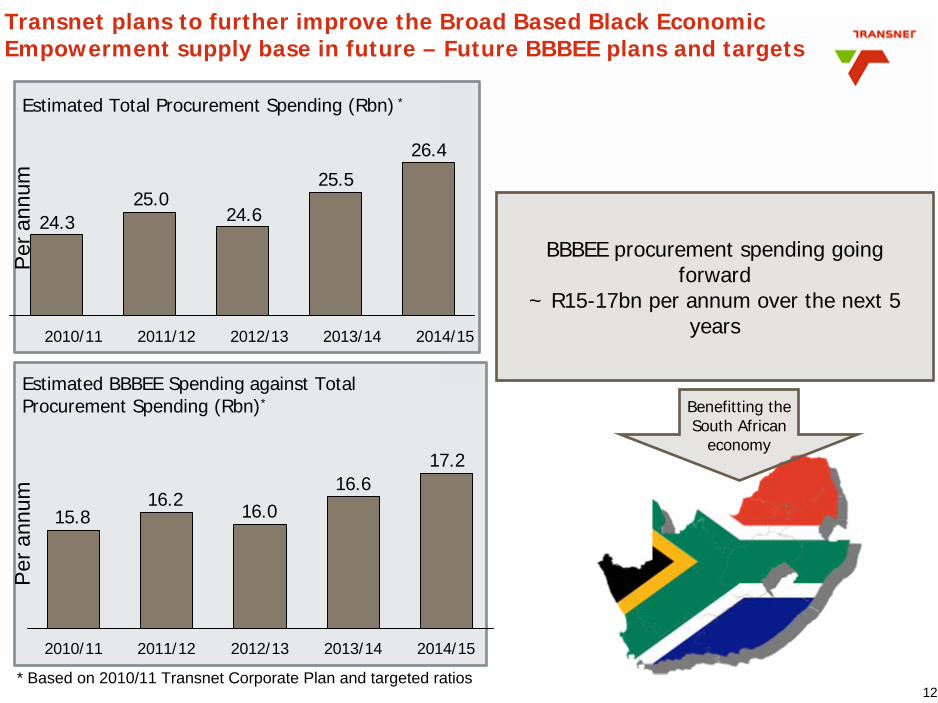

Transnet plans to further improve the Broad Based Black Economic Empowerment supply base in future – Future BBBEE plans and targets

12

Estimated BBBEE Spending against Total Procurement Spending (Rbn)*

Estimated Total Procurement Spending (Rbn) *

BBBEE procurement spending going forward

~ R15-17bn per annum over the next 5 years

26.4

25.5

24.625.0

24.3

2014/152013/142012/132011/122010/11

17.216.6

16.016.2

15.8

2014/152013/142012/132011/122010/11

Per

ann

umP

er a

nnum

Benefitting the South African

economy

* Based on 2010/11 Transnet Corporate Plan and targeted ratios

13

ACCESS TO FACILITIES - PIPELINESThe Charter for South African Petroleum and Liquid Fuels Industry provides that owners of facilities such as

SBM’s, pipelines, depots and storage tanks “provide third parties with non-discriminatory access to

uncommitted capacity”. Transnet recognises this as critical to the economic development and prosperity of

our country. Furthermore, as a responsible corporate citizen and an organ of state, Transnet attempts to

comply with all statutory requirements.

One of the objects of the of the Petroleum Pipelines Act (PPA), Act No. 60, 2003, Section 2(d) is to “promote

equitable access to petroleum pipelines, loading facilities and storage facilities”.

Another, Section 2(g) is to “promote companies in the petroleum pipeline industry that are owned or

controlled by historically disadvantaged South Africans, by means of licence conditions to enable them to

become competitive’.

The powers and the duties of the authority (NERSA), Section 4(g) includes “monitor and take appropriate

action, if necessary, to ensure that access to petroleum pipelines, loading facilities and storage facilities is

provided in a non-discriminatory, fair and transparent manner”.

Transnet Pipelines believes that it complies with the PPA and operates under the “the common carrier”

principle, giving effect to Section 20(g) of the PPA, which states that “shipper’s of petroleum must have

access to petroleum pipelines and a pipelines capacity must be shared among all users and prospective

users thereof in proportion to their needs and within the commercially reasonable and operational constraints

of the pipeline, ….”.

14

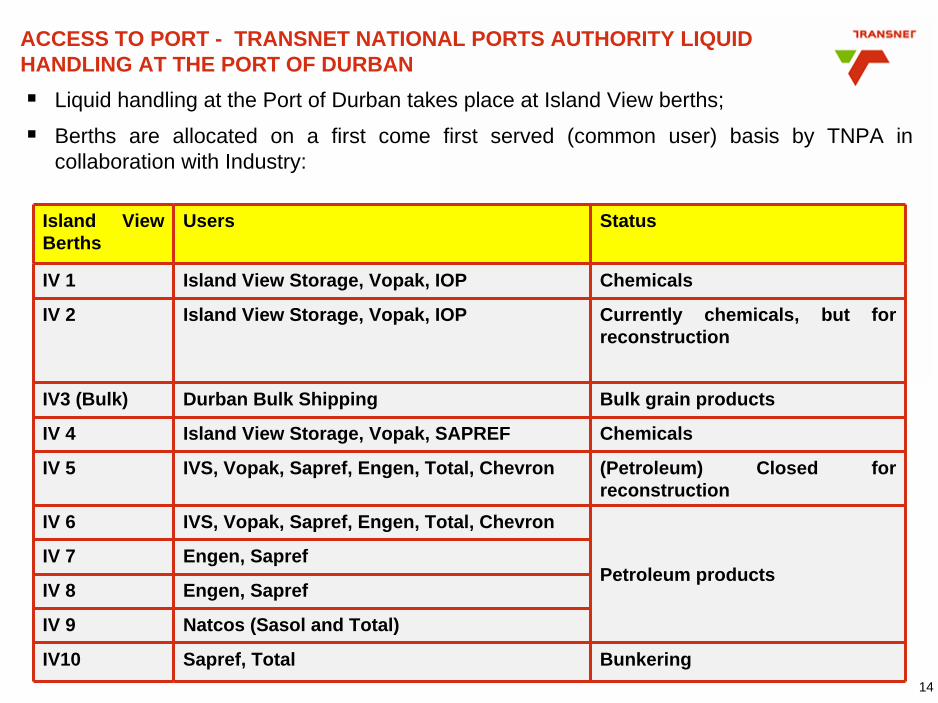

Liquid handling at the Port of Durban takes place at Island View berths;

Berths are allocated on a first come first served (common user) basis by TNPA in collaboration with Industry:

Island View Berths

Users Status

IV 1 Island View Storage, Vopak, IOP Chemicals

IV 2 Island View Storage, Vopak, IOP Currently chemicals, but for reconstruction

IV3 (Bulk) Durban Bulk Shipping Bulk grain products

IV 4 Island View Storage, Vopak, SAPREF Chemicals

IV 5 IVS, Vopak, Sapref, Engen, Total, Chevron (Petroleum) Closed for reconstruction

IV 6 IVS, Vopak, Sapref, Engen, Total, Chevron

Petroleum productsIV 7 Engen, Sapref

IV 8 Engen, Sapref

IV 9 Natcos (Sasol and Total)

IV10 Sapref, Total Bunkering

ACCESS TO PORT - TRANSNET NATIONAL PORTS AUTHORITY LIQUID HANDLING AT THE PORT OF DURBAN

IV1

IV2

IV3

IV4

IV5

IV6

IV7

IV8

IV9

Bunker Berth (IV10)

15

16

ACCESS TO FACILITIES – PORT

Port Infrastructure provided at the South African Commercial ports consists of common-user

berths, the provision of marine services (pilots, tug assistance and berthing services) to all

vessels calling at the SA ports and availability of land on which liquid handling and storage

facilities are constructed;

All vessels have equal access to marine services and liquid bulk berths at the ports are

allocated to vessels on a first-come first served bases (allocation happens via Industry);

Common-user berths are available for use by terminals who has pipeline connections between

the berth and the terminal – access to berths are constrained if a potential interested party

does not have access to land and a liquid handling/storage facility;

Island View is saturated for space, except for Lot 100 (Castrol lease expired)

The environmental sensitivity of liquid terminals also leads to more stringent approvals to be

able to construct and operate a facility;

When land becomes available for new liquid handling terminal facilities, TNPA follows an open

tender process to allocate land to new terminal operators;

All tender processes will provide for BBBEE targets as per the Port Regulations (Sections 2/3)

17

ACCESS TO FACILITIES - PORTSection 80(1)(a) of the National Ports Act, 2005 (Act No. 12 of 2005) (“the Ports Act”) provides

that the Minister of Transport may, by notice in the Gazette, make regulations in respect of “a

framework for the economic participation and empowerment of historically disadvantaged

groups in port operations”.

The Ports Regulator has commissioned an economic review of participation in port operations

by public entities, private entities and public private partnerships as required by the Ports Act.

Transnet awaits the outcome and recommendations of this study.

TNPA is obliged under the Ports Act to annually submit a Broad-Based Black Economic

Empowerment (“BBBEE”) report to the Ports Regulator. The first report was submitted on 26

November 2008.

The objectives of this report is to outline to the Ports Regulator how the measures taken by the

Authority have enhanced access to and participation in ports services and port facilities by

black people in terms of Regulation 4(1).

Further, TNPA has requested the Ports Regulator to clarify its approach and understanding of

the interpretation of the Regulations.

18

ISLAND VIEW BERTH 6

Berth infrastructure is a logical extension of the terminal and not a separate business

All berths in Island View including Berth 6 are common user berths

Berth 6 part of Energy Security Master Plan initiatives supplying into the NMPP

Berth 6 failed and was reconstructed in 2006. Industry has a deemed right to the loading arms

on this berth. These were recommissioned by industry in 2009

Mandatory provision for a 5% HDSA Co-owner over and above BBBEE to invest in the loading

arms. Operator (SAPREF) has appointed a transaction advisor

TNPA oversight role and review periods apply

ACCESS TO FACILITIES - PORT

19

WAY FORWARD

TNPA is mandated with an oversight role for all Port tenants. A deemed licence conversion

process and current lease commercialisation processes incorporate regulatory prescription of

minimum level 4 BBBEE within 3 years.

Harmonise the role of various regulators that come to bear on HDSA participation.

Focus initiatives on identification of storage (tankage) opportunities for HDSAs.

Consideration by the Minister of Transport of Section 79 directive to “restrict” tenders for land in

Island View (Lot 100 available and Chevron site available in 2015)

Fast track environmental approvals with Department of Environmental Affairs (DEA)

TPL to facilitate access to the New Multi-Product Pipeline (NMPP) where possible.