Embed Size (px)

Citation preview

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED–

PUBLIC DATA

Direct Testimony and Schedules Ruth K. Lowenthal

Before the Minnesota Public Utilities Commission State of Minnesota

In the Matter of the Application of Northern States Power Company for Authority to Increase Rates for Electric Service in Minnesota

Docket No. E002/GR-15-826 Exhibit___(RKL-1)

Employee Compensation and Benefits

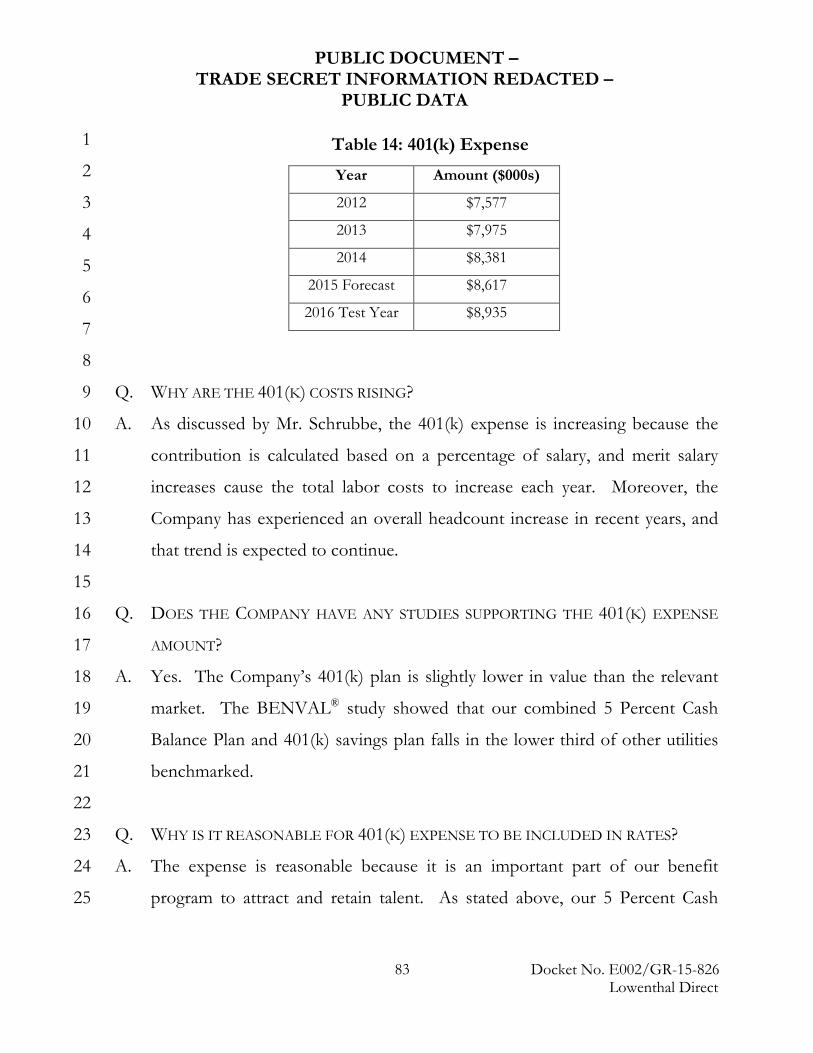

November 2, 2015

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

Table of Contents I. Introduction 1

II. Total Rewards Recovery Request Overview 5

III. Our Compensation and Benefit Levels are at or Below Market Levels

10

A. Total Cash Compensation Study 11

B. Health, Welfare and Retirement Benefits Study 17

IV. Total Rewards Program Cost Mitigation Measures and Resource Realignment

19

A. Cost Mitigation Measures 19

B. Resource Realignment 26

V. Resulting Challenges 30

A. Hiring Challenges 32

B. Retention Challenges 39

C. Emerging Issues Affecting Hiring and Retention Challenges 41

VI. Total Cash Compensation 44

A. Base Salary 45

B. AIP 48

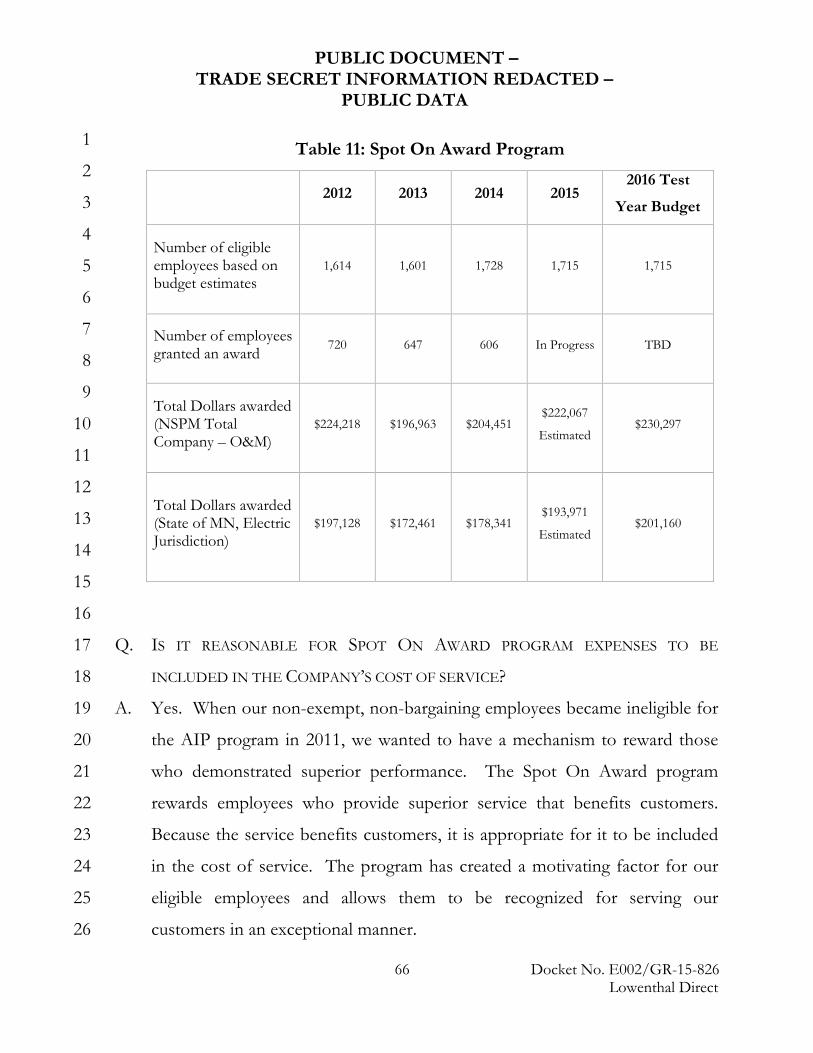

C. Spot On Award Recognition Program 64

VII. Active Health and Welfare Costs 67

VIII. Employee Retirement Programs 74

A. Defined Benefit Plan 75

B. Defined Contribution Plan 82

C. Retiree Medical Benefits 84

IX. Conclusion 86

i Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

Schedules

Statement of Qualifications Schedule 1

Total Rewards Program Components and Costs Schedule 2

Towers Watson Compensation Study (Non-Public) Schedule 3

Towers Watson BENVAL® Study (Non-Public) Schedule 4

Retirement Program Summary Schedule 5

2013, 2014 and 2015 AIP Documents Schedule 6

Dental, Vision, Life Insurance, and Disability Summary Schedule 7

Prefiled Discovery (Non-Public) Appendix A

ii Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

I. INTRODUCTION 1

2

Q. PLEASE STATE YOUR NAME AND OCCUPATION. 3

A. My name is Ruth K. Lowenthal. I am the Vice President, Total Rewards for 4

Xcel Energy Services Inc. 5

6

Q. PLEASE SUMMARIZE YOUR QUALIFICATIONS AND EXPERIENCE. 7

A. As Vice President of Total Rewards, I oversee Total Rewards (Compensation, 8

Employee Benefits for Retirement and Health and Welfare), Payroll, HR 9

Operations, Talent Management and Recognition. My statement of 10

qualifications is included as Exhibit___(RKL-1), Schedule 1. 11

12

Q. WHAT IS THE PURPOSE OF YOUR TESTIMONY IN THIS PROCEEDING? 13

A. I support Northern States Power Company’s (NSPM or the Company) 14

request to recover in electric rates the costs associated with our employee 15

compensation and benefits, which are elements of the Company’s Total 16

Rewards Program. 17

18

Q. ARE YOU PROVIDING ANY INFORMATION IN RESPONSE TO THE COMMISSION’S 19

MAY 8, 2015 ORDER IN DOCKET NO. E002/GR-13-868? 20

A. Yes. In compliance with Order Point 29 I discuss Key Performance 21

Indicators (KPI) for purposes of our Annual Incentive Program (AIP). 22

23

Q. DO YOU PROVIDE ANY ADDITIONAL INFORMATION RELATED TO 24

COMPENSATION AND BENEFITS? 25

1 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

A. Yes. To prepare testimony for this case, we reviewed the discovery related to 1

compensation and benefits from Docket No. E002/GR-13-868. I have 2

incorporated some of those discovery responses into my testimony through 3

expanded discussion and schedules. We are also providing additional 4

information in the form of pre-filed discovery, which can be found in 5

Appendix A to my testimony. Appendix A also provides a list of each 6

information request from the 2013 rate case that we have incorporated into 7

this case, indicating where it is included in my testimony or schedules, or if it 8

is provided in Appendix A. 9

10

Q. PLEASE PROVIDE A SUMMARY OF YOUR TESTIMONY. 11

A. Our Total Rewards Program is of the utmost importance to our employees 12

and customers as these compensation and benefit costs are necessary to 13

attract, motivate, and retain the talent necessary to keep the lights on. Thus, it 14

is critical we recover the full amount of costs requested in this case. We have 15

taken internal cost mitigation measures, we have realigned resources, and, as 16

we have done in previous cases, we have limited our Total Rewards Program 17

cost recovery request in this case. We are not asking for recovery of any 18

amounts that the Commission has previously found to be unreasonable, and 19

our request is consistent with Commission precedent. For instance, we are 20

not seeking recovery of several elements of compensation that we will pay, 21

including a portion of our AIP costs, long-term incentive, nuclear retention, 22

and non-qualified pension expense. 23

24

As evidenced by our most recent Towers Watson survey discussed below, 25

even with AIP our total cash compensation levels are in line with, or slightly 26

2 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

below, the market. And if AIP were excluded (or, an employee did not earn 1

100 percent of their AIP) our total cash compensation would lag the market 2

by 14.7 percent. 3

4

Because of our limited requests and disallowances in prior cases, we have not 5

recovered all of the costs necessary to attract, motivate, and retain our 6

valuable employees. For instance, we have recovered less than 65 percent of 7

the AIP costs we have actually paid to employees over the past ten years. 8

Our expectation as a business is to provide safe and reliable service for our 9

customers. We are requesting to recover the costs necessary to allow the 10

Company to maintain and invest in our most important internal assets, our 11

employees. The consistent reductions and disallowances we continually 12

encounter are eroding our ability to pay for reasonable and necessary 13

compensation and benefit expenses. We cannot continue to pay at or below 14

market levels, make internal cost cuts year over year, request less than our full 15

cost of doing business in each rate case, and receive additional disallowances 16

on top of that. This pattern of under-recovery is not sustainable, and the 17

results would not be good for our customers or employees. 18

19

While many of the challenges associated with under-recovery of these costs 20

are familiar, like recruiting and retention, we are also seeing new issues 21

emerging. For instance, STEM (science, technology, engineering and math) 22

job openings are increasing while the corresponding skilled labor force is not. 23

As discussed below, we have a great need for job candidates in the STEM 24

category in our business, yet the job pool does not meet that demand. 25

26

3 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

Another contributing problem lies in the transition from baby boomers to 1

millennials and the difference in expectations between the generations. For 2

example, millennials are characterized by desiring quick career progression, 3

whereas most of our jobs require years of skill-building and on-the-job 4

training before career advancement is possible. Millennials also seem to 5

desire higher compensation and benefit levels at the outset than previous 6

generations, and our below-average compensation package impairs our ability 7

to compete for those employees with other companies who pay at or above 8

market compensation levels. While we are currently able to offer our new 9

employees health and welfare benefits generally comparable to our industry 10

peers, our new hire retirement benefit is significantly lower than our peers. 11

Although we made cost-saving changes to our retirement program, it puts us 12

at a disadvantage when we are trying to attract new candidates. 13

14

Finally, we are also affected by the fact that there are more people leaving the 15

workforce than joining it due to the lower birth rates after the baby boomer 16

generation. This means that not only are there fewer people to choose from 17

when selecting candidates, but even less of the population now has the 18

developed skills we need for many of our positions. 19

20

Despite these ongoing and emerging challenges, we have made efforts to 21

mitigate costs and use our resources more strategically in support of our 22

operational goals. Our mitigation efforts include elimination of the option for 23

employees to buy or sell Paid Time Off (PTO), a distinction between 24

dependent and employee healthcare coverage (and the provision of greater 25

4 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

coverage to employees), and the addition of new requirements that will limit 1

our exposure to increasing pharmacy costs. 2

3

In addition to our cost mitigation efforts, we have also made a concerted 4

effort to use our resources more strategically. For instance, while we have 5

always made it our goal to provide market-competitive compensation that is 6

linked to performance, we continue to place greater emphasis on 7

strengthening the link between employee pay and performance, thereby 8

providing larger rewards to our highest performers. This has not affected our 9

overall need for compensation levels; it merely targets our resources more 10

strategically. We view this as a positive move for our customers that should 11

be supported by the Commission and others, as it rewards performance. 12

13

When combining these challenges with our resource realignment efforts, and 14

the under-recovery of our costs, it is evident that we simply do not have the 15

capacity to absorb any further disallowance of our costs without making 16

significant changes to our Total Rewards Program. Considering the previous 17

cuts to our existing programs, the fact that we pay at, or below, market levels, 18

and the fact that we do not recover all of the costs we actually do pay, we 19

need every dollar requested to continue to be successful in the future. 20

21

II. TOTAL REWARDS RECOVERY REQUEST OVERVIEW 22

23

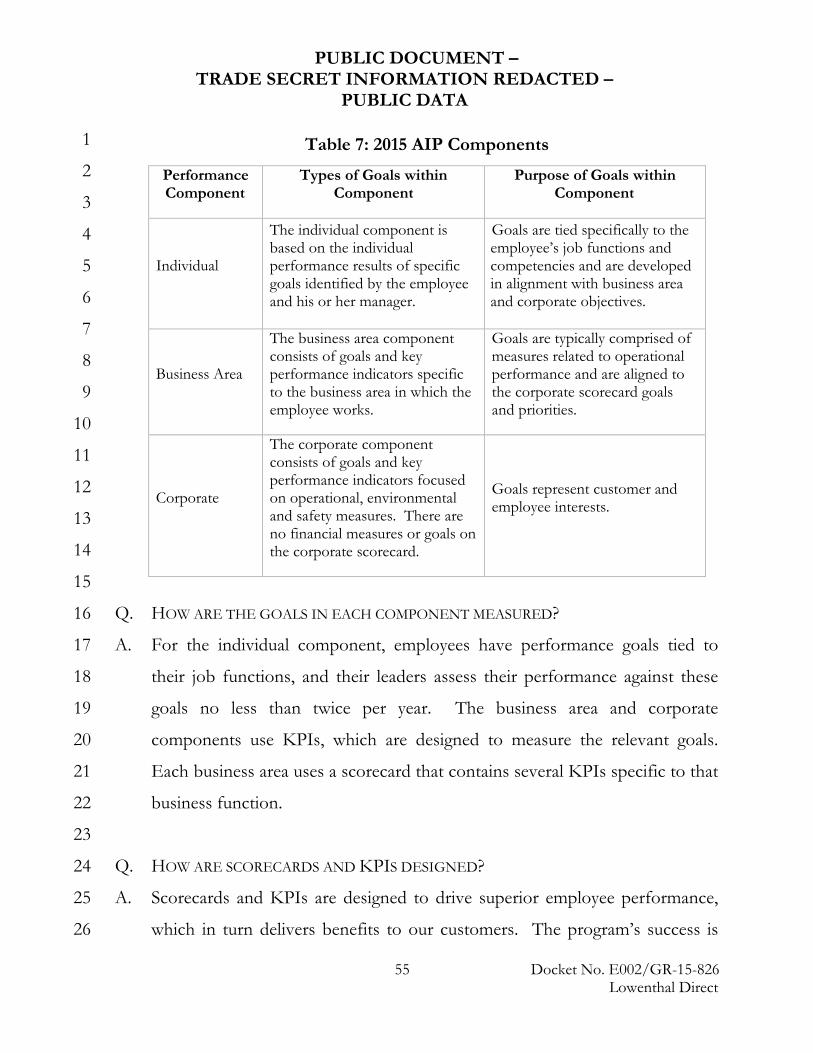

Q. WHAT ARE THE ELEMENTS OF THE TOTAL REWARDS PROGRAM? 24

A. The Total Rewards Program includes the following components of 25

compensation and benefits: 26

5 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

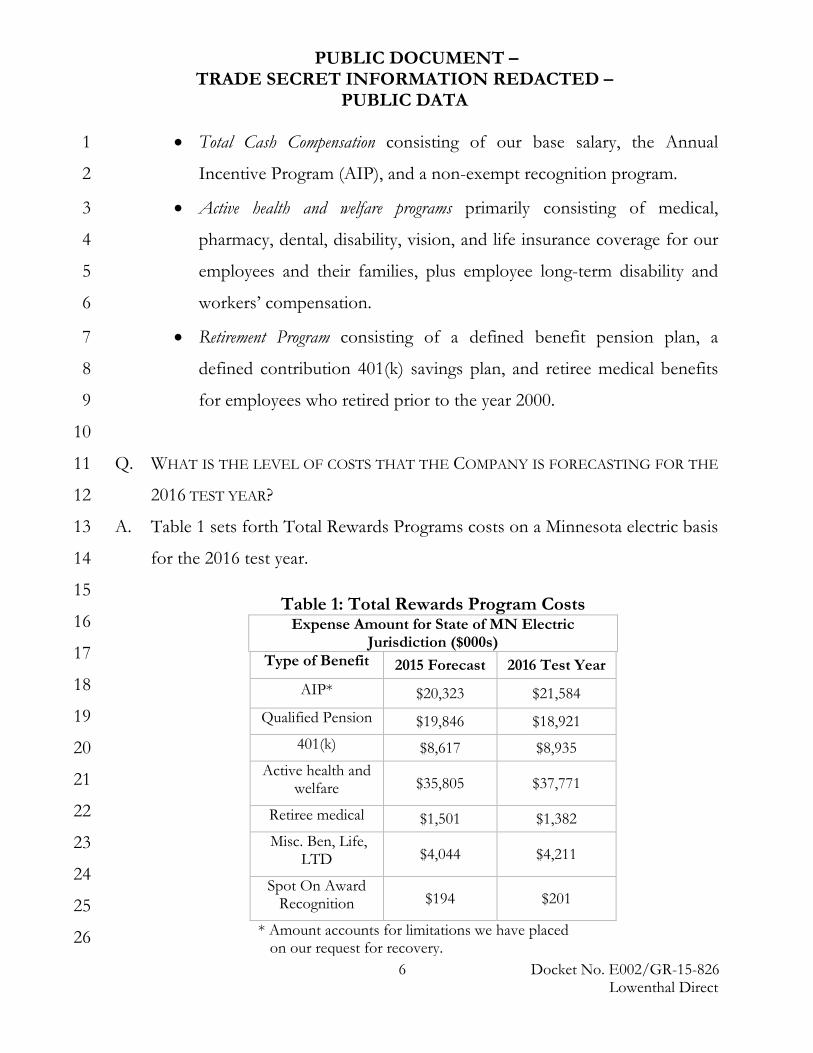

• Total Cash Compensation consisting of our base salary, the Annual 1

Incentive Program (AIP), and a non-exempt recognition program. 2

• Active health and welfare programs primarily consisting of medical, 3

pharmacy, dental, disability, vision, and life insurance coverage for our 4

employees and their families, plus employee long-term disability and 5

workers’ compensation. 6

• Retirement Program consisting of a defined benefit pension plan, a 7

defined contribution 401(k) savings plan, and retiree medical benefits 8

for employees who retired prior to the year 2000. 9

10

Q. WHAT IS THE LEVEL OF COSTS THAT THE COMPANY IS FORECASTING FOR THE 11

2016 TEST YEAR? 12

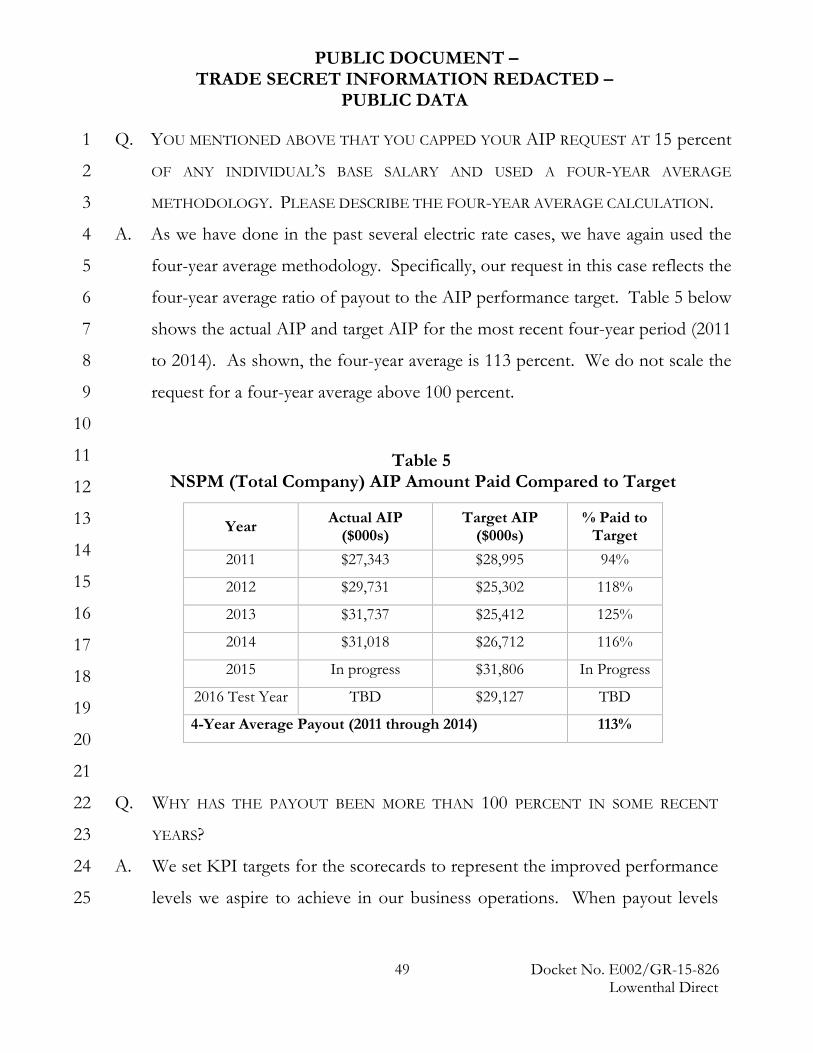

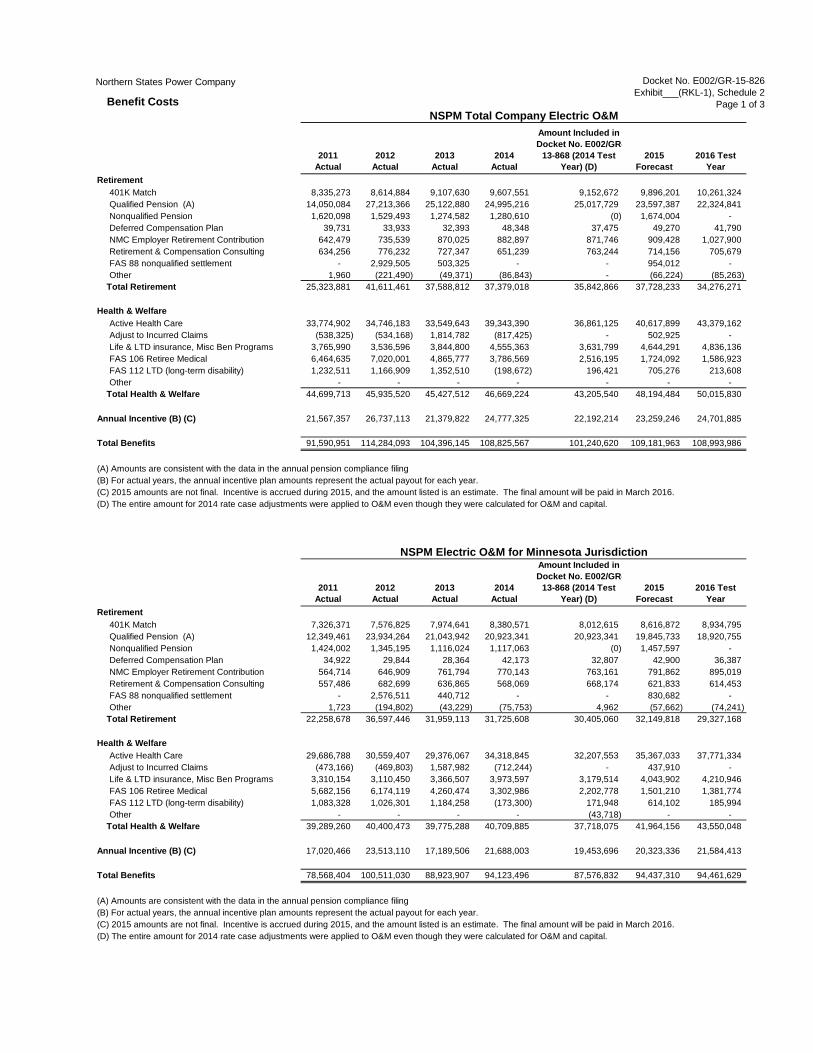

A. Table 1 sets forth Total Rewards Programs costs on a Minnesota electric basis 13

for the 2016 test year. 14

15

16

17

18

19

20

21

22

23

24

25

26

Table 1: Total Rewards Program Costs Expense Amount for State of MN Electric

Jurisdiction ($000s) Type of Benefit 2015 Forecast 2016 Test Year

AIP* $20,323 $21,584 Qualified Pension $19,846 $18,921

401(k) $8,617 $8,935 Active health and

welfare $35,805 $37,771

Retiree medical $1,501 $1,382 Misc. Ben, Life,

LTD $4,044 $4,211

Spot On Award Recognition $194 $201

* Amount accounts for limitations we have placed on our request for recovery.

6 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

1 Q. HOW DO THOSE TEST YEAR AMOUNTS COMPARE TO ACTUAL TOTAL REWARDS 2

PROGRAM COSTS IN PRIOR YEARS AS WELL AS THE 2016 TEST YEAR? 3

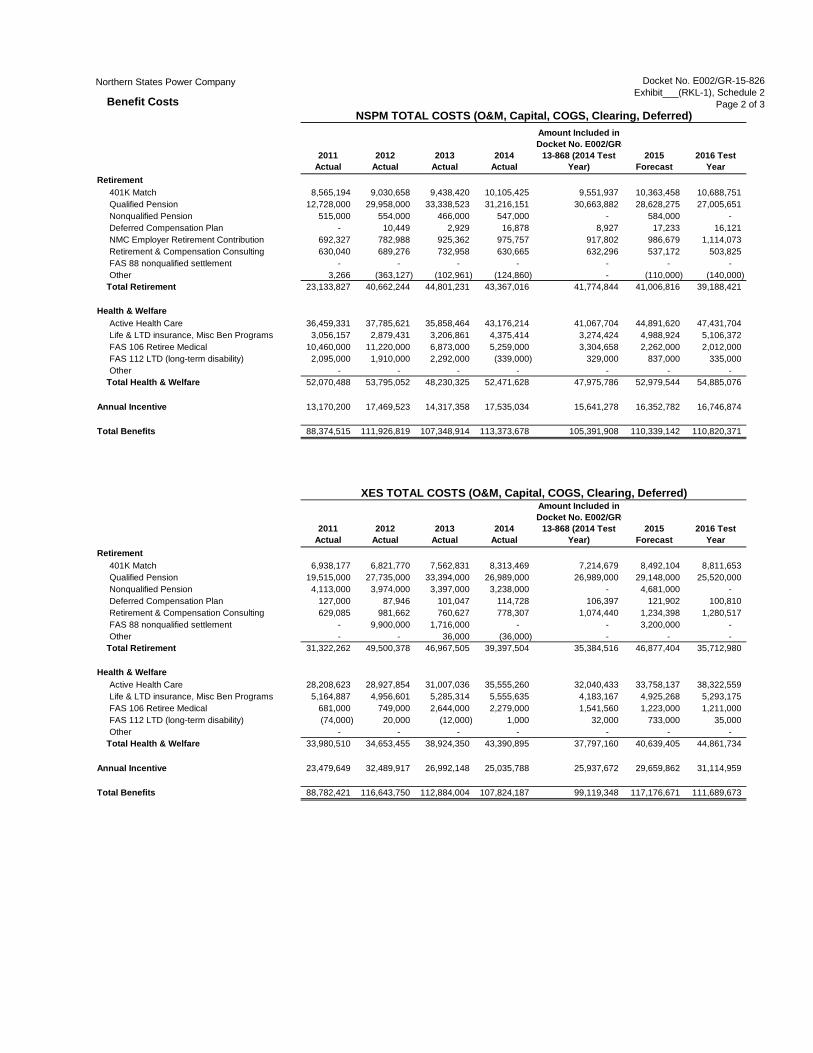

A. The actual amounts of Total Rewards Program costs for prior years and the 4

2016 test year, segregated by capital and expense, are set forth in 5

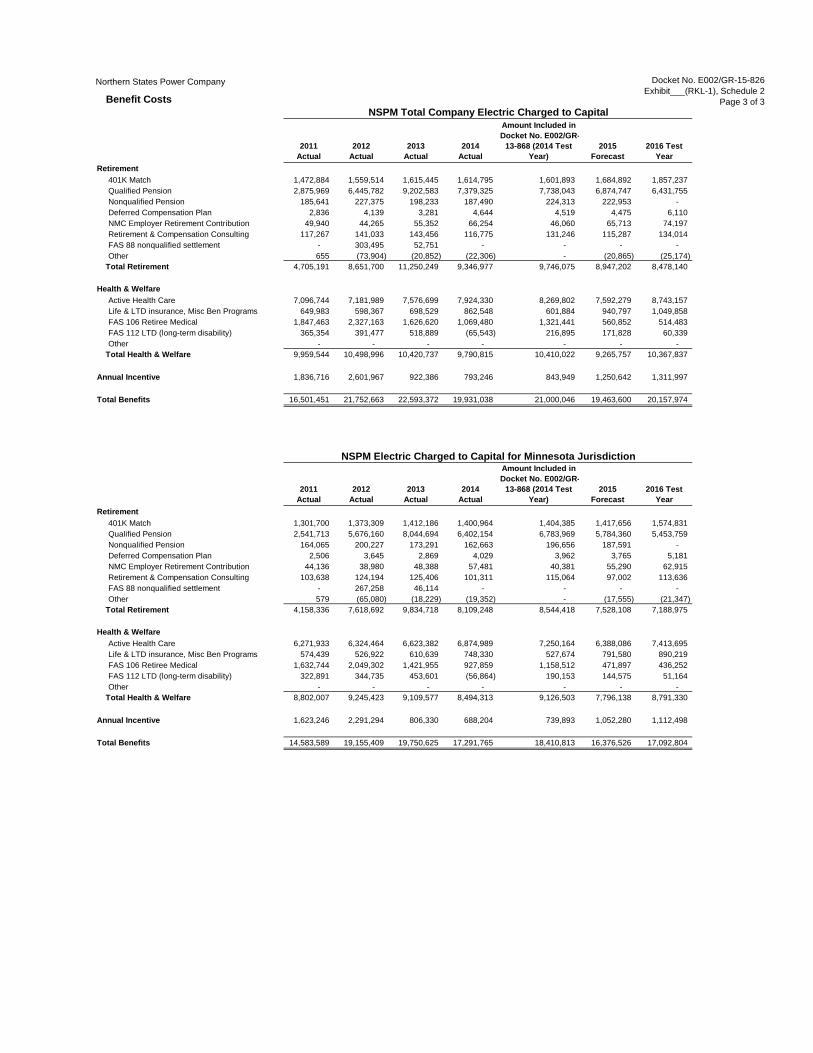

Exhibit___(RKL-1), Schedule 2. 6

7

Q. WHAT IS THE LEVEL OF O&M EXPENSE THAT HUMAN RESOURCES SEEKS TO 8

RECOVER FOR THE 2017 AND 2018 PLAN YEARS? 9

A. Our Total Rewards Program forecasted 2017 and 2018 increases in O&M 10

expenses are set forth in the “budget walk forwards” in Volume 6 of the 11

Company’s initial rate case filing. Company witness Mr. Aakash H. 12

Chandarana explains the basis of the Company’s overall approach to its O&M 13

expense requests for the 2017 and 2018 Plan Years, and Company witnesses 14

Mr. Charles R. Burdick and Mr. John Mothersole explain the basis for the 15

Company’s selection of the particular factors used in our rate requests for 16

these years. 17

18

Q. IS THE COMPANY SEEKING TO INCLUDE ALL OF THE COSTS OF THE TOTAL 19

REWARDS PROGRAM IN ITS TEST YEAR COST OF SERVICE? 20

A. No. We are not requesting rate recovery of the following elements of 21

employee compensation: 22

• Long-term incentive compensation costs; 23

• Nuclear retention program costs; 24

• Non-qualified pension benefits; and 25

• Certain pension benefits for senior executives. 26

7 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

In addition, we have limited our request for AIP recovery. 1

2

Q. HOW HAVE YOU LIMITED YOUR AIP COST RECOVERY REQUEST? 3

A. We have limited our request for AIP cost recovery in several ways, consistent 4

with previous rate cases and Commission precedent. First, we are requesting 5

rate recovery of our incentive compensation costs subject to a four-year 6

average payout of AIP – capped at 100 percent performance target and 7

limited to a cap of 15 percent of base salary. Therefore, customers are not 8

funding the full cost of employee compensation. This cap not only 9

implements the Commission’s original intent1 of excluding recovery of part of 10

the incentive compensation costs related to executives, but it also excludes 11

recovery of part of the incentive compensation paid to middle management 12

employees as part of their total compensation package. 13

14

Second, we are proposing to retain the refund mechanism that would provide 15

customer refunds if actual incentive compensation payouts are lower than the 16

test year level approved in rates. By including this previously approved 17

Commission safeguard, we are able to balance the interests of our customers 18

while providing our employees with market-competitive cash compensation. 19

20

Finally, we request recovery of only the target level incentive amount, so if 21

our employees perform beyond their specific goal targets and the Company’s 22

operational goals, our customers receive this added benefit at no extra cost. 23

Please see the testimony of Company witness Ms. Anne E. Heuer for a 24

25

1 Docket Nos. E002/GR-92-1185 and G002/GR-92-1186. 8 Docket No. E002/GR-15-826

Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

description of this AIP adjustment. 1

2

Q. YOU MENTIONED THAT YOU ARE NOT SEEKING RECOVERY OF THE NUCLEAR 3

RETENTION PROGRAM COSTS IN THIS CASE. IS THIS PROGRAM STILL 4

ONGOING? 5

A. Yes. As discussed further by Company witness Mr. Timothy J. O’Connor, we 6

are not seeking recovery of nuclear retention program costs (approximately 7

$900,000 in 2016) in this case to limit the number of contested issues. 8

However, these costs remain critical to attracting and retaining quality nuclear 9

employees in the current marketplace, and we will continue to incur these 10

costs in 2016 and beyond. 11

12

Q. ARE YOU SEEKING RECOVERY OF ANY COSTS FOR LONG-TERM INCENTIVE 13

(LTI) COMPENSATION? 14

A. No. Similar to our nuclear retention program, while we continue to offer this 15

program to our employees and believe it is imperative to attracting and 16

retaining these employees, we are not requesting recovery of the LTI costs in 17

this case to limit the number of contested issues. 18

19

Q. ARE YOU SEEKING RECOVERY OF COSTS FOR ALL OF THE COMPANY’S 20

EMPLOYEE RETIREMENT PLANS? 21

A. No. Though we have previously asked for recovery of these costs, in order to 22

minimize the disputed issues and be consistent with previous Commission 23

precedent, we are not seeking recovery of the Supplemental Executive 24

Retirement Plan (SERP) or non-qualified pension costs in this case, even 25

though these benefits are an important part of a Total Rewards Program 26

9 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

package that gives us the ability to attract and retain the right management 1

talent necessary for our business. 2

3

Q. WHAT DO YOU CONCLUDE ABOUT YOUR TOTAL REWARDS PROGRAM COST 4

RECOVERY REQUEST IN THIS CASE? 5

A. While all of the Total Rewards Program components are necessary to attract 6

and retain our valued employees, we have made a concerted effort to 7

minimize the issues at dispute in this case and to keep our request consistent 8

with Commission precedent and previous rate cases. 9

10

III. OUR COMPENSATION AND BENEFIT LEVELS ARE AT OR 11 BELOW MARKET LEVELS 12

13

Q. DO ANY INDEPENDENT STUDIES DEMONSTRATE THAT THE COMPANY’S 14

TOTAL REWARDS PROGRAM IS CONSISTENT WITH MARKET VALUES? 15

A. Yes. Although I am not aware of a single study that compares the entire array 16

of cash compensation, health and welfare benefits, and retirement benefits 17

among companies, we have an independent study from Towers Watson 18

showing the reasonableness of the Company’s total cash compensation. We 19

have another independent study showing the reasonableness of the 20

Company’s health and welfare benefits and retirement benefits. I provide 21

both of these studies as Exhibit___(RKL-1), Schedules 3 and 4, respectively. 22

Together, these studies demonstrate that the Company’s Total Rewards 23

Program is reasonable. 24

25

Q. WHY DOESN’T THE COMPANY USE A SINGLE STUDY TO COMPARE TOTAL CASH 26

COMPENSATION AND BENEFIT PROGRAMS AMONG COMPANIES? 27 10 Docket No. E002/GR-15-826

Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

A. It is my experience as a Human Resources (HR) professional that broad-based 1

studies evaluating both cash compensation and benefits are neither helpful 2

nor insightful for confirming market comparability. Where separate studies 3

are able to analyze individual components of a benefit program, overall 4

studies need to be adjusted for demographic differences across multiple 5

organizations so that the analysis is focused on differences in plan design 6

provisions, as opposed to an actual dollar value of a program. 7

8

Therefore, it is more typical, efficient, and meaningful for companies, 9

including NSPM, to assess the market-competitiveness of these components 10

separately, which is how we have historically assessed market comparability. 11

In addition, a single study would be more difficult to administer because 12

overall benefit programs are broad-based with numerous complex 13

components that are measured differently than pay. That could lead to less 14

reliable results as study participants, such as NSPM, would likely be less 15

certain about responding to survey questionnaires. For example, our market 16

survey for benefits, BENVAL®, captures data from a wide variety of benefit 17

plans and industries at a national level. General benefit surveys tend to 18

capture basic programmatic questions, which can be difficult to assess when 19

medical plan options and designs are very different. 20

21

A. Total Cash Compensation Study 22

Q. BRIEFLY SUMMARIZE THE FINDINGS OF THE TOTAL CASH COMPENSATION 23

STUDY PERFORMED BY TOWERS WATSON. 24

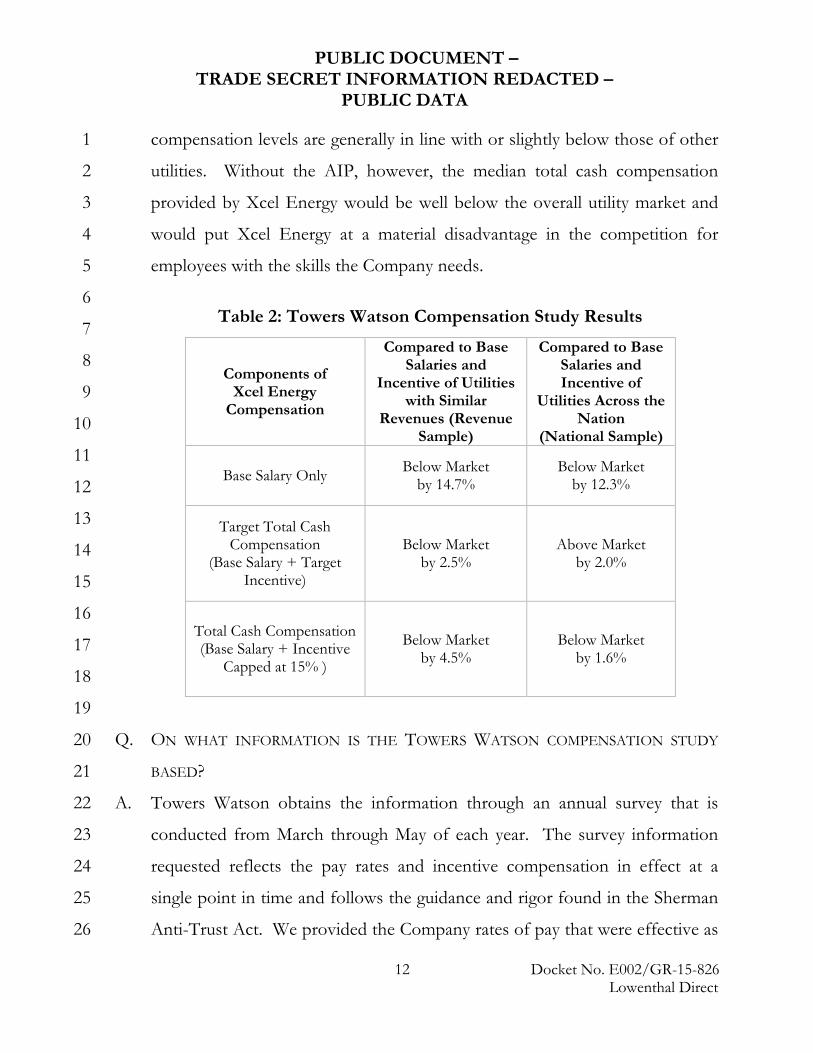

A. As shown in Table 2 below, the 2015 Towers Watson compensation study 25

finds that, with the inclusion of the AIP, Xcel Energy’s median total cash 26

11 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

compensation levels are generally in line with or slightly below those of other 1

utilities. Without the AIP, however, the median total cash compensation 2

provided by Xcel Energy would be well below the overall utility market and 3

would put Xcel Energy at a material disadvantage in the competition for 4

employees with the skills the Company needs. 5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

Q. ON WHAT INFORMATION IS THE TOWERS WATSON COMPENSATION STUDY 20

BASED? 21

A. Towers Watson obtains the information through an annual survey that is 22

conducted from March through May of each year. The survey information 23

requested reflects the pay rates and incentive compensation in effect at a 24

single point in time and follows the guidance and rigor found in the Sherman 25

Anti-Trust Act. We provided the Company rates of pay that were effective as 26

Table 2: Towers Watson Compensation Study Results

Components of Xcel Energy

Compensation

Compared to Base Salaries and

Incentive of Utilities with Similar

Revenues (Revenue Sample)

Compared to Base Salaries and Incentive of

Utilities Across the Nation

(National Sample)

Base Salary Only Below Market by 14.7%

Below Market by 12.3%

Target Total Cash Compensation

(Base Salary + Target Incentive)

Below Market by 2.5%

Above Market by 2.0%

Total Cash Compensation (Base Salary + Incentive

Capped at 15% )

Below Market by 4.5%

Below Market by 1.6%

12 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

of March 2015 per the survey instructions. The other participants in the 1

survey, which are part of a comparison group of U.S. electric and gas 2

companies similar in size to Xcel Energy Inc. with comparable median 3

revenues of $5.0 billion, also provided information to Towers Watson during 4

the period of March through May 2015. In fact, there were 46 investor-5

owned energy services companies included in this study. 6

7

Q. DOES THE COMPENSATION INFORMATION SUBMITTED BY OTHER COMPANIES 8

INCLUDE 2015 INCREASES, OR DOES IT INCLUDE ONLY 2014 COMPENSATION 9

RATES? 10

A. The pay rates used reflect the compensation levels in place at the time the 11

survey was completed between March through May 2015 in accordance with 12

the survey instructions. 13

14

Q. WHAT WAS THE PERCENTAGE INCREASE REFLECTED IN THE COMPANY’S 15

SALARY INFORMATION SUBMITTED TO TOWERS WATSON AS COMPARED TO 16

THE PREVIOUS YEAR’S STUDY? 17

A. We provided Towers Watson the pay rates that were in effect as of March 16, 18

2015, which was a three-percent average increase over the pay rates effective 19

March 2014. 20

21

Q. IS IT COMMON FOR COMPANIES TO RELY UPON STUDIES SUCH AS THE TOWERS 22

WATSON COMPENSATION STUDY FOR COMPENSATION COMPARISON 23

PURPOSES? 24

A. Yes. It is very common for companies trying to ensure that their 25

compensation is market-competitive to use third-party consulting firm survey 26

13 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

data for benchmarking purposes. The use of surveys is a widely accepted 1

practice that employers use to compare their compensation levels to what is 2

going on outside of their own company which is a check-in on the reality of 3

the labor market. 4

5

In my past jobs, I also experienced the use of compensation surveys. They 6

were an important data resource used for designing and maintaining market-7

competitive compensation programs. Our Company’s human capital is our 8

talented and skilled workforce. They are a vitally important resource that is 9

needed to run our company just like the other capital resources in our 10

business. 11

12

The management of HR functions very much like other business functions. 13

For example, if we need to source a specially designed component for one of 14

our production generators, our procurement experts realize that we will not 15

be able to purchase the component for 15-20 percent below the market value 16

of comparable components. Conversely, we do not want to overspend 17

beyond their comparable reference point for the component either because 18

we have a limited budget to maintain operations. This same business 19

management principle exists for our human capital. We realize that we 20

cannot underpay and have no desire to overpay for our human capital 21

compared to what is happening in the market. Benchmarking our 22

compensation programs to survey market data is a best practice that allows us 23

to monitor what is happening in the external market for labor and 24

compensation programs. 25

26

14 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

Q. IS THE TOWERS WATSON COMPENSATION STUDY THE ONLY STUDY THE 1

COMPANY RELIES UPON FOR PURPOSES OF BENCHMARKING ITS TOTAL CASH 2

COMPENSATION LEVELS? 3

A. No. The Company routinely uses a number of additional third-party surveys 4

to compare its total cash compensation levels, merit pay increases, and 5

programs to those of other firms, including both other utilities and non-6

utilities. These studies are discussed further below in the section regarding 7

the Company’s cash compensation. 8

9

Q. WHAT IS THE COMPANY’S PRINCIPAL OBJECTIVE WHEN IT PERFORMS ITS 10

BENCHMARKING COMPARISONS? 11

A. Our goal in reviewing such survey information is to determine the market-12

competitive compensation rate for a given job and skill set, considering 13

companies with which Xcel Energy competes for talent. 14

15

Q. DOES THE COMPANY SET SALARIES FOR POSITIONS USING SUCH THIRD-PARTY 16

DATA? 17

A. Yes. Using the data provided by third-party surveys, the Company selects 18

benchmark positions that are representative of the Company’s similar 19

positions. We then use the compensation data provided by the survey (for 20

the position being evaluated) to select the appropriate pay grade within our 21

salary structure and to assign the pay grade for that position. After we 22

determine where a particular position should be placed within our salary 23

structure, an employee’s compensation within the pay grade will be 24

individually determined based on several factors, including experience, skills, 25

and performance. 26

15 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

1

For each eligible pay grade within the salary structure, the Company also sets 2

AIP compensation targets. The employees in those pay grades have the 3

ability to earn a target AIP payout if levels of performance are met under Xcel 4

Energy’s AIP. Just as we determine our base salary ranges by looking to 5

market survey data, we also set our AIP targets to deliver market-comparable 6

total cash compensation based on those same surveys. Survey data is 7

refreshed every year so that we can ensure our salaries and incentive 8

opportunities remain competitive and are aligned with the market. 9

10

Q. WHAT DO YOU CONCLUDE REGARDING THE MARKET-COMPETITIVE NATURE 11

OF THE COMPANY’S TOTAL CASH COMPENSATION? 12

A. The Towers Watson compensation study demonstrates that, with the 13

inclusion of the AIP, the Company’s total cash compensation levels are in line 14

with the market. However, if the AIP were excluded, our total cash 15

compensation would lag the market by 14.7 percent (compared to utilities 16

with similar revenues), which would put us at a material disadvantage when 17

competing for talented employees. 18

19

Q. PLEASE EXPLAIN WHAT YOU MEAN WHEN YOU STATE THAT AN EMPLOYEE’S 20

TOTAL CASH COMPENSATION WOULD LAG THE MARKET BY 14.7 PERCENT 21

WITHOUT AIP. 22

A. Assume that the market rate for a particular job is $100 per year, and that 23

other employers are paying $100 per year to employees who are capable of 24

performing that job. Our base salary for that job would be $85.30, but with 25

the AIP the employee would have the opportunity to earn $100. Or stated 26

16 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

alternatively, without the AIP, the Company’s employees would earn only 1

$85.30 for performing the same job that other employers would pay them 2

$100 to perform. Essentially, without AIP our employees would not be paid 3

competitively. We would need to add a comparable amount to their base 4

salary, which would then become a fixed cost to the organization and our 5

customers, or we would likely lose our most talented employees. 6

7

B. Health, Welfare and Retirement Benefits Study 8

Q. YOU INDICATED EARLIER THAT THE COMPANY ALSO HAS AN INDEPENDENT 9

STUDY DEMONSTRATING THE REASONABLENESS OF THE HEALTH AND 10

WELFARE AND RETIREMENT PROGRAM BENEFITS COMPONENTS OF ITS TOTAL 11

REWARDS PROGRAM. PLEASE DESCRIBE THAT STUDY. 12

A. Towers Watson collects health, welfare, and retirement benefit plan 13

provisions from hundreds of employers in all industry sectors and measures 14

the value of these programs. This analysis tool, known as BENVAL®, 15

compares new retirement and health and welfare benefit programs. The tool 16

compiles each benefit separately as well as on an entire health, welfare and 17

retirement benefit program basis. There were 40 energy services companies 18

in the comparison group for the Company. The study presents relative value 19

assessments of the competitiveness of a corporation’s entire benefit program. 20

It is based on a common set of actuarial assumptions and a standard 21

employee population that is a representative sample of large U.S. companies. 22

Thus, the analysis establishes a controlled environment in which differences 23

in value among employer plans are exclusively a function of differences in 24

plan design provisions. The results are normalized to a scale where a 25

company providing the average benefit value would be shown at 100. Higher 26

17 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

amounts reflect companies who provide benefits above the average, while 1

lower amounts are shown for companies whose benefits are below the peer 2

group average. 3

4

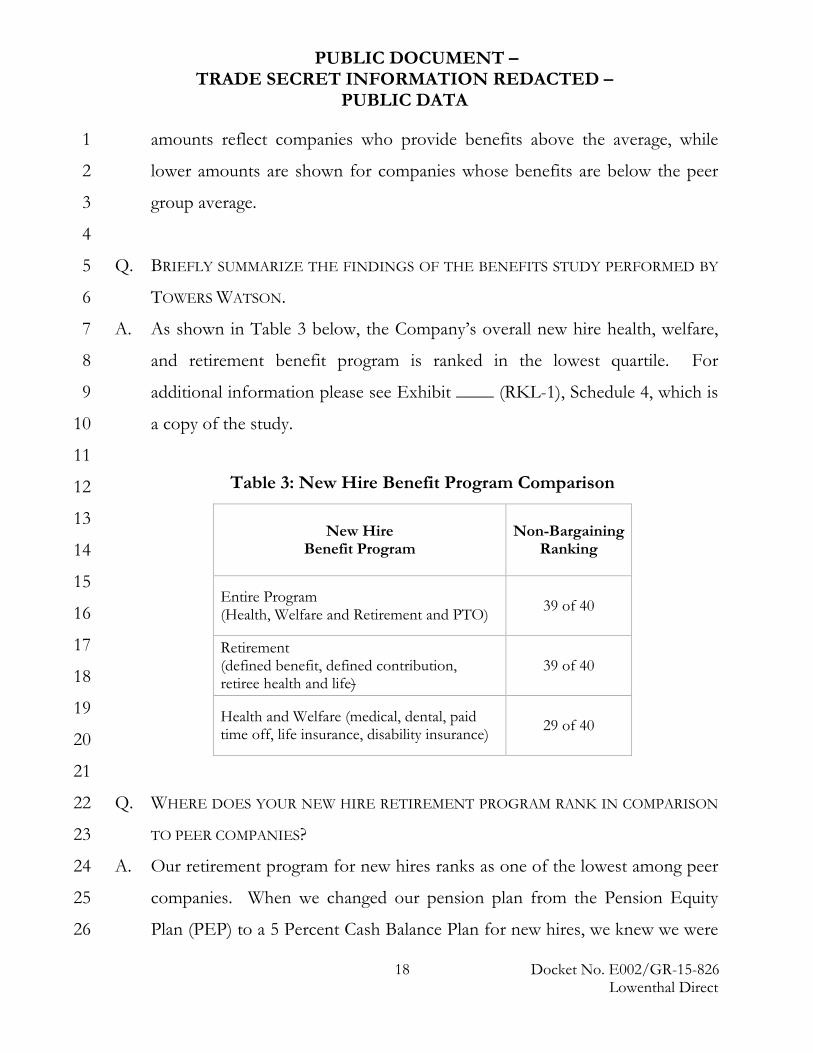

Q. BRIEFLY SUMMARIZE THE FINDINGS OF THE BENEFITS STUDY PERFORMED BY 5

TOWERS WATSON. 6

A. As shown in Table 3 below, the Company’s overall new hire health, welfare, 7

and retirement benefit program is ranked in the lowest quartile. For 8

additional information please see Exhibit ____ (RKL-1), Schedule 4, which is 9

a copy of the study. 10

11

12

13

14

15

16

17

18

19

20

21

Q. WHERE DOES YOUR NEW HIRE RETIREMENT PROGRAM RANK IN COMPARISON 22

TO PEER COMPANIES? 23

A. Our retirement program for new hires ranks as one of the lowest among peer 24

companies. When we changed our pension plan from the Pension Equity 25

Plan (PEP) to a 5 Percent Cash Balance Plan for new hires, we knew we were 26

Table 3: New Hire Benefit Program Comparison

New Hire Benefit Program

Non-Bargaining Ranking

Entire Program (Health, Welfare and Retirement and PTO) 39 of 40

Retirement (defined benefit, defined contribution, retiree health and life)

39 of 40

Health and Welfare (medical, dental, paid time off, life insurance, disability insurance) 29 of 40

18 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

leading the industry with the reduction in our pension benefit level. 1

Ultimately, we thought that we would be closer to the median once other 2

companies began making the same type of pension benefit reductions. 3

However, we have found that our peer companies have not moved as quickly 4

as Xcel Energy with this particular change. 5

6

Q. WHAT DO THE TWO STUDIES SHOW INSOFAR AS THE COMPANY’S OVERALL 7

CASH COMPENSATION AND BENEFITS PROGRAMS ARE CONCERNED? 8

A. The two studies demonstrate that the Company’s overall level of 9

compensation and benefits is at or below the median level of total 10

compensation and benefits offered by peer companies. We believe an overall 11

level of total rewards that is at or slightly below the median strikes a fair 12

balance between the interests of the Company and its customers. 13

14

IV. TOTAL REWARDS PROGRAM COST MITIGATION 15 MEASURES AND RESOURCE REALIGNMENT 16

17

A. Cost Mitigation Measures 18

Q. YOU MENTIONED THE COMPANY HAS TAKEN STEPS TO MANAGE THE TOTAL 19

REWARDS PROGRAM COSTS. CAN YOU EXPAND ON THAT STATEMENT? 20

A. Yes. We continually monitor our compensation to ensure it is competitive 21

with the market, and we make changes as necessary. As a result of these 22

evaluations, we have recently made design modifications to our AIP, PTO, 23

health and welfare benefits, and retirement benefits. 24

25

Q. HOW HAS THE AIP BEEN MODIFIED IN RECENT YEARS? 26

A. We have taken the following actions within the past four years: 27 19 Docket No. E002/GR-15-826

Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

• We eliminated AIP payments to non-exempt, non-bargaining 1

employees, who previously were included in the AIP at a six percent 2

target payout percentage. 3

• We eliminated our Control Room Operators from the AIP program 4

when we determined they no longer met the overtime exemption test. 5

• We eliminated eligibility for employees hired on or after October 1 of a 6

program year because they have not been in the job long enough to 7

produce results for that year. 8

• We prorate incentive awards for employee job movement that results 9

in a change in incentive opportunity. 10

• We added a provision that employees must be employed with Xcel 11

Energy on the actual date the AIP is paid. 12

• We eliminated all incentive pay for any employee who did not meet 13

acceptable levels of performance. 14

15

Q. DISCUSS SOME OF THE MEASURES THE COMPANY HAS TAKEN TO MANAGE THE 16

COSTS ASSOCIATED WITH THE HEALTH AND WELFARE BENEFITS. 17

A. The Company has made the following design changes: 18

• We have reduced the number of health insurance plans available to 19

employees from four to one. Since 2009, the only medical plan that the 20

Company has made available to employees is the HDHP plan I 21

described earlier. 22

• Beginning in 2011, the Company increased employees’ out-of-pocket 23

costs in the HDHP by introducing co-insurance, which means that 24

even after meeting their high deductible, our employees continue to 25

20 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

pay co-insurance on additional medical and pharmacy claims up to 1

$3,500 per individual or $7,000 per family. 2

• Beginning in 2011, the Company implemented pharmacy cost-3

containment programs that require employees to pay additional out-of-4

pocket expenses if they choose to purchase drugs in a less cost-5

effective manner. Over the years, the Company has added program 6

requirements to manage exposure to increasing drug costs, such as 7

prior drug authorization, step therapy programs and drug exclusions 8

related to specific compound drugs. 9

• In 2012, the Company lowered the plan costs by reducing the 10

Company/employee cost split from 80 percent to 75 percent under the 11

HDHP, shifting a greater portion of the cost to employees in the form 12

of premiums. 13

• In 2015, the Company kept pace with benefit trends by subsidizing 14

dependent coverage less than employee coverage, resulting in 15

additional cost to employees in the form of increased premiums. 16

• In 2010, adult orthodontia coverage was eliminated from the non-17

bargaining and bargaining dental plans. 18

• In 2011, the Short-Term Disability program was reduced from 100 19

percent income replacement for 26 weeks to 100 percent for the first 20

13 weeks, and then 70 percent of income replacement for the 21

remaining 13 weeks. 22

• In 2012, the Company launched a new wellness program, My Health 23

Choices, to further drive toward a healthier employee population 24

through wellness education and lifestyle changes. 25

21 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

• In 2015, the Company reduced our PTO liability by eliminating a PTO 1

Buy and Sell Program that allowed employees to purchase more and 2

return unused PTO. This legacy benefit was underutilized as originally 3

designed and was no longer administratively cost-effective. 4

• Since our last rate case filing in 2013, our annual deductibles for our 5

non-bargaining employees increased by $250 and $500 for individual 6

and family coverage, respectively. 7

8

Q. WHAT HAS BEEN THE EFFECT OF THESE CHANGES? 9

A. While many of these changes have directly increased costs for our employees, 10

they have also allowed the Company to better manage overall healthcare costs 11

and the rate at which our costs increase. Employee contributions to health 12

and welfare benefits have increased, but the ways in which our employees 13

access healthcare and consume healthcare services have also improved. For 14

example, we have seen improved use of urgent care facilities as opposed to 15

hospital emergency room visits for acute injuries and illness, and we also have 16

a very high rate of generic prescription drug use. This change in behavior has 17

the potential to mitigate healthcare cost increases for the Company as well as 18

the employees. 19

20

Although it is difficult to identify direct savings from these changes, the intent 21

of the plan modifications was to mitigate cost increases on a long-term basis, 22

in part by motivating employees to be more cost-conscious consumers of 23

medical and dental care, but also to live healthier lifestyles. We also know 24

that it can take time to see cost impacts resulting from program design 25

changes and that health care reform presents us with some unknown impacts 26

22 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

to our costs. Based upon the cost trends discussed by Company witness Mr. 1

Richard R. Schrubbe, it appears that our efforts to slow the pace of health 2

care cost increases are succeeding. 3

4

Q. WHAT ELSE HAS THE COMPANY DONE IN REGARD TO COSTS ASSOCIATED 5

WITH THE HEALTH AND WELFARE BENEFITS? 6

A. We have increased communications around a series of programs that have 7

been designed to help control our costs by improving the overall health and 8

welfare of our employees. These programs include counseling and coaching 9

for plan members who are seeking treatment for a condition, engaging plan 10

members proactively to help modify behaviors and health risks, and providing 11

education materials to help plan members make informed decisions. 12

13

The Company also renegotiates contracts with benefit vendors on an ongoing 14

basis. These negotiations focus on administrative fee reductions, better 15

performance guarantees and rebates, and improved discounts on provider 16

networks. All contribute to our ability to mitigate the increasing healthcare 17

costs and benefit administration costs charged by third parties, which limit the 18

impact of the cost of doing business for our customers. 19

20

Q. WHAT ADDITIONAL PLANS DOES THE COMPANY HAVE TO HELP MITIGATE 21

HEALTH AND WELFARE COSTS? 22

A. The Company is closely examining emerging benefit design strategies that 23

would drive our employees and their covered family members to high quality, 24

cost-efficient healthcare providers. We are following marketplace activity 25

23 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

changes that are a result of healthcare reform and assessing the resulting 1

impact to our employer-provided coverage. 2

3

We are also assessing programs that will provide more cost-effective 4

opportunities for employees. For example, we are looking at telemedicine 5

options, such as mobile, desktop or telephonic healthcare access for routine 6

visits. These non-traditional visits with a trained physician are convenient and 7

provide a less expensive option for employees and the Company. We are also 8

looking at Centers of Excellence that focus on specialty orthopedic 9

procedures such as spinal fusions, knee and hip replacements. This type of 10

specialty care model provides patient support and education in tandem with 11

high quality and lower cost services. We continue to review the possibility of 12

increasing medical premiums for those employees and their dependents who 13

use tobacco products, increasing their health risks. 14

15

Q. HAS THE COMPANY UNDERTAKEN ANY INITIATIVES TO REDUCE THE COSTS OF 16

ITS DEFINED BENEFIT PENSION EXPENSE? 17

A. Yes. We made the following changes to our defined benefit plan: 18

• Effective January 1, 2011, bargaining employees who are hired, rehired 19

and transferred into the bargaining unit on or after January 1, 2011 are 20

no longer eligible for the 10 percent PEP. Instead, these employees 21

participate in a 5 Percent Cash Balance Plan formula without pension 22

supplements (i.e., Retirement Savings Account or Social Security 23

Supplement). 24

• Effective January 1, 2012, non-bargaining new hires and rehired 25

employees hired on or after January 1, 2012, are no longer eligible for 26

24 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

the 10 percent PEP. Instead, these employees participate in a 5 1

Percent Cash Balance Plan formula without pension supplements (i.e., 2

Retirement Savings Account or Social Security Supplement). 3

4

Q. HAS THE COMPANY UNDERTAKEN ANY INITIATIVES TO REDUCE THE COSTS OF 5

ITS RETIREE MEDICAL EXPENSE? 6

A. Yes. We completed a thorough evaluation of the healthcare options available 7

to Medicare-eligible retirees through the individual market related to medical 8

and prescription drug coverage, and we found that those plans provide broad, 9

comprehensive coverage at affordable costs. Therefore, we took a new 10

approach effective January 1, 2013 to transition our Medicare-eligible retirees 11

and their Medicare-eligible spouses and dependents from the Company plan 12

options to the individual market. 13

14

These initiatives reduced the Company’s financial liability and administrative 15

responsibilities, and it gave us the opportunity for significant cost savings for 16

retiree groups that still had premium subsidies. 17

18

Q. HAVE THESE INITIATIVES RESULTED IN REDUCED RETIREE MEDICAL 19

EXPENSE? 20

A. Yes, as discussed by Mr. Schrubbe, these actions have reduced retiree medical 21

expense. 22

23

Q. PLEASE SUMMARIZE THE MOST RECENT CHANGES TO THE COMPANY’S 24

RETIREMENT PROGRAM. 25

25 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

A. We continually monitor and evaluate our retirement program to ensure we 1

align with the market as well as our workforce needs. This effort has resulted 2

in a number of modifications that have resulted in steadily lower total pay 3

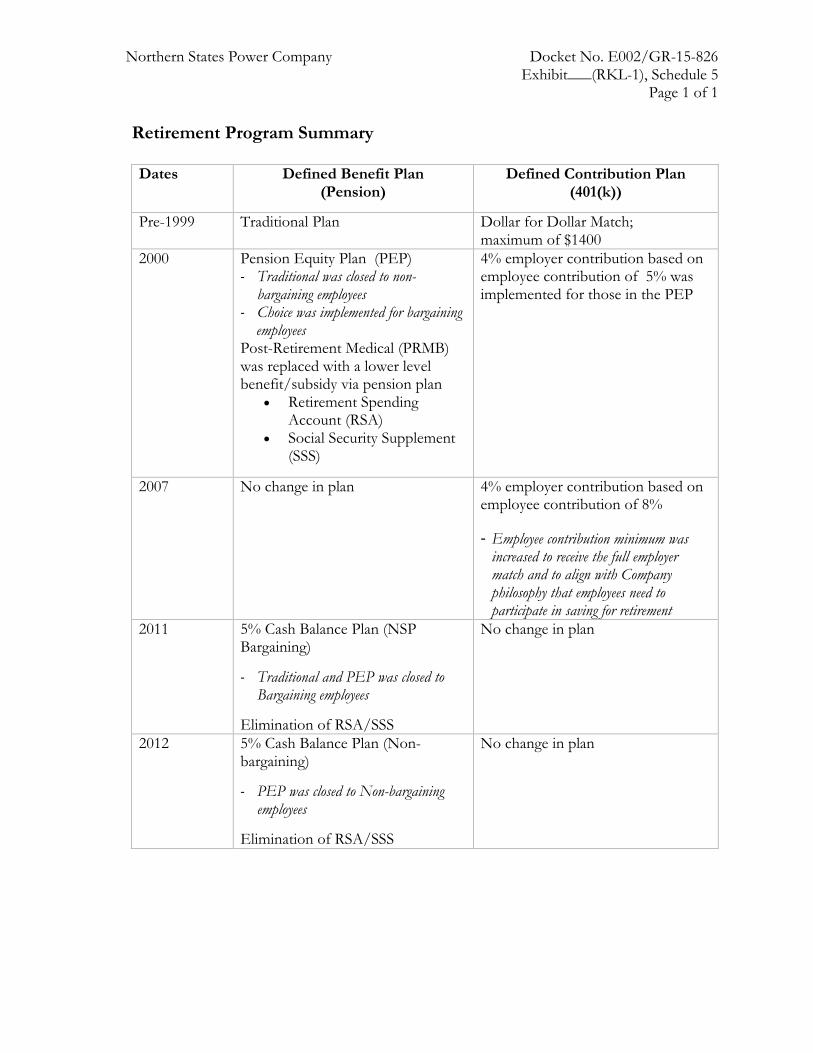

replacement income levels for employees. Exhibit___(RKL-1), Schedule 5 4

identifies our efforts to date. 5

6

B. Resource Realignment 7

Q. IN ADDITION TO THE COST SAVING INITIATIVES DISCUSSED ABOVE, YOU ALSO 8

MENTIONED SOME RESOURCE REALIGNMENT EFFORTS THE COMPANY HAS 9

UNDERTAKEN. CAN YOU EXPLAIN WHAT YOU MEAN BY THAT? 10

A. Yes. In an effort to get the most value out of our existing program, we have 11

evaluated opportunities to focus our resources more strategically. For 12

instance, we have recently initiated greater emphasis on strengthening the 13

linkage between employee pay and performance, thereby providing larger 14

awards to our highest performers. 15

16

Another way in which we have aligned our resources more strategically is by 17

undertaking an effort to develop and transfer the knowledge necessary to run 18

our business successfully with our existing workforce, despite our increasing 19

attrition levels. Although we have always had knowledge transfer tools in 20

place, our forecasted attrition levels discussed later in my testimony have 21

caused us to refocus and heighten our efforts in this area to ensure we are 22

prepared for the future. These steps include proactively identifying critical 23

near-term retirements and succession opportunities to ensure these changes 24

do not leave areas of vulnerability. We also have formal leadership, rotational, 25

and technical skill training programs. While these efforts will not completely 26

26 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

offset our attrition levels, they are better preparing us for the upcoming loss 1

of knowledge. 2

3

Q. PLEASE DESCRIBE THE PAY-FOR-PERFORMANCE PHILOSOPHY. 4

A. The Company has had a long-standing pay-for-performance philosophy 5

which further correlates rewards with work expectations and performance 6

make an even greater distinction between exceptional work and successful 7

work. Consequently, those employees who are performing at levels less than 8

satisfactory will receive far less pay. This philosophy serves to motivate 9

higher performance, set clearer expectations, and recognize and drive 10

continuous improvement. Our renewed emphasis in this area has not 11

affected our overall need for greater compensation levels; it merely targets 12

spending our resources more strategically. 13

14

Q. HASN’T THE COMPANY ALWAYS LINKED MARKET-COMPETITIVE 15

COMPENSATION TO PERFORMANCE? 16

A. Yes. However, this new effort places a greater emphasis on strengthening the 17

link between employee pay and performance, thereby providing larger 18

rewards to our highest performers. We believe practicing greater pay 19

differentiation will help motivate and raise performance levels. 20

21

Q. CAN YOU DISCUSS THE STEPS THE COMPANY IS TAKING TO DEVELOP AND 22

TRANSFER KNOWLEDGE? 23

A. Yes. As discussed further below, our forecasted attrition levels have caused 24

us to refocus and heighten our efforts in this area to ensure we are prepared 25

for the future. Accordingly, we are taking a number of steps to ensure that we 26

27 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

are developing and capturing the knowledge and skills needed to run our 1

systems effectively, including the following: 2

• Apprenticeships. We have more than 30 apprenticeship programs across 3

our generation, transmission, and distribution functions. In these 4

apprenticeship programs, which may span two to four years, employees 5

receive formal and on-the-job training to develop technical skills, and 6

we have oversight committees to measure the employees’ development 7

and progress. 8

• Technical Skills. We provide training programs that support more than 9

1,400 qualification programs to ensure employees’ technical skills are 10

maintained, and we film specialized subject matter experts performing 11

key plant functions and technical activities in order to preserve that 12

knowledge for future employees. 13

• Knowledge Transfer. We have a self-directed knowledge transfer process 14

in place to ensure that key information is documented and transferred 15

from one employee to another employee. The goal of the process is to 16

help managers identify, prioritize, and transfer critical knowledge from 17

employees who are leaving the organization due to retirement or other 18

forms of attrition. 19

• Leadership Program. We have a pre-supervisory leadership development 20

program and a core leadership program. We also have a leadership 21

succession plan with development plans for successors for critical 22

positions. In the past few years, we added a frontline leadership 23

development program, we continue to enhance our new leader 24

development program, and we created a high-potential development 25

program. Since 2011, there have been 452 participants in our pre-26 28 Docket No. E002/GR-15-826

Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

leadership program, resulting in 150 promotions to leadership 1

positions. An additional 56 employees were developed and accepted 2

other jobs within the Company. 3

• Rotational Programs. Many business areas have rotational programs in 4

which employees learn different skills that enable knowledge transfer. 5

• e-Learning. We have more than 50 e-learning options on non-technical 6

topics. 7

• Productivity through Technology. As discussed by Company witness Mr. 8

David C. Harkness, we are currently going through a multi-year project 9

to upgrade our technology and redesign business processes and 10

procedures with thorough documentation. This project will drive 11

greater effectiveness and will also provide a long-term documentation 12

platform providing for improved knowledge transfer across the 13

Company. Upon completion, this project should aid in the growth and 14

development of newer employees who will fill openings created by 15

retirees and normal attrition. 16

17

Q. DO THESE INITIATIVES ENSURE THAT THE COMPANY WILL BE ABLE TO OFFSET 18

THE DETRIMENTAL EFFECTS OF ATTRITION? 19

A. No. These initiatives will help us impart, preserve, and transfer knowledge, 20

but they must be offered in tandem with a compensation package that is 21

sufficient to attract and retain employees. 22

23

Q. HAS THE COMPANY STRATEGICALLY TARGETED ANY EFFORTS TO ADDRESS 24

RECRUITING CHALLENGES? 25

29 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

A. Yes. The Company has developed a number of creative ways to address our 1

recruiting challenges and target our resources most effectively. For example, 2

we have an award-winning program expressly designed to recruit and hire 3

veterans of the United States armed forces.2 We actively recruit veterans 4

because their skills translate well to a utility environment, and their work ethic 5

and leadership skills are outstanding. Employees with military service 6

demonstrate leadership skills, high performance standards, and commitment 7

to teamwork. Currently, about 10 percent of Xcel Energy’s employees are 8

military veterans, with many represented in management, but the need for 9

new, qualified employees grows with more than half of our workforce eligible 10

to retire over the next ten years. 11

12

Q. WHAT DO YOU CONCLUDE ABOUT THE COMPANY’S TOTAL REWARDS 13

PROGRAM DESIGN CHANGES AND RESOURCE REALIGNMENT INITIATIVES? 14

A. The Company has undertaken a variety of initiatives to manage our expenses 15

and we believe these initiatives have been successful and allowed the 16

Company to better manage overall Total Rewards Program costs. 17

18

V. RESULTING CHALLENGES 19

20

Q. WHAT CHALLENGES IS THE COMPANY FACING AS A RESULT OF THE UNDER-21

RECOVERY OF COSTS, COST MITIGATION EFFORTS, AND OFFERING 22

COMPENSATION THAT IS AT, OR BELOW, MARKET LEVELS? 23

2 Xcel Energy was named one of GI Jobs’ Top 100 Military Friendly Employers for the last five years and won the Most Valuable Employer for Military by CivilianJobs.com. 30 Docket No. E002/GR-15-826

Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

A. The Company is facing a multitude of challenges with respect to its workforce 1

and our need to offer competitive compensation and benefits is greater than 2

ever. The electric industry is becoming more complex and technically 3

demanding. At the same time, we are facing more competition than ever for 4

the employees who have the skills and training to fulfill those roles in the 5

Company. Moreover, a significant portion of the Company’s workforce is 6

eligible for retirement, which makes it imperative for us to hire, train, and 7

retain new employees as well as retain those who are retirement eligible so 8

that knowledge transfer can occur. 9

10

Q. DO YOU HAVE A BREAKDOWN OF YOUR OVERALL WORKFORCE? 11

A. Yes. More than 75 percent of the Company’s employees based in Minnesota 12

are linemen, engineers, plant system operators, and other employees in skilled 13

field positions. The remaining employees support our customers, regulators, 14

investors, other employees, and the administration of our business. 15

16

Q. WHAT TYPES OF SKILLS ARE NECESSARY TO PERFORM THESE JOBS? 17

A. We expect our employees to have a variety of technical, communication, 18

interpersonal and educational skills. From skilled technical positions through 19

the Company’s senior management team, the requisite skill-set bar is high. 20

For example, our Cyber Security Program Manager job requires a Bachelor’s 21

degree in Management Information Systems, Computer Science or 22

Engineering, and it also requires five years of cyber security-related risk 23

management or compliance experience, including proven success defining 24

business and technical security or compliance solutions. 25

26

31 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

Q. WITH WHOM DOES XCEL ENERGY COMPETE FOR QUALIFIED EMPLOYEES? 1

A. Xcel Energy competes for talent within both the utility and the non-utility 2

sectors. Utility sector competition generally takes place for jobs specific to 3

utility operations and the delivery of utility services, such as engineers, plant 4

operators, technicians, welders, and machinists. We also compete with other 5

utilities for corporate employees such as regulatory accountants and load 6

forecasters. In addition, we compete with non-utility employers for jobs that 7

are not specific to utilities, such as finance and accounting analysts, marketing 8

analysts, designers, information technology specialists, human resource 9

generalists, and customer service representatives. 10

11

A. Hiring Challenges 12

Q. PLEASE DESCRIBE AT A HIGH LEVEL THE RECRUITING CHALLENGES THAT THE 13

COMPANY FACES. 14

A. Prospective employees with the specific skill sets and training required for 15

technical or specialized careers are in high demand. There is a limited pool of 16

candidates, and the Company competes for them on a national, regional and 17

local basis. In fact, some of the employee positions that we need to fill, such 18

as electrical engineers and nuclear technicians, are in such high demand that 19

their salaries are growing faster than the salaries of other positions. Due to 20

the unique nature of many of our highly technical utility jobs, we need to hire 21

experienced employees that can perform in their roles quickly as opposed to 22

being able to use entry-level talent. 23

24

Q. ARE THERE ANY UNIQUE RECRUITING CHALLENGES WITHIN THE STATE OF 25

MINNESOTA? 26

32 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

A. Yes. According to the Bureau of Labor Statistics, Minnesota had a 3.9 1

percent unemployment rate in June 2015, the eighth lowest in the country and 2

well below the national average of 5.3 percent. In July 2014, Minneapolis had 3

a jobless rate of 4.0 percent, the lowest jobless rate in the nation among large 4

metropolitan areas.3 According to the Minnesota Department of Employment 5

and Economic Development, Minnesota has more Fortune 500 firms per 6

capita than all but one state,4 and Minnesota is tied for eleventh-most Fortune 7

500 companies in the nation.5 In 2015, the 17 Fortune 500 companies in the 8

state include some of the world’s most recognized brands and firms, such as 9

3M and General Mills, with whom we compete for engineers, IT, marketing, 10

and other skilled employees. 11

12

We also compete for talent with many other large employers that have a 13

significant presence in Minnesota but are no longer headquartered in 14

Minnesota or are privately held and are not included on the Fortune 500 list, 15

such as Medtronic, Spartan Nash, and Cargill. In 2015, there are also eight 16

additional Fortune 1000 companies headquartered in Minnesota, mainly in the 17

Minneapolis-St Paul area.6 Recently, CNBC named Minnesota “America’s 18

Top State for Business” for 2015, moving up from number 6 in 2014, based 19

on the highest combined score from ten categories.7 20

3 See http://www.startribune.com/twin-cities-jobless-rate-is-the-lowest-for-large-u-s-metro-area/265471401/ (accessed on Aug. 17, 2015). 4 See http://mn.gov/deed/business/locating-minnesota/companies-employers/fortune500.jsp (accessed on Aug. 28, 2015). 5 See http://mn.gov/deed/business/locating-minnesota/companies-employers/fortune500.jsp (accessed on Aug. 28, 2015). 6 See http://www.geolounge.com/fortune-1000-companies-list-for-2015/ (accessed on Aug. 31, 2015) 7 See http://mn.gov/deed/newscenter/social-media/blogs/deed-developments/blog-entry.jsp?id=466-166368 (accessed on Aug. 31, 2015). 33 Docket No. E002/GR-15-826

Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

1

In addition, there are five other investor-owned electric utilities that serve 2

Minnesota, as well as more than 40 cooperatives and more than 20 municipal 3

providers with whom we also compete for talent.8 Finally, the costs of labor 4

in Minneapolis and St. Paul are 10 percent above the national average. 5

6

Q. ARE SOME TYPES OF JOBS HARDER TO FILL THAN OTHERS? 7

A. Yes. According to Forbes magazine, Minnesota is the fastest-growing state for 8

tech jobs, and the STEM jobs are in high demand across Minnesota as well.9 9

This shortage of skilled technical talent is accelerating wages for these job 10

categories faster than other areas. 11

12

Q. DO YOU HAVE ANY EXAMPLES OF THE COMPANY’S RECRUITING CHALLENGES 13

AS FAR AS TECHNICAL POSITIONS ARE CONCERNED? 14

A. Yes. In 2014, the Company filled 495 jobs with external candidates. Of 15

these, 62 jobs that fell mainly in technical areas were open for 130 days or 16

more (actual average for this group of jobs was 185 days open), although our 17

average time to fill a job during this period was 65 days. Jobs such as 18

Lineman (147 days), Senior Turbine Engineer (218 days), Transmission 19

Superintendent (145 days), Senior Information Systems Auditor (189 Days) 20

and Field Construction Manager (134 days) were particularly difficult to fill. 21

8 See http://mn.gov/puc/electricity/utility-companies/cooperatives/index.html and http://mn.gov/puc/electricity/utility-companies/municipals/index.html (accessed on Aug. 21, 2015) 9 See http://www.forbes.com/sites#/sites/susanadams/2015/08/18/the-fastest-growing-states-for-tech-jobs-in-2015/ (accessed on Oct. 23, 2015)

34 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

The length of time these jobs have remained open is evidence of the active 1

and robust job market in Minnesota for technical positions. 2

3

From the examples above, the Company received 28 applicants for the Senior 4

Turbine Engineer opening during this period, but only four candidates met 5

the minimum qualifications for the job. The Company offered the job to 6

three successive candidates and received declines from the first two 7

candidates due to either salary or personal reasons, before receiving final 8

acceptance. Regarding the Transmission Superintendent opening, the 9

Company received 25 applicants with eight qualified candidates meeting the 10

minimum job requirements. After interviews with four of the candidates, the 11

Company made an offer, then had to counteroffer with a higher salary, before 12

the candidate finally accepted. 13

14

Q. WHY IS IT SO DIFFICULT FOR THE COMPANY TO ATTRACT THOSE TYPES OF 15

EMPLOYEES? 16

A. The short answer is that our compensation is not high enough compared to 17

the companies with whom we compete for employees. With respect to 18

engineers, for example, we compete not only with other utilities, but also with 19

consulting firms that generally offer significantly higher pay and benefits, 20

according to feedback we receive from candidates and search firms. Because 21

of the highly technical nature of the engineering responsibilities at Xcel 22

Energy, we must often hire engineers with a senior level of experience, which 23

is difficult to accommodate in our pay range. For instance, in 2013 and 2014, 24

we hired 107 candidates for engineering-related professional and leadership 25

positions in Minnesota. The average time to fill these jobs was 105 days from 26

35 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

the initiation of the process through offer acceptance. Nineteen of these 1

positions were open for more than 200 days. 2

3

Another example relates to our search for an Engineering Supervisor for our 4

Nuclear area. This position has been open since September 17, 2014. There 5

were 18 candidates from the applicant pool who met the minimum job 6

requirements and advanced to our leader assessment process, which measures 7

the candidate’s leadership skills and competencies. Upon completion of our 8

review, only three of the candidates were deemed suitable. We made offers to 9

two of these candidates, but both rejected our offer. This job remained 10

unfilled for more than nine months. 11

12

We struggled to fill a number of other jobs that were open for more than 200 13

days, including a Safety and Training Consultant position that required 14

multiple offers before a candidate accepted; a Journeyman Lineman position 15

for which eight candidates pulled out of the process before an offer was 16

accepted; and a Senior Information Technology Business Manager position 17

that had six candidates who withdrew from consideration or rejected our 18

offer before we filled the position. 19

20

Q. DOES THE COMPANY CURRENTLY HAVE JOB OPENINGS THAT ARE PROVING 21

DIFFICULT TO FILL? 22

A. Yes. We have 122 current openings in Minnesota, with three openings 23

having been very difficult to fill: Senior Engineer for Energy Supply, SAP 24

Implementation Business Integration Manager for Business Systems, and 25

Bargaining Apprentice System Relay Specialist for Utilities. On average, 26

36 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

these jobs have been open for more than 165 days. In the case of the Senior 1

Engineer, only one of the 176 candidates met the combustion turbine 2

specialty requirements for the job, but that candidate was not willing to 3

work for the salary level we were willing to offer. 4

5

Q. THE MEDIA HAS REPORTED THAT OTHER COMPANIES IN MINNESOTA HAVE 6

RECENTLY HAD LAY-OFFS. HAS THE COMPANY BEEN ABLE TO REDUCE ITS 7

HIRING CHALLENGES BY HIRING SOME OF THOSE LAID-OFF WORKERS? 8

A. No. Many of the employees who were laid off by other employers in 9

Minnesota do not have the technical skills that our Company needs for the 10

jobs that are hardest to fill. And those employees who have those technical 11

skills are in such high demand that their salary expectations exceed what we 12

are able to pay. 13

14

Q. YOU TESTIFIED EARLIER THAT THE COMPANY ALSO FACES REGIONAL 15

RECRUITING ISSUES. WHAT ARE THOSE ISSUES? 16

A. The robust job market in neighboring states has made it more difficult to 17

recruit employees. In recent months the unemployment rates in North 18

Dakota and South Dakota have stood at 3.1 percent and 3.8 percent, 19

respectively, the second lowest and sixth lowest rates in the nation.10 In fact, 20

the demand for workers in North Dakota has caused the average annual wage 21

in the oil and gas industry to exceed $111,400 in some parts of the state.11 22

23

10 See http://www.bls.gov/web/laus/laumstrk.htm (accessed on Aug 17, 2015). 11 See http://www.washingtontimes.com/news/2014/jul/9/job-service-oil-counties-tops-in-n-dakota-wages/?page=all#! (accessed on Aug. 17, 2015). 37 Docket No. E002/GR-15-826

Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

Q. AT A NATIONAL LEVEL, WHAT IS DRIVING THE INCREASE IN COMPETITION IN 1

THE COMPANY’S LABOR MARKET? 2

A. There are several developments on a national level that are making it more 3

difficult to recruit qualified applicants. 4

5

For instance, the nuclear industry is facing a shortage of experienced and 6

highly-skilled workers. We have had difficulty hiring for nuclear operations 7

positions because employees with utility and nuclear generation-related 8

experiences are in short supply. Working at nuclear plants requires an 9

extensive set of specific skills, knowledge and expertise on specialized 10

equipment, and the demand for this unique skill set exists in the nuclear 11

industry both nationally and internationally. The persistent demand for 12

nuclear employees has caused and continues to cause compensation 13

expectations of nuclear professionals to rise in comparison to other 14

professional areas. There will be increased pressure going forward to match 15

perceived compensation levels and to attract employees with what they 16

believe is a competitive offer. 17

18 In addition, there is a highly competitive national market for skilled talent 19

with cyber security experience, and there is a limited pool of qualified 20

candidates. Cyber security attacks on information systems are becoming 21

increasingly common, and threats to information security can significantly 22

impact any business by interrupting service and losing customer confidence 23

when data breaches or unplanned outages occur. To defend against emerging 24

threats, we are raising the level of employee expertise and sophistication of 25

our critical systems by making investments in our people and our technology. 26

38 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

Xcel Energy has more than 50 critical systems that are deemed to be required 1

for delivery of our gas and electric services, satisfaction of regulatory 2

compliance requirements, and continuation of core business functions. We 3

are competing for these employees with other businesses who are facing 4

similar threats to their information systems. 5

6

B. Retention Challenges 7

Q. PLEASE DESCRIBE THE RETENTION ISSUES FACING THE COMPANY. 8

A. Many of our retention issues are related to our recruiting challenges. Just as 9

we have a need for skilled candidates, so do other utilities and energy industry 10

participants. Many of our employees are viable candidates for other utilities 11

and energy industry participants because of the experience, knowledge and 12

skills they have acquired while working for the Company. 13

14

For example, in the fall of 2014, we graduated ten new Senior Reactor 15

Operators from a two-year class. This class, which is conducted internally 16

and accredited by the Nuclear Regulatory Commission, is considered to be 17

one of the most difficult classes in the industry. The candidates had several 18

years of nuclear experience and were selected to be part of our future Control 19

Room Supervisory team that would ultimately assume the responsibilities 20

currently held by several of our seasoned and retiring leadership staff. Since 21

graduation from the class, we have lost two of the candidates to other nuclear 22

facilities, creating a strain on our shrinking operator pool and our training 23

resources. 24

25

Q. DO YOU HAVE CONCERNS OVER ATTRITION LEVELS WITHIN THE COMPANY? 26

39 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

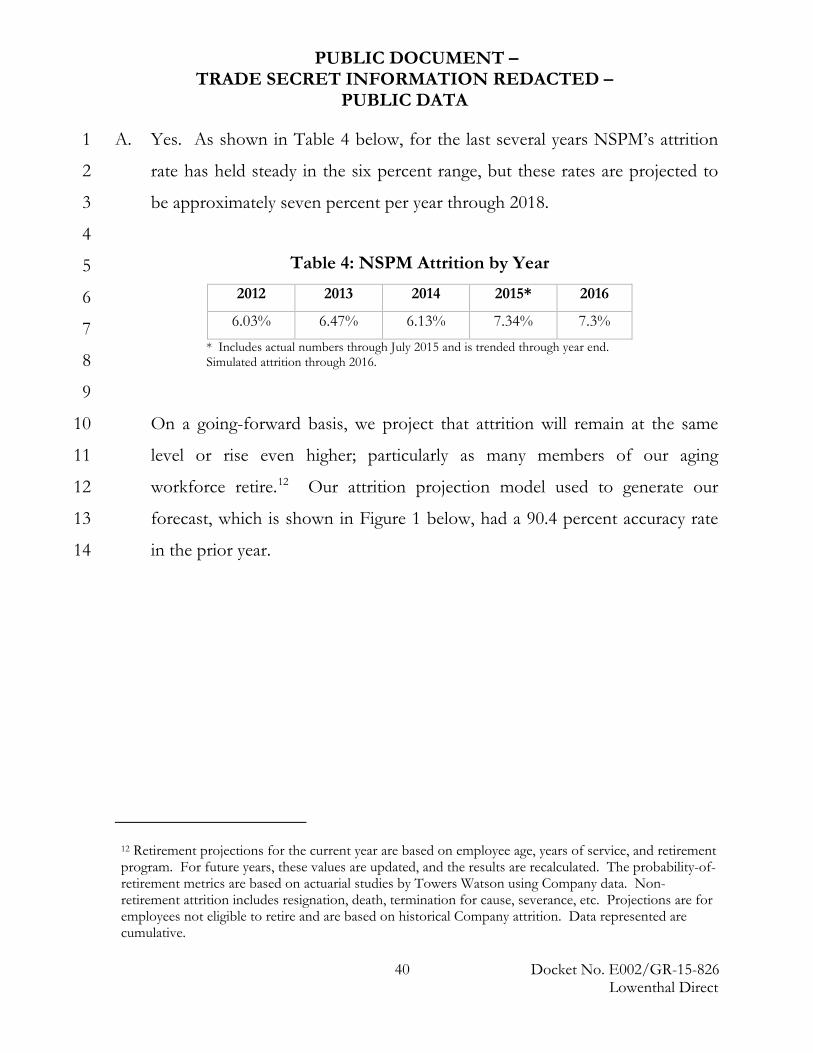

A. Yes. As shown in Table 4 below, for the last several years NSPM’s attrition 1

rate has held steady in the six percent range, but these rates are projected to 2

be approximately seven percent per year through 2018. 3

4

5

6

7

8

9

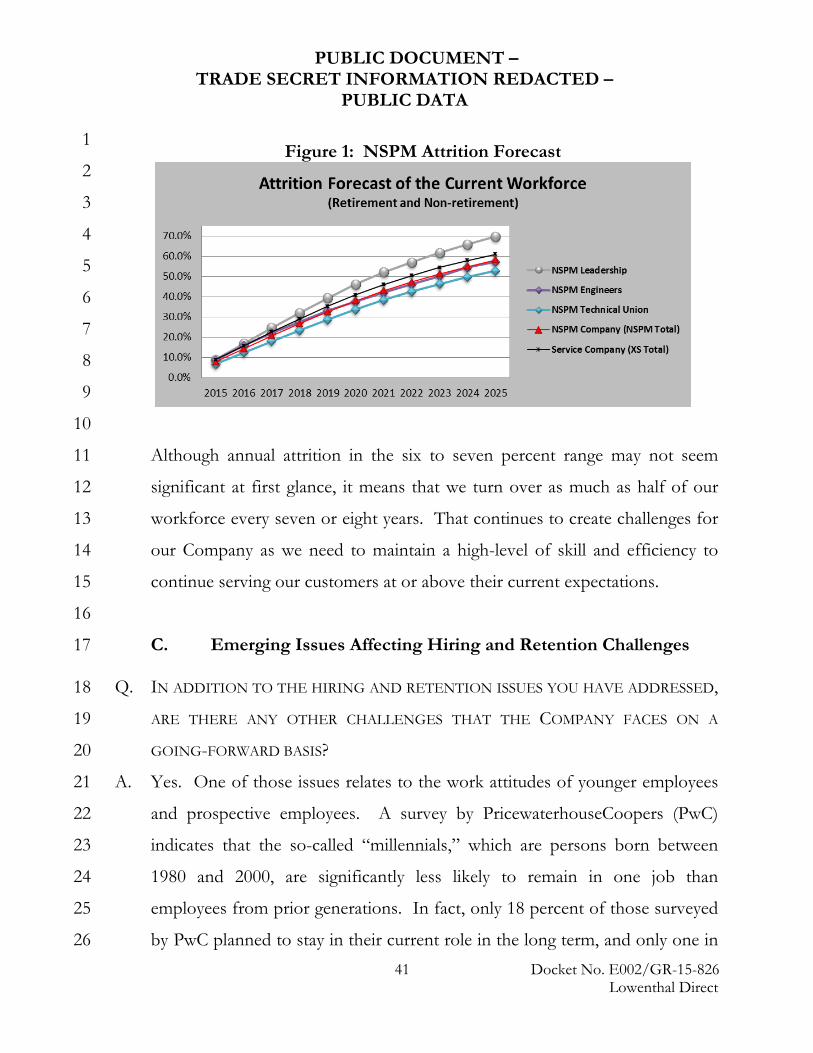

On a going-forward basis, we project that attrition will remain at the same 10

level or rise even higher; particularly as many members of our aging 11

workforce retire.12 Our attrition projection model used to generate our 12

forecast, which is shown in Figure 1 below, had a 90.4 percent accuracy rate 13

in the prior year. 14

12 Retirement projections for the current year are based on employee age, years of service, and retirement program. For future years, these values are updated, and the results are recalculated. The probability-of-retirement metrics are based on actuarial studies by Towers Watson using Company data. Non-retirement attrition includes resignation, death, termination for cause, severance, etc. Projections are for employees not eligible to retire and are based on historical Company attrition. Data represented are cumulative.

Table 4: NSPM Attrition by Year

2012 2013 2014 2015* 2016

6.03% 6.47% 6.13% 7.34% 7.3%

* Includes actual numbers through July 2015 and is trended through year end. Simulated attrition through 2016.

40 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

1

2

3

4

5

6

7

8

9

10

Although annual attrition in the six to seven percent range may not seem 11

significant at first glance, it means that we turn over as much as half of our 12

workforce every seven or eight years. That continues to create challenges for 13

our Company as we need to maintain a high-level of skill and efficiency to 14

continue serving our customers at or above their current expectations. 15

16

C. Emerging Issues Affecting Hiring and Retention Challenges 17

Q. IN ADDITION TO THE HIRING AND RETENTION ISSUES YOU HAVE ADDRESSED, 18

ARE THERE ANY OTHER CHALLENGES THAT THE COMPANY FACES ON A 19

GOING-FORWARD BASIS? 20

A. Yes. One of those issues relates to the work attitudes of younger employees 21

and prospective employees. A survey by PricewaterhouseCoopers (PwC) 22

indicates that the so-called “millennials,” which are persons born between 23

1980 and 2000, are significantly less likely to remain in one job than 24

employees from prior generations. In fact, only 18 percent of those surveyed 25

by PwC planned to stay in their current role in the long term, and only one in 26

Figure 1: NSPM Attrition Forecast

41 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

five (21 percent) said they would like to stay in the same field and progress 1

with one employer.13 Because of the significant amount of training necessary 2

to perform many of the jobs that are most challenging for the Company to 3

fill, that makes it even more imperative that we be able to offer compensation 4

packages that are attractive to our current and prospective future employees. 5

6

Q. DO MILLENNIALS PRESENT ANY OTHER HIRING CHALLENGES FOR THE 7

COMPANY? 8

A. Yes. That same PwC study states that younger workers value flexibility in 9

working arrangements, including the opportunity to telecommute. Although 10

telecommuting is an option for some of the Company’s employees, there is 11

obviously no way for a lineman or a power plant operator to telecommute. 12

That diminishes the attractiveness of our field positions to be filled by 13

prospective employees from the millennial generation. 14

15

In addition, the PwC study indicates that one of the most important attributes 16

of employment for millennials is the opportunity for rapid career progression. 17

A number of the positions in the Company require training and 18

apprenticeship programs that can last several years, which reduces the 19

attractiveness to join our Company by candidates. 20

21

Q. WHAT OTHER EMERGING CHALLENGES DOES THE COMPANY FACE WITH 22

RESPECT TO HIRING AND RETENTION CHALLENGES? 23

13 See https://www.pwc.com/gx/en/managing-tomorrows-people/future-of-work/assets/reshaping-the-workplace.pdf (accessed on Oct. 23, 2015).

42 Docket No. E002/GR-15-826 Lowenthal Direct

PUBLIC DOCUMENT – TRADE SECRET INFORMATION REDACTED –

PUBLIC DATA

A. Like other Minnesota employers, the Company faces a future with fewer job 1

applicants. As seen in Figure 2 below, according to the Minnesota State 2

Demographic Center, in 2020 labor force growth rates will hit record lows.14 3

That also makes it more important for the Company to be able to attract the 4

anticipated lower number of candidates with a competitive compensation 5

package. 6

7