Embed Size (px)

Citation preview

NOMBRE DEL DEPARTAMENTO 1

Public finances and inflation:

the case of Spain

PRELIMINARY WORK

Javier J. Pérez (Banco de España)

Joint work with S. Hurtado, F. Martí, and P. Hernández

This presentation does not necessarily reflect the opinions of the Banco de

España or the Eurosystem

Departamento de Coyuntura y

Previsión Económica

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

2

Overview

Implications of a low inflation environment for…

Fiscal consolidation (some accounting examples)

PUBLIC DEBT: The consolidation episode of the 1990s vs now

PUBLIC SPENDING: impact of measures in a low-inflation framework

PUBLIC REVENUE: limits to tax collection

Some simulations using Bank of Spain’s MTBE

INFLATION SHOCKS: inspecting the channels - oil prices, profit margins

Medium-term fiscal sustainability safeguards

PENSION SUSTAINABILITY: the “revaluation index”

Departamento de Coyuntura y

Previsión Económica

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

3

Overview

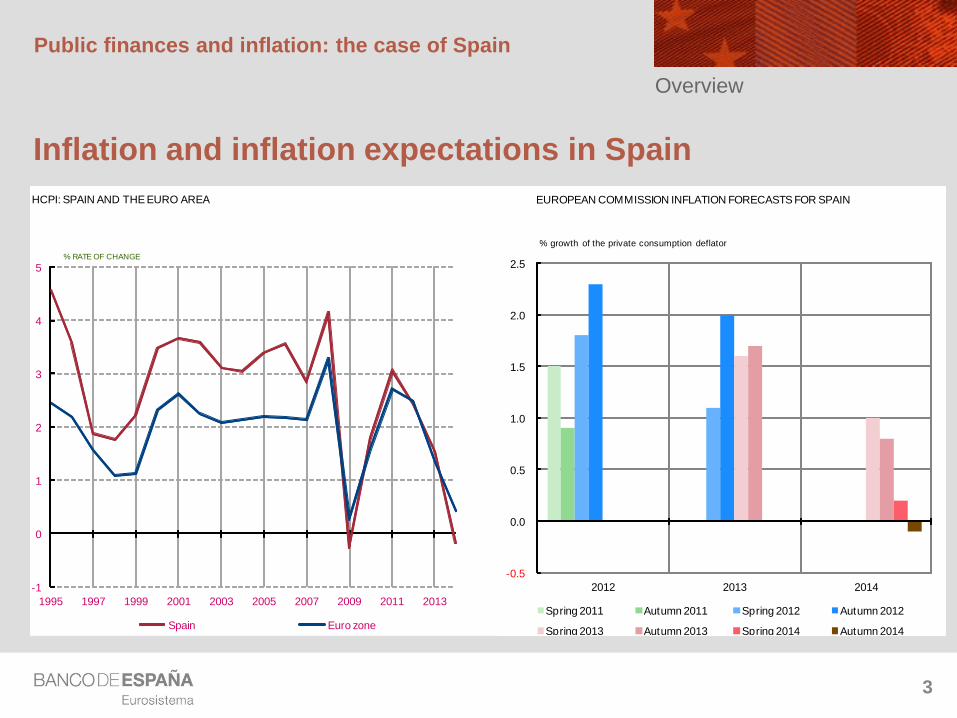

Inflation and inflation expectations in Spain

Departamento de Coyuntura y

Previsión Económica

HCPI: SPAIN AND THE EURO AREA

-1

0

1

2

3

4

5

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Spain Euro zone

% RATE OF CHANGE

SOURCE: Noational Statistics Institute

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2012 2013 2014

Spring 2011 Autumn 2011 Spring 2012 Autumn 2012

Spring 2013 Autumn 2013 Spring 2014 Autumn 2014

% growth of the private consumption deflator

EUROPEAN COMMISSION INFLATION FORECASTS FOR SPAIN

NOMBRE DEL DEPARTAMENTO

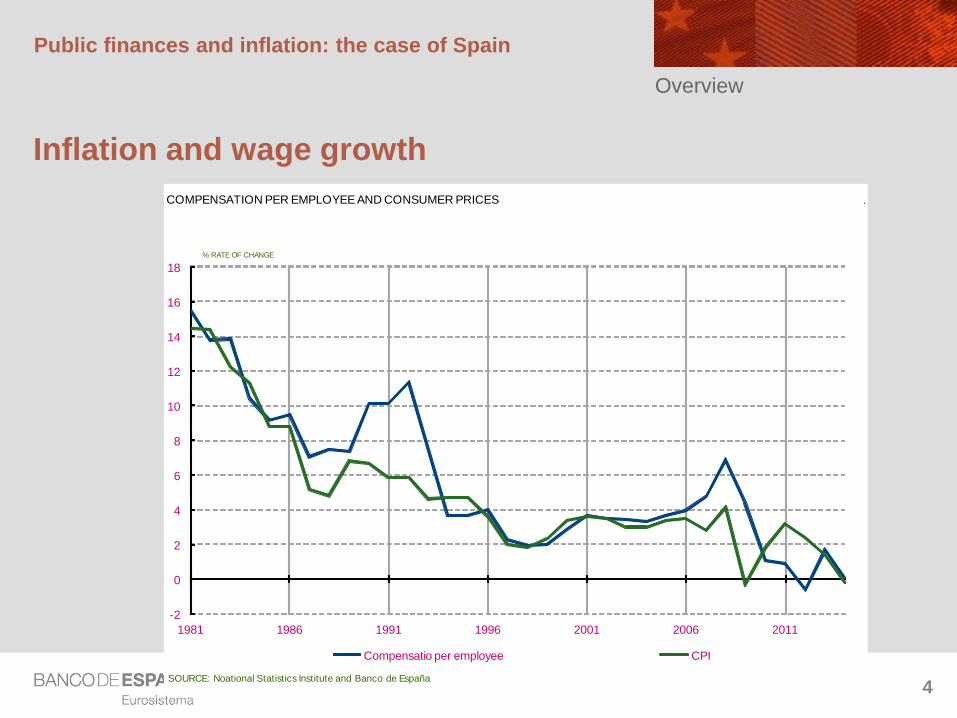

Inflation and wage growth

Public finances and inflation: the case of Spain

4Departamento de Coyuntura y

Previsión Económica

COMPENSATION PER EMPLOYEE AND CONSUMER PRICES .

-2

0

2

4

6

8

10

12

14

16

18

1981 1986 1991 1996 2001 2006 2011

Compensatio per employee CPI

% RATE OF CHANGE

SOURCE: Noational Statistics Institute and Banco de España

Overview

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

5

Fiscal consolidation

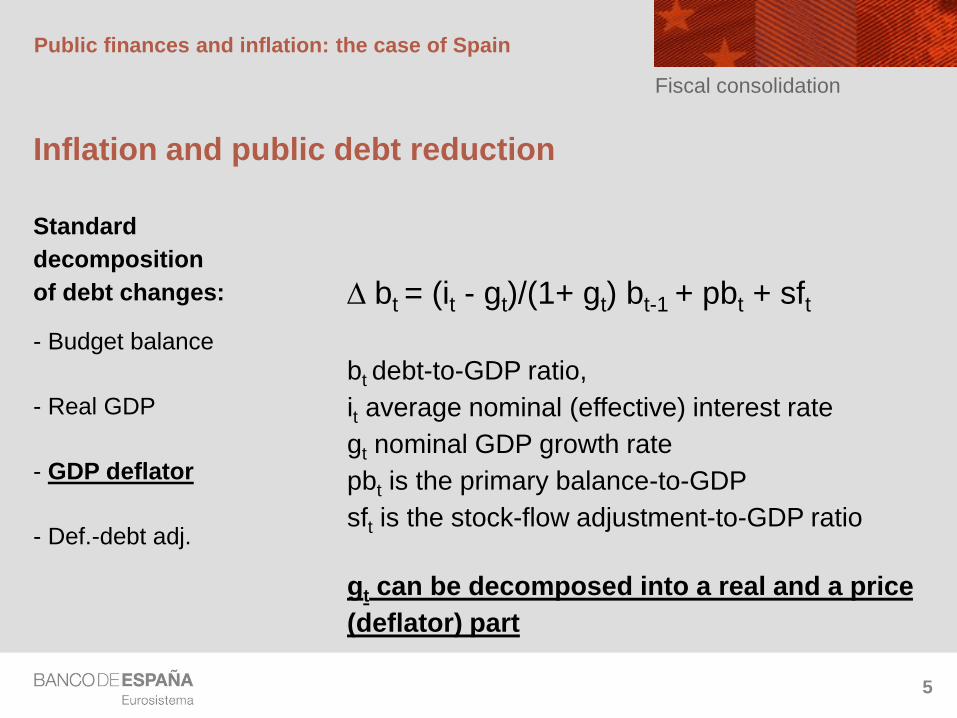

Inflation and public debt reduction

Standard

decomposition

of debt changes:

- Budget balance

- Real GDP

- GDP deflator

- Def.-debt adj.

Departamento de Coyuntura y

Previsión Económica

D bt = (it - gt)/(1+ gt) bt-1 + pbt + sft

bt debt-to-GDP ratio,

it average nominal (effective) interest rate

gt nominal GDP growth rate

pbt is the primary balance-to-GDP

sft is the stock-flow adjustment-to-GDP ratio

gt can be decomposed into a real and a price

(deflator) part

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

6

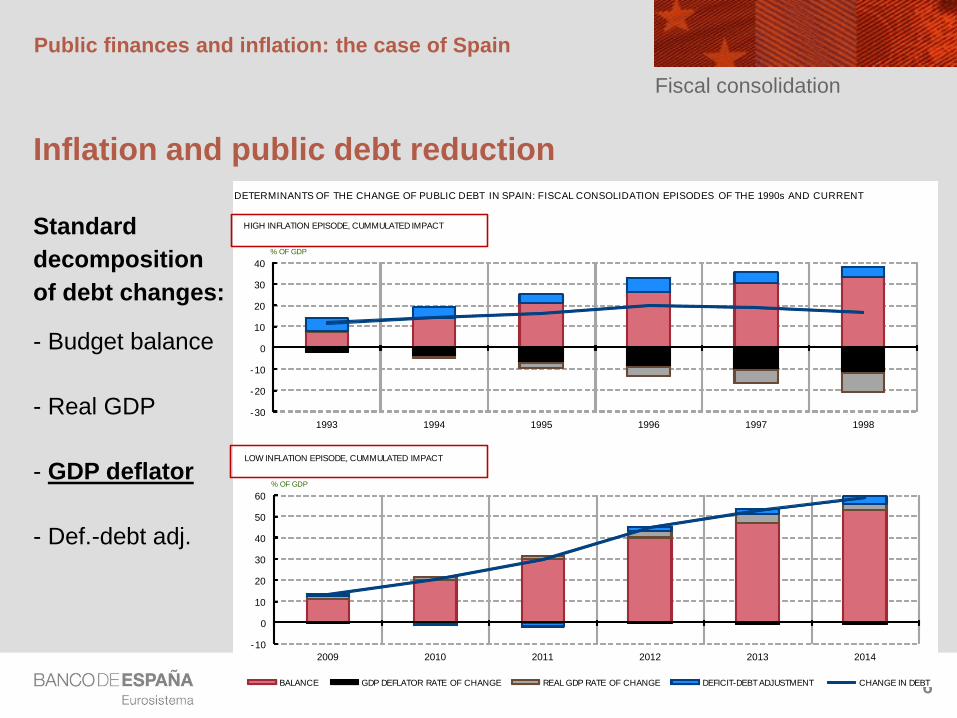

Fiscal consolidation

Inflation and public debt reduction

Standard

decomposition

of debt changes:

- Budget balance

- Real GDP

- GDP deflator

- Def.-debt adj.

Departamento de Coyuntura y

Previsión Económica

DETERMINANTS OF THE CHANGE OF PUBLIC DEBT IN SPAIN: FISCAL CONSOLIDATION EPISODES OF THE 1990s AND CURRENT

-10

0

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014

BALANCE GDP DEFLATOR RATE OF CHANGE REAL GDP RATE OF CHANGE DEFICIT-DEBT ADJUSTMENT CHANGE IN DEBT

LOW INFLATION EPISODE, CUMMULATED IMPACT

% OF GDP

-30

-20

-10

0

10

20

30

40

1993 1994 1995 1996 1997 1998

HIGH INFLATION EPISODE, CUMMULATED IMPACT

% OF GDP

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

7

Fiscal consolidation

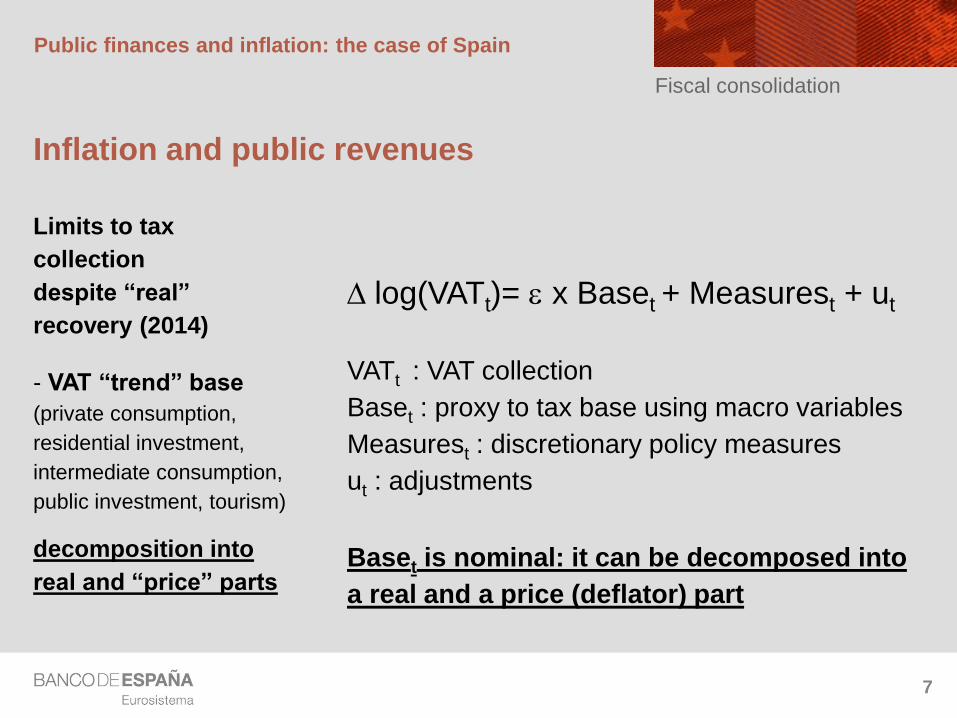

Inflation and public revenues

Limits to tax

collection

despite “real”

recovery (2014)

- VAT “trend” base

(private consumption,

residential investment,

intermediate consumption,

public investment, tourism)

decomposition into

real and “price” parts

Departamento de Coyuntura y

Previsión Económica

D log(VATt)= e x Baset + Measurest + ut

VATt : VAT collection

Baset : proxy to tax base using macro variables

Measurest : discretionary policy measures

ut : adjustments

Baset is nominal: it can be decomposed into

a real and a price (deflator) part

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

8

Fiscal consolidation

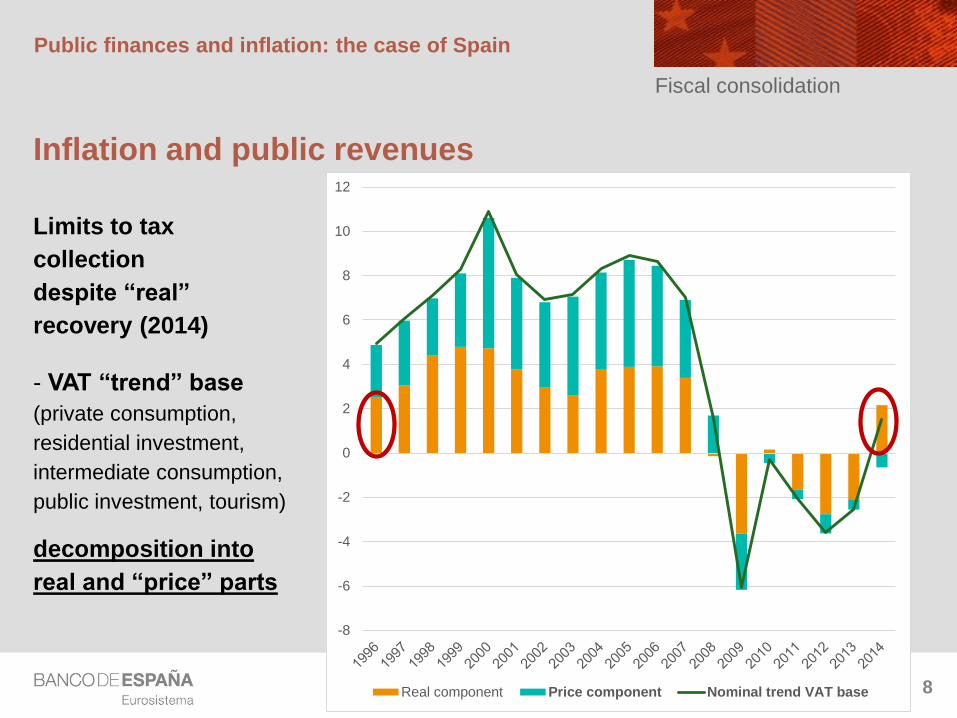

Inflation and public revenues

Limits to tax

collection

despite “real”

recovery (2014)

- VAT “trend” base

(private consumption,

residential investment,

intermediate consumption,

public investment, tourism)

decomposition into

real and “price” parts

Departamento de Coyuntura y

Previsión Económica

-8

-6

-4

-2

0

2

4

6

8

10

12

Real component Price component Nominal trend VAT base

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

9

Fiscal consolidation

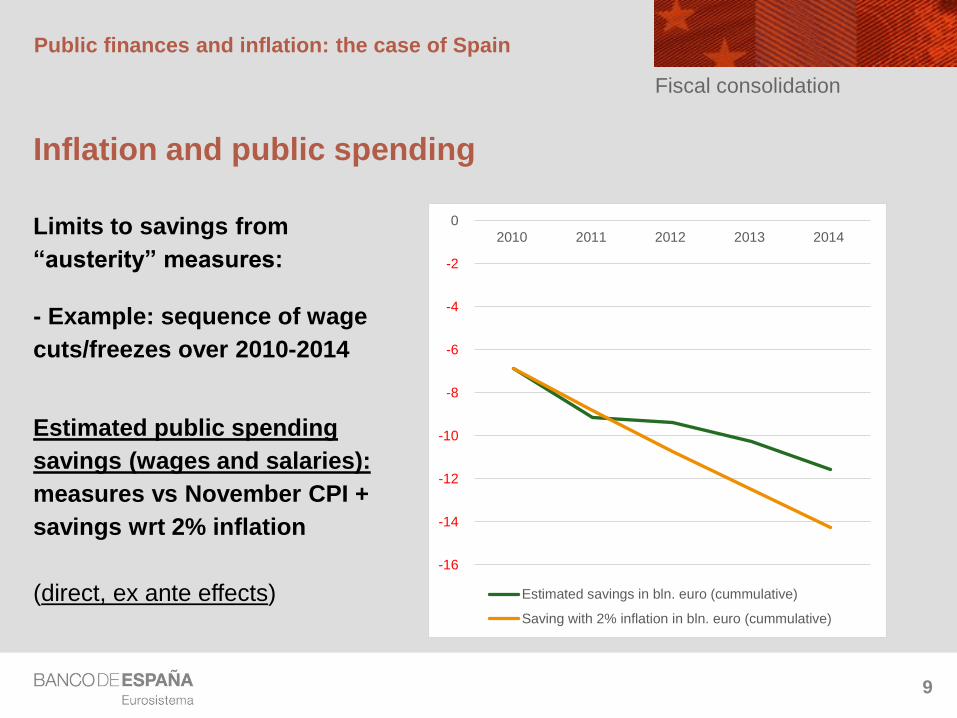

Inflation and public spending

Limits to savings from

“austerity” measures:

- Example: sequence of wage

cuts/freezes over 2010-2014

Estimated public spending

savings (wages and salaries):

measures vs November CPI +

savings wrt 2% inflation

(direct, ex ante effects)

Departamento de Coyuntura y

Previsión Económica

-16

-14

-12

-10

-8

-6

-4

-2

0

2010 2011 2012 2013 2014

Estimated savings in bln. euro (cummulative)

Saving with 2% inflation in bln. euro (cummulative)

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

10

Inflation shocks

Inflation shock

The source of the “inflation shock”is key

Oil price shock (10% reduction)

Margin shock (-1pp CPI non energy)

MTBE model – simulate response of

Private consumption deflator / Compensation per employee.

Real GDP / Real private consumption / Real private investment

Direct taxes to households (wages) / Indirect taxes / Public spending

Public deficit / Public debt

Public spending does not react but for: interest, U, other transfers Departamento de Coyuntura y

Previsión Económica

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

11

Inflation shocks

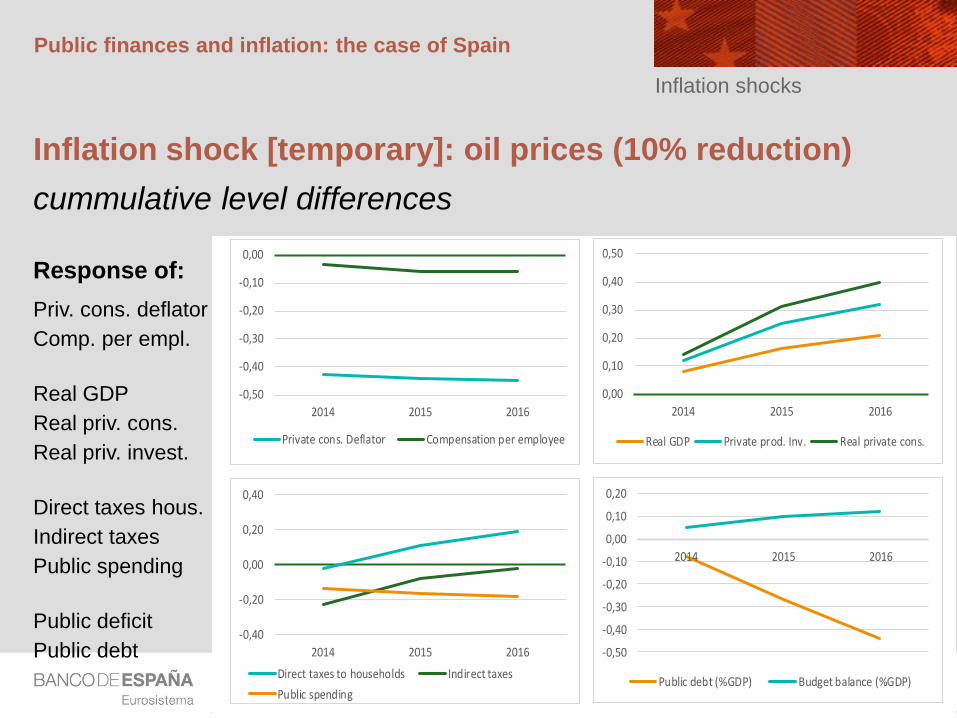

Inflation shock [temporary]: oil prices (10% reduction)

cummulative level differences

Response of:

Priv. cons. deflator

Comp. per empl.

Real GDP

Real priv. cons.

Real priv. invest.

Direct taxes hous.

Indirect taxes

Public spending

Public deficit

Public debtDepartamento de Coyuntura y

Previsión Económica

-0,50

-0,40

-0,30

-0,20

-0,10

0,00

2014 2015 2016

Private cons. Deflator Compensation per employee

0,00

0,10

0,20

0,30

0,40

0,50

2014 2015 2016

Real GDP Private prod. Inv. Real private cons.

-0,40

-0,20

0,00

0,20

0,40

2014 2015 2016

Direct taxes to households Indirect taxes

Public spending

-0,50

-0,40

-0,30

-0,20

-0,10

0,00

0,10

0,20

2014 2015 2016

Public debt (%GDP) Budget balance (%GDP)

NOMBRE DEL DEPARTAMENTO

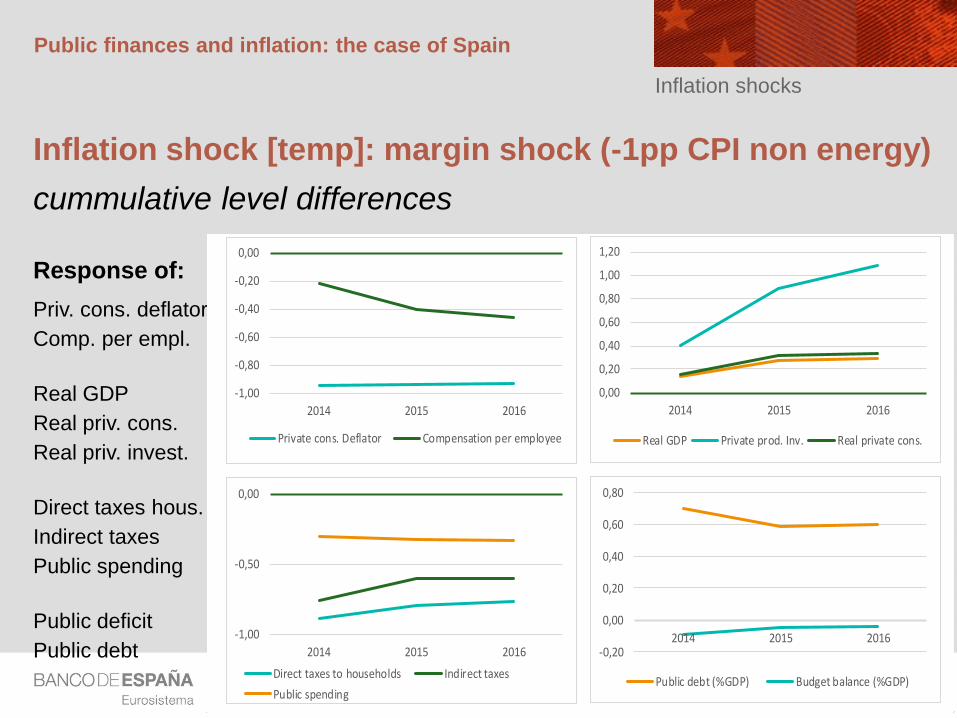

Inflation shock [temp]: margin shock (-1pp CPI non energy)

cummulative level differences

Response of:

Priv. cons. deflator

Comp. per empl.

Real GDP

Real priv. cons.

Real priv. invest.

Direct taxes hous.

Indirect taxes

Public spending

Public deficit

Public debt

Public finances and inflation: the case of Spain

12

Inflation shocks

Departamento de Coyuntura y

Previsión Económica

-1,00

-0,80

-0,60

-0,40

-0,20

0,00

2014 2015 2016

Private cons. Deflator Compensation per employee

0,00

0,20

0,40

0,60

0,80

1,00

1,20

2014 2015 2016

Real GDP Private prod. Inv. Real private cons.

-1,00

-0,50

0,00

2014 2015 2016

Direct taxes to households Indirect taxes

Public spending

-0,20

0,00

0,20

0,40

0,60

0,80

2014 2015 2016

Public debt (%GDP) Budget balance (%GDP)

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

13

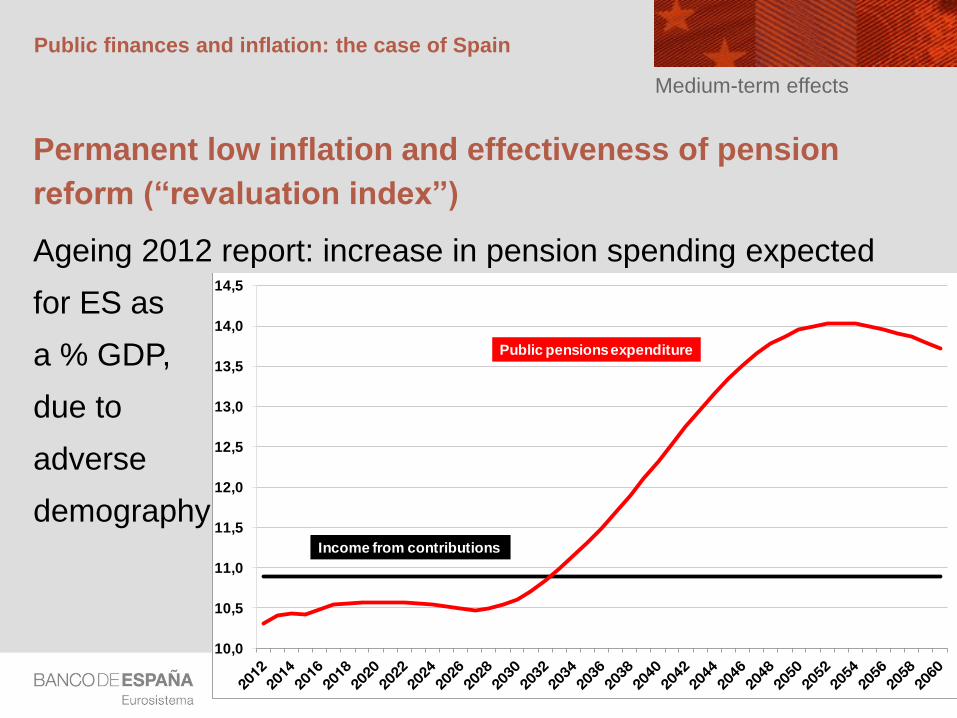

Medium-term effects

Permanent low inflation and effectiveness of pension

reform (“revaluation index”)

Ageing 2012 report: increase in pension spending expected

for ES as

a % GDP,

due to

adverse

demography

Departamento de Coyuntura y

Previsión Económica

10,0

10,5

11,0

11,5

12,0

12,5

13,0

13,5

14,0

14,5

Pension System Scenario 2012 Ageing Report(% of GDP)

Public pensions expenditure

Income from contributions

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

14

Medium-term effects

Permanent low inflation and effectiveness of pension

reform (“revaluation index”)

Reforms in 2011 and 2013. The 2013 one includes a

sustainability factor and a revaluation index

The revaluation index: The minimum and maximum

annual revaluation levels were set at 0.25% and the CPI

plus 0.5% respectively.

Pensions would grow above 0.25% only when the Social

Security System is, broadly speaking, in surplus (in

structural terms), and in line with fundamentalsDepartamento de Coyuntura y

Previsión Económica

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

15

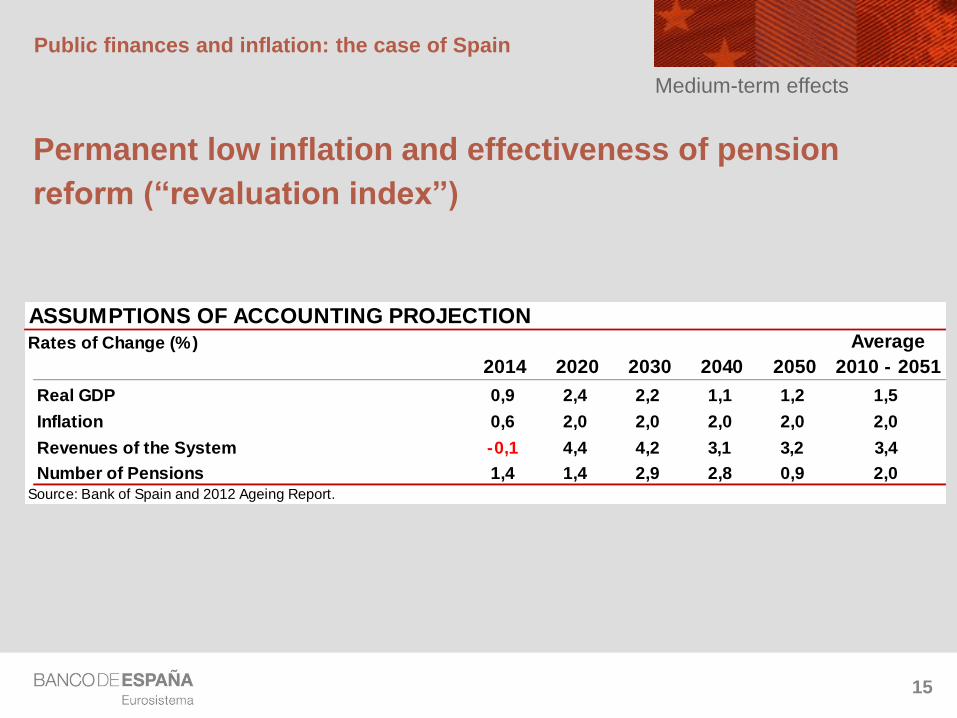

Medium-term effects

Permanent low inflation and effectiveness of pension

reform (“revaluation index”)

Departamento de Coyuntura y

Previsión Económica

ASSUMPTIONS OF ACCOUNTING PROJECTIONRates of Change (%) Average

2014 2020 2030 2040 2050 2010 - 2051

Real GDP 0,9 2,4 2,2 1,1 1,2 1,5

debido a:Inflation 0,6 2,0 2,0 2,0 2,0 2,0

- Tasa de variación de ingresosRevenues of the System -0,1 4,4 4,2 3,1 3,2 3,4

- Tasa de variación número de pensionistasNumber of Pensions 1,4 1,4 2,9 2,8 0,9 2,0Source: Bank of Spain and 2012 Ageing Report.

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

16

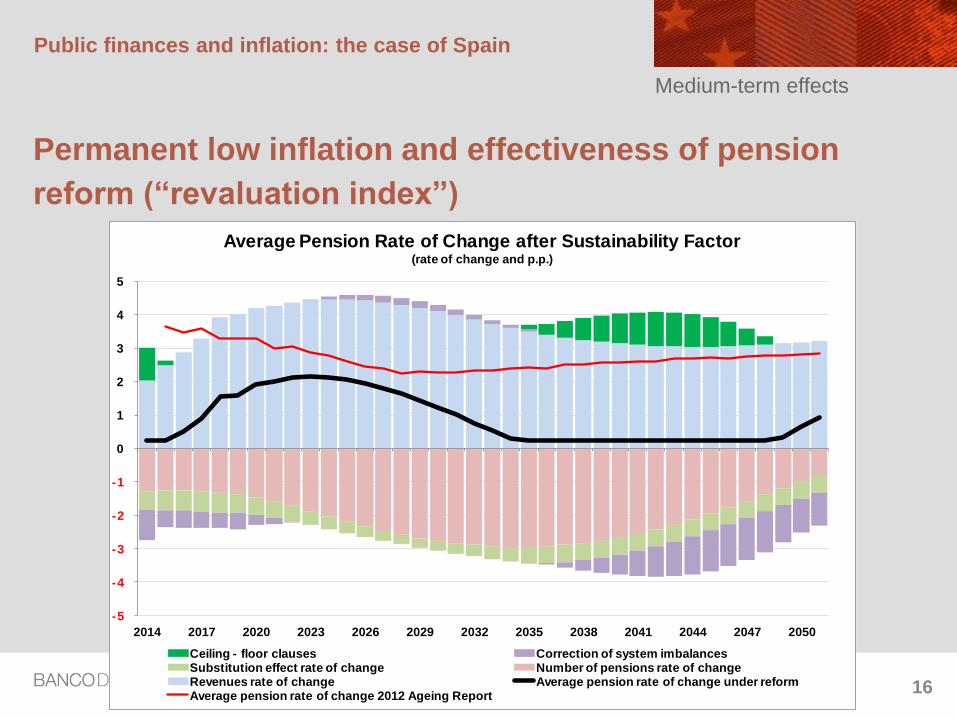

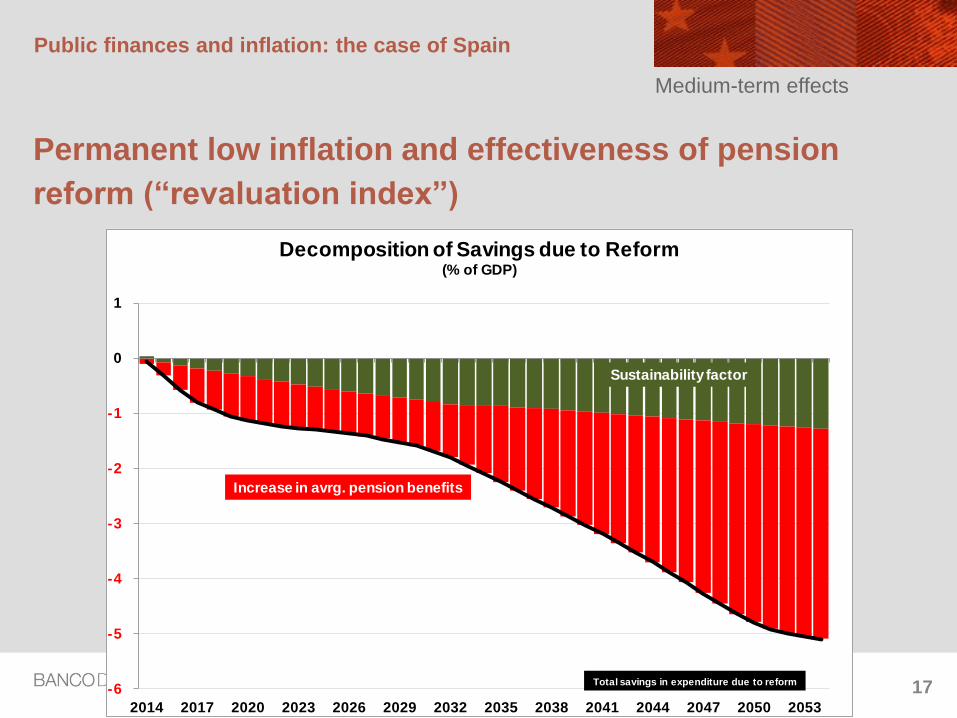

Medium-term effects

Permanent low inflation and effectiveness of pension

reform (“revaluation index”)

Departamento de Coyuntura y

Previsión Económica

-5

-4

-3

-2

-1

0

1

2

3

4

5

2014 2017 2020 2023 2026 2029 2032 2035 2038 2041 2044 2047 2050

Average Pension Rate of Change after Sustainability Factor(rate of change and p.p.)

Ceiling - floor clauses Correction of system imbalancesSubstitution effect rate of change Number of pensions rate of changeRevenues rate of change Average pension rate of change under reformAverage pension rate of change 2012 Ageing Report

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

17

Medium-term effects

Permanent low inflation and effectiveness of pension

reform (“revaluation index”)

Departamento de Coyuntura y

Previsión Económica-6

-5

-4

-3

-2

-1

0

1

2014 2017 2020 2023 2026 2029 2032 2035 2038 2041 2044 2047 2050 2053

Decomposition of Savings due to Reform(% of GDP)

Sustainability factor

Increase in avrg. pension benefits

Total savings in expenditure due to reform

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

18

Medium-term effects

Permanent low inflation and effectiveness of pension

reform (“revaluation index”)

“Savings” (pension expenditure) depend crucially on

inflation assumptions

Sanchez (2014, BE WP – OLG model): “Our simulation

indicates that a persistently low inflation could be (in the long

term) as harmful for the success of the reform as poor

immigration and productivity.”

Departamento de Coyuntura y

Previsión Económica

NOMBRE DEL DEPARTAMENTO

Public finances and inflation: the case of Spain

19

Summary

Implications of a low inflation environment for…

Fiscal consolidation (some accounting examples)

PUBLIC DEBT: The consolidation episode of the 1990s vs now

PUBLIC SPENDING: impact of measures in a low-inflation framework

PUBLIC REVENUE: limits to tax collection

Some simulations using Bank of Spain’s MTBE

INFLATION SHOCKS: inspecting the channels - oil prices, profit margins

Medium-term fiscal sustainability safeguards

PENSION SUSTAINABILITY: the “revaluation index”

Departamento de Coyuntura y

Previsión Económica

NOMBRE DEL DEPARTAMENTO 20

THANKS FOR YOUR ATTENTION

Public finances and inflation:

the case of Spain

Javier J. Pérez (Banco de España)

Joint work with S. Hurtado, F. Martí, and P. Hernández

Departamento de Coyuntura y

Previsión Económica

NOMBRE DEL DEPARTAMENTO

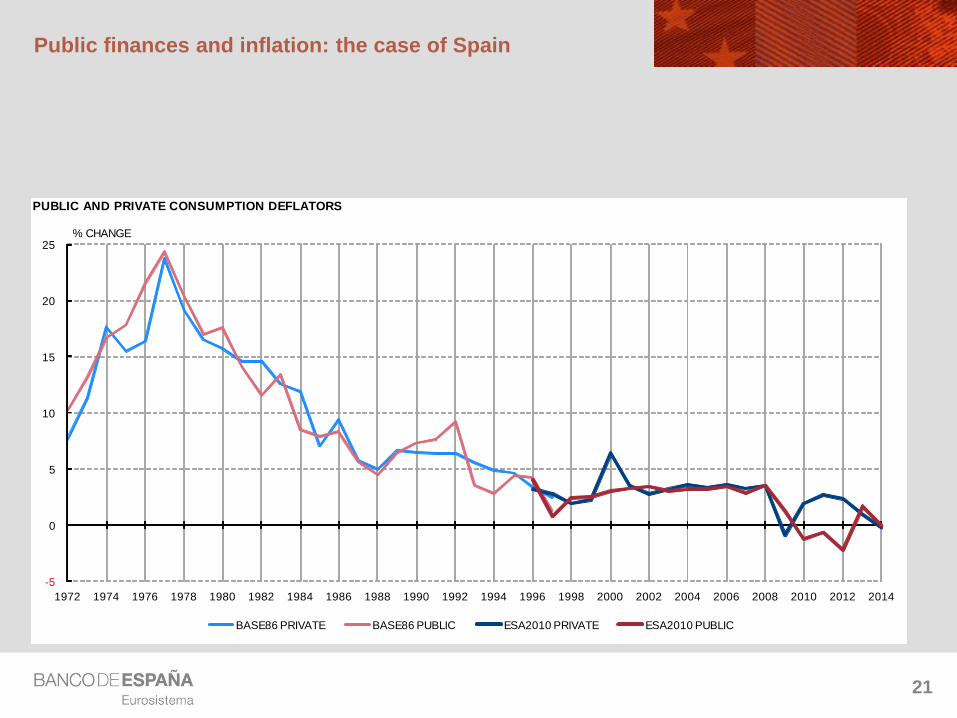

Public finances and inflation: the case of Spain

21Departamento de Coyuntura y

Previsión Económica

PUBLIC AND PRIVATE CONSUMPTION DEFLATORS

-5

0

5

10

15

20

25

1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

BASE86 PRIVATE BASE86 PUBLIC ESA2010 PRIVATE ESA2010 PUBLIC

% CHANGE